Abstract

In 2001, the Communications Convergence Bill (CCB) of India envisaged a future in which fixed line, wireless telephony, and cable TV services could be integrated to be provided over the same infrastructure. Further, the infrastructure layer could be unbundled from the services layer, and be provided in a non-discriminatory manner to all service providers. This commentary traces the evolution of these two ideas - technology neutrality and functional separation, in the changing licensing frameworks of Indian telecommunications from 2001 to the present. We propose a new licensing framework that recognises the modularity of 5G technologies and the evolving market conditions.

Keywords

On 5 August 2024, US District Judge Amit Mehta ruled that Google illegally maintained a monopoly in search, saying that the tech giant paid companies to make Google the default search engine on smartphones and other devices. This judgment is only the latest development in a longstanding debate on the increasing market power of tech giants and its implications on communications and the broader digital economy. The changing nature of technology has not only led to functional convergence in the delivery of communication services, it has also altered industry linkages and business models. Without mandating any particular structure, our paper lays out the contours of a regulatory regime that would create a level playing field for all sectors and service providers in the digital economy. In the next section, we start by presenting the long history of proposals in the Indian context, espousing regimes similar to the one we are proposing and an overview of market developments in India. In the subsequent section, we elucidate international best practices and Indian compulsions that warrant an urgent relook at earlier proposals. We then present details of a new licensing framework and go on to detail the operational issues, including stakeholder views and revenue implications, followed by the concluding section.

THE LONG ROAD FROM THE COMMUNICATIONS CONVERGENCE BILL OF 2001

Over the past three decades, Indian telecommunications have leapfrogged to become the second-largest telecommunications market in the world. The number of cellular mobile subscriptions has crossed the 1 billion mark, and 4G subscriptions alone have crossed 800 million. While 5G mobile services are rapidly being rolled out in the country, it is time to relook at the telecom licensing framework in India to enable the growth of ‘5G and beyond’ networks and services.

The business model of the telecom industry was based on long-term infrastructure investments financed through usage-based connection fees. Today, competitors of traditional operators do not necessarily require their network infrastructure—for example, new-age over-the-top (OTT) communication service providers ride on top of the telco network. Network connection is, therefore, becoming commoditized. Further, the telecom value chain has undergone a tremendous transformation, including innovative applications and convergent services. However, increasing data volumes and mobile usage require upgrading and modernization of the network that licensed telecom operators provide. It is in this context that this paper argues for a new licensing and regulatory regime for the telecom industry in India that delivers higher investments and consumer choice (Czarnecki et al., 2017).

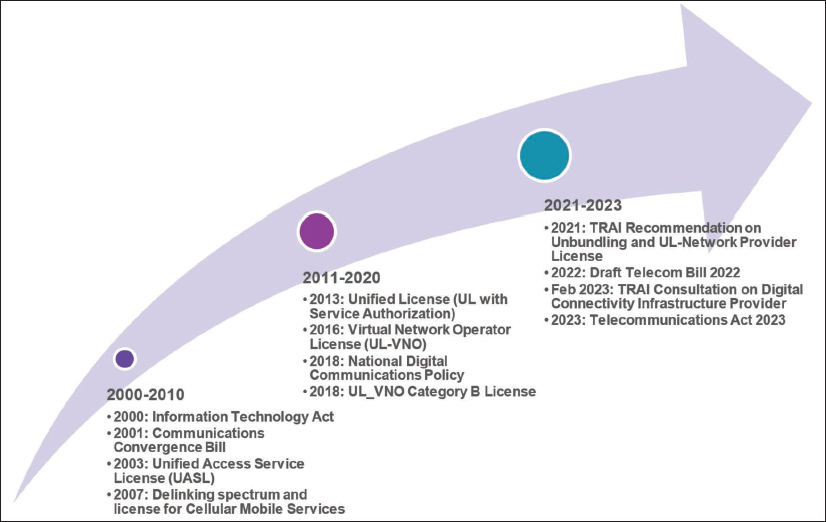

Communications Convergence Bill of India (2001)

The Communications Convergence Bill of India (GoI, 2001) was drafted in 2001 at a time when the three services of telephony, internet and broadcasting were being provided through different technologies, namely cable-based fixed-line and cellular mobile services. From a technological point of view, the prospect of ‘convergence’ in which all three services could be provided using the same medium, and each service could be provided using any of the three media, had become a reality. This multiplicity of possibilities spawned a new vision for regulation and licensing based on two fundamental principles:

Technology neutrality and

Functional separation of services from infrastructure facilities

Prior to 2001, telecom regulation in India largely followed a ‘command and control’ approach (Prasad & Sridhar, 2014). A key disadvantage of this approach is the regulator’s predetermination of technologies to be deployed by operators (OECD, 2006). In contrast, the bill envisioned a technology-neutral regime in which carriers have the flexibility to deploy appropriate technology without the administratively determined mandate of the regulator (El-Moghazi et al., 2019). For actualizing the functional separation principle, the Bill conceptualized the creation of a new entity, referred to as the ‘Network Service Provider’, that would use infrastructure facilities, including earth stations, cable infrastructure, wireless equipment, towers and ducts to provide bandwidth services.

During this time, telecommunications services were also provided by cellular mobile service providers whose licences came bundled with radio spectrum. Further, the licensing terms and conditions specified the technology for wireless services (i.e., 2G and 3G). On the recommendation of the Telecom Regulatory Authority of India (TRAI), the Department of Telecommunications (DoT) announced the guidelines for a Unified Access Service Licence, which allowed the use of any technology (both wireline and wireless) for the provisioning of network access service.

