Abstract

In this commentary, we trace the economic and spatial consequences of the Covid-19 pandemic in terms of potential business failure and the associated job losses across the 100 largest cities and towns in the United Kingdom (UK). The article draws on UK survey data of 1500 firms of different size classes examining levels of firm-level precautionary savings. On business failure risk, we find a clear and unequal impact on poorer northern and peripheral urban areas of the UK, indicative of weak levels of regional resilience, but a more random distribution in terms of job losses. Micro firms and the largest firms are the greatest drivers of aggregate job losses. We argue that spatially blind enterprise policies are insufficient to tackle the crisis and better targeted regional policies will be paramount in the future to help mitigate the scarring effects of the Covid-19 pandemic in terms of firm failures and the attendant job losses. We conclude that Covid-19 has made the stated intention of the current government’s ambition to ‘level up’ the forgotten and left-behind towns and cities of the UK an even more distant policy objective than prior to the crisis.

Introduction

Contemporary Covid-19 research has shown that up to around 10% of UK businesses are at immediate risk of failure due to insufficient precautionary savings, and that this risk was unequally distributed across different size classes of firms, with micro and small most at risk (Cowling et al., 2020). The Organisation for Economic Co-operation and Development (OECD) estimates that more than half of all small and medium-sized enterprises (SMEs) face severe loss of revenue due to the pandemic (OECD, 2020). The impact of the interplay of weak revenues and low cash reserve is complex, with different firms responding in disparate ways to mitigate these financial constrictions. While some will adjust to this hostile prevailing environment via financial bootstrapping techniques (Winborg and Landström, 2001) or accessing government support schemes, others will quickly become insolvent due to liquidity pressures. 1

In this commentary, we trace the economic consequences in terms of potential business failure due to liquidity problems and the associated job losses across the 100 largest cities and towns in the UK. Using firm-level precautionary savings as a rough proxy for firm-level resilience, we look at how different locations may be affected in terms of their financial resilience in light of the Covid-19 crisis. The management of working capital (i.e. the management of current assets and current liabilities) focuses on the short-term financial position of a business and typically represents one of the most important challenges facing firms (La Rocca et al., 2019). Therefore, holding cash reserves insures, or hedges, against the potential risk that future income streams are disrupted and potentially lower than expected, which is crucial for firm-level resilience to shocks (Cowling et al., 2020).

In recent years, there has been mounting criticism levelled at small business scholars for paying insufficient attention to spatial and contextual factors when examining entrepreneurial phenomenon (Welter, 2011; Welter et al., 2019). This has been brought into sharp relief during the Covid-19 pandemic which has unfolded unevenly across different socio-economic groups, geographical areas and localities across the UK (Dorling, 2020). This aspatial focus has undoubtedly hindered our understanding of how different localities are affected by crisis situations and how entrepreneurial resilience levels vary across different spatial locations and local communities (Korsgaard et al., 2020; Roundy et al., 2017). This article seeks to counter this tendency by specifically examining the geographical impact of the Covid-19 pandemic on firms in different cities across the UK.

During the current pandemic, there has been a growing body of evidence, from a wide array of economies, suggesting that the firms most negatively affected are the most nascent start-ups and micro-sized firms (Brown et al., 2020b; Cowling et al., 2020; Kuckertz et al., 2020; Martinez-Cillero et al., 2020). There is also strong evidence that certain sectors have been the hardest hit by various national and regional lockdowns, such as retail, hospitality, food service and construction (OECD, 2020). There is an over-representation of SMEs in the sectors which are disproportionately affected by lockdowns. 2

However, to date there has been an absence of evidence examining the spatial locations where these firms will be the most adversely affected. This crucial omission is concerning for a number of reasons. First, the bulk of evidence suggests that economic shocks have a disproportionate impact on certain types of non-core regions and cities. Evidence from the global financial crisis (GFC) demonstrates that the areas most affected were peripheral regions, whereas the least affected were core regions and capital cities which typically have a disproportionate amount of high-tech or knowledge-based industries (Bishop, 2019; Blažek et al., 2020; Martin et al., 2016b). Indeed, this is a key recurring theme emerging from the growing literature on regional resilience since the GFC (Bachtler and Begg, 2018).

