Abstract

In January 2017, Vittorio Colao, the Vodafone Group CEO, and Kumar Mangalam Birla, the chairman of the Aditya Birla Group, announced a merger to form Vodafone Idea. The merger was expected to create a successful telecom company with the largest market share. Contrary to expectations, the merged entity kept struggling on various non-financial and financial business fronts. The current case discusses the motives for the merger, expected synergies, post-merger challenges and financial performance of the combined entity. The case presents the potential future strategies and a dilemma about the prospects of survival and growth of the newly created entity “Vi”.

In January 2017, Vittorio Colao, the chief executive officer of Vodafone Group, and Kumar Mangalam Birla, the chairman of the Aditya Birla Group, announced the decision to go forward with a merger of equals to form Vodafone Idea, the largest telecom service provider in India in terms of customers and revenue. The merger, which was completed on 31 August 2018, was the biggest merger in the history of the Indian telecom industry. Vodafone India Ltd had a customer base of 204.68 million with a market share of 18.16%, and Idea Cellular Ltd had a customer base of 190.51 million with a market share of 16.9%. The merger resulted in a combined entity with a customer base of around 400 million and a combined market share of 35%, thereby paving the way for the creation of, potentially, the largest service provider in the Indian telecom sector.

INDIAN TELECOM SECTOR

The growth of the Indian telecom sector got a boost after its deregulation in 1991 and the entry of private players (Jain et al., 2017). To regulate and promote competition among these players, the Government of India (GoI) founded the Telecom Regulatory Authority of India (TRAI) in 1997. Post the setting up of TRAI, the Unified Access Service Licensee (UASL) regime was introduced by the Department of Telecommunications (DoT) in 2003, allowing the existing cellular licence holders to offer fixed and mobile services under a single licence. The telecom sector also witnessed a technological evolution in moving to 4G in 2009 from the 1G network during 1981–1991. The introduction of 4G increased usage and, hence, the subscriber base for telecom companies. Further, in 2011, mobile number portability (MNP) was introduced, allowing users to switch between service providers without changing their mobile numbers; this facility was available to customers free of cost.

The Indian telecom sector offers standard voice and data products in an evolving technological environment and is thus characterized as highly competitive and disruptive. Its customers are highly price-sensitive, leaving less room for companies to create brand differentiation. The only survival route for companies is to offer aggressive pricing plans. The industry is highly capital-intensive in terms of spectrum requirements and investment in telecom infrastructure. The industry is marked by strong regulatory control, with the government deciding on the spectrum auctions and the tariffs being charged. There is a growing rural subscriber base along with urban subscribers. There are only a few providers of telecom equipment, such as ZTE, Huawei, Cisco, Nokia and Qualcomm, and most of them are concentrated in China.

