Abstract

Stronger family relationships predict positive health outcomes: a relationship that is partially due to the range of emotional, practical and informational support that families can provide. Yet not all families possess these resources. A survey study in a disadvantaged community in Nottingham, UK (N = 142) demonstrated that family identification positively predicts ability to cope with financial stress, but that this relationship is moderated by whether family support is present or absent. Semi-structured interviews with 10 members of different families from the same community shed further light upon the nature of this relationship: individuals report that they tend to turn to their family rather than friends or community services in times of financial hardship, even though their family are unlikely to be able to support them effectively, and that this is often due to feelings of embarrassment or finance-related stigma. Our findings highlight the complex role that families can play in finance-related issues, as well as the need to encourage individuals to seek financial support from sources which provide effective (rather than emotionally comfortable) assistance.

The study of the health benefits of groups increasingly acknowledges the profound impact of family relationships upon health and well-being (Sani et al., 2012). Psychological identification with one’s family can provide access to the emotional, informational and practical resources necessary to deal with many challenges (Parra et al., 2018; Rodriguez et al., 2018). However, the absence of family support can have negative psychological consequences, leaving members susceptible to threats and pressures (Parra et al., 2018; Rodriguez et al., 2018; Swartzman et al., 2017). In particular, financial pressures can impede upon the support that families provide to their members and leave them vulnerable to poor mental health and relationship breakdown (Conger & Conger, 2002). However, little research has explored how this absence of support has its negative effects, and research to date has yet to examine how the absence of support affects the family’s ability to promote psychological resilience to financial stress.

This paper delineates the current understanding of how financial stress can negatively affect family members’ well-being and how positive family group processes can provide resilience to stress. In doing so, it identifies the need to examine the effects of limited support on how families help their members cope with financial stress. We use a mixed methods approach to explore how these dynamics affect individual family members in a socio-economically deprived community. In an initial survey, we test the prediction that the relationship between family identification, well-being and financial stress is moderated by levels of family support. We then use in-depth interviews with residents of the neighbourhood to explore their lived experiences of how their families help them cope with financial challenges.

Family financial stress

Financial stress has a particularly corrosive effect on families and their coping abilities (Voydanoff, 1990; Conger et al., 2010). Changing patterns of employment, as well as personal loss of earnings, predict subjective financial uncertainty and strain (Voydanoff, 1990), which in turn predicts poor health, and relationship discord/breakdown. Amongst children, negative outcomes include reductions in psychological well-being, increased likelihood of delinquency and poor educational attainment (e.g. Kajonius & Carlander, 2017). Financial deprivation is thus associated with a range of recognisable and distinct impacts on family members’ health and well-being.

The Family Stress Model (FSM; Conger et al., 1992; Conger & Conger, 2002) identifies the specific psychological and behavioural processes underpinning these effects. Conger et al. (1992) refined the range of factors that predict feelings of economic stress: reduced income, high debt to asset ratio, unstable work and inability to pay bills all contribute to feelings of ‘economic pressure’. It is this subjective feeling of economic pressure which serves to mediate the impact of economic hardship upon family well-being, specifically through its effects on members’ mental health (Conger et al., 1992). Depressed mood and emotional distress lead to more negative interactions between partners, which can be further exacerbated by disagreements over financial issues, resulting in relationship quality decline, thereby increasing the likelihood of relationship breakdown (Conger et al., 1999). In effect, the FSM specifies that the psychological mediators of the experience of economic stress and its emotional consequences are responsible for the negative interactional consequences in family life.

As stated, the FSM is typically conceptualised as unidirectional, with exogenous financial factors impacting upon psychological and behavioural processes. However, as the authors themselves cede, relations within the model are likely to be reciprocal over time, such that negative impacts of economic stress on families are likely to have consequences for members’ future economic activities (Conger et al., 2010). Conversely, family emotional support, instrumental assistance and collective problem-solving soothe the negative effects of economic pressure on mood and partners who support one another in times of economic hardship are less susceptible to its effects (Conger et al., 1999). Similarly, alternative ‘strength-based approaches’ (Benzies & Mychasiuk, 2009), show that while financial stress disrupts family functioning, protective factors and coping strategies can strengthen the family’s resilience to future challenges.

Moreover, the FSM is strangely individualistic in its focus. While it considers spousal and parenting interactions, its focus is on the individual family member’s psychological characteristics and experiences, as well as the actions of each individual towards other family members. What is lacking is an appreciation of the extent to which individuals feel themselves to be part of their family; how this provides access to shared emotional, practical and informational resources; and how these collective dynamic factors allow (or fail to allow) the individual to cope with financial stress. Next, we consider the role of these group processes in helping family members cope with stress.

Families and resilience: Social identity and stress

The Social Identity Approach to Health (SIAH, Haslam et al., 2018; Haslam et al., 2012) views social groups as pivotal to the ways in which their members perceive and respond to stress. Research in this tradition distinguishes between how an individual’s ‘primary appraisal’ (interpretation of potential threats) and ‘secondary appraisal’ (perceived ability to cope with threats) are shaped by their group memberships (Wakefield et al., 2019). In terms of primary appraisal, group identity directly reduces stress by interpreting potential threats as either irrelevant or manageable. In an extreme example, Haslam et al. (2005) found that by virtue of their shared occupational identity, bomb-disposal workers rated their work as no more stressful than that of bar-staff.

In terms of secondary appraisal, groups have been shown to enhance the individual’s perception of their ability to cope with threats through their provision of different types of social support, including emotional, practical and informational assistance (Haslam et al., 2004). In terms of informational support, Haslam et al. (2004) demonstrated that sharing an identity facilitates social influence during challenges, such that reassurance from ingroup (but not outgroup) members reduces one’s stress. Sharing an identity also increases the provision and receipt of helping or practical support (e.g. Levine et al., 2002). Furthermore, the belief that such support will be available during hardship reduces the experience of stress, and the more groups to which one belongs, the more pronounced this effect is likely to be (Iyer et al., 2009).

