Abstract

This study investigates the institutionalization of the crypto-economy from an institutional theory perspective and also examines the role of existing institutional pillars in its development. The path analysis using global institutional indicators reveals that the development of the crypto-economy is significantly affected by regulatory, cognitive, and normative factors of a country. Further, the regulative pillar fully mediates the relationship between the social pillar and the crypto-economy. While we find convincing evidence that a country’s social pillar endorses crypto-economy, its indirect effect is more prominent and significant than the direct effect.

Executive Summary

The article marks a transformative shift from traditional economic institutions to technologically driven ones. This study explores the institutionalization of the crypto-economy through the lens of institutional theory, examining the roles of regulatory, cognitive and normative pillars. Our findings indicate that these institutional pillars significantly influence the development of the crypto-economy. Specifically, the regulatory pillar mediates the relationship between the social pillar and the crypto-economy, highlighting the indirect but substantial impact of a country’s social framework on crypto-economic growth. We refer to the cognitive and normative pillars collectively as the social pillars. Technological advancements and the rise of blockchain technology have spurred the growth of innovative fintech organizations, creating profitable investment opportunities and addressing cross-industry challenges such as data security and transparency. Although existing literature primarily focuses on micro-level drivers, it is crucial to conduct macro-level analysis to understand the broader institutional factors that support the development of the crypto-economy, as micro-level insights alone do not adequately capture macro-level growth dynamics. As a result, our research employs path analysis using global institutional indicators, demonstrating that the cognitive and normative institutional pillars significantly influence the regulatory pillar, which in turn affects the crypto-economy. These findings suggest that countries with robust institutional frameworks are better positioned to adopt and benefit from crypto-economic technologies. Furthermore, understanding these macro-level factors can guide policymakers in less absorptive countries to stimulate regulatory institutions that support the crypto-economy. This institutional perspective is crucial for identifying future leaders and laggards in crypto-economic development and for understanding inter-country differences in crypto-economy adoption. In conclusion, the study underscores the importance of a supportive institutional framework for the development and adoption of the crypto-economy, emphasizing the interconnected growth of fintech technology and the need for empirical research to address broader developmental issues.

With the current pace of technological advancement, the old economic institution is waning, yielding to a new order. In this constantly evolving scenario, scholars predict that the crypto-economy will be the monetary future of the economy (Goundar et al., 2021; Pashkevych et al., 2020; Tomić et al., 2020). The development of the crypto-economy has, in turn, spurred the growth of several innovative fintech organizations (Gryshova & Shestakovska, 2018; Ku-Mahamud et al., 2018; Ku Ruhana & Omar, 2018; Mutambara, 2019) that have become ground for profitable investments (Bondarenko & Antonov, 2019). A crypto-technology–based institution is the new economic infrastructure grounded in crypto-economics (Berg et al., 2019).

Therefore, it becomes important to understand the development of crypto-economy, along with the new innovative financial technology, blockchain, whose growth is interconnected. The study becomes pertinent as the foundational technology of crypto-economy, that is, blockchain technology, can provide a pragmatic solution to many cross-industry problems (Hughes et al., 2019; Pawczuk et al., 2019) it faces, such as data security and storage and transparency. The broad application of blockchain has led to the development and increased adoption of the crypto infrastructure (Cunningham, 2019; Woodside et al., 2017). However, there is a need for empirical and rigorous research to address the broader issues of its development.

Existing literature focuses on the micro-level drivers of crypto-economy but misses the more comprehensive macro-picture. In the context of the crypto-economy, the technological aspects have received much research interest, primarily from the micro-perspective. Holtkemper and Wieninger (2018) study the technological features that drive its adoption. Knauer and Mann (2020) investigate the factors that drive consumers to adopt crypto-economy while Queiroz and Wamba (2019) focus on the drivers in the supply chain networks. Thus, it is seen that while the micro-drivers of the crypto-economy have been studied, literature remains silent on the macro-view and the institutional characteristics that support its development. This builds the case for studying the macro idea and the institutional perspective to gain a universal understanding of issues related to crypto-economy, such as data security and privacy policy. Further, there is also a need to study the inter-country differences to understand why crypto-economy flourishes in certain economies and not others.

