Abstract

Money has been a polarising and unresolved socio-economic issue for more than 300 years. In this article, we explore how the state became increasingly involved in money and, through the words of prominent monetary theorists, identify the problem of the state in money. We analyse Bitcoin to see if it is a solution to this problem but move on to contend that the political dimension needs to be the focus of theory in the 21st century and that control of the supply of money, and the power that it gives, is the root of contention.

Introduction

Money is ‘the pivotal institution of modern capitalism’ (Ingham, 2004: 18). Yet, debates about the form of money, its politicisation, and even about what it is, have persisted for millennia (Ingham, 2020: 3). As much as money is an enabler of society, it has also been viewed as a perennial source of evil (Ferguson, 2008: 1–2). Should money be abolished altogether or could it be transformed to become a ‘means of improving society’ and achieving ‘monetary utopia’ (Dodd, 2012: 146–7)? Theory remains divided. However, amongst the many dualisms and conflicts, there is a common theme that emerges: the problem of the state in money.

In this article, we evidence this problem through several prominent monetary thinkers. We then introduce Bitcoin, which emerged as a reported counter to this problem, and note that it has been met with scepticism, criticism and even dismissal. Using Ingham’s ‘money question’, we analyse Bitcoin to examine these concerns. There are two elements: ‘first, an adequate theory of money – what it is and how it is produced; and, second, the essential political dimension – who controls the production of money; how much; to what ends?’ (Ingham, 2020: 135).

To the first element, we apply Georg Simmel’s seminal The Philosophy of Money to examine Bitcoin from a technical perspective. We argue that debate should move beyond the traditional and fundamental clash of commodity theory versus claim theory, thereby framing the second element of the money question as the most important. We contend that the political dimension is at the heart of the debate about money and that at the epicentre of centuries of tension is one issue: supply. In the 21st century, this is where we need to focus debate about the future of money. Society depends on it.

Money – The Fundamental Clash

For centuries, the main divide amongst monetary scholars has been commodity versus claim theory. For commodity theorists, money emerged from barter, as an object to exchange with and value other commodities. Cows, salt and even shells were used as money (Menger, 1892: 239). However, precious metals soon became the commodity of choice, as they were durable and enabled division and reconstitution. Commodity theory expressed itself as metallism, where sound money is based on the scarcity of precious metals ‘with intrinsic value’, such as gold. This is also the classical view of money in economics, as merely a ‘medium of exchange’. Claim theorists, however, view money in an abstract sense as a ‘claim, or credit, measured by a money of account’ (Ingham, 2006: 260). Money is more than just a technical device, with a ‘life and an importance’ of its own (Schumpeter, 1954: 265); or to Ingham, money is ‘a dynamic independent economic force’ (2020: 5).

Metallism dominated the late 17th century and was advocated by the likes of John Locke (Ingham, 2020: 18). It was during this period that King William III of England passed an act to raise funds for war against France, leading to the formation of the Bank of England in 1694. The bank issued promissory paper notes, which could be redeemed for precious metal ‘to the bearer on demand’. This was effectively still a metallist system, with the paper ‘representing’ the underlying precious metal. But, in 1797, following further concern over revolutionary France, the Bank Restriction Act was passed, and the bank suspended the conversion of notes into gold (O’Brien and Palma, 2020). This was a watershed moment – trust that paper could be exchanged for precious metal was broken. And it was the state that broke this trust. There followed over 200 years of debate about commodity versus claim theory, about the merits or otherwise of a gold standard, of fiat currencies and about various new, competing theories of ‘what to do’ with money. And the state remains integral to this discussion.

The Problem of the State

The Bank Restriction Act highlighted a long-standing area of contention – that weakness in the form of money enables those in power to debase it, to their advantage. In the era of precious metals coins were physically debased and, with the advent of paper notes, the same effect was achieved by printing more notes than were backed by gold. As Adam Smith puts it in The Wealth of Nations of 1776: The avarice and injustice of princes and sovereign states, abusing the confidence of their subjects, have by degrees diminished the real quantity of metal … to pay their debts and to fulfil their engagements. [This is] … favourable to the debtor … ruinous to the creditor, and … sometimes produced a greater and more universal revolution in the fortunes of private persons, than could have been occasioned by a very great public calamity. (Smith, 2007: 25–6)

We see here a seemingly inescapable paradox of money; metal restricts spending, but without it, confidence in government money falters. Even Knapp, author of The State Theory of Money, who argued that ‘money is a creature of law’, described paper money as a ‘degenerate’ and even ‘dangerous’ form (1924: 1–2). Keynes may have lost confidence in gold, but the age-old problems of money persisted: It is natural … that prudent people should desiderate a standard of value which is independent of Finance Ministers and State Banks. The present state of affairs has allowed to the ignorance and frivolity of statesmen an ample opportunity of bringing about ruinous consequences in the economic field. (Keynes, 1923: 169) The great inflations of our age are … government made. They are the off-shoots of doctrines that ascribe to governments the magic power of creating wealth out of nothing. (Von Mises, 2009: 9) I don’t believe we shall ever have a good money again before we take the thing out of the hands of government. That is, we can’t take it violently out of the hands of government. All we can do is by some sly roundabout way introduce something they can’t stop. (quoted in Harvey and Branco-Illodo, 2020)