A second factor why this research lacunae is vitally important concerns the direction of public policy during the pandemic. Thus far, most of the UK’s business support policies have applied universally across the country. Indeed, all of the main support schemes such as the British Business Bank’s Bounce Bank Loan Scheme (BBLS) and Future Fund are open to UK start-ups and SMEs irrespective of a firm’s geographic location. 3 Despite this, initial evidence shows that by far the largest beneficiaries of some of these schemes are firms located in London and the South-East of England, which feature the largest proportion of the overall UK’s business stock. Data from the BBLS show that nearly half of all awards went to firms based in these south-east locations, which is broadly in line with its stock of UK firms. 4 However, 61% of all Future Fund awards went to companies based in London, and only 11% of the awards went to firms in the north-west, north-east and Yorkshire and Humber despite these areas constituting around 20% of the nation’s business stock. 5 A mere 3% of Future Fund awards went to firms located in the three devolved nations which cumulatively comprise 12% of the business stock. This means that the firms in the areas most adversely affected by the Covid-19 pandemic may not be accessing the available support. This could potentially have significant long-term implications for these regions which are now facing a protracted recession owing to the crisis. Therefore, empirically examining the geography of the firms most likely to be endangered by the shock of the crisis is crucial from a policy perspective.

The remainder of the commentary is as follows. First, we briefly examine the literature on regional resilience and entrepreneurial ecosystems (EEs). Second, we outline the article’s data and methodology. Third, we highlight the key findings. Finally, we conclude and end with some important policy considerations.

Literature review

In response to growing calls for more contextually focused entrepreneurship research highlighted above, there has been a growth of two key strands of literature in recent years – regional resilience and EEs – which have attempted to fill this gap. These are complex constructs which can only be roughly sketched out in such a brief commentary article but are important analytical tools for examining differential responses to crisis events. It seems no coincidence that both streams of literature have been advanced by a confluence of entrepreneurship scholars and economic geographers (Alvedalen and Boschma, 2017; Brown and Mason, 2017). The intersection of these disciplines potentially offers fruitful insights into the powerful role context and geography play in shaping and mediating the nature of the entrepreneurial process.

Regional resilience and EEs

In recent years, there has been a rapid expansion of academic interest in the concept of ‘regional resilience’, a term invoked to describe how regions respond to exogenous shocks and disequilibrium (Boschma, 2015; Bristow and Healy, 2014; Hassink, 2010). Regional resilience is defined as the ability of a region or location to ‘resist, absorb, adjust to, and recover successfully from shocks or disturbances that disrupt that entity’s or system’s pre-shock state’ (Martin and Gardiner, 2019: 1802). An expanding empirical literature has revealed how different locations have differing capabilities to deal with exogenous or unforeseen shocks (Bishop, 2019; Blažek et al., 2020; Martin et al., 2016b). This concept is of critical importance as differences in resilience to major shocks contribute to determining the long-run growth paths of different regions (Bristow and Healy, 2014).

While this body of evidence shows how aggregate economic performance is affected by cyclical shocks, it fails to properly explain how different types of firms, specifically SMEs, adapt, change and reconfigure themselves to accommodate destabilising unforeseen shocks (Brown et al., 2020a). Notwithstanding this, prior evidence suggests that the smallest firms are disproportionately affected by chronic uncertainty due to lower resilience levels to unexpected shocks (Williams and Vorley, 2017). For example, a recent study examined credit scores in SMEs to assess firm resilience during the post-GFC period which showed firm closure was often precipitated by falling credit scores in the years prior to foreclosure (Soroka et al., 2020). Indeed, while there is limited evidence regarding resilience in SMEs (Wishart, 2018), it has been vividly illustrated that entrepreneurship is central to creating more resilient regional economies (Williams and Vorley, 2014). In sum, the resilience literature suggests that where your small business is located matters acutely, especially when faced with crisis episodes.