We propose that the development/adoption of the crypto-economy in a country can only happen within the existing institutional framework that is more attuned to its needs. The crypto-economy, being institutional, depends on the country’s existing institutional characteristics. From the logic of the institutional theory, weak cognitive, normative and regulatory institutional pillars can potentially obstruct its development and vice versa. Accordingly, we investigate the following research question:

How Do Institutional Pillars Influence the Adoption of the Crypto-economy in Any Country?

This study establishes a path model to capture the relationships among various global indicators. We structure the article into seven sections. The next section provides the theoretical and empirical backgrounds of the existing institutions and how they can support crypto-economy. We describe the data, variables and measurements used for analysis in the section after that. The subsequent sections report the results of the path analysis and details the theoretical implications, practical suggestions and research limitations. The last two sections include the conclusion and list the limits of the research and future research directions.

THEORY AND HYPOTHESES

Blockchain, the Foundation of the Crypto-economy

Blockchain technology, the backbone of the crypto-economy, is also known as the internet of trust, given its ability to address the various trust issues in any organizational context. Blockchain is a dispersed and decentralized database comprising an invariably growing list of ordered blocks (Swan, 2015). It offers greater transparency through the multiple immutable copying of the transactions (Niranjanamurthy et al., 2019; Seebacher & Schüritz, 2017) that ensure trust in the network (Christidis & Devetsikiotis, 2016). It is also a decentralized transactional database technology that facilitates inherent tamper-resistant immutable transactions across a network of participants called nodes (Glaser, 2017). The immutable distributed ledger technology prevents information tampering, leading to greater trust amongst the users. In principle, this guarantees a single truth across different agents who may or may not trust each other. Thus, blockchain transforms the very notion of trust. It substitutes ensuring trust through social capital with trust through technology. In blockchain, a change in the ownership of a unit of value is written as a transaction record into a block of data and replicated across all the devices participating in the ledger. Thus, each block may contain multiple transaction records of value. Also, each block holds a hash of the previous block effectively containing a representation of all the prior transactions in the chain. Because the hash value stems from the previous data, the process is not reversible. Therefore, all these accounts in the distributed ledger are there for all participants to see and approve, thereby ensuring transparency even though no two participants know each other. Why crypto-economy is akin to an institution.

Crypto-economy is a digitized decentralized economic system with anonymous actors (Kaal & Calcaterra, 2017). It is controlled by cryptographic techniques and not by trusted third parties (Pilkington, 2016). It is akin to any other economic system; however, it requires knowledge structures, enforcement and built-in incentive mechanisms (Allen, 2017). Also, unlike the traditional economic system, it is not confined by single geopolitical regulations (Pilkington, 2016). The crypto-economy is based on advances in technologies and requires wide-ranging organizational and behavioural alteration for successful social practice (Graglia & Mellon, 2018).

Institutions are enduring patterns of social practice (Lawrence, 2008). They are about the means needed to pursue the ends (Khalil, 1995); in the context of the crypto-economy, the blockchain-empowered business processes consisting of distributed digital hyperledger become the means to pursue required business goals. A hyperledger-based technology solution also requires a new means of monetary transaction, taking over the conventional means of monetary exchange, which is anticipated to change the existing social practice of value exchange. The arguments presented validate the crypto-economy as an excellent example of an institution. To hypothesize and operationalize our inquiry, we examine the dynamics of institutional interaction and the impact of existing institutions on the evolution of the new ones. To do so, we look at the critical components of the institutional theory.

The Three Pillars of the Institutional Theory

Hotho and Pedersen (2012) proposed three strands for the institutional theory: organizational institutionalism, institutional economics and comparative institutionalism. Each strand offers a different conceptualization and the mechanisms of institutional influence on various outcomes (Kostova et al., 2020). Most studies draw the measurement of institutional parameters from these strands, sometimes explicitly specifying and other times without an apparent reference (Kostova et al., 2020). Organizational institutionalism is rooted in sociology, while institutional economics has its roots in economics. Comparative institutionalism studies the interdependence of institutions in different areas of socio-economic life (Kostova et al., 2020). Organizational institutionalism views institutions as relatively stable social structures composed of three components: regulative, normative and cognitive (Kostova et al., 2020; Meyer & Rowan, 1977; Powell & DiMaggio, 1991; Scott, 1995). Economists address these elements as the three institutional pillars of society. At a broader level, existing institutional pillars influence the building process of new institutions (Halinen & Törnroos, 1998). The comparative institutionalism theory proposes typologies of national institutional systems, such as the liberal market economy and coordinated market economy (Hall & Soskice, 2001; Kostova et al., 2020; LaPorta et al., 1998; Nelson & Rosenberg, 1993; Whitley, 1999). A comprehensive view of institutional theory enables us to select the most appropriate institutional theoretic strand to use in the context of our study. We adopt a composite institutional view comprising of organizational and comparative institutionalism. In our integrated theoretical approach, we borrow the concept of institutional pillars from the organizational viewpoint and institutional complementarity from the comparative viewpoint. All societies are different; therefore, institutions differ across the spectrum based on their chosen mode of collective decision-making, due process of law and power distribution (Acemoglu & Robinson, 2008a). Not only to the formation of new institutions such as crypto-economy but the institutional difference can also be attributed to the collective rules on the security of property rights, entry barriers, the set of economic contracts and the distribution of income and wealth (Acemoglu & Robinson, 2008a). Our theoretical viewpoint leads us to explore the role of cognitive, normative and regulative institutional pillars (RGPs) in supporting further growth of the crypto-economy.

Cognitive and Normative Institutional Pillar

Cognitive and normative institutions (CNPs) are collectively categorized as social institutions (Trevino et al., 2008, p. 129). Compared to regulative institutions, normative and cognitive institutions play a principal role in stabilizing an evolving economy (Bianchi et al., 2015). Therefore, it is impossible to understand the emergence of an institution without considering the impact of the cognitive and normative pillars (Grosse & Trevino, 2005; Trevino et al., 2008). In the institutional development process, a country’s indicators, such as economic, human and political capital, signal its development. Trevino et al. (2008) consider these indicators as the cognitive and normative institutional pillars of a country. According to scholars like Lipset (1959), Lerner (1967) and Acemoglu and Robinson (2008a, 2008b), the process of national development remains unsuccessful in the absence of the right and stable institutional environment and requires old institutions to pave the way for the new ones. Accordingly, we argue old institutions pave the path for newer institutions, such as the crypto-economy. Based on the institutional interaction arguments presented, we hypothesize:

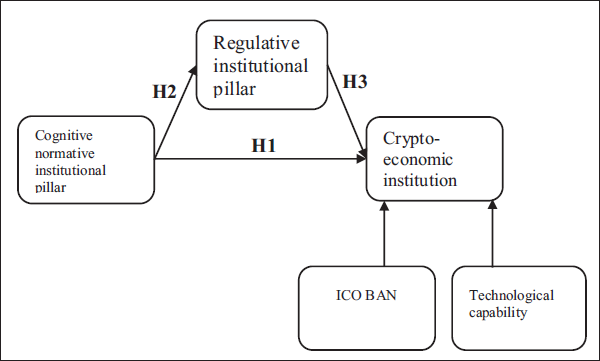

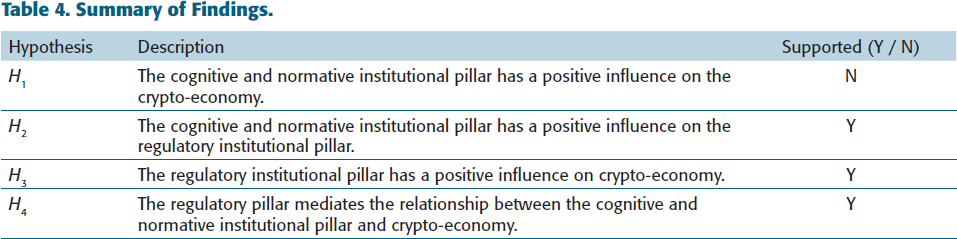

H1. Cognitive and normative institutional pillars have a positive influence on the crypto-economy.

Regulative Institutional Pillar

In line with comparative institutionalism and following the direct effect of the cognitive and normative institutional pillars on the evolution of the crypto-economy, we explore how they influence the RGPs. The RGP is an established system of rules backed by formal institutions of law (Noruwa et al., 2018). Recently, Armanios and Eesley (2021) demonstrated the crucial role of CNPs in regulatory changes and recommended that proposed regulations need to align with the cognitive and normative elements of any society. Therefore, we conclude normative and cognitive institutions will have an effect on the regulatory institutions (De Laurentis, 2021) and hypothesize:

H 2. Cognitive and normative institutional pillars have a positive influence on the regulatory institutional pillars of any society.

In a digital world, the needed institutional change is primarily rooted in transparent and efficient economic institutions (Bhuiyan, 2011). As regulatory institutions are rules and resources sustained by the social systems across time and space, they have rich endowments in finance-related institutional matters (Zhao & Kim, 2011). The ‘right’ set or formalization of institutions is considered a precondition for development (Acemoglu & Robinson, 2008a; Lerner, 1967; Lipset, 1959). Earlier, we argued that crypto-economy is an example of a financial institution. Therefore, we hypothesize:

H 3. Regulatory institutional pillars have a positive influence on the crypto-economy.

Regulatory Pillar (RGP) Mediation Hypothesis

Out of the three institutional forces, regulatory/coercive, cognitive/mimetic and normative, the regulatory pillar has been predominantly researched in institutional change, while the other two have been mostly ignored (Trevino et al., 2008). Whereas all the factors in coherence are responsible for bringing institutional genesis or change (DiMaggio & Powell, 1983; Scott, 2001). The regulative institutional force defines enforcement mechanisms and so it is mainly coercive in nature. As a result, regulative institutions inhibit the development of new behaviour, especially when it is outside the accepted norms (Trevino et al., 2008). However, following social norms is likely to facilitate the new behaviour, as in the case of the crypto-economy, which we hypothesized as H1. As a result, in such a scenario, in the presence of regulative institutions, social institutions significantly impact new institution building (Trevino et al., 2008). Therefore, building the crypto-economy as an institution is expected to be more significant in the presence of the regulatory pillar. Hence, the regulatory pillar is likely to mediate the relationship between the cognitive normative pillar and crypto-economy.

H 4. Regulatory pillar is likely to mediate the relationship between cognitive normative pillar and the crypto-economy.

Control Variables

Besides the institutional variables, several other variables might influence the crypto-economy. A valid conclusion of a hypothesis is only possible when we control our hypothesis for all such variables. However, it is not feasible to include all such variables in any model so to minimize the omitted variable bias, we integrate the following control variables into our model, based on literature:

Technological Capabilities

Technological capability plays a vital role in crypto-economy adoption (Philippi et al., 2021). Therefore, we integrate technological capability as a control variable in our model.

Initial Coin Offering (ICO) Regulations

ICO is a critical component of the crypto-economy (Allen et al., 2021). Regulating ICOs is the first step in controlling the disruptive potential of the crypto-economy. After integrating the control variables, our final model is presented in Figure 1.

Hypothesized Model.

DATA, MEASUREMENT AND METHODS

Cognitive and Normative Institution Pillars

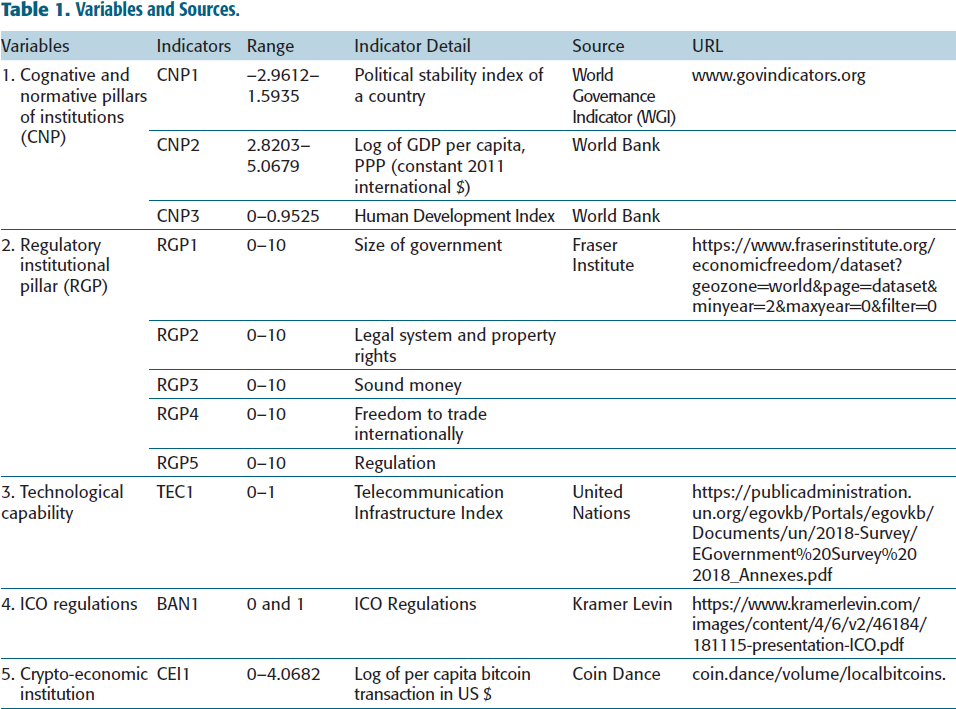

The construct CNP is cultural-cognitive, and so it is well -reflected in socio-economic attainment (Trevino et al., 2008). Trevino et al. (2008) termed economic capital, human capital/knowledge and political stability/democracy as cognitive and normative pillars. Following Trevino et al. (2008), three critical variables—political stability score, gross domestic product (GDP) and human development indices (HDI)—sourced from the World Governance Indicator (WGI) and World Bank, are used to measure CNP. The political scenario of the host country is symbolic representation of its stability or otherwise (Trevino et al., 2008, p. 123). Political uncertainty is seen as an honest reflection of the CNP (Trevino et al., 2008, p. 124). The political stability index from the voice and accountability parameter of WGI captures experts’ perceptions of ‘the extent to which citizens can participate in selecting their government, as well as freedom of expression, freedom of association, and a free media’. The index has normalized values and is termed CNP1. Our study uses the log values of GDP as the second indicator of CNP, with the term CNP2. The next variable, human capital, represents national strength in modern economies (Becker, 2002). We use the New World Bank Human Capital Index (HCI) to measure CNP3 (Kraay, 2018). For our analysis, we have brought all the data of CNP belonging to the year 2017. Table 1 provides more details about these variables.

Variables and Sources.

Regulative Institutional Pillar (RGP)

We measure the variable RGP through five parameters at the national level: government size as RGP1, legal systems and property rights as RGP2, sound money as RGP3, freedom to trade internationally as RGP4 and regulation as RGP5. We borrow all these variables from The Fraser Institute (2019). For our analysis, we employ data from RGP for the year 2017.

Crypto-economic Institution

The outcome variable crypto-economic institution (CEI) is derived from the homepage at coin.dance/volume/localbitcoins. CEI as a construct is measured by a single item, the total bitcoin transactions within a country. Because crypto-economy has various forms, it is very difficult to consider all of them in the study. Therefore, we only employ one form, that is, bitcoin for measurement purposes. To achieve the per-capita volume of bitcoins, we divide a country’s population by the volume of bitcoin. Further, as an economic indicator with large variations in the volume from country to country, we take the log conversion of the data. The countries where no bitcoin volume is found, the CEI is considered zero. CEI measures the actual volume of the bitcoin. For our analysis, we sum all the bitcoin transactions in a particular country from 2012 to 2018. Therefore, in our study, CEI is the outcome variable representing cumulative bitcoin transactions from 2012 to 2018. Aggregating all the transactions helps remove the year bias and inform about the unbiased average per-capita bitcoin transaction per year.

Control Variables

Besides the institutional variables, we also have two control variables: technological capabilities and ICO regulations. The measurement of these variables is as follows:

Technological Capabilities

IT-related skills are required for the smooth functioning of the crypto-economy. Therefore, we use telecommunication infrastructure to measure the variables influencing all IT skills. This variable is brought from the United Nations’ telecommunication infrastructure report, which is one of the reliable data sources for many macroeconomic variables. The data collected and used are from 2017.

ICO Regulations

ICO regulation is an item variable taken from Kramer Levin, a legal firm headquartered in New York with offices in Silicon Valley, Washington, DC, and Paris (Levin, 2022). The firm studies the nature of regulations of various countries on various parameters and, accordingly, it has prepared a detailed report on the status of ICO regulation for various countries. For our analysis, this variable is binary. We use 1 for countries that have banned ICO and 0 for other countries. ICO regulations are from the Kramer Levin report published in 2018.

We reflectively measure the variables CNP and RGP. At the same time, the dependent variable, crypto-economy, and both the control variables are single-item variables. Our study uses global indicators derived from six sources. Table 1 reports the descriptive statistics. Two of the model’s variables, CNP and RGP, are latent variables. Latent variables are indirectly measured through indicator variables. Table 1 also illustrates the total number of indicators used to measure the variables.

Further, it mentions the range of a particular variable, its explanation, source and the URL from where it is extracted. The range is the maximum and minimum values of the said variable. The details of the variables are as follows:

The research aims to identify and validate the mechanism to understand how existing institutional pillars of a nation influence the adoption of the crypto-economy in a country. In the preceding section, we formulated a structural model based on the institutional theory. Structural equation modelling (SEM) is the most recommended method for analysing the structural model (Hoe, 2008; Singh, 2009). SEM is a statistical technique that allows researchers to simultaneously examine multiple hypotheses (De Guzman et al., 2014)and their interdependence in a multivariate context (Singh, 2009). We find SEM to be a suitable method to analyse our proposed framework, as explained in the next section.

ANALYSIS AND RESULT

Instrument Validation

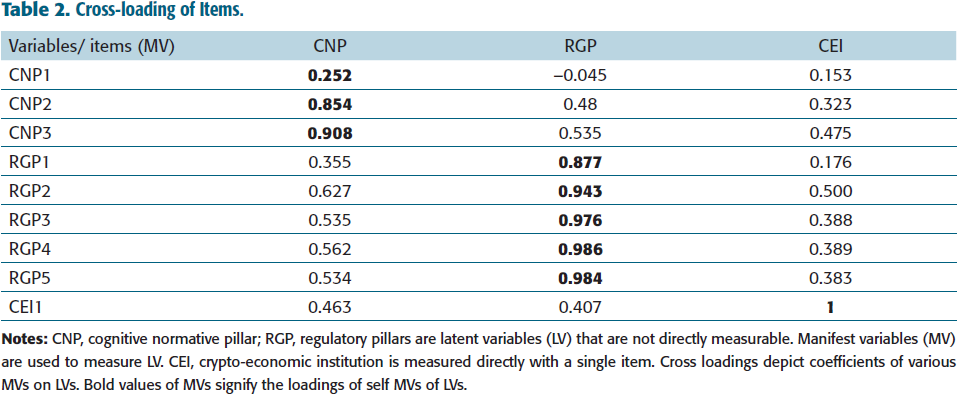

As we propose SEM, we use PLS-SEM for our analysis. In SEM, variables are indirectly measured through a measurement instrument. To validate the measurement instrument, we follow the reliability and validity check methods of SEM (Carmines & Zeller, 1979). The reliability of the measurement items is checked using cross-loading of various items on the constructs, and the results are shown in Table 2. The bold figures are the outer loadings of instruments on the constructs. For CNP, the outer loading of CNP1 is 0.252, less than 0.7. The accepted item loading of a construct in literature is 0.7 and so dropping items with less than 0.5 loadings is recommended (Roostika & Muafi, 2014). Therefore, we drop the item CNP1 from our model. The rest of the items are valid measures of CNP. For RGP, all the items are as prescribed in the literature. Thus, the reliability of the indicators is established. CNP and RGP are reflective constructs, and CEI is a single-item construct. Cross-loading of the items in Table 2 also demonstrates discriminant validity. The cross-loading of the indicators on an ascribed construct has to be higher than their loading on other constructs (Hair et al., 2011; Hair Jr et al., 2016). This criterion of discriminant validity is satisfied in our case.

Cross-loading of Items.

After dropping CNP1 from the model, in Table 3, we show robustness statistics. The first three columns of the table present the correlation among variables. The bold figures in the CNP and RGP columns are square roots of the average variance extracted (AVE). AVE is critical in establishing reliability in the multi-indicator measures (Sørensen & Slater, 2008), and this is satisfied in our model. A value of more than 0.50 value of AVE is considered adequate for convergent validity (Giannakos et al., 2012). For all our constructs, the value of AVE is more than the specified value.

Correlations, Cronbach’s Alpha and Composite Reliability.

Further, the table illustrates Cronbach alpha and composite reliability. Cronbach’s alpha is a coefficient of reliability (or consistency) that measures how closely various construct items are related to each other (Santos, 1999). A value of more than 0.7 is an acceptable Cronbach alpha coefficient in social science research (Santos, 1999). For all the constructs of our study, the Cronbach alpha value is more than 0.7. Composite reliability is another measure of the reliability of constructs with multiple items (Raykov, 1998). Similar to Cronbach’s alpha, the acceptable minimum value for composite reliability is also 0.7 (Lim et al., 2016), which we observe for all the constructs of our research.

Therefore, before analysis, we establish the convergent and discriminant validity of the measurement scale and demonstrate that they behave similar to the similar variables and opposite to the dissimilar ones.

Basic Results

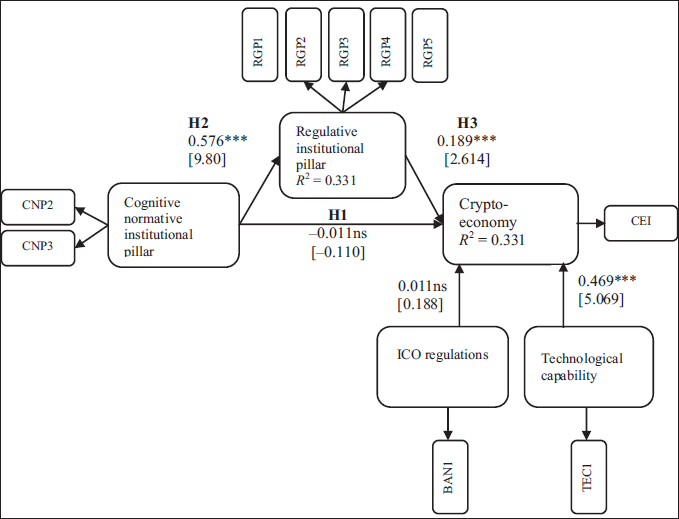

Our hypotheses aim to analyse the three associations: CNP to CEI, CNP to RGP and RGP to CEI. Of the three variables, CEI is the dependent variable, CNP is the independent variable and RGP is the mediator variable. Besides these three variables, we also control for the ICO regulations and technological capability as they are seen to impact CEI. All associations among the variables are investigated and the results are described in Figure 2. CEI is found to be significantly associated with RGP but not CNP. However, the indirect association between CNP to CEI is also positive and significant. The core interest of our study is to identify the responsible chain of variables that mediate the evolution of the crypto-economy in the presence of existing institutions. Out of the four hypotheses we investigate, except H1, all are significant, and we find the signs as expected. For significant associations, the statistical significance of the relationships is more than the 5% level. Results indicate that one standard deviation increase in CNP increases RGP to 0.576 standard deviations. One standard deviation increase in RGP increases crypto-economy by 0.189 standard deviations. Further, there is no direct impact of CNP on the crypto-economy, but there is an indirect impact.

Our results are achieved in the presence of two control variables: technological capability and ICO regulations. In summary, Table 4 presents the results of the four hypotheses.

Summary of Findings.

To assess the significance of mediation, we conduct the Sobel test whose results are shown in Table 5. The results of the test are significant, depicting the significant mediation effect of RGP between the association of CNP and CEI. We use Soper’s (2021) software to calculate the Sobel test value using four variables. The value is the coefficient and standard error of the independent variable to the mediator variable, and the mediator variable to the dependent variable. Table 5 summarizes all four measures, Sobel test value and Sobel test significance.

Sobel Test for Mediation.

DISCUSSION

Currently, the literature on the development of crypto-economy focuses on the micro-factors that promote its adoption. The primary reason we argue for this trend is that the development of the crypto-economy is limited due to a limited user base as technical skills are required to adopt crypto-economy. However, once the crypto-economy permeates a larger community and attains efficiency, it could facilitate the next stage of national development/transformation. Countries with the absorptive capacity to use this technology effectively are likely to lead in finance, trade and other data-driven sectors. An examination of the macro-level factors in this research brings to light future leaders and laggards in crypto-economic development. Further, an understanding of the factors governing crypto-economy may also be used as policy guidelines to stimulate regulatory institutional pillars that can promote its development by the less absorptive countries.

Our proposed model is a path model of the crypto-economy that examines its institutionalization mechanism through the lens of institutional economics. The primary purpose of using this lens is to understand the institutionalization process of upcoming financial technology. Institutionalization is a social development process, and its study involves the examination of its preconditions and indicators. Further, institutional economics focuses on the right (formal, monetary, efficient and transparent) structure of the market and society and their interlinkages (Acemoglu & Robinson, 2008a, 2008b; Lerner, 1967; Lipset, 1959). Thus, some important indicators of the institutional economy are the nature and impact of existing institutions and their strengths.

Our proposed model uses cognitive and normative institutional pillars to predict an upcoming institution. Rather than exploring and hypothesizing a complex model of institutional economic indicators, we prefer to employ a basic model consisting of the relationship between fundamental variables of any economy social (cognitive and normative) and the regulatory institutional pillar.

In our operationalized model, comprising of cognitive and normative and regulatory institutional pillars of an economy, only the regulatory institutional pillar directly and significantly influences the crypto-economy’s development. At the same time, the impact of the cognitive and normative pillars is indirect and occurs only in the presence of the regulatory pillar. The result has multiple ramifications for academics as well as practice. For academics, we find that all three pillars are not the same and have a differential impact on the development of the crypto-economy. The social institutional pillar offers only the foundational preparation; however, the real impact is due to the regulatory pillar. Another point of academic interest is that the political stability of a country is not a good reflection of the social pillar, as argued by Trevino et al. (2008). The reason for this needs further investigation. Our most exciting finding is that although the regulatory pillar has a decisive role in the growth of the crypto-economy, the ICO regulation has no part to play. The contrasting impact of the generic strength of the regulatory pillar and ICO regulation is interesting to note. We find that institutional formation results from long-term institutional interaction; in the short term, any specific rules offer an insignificant impact. The ICO ban is a recent phenomenon and is not likely to have any impact on the crypto-economy.

Further, if the ICO ban spills to neighbouring countries, we will likely get an insignificant result. However, the arguments demand a rigorous analysis to identify a satisfactory conclusion. In practice, countries willing to develop crypto-economy need to have a robust regulatory base. This finding also empirically illustrates that economies having strong institutional pillars will adopt emerging technologies like crypto-economy more effectively than others.

CONCLUSION

Our research aimed to reveal the effect mechanism of existing institutions on the development of crypto-economy in any economy. We find that existing institutions and their ability to evolve play a critical role in the adoption of the crypto-economy. Observing the development process through the lens of institutional economics, we find that the institutions, new or existing, are essentially a by-product of historical development. We find that both institutional pillars, social and regulatory, affect the adoption of the crypto-economy, and the regulatory pillar mediates the relationship between the social pillars and the crypto-economy. While some work in economic literature has focused on the impact of the existing institutions in poor economies (Schneider & Enste, 2000; Trevino et al., 2008), this work examines the effect at the global level. Recent research has also found that institutional quality mediates institutional factors that are economic in nature (Osode et al., 2020).

LIMITATIONS AND FUTURE WORK

Empirical studies on institutional economics have their limitations, as institutional variables potentially have a circular relationship. We follow a very simplistic view of institutional economics to establish the relationship. A study of the relationship among these variables following multiple theoretical lenses will further enrich the outcome of this study. Additionally, our interest was in unwrapping the mechanism of the crypto-economy development in the presence of existing institutional pillars. We feel that the present outcome is academic and of practical interest; however, further exploration is required to bring it to the level of policy implication. For example, integrating other control variables could further authenticate the relationship.

Furthermore, we have worked with data constraints. Our choice of analysis was static and not longitudinal. A longitudinal panel data analysis might throw more light on the outcome. In the future, the study could be expanded in the following two ways: first, we may use the proposed framework for other related or not-so-related social constructs, which will ensure the practical applicability of our proposed model. Secondly, to make the study more robust, the proposed model may use other representative variables of the crypto-economy, as the present study only uses a volume of bitcoin. Including other crypto-economic variables, such as other crypto-currencies will confirm the generality of the proposed framework. Finally, our study covers one illustrative case of existing institutional pillars connecting the crypto-economic institutionalization processes. We need many similar studies in another crypto-economic context to further endorse and advance the proposed framework.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.

e-mail:

e-mail:

e-mail:

e-mail: