Abstract

Foreign direct investment (FDI) has gained prominence in international economics over the past three decades. Primarily, the belief that FDI influences economic growth of the host country, set the stage for the empirical research focused on the FDI–growth nexus. The growth literature, however, reveals mixed evidence regarding the role of FDI in promoting growth. Despite the conflicting evidence, developed and developing economies have attached immense economic and political importance to FDI. It is noteworthy that BRICS (Brazil, Russia, India, China and South Africa) economies are representative developing economies and have emerged as significant FDI destinations, having witnessed an immense surge in inward FDI over the past few decades. It is against this backdrop that the present study attempts to assess the impact of FDI inflows and select macroeconomic variables, namely macroeconomic stability, human capital, financial development and trade openness (TO), on the economic growth of developing BRICS economies. The study examines both short-run and long-run relationships between FDI inflows, select macroeconomic variables and economic growth by employing the dynamic panel autoregressive distributed lag (ARDL) model, unlike most of the previous studies.

For this study, secondary data covering a reference period of 32 years (1987–2018) were used. The data on GDP growth (GDPG), FDI inflows, inflation (INF), human capital, private sector bank credit (proxy for financial development) and TO have been collected from the World Investment Reports published annually by United Nations Conference on Trade and Development (UNCTAD) and World Bank (World Development Indicators). The findings revealed a long-run cointegration among FDI, host country characteristics (TO, human capital, financial development and macroeconomic stability) and economic growth in BRICS.

The process of economic development has become much more complex, and perhaps this precedes a more elaborate set of theories to explain fully the intricate dynamic relationship between public investment, private investment and FDI, which, while interacting with other country-specific macroeconomic features, is believed to reveal a synthetic pattern of economic growth. Because of this belief, FDI has achieved great significance in international economics. It has propelled researchers worldwide to study the FDI–growth nexus, especially in the economies experiencing the deficiency of capital investment. Many researchers have opined that the flow of FDI could fill the gap between desired investment and domestically mobilized capital (Hayami & Godo, 2005; Todaro & Smith, 2011), and FDI tends to accelerate development through effective strategies and break the vicious cycle of underdevelopment (Hayami & Godo, 2005). Although economists and policymakers often find themselves utterly bewildered about the ostensible relationship between FDI and economic growth, both developed and developing economies have attached immense political and economic importance to this source of investment.

Economic growth and development theories suggest that the factors generally responsible for the increase in economic growth are capital accumulation, technological progress and natural resources. The interaction of these factors has led to the development of different theories of economic development in the growth literature. In many theories, capital accumulation is considered to be a catalyst of growth in an economy. FDI influences the rate of economic growth of the host country in two ways: capital widening (through capital formation) and capital deepening (through technology transfer). In this context, the two main theoretical perspectives that provide the framework for analysing the growth effect of FDI are neoclassical and endogenous growth theories. Inward FDI flows result in an increase in physical capital stock, known as capital widening. Capital widening is the increase in the physical capital stock that improves the per capita capital and ultimately increases output per capita (Solow, 1956). According to the neoclassical growth theory propounded by Solow (1956), this growth may not continue in the long run due to the diminishing return to capital, implying that the neoclassical school of thought suggests that the inward FDI flows may promote economic growth in the short run and not importantly in the long run.

Contrary to this, capital deepening influences growth through spillovers in the form of technology and knowledge. It is well-known that FDI not only increases the physical capital stock of the host economy but also brings technological improvement increasing productivity, leading to both short-run and long-run growth in the FDI-receiving country (Romer, 1994). In this context, the endogenous growth theory developed by Romer (1994) suggests that the main channel responsible for long-run growth in an economy is technological progress. Therefore, if FDI brings new technology and knowledge to the host country, it can promote long-run economic growth.