Of the myriad of socially significant groups, the family is arguably the most critical for individuals’ resilience to life stress. Family identification (a subjective sense of belonging to the family) is associated with better life satisfaction, lower depression, lower perceived stress (Sani et al., 2012), less psychological distress (Miller et al., 2015) and lower paranoid ideation (Sani et al., 2017). The family’s importance for stress-related coping is especially pronounced in family-oriented cultures (Acero et al., 2017).

Family identification and family support play important roles in buffering the impact of stress and discrimination (Rodriguez et al., 2018). For instance, Acero et al. (2017) show that, across a range of qualitative investigations in different contexts, an individual family member falling ill promotes family solidarity because the illness is experienced collectively by the whole family (especially in collectivist cultures). Families also enhance well-being through participation and belonging: Hanke et al. (2016) found family identification (which predicted well-being) was fostered by participation in family celebrations. Families also provide continuity via traditions, which are positively associated with family functioning and psychological well-being (Herrera et al., 2011). These types of support are well-established in research that explores how group members cope with stress and trauma (see Drury, 2018; Kellezi et al., 2019).

There is also growing recognition of the way in which families can protect their members by providing longer-term sources of support and continuity. Fivush et al. (2008) found that telling family stories facilitates intergenerational experience sharing. This is beneficial for children’s sense of self, as it furnishes them with a sense of place and family identity. Family collective continuity can also be a source of resilience in stressful times as it provides enhanced intragroup connections, group esteem and purpose (Herrera et al., 2011).

However, just as collective processes within families (and within groups in general) can support well-being, they can also lead to vulnerability through their absence. Some previous research has shown that high levels of family judgement, unreceptiveness or lack of support while one member is experiencing stress negatively predict well-being (Parra et al., 2018; Rodriguez et al., 2018; Swartzman et al., 2017). This is partially explained by the family’s exposure to the individual member’s stressors adding to the distress of all members. Kellezi et al.’s (2019) research with immigration detainees shows a similar process: while families were a valuable source of support, some detainees decided not to seek that support for fear of burdening loved ones with their suffering. While families can be an important source of support during stressful times, they can potentially be a source of vulnerability in situations where support is lacking, or even a burden in situations where distress is shared.

In relation to financial stress, our previous research has shown that family identification does indeed predict lower financial stress (Stevenson et al., 2020). In two local community surveys, we showed how respondents’ family identification positively predicted well-being, which in turn was associated with better financial coping. In effect, family identification served to provide collective psychological resilience to dealing with financial challenges. However, this work was conducted in relatively affluent neighbourhoods where residents were largely economically active, and families could be expected to have the time and emotional, informational and practical resources to share. Research has yet to explore the effects of limited or absent social support on the relationship between family identification and financial stress, and so we turn to a particular residential area where households are known to lack these resources.

The current study

In the current paper, we develop our approach to consider families from a disadvantaged neighbourhood in Nottingham (UK), where household resources (including the ability to help fellow family members) are likely to be limited. We use a mixed methods approach to first quantitatively examine how family members report their family dynamics and financial stress and then follow this with a qualitative exploration of how individual family members from this same area talk about their experiences of coping with financial stress.

Following from the assumptions of SIAH, in Study 1, we predict that family identification will correlate positively with well-being (Haslam et al., 2018). In line with our previous work on families and financial stress, we secondly expect that family identification will predict less financial stress via improved well-being (Stevenson et al., 2020). Third, we predict this relationship will be contingent upon the receipt of family support, such that identifying with a family perceived as unsupportive will not confer these resilience effects upon participants. Finally, we expect that residents’ own accounts of their financial stresses and coping strategies in Study 2 will reflect these patterns and shed light on specific social perceptions and practices underpinning these dynamics.

Study 1

Materials and methods

Participants and procedure

One-hundred and forty-two residents from the St Ann’s area of Nottingham (UK) completed an online survey (58 identified as male, 83 identified as female, 1 unknown; Mage = 40.44 years, SD = 14.35, age range = 19–77 years) between 1st March and April 14, 2018. Power analysis with GPOWER (Erdfelder et al., 1996), assuming an alpha significance criterion of .05 (two-tailed), power of 80% and a medium effect size of .30, indicated a required sample size of 84.

St Ann’s was selected because it falls within the highest 10% of deprived English areas and has a reputation for marginalisation and disadvantage (McKenzie, 2015). Economic and health inequalities in the UK have increased sharply over recent decades as a result of austerity-based social and economic policies (Marmot, 2020). The city of Nottingham with its post-industrial economic structure has been particularly vulnerable to the ill-effects of deprivation, and St Ann’s has the highest number of both Incapacity Benefit and Income Support claimants in the city (McKenzie, 2015).

Postal invites were sent to all homes (N = 6500; 2.18% response rate) with a link to an online survey. Participants were entered into a prize draw for vouchers worth £50, £100 and £150. Ethical permission was granted by the lead authors’ institution.

Measures

Family identification was measured with Doosje et al.’s (1995) four-item scale. Participants rated their agreement with each item (e.g. ‘I see myself as a member of my family’) using a 1 (‘strongly disagree’) to 7 (‘strongly agree’) scale. The mean was obtained, with higher values indicating stronger identification (M = 5.90, SD = 1.57, α = .96).

Family support was measured with Haslam et al.’s (2005) four-item scale concerning emotional, instrumental and informational support. Participants rated their agreement with each item (e.g. ‘Do you get the emotional support you need from other members of your family?’; ‘Do you get the help you need from your family?’) using a 1 (‘strongly disagree’) to 7 (‘strongly agree’) scale. The mean was obtained, with higher values indicating stronger support (M = 5.45, SD = 1.84, α = .97).

Well-being was measured with the five-item WHO5 Well-being Index (WHO, 1998). Participants rated their agreement with each item with reference to the past 2 weeks (e.g. ‘I have felt cheerful and in good spirits’) using a 0 (‘at no time’) to 5 (‘all of the time’) scale. The mean was obtained, with higher values indicating better well-being (M = 4.02, SD = 1.20, α = .90).

Financial stress was measured with a scale used by Crandall et al. (2017). Participants rated their agreement with six items (e.g. ‘How stressful was difficulty meeting monthly payments on bills over the past 12 months?’) on a 1 (‘not at all stressful’) to 4 (‘very stressful’) scale. The healthcare payment stress item was removed, due to the UK having a National Health Service. One participant had one of these four values missing so it was replaced with the mean of the other three values. Two items were scored differently: ‘During the past 12 months, how much difficulty have you had in paying your bills?’: 1 = ‘no difficulty’ to 5 = ‘a great deal of difficulty’) and ‘Over the past 12 months, at the end of each month, do you generally end up with…’: 1 = ‘more than enough money left over’ to 4 = ‘not enough money to make ends meet’). The mean was obtained, with higher values indicating higher stress (M = 1.89, SD = 0.86, α = .92). Further information about this measure can be found in supplemental materials.

Finally, age, gender (1 = male, 2 = female), relationship status (0 = not in a relationship, 1 = in a relationship) and household income before tax (1 = £0–£18,500; 2 = £18,501–25,500; 3 = £25,501–£37,500; 4 = £37,501+; M = 2.46, SD = 1.17) were measured, with the latter measure representing the UK’s 2018 quartiles of net income (DWP, 2018). These variables are known to impact upon well-being and financial stress, so were conceptualised as control variables. More information about survey items can be found in supplemental materials.

Results

Plan of Analysis

After investigating intercorrelations, we explored whether there is a conditional indirect effect of well-being on the relationship between family identification and financial stress for participants experiencing high levels of family support.

Descriptive Statistics

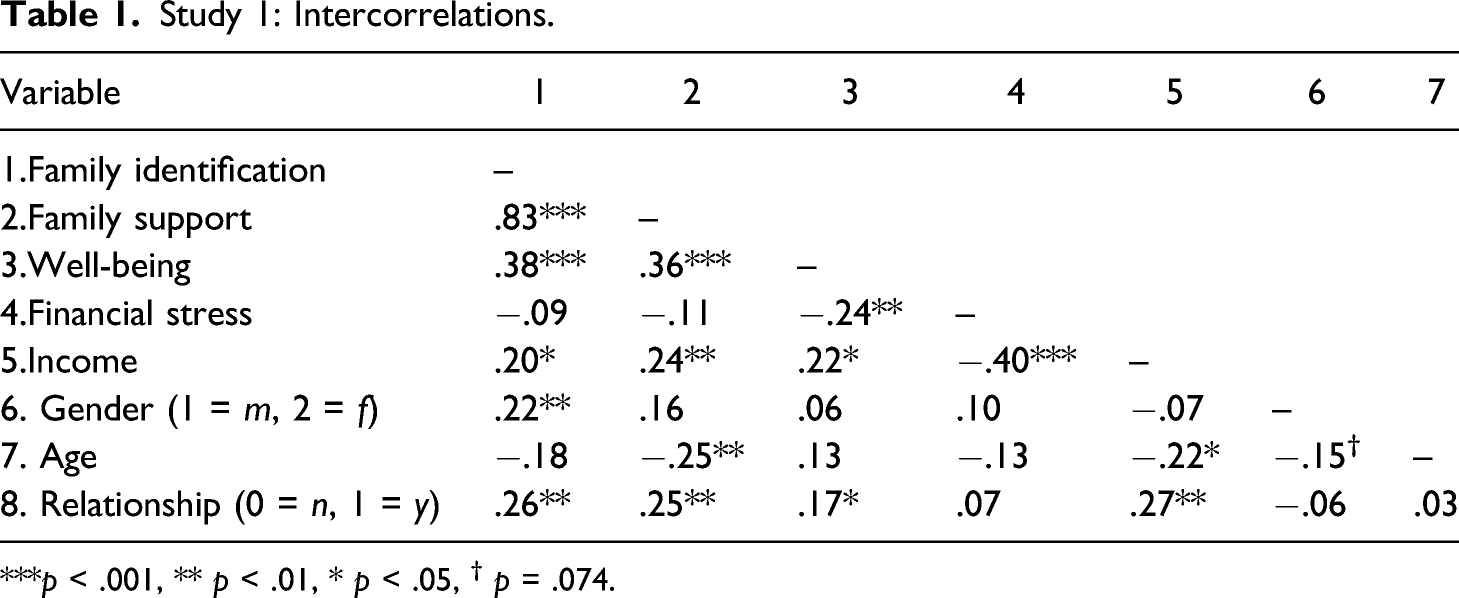

Study 1: Intercorrelations.

***p < .001, ** p < .01, * p < .05, † p = .074.

Conditional Indirect Effect Analysis

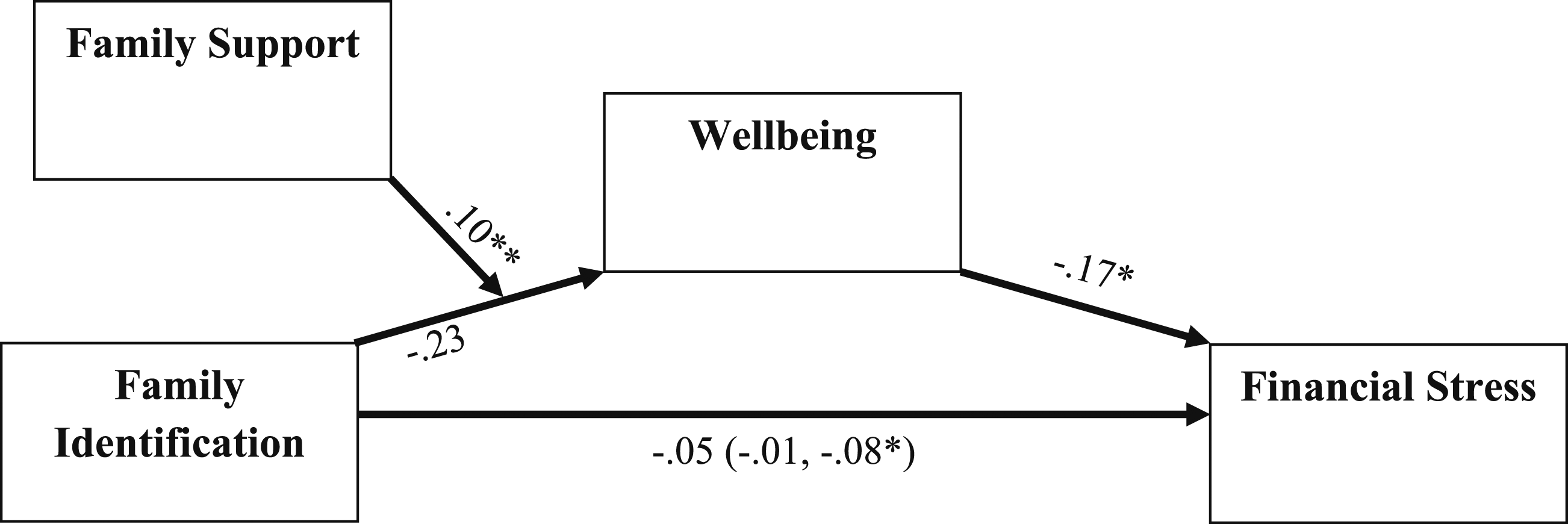

We used model seven in version 3.0 of Hayes’ (2017) PROCESS macro to test the prediction that there would be a conditional indirect effect of well-being on the relationship between family identification and financial stress for participants experiencing high levels of family support. This model (Figure 1) tests an indirect effect model (i.e. whether a predictor [family identification] predicts an outcome [financial stress] via a mediator [well-being]) and investigates whether the predictor-mediator path is moderated by a moderator (family support). The analysis involved 5000 bootstrapping samples with 95% confidence intervals (LLCI/ULCI), using the percentile method. Values were mean-centred for the construction of products. Age, gender and relationship status were controlled for. Income was omitted from the analysis as this variable was found to be too closely related to self-reported financial stress, resulting in the model becoming non-significant. Coefficients are unstandardised. Study 1: Depiction of model (control variables not pictured). Value on the moderator arrow (.10) is the predictor/moderator interaction; on the c path, value outside brackets is the direct effect and values inside brackets are the conditional indirect effect at low/high moderator levels, respectively. ***p < .001, **p < .01, *p < .05.

When the other variables were included in the model, family identification no longer predicted well-being (Coeff = −.23, SE = .16, t = −1.42, p = .16, LLCI = −.55, ULCI = .09), but the family identification/family support interaction did, thereby indicating that family support moderated the relationship between family identification and well-being (Coeff = .10, SE = .03, t = 2.93, p = .004, LLCI = .03, ULCI = .16). Well-being was a significant negative predictor of financial stress (Coeff = −.17, SE = .07, t = −2.56, p = .012, LLCI = −.30, ULCI = −.04. The direct effect of family identification on financial stress was non-significant (Effect = −.05, SE = .05, t = −.90, p = .37, LLCI = −.15, ULCI = .06), but the conditional indirect effect of family identification on financial stress through well-being was significant at high levels (+1 SD) of family support (Effect = −.08, Boot SE = .05, Boot LLCI = −.18, Boot ULCI = −.005), but not at low levels (−1 SD; Effect = −.01, Boot SE = .02, Boot LLCI = −.05, Boot ULCI = .03). The index of moderated mediation was significant (Index = −.02, Boot SE = .01, Boot LLCI = −.04, Boot ULCI = −.001). This index provides a test of the significance of a moderated mediation model (for details, see Hayes, 2015).

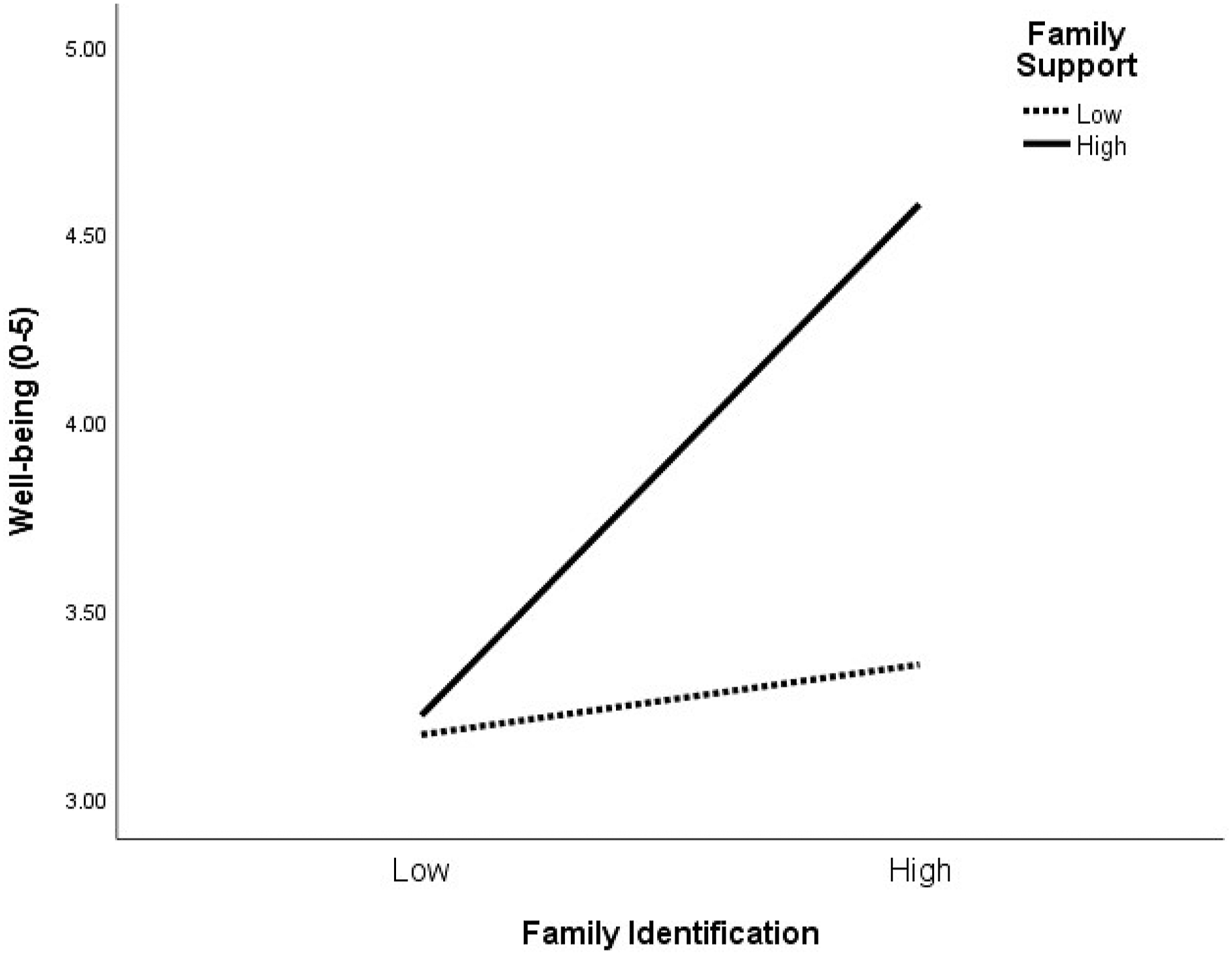

We used simple slopes to explore the moderating effect of family support on the relationship between family identification and well-being (Figure 2). Participants who received high levels of family support experienced a significant positive relationship between family identification and well-being (Effect = .45, SE = .15, t = 2.98, p = .003, LLCI = .15, ULCI = .75), while this relationship was non-existent for those who received low levels of family support (Effect = .06, SE = .11, t = .57, p = .57, LLCI = −.15, ULCI = .28). Study 1: Simple slope analysis of the moderating effect of family support on the relationship between family identification and well-being. ‘Low’ = −1 SD (p = .57) and ‘High’ = +1 SD (p = .003).

Discussion

Study 1 reveals that even after controlling for age, gender and relationship status, high levels of family identification predict high levels of well-being, but only for participants who perceive themselves as experiencing high levels of family support. In turn, high levels of well-being predict low levels of financial distress. These findings are consistent with the complex account of family identification presented in the Introduction: while there is evidence to support the idea that family identification is a key predictor of health and well-being (e.g. Sani et al., 2017; Wakefield et al., 2016), this relationship is not necessarily straightforward, especially in the context of stigmatised problems such as financial stress. While numerous studies within the Social Identity Approach to Health support the idea that social support is a key mediator of the relationship between group identification and well-being (e.g. Haslam et al., 2005), Study 1 hints at an important caveat to this model. Specifically, it assumes that the members of the group with which one identifies are willing and able to provide the support required to enhance one’s well-being, which then in turn predicts reductions in financial stress. As we have shown, participants who identified strongly with their family but for whom such support was not available experienced no better well-being than participants who identified weakly. Since we also found that low levels of well-being predicted higher levels of financial stress, this indicates that family identification is not always going to buffer against such stresses: group-related support must be available and accessible for such benefits to occur. We consider the theoretical and practical implications of these findings in the General Discussion.

Study 1 raises additional intriguing questions: what different types of social support do people receive or not receive from their families (e.g. emotional and financial), and how does the presence or absence of this support relate to feelings of well-being and financial stress? What contexts create the situation where people identify strongly with their family, but are unable or unwilling to receive support from them, and what are the implications of this for family relationships? To explore these issues in more depth, we conducted semi-structured interviews with residents of this same area.

Study 2

The aim of Study 2 was to support and expand upon Study 1 by addressing the aforementioned issues raised by Study 1, which we felt could be achieved effectively by exploring the lived experiences of St Ann’s residents via semi-structured interviews.

Materials and methods

Participants and procedure

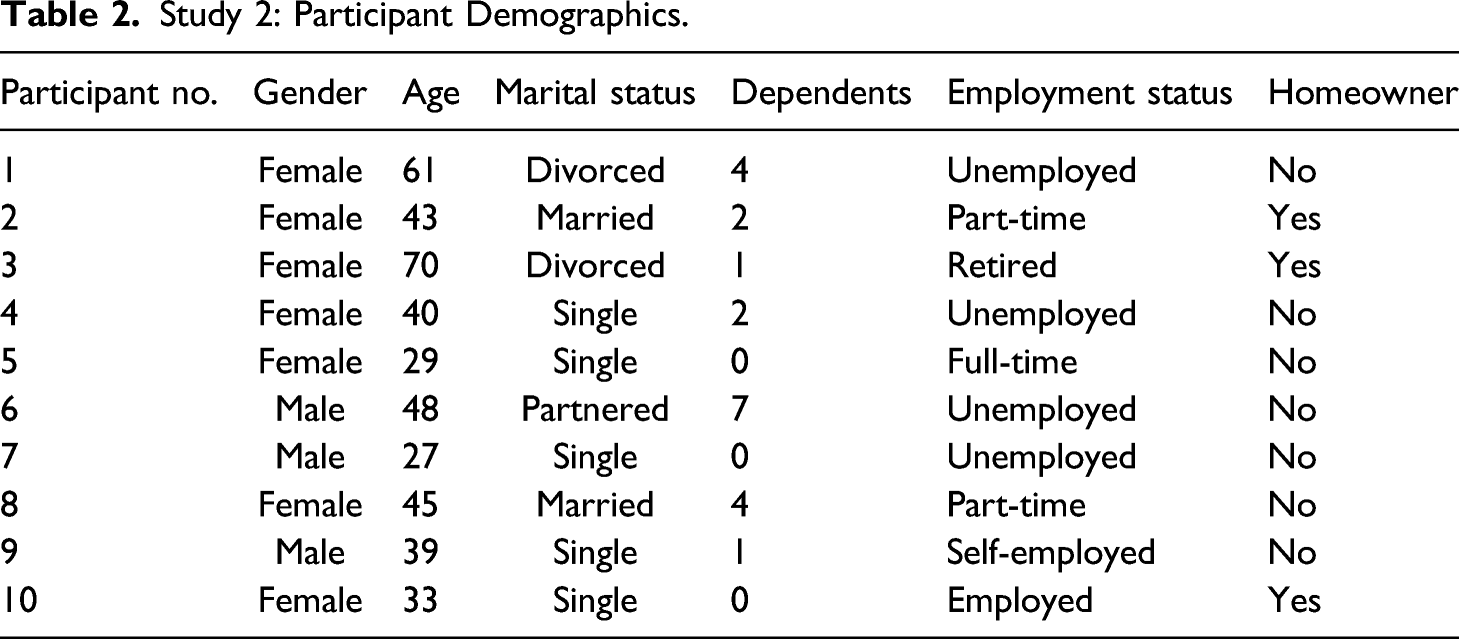

Study 2: Participant Demographics.

Interviews lasted 35–45 min and were recorded with the participants’ consent (after being informed their data would be anonymised). Ethical permission was granted by the College Research Ethics Committee of the lead authors’ institution.

Analytic Procedure

All interviews were transcribed verbatim. A theoretically driven thematic analysis was conducted, as outlined by Braun and Clarke (2006, 2013). Specifically, it adopted a deductive approach to shed light on theoretically based relationships identified in Study 1: those between family identity, family support, well-being and financial stress. After data familiarisation, the fifth author searched the dataset for extracts which had potential relevance to the research questions (i.e. all instances where participants discussed financial hardship and its relevance to their families). The fourth author, in collaboration with the rest of the team, categorised, sorted and resorted codes into possible themes through exploration and interrogation of the relationships between extracts and themes. Given the small number of diverse participants, the analysis’ key focus was to illustrate participants’ variety of experiences.

Results and discussion

Theme 1: Financial challenges and well-being

Participants reported a range of previous and current financial challenges that affected their lives. Most were unemployed or in low-paid work, and many experienced high levels of uncertainty as to future income. The resultant challenges ranged from inability to pay bills to being encumbered with debt.

In terms of financial insecurity, short-term insecure work was experienced as particularly corrosive to long-term financial planning: Participant 4: I’ve always felt insecure and even now on a regular basis my jobs never seem to last long so one minute I think I’m going to be alright because erm going to have money coming in a constant income to rely on and my benefits are sorted and everything’s ok, then the next minute I lose the job, for whatever reason and I’m back to square 1 and I have to start it all over again and its never stable for very long, its hard!

Financial insecurity also increased vulnerability to penalty. As one participant recounts, missing a single council tax payment resulted in a costly court appearance: Participant 9: like, council tax, trying to take me to court cos I missed one, I missed a payment and they say right now you’ve missed a payment you’ve got to got come to court. And then I say do I need to come to court really, I can pay it now, do you know what I mean. No no no you gotta come to court then I got to pay court fees and now I’ve got a debt with them because of this and that. Just, it’s just like, it’s just nonsense man, like ah, I can’t explain that kind of pressure it puts you under because it’s like.

For some, the continual financial struggle resulted in debt. This constituted an additional financial concern, often compounded by feelings of futility where repayments only ever covered the loan’s interest. Some found it very difficult to pay off debts: Participant 9: Yeah, what’s more stressful because that’s stressful still because obviously you don’t know when you coming, you’re just living from one debt to another, basically, do you know what I mean. Even when you’re getting paid every month you just go more and more in debt cos you can’t keep up with everything.

Participants described anxiety related to debt and finance management, as well as how the worry was leading to them feeling low and experiencing illness: Participant 6: Some days you can get up in the morning and think you know something I can’t even be arsed to go out today and I do feel like that some days but that’s part of life you know you have your ups and downs you feel ill you know everyone gets ill, and things like that you just had to take it day by day you can never book weeks ahead or days ahead because you can never know what’s going to happen the next day.

Savings were an important part of restoring financial stability and reducing anticipated future financial stresses. Participants described attempting to regularly save small amounts and the efforts they made to ensure they had money in hard times: Participant 4: My rainy day fund might be for if I’ve used a lot of electricity in the winter you know and I need a bit more for electricity or something like that you know.. it’s hard but I try my best and you just have to get on with it don’t you.

Saving was an important strategy to maintain control and address financial distress, but inability to save served as a further stressor.

In terms of other coping strategies, some participants described help-seeking reluctance: Participant 8: Well I never normally like to ask for help, I just like to get on with it there’s always a way. Sometimes you just try to just forget about what to think you want to the money to do and think about something in the meantime to occupy your thoughts and take your mind away from that and if you really want to money to do it just try and work towards it, I’ve had to sacrifice myself a lot of the time to do a bit of saving in order to do what I want to do.

For others, this reluctance centred on their perceptions of the source of assistance. Some refused to use foodbanks, even when poor diet threatened their health. Others admitted to using foodbanks, but declined to approach formal financial support sources: Participant 1: Oh yeah, I don’t use the foodbanks, they ask me at the hospital when I went, my potassium levels keep going too low so I end up in hospital because it affects my heart, so yeah. Participant 8: I mean I’d use foodbanks if I need to desperately, but I’d never go to the bank for help or anything like that.

However, there was one support source with which participants had a very different type of relationship: family. The next theme highlights the role of family in financial distress.

Theme 2: Family financial support and collective coping

The participants’ range of family relationships was broad: from fraught interactions to extremely close ties. Participants with strong relationships constructed their family as a unit where members engaged in reciprocal helping and financial support-giving. In these circumstances, support-provision was considered an explicit and expected responsibility: Participant 6: Family, family we have always been a strong family, my side we’ve always been close…..I wouldn’t go to a bank! No, I’ve got my family, I’d just ask my family, I don’t do interest rates I just ask my family and they do me and we help each other, that’s what families all about we help each other to live and survive really, so, we’ve all got to survive so.

Participant 6 describes the consistency and reliability of this support, its success and the reciprocal basis on which help is given and returned. Others who mentioned close relationships with family members described financial relationships which did not involve reciprocal giving, but instead relied on a responsibility to pay back money owed. These cases typically involved adult children borrowing from parents or more financially secure siblings: Participant 5: I was sort of playing catch-up I was trying to pay my mum and dad what I owe them, and that was all usual things, so all of what I’ve just said about the car, phone, bill, my loan I was paying off, it was everything that I had so I think I had… well I think my bills probably amount to about 500 a month and I was having to borrow that off my parents just to get by really. So obviously when I did get a job I had to pay that off and still continue to pay my car insurance at the same time.

Others described close relationships with family members which involved small financial gestures, but participants were clear that this was not explicit borrowing. One participant described how grandparents would give money to grandchildren; however, this was depicted as a treat rather than a necessity, and the participant was very clear that they had not requested money: Participant 8: I get money sometimes like my kids’ granddad gives my kids some money sometimes when we go and see, but like I’ve never asked for it, I never asked nobody.

Others expressed strong desires not to rely on family for financial support, as this would threaten self-reliance. For some younger participants, this was a statement of independence from parents, while for others, having to rely on family financial support would indicate poor financial judgement: Participant 7: Nope, no I’m financially capable of doing it myself, I do it all myself, I’m at the age now where I want to do it myself. Participant 9: I don’t like borrowing off nobody. Not my friends, not my family, not nobody. I’d rather think if it’s not in my possession it weren’t meant to be mine at that time, if I can’t, you know, afford to buy it or whatever.

As Participant 7 explains, while family can provide support, it is important to manage familial financial relations carefully. These positive and supportive relationships contrasted with others who described fraught familial interactions. The next theme highlights this, as well as the financial burdens deriving from family relations.

Theme 3: Family, financial distress and responsibility

Some participants reported an absence of family in their lives. This was sometimes due to breakup or physical distance and was often associated with a sense of isolation and vulnerability. Such absence was seen as contributing further to financial insecurity: Participant 4: No, I’ve got no family that can help me really...I followed the love of my life who lived in St Ann’s so I wanted to move there to be with him… No, I didn’t know anybody bar him, I didn’t know anybody else, I came here for him, he obviously had his family here who I met but I came here knowing no-one.

Some described family relations being strained, in part due to financial concerns. The conflict between family members led some to refuse to seek family support: Participant 8: But when it comes to my family, I’d say nothing to them, no I’d rather talk to a stranger than say anything to them, at the moment. No my family’s not really my family, they see me as a spoiled child as when my dad was around they thought I get everything I asked for and it was just jealousy so they’re not really my cuppa tea.

For parents and caregivers, family identification came with additional financial responsibility. This was reflected in terms of prioritising spending in order to meet dependants’ needs: Participant 6: I love my kids, I give them everything, I mean if I had my last penny and they wanted it they could have it, my kids are urmm…that’s what I’m here for, if I put them on this earth I have to support them.

This also had the consequence of increasing the financial pressure on carers, for whom the burden of saving to meet dependants’ basic needs exacerbated financial concerns: Participant 4: I mean I’ve got a jar I keep hidden in my house and then I just try to put into it as much as I can when I can, just for emergencies as well, like house repairs. I mean you never know when you might need something for a rainy day, for when you know anything you could happen, the kids are always getting holes in their shoes or growing out of them.

In some circumstances, family breakup was the catalyst for financial hardship. In addition to a reduction in the availability of familial support, breakup often resulted in difficulties surrounding work and childcare for the custodial parent: Participant 3: When I got divorced, and I erm it’s the first time I claimed benefits, I had to sign on, I had..to…I was working in the evenings with a 7 year olds child and when I got divorced he couldn’t be left at home, so I had to give the job up.

In sum, participants reported a range of financial concerns which arose from the absence of family, the financial burdens imposed by family or family breakup. In all cases, these served to reduce financial security and increase distress.

Discussion

Our participants were selected for diversity, in order to span as wide a range of financial hardship and family support experiences as possible. While other more in-depth studies of financial coping may attest to the prevalence of specific social and cultural practices, our analysis illustrates the variety of experiences. From this, we aim to shed light on the possible interpretations of the relationships between family identity, social support, well-being and financial stress uncovered in Study 1.

From participants’ spontaneous accounts, we note that this area is characterised by deep-rooted financial deprivation which pervades every aspect of residents’ lives and interactions. While residents can sometimes put aside these challenges to ‘just get on with it’, in the main these pose real barriers to participation in community life and present significant challenges to individuals and their families in maintaining a decent quality of life. Deprivation thus exacts a high cost on well-being.

Against this background, families can be a source of support in times of financial need. Families constitute an arena of intimacy for some, in which financial burdens can be shared as part of a broader understanding of ‘looking out for one’s family’. Others are keen to distance themselves from any associations with inappropriate financial dependency, or to complicate family relationships with the burdens of indebtedness or expectations of reciprocal giving. Thus, for these respondents, finance is generally considered bad for family relations.

However, for others, it is the lack of strong family relationships which fosters financial issues. Absence of family leaves an individual exposed to financial crisis: without a circle of reliable intimates, a financially vulnerable individual can lead a precarious existence, which promotes anxiety around financial threats. More subtly, family can itself constitute a financial threat. Expenses incurred by one family member can have seriously debilitating effects on others, while relationship breakup represents a major financial disruption to family members. Thus, through absence, dysfunction or dissolution, family can cost an individual dearly. We discuss the implications of these findings for theory and previous research below.

General Discussion

Research on the Social Identity Approach to Health has previously shown that family constitutes a fundamental social group for most individuals, shaping their sense of self, their world view and their ability to cope with the challenges (Sani et al., 2012, 2017; Miller et al., 2015). Conversely, research on the FSM (Conger et al., 2010) has shown the potential for financial stress to undermine family cohesion with corrosive effects on the health and well-being of family members. Our work here provides further evidence for the important relationship between family cohesion, well-being and the experience of financial stress. However, it also progresses our theoretical understanding of the relationship between these elements by further attesting to the ability of family identification to predict both well-being and lower stress and by illustrating the key facilitating role of social support in this set of relationships.

In line with strengths-based approaches to family financial resilience (Benzies & Mychasiuk, 2009; Stevenson et al., 2020), our quantitative findings support the contention that the well-being of family members is pivotal to their ability to cope with financial challenge, suggesting that even in deprived communities, more cohesive families can provide mental resilience to cope with stress. Our qualitative findings converge upon this conclusion, illustrating that close-knit families can indeed provide support to enable members to cope with financial challenges, while the absence of this cohesion can be a source of emotional distress and financial vulnerability.

However, our findings also point to an important caveat in this relationship. In the absence of family support, identification does not predict well-being and, in turn, does not predict the reduction of financial stress. In other words, the benefits of family identification upon well-being and financial stress appear to be contingent upon the presence of support from other family members. Unlike previous research which demonstrates the negative impact of family membership when families are rejecting or judgemental (Rodriguez et al., 2018; Swartzman et al., 2017), this lack of positive relationship occurs where there is an absence of support. It is worth recalling that this result occurs after controlling for gender, age or relationship status and so pertains across a broad range of family memberships.

Our qualitative analysis sheds light on why this might be the case. In line with previous analyses (Charles & James, 2005), family financial dynamics are complex, such that even when ties are close, support may not be forthcoming. Some respondents did indicate that their families lack the basic resources to help them, even if they needed it. Others indicated that they themselves were the source of financial support to other dependants in their families, with children, non-earning adults and older relatives potentially relying on them for financial support. However, in line with Kellezi et al. (2019), others indicated that they perceived seeking financial assistance as shameful, burdensome, or as having the potential to place strain upon family ties, making them unwilling to taint relationships by seeking this form of support. In other words, there is a range of specific situations in which family identification does not alleviate financial stress, due to the lack of support sought or received from family members.

Theoretical Implications

The theoretical implications are twofold. For the Social Identity Approach to Health, this research points to the need to consider if groups can provide support to their members in order to help them face threats and challenges. If they cannot, this might provide a barrier to group processes benefitting health and well-being, which in turn suggests that economic and other forms of material deprivation may have suppressant effects on the benefits of group processes (see also Evans et al., 2008). Second, it draws attention to the particularly corrosive effects of economic deprivation, as previously noted by Stevenson et al. (2014): stigmatised forms of disadvantage can undermine support processes by inhibiting intragroup support-seeking and giving. The shame associated with financial deprivation may thus deny familial assistance to those who need it most. Third, for the Family Stress Model (Conger & Conger, 2002), it indicates that over and above the individual level effects of economic stress, the corrosive impact of financial deprivation may emerge from its ability to undermine the family’s collective coping mechanisms. In line with previous research which has highlighted the negative impacts of judgement, unreceptiveness or lack of support from family members during crises (Rodriguez et al., 2018; Swartzman et al., 2017), the inability or unwillingness to give or receive support in times of financial need may have an additional negative impact on family members’ mental health.

Limitations

Our research has several key limitations which cause us to qualify our results. Perhaps most notably, the target community possesses a number of distinctive characteristics. St Ann’s has the highest number of Incapacity Benefit and Income Support claimants in Nottingham and suffers from a negative reputation which means that residents often mistrust outsiders and shy away from inquiries. Hence, while we can be confident that the area is afflicted with a high level of deprivation, our samples are likely to be highly self-selecting and may not represent their wider community, or similar communities across the UK.

Further work is thus required to determine the replicability of our findings in other communities. Indeed, future research should attend to the relationship between neighbourhood and family groups including extended family inside and outside of the local neighbourhood. Moreover, longitudinal survey and interview work is required to determine if identity-based relationships impact on participants’ ability to cope with future financial challenges. Future work should also record and examine the potential impact of participants’ race/ethnicity, sexual orientation and disability status.

Policy Implications

Our work has several tentative policy implications. First, in light of the negative health effects of austerity policies such as those imposed in the UK (Marmot, 2020), reducing financial support to the most economically vulnerable families may serve to further undermine their self-sufficiency. Our work implies this because it shows that families possess collective coping capabilities, but it also shows that without the necessary resources they will not be able to use these capabilities effectively: families need help to help themselves. Second, agencies providing financial advice and support to individuals (such as the UK’s National Association of Citizens Advice Bureaux) should appreciate the complex and variable impact of stigma upon how individuals and families respond to financial difficulty. Our work implies this because it shows that, for some individuals, embarrassing financial issues are kept within the family, even when the family does not possess the resources required in order to provide effective help. Others keep finance and family separate, even when they might benefit from familial support. Either way, our work suggests that the stigma of financial disadvantage hinders the group dynamics of seeking and receiving support, and this finding implies that the challenge for financial services is to recognise, negotiate and overcome this barrier. Our findings suggest that achieving this goal would facilitate a significant improvement to the well-being of some of the most economically deprived families.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Open Research Statement

As part of IARR’s encouragement of open research practices, the authors have provided the following information: This research was not pre-registered. The data used in the research cannot be publicly shared but are available upon request. The data can be obtained by emailing the corresponding author (