In tandem with the work on regional resilience, there has also been a rapid proliferation of literature on EEs (Cao and Shi, 2020). In recent years, many OECD countries have embraced the concept of EEs as a means of informing their economic development activities aimed at boasting entrepreneurship, marking it out as the latest ‘fad’ in enterprise policy (Brown and Mawson, 2019). EEs in essence are the union of localised cultural outlooks, social networks, incubation facilities, funding sources, universities and active economic policies supportive of innovative new ventures (Brown and Mason, 2017). Together, these factors influence how new firms emerge, grow and shape their capacity to thrive. A key feature identified by the burgeoning literature is the marked levels of observable heterogeneity within different EEs (Brown and Mason, 2017). Cities and urban locations are becoming an important spatial unit of analysis when examining EEs (Xu and Dobson, 2019). A key facet detected within the literature on EEs is the fundamental importance of agglomeration economies found in urban economies which often accrue key benefits for entrepreneurial actors in terms of access to resources, dense networks, human capital, sources of innovation, potential customers and so on (Mason and Brown, 2014). Conversely, EEs located in more peripheral or rural economies often suffer liabilities which hinder the entrepreneurial process, such as low start-up rates, a lack of resources, an anaemic entrepreneurial culture and limited role models (Miles and Morrison, 2020). Entrepreneurial resilience can also be heavily undermined in peripheral and post-industrial EEs with low levels of entrepreneurial ambition and dynamism which can often stymie business growth in SMEs (Gherhes et al., 2020).

In sum, the literature on regional resilience and EEs both point towards a complex array of factors that coalesce to mediate that firm-level behaviour and certain peripheral locations seem less well-equipped than others to generate business growth and sustain firm-level resilience. This is likely to prove especially problematic for smaller firms during an existential economic shock such the current pandemic. These concepts are important to help us understand how firms in different locations cope with and absorb major shocks to their financial operations during a crisis episode. Using firm-level precautionary savings as a rough proxy for resilience, we look at how different locations may be affected in terms of their financial resilience in light of the Covid-19 crisis.

Data and method

The data we used for this research are from a UK survey of the active business population (excluding non-employer self-employed businesses) conducted in 2018–2019. A total of 1500 businesses were surveyed by IFF Research using Computer-Aided Telephone Interviewing (CATI). The sample only refers to firms with employees and excludes the self-employed. To ensure that our achieved sample was representative of the known business population, a size class–industry weighting was constructed and applied to the sample during analysis. The data are the same as those used in Cowling et al. (2020) and contain detailed information relating to how businesses distribute their surplus earnings and profit, if they have any, including whether they retain cash in the business as a precautionary step. It is this precautionary saving that reduces the risk that a business will run out of cash (liquidity) when faced with a deterioration in trading conditions such as we are experiencing during the extended Covid-19 crisis. Firms that either had no profit or free cash to save, and those that did but failed to save for precautionary reasons, were deemed to be at significant risk of failure. This forms the first stage of our analytical chain. Full and detailed estimates of this firm risk modelling process are contained elsewhere (Cowling et al., 2020). At the firm size class level, this study established that 8.46% of micro businesses (0–9 employees), 10.77% of small firms (10–49 employees), 4.20% of medium-sized firms (50–249 employees), and 3.58% of large firms (250+ employees) across the entire UK business population were at severe risk.

The second stage was to establish the precise firm size distributions across the 100 largest cities and towns in the UK, measured by population, as this was found to be the key variable in determining risk of failure during Covid-19 due to running out of cash. For this, we referred to the business population tables (Local Authority county – Business Register and Employment: Table 5, Office for National Statistics) which provide detailed firm size distributional and employment data at the local and regional level. These data were then used to calculate the precise number of firms of each size class (micro, small, medium and large) in each of our 100 cities and towns predicted to be at severe risk of running out of cash during Covid-19. We then simply multiplied, for each size class of firm, the number of at-risk firms within that size class located within each individual town or city by their average employment to arrive at an estimate of (a) the total number of firms at severe risk (of running out of cash) and (b) the potential job losses if those firms failed. As our focus is on the main largest individual town and cities, we report our estimates at this spatial level.

Results

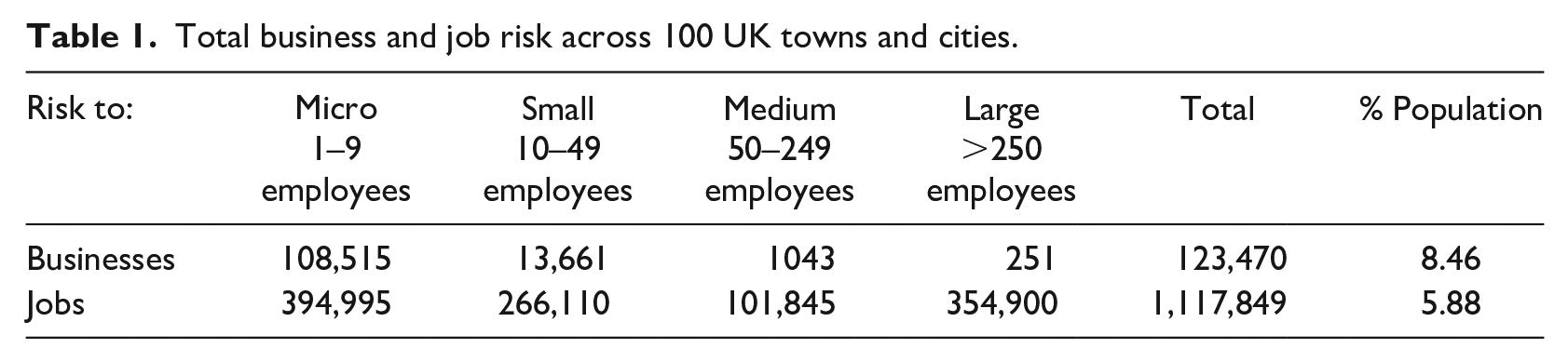

The first issue we address is the total number of businesses at severe risk and the jobs associated with these at-risk businesses across the 100 largest UK towns and cities by population. At the aggregate level, we estimate that 123,470 businesses are at risk of running out of cash, and this total figure is dominated by an estimated 108,515 micro businesses, employing between one and nine people. At the other end of the size class distribution, we estimate that 251 large businesses are at risk. Obviously, the potential job losses associated with these at risk businesses vary very considerably across size classes, with the average micro business having 3.64 employees compared to average employment in a large business of 1414.18.

Table 1 details the potential job losses associated with these at-risk businesses, which totals 1,117,849 UK workers or 5.88% of the total working population employed in private businesses in the largest 100 towns and cities. While potential job losses among micro businesses spread across the country are the single largest source at 394,995, it is also the case that potential job losses from the very few failures in large businesses are also a key component of aggregate total potential job losses at 354,900.

Total business and job risk across 100 UK towns and cities.

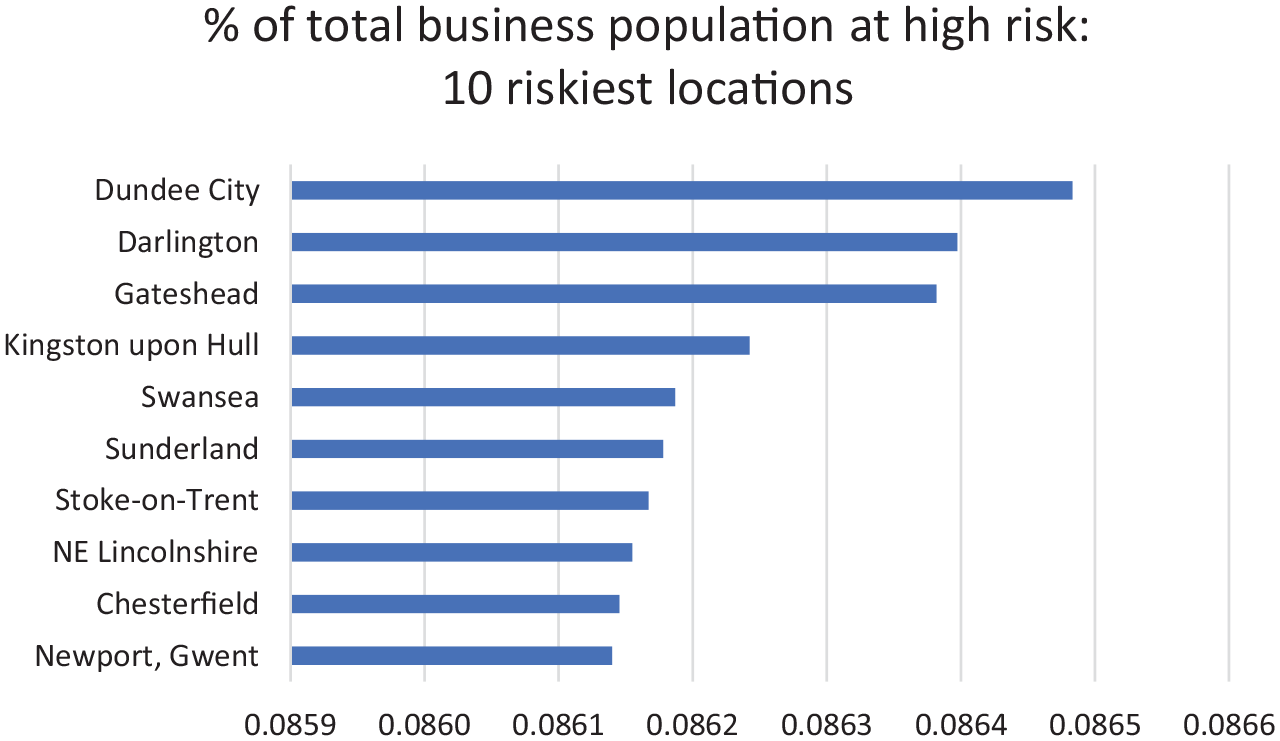

Next, we focus on the unequal distributions of business and employment risk across the 100 largest towns and cities. From Figure 1, we can observe that there is not a single Southern English city or town in the top 10 most at-risk business failure locations. The highest business risk is in the Scottish city of Dundee where 8.65% of the total business population are at risk. There are also high concentrations of at-risk firms in peripheral English North Eastern cities and towns, including Darlington, Gateshead, Kingston-upon-Hull, Sunderland and also North East Lincolnshire. In addition, there are two English Midlands localities, Stoke-on-Trent and Chesterfield, and two Welsh areas, Newport and Swansea. We note that all these top 10 towns and cities are also associated with high levels of Covid-19-related incidence and associated restrictions.

Business risk: ten highest risk local areas.

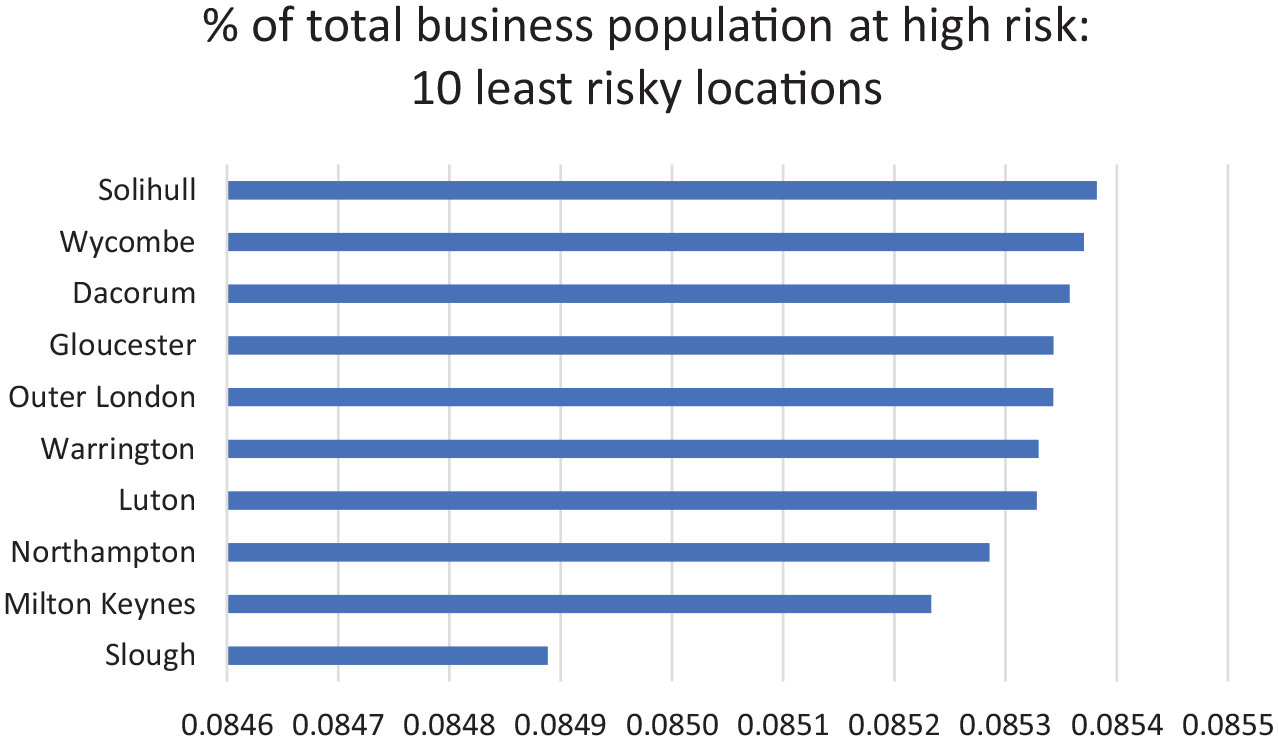

For comparative purposes, Figure 2 depicts the lowest 10 locations for businesses at risk. With the notable exception of Warrington in the North-West of England, the vast majority of low-risk areas are in London and the South-East of England, with the notable Midlands exceptions of Northampton, Gloucester and Solihull. We note here that the wealthiest regions are located in London and the South-East of England. In its entirety, we begin to see a picture that separates the country along similar lines as we observe the distribution of wealth and incomes. Poorer and peripheral areas and regions have the highest incidence of business risk, and richer and London-centric areas and regions have the lowest amount of firms at risk. This suggests that, at the business level, comparatively more firms in poorer and peripheral areas will disappear during the Covid-19 epidemic and that this inequality of impact on the business population will further disadvantage these areas in the post-Covid-19 era.

Business risk: ten lowest risk local areas.

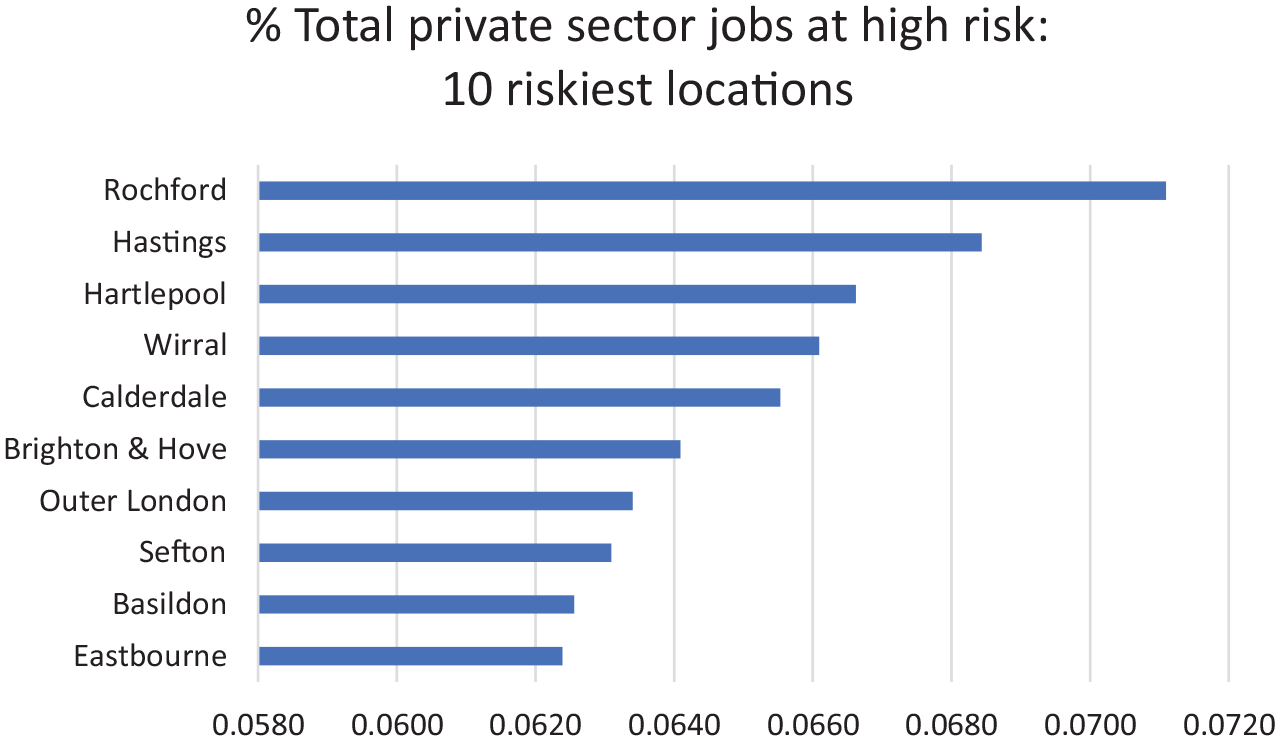

We now turn our attention to the potential job losses associated with businesses at risk. Figure 3 shows the share of total jobs that are associated with at-risk businesses within each locality. The first point of note is that the potential job losses are much more geographically and spatially diverse than was the case for business risk which was heavily concentrated in poorer and peripheral areas. For example, Rochford in Essex (a South Eastern English county) has the highest potential job losses out of local employment at 7.11%. Hastings in Sussex (again a South Eastern English county) has the second highest potential job losses at 6.84%. However, a number of Northern English cities and towns are represented in the top 10 for job losses (Hartlepool, Wirral, Calderdale and Sefton), but so too is Outer London.

Job risk: ten highest risk areas.

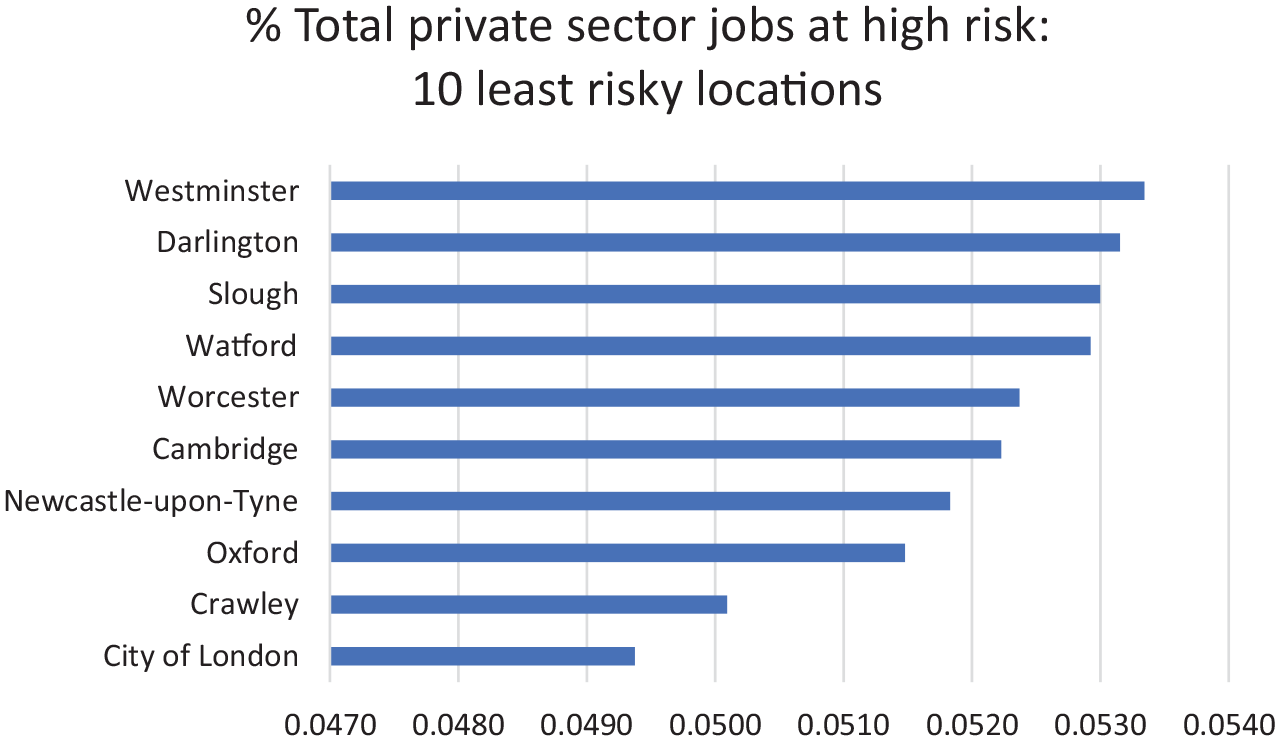

In terms of the lowest 10 at-risk job loss areas (see Figure 4), again we observe a broad geographical spread, with the City of London having the lowest rate of potential job losses at 4.94%, but also Northern English cities and towns such as Newcastle-upon-Tyne and Darlington having low potential job loss rates. It is also interesting to note that regionally important cities such as Cambridge, Oxford and Worcester, and great mediaeval cathedral cities also appear at low potential risk of job losses due to business failure. This could be associated with high levels of knowledge-intensive firms in these more sophisticated locations. The distribution of potential job losses is much wider than that apparent for business failure across both towns and cities, which highlights the importance of the relative size distribution of firms within each locality. And this is important as there is a vastly different probability, even in good economic times, of an individual finding a new job in the South-East of England than is the case in the peripheral and poorer regions outside of this disproportionately wealthy part of the UK.

Job risk: ten lowest risk areas.

Discussion and conclusion

We were initially concerned about potential business failure across the UK due to Covid-19. But we were also aware that these ‘at-risk businesses’ employ millions of workers whose jobs were at risk too. In this commentary, we combined the two and questioned whether or not there was a particular geographic pattern to this unfolding crisis as some have suggested (Dorling, 2020). Our results clearly show that business risk is unequally concentrated in poorer and more peripheral towns and cities, implying that any potential economic recovery will be more difficult to achieve given their already lower starting point pre-crisis. In line with other research on regional resilience, this clearly suggests that the impact of the current Covid-19 crisis is likely to have a strong spatial dimension due to weaker firm resilience within these northern and peripheral geographic locations (Martin et al., 2016b). This was particularly important as the current UK government has stated its desire to pursue a ‘levelling-up’ agenda that aims to redress the long-established economic inequalities while also pursuing a distinct local and regional approach to battling the medical aspects of the Covid-19 crisis.

However, due to specific town and city-level distributions of firm size classes, which is the main driver of business failure, the potential loss of employment due to business failure was quite different at a spatial level and much more widely distributed across UK towns and cities. In this sense, two towns with an equal share of at-risk businesses could have very different job losses associated with business failure due to a significant difference in their firm size class distributions.

So what does this mean for the post-Covid-19 levelling-up agenda? First, poorer northern peripheral towns and cities will have a much reduced business stock so that unless this is offset by dynamic entry of new businesses, their total capability will be reduced. Second, for those individuals who have lost their jobs due to business failure, it is the potential of the business sector to provide new jobs for them that will determine their future economic outcomes. And we know wealthier regions and core urban ecosystems have the consumer demand and entrepreneurial resources to support future firm growth, which will absorb some of this new unemployment. But this is less likely to be the case in poorer and more peripheral localities that also have proportionately fewer businesses per se; hence, the resultant affect will be magnified in these areas. We conclude that the stated levelling-up agenda just became even harder to achieve due to the economic impacts of Covid-19.

The policy implications arising from the proceeding analysis are crucial. To mitigate the uneven spatial impact of the crisis on the economy, the government should make a concerted effort to ensure that regional policy is significantly bolstered during the post-pandemic era. Given that the UK is already one of the most inter-regionally unequal countries in the industrialised world (McCann, 2020) where the gap between the south and north is ‘long-standing, cumulative and systemic’ (Martin et al., 2016a: 355), the impact of the Covid-19 crisis makes this an even more pressing policy imperative. In tandem with this, spatially blind enterprise policies such as the Future Fund need to be more geographically targeted towards firms in more northern and peripheral locations, especially as such a scheme benefits growth-oriented start-ups capable of generating new jobs. There could be arguments for these types of Covid-19-related support instruments to be spatially calibrated, so firms in certain locations receive higher levels of incentives, and vice versa, in more advantageous regions like London and the South-East of England. To mitigate the anticipated jobs losses in times of crisis, much more bold and imaginative policy measures are urgently required.

Footnotes

Acknowledgements

The authors are very grateful to the reviewers for their considered comments. They also wish to thank the Editor, Susan Marlow, for her very helpful suggestions. The usual disclaimer applies.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.