Abstract

This article criticizes the way fossil capitalization dispossesses the future. Turning fossil fuel into capital entails the legal enclosure, calculative cheapening, and material extraction/pollution of the future. Fossil investors’ ‘present values’ hinge on the misery of those dispossessed by climate emergencies. Fossil capitalization is premised on ‘future theft’ understood as a temporally inverted form of ‘original accumulation’. The durability of inequality created by asset wealth is compounded by the durability of carbon waste. Climate economics legitimizes and entrenches this pattern by discounting the future and failing to assign responsibilities for climate costs. Tort litigations allow climate victims to sue fossil fuel companies for compensation. However, they remain limited by the strictures of liberal property law. Climate reparations promise to overcome these limits by reclaiming the stolen future without recourse to previously settled property rights. Still, they cannot escape the vicious tempo-material trajectories engendered by fossil assets and their carbon afterlives.

Introduction

The climate movement has changed the political status of the future. The future no longer serves, as it did in postwar Western welfare states, as an inexhaustible resource to tame distributional conflicts between labor and capital by promising workers that they and their children will be better off tomorrow. The future has become a scarce resource. It has changed from a means to resolve into the very source of distributional conflicts. Rival parties stake a claim on it as evidenced by accusations of ‘future theft’ articulated by the climate movement: ‘You are stealing our future in front of our eyes’, the 15-year-old Greta Thunberg hurled at the politicians at the 24th Conference of the Parties (COP24) in Katowice. The climate movement’s grievance over future theft resonates with critiques of how financial capitalism appropriates time and ‘extracts revenue from the future’ (Mitchell, 2020: 53). Financial capital – whether in the form of a direct investment, equity, or credit – is premised on revenue it generates in the future – dividends, rents, and interest payments. Because of the workings of interest rates and the peculiarities of financial valuation (Doganova, 2024), investors and lenders get future revenues at a ‘discount’. The difference between present and future value underpins their profits. Capital is not just premised on cheap labor and cheap nature (Moore, 2015), but also on a cheap future.

This article introduces the notion of future theft that brings together and extends economic and ecological critiques of intertemporal dispossession. It goes where both concerns meet: fossil capitalization understood as the way fossil fuels become and operate as capital. Here finance’s exploitative relation to the future finds its most devastating but also most glaring expression. Fossil assets not only discount but dispossess the future because they call forth climate damages occurring long after they have exhausted their lifetime. This undermines the common justification for the devaluation of the future and the virtue of private property and investment more generally, namely that it makes the future richer. It makes the critique of capital’s future extraction more salient. In turn, this focus shifts the attention of climate critique from climate summits to the fossil economy, from international treaties to property law, from the atmospheric climate ‘imperium’ to the subterranean ‘dominium’ over fossil fuels.

I elaborate my notion of future theft against alternative framings that conceptualize climate theft differently or deny its existence altogether. For Thunberg – and large parts of the Euro-American climate movement – the struggle over the future is an intergenerational conflict between grown-ups and children, boomers and gen zetters, present and future generations. Climate economists would respond that there is no theft if the costs for climate mitigation and the benefits of averted damages are balanced efficiently. As I will show, this view legitimizes, entrenches and extends future theft. In contrast, the focus on fossil capitalization shifts attention to the exploitative and dispossessive intertemporal but not simply intergenerational relationship between owners of fossil fuel assets and those affected by climate damages. Inspired by Marxist class analysis that focusses on social asymmetries mediated by property in which the wealth of one party systematically depends on the misery of others, I argue that fossil asset owners claim future revenues in the present that others must pay for – economically and ecologically – in the future. Fossil assets mediate socio-ecological ‘class’ relations, not only as a means of production and ‘durable wealth’ (Beckert, 2022) accumulation but also as a means of climate destruction and durable carbon waste accumulation. I show how this exacerbates inequalities in the neoliberal ‘asset economy’ (Adkins et al., 2020).

However, this relationship does not translate easily into the kind of political antagonism Marxist notions of class struggle suggest. Fossil fuels belong to petro-states – many in the Global South, some rich, some very poor – and have historically enabled the wealth of western industrialized countries. In the age of intense financial intermediation, fossil assets are not just in the hands of a few Rockefellers but also in investment portfolios of workers’ pension funds. Similarly, victims of future theft seem to be everywhere and nowhere. Everywhere because everyone is potentially affected by climate emergencies. Nowhere, because the stolen future, it seems, has yet to arrive. To counter this delusive elusiveness, and to give a sense of what kind of political tremors might emerge along the faultline between fossil owners and climate victims, I zero in on a climate tort in which a Peruvian farmer sues a German energy company for climate damages. Beyond the cast of actors, the case is highly suggestive because it reveals that climate damages have already arrived in the present. The case addresses future theft in a reparative and not simply preventative mode. It is not just about protecting ‘future generations’ but about compensating climate victims now. This prompts me to ask if and how climate reparations can redeem future theft understood as a historical injustice that has never ended but stretches into the future.

By mobilizing and extending approaches from valuation studies (Birch and Muniesa, 2020; Doganova, 2024; Muniesa et al., 2017) and critical political economy (Mitchell, 2020; Nitzan and Bichler, 2009), the article sets out to illuminate the dispossessive logic of fossil capitalization as a form of a future theft understood as a temporally inverted ‘original accumulation’ (Marx, 2024 [1867]: 650–92). I then show how hegemonic climate economics repeats the appropriative tendencies inscribed in fossil capitalization. Climate economics devalues the future by discounting climate costs and relies on acts of ‘air-appropriation’ (Folkers, 2020), in which appropriation proceeds through pollution (Serres, 2010). I then turn to climate jurisprudence and show how torts mobilize the matrix of responsibility inscribed into liberal notions of property. While climate torts are illuminating because they can stage a confrontation between fossil asset owners and climate victims, their political value remains limited due to the strictures of liberal property law. I will therefore probe if and how climate reparations (Burkett, 2009; Táíwò, 2022) go beyond these limits.

