Abstract

The research article focuses on the impact of the COVID-19 pandemic that contributed to a surge in cable cord-cutting in mature as well as emerging markets such as India. The objective of this study was to provide a detailed understanding of the motivating forces behind consumers’ intention to cut the cord of television cables. This research article has tried to examine the impact of four factors, namely, (a) perceived advantage, (b) perceived value, (c) perceived compatibility and (d) perceived substitutability on the intention of the consumers’ cord-cutting. The research data were collected from 186 Subscription Video on Demand subscribers by circulating an online questionnaire and administering Amos 23.0 for analysing the data. The data analysis result revealed that consumers’ intention for cord-cutting was influenced by perceived compatibility, perceived value, perceived advantage and perceived substitutability. This research study intends to provide direction to pay TV subscription providers to understand the factors that influence cord-cutting and to motivate consumers to retain a minimal subscription leading to cord-shaving.

Keywords

Introduction

Over time, media and entertainment have undergone a paradigm shift. Entertainment in the past usually meant a handful of dull television channels or listening to limited radio stations or reading the news on various print media (Tefertiller, 2018).

Different forms of media have evolved based on the dynamic needs of the consumer. Evolving patterns of public consumption of entertainment, coupled with the combination of new digital distribution methods continue to challenge traditional Media and Entertainment (M&E) business models (Snider, 2018). Such shifts in consumption patterns have also marked the beginning of a dramatic transformation that is constantly reshaping the entire M&E ecosystem. Considering the tough level of competition in the M&E landscape, M&E companies are keeping continuous track of viewer behaviour patterns to sustain viewership (Massad, 2018). Over-the-Top (OTT) platforms have generated an opportunity and confabbed with consumers through trends, micro-targeting them with customized offerings. This indeed has leveraged an explosion in the media world by creating challenges and developing a level playing environment for OTT content providers (Gardener, 2020).

One of the biggest factors behind this surge is the rapid advancement in technology. Fuelled by the sub-cultural divide that has also been created by the same technology, the neo-empowered viewer constantly demands enriched content (Sundar & Limperos, 2013). Hence, providers of entertainment content need to constantly rethink and redesign their broadcast content to suit the taste of their consumers. Facilitated by the unprecedented growth in media consumption, suppliers must deal with a double-edged challenge wherein they need to strike an equilibrium between risks and returns (Snider, 2018).

As a consequence of the shift in the perception of entertainment for modern-day consumers which has been largely affected by varied factors, especially digitization (EY & FICCI, 2019),this transformation has led to ‘cord-cutting’, which refers to the situation where consumers cancel their traditional pay TV subscriptions and opt instead for web-based streaming content (Prince & Greenstein, 2017). The cord-cutting situation has led to this type of indulgence in web-based content. To evoke a picture of breaking the link between access to conventional cable television and the customer, the term cord-cutting is metaphorically used. The facilitators of this paradigm shift in preference include the geographical penetration of telecom operators, data plan quality and affordability, the existence of web-based content, web-enabled televisions, common streaming devices such as Apple TV, Google Chromecast and Amazon Fire Stick, and web streaming services such as Netflix and Amazon Prime subscription pricing (Kim, 2016). These variables have created a viable alternative for consumers who satiate their entertainment needs by gradually progressing towards cable cord-cutting.

Nearly all the popular streaming platforms are accessible in the form of apps that can be easily operated on smartphones and watched at one’s convenience (Kim et al., 2021). In the initial stages, it is perhaps relaxation that is the prime influencer for OTT subscription but the real motivation for the continuation of the subscription is the entertainment factor. Consumers renew their subscription based on the entertainment provided on the OTT platform. This finding is in line with the research carried out by Tefertiller and Sheehan (2020) on the adoption of OTT based on entertainment factors and cord-cutting.

By providing a forum that allows individual viewership, Subscription Video on Demand (SVOD) services have created tremendous disruption in the content consumption space. In terms of personal entertainment, they have been catalytic in offering the luxury of viewing at the time, location and interface of one’s convenience (Doyle, 2014). SVOD gives the viewer the option of watching what they want at any time of the day, as opposed to television, where programmes operate according to a timetable. The massive rise in the popularity of SVOD platforms has had a major impact on the growth and survival of linear media companies such as cinema and broadcast television in many developed markets. A study by The Nielsen Company (2014) has suggested that 40% of Generation Z (ages 15–20), 38% of Millennials (ages 21–34) and 30% of Generation X (ages 35–49) are potential customers who are preparing to cut the cable on their cable subscriptions.

As per analysts, the underlying factors for the drop in web-streaming cable subscriptions include an increase in subscription rates for cable television combined with a growing number of streaming services. Such subscription platforms are also serving as replacements for those perceived as entertainment alternatives to conventional viewing (The Nielsen Company, 2014). Cord-cutting, which reflects a transition from one medium to another, demands that media replacement be viewed as a method of replacement rather than a complementary mechanism. In such a case, instead of supplanting a previous medium, a new medium is introduced to the daily media diet of a customer (Van den Bulck & Donders, 2014). As per the PWC (PwC, 2019) report, the tremendous growth of SVOD has been largely due to certain features in such platforms that define effective consumer-first companies and sectors. These platforms use advanced audience analytics techniques which allow for the creation of more personalized content and suggestions to optimize the experience of viewers (Chulkov & Nizovtsev, 2015). It makes it easier for the service provider to find content and remain on the service for longer, providing new packaging formats and an array of payment models.

From opposition to new technology to their mass adoption, digital infrastructure has grown. In the digital environment, performance depends on different factors such as timeliness of marketing consumer experience and the desire to continually evolve and change according to market trends (Tse, 2016). SVOD systems are expected to define and build digital solutions that include strategies for anticipating, influencing and reacting to consumer actions.

There is, however, a lack of clarity regarding the reasons why subscription platforms have become entertainment alternatives (Tse, 2016). This study aims to address the gap by providing an overview of the stupendous growth of SVOD while also explaining the basic driving forces behind the cord-cutting intention of consumers. Based on the Media Substitution Theory, this research aims to propose key strategies for promoting cord-shaving.

Research Objectives

To provide an overview of the changing media landscape in India

To discuss the possible drivers responsible for the cable cord-cutting intention among consumers

To develop strategies for pay TV sustainability in the form of cord-shaving

India’s Online Video Landscape

The online video industry of India is potentially one of the world’s most exciting markets and companies. As per the PWC report (PwC, 2019), India is expected to have more than 500 million online video subscribers by the financial year 2023, making it the second-largest market in the world, next only to China. Video traffic has grown from 1.5 EB per month in 2017, with video use accounting for 77% of all internet traffic until 2022.

With the mounting penetration of the internet and smart-connected devices, the global market size of OTT platforms has reached USD 101.42 billion in 2020 and it is anticipated to reach USD 223.07 billion by 2026, recording a CAGR of 13.87% (Mordor Intelligence, 2020). It is estimated that the OTT market for India is expected to grow by 45% by the end of fiscal 2023 (Gupta & Singharia, 2021).

The growing usage may be attributed to the available content choices, the scope of the interactivity with video and various sightseeing possibilities. As India witnesses a shift in the concept of mass entertainment, films and sports are probably ‘drivers’ while digital original series will probably become one of the most significant tools to describe this cultural shift. The scope for an ‘a-la-carte’ model of media consumption shall be facilitated by several drivers, including the ISP/network affiliate, original equipment manufacturer (OEMs), broadcasters, movie studios and tech-aggregator channels, all of which play a key role in the creation of this public universe. Analysts estimate India to remain a difficult market as far as diversity of viewers based on language, content genres, access and several million user cohorts is concerned. In Tier 3 markets in India, consumers are more likely to experience increased internet usage for the first time with online video, thus making it a pivotal tool to achieve the vision of a real ‘Digital India’ (EY & FICCI, 2019).

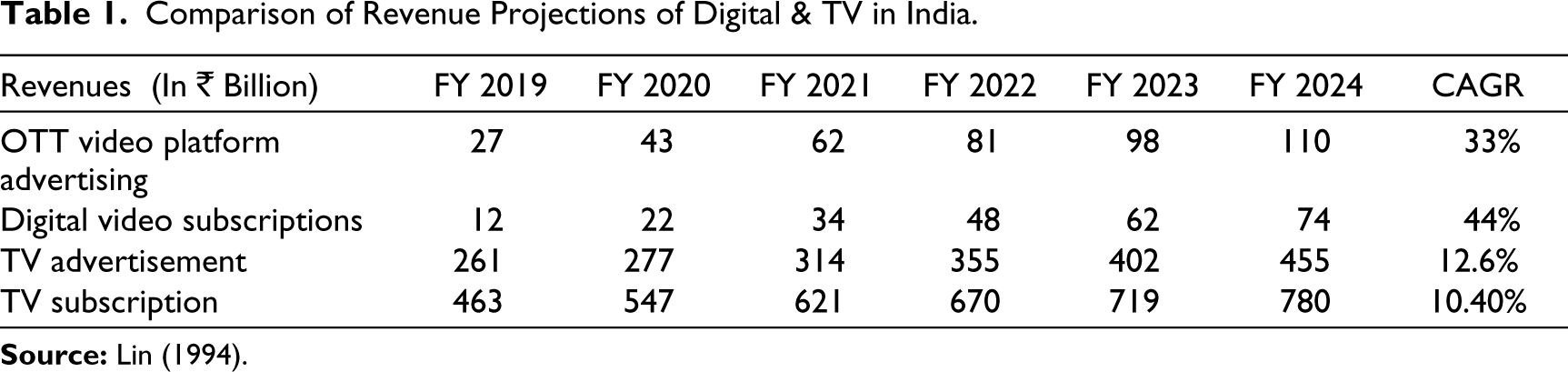

According to KPMG India Analysis (Lin, 1994), the revenues through video platform advertising and digital video subscriptions are growing at a vast pace. As seen in Table 1, revenues are estimated to reach ₹110 billion by the end of 2024. The number of cord-cutters is on the verge of a serious escalation in the coming 5 years. Although the Indian OTT market is at a nascent stage, it has already started entering the growth phase of its life cycle. However, the growth is subject to Foreign Direct Investment (FDI) policies, government subsidies, Telecom Regulatory Authority of India regulations, increased internet penetration among other factors.

Comparison of Revenue Projections of Digital & TV in India.

According to a report (ASSOCHAM-PwC, 2017), despite the disruption caused by cord-cutting, television is still the largest sub-segment in the Indian media and entertainment industry and will continue to grow in the years to come. The biggest challenge for OTT service providers would be market penetration in rural India since television is the most popular source of entertainment there. As seen in the figure, the revenues from TV advertisements are estimated to reach ₹455 billion, overtaking those in the UK, Germany, France and Brazil. However, the increasing phenomena of cord-cutting and the quality of content provided by the OTT platforms are posing a huge threat to pay TV subscribers. As a result, pay TV companies are targeting rural viewers by providing regional content which is appealing to the intended target segment.

Review of Literature

Media Substitution Theory

The assumptions of the Media Substitution Theory are based on the premise that individuals tend to examine, rank and select the entertainment medium that most suits their preference (Case & Given, 2016). The customary viewers have been primarily affected by the continuous spurt in technological innovation in the M&E industry, initially facilitated by the launch of cable TV which altered the viewers’ association with traditional TV viewership (Krugman, 1985; Steiner & Xu, 2018). The viewers’ perception and usage of traditional media, such as theatre and television, were further transformed by the introduction of video cassette recorders (VCRs) (Henke & Donohue, 1989). According to past studies, the diffusion of innovation is successful when the newer one disseminates the content in a more strategically profitable manner as compared to the old one (Lin, 2008). In other words, the elements facilitating media substitution encompass enhanced technical capabilities and value-proposition (Lin, 2004).

New Technology Leading to Gratification

The effect of innovative technologies leading towards gratification has been discussed by several researchers. In their attempt to explore the various kinds of motivation behind new media adoption and usage, a few authors (Krcmar & Strizhakova, 2009) are of the view as far as the use of media is concerned, that the motivation varies depending on the nature of the media. They also emphasize the fact that developing typologies without integration does not adequately advance use and gratification as a meaningful approach. Upon subsequent scrutiny of extensive literature based on gratification typologies and their coherence, it is suggested that typologies be clubbed to form three to four broad groups (Sundet, 2016). Incorporating typologies is emerging as an essential approach in applying uses and gratifications to new communication technologies. A significant part of past research (Chen, 2011) reveals that a large amount of conceptual overlap has occurred with studies from the past. However, the emergence of distinct gratifications are also prevalent. For instance, in a study on Facebook, gratifications explored those items of the questionnaire that relate to habit, pastime, relaxation and entertainment, loaded together (Papacharissi & Mendelson, 2007). This suggests that the configuration of gratifications is constantly changing for newer forms of media. However, research (Sundar, 2008) also indicates that technological affordances are also perceptually and mentally critical. They suggest that researchers focusing on uses and gratifications should avoid viewing media gratifications as a factor based solely on one’s psyche. This will consequentially limit their understanding and appeal of new media (Ghalawat et al., 2021).

Evolution of Web-Streaming Services

Coupled with other web-based streaming services, platforms such as Netflix and Amazon Prime have caused a paradigm shift in the media consumption landscape by not only providing content, but also additional unique content delivered by a variety of gadgets (Ellingsen, 2014). In that capacity, these OTT service providers are positioning themselves to compete with conventional TV subscriptions. As a result of such fluctuations, media conglomerates have lost control over their system of distribution, thereby suffering substantial losses (Perren, 2010). In their continuous effort towards an improved lifestyle and promising future growth, consumers have resorted to cord-cutting and completely redefined their media viewing options (Crawford, 2015). Hence, to have a better understanding of the media substitution process, it is pivotal to study the media adoption process (Lin, 1994). Several researchers have also highlighted the rapid penetration and adoption of web streaming because numerous well-known web-streaming technologies were relatively new or non-existent at that point in time (Tefertiller, 2018). These individuals can be characterized as innovators and have been influential in facilitating the widespread adoption of OTT content (Rogers, 2003). Content creators of the OTT platforms need to produce more entertaining programmes by introducing structural changes in their content creation, performance, presentation and advertisement to attract more consumers and earn their loyalty (Yousaf et al., 2021).

Drivers of Cord-Cutting

The phenomenon of cord-cutting is not dependent merely on dissatisfaction and pricing. It could also be a result of the technological lifestyles of individuals. According to research based on Americans, conducted by The Nielsen Company (2016), on an average, each American owns four digital devices and the average U.S. consumer spends about 60 hours a week consuming content across these devices. As per previous research (Rizzo, 2014), increased speed of the internet, coupled with the multiple online programming services being offered, plays a major role. This has easily accommodated the escalating consumer demand for online services that work in coherence in delivering maximum value. As far as consumer demographics are concerned, the availability of high-quality and cost-effective technology is being appreciated, specifically by young consumers. A research study by Rizzo (2014) argues that it is not just the younger consumer that is making radical new purchase decisions. Between 2010 and 2011, there was a phenomenal rise in television ownership across households. However, by 2013, this number had dropped to a large extent. The study further indicates that the time spent on television viewing is now being redirected to mobile devices and related activities in which one is completely engaged with the devices. Recently, a few researchers have identified the motivation for the use of the vertical video-based service, Tik Tok.

Defining the Constructs

Cord-cut Intent

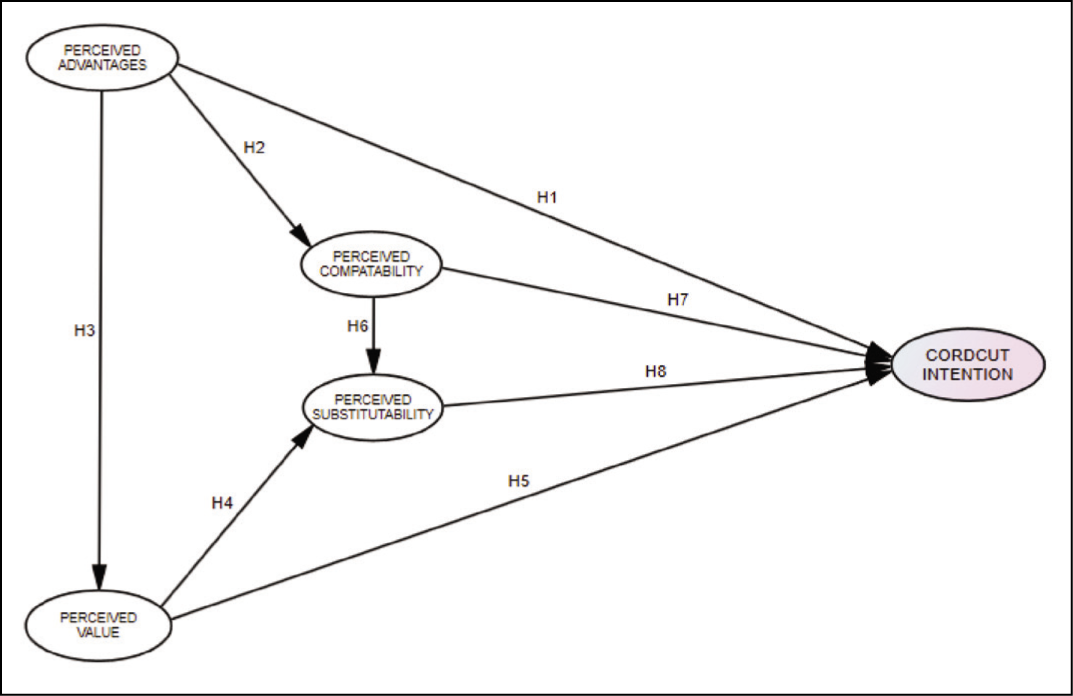

The intent to cut the cord on cable connections implies that consumer intends to end the cable subscription and switch to streaming via the web to access TV (Rizzo, 2014). The discernible advantage of web streaming was the best predictor of cutting the cord, the consumers’ general irritation with TV and ease of use of web streaming also influenced cord cutting. According to Rizzo (2014), the affordability of streaming web services best explains the intentions of consumers for cord cutting (Figure 1).

Proposed Research Model.

H1: Consumers’ intention to cut cords will be facilitated by the perceived advantages of SVOD.

H5: The consumers’ intention to cut the cord will be facilitated by the perceived value of SVOD.

H7: Consumers’ intention to cut the cord will be facilitated by the perceived compatibility of SVOD.

H8: Consumers’ intention to cut the cord will be facilitated by the perceived substitutability of SVOD.

Perceived Value

Perceived value has been found to have a profound impact on the adoption of newer means of entertainment. According to researchers (Rizzo, 2014), cost advantages and value may be evaluated as the most important and primary variable for home entertainment services. In this context, the author found that the perceived value can be divided into three dimensions, namely, symbolic value, utilitarian value and hedonic value. When cost-cutting comes into play, these three dimensions have a very important effect on the consumer’s decision to make the move from cable TV to SVOD (Lin, 2008).

H4: Perceived value of SVOD will significantly impact perceived substitutability.

Perceived Compatibility

The level at which television and innovation are perceived as being compatible and consistent with the present values, experiences from the past and needs of the new consumers’ aimed at considering the available options of web streaming services to cable TV, has shown that web streaming services are not seen as a feasible option by general viewers (Cha & Chan-Olmsted, 2012). This is because the present research has shown that streaming via the web or watching via the PC is quite different from conventional TV viewing.

H2: Consumers’ perceived compatibility will be significantly impacted by the perceived advantages of SVOD.

Perceived Advantages

According to researchers (Rogers, 2003), the perceived advantages of newer technology can be explained as the relative benefit it offers over traditional ones. It may be defined as ‘the extent to which individuals perceive an innovation to be better than the technology it supplants’. In his study, Cha (2013) was of the view that consumers perceiving online viewing to be comparatively more beneficial than conventional cable TV indicates that it is a strong predictor of online viewing and has a negative connection to conventional television viewing.

H3: Perceived advantages of SVOD will significantly impact its perceived value.

Perceived Substitutability

As the phenomenon of cord-cutting is skewed towards the Media Substitution Theory, the underlying factors propelling the behaviour are crucial. The factor of perceived substitutability will specifically play a key role (Snider, 2018). According to Cha (2013), in a situation where consumers might perceive web streaming to be like conventional cable TV, they might still find the former to be quite different from pay TV. As per the author, if consumers’ cord-cutting intention is expected to have a positive relationship with perceived substitutability, substitutability may be less associated with the choice of entertainment as compared to other factors.

H6: Consumers’ perceived substitutability will be significantly impacted by perceived compatibility.

Proposed Research Model

Research Methodology

By adopting a snowball sampling technique, an online questionnaire was administered via google forms, to test the hypothesis. Intending to ensure quality results, the survey was short and focused. Lengthy surveys often lead to disengagement from the respondent’s end. The survey was pre-tested on 10 SVOD users, and based on the feedback, a few statements were modified. A brief voice message was sent to them via WhatsApp before administering the questionnaire, to provide clarity on the objective of the study. The items in the questionnaire consisted of a Likert scale and were close-ended. A gentle reminder was also sent to the respondents after a week of sharing the questionnaire. We received 208 complete responses. However, 22 responses were removed on account of being outliers. The outliers were calculated based on the upper and lower boundary from the standard deviation of the mean of the values assuming a normal distribution. As far as gender was concerned, 58.3% (N = 186) of the respondents were males (n = 108) and the remaining 41.7% were females (n = 78). With an average age of 34.5 years, most of the sample comprised working professionals (83.3%, n = 155), with self-employed respondents representing 8.6% of the sample (n = 16), while the rest of the sample were students (8.1%, n = 15). On an average, the respondents had subscribed to three streaming channels, the most popular ones being Netflix (58%, n = 108), Amazon Prime (22%, n = 41), Zee5 (14%, n = 26). Only 6% (n = 11) had subscribed to others (Hotstar, Sonyliv and Voot). As far as the frequency of consumption was concerned, on an average, the respondents spent around 75 mins each day on weekdays and 120 mins on average over weekends. A total of 87% (n = 162) of the respondents preferred to watch content on their mobile phones, with 24% (n = 45) of them preferring regional content.

Reliability and Multicollinearity Analysis

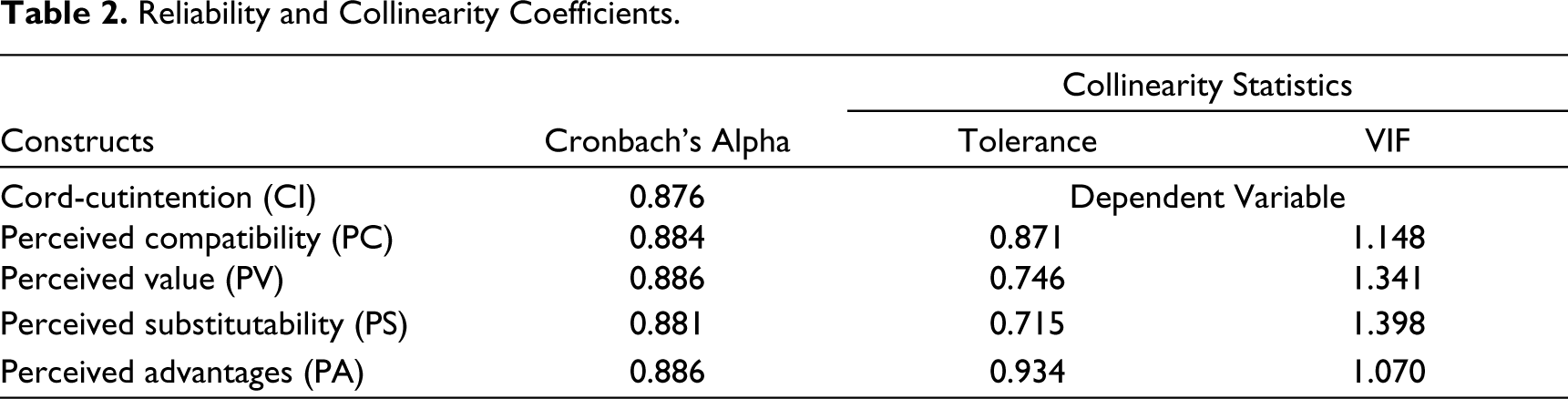

Upon subsequent reliability assessment of the collected data, the Cronbach’s alpha for all items used in the scale was above 0.87 which exceeds the recommended threshold value of 0.70 as shown in Table 2. The table also depicts the coefficients obtained for the collinearity statistics. As seen in the table, all the variance inflation factor (VIF) values lie between 1.070 (perceived advantages) and 1.398 (perceived substitutability), coupled with high tolerance values, thereby indicating no symptoms of multicollinearity.

Reliability and Collinearity Coefficients.

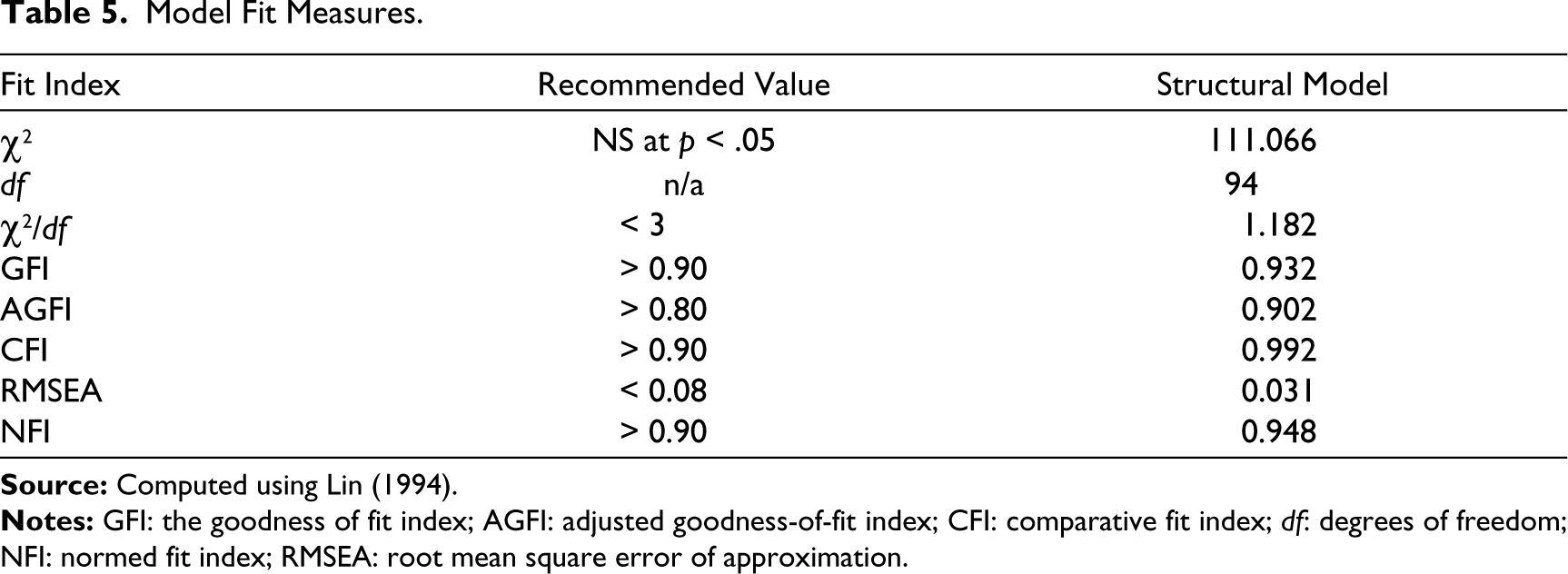

Confirmatory Factor Analysis

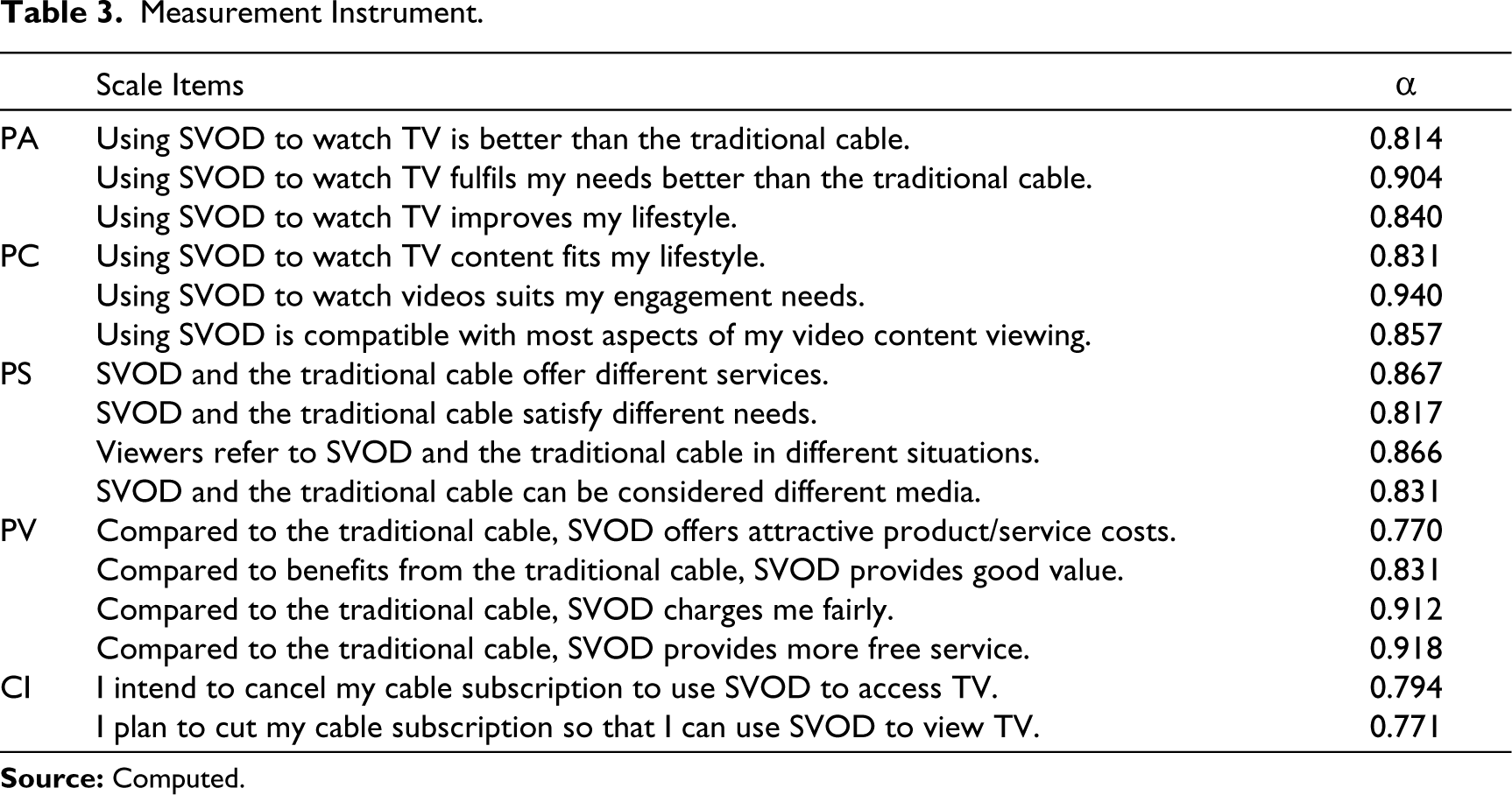

All five constructs, namely, perceived advantages, perceived value, perceived compatibility, perceived substitutability and consumers’ cord-cutting intention were measured as latent variables in the model. Through confirmatory factor analysis (CFA), all five variables were allowed to co-vary freely. According to the results: relative χ2 (CMIN/df) was 1.110 which lies within the range of 1 and 3 and is indicative of a reasonable fit. The root mean square error of approximation (RMSEA) = 0.024 is less than 0.08 which indicates a reasonable error of approximation. Goodness of fit (GFI) = 0.937 was above the recommended value of 0.90 and is indicative of a good fit, comparative fit index (CFI ) = 0.995 was close to 1 and is indicative of a good fit and Tucker–Lewis coefficient (TLI) = 0.994 which also indicates a good fit as the value was closer to 1. Table 3 shows the individual variables along with their factor loadings (FL), obtained from the CFA after the loading has been extracted below the cut-off value of 0.50. The Cronbach alpha of all items used was above 0.70 after a subsequent reliability evaluation of the data obtained, which surpassed the suggested threshold value of 0.70. The calculated FL were higher than the suggested factor value of 0.50 and ranged from 0.770 (PV1) to 0.940 (PC2). Subsequently, all the scale items were retained due to adequate FL for the structural model evaluation. Based on the obtained values, we retained the measurement model for further structural modelling and testing of hypotheses.

Measurement Instrument.

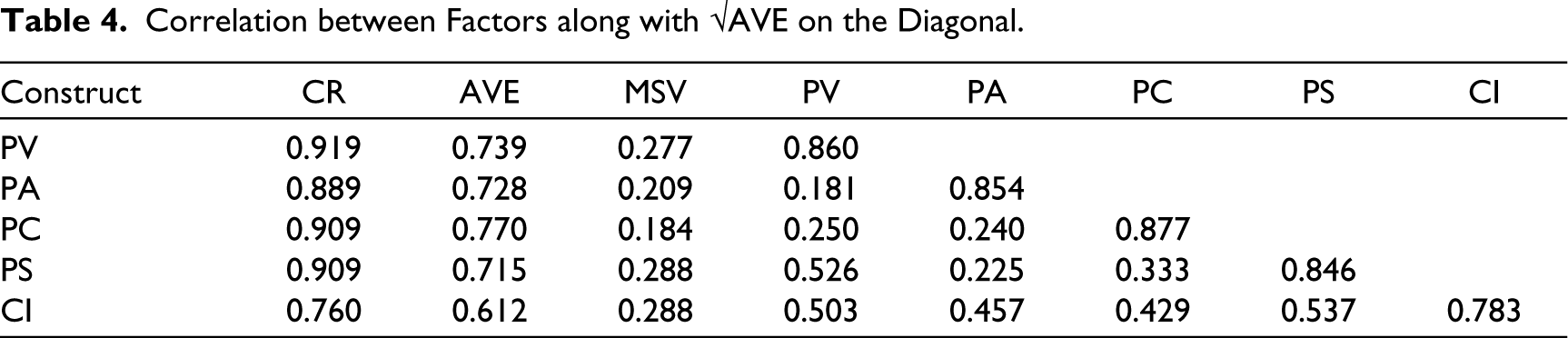

Discriminant and Convergent Validity

As extremely important indicators of measurement model evaluation, convergent validity (CV) and discriminant validity (DV) were subsequently measured. To measure CV, composite reliability (CR) and average variance extracted (AVE) were calculated. Successively, as seen Table 4, the AVE values for all constructs ranged from 0.612 (CI) to 0.770 (PC), which was greater than the recommended value of 0.50. Also, the CR values were within the range of 0.760 (CI) and 0.919 (PV) which are quite satisfactory and far above the recommended value of 0.70. The obtained AVE and CR values in our analysis are indicative of CV. To achieve a satisfactory DV, the square root of the AVE of a construct should be greater than its correlations with other constructs. As indicators of an appropriate level of DV, the values indicated diagonally were greater than the off-diagonal values as seen in Table 5 and the square root of the AVE (bold diagonal values) also surpassed the inter-construct correlations.

Correlation between Factors along with √AVE on the Diagonal.

Model Fit Measures.

Evaluation of Structural Model

The SEM output obtained from the analysis done by using Amos 23.0 was evaluated based on the recommended indices for a model fit. To improve the overall model fit, we utilised the function of modification indices. Based on the suggestions obtained from the output, direct covariates’ paths were added between some error terms, which improved the overall model fit to an agreeable extent.

The results illustrated in Table 5 suggest that the proposed model was an excellent fit; the relative χ2 (CMIN/df) statistic was 1.182, which was well below the recommended value of < 0.03, (Massad, 2018). The GFI and CFI indices obtained had a value of 0.932 and 0.992, respectively, both of which surpassed the cut-off value of > 0.90 (Prince & Greenstein, 2017). The RMSEA index was .031 which is within an excellent range and the indices obtained for NFI was 0.948, which was above the recommended value of > 0.90.

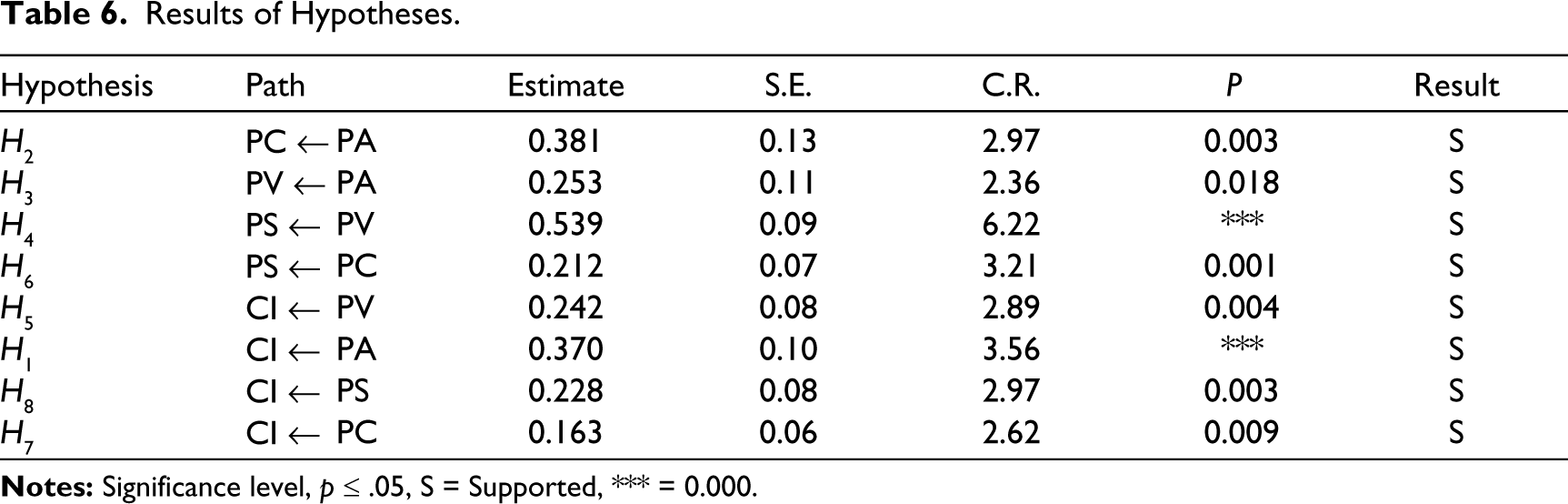

Results of Hypotheses

Once the model fit based on the recommended indices was evaluated, we examined the hypothesized relationships. The path coefficients obtained through SEM are illustrated in Table 6. As seen in the table, all paths display a significant relationship between the constructs. As is evident from the table, the results of the path coefficient indicate that all hypotheses H1–H8 were supported. Specifically, PV, PAs and PS had a significant impact on cord-cutting intention. It was also observed that PC had a significant and positive impact on the cable-cord-cutting intention of consumers and PA significantly influenced the PV.

Results of Hypotheses.

Conclusion and Discussion

Findings

The study was conducted to identify and validate the drivers of consumer intention to cut the cord. According to the results obtained from the SEM analysis, the key drivers were: PV, PA and PS. Perceived compatibility showed no significant impact on the cord-cutting intention. Based on the results of the hypotheses, the major findings of our study are the following: (a) Consumers’ intention to cut the cord was facilitated by the PA of SVOD; (b) Consumers’ PC was significantly impacted by the PA of SVOD; (c) PA of SVOD had no significant impact on its PV; (d) PV of SVOD was significantly impacted by PS; (e) Consumers’ intention to cut the cord was facilitated by the PV of SVOD; (f) Consumers’ PS was significantly impacted by PC; (g) Consumers’ intention to cut the cord was not facilitated by the PC of SVOD; and (h) Consumers’ intention to cut the cord was facilitated by the PS of SVOD. The findings of our study were consistent with the findings of the investigation that has explored the impact of similar factors on U.S. consumers’ intention to cut the cord. The impact of the PA and PC seems to have a significant influence on the consumers that drives them to cut the cord. This leads to PS based on the derived PV.

Managerial Implications

According to the findings of our study and considering the tremendous adoption and penetration of SVOD, pay TV service providers must develop necessary strategies to retain their position in entertainment media. Although the scope of market penetration for pay TV is tremendous in many countries, the estimated growth of online content is posing a serious threat. Directionally, the following innovation strategies can be developed by practising managers and marketers to foster cord-shaving:

Continuous Investment in Next Generation Pay TV Services

With a strong focus on developing their core proposition and next-generation set-top boxes, more than half the pay TV providers have started making additions to their portfolios in the past year. To support advanced functionality, they have included third-party apps, tailored recommendations and included access to 4K content. Companies need to continue such investments to ensure that they meet the needs and expectations of the consumers. A partnership with telecom majors and cable providers is already on the rise, leading to a platform which facilitates cable providers formulating innovative strategies as they already have the necessary infrastructure in place to easily launch better services. The boost of such sharing economies and joint business models holds the key to progress in the years to come.

More Diverse Multiscreen Pay TV Propositions

According to several research studies in the recent past, delivering a seamless, customized consumer experience will be the key in the future, especially considering increased churn and cord cutting. In the context of changing consumer segments and shifts in consumption patterns, the overall experience of the viewer will be a key driver in retaining the current market position. Pay TV companies can benefit from advanced data analytics enabling them to improve viewer retention, reduce switching, deliver relevant advertising, increase customer acquisition and development of new products by automating customer service and care.

Content Creation and Curation

In the present-day context, content is king. In fact, one of the main reasons behind the tremendous success of OTT platforms is the content they provide to the viewers. Understanding the psyche of the viewers and designing a wide array of content are the needs of the hour for pay TV service providers. As presented in one of the analyses, they need to explore different ways to appeal to different genres. The process of content curation begins with sourcing which refers to finding the appropriate content needed to be a part of many different social communities. To increase viewership, companies should ensure that the kind of content they are sourcing appeals to the intended segment. To be an orchestrator of content, fragmentation of content streams and making the pay TV subscription primary are possible by sourcing and adding new content.

Diversification and Connectivity

Real opportunities for the pay TV industry are presented by adjacent services such as mobile and fixed-line connectivity, creating a means to become more embedded in the mindset of consumers. Also, there lies the tremendous potential for smart homes and advanced advertising, with most companies already recognizing these areas as strategically important. In their pursuit of sustainability, television companies need to recognize the viewers’ appetite for small bites of content. This new format will lead to a new approach to enhance audience participation and strike better commercial deals.

Conclusion

In this article, we have already highlighted the recent trend in cord-cutting and the amount of traction it is gaining, all of which are posing to be serious challenges for pay TV service providers. A few researchers and analysts are in denial of the downfall of pay TV, as cable, DBS and telephone companies have attempted to keep up with the rapidly evolving video consumption landscape. Anticipating a future decline, pay TV companies have already started introducing low-priced subscription bundles and are offering economical and flexible options to retard the loss of customers. Another significant aspect is the conflict arising between cable networks and pay TV operators due to economical pricing and exclusion of an expensive network. Contextually, high-priced networks such as sports channels are experiencing a contraction in their subscriber base. In their continuous strive to stay relevant, pay TV service providers have already started competing in the streaming video market. Our study argues that the aftermath of cord-cutting and the extent of sustainability of pay TV will differ across platforms. Cable and telephone companies are not experiencing as much subscriber churn and revenue losses as pay TV companies. The information provided in this study suggests that, although pay TV is experiencing a slow decline, a large part of pay TV’s subscriber base is willing to remain intact. Marketers of pay TV companies must try to adopt the strategies discussed in this study. These strategies aim at ensuring the sustainability of major pay TV contributors who should focus on maximizing their value proposition in order to retain and possibly expand their customer base in future. They also need to continuously reinvent themselves to keep up and be relevant despite the changes across the industry. In this time and era of complete digital advocacy, a transformative effort is required by traditional players who should aim for the kind of change that demands equal measures of clear thinking and calculated risk-taking.

As digitized behaviour develops, there is, by all accounts, a developing accord that later, subscription-based models will have a more noteworthy job in digital platform monetization. For practicing managers, it is crucial to understand that by the year 2030, expenditure on digital media and consumption will no longer be viewed as an indulgence. In fact, it will be the new normal. The phenomenon of cord-cutting is expected to reach its peak and hence differentiation across consumer archetypes will be crucial. Therefore, the differentiation will revolve around geo-demographics, extent of digital sophistication and sociocultural factors.

Limitations and Future Research Directions

However, our study is not devoid of limitations. To begin with, our study focused on a smaller sample and their behaviour regarding cable cord cutting. To establish the generalizability of our findings, researchers should test the hypothesis on a larger demographic sample and should also replicate the same in other countries and generations. Future researchers can replicate the study and make subsequent explorations by examining the moderating effect of demographic variables.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.