Abstract

This study analyses heuristic factors affecting investor sentiment and investment decision-making in the Indian stock market. A quantitative approach is formulated with the questionnaire design for the collection of primary data regarding investor sentiment, representativeness heuristic bias, overconfidence and availability bias. The data are collected from the structured questionnaires from individual investors. The collected data were analysed using partial least square structural equation modelling to examine the relationship between the constructs: investor sentiment, representativeness heuristic bias, overconfidence and availability bias. This paper provides empirical insights into the association of heuristic factors that positively influence investor sentiment and investment decision-making. It encourages investors to make reasonable choices and to control and understand their risk. The study sheds light on the impact of investor sentiment on investment decision-making and its antecedent. It shows that investors depend on sentiment when making investment choices. Policymakers should provide consumers with knowledge and appreciation of the correct stock choice; various campaigns considering the different groups of investors will benefit decision-makers and institutional financial practitioners. This paper allows investors to pick the proper investment assistance to avoid making wrong decisions that arise as an outcome of the attitude of investors.

Introduction

Investor sentiment is one of the true measures of behavioural finance, which is why it has been used extensively in the stock market in recent years. The rational thinking process rules the field of finance to a great extent. An investor’s rational decisions are supported by sound theory based on relevant facts. According to academicians and practitioners, decision-making is a challenging task for market participants. The classical theory is focused on the market and the rational thinking process of the investor. The intense classical standard financial theory states that an investor is a rational decision-maker in all financial decisions. Such investors tend to have a good vision of the forthcoming uncertainty in investments. After the global expansion of financial markets, investors need to become more knowledgeable, aware and well-informed when it comes to keeping an eye on and handling their investments (Ahmed et al., 2022). Due to the complexity of financial goods and services made available to the general public and the need for informed judgements, this becomes crucial (Hastings et al., 2013).

The behaviour finance theory focuses mainly on studying investors’ irrationality and stock market investment and the cognitive process of investment behaviour. Behavioural finance also assumes that humans have bounded rationality and a reduced ability to digest information, as opposed to classical finance’s assumption that people use entire knowledge for choice. Human emotions and feelings have a major role in the irrational decisions made by investors (Tversky & Kahneman, 1992). An investor’s behaviour can be predicted, analysed, reviewed and judged to understand investment psychology (Fromlet, 2001). Understanding the various aspects of an investor’s behaviour, such as judgement, emotional, social and intellectual characteristics, as well as their limited cognitive capacities, which are important stock market drivers, is emphasized by behavioural finance (Trifan, 2020).

Modern finance describes the link between the investment performance of individuals and heuristics. Investor sentiment has been an exciting field in finance for many years. The study of Brown and Cliff (2005) and Baker and Wurgler (2007) focused mainly on how investor sentiment influences asset prices in the stock market. Heuristics are strategies, procedures or other mental shortcuts a person can employ to address various challenging situations (Ritter, 2003; Tversky & Kahneman, 1973). Heuristics help to make sense of the natural world relatively consistently while minimizing mental burden. However, the results obtained through heuristics can occasionally lead to logical errors, resulting in undesirable effects (Tversky & Kahneman, 1973). Cognitive biases are systematic errors classified into three categories: anchoring and adjustment, availability heuristic and representative heuristic. Different investors have studied and employed these heuristics to speed up the decision-making procedure associated with logical decision-making which necessitated a full review of all existing data (Shefrin, 2000). Behavioural scientists have investigated the effect of heuristics on investment decisions (Barber & Odean, 2000; Waweru et al., 2008), their research being focused on developed countries.

The researcher attempts to identify the different factors that influence investors. This paper shows an association between heuristics, investor sentiment and investment decision-making. Online platforms are increasing with time, offering high flexibility to minimize the uncertainty in decision-making. These platforms guide the investor by giving real-time data and a quick analysis with a suitable prediction regarding the stock market. This trend is highlighted in the work of Barber and Odean (2001), who mainly focused on the investment performance and trading behaviour of those investors who switched from the traditional trading model to an online channel platform. Investor sentiment can be termed as the positive movement of an investor regarding specific stocks, allowing them to arbitrage through the price deviations in the security market. It may include investor participation, optimism and stock market outlook. This paper puts forth literature on heuristic investor sentiment in the stock market.

The key aim of this study is to find out how heuristic aspects, namely, overconfidence, availability bias and representativeness impact investor sentiment, leading to investment decision-making. Hence, the main objective framed for the present study is to find out how heuristic factors influence investor sentiment, investment performance and decision-making in the stock market. It explains the relationships between these elements to help investors know their behaviour in stock selection and make a better investment choice. Generally, this study mainly aims at the association between investment performance and heuristics and at ascertaining the mediating effect of investor sentiment which in turn influences the investment decision-making of individuals.

This paper is structured as follows. The first section includes a review of the research work undertaken in behavioural finance by eminent researchers. In the second section, a theoretical framework is designed and discussed based on the literature reviewed and the framing of the hypothesis is done. The third section shows how the research methodology empirically tests the theoretical framework. The fourth section showcases the analysis and outcomes of the paper. The fifth section talks about the discussion of the study while the sixth section elucidates the limitations and scope for future research. The final section highlights the implications and conclusion of the study.

Research Model and Hypothesis Development

This paper is built on the foundation of an eminent researcher’s work in behavioural finance. Studies on behavioural finance demonstrate that the emotions and anxieties of stock market investors influence their decision-making. Direct information from behavioural finance shows that variations in investor sentiment strongly impact investing decisions (Guo et al., 2017). Research in this field reveals that psychological factors rather than rationality influence the behaviour exhibited by investors. The general attitude of investors toward the financial market is referred to as investor sentiment. It depicts the sentiment, attitude, expectation or confidence of investors and could affect how they make decisions (Haritha & Uchil, 2020). Sentiments influence the movement of the price of a security in the market. If there is a bullish market, there is a price rise, while a bearish market sees a fall in prices. Investor sentiments lead to beliefs about the future cash flow and the risk of the security. The prevalent sentiment of the market leads to overpriced and under-priced stock (Baker & Wurgler, 2006). It explores the possible effects of optimism/pessimism bias on investors’ reactions towards information collection, processing and decision-making. Individual investor decisions on the securities exchange are critical in deciding market development, which then manages the economy (Kengatharan & Kengatharan, 2014). Haritha and Uchil (2019) studied the impact of investor sentiment on investment decision-making in the Indian stock market. Investor sentiment can be described as an investor’s positive tendency towards individual equities that enable them to arbitrage across price fluctuations in the stock market. It could consist of optimism, investor interest and stock market expectations. The stock market comprises various participants who interact with each other and with society at large; it is evident that an individual’s psychological factors play a role in decision-making.

Heuristics Theory

The heuristics theory is an easy and efficient rule that individuals use in the absence of reliable information to avoid complexity (Bingham & Eisenhardt, 2011). Kahneman and Tversky (1974) identify three main heuristics investors can use while making decisions; they are anchoring, representativeness and availability bias. When investors use heuristics, they reduce their mental energy in decision-making. Yet, there can be mistakes in judgement and, consequently, investors make incorrect investment decisions, leading to an inefficient market. ‘A heuristic is a strategy that ignores part of the information to make the decision more quickly, frugally and accurately than more complex methods’ (Gigerenzer & Gaissmaier, 2011). Kahneman and Tversky (1979) stated that irrational individuals used heuristics when making decisions even if they failed to assess the ideal probability. Numerous financial and economic researchers contend that specific heuristics can affect financial decision-making and estimate economic factors (Abarbanell & Bernard, 1992; DeBondt & Thaler, 1990).

Investment is the act or state of investing money with the expectation of a better benefit. Haritha and Uchil (2019) found that investor sentiment implies the aggregate degree of investor perception toward capital market securities. This displays the investors’ emotions, attitudes and perceptions that could affect their investment decision-making. Sentiment affects the stock action of consumer protection. Both events can happen—the price falls in the bearish market and the price rises in the bullish market, contributing to confidence in the security risk and the potential cash flow. Each investor wants his investment to yield maximum returns. Research in recent decades has shown that rational and optimal decision-making depends on understanding finance; the more financial knowledge an individual has, the more reasonable a decision is (Merton, 1987). Individual thoughts and opinions of investors can change the decision-making procedure from rational to irrational (Baker & Nofsinger, 2002).

Availability Heuristic Bias

Availability heuristic bias is a cognitive heuristic that denotes people’s predisposition to make decisions based on readily available information and other relevant circumstances (Tversky & Kahneman, 1973). Individuals use the availability heuristic to assess the likelihood of an occurrence based on readily obtainable facts and the ease with which significant cases spring to mind (Brahmana et al., 2012). Consequently, local companies are preferred over international equities while investing. When decision-makers base their judgement on present information rather than the cumulative ancient and comprehensive information, the availability heuristic is frequently used, resulting in biased decision-making (Kliger & Kudryavtsev, 2010). Based on readily available information, stock market investors give an asset more weight (Pompain, 2012). This behaviour can be seen in the financial market when investors favour local companies’ stock over multinational companies’ stock since they are familiar with local companies and have readily available information about them (Waweru et al., 2008). The availability heuristic is a cognitive bias that refers to an investor’s trend to evaluate an investment opportunity based on readily available knowledge and information while neglecting alternatives. This investor tendency leads to irrational conduct which impacts investment performance (Folkes, 1988). Steen (2002) found that the investors’ views change when news and information about the economy and firm performance become available, resulting in a specific outline of the stock market and influencing investment decisions. Inappropriate information might also affect investment decisions. These unrelated data hurt investment decisions because the investors’ risk attitude alters due to readily available data, influencing investment decisions (Weber, 2010). When analysing a financial asset in the stock market, individual investors evaluate its return and risk to a peer and then react based on the investment (Brauer & Wiersema, 2012). This information may encourage investors to shift their portfolio selection towards liabilities rather than assets which helps investment decisions. Instead of considering all critical information when analysing security, investors may analyse only the recent and readily available data (Wang et al., 2014). The availability heuristic significantly impacts investing decisions. Several studies have shown that when investors have more critical information, they feel relaxed when making decisions (Shah et al., 2018). The availability heuristic substantially affects investor decisions since it leads to investors incorrectly perceiving a stock with high earnings as a less risky security and a stock with low earnings as precarious security, leading to inefficient investment decisions (Ganzach, 2000).

H1: Availability heuristic bias significantly influences investor sentiment towards investment decision-making.

Representativeness Heuristic Bias

The representativeness heuristic describes the extent to which individuals understand a trait as representative of the subject as a whole, regardless of whether or not the characteristic is related to the subject material (Khan et al., 2017). The representativeness heuristic measures the degree to which an incident resembles the population (DeBondt & Thaler, 1995). An individual’s tendency to create findings about a social occurrence based on preconceptions is referred to as representativeness. Individual investors are vulnerable to two sorts of representativeness in the financial market: base rate negligence and sample size negligence. Investors consider irrelevant information when determining the value of an item for investing reasons, known as base rate neglect (Ahmad et al., 2017). While investors focus on buying ‘hot’ stocks with immense earning potential rather than stocks with low earning potential in the financial market, this conduct implies using the representativeness heuristic. Investor overreaction in the stock market is caused by this tendency (DeBondt & Thaler, 1995).

Investors are often known to exaggerate the possibility of irrelevant information or something scarce while underestimating the likelihood of general subject-related characteristics (Chandra, 2016). Investors used heuristics in various situations to speed up decision-making and drawing conclusions (Ricciardi & Simon, 2001). The representativeness heuristic bias (DeBondt & Thaler, 1995) is a cognitive bias that affects investment decisions and stock prices. Investors in the stock market put further weight on conspicuous information and credit it to the firm’s achievement or failure while discounting other pertinent aspects, resulting in overreaction (Antunovich & Laster, 1998). According to Kaestner (2006), investment decisions in the stock market are influenced by the representativeness heuristic in two ways. First, when projecting a firm’s future performance, investors see comparable information as a trend and give the present information about a firm more weight, causing them to overreact. Second, investors may understand a chain of related data as a reversion to mean even though the series is too short. Investors make investment decisions based on the stock’s prior performance as a proxy (Pompain, 2012). It assumes that a stock with a long history of higher earnings will produce related results in the future even though historical performance is not a consistent indicator of future performance.

Likewise, people believe that a stock with a terrible track record will continue the same way in the future, leading investors to make irrational decisions. As a result, they prefer to invest in stocks following a price increase and expect the trend to continue while avoiding stock investments when prices are lower than their fair worth (Baker & Ricciardi, 2014). According to several studies, this idea is not a critical factor in stock market investor behaviour (Charness et al., 2010). Even though several researchers studied the representativeness heuristic to better describe and understand investor behaviour in the stock market, they came up with mixed results.

H2: Representativeness heuristic bias significantly influences investors’ sentiment towards investment decision-making.

Overconfidence Heuristic Bias

The heuristics theory is defined as shortcuts in decision-making that people use to reduce the work involved in the process (Shah & Oppenheimer, 2008). Winning choices are created on vital facts and demonstrative evidence (Nicholson, 2013). For instance, overconfidence in behavioural finance is one of the best-known psychological characteristics of heuristics (Baker et al., 2017). It is the strongest heuristic in which the individual uses whatever is in making investments (Waweru et al., 2008). People deny several considerations in a state of uncertainty, such as evaluating a stock (Tversky & Kahneman, 1974). Overconfident investors ignore minimal possible risks and only take into account recently happened events. This raises the possibility of losses, which lowers investors’ confidence and raises their tolerance for risk (Bracha & Brown, 2012; Van den Steen, 2004). Investors use heuristics in unpredictable circumstances because they regularly struggle to accurately assess the probability of an incident occurring (Gilovich et al., 2002). According to the heuristics theory, overconfident investors overrate their cognitive abilities and judgement (Pompian, 2011) and knowledge and ability (Fischhoff et al., 1977). In keeping with the theory, overconfident investors focus on their knowledge consistency and place more importance on their private information (Daniel & Titman, 2006) to avoid confusion and thereby create quicker decisions. It overestimates the veracity of their private knowledge because they place more trust in it than they should in information that is freely accessible. Although it encourages trading, such overconfidence lowers investment efficiency (Oberlechner & Osler, 2008; Odean, 1998). Hence, we develop the following hypothesis.

H3: Overconfidence heuristic significantly influences investors’ sentiment towards investment decision-making.

Hypothesized Model

Research Methodology

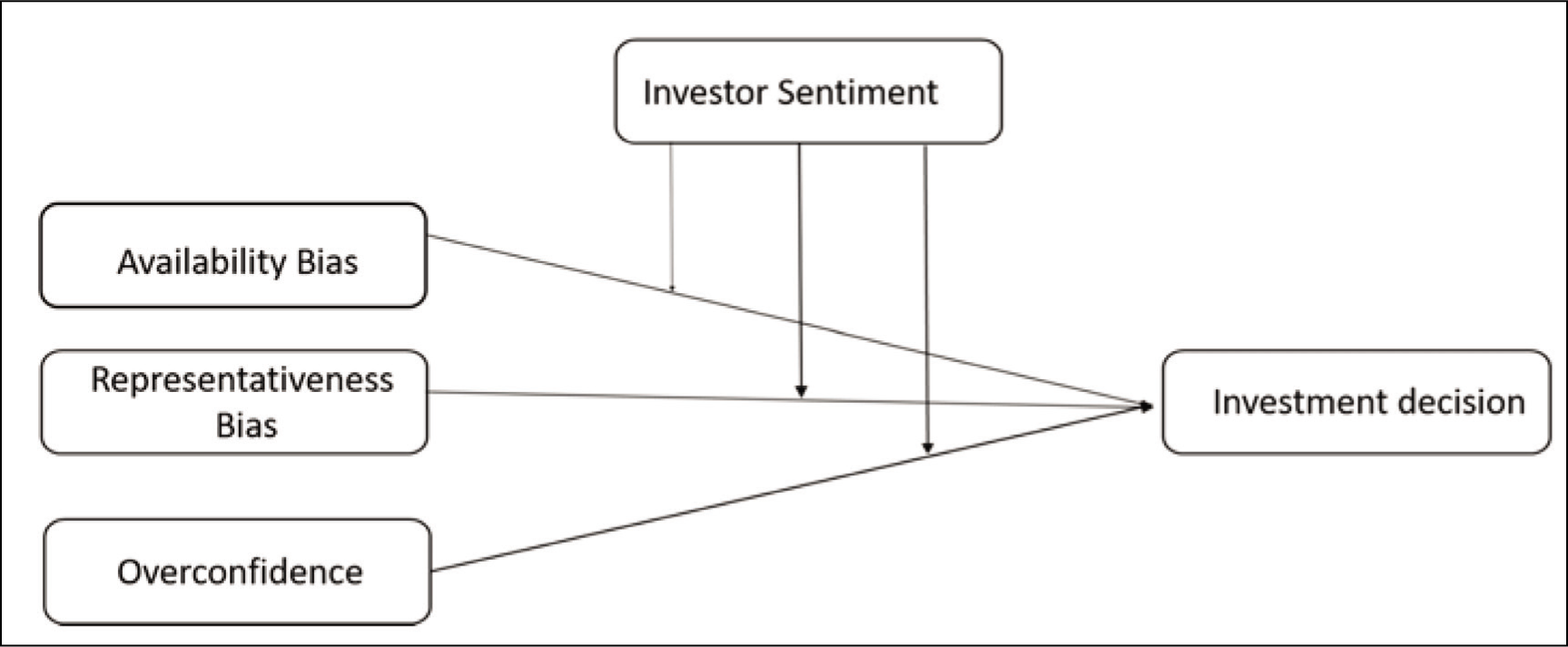

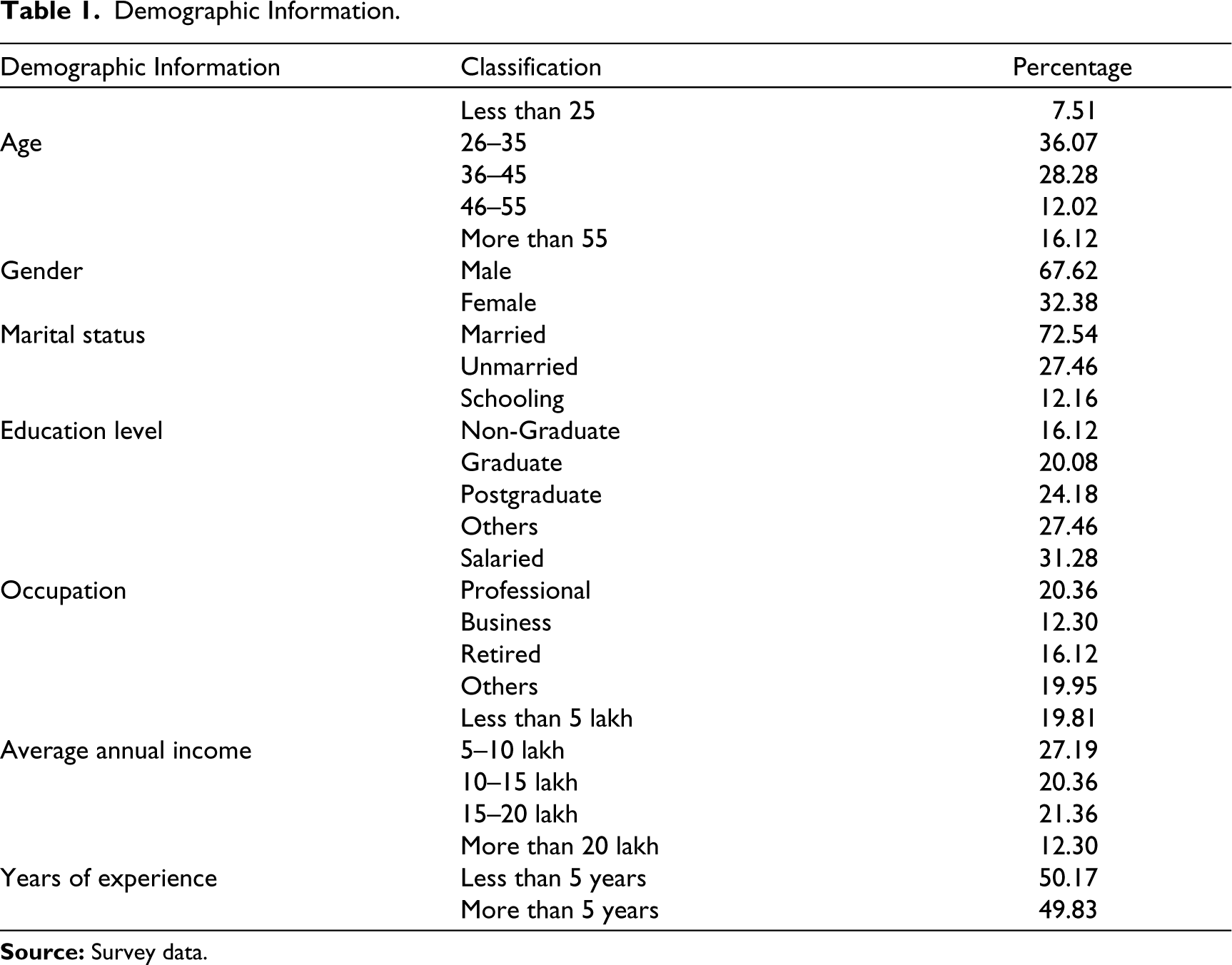

A quantitative technique was adopted to investigate the influence of herding behaviour and awareness on investor sentiment leading to investment performance. In this study, primary data were obtained through the survey method in the form of a structured questionnaire. The respondents selected were individual investors. We used a simple random selection technique to send survey questionnaires to investors. Simple random sampling is a type of probability sampling in which each respondent has an equal and reasonable chance of being selected for the survey. Simple random sampling has the virtue of being simple to use along with having a high degree of generalizability. The structured questionnaire consisted of two parts: personal information and heuristic factors (availability bias, representativeness bias, overconfidence and investor sentiment) influencing investor sentiment and investment decision-making (Figure 1). Investor sentiment was divided into investor participation, optimism and stock market outlook. The questionnaire was constructed using concepts from the literature review. The questionnaires were circulated among 295 individual investors in the Karnataka region using the convenient sampling technique. Of the 295 questionnaires, 235 were reverted which implies that the answer rate was 80%. Out of these, 15 responses were excluded because they were incomplete. 220 respondents agreed to participate in the survey and were used for the final analysis. To obtain client information, the researcher approached a brokerage firm that acted as a mediator. The questionnaires were sent through e-mails, personal contacts and participation in the brokerage house.

Conceptual Model of the Effect of Heuristics on Investment Decision-making and the Mediating Role of Investor Sentiment.

The questions were brief and clear-cut. The five-point Likert scale rates the opinion and response of the investors to be respondents on a scale of 1 to 5, indicating the extent of respondent agreement or disagreement to a statement aimed to recognize the factors which affect investor sentiment in the stock market varying from totally disagree to agree (1 = strongly disagree to 5 = strongly agree). Availability heuristic questionnaire items were adapted from Luong and Thu Ha (2011), Kudryavtsev et al. (2013) and Waweru et al. (2008). The scale of representativeness heuristic was adapted from Sarwar et al. (2014), Waweru et al. (2008) and Luong and Thu Ha (2011). The investor sentiment questionnaire contained items that were adapted from Shiller and Pound (1989) and Singhvi (2001). The investment decisions scale items adapted from Scott and Bruce (1995). They devised a decision-making measure from which we derived irrational decision-making behaviour (Rasheed et al., 2018) as the fundamental goal of our research is to examine the irrational behaviour of investors against the setting of the Indian stock market.

The researcher developed the remaining items through a wide-ranging review of the literature, objectives and research hypothesis. Some items were removed from the questionnaire through a process of reliability and validity.

Method Used for the Study

The demographic evidence of the respondents is demonstrated in Table 1. It consists of marital status, gender, age, occupation, educational qualification, annual income and experience for this study.

Analysis and Results

Model Testing

Structural equation modelling (SEM) is an advanced method of the general linear model that aids investigators in analysing regression equations (Hair et al., 2006). It is a widely accepted leading multivariate method used for social sciences. This also used linear relationships between variables to be specified and estimated (Hair et al., 2006). SEM is specially used in scientific theories because it helps understand how a set of variables defines them and how they relate to each other (Byrne, 2013). SEM is a statistical tool with several benefits in social sciences.

Demographic Information.

Partial least square (PLS)-based SEM was used for this study, and it is a variance-based technique of SEM. While covariance-dependent SEM is a common approach, recent research suggests the increasing acceptance of PLS-SEM on the basis of different aspects (Hair et al., 2014). For the present study, PLS-SEM was selected for numerous reasons. Sosik et al. (2009) suggested that soft modelling tackles small sample sizes, emerging theories and subjective interpretation phenomena in group and organizational studies. A meta-analysis of PLS-SEM research findings from various business areas establishes that most research uses PLS for three key reasons: small sample sizes, non-normal data and formative models (Hair et al., 2014). It has simple distributional assumptions without expecting a particular distribution pattern (Chin 2010; Henseler et al., 2009). Therefore, the concept of normality in PLS is not violated. In general, due to the limited sample size and soft division expectations, PLS-based SEM was used for the present study. WarpPLS was the software instrument used for the analysis of SEM. It is a new addition to the package based on PLS-SEM and has the other benefits of treating nonlinear relationships generally associated with behavioural data. Therefore, WarpPLS helps users give a realistic image of the information. PLS-SEM incorporates a two-phase result reporting strategy. The evaluation of the outer or the measurement model is done as the first step by determining the validity and reliability of the constructs selected for the analysis.

A univariate no-normality test was used before exploratory factor analysis (EFA) based on kurtosis and skewness. Amongst all the variables, the extreme was 1.74 for skewness and 1.81 for kurtosis for each variable within the standard limits (Kline, 1998). EFA was employed to decide the factor arrangement and later, normal distribution was tested. The varimax was selected for the EFA. The varimax rotation preferred depends on the purpose of research and the requirements to minimize the vast number of variables to uncorrelated variables of the small number (Hair et al., 1998) to apply the items of the factor analysis based on investor sentiment and their factors affected in the stock market, it was essential to test the Kaiser–Meyer–Olkin (KMO) measure of the adequacy of sampling (Zhang et al., 2003).

The KMO measure of sampling adequacy and Bartlett’s test determine the factor analysis methods. It is a statistic that shows the extent of difference in the variables that might be affected by the reduction of factors. Kaiser (1960) suggested the minimum value to be 0.5 and the highest value to be above 0.9. This study obtained a KMO value (0.827), indicating that the factor analysis is appropriate for the data being used in the present study. Also, Bartlett’s test value of sphericity is 0.001, which indicates an essential association among the variables. The test results support the fact that factor analysis is highly useful for these data. Bartlett’s test of sphericity of the value is χ2 = 5,482.46; sig. −0.001** shows that the hypothesis covariance matrix of variables and item variance was rejected indicating that factor analysis was appropriate for this study. In the principal component analysis, the eigenvalue of the four factors is greater than or equal to 1.0 (Kaiser 1960), thus describing 82.66% of the variance.

Only those variables with a factor loading of 0.70 and higher can be considered (Bohrnstedt & Knoke 1994). In this study, all the variables are valued above 0.70, which is acceptable. The variables are then tested for availability and reliability in the case of validity acceptance. The items’ construct of reliability was assessed by estimating the coefficient value of Cronbach’s alpha. It specifies the internal consistency of the variable and alpha range from 0.75 to 0.87 and the values are measured as tremendous and beyond the recommended value of 0.70 (Nunnally, 1978). The importance of reliability is over 0.70, demonstrating an excessive level of internal consistency between each construct item. Estimating reliability can be done by two assessment measures: Cronbach’s alpha and composite reliability. It measures variation as a response of different variables reliably across the elements in a standard, which means internal consistency reliability (Brown, 2002). The reliability of the data was tested with the help of Cronbach’s alpha method. It allows us to measure the reliability of various classifications.

Cronbach’s alpha is a degree of internal regularity, the closeness of a group of items. Composite reliability and Cronbach’s alpha are used to assess measures for the reliability of all constructs. It measures the degree of responses using composite reliability as suggested by Hair et al. (2006). If the value is higher than 0.8, the scales indicate good composite reliability (CR). Convergent validity is mainly considered for checking every interrelated construct’s related scales. It is revealed to estimate the average variance extracted (AVE), the value is equal to or greater than 0.50, and the CR is more significant than AVE (Henseler, 2015). Therefore, the reliability and validity of the measurement model were confirmed.

The structural model describes the associations between the latent variables in the present research. The structural model in PLS-SEM is assessed using the explanation for the variance of the endogenous constructs (R2), predictive relevance of the model (Q2) and calculation of effect sizes (f2) (Chin, 2010). The proposed hypotheses are stated and tested along with all the path coefficients and the P values. Consequently, the mediating mechanism is also investigated by analysing the indirect effects. In addition to other results, WarpPLS also determines multiple model-fit indices, three of which are widely documented. These are average R2 (ARS), average path coefficient (APC) and average variance inflation factor (AVIF) (Kock, 2017). The AVIF value should be less than 3.3 explicitly for multiple-indicator frameworks (Kock, 2017). The model fit demonstrates that they are beneficial for assessing the model’s consistency in multiple model comparisons. The p values for ARS and APC are substantial at 0.05 or lesser (Kock, 2011). The path coefficients are measured as per their meaning, significance and relevance. PLS-SEM employs bootstrapping to measure P values when the data are not assumed to be distributed normally.

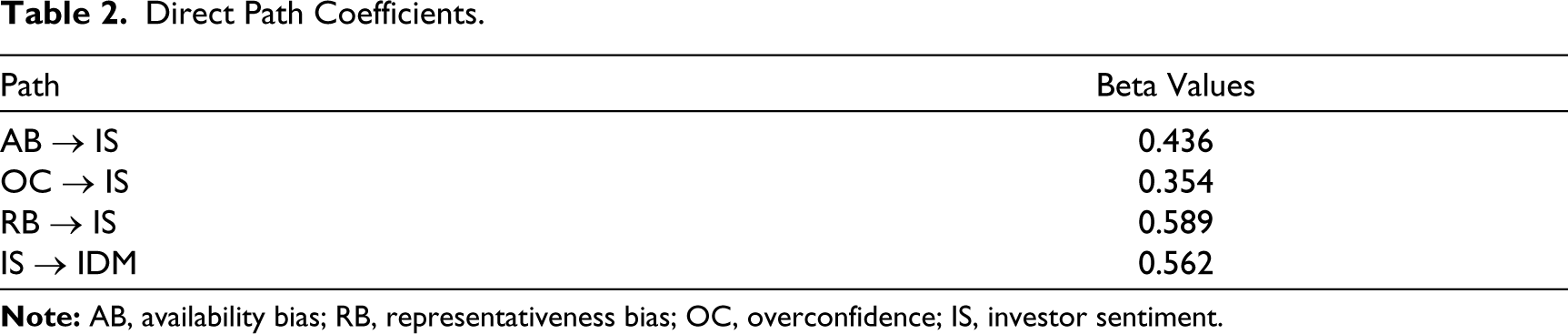

Furthermore, WarpPLS describes nonlinear associations between latent constructs specific to social science research and the automatic adjustment of the warping coefficient (Kock, 2010). Cohen’s (1988) criteria are used to estimate effect sizes, with values of 0.02, 0.15 and 0.35 representing the little, medium and strong influence of the predictive items on the dependent items. Table 2 illustrates the direct path coefficients. The significant findings of the path study demonstrate strong support for the associations among the items which provide ample proof to substantiate H1–H3.

Direct Path Coefficients.

Mediating Effect

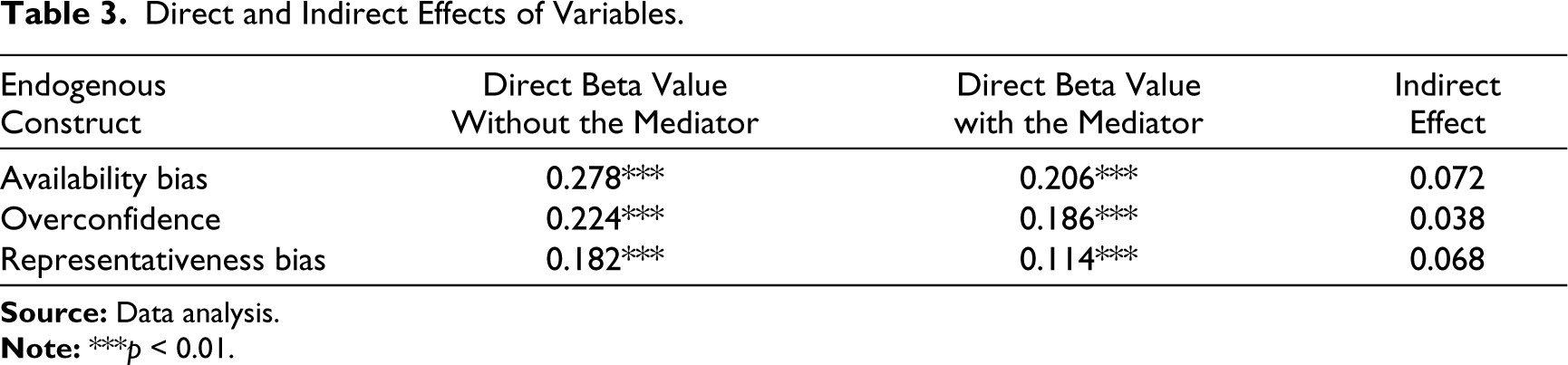

The indirect influence was studied to analyse the mediating influence of investor sentiment on the relationship between heuristics factors and investment decision-making. WarpPLS automatically generates indirect effects that allow users to explore the mediating impact directly without resorting to intermediate order to calculate the conventional method (Baron & Kenny, 1986). WarpPLS combines (Hayes & Preacher, 2010) for linear and nonlinear relationships (Preacher & Hayes, 2004) and for calculating the mediating effect. The total impact signifies the direct effect of the heuristic on the result besides the indirect influence of the mediator. Table 2 shows the direct consequence of the path coefficient. The outcomes demonstrate the direct and indirect effects of heuristics on investment performance. The direct impact of the heuristic is substantial and, therefore, partial mediation can be inferred in these cases.