Fossil Capitalization: Accumulation by Future Dispossession

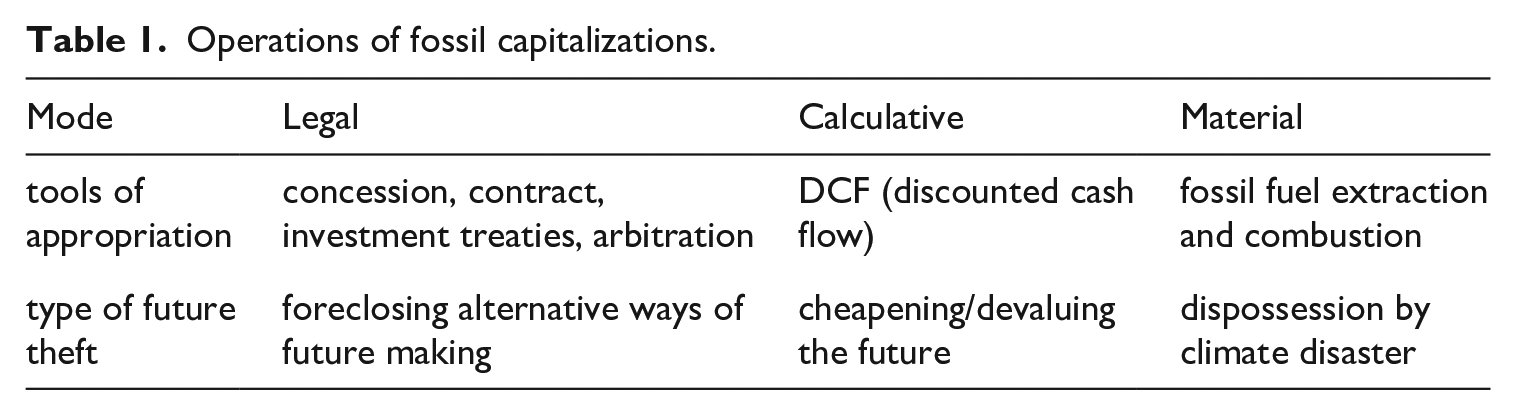

This section shows how fossil fuels have become an asset through three operations of capitalization – legal, calculative, and material – each of which appropriates the future in a particular way. I will go beyond existing capitalization approaches by showing what happens after fossil fuels have exhausted their lifetime as an economic asset and become ecological liabilities. I thus maintain that it matters what matter gets capitalized, because the contingent and contradictory conjuncture between capitalist temporalities and the material temporality of fossil fuels and their residuals (Folkers, 2021) engenders ‘future theft’.

Preemption: The Legal Enclosure of the Future

In most countries the national state acts a as ‘property-owning unit’ (Coronil, 1997: 50) of fossil fuels (Asdal and Lahn, 2024; Bridge and Le Billon, 2017: 27). States often exploit their reserves in cooperation with oil and gas companies. There are countless juridical techniques through which companies gain access to gas, coal, and oil reserves. However, there are two basic forms: concessions and contracts (Christophers, 2020: 99). The concession, prevalent in the first part of the 20th century, engendered ‘a colonial extraction regime in which the state grants private companies ownership of the subsoil’ (Appel, 2019: 141). Through the concession, the imperium of oil states is literally and symbolically undermined by the dominium of private companies. The juridical perforation of the territory goes along with the physical drilling of wells.

The introduction of contractual models in which the state always remains the owner of the resource changes the appropriation regime. In Production Service Agreements, for example, states and companies negotiate how to share the future profits from oil or gas projects (Appel, 2019: 137–71; Radon, 2007). The territorial appropriation of the subsoil gives way to a temporal regime of appropriation (on temporal appropriation see Doganova, 2024: 247–8). The companies no longer own the oil in the ground. Rather, in return for their investments, they can claim their share of the future cash flows it generates. They don’t own fossil fuels but become shareholders of fossil assets. To secure these claims, investors mobilize legal tools to secure ‘the life span of their assets’ (Pistor, 2019: 14). In the fossil fuel industry this ranges from ‘stability clauses’ in extraction contracts to international investment treaties that prevent states from adopting stricter social or environmental legislation (Dehm, 2023: 270–1; Radon, 2007). Taken together, these legal tools enclose the future. Like the enclosure of land, this involves not only fencing in a given terrain but making available a future that is ‘open for business’ exclusively. This requires draining the swamps of democratic visions, revolutionary hopes, and concerns over coming generations, to bulldoze the ‘deep future’ of planetary timescales, to clear it from the material entanglements that connect past, present, and future. It creates a capitalist revenue horizon: a flat temporal domain that becomes calculable in terms of abstract monetary units. The temporal landscape created for fossil investors forecloses the democratic promise of collective future making.

