Abstract

Case Analysis

The merger of Vodafone India Ltd. with Idea Cellular Ltd, the biggest in the history of the Indian telecom sector, took more than 18 months to execute from its announcement in January 2017. With a combined market share of 35% and a customer base of 400 million, the merged entity was the Titanic, created to rewrite the trajectory of the telecom sector in India. However, the Vodafone Idea saga has been one of turbulence and unrest. This case examines the background of the merger, the challenges faced by the merged entity, and the future of the merged entity.

Changes in the Telecom Sector

The telecom sector in India started growing after the 1991 deregulation and the subsequent establishment of the Telecom Regulatory Authority of India (TRAI) in 1997. This growth was supported by the introduction of the Unified Access Service License (UASL) in 2003, 4G technology in 2009, and mobile number portability (MNP) in 2011. In just two decades, the telecom sector emerged as a highly competitive, government-regulated space that required all players to differentiate themselves through aggressive pricing plans. With as many as ten dominant players, the market was crowded and challenging despite the steady growth.

The entry of Reliance Jio in 2016 changed the landscape of the telecom sector entirely. With its offer of unlimited high-speed 4G bandwidth at the cheapest possible rates, Jio successfully managed to make mobile telephony accessible to 90% of the Indian population. The penetrating pricing approach yielded significant benefits for Jio: it made competitors bleed and made substantial inroads into the market by fueling customer demands for better data speeds. This strategy resulted in a vicious price war that pushed out the smaller players and resulted in a 3% to 5% decline in the sector’s total revenue. During this time, the number of wireless subscribers in India increased from 876.81 mn in 2013 to 1170.17 mn in 2017 (drawn from the case).

Attracted by the overall market potential and the steady increase in users, all the players adopted strategies to match their strengths despite the tremendous pressure to deliver more at lower prices to the users. The prominent players consolidated their resources in a bid to take on Jio. It is against this backdrop that the Vodafone—Idea merger was announced.

Market Conditions: The Merger and Potential Benefits

The new entity arising from the merger of Vodafone India and Idea Cellular was poised to become the largest telecom company in India by size, which would enable both partners to combine their resources, gain synergies, expand their customer base as well as their market share and, above all, beat competition from Jio. It was expected that the new entity would turn out to be the largest and leading performer in the Indian telecom sector.

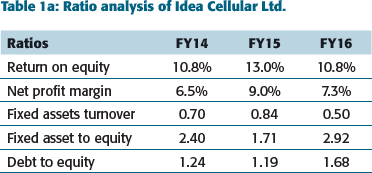

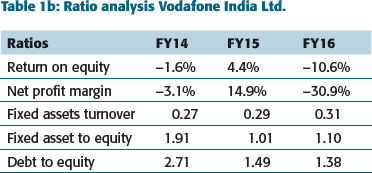

Prior to the merger, both companies were facing challenges in maintaining profitability since the entry of Reliance Jio. In the case of Idea Cellular, the profit after tax declined from FY2015 to FY2016, leading to pressure on profit margins and return on equity, while Vodafone India’s profit turned into substantial losses in 2016. Tables 1a and 1b below provide the financial ratios (based on the data given in Table 1 of the case) of the two companies for three years before the merger, showing poor financial performance to be one of the formidable reasons for the merger.

Ratio analysis of Idea Cellular Ltd.

Ratio analysis Vodafone India Ltd.

The merger of Vodafone and Idea was intended to achieve cost synergies for the merged entity. Along with this, there was a plan to bring energy savings and operational efficiencies by eliminating the older global system for mobile communication (GSM) sites. Sharing of infrastructure, combined advertising, as well as a reduction in general and administrative costs, were other opex synergies that were expected. The merger was a way to significantly improve the merged entity’s profit margin. The weeding out of redundancies and consolidation of assets was expected to bring about increased capex synergies and an overall debt reduction, resulting in a combined net debt/EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio of 3.

Further on, the merger was also expected to have increased the presence of the combined entity in various telecom circles (also called ‘telecom service areas’), viz., ‘metro circles’ and ‘A’, ‘B’, and ‘C’ circles. The combination was predicted to make the merged entity the largest cellular services provider or a strong number-two player in the leading circles such as metro circles and A and B circles. On the other hand, in circle C (smaller circles), the company planned either to upstage other players or remain dormant. This increase in market share was expected to bring about improved cost efficiency and help the merged entities improve the EBITDA margin.

Post-Merger Challenges

The merger was expected to create a successful telecom company with the largest market share. It was expected to result in various synergies for the merged entity. However, several internal and external factors resulted in various post-merger challenges for the combined entity, due to which the expected synergies could not be realized. The merged entity, contrary to expectations, is still struggling with various non-financial and financial business aspects, such as:

Improper human resource management and integration was a critical challenge for the merged entity. Nahavandi and Malekzadeh (1990) identified that culture plays a vital role in the implementation strategy of a merger. Implementation strategy defines the degree to which different systems of the acquired and acquiring firms will combine and the extent to which their employees will communicate. A clear implementation strategy is significant for achieving merger synergies, and this strategy depends on the mode of acculturation of the acquirer and the acquired firm.

Apart from cultural gaps and communication issues for employees, the merger also resulted in the layoff of many employees. By the time the merger was completed in 2018, Vodafone Idea laid off almost one-third of its employees, to bring down the duplicate resources. This headcount further declined after laying off another 4000-5000 employees who could not be accommodated. The company also withheld promotions and increments of existing employees to cut costs, fight the existing competition, and maintain a leading position in the telecom sector. This continued job loss, lack of incentives, and nonpayment of salaries as per industry standards created fear and insecurity among the employees, leading to the further loss of morale.

Future of the Merged Entity

Despite the integration challenges faced by Vodafone–Idea, the company took several strategic initiatives with the objective of creating a blueprint for increasing revenue and profitability and strengthening the merged entity’s competitive position in the telecom sector.

All these strategies helped Vodafone Idea to improve its EBITDA margins. However, the company still has a huge outstanding debt and AGR dues, leading to a high interest burden, thereby resulting in a negative net profit margin. Therefore, although the company has shown signs of recovery, it still has a long way to go to become a profitable player in the telecom market.