Abstract

This study investigates the impact of CEO narcissistic traits on risk disclosure within Iran's corporate governance framework, analyzing 1,480 firm-year observations from Tehran Stock Exchange-listed companies (2013–2022). We measure CEO narcissism by the size of signatures on annual reports and assess risk disclosures using a specialized bag-of-words model for Persian Management Discussion and Analysis (MD&A) documents. Our results reveal a significant positive relationship between CEO narcissism and the extent of risk disclosures, supporting theories of Self-Promotion and Visibility Enhancement. These findings are validated through sensitivity analyses that adjust for variations in narcissism measurements across different time periods and CEO tenures, alongside recalculating model standard errors with various clustering methods. Further tests across business, operational, and financial risk dimensions consistently show the positive impact of CEO traits on corporate risk communication. We employ firm fixed effects, apply entropy balancing, and focus on periods of CEO transitions to address potential biases and endogeneity concerns. Additionally, our analysis explores the moderating role of board composition, which significantly interacts with CEO narcissism to affect disclosure practices. The post-2015 regulatory environment is also analyzed as a moderator, highlighting that regulatory changes amplify the influence of narcissistic traits on disclosures. Employing established methodologies corroborates these findings, further demonstrating the profound effect of CEO traits on corporate risk communication in a non-Western context. This research enhances understanding of how leadership traits influence corporate transparency and risk disclosure.

Keywords

Introduction

This study aims to explore the link between CEO narcissistic traits and risk disclosure practices amid the complexities of Iran's changing corporate and regulatory environments. The increasing demands for transparency and accountability in financial reporting highlight the need to understand executive behaviors, especially CEO narcissism, and their effects on corporate disclosures (Lander & Auger, 2008). As financial markets face growing uncertainties in the political, social, and economic arenas (Badia et al., 2020; Bochkay and Joos, 2021), examining the influence of executive traits on firm practices has become essential.

CEO narcissism is characterized by grandiosity, self-focus, and a constant need for admiration and approval (Cragun et al., 2020). These traits significantly affect a firm's disclosure practices, as narcissistic CEOs tend to present firm disclosures that boost their self-image (Marquez-Illescas et al., 2019; Zhang et al., 2017). They often provide overly optimistic earnings forecasts and may omit expenses from non-GAAP earnings, leading to potentially lower-quality disclosures (Abdel-Meguid et al., 2021). The decision-making of these CEOs is also heavily influenced by their experiences on other boards, leading them to adopt strategies that significantly differ from their peers. This often results in bold, attention-grabbing corporate actions that can cause significant performance variations (Chatterjee & Hambrick, 2007; Zhu & Chen, 2015).

Such behaviors highlight the significant role of narcissistic leadership in potentially reducing board influence (Ahn et al., 2020), skewing strategic decisions (Zhu & Chen, 2015), and presenting stakeholders with biased financial disclosures (Buchholz et al., 2020). Additionally, the communication of risk information is particularly impacted, offering vital insights into the current and potential risks facing organizations, affecting their sustainability and stakeholder trust (Elamer et al., 2019; Elamer et al., 2020). Advancements in risk disclosure theory highlight the significance of understanding a firm's risk exposures for efficient capital allocation. Heinle and Smith (2017) elucidate that risk disclosure can lower the cost of capital by reducing the variance uncertainty premium, a benefit that becomes more pronounced under conditions of high initial uncertainty about a firm's cash flow variance—conditions common in dynamic and volatile markets like Iran. Their model further demonstrates that precise and credible risk disclosures can profoundly influence investor perceptions by narrowing the perceived distribution of future cash flow variances, thereby potentially enhancing the overall market valuation of the firm.

Extensive risk disclosure by narcissistic CEOs can serve dual purposes, each reflecting distinct underlying motivations and strategic goals (Chatterjee & Hambrick, 2007; 2011). On one hand, increased disclosure may signal a commitment to transparency and regulatory compliance (Peters & Romi, 2014; Stapleton & Hargie, 2011), portraying the CEO as a responsible leader who prioritizes shareholder interests and aligns with international standards for corporate governance (Blankespoor & deHaan, 2020). This commitment supports the notion that transparency enhances market confidence and reduces informational asymmetries between management and investors, thereby potentially lowering the cost of capital (Heinle & Smith, 2017). Dabbebi et al. (2022) suggest that narcissistic CEOs often disclose more about social and governance activities, which could be interpreted as an effort to project transparency.

On the other hand, by disclosing a broad array of risks, narcissistic CEOs may also seek to demonstrate their competency in identifying and managing complex challenges, thereby reinforcing their personal image of capability and control (O’Reilly & Chatman, 2020; Zhang et al., 2017). By projecting their foresight and managerial prowess, narcissistic CEOs aim to solidify their reputation and authority within the corporate and investor communities (Chatterjee & Pollock, 2017). While these disclosures might appear transparent, they could be strategically crafted to impress stakeholders with the CEO's assertiveness and proactive management style, rather than to genuinely inform them of potential risks. Moreover, research indicates that the penchant of narcissistic CEOs for risk-taking, particularly when they serve as board chairs, leads to increased corporate risk-taking, which is often viewed negatively by debt markets, resulting in higher bond yields and borrowing costs (Kim & Anderson, 2024; Tuggle et al., 2024). Marquez-Illescas et al. (2019) and Chatterjee and Hambrick (2011) also note that these CEOs are influenced by social praise and may use positive earnings announcements to bolster their grandiose self-image, further complicating the interpretation of their motivations behind risk disclosures.

The coexistence of these motivations—desire for transparency and demonstration of competency—introduces complexity into the interpretation of risk disclosures. Stakeholders face the challenge of discerning whether these disclosures are primarily aimed at enhancing organizational transparency and trust, or if they serve as a strategic tool for the CEO to manage personal image and exert influence over stakeholders. Despite extensive studies on CEO behaviors, a significant gap remains in fully understanding how narcissistic traits specifically influence actions related to risk disclosure. The literature underscores the critical role of effective risk disclosure in enhancing transparency and reducing information asymmetries between corporate management and stakeholders. However, ongoing debates continue regarding its regulation and effectiveness (Adam-Müller & Erkens, 2020; Deumes & Knechel, 2008). Further research is needed to detail the mechanisms through which narcissistic CEOs may manipulate risk disclosures to align with their personal image and strategic goals, directly impacting corporate governance and external perceptions.

Iran's unique corporate governance environment—marked by state influence, recent regulatory reforms, and cultural specifics—provides a valuable context for examining how CEO narcissism affects risk disclosures. State ownership and politically driven CEO appointments often amplify the potential for narcissistic leaders to shape disclosure practices to serve personal or organizational agendas (Mohammadrezaei et al., 2013; Tajeddini & Trueman, 2016). Furthermore, stringent regulatory requirements for detailed risk disclosures, especially in critical sectors like banking and oil, present both opportunities and challenges for narcissistic CEOs to project an image of control and competence while navigating the country's volatile economic and political environment (Kashani & Shiri, 2022; Salehabadi, 2013). These dynamics are further influenced by cultural norms such as high power distance and uncertainty aversion, which shape how narcissistic tendencies manifest in governance and disclosure strategies. Coupled with economic sanctions and political instability, these factors significantly affect business operations and the standards for risk disclosures (Ahmadi, 2018; Kuźnar, 2024). In this intricate setting, narcissistic CEOs may craft corporate narratives that obscure transparency and potentially mislead stakeholders. Despite this rich context, a substantial research gap persists in detailing how narcissistic CEO traits translate into governance actions impacting risk disclosure. For further details on how these executive traits interact with Iran's corporate governance frameworks to influence risk disclosure, refer to Section 2.

Building on this, our theoretical framework incorporates the Upper Echelon Theory, which asserts that organizational outcomes mirror the values and cognitive bases of senior executives (Hambrick & Mason, 1984). Supporting this perspective, research by Bonelli (2014) and Quttainah (2015) indicates that executives’ backgrounds significantly shape their strategic decisions. We examine both the positive and negative impacts of narcissism on risk disclosures: on the positive side, according to Self-Promotion Theory and Visibility Enhancement Theory, narcissistic CEOs might utilize risk disclosures to boost their public image and assert dominance. Self-Promotion Theory argues that narcissistic leaders use disclosures as a platform to highlight their effectiveness and foresight, potentially enhancing transparency (Awuah et al., 2024; Heavey et al., 2020). Visibility Enhancement Theory suggests that such CEOs employ disclosures to maintain or enhance their presence within corporate and investor circles, thereby influencing governance and stakeholder perceptions (Chatterjee & Pollock, 2017; Liu et al., 2016).

Conversely, Risk Concealment Theory and Manipulation Theory highlight the potential negative consequences. Risk Concealment Theory posits that narcissistic CEOs may obscure or minimize risks to portray stability and control (Akstinaite et al., 2020; Cormier et al., 2016). Manipulation Theory suggests that these CEOs could manipulate disclosures to present an overly positive outlook, which may mislead stakeholders (Buchholz et al., 2018; Marquez-Illescas et al., 2019). These theoretical perspectives form a robust basis for our hypothesis that CEO narcissism could influence risk disclosure practices in Iran both positively and negatively. A detailed exploration of these frameworks and their empirical support is presented in Section 3.

In our research, we analyze data from 1,480 firm-year observations of companies listed on the TSE between 2013 and 2022. We measure CEO narcissism (CEONAR) by the size of their signatures on annual reports, following a method validated by Ham et al. (2017; 2018), which links signature size to narcissistic traits. For risk disclosures (RISKDISC), we follow the approach of Lajili et al. (2024). We use a specialized bag-of-words model tailored for Persian MD&A documents. This model enables us to perform a detailed text mining analysis through NLP techniques, allowing us to evaluate the scope and quality of risk disclosures.

We find a positive and statistically significant relationship between CEO narcissism and the extent of risk disclosures, indicating that more narcissistic CEOs tend to disclose risks more extensively. This behavior is likely driven by their desire for self-promotion or to project an image of transparency and managerial control. These results are consistent with both the Self-Promotion and Visibility Enhancement theories, which argue that narcissistic CEOs may strategically use disclosures to enhance their visibility and manage stakeholder perceptions (Buchholz et al., 2020; Marquez-Illescas et al., 2019). To ensure the validity and stability of our results, we performed sensitivity analyses on the measurement of CEO narcissism and its impact on risk disclosures. These analyses tested the robustness of our findings under various scenarios, such as changes in the measurement of narcissism over different periods in a CEO's tenure and across their multiple positions in different firms. Additionally, we recalculated the model's standard errors using various clustering methods to address potential correlations within groups, enhancing the reliability of our conclusions.

Additional tests examining the impact of CEO narcissism on different risk dimensions—business, operational, and financial—consistently show that narcissistic CEOs influence all three categories, confirming the extensive impact of CEO traits on corporate risk communication. To address potential biases and endogeneity issues, we apply firm fixed effects, entropy balancing, and focus on periods of CEO transitions. Each method robustly links CEO narcissism to increased risk disclosure. Furthermore, our investigation explored the influence of corporate governance structures, particularly board composition, on the narrative around risk disclosures. We found a significant interaction between CEO narcissism and board structure, which moderated the relationship between narcissism and risk disclosure practices. Moreover, the post-2015 regulatory environment serves as a critical moderator in our analysis, revealing that the regulatory changes significantly intensify the impact of narcissistic traits on disclosure practices. Utilizing methodologies from Kravet and Muslu (2013) and Campbell et al. (2014), we analyzed risk disclosures in MD&A reports of Iranian companies, revealing significant associations between CEO narcissism and different dimensions of risk, which highlights the profound impact of CEO traits on corporate risk communication.

This study bridges personality psychology and corporate governance within a non-Western framework, broadening the scope of literature which traditionally focuses on Western settings. It offers empirical support for theories of narcissism and risk disclosure, exploring the nuances of Iranian corporate governance and refining established leadership and disclosure theories. This manuscript specifically contributes to the literature on the intersection of executive personality traits and corporate disclosure practices, focusing on how CEO narcissism influences firms’ voluntary disclosures. By examining how narcissistic tendencies drive disclosure behaviors in non-Western settings, particularly in Iran, this study extends the dialogue initiated by works such as Rijsenbilt and Commandeur (2013) and Olsen et al. (2014), which explore CEO narcissism's effects on corporate strategies and financial reporting quality. Moreover, our research enhances understanding of the specific pathways through which CEO narcissism can affect the scope and quality of information disclosed, contributing to theories like Upper Echelon Theory and Visibility Enhancement Theory. We uniquely apply these theories to explore how narcissistic CEOs may use voluntary disclosures not only to enhance their personal image but also to navigate and potentially exploit the distinctive governance structures and cultural nuances present in emerging markets. This adds a critical dimension to the literature by highlighting the impact of context-specific factors on the relationship between CEO narcissism and disclosure practices, which has been underexplored in predominantly Western-centric studies.

Practically, the insights help structure corporate governance in Iran and similar markets, guiding the development of policies that address the challenges posed by narcissistic leadership. This could include implementing oversight mechanisms to check the powers of dominant CEOs, enhancing accountability, and protecting stakeholder interests. Internationally, the findings are vital for investors and corporations in emerging markets, showing how narcissistic traits in leadership can affect disclosure practices and corporate health—key factors for informed investment decisions. From a policy-making angle, the research underscores the need to integrate psychological insights into regulatory frameworks, suggesting policies that enhance transparency and curb the excesses of narcissistic leadership, thus promoting healthier corporate environments. Theoretically, the study enriches Upper Echelon Theory by linking CEO traits to corporate risk disclosure outcomes and supports the Self-Promotion and Visibility Enhancement Theories that view disclosures as strategic tools used by narcissistic CEOs to boost their image.

This paper proceeds as follows: Section 2 examines the interplay between CEO narcissism and risk disclosure in Iran. Section 3 discusses theoretical frameworks and hypothesis development. Section 4 details the research design, while Section 5 presents the results. Section 6 conducts additional tests, and Section 7 concludes with reflections and implications of the findings.

The Dynamics of CEO Narcissism and Risk Disclosure in Iran's Corporate Sector

This section explores the unique interaction between CEO narcissism and risk disclosure within Iran's corporate governance, economic, and cultural environments. Understanding these nuanced impacts is essential for a comprehensive grasp of their effects on corporate transparency and stakeholder communication.

Firstly, Iran's corporate governance is distinctly shaped by its political structure and economic system (Chehabi, 2001), where state ownership and control over large sectors of the economy play a critical role (Khajeheian et al., 2021). Unlike more market-driven economies, many Iranian companies are either state-owned or have significant state participation (Tajeddini & Trueman, 2016), leading to unique governance challenges that are not as prevalent in Western settings. The Iranian Commercial Code (Research Group of Private Law, 2002) and the Securities Market Act of Iran (Salehabadi, 2013) impose specific corporate governance requirements that are tailored to manage the complexities associated with state influence. These include mandatory risk disclosure regulations that are more stringent for companies in sensitive sectors such as oil and gas, banking, and telecommunications. For instance, companies listed on the Tehran Stock Exchange (TSE) are required to provide detailed disclosures on financial risks, operational risks, and market risks, which are rigorously scrutinized to maintain state interests and public trust (Kashani & Shiri, 2022; Rahmani et al., 2021). Secondly, CEO appointments in Iran often reflect political considerations, with decisions significantly influenced by governmental policies (Mohammadrezaei et al., 2013). This unique setup can enhance the tendencies of narcissistic CEOs to manipulate disclosure practices for personal or organizational gain, especially in light of efforts to improve transparency and align with international governance standards. These efforts aim to increase executive accountability, enhance financial reporting quality, and protect minority shareholder interests (Akrami & Momen, 2023). Analyzing how narcissistic behaviors of CEOs adapt to these evolving conditions reveals the dynamic interaction between executive personality and corporate disclosure practices.

Thirdly, in Iran, the regulatory emphasis on risk disclosure is particularly significant due to the country's volatile economic environment and international sanctions (Blue et al., 2024; Rajabalizadeh, 2025). The TSE regulations, revised post-2015 nuclear deal, require listed companies to extensively disclose risks that might affect their operations or financial performance (Draca et al., 2019; Salehi et al., 2018). These disclosures are not just procedural but are crucial for maintaining investor confidence and market stability amid economic uncertainties. Specifically, the regulations mandate that disclosures must cover areas such as currency risks, sanctions-related risks, and geopolitical tensions, which are uniquely pertinent to Iranian companies (Neifar & Jarboui, 2018). This regulatory framework provides narcissistic CEOs an opportunity to enhance their public image by demonstrating vigilance and proactive management of these complex risks (Salehi et al., 2021). It also allows them to manipulate disclosures to project stability or deflect from managerial shortcomings, playing into the narrative of control and competency (Ramzi et al., 2023). Moreover, Iran's challenging economic and political landscape, characterized by sanctions and instability, profoundly affects business operations and risk disclosure standards (Ahmadi, 2018; Kuźnar, 2024). Amidst this challenging economic and political landscape, narcissistic CEOs might use these conditions to shape corporate narratives that favor their image, often resulting in skewed or misleading risk disclosures (Amernic & Craig, 2007). The economic pressures and political flux provide opportunities for such CEOs to either assert aggressive strategies showcasing their dominance (Lovelace et al., 2018) or adopt conservative tactics to obscure company weaknesses (Kowalzick & Appels, 2023). This behavior pattern provides a fertile ground for examining how narcissistic tendencies under economic and political duress influence the nature and veracity of disclosed corporate risks.

Finally, the cultural framework within Iranian corporations, defined by high power distance and a strong aversion to uncertainty (Rajabalizadeh, 2025; Soltani et al., 2015), offers a context in which CEO narcissism could either be amplified or moderated. Narcissistic CEOs might use the cultural norm of power distance to enforce their decisions without opposition, potentially centralizing power and limiting transparent decision-making (Cortes-Mejia et al., 2022). Moreover, their response to the cultural preference for clear guidelines and predictability might result in overly confident and risky corporate disclosures during uncertain times, appealing to stakeholders’ need for stability but risking significant misrepresentations (Cho et al., 2016). Understanding these cultural dimensions is crucial for dissecting how narcissistic tendencies shape corporate governance and risk disclosure strategies in Iran. In light of these diverse influences, it is clear how deeply narcissistic tendencies of CEOs are woven into the fabric of corporate governance and risk disclosure strategies in Iran. The next section will provide a theoretical foundation for our hypotheses development based on the Iranian context, further analyzing how these executive traits interact with local corporate dynamics to shape disclosure practice.

Theoretical Frameworks, Empirical Evidence, and Hypothesis Development in Iran

Exploring the influence of CEO narcissism on corporate risk disclosures involves a theoretical approach rooted in Upper Echelon Theory, as introduced by Hambrick and Mason (1984). This theory suggests that organizational outcomes, like strategic decisions and performance, reflect the values and thoughts of top executives. Supported by research from Bonelli (2014) and Quttainah (2015), it is argued that executives’ backgrounds impact their strategic decisions, a concept further explored by Carpenter et al. (2004) through demographic studies. This framework guides our analysis of how narcissistic traits in CEOs might affect their risk disclosure practices, investigating both the potential benefits, such as increased transparency to enhance their image, and the drawbacks, such as the risk of information manipulation.

To deepen our understanding of these behaviors, we also draw on Psychodynamic Theory, which examines the unconscious motivations and emotional drives behind individual actions (Berlin, 2011; Shaver & Mikulincer, 2005). This theory, elucidated by research, suggests that narcissistic traits, including a heightened need for admiration and an inflated self-view, can compel CEOs to engage in distinctive disclosure behaviors that serve both self-promotion and defensive purposes (Chatterjee & Pollock, 2017; Dabbebi et al., 2022; Marquez-Illescas et al., 2019). For example, a CEO might use extensive disclosures to project an image of competency and control, or alternatively, manipulate disclosures to conceal weaknesses and maintain an illusion of stability. This dual impact reflects in the decisions where narcissistic CEOs are observed issuing more positive earnings announcements, promoting social and governance activities, and engaging in practices like opportunistic insider trading under specific conditions (Jiang et al., 2023). Additionally, insights on linguistic markers of deception (McCornack et al., 2014) in earnings calls suggest that these executives may also use specific language features to mislead or manipulate stakeholder perceptions during high-stakes communications (Burgoon et al., 2016; Burgoon & Qin, 2006).

These two foundational theories—Upper Echelon and Psychodynamic—provide a comprehensive framework for analyzing the complex interplay between CEO personality traits and their impact on corporate governance and risk disclosure practices. By leveraging both theories, we gain insights into the conscious strategic decisions influenced by CEOs’ backgrounds and the unconscious motives that drive their behavior in risk management. With this dual theoretical foundation, we investigate how subsidiary theories such as Self-Promotion Theory and Visibility Enhancement Theory can posit positive relationships, while Risk Concealment Theory and Manipulation Theory can illustrate the potential negative impacts.

Positive Dynamics: The Strategic Advantages of Narcissistic Leadership in Risk Disclosures

Exploring how CEO narcissism influences risk disclosures, we focus on two theories: Self-Promotion Theory and Visibility Enhancement Theory. These frameworks explain how narcissistic CEOs might use risk disclosures extensively and strategically to enhance their image and impact corporate governance and stakeholder views significantly.

Narcissistic CEOs, motivated by a desire for admiration, often see risk disclosures as a way to showcase their leadership skills and proactive governance (Awuah et al., 2024). According to Self-Promotion Theory, these leaders are not merely sharing information but are shaping stakeholder perceptions of their leadership and the company's outlook (Heavey et al., 2020; Yi et al., 2020). Awuah et al. (2024) argue that these CEOs leverage disclosures to assert control and project an image of effective leadership. Furthermore, Heavey et al. (2020) and Yi et al. (2020) provide evidence that narcissistic CEOs use these disclosures to favorably manipulate stakeholder views. Buchholz et al. (2020) add that such CEOs engage in earnings management early in their tenure, using risk disclosures to construct a successful image through strategic emphasis or minimization of certain risks. In Iran, where corporate governance is adapting to regulatory, economic, and cultural shifts, the proactive disclosure practices of narcissistic CEOs could have positive implications. By meeting demands for transparency amid international scrutiny, these CEOs craft narratives of competence and reliability, potentially improving the firm's reputation with global investors and local stakeholders, thus stabilizing the company's image in a volatile market.

Moving from self-promotion to Visibility Enhancement Theory, we see that narcissistic CEOs use risk disclosures strategically to enhance their visibility and maintain a prominent position in corporate and investor circles (Chatterjee & Pollock, 2017). Such visibility is linked to company performance and investor confidence. Liu et al. (2016) suggest that highly visible CEOs, influenced by narcissism, often undertake higher-risk activities, such as in R&D, to boost their public image and their firms’ perceived innovativeness. However, the relationship between CEO narcissism, visibility, and stakeholder perception is intricate. Marquez-Illescas et al. (2019) observe that while narcissistic CEOs aim to boost their visibility with bold disclosures, these can sometimes negatively impact investors’ views on management's credibility, possibly deterring investment due to perceived manipulation. Chatterjee and Hambrick (2011) note that narcissistic CEOs, driven more by social praise than objective performance metrics, use disclosures to gain positive media portrayal. Similarly, Blankespoor and deHaan (2020) show that CEOs often use press releases to improve media representation, sometimes at the cost of transparency. In Iran's unpredictable market, where media impact and international visibility are crucial, narcissistic CEOs may use risk disclosures to navigate economic sanctions and political challenges, presenting themselves as capable leaders. This not only solidifies their leadership but also draws investment by highlighting their decisive and visionary approach.

Considering both the Self-Promotion and Visibility Enhancement Theories, and supported by empirical studies, we predict a positive link between CEO narcissism and risk disclosures in Iran. These traits likely prompt CEOs to craft disclosures that not only enhance their image but also improve organizational transparency amidst a complex regulatory and economic environment.

Negative Dynamics: The Perils of Narcissistic Manipulation in Risk Disclosures

Contrasting with the positive aspects of CEO narcissism, some theories highlight potential downsides, such as less transparency and potentially deceptive behaviors. Two key theories—Risk Concealment Theory and Manipulation Theory—outline how narcissistic traits might lead CEOs to withhold or distort critical risk information.

According to the Risk Concealment Theory, narcissistic CEOs may hide or minimize risks to maintain an image of control and invulnerability (Akstinaite et al., 2020; Cormier et al., 2016), a behavior that might be more evident in cultures with high power distance, like Iran. This approach correlates with accounting issues like information asymmetry, where leaders might manipulate information to mask vulnerabilities (Bergh et al., 2019). Research indicates that narcissistic leaders often make riskier decisions and engage in earnings manipulation to present an illusion of success. ' note that these CEOs are inclined to take risks with disregard to the potential negative outcomes. Capalbo et al. (2018) observe that such leaders might positively manage earnings, sometimes inaccurately reflecting the business's actual performance. Chatterjee and Hambrick (2011) argue that these CEOs are more driven by social praise and media attention than by objective performance metrics, leading to manipulated disclosures to suit their preferred image. Additionally, Olsen et al. (2014) found that companies under narcissistic CEOs often report inflated earnings-per-share and stock prices, achieved through real activities rather than accrual manipulations. In Iran, where authority and control are culturally significant, narcissistic CEOs may heavily utilize risk concealment strategies, especially given the country's economic sanctions and political instabilities. This tendency to maintain control can intensify the use of such deceptive practices in the Iranian business landscape.

Building on the concept of risk concealment, Manipulation Theory (McCornack et al., 2014) delves into how narcissistic CEOs might craft disclosures to project an overly optimistic company image. This includes selective disclosures and embellishing company prospects while downplaying risks. Studies show that such leaders often manipulate financial disclosures to cast their companies in a more favorable light. Marquez-Illescas et al. (2019) and Buchholz et al. (2018) noted that firms with narcissistic CEOs frequently use optimistic language in earnings announcements and 10-K filings, often unaligned with actual performance. This abnormal optimism is not just about shaping current perceptions; it strategically supports future equity offerings and increased R&D investments (Buchholz et al., 2018). Moreover, these CEOs are known for managing earnings, particularly during their initial tenure, to forge a successful track record (Buchholz et al., 2020; Capalbo et al., 2018). However, the market often views such disclosures skeptically, recognizing the potential bias (Marquez-Illescas et al., 2019). In Iran's challenging economic and political climate, narcissistic CEOs may use risk disclosures misleadingly to portray the company's resilience and market position. This is especially crucial in heavily monitored sectors or those vital to national interests, where maintaining a favorable image is key to a CEO's career and political influence. In such a high-stakes environment, the likelihood of disclosure manipulation by narcissistic CEOs underscores the need for increased vigilance among stakeholders and regulators to ensure that disclosures accurately reflect the company's true financial health and operational stability.

After examining both Risk Concealment Theory and Manipulation Theory, it is clear that while narcissistic CEOs may use disclosures to enhance their visibility and authority, such actions often harm transparency and accuracy in reporting. In Iran, the need to maintain a positive public image under tough conditions might push narcissistic CEOs towards more frequent deceptive practices. This situation highlights the risks of narcissistic leadership in environments that require honest and robust disclosures.

Having considered the theories and empirical evidence supporting both positive and negative relationships between CEO narcissism and risk disclosures, and considering the specific context of Iran, it becomes clear that the impact of narcissistic leadership on disclosure practices can be complex and multifaceted. Narcissistic traits can drive CEOs to either enhance transparency to bolster their image or compromise disclosure integrity to conceal vulnerabilities. This dual potential underscores the need for a nuanced understanding of how personality traits interact with cultural and economic factors to influence corporate governance practices. Given the conflicting potentials of CEO narcissism to influence corporate disclosures in both beneficial and detrimental ways, we propose a non-directional hypothesis:

Research Design

Sample and Data

Data for this study were sourced from CODAL, managed by the Securities and Exchange Organization (SEO) of Iran, and included firms listed on the TSE from 2013 through 2022. Starting with 3,230 firm-year observations, adjustments were made for specific exclusions (refer to Table 1), resulting in a refined sample of 1,550 firm-year observations. After excluding damaged PDF files, the final sample for analysis was 1,480 firm-year observations. We converted the annual financial statements and MD&A PDFs into text files using a Python script, which facilitated the text mining analysis for calculating variables related to risk disclosures. 1

Sampling Table.

Dependent Variable: Risk Disclosure

In this study, we focus on measuring risk disclosure, incorporating categories such as business, operational, and financial risks as detailed by Lajili et al. (2024). Appendix A lists the original bag of words for these categories. We have developed a specialized bag-of-words model to analyze risk disclosures within Persian MD&A documents. This model involved translating key risk-related terms into Persian, supported by the Google Translate API and refined through discussions with bilingual Persian-speaking financial experts. The accuracy of these translations was further ensured by reviews from academic faculty members specialized in finance and linguistics, as well as consultations with authoritative Persian dictionaries. To address the linguistic similarities between Persian and Arabic, which are prevalent in Iranian financial discourse (Rajabalizadeh, 2023; Rajabalizadeh & Schadewitz, 2025b), we included terms that bridge both languages. This approach is essential to fully capture the range of risk-related concepts in Persian financial narratives. The refined keyword set for our risk disclosure variable (RISKDISC) consists of 82 precise terms. We compute the risk disclosure index by taking the natural logarithm of the total counts of these words plus one.

Independent Variable: CEO Narcissism

In alignment with recent studies within the accounting field, the size of a signature has been identified as a subtle yet effective indicator of an individual's narcissistic traits (Chou et al., 2021; Church et al., 2020; Ham et al., 2017; 2018). Research has consistently shown that larger signatures correlate with higher levels of self-esteem, ego, dominance, and self-regard, making it a viable proxy for narcissism.

In our study, we examined the hand-written signatures of CEOs from publicly listed Iranian companies, specifically those included in the declarations within annual reports. This approach was chosen to circumvent the inaccuracies associated with automated signatures. Our methodology aligns with the approach used by Ham et al. (2017, 2018), which has been rigorously validated in prior studies and is recognized for its robustness in measuring narcissistic traits. Psychological research, including foundational studies like Raskin and Terry (1988), portrays narcissism as a stable personality trait across an individual's adult life. This underpins our decision to treat the signature size as a static measure, reflecting the CEO's enduring personal characteristics rather than transient states. We collected the most recent signature of each CEO from the most publicly visible sections of the annual reports, financial statements, and MD&A documents. This ensures that the signatures are reflective of the CEOs’ current administrative tenure and their public-facing communications. Where relevant, we also gathered historical signatures of previous CEOs to facilitate a broader analysis of leadership behavior and trends across different regimes within the same firms. This comprehensive approach allows us to capture a nuanced view of executive personality traits and their impact on corporate governance and communication strategies.

Utilizing the methodology established by Ham et al. (2017; 2018), we used ImageJ software to precisely measure each signature. This involved enclosing the signature within a tightly fitted rectangle, ensuring each side of the rectangle touched the furthest extent of the signature. We then calculated the area of this rectangle (length times width) and normalized this by the number of characters in the CEO's name to account for variations in name length. The average of these normalized areas was calculated across all observed signatures to determine the typical signature size for each CEO. To quantify the level of narcissism, we took the natural logarithm of the average signature size. This measure serves as our primary independent variable for assessing CEO narcissism (CEONAR) in the context of corporate governance and decision-making.

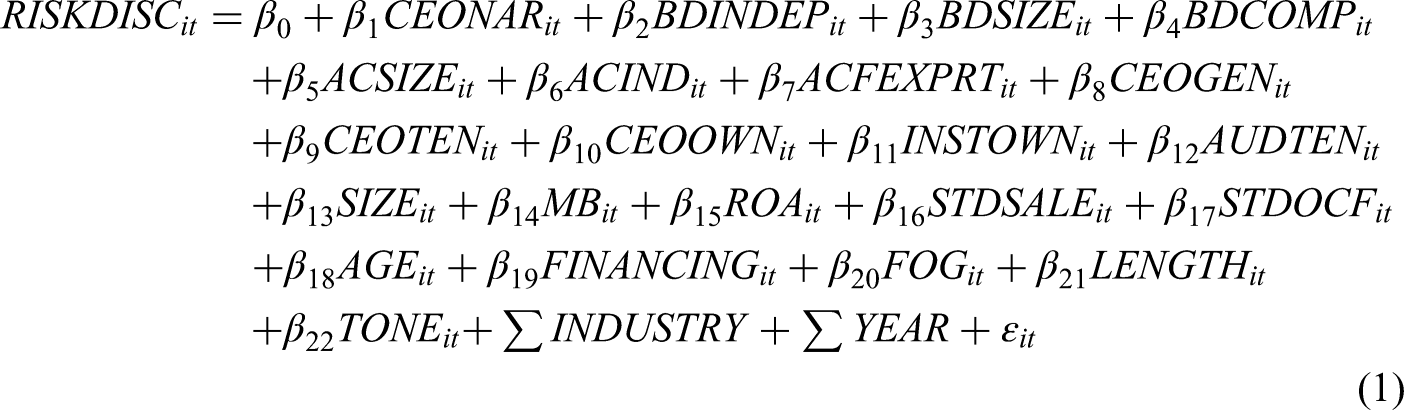

Main Model

Our main model aims to estimate the impact of CEO narcissism on risk disclosure among publicly listed Iranian companies.

The model incorporates a range of control variables to isolate the impact of CEO narcissism on risk disclosure, drawing from both international (Church et al., 2020; Ham et al., 2017; 2018; Lajili et al., 2024; Monjed & Ibrahim, 2020) and Iranian studies (Hesarzadeh and Rajabalizadeh, 2019; Rajabalizadeh, 2023; Rajabalizadeh & Oradi, 2022; Rajabalizadeh & Schadewitz, 2025a). This diverse literature base helps illuminate the complex interplay between corporate governance, financial characteristics, and disclosure practices.

Variables such as BDINDEP, BDSIZE, and BDCOMP reflect board dynamics, hypothesizing that a higher proportion of independent directors or a larger, more diverse board could enhance risk disclosure quality. ACSIZE, ACIND, and ACFEXPRT highlight the role of the audit committee, where size and expertise are expected to bolster risk evaluation and reporting. CEO gender (CEOGEN) and tenure (CEOTEN) are included to consider the potential impact of leadership stability and gender diversity at the top level. CEOGEN assesses the influence of gender diversity among leadership, while CEOTEN reflects the CEO's experience and potential stability in leadership, both of which are hypothesized to affect risk disclosure practices. CEOOWN and INSTOWN address ownership structures that may affect transparency, while AUDTEN focuses on the potential influence of auditor tenure on disclosure. Additionally, SIZE, defined as the natural log of total assets, has been included to capture variations in disclosure norms and capabilities across different-sized firms. Financial health indicators like MB and ROA, along with STDSALE and STDOCF, provide context on the company's financial stability and its effect on risk disclosures. AGE denotes company maturity, theorizing that older companies may have more established disclosure practices. FINANCING is included to capture the disclosure needs triggered by recent significant financing activities. Readability and sentiment measures such as FOG, LENGTH, and TONE are incorporated to assess how information presentation affects stakeholder perceptions. Together with year and industry effects detailed in Appendix D, these variables form a robust framework to analyze the influence of CEO narcissism on risk disclosure, ensuring a thorough examination of the determinants of transparency in corporate communications.

Results

Descriptive Statistics

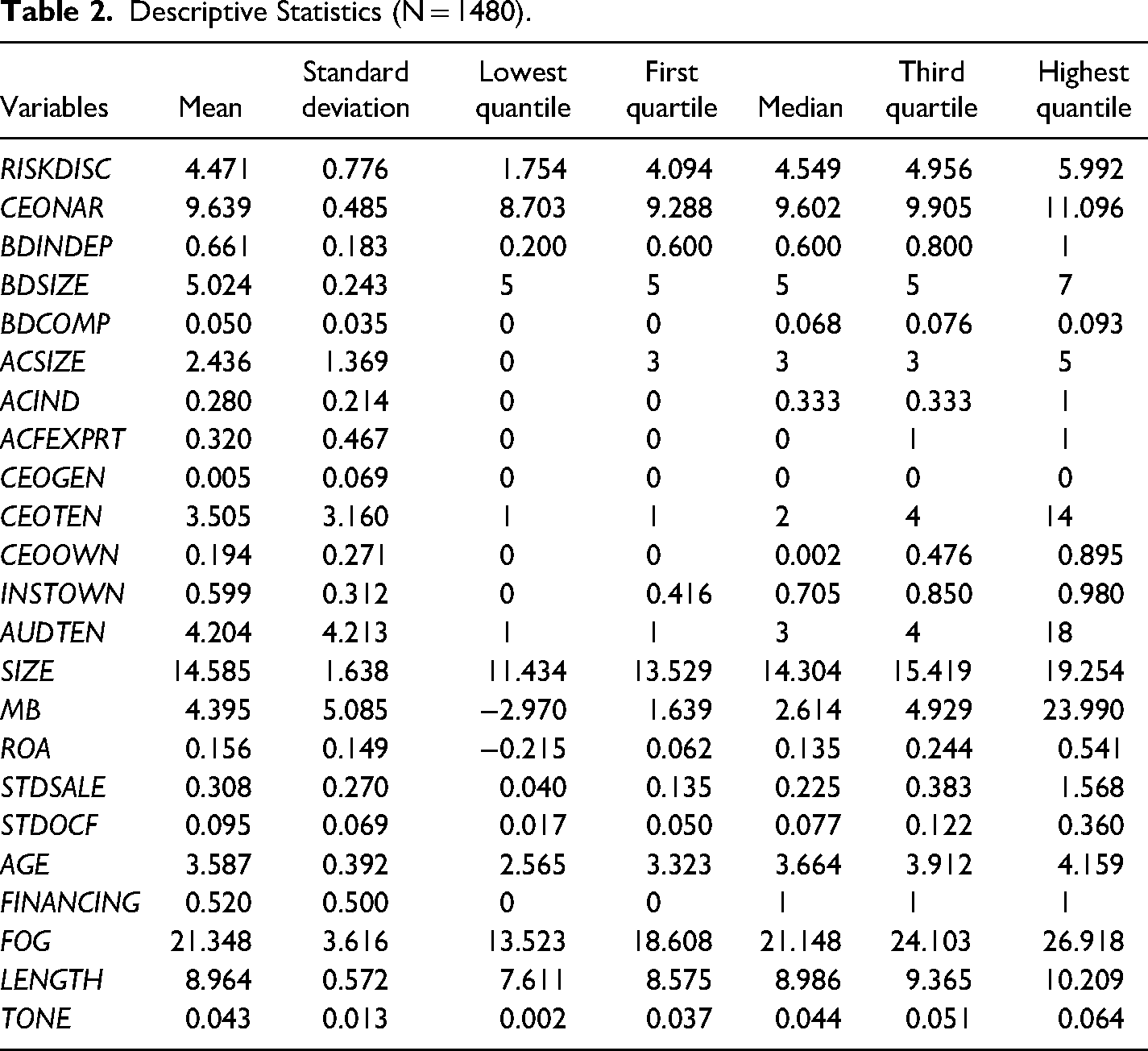

The descriptive statistics of our study are detailed in Table 2. The mean value of the risk disclosure index is 4.471, with a standard deviation of 0.776. The distribution of RISKDISC values ranges from a low of 1.754 to a high of 5.992, indicating varying levels of risk disclosure practices among the firms. Given that this study introduces the measurement of risk disclosure in the Iranian market, there is no existing benchmark for comparison, making these findings foundational for understanding risk communication in this context. CEONAR has a mean of 9.639 and a standard deviation of 0.485, with values ranging from 8.703 to 11.096. This measure is pioneering in the Iranian market, though it aligns closely with similar studies internationally, such as the mean narcissism score of 9.659 for CFOs by Xiang and Song (2021). This comparability supports the relevance and validity of our narcissism metric in assessing executive personality traits within an Iranian corporate governance framework.

Descriptive Statistics (N = 1480).

Among notable control variables, BDINDEP and BDSIZE reflect board characteristics, where the average percentage of independent directors is 0.661 and the typical board size is approximately 5 directors. These board metrics suggest a moderate level of independence and a compact board size, which are critical for effective oversight and governance. Additionally, CEOGENDER and CEOTENURE are incorporated to explore the impact of leadership characteristics on risk disclosures. The data shows that a significant majority of CEOs are male, with an average tenure of 3.505 years, reflecting the potential stability and experience in leadership roles. INSTOWN averages 0.599, indicating significant institutional presence and potential influence on corporate transparency and governance practices. The average auditor tenure is 4.204 years, suggesting a balance between auditor familiarity and independence. SIZE, measured as the natural log of total assets, averages 14.585, highlighting the scale of operations and its potential impact on risk disclosures and corporate behavior. The average MB ratio is 4.395, which indicates high market valuation relative to book value, a factor that could influence strategic decisions and risk-taking behaviors. FOG, the readability of financial disclosures with an average of 21.348, tends to be complex, which might impact stakeholder understanding and reaction to disclosed information.

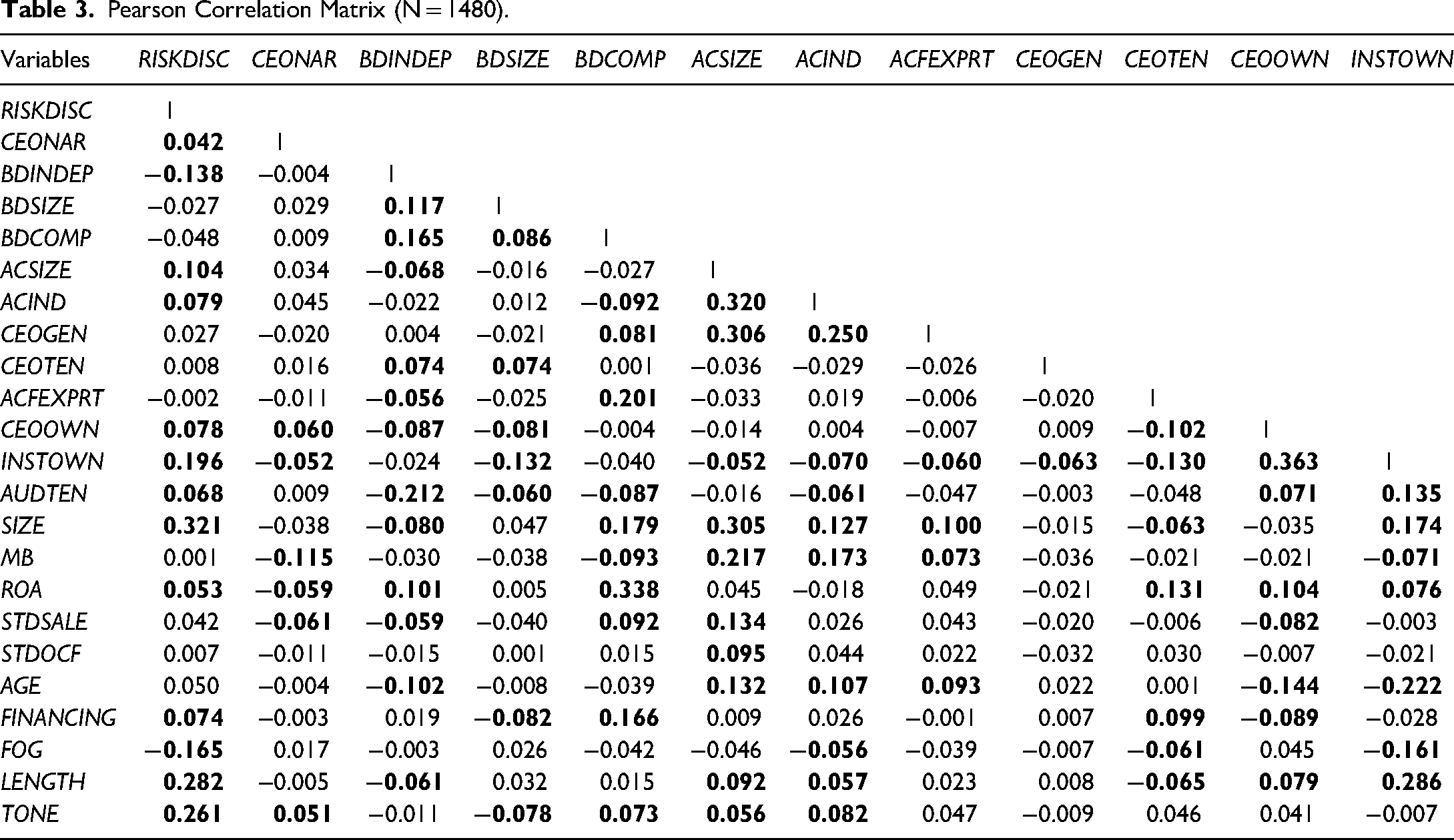

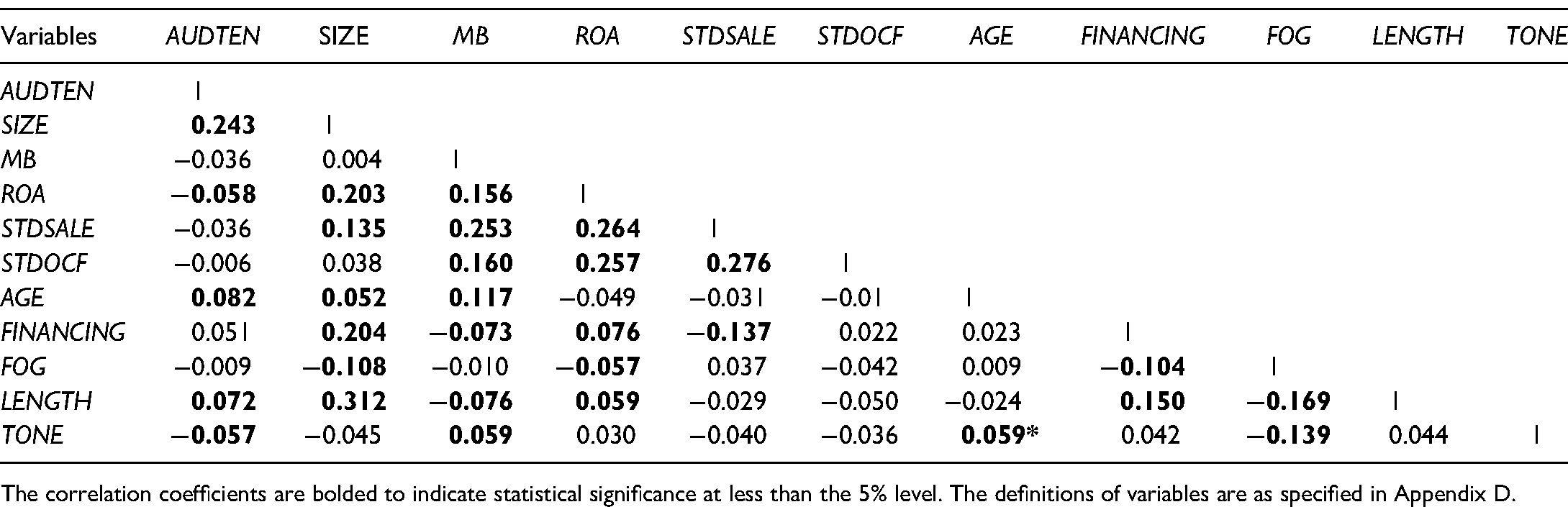

Table 3 displays the Pearson correlation matrix, illustrating relationships between key variables. There's a positive and meaningful correlation (0.042) between risk disclosure (RISKDISC) and CEO narcissism (CEONAR), suggesting that higher CEO narcissism levels might be associated with more extensive risk disclosures. Additionally, certain control variables show significant correlations with RISKDISC: SIZE is positively correlated at 0.321, indicating that larger firms tend to provide more comprehensive risk disclosures; institutional ownership (INSTOWN) is positively correlated at 0.196, indicating that firms with greater institutional ownership are likely to provide more thorough risk disclosures; the length of disclosures (LENGTH), with a correlation of 0.282, implies that longer disclosures are associated with more detailed risk information; and the tone of the report (TONE), showing a correlation of 0.261, suggests that a more positive tone is associated with extensive risk information. These correlations among the control variables and both the dependent and independent variables enhance the robustness of our regression analysis, ensuring a comprehensive understanding of the factors influencing risk disclosure 2 . Detailed description of variables is further detailed in Appendix D.

Pearson Correlation Matrix (N = 1480).

The correlation coefficients are bolded to indicate statistical significance at less than the 5% level. The definitions of variables are as specified in Appendix D.

Regression Results

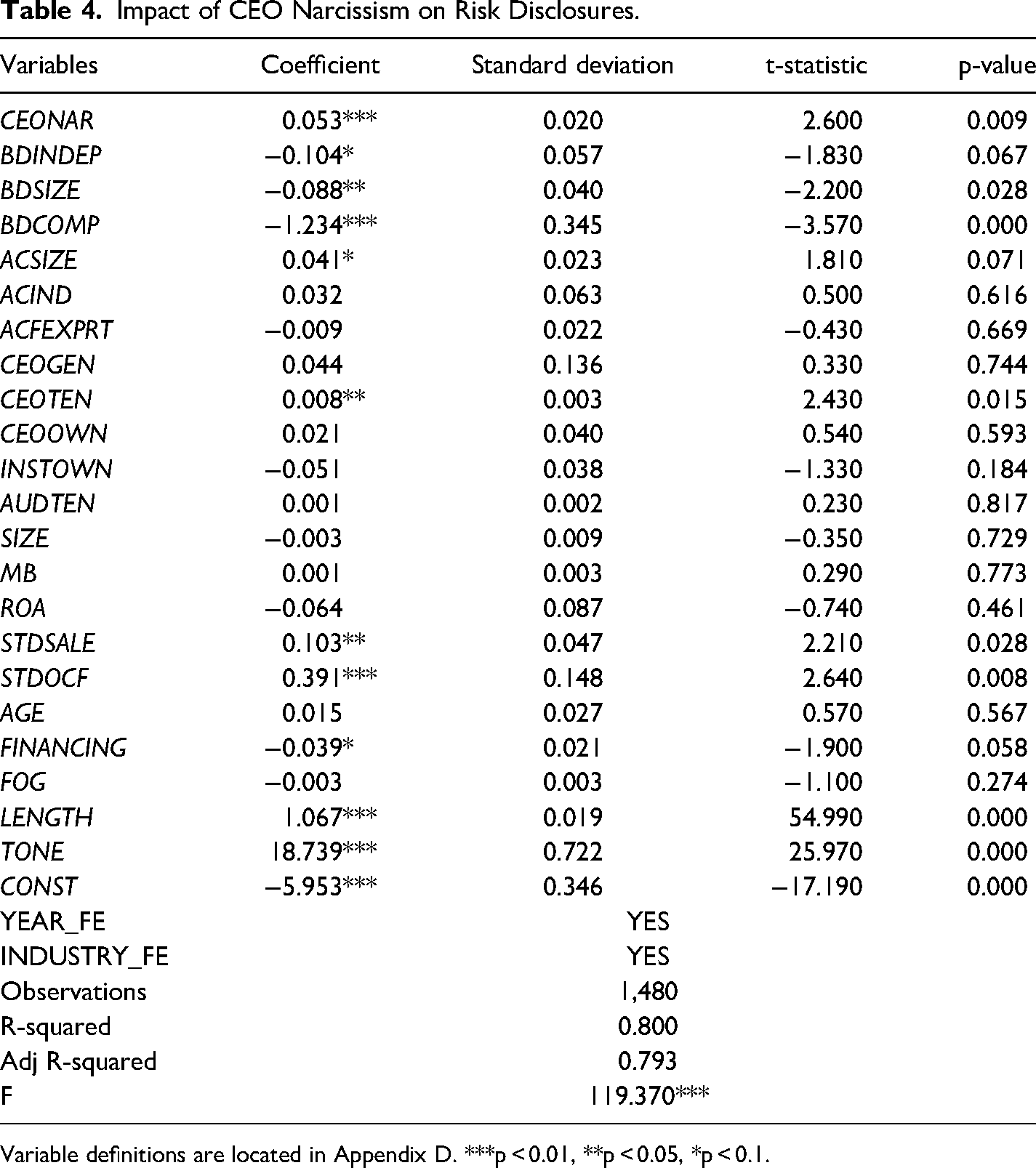

Table 4 provides the results of the regression analysis examining the impact of CEO narcissism (CEONAR) on risk disclosures (RISKDISC) among publicly listed Iranian companies. The analysis includes 1,480 observations and controls for year and industry fixed effects. The model demonstrates a strong fit, evidenced by an R-squared value of 0.800 and an adjusted R-squared of 0.793, indicating that approximately 79.3% of the variability in risk disclosures can be explained by the model's variables.

Impact of CEO Narcissism on Risk Disclosures.

Variable definitions are located in Appendix D. ***p < 0.01, **p < 0.05, *p < 0.1.

The coefficient for CEO narcissism is 0.053, significant at the 1% level (p-value = 0.009), suggesting that higher levels of CEO narcissism are associated with an increase in the extent of risk disclosures. 3 This positive relationship implies that more narcissistic CEOs may engage in more extensive disclosure of risks. This finding aligns with theories like Self-Promotion and Visibility Enhancement, suggesting that narcissistic CEOs use disclosures strategically to enhance their public image and control over corporate narratives (Awuah et al., 2024; Heavey et al., 2020). The economic impact of CEO narcissism on risk disclosures, while statistically significant, shows a moderate effect size. The coefficient indicates that a one standard deviation increase in CEO narcissism leads to a 0.053 unit increase in the risk disclosure index. Given the mean level of risk disclosures, this effect, while not overwhelming, is non-negligible and highlights the influence of CEO personality traits on corporate communication strategies.

The control variables significantly enhance our understanding of the factors that shape risk disclosure practices, demonstrating how governance structures and report characteristics interact with executive traits to influence corporate transparency. The negative relationship of BDINDEP with risk disclosures, significant at the 5% level, suggests that a higher percentage of independent directors may correlate with a tendency towards more succinct and focused disclosures rather than more extensive ones. Similarly, both BDSIZE and BDCOMP show negative coefficients, significant at the 5% and 1% levels, respectively, indicating that larger board sizes and higher female representation, contrary to expectations, are associated with less extensive risk disclosures. This might suggest a more conservative approach to governance and communication by these boards. ACSIZE is marginally significant with a positive coefficient, suggesting that larger audit committees may be associated with more comprehensive risk disclosures, potentially due to the broader range of expertise within these committees. CEOTEN also demonstrates a positive relationship with risk disclosures, implying that longer CEO tenure may be correlated with a more thorough approach to risk disclosure. This could result from greater organizational familiarity and strategic insights acquired over time.

Moreover, STDSALE and STDOCF both exhibit positive relationships with risk disclosures, indicating that firms with more variability in sales and cash flows disclose more about their risks, possibly to address stakeholders’ information needs under uncertainty. FINANCING shows a marginally significant negative effect, suggesting that firms engaged in recent significant financing activities might adopt a more conservative approach to risk disclosure. Additionally, LENGTH and TONE, which have large positive coefficients and are significant at the 1% level, highlight that longer documents and more positive tones in disclosures are strongly associated with more extensive risk disclosures. These findings underscore the complex interplay between corporate governance and personality traits of executives in shaping the transparency of risk disclosures, carrying practical implications for stakeholders like investors and regulators who evaluate the quality and sufficiency of such disclosures.

Sensitivity Checks

Sensitivity Analysis of CEO Narcissism Measurement

To bolster the credibility and robustness of our findings, we undertook a series of sensitivity analyses focusing on the measurement of CEO narcissism and its implications on risk disclosures. These analyses were essential to test the stability of our results under various conditions and assumptions, particularly concerning the static nature of the narcissism proxy and the handling of CEOs with multiple tenures across different firms. Due to the intricate nature of the analyses and the need for brevity, the results of these sensitivity checks are presented in an untabulated format, summarizing the primary outcomes and ensuring clarity in the communication of our findings. The first part of our sensitivity analysis addressed the potential variability in the measurement of narcissism, given its theoretical stability as a personality trait, by re-evaluating the proxy at different points in a subset of CEOs’ tenures. The second part examined the effect of CEOs who served in multiple firms within our dataset, assessing whether their repeated appearances could skew the overarching conclusions of our study.

Sensitivity Analysis for Static vs. Non-Static Narcissism Proxy

This section evaluates the robustness of our findings using a static measurement of CEO narcissism against potential variations over time. Given the nature of narcissism as a stable trait, our primary analysis employs a static proxy, measuring the signature size once during the CEO's tenure. To validate this approach, we conducted a comparative analysis where available, measuring the signatures at multiple points during the tenure of a subset of CEOs. Hence, a subset of 30 CEOs whose tenure spanned more than five years was selected. For these CEOs, signatures were collected at three points: at the beginning, middle, and end of their tenure. Regression models identical to the primary study were run for each set of signatures to detect any significant variations in the measured effect of narcissism on risk disclosures. The comparative analysis showed negligible variations in the regression coefficients across different time points, confirming the assumption that narcissism, as reflected through signature size, remains relatively stable over time. The p-values and coefficients remained within a 5% range of those reported in the main analysis, supporting the use of a static proxy.

Handling Multiple Tenures of CEOs

In instances where CEOs were associated with multiple companies during the sample period, we analyzed the implications of treating each tenure independently. This section reports on a sensitivity check conducted to ascertain if the inclusion of multiple tenures by the same CEO influenced the overall results. We identified 75 firm-year observations where CEOs changed firms during the study period. Each tenure was treated as independent in the primary analysis to maintain the contextual integrity of each firm's data. The primary analysis was rerun excluding these 75 observations to evaluate the impact of their inclusion. Excluding the 75 firm-year observations associated with CEOs who had multiple tenures resulted in a sample size reduction to 1,405 firm-year observations. The analysis demonstrated that the main results were consistent with those obtained from the full sample, indicating that the presence of multiple tenures did not significantly affect the study's findings. This was evidenced by the persistence of similar p-values and the stability of regression coefficients, reinforcing the validity of our original model.

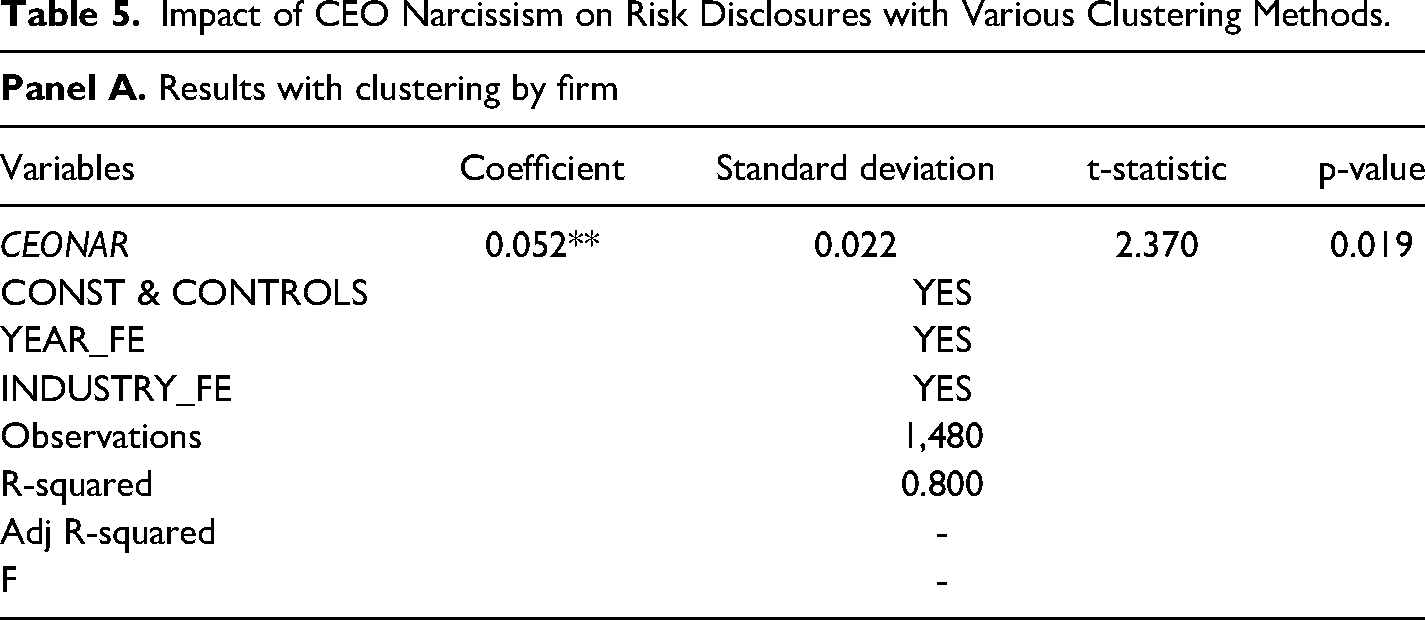

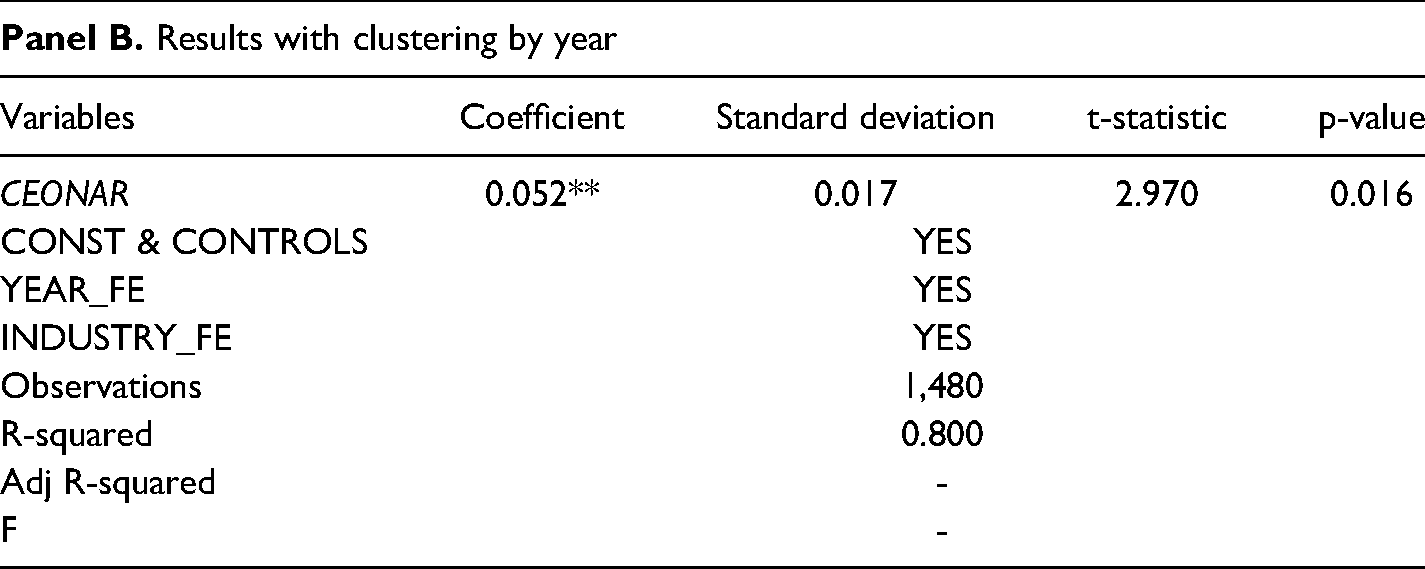

Sensitivity Checks for Clustering Standard Errors

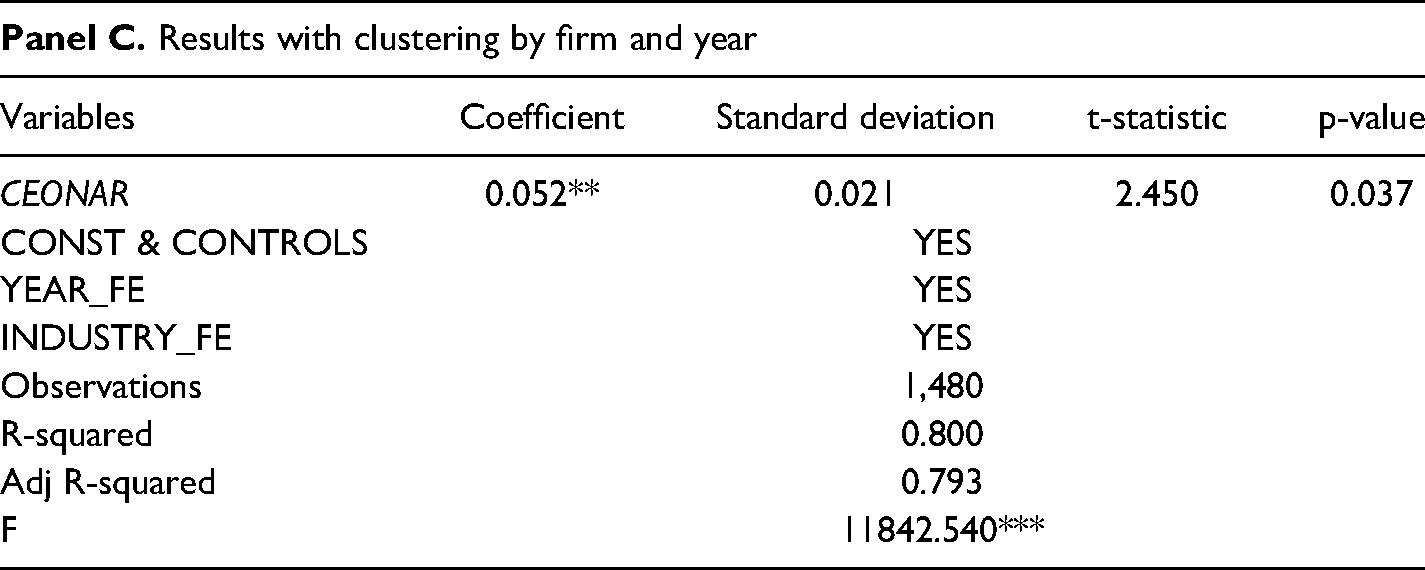

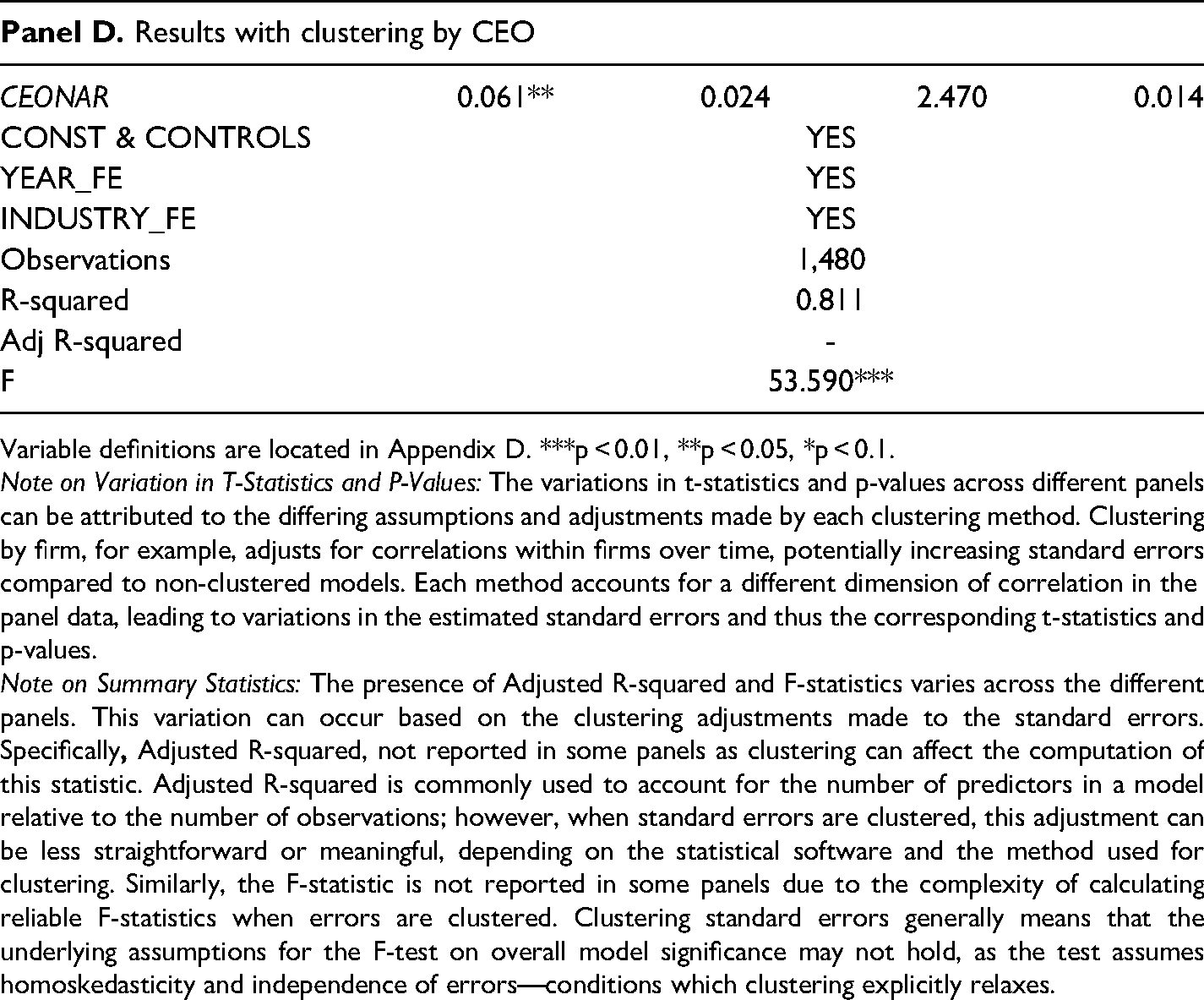

We conducted sensitivity checks by recalculating the model's standard errors using different clustering methods to ensure the robustness of our results against various assumptions about error correlation. The analysis was clustered by firm, year, both firm and year, and CEO. These methods are crucial for accounting for potential correlation within groups that standard errors may not capture if treated as independent. Clustering by firm approach addresses the correlation of residuals within the same firm over time, potentially caused by firm-specific practices and policies that affect risk disclosure consistently. Clustering by year accounts for common shocks or policy changes affecting all firms in a given year, ensuring that temporal externalities do not bias our inference. Clustering by firm and year (multiway clustering) provides a stringent test against the possibility of correlated errors both within firms and across years, offering the most conservative standard error estimates. Finally, clustering by CEO considers the individual effects of CEOs who may influence multiple observations through their tenure across different periods or firms. The results, as detailed in Table 5, affirm the positive impact of CEO narcissism on risk disclosures across all clustering methods, with slight variations in significance levels and coefficients, reflecting the robustness of our findings across different error structures.

Impact of CEO Narcissism on Risk Disclosures with Various Clustering Methods.

Variable definitions are located in Appendix D. ***p < 0.01, **p < 0.05, *p < 0.1.

Note on Variation in T-Statistics and P-Values: The variations in t-statistics and p-values across different panels can be attributed to the differing assumptions and adjustments made by each clustering method. Clustering by firm, for example, adjusts for correlations within firms over time, potentially increasing standard errors compared to non-clustered models. Each method accounts for a different dimension of correlation in the panel data, leading to variations in the estimated standard errors and thus the corresponding t-statistics and p-values.

Note on Summary Statistics: The presence of Adjusted R-squared and F-statistics varies across the different panels. This variation can occur based on the clustering adjustments made to the standard errors. Specifically

Additional Tests

CEO Narcissism and Specific Risk Dimension Disclosures

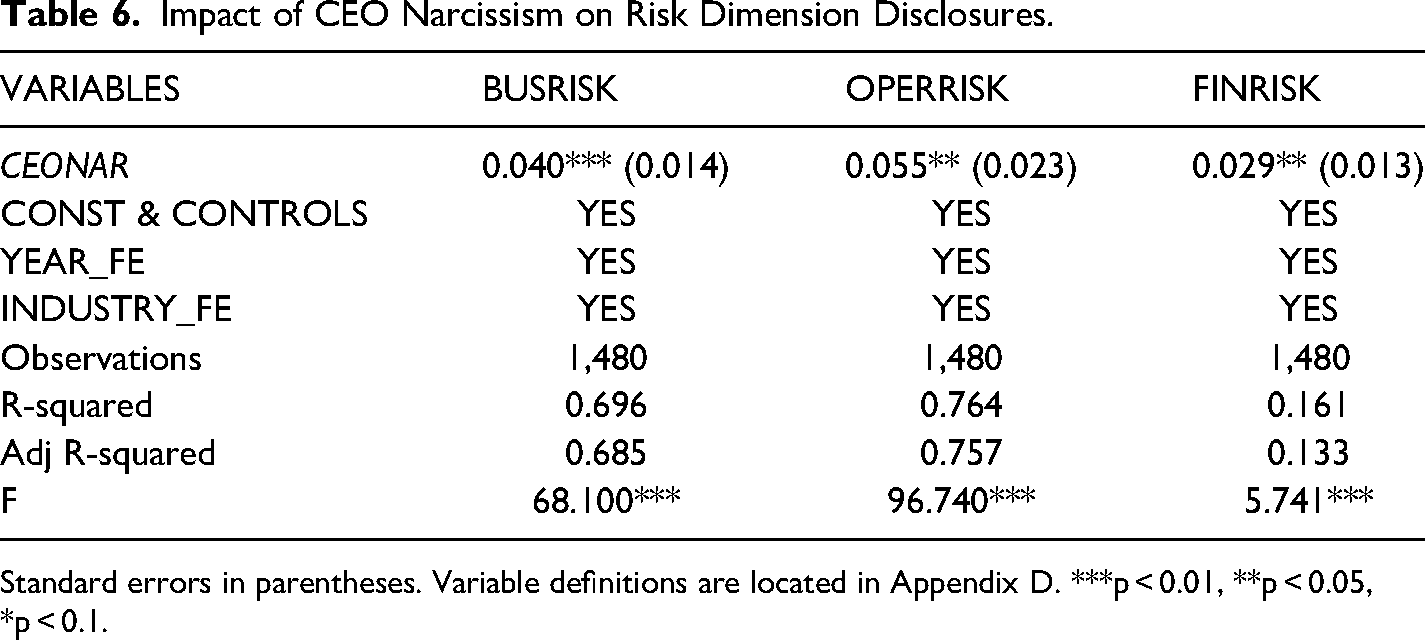

Following the framework established by Lajili et al. (2024), we have divided the risk disclosure variable into three subcategories: business risk (BUSRISK), operational risk (OPERRISK), and financial risk (FINRISK). This disaggregation allows us to examine how CEO narcissism influences each specific area of risk disclosure, providing a nuanced understanding of the relationship between executive traits and corporate transparency.

CEO narcissism might be expected to influence these categories differently based on the CEO's personal inclination towards various aspects of the business. Narcissistic CEOs, who are often characterized by a grandiose sense of self-importance and a preference for being admired (Rijsenbilt & Commandeur, 2013), may be more inclined to disclose risks that they believe can be managed or mitigated under their leadership, thereby enhancing their image as competent and proactive leaders (Cragun et al., 2020; Martínez-Ferrero et al., 2024). In particular, business risk disclosures might be influenced as narcissistic CEOs could prefer to highlight risks where their direct actions and decisions have mitigated potential threats (Buyl et al., 2019). Operational risk disclosures could be detailed to demonstrate the CEO's involvement in and control over the daily operational efficiencies and innovations (Buchholz et al., 2018; Elzahar & Hussainey, 2012). Financial risk disclosures might be selectively disclosed to portray financial prudence and strategic foresight, supporting the CEO's self-framed narrative of financial stewardship (Bajo et al., 2022).

Table 6 presents the results of the regression analysis on how CEO narcissism impacts these specific risk disclosures. The results indicate that CEO narcissism has a significant positive impact on business risk disclosures (coefficient = 0.040, p < 0.01), operational risk disclosures (coefficient = 0.055, p < 0.05), and financial risk disclosures (coefficient = 0.029, p < 0.05). These findings suggest that higher levels of CEO narcissism are associated with more extensive disclosures across all three risk categories. The results are generally consistent with the main findings, reaffirming that CEO narcissism contributes meaningfully to the extent of risk disclosures made in corporate communications. This positive relationship across all categories aligns with the notion that more narcissistic CEOs tend to use risk disclosures as a strategic tool to enhance their personal image and the perception of their effectiveness as leaders.

Impact of CEO Narcissism on Risk Dimension Disclosures.

Standard errors in parentheses. Variable definitions are located in Appendix D. ***p < 0.01, **p < 0.05, *p < 0.1.

Enhancing Causal Inference in CEO Narcissism and Risk Disclosure Analysis

In our pursuit of a robust analysis, we employed advanced statistical methods to address potential biases and affirm the reliability of our findings regarding the impact of CEO narcissism on risk disclosures. These methods ensure that our results are not merely artifacts of model specification or sample selection but reflects genuine relationships within the data. To strengthen our confidence in the causal relationship between CEO narcissism and risk disclosures, we incorporate firm fixed effects, apply entropy balancing, and focus on periods of CEO transitions in our analysis. Each approach serves to control for unobserved heterogeneity, ensuring that the observed effects are attributable to variations in CEO narcissism and not to other confounding factors.

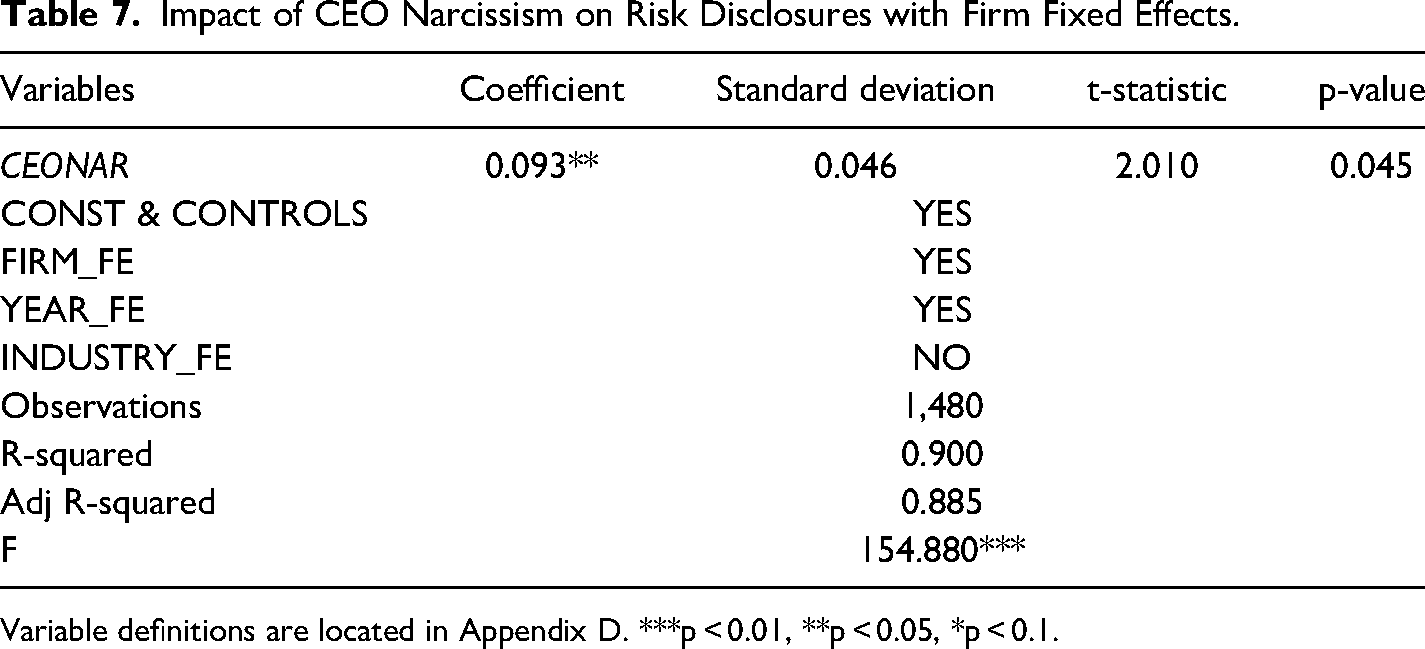

Firm Fixed Effects Analysis

This approach controls for all time-invariant characteristics of firms (Davies et al., 2008), allowing us to isolate the effect of CEO narcissism from other static traits that could influence disclosure practices. By including firm fixed effects, we aim to capture the true impact of CEO personality on disclosure behaviors within the same firm over time. Table 7 delineates the regression results. The coefficient for CEO narcissism stands at 0.093, marked significant at the 5% level (p-value = 0.045). This finding indicates that CEOs with higher narcissism levels are associated with an increase in risk disclosure. This analysis reveals that CEO narcissism significantly influences how firms communicate risks, suggesting that personality traits of corporate leaders can drive transparency levels in financial reporting.

Impact of CEO Narcissism on Risk Disclosures with Firm Fixed Effects.

Variable definitions are located in Appendix D. ***p < 0.01, **p < 0.05, *p < 0.1.

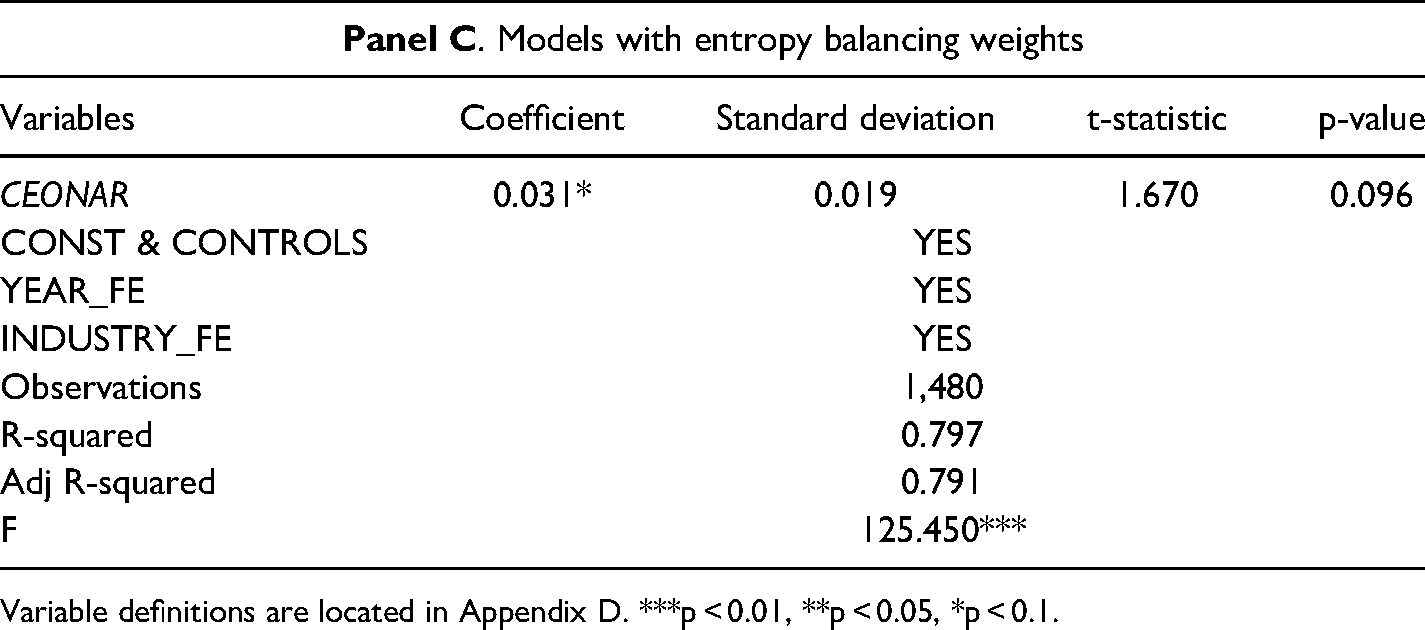

Entropy Balancing

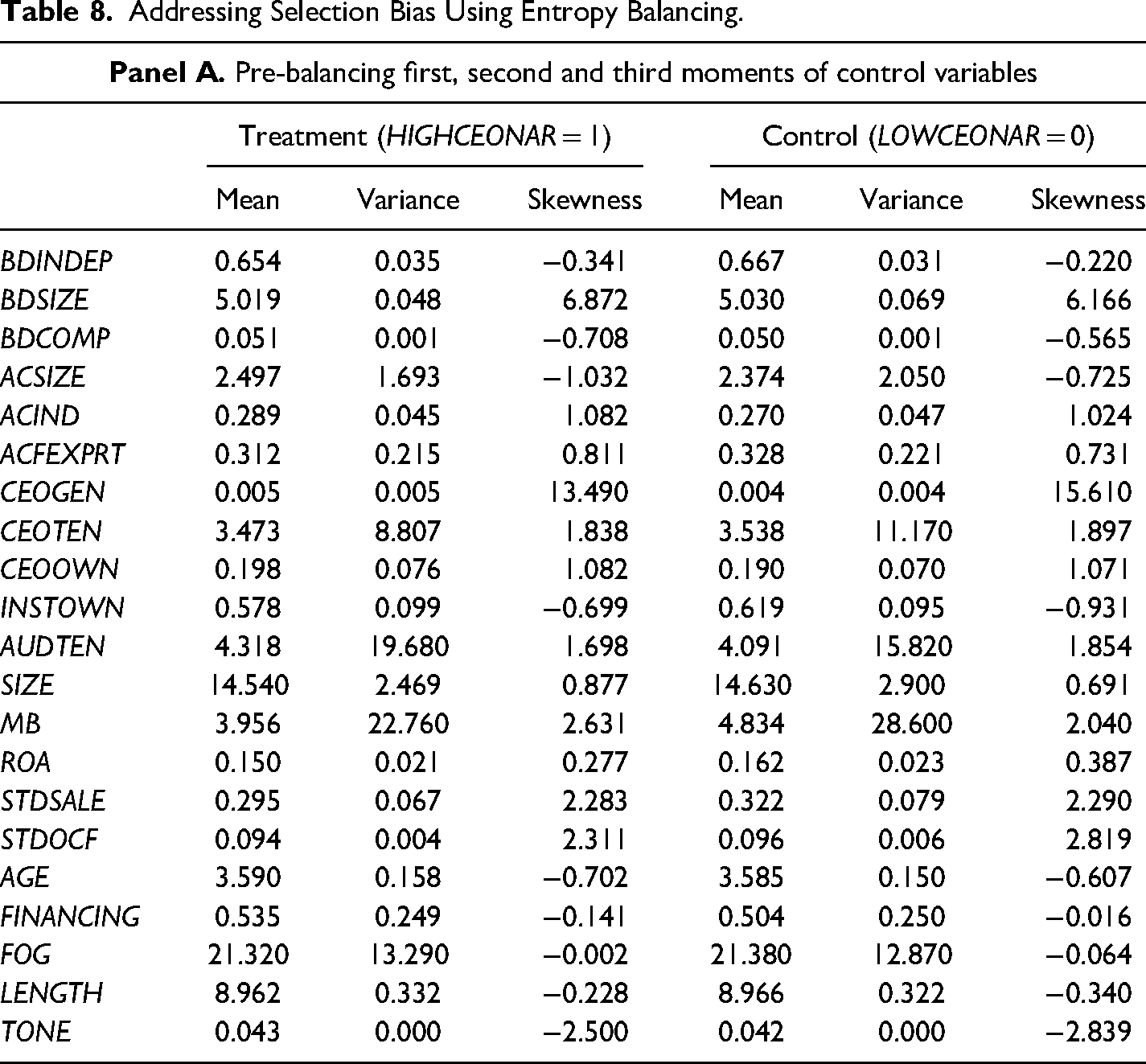

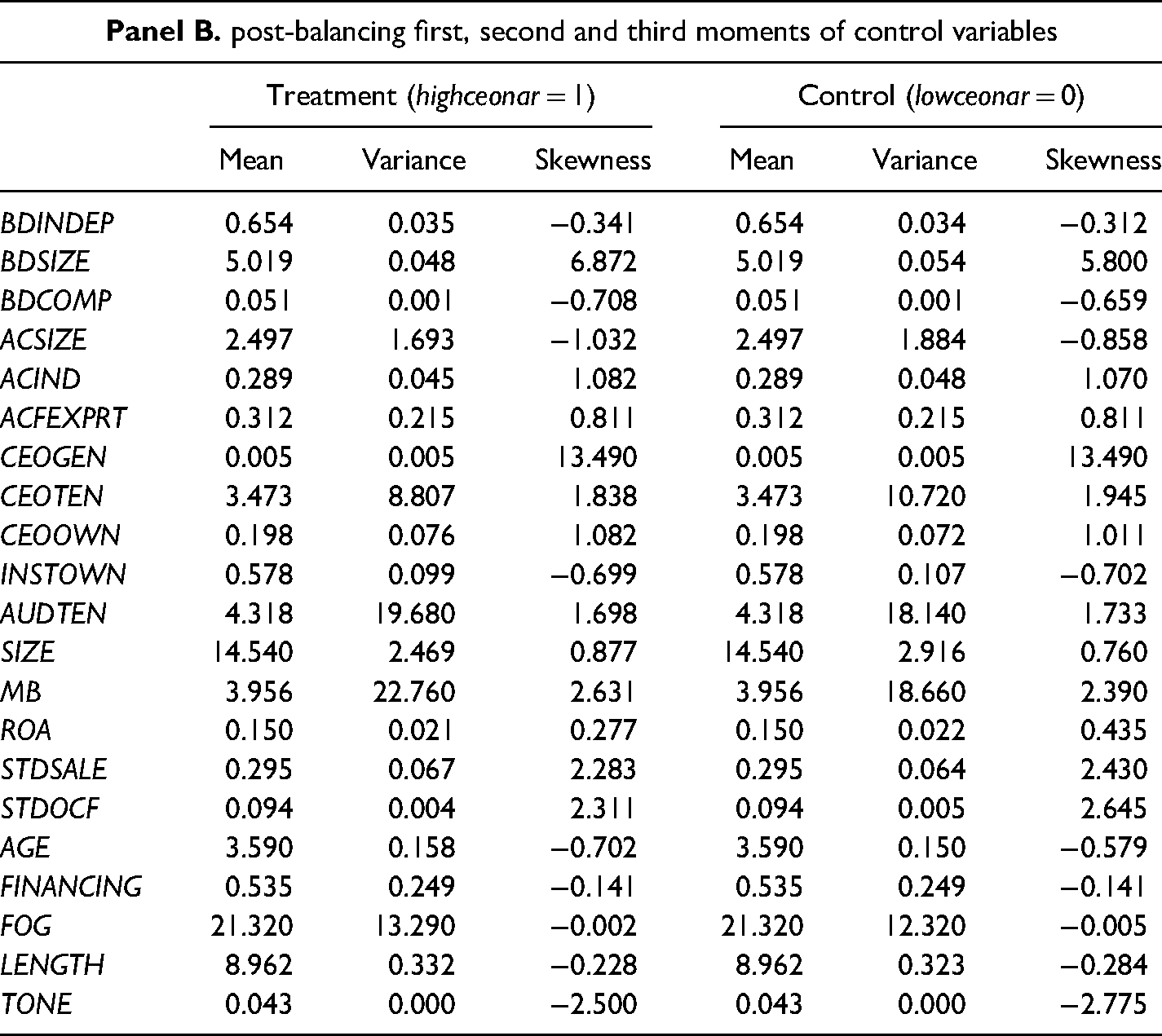

Entropy balancing adjusts the sample to create a synthetic control group that mirrors the treatment group in terms of key covariates (Hainmueller, 2012). Table 8 showcases the efficacy of entropy balancing in addressing selection bias for the study of the impact of CEO narcissism on risk disclosures. This method ensures that the treatment (HIGHCEONAR = 1) and control (LOWCEONAR = 0) groups are comparable across all measured covariates before the analysis, enhancing the causal interpretation of the results.

Addressing Selection Bias Using Entropy Balancing.

Variable definitions are located in Appendix D. ***p < 0.01, **p < 0.05, *p < 0.1.

Before applying entropy balancing, there were slight differences between the treatment and control groups across several control variables such as board independence (BDINDEP), board size (BDSIZE), and other governance and firm characteristics. These differences are shown in terms of means, variances, and skewness, which can affect the outcomes of the analysis if left unaddressed. After entropy balancing, the first, second, and third moments (mean, variance, skewness) of all control variables were aligned between the treatment and control groups, indicating successful balancing. This alignment suggests that any subsequent analysis on the impact of CEO narcissism can be more confidently attributed to the effects of CEO traits rather than confounding factors.

The model with entropy balancing weights presents a coefficient for CEONAR of 0.031, significant at the 10% level (p-value = 0.096). This result indicates a modest but statistically significant impact of CEO narcissism on risk disclosures when accounting for potential selection biases. This analysis illustrates the importance of controlling for selection bias in observational studies, particularly when exploring the effects of leadership traits like narcissism on organizational outcomes. By successfully balancing the covariates between groups, the study minimizes the risk of spurious associations and strengthens the credibility of the findings that higher levels of CEO narcissism indeed lead to more extensive risk disclosures.

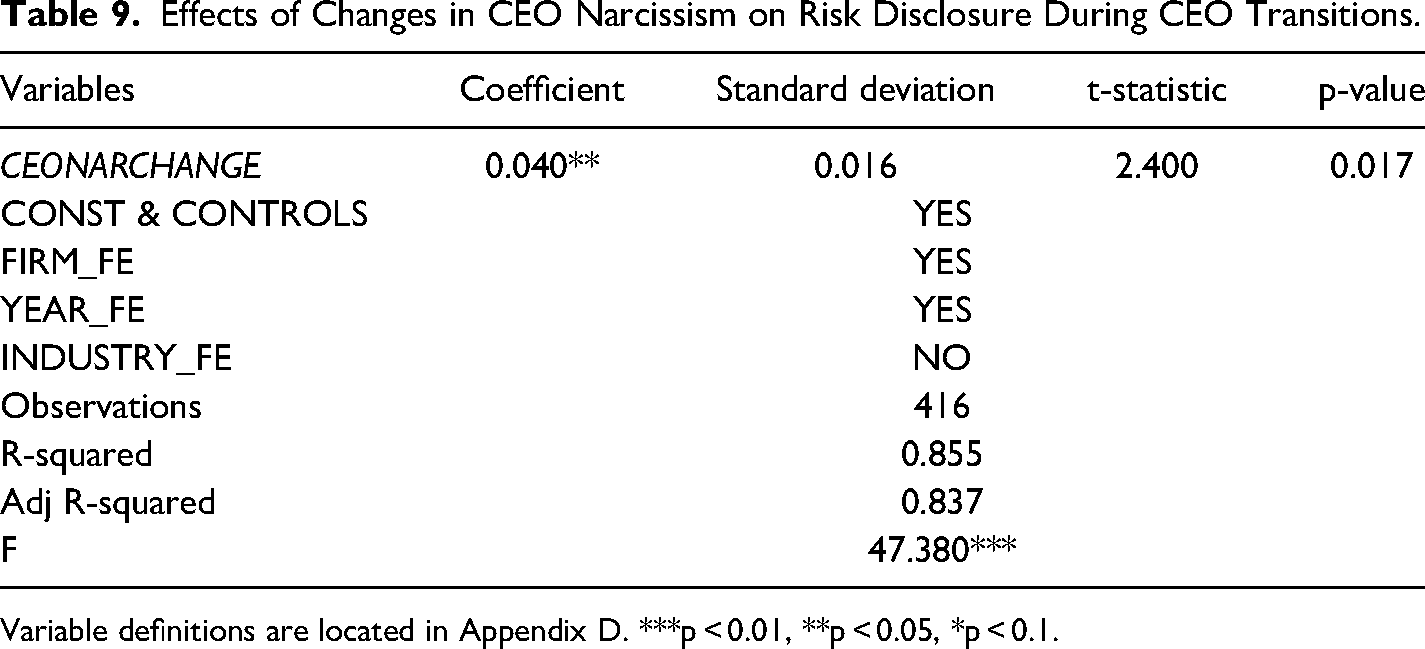

Impact of CEO Leadership Transitions: An Analysis of CEO Tenure and Narcissism Changes

In this section, we focus on a nuanced exploration of how transitions in leadership, particularly changes in CEO narcissism associated with CEO tenure changes, influence the extent and nature of risk disclosures. Acknowledging the complexity of isolating effects directly associated with changes in leadership traits, we employ a fixed-effects regression model that controls for firm-specific and year-specific variations. Our model is specifically designed to assess the impacts of changes in CEO narcissism that coincide with CEO transitions.

We first generated a CEOCHANGE variable by tracking resets in CEO tenure, indicative of a new CEO appointment. Corresponding to each CEO change, we calculated the CEONARCHANGE variable, which measures the change in narcissism based on the signature size from the year before to the year of the CEO change. This involved creating a lagged narcissism variable and subtracting it from the current year's narcissism score only in years with a CEO change. Given our focus on the impact of CEO changes, we reduced our dataset from 1,480 observations to 416, retaining only those observations where a CEO change occurred. This was essential to isolate the effects of leadership transitions on risk disclosure practices. 4

As presented in Table 9, the coefficient for CEONARCHANGE is 0.040 (p = 0.017), indicating a statistically significant positive impact of changes in CEO narcissism on risk disclosure practices. The results, controlled for firm and year fixed effects, showcase robustness against unobserved heterogeneity and potential omitted variable bias. The findings suggest that shifts in narcissism traits due to CEO changes have a tangible effect on how firms communicate risks. The increase in narcissism following a CEO change could lead to more extensive or pronounced risk disclosures, potentially reflecting the new leader's desire to imprint their strategic vision or manage stakeholder perceptions proactively (Marquez-Illescas et al., 2019). This result contributes to the ongoing debate on the influence of executive personality traits on corporate communication strategies, emphasizing the critical role of leadership dynamics in shaping organizational transparency. It also resonates with theoretical perspectives that posit a link between leadership changes and shifts in corporate policies, particularly in environments where executive visibility is crucial.

Effects of Changes in CEO Narcissism on Risk Disclosure During CEO Transitions.

Variable definitions are located in Appendix D. ***p < 0.01, **p < 0.05, *p < 0.1.

Moderating Effects of Board Composition

In our comprehensive investigation into how corporate governance frameworks can shape the narrative around risk disclosures, we specifically focused on the structure and composition of boards due to their potential to significantly influence CEO behaviors, particularly in terms of narcissism. The premise of our study is grounded in the hypothesis that the collective attributes of the board—such as the degree of independence (BDINDEP), the total number of directors (BDSIZE), and the percentage of female directors (BDCOMP)—can act as critical levers in moderating the impact of CEO narcissism on the transparency and efficacy of risk communication. By employing Principal Component Analysis (PCA), we synthesized these various dimensions of board composition into a singular composite measure (BDCOMPST). This methodological approach allowed us to capture the essence of board dynamics more holistically, assessing the combined impact of these governance traits rather than examining them in isolation.

The untabulated significant interaction found between CEO narcissism and our board composition composite, indicated by a coefficient of 0.505 (p = 0.005), illustrates a clear moderating role of the board. This finding suggests that as the integrated characteristics of the board are strengthened, they enhance the potential for narcissistic tendencies of CEOs to manifest in the risk disclosure practices 5 . This amplification could be attributed to the increased confidence narcissistic CEOs might feel when they perceive the board's composition as supportive or less likely to challenge their authority. Consequently, this underscores the importance of a nuanced understanding of board characteristics, which are pivotal in navigating the complex interplay between executive traits and corporate governance outcomes.

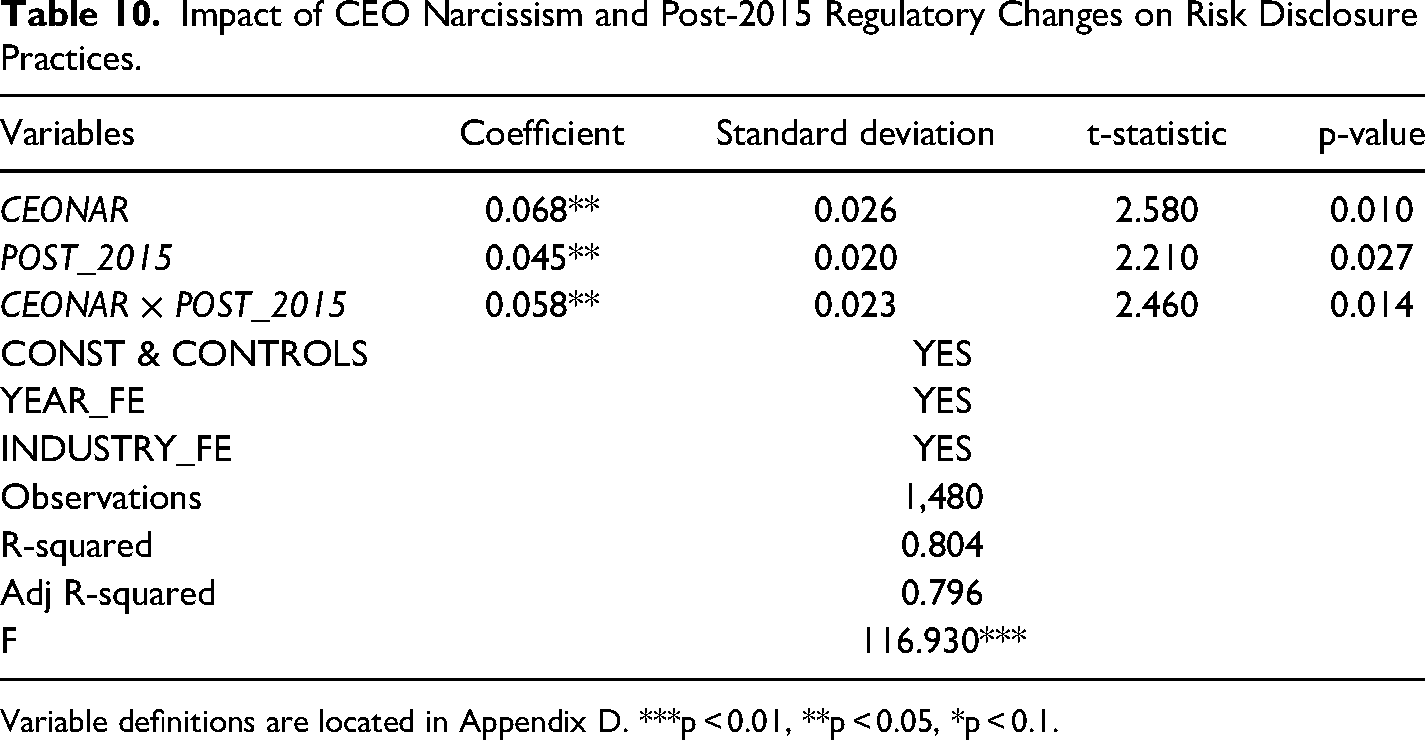

The Moderating Effect of Enhanced Regulatory Scrutiny Post-2015

Following the 2015 revision of risk disclosure regulations in Iran, there has been an increased emphasis on transparency and accountability in corporate governance. This regulatory shift provides a unique backdrop to explore how narcissistic CEOs may have adjusted their risk disclosure practices in response to these changes. Previous studies suggest that narcissistic CEOs are more likely to engage in behaviors that enhance their personal image and visibility (Amernic & Craig, 2007; Lovelace et al., 2018). With the regulatory changes post-2015 that demand more detailed and frequent risk disclosures (Draca et al., 2019; Salehi et al., 2018), it is plausible that the visibility of corporate governance practices would become a more significant aspect of CEO strategy. Rajabalizadeh (2025) and Blue et al. (2024) argue that in volatile economies like Iran, intensified scrutiny could push narcissistic CEOs to further amplify risk disclosures to align with heightened regulatory and public expectations, potentially to enhance the government's image or their own.

To test this hypothesis, we introduced an interaction term between CEO narcissism and a post-2015 dummy variable (CEONAR × POST_2015) into our regression model. The results, as presented in Table 10, indicate significant findings. The coefficient for CEO narcissism (CEONAR) is positive and statistically significant (Coefficient = 0.068, p-value = 0.010), suggesting that higher levels of CEO narcissism are associated with more extensive risk disclosures. The POST_2015 variable is also significant (Coefficient = 0.045, p-value = 0.027), indicating an overall increase in risk disclosures following the regulatory changes. More importantly, the interaction term (CEONAR × POST_2015) is positively signed and significant (Coefficient = 0.058, p-value = 0.014), supporting the hypothesis that the effect of CEO narcissism on risk disclosure has intensified in the post-2015 period.

Impact of CEO Narcissism and Post-2015 Regulatory Changes on Risk Disclosure Practices.

Variable definitions are located in Appendix D. ***p < 0.01, **p < 0.05, *p < 0.1.

Our analysis demonstrates how CEO narcissistic behavior adapts under more stringent regulatory frameworks post-2015, showing significant changes in risk disclosure practices. The findings indicate that even deeply ingrained personality traits such as narcissism can be shaped by regulatory environments. This interplay adds a critical dimension to our understanding of leadership in corporate governance and provides empirical evidence on how narcissistic CEOs might modify their strategies to maintain or enhance their public image in response to regulatory demands. This insight is crucial for both academic and practical applications, helping to inform better corporate and regulatory policies.

Additional Risk Disclosure Measures

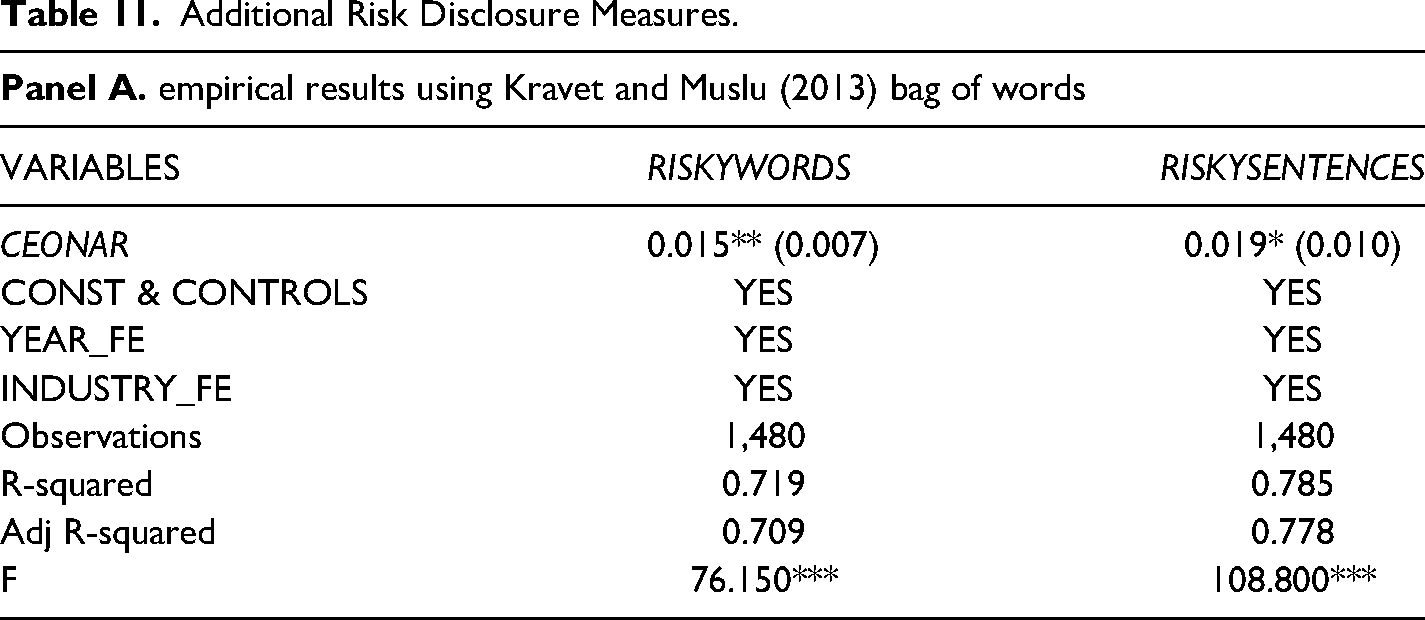

In this section of the analysis, we extend our examination of risk disclosures by incorporating the methodology developed by Kravet and Muslu (2013). This approach enhances our understanding of the narrative risk information presented in the MD&A reports. As with the main independent variable section (4.2), we have tailored the Kravet and Muslu model to the Persian context, enabling a focused analysis of risk disclosures within Persian MD&A documents. Initially, we constructed a specialized bag-of-words model based on the framework provided by Kravet and Muslu (2013). This model was specifically adapted to the Persian language to effectively capture the nuances and expressions relevant to risk disclosures in the region. The adaptation process involved translating and culturally contextualizing the original bag of words to ensure that the terms are applicable and meaningful within the Persian corporate reporting environment.

In the analysis of risk disclosures within the MD&A documents, we employ two distinct measures derived from a specialized bag-of-words model detailed in Appendix B. The first measure, direct mention of risks (RISKYWORDS), quantifies the occurrences of words that directly refer to risks or riskiness. This approach captures the explicit references to risk and provides a quantitative measure of the frequency with which these disclosures are stated in the documents. For statistical analysis, we used the natural logarithm of RISKYWORDS to stabilize variance and normalize the distribution. The second measure, sentence-level risk identification (RISKYSENTENCES), refines the analysis by identifying sentences that contain any risk-related keywords from the list provided in Appendix B. This measure classifies a sentence as pertaining to risk based on these specific lexical choices, offering a more nuanced understanding of how risk is communicated in corporate narratives. We similarly applied the natural logarithm to RISKYSENTENCES for consistency in analytical treatment. These methods together enhance our ability to assess the depth and nature of risk disclosures in corporate reporting. 6

The regression results, displayed in Panel A of Table 11, reveal significant associations between CEO narcissisms and both measures of risk disclosure. Specifically, CEONAR positively correlates with RISKYWORDS, with a coefficient of 0.015, significant at the 5% level (p < 0.05). This suggests that higher levels of CEO narcissism are associated with an increased usage of explicit risk terms in the documents. Similarly, for RISKYSENTENCES, the coefficient is 0.019, significant at the 10% level (p < 0.10), indicating that more narcissistic CEOs tend to include a higher number of sentences containing risk-related keywords. These findings underscore the influence of CEO narcissism on the transparency and depth of risk disclosures in MD&A sections.

Additional Risk Disclosure Measures.

Standard errors in parentheses. Variable definitions are located in Appendix D. ***p < 0.01, **p < 0.05, *p < 0.1.

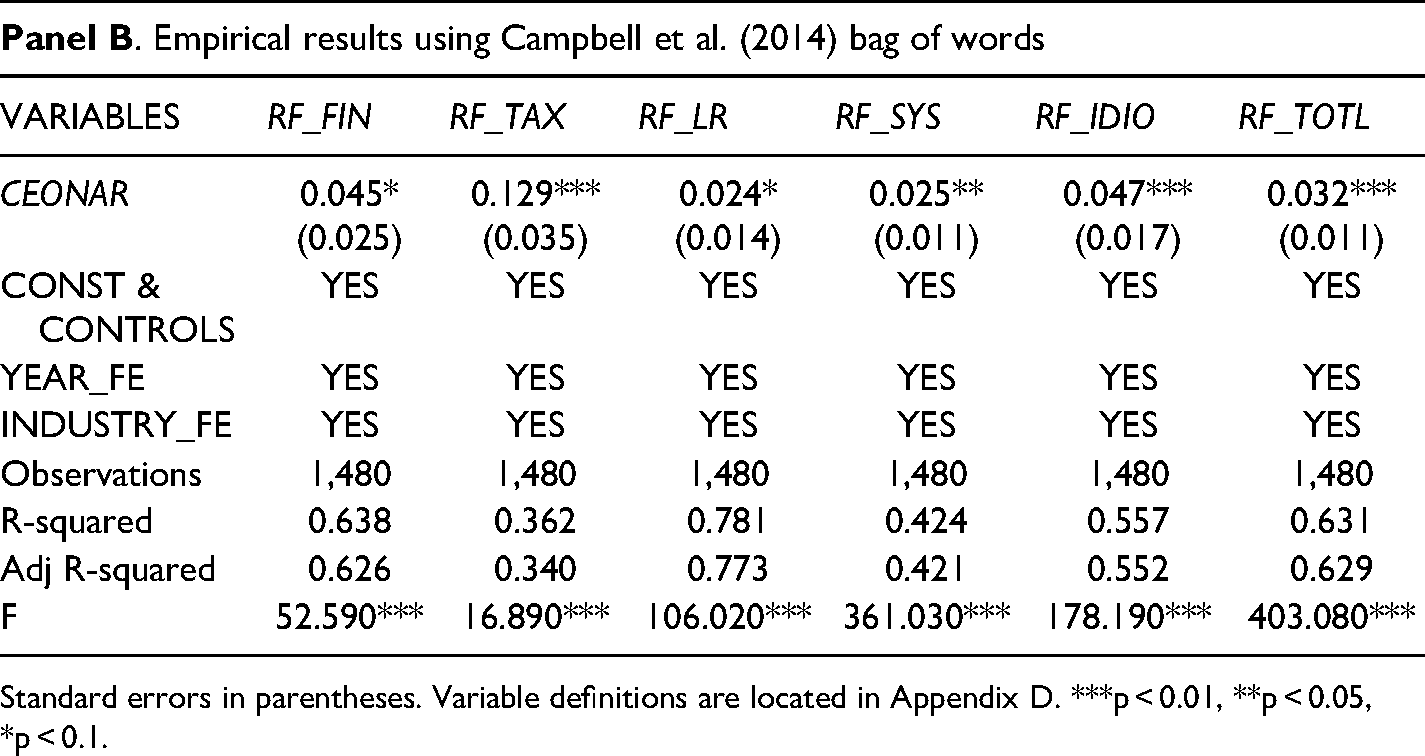

In continuation of our analysis on risk disclosures, we adopted the Campbell et al. (2014) methodology to further examine the narrative risk information presented in the MD&A reports of publicly listed Iranian companies. This methodology differentiates various types of risks into distinct dimensions, allowing for a more granular analysis of risk disclosures. For this approach, we adapted the original Campbell et al. (2014) model to the Persian context, incorporating culturally relevant adaptations and translations of risk-related terms. 7 This customization included the development of a specialized bag-of-words model, detailed in Appendix C, which categorizes risk into five main dimensions: financial risk (RF_FIN), tax risk (RF_TAX), litigation risk (RF_LR), other-systematic risk (RF_SYS), and other-idiosyncratic risk (RF_IDIO). Additionally, we introduced a total measure (RF_TOTL) that aggregates all the keywords from these categories to provide a comprehensive measure of risk disclosure. 8

The regression results from Panel B of Table 11 illustrate significant associations between CEO narcissism and various measures of risk disclosure, revealing a nuanced pattern of influence across different risk dimensions. Notably, CEONAR positively correlates with financial risk disclosures (RF_FIN), evidenced by a coefficient of 0.045, significant at the 10% level. 9 This finding is complemented by a strong positive relationship with tax risk disclosures (RF_TAX), where the coefficient is 0.129, significant at the 1% level. Additionally, litigation risk disclosures (RF_LR) show a significant impact with a coefficient of 0.024, also significant at the 10% level. Systematic risk disclosures (RF_SYS) are similarly associated, with a coefficient of 0.025, significant at the 5% level, while idiosyncratic risk disclosures (RF_IDIO) display a robust relationship with a coefficient of 0.047, significant at the 1% level. Lastly, the overall impact on total risk disclosures (RF_TOTL) is significant, with a coefficient of 0.032, significant at the 1% level. This detailed exploration of risk disclosures using the Campbell et al. (2014) approach provides a comprehensive understanding of how different types of risks are disclosed in corporate narratives and underscores the significant influence of CEO narcissism on these disclosures. The results highlight the critical role of CEO personality traits in shaping corporate communication strategies regarding risk, emphasizing the strategic use of narrative to manage public and investor perceptions.

Conclusion and Reflections

This study sheds light on the intricate link between CEO narcissism and risk disclosure within Iran's unique corporate governance framework. The findings reveal a strong positive correlation, indicating that narcissistic CEOs are likely to engage in extensive risk disclosure, driven by both self-promotion and a desire to increase visibility, consistent with Self-Promotion and Visibility Enhancement theories. Our use of advanced statistical methods such as firm fixed effects, entropy balancing, and propensity score matching lends strong support to the influence of narcissistic traits on corporate transparency. By examining these traits within Iran's specific governance context, this research enriches the understanding of how executive personalities can shape corporate disclosure strategies, adding depth to the global conversation on corporate governance and transparency in emerging markets.

Key insights from this research include the significant impact of CEO narcissism on the extent and nature of risk disclosures, suggesting that these CEOs use disclosures not merely to inform but to shape stakeholder perceptions and boost their own image. This finding prompts a reevaluation of the traditional negative perceptions associated with narcissistic CEOs, revealing the complexity of personality effects in corporate environments. It highlights the importance for corporate boards and regulators to include personality assessments in CEO evaluation and monitoring processes.

While this study offers valuable insights, it has limitations due to its methodology and scope. Using CEO signature size as a proxy for narcissism, although literature-supported, might not fully capture this complex trait, potentially overlooking aspects like interpersonal behavior and cognitive biases that could influence disclosure practices. Additionally, focusing solely on Iran's corporate environment might limit the generalizability of the findings, as the unique political, economic, and cultural factors in Iran may not be representative of other settings.