Property law has always come with the powers of ‘time binding’ (Luhmann, 1993). Already Jeremy Bentham broke with the Lockean notion of property as an effect of past labor to construe it as a legal claim on the future: ‘Law alone is able to create a fixed and durable possession [. . .]. Law alone can accustom men to bow their heads under the yoke of foresight’ (Bentham, 1978: 50). The state-secured durable claim on property both protects and produces the investment horizon. The security of property is the foundation of economic expectations, the fundamental act of sovereign ‘de-risking’ that provides the bedrock on which the ever more baroque cathedrals of financial risk and revenue calculations can settle. However, the trajectory from property to expectation can also be reversed. As investment treaties and extraction contracts protect future revenue, they create a quasi-property right of the thin air of future expectations. They legally hedge the appropriation of the monetary future that has already taken place. Investment becomes a form of ‘preemption’ 1 in which law subsequently protects a claim on a future finance that has already been seized.

Discounting: The Calculative Cheapening of the Future

For oil and gas companies, knowing the value of assets is crucial to decide which oil and gas fields are worth investing in. The standard calculative format for this is the internal rate of return (Field, 2022) – a calculative device of the discounted cash flow (DCF) family that allows them to easily compare the viability of different investment opportunities. The basic assumption in DCF is that the present value of an asset is the sum of the expected future monetary returns (Muniesa et al., 2017). In the fossil fuel industry, the selling of coal, oil, and gas generates this income so that the geological prospection of the subsurface and the economic prospection of future market prices determine present value.

Yet the present value of assets depends on one further factor: the discount rate (Doganova, 2024). Expected returns are discounted according to a previously determined ‘rate’. Justifications of discounting usually invoke the idea that investors deserve a reward for the risks they take and for not consuming their wealth in the present. Thanks to their risk and restraint – the reasoning goes – the future becomes investible and more prosperous. Yet the effects of discounting suggest the opposite. Discounting cheapens the future. It makes an asset much cheaper in the present than it promises to be in the future. With a 5% discount rate, a cash flow of 100 euros a year from now is only worth 95.24 euros. The discount rate expresses the rate of return and allows investors to cash in the difference between their present investments and their future revenue. Accordingly, discounting, as Timothy Mitchell (2020: 53) argues, ‘extracts revenue from the future’. Jason Moore (2015: 147) has argued that fossil fuels are ‘cheap energy’ because their extraction ‘appropriates’ unpaid biospheric work/energy. However, for the investor the value of fossil assets does not derive so much from past work as from future expectations. Cheap fossil energy is not only premised on cheap nature but also on a discounted, cheap future. Discounting also limits the temporal horizon relevant to investors. As the value of future cash flows shrinks every year, far-future returns matter little for the present value of an asset. After a ‘forecast period’ of usually 10 years, the ‘terminal value’ just lumps together the residual value of the future in a single number. Discounting carves out a near future horizon of revenue expectation and abstracts from the much longer future that fossil capitalization sets in motion.

As Liliana Doganova (2024: 10) observes, the discount rate is an inverse interest rate. However, both investments and debts place a ‘burden of repayment’ (Mitchell, 2024) on the future. Tenants must repay real estate investors’ revenue expectations with rising rents. Patients must repay pharmaceutical companies’ ‘cost of capital’ with high drug prices (Doganova, 2024: 210f.). In the case of the fossil fuel industry this burden initially falls on extractive workers and energy consumers. To meet revenue expectations, wages must comply with estimated production costs and prices need to remain high. Historically, oil companies and petrostates have repeatedly curtailed their output to increase the oil price (Mitchell, 2011: 163). The strategic disruption of fossil fuel supplies in geopolitical conflicts has, for example, caused prices to rise and fossil asset values to appreciate.

With Thorstein Veblen one may criticize such practices as ‘sabotage’. For him, the ‘larger meaning of the Security of Property’ is that ‘[o]wnership confers a legal right of sabotage’ (Veblen, 1997: 66f.) by wasting the potential to increase material wealth in favor of pecuniary returns. However, in times of climate emergency, the problem is not so much that fossil fuel companies hold back their resources but that they sell them – not that they waste their resources but that they waste, or pollute, the atmosphere. To avoid their assets from becoming ‘stranded’, thus losing some or all of their value, fossil companies must sell amounts of fuel bound to cause disastrous degrees of global heating (Folkers, 2024). Sabotage becomes ecotage. The security of the fossil asset confers a legal right to abuse nature. Such acts of ecotage place a hitherto unimaginable economic and ecological ‘burden of repayment’ on the future.

Extraction/Pollution: The Material Dispossession of the Future

The capitalized future is not ‘just’ calculative or ‘fictive’. It has all too real effects. After purging, enclosing, limiting, molding, and cheapening the future through a complex legal-economic apparatus, capitalization requires oil and gas companies to materialize the future they have already claimed. For the calculative future to become ‘true’, capitalization must set in motion a trajectory in which revenue expectations hold up. It needs to produce a future that recursively solidifies the material ground for the preceding legal-economic appropriation – it must make up a world in which its calculative formalizations gain traction. In the fossil fuel industry this means funding extractive projects and building infrastructures that materially underpin the revenue claims on the future.

Mediated by technology, capital becomes a terraforming force. As the extraction of fossil fuels has become ever more capital intensive, the investors’ return expectations became a crucial factor in disclosing exploitable resources. When investors can expect revenues that make ever bigger capital expenditures worthwhile, they can fund more expensive extractive infrastructures to recover previously unavailable reserves. The financial future decides the extractability of geo-historical reserves. It thus seems as if the resources exist only by virtue of their capitalization. Marx (2024 [1867]: 129) already observed that capital becomes its own recursive cause when the offspring start to produce their own parents. This also goes for the co-production of fuels and capital in fossil capitalization: fossil fuels create the value of capital, but capital creates fossils as extractable fuels in the first place.

Expressing the ontology of capital, oil and gas companies construe extraction as ‘production’ of fossil fuels. This echoes the colonial ideology of ‘improvement’ that sought to legitimize the appropriation of indigenous land. In his theory of property, John Locke (1982 [1689]) famously argued that turning ‘common’ land into private property is justified if its owner cultivates and thus improves it through labor. Fossil corporations’ understanding of oil and gas ‘production’ reproduces this trope but, tellingly, removes labor from the equation. For them it is capital’s ‘seed funding’ that allows us to harvest fuels deemed unextractable before. Fossil capitalization seems to increase ‘the common [fossil] stock’ (Locke, 1982 [1689]: 294) of mankind by turning it into an asset and thus enriching the future. While the idea of fossil fuel ‘production’ pretends to salvage underground resources from being ‘wasted’, it in fact engenders two kinds of ‘wasting’: extraction and pollution. Recovering and using fossil fuels irreversibly wastes the stock of available energy on the planet. It does not ‘add’ something to nature but instead subtracts it. More importantly, the fossil industry is wasteful because it pollutes the atmosphere with CO2 emissions. As the energy source of industrialization, fossil fuels have become one of the biggest sources of production. However, they are also the biggest source of pollution and destruction. The double waste they engender undermines the logic of productive appropriation, the link between labor/production and property/prosperity that informed the moral economies of proponents and critics of liberal ownership regimes from Locke to Marx.

This constitutes the unique role of fossil capitalization. Like other assets wrought from the earth, it appropriates nature. Like other forms of capitalization, it relies on a cheap discounted future. But fossil assets come with an economic and ecological surcharge on the planetary future. Fossil values – claimed in the present and ‘extracted’ from the future – not only rely on paybacks from extraction workers and energy consumers. The carbon waste they produce demands payback in the form of biospheric work of carbon sequestration. The climatic changes they trigger require adaptation work that is mostly unpaid or underpaid (Johnson et al., 2023). Finally, the ecological destruction global heating causes is already responsible for enormous waves of dispossession ranging from damaged homes and deteriorating property values to the disappearance of whole islands, coastal regions and the uninhabitability of ever larger parts of the planet. The creation of fossil assets does not improve but rather impoverishes ‘the future’ – or, to be more precise, the future revenues fossil assets generate for investors tacitly rely on the burdens of those affected by climate damages.

Fossil capitalization relies on a temporally inverted form of what Marx (2024 [1867]: 650–92) called ‘original accumulation’. Marx famously argued that capitalism is borne out of a violent process of expropriation that created the conditions for exploitation – the separation of workers from the means of production. Critical theorists have extended Marx’s concept, emphasizing that large scale expropriation is not a single event but a recurring feature of capitalism (Harvey, 2014). This characterizes fossil capitalization, as extractive projects are often accompanied by massive forms of dispossession, especially of indigenous lands (Watts, 2012). However, future theft entails a further twist. In fossil capitalization dispossession not just precedes accumulation but also follows it. Since present fossil asset values are premised on future climate emergencies, fossil accumulation delays dispossession and defers it into the future and to places often far removed from the sites of extraction and combustion. If, as Marx (2024 [1867]: 651) maintained, the original accumulation is the ‘prehistory’ of capitalism, ecological dispossession is its posthistory. Nevertheless, future theft is no less constitutive than past expropriations because fossil assets are only valuable because they discount and disavow their constitutive future violence.

Whereas Marx (2024 [1867]: 682) saw expropriative state violence as the ‘hothouse’ breeding capital, fossil capitalization delegates dispossession to a seemingly natural agent: the slow violence of fossil residuals (Folkers, 2021) that create a hothouse earth breeding storms and droughts, fires and floods. These delays and delegations allow investors to divest themselves from the destructive effects of their investments, to disown the liabilities of their assets. By limiting the relevant time horizon to the near future, discounting makes the deep climate future that fossil capitalization brings forth invisible. By cheapening and limiting the future, fossil capitalization engenders and hides ‘future theft’ (Table 1).

Operations of fossil capitalizations.

Climate Economics: Capitalizing the Atmosphere, Discounting the Future, Legitimizing Theft

Rosa Luxemburg (2015) has argued that capitalism relies on the constant appropriation of non-capitalistic milieus. Fossil capitalization also produces and relies on an outside; but it is not just spatial but also temporal. It introduces a financial asset life outlived by its ecological liabilities. Carbon emissions are the afterlife of past financial near futures and, at the same time, material operators of the planetary far future. With the growing awareness of the climate crisis, attempts to take the destructiveness of carbon emissions into account economically emerged. Climate economics and the political technologies they envision – carbon taxes and markets – seem to address the overshoot of fossil property as they seek to ‘internalize’ the ‘social cost of carbon’. At first glance this reverses the appropriative gesture of fossil capitalization. It does not exploit an outside but rather folds the outside in by ‘pricing externalities’. Yet, to do so the outside is made economically digestible by turning the slow and fast violence of climate dispossession into a mere matter of ‘social cost’ (Coase, 1960). Like the appropriative acts discussed previously, internalization creates its own terrain by turning the scarred landscape of climate damage into a flat surface of cost.

The inaugural act of climate economics is the seizure of its domain. It claims the atmosphere as a ‘common property of mankind’ (Edenhofer et al., 2013: 2). Unlike the fossil dominium, which is ruled by its private or state owners, the atmosphere, as a global common, can be brought under the rule of the climate imperium. But what allowed for and made necessary this becoming property of the atmosphere? Edenhofer et al. (2013: 10) argue that the atmosphere is an asset whose net present value derives from the ‘climate rent’ generated by selling pollution rights. This reasoning reveals the secret of how the atmosphere became property in the first place. The economic value of the atmosphere, we learn, does not derive from its ecological capacity to create a balanced temperature but from its economic appropriation as a dumb space for carbon emissions.

To subvert theories of productive appropriation according to which something becomes property by mixing it with work (Locke, 1982 [1689]: 288), Michel Serres (2010) introduced the concept of ‘appropriation through pollution’, according to which something becomes property by mixing it with waste. This does not only hold true for the curious cases Serres discusses, like spitting on food to claim it for yourself, but also for the way the atmosphere became ‘common property’ in and through its ecological wreckage. The pollution of the atmosphere with CO2 emissions appropriated the atmosphere. In a logic reminiscent of that of preemption discussed above, the material act of pollutive ‘air-appropriation’ (Folkers, 2020) thus preceded the subsequent declaration of the damaged atmosphere as a global common. Only because of this pollutive seizure did it become possible for climate scientists to measure and map the atmosphere in terms of carbon molecules. In carbon budgeting the parts per million of carbon in the atmosphere indicate the ‘atmospheric capital’ (WBGU, 2009: 2), the dumb space left to pollute without exceeding certain temperature thresholds. This provides the calculative bedrock for the economic distribution of limited atmospheric pollution rights.

Once established, this logic started to spill over to other earth spheres. The ‘cost of carbon’ is now the most prominent accounting unit to value the biosphere. In ‘natural capital’ accounting, trees, wetlands, even whales (Buller, 2022: 1) become valuable because they sequester carbon. Again, the calculative and legal work of turning nature into a carbon sink and thus a ‘carbon asset’ (Langley et al., 2021) depends on the preceding pollutive appropriation through the carbon residuals of fossil fuels. Atmospheric appropriation engenders biospheric appropriation. Pollution breeds property. It turns nature into capital. Pollution achieves what production could never do. It spawns a boundless über-appropriation that, while exceeding the limits of private property, does not end ownership per se. It rather turns the entire planet into property and assigns ‘mankind’ as its owner.

The assigning of a property title to the atmosphere raised the question of how to ab/use it most efficiently. How to pollute it in a way that none of its waste disposal capacity is ‘wasted’, so left unexploited. This led to the search for an ‘optimal climate change’ (Randalls, 2011) which the czar of climate economics, William Nordhaus, described as finding the sweet spot ‘between wrecking the economy and wrecking the world’ (Nordhaus in Buller, 2022: 18). To identify the atmosphere’s ‘maximum sustainable yield’, climate economists conduct a cost-benefit analysis weighing the costs for decarbonization against its benefit – the avoided costs of future climate damage. Long before ‘loss and damage’ became a prominent concern in climate politics, this analysis addressed the problem of climate destruction from an economic perspective. Since climate cost-benefit analyses are about an intertemporal distribution, they – like asset valuations – use discounting, which reduces the future costs of climate damages in relation to the current benefits of fossil fuel combustion. Climate economists usually justify this by the assumption that since ‘the future’ will be richer, it will be better equipped to deal with climate damages (Dasgupta, 2008). ‘We’ cannot curtail fossil growth too much now, because ‘our children’ will need it to be rich enough to deal with the fallout of this growth. Discounting once again cheapens the future, which lowers the ambition to fight climate change. In addition, discounting – again – limits the future to be taken into account. As Archer (2016) shows, each carbon molecule causes climate perturbations over one hundred thousand years on its long journey through the earth system. However, when translating these damages into discounted cost, the future horizon shrinks to a few decades (Archer, 2016: 172). Discounting not only limits the lifetime of a fossil asset but also abstracts from its long carbon afterlife as ecological liability. Discounting underpins the fossil revenue horizon twice: by allowing investors to buy fossil assets cheaper in the present and by reducing the ‘social costs of carbon’, making it less likely that fossil assets are ‘stranded’ due to stricter climate regulation. High discount rates prevent climate economics from preempting further future theft. If the full carbon cost of fossil assets would have to be considered in their valuation, they could have never been borne and fossil fuels never extracted.

Yet, the logic of climate economics is flawed beyond discounting. It does not consider who will have to bear the actual costs of carbon and who is responsible for them. In fact, Ronald Coase (1960) introduced the concept of ‘social cost’ to dodge the legal problematic of liabilities for property damages caused by other properties – for example, one farmer’s cows trampling on another farmer’s cornfield. Instead of holding one party liable, one should assume a reciprocal relation of costs and benefits to be balanced in a way that increases the welfare of all involved parties. This displacement of legal responsibility in favor of economic efficiency casts its long shadow over the contemporary political economy of climate change. In hegemonic climate economics and politics there are no serious considerations to mobilize the revenues from ‘using’ the atmospheric asset to fund compensations for the damages of global heating. The neoliberal strategy to put a price on carbon was never about covering future costs but about sending price signals to steer market behaviour.