Unified Licence Regime (2013)

After some incremental changes, such as the delinking of the spectrum from the licence in 2007, the Unified Licence (UL) regime was announced by the government in 2013 (DoT, 2013), under which entities obtain a single licence in the first stage and subsequently obtain service-level authorizations for various services, including the internet, National Long Distance, International Long Distance and satellite communication services. Spectrum was delinked from the licence and had to be obtained separately through a defined methodology. The UL represented a step towards convergence as it allowed a single entity to provide telephony and internet services. However, it stopped short of incentivizing the functional separation of the infrastructure and services layers to nudge the industry in the direction envisioned in the Communications Convergence Bill.

National Digital Communications Policy 2018 and Beyond

In the National Digital Communications Policy 2018, the DoT envisioned the unbundling of infrastructure, network, services and application layers through differential licensing (GoI, 2018). In 2021, TRAI, in its recommendations on ‘Enabling Unbundling of Different Layers Through Differential Licensing’, proposed that separate authorization under UL be created for an Access Network Provider (TRAI, 2021). The Access Network Provider would be responsible for all the network-related terms and conditions specified in the Access Service Authorization under the UL. The clauses related to service delivery would not apply to this category of providers. Though this move is intended to functionally separate infrastructure, network access and service delivery, there were no incentives put into place to ensure a transition of integrated telcos to becoming functionally separate. As a result, the concept of the Access Network Provider did not gain much traction, and the recommendations of the regulator were not accepted by the DoT. However, in 2022, DoT requested TRAI for recommendations on creating a new category of licence—Telecom Infrastructure Licence. In response, TRAI published a consultation paper titled ‘Introduction of Digital Connectivity Infrastructure Provider (DCIP) Authorisation under Unified License’, seeking inputs on their proposal of introducing a DCIP that in TRAI’s framework would operate both at the infrastructure and network layer (TRAI, 9 February 2023).

The recently enacted Telecommunications Act, 2023 (DoT, 2023), acknowledges the change in technology and the emergence of competing internet and satellite-based communication services. Replacing the Indian Telegraph Act 1885 and the Indian Wireless Telegraphy Act 1933 it lays out authorization for providing telecommunication services, possessing radio equipment and establishing and operating telecommunications networks. It also provides for auctioning and administrative allocation of spectrum as well as mechanisms to exercise the right of way for laying down telecom infrastructure. These changes recognize the profusion of services possible in a 5G world and the need for quick upgradation of telecom infrastructure. The TRAI recently concluded its consultation on the ‘Framework for Service Authorisations’ to be granted under the Telecommunications Act, 2023, for perspectives on authorization versus licensing, authorization structure and so on, with a view on long-term regulatory stability. However, the Act falls short of the functional separation of services and infrastructure layers.

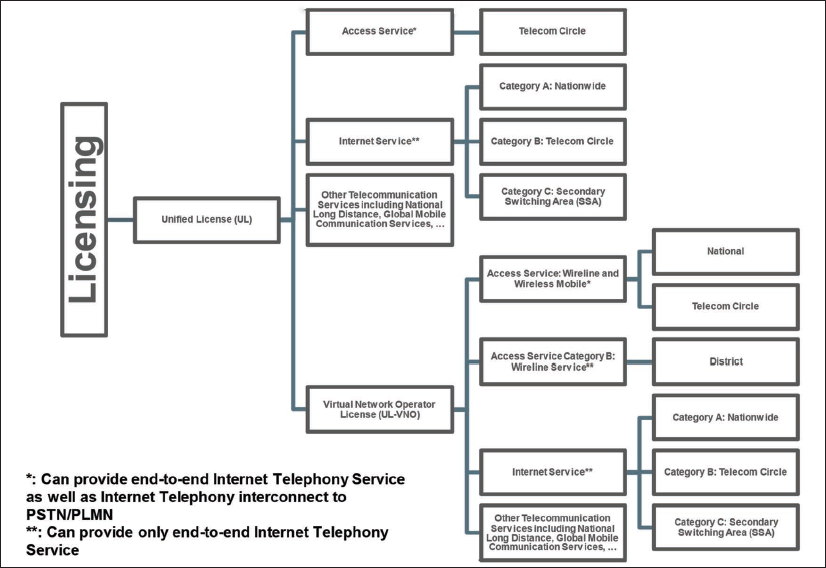

The evolution of the telecom licensing framework and its current form are provided in Figures 1 and 2, respectively.

Evolution of the Licensing Framework in India Since 2000.

Current Licensing Structure with Authorized Services and Defined Service Areas.

The current licensing framework, as illustrated in Figure 2, is defined by two notable features:

Introduction of the Virtual Network Operator (VNO) licence in 2016 that separated network provisioning from services (DoT, 2016). The VNO licensees typically lease network capacity from network providers on a wholesale basis and provide their branded communication services to retail users; and

Introduction of VNO Category B licence for wire-line in 2018 that refined the Licence Service Area down to the district level to enable participation of smaller operators who do not own networks in the provisioning of access services (DoT, 2018).

Current Market Dynamics

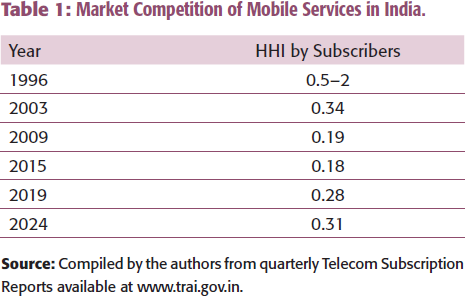

The telecom market in India has gone through lots of vagaries since the first set of cellular mobile licences was given in 1995. Table 1 provides a glimpse of the market structure over the years. The Herfindahl–Hirschman index (HHI) by subscriber base is presented in Table 1, with lower HHIs indicating more intense competition in the market.