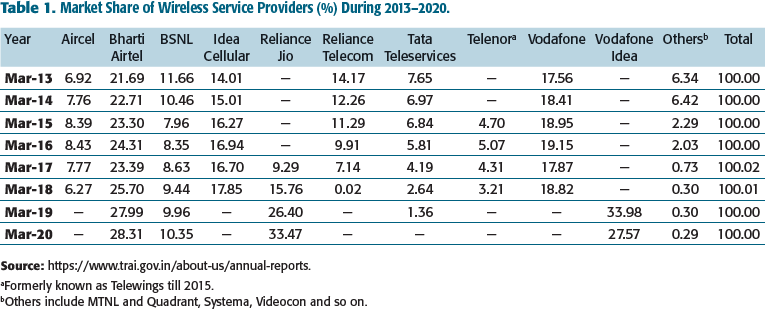

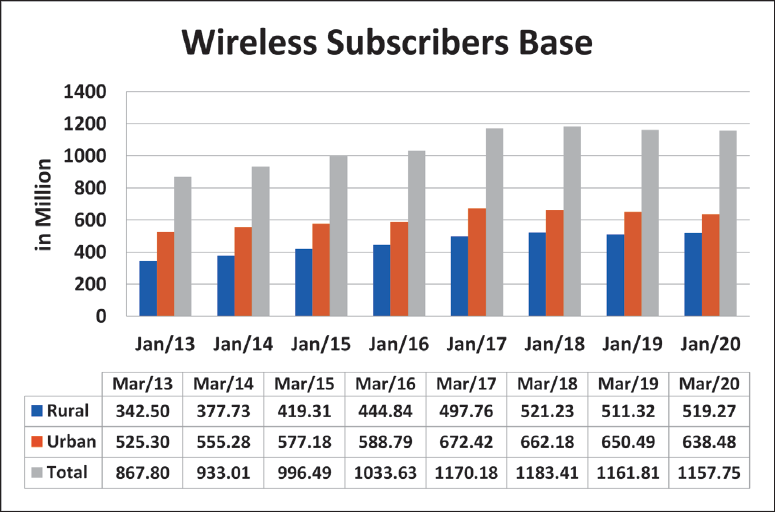

All these developments have made the telecom sector a disruptive market. Table 1 shows the market share of various wireless service providers in India during the period ranging from 2013 to 2020. The rural and urban subscriber base data are given in Figure 1.

Market Share of Wireless Service Providers (%) During 2013–2020.

aFormerly known as Telewings till 2015.

bOthers include MTNL and Quadrant, Systema, Videocon and so on.

Any disruption resulting in the pruning of existing players leads to the advent of compounders that become detrimental to existing players. Similarly, the telecom industry in India also witnessed an unprecedented disruption with the entry of Reliance Jio Infocomm Ltd in 2016 and its offerings of free voice and mobile data. Jio was able to identify the needs of customers, resolve their conventional problems of calling and connecting by offering them unlimited high-speed 4G bandwidth at the cheapest possible rates with the intention of making the other companies bleed. In line with its predatory pricing strategy, Jio’s cheapest plans began at just over $2 per month, making mobile telephony accessible to 90% of the Indian population. It started winning over the market with its cheap data and good speed. With the advancement of technology and the move towards a digital economy, people started using data-driven services more frequently, which fuelled their consumption of data and the need for higher speeds. Jio met these requirements better than the other players, with detrimental consequences for them. Companies such as Vodafone, Idea and Bharti Airtel had to reduce their prices owing to competition and a vicious price war, thereby losing revenue due to a fall in ARPU (average revenue per user). This resulted in a decline in the total revenue of the telecom sector by 3%–5%. Despite heavy spending on marketing and advertising, prices overpowered the brand consciousness of customers. Some players tried to overcome the price competition through new product lines, namely tying up with over-the-top (OTT) platforms to provide media content to customers. For instance, Reliance Jio tied up with Amazon, Hotstar and Netflix to gain differentiation in this segment.

In the face of insurmountable pressure and high costs, some small players like Videocon and Systema were forced to exit the market. The large players like Bharti Airtel, Vodafone India and Idea Cellular went on a consolidation spree, which was seen as a move to increase the size and bring economies of scale to telecom services. Despite the excessive competition, there was a scope for growth as there was an increasing need for voice and data services. The total number of wireless subscribers in India was 876.81 million in 2013, which increased to 1,170.17 million in 2017, according to the Telecom Regulatory Authority of India (TRAI), Annual Reports 2013–2017. In the wake of the ongoing churn in the market, Vodafone India and Idea Cellular decided to make the strategic move of creating a new entity, thereby becoming the largest telecom company in India by size, that would enable them to combine their resources, gain synergies, expand their customer base as well as their market share and, above all, beat competition from Jio. It was expected that the new entity would turn out to be the largest and leading performer in the Indian telecom sector.