The empirical studies conducted in the area have revealed mixed evidence regarding the impact of FDI on the economic growth of the host country but as such there is no consensus about the impact of FDI on economic growth. BRICS economies represent developing economies and have emerged as significant FDI destinations. It is against this backdrop that the present study has made a modest attempt to assess the short-run and long-run impact of FDI inflows and select host-country characteristics, namely TO, human capital, financial development and macroeconomic stability on the economic growth of BRICS employing the dynamic panel ARDL model, unlike most of the previous studies conducted in this regard.

REVIEW OF LITERATURE

The FDI–growth relationship has been extensively studied by researchers. However, the studies have used different samples, time periods and methods revealing mixed evidence regarding the role of FDI in promoting growth in the host economy (FDI-receiving economy). Many empirical studies have found a significant positive impact of FDI on the growth of the host country (Bouchoucha & Ali, 2019; de Mello, 1999; Feridun & Sissoko 2011; Hansen & Rand, 2006; Pegkas, 2015; Sahoo & Mathiyazhagan, 2003; Szkorupová, 2014; Tiwari & Mutascu, 2011; Yao, 2006; Zhang, 2001). Some studies, however, found that FDI exerts a negative impact on the growth of the host economy (Herzer, 2012; Mencinger, 2003), whereas others found that no significant relationship exists between FDI and growth (Carbonell & Werner, 2018; Gunby et al., 2017; Hussein, 2009; Ledyaeva & Linden, 2006; Lian & Ma, 2013). An important strand of growth literature reveals that the impact of FDI on growth is not independent but depends on the characteristics prevalent in the host economy. Carkovic and Levine (2002) conducted an extensive study on the FDI–growth nexus in a set of 72 developing countries, and the results revealed that the growth-enhancing effect of FDI is not independent of other determinants of growth. Various empirical studies have suggested that FDI has an impact on growth only in the presence of host country characteristics like macroeconomic stability, human capital, financial development and TO. It was found that the growth-enhancing effect of FDI depends on economic stability in host countries (Jallab et al., 2008; Prüfer & Tondl, 2008). Alguacil et al. (2011) found that economic stability exerts a significant influence on the relationship between FDI and growth. Abdelmalki et al. (2012) revealed that FDI has a positive impact on growth as long as INF (a proxy for macroeconomic instability) does not reach a certain threshold, and similar results were obtained by Bengoa and Sanchez-Robles (2003). Some studies indicate that the growth impact of FDI is contingent upon the level of human capital present in the host economy (Borensztein et al., 1998). Balasubramanyam and Mahambare (2003) found that the ability of FDI to enhance growth depends on human capital. Li and Liu (2005) also stressed the importance of human capital to help developing countries reap the growth benefits of inward FDI. Cao and Jariyapan found that FDI on interacting with human capital positively influences growth, and similar results were obtained by Alfaro and Charlton (2007) and Iqbal and Mumit (2017). Development of financial markets also plays an important role in the FDI–growth relationship as revealed by the empirical studies conducted by Alfaro et al. (2004, 2009) and Kelly (2016). Alfaro and Chauvin (2020) suggested that the spillover benefits of FDI are more evident for countries which have sufficiently developed financial markets. Durham (2004) while examining the impact of FDI on growth rejected the view that FDI has an independent effect on growth but instead stressed that the growth performance of FDI depends on the level of financial development present in the host country. TO is also an important host country characteristic for understanding the FDI–growth nexus. It has been proven empirically that open economies are often associated with higher growth rates (Edwards, 1998; Greenaway et al., 2002; Harrison, 1996). The ability of FDI to promote growth is greater in open economies (Nair-Reichert & Weinhold, 2001). Nunnenkamp and Spatz (2003) found a positive FDI–growth relationship in the case of developing countries, but this nexus was found to depend on host country characteristics like GDP per capita, human capital and TO. Atique et al. (2004), Balasubramanyam et al. (1996) and Kohpaiboon (2003) revealed that the growth impact of FDI is greater in those countries following an export-promotion policy than in the countries that pursue an import-substitution policy, supporting the Bhagwati hypothesis. Adhikary (2011), Khamphengvong et al. (2017) and Yusoff and Nuh (2015) found a positive impact of FDI and TO on economic growth using different samples and empirical methods.

According to the UNCTAD database, the inward FDI flows in BRICS countries have increased tremendously from US$ 3,032 mn in 1985 to US$ 258,941 mn in 2018. As per the UNCTAD Handbook of Statistics, four countries in the BRICS bloc, namely Brazil, Russia, India and China, were listed in the top 20 host economies for attracting inward FDI in 2017 (UNCTAD, 2018). In the last decade, there has been an immense surge in inward FDI flows in BRICS (Kapoor & Tewari, 2010; Nistor, 2015). These countries offer huge benefits like low-cost labour, resources and huge market size to attract foreign investors. A few studies have assessed the growth impact of FDI in BRICS countries, finding a positive nexus between the two (Agrawal, 2015; Hayrdaroglu, 2016). However, the question of whether FDI impacts the growth of BRICS countries is not yet addressed in depth and therefore calls for greater attention from researchers.

It can be synthesized from the literature that there is mixed evidence regarding the role of FDI in promoting economic growth of FDI-receiving (host) countries. Moreover, a good number of empirical studies reveal that the growth-enhancing effect of FDI is not independent but depends on the host country characteristics prevalent in the host economy, like TO, human capital, financial development and macroeconomic stability. The present study differs from earlier studies in two ways. First, the study focuses on the dynamic interactions among the select country-specific macroeconomic variables by using the panel ARDL model and is among the few studies that have employed the ARDL model to understand the nexus between FDI and economic growth. Second, previous studies focused either on evaluating the relationship between the FDI and economic growth or on understanding the link between FDI, economic growth and one or two macroeconomic variables. Furthermore, other studies have focused on understanding the link between the FDI, macroeconomic variables and economic growth using either multivariate regression or static panel data models. However, the dynamic panel ARDL approach used in the present study aims to examine the short-run as well as long-run relationship between FDI, important macroeconomic variables (as identified from the synthesis of literature) and economic growth in the fastest emerging BRICS economies which have attracted significant FDI flows over the past decades.

DATA AND METHODOLOGY

Secondary data covering a reference period of 22 years from 1997 to 2018 were used in the study. The data on GDPG, FDI inflows, TO, human capital, private sector bank credit, stock market capitalization (SMC), INF and debt-to-export (DTE) ratio were collected from the World Investment Reports published annually by UNCTAD and World Bank (World Development Indicators). INF and DTE ratios were used as proxies for macroeconomic instability (Abdelmalki et al., 2012; Alguacil et al., 2011), gross enrolment ratio (GER) as a proxy for human capital (Abbas & Mujahid-Mukhtar, 2001) and private sector bank credit and SMC for financial development (Durham, 2004; Kholdy & Sohrabian, 2005).

The descriptive or summary statistical measures used for understanding the general behaviour of data were mean and standard deviation. After descriptive analysis, correlation analysis was performed to assess the degree of the linear relationship between the variables through the correlation coefficient.

Unit root test was conducted afterwards to test the stationarity of variables in a data set. A series of data is said to be stationary if its statistical properties, such as mean, variance and covariance, are constant or time-invariant. We used the standard test for unit root, namely the Im–Pesaran–Shin (IPS) test (Im et al., 2003). In this test, the parameter pi is allowed to vary across panels. To test the stationarity of the variables using the IPS test, the following null hypothesis was tested.

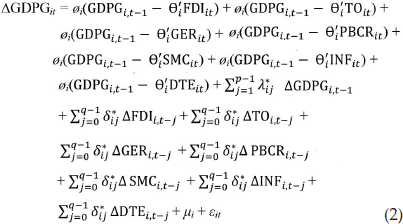

To develop and ascertain the cointegration and long-term relationship among variables, one needs to specify how many lags to include for panel ARDL model. In this study, the default criterion, that is, Schwarz Bayesian Information Criterion, was used to specify the number of lags to be used. To achieve the main objective of understanding the short-run and long-run effects of FDI and identifying macroeconomic variables on the GDPG of BRICS countries, panel ARDL approach was used in this study. The ARDL model, as developed by Pesaran and Shin (1997) and Pesaran et al. (2001), produces the estimates of the long-run coefficients that are highly consistent regardless of whether the underlying explanatory variables are integrated of order zero, that is, I(0) or order one, that is, I(1) or a combination of both. A key characteristic of cointegrated variables is their response to any deviation from the long-run equilibrium. This characteristic signifies an error correction model in which the variables’ short-run dynamics are affected by such deviation. Therefore, the equation for the model is as follows:

where øi is the coefficient of speed of adjustment to the long-run equilibrium. In case øi = 0, then there is no evidence of existence of a long-run relationship. øi is expected to be negative under the assumption of variables returning to a long-run equilibrium. The vector θi′ denotes the long-run relationship among the variables and the notation ‘∆’ denotes the first difference operator.

The panel ARDL model is specified for testing the relationship among the variables of interest, that is, the dependent variable, GDPG and the regressors, namely FDI inflows (FDI), TO, GER, private bank credit (PBCR), SMC, INF and DTE ratio. Based on the model specified in Equation (1), the equation for our panel ARDL model is as under:

Equation (2) can be estimated by the following estimators: pooled mean group (PMG) estimator and mean group (MG) estimator. The PMG estimator allows heterogeneity in the short run (like the MG estimator) but imposes a long-run slope homogeneity for the countries. MG estimator allows both intercepts and slope coefficients (both short-run and long-run) to differ across countries. The condition necessary for the validity of this model is to have a sufficiently large time-series dimension of the data.

After estimating Equation (2) with the PMG and MG estimators, we used the Hausman test to choose the best estimator for running the panel ARDL model. By applying the Hausman test, we can check for significant differences between the two estimators. The Hausman test is a highly reliable test to examine whether the PMG model or the MG model is effective in explaining the relationship among the variables (Pesaran et al., 1999). The null hypothesis of the test is that there is no significant difference between PMG and MG estimators. Finally, we conducted a panel Granger causality test to examine whether the selected covariates Granger-cause the dependent variable (GDPG) or not (Juodis et al., 2021).

RESULTS AND DISCUSSION

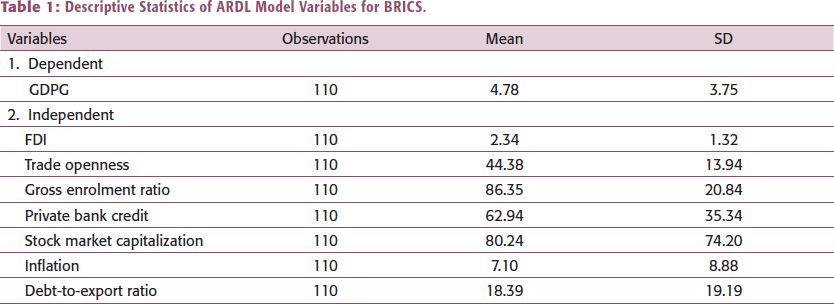

The results of the summary statistics of the variables used in the study are depicted in Table 1. As is evident from Table 1, mean score of the dependent variable GDPG is 4.78, and its standard deviation is 3.75, showing very little dispersion from the mean. The results of the summary statistics for independent variables clearly show that more dispersion, in terms of SD, is recorded, in the case of TO, GER and PBCR. A healthy economic growth (GDPG) is observed in BRICS for the period under study, and less variability is witnessed in economic growth and FDI inflows in the bloc.

Descriptive Statistics of ARDL Model Variables for BRICS.

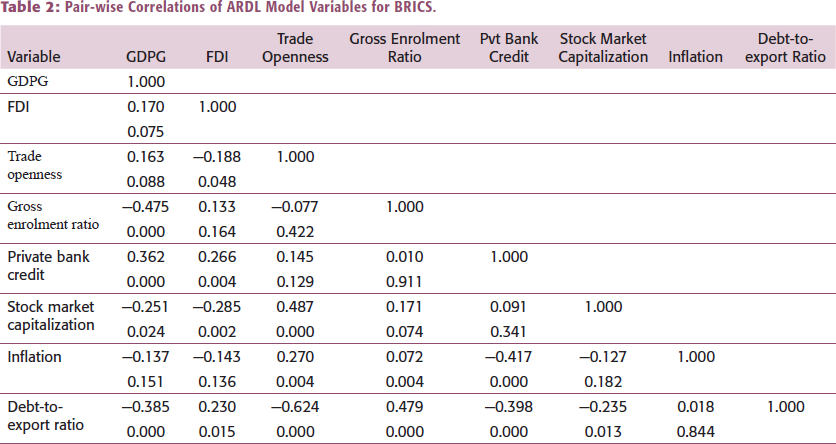

The correlation results of all the variables under study are presented in Table 2. The correlation analysis indicates that none of the variables has a correlation coefficient of 0.70 or more; as such, this model will pass the multicollinearity test. Had the variables suffered from the multicollinearity issue, the regression analysis would yield spurious results of those variables with a coefficient of correlation equal to 0.70 or greater (Cooper & Schindler, 2014) as it leads to wider confidence intervals, insignificant t-statistics and unnecessarily high R-squared (goodness of fit) values. The results reveal that FDI, TO and PBCR have a significant positive correlation with GDPG, whereas GER, SMC and DTE ratio have a significant negative correlation with GDPG.

Pair-wise Correlations of ARDL Model Variables for BRICS.

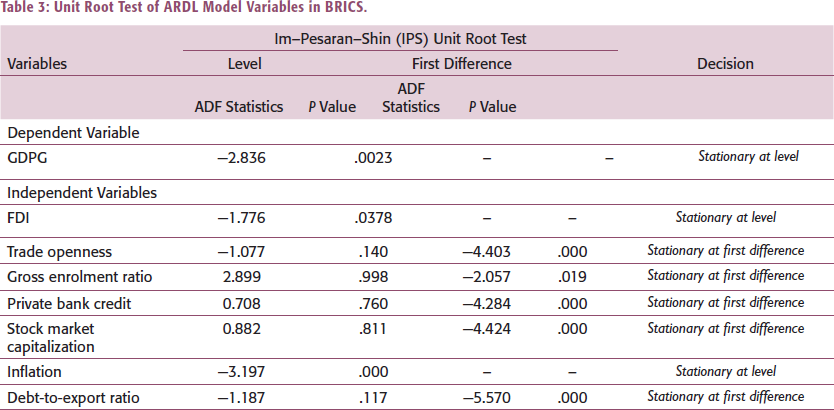

The results of the IPS unit root test presented in Table 3 indicate that GDPG, FDI and INF are stationary at level, whereas other variables are stationary at first difference. The null hypothesis is discredited for GDPG, FDI and INF at level and for other variables at first difference as the p value < .05. This implies that the ARDL model is appropriate for analysis as the variables are integrated into order zero, that is, I(0), and order one, that is, I(1).

Unit Root Test of ARDL Model Variables in BRICS.

The results in Table 4 containing the Hausman test indicate that p value (.104) is greater than 0.05, as such null hypothesis of difference in coefficients is not systematic or the difference between PMG and MG estimation is not significant or the PMG estimator is efficient and consistent, is accepted, and it is deduced that PMG estimator is efficient and consistent, but MG estimator is not.

Hausman Specification Test of ARDL Model.

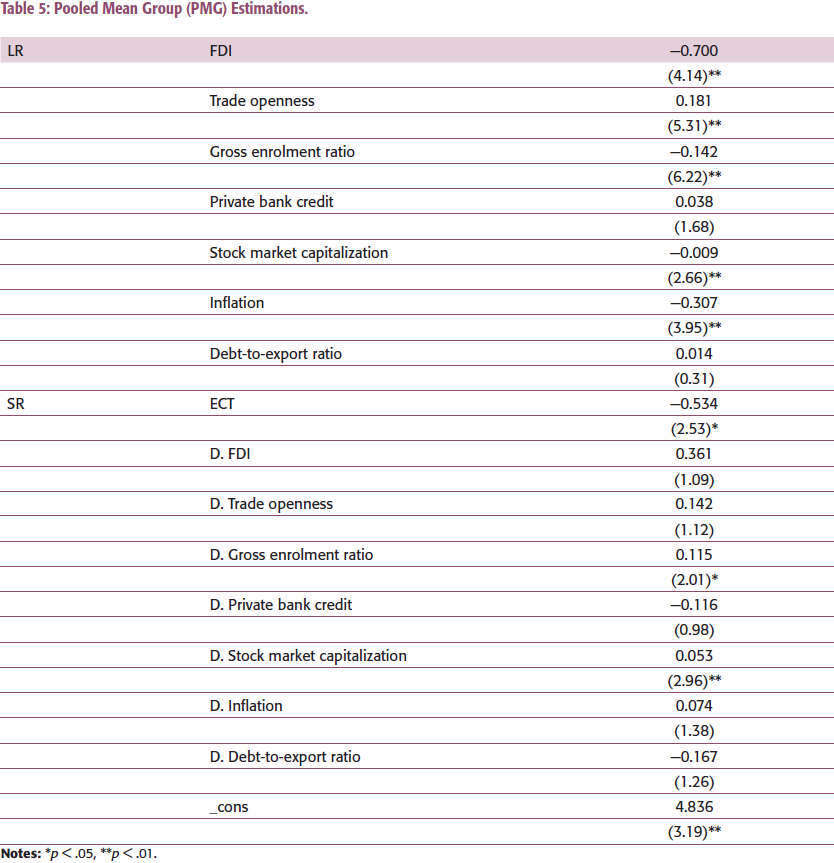

PMG estimator was used to estimate the relationship between the dependent variable (i.e., GDPG) and independent variables (i.e., FDI, TO, GER, PBCR, SMC, INF and DTE ratio) of the BRICS by using panel data. The results in Table 5, containing the long-run coefficients of the PMG model, indicate that FDI (−0.700), human capital (−0.142), SMC (−0.009) and INF (−0.307) have long-run statistically significant negative impact on GDPG, supporting the findings of some previous studies having used different estimation methods (Abdelmalki et al., 2012; Bleaney, 1996; Herzer, 2012; Mencinger, 2003). This reveals that in the long run, a one-percentage-point increase in FDI has the potential to bring a 0.70-percentage point decrease in the GDPG of BRICS countries. TO (0.181) has a significant positive influence on GDPG in the long run, corroborating the results of past studies (Adhikary, 2011; Balamurali & Bogahawatte, 2004; Khamphengvong et al., 2017). The error correction term (ECT)

Pooled Mean Group (PMG) Estimations.

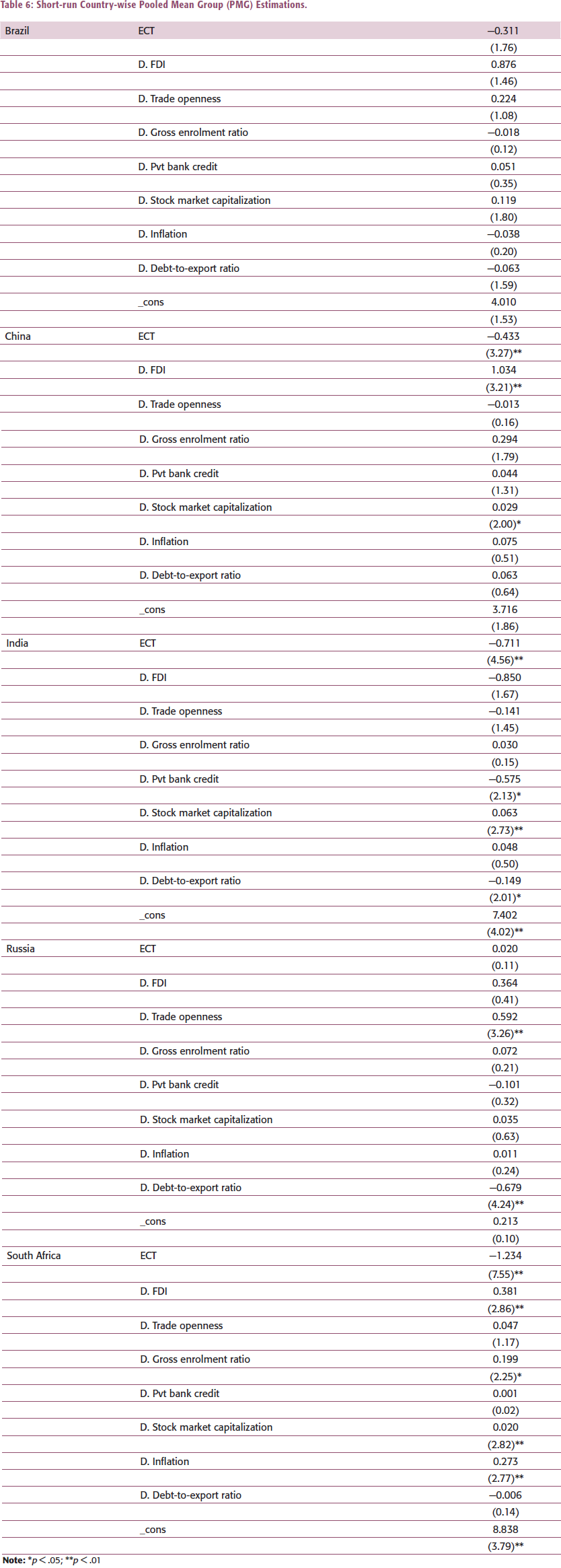

Importantly, one of the assumptions of the PMG model is that unlike long-run coefficients, short-run coefficients and ECT are not homogenous for all the countries or cross-sections in the panel. In this regard, the short run results and ECT for each country in the BRICS group derived from the PMG estimator are reported in Table 6. The select macroeconomic variables have no significant short-run impact on GDPG in the case of Brazil, and the ECT is also not significant.

Short-run Country-wise Pooled Mean Group (PMG) Estimations.

The short-run coefficients for China indicate that FDI (1.034) positively impacts GDPG, and the ECT shows a long-run cointegration among the variables, meaning that any deviation from long-run equilibrium is corrected at −0.433 adjustment speed. Moreover, the results also reveal that except financial development, in terms of SMC (0.029), no other macroeconomic variable has a short-run statistically significant impact on GDPG for China.

The ECT for India shows a long-run cointegration between FDI, GDPG and other macroeconomic variables (host country characteristics), meaning that any deviation from long-run equilibrium is corrected at −0.711 adjustment speed. Moreover, the results also reveal that PBCR (−0.575), SMC (0.063) and DTE ratio (−0.149) have short-run statistically significant impact on GDPG of India.

The ECT for Russia reveals no long-run cointegration between the dependent and explanatory variables. Moreover, the results also indicate that except for TO (0.592) and DTE ratio (−0.679), no other macroeconomic variable has a short-run statistically significant impact on the growth of Russia.

The ECT (−1.234) for South Africa shows a long-run cointegration among the variables. FDI (0.381) exerts a positive short-run impact on the growth of South Africa. Moreover, human capital (0.199), SMC (0.020) and INF (0.273) also exert a significant positive short-run impact on the growth (GDPG) of the country.

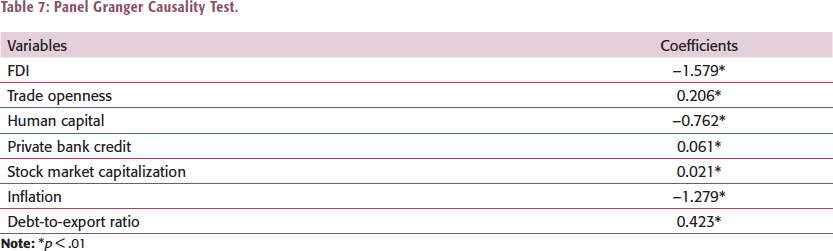

The results of the panel Granger causality test (Table 7) reveal that FDI, human capital and INF negatively Granger-cause economic growth in BRICS. Moreover, the remaining select host country characteristics positively Granger-cause GDPG in BRICS countries.

Panel Granger Causality Test.

CONCLUSION

The present study examines the FDI–growth nexus over the period 1997–2018. The study uses the panel ARDL model and focuses on the BRICS economies with tremendous potential for FDI attraction. The findings revealed a long-run cointegration among FDI, host country characteristics (TO, human capital, financial development and macroeconomic stability) and economic growth in BRICS. The results suggest that FDI inflows, INF, human capital and SMC have a significant long-run negative impact on the economic growth of the BRICS bloc. In contrast, TO has a positive long-run impact on growth. Granger causality test revealed that FDI, human capital and economic instability proxied by INF negatively Granger-cause economic growth in BRICS, whereas the remaining select host country characteristics positively Granger-cause GDPG in BRICS countries. The negative impact of FDI on growth supports Solow’s proposition that FDI-induced growth may not continue in the long run due to diminishing returns to capital and that FDI may promote growth in the short run (Solow, 1956), as could be seen from our country-wise short-run results in the case of China and South Africa. INF exerts a negative long-run impact on growth, indicating that macroeconomic instability is detrimental to growth in the long run. Although the impact of SMC is negative, the magnitude of the coefficient (−0.009) is small enough to ignore its impact. However, the negative long-run impact of human capital on growth could be attributed to the heterogeneity in the cross-sections (i.e., the BRICS countries), as extended by Pelinescu (2015) in his study. The heterogeneous short run country-wise revealed that FDI has a positive impact on growth in the case of China and South Africa. Financial development proxied by SMC has a positive impact on the growth of China, India and South Africa in the short run. Human capital and INF have a positive short-run impact on the growth of South Africa. Macroeconomic instability proxied by DTE ratio has a short-run negative impact on the growth of India and Russia, whereas TO has a positive impact on the growth of Russia.

Based on the results, it is suggested that policymakers focus on trade liberalization measures and development of financial markets for better growth outcomes. Also, the policymakers of the BRICS group should maintain the macroeconomic stability given the negative growth impact of INF found in the study. Moreover, research reveals that FDI results in a negative growth impact in countries with low levels of human capital (Borensztein et al., 1998). This raises doubts about the sufficiency of human capital development in the case of BRICS owing to the negative long-run coefficient of FDI. Therefore, policymakers should look into the sufficiency of human capital followed by appropriate policy intervention for sustained human capital development in BRICS. Based on the country-wise short-run results, it is suggested that policymakers of China and South Africa attract more inward FDI and focus on financial development to promote growth. India should focus on the development of financial markets, given its positive growth impact and maintain the economic stability in the country. Based on the findings in the case of Russia, policymakers should focus more on trade liberalization and maintenance of economic stability for sustained economic growth.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

e-mail:

e-mail: