Abstract

This study examined the multifaceted effects of financial literacy on the inclusion of economically disadvantaged populations. Structural equation modelling with smart partial least squares (PLS) was employed to analyze the effects of financial literacy on financial inclusion. This study reveals that financial literacy exerts a multi-dimensional influence on households’ financial inclusion below the poverty threshold. Additionally, it indicates that improved access to financial services is correlated with increased usage of these resources. This study shows that access to financial services and financial literacy play a significant role in increasing households’ use of financial products, thereby promoting greater financial inclusion.

Executive Summary

This study assessed the impact of financial literacy on financial inclusion among households living below poverty line (BPL) in Kerala. It is based on primary data collected through a structured questionnaire from a sample of 384 BPL households using random sampling. To assess the influence of financial literacy on inclusion, partial least squares structural equation modelling (PLS-SEM) was used. The results revealed that financial literacy has a significant impact on financial inclusion among BPL households. Access to financial services is positively related to the usage of financial services. This study also highlights that financial literacy and access to financial services are major factors contributing to financial usage by BPL households, thereby fostering financial inclusion. There is a gap in the literature regarding the impact of financial literacy on the inclusion of BPL households. This gap has been filled by this study through its multi-dimensional analysis of financial literacy and inclusion. Financial literacy has subdimensions, such as financial awareness, knowledge, attitude and behaviour. Similarly, financial inclusion has subdimensions, such as financial access, affordability, quality and usage. This study highlighted the significance of knowledge of financial services in fostering financial inclusion in rural areas and vulnerable sections of society.

The concept of financial literacy encompasses the essential components of awareness, knowledge, competencies, perspectives and conduct required to make informed financial decisions with the aim of attaining financial well-being. Globally, financial literacy rates are low, with only 33% of individuals comprehending basic financial principles, and approximately 3.5 billion people worldwide lack financial literacy. This figure is alarmingly high when contrasted with the 2 billion unbanked individuals globally, indicating that 1.5 billion individuals with bank accounts may be financially illiterate (Fanta & Mutsonziwa, 2021). The pervasive issue of financial illiteracy is not confined to developing nations but is also a significant concern in developed countries. Nevertheless, literacy levels are particularly deficient in developing nations, as evidenced by a global survey on financial literacy (Fanta & Mutsonziwa, 2021).

Financial literacy was first introduced in the USA in 1787 (Garg & Singh, 2018). This occurred when John Adams, in correspondence with Thomas Jefferson, acknowledged the need for financial literacy to address the widespread confusion and distress across America stemming from a lack of understanding of credit, currency circulation and coin characteristics. Garg and Singh (2018) identified a significant challenge in researching financial literacy. This challenge arises from the absence of a clearly defined definition of financial literacy in existing literature. Anshika et al. (2021) define financial literacy as encompassing an understanding of fundamental financial principles and the capacity to perform basic calculations related to finances. Priya Kumari (2023) explored how financial literacy empowers individuals to effectively manage and regulate their financial affairs.

Financial inclusion is the process of enabling all members of society to access financial services and products. Financial inclusion allows people to conveniently access financial services and assists them in making financial planning and decisions, owing to its accessibility and availability (Çera et al., 2021). The NSFI (2020) recognized financial inclusion as a vital catalyst for global economic growth and poverty reduction. Without proper access to formal financial services, individuals and businesses resort to their own limited resources or costly informal financial options to meet their financial needs and pursue growth opportunities. A significant number of people within a nation do not have access to financial products and services (Bhatia & Singh, 2019).

Research carried out by Ariana et al. (2024) emphasizes that both financial and digital literacy play a crucial role in boosting financial resilience. Initially, financial literacy facilitates financial inclusion, which subsequently enhances financial decision-making and ultimately fortifies resilience against financial shocks. This insight is particularly pertinent for marginalized groups, suggesting that enhancing these literacies can enable individuals to better manage financial risks. According to Fernández-López et al. (2023), individuals with high levels of financial inclusion exhibit greater financial resilience. The perception of one’s own financial knowledge plays a role in reducing vulnerability, indicating that engaging with and having access to financial services enhances one’s capacity to endure financial disruptions. Patil and Kumar (2025) highlighted the positive impact of financial inclusion on enhancing financial resilience, particularly among vulnerable populations. They emphasized the critical roles of digital access and financial literacy in fortifying this relationship and urged more localized research efforts in developing countries.

Kerala is situated on a narrow strip of land between the Arabian Sea and the Western Ghats, occupying the southwestern portion of the Indian subcontinent. The state spans approximately 39,000 km and is characterized by an exceptionally high population density, with 747 individuals per km, significantly surpassing the national average of 267 per km. Although Kerala faces poverty, it stands out for its remarkable social development indicators, which are notably superior to those of the other Indian states. The literacy rate in Kerala, at 91%, is particularly impressive, approaching the levels typically observed in industrialized countries and emphasizing the state’s achievements in education, despite its economic constraints (Véron, 2001).

People who are unable to meet their basic necessities or achieve a minimal standard of living are considered poor. Poverty in Kerala can be understood by examining the classification of the ration card as BPL, that is, for families falling BPL and above poverty line (APL, families that do not qualify for BPL or Anthyodaya Anna Yojana (AAY)). There are a total of 9,394,853 ration card holders in the state Government of Kerala (2024), of which 359,168 are priority household ration (PHH, a pink colour card issued to family’s annual income below 24,200) and 590,569 are AAY (a yellow colour card issued to the poorest of the poor such as households with no stable income) cards coming under BPL. In this study, data were collected from both BPL-PHHs and AYY holders. To make these underprivileged people part of mainstream financial inclusion, that is, financial access, usage, affordability and quality, is necessary. At the same time, to achieve financial inclusion, individuals are required to have financial literacy that includes financial awareness, knowledge, attitude and behaviour.

This study examined how various dimensions of financial literacy affect financial inclusion in households living in BPL in Kerala, India. Specifically, this study focuses on individuals holding AAY ration cards, which fall under the PHH card category. Our study used a model to investigate the effect of financial literacy on financial inclusion. Furthermore, we conducted an analysis using structural equation modelling to validate the significance of our proposed model. This study addresses the pressing need for financial literacy as the understanding of financial services has garnered considerable attention from scholars, government officials, educators and policymakers. This study significantly enhances the existing body of knowledge across several interrelated domains, including financial inclusion, rural development, economic advancement, banking systems, microfinance initiatives, poverty alleviation strategies and efforts to reduce disparities in financial education and accessibility.

REVIEW OF LITERATURE

Financial Literacy

Khawar and Sarwar (2021) opined that a sound understanding of financial matters is essential for every individual to avoid issues related to money. Cupák et al. (2021) reveal that financial literacy occupies a pivotal role in shaping financial behaviour, making it a critical factor in addressing significant contemporary economic challenges like the increasing levels of inequality (Williams et al., 2022). Each person’s level of financial literacy and behaviour regarding money directly affects their financial well-being. It supports decision-making processes, whether they involve investments, borrowing or saving (Hermawan et al., 2022). Individuals who are financially literate have the skills to prepare for retirement and effectively manage savings (Lusardi & Mitchell, 2014). Financial behaviour and literacy are influenced by a person’s household earnings, wealth and socio-economic environment (Buckland et al., 2024).

Financial Inclusion

Nguyen and Luong (2023) find that improving financial inclusion is essential for enhancing economic growth and reducing inequalities in wealth. According to Ren et al. (2023), financial inclusion is a process that ensures all people within a country have access to, affordability of, and use of the financial system. Mahmood et al. (2022) stated that promoting inclusive finance has the potential to serve as a catalyst for fair and comprehensive growth, enabling individuals to compete effectively in economic opportunities (Bhatia & Singh, 2019). Financial services that are affordable to everyone have emerged as a fundamental priority in numerous countries, including India (Çera et al., 2021). Establishing an inclusive economy accessible to all in terms of financial products and services requires prioritizing awareness among the financially excluded. Financial literacy stands out as a key programme. Some strategies to attain financial inclusion include reducing interest rates, deploying targeted government expenditure, decoupling financial inclusion from environmental influence and establishing specialized banking facilities for the underprivileged (Ozili, 2022; Priya Kumari, 2023). Financial inclusion aims to ensure that everyone, particularly underserved individuals, has access to and can use financial services. On the other hand, financial literacy provides people with the understanding and assurance required to use these services effectively. Consequently, financial literacy and inclusion are intrinsically linked; financial literacy serves as a crucial facilitator of financial inclusion, enabling individuals to navigate the financial system, access it and benefit from it. This connection lays the groundwork for exploring how each influences the other.

Impact of Financial Literacy on Financial Inclusion

Leon (2020) commended that enhancing financial literacy not only boosts individuals’ capacity to make informed financial choices but also enhances their self-assurance, thereby enabling them to confidently utilize formal financial services. Umer et al. (2023) emphasize that the significance of improving cognitive skills and financial literacy among women is crucial for fostering financial inclusion. Mujiatun et al. (2023) found empirical evidence demonstrating the direct influence of financial literacy theory on both financial inclusion and business operations within the halal tourism industry. Nagpal et al. (2022) identified a positive relationship between financial knowledge and behaviour across the three financial literacy dimensions. Hasan et al. (2021) showed that a firm’s development and access to finance were favourably influenced by financial literacy. Leon (2020) opined that individuals are directed to take action that affects financial inclusion and reach financial services when they assess a behaviour or attitude that helps them attain particular goals. Jin et al. (2024) revealed that financial inclusion is greatly influenced by household and financial literacy. Okello Candiya Bongomin et al. (2024) tailored financial education to improve consumer protection and encourage financial inclusion. Candiya Bongomin et al. (2007) concluded that only the financial literacy component substantially and favourably affects the financial inclusion of low-income rural Ugandan families. Mindra and Moya (2017) identify the relationship between financial literacy, attitude and financial inclusion. The implementation of financial literacy programmes aims to improve the financial knowledge of marginalized groups in society (Singh & Malik, 2022).

The existing body of research characterizes financial inclusion through four primary dimensions: access, affordability, usage and quality of financial services. This study adopts this framework by interpreting the use of financial services as a consequence of three other dimensions: access, affordability and quality. Figure 1 depicts this logical sequence and illustrates how improvements in access, affordability and quality can lead to increased usage.

The literature review was critically examined to enhance the analysis of sub-themes. Although there is general agreement on the positive link between financial literacy and financial inclusion, some studies highlight subtle differences, such as the distinct effects of components like attitude, knowledge and behaviour, indicating that not all findings are completely consistent. Additionally, structural obstacles such as low income, restricted access to formal financial services, insufficient targeted financial education and sociocultural limitations, particularly impacting marginalized groups, have not been thoroughly examined in the current literature. Key findings suggest that financial literacy boosts confidence, decision-making and access to financial systems, especially when interventions are customized for vulnerable populations. However, there are notable gaps, including a lack of focus on BPL households in rural India and a limited exploration of how awareness of government schemes might affect the relationship between financial literacy and inclusion. This study aims to fill these gaps by examining the contextualized impact of financial literacy on financial inclusion among BPL households with an emphasis on structural challenges. Therefore, financial literacy influences financial inclusion. Building on this evidence, it is anticipated that the financial literacy level of BPL households also influences their financial inclusion. Therefore, the following hypothesis was formulated:

H1: The financial literacy of BPL households in Kerala significantly influences their financial inclusion.

THEORETICAL BACKGROUND

Financial literacy can be described as practical knowledge and understanding of the responsibility for managing personal finances. It encompasses the ability of individuals or families to effectively utilize various financial tools and skills to handle income, expenditures, savings, investments and debt. A crucial aspect of financial literacy is understanding how to protect one’s financial future, optimize savings and investments, make wise spending and borrowing decisions and enhance income. To improve financial literacy, individuals can access resources such as books, magazines, journals and online content; engage with audiovisual materials; and consult financial professionals. This knowledge empowers people to make informed decisions regarding money and financial well-being (Singh et al., 2024). The Organization for Economic Cooperation and Development (OECD) characterizes financial literacy as a combination of attitudes, behaviours, knowledge, skills and awareness essential for making sound financial decisions and achieving personal monetary well-being (Van Nguyen et al., 2022).

Financial literacy encompasses the comprehension and acquisition of knowledge of various monetary matters, including fiscal management, capital allocation and individual financial planning. Broadly speaking, financial literacy involves the ability to handle personal finances, make sound and efficient monetary choices (such as investments, purchases or real estate acquisitions), plan for children’s educational expenses and prepare for future financial needs. Additionally, it encompasses the skills needed to budget and allocate funds effectively, handle credit responsibly, compute simple and compound interest rates, and judiciously utilize money. Financial literacy equips individuals to understand diverse financial concepts, markets and instruments, such as stocks, bonds and mutual funds, thereby improving their economic position and mitigating financial risks. A combination of knowledge, awareness and attitude regarding financial products and services enables people to make judicious and appropriate monetary choices. A crucial aspect of financial literacy is demonstrated through an understanding of financial products (Murugesan & Manohar, 2022).

According to Sarma, financial inclusion refers to a system that facilitates easy access to, availability of, and use of formal financial services by all individuals in an economy (Mahmood et al., 2022). Financial inclusion refers to the provision of affordable and beneficial financial services to underprivileged and low-income individuals in a sustainable manner (Naili et al., 2023). According to Allen et al. (2016), financial inclusion refers to the endeavour to provide all individuals in an economy with access to essential formal financial services that are secure, suitable and cost-effective. This process particularly targets underserved populations such as women, individuals with disabilities, and those without employment (Jin et al., 2024). Financial inclusion encompasses the provision of affordable financial services to underprivileged segments of society, with minimal transaction costs and fees (Deepamala, 2017).

According to Ren et al. (2023), financial inclusion refers to the process that ensures that all economic participants have ready access to, availability of, and utilization of the financial system. This concept involves providing underprivileged and economically marginalized individuals with access to formal financial services, including essential bank accounts, credit facilities, insurance products and payment systems, at affordable rates and in a timely manner (Khuan, 2024). The core aim of financial inclusion is to extend banking services to individuals who lack access, thereby enhancing the quality of life and fostering economic progress. This concept encompasses the reach, adoption and obtainability of various financial offerings, including lending facilities, insurance products and savings options. Financial inclusion is frequently advocated as a policy mechanism to bolster the investment potential of economically challenged households. By providing these households with opportunities to accumulate greater savings for productive investments such as educational pursuits and skills training, financial inclusion can potentially enhance their capacity to make meaningful investments in the future (Bari et al., 2024).

The capacity approach developed by Sen (1999) offers a comprehensive framework for evaluating social structures and individual well-being while also guiding policy creation and societal improvement. This approach has wide-ranging applications, including development studies, welfare economics, social policy and political philosophy. It can be used to evaluate various aspects of human well-being, such as poverty, inequality and the overall welfare of a group. The capacity approach serves as a versatile tool for shaping and assessing policies, ranging from welfare state design in affluent societies to development initiatives implemented by governments and non-governmental organizations (NGOs) in developing countries. Additionally, it can function as an alternative method for conducting social cost-benefit analyzes. A key aspect of the capability approach is its emphasis on individuals’ abilities, specifically on what they can effectively accomplish and become (Robeyns, 2005). This theory suggests that enhancing financial literacy enables individuals to make sound monetary decisions. As people become more financially literate, they are more likely to effectively manage risks, use financial services and improve their economic well-being, promoting greater financial inclusion. Moreover, the capability approach emphasizes the importance of providing individuals with the freedom to pursue aspirations. In the context of financial inclusion and literacy, this concept implies that people have access to a diverse range of financial products and services that align with their specific needs.

Conceptual Framework

The proposed model, created on the basis of literature and theory background, was expected to be in line with survey data.

METHODOLOGY

Research Design

This study examined the effects of financial literacy on financial inclusion among households BPL in Kerala. This study employed a combination of descriptive and analytical research designs and utilized survey methods to gather data. By examining the relationship between financial literacy and inclusion, this study aims to provide insights into how financial knowledge influences financial services among the target population.

Population and Sample Size

The population size in the study was 4,182,253, as of 31 October 2023 (Government of Kerala, 2024). An adequate sample size of 384 based on the Krejcie and Morgan table (Morgan, 1970) was found to be representative of the population. With each ration cardholder representing a single unit of analysis, the respondents underwent extensive testing. To assess the impact of financial literacy on inclusion among BPL households, 384 respondents were carefully surveyed from three regions of Kerala, that is, Travancore, Cochin and Malabar, during the data collection process.

Sampling Procedure and Design

This study applied an exhaustive multistage sampling technique to accurately represent Kerala’s varied population. The state was first divided into the Malabar, Travancore and Cochin regions. A district was randomly selected from each region, and a taluk, that is, a sub-district administrative unit, was randomly selected within each district. The next phase of this procedure involved choosing a panchayat for each taluka. In the final stage, 384 BPL households were selected for the study using a purposive sampling method (Teddlie & Yu, 2007). Purposive sampling was employed in the final phase due to experiences during the pilot study at the field level. This method was chosen to ensure that participants who met the study criteria and could effectively participate in the survey were selected, thereby enhancing data reliability. Although this approach is non-random, it is crucial to effectively achieve the research goals while reducing the risk of non-response bias.

Measurement of Variables

The main objective of this study was to assess how financial literacy affects the financial inclusion of BPL households in Kerala. The two crucial concepts considered in this study are financial literacy and financial inclusion. Financial inclusion was assessed using scales adapted from previous studies (Siddiqui, 2021; Singh, 2023), which considered factors of access, usage, affordability and quality, which proved to be valid and reliable. To properly retrieve the respondents’ perceptions, the measurement items for each construct were assessed on a five-point Likert scale, ranging from strongly agree to strongly disagree. After exhaustive reliability and validity testing, a high alpha coefficient and total variance were obtained. These excellent results confirm the efficiency of the assessment instrument employed, ensuring an accurate assessment of the financial inclusion of BPL households.

A broad range of constructs, including financial awareness, attitude, knowledge and behaviour, were considered when assessing financial literacy. Researchers have used measurement scales adapted to fit the needs of this research environment, drawing on previous studies (Banthia & Dey, 2022; Siddiqui, 2021; Singh, 2023). Respondents assessed the items in the questionnaire on a five-point scale. Strong internal consistency and validity were verified by applying reliability and validity tests (Tables 1–3). These results highlight the efficiency of the assessment instrument and enable a comprehensive investigation of the financial literacy of BPL households in Kerala. The questionnaire items are listed in Table 4.

Construct Reliability and Validity.

Discriminant Validity—Fornell–Larcker Criteria.

Heterotrait-monotrait (HTMT) Matrix.

Items Included in the Questionnaire of the Study.

Data Collection

The study utilized a semi-structured questionnaire, with measurement items sourced from prior research studies. Furthermore, exploratory factor analysis (EFA) was employed to refine the questionnaire, eliminating ambiguous and double-barrelled questions to enhance clarity and precision. Most of the data were collected directly by the researchers, and when additional field investigators were involved, they received structured training from the research teams (See Appendix A available online as supplementary material for additional details).

RESULTS

An analysis of the demographic data of the 384 respondents is shown in Table 5. The survey revealed a predominance of female participants (67.4%) compared to male participants (32.6%). The age distribution showed that 56.8% were aged 20–30, 37% were 30–40, and 6.2% fell outside these ranges. Residential patterns were 45.8% from rural areas, 29.2% from semi-urban locales, and 25% from urban centres. The educational background was primarily college level (93.5%), with a small fraction (6.5%) having school or higher secondary education.

Demographic Profile of the Respondents.

Geographically, Malabar represented the majority (85.7%), followed by Cochin (7.6%) and Travancore (6.8%). The increase in respondents from Malabar was not due to a regional concentration of eligible participants, as the target group of female BPL farmers was spread across all selected areas. Instead, the differences in data frequency were due to practical field-level factors such as ease of access, respondent availability and logistical efficiencies encountered during data collection at the Malabar site. Monthly income levels were distributed as follows: 54.2% earned up to ₹6,000, 27.2% between ₹6,000 and ₹12,000, and 18.8% in the ₹12,000–₹18,000 range.

EFA

EFA and principal component analysis (PCA) with Varimax rotation were employed to explore important factors. A high Kaiser–Meyer–Olkin (KMO) measure (0.918) and a statistically significant Bartlett’s Test of Sphericity (p less than .001) were applied to ensure the validity of the data. Variables FB-2 and FAF-5 were removed owing to their small coefficients of efficiency. Ultimately, the study considered 44 elements yielding eight factors. These eight factors were financial awareness, attitude, behaviour, knowledge, affordability, access, usage and quality. Collectively, these were responsible for a considerable percentage (71.89%) of the total variation explained by the model.

Measurement Model

The Cronbach’s alpha value, which measures the internal consistency, is more than the threshold limit of .7 for all dimensions, guaranteeing the reliability of the instrument. Furthermore, for every construct, the average variance extracted (AVE) and composite reliability (CR) values, both of which indicate convergent validity, are above the suggested thresholds of 0.5 and 0.7, respectively, indicating that the items within each construct accurately measure the intended underlying concept. This study later established discriminant validity. Based on the research results, each construct’s AVE square root exceeded its association with the other constructs. Furthermore, every value in the heterotrait-monotrait (HTMT) matrix was less than 0.85, which strongly suggests that each construct has discriminant validity (see Tables 1–3).

Structural Model

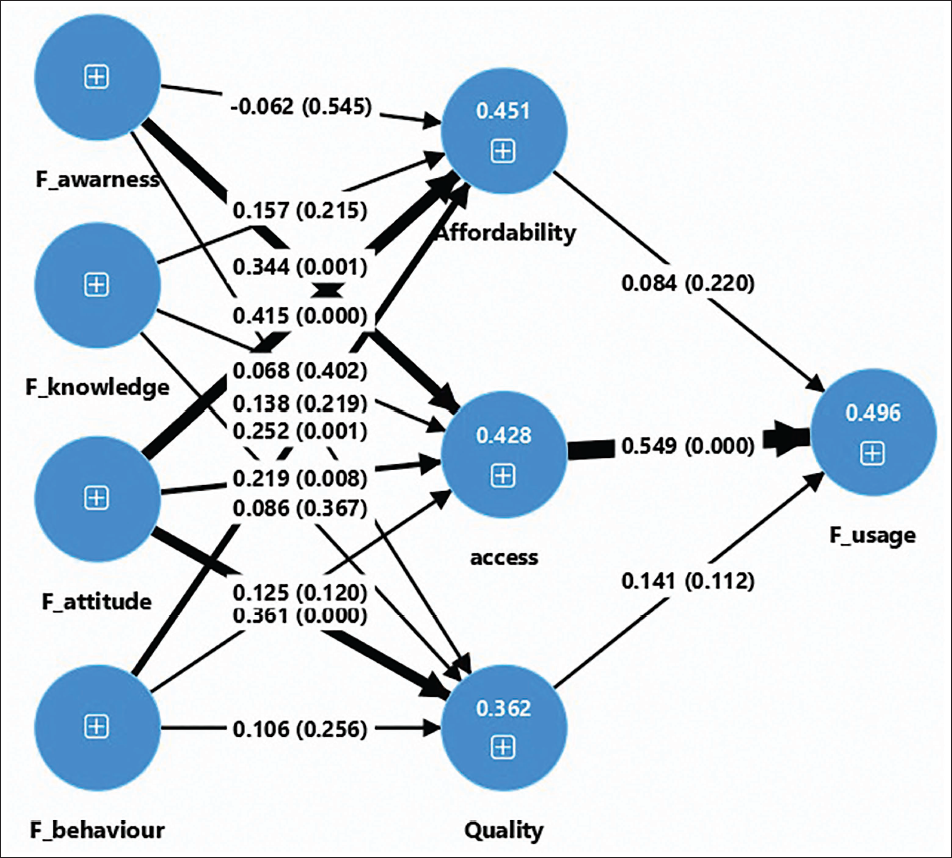

As the structural model indicates the significant role and relevance of the path coefficients, it is essential that the analysis be conducted. Measures like R2 and Q2 are used to assess the model’s quality. These metrics contribute to evaluating the effectiveness and precision of the model’s predictions. The predictive accuracy of R2 is evaluated using threshold values of 0.25, 0.50 and 0.75, which resemble low, moderate and high levels of predictive accuracy. Therefore, it was identified that usage, affordability and access have an almost moderate predictive accuracy, with values 0.496, 0451 and 0.421, while quality has an almost weak predictive accuracy, indicated by the value of 0.362. In addition, the investigator employed the blindfolding strategy in the Q2 test to evaluate the dependent variable’s predictive relevance. In this test, it is generally expected that the Q2 value will exceed zero, and it shows a strong predictive relevance, indicated by the Q2 value is more than 35%.

Path coefficient analysis was then used by the researcher to determine relationships between variables, validate model fit, and locate important factors. Multiple hypotheses and related statistical findings are generated by the investigation (see Table 6). The hypotheses of H1b, H1c, H1d, H1g, H1h and H1o were all accepted with p value less than .05. This shows that there is a significant influence of financial attitude on affordability, attitude towards quality and towards access. Financial awareness has a significant influence on access, whereas financial behaviour influences affordability. Finally, financial access passively influences financial usage. All other hypotheses (H1a, H1e, H1f, H1i, H1j, H1k, H1l, H1m, H1n) were rejected because of insignificant p values (p > .05).

Path Coefficient.

DISCUSSION

This study explores the impact of financial literacy on financial inclusion among female farmers in Kerala who fall under the BPL, a group often overlooked despite efforts to promote financial inclusion. While prior studies have extensively validated the connection between financial literacy and inclusion, this study offers new perspectives by examining this link within the context of economically disadvantaged rural women and by emphasizing the role of structural barriers and socio-economic challenges in shaping these interactions. These findings strongly support our proposed relationship. Specifically, elements of financial literacy, such as financial attitude, awareness and behaviour, were found to significantly improve aspects of financial inclusion, including affordability, access, quality and usage. While these findings align with prior research, they do not specifically target BPL families (Siddiqui, 2021; Singh, 2023; Twumasi et al., 2022). The supported hypotheses include H1B (financial awareness → financial access), H1C (financial behaviour → affordability), H1D (financial attitude → quality), H1G (financial awareness → usage), H1H (financial behaviour → access) and H1O (financial attitude → affordability). These results are consistent with those of previous studies (Siddiqui, 2021; Singh, 2023; Widodo et al., 2022); however, they extend this understanding by confirming that these relationships hold even among socio-economically disadvantaged groups.

Financial attitude has emerged as a particularly strong predictor, exerting a significant and positive influence on multiple aspects of financial inclusion, particularly access, affordability and quality. This indicates that for female BPL farmers, a positive financial mindset and self-confidence are vital for navigating formal financial systems, which are often marked by procedural complexity and institutional mistrust. Furthermore, the results highlight that improved financial access—a crucial aspect of inclusion—is essential for the practical use of services. Even when financial awareness is present, barriers to access, such as travel distance, documentation requirements and digital illiteracy, can hinder usage. The significant relationship between awareness and usage (H1G) highlights the potential of well-designed educational interventions to bridge this gap, but only when accompanied by structural improvements.

The findings also suggest that women with BPL are not a uniform group; their behaviour is influenced by intersecting constraints, including income instability, limited exposure and social norms. While the positive outcomes align with the broader literature on financial inclusion, this study advances the discussion by demonstrating how financial literacy functions differently across marginalized groups. In summary, this study validates key theoretical pathways and provides empirical evidence that financial literacy, particularly attitude and behaviour, can significantly enhance inclusion outcomes in vulnerable populations, which is consistent with prior research (Siddiqui, 2021; Singh, 2023). These results emphasize the need for tailored interventions that not only build knowledge but also boost financial confidence and eliminate systemic barriers for female BPL farmers.

CONCLUSION

The findings of this study yielded several policy-relevant conclusions. Notably, our study demonstrates that, while financial literacy is vital for boosting financial inclusion, certain elements of financial literacy are crucial for realizing specific financial inclusion targets. This insight is critical for the development of effective financial education curricula. The positive impact of financial literacy on financial decision-making is well documented. However, this study is the first to investigate the relationship between financial literacy and financial inclusion on a national scale, focusing on populations living in BPL. This unique approach allows us to examine the varying effects of financial literacy on financial inclusion. Understanding whether financial literacy influences financial inclusion and how this influence differs according to country-specific factors is essential for policymakers to boost financial inclusion. Moreover, analyzing financial literacy and inclusion across multiple countries provides greater external validity than studies that rely on data from a single nation.

The study, conducted in Kerala, examines the role of financial literacy in accessing financial inclusion using a structural equation model. This research focuses on two primary dimensions: financial literacy and financial inclusion. Financial literacy encompasses attitudes, awareness, knowledge and behaviour, whereas financial inclusion comprises access, usage, affordability and quality. Some dimensions yielded inconclusive results due to participants’ limited familiarity with certain financial activities, supporting the hypothesis that a lack of financial knowledge impedes the development of financial access. The empirical findings generally indicate a positive correlation between financial literacy and access to finance. Financial awareness has emerged as a crucial factor in enhancing financial inclusion, with the potential to significantly improve financial communication among rural and low-income populations. A comprehensive understanding of diverse financial services was found to strongly influence financial access and expand the use of other financial services. However, rural respondents’ knowledge remains limited to a narrow range of banking services and activities. The study highlighted that financial institutions have not adequately prioritized educating rural populations about financial access, suggesting a need for improved financial education initiatives in these areas.

This study contributes to the literature on household financial inclusion by being the first to investigate how financial literacy affects the financial inclusion of households living in BPL in Kerala, India. This study examines specific dimensions of financial literacy, including financial attitude, awareness, knowledge and behaviour, as well as aspects of financial inclusion such as access, usage, affordability and quality. The results demonstrate the multifaceted influence of financial literacy on financial inclusion, emphasizing the crucial role of financial attitudes and behaviours in affecting financial affordability, quality and access. Additionally, this study reveals that financial awareness and behaviour influence access and affordability. Finally, the findings indicate that financial access positively affects financial usage.

Policy Implication

Studies on financial literacy among households, BPL play a crucial role in discussions of inclusive finance, highlighting the importance of service-specific knowledge in boosting financial inclusion in rural and vulnerable communities. To address this issue, we propose adopting the Financial Education Programme used by Financial Sector Deepening Kenya (FSD Kenya, an independent trust), which has successfully influenced financial behaviour in low-income groups through community-based, context-sensitive delivery. This approach is particularly applicable to India, a developing nation, because it emphasizes straightforward practical content delivered via trusted local networks using multimedia, interactive sessions and peer facilitators. In India, the programme can be executed through collaboration with local NGOs, self-help groups, panchayats and banking correspondents using regional materials and real-life examples to ensure accessibility and relevance. Implementation should also include training community educators, incorporating digital tools, such as mobile learning, and establishing ongoing support systems. The programme’s impact can be assessed by observing changes in financial product usage, enhanced budgeting practices, and increased confidence in household decision-making. Implementing this model can result in scalable improvements in financial literacy at the grassroots level, thereby directly supporting financial inclusion and empowerment of low-income rural households in India.

Limitation and Future Research

Subsequent research could examine financial inclusion across nations and regions, particularly in less developed and emerging economies, where it remains a concern. Financial literacy metrics can be developed, especially in underdeveloped and developing countries. Additionally, as financial technology has emerged as a leading method of financial communication, there are opportunities for future investigations to examine financial innovation education and the expansion of fintech accessibility across all demographic groups. A cross-sectional research approach can be employed to collect data using a semi-structured instrument. Future research could benefit from implementing a longitudinal design to examine the evolving characteristics of the study samples over an extended period. This study focuses exclusively on households living below the poverty threshold in Kerala, India, excluding other ration card holders from the very poor and upper-class categories. Subsequent investigations may consider expanding the scope to include various ration card holder classifications, other Indian states, and developing countries for comparison.

In addition to these constraints, the results of this study should be interpreted with caution, given its specific context. The research was conducted in certain districts of Kerala, where unique socio-economic, institutional and cultural factors may not represent the conditions in other areas. Consequently, there is a risk of overgeneralization and applying these findings more broadly should be performed with caution. Additionally, while the study shows the important role of financial literacy in promoting financial inclusion, it does not explore deeper structural obstacles, such as intricate bureaucratic procedures, entrenched cultural norms and gender-based exclusions, which can persist even when financial awareness and education are present. These systemic barriers fall outside the scope of the current research but are crucial areas for future study to gain a more comprehensive understanding of the challenges to inclusive financial systems.

To enhance our understanding of the long-term effects of financial literacy, future studies could use longitudinal approaches that monitor individuals or households over extended periods. These methods would enable researchers to evaluate how ongoing financial literacy programmes affect financial inclusion paths and reinforce economic resilience, particularly among vulnerable groups. A longitudinal view would also help understand how financial behaviours change with continuous financial education, shifting economic conditions and adaptive learning. This time-based perspective could offer valuable insights into whether advancements in financial literacy result in lasting changes in saving behaviours, credit utilization, digital financial engagement and risk-management strategies, thereby guiding more effective evidence-based policy measures.

Footnotes

ACKNOWLEDGEMENTS

The authors express their sincere gratitude to the Postgraduate and Research Department of Commerce, Government Victoria College, Palakkad, for providing the necessary academic support and resources to carry out this study. The authors extend their heartfelt thanks to Dr Binu C. Kuryan, Head of the Department, for his constant encouragement and guidance. The authors also acknowledge the valuable assistance of fellow research scholars who contributed to the data collection process.

AUTHORS CONTRIBUTION

Fazal P conceived and designed the study, conducted data collection along with Sunitha TI, and performed the data analysis. Fazal P also prepared the original draft of the manuscript. Sunitha TI contributed to data collection. Dr Mohanadasan T provided critical review and editing of the manuscript and supervised the research process. All authors read and approved the final manuscript.

CONSENT FOR PUBLICATION

This study does not include identifiable individual person data, images or videos.

DATA AVAILABILITY STATEMENT

The data sets generated and analyzed during the current study are available from the corresponding author upon reasonable request.

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

ETHICAL APPROVAL AND INFORMED CONSENT

The study was approved by the Institutional Ethics Committee of the Postgraduate and Research Department of Commerce, Government Victoria College, Palakkad, as documented in the ethical approval letter signed by the Head of the Department. Informed consent was obtained from all participants prior to their inclusion in the study.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.

SUPPLEMENTARY MATERIAL

email:

email:

email:

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.