VODAFONE INDIA LTD

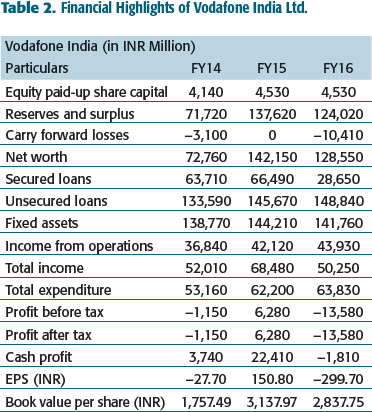

Vodafone India Ltd was incorporated in 1994 to provide telecommunication services in India. It was set up as an Indian subsidiary of 35-year-old UK-based Vodafone Group plc. Vodafone entered India in 2007 through its Netherlands-based subsidiary, which purchased a 67% stake in Hutchison International Telecommunications Ltd from Hutchison Essar India Ltd for approximately INR 458.9 billion. The company soon became very popular due to its various advertising campaigns and became one of the top three telecom operators in India. However, the company faced an INR 103.37 billion tax dispute over its Hutchison Essar deal that, as per Indian tax authorities, was liable to be taxed in India since it involved the purchase of assets of an Indian company. Additionally, the company started facing a lot of competition from other telecom operators like Bharti Airtel and Reliance Jio and wanted to devise a strategy of inorganic growth in the face of the growing disruption in the telecom sector. Hence, Vodafone felt the need for consolidation to overcome these issues and focus on businesses such as voice, data services, leased lines, conferencing and so on. The financial highlights of Vodafone India Ltd from FY2014 to FY2016 are presented in Table 2.

Financial Highlights of Vodafone India Ltd.

IDEA CELLULAR LTD

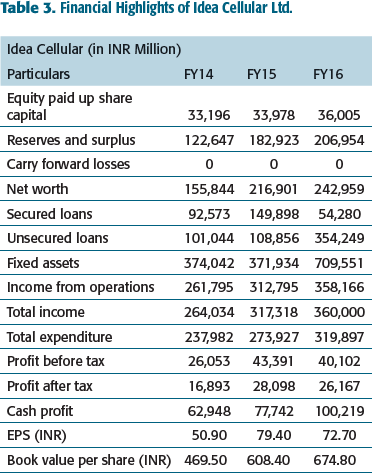

Founded as Birla Communications Ltd in 1995, Idea Cellular got its name after a series of mergers and joint ventures with AT&T Corporation, Grasim Industries and the Tata Group. Idea Cellular finally became a subsidiary of the Aditya Birla Group after the exit of AT&T Corporation in 2004 and Tata Group in 2006. After the Aditya Birla group took charge of Idea, the company redefined its strategy by focusing on expanding the rural area network, where the demand was high but inadequately served. The company soon built a wide distribution network. It grew because of its investments, which focused on economies of scale as well as the popularity of its value-added services. However, the entry of a new player, Jio, started effacing these competitive advantages that Idea enjoyed. Idea Cellular wanted to expand its 4G services to new circles and add new sites (The Economic Times, 2016). However, the tough pricing war by Jio had driven the company into losses, with a 59% drop in its comprehensive consolidated income. This necessitated a shift for the company from a volume strategy to a price-differentiation strategy. The company looked forward to gaining a subscriber base via offerings of 4G at affordable prices. The financial highlights of Idea Cellular Ltd from FY2014 to FY2016 are presented in Table 3.

Financial Highlights of Idea Cellular Ltd.

THE DEAL STRUCTURE: THE MERGER OF EQUALS

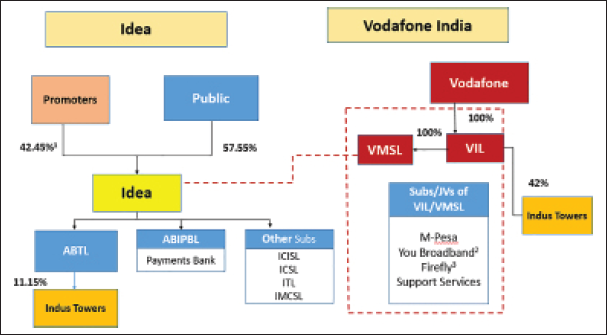

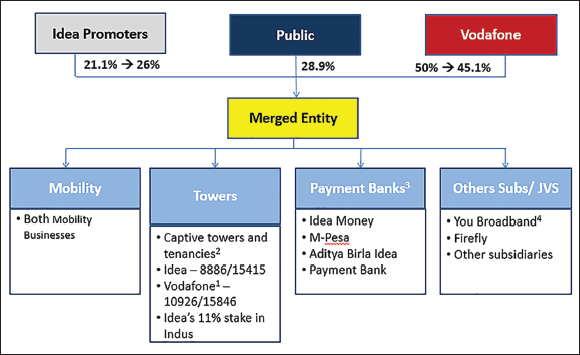

The Vodafone–Idea merger was a merger of equals based on the objective of creating a combined entity under the joint control of Vodafone India and the Aditya Birla Group. Vodafone Group plc decided to deconsolidate and merge its loss-making subsidiary, Vodafone India Ltd (excluding its 42% stake in Indus Towers), with Idea Cellular Ltd (Press Trust of India, 2017). Considering this as a merger of equals, the deal had a swap ratio of 1:1, which implied that every share of Idea Cellular Limited would be exchanged for one share of the merged company. In line with the vision of equalization of ownership by the two promoter companies, Vodafone India and the Aditya Birla Group, Vodafone India transferred its 4.9% stake to the Aditya Birla Group for a cash payment of approximately INR 39 billion (Raju & Madhuri, 2020; Vahia, 2019). This led to Vodafone and the Aditya Birla Group owning a 45.1% and 26% stake, respectively, in the combined company, Vodafone Idea Ltd. This ownership was to be brought to an equal holding of 35.6% by each company within 4 years. Failing this, Vodafone would sell 9.5% of its shareholding in the combined entity to the Aditya Birla Group over the following 5 years. The pre- and post-merger holding structure is shown in Exhibits 1a and 1b.

VODAFONE–IDEA: THE COMBINATION GAINS

The merger of Vodafone and Idea was intended to achieve cost synergies for the merged entity. It was calculated that the newly merged entity would gain or rather save costs to the tune of INR 140 billion (USD 2.1 billion) every year (within 4 years of functioning of the new entity) (Fitch Ratings, 2017). Two-thirds of these savings were expected to come from lower operating expenses, and the remaining was to occur through reduced capital expenditures. The net value of this opex and capex worked out to be INR 670 billion (USD 10.5 billion) at the time of the merger. As a step towards this, the company planned to reduce the tenancy of around 73,000 overlapping sites and reduce tower loading, which could result in an annual cost savings of INR 200 billion. There was also a plan to bring energy savings and operational efficiencies by eliminating the older global system for mobile communication (GSM) sites. Sharing of infrastructure, combined advertising and a reduction in general and administrative costs were other opex synergies that were expected. Vodafone India had a revenue of INR 447 billion, while the revenue of Idea Cellular was INR 369 billion. The revenue of the combined entity was, therefore, worked out to be INR 816 billion. With a lower combined cost, the merger was expected to generate a combined EBITDA (earnings before interest, taxes, depreciation and amortization) margin of 40.6%, while the individual EBITDA margins of Vodafone and Idea Cellular were 29.1% and 30.9%, respectively. Hence, the merger was a way to improve the profit margin of the merged entity significantly.