The Results of Direct and Indirect Variables

Table 3 shows how independent variables have a direct effect on dependent variables. The outcome indicates that the availability bias positively influences investor sentiment (0.278, p < 0.01). Overconfidence also positively influences investor sentiment (0.224, p < 0.01). So does the representativeness bias positively influence investor sentiment (0.182, p < 0.05). Investor sentiment is a mediator between heuristics (availability bias, representativeness bias and overconfidence) and investment decision-making. Investor sentiment also has a positive influence on investment decisions. The presence of a direct impact supports the degree of the meditational instrument amongst heuristic factors (representativeness bias, availability bias and overconfidence) and investment performance.

Direct and Indirect Effects of Variables.

In the case of indirect, specific effects, the availability bias development positively affects the investment decision-making of individual investors via investor sentiment (0.206, p < 0.01). Overconfidence positively influences individual investors’ investment decision-making via investor sentiment (0.186, p < 0.01). Representativeness bias also positively influences individual investment decision-making via investor sentiment (0.114, p < 0.05).

To assess the impact of availability heuristic bias, overconfidence and representativeness heuristic bias on investment decisions, the R2 value is 0.746, indicating that the availability and representativeness heuristics indicate 74.6% of the variation in investment decisions. This explains why heuristics biases such as availability bias, overconfidence and representativeness bias play a significant role in investor stock market investment decisions. Baker and Yi (2016) demonstrated that psychological elements have a high R2 value (0.834) in the investment decision-making of investors.

The availability bias beta value is (β = 0.426), significant at p = 0.016. As a result, H1 is supported, indicating that availability bias significantly impacts the investment decision-making behaviour of the investors. This result is in line with the findings of most prior research. Khan (2015) conducted a study on the impact of availability bias on investment decisions and discovered that availability bias significantly impacts investment decisions. Likewise, Massa et al. (2005) found that availability bias affects the investors’ rational decision-making behaviour and illogical stock market behaviour. The representativeness bias beta value (β = 0.589) is significant at P = 0.03. This supports H2, which states that representativeness bias has a direct and consequential impact on the investment decision-making behaviour of investors. The correlation between overconfidence and investor sentiment (β = 0.354) and p value is 0.011. This result shows that H3 is supported.

Discussion

The present study observes the effect of heuristics on an individual’s investment performance and the association is mediated by investor sentiment. The empirical findings validate this recommendation to a large extent. The behaviour of individual investors creates reasons for discrepancies in the financial market. In brief, heuristics causes investor sentiment. The heuristics cause of investor sentiment is obtained from a wide range of literature generated by expanding descriptive and experimental designs showing individual heuristics in different conditions. The elements of heuristics—availability bias, representativeness bias and overconfidence—are the main aspects that investors use to avoid the difficult decision-making procedure. According to the heuristic theory, investors tend to take firm decisions based on the latest information (Tversky & Kahneman, 1974). Availability bias leads to creating investor sentiment and impacts investment performance. Our results confirm that the availability bias heuristic is the most prominent subsidizing element to the construction of investor sentiment (coefficient = 0.426), and investor sentiment has substantial positive impacts on investment decision-making. In this model, the result recommended that investor sentiment positively influences herding behaviour. Even though the result shows the nature of the relationship between availability bias and sentiment, the values indicate that the intensity of herding is accentuated by sentiment. In the present study, the deal of the variation, which means availability bias power, may explain all the factors other than those reflected in the model; therefore, under certain circumstances, due to sentiments, investors try to imitate other investors who got a better output or who received success through specific decision-making.

This indicates that overconfident investors overrate their skills and knowledge due to self-assignment which results in significant reasons for deviating stock prices. This reliable hypothesis (Odean, 1998) demonstrates that overconfident investors are unrealistically optimistic about the future. Overall, they respond to changes in the stock price over or under. Their perspective toward investment decisions renders the market inefficient. Overconfident investors indulge in excessive market trading in order to attain higher returns. Their irrational behaviour makes them assume they can take it higher and do well in their investment performance. The heuristic investor theory relies heavily on stock selection information (Tversky & Kahneman, 1974), which results in stock price changes and commonly traded strategic goals that are an explanation to create investor sentiment. The strong link between investor sentiment and investment performance demonstrates that it is not just individual investors who rely on their performance on risk and return. Therefore, satisfaction is also an important indicator. Standard finance supporters argue that the inadequate implementation of irrational investors can take them off the stock market. But the study’s outcome shows that irrational investors often operate in the market. The heuristic investor theory heavily relies on stock selection information (Tversky & Kahneman, 1974), which results in stock price shifts and standard stock levels that make investor sentiment. This hypothesis is associated with (Andersen, 2010) the statement that relies on recent experiences to demonstrate investors’ actions towards stock picking. They neglect the stock dynamics in this context and make the economy inefficient. The strong association between the anomalies and the investment performance indicates that investors base their decisions on return and risk, though satisfaction is essential. Behavioural finance supporters argue that the lower performance of irrational investors can wipe them off the stock market. But the effects of our study demonstrate that irrational investors also undertake on the market.

The mediation effect of investor sentiment is significant among all heuristics and investment performance mechanisms which support the behavioural finance theory that investors are satisfied with their investment decisions. Therefore, behavioural factors play a significant role in decision-making. In a way, investors used heuristics to choose inefficient market security and were satisfied with their investment decision. Wang et al. (2006) suggested that investors do not have adequate investment skills and knowledge. Consequently, those who used various heuristics in investment decisions. Parveen et al. (2020) contend that behavioural finance offers a method for understanding market fluctuations and consumer attitudes and studies the validity of market beliefs in more detail. For such a cause, this study considers actual market beliefs that help us determine how the market will respond to investor decisions. On the other hand, investors are happy with their investment decision-making in the context of customer sentiment since they have used heuristics effectively.

This article examines heuristic-driven biases and their impact on investor decision-making in India. This work also found that heuristic-driven biases like availability bias, representativeness bias and overconfidence, directly and significantly impact investor sentiment and investment decisions. This study confirms that different psychological and heuristic-driven biases influence India’s investment behaviour. Investors in India usually choose financial products about which information is easily available and accessible rather than conducting an in-depth evaluation of all data available. Furthermore, people invest in securities based on past returns, management styles and corporate reputations, which may, in turn, lead to poor investing selections. These findings show that investors in a hurry for a quick return focus on the short term and respond to new information. As a result, this study explains the irrational conduct of investors which is typically focused on fast and frugal rules and leads to bad stock market performance and volatility. Our findings are in line with those of Khan (2015), Abdin et al. (2017), Chen et al. (2007), Yaowen et al. (2015) and Massa et al. (2005). They conclude that stock markets are inefficient and investors make investment decisions based on recent prices and trends.

This paper informs investors about the impact of heuristic biases on their investment choices and decisions. It suggests they avoid heuristic-driven biases and other psychological shortcuts during the investment decision-making process. Instead, investors should make a detailed analysis of all relevant data. Furthermore, the study recommends that investors adopt future-oriented behaviour and not bank upon instant outcomes by making instant investing judgements. The work also has ramifications for stock market regulators and policymakers by helping them better understand the functioning of heuristic biases in investment decision-making. They can create policies and raise behavioural aspects in investment decision-making to confirm smooth stock market decision-making. On a larger scale, this research adds to our support of behavioural finance theories by providing a theoretical link between heuristic biases and individual investor investment decision-making in a developing economy.

Limitations and Future Direction for Research

This study greatly contributes to an in-depth understanding of investor behaviour. but the study has a few limitations. The cost and time constraints were significant limitations for the multi-city sample analysis. As the sampling size was restricted to a particular state, the results cannot be generalized. The study measured investor sentiment and the factors influencing the stock market. The results may vary from state to state.

This research limited the emotional factors that could play an important role too. In the future, the study can be extended to add more elements to decision-making and to incorporate how the affective aspect can affect asset pricing and risk–return analysis. This study used variables built from pre-identified antecedent heuristics. Our results indicate that these antecedents can explain only the variance in the heuristic concepts and the variable outcomes. There may be other factors like regret aversion, gambler fallacy and framing that could influence investor sentiment and investment decision-making.

Implications and Conclusion

This paper enhances understanding of the association between investment performance and heuristics in individuals by conceptualizing mediation procedures. Investor sentiment mediators calculate an individual’s investment performance since the stock market combines buyers and sellers. Investor behaviour includes investor sentiment that influences investment performance. The results denote that various aspects of heuristics affect investment performance differently and that multiple components stimulate multiple techniques. By analysing each heuristics component separately, researchers gain insights that help individual investors and financial institutions. The development of behavioural finance has been limited to emerging stock markets. This article provides support in knowing how to act. The effects of behavioural finance are widely applied to developed stock markets. This study is being carried out to verify the appropriateness of using behavioural finance with all types of securities markets.

This research study explains different concepts that traditional finance has failed to prove, like overpricing, underpricing, solely focusing on the stock market among others, thus, giving an even greater understanding of the actual behaviour of investors. Along similar lines, this study has implications for investment organizations that seek to understand and analyse heuristic behaviour more rigorously so as to provide such investors with more credible consultancy data based on real-life behaviour. It helps policymakers understand investors better and develop policies that take these physiological factors into account to ensure the safe functioning of the economy. Before policymakers regarded investors as rational, however, the global financial crisis raised crucial questions about this method. It demonstrated a strong need for behavioural aspects to be incorporated into general principles.

The findings drawn from this paper provide valuable insights to policymakers, investment practitioners and academicians. This study deals with a new perspective on whether sentiments should be regarded as rational or irrational and whether long-term or short-term effects of investor sentiment and asset pricing provide a significant level of sentiment that influences stock market risk and return. All of these are analysed economically or statistically. This work can be incorporated to substantiate investor behaviour and overreaction (Ali et al., 2001; Brahmana et al., 2012). The association between overreaction and sentiment is interpreted (Kukacka & Barunik, 2013). This study adds to the importance of heuristic factors that affect investor sentiment and investment performance in the Indian stock market. Liao et al. (2010) reiterate the findings that investment decision-making can fluctuate with investor sentiment. Research in psychology established a correlation between investor decision-making and sentiment. Mainly, the results illustrate that it goes further towards improving the understanding of the investors’ emotion and sentiment aspects, which affect investment decision-making (Schwarz, 2002) in a developing economy. This research focuses on the idea that investor sentiment is mediating in evaluating individual investment performance. It shows that heuristics-based investor behaviour creates investor sentiment and impacts investment performance. On the basis of this, investors need to recognize investor sentiment when making investment decisions using heuristics since such an investor sentiment will affect the performance of the investment.

We conclude this paper by maintaining that investor sentiment does show a dynamic role in stock price determination in the stock market around the world and is seen to affect stock price movement and decision-making. Since most investors are irrational, there is a massive problem in the balance of demand and supply of stock prices. It reflects the wrong picture; rational investors’ analysis may go wrong with such investor sentiment. It has been proved that all investors are not rational investors on a significant basis because they lack the essential characteristics to become actual investors or investors with the perfect data and capability to understand, evaluate and predict the stock market and its fluctuations. The result typically paints a picture of the behavioural part of variables, which reflects investor sentiment and decision-making. Using the study’s theoretical basis, human beings are organized in the market, and these markets are affected by price movements of sentiment at various rates due to different reasons and different levels of items.

This research opens new insights into the literature on investor sentiment. First, it illustrates the heuristic factors, influenced by investor sentiment and investment decision-making. It diagnoses the investors’ optimistic and pessimistic behaviour conditions. Second, in empirical analysis, the study examines availability heuristic, representativeness and overconfidence affected by the investor sentiment analysis in the Indian market. This study provides a sophisticated heterogeneous influence on the Indian stock market sentiment.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.