Modern Money

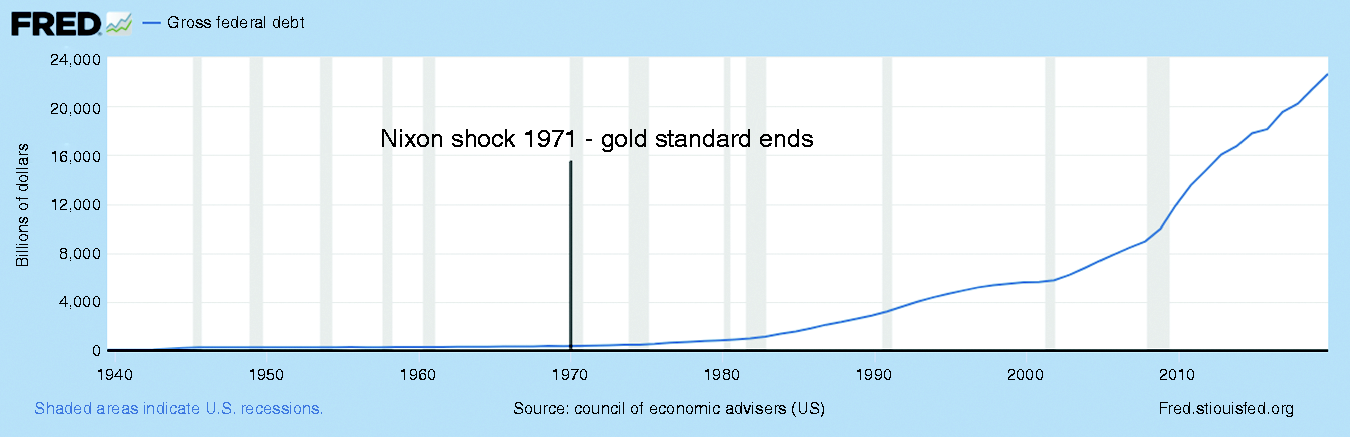

Where the gold standard hoped to limit the supply of money through scarcity enforced by mother nature, later theories also spoke to the issue of supply. For monetarists, who revived the quantity theory of money and accepted that increasing the supply of money led to inflation, supply of government money could be controlled through monetary policy and targets for inflation. Weber, though, in Economy and Society, had also warned that ‘there is no denying that any inflation with the issue of paper money determined by financial needs of the state is in danger of causing debasement of the currency. Nobody, not even Knapp, would deny this’ (1978: 192). Since the final end of the gold standard with the Nixon Shock of 1971, the outcome has been for greater currency devaluation and an explosion of national debt – the US dollar lost 87 per cent of its purchasing power between 1957 and 2008 (Ferguson, 2008: 63).

Governments across the world continue to build up debt through deficit spending, as expenditure exceeds income through taxation. The existing capitalist monetary system of endogenous and exogenous money allows this to happen, often via a central bank in concert with private financial institutions. But in the case of the UK Government, for example, it owns the bank that it owes money to. This raises the question of what we call Schrödinger’s debt: if you borrow money but never have to pay it back, is it really a debt? The ultimate expression of this thinking is Modern Monetary Theory. Chartalist in its origin, Modern Monetary Theory places the state and state money at the centre of the monetary system. As the antithesis of orthodox economic thinking, Modern Monetary Theory’s most important concept ‘is that the issuer of a currency faces no financial constraints’ (Mitchell et al., 2019: 13). That is, a country can never become insolvent and can never run out of the money that it controls the supply of. In this way, Modern Monetary Theory argues that it does not make sense to compare the finances of a state with a household. Furthermore, government should not wait for tax revenue to spend – it must spend first. ‘The cult of austerity’, they argue, is based on outdated gold standard logic (p. 14).

These views are at odds, though, with Mitchell-Innes who wrote in ‘The Credit Theory of Money’, on which Modern Monetary Theory is partly based, that ‘the issue of money is the burden and the taxation … the blessing’ and that ‘because we do not realize that the financial needs of a government do not differ from those of a private person … there can … be no question that the money of the American Government is depreciating’ (1914: 6, 10). Mitchell-Innes is clear that ‘excessive indebtedness’ causes a fall in the value of money and a ‘general rise in prices’ – a depreciation that has become ‘more gradual and therefore more insidious’ (pp. 6, 11). The explosion of debt and now rising inflation across the world, particularly since the coronavirus pandemic, are of great concern. The fact, however, is that the more government money there is in circulation, the poorer we are. Of all the principles which we may learn from the credit theory, none is more important than this, and until we have thoroughly digested it we are not in a position to enact sound currency laws. (Mitchell-Innes, 1914: 7) US Gross Federal Debt (Council of Economic Advisors, 2020).

The Great Financial Crisis of 2007–8 saw a culmination of this last 200 years of economic theory and policy. Monetarist criticism of the Fed’s role in the Great Contraction established the central bank as the lender of last resort. Orthodoxy called for restraint and prudence in financial policy, but this was opposed by others demanding evermore state spending as the solution to lows in the economic cycle. And quantitative easing emerged as a tool of economic policy. Whilst quantitative easing does not involve physically ‘printing’ money, it does involve the creation of money ‘by the tapping of the [central bank] keyboard’ (Ingham, 2020: 95). The divisions still run deep. Henry Ford is frequently quoted as having said that if more people knew how the monetary system worked then there would be a revolution tomorrow (quoted in Ingham, 2020: 44). Or as Murray Rothbard put it, ‘the state is the organization of robbery systematized and writ large’ (1981: 66). Even a former Chair of the US Federal Deposit Insurance Corporation commented, in a nod to the Cantillon effect, ‘I do think the system’s rigged’ and it ‘favour[s] the wealthy’ (CNBC Television, 2019).

Our modern system, based on money creation primarily through bank-issued debt with interest, transfers wealth from the bulk of society to the top (Lietaer, 2001: 54), producing an unstable monetary system and a society where the ‘future doesn’t matter’ (Lietaer, 2014). Usury was condemned throughout much of history until only recently – now it is a systemic feature, concentrating wealth in a minority and driving inequality (Lietaer, 2001: 53). Growing inflation is also correlated with growing inequality (Albanesi, 2007) and excessive debt is related to lower growth (Reinhart and Rogoff, 2010). According to the International Monetary Fund, there were 425 systemic banking, monetary and debt crises between 1970 and 2010 – 10 per year (Lietaer et al., 2012: 10). Monopolistic state money has proven to be far from a resilient, equitable system and, historically, societies with multiple currencies enjoyed greater stability and equality (Lietaer et al., 2012: 9). Perhaps, then, a desecuritisation of other currencies could see them become part of the solution to systemic volatility, rather than merely as a challenge to state monetary hegemony.

The Philosophy of Bitcoin

For some, the answer to many of the questions about the state control of money lies in a new type of non-state money, cryptocurrencies. The first and largest of these, Bitcoin, emerged after the Great Financial Crisis of 2007–8, with the system going live in January 2009. The result of a whitepaper released in 2008 by a pseudonymous Satoshi Nakamoto (Butler, 2019: 331), Bitcoin was designed as a decentralised money – with a fixed supply that stood it in stark contrast to fiat currencies. It has no single, centralised owner or entity that runs it; instead, it is a voluntary, global network based on the use of its open-source software. Crucially, in this way, it is disintermediated from the state and banks (Carney, 2018: 6–7).

How is Bitcoin Technically Different?

Bitcoins are created through a computational process called ‘mining’ (for detail, see Antonopoulos, 2017; also Bjerg, 2016). Miners compete to process batches of transactions known as ‘blocks’ and the first to solve a ‘puzzle’ receives a reward of new Bitcoin. The blocks are then added to the previous record of blocks, hence the term blockchain. Bitcoin has been programmed so that just under 21 million Bitcoins will ever be produced (each Bitcoin can be divided into 100 million sub-units called Satoshis). The supply schedule to issue new Bitcoins is also fixed. The puzzle that miners solve is a Proof-of-Work algorithm that dynamically adjusts so that the puzzle is solved approximately every 10 minutes. When Bitcoin launched, the reward was 50 Bitcoin per block, and this schedule halves every 210,000 blocks (approximately every four years). The reward is currently 6.25 Bitcoin per block following the last halving in 2020. In this manner, the inflation rate decreases towards zero by approximately 2140. With a fixed total supply, Bitcoin is in effect deflationary, as users invariably lose access to some Bitcoins over time. This deflationary policy is a political statement aligned with the Austrian theory of money and establishes Bitcoin as hard money in contrast to the soft money of the state (Hayes, 2019). Whilst we do not know the identity of Satoshi Nakamoto, the roots of Bitcoin go back to the ‘Crypto Wars’ and the libertarian idealism of the cypherpunks, who sought privacy in cyberspace and saw electronic money as part of that vision (Hughes, 1993).

Bitcoin has been controversial since its creation, drawing significant criticism from politicians, bankers, economists, investors and academics (Butler, 2019; Gloerich et al., 2018). Cryptocurrencies have been labelled a security threat in relation to crime (Butler, 2020: 136), scammers abound, and cryptocurrency services have suffered from cyber-attacks (Zamani et al., 2020). Securing the Bitcoin network via the Proof-of-Work algorithm consumes significant amounts of electricity and, in a decentralised system, achieving consensus for software development has proven difficult (Aste et al., 2017: 12–13). There is also discussion about whether the greater early supply of Bitcoin has resulted in a skewed wealth concentration (see Kondor et al., 2014; Schultze-Kraft, 2021). And are peer-to-peer communities as free and open to all as envisioned (Nelms et al., 2018)?