Similarly, economic cost-benefit calculations only account for on an idealized future, not for the way the future will be burdened by the past. They only consider the remaining atmospheric assets in terms of carbon budgets, not the actual ecological liabilities of fossil fuels. The focus on the efficient use of atmospheric assets translated into a neat climate goal has created a dangerous illusion: within the temperature limits, everything will be fine. Even though climate goals based on cost-benefit analysis explicitly acknowledge, and thus legitimize, damages below the temperature threshold, they do not come with meaningful consideration of how to deal with those damages. This becomes painfully obvious today as climate change is no longer just a threatening future but has become a hard felt present reality. We already inhabit the discounted future and must repay the climate debt at a steep interest. It’s payback time! We are doomed to carry the ‘yoke’ of yesterday’s foresight. We will very likely fail to reach our climate goals. But we must also concede that the climate goals have always already failed us. The present climate damages which are still below what economists believed to be an ‘optimal climate change’ are already painful to most, devastating to many, unbearable to more and more. While the atmospheric assets are shrinking rapidly, we are left with fossil liabilities nobody seems to own but everyone must bear – in a common but highly unequal and discriminatory way.

Reclaiming the Stolen Future: From Climate Tort to Reparation

Climate economics abstracts from the polarization of climate victims and perpetrators, of winners and losers in the ‘climate casino’ (Nordhaus, 2013). The accusation of future theft by the Euro-American climate movement challenges this framing by pointing out how discounting future ‘costs’ creates an intergenerational rupture. It delays climate action and disproportionally places climate costs on future generations. However, generational framings tend to divert attention from other climate equity issues (Humphreys, 2022). For decades climate justice advocates have stressed that high emissions in the North have contributed most to global heating whose effects will disproportionately fall on the South (Agarwal and Narain, 1991). In addition, a recent study by Chancel (2022) showed that the richest 10% of the world’s population emit almost four times more than the poorest 50%. Remarkably, the driving force behind this is the same that, according to Chancel’s long-time collaborator Thomas Piketty (2014), also explains rising economic inequality: asset wealth accumulation: ‘the bulk (70%) of emission from the global top 1% comes from their investments rather than from their consumption. This appears to be due to the rise [. . .] in wealth inequality’ (Chancel, 2022: 934f.). It is, in other words, not so much how the 1% spend their money (e.g. on private jets) but how they make their money (as fossil investors). It’s fossil capital, not just carbon consumption. This underlines the importance of focusing on the relation between fossil asset owners and climate victims as an intertemporal and not simply intergenerational relation. Therefore, in the next section I explore what socio-political tremors might emerge along this faultline. I analyse a climate tort that shows the potential as well as the limit of the liberal matrix of ownership for holding fossil capitalists accountable and then reflect on the (im)possibility of just climate reparations.

Climate Torts

Hegel (1991: 73) conceptualized property as the ‘external sphere of freedom’ – the realm of possessed things through which the person’s free will receives an objective existence. Marx showed how this sphere tends to operate independently of willed subjects: as commodity, property assumes a life of its own. Fossil assets extend and explode this tendency. They inflate the radius of their owner’s actions qua CO2 emissions into the deep time of the earth system. This has legal ramifications. By extending their selves into possessed objects, the ‘absentee owners’ (Veblen, 1997) of fossil assets become potentially liable for the latter’s unruly actions, the spills and leaks of property. Property law provides a matrix to address these liabilities and equips propertied victims of damages with legal standing. That is why climate jurisprudence became a privileged site for climate activists seeking to hold fossil companies responsible. In a current climate tort brought before a regional court in Germany, the Peruvian farmer Saúl Luciano Lliuya has sued the energy company RWE for climate damages (Bertram, 2022; Walker-Crawford, 2023). The case connects fossil asset owners and the ‘owners’ of climate costs across long spatio-temporal distances, crossing existing jurisdictions.

Lliuya’s property is threatened by a glacier that is rapidly melting because of global heating. Models show that if part of the glacier should collapse into the glacial lagoon, a giant flood wave could destroy his village (Frey et al., 2018). What prevents the villagers from drowning is a dam and a drainage system. The plaintiffs therefore claim a contribution by RWE for these resilience expenditures. The lawsuit is based on a passage in German property law which prohibits interference with another’s property. The clause usually applies to neighborhood disputes, regulating cases of nuisance between proximate properties. By admitting the action to trial, however, the court recognized that climate change brings about new planetary neighborhoods. The CO2-saturated atmosphere creates a new juridical topology in which distant places become proximate. Remarkably, the legal commentary to the law from 1899 already states:

We live at the bottom of a sea of air. This [. . .] necessarily means that human action extends into the distance. [. . .] [O]ne must not only consider the relationship of neighbor to neighbor [. . .] the scope of the owner’s right can also be made to bear on all people.

2

The atmosphere becomes a medium for the spatial and temporal extension of fossil asset owners’ dominium. It allows them to ‘act’ on distant times and spaces. This constitutes their threatening power over the destiny of the planet but also explodes their legal liability.

The plaintiffs have assembled a cascade of expertise to knit together the casual chain connecting RWE and Lliuya. Hazard modelling shows that Lliuya’s property is threatened by the melting glacier (Frey et al., 2018). Climate attribution studies indicate that global heating is responsible for melting glaciers in the Andes (Stuart-Smith et al., 2021). Carbon accounting reveals the extent to which RWE is responsible for climate change. For the latter, the lawsuit draws on information by the Carbon Majors project, which compiles data on the historic CO2 emissions of the companies which together occupy more than two-thirds of the atmospheric carbon dump (Heede, 2014). RWE has contributed roughly 0.5% of carbon emissions, and therefore should, the plaintiffs argue, bear 0.5% of the cost for flood protection, or $18,800. This form of carbon accounting turns CO2 emissions into forensic evidence. By linking historical emissions to present and future damages, carbon forensics, unlike climate economics, does not present the atmosphere as a finite dumping ground to be exploited as efficiently as possible. Rather it treats it as an archive: not as an almost depleted resource, but as a repository of fossil residuals that can be turned into indexes of historical injustice. Not as a ‘budget’ of remaining atmospheric capital but as a legal balance sheet where emissions enter on the liability side as carbon debt.

While the court case certainly provides an interesting scenario of how to deal with fossil liabilities, it offers little more than ‘environmental justice “light”’ (Bertram, 2022). Climate compensations based on individual court decisions will likely remain sporadic and require resources that victims often don’t have. German non-governmental organizations funding the case have already invested much more in the court proceedings than the amount in dispute. And even if the case succeeds – which is questionable – it remains trapped by strictures of property law that can only reckon with property owners. Compensations in climate torts necessarily reproduce existing distributions of property and wealth. Climate damages in poorer countries are simply cheaper than those in the rich countries. Given the current distribution of wealth and power, it is not unlikely that wealthy owners of waterfront properties have a better chance to receive climate compensations than poor people who would need them most. Nor can torts offer compensations in cases in which clearly assigned property titles don’t exist. They therefore exclude everyone without existing property titles, ranging from the already dispossessed to all communities that don’t conform to Western understandings of property. Historically, this was the reason why slave owners and not the enslaved received compensation after the abolition of slavery. Nowadays, there is the real risk that a similar pattern will ensue. Should governments decide to prohibit further fossil extraction projects, the rules for calculating compensation in international investment treaties often guarantee investors reimbursement for forgone revenues of politically ‘stranded assets’ (Dehm, 2023). They would, in other words, receive compensation for merely expected profits and not only for past costs for extractive infrastructure. In contrast to the super-secured assets of fossil owners, victims of climate damages have no similar claim on the future. They could only claim compensation for actual costs or, in the absence of a legal claim on property, are excluded from compensation altogether.

Climate Reparations

Recent calls for climate reparations (Burkett, 2009; Táíwò, 2022) promise to move the struggle for the repayment of ‘climate debt’ beyond individual compensation for property owners. Historically, reparations have been a vehicle to circumvent the problem that one can only receive compensation or a repayment of debt in the presence of established property claims, or contractual agreements. Reparations transcend the established legal system towards a more fundamental ‘right to have rights’. In this vein, climate reparations could create a legal standing of climate victims in the absence of a previously existing property title. They could address ‘theft’ where that which has been stolen has never been formally owned. 3

However, the problem of ‘future theft’ provides a significant challenge even for the way reparations have traditionally been conceived: addressing past historical injustices. Global heating clearly represents a historical injustice. But it is by no means a problem of the past but will only be aggravated in the future. Its wounds will not heal but be exacerbated with time, because the accumulation of fossil capital not only relies on the past but also on future dispossessions. ‘Climate debt’ cannot be settled once and for all because it extends into the future with compound interest. Reparations traditionally entail the obligation of non-repetition and the elimination of the source of harm (Burkett, 2009). Climate reparations thus imply fossil fuel abolition. However, since – once released in the atmosphere – CO2 will stay there for centuries and heat up the planet further, climate change is nothing but the repetition of the past in the future. Global heating intensifies and sustains other deep-rooted and similarly unfinished historical injustices. As Olúfẹ́miTáíwò (2022: 170f.) writes:

It is not that every aspect of today’s global racial empire is rooted in the impacts of climate change. But every aspect of tomorrow’s global racial empire will be. Climate change is set not just to redistribute social advantages, but to do so in a way that compounds and locks in the distributional injustices we’ve inherited from history.

One of the most important contemporary engines for sustained distributional injustices, both in terms of race and class, is the neoliberal ‘asset economy’ (Adkins et al., 2020). It has widened the gap between rich and poor by making ownership the major source of wealth generation as returns on capital exceed growth in income from labor (Piketty, 2014). This has also made economic inequality more durable. In addition to the extension of asset lifetimes, a variety of legal, economic, and political techniques make it possible to transfer wealth over time, by either passing it to family members (Beckert, 2022) or containing it in the corporation (Davies, 2020). 4 With global heating the durability and escalating dynamics of inequalities created by asset wealth accumulation will be compounded by the ecological durability of carbon waste accumulation. Wealthy fossil asset owners are in the unique position to make a net economic gain from climate change. Because they can transfer their capital over time at compound interest, they and their heirs will likely be economically richer in a costly catastrophic climate future than in an alternative scenario in which their assets are stranded because of stricter climate regulation. For them it really is advantageous to discount future climate costs because they will likely be richer in the future that discounting engenders. Even though the top 10% will – according to estimates by Chancel et al. (2023: 86) – suffer a relative income loss of 3% from climate damages, this will easily be compensated by a return on their investments which ranges between 7% and 9% among the top 1%. The bottom 50%, on the other hand, will have an income loss of 75%, which amounts to complete dispossession. The burden of repayment imposed by climate damages will likely resemble a grotesquely regressive tax on the future.

The twin processes engendered by inherited economic wealth and inherited ecological waste make fossil asset owners the obvious target for climate reparation demands. They are not only disproportionally responsible for global heating. Their wealth is intrinsically bound up with climate damages. As a ‘zombie form that outlives mortal humans’ (Davies, 2020), the fossil corporation seems to be a particularly suitable target for such complex temporal claims, because it represents a non-human legal heir for the legacies of capital and carbon accumulation. However morally and economically justified, the political prospects of targeting fossil capitalists are limited. The ongoing-ness of the climate emergency not only deprives its victims of any sense of closure. Its costs will also likely overwhelm its perpetrators. All existing estimates indicate that the overall costs of future climate damages will exceed accumulated fossil revenues. Just imagine all the destroyed water pumps and infrastructure, lost harvests and drowned cities all over the world that RWE would have to pay 0.5% for – now and in the deep future. In the economy of planetary energy flows, the energetic ‘return’ of fossil fuels will far exceed the return of fossil capital. As Archer explains (2016: 174): ‘The bad global heating energy from burning a gallon of oil ultimately outweighs the good energy by a factor of about 40 million.’ All that which fossil capitalization discounted to secure ‘present values’ is bound to return as unpayable debt with compound interest in the future. This implies that demands for climate reparations addressing fossil companies are doomed to fail. They can either only claim symbolic compensations or will bankrupt the source of compensations with more ambitious demands. While certainly morally satisfying, this would not help politically or economically.

Fossil capitalization inaugurates a tempo-materially mediated ‘class’ relation in which the exploiters/expropriators will probably have already disappeared before the exploited/expropriated have fully emerged – after all, the latter includes the not yet born. Fossil accumulation’s deferral of dispossessions into the future immunizes fossil asset owners against being held fully accountable. As much as climate reparation might strive to reclaim and redeem the stolen future, it comes up against the irreversibility of the material time of climate change and the contradiction between the finite life of the fossil asset and the virtual infinity of its carbon afterlives. In many ways this situation is extremely frustrating as the final day of reckoning will never arrive. The contemporary moment in which fossil asset owners and climate victims can have their literal and proverbial ‘day in court’ is just a blip in the deep time of the earth system – an important one, to be sure, not to be missed to claim as much payback as possible.

In the climate long run, however, when even the zombie fossil corporations will be dead, it will no longer be possible to fully reclaim the stolen future from its thieves. Rather, there is reason to fear that climate damages will eventually really become ‘social costs’ – but neither in an efficient Coasian nor in an equitable socialist sense. The best one could hope for would probably be something like a tax funded or subsidized climate insurance mechanism that socializes risks. The experience of the social insurance in the welfare state (Ewald, 2020) suggests that this might be much more effective in providing existential support to climate victims than fighting for compensation in court. Non-governmental organizations have long called for public climate insurance schemes to be partly funded by the revenue from carbon taxes which could – given the wealth-emission and poverty-vulnerability nexus – in fact be redistributive if designed appropriately (Richards and Boom, 2014). Still, the source of such tax revenues will – hopefully – dry out at the time when it would be needed most. In contrast to the welfare state counting on rising tax income due to economic growth, a future climate risk regime would have to cope with a diminishing carbon tax base. But even a just way to socialize climate cost could only offer financial compensation for losses that are often incommensurable. It cannot redeem existential injuries. It can compensate you for belongings but not the world you belong to.

These limits indicate the need to go beyond the logic of ‘social cost’ and capitalist ownership. For Marx (2024 [1867]: 791) the revolution was a reversal of the original accumulation, the reappropriation of what was stolen during the dispossessive beginning of capitalism. The ‘expropriators are expropriated’. This reappropriation was not simply restitutive. The revolution would also reappropriate the wealth generated through exploitation made possible by the original dispossession. However, the logic of capitalist pre-appropriation – future theft as temporally inverted ‘original accumulation’ – complicates socialist re-appropriation. Dispossession is yet to come. If the value of fossil assets is not simply based on past labor, but on the economic and ecological burdens they impose on the future, one cannot appropriate material wealth without the waste that goes along with it. Capital’s ecological afterlife would extend into post-capitalism. The revolution must therefore be reparative and not just re-appropriative. It needs to redeem past exploitations and future dispossessions – not only seize the wealth tied up in the shackles of private property but repair the damage caused by the polluting logic of appropriation.

Conclusion

The climate emergency makes the negativity of property – destruction and dispossession – a more and more widely shared experience. This calls for an ecological critique of property that emphasizes the pollutive rather than productive character of appropriation. This article provides steps towards such a critique by illuminating the logic of future theft as a temporally and materially mediated class relation between fossil asset owners drawing value from and victims of climate damage becoming dispossessed in the future. Fossil asset ownership creates durable economic wealth for some but ecological waste for everybody. The contradiction of fossil capitalism between individual enrichment and collective impoverishment is glaring. But the temporal schism between the accumulation of fossil capital and the dispossession it depends on prohibits holding fossil companies and their shareholders fully accountable for climate damages. Carbon liabilities will outlive the fossil assets. However, this also prohibits finding refuge in the old apologies of property. Property is not productive but pollutive, it does not secure but endanger the future, it does not improve but ruin the planet and its inhabitants.

Footnotes

Acknowledgements

I presented different parts and versions of this article at the Institute for Advanced Study in Princeton, Helsinki-University, Sciences Po Paris, Central European University in Vienna, Phillips-University Marburg, and online at the University of Jena and the School of Advanced Study, University of London. I thank the organizers for the invitations, the various prompts that inspired me to explore different facets of the article, and thought-provoking discussions. I would also like to thank the contributors to this Special Issue for an extremely insightful zoom discussion of my article. Last but not least, I thank the four anonymous referees for their enormously perceptive and productive comments.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The work on this article has been funded by a grant from the German Research Foundation (Grant No. 433336180).