Post the merger, higher availability of spectrum and a high-capacity single radio access network (SRAN) were expected to reduce the capex requirement. The merged entity could avoid overlapping broadband equipment and duplication of infrastructure required for the expansion and upgradation of the 4G network, bringing in capex synergy. It was predicted that the merger would also enable a lower requirement for fiber and electronics to build a large broadband capacity. The merged entity was also expected to have lower leverage as compared to the leverages of the two individual companies. This reduction in debt was to be achieved by the sale of tower assets by both companies. Additionally, the synergies resulting from capex would lead to a lower debt requirement. The net debt of the combined entity would be INR 993 billion, as compared to the individual debts of INR 527 billion (net debt/EBITDA of 4.6) and INR 552 billion (net debt/EBITDA of 4.3) for Idea Cellular and Vodafone India, respectively. This was expected to result in a combined net debt/EBITDA ratio of 3. The average EV/EBITDA multiple of both companies worked out to be 6.35 (the average of 6.4 for Vodafone India and 6.3 for Idea Cellular, as mentioned above) (Philipose, 2017). On the other hand, the EV/EBITDA multiple of their closest competitor, Bharti Airtel (the only pure-play telecom company in the sector), stood at 6.92. 1

Additionally, prior to the merger, the spectrum held individually by Vodafone and Idea was 411 MHz and 316 MHz, respectively. This was significantly less than the spectrum holding of 860 MHz by Bharti Airtel and 650 MHz by Reliance Jio. Owing to a lower spectrum holding but increased data usage requirements by customers, both Vodafone and Idea were unable to perform competently. A merger between these two was expected to put them in the league of Bharti Airtel and Jio by bringing their combined spectrum share to 728 MHz.

Further on, the merger was also expected to have increased the presence of the combined entity in various telecom circles (also called ‘telecom service areas’), namely ‘metro circles’ and ‘A’, ‘B’ and ‘C’ circles. The combination was predicted to make the merged entity either the largest cellular services provider or a very strong number-two player in the leading circles, such as metro circles and A and B circles. On the other hand, in circle C (smaller circles), the company planned to either upstage other players or remain dormant. Prior to the merger, each company had a suboptimal market share in these circles. With a combined customer base of around 400 million, the merged entity was expected to outstrip Bharti Airtel and Reliance Jio, the then-largest players. This increase in market share was expected to bring about improved cost efficiency and help the merged entities to improve their EBITDA margin.

The merged entity planned to launch digital services like VoIP (Voice over Internet Protocol), VoLTE (Voice over Long-Term Evolution), 2 information and cloud storage services. It also envisioned the launch of payment bank services where Idea Cellular already had domain expertise in the Indian market.

THE MERGED ENTITY: A LIMPING HORSE

The merger was expected to result in the creation of a successful telecom company with the largest market share. The merged entity, contrary to expectations, is still struggling with various non-financial and financial business aspects.

Employee Dissatisfaction

Vodafone India and Idea Cellular had quite different organizational cultures that were difficult to synchronize and unify. Vodafone India was a multinational, multicultural organization with an open culture, while Idea Cellular was an Indian, unicultural organization with a traditional mindset. Due to this, the merger faced issues related to acculturation. 3 After the merger, the employees of both companies did not find themselves fitting in well with the merged entity. They were wary of taking directions from managers who earlier belonged to a rival firm. This created a communication gap among employees. The lack of effective communication started affecting the performance of employees, and, hence, the market share of the merged entity started declining.

At the time of the merger in 2017, Vodafone India and Idea Cellular had a total workforce of 25,000. However, by the time the merger was completed in 2018, Vodafone Idea laid off almost one-third of its employees to bring down duplicate resources (CNBC TV18, 2018). This headcount declined after laying off another 4,000–5,000 employees who could not be accommodated (Ganjoo, 2018). This continued job loss created fear and insecurity among the employees, leading to a further loss of morale. The company also withheld promotions and increments for existing employees to cut costs, fight the existing competition and maintain a leading position in the telecom sector (Sengupta, 2018).

