Abstract

This article highlights emerging patterns of domestic remittance arrangements among migrant construction workers from West Bengal in Kerala that have now become defunct because of COVID-19. Earlier field surveys and in-depth interviews showed how Bengali migrant construction workers, relying on networks of friendship and trust, were learning to remit through formal channels, in contrast with many micro-studies showing the dominant role of informal channels in domestic remittances. High wage rates in Kerala enabled such migrant construction workers to send significant amounts, used for productive activities besides household expenses. However, there were significant changes in arrangements, before COVID-19 enforced a dramatic suspension of remittances, raising important questions about future possibilities.

Introduction

According to Deshingkar (2006), in a large country like India, with considerable regional disparities, internal migration may be even more important than international worker migration, certainly in terms of the numbers of people involved, possibly even regarding remittance volumes. There is a dearth of official data about domestic remittances in India, while realisation of the importance and scale of these remittances transpires through micro-level studies. These refer to socio-economic variables and particular forms of migration, often omitted from national surveys, thereby adding important insights regarding the dimensions and patterns of domestic migration and remittances (Thorat & Jones, 2013). Studying Oriya migrant workers in Gujarat, Ghate (2005: 1740) observes that ‘in order to minimise search costs, areas sending out migrants tend to specialise in particular destinations’. Such micro-level studies also highlight the importance of various remittance arrangements through informal channels. Sending money through friends, relatives and co-workers visiting the home, or carrying it personally when going home, are prominent informal channels (Sahu & Das, 2008). Some studies have shown that since formal channels such as banks and post offices remain inaccessible in many localities for a variety of economic, institutional and social reasons, most internal migrants depend on informal money transfer practices and systems (Ramamurthy, 2010; Sahu & Das, 2008). To what extent this is the case for all types of internal migration in India is simply not known, but there are also efforts, in some cases, to provide remittance services (Ghate, 2005).

The purpose of sending remittances and their uses constitute another important aspect of migration studies. Several studies (Banerjee, 1986; Parida & Madheswaran, 2011) report that the major end use of remittances is household consumption. A study of 12 villages in Jharkhand (Dayal & Karan, 2003) found that migrant households consume better diets and spend on average 15 per cent more on food than non-migrating households. Remittances are also used for a variety of productive purposes. Sundari (2005) studied 955 migrant households in Tamil Nadu. She found that while many migrant households lost assets due to the process of migration, 57 per cent of lower income migrant families had seen their household income increase and, more importantly, 53 per cent had increased their asset holdings. This happened particularly in migrant households of the upper income group (Sundari, 2005: 2302). In many cases, migration is linked to debt cycles, and remittances are used for repaying debts. According to national sample data for 2007–2008 (NSSO, 2010), about 10 per cent of rural Indian households reported that remittances are used to repay debt. Remittances also cover deficits created by losses in agriculture, or meet expenditures of large magnitude for marriages, festivals and ceremonies (Bird & Deshingkar, 2009). Thus, in South Asia, it is imperative to study the usage of remittances in migrants’ households of origin to assess the impacts that migration has on development in rural communities (Ranathunga, 2018).

Linked to Reja and Das (2019), this article focuses on various aspects of remittance arrangements among construction labour migrants from West Bengal in Kerala, a recently developed migration stream, spanning a huge distance. Given the vast linguistic and cultural differences involved between the origin and destination states, Kumar (2011) portrayed this migration stream as similar to international migration, but they remain of course migrant workers within India. The present article first provides a brief overview of internal migration and remittance sizes in India and then discusses the database and methodology used for this study. The article’s main focus concerns the remittance behaviour and arrangements of Bengali migrants, particularly the type of channels they used to send remittances and the specific purposes for which remittances are used. Towards the end, a brief update regarding the impacts of COVID-19 on this scenario is provided, as the remittance flows are presently suspended, raising questions about future possibilities to resume such arrangements.

Internal Migration and Remittances in India

India’s latest government data on migration (Census of India, 2011) show that the hugely important phenomenon of migration increased, since 2001, by nearly 7 percentage points. The percentage of people who were classified as migrants is 37.64 per cent of the population or 455 million, compared with 30 per cent or 307 million people of the total population of 1,028 million people in India in the 2001 Census. Of this total, nearly 68 per cent constitute female migration, with most of these women moving for marriage purposes (Census of India, 2011). Similar figures are reported by Sundari (2005: 2295). Nearly 24 per cent of male migrants moved for work or employment, both within and beyond state boundaries.

Given the focus of the present article, it is pertinent to mention that nearly 12 per cent of migrants in the 2011 census were interstate migrants, about 54 million people. Out of these, 23 million were male migrants, and nearly 50 per cent had moved for work/employment. Kerala witnessed a huge influx of labour migrants from far eastern and north-eastern states such as West Bengal, Odisha, Bihar, Uttar Pradesh, Assam and, recently, Manipur (Kumar, 2011). According to the report of the Gulati Institute of Finance and Taxation by Narayana et al. (2013), Kerala has a migrant labour population of 2.5 million, projected to rise to 4.8 million in the next 10 years. West Bengal holds the largest share, with about 20 per cent of this total migrant labour force.

India was the top remittance-receiving country in the world in 2018 at US$78.6 billion, gaining 2.9 per cent of its gross domestic product (GDP) from remittances (World Bank, 2019). Kerala is the state of India receiving the highest international remittances. Several studies (Azeez & Begum, 2009; Prakash, 1998; Zachariah et al., 2001) have assessed the volume, nature and impacts of overseas remittances on Kerala’s economic and social structure, while very few studies exist regarding domestic remittances in India. Compared to international remittances, it is very difficult to estimate the size of domestic remittances because internal remittances are mostly sent informally either by hand-carrying, or through trusted friends and relatives, making it difficult to capture such remittances in official data. According to Tumbe (2011), the estimated internal remittances in India were worth US$10 billion in 2007–2008. Internal remittances are particularly important for poverty reduction, since internal migration between regions, states or districts and between rural and urban areas, is more likely to involve poorer people (Deshingkar, 2006).

Database and Methodology

The present study is based on a field survey carried out during April–July 2013 in the district of Ernakulam in Kerala and described by Reja and Das (2019: 127–8). The survey sample included 300 migrant construction workers from West Bengal who had been working in Kerala for at least 6 months. Snowball sampling technique was applied, and data were collected through a structured, pre-coded schedule. In-depth interviews of 30 migrants provided more detailed insights. The parts of the interviews relevant for this article focussed on arrangements, channels and volumes of remittances and their use by household members. In addition, to assess more recent modes of transfer of remittances, telephone interviews, which are becoming an increasingly popular data collection method (Block & Erskine, 2012), were conducted. A total of 50 migrants from the informant pool of 300 men were interviewed by telephone during August 2020 to also capture the effects of COVID-19. Multiple response techniques were applied to analyse the purposes of remittance use, since the sampled migrants often cited more than one purpose.

Migrant Workers’ Labour Activities and Wages

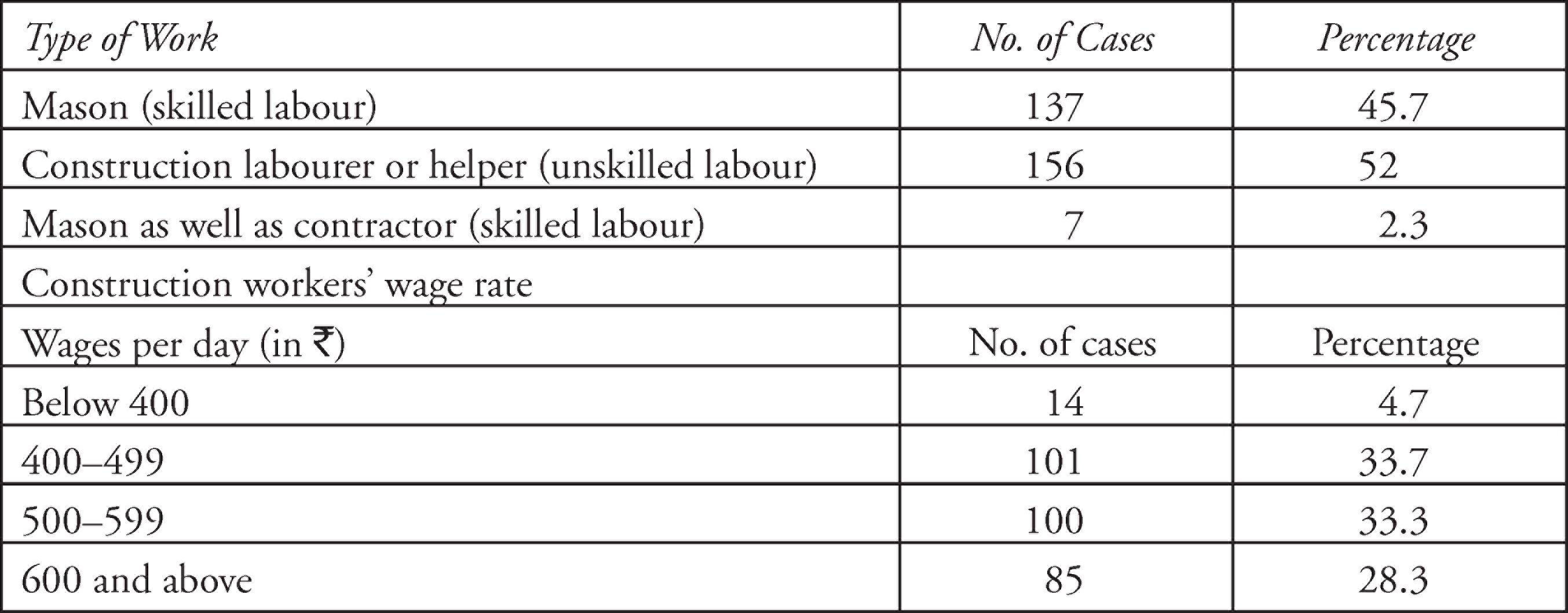

Before going into details about the remittance arrangements of Bengali labour migrants in Kerala, it is pertinent to highlight some aspects of the migrants’ labour activities and wages as the main source of remittances. As Table 1 shows, the study identified that 52 per cent were unskilled labourers, while the rest were considered skilled workers such as masons, and there were seven masons-cum-contractors (2.3%).

The Bengali migrant construction workers in Kerala were far better off, wage-wise, than at their native place or last working place anywhere in India (Reja & Das, 2019: 134). Table 1 confirms that more than two-thirds of the sampled migrants reported daily wages between ₹400 and ₹600, and more than one-fourth of migrants reported earning more than ₹600 per day. The average daily income of these migrant construction workers was ₹516.32, two to three times higher than the average daily income they would get in their home state. This is also the highest daily wage rate compared to other states of India (Zachariah & Rajan, 2012).

Type of Work and Wage Rate of Bengali Migrant Workers

Remittance Size, Frequency, Channels and Cost of Sending Remittances

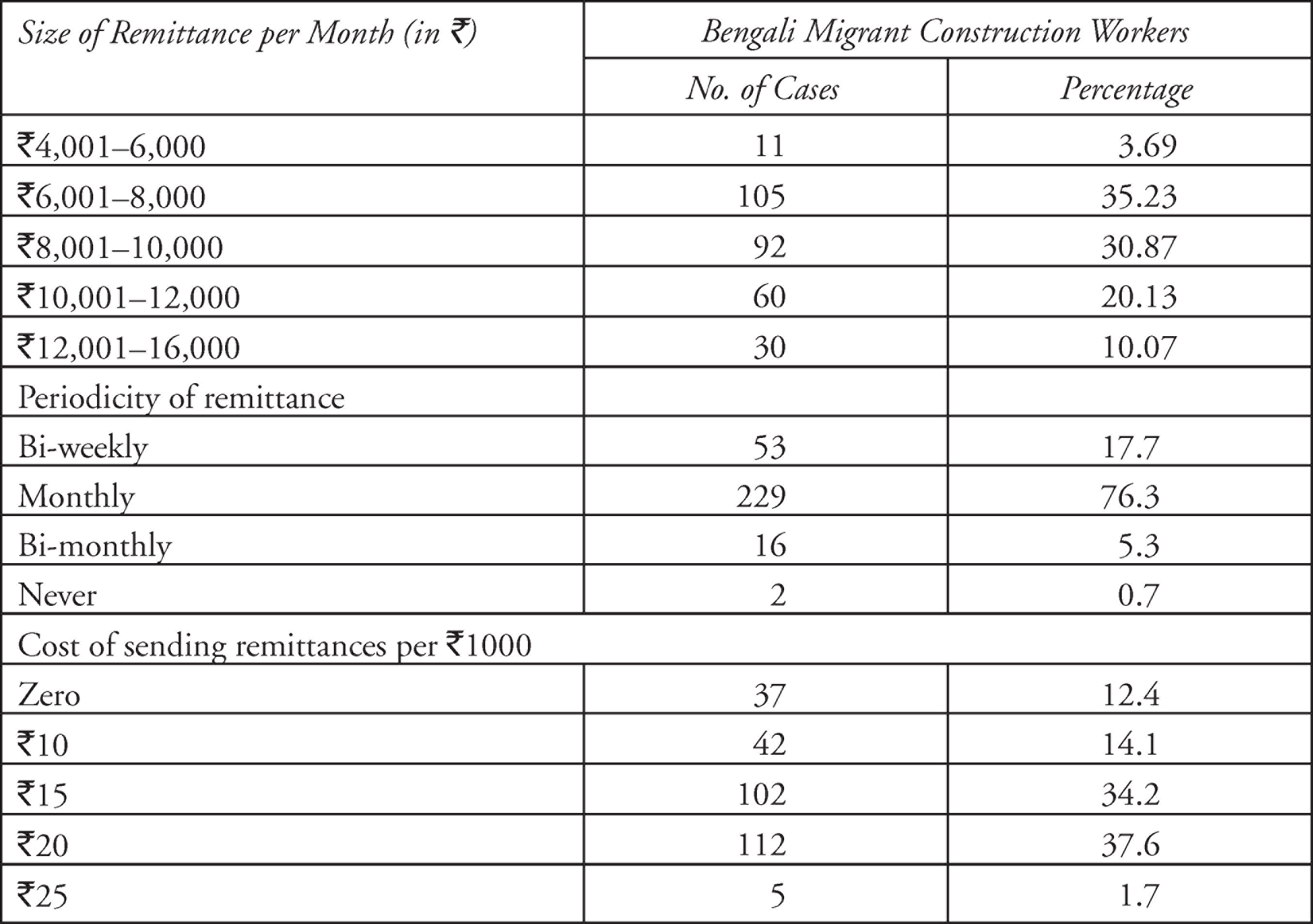

These high wage rates enabled Bengali migrant construction workers to remit significant amounts. The remittance sizes are detailed in the first part of Table 2. The remittance size per month varied between ₹4,000 and ₹16,000, the average amount sent being nearly ₹9,500. About two-thirds of migrants remitted a monthly amount of ₹6,001–10,000. Nearly one-third sent over ₹10,000 per month, a very large amount in the context of internal labour migration.

Table 2 also shows that barring two individuals, all Bengali worker migrants would usually send remittances home on a regular basis. More than 75 per cent of migrants tended to remit monthly, while a little over 15 per cent sent money every 2 weeks. Regarding the recipients of remittances, the study found that the remittance was sent to one particular reference person. In about 56 per cent of cases, the recipients were the parents, in 42 per cent the wife, the rest were elder brothers.

Distribution of Bengali Workers by Size, Periodicity and Cost of Remittances

The transfer of money back home is always a great cause of concern for migrants. Studying the remittance sending mechanisms of Oriya migrants, Sahu and Das (2008) observed that sending money safely with minimum costs and within the shortest possible time caused major anxiety for migrant workers. Remittance needs have traditionally been thought to be met well by money orders from post offices, demand drafts by banks and through informal sources, including physical carrying of cash by the workers themselves, or their relatives and friends (Ghate, 2005: 1741). The medium of sending remittances used to be different for international and internal migration. Innovations in electronic transfer of money, such as green channel and ATM card-to-card transfers, may encourage migrants to use this transfer mechanism rather than older formal channels like money orders or bank drafts. Such easy and speedy transfer of money mechanisms may also reduce the use of informal channels of remittances.

Asking the Bengali migrant construction workers whether they were heavily dependent on informal money transfer systems, or to what extent they used formal channels for sending remittances, was the most relevant question for the present article. In 2013, the entire sample of Bengali migrant construction workers sent remittances through banks, and hence, used formal channels for money transfer. This was somewhat in contrast with other micro studies (Jain, 2010; Sahu & Das, 2008; Thorat & Jones, 2013), which showed that informal channels are dominant among internal migrants. Researching this further, we found some interesting arrangements. Firstly, the main reason behind this use of bank transfers was the long distance between Kerala and West Bengal acting as a barrier for sending remittances through informal channels such as home visits by friends, relatives and co-workers, or carrying money personally when going home. Secondly, Kerala is well connected with bank branches, and thirdly, modern innovative mechanisms of easy and speedy electronic transfer of money are considered as safe and attractive.

However, in 2013, most of these migrants did not yet have a bank account of their own and sent money using another person’s bank account. This arrangement meant most migrants would have to pay a certain extra charge for using a trusted person’s bank account. Table 2 shows the distribution pattern of these charges, added to the actual remittance amounts. About 70 per cent of migrants gave remittance charges of about ₹15–20 per ₹1,000, while about 15 per cent paid an extra ₹10 per ₹1,000. The reason why these remittance charges were different is intriguing and was an altogether different story.

The persons involved in this money transfer are other migrant construction workers. These people were obviously trusted to take responsibility for transferring the money at a minimum charge for people of their own home locality. Notably, the charges were higher when the distance between the account holder’s house and the migrants’ house where the money had to be disbursed was greater. Migrants with an account who are involved in this business of money transfer of fellow migrants usually accept responsibility if the fellow migrant’s house at their place of origin is about 15–20 kms, and a maximum of 35 kms away. The manner in which the remittance reaches the migrant’s home is yet another story. In most cases, the migrants who send the remittances have a bank account in the name of a family member, often the migrant labourer’s wife. When money is deposited in this account, the household members are informed via telephone that the remittance money has been sent. Then one of the household members, mainly the father or the wife, would withdraw the money from the bank and bring it home. If the unbanked migrant’s house is near to the account holder’s house, then a family member might collect the remittance from the account-holding migrant worker’s family as cash. If the fellow migrant’s house is far away, then a family member of the account holder would take responsibility for delivering the remittances to the fellow migrant’s house. In such cases, the remittance charges levied by the account holder become higher.

We also found other means of transferring money to the doorsteps of the migrants’ households. As most migrants belong to the same locality, sometimes, someone from the locality acts as a sub-agent and takes responsibility for sending the money to specific migrants’ households. Being a local resident, this person is well acquainted with the people who migrated to Kerala. In this case, the most influential migrants, either a contractor or mason from a particular locality in West Bengal, collects money from migrants of their locality and takes a third of the extra charge, while the account holder and sub-agent at the place of origin will take two-thirds of the remittance charges. These complex arrangements mean that although all remittances are formally channelled through bank accounts, the processes in which the actual remittance payment to the migrant’s family is arranged and disbursed by various agents incorporate a large amount of informality.

At the place of work in Kerala, among migrants who used to send money through this transfer process, this was popularly known as TT channels, the name deriving from transfers of taka, the Bengali word for rupees. Migrants involved in this TT process usually came to fellow migrants’ rooms in the evenings after the day’s work and enquired who would like to send money home. They then collected cash from fellow migrants and deposited this into their own account on the next day and subsequently disbursed this money to the fellow migrants’ house through family members or agents. All men reported that the banking facilities in Kerala are very good, and they hardly face any problems in this transaction of money. Most migrants indicated that they use public sector banks for money transactions. Therefore, in 2013, it was found that this formal-cum-informal transfer of money to the home state depended crucially on trust, social networks and personal relationships.

However, during the more recent telephone interviews, it transpired that the mechanisms of sending remittances had subsequently changed in line with technological advancement. The Bengali migrants now reported using various mobile apps, such as Paytm, PhonePe and Google Pay, for sending remittances. Besides, the Pradhan Mantri Jan Dhan Yojana (PMJDY), a financial inclusion programme, appears to have had much impact for remittance-receiving households. The PMJDY programme, launched by the Government of India in 2014 to ensure access to financial services, involved creation of basic savings and deposit accounts, facilitating remittances, credit, insurance and pension in an affordable manner. This has brought millions of Indians into the banking sector. It was found through telephone interviews that by 2020, almost every migrant household had a bank account under PMJDY, which certainly reduced the informal arrangements that existed earlier at the receiving end of the remittance-sending process.

Use of Remittances

In most micro-studies, the uses of remittances are based on household surveys, but the present study collected the data on the uses of remittances from the individual migrants at their place of work. The survey interviews found that in many cases, the migrant is the only earner and also the head of the family. Hence, his opinion about the uses of remittances is most important. In that sense, the collected data are reliable and would tend to show a true picture about how the remittances are used.

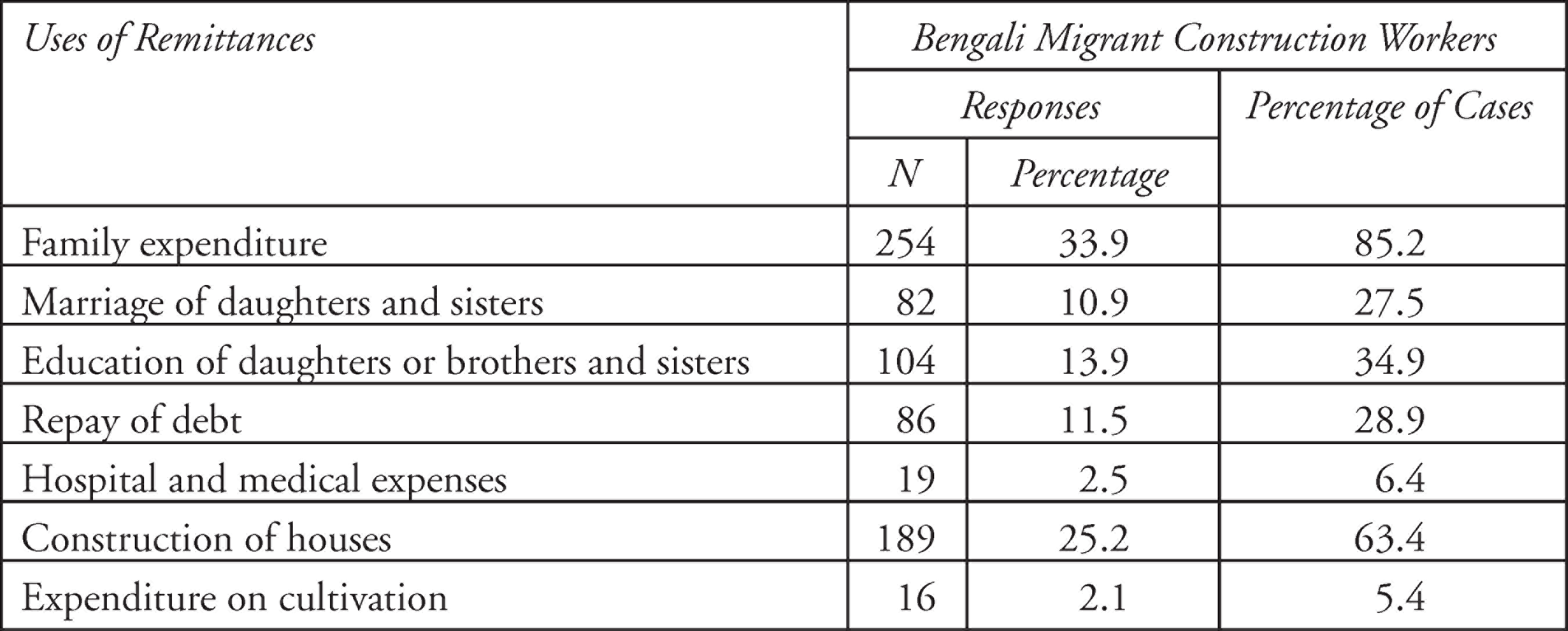

From the multiple responses, as shown in Table 3, it can be observed that about 85 per cent of the Bengali migrants reported to use remittances for family expenditure, 33.9 per cent of all responses, the most popular one. This result is in accordance with many migration micro-studies. In his study on Delhi migrants, Banerjee (1986) showed that about 93 per cent of the remitters sent money for household expenses. Using the NSS0 (2010) data, which are for 2007–2008, Parida and Madheswaran (2011) have shown that household consumer expenditure constituted the prime use of remittances in both rural and urban areas, with nearly 95 per cent of households in rural areas and 93 per cent in urban areas reporting this use of remittances. The next important use of remittances reported by the Bengali migrant construction workers was the construction of their own houses. After meeting the basic family expenditure, they aspired to construct their own solidly built (pucca) residence at their birthplace. Much empirical evidence confirms that remittances are used mostly for basic subsistence needs, and after those needs are met, money is spent on housing improvements and eventually on land purchase (Stahl & Arnold, 1986). Many migration studies (Azeez & Begum, 2009; Zachariah et al., 2001) have shown the particular impact of Gulf remittances on the housing sector in Kerala. In the present study, we believe that being construction workers themselves, since about 70 per cent of migrants are engaged in building houses and complexes, Bengali migrant construction workers have an inner desire to build a pucca house in their native place, and their fairly high incomes in Kerala certainly met and nurtured their wishes in this regard.

As Table 3 further shows, Bengali migrants also mentioned the use of remittances to repay debts. Nearly 29 per cent of migrants reported that their remittance was used to repay debts, which was 11.5 per cent of all responses. The use of remittances for the purpose of marriage of daughters/sisters was also indicated as particularly important. Nearly 28 per cent of migrants reported their remittance being used for the marriage of daughters/sisters, which was 10.9 per cent of total responses, the fifth highest response. Besides, a meagre percentage of migrants reported use of remittances for hospitalisation and medical expenses. A small proportion of the remittances was also used for improving agricultural production or was invested for better agricultural practices.

Distribution of Bengali Workers by Use of Remittances

Conclusions and COVID-19 Update

The present study confirms that in 2013, a sizeable amount of remittances was involved in this particular inter-state migration, transferred through banks to the migrants’ origin state, which at first sight is considered to be a formal mode of sending remittances. However, as this article shows, since, in 2013, most migrants did not have bank accounts of their own and had to rely on trusted fellow migrants or agents for transfer of money, there was an urgent need of financial inclusion strategies to cater to the needs of these domestic migrants, given also that domestic remittances offer a big opportunity of business growth for financial institutions in India. Notably, by 2020, financial inclusion programmes like PMJDY had brought many migrants into the banking system, with significant impacts on remittance arrangements for the receiving households. From the pattern of use of remittances, the study found that although remittances were used predominantly for family expenses, impacts on productive activities could also be observed, as a sizeable portion of the money was used for construction of houses, for educating children or siblings and also for marriage arrangements for sisters or daughters.

However, during 2020, the impact of Covid-19 on the migrants examined here and their remittances has been disastrous, and some brief comments are pertinent. There was a pan-Indian complete lockdown for 21 days in Phase I from 25 March to 14 April 2020, and for another 19 days in Phase II from 15 April to 3 May 2020, as a control measure to curb the spread of coronavirus. Then, in two later phases of lockdown of altogether 4 weeks (Phase III from 4 to 17 May and phase IV from 18 to 31 May) some limited activities were allowed in areas where COVID cases were less in number. During this whole lockdown period, labour migrants in general, and interstate migrants in particular, were hit very hard and faced multiple hardships (Ullah et al., 2020). The World Bank (2020) reports how lockdowns, loss of employment and social distancing prompted a chaotic and painful process of mass return for internal migrants from mainly urban areas to their native villages in India.

The Bengali migrant construction workers in Kerala also suffered a lot during these lockdown periods. Despite various efforts by the Kerala government to restrict chaotic return migrations of migrant labourers, by providing food, shelter and other necessaries, distress levels among migrant workers escalated. News of return of Bengali migrant workers from Kerala surfaced in various newspapers during this period. Abraham (2020) reports how Kerala buses made enormous profits by taking Bengali workers home, as the ‘special trains’ arranged by the Indian Railways were not enough to accommodate those who wanted to leave Kerala.

During our telephone interviews in August 2020, some of these migrants recounted a number of factors forcing them to return to their native villages. Firstly, loss of work was the main reason behind their return from Kerala. Secondly, they were suffering high degrees of anxiety and fears regarding the COVID-19 pandemic. Thirdly, many migrants expressed their loneliness in this difficult time, which made them desperate to unite with their families. Fourthly, the fear of death from this infection without seeing their family members loomed large among migrants. In the telephone interviews, many men said that some money was sent from their home to meet their travel expenses and other costs, and some migrants’ families even borrowed money from relatives and neighbours.

The size of domestic remittances of course recorded a massive dip during this lockdown period. According to Shukla and Manikandan (2020), the remittances from within India, pegged at around ₹2 trillion annually, plunged about 80 per cent in the lockdown period. Bengali migrant workers who remained stuck in Kerala during the lockdown reported that now there was nothing left to send home as remittances, as they lost their daily work and livelihoods.

This terrible scenario raised important questions about the future. As Reja and Das (2019) found, and this article confirms, the strong social networks and friendships that facilitated the worker migration from West Bengal to Kerala are still intact and may be reactivated as soon as some kind of normalcy returns. The construction workers will have gained important skills and experience through their work in Kerala, and may seek to resume their earlier positions, as there will be a continuing need for construction workers. Unless Keralites themselves pick up those blue-collar jobs, there will be a continuing need in Kerala for migrant workers from other states. The changing patterns of remittance arrangements identified in this article may then be resumed, now more fully formal than in 2013. However, at the time of writing this article, there are simply no more remittances from these migrant construction workers, and future research may seek to examine the various fallouts of the pandemic in rural West Bengal itself.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.