Abstract

Digital payments have emerged as the predominant payment method in India since the introduction of the unified payments interface (UPI) in 2016. This study investigates how this digital transformation has impacted the ease-of-doing business for people residing in rural India. We conduct a computational thematic analysis using a topic modelling technique to analyse unstructured feedback given by sole-ownership-type entrepreneurs operating in the unorganized labour market in rural India to identify the beneficial aspects of UPI on their businesses. The analysis reveals that UPI users appreciate the ease of transactions, unconstrained access to funds, wider reach of customers and transparent monetary transactions.

Executive Summary

Digital payments have emerged as the predominant method of payment in India since the introduction of the unified payments interface (UPI) in 2016. India has been traditionally a cash-heavy economy, and Indian businesspeople have been accustomed to drawing cash from banks or ATMs to conduct transactions. India does not boast a robust banking system in its rural corners. This creates huge inconvenience among rural traders to execute financial transactions due to a lack of funds. The advent of UPI has brought about a significant change to the professional activities of rural Indians. This study undertakes a scoping investigation of the extent to which this digital transformation has impacted the ease-of-doing business for people residing in rural areas of India. We conducted a computational thematic analysis through semi-structured interviews with 801 UPI users in rural locations of India, utilizing the topic modelling technique latent Dirichlet allocation. This approach is intended to address the issue of credibility that is commonly cited as a major drawback of qualitative research designs. The primary objective was to comprehend the major issues shared by the users regarding their UPI experience with regard to their business-related transactions. The analysis reveals that businesspeople from rural India who have been using UPI appreciate the ease of transactions facilitated by this technology and are content with the benefits it offers to entrepreneurs and workers in the unorganized sector. In terms of ease-of-doing business, the findings revealed that the major benefits were in terms of leveraging more transactions with tourists, which were earlier declined due to a lack of cash, more transparency of transactions, speed of transaction and reduced reliance on middlemen. However, the participants also expressed concerns about security issues and challenges arising from inadequate infrastructure, lack of a legal framework to safeguard against such type of malicious attacks and the potential for fraud.

The landscape of payment systems in India has undergone a significant transformation with the integration of digital technology. The introduction of the unified payments interface (UPI) by the National Payments Corporation of India (NPCI) in 2016 has spurred a substantial increase in digital transactions (Ahluwalia, 2021). This evolution, witnessed over the past few years, is propelled by government initiatives, technological advancements and evolving consumer preferences. The success of the Digital India Campaign, aimed at making government services electronically accessible to all citizens and fostering a digitally empowered society, is evident in its widespread adoption across the country (Indian Express, 2015). The adoption of digital payment methods represents a major transformation in the country’s payment landscape (Tiwari et al., 2019). These collective efforts stand as one of the most notable success stories in the digital transformation of society (Dani, 2022).

The initial step in this transformative process can be attributed to the initiative of targeting every Indian who had been without a bank account even after more than 65 years of Independence. The government strategically extended the reach of banks to the remotest corners of India’s vast landscape, to integrate every individual or at least every family, into the country’s financial system (Kajol & Singh, 2022; Sahu & Singh, 2018). This landmark achievement facilitated their inclusion in the mainstream economy, ensuring direct disbursement of their dues into bank accounts and significantly heightened their awareness of banking transactions. With time, the increased availability of banking services and improved network connectivity further enhanced their familiarity with digital transactions, encompassing internet banking and the emergence of the UPI system (Sivathanu, 2019). The UPI penetration rate stands at 56% for the bottom 40% of India’s population (average annual household income: INR 1.10 lakh1) while the same for the poorest income group is 26%, as per the SIDE Report, 2023. The major players in the UPI market of India are PhonePe, Paytm and Google Pay. PhonePe constitutes four thousand million in volume and seven trillion INR in value, while Google Pay constitutes three thousand million in volume and four trillion INR in value (Gupta, 2023).

The latest figure released by the NPCI reveals that the digital payments in India have recorded 8.9 billion transactions in April 2023, with a total value of INR 14.07 trillion (Kayastha, 2023). While this is encouraging and commendable, there remain certain causes for concern among the end users about the benefits of using this new technology, and this has resulted in roadblocks in the way of UPI’s universal adoption in India at the desired level (Agarwal, 2021). In recent times, there has also been a slow dip in UPI usage in India (Kayastha, 2023). UPI frauds are also on the rise in the post-COVID scenario (Bhati, 2023), and there is still a major section of Indian society that trusts paper currency transactions to UPI (Baghla, 2018; Ligon et al., 2019).

In the context of the above, the present study attempts to probe Indian rural citizens’ perception towards their experience of using digital payment options and whether they are satisfied or if they have any concern regarding such use through a thematic analysis of qualitative feedback shared by business owners and customers from rural India. We have used a computational thematic analysis approach through topic modelling (Blei, 2012) to identify the topics and the corresponding themes representing the topics. Subsequently, we highlight the sentiment analysis findings. Finally, the study draws a conclusion and provides policy recommendations in context to the findings.

LITERATURE REVIEW: USER REACTION TOWARDS ADOPTION OF UPI FACTORS THAT MAY HINDER UPI ADOPTION IN RURAL INDIA

One of the major factors which may hamper the adoption of new technology by people is the issue of novelty. Ejiaku (2014) highlights that in the case of developing nations, this challenge is even bigger. The perceived novelty of a new technology stems from various attributes such as unfamiliarity, complexity, believability and relative advantage (Mukherjee & Hoyer, 2001; Rogers, 1962). Depending on how end users perceive the novelty of new technology, their affective states are influenced accordingly (Clark, 1982). Such affective states may lead to unpleasant reactions in the mind of the end user if they comprehend the stimuli as an unprecedented experience, or it can also create a pleasant reaction if the stimulus is able to create interest in the mind of the end users (Smith & Ellsworth, 1985). A principal reason behind the slow adoption of digital technologies in emerging economies is the perceived novelty of the technology to end users.

As per the theory of technology diffusion (Rogers, 1962), any new idea or product becomes popular and diffuses through a specific population or social system gradually with time. It can be speculated that how consumers perceive the novelty of a new technology will influence their perception of the rewards and risks associated with it. In the context of research on IT innovation, the role of perceived novelty has not been explored in depth (Featherman & Pavlou, 2003; Venkatesh & Davis, 1996).

In the context of digital payments, Indian end users may have to deal with the novelty of the system, as they have been traditionally accustomed to cash transactions. India has also been slow towards the adoption of information and communication technology, and it is only in the decade between 2010 and 2020 that rapid growth in innovative technologies such as mobile apps, e-commerce, online transactions and online payment systems became popular (Bodur et al., 2015). UPI is a similar type of technological innovation regarding which the general Indian public had very little idea or orientation before 2015. Hence, it is natural for Indian users to feel apprehensive about using digital payments through UPI. However, empirical studies have not yet been able to understand the main reasons behind the lack of technology adoption in the digital payment context, and whether novelty plays any role in this context (Kumar & Chawla, 2023). Hence, in this study we aim to investigate this aspect.

Another major factor which might hinder the adoption and use of digital technology is the lack of trust in using such technologies. Trust is one of the main reasons why consumers make the final decision to purchase any product (Oliveira et al., 2017). Factors such as security and risk play an important role in purchasing any product or service in a digital context (Gefen & Straub, 2004; Kim et al., 2008). Especially when a service is related to financial transactions through online networks, as in digital payment services, then the issue of trust becomes even more critical (Agárdi & Alt, 2022; Qasim & Abu-Shanab, 2016). Trust is an essential driver of technology adoption and helps in mitigating their perceived uncertainty and developing long-lasting relationships (Mcknight & Chervany, 2001; Patil et al., 2020).

One of the major issues that causes a lack of trust in the context of online payment systems is the increase in cyberattacks in recent times. Issues of phishing and other cyber frauds have been reported several times in recent times (Reaves et al., 2017; Tan et al, 2014). The Tesco Bank in the United Kingdom has reported a theft of $5 million from thousands of customers, and bitcoins worth a value of $65 million were stolen from a Hong Kong digital currency exchange (Gibbs, 2016). In countries like Ghana, more than 100 million dollars of cybertheft issues have been reported (Amofah & Chai, 2022). In India, the situation is equally dire, where more than half of financial frauds involve digital payment-related scams (Bloomberg, 2025). In India, UPI accounts for transactions worth $3 trillion per year, and it has become a hotbed for scammers and cyber fraudsters. Therefore, there is a need to explore how the perceived trust of Indian consumers towards UPI leads to their decision to use digital payment systems (Pillai et al., 2019).

From the literature, it is understood that novelty and trust play an important role in helping consumers make decisions to use digital payment systems. In the Indian context, studies have not been conducted to check the effect of trust and novelty as drivers of rural business owner’s decision-making towards digital payment app use (Al-Qudah et al., 2024; Sahi et al., 2022). Other factors may also be involved in this context. Hence, we decided to adopt a qualitative perspective while developing our research design. In the subsequent sections, the methodology, sample selection and analysis are described.

METHODOLOGY

The aim of this research is to explore and analyse qualitative responses provided by rural Indian businesspeople involved in small and micro enterprises to discern and uncover the central themes of the discussion and subsequent observations related to their use of UPI/digital payment. This examination employs computational thematic analysis, as outlined by Delgosha and colleagues (2022), utilizing the LDA technique (Ossai & Wickramasinghe, 2023). LDA has gained popularity as a data analysis technique for effective extraction of latent themes from a textual corpus (Maier et al., 2021). LDA models draw on an abstract hypothetical probabilistic process that implies different assumptions. It has proven to be a powerful approach for quickly identifying major thematic clusters in large text corpora and modelling topics as latent structures within a text corpus. The primary topics of discussion from the consumer standpoint are visually represented through multidimensional scaling.

Sample Selection

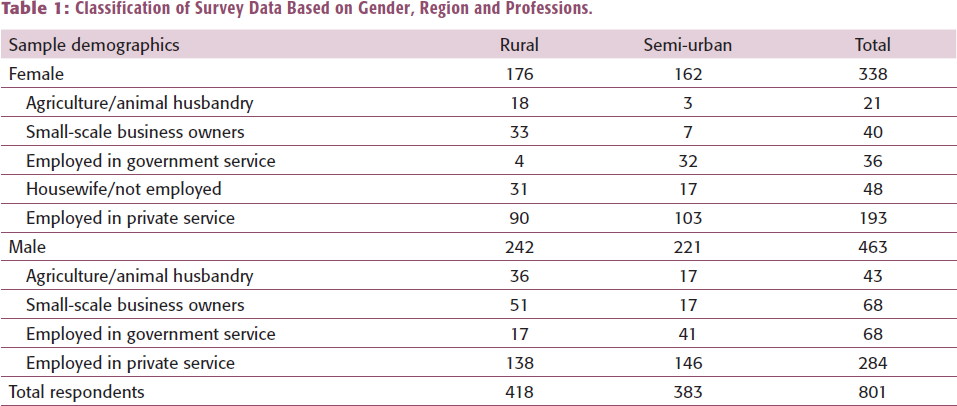

The data were gathered through a questionnaire-based survey. The questionnaire captured individual data, such as their age groups, professions and regions across India, covering the eastern, western, northern, southern and northeastern states. Throughout the process, 846 responses were collected from 12 different states in India. Following data cleaning procedures, a final sample of 801 usable responses was considered for the present analysis.

Descriptive Analysis of Primary Data

The collection of primary data was carried out via a survey based on semi-structured questions, encompassing rural Indian respondents from a nationwide survey that spanned 27 states and Union territories in India between May 2024 to July 2024. The survey ensured representation from various professions and regions. This study is based on a final sample size of 801 participants. Gender-wise classification reveals that 338 female and 463 male respondents were interviewed during the survey. Further details regarding the classification of samples by gender, region and profession can be found in the accompanying Table 1.

Classification of Survey Data Based on Gender, Region and Professions.

QUALITATIVE ANALYSIS OF CONSUMER PERCEPTION TOWARDS UPI

Emic and etic approaches, each carrying inherent strengths and weaknesses, have fuelled ongoing scholarly debates regarding their comparative efficacy (Delgosha et al., 2022). A growing consensus among scholars favours innovative techniques that can synergize the strengths of both approaches, mitigating the inherent trade-offs between quantitative and qualitative research designs (Creswell & Clark, 2011; Wu, 2022). This study adopts a computational thematic analysis approach, employing the topic modelling technique with LDA as proposed by Blei (2012) to extract key topics from qualitative responses obtained in our survey. Topic modelling is a technique designed to automatically identify and unveil topics present in a corpus, revealing latent patterns within it (Blei, 2012). As an unsupervised approach, topic modelling is adept at discovering and examining clusters of words, referred to as ‘topics’, within extensive textual data. These topics are characterized as recurring patterns of co-occurring terms in a corpus. Topic Models serve various purposes, including document clustering, organizing large volumes of textual data, information retrieval from unstructured text and feature selection. Among the array of topic modelling techniques, this study specifically adopts the LDA approach. LDA is the most popular topic modelling technique and is used to find the relationship between several documents in a corpus (Blei, Ng & Jordan, 2003). LDA assumes documents are produced from a mixture of topics.