Customer Dissatisfaction and Loss of Subscribers

It was hardly a year after the merger that Vodafone Idea customers started expressing their concerns and dissatisfaction with a plethora of connectivity issues such as low connectivity, slow internet speed and call drops (The Times of India, 2019; Vahia, 2019). Vodafone Idea was required to speed up its system integration process and address the problems that the customers were facing to avoid losing them. Although Vodafone Idea assured a rapid integration, it took longer than anticipated, blaming the monsoons for the delays. Later, though the company claimed to have finished the network integration in top priority circles such as Maharashtra and Goa, the customers continued to complain of connectivity issues. Many customers also complained about not receiving any calls or messages that could inform them about the expected trouble in connection. The increasing dissatisfaction of customers, along with the newly available option of MNP, led to customers switching to other companies in hordes and a consequent substantial decline in the wireless subscriber base of Vodafone Idea from 433.91 million in 2017–2018 to 394.84 million in 2018–2019 and later to 319.17 million in 2019–2020.

Issue of Adjusted Gross Revenue Dues

Another setback for Vodafone Idea happened in October 2019 when the Supreme Court of India widened the definition of adjusted gross revenue (AGR) and ordered telecom companies to pay a hefty amount of more than INR 1,000 billion demanded by the DoT (CNBC TV18, 2020). At this stage, Vodafone Idea was already facing huge losses and had the lowest market share in revenue. The promoters were already not interested in investing further in the merged company, considering the intense competition that would make any new investment less useful in turning the company profitable. The AGR issue added fuel to this fire, as paying these dues would require Vodafone India to raise additional funds (Philipose & Sree Ram, 2020). The promoters refused to own the huge liability of INR 283 billion imposed by the Supreme Court unless the government offered support.

Subdued Financial Performance

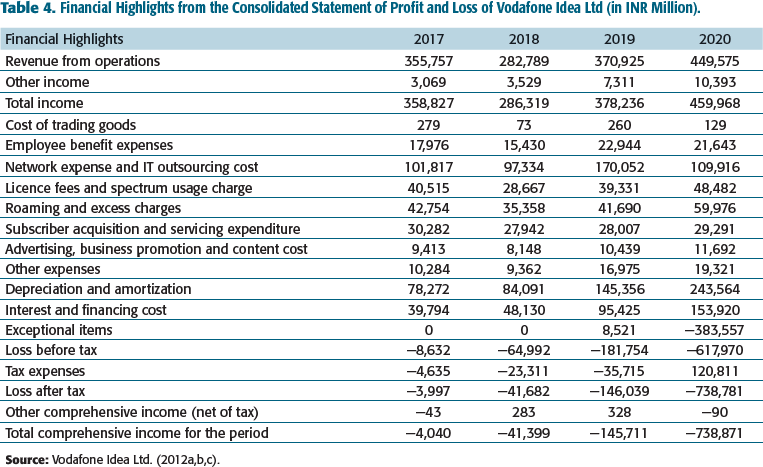

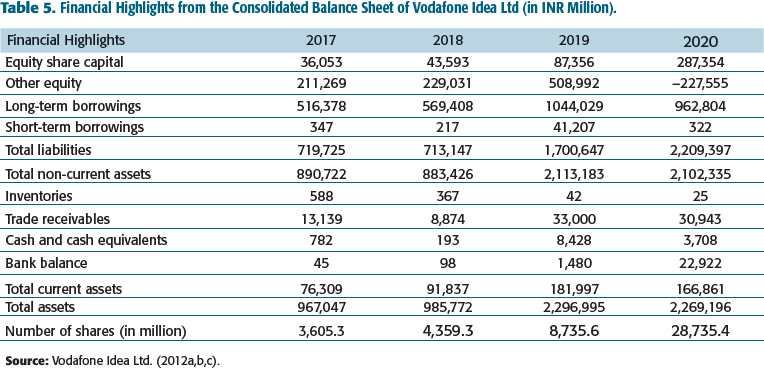

The merger of Vodafone and Idea took almost one-and-a-half years to complete due to the size and complexity of system integration and the government’s pre-requisite to clear dues of nearly INR 1,900 billion on account of pending licence fees, spectrum usage charges (SUC) and one-time spectrum charges (Abhijeet, 2019). The merger created an entity that suffered from exorbitant costs and non-existent profits, as shown in Table 4. Although the company projected a reduction in debt due to the sale of tower assets, its total debt (short-term and long-term) increased by 10.2% in FY18 and 90.5% in FY19, as presented in Table 5. In FY20, the company reduced its debt by 11.3%, yet the value of the debt stands at INR 1,085.2 billion, almost twice the amount of the debt in FY17 (INR 516.7 billion). This upsurge in debt in FY19 was due to the deferred payment of liabilities towards spectrum, amounting to INR 876.5 billion, to the DoT. As a result of this, the net debt to EBITDA of the company increased from 4.9 in FY17 to 5.9 in FY18, while it peaked to 22.2 in FY19. In FY20, the net debt to EBITDA declined to 5.9, which was still very high compared to the company’s post-merger target of 3.0. Hence, the merger, which had the objective of deleveraging, resulted in a huge debt trap for the merged entity.

Financial Highlights from the Consolidated Statement of Profit and Loss of Vodafone Idea Ltd (in INR Million).

Financial Highlights from the Consolidated Balance Sheet of Vodafone Idea Ltd (in INR Million).

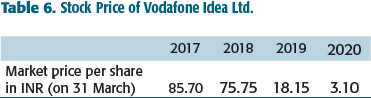

Insurmountable debt in the form of pending spectrum dues and associated costs, along with high operating expenses (88.9% of the revenue in FY19, mainly due to large network and IT outsourcing costs, amounting to 45.8% of the revenue), resulted in huge losses to the company. Consequently, the company’s ability to invest in new technology to offer 4G infrastructure took a hit, and it kept using conventional calling instead of VoLTE, the technology adopted by Jio. Thus, the company was caught in a vicious cycle, wherein the use of old technology resulted in poor service quality (call drops and poor connectivity), leading to a sizeable customer exodus and further losses. Although the company’s ARPU improved to 119 in 2020 as compared to INR 108 in 2019, it was still the lowest in the industry. The impact of all these challenges can be observed in the stock price of the merged entity, as presented in Table 6.

Stock Price of Vodafone Idea Ltd.

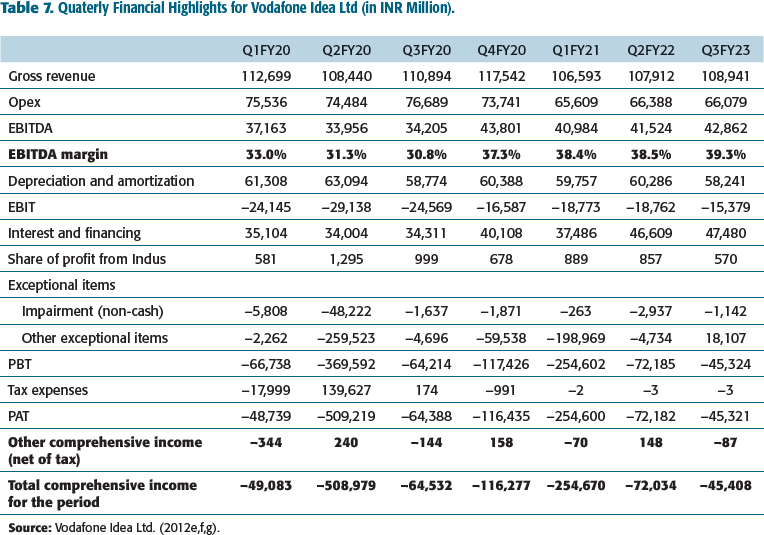

Although the quarterly results of FY21 (Q1, Q2 and Q3) indicate a quarter-on-quarter increase in revenue, the total revenue of the three quarters is still 2.58% lower than the total revenue of the first three quarters of FY20 (refer to Table 7). The company reduced its opex significantly, resulting in a substantial improvement in its quarter-to-quarter EBITDA margins. The values of EBITDA margins were 30.8% in Q3 of FY20, while they improved to 39.3% in Q3 of FY21. Consequently, the company experienced a reduction in post-tax losses. If a similar trend continues, the merged entity may become profitable and achieve the objectives of the merger.

Quaterly Financial Highlights for Vodafone Idea Ltd (in INR Million).

KEY STRATEGIC INITIATIVES

To meet the integration challenges, the company planned several strategic initiatives. The company adopted a focused approach to investment in 4G networks. It intended to concentrate on the rural and semi-urban markets, focusing on investing in 16 priority circles that contributed towards 94% of its revenue and 86% of the industry’s revenue. The company also aimed to seffectively utilize its capex and add to its 4G capacity in these areas to offer a superior experience to its existing customers through its claim of being India’s fastest 4G network. The company also intended to launch 5G services and cut down on 3G and 4G tariff plans to beat the predatory pricing strategy of Reliance Jio. An additional move in this regard was keeping a minimum low-value recharge to take over Jio, especially in rural and semi-urban markets.

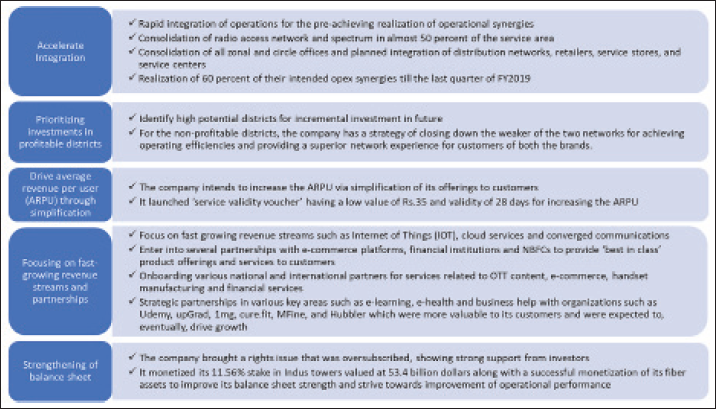

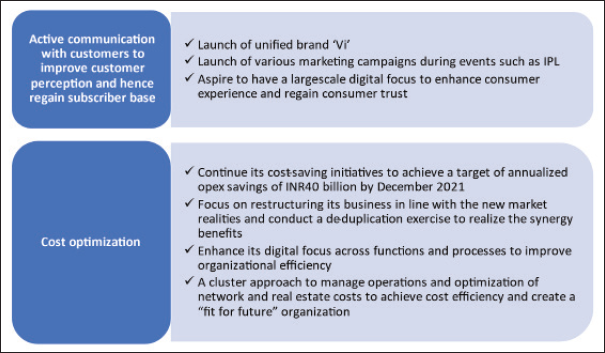

To realize the full advantage of the merger, the company devised a well-laid-out five-pillar strategy. The strategy aimed to increase revenue and profitability as well as strengthen the competitive position of the merged entity in the telecom sector. The five pillars of this strategy are shown in Figure 2. The additional initiatives taken in this direction have also been presented in Figure 3.

THE ROAD AHEAD?

Although Vodafone India and Idea Cellular merged to become the dominant players in the Indian telecom sector due to the realization of the synergies envisaged during the merger, there were several hurdles it faced. Post-merger, Vodafone Idea lost a substantial portion of its talent pool, its subscriber base and, most importantly, the trust of its users due to the lack of concern by the promoters towards the business. Although the company went for a rebranding exercise by launching the brand ‘Vi’, it had already lost ground to competition by then. It also got caught up in the issue of AGR dues and ultimately showed a subdued financial performance. To meet the obligation of AGR dues, other companies in this sector were also considering a prospective tariff hike to increase the ARPU. The government was also exploring possibilities for the revival of companies in the sector that were heavily burdened with AGR dues (Thakur, 2020). Given this background, the company needs to maintain its focus on key initiatives and liaison with the government and other players in the industry (Kaushik, 2019). Additionally, the company must infuse funds to pay off the high existing debt, settle the AGR dues and inject money for fresh initiatives.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.

NOTES

e-mail:

e-mail:

e-mail: