Abstract

This article interrogates the extent to which tax laws are capable of empowering Indigenous peoples. It employs the concept of an Indigenous tax space, which places spatiality at the center of the settler colonial project. The socio-legal history of the Native Village of Kluti Kaah, an Ahtna tribe from southcentral Alaska, constitutes the main case study. In 1987, the tribe attempted to tax the Trans-Alaska Pipeline that passed through its traditional lands, creating an Indigenous tax space wherein tax law and discourse congregated to express and enact Indigenous agency. The article argues that the Indigenous tax space (1) provides a rare opportunity to reappraise the geographies of tax laws and policies and, more broadly, (2) allows us to explore settler colonialism’s previous and ongoing effects upon Indigenous territories.

On 20 November 1996, the Court of Appeals for the Ninth Circuit released two crucial decisions that concerned two Alaska tribes: the Native Village of Venetie Tribal Government (Venetie) (Alaska ex rel. Yukon Flats School Dist. v. Native Village of Venetie Tribal Government, 1996) and the Native Village of Kluti Kaah (Kluti Kaah) (Alyeska Pipeline Service Co. v. Kluti Kaah Native Village of Copper Center, 1996). 1 The former can be found west of the Wrangell Mountains, on the right bank of the Copper River and a stone’s throw from Copper Center; the latter comprises Arctic Village and the Native Village of Venetie, two remote and scattered Gwich’in villages within interior Alaska. The two cases were addressed under the same inquiry: whether Indian country—land owned by the US government on behalf of American Indians, otherwise known as trust land—still existed in Alaska under the Alaska Native Claims Settlement Act (ANCSA), which settled Native land claims in 1971 (Alaska Native Claims Settlement Act [ANCSA], 1971). 2 In Indian country, which includes “reservations,” “allotments,” and “dependent Indian communities,” 3 tribes can exercise a plethora of “inherent” powers, as polities whose sovereignty “has never been extinguished” (original emphases) (US Department of the Interior, 1979: 895; see Newton et al., 2012).

One such power is taxation, which the tribes tested against outsiders circa 1986–1987, at a time when many wondered whether ANCSA lands still were Indian country. Venetie attempted to tax a contractor working on the school building in the Native Village of Venetie (Zahnd, 2023c). Meanwhile, Kluti Kaah had turned its attention to the portion of the Trans-Alaska Pipeline (the pipeline) that ran through Ahtna lands. It specifically targeted the Alyeska Pipeline Service Company (Alyeska), the “operator of the Trans-Alaska Pipeline System” (Alyeska Pipeline Service Co. v. Kluti Kaah Native Village of Copper Center, 1996: 612).

The combined judicial fate of the tribes came to an abrupt end on 20 November 1996, when the court in San Francisco decided that only one should prevail. On that day, Venetie entered Native American legal history, having been granted the potential to revise the scope of Indian country on the one hand and rejuvenate it within Alaska on the other—a prospect that made the State of Alaska shudder (Goldberg, 1997). The rest of Venetie’s story is well documented. The state retaliated with unmatched resources, spending a million dollars to ensure the case reached the US Supreme Court (Goldberg, 1997). Eventually, state officials obtained the court decision they needed to quell the looming spread of Indigenous sovereignty over a space they had no intention of sharing. On 25 February 1998, the nine justices unanimously decided that ANCSA lands no longer were Indian country (Alaska v. Native Village of Venetie Tribal Government, 1998). Be that as it may, on 20 November 1996, when the three judges of the Court of Appeals decided both cases, Venetie had land that was still Indian country, or, more precisely, “dependent Indian community.” But Kluti Kaah no longer did.

At first glance, the two cases look very much alike. Both tribes used the same tax, a business activity tax (BAT), which loosely resembled a consumption tax (Office of Tax Policy, 2007). They also enacted a similar tax system—including a tax code, a dedicated tax court, and a tax commission (Zahnd, 2023c). That was no accident. Both tribes were assisted by two lawyers from the Native American Rights Fund, a Colorado-based non-profit law firm taking test cases nationwide to empower Native American tribes (Zahnd, 2023c). But their resemblances end there. Indeed, each tribe had experienced and reacted to settler colonialism very differently. And space was a key component of their respective history. If Venetie had managed to protect its land base and observe the rise of Alaska as a new settler polity from a relatively safe distance, Kluti Kaah had been consistently entangled with settler colonialism. In broad outline, space was doomed either to be protected or reclaimed, and both Gwich’in and Ahtna territories had been under attack. Yet one question lingers: Why deploy taxation when the legal status of post-ANCSA lands was still blurred? In other words, were the risks too high, as the court decisions ultimately demonstrated?

While Venetie has garnered much scholarly attention (e.g., Carpenter, 1999; Chrisbens, 1998; Ford, 1997; Mitchell, 1997; Zahnd, 2023c), Kluti Kaah has largely fallen through the cracks of Native American legal history. The reason lies in the unfavorable ruling its case received from the Court of Appeals. An adverse court decision is simply less worthy of chronicling and analyzing. Nevertheless, following the work of other scholars who understand the extra-legal importance of lost judicial battles (Boutcher, 2005; NeJaime, 2010), I posit that we should tell the socio-legal history of the tribe not as a companion to Venetie’s but on its own merits. Kluti Kaah’s BAT not only provides yet another example of Indigenous resistance and agency 4 ; it also took place in different circumstances. 5 Most importantly, the tribe’s tax case epitomizes a central feature of Alaska history: the profound socio-legal and spatial impact of oil development on Indigenous sovereignty. Therefore, this article offers a vignette of colonization on the edge of “US settler imperialism” (Arnett, 2018). It is a story that resembles many others because a tribe had been subsumed into what Meredith Alberta Palmer calls a “settler sovereign landscape,” that is, “particular racial and spatial orderings of people and things” (Palmer, 2020: 794) to which US laws greatly contributed to achieving (Palmer, 2020).

Consequently, this article interrogates the extent to which tax law is able to empower Indigenous peoples. In doing so, I put forth the idea of an Indigenous tax space, which places spatiality at the center of the settler colonial project. In doing so, I draw on scholarship on the political and socio-legal role of tax laws and policies in (settler) colonial contexts (e.g., Dennison, 2012; Likhovski, 2017; Sheild Johansson, 2018; Willmott, 2020). In present-day Canada, for example, Kyle Willmott (2022) asserts that the “informal political life of tax” conspires with other ingredients of governmentality, thereby boosting the socio-political clout of the settler state. In the USA, Jean Dennison (2014) demonstrates how tax belongs to what she calls “whitewashing,” namely “a variety of techniques utilized to assert and justify settlement” that bolster settler colonialism’s innate and continuing effort to “eliminate” Indigenous Peoples (Dennison, 2014: 163, citing Wolfe, 2006).

But taxation, several scholars have underscored, can be resisted, dodged, or even used against colonialism (e.g., Manse, 2021, 2022; Redding, 2006; Scott, 2009; Zahnd, 2023a, 2023c). Emily Levitt (2018) analyzes the ways in which tax recently took center stage in upstate New York in the relations between the Cayuga Indian Nation and the non-Indian municipality of Seneca Falls (and, more broadly, Seneca County). The tribe’s rejection of local taxation, she explains, disturbed the deeply engrained and enduring “political imaginary of American citizens” (Levitt, 2018: 70), forcing it to reopen discussions about the place of Native American Indians within a settler society that struggles to accept them both as sovereigns and US citizens (Levitt, 2018; see also Kiel, 2019).

Resistance can also take a radically different form. Around 1974, on the Alaska North Slope, the Iñupiat established a local government, the North Slope Borough, to gain political and economic power on the one hand and to uphold their cultural identity and way of life on the other (Zahnd, 2014). Yet the Borough could exist and thrive through only its ability to tax the very oil reserves that prompted the enactment of ANCSA (Zahnd, 2014). This indigenized local taxation was a cunning way of circumventing federal Indian law that, Robert Porter (1998) argues, has strived to make settler colonialism permanent. By engaging with this body of scholarship and chronicling the spatio-legal history of Kluti Kaah, I make the case for the more positive aspect of tax: its potential to empower and serve Native American tribes rather than settler polities. In fleshing out this argument, I focus on tribal taxation—namely, tribes’ ability to design, enact, and use tax systems upon their members and outsiders (US Department of the Interior, 1979: 445; see Merrion v. Jicarilla Apache Tribe, 1982).

The article also draws on and engages with the work of scholars who have teased out the spatial dimension of settler colonialism and Indigenous sovereignty (e.g., Carroll, 2014; de Hinojosa, 2021; Dillon, 2022; Harris, 2002; Mawani, 2003; Nadasdy, 2012; Parmenter, 2010; Sizek, 2021). These scholars, hailing from a wide range of disciplines, have endeavored to depict and analyze how spatiality underpins the way broader colonial and anti-colonial processes unfold. Thomas Biolsi (2005), for instance, proposes to “reimagine the political space of the nation-state” from the vantage point of Native American tribes and their citizens, as sovereigns compelled to concede powers to others for the former and as members of both a tribal polity and its settler counterpart for the latter. This rescaling comprises “four kinds of indigenous space imagined, fought for, and, to a remarkable extent, achieved and lived by American Indian people in the United States in the present” (Biolsi, 2005: 240; see also Bruyneel, 2007).

The Indigenous tax space is a space wherein tax law and discourse congregate to express and enact Indigenous agency. As such, the notion of this space helps shed light on two points. First, it offers a much-needed yet often neglected alternative for reappraising the “legal geographies of settler and deeply divided multiethnic societies … between such states and their indigenous peoples” (Kedar, 2014: 110). In the case of Kluti Kaah, their desire to summon tax brought critical aspects of tribal sovereignty and identity in relation to space to the fore, ranging from self-determination to jurisdiction and to decolonization. To be sure, tax and space are inherently entangled. “Fiscal geographies,” Liza Rose Cirolia (2020: 34) remarks, “illuminate the multi-scalar and dynamic nature of state-form.” The Indigenous tax space thus can contribute to exploring the spatiality of tax and the “mediating” role (Cameron, 2006: 237) it plays in the relationship between a polity and its taxpayers (Cameron, 2006). Above all, this space holds the potential to unpack the “tax imaginaries” (Makovicky and Smith, 2020) of both tribes and other key stakeholders—including the federal government, state and local governments, and non-Native taxpayers.

Second, the Indigenous tax space helps shed light on settler colonialism’s past and ongoing effects upon Indigenous territories, as it offers the opportunity to look at the history of a tribe anew so that one can understand the “historical legal geography” (Delaney, 2017) in which tribal taxation was enacted (see also Zahnd, 2023c). Therefore, this space provides a novel vantage point from which one may reappraise the complex, entangled, and historically rooted legal geographies of Indigenous sovereignty and settler colonialism (Zahnd, 2023c).

The following sections chronicle the history of an Indigenous tax space, that of Kluti Kaah, from its origins to its enactment and then to when its right to tax was withdrawn by the Court of Appeals. 6 Together, they demonstrate that behind its judicial defeat lay this tribe’s unwavering resistance to colonization; a resistance and agency the BAT bolstered and helped express for the world to see.

The gradual colonization of the area: Institutionalizing settler colonialism

When prospectors found copious quantities of gold in the Klondike in the evening of the nineteenth century, the surge of newcomers to the area was almost instantaneous (Arnold, 1976: 72–73; Gruening, 1954: 103–104; Naske and Slotnick, 2014: 125–128). Copper Center, which the gold-seekers established in 1898 at the confluence of the Klutina and Copper rivers, was the product of this migration (Cole, 1993: 37; Kozely, 1963: 3). 7 The town was conveniently located on the way from Valdez to the Klondike and interior Alaska, offering prospectors and their cargo much-needed rest and shelter (Cole, 1993: 27–44). The Richardson Highway increased the transportation between the coast and the interior that passed through Copper Center (see Cole, 1993: 28; see generally Naske and Slotnick, 2014: 146, 148). As well as the highway, a railroad and steamboats would be developed to facilitate the expansion of mining activities (Simeone, 2018: 166). Game animals such as moose and caribou, on which the Ahtna depended, were the first victims (Haycox, 2002: 208; Simeone, 2018: 166).

The federal government attempted to protect Alaska Natives from colonization, albeit with little success. The 1884 Alaska Organic Act laconically stated that “the Indians or other persons … shall not be disturbed in the possession of any lands actually in their use or occupation or now claimed by them” (Alaska Organic Act 23 Stat. 24 (1884): 26). These property rights, which non-Natives routinely ignored (Banner, 2007: 307–314), would remain the rule until the enactment of ANCSA (Banner, 2007: 13; but see notes 2 and 5). Meanwhile, successive game laws failed to protect subsistence hunting and fishing (Simeone, 2018: 178–180; see Zahnd, 2023b).

Settler colonialism continued to intensify its stamp upon Ahtna territory. On 16 April 1917, special employee for the suppression of liquor traffic Joseph Bourke wrote an alarming letter to Alaska Governor Strong. Bourke (1917) was worried about the “destitute position” which ensnared many Natives in the area. “The whole trouble,” he (1917) reasoned, “is due to the fact that the salmon, their [i.e., the Ahtna’s] natural food, is not now obtainable.” The culprits were the canneries that had been burgeoning in the area (Bourke, 1917). Governor Strong (1917) promptly forwarded Bourke’s letter to Secretary of the Interior William Redfield, who quickly responded. “[T]here is the broad question of policy as to whether a fishery enterprise which produces food for the world at large must be made to suffer in order that 300 Indians can secure a supply of fish easily,” Redfield (1917) pondered. It is not difficult to fathom the Secretary’s opinion on the matter. The Ahtna would have to make way for resource extraction at the expense of their livelihood and cultural identity. “It is well known,” the Secretary (1917) added, “that the natives of the Copper River are about as shiftless as any in Alaska and that they are prone to complain unless they can secure salmon with but little effort.”

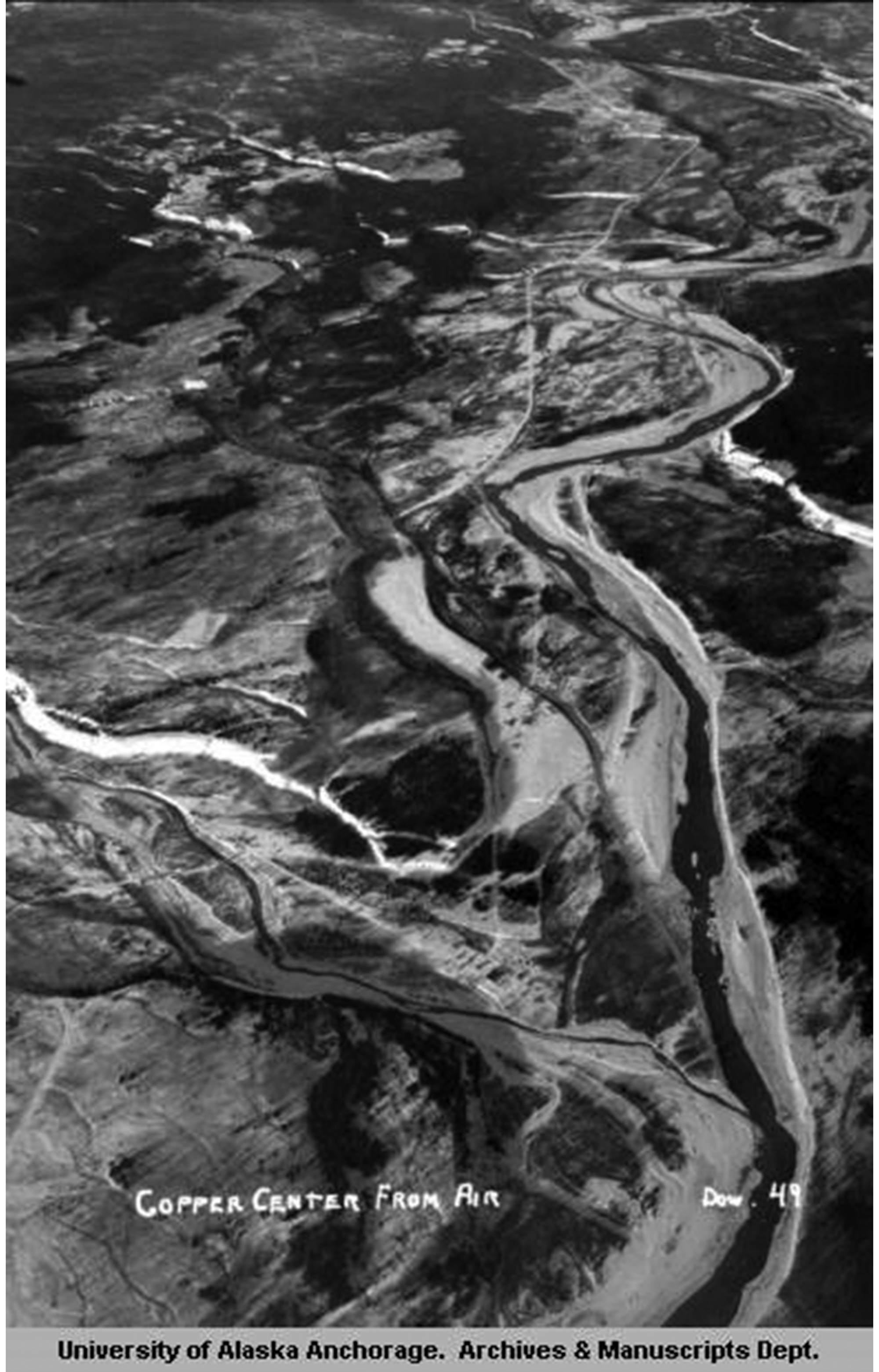

Kluti Kaah, an Ahtna settlement, would gradually form a few miles north of Copper Center, which was its non-Native counterpart (see Figure 1). In 1905, the US government established a reserve of about 1000 acres for the federally run Native school (Case and Voluck, 2012: 87, note 31; Cole, 1993: 67–72; Kozely, 1963: 3), which, as it did elsewhere in Alaska, assisted in curbing nomadism and “civilizing” Alaska Natives (Case and Voluck, 2012: 201–211; Zahnd, 2023a). 8 But the school did not only impact children. “[A]ll able-bodied natives receiving aid,” acting Commissioner Lewis Kalbach (2011) reported to Alaska Governor Walter Clark in 1911, are “required to furnish fuel for the school or to perform some other labor for the benefit of the school or village.” The Native community thus grew while being spatially (and culturally) separated from the white settlement, with the school as its center of gravity (Cole, 1993: 78–81). Meanwhile, the Bureau of Education helped the Ahtna create a governing body, the village council, in the early 1930s (Cole, 1993: 88–89), although Ahtna elder Harry Johns (n.d.: point 6) stressed: “[t]here has been a Native Council here in Copper Center since 1915.” Nevertheless, the formal establishment of the tribal council marked the beginning of a new, remapped space that became more politicized and territorialized. Copper Center then comprised two areas; one Native, the other mainly white.

View of the non-Native area of Copper Center at the bottom of the photograph and the Native area at the top, 1937. Russ Dow papers, 1917–1992. UAA-HMC-0396. University of Alaska Anchorage, Consortium Library, Archives & Special Collection.

Alaska became a state on 3 January 1959, and could select as much as about 103 million acres of land “from the public lands of the United States in Alaska which are vacant, unappropriated, and unreserved at the time of their selection” (Alaska Statehood Act, 1958: Section 6(b); Naske and Slotnick, 2014: 249). 9 The land selection, however, had met Indigenous resistance (Anderson, 2016a; Arnold, 1976; Case and Voluck, 2012: 167), eventually leading to a halt on the selection process from the Secretary of the Interior in 1966 (Arnold, 1976: 114–118; Case and Voluck, 2012: 166–167). The dispute was resolved in 1971 with the enactment of ANCSA, thereby returning over 45 of the 365 million acres that Alaska Natives were claiming (Case and Voluck, 2012: 167–168).

The main impetus behind ANCSA was the state’s need to develop the recently discovered and seemingly infinite oil reserves that lay beneath the North Slope (Case and Voluck, 2012: 167; Landreth and Dougherty, 2011/12: 322). 10 The settlement of the land claims consisted of a cash payment to Natives and the establishment of numerous Indigenously owned corporations that would hold the land in fee simple (Arnold, 1976; Case and Voluck, 2012: 165–198). More precisely, “the State of Alaska [was] divided … into twelve geographic regions, with each region composed as far as practicable of Natives having a common heritage and sharing common interests” (ANCSA, 1971: Section 7(a)). The Act established a corporation for each region, as well as a 13th corporation for out-of-state residents, and each Alaska Native village had its own corporation as well (ANCSA, 1971: Sections 7 and 8; Flanders, 1989: 302). Thus, ANCSA created “two tiers” of indigenously owned corporate entities (Hirschfield, 1992: 1331). Regional corporations could then select a portion of the returned lands within their assigned territory, and so could each village corporation (ANCSA, 1971: sections 7 and 12; Flanders, 1989: 302), making rural Alaska Natives shareholders in both.

With ANCSA, the government ensured that Native claims would never resurface to plague oil exploitation (ANCSA, 1971: Section 4(c)). Indeed, many believed the land claims settlement buried Indian country—including all reservations—once and for all, henceforth turning it into corporate-owned private property (Case and Voluck, 2012: 109; but see Case and Voluck, 2012: 391). 11 In Ahtna territory, a regional corporation—Ahtna, Inc.—was established in 1972 (Simeone, 2018: 193) with eight village corporations, including that of Kluti Kaah in Copper Center (Simeone, 2018). In 1980, Kluti Kaah, which was struggling financially at the time (Hirsch, 1998: 123), merged with its regional corporation, and the Native Village of Kluti Kaah Council became “the successor organization” (Alyeska Pipeline Service Co. v. Kluti Kaah Native Village of Copper Center, 1996: 611–612). In the process, Kluti Kaah transferred land ownership to Ahtna, Inc. (Hirsch, 1998). ANCSA thus provided the Ahtna and other Alaska Natives with land ownership. However, Kluti Kaah no longer owned land directly; instead, tribal members owned land through holding shares in Ahtna, Inc.

A plan to build a pipeline took form shortly after oil was found on the North Slope (Haycox, 2016: 84–85). The Trans-Alaska Pipeline System (TAPS), which Alyeska would later manage (McBeath et al., 2008: 216), took a little more than three years to build. 12 However, the tribe and its territory were not left undisturbed, for “[a]pproximately seven miles of the Trans-Alaska Pipeline passes through the region” (Alyeska Pipeline Service Co. v. Kluti Kaah Native Village of Copper Center, 1996: 611) along the Richardson Highway and west of both Kluti Kaah and Copper Center (Reckord, 1979: 101). From that point forward, the tribe’s territory would lie between the Copper River and the two constructions, the Richardson Highway and the pipeline. In Copper Center, existing spatial segregation underwent profound sociocultural and economic changes (Reckord, 1979: 214): this novel tribal landholding revitalized the Ahtna’s economic and political influence (Reckord, 1979: 177). As a result, tensions among the tribe and the once affluent and influential non-Natives surfaced regularly (Reckord, 1979: 126). Yet friction also occurred amongst the Natives themselves. When some tribal members returned to the area to work for Alyeska, ideological divides over economic development and Indigenous governance were routine (Reckord, 1979: 212–217).

The “portion of the region [where the pipeline was built],” the Court of Appeals noted, “was originally exempted from land available for Natives to select under [ANCSA], because Congress sought to preserve a Pipeline corridor, unencumbered by Native land claims” (Alyeska Pipeline Service Co. v. Kluti Kaah Native Village of Copper Center, 1996: 611–613). This space, within which Indigenous laws and claims had no force, was meant to protect oil exploitation. Consequently, a form of “colonial enclosure,” sustained by “US settler law” and meant to carry out spatial conquest (Curley, 2021b), ensued. “However,” the Court added, “after Ahtna, Inc. and the local Native corporations [including Kluti Kaah] concluded an agreement [in 1974] with Alyeska, the Secretary of the Interior revoked the order exempting this land” from Native selection. Alyeska had indeed “agreed to support the revocation of … [the] federal Pipeline right-of-way”; i.e., the pipeline corridor. “Ahtna, Inc. now owns the land,” the Court concluded, “but it remains subject to a federal right-of-way for the Pipeline” (Alyeska Pipeline Service Co. v. Kluti Kaah Native Village of Copper Center, 1996: 611–613). The enclosure surrounding the pipeline, then, existed to facilitate oil exploitation, which itself was made possible by ANCSA. Conspicuous signs such as gates, fences, and warnings 13 were erected around the corridor to preclude access and exacerbate a Native/non-Native dichotomy. They marked a fixed boundary between two spaces—an Ahtna space and its non-Ahtna counterpart—that were never to overlap.

This was hardly a novel strategy. Enclosures have been widely used in settler colonial locales to reallocate to non-Natives sought-after natural resources. In his study of Indian water right settlements, Andrew Curley (2021b) suggests that “colonial enclosures,” in fact, “fundamentally change a people’s relationship with their environment and ecology.” In the same way, by modifying Ahtna territory, the corridor profoundly changed how both humans and non-humans lived on and moved across the land, thereby disturbing long-established hunting and fishing territories. But worse was to come. The pipeline, the non-Native town of Copper Center, and the Richardson Highway constituted what Andrew Curley (2021a) calls a “colonial beachhead;” that is, an entanglement of settler colonial structures materializing as “a temporal encroachment on Indigenous lands and livelihoods, over time, to augment material and political difference that eventually overwhelms Indigenous nations and curtails certain possibilities” (Curley, 2021a: 2). From the enactment of weak property rights to adverse game laws to the 1905 reserve and, finally, to ANCSA (just to mention a few of the legal processes it used), federal Indian law had brought together all the ingredients necessary to isolate the Ahtna and cement settler colonialism within the area.

The relationship between the tribe and Alyeska began to deteriorate in 1978 when most Ahtna employees were “discharged” (Simeone, 2018: 198). The company had broken the 1974 agreement (or “service contract” (see Hirsch, 1998)) that had addressed the land issue as well as its pledge to “provide employment for Ahtna Natives” (Alyeska Pipeline Service Co. v. Kluti Kaah Native Village of Copper Center, 1996: 613). As a response, Ahtna, Inc. used its status as landowner to contest the pipeline corridor. The corporation barred entrance to the corridor (Simeone, 2018: 198) while stressing the destructive footprint of the pipeline on land and wildlife, and its impact on the Ahtna way of life (Simeone, 2018: 199). Although the dispute was resolved by agreement between the parties, such episodes contributed to escalating resentment, including in and around Copper Center, toward Alyeska and settler colonialism.

In 1984, James McKinley, a traditional chief from Kluti Kaah, was given the opportunity to express his concerns at the tribe’s annual meeting. “Right now,” he cautioned the tribal Council, “the pipeline and that road [i.e., the Richardson Highway] will push you down to the river and there will be no more room to move.” “[I]t’s like that already, now we can’t move anymore,” he bemoaned (Copper Center Village Council, 1984b). By taxing Alyeska, the tribe would address this encroachment on Ahtna space as well as concerns about the impact of the pipeline on the land and wildlife (Simeone, 2018: 198–199); it would also attack the ways the jobs offered by the oil company had diminished people’s ability to return to subsistence hunting and fishing, should they need to (Simeone, 2018: 199).

The enactment of the Indigenous tax space

In January 1985, about two months after the tribe had enacted its first constitution (Native Village of Copper Center, 1984), tribal administrator James Segerquist unveiled the rough outline of a tax he had designed to impose on the pipeline (Copper Center Village Council, 1985a). The tax, which was discussed at a tribal council meeting, was intended to “lev[y] and collec[t] a tariff of one-half mill ($0.0005) on each barrel of oil transported over lands governed by the Native Village of Copper Center, Alaska” (Native Village of Copper Center, 1985a: Section 1). Segerquist did not, however, specify what the phrase “lands governed” referred to. Given the tribe’s recent history with the pipeline, it seems reasonable to assume that both he and the Council (if not most tribal members) did not feel they were bound by the legal—and restrictive—meaning of tribal jurisdiction (see Pasternak, 2014, 2017; Richland, 2021).

The geographical scope of the intended tax underscored Segerquist’s two distinct yet intertwined intentions: finding a way to raise continuous revenue and addressing the pipeline’s social, economic, and environmental footprint. Moreover, the tribal administrator knew that if the tribe wished to reach the legally enclosed pipeline and receive revenue, then the jurisdiction of the tax would need to encompass the space through which it passed. Spatiality and political claims thus coalesced to emerge and thrive through the instrument of taxation. The tax was intended to defy US law and, by extension, settler colonialism. Logically, then, the deliberately vague geographical scope of the tax was meant to embrace the Ahtna’s whole spatial and cultural identity; to remap and reclaim their traditional territory.

Kluti Kaah was not the first tribe that had sought to tax outsiders who wished to extract and sell natural resources. A few years earlier, the Jicarilla Apache Nation led the way towards tribal tax sovereignty, winning a pivotal judicial battle against 19 oil companies operating within its reservation. In 1982, the US Supreme Court ruled that “[t]he power to tax is an essential attribute of Indian sovereignty because it is a necessary instrument of self-government and territorial management” (Merrion v. Jicarilla Apache Tribe, 1982: 137). What seemed unthinkable a few decades previously, that is, asserting tax sovereignty over outsiders and gaining the Supreme Court’s approval to do so, finally had become an invigorating reality to tribes that had access to a taxable economic base. Three years later, the Supreme Court reiterated its support of tribes and their power to tax. This time, the justices upheld the taxes the Navajo Nation had enacted to raise revenue from oil and gas companies—the first two taxes of its modern history as a tribal government (Kerr-McGee Corp. v. Navajo Tribe of Indians, 1985; see Krakoff, 2009). And even though the tribe had designed these taxes to target oil and gas companies, both prevailed in the Supreme Court. One of these taxes was a BAT.

The Jicarilla’s success resonated strongly in Copper Center. On 2 April 1984, the Council first considered the possibility of taxing the pipeline (Copper Center Village Council, 1984a). When Segerquist presented his ordinance several months later, he explicitly mentioned the recent victory of the Jicarilla as a reason why Kluti Kaah should try to tax the pipeline (Native Village of Copper Center, 1985a: accompanying text). Nevertheless, two significant hurdles loomed large over his plan. Unlike the Jicarilla (and the Navajo), ANCSA had heavily endangered the fate of Indian country and, consequently, that of territorially based sovereignty over non-Indians. Furthermore, the pipeline would probably remain immune to legal attack because the federal right-of-way protected the corridor. To make the matter more intricate, Segerquist was no tax expert. Conscious that the structure of his proposed tax could not fully protect its core purpose, he swiftly decided to seek outside assistance. Two lawyers, Lare Aschenbrenner and Bob Anderson, responded favorably to the tribe’s request. As it turned out, Segerquist and the tribe could not have picked better allies.

The two attorneys, who opened their office on 1 October 1984 (Native American Rights Fund (NARF), 1975: 4), did not work independently. They were staff members of a much larger Colorado-based legal organization: NARF, a non-profit charitable organization (NARF, 1980: 12) that was not new to Alaska Natives. It first gained popularity when assisting the Iñupiat in obtaining their public local government—the North Slope Borough—in a particularly tense post-ANCSA climate (NARF, 1975, 1984: 4). More cases followed, strengthening NARF’s (1980) reputation as a pro-Native rights juggernaut (Carpenter and Wald, 2013; NARF, 1984: 4). The Alaska office would continue the work NARF had started with the Iñupiat: to ensure that ANCSA would not endanger tribal sovereignty, identity, or territoriality (NARF, 1984).

Timing was on the side of Kluti Kaah. Over a period of just a few years, Anchorage welcomed several key lawyers who would swiftly become decisive players in defending tribal rights and cementing “the modern era of ‘tribal self-determination’” (Targ, 2006) in Alaska. Just like their predecessors who had led the “tribal sovereignty movement” throughout the contiguous United States (Roy, 2017; see Carpenter and Wald, 2013), these individuals were prepared to go to court with one case at a time, in the name of Indigenous empowerment and for the greater good. Lloyd Miller was one such individual. Soon after starting his career, he opened the first Alaska office of a prominent Washington, D.C.-based US law firm; and it would not take long for him to become one of the foremost experts in Alaska tribal law. 14 David Case would also shape the course of tribal sovereignty in Alaska. In 1984, he published Alaska Natives and American Laws (Case, 1984), which instantly became a reference in the field and helped many lawyers and tribes uphold Alaska Natives’ rights and sovereignty. Although Case held a visiting position at the University of Alaska Fairbanks, he remained, first and foremost, a lawyer committed to representing Alaska tribes. Meanwhile, in October 1984, Aschenbrenner and Anderson opened NARF’s Alaska office on K street, in the heart of then-bustling downtown Anchorage (Aschenbrenner, 2016; NARF, 1984: 4). Aschenbrenner and Anderson, the tribe’s future counsels, would also become the principal architects and proponents of tribal self-determination.

Aschenbrenner worked for NARF from 1977 to 1982, mainly in the Washington, D.C. office (NARF, 1980: 89, 1983: 15). He then left NARF temporarily to be the Navajo’s Deputy Attorney General from 1982 to 1984 (Aschenbrenner, 2016). During his tenure, he had the opportunity to follow through the tribe’s quest to assert its power to tax. When the Supreme Court finally settled the matter on 16 April 1985, Aschenbrenner had already left his position with the Navajo to return to NARF and spearhead the opening of its Alaska office (Aschenbrenner, 2016). Yet he did not remain oblivious of the Navajo’s victorious day, which they would henceforth celebrate as “Navajo Nation Sovereignty Day” (Krakoff, 2009: 36). More importantly, he bore in mind that the BAT was among the two taxes that successfully survived the decade-long fight of the Navajo (Aschenbrenner, 2016). Thus, Aschenbrenner quickly determined that a BAT, with its broad scope (see Office of Tax Policy, 2007), could access Alyeska’s profits under the guise of a general tax policy toward Ahtna and non-Ahtna businesses (Aschenbrenner, 2016).

Aschenbrenner, Anderson, and Kluti Kaah joined forces to design the tax code that the tribe would enact on 4 October 1985 (Copper Center Village Council, 1985b). It was thus agreed that the Navajo BAT would serve as a model for Kluti Kaah. Aschenbrenner contacted the Navajo Nation to inquire about the tax’s intricacies (Aschenbrenner, 2016) and started to transplant it to Alaska. Meanwhile, Ahmed Kooros, an expert in pipeline economics, was hired “to provide advice and consultation in connection with the preparation and implementation of the village’s business activity tax” (Kooros, 1987: 3). Kooros, who had previously worked with Native American tribes, including the Navajo Nation (Kooros, 1987: 2), recommended a “reasonable tax rate” of 5 percent (Native Village of Kluti-Kaah, 1988: 2), and was the first person to translate the fiscal power of the BAT into tangible numbers. According to his approximation, the tribe could levy about half a million dollars yearly (Kooros, 1987: 3).

On 4 October 1985, Kluti Kaah enacted the first version of its tax code, which comprised two chapters. The first chapter, entitled “Business Activity Tax,” laid out the contours of the tax, while the second described how the tribe would implement it (Copper Center Village Council, 1985b, 1985c). In March 1986, a Tax Commission followed (Copper Center Village Council, 1986a). The tax was very complex and had little resemblance to the one James Segerquist had initially designed. Both chapters totaled 116 sections, most of which came from the 1984 version of the Navajo BAT. Aschenbrenner and Anderson had turned a two-page ordinance into a 61-page tax code in a relatively short time. They and the tribe expected the freshly enacted BAT to generate a substantial stream of revenue, precisely $462,486.43, that Alyeska alone would contribute annually (Kooros, 1987: 3).

Tax revenues, sovereignty, settler colonial history, and Ahtna empowerment

A month after the code's enactment, Kluti Kaah modified the tribal constitution, making its power to tax explicit (Native Village of Copper Center, 1985b). With a last piece of fine tuning, 15 everything was finally ready to field test the BAT in January 1987. However, unlike the Jicarilla or the Navajo, Kluti Kaah had to contend with a much weaker case of tribal sovereignty over non-members. With possibly no Indian country to sustain it, the tax could have been doomed to a swift and uneventful death. But neither the tribe nor the attorneys were willing to accept this fate, and the tax encapsulated two complementary contentions: the tribe’s desire to reclaim its territory and the attorneys’ refusal to accept that ANCSA had legislated Indian country in Alaska out of existence once and for all. Yet hope remained. To save Indian country and ipso facto territorially based tribal sovereignty over non-members, ANCSA had only left one option worth fighting for: whether dependent Indian communities still existed. To Aschenbrenner and Anderson, the BAT provided the perfect opportunity to generate a lawsuit and determine whether that possibility could become a reality (Anderson, 2016b; Aschenbrenner, 2016). Hence, their goal was twofold: (1) to help the tribes prevail and implement their tax system, and (2) to test the post-ANCSA scope of tribal sovereignty and jurisdiction (see also Zahnd, 2023c).

Accordingly, the attorneys and the tribe ensured that the Indigenous tax space would defy US law. The “Territorial jurisdiction of the Copper Center Village,” the tax code stated, “means all lands constituting Indian country over which the Copper Center Village Council exercises governmental authority including but not limited to, lands owned by the Copper Center Village” (Copper Center Village Council, 1985c: Section 146). With the reimagined territorial scope of this new tax, Kluti Kaah blatantly attacked the pipeline’s enclosure. But if the tribe wanted its claim to be taken seriously by most outsiders (including by US courts), the potential vastness of the Indigenous tax space needed to be clearly delineated. In other words, Kluti Kaah had to demarcate the area within which it exercised “governmental authority” (Copper Center Village Council, 1985b). It needed to show concretely where settler colonialism had encroached the most on Ahtna territory.

The Council, therefore, added that “the efficient and effective administration and enforcement of Tribal Tax laws, as well as administrative convenience, requires that the territorial extent of Tribal Tax laws be specifically defined, and readily identifiable by those subject to such tax.” The Indigenous tax space was thus expected to specifically consist of “the area most heavily used and occupied by the Native people of Copper Center Village and upon which they are most dependent.” This area, the Council continued, “includes that portion of the Copper River Basin adjacent to the confluence of the Copper and Klutina Rivers located within Township 2 North, Range 1 West and Township 2 North, Range 1 East, Copper River Meridian” (Copper Center Village Council, 1985b). Logically, the area encompassed the native and non-native parts of Copper Center, including most non-native businesses that lay within it. It also included a significant portion of the pipeline and the tribe’s main hunting and fishing grounds, which extended well beyond Copper Center. In short, the Indigenous tax space comprised the land that needed the most urgent, radical remapping. What that space signaled, therefore, was that whether the lands were Indian country or not was irrelevant. What truly mattered to the tribe, and what should have mattered at all, was to have a space that suited its cultural identity and way of life but also ensured its fiscal prosperity.

The Indigenous tax space was as much inward looking as it was outward looking. It addressed non-Natives both within and beyond Copper Center. Copper Center, a town that had previously been spatially segregated, had undergone profound changes, mainly because ANCSA and the pipeline had reshuffled power relations between the Ahtna and non-Ahtna (Reckord, 1979: 177). In doing so, Reckord (1979) points out, the two colonial apparatuses had inevitably disturbed the previous order of things, thereby reversing the long-established, non-Native economic and political dominance while exacerbating racial and cultural divisions. Although the town still resembled its old self, the content of its spatial layout had evolved considerably. The Ahtna had ceased to be the powerless and landless (at least from the strict viewpoint of land ownership) neighbors of seemingly more influential non-Natives. ANCSA and oil had made the tribe and its members wealthy landowners via Ahtna, Inc., who henceforth had greater control over the area. Their newfound economic power had dramatically transformed outsiders’ perceptions of their sovereignty. Paradoxically, as Jessica Cattelino (2010) explains, the existence of both wealth and tribal sovereignty in one group tends to confuse outsiders, who perceive that wealth precludes sovereignty (see also Lewis, 2019). The tax exacerbated this “double bind of American Indian need-based sovereignty” (Cattelino, 2010). Nevertheless, the tax law sought to reconnect these two elements that outsiders wanted to split. The Indigenous tax space re-Indigenized tribal power and governance by giving post-ANCSA Kluti Kaah jurisdictional means over its territory.

The tribe, the resolution that enacted the code explained, had chosen to unambiguously connect the fate of the tax to that of the pipeline. “[T]here have been,” the Council began, “numerous changed conditions over the past few years, many if not most of which attributable to the construction, operation and maintenance of the Trans Alaska Pipeline System from Prudhoe Bay to Valdez, Alaska by Alyeska Pipeline Service Company.” And “these changed conditions,” it added, “have caused numerous negative effects, both direct and indirect, upon the Native People of Copper Center Village.” The Council carefully went on to elaborate these “numerous changed conditions.” The pipeline, it first lamented, was responsible for “the almost total destruction of the Copper Center moose population and widespread decimation of other fish and wildlife upon which the Native people of Copper Center have depended for subsistence since time immemorial.” 16 The Council then turned its attention to the skyrocketing, non-Indian population that the pipeline had attracted since its construction, and more particularly on the “negative social consequences” that had ensued ever since. These “include[ed],” for instance, “increased crime, use of drugs, alcoholism, unemployment, racism, and a relentless assault upon the culture and way of life of the Native people of Copper Center” (Copper Center Village Council, 1985b).

The tribe did more than merely enumerate the pipeline’s dire effects on its land. It explained that Kluti Kaah had had to adjust its role as a polity to protect its members’ wellbeing from an overwhelming non-Indian presence and at the same time provide the newcomers with appropriate public services and infrastructures. “[T]hese adverse effects and changed conditions,” the Council stated, necessitate new housing, roads, sewers, water systems, utilities and the entire infrastructure that civilization requires, including, for example, the establishment of courts, additional police, fire protection, juvenile officers, recreational facilities for young and old and the entire array of public services in the fields of health, education and welfare.

Hence, the resolution crystallized both fiscal and non-fiscal endeavors in one instrument. First, it was obvious that a steady stream of revenue would benefit Kluti Kaah for years to come. After all, as long as oil kept flowing and was sufficiently valuable to be worth extracting and transporting, the pipeline would remain physically embedded in its surrounding habitat. James Segerquist would later explain that “my idea when I drafted this ordinance [i.e., the first tax] was to obtain money for the tribal government, village government.” “That was my duty,” he added. “I thought, [my duty] was to try to sustain our government by—with grants [sic], taxes and whatever was available” (Segerquist, 1990). Alyeska was a substantial and easily targetable taxpayer. In this case, its very immobility had left the tribe in a predicament. On the one hand, the pipeline unarguably offered an extraordinary opportunity to ensure substantial tax revenue. On the other hand, however, it had also created many of the “changed conditions” that had precisely given rise to the need to raise additional revenue, as the tribal resolution explained (Copper Center Village Council, 1985b). In other words, the pipeline was both the cause and the solution.

Second, James Segerquist’s statement should not overshadow or undermine his own (and the tribe’s) broader goal. Indeed, it was clear that the Council was attempting to use this means to put forth a solid political manifesto. Levying a tax represented their powerful and unyielding wish to express their sovereignty in Ahtna territory. At the time, what the tribe sought to assert was both grand and bold. ANCSA had compelled it to question the future breadth and depth of its sovereignty. Indian country, the prerequisite for territorially based tribal sovereignty over non-members was not guaranteed post-ANCSA survival. With its proposed tax law, Kluti Kaah had carved out a space where federal Indian law gave way to tribal law.

This radical conception of sovereignty echoes Audra Simpson’s “refusal” to accept settler colonialism (2014: 11), because the Indigenous tax space mandated outsiders to acknowledge Indigenous sovereignty and cultural identity (Simpson, 2014). In doing so, therefore, the space revitalized tribal agency de facto. Tax law and discourse shook the established legal and extra-legal frame that settler colonialism had been implementing on these groups for decades. Tribal empowerment, which Aschenbrenner and Anderson helped take material form, was possible only because of the tribe’s unfaltering faith in its sovereign status—a sine qua non-prerequisite to becoming sovereign in the eye of outsiders (Porter, 2002). “Only if there is belief,” Porter reasons (2002: 106), “will the moat get dredged, only if there is belief will the drawbridges be drawn up, and only if there is belief will the longhouse be rebuilt.” Indigenous sovereignty was thus formed around the “belief that an Indigenous people have in their own sovereignty” and the “ability of an Indigenous people to take action to carry out their belief in their own sovereignty.”

In a similar vein, Angela Riley (2006: 961) has advocated “living sovereignty,” which, she explains, entails that “tribal governments—if they seek to be treated as sovereigns—ought to act accordingly, without allowing the colonial powers to limit their vision of governance.” With the assistance of the attorneys, Kluti Kaah could not have been more resolute. The tax encapsulated the tribe’s willingness to reclaim sovereignty within a space that had eroded its sovereignty for too many years, together with the attorneys’ eagerness to fight for the future of tribal sovereignty throughout the state. The Indigenous tax space also pointed towards the overall failure of settler colonialism and its assimilative agenda, demonstrating that a “nested” (Simpson, 2014) sovereignty could survive multidimensional and ongoing encroachments—and even fight back.

Nevertheless, Porter adds an essential caveat to Indigenous sovereignty. To have teeth, he cautions, belief must be “recognized and respected” (2002: 102). This warning underscores the “interdependent” (Cattelino, 2008) or “entangled” (Dennison, 2012, 2017) nature of sovereignty. As a result, sovereignty is a “practice that further imbricates you with other polities” (Dennison, 2017: 687). Neither the state nor Alyeska believed in tribal sovereignty. But Kluti Kaah did. Meanwhile—and somewhat ironically—the two attorneys Aschenbrenner and Anderson relied on Porter’s third prong of sovereignty. They needed Alyeska and the state of Alaska to disbelieve in Ahtna sovereignty so litigation could ensue. The pipeline epitomized the fact that “all parties become ensnared in ongoing negotiated compromises, which are both full of strain and mutually beneficial, often at the same time” (Dennison, 2017: 686). In the case of Kluti Kaah, it was essential to regain jurisdictional power for political reasons, while fulfilling more pragmatic economic needs. The tax revenue would have facilitated and bolstered the implementation of sovereignty.

As a space that, to outsiders, conjured both present-day issues and open critiques of past colonial processes, the Indigenous tax space allowed Kluti Kaah (and the attorneys) to address—and potentially harness—the spatial, economic, political, and sociocultural imprint of settler colonialism upon Ahtna territory using tax law. It was also a discursive tool that gave Kluti Kaah the power to speak to those who rarely listened and, in the process, confront them with the fact that colonization had failed to “eliminate” (Wolfe, 2006) the Ahtna from their homeland.

Yet what Kluti Kaah attempted to do was somewhat risky. Alyeska was a significant employer in the area and thus was potentially able to destabilize tribal power. And to make the matter even more complex, the service contract that bound the company to Ahtna, Inc., the regional ANCSA corporation, concerned not only Kluti Kaah’s tribal members but also those from other Ahtna villages (Hirsch, 1998: 176). As Brian Hirsch (1998) points out, the contract generated much-needed revenue for the regional corporation, which subsequently was passed down to surrounding villages and their Ahtna inhabitants as dividends. And although Kluti Kaah had its own political quest, Hirsch (1998) adds, it was possible that other tribes had different views on the matter. In fact, the situation of the other tribes was rather uncomfortable. On the one hand, they could potentially reap the benefits of Kluti Kaah’s quest for Indigenous sovereignty—although not directly, as they needed to have an economic base substantial enough to enact a tax system that would generate revenue (Hirsch, 1998). On the other hand, however, the amount of the dividend they received from Ahtna, Inc. depended greatly on its contract with Alyeska (Hirsch, 1998).

The Indigenous tax space bore witness to sovereignty’s multifaceted dimensions and pragmatic shortcomings while exacerbating inter-tribal relationships and generating diverging ideologies and interests. On 9 January 1987, the Copper Center Village Council formally informed Alyeska of its imminent intention to levy the BAT (Copper Center Village Council, 1987), but to no avail. 17 Instead, the company struck back in the US courts: arguing, among other things, that Kluti Kaah was not a tribe (i.e., not a sovereign polity) and that it could not exercise jurisdiction over non-members because it lacked territorial sovereignty (i.e., Indian country did not exist) (Alyeska, 1987: 10–11). The year after Kluti Kaah lost the case in the Court of Appeals, Alyeska, perhaps still infuriated with the tribe, terminated its two-decade old service contract with Ahtna, Inc. (Hirsch, 1998: 177).

If the Indigenous tax space appeared to be a straightforward response to the pipeline, it was ANCSA that provided the central motives behind the enactment of the tax—both for the tribe and the attorneys. To the former, the act led to a realignment of economic power within Copper Center and an opportunity to revitalize tribal laws and governance. The latter saw it as the very essence of their motivation for designing the tax system, hoping for a chance to fight for the Indian country status of post-ANCSA lands in court (see Zahnd, 2023c). But the Indigenous tax space also was the byproduct of a much longer history. Well before the advent of ANCSA and the pipeline, colonization had already sprinkled waves of systemic change throughout the area. And by analyzing this history, we can see how the fight for tribal taxation and the space it created bolstered Indigenous agency and pointed towards settler colonialism’s overall failure to erase Indigenous sovereignty and cultural identity.

Footnotes

Acknowledgements

First and foremost, I am grateful to tribal administrator Katherine McConkey, who generously granted me access to some of Kluti Kaah’s documents. I thank the three anonymous reviewers for their insightful comments, as well as Tariq Jazeel and Natalie Oswin for their editorial support. Thanks are also due to Catherine Albiston, Jessica Cattelino, Seth Davis, Gráinne de Búrca, Miriam Driessen, Mark Gergen, Manuel A. Gómez, Shari Huhndorf, Nanna Kaalund, Bryan Lintott, Fernando Pastor-Merchante, Morgan Seag, Karen Seif, Elizabeth Walsh, and the 2019–2020 Berkeley Empirical Legal Studies Fellows, for their thoughtful comments and suggestions on earlier drafts. Finally, the Hauser Global Law School Program at NYU Law provided me with much-needed support to write and finalize the version submitted to the journal.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.