Recent investigations by Gauthier and colleagues (2023) assert the superiority of computational thematic analysis over manual approaches. There is a growing advocacy for an integrated approach that combines computational and qualitative methodologies, ensuring a richer and more in-depth analysis devoid of the subjectivity inherent in manual qualitative analysis. While Gauthier and colleagues have developed a user-friendly toolkit for computational thematic analysis using Jupyter Notebook as the operating platform, our proposal advocates an even simpler approach using the Orange software (Demšar et al., 2013). This enables users to apply computational thematic analysis directly, without the need for a coding interface.

Topic modelling serves as a statistical analytical tool primarily employed in natural language processing (NLP). Within topic modelling, the LDA technique plays a key role in classifying and analysing text within documents to discern specific topics. For our primary survey based on questionnaires, LDA constructed a topic-per-document model and a words-per-topic model from the responses obtained. This methodology has gained popularity among researchers (Tidhar & Eisenhardt, 2020) for its capacity to synergistically harness the computational power of algorithms and the insightful depth of qualitative investigations.

Given the diverse qualitative responses received in the survey on digital payment methods, LDA analysis is deemed suitable for extracting a nuanced set of inferences. The guidelines given by Maier and colleagues (2021) were followed to ensure reliability and validity of the analysis. At first, rigorous cleaning and preprocessing of the data was conducted; details are provided in the Appendix. The detailed steps followed to ensure the reliability and validity of the data analysis process are described, as per the guidelines provided by Maier and colleagues (2021).

Step 1: Establishing Reliability and Validity

One important aspect for assessing the rigour of a topic model is in terms of the degree of replicability (reliability) of the model and the degree of the model’s interpretability (validity), both of which need to be checked and reported (Levy & Franklin, 2014). The reliability of the topics generated was measured using the technique suggested by Niekler and Jähnichen (2012). In this approach, two different topic models ‘A’ and ‘B’ are compared to find their similarities. With respect to each topic in model ‘A’, the probability values of N topic words are compared with the probabilities of each of the N topics’ most frequent words from all the topics belonging to model ‘B’. Topics from both models were deemed similar if the Cosine similarity (t) of their top-word probabilities was greater than the threshold cutoff criteria of 0.7. In our study, the aggregate inter-topic Cosine similarity score from this analysis was 0.81, thus fulfilling the reliability criteria.

With regard to interpretability, we conducted a computation of the Perplexity score as recommended by Blei and colleagues (2003). This was done by partitioning the corpus into two portions, one containing a significant chunk of the data (80%), and the remaining segment (20%) served as the holdout data. Based on how well the model predicted the topics from the holdout data, the overall goodness of fit of the model was computed. We observed that our model was able to generalize onto the holdout sample with an accuracy of 83%, which is acceptable. Hence, the interpretability of our study is established.

Step 2: Determining the Most Optimum Number of Topics

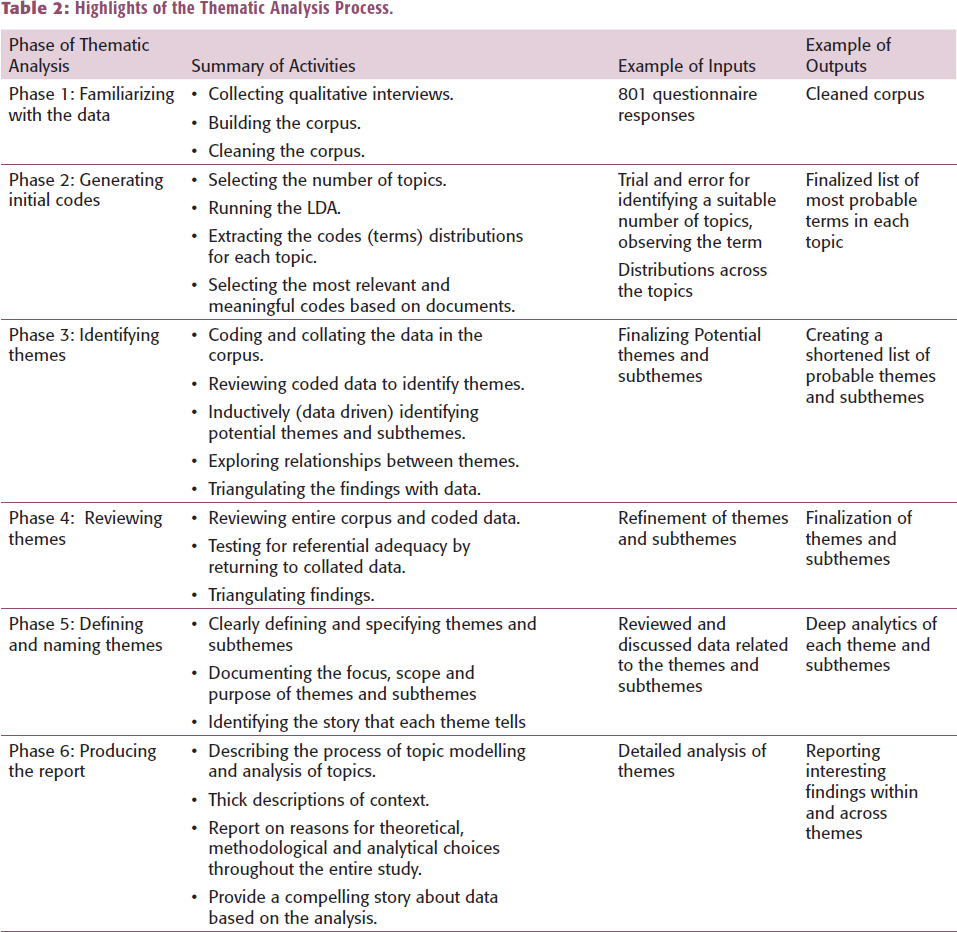

The LDA algorithm requires the user to specify the value for the number of topics to be extracted (K). One way of identifying the optimal number of topics is by trial-and-error procedures (Blei, 2012). In this approach, researchers iteratively apply different values for K and other hyperparameters such as document-topic density (α), topic-word density (β) and select the value producing more meaningful topics as the outcome. We varied the value of K from 5 to 50 to check each model’s performance. The researchers shared their results with an external expert, and together they analysed the iterative models using a LDA visualization tool called LDAVis, as recommended by Sievert and Shirley (2014).

Accordingly, a topic model with k = 10 was identified as the most representative of the data (refer to Table 2). Since the documents in this study are substantially lengthy, the thematic analysis technique was applied (Braun & Clarke, 2006) to systematically identify, organize and describe patterns from our corpus.

Highlights of the Thematic Analysis Process.

Step 3: Thematic Analysis

In thematic analysis, a theme refers to any major issue concerning the research questions that revolves around a repeated set of content (Braun & Clarke, 2006). The main appeal for using thematic analysis lies in its ease of conducting and interpreting the analysis which helps in countering certain methodological challenges (e.g., vagueness, rigour and complexity) compared to other methods in recognizing what a topic has been exactly written about (Braun & Clarke, 2006). We used the thematic analysis method for detailed analysis of the corpus to identify interesting topics hidden in the responses. Braun and Clarke (2005) have elucidated six steps for conducting thematic analysis. The analysis involves recursive introspection of themes in a back-and-forth manner.

At step 1, researchers become familiar with the data through a careful, in-depth understanding of the corpus. At the next step, the researchers identify significant portions of the corpus as certain meaningful patterns and label such instances as unique codes. The researchers then analysed the codes to identify the overarching themes which represent the codes. After the themes have been articulated, researchers revisit them iteratively to check their appropriateness.

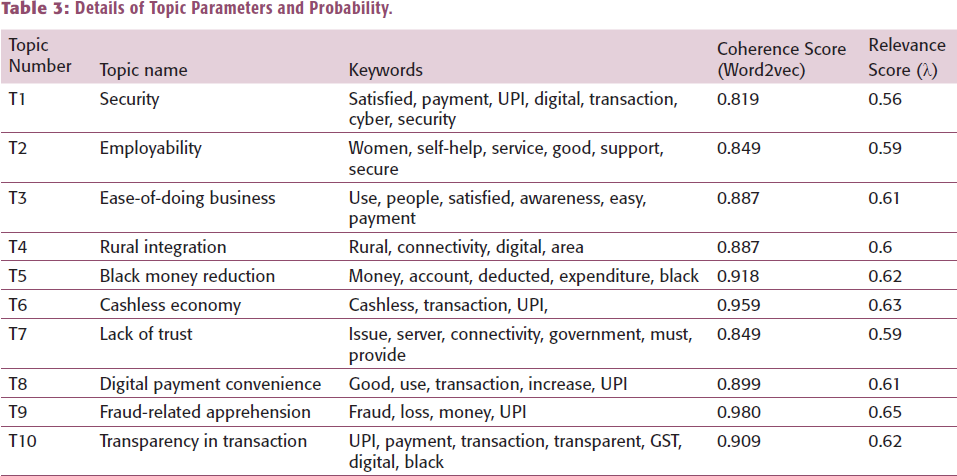

However, one major shortcoming of thematic analysis is that the identification of themes is a very subjective process, due to which the credibility of such analyses has been questioned (Nowell et al., 2017). That is where NLP-based topic modelling can be a better technique to identify the themes through probabilistic distribution of words in documents (Delgosha et al., 2022). This approach is known as computational thematic analysis. NLP-based topic modelling provides a systematic structure to the first three steps of the conventional thematic analysis. In computational thematic analysis, topics are identified in terms of coherence (Mimno et al., 2011, p. 264) and relevance (Sievert & Shirley, 2014). The coherence score measures the extent to which similar words pertaining to a certain topic are related to each other. We used the Word2vec model to compute the coherence score. For all topics, the coherence scores were observed to be greater than 0.8, indicating a higher similarity between words within each topic. The relevance metric, developed by Sievert and Shirley (2014, pp. 66–67), represents the relative weight of the words in the topics. By manipulating the weighting parameter λ, researchers can decide which top words should be given how much weight in order to reorder the same in ascending or descending order. Sievert and Shirley (2014, p. 67) recommend a value of λ close to 0.6 to be a good indicator of relevance. In our study, the λ scores for all ten topics were in the range of 0.55–0.65, fulfilling this criterion as well.

The themes were defined as labels of the corresponding topic based on the words and documents that were highly associated with each topic (Schmiedel et al., 2019). The final identified topics are depicted in Table 3.

Details of Topic Parameters and Probability.

Step 4: Thematic Analysis of Individual Responses in the Context of UPI Users

Finally, the topics were assessed, and representative themes were identified following Brawn and Clarke’s (2015) reflexive thematic analysis procedure. The ten topics identified in the topic modelling process emerged into four broad themes through iterative verification of the corpus. These four overarching themes comprehensively encompass all the topics identified in our primary survey. A brief description of each theme is presented below.

Theme 1: Financial Transaction Agility

The first theme explores how UPI has transformed Indians’ payment mindset from a reliance on physical cash. Respondents highlighted challenges with the previous cash-based system, including difficulties obtaining change, ATM cash shortages during emergencies and issues with damaged currency. Topics 6 and 8 delved into these concerns.

I feel UPI has made it easier for us to do business transactions since the dependence on banks and ATMs has reduced a lot, … in our village sometimes there are prolonged power outages during which ATM machines don’t work. (Participant 121, male, 34 years, small grocery shop owner)

Additionally, respondents noted that UPI apps often provide discounts or cash benefits, which further enhances the initiative’s appeal to the public, as discussed in our survey.

I could not believe my eyes when one of my friends explained to me about cash back opportunities through UPI apps, … my customers have also become appreciative of this feature and nowadays I seldom do cash transactions. (Participant 76, female, 41, vegetable shop owner)

Theme 2: Lack of Trust

The second theme revolves around the cybersecurity challenges and the potential for fraud associated with the rise of online payment systems. Some respondents shared experiences of falling victim to phishing scams, where fraudulent websites tricked them into making payments. The respondents mentioned specific third-party websites for such deceptive activities.

I got scammed by a fake QR Code, the moment I made the payment, a substantial amount of money got deducted from my bank account, … I got the message also much later, till date I am still pursuing the bank to settle this issue, I have become afraid of UPI … not going to use it any more ever. (Participant 411, male, 36 years, small business owner)

The respondents also raised concerns about the potential threat from scamming rackets and have made requests to the government to take more stringent steps to ensure such events do not recur in the future. Topics 1, 7 and 9 cover these concerns.

Several scams have happened in our village ward, we share information through targeted advertisements and leaflets, but the awareness is very low due to lack of knowledge and communication gap … we need intervention from the Centre in this matter, it is too big a problem for us to manage. (Participant 80, male, 51 years, village cooperative manager)

Theme 3: Implications for Middlemen Bypassing

A few participants noted that UPI sparked a revolution in India, surprising many with the rapid adoption of the cashless economy concept. The impact and the swift growth of the digital and UPI payment system are attributed to the government’s vision towards cashless transactions and a less cash-dependent economy.

Most respondents expressed a positive reception to this transformation, highlighting the enhanced ease-of-doing business in recent years.

My shop is in a tourist destination, and everyday so many people visit our small town; earlier there were times when the tourists will want to pay through UPI, and I would reject them since I did not know about UPI, … I lost so many customers that way…. Now even foreigners are using UPI, it is so quick and also no headache of carrying back the day’s earnings in loose cash, not safe for girls like me. (Participant 662, female, 28 years, handicraft shop owner)

Respondents attributed the changes to the government’s initiatives aimed at promoting digital transactions in businesses, spanning from large enterprises to small businesses and local traders. Numerous participants highlighted the role of UPI in enabling their participation in online transactions. Some shared firsthand experiences of engaging in small-scale business ventures, such as agricultural start-ups, highlighting how the UPI system facilitated their transactions. Additionally, respondents noted that digital transactions not only boosted their own businesses but also contributed to job creation as increased business activities led to employment opportunities.

When I started my firm, I got so much support from my relatives, some of them who were working in big cities sent me capital through UPI…. UPI based transactions are now a part and parcel of my business, whether it is procuring the fish, or customer transactions, and even payment of salaries … it has made my life simple. (Participant 8, male, 30 years, fishery startup owner)

This recurring theme was echoed in topics 2, 3 and 4.

Theme 4: Enhancing Transparency in Business Transactions

The last theme reflects the respondents’ perception of the positive effect of UPI on combating black money and reducing corruption related to it. As people are gradually moving towards conducting business transactions without cash, there has been a surge in various digital payment modes following demonetization in 2016.

A significant number of respondents believed that transactions through UPI have led to more clarity towards certain service taxes. Many participants also expressed their view that this shift has contributed to combating the issue of black money in Indian society.

UPI has made it very transparent for our domestic transactions, I can easily get electronic receipts in my mobile where all information about the Goods and Services Taxes (GST) is mentioned,… it makes me feel honest and responsible compared to doing cash transactions. (Participant 145,female, 35 years, privately employed).

Although the opinions of the experts differ, Sikdar (2020) claims that demonetization and the subsequent adoption of UPI have led to a reduction of about 15% in black money held in cash. Topics 5 and 10 delve into this thematic area.

CONCLUSION

The introduction of the UPI has revolutionized the payment ecosystem in India, offering a seamless, user-friendly and secure platform for inter-bank transactions. Since its inception in 2016, UPI has rapidly emerged as the fastest-growing payment system in the country, facilitating over 10 billion transactions monthly. Despite its transformative impact, UPI encounters various challenges, including concerns related to data privacy and competition from alternative payment systems. Our study, employing the topic modelling technique and sentiment analysis, unveiled intriguing findings. These encompass both user satisfaction and minimal challenges associated with the UPI payment system. The analysis, delving into respondents’ responses, indicates that the shift towards UPI as the preferred mode of payment is primarily attributed to user-friendly technology, enticing discounts or cash benefits, and various government incentives such as ‘Lucky Grahak Yojana’ or ‘Digi-Dhan Vyapar Yojana’, along with rewards, subsidies and the receipt of government scheme benefits. Notably, digital transactions have also enhanced business operations, streamlining the ease-of-doing business for respondents.

Additionally, some respondents highlighted that UPI and cashless payments contributed to a reduction in their daily spending and aided in addressing issues related to black money. Nevertheless, respondents shared concerns about poor network connectivity in some areas, particularly in the rural sector. Hence, the government should expedite its revamped BharatNet Project for laying optical fibre cables to enhance internet access in rural and remote areas where internet connections are poor. Similarly, some respondents also expressed concerns about online cheating and fraud, urging the government to implement more stringent measures for its eradication. It is important to note that online cheating and fraud are evolving challenges, and governments continue to adapt their strategies to address emerging threats in the digital landscape. The Government of India is cognizant of this issue, with over 95,000 UPI-related fraud cases reported in the fiscal year 2022–2023, as disclosed by the Union Ministry (Mudaliar, 2023)—an increase from 84,000 in the preceding financial year. Despite the rise in UPI-related fraud cases, the growth rate of UPI transactions, which reached approximately 360 million in February 2023, has outpaced the growth rate of fraud cases. This suggests that certain measures have been effective in mitigating the growth of fraud cases in UPI transactions. Notably, a national cybercrime reporting portal has been established for grievances, and the government agencies have repeatedly alerted the nation to remain vigilant against online cheating and fraud. The assurance of a reduction in online fraud and flawlessness in transactions will surely increase confidence among users. UPI will indeed persist as the preferred mode of transactions, with exponential growth.

Theoretical Implications

This study sheds light on the user intention towards UPI from a rural and urban comparative lens in the context of India. As such, the findings render support for the unified theory of acceptance and use of technology (UTAUT), proposed and popularized by Venkatesh and colleagues (2003). The UTAUT posits that users will be motivated towards using certain technology depending on the extent to which they perceive the system to be beneficial for them in terms of (a) performance expectancy, (b) effort expectancy, (c) social influence and (d) facilitating conditions. Using the UPI interface leads to an enhanced ease-of-doing business with both local and foreign customers, including tourists. Hence, UPI is expected to improve the performance expectancy of rural and semi-urban business owners. From the consumer’s perspective, too, such technology helps in uninterrupted ease of transactions, resulting in achieving their objectives irrespective of constraints such as power outages and insufficient funds in ATMs. Our participants have confirmed that UPI has a very simple user interface for users with limited technology exposure, which results in higher effort expectancy. The word-of-mouth popularity of UPI in rural and semi-urban India is really noteworthy, and the social influence factor of UTAUT is observed to be in full force behind the rapid adoption of UPI in the study context. Lastly, thanks to the Government of India’s promotion of the technology and the deeper penetration of the internet in India’s rural and semi-urban landscape, the right facilitating conditions are available to drive the adoption of UPI in the context of our study.

This study also provides validation for the theory of technological diffusion (Rogers, 1962). The Indian rural market is currently experiencing a growth phase in UPI adoption, following a relatively slow start. Given the huge population base and untapped users across India, the growth phase is expected to continue for an extended period in the future.

Managerial Implications

This study suggests that rural and semi-urban India can be tapped for several cross-functional industrial expansions, especially in sectors that rely heavily on digital payment-based transactions. The findings from this study provide validation to business entities that expanding to previously untapped consumers located in geographically remote locations has become more feasible due to UPI, in parallel expansion of infrastructure, internet penetration and rise in smartphone users (Kumar & Chawla, 2023). Managers may take note of this study to consider the feasibility of their aggressive expansion plans to the hinterlands of India and reap the benefits of the vast, untouched consumer base that resides there.

Limitations and Future Directions

This study, like many others, has a few methodological shortcomings. To begin with, the choice of LDA for the computational thematic analysis may be criticized due to the recent rise in popularity of transformer-based topic modelling techniques such as the bidirectional encoder representations from transformers (BERT) technique (George & Sumathy, 2023). In this regard, the choice of LDA was based on the application of the same in similar study contexts and the lack of knowledge the researchers had about BERT.

Alternatively, we could have considered non-parametric topic modelling techniques such as hierarchical Dirichlet processing (HDP). This alternative was not explored due to the extended time taken by HDP for computing the results. Lack of sufficiently robust hardware restricted the authors from considering this approach. Although topic modelling helped in identifying the key topics, the process is still a relatively novel technique; hence, as researchers, there may be shortcomings in the execution.

Having acknowledged these, we believe that our study makes a novel contribution to the extant literature on technology adoption in a developing market’s non-urban segment. In many ways, this study offers several ideas for future research. For example, studies may be directed towards understanding the phenomenon studied in this research through an objectivist lens. Future studies may also wish to explore the perspective of women’s empowerment in relation to UPI technology in a similar social context. Studies may also be planned to understand the impact of UPI on enhancing livelihoods and economic conditions using a panel data approach. We sincerely hope that our study raises interesting research questions that can be pursued by eager researchers.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.

NOTE

e-mail:

e-mail:

e-mail:

APPENDIX: TEXT CORPUS CLEANING PROCESS

The initial stage in any text mining process involves corpus pre-processing. To clean the corpus comprising responses from all 801 participants, we utilised the NLTK package in Python (Bird et al., 2009). The cleaning process encompassed several sub-steps to prepare the data for subsequent use. Essentially, the text needs to be sanitised through six sequential steps as outlined by Maier and colleagues (2021): (a) tokenisation (breaking down corpus into short word chunks), (b) lowercase transformation (uppercase words are converted to lowercase forms), (c) stop-word removal (in any language there are supporting words such as ‘the’, ‘a’, ‘is’, ‘am’, ‘are’ etc. which are as such not important as far as the meaning of the corpus is concerned, (d) filtering out punctuations, symbols, numbers etc., (e) lemmatisation (converting word forms such as verbs, adjectives, adverbs etc. into root words) and lastly, (f) relative pruning, which can help in removing very rare and extremely frequent word occurrences from the observed data. We used an upper and lower cutoff of words appearing for more than 99% of the documents or less than 1% of all documents to specify the pruning (Denny & Spirling, 2017).