Abstract

Indians have had a fascination for possessing gold since ancient times. I document the sacredness of gold, ancient references to jewellery, gold extraction and minting technology, its function as money and store of value, and specie inflow due to trade surplus with the Occident up until the medieval era. India’s gargantuan stock of about 28,000 tonnes of gold is hoarding and not savings. Today, gold demand is causing leakage from the circular flow of gross domestic product and trade deficit. Policy suggestions are made that will re-channel idle excess stock of gold into financial markets, reduce the trade deficit and contribute to gross domestic product growth.

Keywords

INTRODUCTION

Just a fortnight prior to the Diwali celebrations in November 2021, the Royal Mint of the United Kingdom released a 20-gram gold bar for sale, intricately engraved with the image of Lakshmi, the goddess of wealth, prosperity and beauty. The gold bar, retailing at £1,080, was described by the Royal Mint as a reflection of diverse cultural celebrations in the country (PTI, 2021). Of course, Indians all over the world in general, and India in particular, are fond of buying gold on auspicious occasions such as Diwali, Akshay Trutiya, Ugadi, Gudi Padwa, weddings and quite a few other auspicious days around the year. As reported by the World Gold Council (WGC, 2017, pp. 7, 87), the total household stock of gold in India is about 23,500 tonnes, and about 4,000 tonnes of it is held by temples. Moreover, in the recent past, i.e., since 2017, an additional amount of about 4,000 tonnes of gold has been imported into India (BS, 2022). Furthermore, about 760 tonnes of gold is held in the country's official reserves. Compared to this, the largest official forex reserves in the world are with the United States, which holds about 8,134 tonnes of gold (IFS, 2021). With the price of 22-carat gold hovering at about ₹4,750/gm in early June 2022, the value of India's cumulative stock of gold would amount to a whopping sum of about ₹134.24 trillion or about $1.74 trillion.

Given the above statistics, it should not come as a surprise that India accounts for 25% of the annual global demand for gold. Used mostly for jewellery, India's 22-carat gold stock is one of the purest in the world. Importantly, almost all of the gold demand is met through imports, with barely about 1.5 tonnes produced domestically (GOI, 2018, pp. 18, 45). In the 2020–2021 union budget, the basic customs duty on gold imports was reduced to 7.5% and the import value surged to about ₹2.54 trillion during that financial year (WGC, 2021). Correspondingly, India's trade deficit for the year 2020–2021 was ₹7.56 trillion (RBI, 2021a). This means that about 33.6% of India's trade deficit is accounted for by gold imports alone. India's infatuation with gold gets etched in bold relief against her yearly per-capita gross domestic product (GDP) of just about $2000. For a country which gets placed on the lower side of the lower-middle-income economies (WB, 2022), gold's significant contribution to the trade deficit is a matter of concern. Moreover, in a capital-starved developing country, the accumulation of huge gold stocks can be construed as hoarding and not savings, which otherwise would be available to firms via financial markets for investment purposes.

Science philosopher Michael Ruse (1987, pp. 377–381) said that science without history is like a man without memory. Moreover, to paraphrase the late economist Joseph Schumpeter, one of the ways we can profit from the study of history is that we may learn about the detours, wasted efforts and blind alleys (Schumpeter, 1954, pp. 3–4). The history of India's obsession with gold goes back to ancient times. In this context, the article explores the various dimensions of gold in the Indian economy through the ages. I underscore the sacred dimension of gold in the Indian subcontinent in the second section. The third section addresses the importance Indians have attached to gold jewellery since ancient times and gives a few examples of the types of jewellery used then. The availability of gold in various forms in ancient India and the technological know-how to extract it are covered in the fourth section. That the Indians had an understanding of the precious metal as a medium of exchange and store of value is shown in the fifth section, and the sixth section describes the changed character of the specie flow leading up to modern India. The linkage between the circular flow of GDP and the demand for gold is described in the seventh section. Thereafter, the eighth section provides gold policy prescriptions for various stakeholders such as policymakers, bankers, jewellers, gold associations and exporters that can re-channel India's excess gold stock into financial markets, jewellery making and exports. Finally, concluding observations are made in the ninth section.

SACREDNESS OF GOLD IN ANCIENT LITERATURE

The attributes of gold had caught the imagination of Indian seers many millennia ago. The innate understanding that gold was the most noble metal (corrosion resistant), was malleable, and, of course, had a radiant yellow hue was not lost on them. These attributes bestowed sacred references to gold at several places in ancient Indian literature. In fact, the very creation of the universe is expressed in reference to gold. In the Rig Veda, the foremost of the sacred books of Hindus composed not later than the second millennium BCE, one finds reference to gold in the Hiranyagarbha Sukta (Hymn 121), which appears in the 10th Mandala (Book) of the Rig Veda (Griffiths, 1886; Sharma, 2013). The word ‘Hiranyagarbha’ (in Sanskrit, हिरण्यगर्भ) literally means a golden seed, golden egg or golden womb. The seer who penned the hymn describes that the golden womb is the source of the creation of the universe. The ‘golden’ part is supposed to represent primal radiant energy from which Brahman (Godliness) has emerged. In the Upanishad literature, which followed the Vedas, Hiranyagarbha is considered as the soul of the universe (e.g., Tyagishananda, 1949, p. 102).

Before mentioning Hiranyagarbha in the Rig Veda, there is a supplementary hymn in praise of Goddess Lakshmi titled Shri Sukta at the end of Book 5 of the Rig Veda. The Shri Sukta hymn describes Goddess Lakshmi as one who shines with a golden hue and wears golden garlands. In the Buddhist and Jain literature, too, one finds adoration for Lakshmi. Though Buddhism and Jainism are monastic reform orders, that turned away from Vedic rituals circa the 6th century

Lakshmi appears on gold coins issued during the reign of the Gupta dynasty around the 3rd and 4th century

GOLD JEWELLERY IN ANCIENT INDIA

While Vedas are sacred texts, a significant part of the texts is also dedicated to philosophical thoughts, arts, crafts, music and dance. Rock-carved figures, metal statues and temple sculptures that are available from circa 3rd century

There are quite a few references to gold ornaments in other Vedic literature. Vajasaneyi Samhita version of the Yajur Veda (Griffith, 1899; pp. 256–258) mentions jewellers (30.7) and goldsmiths (30.17). In the Atharva Veda, there are many references to gold jewellery. For example, an ear ornament (pravarta) is mentioned in (15.2.1), gold amulets in (1.35), head ornament (kurira) in (6.138.2) and necklace of Nishka gold coins (nishariya) in (5.14.3). In Tamil literature, the word used for the Nishka gold coins is kasu maalai. Similarly, Shatapatha Brahmana mentions a golden chain (rukma pasha) in (6.7.1–7). In the Sankyayana Gruhya Sutra text, a spouse is expected to sing songs wearing many gold ornaments (MGG, 2017a). In the post-Vedic period, in the 4th century

Along with wearing and manufacturing gold jewellery, one also finds positive connotations associated with gold and gold jewellery. Some references are very practical, and others are faith-based. For example, the poet-philosopher Bhartrihari pens a witty couplet in his Sanskrit treatise Nitishataka that all good qualities (being beautiful/handsome, connoisseur, good orator, master of scriptures, hailing from a noble family) are attributed to a person who possesses gold (Joglekar, 1911). Bhartrihari drives home a real and practical truth that with the acquisition of gold and riches, virtues get attached to a person irrespective of whether or not such qualities reside in that person. Similarly, the Atharva Veda narrates a belief that one who dies of old age becomes what he wears—if it is gold, one will get the splendour, strength and brilliance of gold (MGG, 2017a).

GOLD EXTRACTION IN ANCIENT TIMES

The sacredness associated with gold and the elaborate descriptions of the gold jewellery could not have materialized without the knowledge of extracting gold from natural resources. Ancient Indian literature specifies four different ways of gold extraction. One was to extract gold by panning gold particles from the alluvial placer gold deposits. Again, one of the earliest references to gold extraction occurs in the Rig Veda. There are references to alluvial placer gold being extracted from the river beds, particularly from rivers Sindhu (Indus), Sarasvati, Jambu and Ganga. The Sindhu River was an important source of gold. In the Nadistuti Sukta of the Rig Veda, the Sindhu River is also referred to as Hiranyayi (10.75.8), i.e., giver of gold, and since the path contained alluvial gold, it was also referred to as Hiranya-vartanih (8.26.18). One of the seers, Sayana mentions that both banks of Sindhu had gold. Similarly, gold obtained from the river Jambu was called Jambunada, and that from the river Ganga was called Gangeya. In fact, there are modern references to the source of the Sindhu River, where gold mines existed in Manasarovar and Thokjalyug (IGNCA, 2021).

Moreover, in the epic Mahabharata, there are references to pipilika gold (ant gold) being showered upon King Yudhishthira at the Rajasuya Yagna (coronation sacrifice) ceremony. Pipilika gold was of high quality and came in powder form. This gold was called 'ant gold' because it was extracted by panning the auriferous soil of the ant/termite hills containing placer gold deposits. Buddhist treatise Anguttara Nikaya, written in the Pali language, also refers to the extraction of gold dust and particles from the alluvial placer gold deposits. Furthermore, Kautilya, in the Arthashastra, refers to a naturally occurring liquid with dissolved gold found in rock crevices. One unit (pala) of such gold could be used to transmute 100 palas of copper or silver through gold coating. Later, circa 4th century

Shatapatha Brahmana refers to gold being obtained by mining and smelting ore (IGNCA, 2021). Kautilya too had identified various kinds of gold ores (suvarna-dhatav) and the way to process them in chapters (2.12) and (2.13) of the Arthashastra. He clearly stated in chapter (2.12) that the director of mines (aakaradhyaksha) had to be an expert in the science of (metal) veins in the earth, metallurgy and the art of smelting. Various tests for assaying gold are also part of the text. He alludes to touchstones from the regions of Kalinga and Tapi to be the best ones to test gold. The details with which Kautilya has given information on gold ores, processing, testing and manufacturing of articles indicate the high level of metallurgical advances already made by the 4th century

MINTING OF GOLD CURRENCY

If the ancient Indians had cast gold into a sacred mould, if the artisans had expressed their creativity through gold jewellery, and if the geologists and metallurgists had mastered the science of extracting gold, ancient Indians had also understood the importance of minting gold coins as a medium of exchange and store of value. Del Mar (1885, p. 68) asserts that the stamping and casting of coins occurred in India prior to the advent of the Greeks. According to Bhandarkar (1921, pp. 46–47), the beginning of the art of coin making must be placed much before the 7th century

Jataka tales also corroborate the use of gold coins. Jatakas are stories from the pre-Buddhist literature reflecting on the socio-political life in India around the 7th century

By the post-Vedic period, however, easily panned deposits of alluvial placer gold had dried up (Del Mar, p. 70). Karshapana coins made of silver and/or copper had become more prevalent. In this period, we find references to the minting of coins in the Arthashastra. Kautilya draws references to the superintendent of mint (Lakshanadhyaksha), and next in the hierarchy was the coin examiner (Rupadarshaka) under him. They oversaw the circulation of coins in the economy and the replenishment of the treasury. Circulating counterfeit coins was to be punished heavily with 1,000 Karshapanas, and those who deposited such counterfeits in the government treasury would attract the death penalty (4.1.48). Post-Kautilya and after the death of Ashoka in the 3rd century

That the gold was getting scarce had become obvious from the fact that not even once Kautilya made any reference in Arthashastra regarding the production of gold coins. Though cheaper than gold, even silver was getting relatively scarce. As a result, while both gold and silver were a good store of value, rulers had to pay attention to the more immediate function of money—the medium of exchange. Samples collected by Cunningham showed 20% copper and other alloys in the silver Karshapanas (Bhandarkar, 1921, p. 162). However, one notices that Kautilya had allowed 31.25% of copper and other hardening alloys to produce a silver Karshapana (2.12.24). This shows that as silver continued to become expensive, Kautilya allowed an increased proportion of copper in the silver Karshapana. Muller (1859, p. 289) also alludes to an anecdote where Kautilya had re-minted 100 million Karshapanas into 800 million Karshapanas to finance a war against the Magadha king Dhanananda. He perhaps increased the alloy content of the coins and/or gave a silver coating to the copper coins to increase the money supply. This anecdote may be one of the first recorded instances of quantitative easing of money. A similar increase in money supply was carried out by the Bactrian kings, rulers of Hindu Shahi of Kabul and the subsequent rulers (Bhandarkar, p. 164).

CHANGED CHARACTER OF SPECIE FLOW INTO INDIA

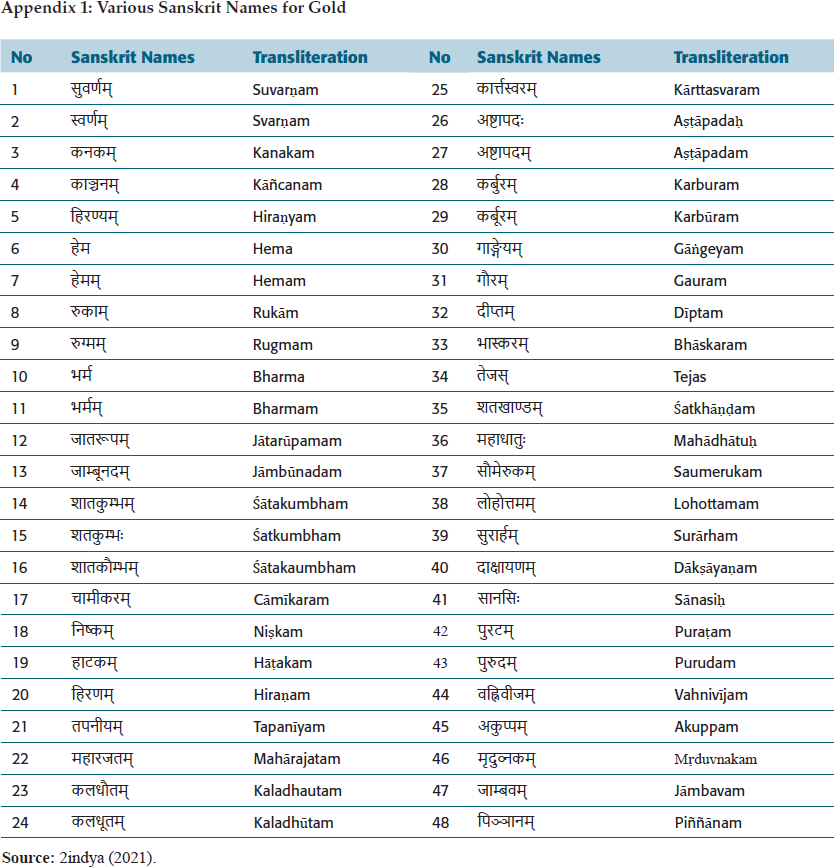

From the recorded history, starting with the Vedic period, we know that gold acquired the status of being auspicious, a fine medium for jewellery, a medium of exchange and a store of value. Therefore, gold has had more than 40 unique names in Sanskrit, most derived as adjectives, depending upon the forms in which it was found, the regions or the rivers where it was found, its sensory attributes, its metallic properties, its end-use in jewellery, and its literary and sacred connotations (see the Appendix). Gold seems to have been available in relative abundance during the Vedic period to be used as a medium of exchange. During the Vedic period, the relative value of gold and silver was 1 silver = 1 gold. Some trade had already begun with the Occident by the end of the Vedic period. Ambedkar (2019, pp. 19–20) quotes that the greed for gold, whetted by the presence of Indian goods in Greece, was the object of Alexander's expedition to North-western India. After Alexander's retreat from India along the Sindhu River and the subsequent establishment of the Mauryan empire by Chandragupta, there was a heightened activity of trade with Greece and Rome. Around that time, the relative value of gold had changed to 2 silver = 1 gold. While gold was becoming scarcer over the millennia, it continued to be minted by rulers for commemorative purposes and large transactions until the late medieval period.

By the turn of the common era, the newly found insatiable interest in Indian textiles, iron, spices, perfumes, silk, gems and exotic birds and animals meant that Indian merchants received volumes of precious metals such as gold and silver. By then, Romans were allegedly calling India the land of the Golden Sparrow (Soney ki Chidia). In the 1st century

In these times of prosperity, it should not come as a surprise that between 355

With the continued specie flow into India, the tradition of minting gold coins continued for a while. In the 12th century, King Vigraharaja IV of the Chahamana dynasty from the present-day state of Rajasthan had minted gold coins called Rama-tankas. Similarly, mint master of the Delhi Sultanate, Thakkar Pheru made a mention of gold coins known as Sita-Rami in his work Dravya-Pariksha written in 1318 CA (Gupta & Shastri, 1993, pp. 201–202). As late as the 16th century, the system of minting coins in gold (Mohur), silver (Rupiya) and copper (Dam) was initiated by Sher Shah Suri and carried forward by the Mughals. However, as has been said earlier, gold remained more of a store of value. It began to be used mostly for minting commemorative coins. Silver coin named Rupiya, named after the Sanskrit name Raupya for silver, became the commonly used currency. This Rupiya coin became the precursor of the modern Indian currency, the Rupee (Reserve Bank of India (RBI), 2021b). It should not come as a surprise that in modern times, countries in the neighbourhood of the Indian subcontinent, from Mauritius to Maldives, Seychelles to Sri Lanka, India to Indonesia and Nepal and Pakistan all have the word Rupiya or Rupee in the name of their official currency.

If the sacredness, production, jewellery making, minting and the specie inflow into India due to her prolonged trade surplus with the rest of the world had justified India being called the land of the Golden Sparrow, it also meant that hordes of invaders were attracted to her wealth. Just to give a few examples, if Mahmud of Ghazni raided India 17 times to plunder her treasures (Anjum, 2007), Nadir Shah too ransacked Delhi for many days, looting the famous Golden Peacock throne (Singh, 1963, p. 237). Even Ahmad Shah Abdali invaded India 9 times in the 18th century looting many parts of North-western India, including Delhi. By 1761, while the Marathas did not win the battle of Panipat against Abdali, they succeeded in stopping the onslaught of invaders from the North-west. By 1771, Marathas recaptured Delhi, rescued the Mughal emperor Shah Alam II from the clutches of the British and the Indians could rule themselves till 1786 under the patronage of Marathas (Mehta, 2005, pp. 137–140). In the course of three decades thereafter, however, the Marathas, too, lost to the British East India Company by 1818.

These developments characterized a point of inflection for the specie flow into India. Recurring foreign invasions and looting affected trade adversely, and the specie flow into India as compensation for India's exports stopped. Moreover, the Industrial Revolution in England in the 18th century, the concurrent colonization of India by the British East India Company, and the exploitative trade practices employed by the British crown resulted in economic 'drain' from India (Naoroji, 1901). What this meant was that India was now stuck in a perpetual trade deficit with Europe, and gold was no longer pouring in from the rest of the world. Furthermore, with rising incomes and standards of living worldwide and the relative scarcity of gold to support economic transactions, gold had lost its function as a medium of exchange. Gold production in India too had almost stopped leading up to the 20th century. In fact, close to 1,000 tonnes of gold was produced and sent to England by the British engineering firm John Taylor and Sons from Kolar Gold Fields (KGF) in Karnataka prior to India's independence. Barely any gold was left in the mines when KGF was nationalized in 1956.

While the specie inflow and production of gold had stopped over the centuries and the country had accumulated huge stocks of gold over millennia, the religious, cultural and aesthetic affinity for buying gold and gold jewellery continued unabated. Today, with India being the fastest-growing economy in the world and having enjoyed an average GDP growth rate of more than 7% since 1991, the absolute demand for gold by Indians has been rising. Econometric studies show that the short-run price elasticity of demand for gold in India is −1.2, and the long-run price elasticity of demand is −0.4 (WGC, 2021, p. 4). It is a stylized fact that consumer durables have a higher price elasticity of demand in the short run but a much less elasticity in the long run. A price elastic demand for gold in the short run and price inelastic demand in the long run is a clear corroboration of the fact that gold is considered a highly prized consumer durable by Indians. In fact, gold as a consumer durable seems to be fulfilling the function of a store of value when juxtaposed against the macroeconomic phenomenon of inflation. If one compares the rate of appreciation of gold price vis-a-vis the rate of inflation, gold has outperformed inflation. For example, during the period of 4 decades from 1980 to 2020, while the historical annual return on gold was 9.6%, the rate of inflation was 6% (ETMoney, 2021). Clearly, it has made sense for Indian households to buy gold as a hedge against the loss of purchasing power of the Indian Rupee.

The inflection point in India's specie flow occurred during the late medieval and early colonial times. It has meant that gold, which had been sent to India for millennia as a means of payment for her trade surplus, is now being imported by India instead, contributing significantly to her trade deficit. Gold imports of more than 4,000 tonnes in the last five years are to be viewed in this historical context. For a developing country like India, as referred to in the introduction section, gold imports contributing a third of her trade deficit is a matter of concern. Moreover, accumulating huge gold stocks can be construed as hoarding, not savings. In a capital-starved developing country, if households park more of their savings not in gold but in financial markets, more funds would be available to firms for investment purposes. I elaborate on these points in the next section.

CIRCULAR FLOW OF GDP AND GOLD DEMAND

The multi-millennial association of gold with sacredness, the continued obsession of Indians with gold jewellery and their perception of gold as a permanent abode of purchasing power have come at a cost. As reported earlier, for an emerging economy like India, despite having an accumulated stock of gold of more than 28,000 tonnes valued at a whopping sum of ₹134.24 trillion or about $1.74 trillion, India continues to account for 25% of annual global demand for gold. Of the ₹7.56 trillion trade deficit during the financial year 2020–2021, gold imports accounted for ₹2.54 trillion—more than a third of the trade deficit. Augmenting the domestic supply of gold to counter imports is not an option as of now, at least in the foreseeable future. If KGF mines in Karnataka had stopped producing gold many decades ago, yearly gold production at the Hutti Gold Mines, also in Karnataka, is barely about 1.5 tonnes. The 12th five-year plan working group had outlined that with new investments, production could potentially be augmented to about 70 tonnes by 2030 (GOI, 2018, pp. 34, 44–45). This is a pittance compared to India's annual import of about 900 tonnes of gold.

Moreover, hitherto absent gold demand from the industrial sector is also likely to go up substantively. A mobile phone contains 0.034 grams of gold. As an efficient and corrosion-free conductor of tiny current, gold is used in all electronic goods, appliances and components. It will also be required for the sustainable generation of electricity through photocell panels. In fact, gold has become an extremely dependable material in all space applications, including making satellites, rockets and rovers (MEC Mining, 2020). There are uses in the medical field, be it dentistry, medicines (Ayurvedic and allopathic) or medical equipment. Currently, the worldwide use of gold for technology purposes accounts for 8% of the yearly global demand (Statista, 2021). India's current annual demand for industrial use is barely 1.4% (GOI, 2018; p. 34); however, with the government's focus on Aatmanirbhar Bharat, aiming to take the contribution of technology and manufacturing to 25% of GDP, there is a huge potential for growth in gold demand from the industrial sector.

Given this context, most of the gargantuan stock of India's idle gold cannot be viewed as accumulated savings but as hoardings. In the domestic circular flow of GDP of an economy, if taxes, imports and savings are the leakage from the circular flow, government spending, exports and investments are the corresponding injections in this circular flow. Injection of government expenditure on public good assets, private investments that build demand and capacity to produce goods and services, and foreign demand for domestically produced goods (exports) are the engines of growth for GDP. Demand for gold turns out to be a double whammy. The demand for gold is met by imports, which is a leakage from the domestic circular flow of income, and to the extent that household money goes into buying gold and not into stocks, bonds, mutual funds, bank deposits and/or postal savings accounts; private firms and government are deprived of the opportunity to borrow these funds from financial markets and make investments to produce goods, services and public good assets. Gold holdings, thus, become a leakage from circular flow, for which there is no corresponding injection of investments into the domestic economy. Unexploited investment opportunities mean that GDP, employment and standard of living do not increase to their potential level through the income-multiplier process and the economy operates at a low-level GDP equilibrium.

Clearly, therefore, there is a scope for adopting an effective gold policy and stakeholder initiatives that enhance recycling idle excess stock of gold and channel it for productive purposes through financial markets. Re-channelling idle gold stocks will reduce annual gold imports significantly and save precious foreign exchange for the country. Trade deficit, of course, can also be reduced by increasing exports of gold jewellery. Moreover, the policies will have to not only convert the existing stock of hoardings into financial savings and investment but also increase the propensity of the flow of current annual savings going into financial markets. To give an example, if China's gross domestic savings rate has averaged more than 45% in the last decade (WB, 2021), India's gross domestic savings rate was only about 30.1% of GDP in the year 2018–2019. Out of this, 18.2% was the annual household savings rate (GOI, 2021a). However, the annual household financial savings rate was only 7.2% (RBI, 2020). A study conducted by NCAER has indicated that nearly 11% of Indian households' savings are in gold (GOI, 2018, p. 84). In the following section, I discuss the possible gold policy prescriptions and initiatives for various stakeholders such as policymakers, bankers, jewellers, gold associations and exporters.

FEATURES OF GOLD POLICY

Recalibrate Existing Gold Monetization Scheme

One of the critical components of the government policy would be to re-channel the existing stock of excess gold, which remains idle in private hands. Of course, householders, temples and trusts would keep some gold jewellery with them for regular use and some more for festive occasions. However, the additional idle stocks of gold items can be made available to jewellers and industry through the market. To this effect, the Gold Monetization Scheme (GMS) was announced in the union budget of 2015–2016, whereby individuals could deposit gold with banks and earn interest of about 2.5%. However, by 2018, only about 10 banks participated in the scheme, and only a few branches would act as collection centres for GMS deposits. Consequently, the scheme attracted only 11 tonnes of gold. Clearly, the scheme has to be recalibrated to sound more attractive and efficient as well. The number of banks and their branch network for deposit collection need to be substantially widened to access the existing stock of gold. Some pecuniary incentives for banks would be required. Contrary to perceptions, disproportionately large gold holdings in smaller quantities are with the lower-wealth strata of the society. Rural India accounts for 60% of the gold jewellery demand (GOI, 2018, p. 34). Therefore, bank branches in rural areas need to participate in GMS scheme with deposits as small as 1 gram. Just as the government allowed Jan Dhan bank accounts to be opened even with zero bank balance, a similar initiative could be taken for the penetration of GMS. Importantly, banks could be incentivized for their effective participation by allowing their gold deposits to be counted in their RBI-mandated cash reserve requirement (CRR).

Behavioural Nudges by Policymakers and Bankers

Furthermore, it would help to give behavioural nudges to customers to open GMS accounts. For example, in the case of the LPG subsidy, initially government had appealed to the conscience of the people through print and electronic media to give up the subsidy. Many gave up their subsidy voluntarily before it got removed eventually. Policymakers and bankers could give similar nudges to individual customers, religious trusts and temples through print and electronic media to deposit their idle gold, gold coins and gold jewellery in GMS. The nudging could happen by providing information that the GMS gold deposits are not only secure with banks, but they earn an interest of about 2.5%; that the customers will enjoy appreciation of gold price since they will have the flexibility either to take cash or gold at the end of the maturity; and that there is no wealth tax, capital gains tax and income tax on valuation, appreciation and interest, respectively (GOI, 2021b). In fact, customers would also save the fee they have to pay otherwise when they keep their gold in bank lockers. The gold coins were a medium of exchange in Vedic times and eventually gave way to silver coins, copper coins, paper currency and now electronic transactions. Nonetheless, people retained faith in the ever changing medium of money. Similarly, Indians could also retain the auspiciousness associated with their idle physical gold, gold coins and gold jewellery, albeit in the form of modern gilt-edged gold deposit receipts. An important incentive in this context would be to cover the gold deposits with a deposit insurance scheme for the customers.

Bankers to Synergize Their Gold Loan Schemes

GMS can be promoted through the banks' gold loan network as well. Gold loans have been very popular in India due to their ease of access, minimal documentation, quick disbursal, relatively low interest rate, low default rates and, of course, no collateral requirement other than gold itself. Importantly, in the last decade, commercial banks and non-bank financial companies, in particular, have made inroads in both the rural and urban gold loan markets. The gold loan assets under management (AUM) were growing in double digits and were expected to exceed more than ₹31 billion by the year 2020 itself (KPMG, 2017, pp. 9, 17). It is pertinent to note that while the hallmarking of gold has already been standardized by the Bureau of Indian Standards, the KYC norms are also well established by the central government. Therefore, a two-way synergy between GMS deposits and gold loans can exist. When gold loans are repaid, the gold collateral could potentially be converted into GMS deposits, and new GMS deposit holders will also have easier access to gold loans if the need arises. Importantly, in both cases, documentation of gold and customer authentication will not have to be duplicated. This way, customers will have more flexibility and bank overheads, and the network will be used more efficiently.

Promoting GML and Other Complementary Schemes

Concurrently, as the GMS network infrastructure is widened sufficiently and banks generate substantive gold deposits, the complementary Gold Metal Loan (GML) scheme for goldsmiths and jewellers can be widely promoted. Under GML, banks will be able to use the gold deposits of the customers to provide gold inventory needs of jewellers at competitive interest rates. India's GDP growth rate was more than 8.5% in 2021. It continues to be the fastest-growing major economy in 2022. Therefore, demand for gold jewellery will continue to be high in India, for which the GML scheme would come in handy to jewellers for their working capital needs of gold. Similarly, the Indian Gold Coin (IGC) scheme, which was introduced along with the GMS in 2015–2016, can also be effectively used by banks. With the GMS gold deposits at their disposal, banks should be allowed to meet the demand of fresh customers looking to purchase minted gold coins through IGC. Recycling of gold through these mechanisms has the potential to reduce imports substantially.

Similarly, once private idle gold holdings are channelled through the banks, other gold-based financial instruments will also be useful to recycle those gold stocks for new gold customers. For example, a gold-backed exchange-traded fund (ETF) is listed on the National Stock Exchange and Bombay Stock Exchange. It is fully backed by gold of 99.5% purity. This market will develop well when recycled gold deposits through GMS are available for onward loan or sale by banks. The development of such a market will help household savings go into financial investments rather than physical gold hoardings. The Sovereign Gold Bond (SGB) scheme was yet another instrument issued in 2015–2016. However, it has not been backed by gold. As pointed out by Reddy (2017, p. 22), the efficacy of this instrument and its benefits are not that obvious both to the government and the buyers. Niti Aayog Committee (GOI, 2018) also proposed a Gold Saving Account (GSA) in addition to GMS. GSA would allow customers to save up in rupees, but the accumulated amounts are translated into physical gold. This instrument is meant mostly for lower-income new customers to buy gold. Furthermore, the newly formed India International Bullion Exchange (IIBX) from GIFT City, Gandhinagar, Gujarat, can provide a transparent ecosystem for trading gold, which will aid the functioning of other gold schemes.

Branding and Export Promotion by Industry

There is always a temptation to reduce imports by increasing customs duty on gold. Any effort to increase customs duty from the existing level of 7.5% should be resisted. Decades of experience suggests that higher customs duty leads to circumvention of rules, under-invoicing, smuggling and black marketing, usually with the active participation of anti-social elements of the society. Importantly, a high import duty acts as high export tax, particularly when products are re-exported with domestic value addition. In fact, one way to reduce the trade deficit on account of gold imports is to export gold jewellery. The recent trend in the export of gold jewellery is encouraging. As reported by the Gems and Jewellery Export Promotion Council (GJEPC), in 2019, India exported ₹11.5 billion worth of gold jewellery accounting for 11.3% of world exports (GJEPC, 2019, p. 8). There is a good potential for branding, marketing and export of handcrafted Meenakari, Kundan and other Indian jewellery types. GJEPC, jewellers, exporters and the Indian Bullion and Jewellers Association (IBJA) may undertake consorted efforts to market Indian jewellery abroad through roadshows and exhibitions.

Museo del Oro, a gold museum in Bogota, Colombia, claims to be the world's largest gold museum (MGG, 2018b). Established almost eight decades ago, this museum showcases pre-Columbian gold artefacts as Colombia's national heritage. In comparison, India's multi-millennial gold heritage would be a much larger national asset. In the Indian context, as households, trusts and temples take inventory of their idle gold stocks with a view to participate in GMS; it is hoped that precious coins, jewellery, artefacts, statues, figurines and perhaps related sacred texts and scientific treatises associated with gold will come to light. While voluminous generic gold items can be deposited under GMS, priceless gold objects can be displayed in a magnificent state-of-the-art gold museum. A consortium of GJEPC, IBJA, IIBX, RBI and India Gold Policy Centre at the Indian Institute of Management Ahmedabad (IIMA) may lead this effort. Visitors would be happy to pay a price to watch 'India's multi-millennial gold heirlooms at a dedicated museum. An Indian Gold Museum, potentially the largest in the world, could become the brand ambassador of India's gold jewellery in the international market. This will be another practical extension of the gold monetization effort.

Taming of the Inflation

Gold is called a noble metal, not just because it is aesthetically appealing but because its physical quality does not depreciate. It is a high-value low-volume investment item. Moreover, its store of value function gets juxtaposed against the macroeconomic phenomenon of inflation. As reported earlier, the return on investment in gold has fared better in relation to the rate of inflation. The rate of inflation in India has been relatively higher than those in stable Western democracies, and, therefore, it has made sense for Indian households to buy gold as a hedge against the loss of purchasing power of the Rupee. Of course, the gains of holding gold can only be realized if one were to sell the gold eventually. Households rarely do that. At best, they have the practice of taking gold, gold coins or old gold ornaments to the jewellers for converting them into newer types of jewellery items. What this tells us is that the propensity to retain and buy excessive amounts of gold may go away only if inflation is sustainably tamed. Although RBI has a policy target of maintaining inflation at 4% within a band of ±2%, the current retail inflation has been more than 7.5%. While short-term fluctuations will always be there, RBI would do well in taming the long-run inflation closer to the lower bound of the inflation band. This will wean households away from hoarding gold and channel more of their savings into the financial market.

CONCLUDING OBSERVATIONS

Gold has acquired a unique status among households in the Indian subcontinent. This unique status is a result of an uninterrupted, multi-millennial, civilizational association of gold with sacredness, durability, beauty, aesthetics, availability and its use as a medium of exchange and store of value. Moreover, historically, India has had a trade surplus with the Occident, which resulted in an inflow of gold and gold coins. As a result, therefore, the accumulated stock of gold in India has surpassed more than a whopping 28,000 tonnes. A point of inflection was reached during the late medieval and early colonial periods when India neither enjoyed a trade surplus with the rest of the world nor was gold being used as a medium of exchange. Today, however, the continued popularity of gold and the rapid GDP growth has resulted in strong domestic demand for gold, which has not been matched by specie inflow or domestic production. As a result, the yearly demand for gold is matched exclusively by imports valuing more than ₹2.5 trillion, accounting for about a third of India's trade deficit. Also, unlike most savings, which get injected into the circular flow of GDP through financial markets, gold purchases by households are hoardings which contribute to the leakage from the circular flow of GDP.

To address this issue, the union budget of 2015–2016 had come up with an initiative to channelize the stock of gold through GMS. The initiative has not succeeded. A focused, multi-pronged approach would be required to recycle the gargantuan existing stock of gold. Participation of banks and collection branches has to be much wider, both in urban and rural areas. Banks could be incentivized for their effective participation by allowing their gold deposits to be counted in their mandatory CRR. Also, an extension activity may be required to nudge households to access GMS by informing them about the security, avoidance of locker charges, interest earnings, exemptions from wealth, capital gains and income taxes, flexibility of taking cash or gold on maturity and, of course, emphasizing faith in the banking system—be it for current accounts, saving accounts, fixed deposits or the GMS gold deposits. Gold deposit accounts can also be covered by the deposit insurance scheme. These initiatives can get a further boost if the banks and branches synergize their network of popular gold loan schemes with GMS.

Concurrently, as the GMS network infrastructure gets widened and banks generate substantive gold deposits, the complementary GML scheme meant for goldsmiths and jewellers can be widely promoted which will provide for gold inventory needs of jewellery manufacturing, both for domestic sales and exports. As the gold stocks start getting recycled, it will also infuse increased liquidity in the gold market through gold-based instruments such as ETF, IGC, SGB, GSA and the newly established IIBX. In fact, export promotion of gold jewellery could also effectively reduce the trade deficit. Jewellers, exporters, RBI and a few gold associations can initiate marketing efforts for traditional gold jewellery and create a global image for the Indian brand by instituting the largest gold museum in the world. And, of course, RBI maintaining a low rate of inflation over a sustained period of time can lower the propensity of households to hold on to excessive amounts of gold. The multi-pronged approach described above could reduce India's dependence on gold imports and save precious foreign exchange. And, of course, channelizing more household savings into financial markets will inject more investments in the circular flow of the economy, contributing to increased employment, income and standard of living.

If Michael Ruse had opined that science without history is like a man without memory, Joseph Schumpeter had also said that we do stand to profit from visits to the lumber room, provided we do not stay there too long. Surely, India can profit from taking a pause and recalibrating the dynamics of her millennia-old gold room. The continued fetish for gold can be turned into an opportunity with an appropriate mix of initiatives by policymakers, bankers and industry leaders. If the Royal Mint of the United Kingdom can leverage sacredness by selling gold bars engraved with Goddess Lakshmi, India can capitalize on its golden heritage to create a global brand for its bullion.

Various Sanskrit Names for Gold.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.

NOTES

e-mail: