Abstract

How did the great financial crisis (GFC) of 2008–2010 impact on R&D and innovation in the United Kingdom and internationally? What can we learn about the likely innovation effects of the COVID-19 crisis on small and medium enterprises (SME) innovation? Numerous international studies suggest the strong procyclicality of R&D and innovation investments in firms: investment rises in recovery and falls sharply in times of crisis. This procyclicality is driven in firms by both internal financial resources or slack and varying market incentives for innovation. Cash constraints, in particular, may impact most strongly on R&D and innovation investments by smaller firms. In the United Kingdom, the proportion of innovating firms fell by around a third during the GFC and took around four to six years to recover. Recovery was also uneven – notably weaker in some sectors and regions. The COVID-19 crisis seems likely to leave many firms financially weaker, with the most significant impacts on the willingness or ability of SMEs to sustain R&D and innovation. Where firms are able to sustain these investments, however, the evidence from the GFC suggests that they will lead to better survival chances, stronger growth and higher profitability. Some additional financial support for innovation has been announced by the UK government. Whether this will be sufficient to sustain SME levels of innovative activity, however, remains to be seen.

Introduction

Innovation – the introduction of new products, services and ways of doing business – will be a critical element of the recovery post-COVID-19. Undertaking R&D and innovation is always risky, however, with uncertain technical and commercial outcomes. In a recent review of the literature on innovation failure, Rhaiem and Amara (2019) estimate the proportion of innovative projects failing, wholly or in part, to be between 40% and 90%. As we move beyond the immediate COVID crisis, firms with less financial slack may be less willing to make such risky investments. Weak market demand, and potentially volatility, may also reduce the incentives to innovate. Here, we look back at the aftermath of the great financial crisis (GFC) of 2008–2010 and examine how it affected R&D and innovation in the United Kingdom and internationally, with a particular focus on the implication for small and medium enterprises (SMEs). We then consider what implications this has for R&D and innovation in SMEs in the United Kingdom in years to come. The argument develops as follows. In section ‘Innovation after the GFC – credit constraints, procyclicality and a lack of demand’, we provide an overview of the international research literature on the effects of the GFC on R&D and innovation. Few of these studies relate specifically to SMEs but they do provide an indication of how financial pressures and changes in markets impacted on the behaviours of firms more generally. Section ‘UK innovation trends after the GFC – a slow recovery’ focuses more specifically on the United Kingdom and uses data from the UK Innovation Survey (UKIS) and Business R&D surveys to examine some of the main trends in innovation activity after the GFC. Section ‘R&D and innovation after COVID-19’ summarises the key lessons and considers what we can infer about R&D and innovation in SMEs post-COVID-19.

Innovation after the GFC – credit constraints, procyclicality and a lack of demand

The GFC had significant and lasting effects on the global economy. It limited access to finance for many smaller firms internationally and reduced growth rates and the incentives for innovation. In this section we consider how R&D and innovation behaviour changed during, and after the GFC, drawing on international research evidence. We focus on the empirical evidence, but it is worth noting that theoretical arguments exist, which could explain both countercyclical and procyclical R&D and innovation investments. Schumpeterian growth models imply counter-cyclical R&D investment over the business cycle (Aghion et al., 2012), with economic crises creating the conditions for new innovation by lowering factor prices and creating a stock of idle resources (Schumpeter, 1934). The central argument here is one of ‘creative destruction’ where, during times of recession, there is a reallocation of resources towards new entrants (Aghion et al., 2014). Conversely, if access to credit in order to finance innovative activities becomes limited during a recession, firms may become cash constrained, and R&D investment becomes procyclical (Aghion et al., 2012). For example, using US firm-level data on non-federally funded, high-technology firms, Kabukcuoglu (2019) examines the cyclicality of R&D activities. Findings suggest that R&D investment is procyclical due to binding financial constraints. Sub-sample results for small firms and young firms – firms that may be more likely to face financial constraints – support the main findings. Furthermore, findings indicate that R&D stocks of the median firm without access to bond markets could have increased by a further five percentage points if liquidity constraints were removed (see also Burger et al., 2017). In another empirical study, Paunov (2012) uses regression analysis to examine the role of financial constraints in determining innovative investments in Latin America. Findings show that private investments in innovation are largely procyclical. On average, one in four firms engaged in less innovative investment during the GFC.

The data indicate that during the crisis, larger firms were stronger process innovators than smaller firms, whereas the proportion of larger and smaller firms undertaking product innovation during the crisis was similar. Essentially similar results emphasising the impact of financial constraints and the procyclicality of R&D and innovation investments are found by Campello et al. (2010) in a survey of senior managers across 39 countries and by López-García et al. (2013) in a more focused examination of the impact of credit constraints on 3200 Spanish firms. In Campello et al. (2010), a higher proportion of small firms, compared to large firms, said that they were ‘very affected’ by financial constraints during the crisis, and a higher proportion of the latter stating they were ‘not affected’. The proportion of firms indicating that they were ‘somewhat affected’ by financial constraints was similar across the two subgroups. Many of these studies suggest that procyclical R&D and innovation investment during the GFC is the result of the credit constraints that existed at the time. Adopting an alternative approach, Argente et al. (2018) investigate changes in innovation outcomes – the extent of product innovation and reallocation – in the US consumer goods sector during the 2007–2013 period. Findings suggest that during the GFC, product reallocation was strongly procyclical; the quarterly reallocation rate declined by more than 25%, with the majority of this reduction occurring within firms and resulting from a decline in the creation of new products during the recession. In addition, the rate of product reallocation was strongly related to the innovation efforts of firms, and those firms that had higher reallocation rates grew faster, produced higher quality goods and experienced increases in productivity.

The cyclicality of R&D spending during the GFC is often examined without any consideration of firm heterogeneity. Schmitz (2014), however, investigates whether small-firm and large-firm R&D-investment responses differ during times of recession. Using data on German firms, Schmitz (2014) finds that the median small firm reduced its R&D spending by more than the median large firm. This resulted in the development of a significant gap in the relative R&D intensity of small and large firms during the GFC years.

UK innovation trends after the GFC – a slow recovery 1

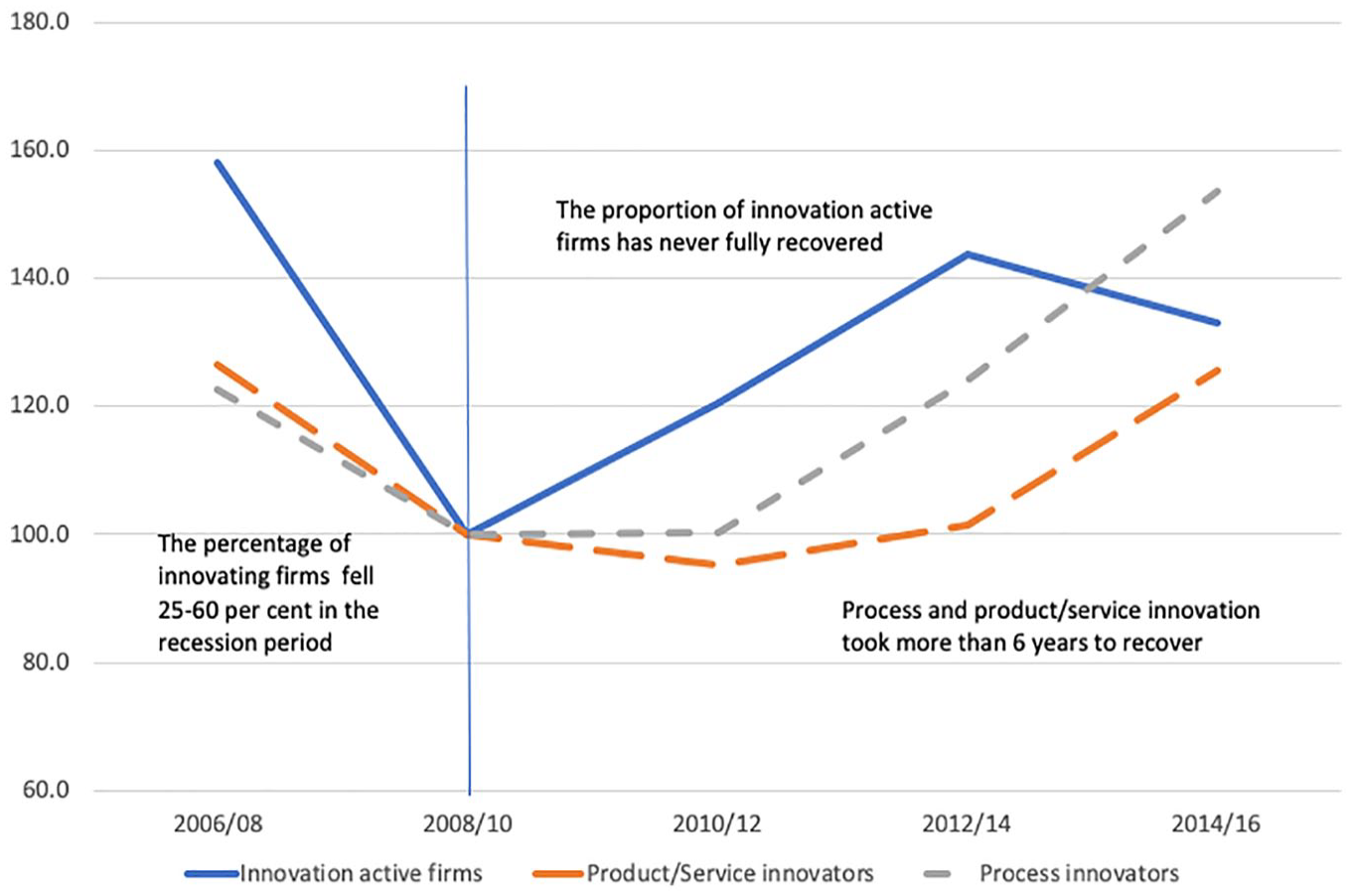

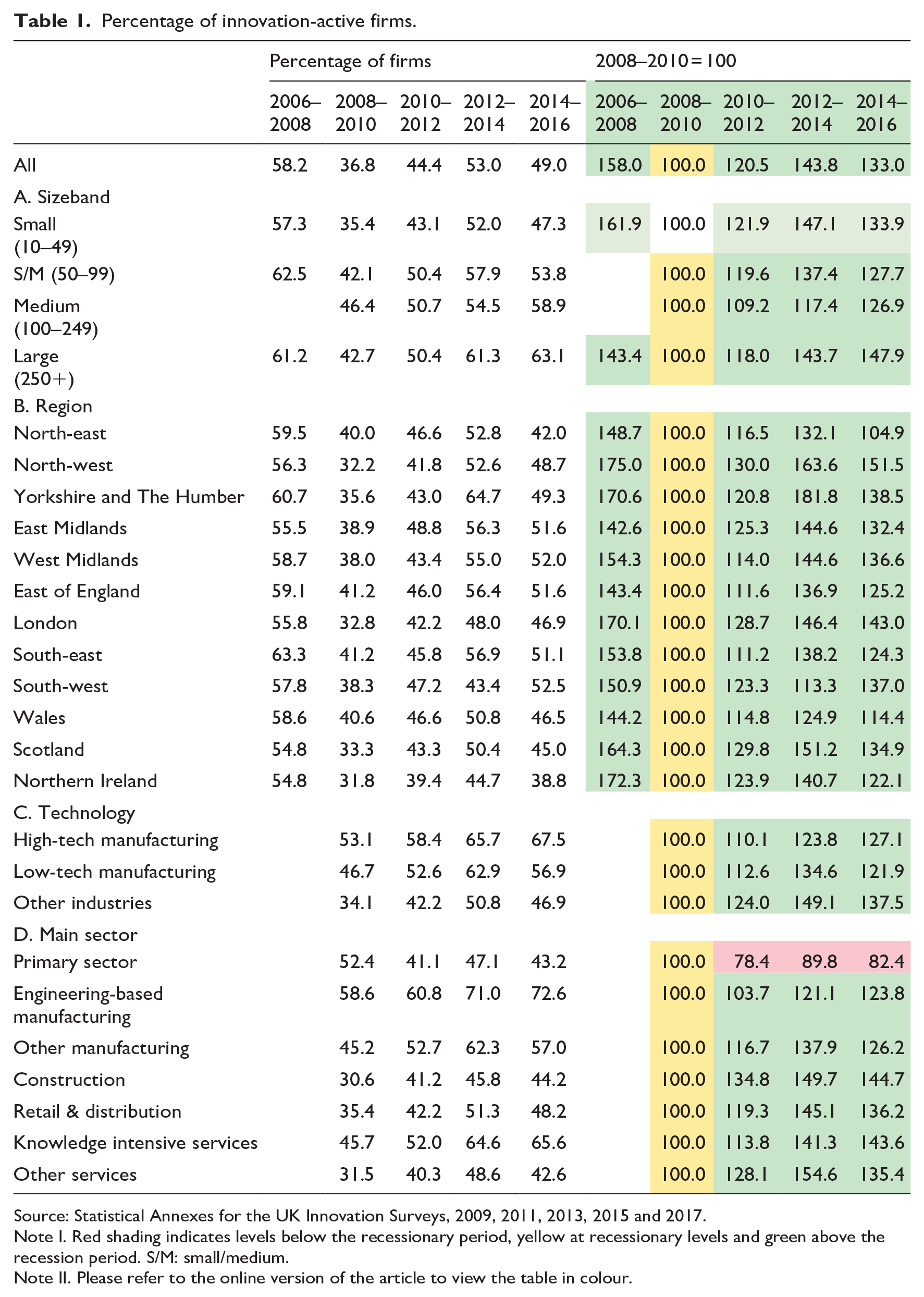

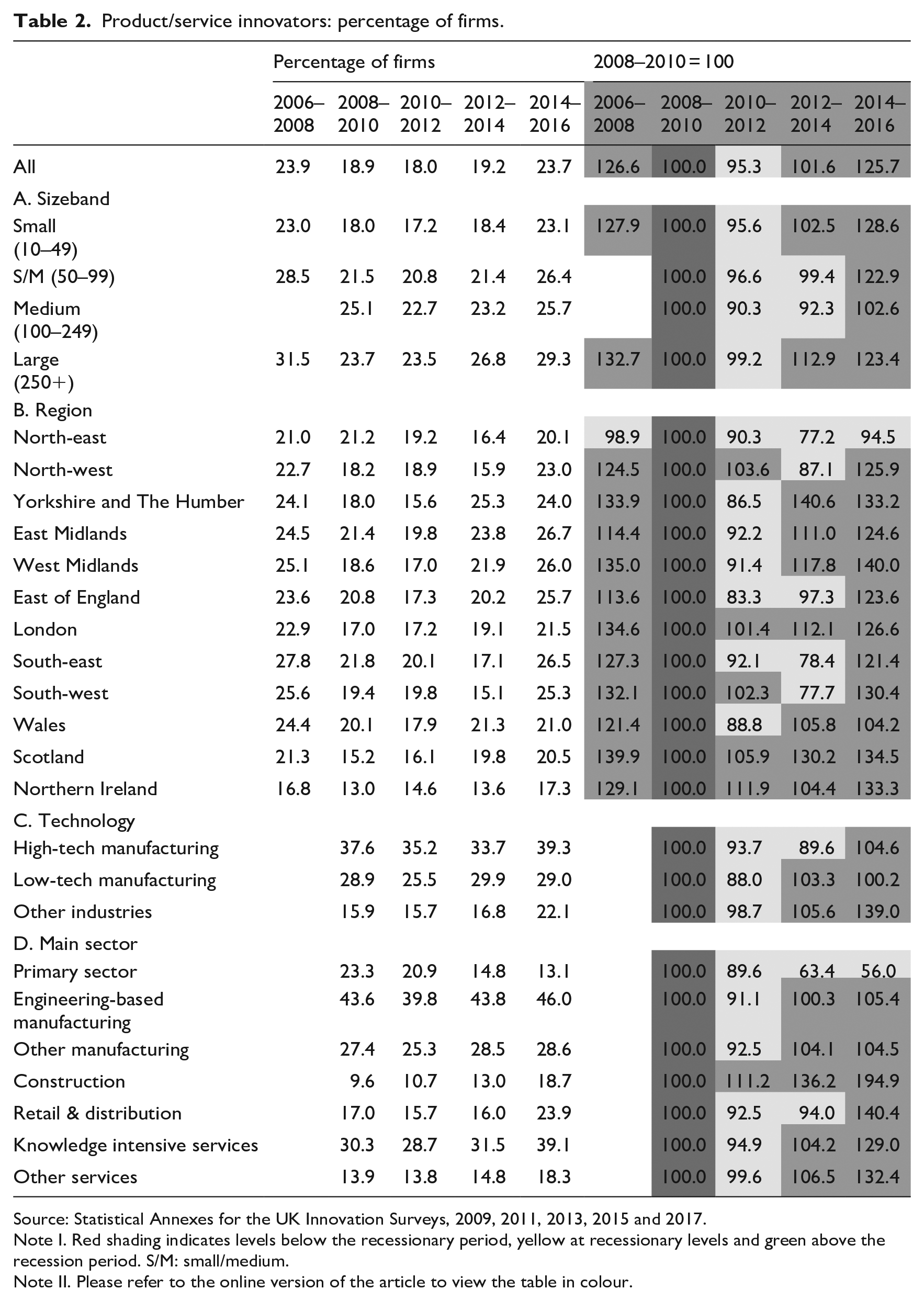

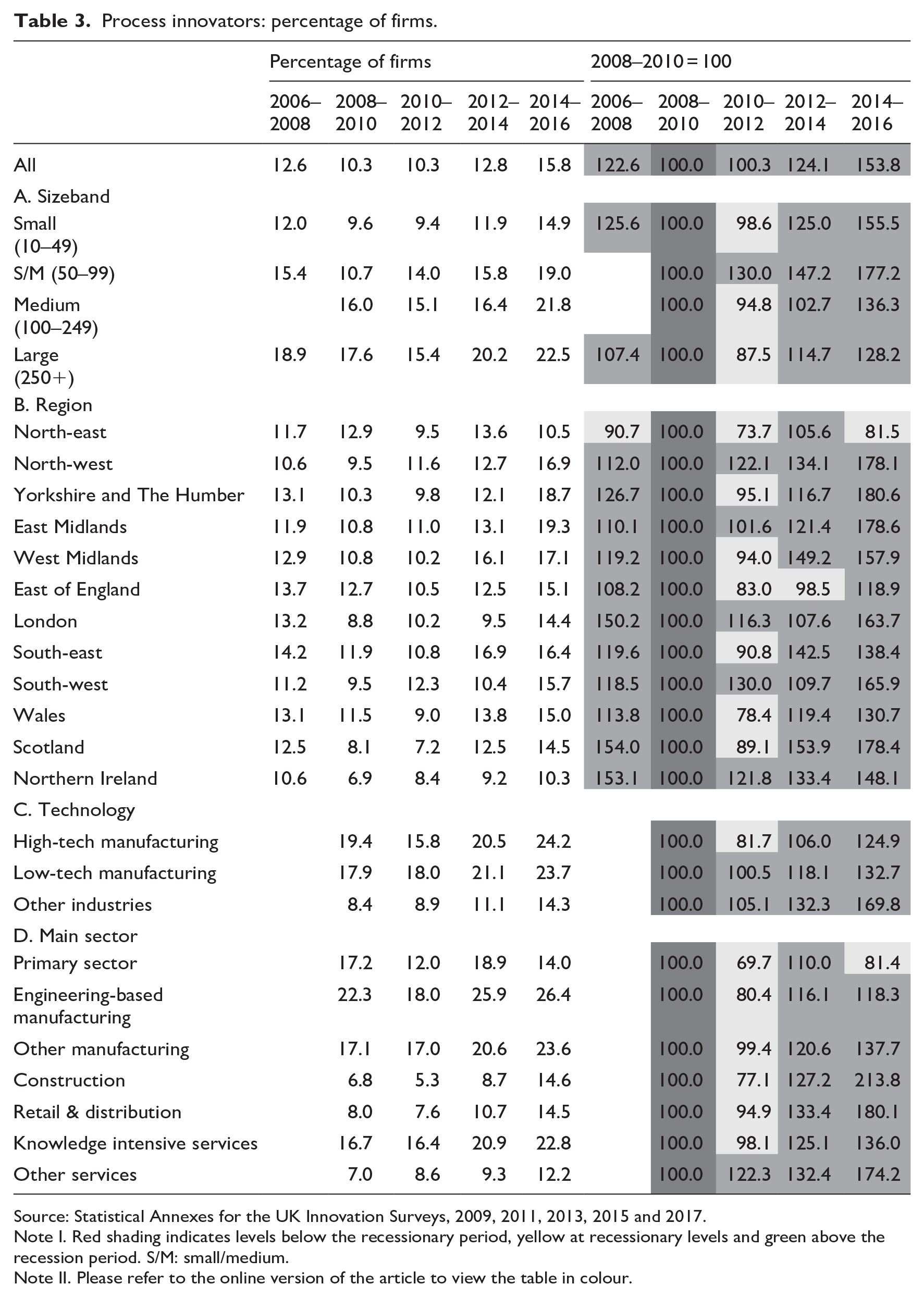

There has been limited prior work on the impact of the GFC on R&D and innovation in the United Kingdom. In this section we, therefore, draw upon survey data to provide an overview of trends in innovation during and after the GFC. The UKIS is the primary source of data on innovation in UK firms (with more than 10 employees) and is conducted every two years. 2 Each wave of the survey relates to innovation activity in the previous three years. One wave covered the period 2008–2010, the great recession period, with the previous wave covering the pre-recession 2006–2008 period. Subsequent waves of the survey provide an overview of the post-crisis behaviour. This survey provides three indicators relating to the extent of innovation activity across the population of UK firms: the percentage of innovation-active firms (Table 1), the percentage of product/service innovators (Table 2) and the percentage of process innovators (Table 3). The initial columns in each table provide the percentage of firms undertaking each activity, and the later columns provide an indexed form of the data using the recession period 2008–2010 as the baseline (2008–2010 = 100). Green cells represent above recession level and the red cells below recession levels. In terms of these innovation metrics the UKIS suggests the following:

The percentage of innovation-active firms (Table 1 and Figure 1) – those either innovating or investing in innovation – fell sharply from 2006 to 2008 (58.2%) to the recession period (36.8%). In 2014–2016 aggregate levels of innovation activity on this metric had not recovered their pre-recession levels (49.0%). This was true of almost all sectors and regions, as well as smaller firms. By 2014–2016, levels of innovation activity in larger firms were marginally above that in the pre-recession period (Table 1). The recovery in innovation levels post-recession was slower in manufacturing than in services (Table 1). Levels of innovation activity in the primary sector and North-east remained particularly weak throughout the post-recession period until 2014–2016 (Table 1).

Around 1:5 UK firms report product or service innovation over a three-year period (Table 2). The proportion fell by 26.6% to the recession (Figure 1) and had only recovered this level of activity by 2014–2016, six years after the recession. In part, this reflects a continued fall in the proportion of innovating firms in the years immediately following the recession (Table 2). This post-recession fall was evident in all sizes of firms with innovation recovering most quickly in larger and small (10–49 employees) firms. A number of regions also experienced further falls in levels of product/service innovation after the recession with the picture in the North-east and the Primary sector being particularly weak (Table 2).

Process innovation is typically reported by around 1:6 UK firms (Table 3 and Figure 1). Levels of process innovation activity dropped by around a fifth between 2006–2008 and 2008–2010 and recovered steadily thereafter. By 2014–2016, activity levels were well above their pre-recession level. In this sense, process innovation rebounded significantly more quickly than product or service innovation. Process innovation increased more rapidly in smaller firms post-recession, and by 2014–2016, levels of activity were higher than the pre-recession level in most sectors and regions. The primary sector and the North-east are again notable exceptions (Table 3).

The percentage of innovating firms in the United Kingdom.

Percentage of innovation-active firms.

Source: Statistical Annexes for the UK Innovation Surveys, 2009, 2011, 2013, 2015 and 2017.

Note I. Red shading indicates levels below the recessionary period, yellow at recessionary levels and green above the recession period. S/M: small/medium.

Note II. Please refer to the online version of the article to view the table in colour.

Product/service innovators: percentage of firms.

Source: Statistical Annexes for the UK Innovation Surveys, 2009, 2011, 2013, 2015 and 2017.

Note I. Red shading indicates levels below the recessionary period, yellow at recessionary levels and green above the recession period. S/M: small/medium.

Note II. Please refer to the online version of the article to view the table in colour.

Process innovators: percentage of firms.

Source: Statistical Annexes for the UK Innovation Surveys, 2009, 2011, 2013, 2015 and 2017.

Note I. Red shading indicates levels below the recessionary period, yellow at recessionary levels and green above the recession period. S/M: small/medium.

Note II. Please refer to the online version of the article to view the table in colour.

R&D and innovation after COVID-19

The COVID-19 crisis shares two significant similarities to the 2008–2010 GFC. First, both were, or are sharp exogenous shocks rather than business-cycle fluctuations. Second, both have affected firms through sharply reduced liquidity – the GFC through a sharp reduction in the availability of commercial finance and the COVID-19 crisis through sharply reduced turnover. In both cases, financial stringency will force firms to make rapid strategic decisions about areas of spend and potential savings. The evidence from the international research literature and UK trends post the GFC suggests that R&D and innovation are strongly procyclical, and we should, therefore, expect sharp falls (perhaps a third) in the proportion of innovating firms, with only a slow recovery to previous levels of innovative activity.

These effects will not be uniform across firms. The evidence from the GFC suggests that firms which entered the COVID-19 crisis with stronger cash positions may also emerge more strongly. For example, Joseph et al. (2020) use firm-level data for private and publicly listed UK firms during the 1999–2014 period to investigate whether a firm’s pre-crisis cash position relative to its industry rivals is a strong predictor of the firm’s long-term investment after the financial crisis. Findings suggest that the tightening of credit constraints during the crisis allowed cash-rich firms to gain a strategic advantage over financially constrained rivals. The impact of relative cash was particularly large for young and small firms – those firms more likely to become financially constrained during a crisis. In addition, cash-investment sensitivities were larger for firms operating in industries where the average firm was younger or smaller. Continuing to invest during the crisis gave the cash-rich firms a competitive edge that would continue into the recovery period. Having financial slack – or cash at hand – when a crisis strikes gives firms a considerable advantage in both the short and longer term. A study by La Rocca et al. (2019), who examine how cash holdings affected performance in European SMEs, supports these results. Lee (2015), in a study of Korean firms, suggests that the relationship between financial slack and innovation is the strongest in younger and smaller firms. The implication is that the financial position of firms pre-crisis will influence longer term outcomes, particularly among SMEs.

After the worst of the COVID-19 crisis has passed, firms with greater financial slack may also be able to undertake different types of (more radical and risky) innovation than more financially constrained firms. Latham and Braun (2008) show how managers use financial slack to speedily implement firm strategy and accelerate recovery. Bruneel et al. (2016) show that firms with higher levels of financial slack are inclined to undertake explorative knowledge sourcing (distant search efforts with universities), the basis for radical innovation, whereas firms with low levels of slack are more inclined to undertake exploitative (near-term support and problem-solving) knowledge sourcing and incremental innovation. Evidence from the GFC, although not specific to SMEs, also suggests that crisis effects on innovation will vary strongly between sectors and regions. For example, Delgado et al. (2015) examine the part played in recovery by regional clusters in the United States, and suggest that strong clusters not only improve regional employment growth over time, but also improve the resilience of regional economies to downturns. Perhaps less obviously, cultural factors may also play a part in shaping how strongly firms in different economies rebound after a crisis. For example, Petrakis et al. (2015) examine whether changes in innovation and competitive performance in 24 European countries during and after the GFC (2008–2013) were due to the macro conditions at the time or more long-lasting forces such as the economy’s cultural background. Their data imply the existence of two clusters of countries: First, an anti-innovation cluster where there is a reluctance to invest in and use new technologies and where there is a low level of interpersonal trust. Second, a pro-innovation cluster where firms feel safe and tend to take risks. Regression analysis suggests that an economy that has or is developing a pro-innovation culture is able to perform better in the future, despite adverse international conditions.

The evidence suggests that firms which are able to sustain their innovation activity will gain a significant advantage in any post-COVID recovery. For example, Flammer and Ioannou (2015) use regression analysis to investigate how US firms adjusted their investments into key resources – both tangible and intangible – during the GFC (2007–2009). Firms that continued to invest in R&D and innovation by (1) becoming more efficient and innovative, (2) adapting more easily to shifting needs and demands of suppliers, consumers and other stakeholders, and (3) enhancing their organisational resilience, were able to sustain competitiveness. This is confirmed by European evidence provided by Spescha and Woerter (2019), who suggest that non-innovative firms suffered the most significant losses during the economic crisis. R&D-based innovations, which may be more radical than non-R&D-based innovations, generating products or services of a greater innovation depth, also provide stronger insulation against economic crises (Laursen and Salter, 2006): firms that undertake R&D-based innovation experience more stable growth development than non-R&D innovators. Furthermore, there is evidence to suggest that previous innovation experience during periods of recession strengthens a firm’s ability to invest in R&D during a new crisis (Amore, 2015). In an empirical analysis of US firm data spanning the 1980s, 1990s and early 2000s (a period that includes three downturns in the US economy), Amore (2015) finds that innovative behaviour during the early 1980s recession had a significant, positive effect on R&D investment during subsequent recessions. These findings may suggest the presence of organisational learning, with firms following previous recession innovation strategies when a new crisis occurs (Audia et al., 2000; Boeker, 1997).

Sustaining innovation during a crisis may be more difficult in smaller firms which may be hardest hit by post-crisis liquidity constraints. However, where it is possible, the evidence suggests that SMEs benefit significantly from R&D and innovation investments, both in terms of survival and profitability. For example, Jung et al. (2018) use data for 588 Korean manufacturing SMEs during the 2008–2014 period, to examine whether undertaking R&D investment increases the probability of firm survival during a recession. Results suggest that technologically capable SMEs can increase their chance of survival by investing in R&D and innovation. Castillejo et al. (2019) examine the effectiveness of innovation and internationalisation strategies among Spanish SMEs during the GFC. Both strategies are key determinants of firm performance, and results indicate that mark-ups are larger at the beginning of the GFC for SMEs undertaking R&D or SMEs engaging in both R&D and exporting activities.

UK support for R&D and innovation

UK government attention during the GFC focused primarily on maintaining the integrity of the banking sector, although many smaller firms still experienced significant borrowing constraints. This inevitably influenced liquidity and a firm’s willingness to invest in R&D and innovation. The UK government’s austerity measures and moves to centralise the then regionalised structure of business support in the United Kingdom also meant that few specific measures were implemented to directly support R&D and innovation after the GFC. One important exception was the development of the Catapult network of technology intermediaries, which has grown and developed significantly over the past decade. 3 Other measures such as R&D tax credits have also become significantly more important in the United Kingdom since the GFC. As part of its response to the COVID-19 crisis, the UK government put in place significant measures to support UK businesses including a furlough scheme to support employment during the lock-down and a range of guaranteed business loans. Despite these very significant measures, the impact of lock-down on firm liquidity and financial reserves has been substantial. The implication of previous research emphasising the procyclicality of R&D and innovation investment and the UK trends analysis reported earlier is that this liquidity crisis will significantly impact on the R&D and innovation spending of firms. A recent survey of holders of UK government R&D and innovation grants, for example, suggested that around a third of firms were planning to cut their R&D spending by more than 50% over the next three months. These short-term cuts will have longer term consequences for levels of innovation, growth, profitability and resilience.

The UK government has published an R&D roadmap intended to set strategic guidelines for supporting R&D and innovation post-COVID. This reaffirms the ambition to raise R&D spending to 2.4% of gross domestic product (GDP) by 2027. This target looks all the more challenging given the likely effects of COVID-19 on business R&D and innovation spend. However, supporting R&D and innovation has been central to the UK government’s and the European Union (EU) response to the COVID-19 pandemic. 4 In the United Kingdom, the importance of R&D innovation to future recovery has been recognised in the announcement of a £1.5 billion loan and grant package for the United Kingdom’s most innovative companies. 5 Fast-growing, equity-backed firms will be able to access matched loan funding, while firms already in receipt of Innovate UK funding will be able to access additional loan and grant finance. A group of 1200 other innovating firms will also be able to access additional funding. The evidence suggests that both the UK government’s general measures to support liquidity and these targeted innovation supports will help to offset anticipated falls in R&D and innovation in 2021. Whether these measures will be sufficient to offset the procylicality of R&D and innovation decisions in the United Kingdom and move us closer to the long-term target, however, only time will tell.

Footnotes

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.