Economic commentators have argued that Bitcoin cannot even be considered money as it has no ‘value’ (as opposed to gold, which can be used for other purposes) (Yermack, 2013; Torpey, 2017). But this has been challenged by Hayes (2017, 2018), who shows that the marginal cost of production is related to prices and argues that Bitcoin has intrinsic value through the intangible computational labour expended in the mining process. Ingham, too, dismisses cryptocurrencies, as they do ‘what money should not do: that is, introduce uncertainty into transactions’ (Ingham, 2020: 114). They are also volatile; in 2021, Bitcoin surged to a new high before again falling more than 50 per cent in a matter of weeks. This may be due to immaturity as money, but others claim Bitcoin is far from the stable currency needed for a base money regime, nor is its demand elastic (Luther, 2020). Bitcoin’s supply does not change relative to demand and remains constant in response to the dynamically adjusted difficulty of the Proof-of-Work algorithm. It is worth noting, however, that cryptocurrencies can be designed with a variety of properties, including even a dynamic supply schedule (Ampleforth, 2021).

These debates are symptomatic of a struggle by monetary theorists to define what Bitcoin is. Is it a commodity or fiat, or perhaps private fiat money, or even synthetic commodity money (Luther, 2018)? Luther also took Bitcoin’s existence to question Von Mises’ Regression Theorem, but this was refuted by Pickering (2019: 608), who argues that the theorem explains ‘the purchasing power of money using the subjective marginal utility theory of value’, not which commodities can emerge as money. But for all these discussions, it may be a moot point as to whether Bitcoin is money; in practice, it is used across the world as such. Coinbase, a prominent cryptocurrency exchange, saw its customer base rise from 35 to 54 million in the six months before its stock market listing in 2021. Demand and usage of cryptocurrencies continue to grow – Bitcoin alone settles in the region of 300,000 transactions, and as much as $45 billion in Bitcoin is sent per day (Bitinfocharts.com, 2021).

If Smith, Knapp, Keynes, Von Mises, Hayek and others have acknowledged the problem of the state in money, then why does Bitcoin receive such opposition? The arguments outlined provide some explanation, but many of them ‘apply equally… to our current forms of conventional money’ (Bjerg, 2016: 69). For example, if Bitcoin is criticised as a largely speculative vehicle, what do we make of the foreign exchange market where trade is 98 per cent speculative and whose volume dwarfs Bitcoin at over $2 trillion per day, even as far back as 2000 (Lietaer, 2001: 314)? In this way, ‘Bitcoin is no more fake than more conventional forms of money’ (Bjerg, 2016: 68). In the following sections, we turn to the first element of Ingham’s money question to resolve some of this confusion about money and Bitcoin. We use Simmel’s The Philosophy of Money to theoretically examine whether Bitcoin is money. Commodity versus claim theory has been such a fundamental divide for so long that it is essential to give this due consideration.

Chapter 1 of The Philosophy of Money – Value and Money

Value

That Bitcoin has no ‘value’ is an oft-used criticism in popular discourse, that speaks to commodity versus claim theory (Torpey, 2017). But does money need to have ‘value’? And what is value anyway? In Chapter 1 of The Philosophy of Money, Simmel notes that ‘an object does not gain a new quality if we call it valuable; it is valued because of the qualities it has’ (2004: 57). Value, therefore, is not a quality of an object, but a judgement of an object made by another (p. 60). To those that say that Bitcoin has no value, they are correct – but then no object, including gold, has intrinsic value either. Value is a subjective assessment. Another simple way to think of this is that value is not fixed and inherently measurable, unlike an actual quality of an object, like weight. It is a unit of measurement, and like all our abstract measures ‘no one has ever seen an ounce or a foot or an hour’ (Innes, 1914: 4). Whether the form of money is Bitcoin, gold or fiat, money has no intrinsic value and our practical notions of value only appear as one item is exchanged for another.

Utility and Scarcity

Some claim Bitcoin has no utility, whilst proponents often cite its scarcity in contrast to fiat currencies (Butler, 2019: 332). Simmel describes scarcity as supply, a quantitative relationship between an object and the total available, but it is utility that ‘appears as the absolute part of economic values’ (2004: 88). Interestingly, for Simmel, utility is ‘the desire for the object’; it is not about usefulness but rather economic activity as a result of demand. In fact, Simmel observes that ‘we desire, and therefore value economically, all kinds of things that cannot be called useful or serviceable’. And so, if usefulness is all that is in demand, we must accept that it is demand that is the driver of economic activity (Simmel, 2004: 88–9). Furthermore then, we realise that not all useful objects are in demand. A tree in a remote forest has uses for fire or as a building material but, in that context, there is no demand for it, therefore no utility, no economic activity. The claim, therefore, that Bitcoin has no utility is not valid according to Simmel. There is great demand for Bitcoin and so great utility, as it is driving the exchange of many objects and an enormous amount of economic transaction.