Market Competition of Mobile Services in India

Starting as a duopoly, the Indian cellular mobile subscriber market in India saw the emergence of up to 12 operators in 2011 (Prasad & Sridhar, 2014). The new entrant, Reliance Jio (RJio), with its deep pockets, launched its 4G mobile broadband service at a very low price point of about ₹149 per month for up to 1 gigabytes (GB) per day in 2015. At that point, the incumbents were charging 4 paise/100 KB, with caps of 1–2 GB/month. Moreover, RJio used electronic know your customer (e-KYC) using Aadhaar-based identity verification to reduce the time of onboarding customers from the then prevailing delay of 3 days down to about 15 minutes. Further, RJio started 4G mobile service as a green field project, thereby bypassing the older generations and enabling superior broadband service compared to the incumbents. RJio was one of the few telcos to bundle 4G-enabled, affordable feature phones with their service to quickly acquire customers across all segments. This resulted in a huge increase in the subscriber base (through either churn from the incumbents or new acquisitions in the form of a second subscriber identification module (SIM) for those having multi-SIM handsets) for RJio, starting from scratch in 2016 to 186.6 million in 2018, 426 million by 2021 and 460 million currently, with a market share of around 40% by March 2024. This phenomenal growth has a substantial impact on competition with HHI increasing from 0.18 in 2015 to 0.31 as of March 2024. The incumbents filed a case at the Competition Commission of India (CCI), accusing RJio of practising predatory pricing. The incumbents also charged RJio with using the financial strength of the Reliance conglomerate in other markets to enter the telecom market, thereby contravening certain clauses of the Competition Act 2002. However, CCI cleared RJio of contravening Sections 3 and 4 of the Competition Act (CCI, 2017).

Apart from providing RJio mobile broadband services, RJio has also started bundling JioCinema—the OTT video service. As the official OTT broadcaster of the Indian Premier League (IPL) cricket from 2023 until 2027, JioCinema scaled to 450 million users watching the 2023 IPL edition and further to 620 million in 2024. These developments indicate the close bundling of infrastructure and services on the one hand and telecom services with OTT services on the other hand.

The two leading incumbent service providers, Airtel and Reliance Jio, own almost 70% of the services market. The concentration of market power among traditional private sector service providers also creates a rationale for reducing the barriers to entry of new categories of service providers. This can be enabled by unbundling services and infrastructure or, in other words, functional separation of services and infrastructure. However, as in previous initiatives, not much has been done by way of introducing incentives that would, at the very least, help to overcome the inertia involved with moving to a new industry structure. This also holds true for the latest reform through the Telecommunications Act, 2023. It is in this context that this paper explores an alternative licensing framework that recognizes the technology convergence and market evolution and promotes competition in the provisioning of communication services.

FUNCTIONAL SEPARATION OF INFRASTRUCTURE AND SERVICES LAYERS

The liberalization of India’s telecom sector, which began in the early 1990s with the announcement of the New Telecommunications Policy (1994), led to spectacular transformation. It resulted in one of the fastest-growing telecom networks in the world. Recent endeavours to reform are, however, incremental. In 2022, the government approved certain structural and procedural reforms such as the elimination of spectrum usage charges, facilitating right of way, allowing 100% FDI and so on; however, it had little impact on improving market competition. While the need for functional separation between infrastructure and services has been articulated with varying degrees of intensity since 2001, the rapid technological changes, service innovations and changes in business models have made it more pressing now than ever before. Similar approaches are being tried in jurisdictions other than India.

International Practices

Functional separation has been used as a regulatory remedy by several countries to address concerns of market power. Vertically integrated firms that operate at both the infrastructure and service layers with significant market power can self-preference their own retail services. Functional separation breaks the walled garden within the network infrastructure and retail services entity, enabling better access to essential facilities by other competitors. It also incentivizes new investments in the upgradation of network and service innovation. For integrated businesses, functional separation leads to different services or activities being performed by separate operating divisions of the same firm. This may also involve separate management for relevant divisions (Dounoukos & Henderson, 2003). Regulatory authorities can encourage such behaviour by imposing equivalence of inputs (EoI) or equivalence of output (EoO). EoI implies that the same products and processes are offered to competitors as the operator’s own retail arm, while EoO implies that the products offered by the operator to its own retail business and other operators are functionally comparable. The remedies must, however, be proportionate to the degree of concentration (Cullen International, 2019).

Countries also adopt other types of separation—accounting, legal or structural separation. Of these, accounting separation is the least stringent, and legal separation is the most stringent, with functional separation lying in between. In 2006, Cave (2006) defined eight separation options—accounting separation, creation of a wholesale division, virtual separation, business separation, business separation with localized incentives, business separation with separate governance arrangements, legal separation and ownership separation. As early as 2008, Sweden implemented functional separation by amending the Swedish Telecommunications Act 2008 to include mandatory functional separation as one of the powers of the Swedish telecommunications regulator (Teppayayon & Bohlin, 2010). It is along the lines of voluntary functional separation introduced by Italy, where vertical separation remains the decision of the individual company. Other countries, such as the United Kingdom and New Zealand, have imposed involuntary separation. In 2006, the United Kingdom functionally separated its fixed-line network (Curwen & Whalley, 2010), and New Zealand opted for structural separation (Congedo, 2015), mandating the breaking up of telecom operators to create open basic networks (European Telecommunications Network Operators’ Association [ETNO], 2010). Functional separation has also been adopted by Ireland, Poland and Australia. Cave and Mariscal (2020) analyse the effect of accounting, functional and structural separation adopted as part of the 2013 telecom reform in Mexico and conclude that they indeed were successful policy reforms in making mobile services affordable to the low-income groups in the country.

The US telecommunications industry offers a very comprehensive case study that highlights the difficulties of employing separation requirements to address competition concerns in a dynamic technological environment. It is pointed out by Gilbert (2021) that the history of deregulation of the US telecommunications industry teaches us that there are potential economic benefits from separating monopoly services from services that can be supplied in competitive markets, but there are also formidable obstacles to creating durable boundaries that do not interfere with competition and innovation. The policymakers have to be conscious of their efforts to address structural or functional separation based on monopoly bottlenecks and enable rules that do not hinder innovation and that facilitate competition.

Recently, Rossi (2022) has explored the application of functional separation and voluntary separation principles included in the 2009 European Union regulatory framework on non-discriminatory access criteria. It is indicated that the different provisions related to forms of vertical separation have changed through time, along with changes in technology, changes in the theoretical perception of the severity of incumbents’ incentives to discriminate and changes in the objectives pursued by regulation. Europe has also witnessed a number of voluntary separations wherein new entrants, publicly funded entities and private operators voluntarily chose to adopt a wholesale-only business model without retail operations. Examples of voluntary separation across countries such as Czech Republic, Netherlands, Austria, Slovenia, Italy, Croatia and Ireland are provided in Queder (2020).

The European approach is informed by a new perspective on the boundaries of service competition. The Directive (EU) 2018/1972 of the European Parliament and of the Council (EU, 2018) states:

end-users increasingly substitute traditional voice telephony, text messages (SMS) and electronic mail conveyance services by functionally equivalent online services such as Voice over IP, messaging services and web-based e-mail services. In order to ensure that end-users and their rights are effectively and equally protected when using functionally equivalent services, a future-oriented definition of electronic communications services should not be purely based on technical parameters but rather build on a functional approach. While ‘conveyance of signals’ remains an important parameter for determining the services falling into the scope of this Directive, the definition should cover also other services that enable communication. From an end-user’s perspective it is not relevant whether a provider conveys signals itself or whether the communication is delivered via an internet access service.

In line with the approach of functional equivalence, one of our recommendations is to level the regulatory playing field between Virtual Network Operators and OTT Communications Apps. However, one must also be sensitive to the differences in these two kinds of entities that stem from their different operational models. For instance, VNOs are able to use the publicly assigned numbering system, while OTTs are not. The EU treats any entity whose users are able to connect to number-based systems as a number-based interpersonal communications service. Hence, OTT communications providers would not fit into this category. However, the differentiated regulatory perspectives towards these two types of service for the provisioning of emergency services, and compliance to net neutrality need to be clearly spelled out.

Functional Separation in the Indian Context

The need for functional separation in the Indian telecom market is being driven by three forces:

Market Concentration: With the recent and consistent increase in concentration in telecom services, the sector in India is slowly inching towards a duopoly. The HHI, which is the measure of market concentration, almost doubled from 0.17 in December 2017, following the launch of Reliance Jio, to 0.31 in December 2023. This is despite the government’s efforts to strengthen the ailing public sector service provider. With the competitive pressure easing, we also see a rise in tariffs, the most recent hike being in the range of 11%–25% (July 2024). In order to preempt anti-competitive and discriminatory conduct by incumbents, infusing competition in the services layer is necessary.

Rapid Innovation in the Services Layer: As highlighted in the new Act, there is a wide variety of services and service providers coming into being as the world adopts 5G technologies. The services layer is witnessing competition not only amongst the VNOs but also from the OTTs who provide substitutable communication services such as internet telephony, instant messaging and group calling. The reported number of WhatsApp users in India is over half a billion, over the critical mass for any communication service in India. The recent legal battle between WhatsApp and the government, with the former threatening to exit the market, highlights its foothold in the Indian market.

While a VNO leases network capacity from the network operator, OTT communication service providers do not, as they provide services over the internet and hence are ‘untethered’ from the underlying network. Thus, these services provided by the VNOs and OTTs are functionally equivalent even though they are operationally disparate and, hence, need to be addressed with somewhat similar regulatory principles. To facilitate innovation in service provisioning, it is important to ensure that every service provider does not need to own elements in the infrastructure layer to be able to compete effectively with other service providers. This approach is sometimes referred to as the Bell Doctrine (Joskow & Noll, 1998), which was used in the antitrust case against AT&T in the United States in 1982. Under this principle, when an industry has two layers comprising an essential service layer and a layer that rides on top, the two layers must be unbundled in order to allow a startup in the overriding layer to compete without having to incur the heavy capital expense of building out the infrastructure layer.

Optimal utilization of the infrastructure layer: The infrastructure layer is complex, with several players providing different components of the network. The telecom network has evolved from an elementary architecture comprising radio equipment and physical infrastructure to a software-led ecosystem that includes cloud storage companies, software developers and municipalities, besides the traditional network entities (Elayoubi et al., 2017). As recommended by TRAI (2021), access network providers that integrate the various components and provide the network infrastructure to the service layer entities are needed. In the absence of such an entity, transaction costs for service providers would become unmanageable, as they would have to negotiate separately with individual entities of the infrastructure ecosystem. Further, in order to optimally utilize the network infrastructure and avoid inefficient duplication of network costs, the infrastructure should be provided in a neutral and non-discriminatory manner to the various service providers. Thus, it is necessary that the infrastructure layer operates at an arm’s length from the services layer. Steps have already been taken in the UL (VNO) access service category B authorization in which a VNO can provide wire-line services over the infrastructure of the network access provider at the district level. A comprehensive regime of functional separation, along with equal access to the infrastructure layer, is likely to promote competition in the services layer.

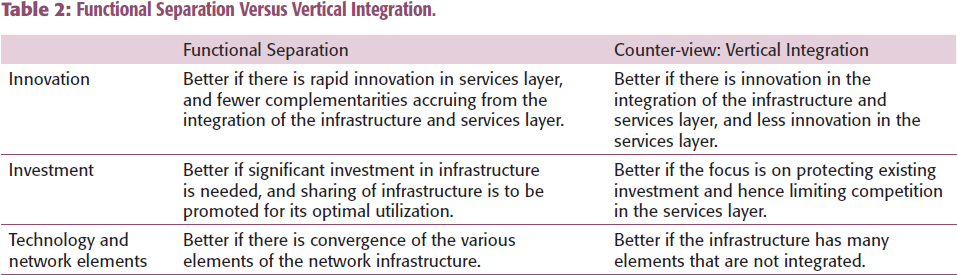

The main arguments of functional separation vis-a-vis vertical integration are highlighted in Table 2.

Functional Separation Versus Vertical Integration.

A NEW LICENSING FRAMEWORK

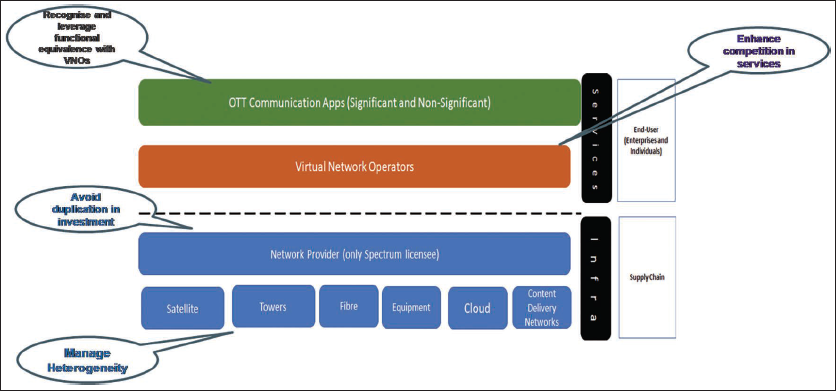

Given the balance of considerations, we recommend the functional separation of infrastructure and services layers of the sector and the creation of an integrated entity–network service provider, in the infrastructure layer. The proposed structure is shown in Figures 3.

The Layered Approach to Regulating Digital Communications.

For businesses to operate efficiently within and across layers, we propose a licensing framework that is based on the principles of proportionality. There are three levels of service authorization: (a) Licensing: the entity requires prior permission to operate and must pay associated licence fees. (b) General authorization: entities must satisfy certain criteria for the provisioning of services and pay a nominal authorization fee. (c) Registration: entities only need to register to operate by paying a nominal registration fee. In other words, they can commence operation without prior permission. However, they may be restricted from operating in case they do not follow the general guidelines. A broad overview of the entire framework is provided below:

In line with our regulatory model of functional separation, we create a two-layer system for infrastructure and services, respectively.

In the infrastructure layer, we conceive of an entity—the network provider, that is entitled to bid for spectrum and that integrates together all the entities in the physical and network layer such as content delivery networks (CDNs), cloud storage providers, tower companies and optical cable providers to provide network bandwidth on a wholesale basis to communication service providers. This is in line with TRAI’s recommendations on unbundling (TRAI, 2021). The network provider needs to obtain a licence as its operation involves scarce resources such as spectrum, and it is provided with rights to set up infrastructure in an oligopolistic market. Licence fee continues to be set at the prevailing rate of 3% of adjusted gross revenue (AGR). Network providers shall be mandated to provide equal access on equal commercial terms to communications service providers. They need to fulfil rollout obligations and are charged a universal service levy (USL) at the prevailing rate of 5% of the AGR.

In the services layer, we identify two types of entities: VNOs that lease network bandwidth from the network providers and OTT communications providers that are untethered from the underlying network. Both VNOs and OTT communications providers are divided into significant and non-significant service providers, based on the proportion of traffic carried by them. All VNOs and significant OTT communications providers are charged a separate broadband infrastructure levy (BIL) for the use of the underlying network infrastructure. The levy can be designed and implemented such that the contributions are only utilized for the purposes of expanding and improving broadband infrastructure in the country.

Quality of service requirements shall be applicable to all service providers, namely the VNOs and OTT communications providers.

Emergency service requirements shall be applicable only on significant VNOs as per the existing UL (VNO) guidelines (DoT, 2016).

Net neutrality regulation shall be applied to all VNOs as prescribed in DoT (26 September 2018). However, there is a realization that networks, 5G and beyond, will witness more customized network provisioning through technologies such as network slicing. Hence, we allow this possibility to be treated as being compliant with net neutrality regulation, provided that such VNOs offer minimum guaranteed quality of service for the public network as prescribed by the telecom regulator.

Network security/data privacy and data protection and lawful interception will be regulated as given in DoT (2016).

As the heterogeneity of the market is likely to increase with 5G, we suggest that the granularity of LSAs be increased in line with the UL (VNO) Category B access service licence for mobile services as well (DoT, 31 August 2018).

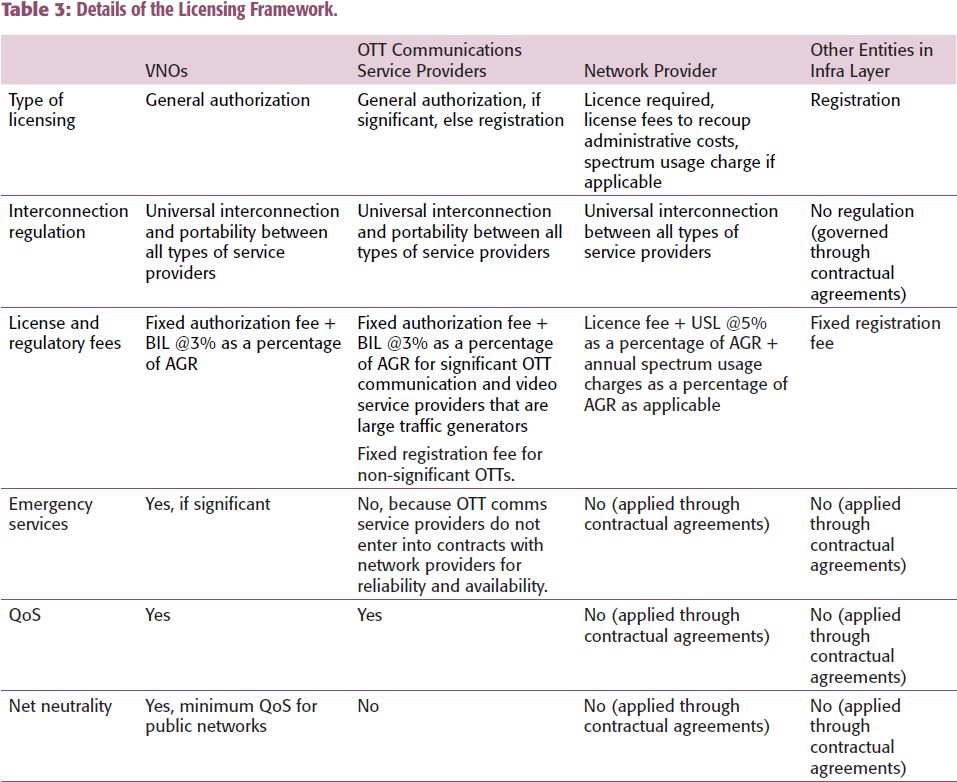

The proposed licensing structure is shown in Table 3.

Details of the Licensing Framework.

IMPLEMENTATION FRAMEWORK

Views of the Stakeholders

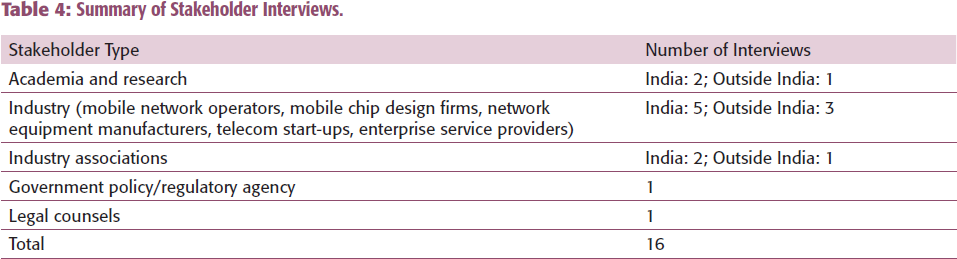

The regulatory and licensing structure proposed is very different from the extant one and, hence, is likely to face opposition from different stakeholders. During the research, we discussed the structure with experts from the licensed telecom and internet service providers (TISPs); associations such as the GSM Association, Cellular Operators Association of India that represent the TISPs; associations such as the Internet and Mobile Association of India and Broadband India Forum that represent the interests of OTTs and internet firms, legal counsels, researchers and academics regarding the implications of the proposed framework (please refer to InViCT, 2023, for details). Table 4 provides a summary of the stakeholder interviews that we conducted.

Summary of Stakeholder Interviews.

On Functional Separation and Licensing

We elicited responses from the stakeholders regarding their views on functional separation and the proposed licensing structure. The inputs are summarized below:

The OTT services are beginning to substitute telecom services. While the OTTs and others are carrying out backward integration into the provision of the network, the TISPs are also engaging in forward integration into the application layer and backward integration into the product and device space as they attempt to compete in this changing landscape. However, the connectivity part of the telecom value chain is shrinking with more value added in other parts, such as content. Hence, the regulator should look at the entire value chain for regulatory purposes.

Networking is the forte of TISPs. However, newer technologies such as cloud platforms and software-defined networks are technology areas where the large internet firms and OTTs compete with TISPs. Hence, a competitive collaboration encouraged by a newer regulatory regime is required for the best outcomes. The TISPs have already started working with tech companies to provide industry-specific niche services.

While the spread of connectivity up to 4G was led by the TISPs and a regulator focused on telecommunications, the road ahead requires us to expand along a number of dimensions, including greater sharing of infrastructure and an appreciation that data connectivity is a very small and perhaps shrinking part of the digital value chain.

License conditions for telecom are quite stringent compared to any other regulated industries. They include call monitoring, providing information to the state for national security and so on. Separating infra and services and formulating regulations and rights across these two broad layers may be an option to deal with this issue.

Hence, there is a broad consensus about the need to relook at the existing licensing framework and incorporate functional separation as being advocated and practised by other countries such as the United Kingdom, Sweden and New Zealand. Needless to say, the TISPs are the proponents for including OTTs in the licensing framework.

On Regulatory Inertia and Capacity

The objective of telecom regulation should be clearly defined in terms of universal access, consumer interest and competition. It should not be to maximize revenue.

Regulation and policy have been agnostic about technology evolution. Telecom sector regulation was always focused on scarce natural resources such as spectrum. Regulation and the Telecom Act 2023 (DoT, 2023) ignore all aspects of innovation.

Integration of regulation of the tech sector and telecom sector is evolving. They were treated separately until the OTT consultation paper was initiated by TRAI (2018).

Light touch regulation is very aspirational. The Indian regulators use overreaching regulations instead of light touch, such as data localization rules as specified in the Digital Personal Data Protection Act, 2023 (MeiTy, 2023).

We need to augment the capacity and autonomy of the sector regulator.

There is a need for an independent cadre for TRAI, and the cadre should invite experts from the industry and academia at market price as consultants. There should also be financial autonomy for the sector regulator.

The United Kingdom is developing a horizontal unit called the Digital Economy Unit to deal with regulatory issues across the digital value chain.

Extraterritorial jurisdictional regulations are not refined to address OTT firms and services; for example, the internet telephony restrictions as imposed under UL did not work well.

While acknowledging the need for regulation to adapt to the changing technology landscape, the stakeholders indicated the need for autonomy and flexibility of the regulator to frame rules suitable for the new digital value chain.

Incentive Structure to Catalyse the New Framework

Given the legacy of current market incumbents, it is important that our recommendations do not come as mandates but as ‘nudges’ that would be channelized through tax and other incentives. This would allow for the natural reorganization of the industry to its new equilibrium, rather than forcing a structure that could cost in terms of reduced efficiencies. The new incentive structure is as follows:

Currently, licensed TISPs that undertake functional/legal separation will pay spectrum usage charges only on revenue of network services that are sold on a wholesale basis to the VNOs. This will reduce the regulatory burden on the network providers and will act as an incentive for the existing TISPs to migrate to the new regime.

Lower rates of USL, referred to as the BIL in the services layer as compared to the infrastructure layer, shall incentivize separation of networks and services layer by the TISPs. Consequently, the VNOs will pay lower regulatory charges.

The BIL proposed to be paid by the VNOs and OTT communication service providers will compensate the network providers for the usage of the network capacity, and provide enough finances to augment the network capacity in urban and semi-urban areas of the country.

The incentives for the government to adopt the new approach are examined in the section on economic implications.

A wide spectrum of industry configurations are possible within our regulatory framework, ranging from the current vertically integrated structures to completely unbundled formations and everything in between. The precise configuration would be dynamically determined via the options the TISPs choose from the proposed licensing regime.

Possible Concerns from Existing Licensed TISPs

Despite the above economic incentives that can possibly promote functional separation, following are the concerns expressed by the TISPs regarding the migration to the new regime.

The contractual agreement between network providers and VNOs shall not be construed as a violation of net neutrality principles as specified in TRAI (2017). Net neutrality shall be equally applicable to both telecom and content providers.

There has to be an economic incentive for the TISPs to migrate to the proposed regime.

The institutional arrangements for distributing BIL back to the network providers shall be worked out with all stakeholders, including the DoT and TRAI. The TISPs also expressed concern regarding the effectiveness of the distribution mechanism.

Our recommendation of functional separation of network provisioning and service provisioning is likely to lead to increased competition in the services layer. Our recommendations will also lead to an unbundling of network components, as a wide variety of entities are likely to enter into contracts with each other and the network provider to leverage the full potential of 5G technologies at the services layer. On the other hand, through functional separation, there can be efficiencies, economies of scale and innovation at the network layer level.

Fiscal Implications

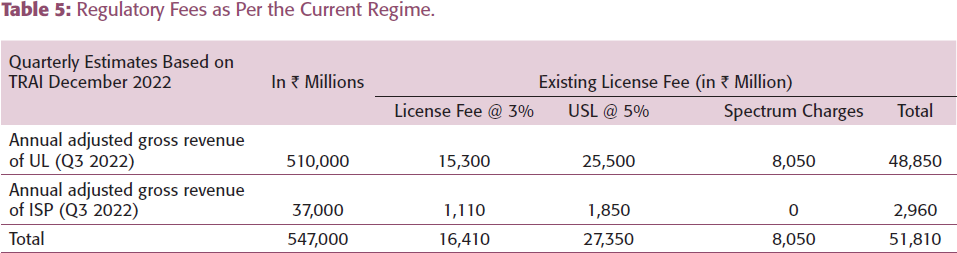

Our recommendations have important implications on the revenue accruing to the government. We project revenue estimates for the government as per our recommendation and compare them with the revenue accrued under the current licensing regime. The baseline used is the AGR, license fee at 8% (3% license fee + 5% USL/BIL) and annual spectrum usage charges as provided by TRAI (2023). The following are the other data that we have used in the calculations:

The OTT communication providers, such as WhatsApp and Zoom, earn revenue through (a) business users and (b) advertising. The annual revenue from WhatsApp business is estimated to be around $1 billion/year (MoneyControl, 2023).

The estimated annual revenue of OTT video service providers is ₹ 300 billion (Statista, 2023a).

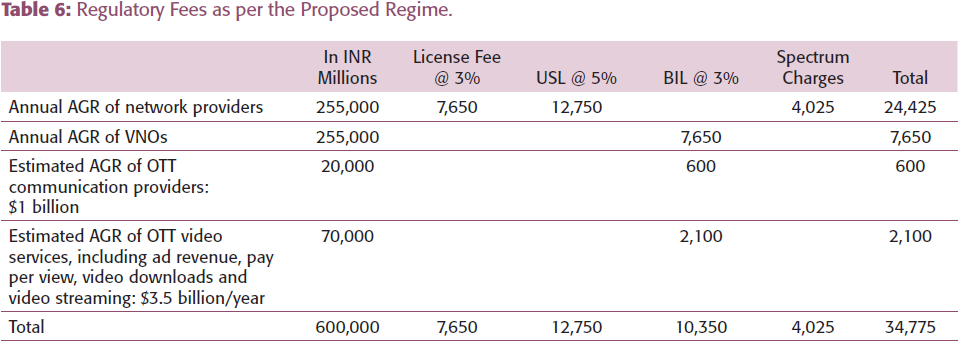

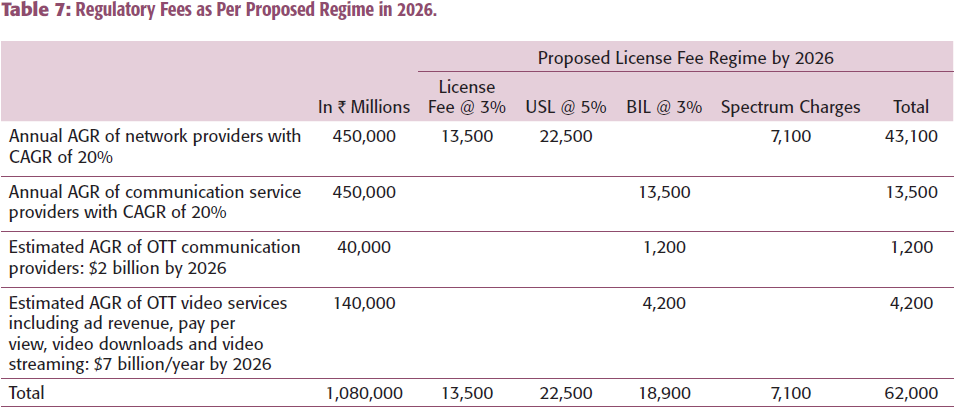

Tables 5 and 6 show the results of comparing the existing license fees with the proposed license fee structure. Though the quarterly estimated regulatory fee is less in our proposed structure, we expect it will match up soon due to the increased usage of broadband for both communication and video services. To demonstrate this, we have simulated the scenario for 2026 with the following assumptions:

Regulatory Fees as Per the Current Regime.

Regulatory Fees as per the Proposed Regime.

A compounded annual growth rate (CAGR) of 20% in AGR of network providers and VNOs for the next three years.

Growth of OTT communications and video services revenue to $7 billion by 2026 (Statista, 2023b).

The estimated regulatory fees as per the proposed regime with forecasted revenue estimates of various entities as of 2026 are presented in Table 7.

Regulatory Fees as Per Proposed Regime in 2026.

From Tables 5 to 7, we can see that in a very short time, the total revenue catches up to existing levels due to the increase in revenue of various operators and service providers, despite the reduction in fee as a percentage of AGR. Hence, we recommend that the licensing fee structure be revamped taking into account the growth of broadband networks and usages across segments of society. This will also send a positive signal to the industry to invest in infrastructure and services to provide quality and affordable broadband services to the nation at large.

CONCLUSION

We are at a point in time where the longstanding proposals for functional separation and infrastructure integration are more urgently needed than ever before. The licensing and regulatory framework needs to be sensitive to the greater modularity possible with 5G technologies. Our proposal reflects the attempts to design a licensing structure that would nudge the industry towards exploiting the new opportunities enabled by 5G technologies and the synergistic alliance between the blurring boundaries of the telcos and the internet firms.

Researchers are split between the benefits of functional separation versus vertical integration. A recent study on digital platforms indicates that though structural or functional separation can address some complaints lodged against activities by dominant platforms, experience demonstrates that separation requirements are difficult to administer and can harm innovation (Gilbert, 2021).

The former chairwoman of the US Federal Trade Commission, Ms Lina Khan, also pointed out that while structural separations were previously implemented both as a standard regulatory intervention and key antitrust remedy in network industries, they have been largely abandoned, especially as the technology evolved (Khan, 2019). Though written in the context of digital platforms, Khan (2019) advocates revisiting structural separation to curb market dominance by a few firms.

It merits emphasis that our recommendations are intended to promote service competition, check industry concentration and facilitate the attainment of broadband for all. Our recommendations for network integrators will lead to unbundling of network components, as a wide variety of entities are likely to enter into contracts with each other and enable the network provider to leverage the full potential of 5G technologies. In essence, it will protect efficiencies while allowing more innovation and participation in the infrastructure layer. On the other hand, while functional separation increases transparency, limits non-price discrimination and encourages market competition, there are possible downside risks of increased administrative and regulatory burden. With this consideration, we recommend voluntary separation with built-in financial incentives.

Footnotes

ACKNOWLEDGEMENTS

We acknowledge the financial support provided by the Indian Council for Research on International Economic Relations (ICRIER) and Vodafone Idea Centre for Telecom (InViCT) for this project.

DECLARATION OF CONFLICT OF INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.

E-mail:

E-mail:

E-mail: