Abstract

This article examines how racial capitalism intersects with platform capitalism through the rise of rental platforms and corporate landlords in the post-apartheid housing market. Combining 18 months of fieldwork in Cape Town with the spatial analysis of sales and longitudinal census data, I demonstrate how rental platforms enabled the consolidation of the private rental sector and the emergence of corporate landlords through the classification of tenants centered upon credit scoring. To automate tenant screening solutions, rental platforms leveraged and extended the information dragnet knitted by credit bureaus. This dragnet of unprecedented depth and volume is built upon the infrastructures and devices that enabled the for-profit, racial classification of people, housing and neighborhoods during colonialism and apartheid, notably ID numbers. In the context of racialized indebtedness and housing inequalities engineered by racial property regimes, the use of platforms to sort the “good” from the “bad” tenant and manage rental portfolios shifts mechanisms of segregation and reproduces racialized patterns of capital accumulation across the post-apartheid city. The article argues that rental platforms extend the extractive logic of racial capitalism through two joint rentier mechanisms: the transformation of rental housing into a new asset class; the extraction and assetization of rental data.

Introduction

As cities become increasingly mediated by digital technologies (McNeill, 2021), real estate platforms, otherwise labeled as PropTech, reshape power dynamics and value chains across the real estate industry, affecting how housing is accessed, traded, financed and managed across urban housing markets (Fields and Rogers, 2021; Shaw, 2020). By reconfiguring actors and practices along a “data imperative” (Fourcade and Healy, 2017), real estate platforms interrogate both the making of markets and the renewal of inequalities in the digital era. Given that property markets have historically engineered segregation and unequal wealth accumulation through the racial categorization of people and places (Dorries et al., 2022; Taylor, 2019), a critical line of enquiry investigates how color-blind, yet racially biased, digital technologies (Benjamin, 2019) renew inequalities stemmed from housing markets (Fields and Raymond, 2021; Sadowski, 2020), while forging the rentier structures of platform capitalism through the extraction and enclosure of data (Sadowski, 2019). These joint patterns of platformization and rent exploitation are particularly acute in the rental market, where institutional investors leverage digital technologies to facilitate the transformation of housing into an asset class (Crowell, 2022; Fields, 2019; Nethercote, 2023; Wainwright, 2022; Wijburg et al., 2018).

The interest for data and computers is nothing new for the real estate industry (Sawyer et al., 2014): real estate platforms amplify a historical appetite for fine-grained information in order to value people, housing and neighborhoods through metrics of risk and profit. What seems rather unprecedented is the capacity of platforms, by collecting large volumes of data to classify goods and consumers (Burrell and Fourcade, 2021) to change market structures and upscale the process of social differentiation, a key driver of value creation under capitalism. Real estate platforms unfold precisely across housing markets where differentiation through class (Bourdieu, 2005) and race (Korver-Glenn, 2021) is key to the formulation of value, notably by dispossession and predatory inclusion (Dantzler, 2021). In that sense, platforms question how racial capitalism intersects with platform capitalism as modalities of exclusion and inclusion are renewed under algorithmic opacity (McMillan Cottom, 2020).

This article examines how racial capitalism intersects with platform capitalism through the rise of rental platforms and corporate landlords, focusing on the post-apartheid housing market in South Africa. Connecting urban studies with economic geography, I build upon the three-stage framework developed by Fourcade & Healy to conceptualize how digital technologies reconfigure markets and inequalities (Fourcade and Healy, 2017): adjusting to a “data imperative”, firms first deploy and plug onto an “information dragnet” to harvest digital traces of consumer behaviors. Second, data is fed into scoring algorithms that rank consumers into market-based categories of risk and profit. This classification results in unequal market opportunities and fuels inequalities, producing a “new regime of moralized social classification, backed by algorithmic techniques and dependent on large volumes of quantitative data” (Fourcade and Healy, 2017: 9). The paper argues that rental platforms, powered by the classification of tenants through credit scoring, consolidated a surging private rental sector and allowed the emergence of corporate landlords, thereby renewing the extractive logic of racial capitalism while shifting the mechanisms of urban segregation.

Most of the scholarship on racial capitalism in South Africa is focused on labor and debt (Torkelson, 2021; Webb, 2021), echoing the pioneering theoretical formulations that acknowledged the centrality of cheap black labor and the forced labor system for South African racial capitalism, especially in the mining sector (Levenson and Paret, 2023; Wolpe, 1972). Yet South Africa offers a “paradigmatic instance of a settler political order founded on a racial regime of ownership” (Bhandar, 2018: 185). Racial capitalism was recently taken up by scholars to analyze the urban geographies of South Africa, in particular the legacy of apartheid (Chari, 2021; Desai, 2022; Melgaço and Xavier Pinto Coelho, 2022). In this article, I seek to highlight how the housing market constitutes, aside labour, a foundational site of racial capitalism through the racial ordering of people, properties and places under colonialism and apartheid. This state-driven, for-profit enterprise of classification through racial categories was enabled by the early use of digital technologies, notably to compute ID numbers. This paved the way in the 21st century for the rise of rental platforms and the use of credit scores computed in a context of racialized debt and housing inequalities.

To trace the social structures and technical factors through which racial capitalism intersects with platform capitalism requires to dissect both the legacies and contemporary mechanisms of the housing market. But if the post-apartheid city epitomizes extreme levels of segregation and inequalities, the functioning of the market remains largely unaccounted for, despite recent studies on developers’ practices (Todes and Robinson, 2020) and housing financialization through the rise of mortgage securitization (Migozzi, 2020). This research gap is explained by the characteristics of the South African housing landscape, characterized by enduring informality and the choice of the post-apartheid state to privilege homeownership as a pillar of social justice and poverty reduction. Urban studies focus primarily on the design and delivery of government-subsidized housing policies (Cirolia, 2015; Lemanski, 2011; Oldfield and Greyling, 2015) that promoted homeownership and turned away from the provision of social rental housing (Mabin and Parnell, 1983). Informal housing remains a major topic of pressing social issues as backyard dwellings and informal settlements constitute a dominant property regime for the urban poor (Cirolia et al., 2017; Lemanski, 2009). As a consequence, the market constructed by banks, developers and real estate agencies, where transactions are registered by the Deeds Office, or where tenancy is regulated through lease agreements, remains overlooked. If this market segment essentially caters for the upper quartile of the population in terms of income (over 15,000 rands a month – approximately US$800), it encompasses a large spectrum of the post-apartheid city, from low-income townships to wealthy luxury estates. Given the rise of real estate platforms, this market constitutes a laboratory to understand how racial capitalism intersects with platform capitalism in reshaping the technological political economy of housing.

The first section of the article lays out key articulations between real estate platforms and racial capitalism in the making of housing markets, foregrounding the early use of technology to enforce racial property regimes. The second section examines the trajectory of the housing market under colonialism and apartheid, whereby a state-driven, profit-seeking racial categorization of people, housing and neighborhoods shaped segregation and unequal capital accumulation, using classificatory devices such as title deeds or ID documents. The third section underscores how these computerized infrastructures, conjugated with the explosion of consumer credit, paved the way for the datafication of the South African population through a wide information dragnet structured by credit bureaus around ID numbers. Rental platforms, in a context of rising rental demand, extended this dragnet by harvesting tenant data and designing automated tenant screening solutions, enabling the consolidation of the private rental sector. Residential sorting shifts towards platform-driven, market-based classifications that associate scores with moral categories to sort the “good” from the “bad” tenant, reiterating segregation in the context of racialized indebtedness and housing inequalities. The last section discusses how this algorithmic remaking of the market renews the extractive logic that underpins South African racial capitalism through two joint rentier mechanisms: the construction of housing as a new asset class for corporate landlords; the income-generating assetization of rental data. The conclusion draws implications for future research on the intersection of platform capitalism with racial capitalism resulting from the transnational deployment of real estate platforms.

Real estate platforms: Uploading racial capitalism

In urban studies, the concept of racial capitalism remains mostly applied to North American cities and colonial history. A growing scholarship emphasizes how racial differentiation was key to the creation and extraction of value (Fields and Raymond, 2021) and underlines the role of property as “a race-making institution” (Bonds, 2019) and driver of racial categorization, a process through which racism and capitalism become “fundamentally intertwined” (Hawthorne, 2019). As “value is determined by racialized structures” (Dantzler, 2021: 124), capitalist housing markets, wherein private property is enforced as exclusive and dominant mode of tenure, engineered racial property regimes to allow for capital accumulation by dispossession. Taylor described how legal segregation and predatory inclusion led to unequal and racialized wealth accumulation in the US housing market (2019), where the real estate industry systematically devalorized housing and areas associated with the presence of non-White residents (Korver-Glenn, 2021; Zaimi, 2020). Segregation was therefore not the by-product of a capitalist housing system, but rather the means to generate profit and establish white economic dominance, as exemplified by the colonial roots of the US housing market.

Settler colonialism results precisely from this entanglement of racial domination and capital accumulation through modern property laws and segregation (Bhandar, 2018). The creation and legitimization of racial difference to extract value “from both people and places” (Dantzler, 2021: 118) lay at the heart of the settler colonial city, whereby the urban model results from “the fusion achieved between urban management, land management and social management” (Massiah and Tribillon, 1988: 40, my translation). The global circulation of techniques of property (Rogers, 2017), such as the cadastral, was instrumental to shape land markets at the expenses of indigenous populations. In other words, property constitutes a “technology of racial dispossession and handmaid of racial capitalism” (Nethercote, 2022). Recent works grounded in western contexts underline how the unfolding of digital technologies and data-driven analytics (Safransky, 2020) across racialized housing markets is merely “uploading twentieth century real estate ideologies into twenty-first century information technologies” (Fields and Rogers, 2021).

Real estate platforms add to the list of technologies and devices through which land and housing markets are constructed (Shaw, 2020; Wittekind and Faxon, 2023). While their “profit-making algorithmics systems” (Burrell and Fourcade, 2021: 221) reiterate the processes of categorization and classification that preside over the making of markets (Callon, 2021), the harvesting and enclosure of data generate rentier mechanisms and constitute therefore acentral avenue of capital accumulation under platform capitalism (Birch, 2020). This trend is particularly pronounced in the rental market (Wainwright, 2022): recent research underlines how digital technologies reproduce distorted informational landscapes (Boeing, 2020) or empower corporate landlords to extract rent from vulnerable and racialized tenants (Fields, 2019; McElroy and Vergerio, 2022). The use of a color-blind yet racially biased technology such as credit scoring (Rosen et al., 2021) to automate tenant screening points out to the structural and continuing role of debt in racial capitalism, echoing the earlier applications of credit scoring that created the subprime mortgage market and reproduced predatory forms of inclusion (Poon, 2009; Wyly et al., 2009). Placing their analysis in the longue durée of capitalism and the settler colony, Fields and Raymond underline how housing financialization “combines finance, data, and digital technology with racial hierarchies” through a joint process of abstraction and capital accumulation (Fields and Raymond, 2021: 1631) that turns housing into an asset class. From the lenses of housing markets, racial capitalism could be defined as the for-profit enforcement of racial differentiation over people, property and places, enacted by institutions, policies and practices, where segregation both supports and results from the geography of housing values, which cements racial and class hierarchies and nurtures long-lasting wealth inequalities. It is with this operational definition that I turn to the case of South Africa.

This article employs a mixed-method framework that combines in-depth fieldwork with quantitative analysis. In order to understand the functioning of the real estate industry and chart the role of digital technologies, I conducted 71 interviews for a total of 18 months of fieldwork in Cape Town from 2015 to 2018. The sample of interviewees included real estate agents (n = 31), developers (13), institutional investors (5), mortgage lenders (9), mortgage brokers (7), real estate platforms (4), and credit bureaus (2). To analyze how these actors operate across the spatial structures of the market, I sourced and cleaned deeds data from the City of Cape Town to construct a database of 900,000 geolocated sales that covers the metropolitan area from 1984 to 2017. In parallel, I harmonized data from the 1991, 1996, 2001 and 2011 censuses at the neighborhood level (the subplace level defined by Statistics South Africa). Using old topographic maps, planning documents, and the existing bibliography, I manually recreated the zoning of the Group Areas Act (GAA) to classify each neighborhood and sale in four categories: formerly white-only areas, Coloured township, Black Townships, and post-apartheid areas which designate neighborhoods built after the repeal of the GAA in 1991. Combining the spatial analysis of housing sales, the longitudinal analysis census data, and the content analysis of interviews, I cross-examine the rise of rental platforms and the evolution of segregation within the post-apartheid housing market.

Making markets: The classificatory devices of racial capitalism

In South Africa, rental platforms build upon unparalleled infrastructures of identification and data collection that need to be contextualized within the long iteration of devices used to enforce property rights and construct the market through the racial categorization of people, housing and neighborhoods under colonialism and apartheid. By allowing capital accumulation within the white-owned real estate industry, racial regimes of property secured white economic dominance while justifying land evictions and forced removals for the enforcement of segregation. In that sense, the urbanization of South Africa aptly recalls how “property relations have functioned as a technique of racial domination” (Dorries et al., 2022: 265), and exemplifies the two “dominant forms of production of racial capitalism”: dispossession and displacement (Dantzler, 2021).

Cape Town, a settler colonial city

From the early days of the Dutch Cape Colony in the 17th century, the promulgation of private property through title deeds shaped segregation and promoted white economic dominance while dispossessing indigenous populations. Created in 1839, the municipality of Cape Town and its electoral constituency were “designed to ensure the protection of the interests of the wealthy, white, propertied class” (Bickford-Smith, 1995: 71). Racial segregation intensified throughout the industrialization of the late 19th century (Houssay-Holzschuch, 1999). While this resulted mainly from a “wealth-based differentiation of style of housing” (Christopher, 1983: 146), the use of segregative devices, such as racial covenants in title deeds, picked up in the late 1890s (Bickford-Smith, 1995: 74), despite the fact that official and arbitrary criteria of racial classification remained loosely defined.

Following the creation of the Union of South Africa (1910), the Native Land Act (1913) amplified the racial property regime by systematizing land dispossession (Alexander, 1979) and restricting property rights for Black populations, left with 7% of the land on a national level. The Act cemented the joint classification of property and people by placing “restrictions on land transactions between racial groups” (Ramutsindela, 2013: 292). In Cape Town, urban planning and zoning policies strengthened segregation with the demarcations of the townships of Ndabeni (1901) and Langa (1923) reserved for Black workers. People classified as Coloured were allowed property rights but segregated in specific neighborhoods such as Athlone or Q Town. Disguised under motives of public health comforted by racist stereotypes, economic profit was the main motive behind the forced removals, land expropriations and segregative measures allowed by the Native Urban Areas Act of 1923 and the Slums Act of 1934 (Parnell, 1988).

Simultaneously, the first developers and housing societies in the Cape catering for the “good” and “deserving” white people (Teppo, 2004) explicitly articulated race and class. The Citizen Housing League selected home-seekers on the basis of moral and racial categorization: “they were required to be young, formally married, in receipt of a stable income, not given to wasteful expenditure” (Gordon, 2015). On the other hand, predatory lending was a common denominator for the few residents of color that could afford mortgages. The Usury Act was amended to allow higher fees and interest rates, which rose from 12 to 17% in the township of Alexandra in the 1940s – twice the rate offered to white buyers (Bond, 2000). Through the market, race, class, and urban space were coproduced by the intertwinement of racial hierarchies, housing values and property regimes.

The legacy of apartheid on housing values

Apartheid constitutes a profit-driven, state-controlled enforcement of racial categories upon people, housing and neighborhood, implemented for three reasons (Western, 1981): racism, fear towards racial mixing in working-class areas, and a desire for political and economic hegemony through the dispossession of the Coloured and Indian communities. The National Party therefore placed homeownership and the protection of property values at the center of their electoral campaigns (Western, 1981: 81), instrumentalizing the housing market as a legal and ideological tool to justify apartheid and systematize the racial control over property transfers and residential mobilities. The Population Registration Act (1950) and the Group Areas Act (1951) were brutally enforced upon society, amplifying the existing racial classification of people, housing and neighborhoods. To implement these two pillars of apartheid, public authorities relied on devices such as title deeds, zoning maps and ID documents.

From an early stage, the apartheid regime loved computers to power the project of complete segregation, with IBM providing the machines to store population databases and compute ID numbers. As Breckenridge summarizes, the “centralized population registration was the bureaucratic cornerstone of the Apartheid state, the lynch-pin of the Group Area Act” (2014: 224). On ID documents, one digit indicated the racial category of the card holder, another one designated the suburb as demarcated by the 1951 census. The racial classification of people and neighborhoods were two sides of the same apartheid coin, forged by the state’s “mania for measurement” (Posel, 2000).

At the dwelling and neighborhood level, the Group Areas Act “imposed control throughout the Union of South Africa upon all interracial sales of property and interracial changes in occupation of properties” (Western, 1981: 70). Racial zoning was superimposed on cadastral registries, harmonized with the 1927 Land Survey Act which attributed a unique ID to each erf (plot of land). Both the erf number and the ID number were necessary to finalize a transfer of property as required by the title deed. Consequently, the race of the inhabitant had to match the racial zoning of the neighborhood. In case of mismatch, various tools were used to erase racial diversity, from expropriations to bulldozers, as exemplified by the destruction of District Six in Cape Town. Most importantly, profit was realized both upstream and downstream of the removals and expropriations resulting from these classifications. A white-controlled Community Development Board was tasked with dealing with the properties of “disqualified owners” (Western, 1981: 188), with board members making profit through the resale process. In parallel, white-owned conglomerates acquired a near monopoly over the state contracts that financed the construction of Black townships (Hendler, 1987). “Property-market opportunism” (Western, 1981: 83) is therefore inseparable from the enforcement of apartheid.

Racial differentiation translated into unequal property rights, tenure status, housing products, and lending policies. Black people, whose presence in cities was framed as temporary and illegitimate since the colonial regime, were denied homeownership until 1985 and forced to live in state-built, low-cost rental housing. Redlining was the rule for Black townships, despite late attempts to create a bonded African middle class (Parnell, 1991). With an intermediate ranking on the racial scale, Coloured people could access housing finance in designated townships such as Mitchell’s Plain, facing poor amenities, low standards of constructions, and usury interest rates (Black Sash National Conference, 1980). Reversely, benefiting from tax rebates and lenient legislation (Mabin and Parnell, 1983), the real estate industry was tasked with and profited from fostering homeownership in white-only areas: “the vehicle for this purpose was the building society and the instrument the interest rate on mortgage loans” (Jones, 1992).

Under apartheid, racial categorization dictated a housing journey in terms of location, tenure, and wealth, fostering a divide between propertyless, racialized tenants and white homeowners. The racial property regime profoundly shaped unequal and racialized capital accumulation and housing wealth, generating extreme and long-lasting segregation. In Cape Town, the geography of housing values underscores this engineering: high-value properties located in previously white-only areas, nested on leafy hills in the Southern and Northern Suburbs, contemplate the devalorized housing stock of the sandy Cape Flats, stretching from Langa to Khayelitsha (Figure 1). Colored and Black townships remain today mostly inhabited by Black and Coloured people; white households, despite accounting for 15% of the city's population, represent more than 60% of residents in formerly white-only areas in 2011 (Figure 2(a)).

Housing prices in Cape Town (2016). Prices adjusted to 2016 rand value. Spatial interpolation based on Stewart’s potential model, with the potential package (version 0.2.0, Giraud and Commenges, 2022). Grid resolution: 250m; span: 500m.

(a) Evolution of segregation in the areas defined by the Group Areas Act. (b) Evolution of housing tenure in the areas defined by the Group Areas Act.

From race to scores: Knitting the information dragnet

While racial categories officially disappeared from market regulations with the end of apartheid, the infrastructures to classify the population survived, if not facilitated, the transition to democracy. From the 1990s, South Africa pioneered biometric governance for surveillance and welfare purposes. A “Smart ID Card” system was rolled out from 2013, after many errands and stalemates to design the Home Affairs National Identification System and recycle the enormous databases of ID numbers and fingerprints created during apartheid (Breckenridge, 2014).

The explosion of credit consumption (James, 2014; Schraten, 2020) in the early 2000s added the data flesh to this infrastructural skeleton. Retail stores conducted aggressive marketing campaigns, sending personalized credit cards to Black and Coloured populations. As salaries stagnated, credit supported a “jobless form of growth” (Hart, 2014). While massive, racialized indebtedness structures the post-apartheid society (James, 2014), the extension of consumer credit should also be understood as an unprecedented process of datafication of the population and knitting of a large-scale information dragnet. With cloud computing, each credit application, each account, each late or made payment leaves a digital trace reported by credit providers, then extracted by credit bureaus through ID numbers, via the Data Transmission Hub co-owned by the South African Credit & Risk Reporting Association (SACRRA) and the Credit Bureau Association (CBA). Few countries rival the volume and depth of data hold by credit bureaus, as detailed by this engineer of TransUnion:

South Africa has a wealth of data. We have a lot more data than what is available in some of the other countries. Credit scoring is far advanced in South Africa. If we are to compare what we do here versus what is done in the US, I think we are pretty on par. (I-1, data engineer)

We get data from all credit providers in South Africa: it would be the banks, the finance houses – Wonga, they offer unsecured loans – clothing retailers – Truworths, Edgars, Ackermans, Mr Price, all of them -, furniture retailers – HomeChoice, Luous – and then the Telcom industries – MTM, Vodacom, they give data. That would be the main ones. We also get information from the court, the legal system. That would mostly be negative information. So if you didn’t pay your account, it went through the whole legal process and now there is a court order for you to pay, or you are flagged as high risk. That information is shared. There is also the “enquiry” information, all these daily applications that go through to the bureau: we store that information, which is specific to the bureau. We do have access to the Deeds data. We do have access to commercial data: if you are a principal in the company, we can link you to that company and to the performance of that company. (I-1, data engineer)

“It’s fantastic”: Rental platforms as market makers

A shift in market structures

Despite the governmental focus on home-ownership, the housing market underwent a major restructuring with the surge and consolidation of the private rental sector over the last two decades. Renting became the second form of tenure in Cape Town (31% of households in 2011) and the first one in formerly white-only and post-apartheid neighborhoods (Figure 2(b)). Two factors explain this shift: the property boom of the 2000s, and the rise of the new Black middle class (Southall, 2016).

Historically associated with the cheap housing stock delivered by apartheid, the campaigns of rent boycotts and fierce anti-eviction movements (Oldfield and Stokke, 2006), rental housing was perceived as too risky for investors. At the end of the 1990s, the private rental sector was deemed non-existent on the formal housing market (Morange, 2016). But from 2003 to 2007, the housing market in South Africa experienced a property boom, with buy-to-let sales peaking at 30% (Migozzi, 2020). Skyrocketing values brought housing under a new light for investors:

Twenty years ago, yields on commercial properties would be 10 or 15%, and residential yields were about 3%. There was no incentive, really, to invest in rental stock. There has been yield compression in commercial properties. And the yields on rental stock have gone up. On a low-end rental product, which is the market where we are, between 4000–8000 rands a month, you can actually get a better yield than on commercial property. So it’s becoming more attractive as an investment class. (I-6, CEO of PayProp)

Evolution of median housing prices in Cape Town (1990–2016).

I had a Black woman coming to the office, she was driving a massive 4x4. She was a magistrate, earning like 60 000 rands a month. A very, very nice salary. She wanted to rent a house. I said to my agents: “there is no way she is going to rent. She is gonna buy”. What we discovered: she had a judgment because she had an account against her with Edgars [a popular retailer]. She was a magistrate, but she couldn’t get a bond! (I-10, developer)

Interviewees emphasized how the rise of rentals shifted the value chain of the real estate industry: Prior to 5 years [2012], all developers didn't keep rental stock. A lot of developers see that the rental income is higher, they get good returns. They've got an asset that is growing. So the trend has changed. (I-4, developer)

And since 2008, when the downward spiral came, rentals became an integral part of the business. Today, if you are an agency without a proper rental book, you are in trouble. (I-2, owner of 3 agencies)

I've got 12 agents, and 4 of them are focused on rentals. Rental was perceived as a back-office job, something that would a one page-document … That shift really took momentum 4 to 5 years ago. People realize there is money to be made in the rental side. (I-3, agency owner)

The rise of rental platforms

While previous research on the UK, the US or Australia highlights the role of digital technologies in transforming rental housing into a new asset class in a post-crisis context (Fields, 2019; Nethercote, 2023; Wainwright, 2022), rental platforms in South Africa came into existence in the early 2000s, leveraging the existing information dragnet of credit bureaus. Two of them rose to prominence. Based in Johannesburg, Tenant Profile Network (TPN) entered the market in 2000 as an Internet-based tenant tracking service. Through a partnership with TransUnion, TPN offered credit checks through SMS queries that used the applicant’s ID number. Headquartered in Stellenbosch, PayProp, launched in 2004 as a payment platform, was originally designed to transfer charity donations in the late 1990s and repurposed for the rental market. Both platforms extended the range and depth of their tenant screening services by combining the data hold by credit bureaus with the data uploaded by rental agents (payments, damage to property, evictions etc.): Once we got our first client signed up [in May 2000], we started selling a lot quicker. But of course, you were selling someone an idea: “we're going to have a database of tenant behavior, but you have to share your data to build where we are going”. So it took about five years to start gaining traction, and in 2007 we changed from a being a delinquent database to a rental tenant profile network, collecting monthly behavior patterns (I-5, CEO of TPN)

We have a product called the Tenant Assessment Report, custom-built for rental evaluation. It doesn’t just look out a person’s ability to settle his clothing account, but actually understands the nature of rental payments and forms a predictive view of whether or not the tenant will be able to pay a specific rental amount or not. There are two components: one is your ability to deal with debt; the other one is your potential future debt relative to your rental payment. Think of it as a matrix. (I-6, CEO of PayProp)

It’s fantastic. And although it’s pricy, it offers everything that you would possibly want to offer your landlord as a service. (I-4, director of agency)

Sorting the “good “from the “bad”: Segregation reiterated through platforms

Scores as everyday sorting tools

Credit scoring constitutes a routinized practice to filter home-seekers on the basis of financial behaviors, both on the mortgage and rental markets, renewing mechanisms of segregation. All rental agents interviewed used TPN and/or PayProp, including in Khayelitsha where the private rental sector also picked up. Agents rely on the depth of automated reports to spot the specific types of “bad debt” that signal risk:

We look thoroughly at the whole report. Main criteria are personal loan. It’s usually a warning bell that there is a problem financially (I-11, rental manager)

So the credit check that they [PayProp] do even incorporates assessing whether the tenant has taken out short-term loans, which often the other credit checks don't do. And using a short-term loan to pay the deposit: that’s a red flag. (I-4, director of agency)

The quality of the tenants drops when you start under 6000 rands a month. Then you start to ask for the problems. Our data shows that below 3000, tenants are monstrous. In fact, they are the most risky tenants. (I-11, rental manager)

We only take A and B type of tenants. “A” means that you don’t have debt, so a very good profile. “B” means that you have debt, but you are a good payer. “C” and below, you are not good. (I-8, REIT portfolio manager)

Technology has safeguarded us and our landlords. A lot of guesswork and feeling, went into approving clients in the past. Credit scores definitely cut down bad tenants that we had (…) It has taken a lot of the risk out of the market. (I-2, owner of 3 agencies)

What’s a good tenant? Most of the time we like to get a client that has rented before. We also need them to qualify on 30% of their net income. And obviously he needs not to have any defaults listing against his name. (I-2, owner of 3 agencies)

We don’t take tenants under 622. (I-8, REIT portfolio manager)

The color of credit scores

Legally speaking, racial discrimination is forbidden, and on paper, scoring algorithms are race-neutral. Yet credit scores bear the watermark of racialized debt, an enduring feature of racial capitalism. “Bad debt” is prevalent in South Africa: 38% of consumers have impaired credit records (NCR, 2022). The strong correlation between race and wealth inequalities means that people of color are over-represented within the low scores: 67% of over-indebted consumers are Black African (NCR, 2017). Moreover, a data engineer mentioned that location was a scoring variable – which automatically turns race into a ranking factor due to enduring segregation patterns (Figure 4):

Buy-to-let: the changing production of space in Cape Town. Source: J. Migozzi, 2018.

So we have in general been very creative in finding new ways to score. Using demographic information, or using suburb code information: where you stay, people of … to assist with assessing the risk of consumers. And that’s quite unique. (I-1, data engineer)

The use of credit scoring to make tenancy decisions – or allocate mortgages – renews mechanisms of segregation. In the context of racialized precariousness, indebtedness and housing equity, the pool of home-seekers of color capable to desegregate by renting or buying in the formerly white-only neighborhoods or in the post-apartheid areas built by private developers remains demographically thin. Produced by income inequalities and algorithmic screening, residential sorting results in a timid racial diversity in the new middle-income rental stock produced in the periphery around Parklands, Durbanville, Kuilsriver or Burgundy Estate, where Black, Coloured and white middle class households can afford to rent after passing an acute screening process.

The use of credit scores by real estate professionals is inseparable from a wider attempt to discipline home-seekers, borrowing not from the brutal force of armed repression that backed up apartheid, but rather from the less spectacular process of conquering financial subjectivities:

Previously the only consequence of a bad credit record was “I can't get credit at the retail store”. Now it has a massive effect on your ability to find a place to stay. So people with impaired credit records can't find houses to rent. The consequence that we see in tenancy data is that although South African tenants are heavily indebted, and that the debt relative to the income is growing, our view is that over time, tenants are taking their credit records more seriously. So they are managing their payment profile better (…) The credit scoring system and the rules are producing the results that it wants: a consumer that is aware of its financial position, and that will take responsibility for what they have committed to. (I-6, CEO of PayProp)

Rental platforms: Renewing the extractive logic of racial capitalism

Sorting out the “good” from the “bad” tenant through automated classification is central to capital accumulation and rent extraction. Under platform capitalism, these “digital mediations of tenancy” (Ferreri and Sanyal, 2022) form a “double threat enclosure” (Nethercote, 2023): monetary rent is extracted through payments, while economic rent is sourced from the assetization of rental data. In South Africa, this twofold process largely reproduces the social structures of racial capitalism: rental payments are extracted from a predominantly Black and Coloured income base; tenant data is collected and sold to investors or real estate agents. Meanwhile, in this tech-powered real estate industry and corporate landlords, white people remain overrepresented as business owners, shareholders or property owners, despite the timid de-racialization of corporate elites in South Africa (Freund, 2007).

Using scores to build an asset class

“The essence of an investment in real estate in a good tenant” advertises TPN on its website. By automating tenant screening solutions, platforms enabled the consolidation of the private rental sector and the emergence of corporate landlords:

Technology has empowered estate agents to have bigger portfolios to be able to turn over a bigger number of properties and really make it a business rather than a little smaller mom-and-pop shop. (I-5, CEO of TPN)

Investors can reduce the risk of the investment by appropriate screening. It doesn't resolve all instances, but if helps: you make better tenancy decision. (I-6, CEO of PayProp)

Corporate landlords describe rental platforms as a highly performative device to screen tenants, collect payments, and manage their portfolios, with the aim to reduce risk and minimize vacancy rates:

We got new people to manage our credit vetting. (…) They reduced the arrears and the evictions, and now we have a very stable income base. They use TPN. (…) If you put strict credit controls on your tenants and you do credit checks, you can still fill your blocks with good payers. (I-7, CEO of private equity fund)

We got the right software systems in place. We work with TPN. So we can trace … We do a proper credit check. You need to do it according to the National Credit Act. And also manage it via the Payprop system. So we can pick it up immediately if someone … (…) And obviously we got our service providers and attorneys … to make sure, if they don’t pay, we can start the process to get them evicted. (I-9, developer)

We use TPN and PayProp (…) If there is a particular tenant with a warning bell, we will run the two, just to make sure we are not missing out on something. We are very strict about our criteria, because the investors are relying on us to put in quality tenants in their properties. (I-11, rental manager)

We created our own tenant profile, worked the input for our own scorecard, for what needs to be done, to make sure than the tenant profile is 100% correct. We’ve got access to the tenant’s data, so we can actually see who are those clients that rent from us, and see if they can afford a house in the future. (I-9, developer)

The fundamental change is that the nature of private property ownership for rentals is changing dramatically in South Africa. It's moving from the hands of private, micro investors, our typical client's clients, to a more European model of ownership where pension funds take large position of the market, large quantities of stock. It's a fundamental shift on the market. (I-6, CEO of PayProp)

This assetization of rental housing participates to the integration of South Africa into global financial networks. Owned by the Baltimore-based MMA Capital Holdings, International Housing solutions was acquired in 2018 by Hunt Companies, a large, diversified real estate investment firm headquartered in Texas. Early 2023, its REIT Transcend was acquired by another REIT, Emira Property Fund, listed on the JSE. Rental payments are eventually distributed to corporate landlords’ shareholders via the JSE or across private corporate structures.

Golden data

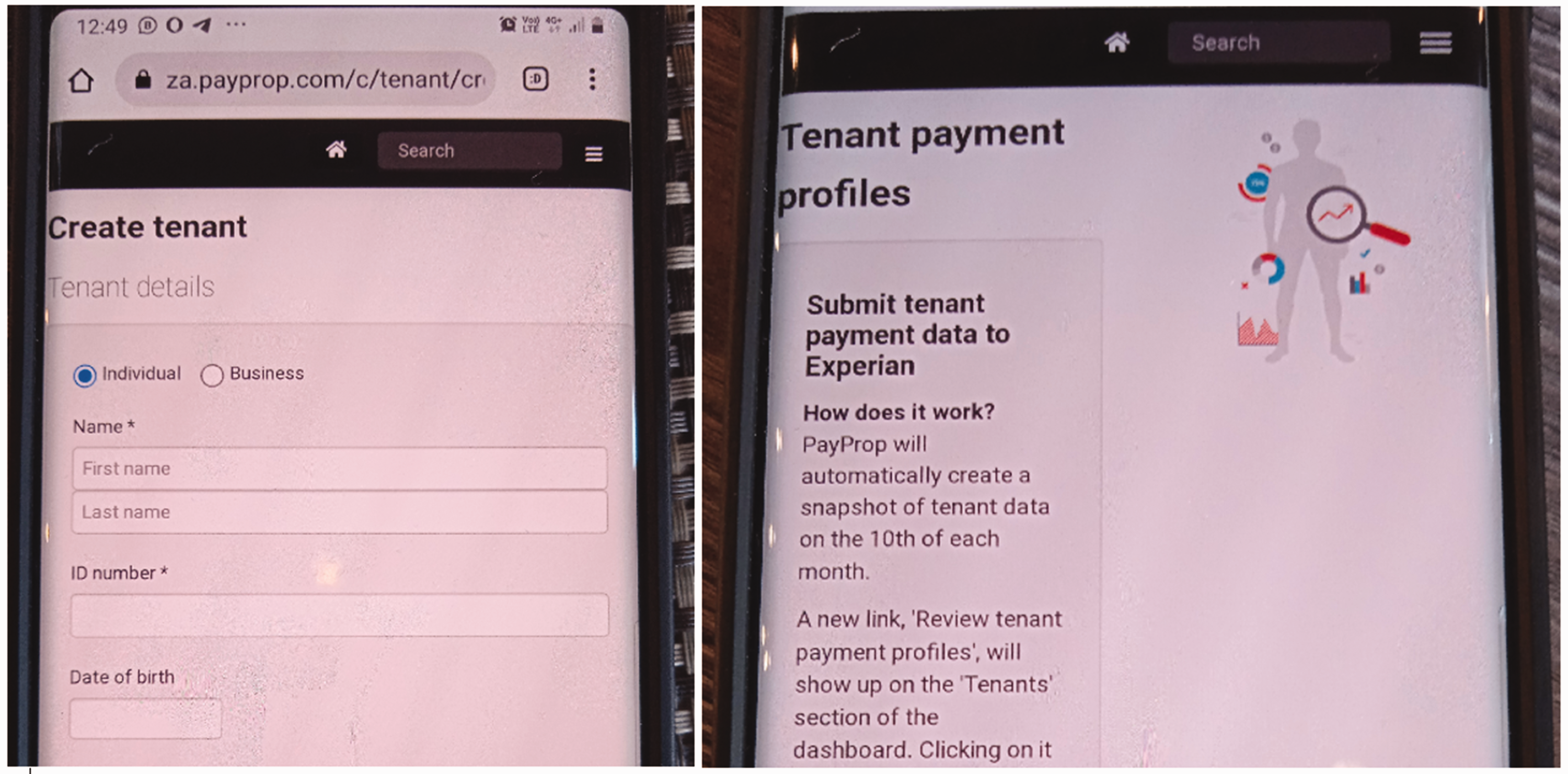

The intersection between platform capitalism and racial capitalism on extractive grounds is also found in the political economy of the information dragnet. Punched during apartheid to enforce segregation, ID numbers allow the automated selection of tenants, but also support the extraction of rental data, framed as an asset by rental platforms to generate income and market capitalization (Birch and Ward, 2022). After processing the data uploaded by their customer’s network, rental platforms sell it in bulk to third-parties and commercialize ready-made reports. PayProp’s dashboard allows to submit data to Experian, adding a rental layer to the information dragnet (Figure 5). TPN sells its data to TransUnion. The resulting market-based classifications extend beyond the scale of the tenant: metrics of risk and profit to guide investors and rental agents are sold at the properties and neighborhoods scales through in-house data aggregation. PayProp’s reports compare provinces and cities based on tenant’s credit scores or income-to-debt ratios, while TPN sources census data and rank neighborhoods according to a “rental payment index” or residential yields. This rentier structure of platform capitalism is even exemplified by professional trajectories within the real estate-tech industry: before joining PayProp in 2022, the former CEO of TPN sat at the board of Transcend, the REIT that does not select tenants below 622.

The assetization of tenant data through ID numbers. Source: J. Migozzi, 2018.

Beyond the consolidation and financialization of a previously disregarded market segment, the rise of rental platforms renews the extractive logics of racial capitalism in South Africa. Racial capitalism was historically rooted in the mining industry, the demand for gold and the forced incorporation of Black labour with computerized ID cards (Alexander, 1979). The minerals–energy complex still underpins the integration of the country into the global economy and its financialized regime of accumulation (Ashman and Fine, 2013). Yet the datafication of home-seekers adds another dimension to this extractive logic. Under platform capitalism, consumer and tenant data constitute a new form of capital (Sadowski, 2019) across the finance and real estate industry, the largest contributor to the SA economy (25% in 2022). As mining conglomerates drill in search of new platinum veins, rental data is a new furrow opened by platforms at the start of the 21st century for credit bureaus, which harvest the social space to find deposits of digital traces, enrich their databases, and design new scoring algorithms to advance techniques of consumer classification. Court archives, tax data, credit accounts, telephone records or censuses are excavated, then valorized – with ID numbers as the chain link, while FinTech firms are regarded as a potential new trench of the “alternative data landscape” (IFC, 2021). Enclosed through proprietary algorithms and accessible through subscription-based dashboards, rental data became an asset through the platformization of the post-apartheid housing market.

Like gold or diamonds connected Cape Town and Johannesburg to the global economy, so do real estate technologies designed in the data-rich environment of South Africa. TPN was acquired in October 2022 by MRI Software, specialized in real estate and headquartered in Cleveland. PayProp, priding itself of channeling US$3.8 billion of rent payments since its creation, is extending towards the UK (2017) and the US (2019) – where racialized rent extraction and capital accumulation are also shaped by the emergence of corporate landlords (Fields, 2019; McElroy and Vergerio, 2022). Starting from Florida and Texas, PayProp, powered by Amazon cloud servers and actively canvassing roadshows and property salons, expands its activities in Alabama, Missouri and Illinois, forging partnerships with global companies such as RE/MAX, echoing how the platformization of the housing market rewires the transnational dimensions of racial capitalism (Go, 2021).

Conclusion

This article analyzed how platform capitalism intersects with racial capitalism through the reshaping of the post-apartheid housing market by rental platforms. Automating tenancy screening and payment solutions, rental platforms scaled up as powerful market makers, consolidating the private rental sector and facilitating the emergence of corporate landlords, while turning the harvesting of rental data into an asset. The trajectory of South Africa illuminates the role of digital technologies in reconstructing racialized housing markets where platform-driven social sorting continues the process of social differentiation that underpins the formation and capture of value.

Amplifying the colonial racial property regime, tech-savvy apartheid constructed a market where housing inequalities in terms of tenure and capital accumulation directly resulted from the racial ordering of people, housing and neighborhoods. Pointing to the convergence between platform capitalism and racial capitalism, the devices and populations databases that enabled the for-profit “hyper-exploitation of Black workers” (Levenson and Paret, 2023) under apartheid paved the way for the hyper-datafication of home-seekers. The information dragnet that enables the classification of tenants is deeply embedded in the engineering of markets under racial capitalism, in particular the use of ID numbers to classify the population in distinct racial categories endorsed with unequal property rights. Yet the intersection between racial capitalism and platform capitalism goes beyond infrastructural plumbing: it speaks directly to the racialized patterns of capital accumulation and property ownership in a market reconfigured through abstract credit scores computed by seemingly race-neutral algorithms. The algorithmic sorting of tenants by credit scores is a key mechanism of value creation both for rental platforms and corporate landlords. By redefining patterns of inclusion and exclusion, rental platforms define market boundaries within the larger South African housing landscape, allowing rent to be captured through the profiling and placing of the “good” tenant in the consolidated private rental sector. In that sense, such patterns of platformization renew the “differential valuation of people” (Dorries et al., 2022: 264) central to urban housing markets under racial capitalism.

South Africa demonstrates how this algorithmic remaking of the market extends the extractive logic of racial capitalism through two joint, platform-driven rentier mechanisms (Nethercote, 2023): the consolidation of the private rental sector that turns housing into a new asset class for institutional investors; the income-generating classification of home-seekers by the harvesting of tenant data. The extraction of rent payments combines with the for-profit enclosure of tenant data through proprietary algorithms and commercial databases. The historical patterns of property ownership forged by dispossession and segregation mean that the profits generated from rental housing through automated tenant screening and platform-driven management are unfolding through and reproducing market structures historically geared towards white economic dominance. This interplay between racial capitalism and platform capitalism renews the political economy of housing and reshapes mechanisms of segregation. Previously orchestrated by the state and its local apparatus on the basis of explicit racial categories, residential sorting as shaped by the private rental sector is indexed on credit scores computed in the context of profoundly racialized indebtedness and housing wealth inequalities. While cherry-picked Black, Indian and Coloured tenants create pockets of racial diversity in a few neighbourhoods, such patterns of inclusion in the post-apartheid market largely reproduce the urban geography of class and race inherited by the for-profit ordering of people and places. In that regard, South Africa highlights how digital technologies continue the process of abstraction with automated scores replacing racial categories in the reproduction of racialized market structures.

This algorithmic remaking of the private rental sector seeks indeed to produce a visible and measurable home-seeker, who needs a good score to call a place home by demonstrating financial discipline. Where in Marikana the mining conglomerates sent the police to shoot the protesting and indebted minors, the real estate industry sees in credit scoring a powerful device to align home-seekers on standardized metrics that signals the “good” tenant from the “bad” one in order to facilitate rent extraction. While it was beyond the scope of this article, researchers should pay attention to the disciplinary effects of credit scoring, and analyze the agency of home-seekers in engaging and negotiating these racialized and increasingly digitized market structures. Fourcade and Healy suggest indeed that credit scores should be understood as a new form of capital, whose stratifying effects affect life chances (2017). Preliminary interviews with tenants and homebuyers in South Africa revealed a contrasted lack of awareness towards the role of credit scores, despite constant injunctions from the real estate industry to check and improve them, and the 2.6 million of credit reports consulted by consumers in 2022 (NCR, 2022). Further research on the rental sector in South Africa is necessary to understand how the consolidation of the rental sector affects the tenant–landlord relationship in terms of inequalities and power relations, and how the shift towards a rentier structure affects segregation patterns. The platformization of the market and the sorting of home-seekers through credit scores, while restricted to the private rental sector and the mortgage market, certainly adds another algorithmic barrier to access the formal housing market for the majority of the urban poor, renewing patterns of exclusions. This puts into sobering perspective the hopes and expectations placed in the private sector to solve the housing crisis and redress the unequal regimes of property ownership in South Africa.

This article also points out to future research directions in order to chart the articulation between urban segregation and consumer classification enacted by the convergence of racial capitalism with platform capitalism. As real estate platforms collect data, people, properties, neighborhoods and cities become classifiable at will through proprietary systems, creating a form of enclosed knowledge on housing markets. The actual scope of this “bird-eye view” of the market and its consequences on everyday practices for the professionals of segregation, such as real estate agents or mortgage lenders, are yet to be fully assessed (Wainwright, 2022), together with the role of credit bureaus within and beyond (South) Africa (Opalo, 2022). Finally, the circulation of data and real estate technologies across the US and UK housing markets through platforms designed in South Africa, rooted in the colonial legacy of racial classification and uploaded by the everyday work of estate agents from Cape Town to Miami, questions the framing of the Bay Area–Wall Street nexus as the epicenter of technological and financial innovations that facilitate the integration of real estate within a global digital stack (Shaw, 2020). The digital architectures and financial networks that enable on a global scale the formulation, extraction and circulation of value from local, unequal and racialized urban housing markets deserve further inquiries to understand how racial capitalism intersects with platform capitalism in conjunctural and transnational ways.

Footnotes

Acknowledgments

This paper was greatly improved by feedback provided by the members of the Digital Transformations in Property and Development Social Science Matrix coordinated by Desiree Fields and Hilary Faxon at the University of California, Berkeley. Prior versions were presented at the International Conference on Africa’s Urban Futures at the Universi

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research that forms the basis for this article received financial support from a PhD scholarship from the French Ministry of Higher Education and Research, a research grant from the French Institute of South Africa, and a Postdoctoral Research Fellowship from the Urban Studies Foundation at the University of Oxford .