Chapter 2 of The Philosophy of Money – The Value of Money as a Substance

Intrinsic Value

But does money need ‘intrinsic value’, achieved through some commodity, or ‘is it enough if money is simply a token’ (Simmel, 2004: 129)? Simmel concludes it does not (p. 130), countering the argument that Bitcoin fails as money as it has no intrinsic value. As a simple explanation of Simmel’s logic, let us assume there are a total of 10 eggs and $10 in the world. It follows that we can calculate a value for one egg, i.e. $1, without the dollar requiring intrinsic value itself.

Primitive economies began by using items of value for money but, Simmel argues, at that stage of an economy it would hardly be possible to do anything else. Who would accept a worthless piece of paper in exchange for something valuable like cattle? Money with value was a necessary starting point but society and money have evolved to move beyond needing this readily exchangeable value. Coins in a pocket do not have value because the metal can be used elsewhere (Simmel, 2004: 141). Even today, ‘metal money stands on an equal basis with paper money as a result of the growing psychological indifference to its value as metal’ (p. 141). The substance of money is not important. In this regard, fiat proves that something without intrinsic value can be money. Fiat does not have a link to precious metals and yet still functions as a medium of exchange. In the same way that it does not matter if a ruler to measure distance is made from plastic, wood or metal, ‘so the scale that money provides for the determination of values has nothing to do with the nature of its substance’ (Simmel, 2004: 146). And the movement from objects of value to ‘symbolic’ money is a marker of cultural development (p. 146). Indeed, for Simmel, the growth of intellectual ability in society and the development of abstract thought is characterised by the development of money closer and closer to a symbolic form, without intrinsic value (p. 150).

Furthermore, Simmel argues that even the most useful object has to give up its usefulness to function as money (p. 151). That is, you cannot use gold for its other purposes when it is being used as money. This comes at a cost – if gold was no longer used as money, then there would be plenty for its other purposes. In this way, hoarding gold contributes to its value and makes it expensive for its other uses (p. 154). The argument that gold is a better form of money than Bitcoin as it has other uses is not correct according to the philosophy of Simmel. Finally, there is an informal logical fallacy, petitio principii, in the argument. The premise that good money has other uses is assumed (whilst Simmel argues the opposite) and used in circular reasoning to declare that gold, therefore, is good money as it has value/other uses. Bitcoin and fiat pass the Simmel test for a pure money, gold does not. Having other uses does not make something a better money – according to Simmel, it makes it worse.

Money as a Symbol

Given, then, that gold is not the best form of money and that fiat passes the Simmel test, why would there be any need for Bitcoin? The problem, as noted earlier, lies in the state’s misuse of money: Although, in principle, the exchange function of money could be accomplished by mere token money, no human power could provide a sufficient guarantee against possible misuse. The functions of exchange and reckoning obviously depend upon a limitation of the quantity of money, upon its ‘scarcity’. (Simmel, 2004: 158)

It is scarcity, or the control of supply, that is the real issue in money for Simmel, and for many of the other thinkers we have discussed, not whether the money is of a physical or abstract form. And it is here that Bitcoin differs from fiat state money, even though both are pure token forms. Simmel, like others, makes the issue of abuse clear here in reference to the Cantillon effect, where those who issue money benefit from spending money before prices have a chance to ‘catch up’: The numerator of the money fraction – the price of commodities – rises proportionately to the increased supply of money only after the large quantities of new money have already been spent by the government, which then finds itself confronted again with a reduced supply of money. The temptation then to make a new issue of money is generally irresistible, and the process begins all over again. I mention this only as an example of the numerous and frequently discussed failures of arbitrary issues of paper money, which present themselves as a temptation whenever money is not closely linked with a substance of a limited supply. (Simmel, 2004: 158–9)

The issue of money then is not about a clash of commodity theorists and claim theorists; as Ingham puts it, ‘the legacy of commodity theory and metallism’s misunderstandings of money should now be laid to rest’ (2020: 40). These debates are a distraction from what matters. Bitcoin is money, just as fiat and gold are. We have argued extensively about why Bitcoin is money, not to say that we should use it as money, but to remove this area of debate from our remaining consideration of the money question, the political dimension. This, we argue, is where the money question solely relates in the information age.

The Political Dimension

If the Simmel test shows that Bitcoin is a purer and better form of money than gold, and if the discussion of symbolic money in The Philosophy of Money also appears to support a cryptocurrency such as Bitcoin, which arguably has a ‘technically feasible’ solution to the misuse of supply, then why does there remain so much opposition to it beyond the criticisms already discussed? The answers lie in the second element of Ingham’s money question, which concerns the political dimension – who controls money, how much is produced and to what ends. Here the divide is Keynesianism/state theory versus the Austrian School, with monetarism and the current system somewhere between the two. Both sides acknowledge the problems of state involvement in money; the contention is over what to do about it.

Von Mises wrote, in reference to socialists, that, ‘economics… figures all too sparsely in the glamourous pictures painted by Utopians’ (2012: xvii). For Von Mises, central planning does not work, due to the ‘problem of economic calculation’ (p. 38). Similarly, governments have proven incapable of centrally managing money. As inflation reached 26 per cent by 1976 in the UK (Ingham, 2020: 77), Hayek wrote, in The Denationalisation of Money, of his ‘despair’ in finding a political solution to inflation (1990: 13). He saw ‘the age-old government monopoly of the issue of money’ as the chief cause of recurring depressions and high unemployment (p. 14). Private industry, he believed, could provide the public with a choice of currencies in satisfaction of ‘the demand for the freedom of the issue of money’. It was in this vein that Bitcoin emerged in 2008 as ‘an entirely novel form of money’ (Ingham, 2020: 111). There has followed a growing body of sociological research about Bitcoin, which we now consider in regard to the political dimension of Bitcoin and money.

Bitcoin as Politics

One of the first surveys of Bitcoin users concluded that Bitcoin means different things to different people (Bashir et al., 2016). This is telling, as there is a reductionist tendency in debate about cryptocurrencies to oversimplify with sweeping statements. For example, many claim that cryptocurrencies are primarily a criminal tool (Butler, 2019: 326–7). Of course, criminals are using them, but the majority of transactions are legitimate (p. 335). The survey authors compare the psychological perspectives of money in terms of security, power, love and freedom. This is linked to the libertarian view, where Bitcoin appears to offer a new social order and its limited supply translates to a loss of power for the state (Bashir et al., 2016: 356). Indeed, a YouTube video called ‘The Declaration of Bitcoin’s Independence’ states that ‘Bitcoin is inherently anti-establishment, anti-system, and anti-state’ (Dodd, 2017: 36).

Another study, by Maurer, Nelms and Swartz (2013), investigated Bitcoin from a semiotics perspective. They showed that Bitcoin ‘provides an alternative to currencies and payment systems that are seen to threaten users’ privacy, limit personal liberty, and undermine the value of money through state and corporate oversight’ (2013: 261). They also observe, like Simmel, that the real meaning of Bitcoin is below the surface level of its use as a currency; that is, as an ‘index of much broader discussions over the nature of money’ (p. 263). Their language alludes to the political essence of the furore surrounding Bitcoin – it is not about transactions per second, it is about the fundamentals of our society, about how it should be run, and, crucially, about who controls the ‘pivotal institution’ of money.

Bitcoin emerged in the world at a time of great social unrest. Without drifting into Stiegler, the philosophy of technology or the debate about ‘technological determinism versus social shaping’ (Schroeder, 2018: 18), Bitcoin (specifically) is a form of activism, in that it would not have been created unless it was designed to challenge something else. Maddox et al. argue that ‘Bitcoin can be seen as an act of social resistance’ (2016: 65). There is an irony here; whilst the state and others have been critical of Bitcoin and the threats that it poses to society, people are using it to protect themselves from the state, to achieve self-sovereignty, and to ‘challenge conventional conceptions of the relations between money and nation-states’ (Bjerg, 2016: 64). In this way, Bitcoin is counter-securitising. The challenge that Bitcoin symbolises, therefore, lies in the political dimension of the money question.

But it is here that we meet a familiar refrain regarding Bitcoin – that it is often difficult to know what it is about. To some it is anti-state, but for others it is about something different. Research also adds to this confusion. For example, Yelowitz and Wilson (2015: 1030) analysed Google trends data to show that ‘computer programming and illegal activity search terms are positively correlated with Bitcoin interest, whilst Libertarian and investment terms are not’. Yet Glaser et al. (2014) concluded that new users were interested in Bitcoin as an alternative investment rather than as a new method of transaction. Researchers have tried to attribute the politics of Bitcoin to particular factions, such as libertarians, but this misses a point borne out in The Philosophy of Money. Bitcoin is not libertarian or right-wing because anyone says it is. Bitcoin has the properties it has and people from different leanings use it for those properties – it is a mistake to then transfer those political leanings back on to Bitcoin as ‘new’ properties. Doing so only clouds our view of Bitcoin. This is important, as it helps explain why there is such a variety of people and groupings using Bitcoin. Users do not define the properties of the system; the system is what it is. Bitcoin is fascinating precisely because it demonstrates many of the contradictions and confusions that characterize money, and its relationship to law and the state, in general. Bitcoin is both a symptom of increasing monetary pluralism in the advanced capitalist societies, and an embodiment of monetary diversity in its own right. Like money itself, Bitcoin is multi-faceted, politically contested and sociologically rich in its functions and meanings. (Dodd, 2017: 36)

Yet Bitcoin receives more criticism than other new forms of payment. Various proposals have been made since the Great Depression aiming to disintermediate money from the banks and Hayek, in the 1970s, put forward other ideas to separate the state from money (Dodd, 2017: 38). But Bitcoin does both; banks are not needed to process the transactions, and the state cannot exercise monetary policy over Bitcoin as it is written in code. Both objections lie in overt concerns that have been present in society for some time. The state has a proven history of being incapable of managing monetary supply, as we have shown, and, in recent years, of being increasingly invasive (Butler, 2019: 332, 336), especially since 9/11 (Amoore and De Goede, 2005). Meanwhile, the banks had a significant role to play in the financial crisis of 2008, which is referenced in the Bitcoin genesis block, and they have been seen by many as corrupt, profligate and greedy, resulting in a loss of trust (Palframan, 2018).

Money and Trust

A Bank of England bulletin notes that ‘money is a social institution that provides a solution to the problem of a lack of trust… money in the modern economy is an IOU that everyone in the economy trusts’ (Mcleay et al., 2014). But this trust has been broken and many no longer trust state money. Simmel is again useful here. Moving from private, commodity-based exchange between two individuals to abstract exchange between larger groups requires the creation of ‘higher supra-individual formations’ (Simmel, 2004: 173). Broader exchange ‘depends upon the economic community or upon the government as its representative’ (p. 176). The community becomes a third party to the exchange. ‘Money transactions would collapse without trust’ and so an economic community needs ‘an element of social-psychological quasi-religious faith’ (p. 178). That Bitcoiners are fervent in their beliefs is a strength for their community, not a weakness, and testament to their corresponding lack of faith in fiat. For all monies, there needs to be belief within an economic circle that the money will be accepted, and for no form is there a 100 per cent guarantee that a money can always be used (p. 179). ‘The guarantee of the general usefulness of money’ and its issuance is undertaken by a ‘representative of the community’ (pp. 179–80), ‘an objective institution’ (p. 182). And at scale, money becomes a ‘public institution’ (p. 184).

In the political dimension, the critical question is not only ‘who’ can this institution be but now also ‘what’? Must it be the state, or can other higher supra-individual formations fulfil this role? Simmel is clear that these ‘formations exist in great variety’ (p. 173). In ancient Greek culture, the relationship between money and the central institution was religious, not political. The institution, therefore, does not have to be the state. Indeed, a Hegelian conception of the nation-state is only 200 years old (Chernilo, 2007: 40). Hayes argues that blockchains ‘are the very institutions they succeed’ (2019: 18); to this we add that Bitcoin is a public institution in the Simmelian sense. Furthermore, Bitcoin is prima facie evidence that other types of higher supra-individual formation can fulfil this role in society, and in money. It is for those in the economic community of Bitcoin to believe in it as money, to have faith in it, and Bitcoin is the third party that provides the degree of guarantee. It is not only the state that can give confidence in money. We tend to over-complicate money and can easily be lost in its philosophy. Money is simply whatever a group of people agree and trust to use as a means of payment (Lietaer, 2001: 41; Bjerg, 2016: 61).

An important theme of The Philosophy of Money is the development of money in parallel to the development of society. As our intellectual ability advanced, money moved from commodity to abstraction. And society evolved from private transactions to ever-widening economic circles. This progress was also marked with a trend towards centralisation, which Simmel saw as mankind’s concentration of energies, forces and unity in order to achieve more with less effort – some examples being machinery, gunpowder, and family (Simmel, 2004: 196–8). The modern state represents an ‘unrivalled concentration of forces’, and money, as it develops, increasingly expresses values in the ‘most concise and condensed way’ (p. 197). Yet, our current financial systems and monies were shaped by an industrial-age world where ‘nationalism, competition, endless growth and colonization were encouraged’ (Lietaer, 2001: x). A national currency was a powerful tool for national consciousness (p. 45), but the creation of hundreds of currencies along nationalistic lines, with its inconveniences, instability and speculation, cannot be a final realisation of the centralisation of money. For Simmel, in an ideal social order money would have no intrinsic value and would be purely symbolic (2004: 191). It would also be centralised in the sense of maximising its force and unity. But our current systems are based on crumbling ‘hierarchies of power based on control’ and ‘hierarchies of politics based on geography’ (Lietaer, 2001: 61). In a global, digital age, our world is deserving of a more fitting money, one that reflects a society that evolves beyond borders, and perhaps one that does not depend upon nation-state law and even violence for its protectionism.

With this in mind, we reimagine the commonly held view that ‘Bitcoin does not rely on trust in a central authority’ and that it ‘is radically different from fiat money issued by a state’ (Bjerg, 2016: 61). Bitcoin is a central authority, a public institution, in the same way that the state performs that role in money. And it is centralising ‘great forces at a single point’ (albeit through a decentralised computing system), combining the energies of hundreds of currencies limited by borders (Simmel, 2004: 196). Bitcoin represents an evolution of higher supra-individual formations and an evolution in money paralleled by a developing global society.

Bitcoin as a Social Movement

Bitcoin is used by a variety of groups, be it criminals, speculators, libertarians, hard-money Bitcoin vigilantes or even just those that find it useful. However, it ‘is arguably a social movement as much as it is a currency’ (Dodd, 2017: 40), based upon the properties of Bitcoin and primarily concerning the disintermediation of the state and the banks. In this way, Bitcoin challenges the ‘memorable alliance’ of the state, the central banks and the private financial institutions that form the basis of our modern capitalist system (Ingham, 2020: 65). This is where the tension lies.

Bitcoin directly challenges the soft money of the state, which puts it in conflict with those that benefit from the power that control of money brings. In this way, we see further evidence that money is more than a means of exchange. It is a ‘source of power – infrastructural and despotic’ that comes from having more money than others but, more importantly, from the ability to create it (Ingham, 2020: 13). Bitcoin does not stop the state accumulating money and power through taxation (leaving aside any collection problems related to self-sovereignty of assets). Specifically, Bitcoin threatens only the state’s ability to wield power by creating money. The implications of this require further study, but the prospect is feared nonetheless: An awful lot of our international power comes from the fact that the U.S. dollar is the standard unit of international finance … It is the announced purpose of the supporters of cryptocurrency to take that power away from us. (US Congressman Brad Sherman, as quoted in Bambrough, 2019)

These are the questions we must concern ourselves with. The state has failed at the second and third elements of our question of money. We do not argue here that Bitcoin can or will replace state money but analyse it to reveal the truth – that the issue of supply is central and remains powerful enough after many centuries to evoke resistance. Supply is the fundamental theoretical issue of our time. Can the state retain power in creating money, as a ‘force for good’? Or is the ‘only way’ to have something that is beyond its power to abuse and misuse?

Conclusion

Centuries of great minds have shown that there is a problem with the state in money; namely that power to create it invariably ends in ruin. There has been a fundamental misinterpretation of several key monetary thinkers in justification or support of government spending without specific plans for the repayment of that debt. The explosion of government-issued money devalues all money, making us all poorer. Schrödinger’s debt is real, and the price is paid by all in society through rising prices and inequality. Bitcoin has emerged as a possible solution to these problems but has often been criticised and dismissed. Using Ingham’s ‘money question’ and Simmel’s The Philosophy of Money as a core text, we have shown that Bitcoin, as well as fiat, are good forms of money that are closer to Simmel’s vision of a ‘final outcome’ than gold. We hope this settles the debate ‘about the nature of money and the relation between money and commodities’ (Bjerg, 2016: 58). We agree with Ingham, that the fundamental clash over commodity versus claim theory should be ‘laid to rest’. Debate must move past these old divisions, as money does not need to be a commodity.

Instead, we must focus on the political dimension of money. Here, the control of supply, and the power that comes from it, is the real source of tension. It is supply that led to metallism, as we turned to gold to temper man’s nature for debasement in an attempt to address the ‘alchemy’ of the state problem in money. Commodity versus claim theory is not about a physical ‘commodityness’. It is about the issue of supply, which transcends the political dimension.

The state has failed throughout history in the management of money, and we may be better off without it monopolising that position. Modern money is founded on outdated industrial age thinking, nationalism, and crumbling hierarchies of power. Trust in it has been broken. Bitcoin has emerged as social resistance and as a new type of higher supra-individual formation, where it is a community institution alongside the state – money as a public institution. And Bitcoin has expanded economic circles beyond the physical, geographic borders of state currency and proven that money does not depend on the state for guarantee. It is for an economic community to believe in a money, and the wider a money is used the better it needs to be. Bitcoin may be very different to state money technically and politically, but it is very similar philosophically. Bitcoin is a centralised institution for money, a machine for the concentration of the forces of value.

For Simmel, the future of money trends towards institutional centralisation and to abstract money, with widening economic circles, and is paralleled by an intellectual advancement of society. Society, at its fullest potential, with increased social and economic differentiation, may find that Bitcoin, or others like it, could be desecuritised as part of the solution to money and its volatility, rather than framing it as only a problem. And a society tending towards individuation and individualisation might lead to such social conditions that the future of money will not be Orwellian, based on the industrial age thinking of hundreds of state monies, enforced by law, threat, coercion and violence. In the information age of the future, economic relations will be Simmelian, based on freedom, choice, and voluntary adoption. ‘Good money does not have so many side-effects as does base money, and… its use need not be so strictly regulated or supervised’ (Simmel, 2004: 194). An ideal society is worthy of ideal money. And the future does matter.

Footnotes

Acknowledgements

Simon Butler was supported as part of the EPSRC Centre for Doctoral Training in Cyber Security at Royal Holloway, University of London (EP/K035584/1).