Abstract

As he checked his mid-priced smartphone on a humid Wednesday morning, Vivek was excited to see a mail from HDFC Life. Perhaps, his ordeal with the term insurance policy was finally over. The relief soon turned into rumination as he saw another puzzling turn to an episode that began around three weeks ago. While this was just another chapter in a continuing saga of consumption dissatisfaction and complaining experiences across various products and services, he was rattled by its sheer perplexity. Perhaps, it happened rarely to others, or, maybe, many people lumped discontent. Though Vivek had learned to moderate his expectations across social contexts, he could not avoid viewing each interaction from the lens of justice. No wonder even his family had termed him a chronic complainer. His thoughts came back to the beginning of this troubling experience. He could have saved a lot of time, and agony, had he simply paid the undue penalty, a pittance, relative to his fortunate state of financials.

At the heart of this episode was this term insurance policy Vivek bought in 2010. Having married Sumedha in 2007 and been blessed with their daughter Akanksha in 2008, he had been contemplating insuring his life for some time. Concurring with expert advice against mixing investment and protection goals, Vivek settled for a modest term cover assuring 16 lakhs, to Sumedha, in the event of his untimely death. Having been a customer of HDFC bank for the last 10 years and being satisfied with their services and, more importantly, with the way his feedback and complaints were attended to, Vivek opted for HDFC Standard Life. Though he was aware that these were two different corporate organizations, Vivek still perceived a common parentage and similar operating philosophy.

Though it was a good 10 years since purchasing this cover, this was the first time Vivek had needed to contact HDFC Standard Life. He paid all his premiums online and on time. It was only when he started this interaction that Vivek came to know that HDFC Standard Life was now HDFC Life. He took this delayed awareness as a metaphor for the relative comfort of a relationship that had now taken a beating. However hard he tried, Vivek could not stop himself from repenting at his decade-old decision of trusting HDFC Life.

THE MACRO-REALITY

Over the past two decades, Vivek had seen a transformation of the Indian market across industries. Though he was somewhat aware of the timeline of economic liberalization in the country (Panagariya, 2004), he could consciously link the changes only up to his minimal maturity as a consumer. From household needs to lifestyle luxuries, Vivek found a near-explosion of choice. In many ways, he felt the oft-repeated adage that the consumer is the king was truly being realized. Beyond his experience, Vivek’s thoughts were accentuated by the popular sentiment reflected across mass media. He read regular claims about the positive influence of competition and technology on consumer options, quality, and customer service (Manish, 2013; Sharma, 2015).

Hitherto enmeshed in this general sense of market optimism, Vivek had found himself regularly troubled by consumption experiences, which negated customer-centricity tenets. Though he accepted the doctrine of fallibility, Vivek also believed in the need to rectify mistakes. However, over the years, he had felt the pain of unheard grievances and hostile firms. Vivek sought the relatively rare opinions and articles that presented such situations, in an effort to reduce his dissonance. He remembered one such reading, wherein evidence of increased dissatisfaction and consumer problems over 40 years was presented (Grainer et al., 2014). This study also reported a miserable 21% resolution rate at the first complaint and the grim reality that four or more complaints were typically needed. Another study by Accenture revealed that 88% of the Indian consumers switch due to service failures, against a global churn rate of 64% (Saha, 2016).

Official figures, too, indicated the inability of current regulatory mechanisms in handling the rising caseload (Dubbudu, 2016). However, complaint statistics across different consumer protection agencies complicated Vivek’s confusion (Exhibit 1). Did he experience anomalies, or was it the real state of affairs in general? The question of whether consumers’ life had improved or deteriorated at a macro level seemed to be a tough riddle. The biggest undeserving sufferers of this paradox were consumers like him, who sacrificed their time for obtaining just resolution(s).

INDIAN LIFE INSURANCE INDUSTRY

The insurance sector in India has seen an extensive transformation with liberalization and foreign investment amid the Insurance Regulatory and Development Authority (IRDA) Act of 1999 (IRDAI, 2007). From an industry restricted to public ownership and control, it has evolved to have a total of 70 insurers; 27 general, 24 life, 7 stand-alone health, and 12 re-insurers, as of March 2019 (IRDAI, 2019a).

Further, the life insurance segment dominates the overall sector, contributing 73.85% to the premium realizations in 2018–2019, against a global share of 54.3% (IRDAI, 2019a). A key distinction prevalent in the industry throughout its existence has been private or public incorporation. Life Insurance Corporation (LIC) of India, hitherto the only life-insurance provider from 1956 till 2000, is the sole public player, as the Government of India owns the majority stake. On the other hand, 23 firms exist with private ownership, with permission of up to 49% foreign stake, raised from 26% in 2014 (PTI, 2014). Despite significant competition posed by private players, LIC has managed to chalk out an impressive performance over the years and clocked a market share of 66.42% in 2018–2019 (Exhibit 2).

Some Indicators of the Indian Life Insurance Industry.

2. Market shares as per total premium collection to reflect core industry position.

3. Changes in competitive position are indicated in bold.

4. ICICI: ICICI Prudential Life Insurance Company Ltd., HDFC: HDFC Life Insurance Company

Ltd., BSLI: Birla Sun Life Insurance Company Ltd., SBI: SBI Life Insurance Company Ltd., Bajaj:

Bajaj Allianz Life Insurance Company Ltd.

5. Penetration denotes the ratio of insurance premium to GDP.

6. Claim settlement ratios were not reported in the initial years.

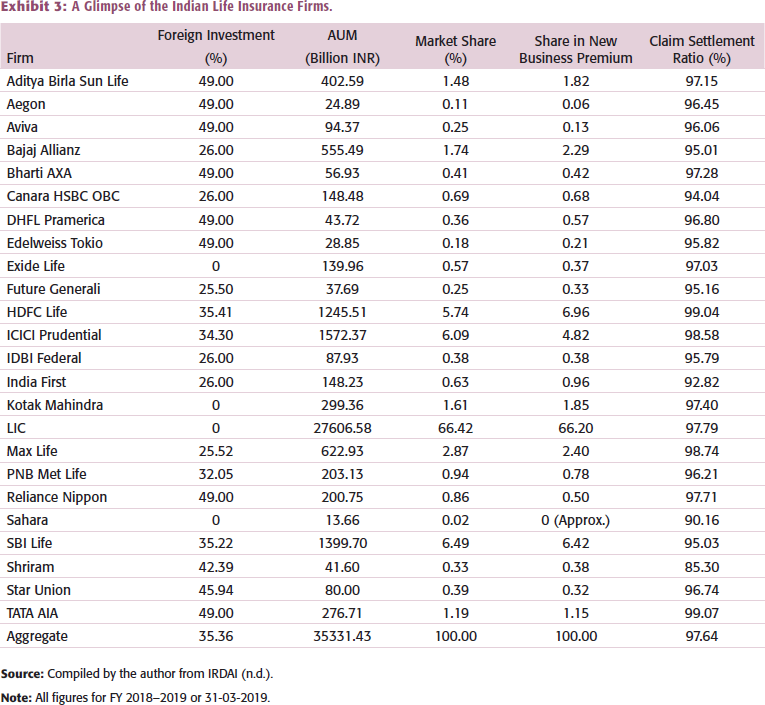

On the other hand, private life insurance players present a mixed bag of achievements and unmet expectations. Many of these firms have been instrumental in introducing innovations, implementing new sales channels, and making insurance cost-effective with aggressive pricing. However, they have not been able to earn the trust of the Indian populace to the extent commensurate with their potential (Coverfox, n.d.b). On a healthier note, their market share, claim settlement ratio, and new business premium have improved over the past few years (Exhibit 3). On the financial front, too, a majority, that is, 20 of them were profitable in 2018–2019 (Coverfox, n.d.b).

A Glimpse of the Indian Life Insurance Firms.

At a macro level, a relative disappointment of the regulatory regime has been the fall in insurance penetration since 2009, when it attained its peak (Exhibit 2). Benchmarking with developed and other emerging economies, penetration rates of various insurance sectors are among the lowest (Aegon Life, 2019). While it raises doubts about the efficacy of policy interventions, it also suggests untapped growth opportunities.

From the perspective of potential dissatisfactory episodes, a multi-tiered system has been put in place to address consumer complaints. Accordingly, insurers are mandated to provide an internal grievance redressal mechanism that operates on an escalation principle, sequentially to higher management levels within the organization (IRDAI, 2017a). Further, the Integrated Grievance Management System (IGMS) has been set up by IRDAI, which allows for complaints to be raised online to the regulator. Alternatively, IRDAI can be approached via other channels such as telephone, post, or email (IRDAI, 2019b). The system is transparently mirrored with the internal network of each insurer. It allows for complainants to check the status of grievances and reopen dockets unsatisfactorily resolved by the insurers.

Further, complainants dissatisfied with the remedy provided by the internal insurer mechanism or the IGMS (IRDAI) can approach the Insurance Ombudsman, who can pass awards binding on the insurers (IRDAI, 2017b). Finally, consumer complainants can take recourse to legal remedies.

HDFC LIFE

HDFC Standard Life Insurance Company Limited enjoys the distinction of being the first private sector life insurer, having entered the industry with three other players; the same year, it was opened to private participation (IRDAI, n.d.). Established as a joint venture between Housing Development Finance Corporation Limited (HDFC) and Standard Life Aberdeen PLC, a global investment firm headquartered in Scotland, HDFC Standard Life has been instrumental in transforming the sector through offering the consumers a comprehensive range of options, provisioning an extensive selling network (Coverfox, n.d.a), and by implementing various process innovations (Jha, 2018). The name of the company was changed to HDFC Life Insurance Company Limited, w.e.f. 17 January 2019 (HDFC Life, 2019). With assets under management of approximately ₹1,250 billion, HDFC Life holds a 5.74% market share in total life insurance premium as of the end of 2018–2019. In this respect, it trails only ICICI Prudential Life Insurance Company Ltd and SBI Life Insurance Company Ltd in the private space (Exhibit 3). Viewing claim handling as a key barometer of customer service and an advertising plank (HDFC Life, n.d.a), HDFC Life has reported a second best claim settlement rate of 99.04% for individual death claims during 2018–2019, surpassing all the bigger players like LIC, SBI Life, and ICICI Prudential Life.

With an intent to provide excellent customer service, as also to abide by the regulations, HDFC Life has put in place an extensive feedback, complaint, and grievance redressal mechanism. A simplistic view of the relevant roles and their linkages underlying the internal structure is depicted in Exhibit 4 (Panel A). This representation excludes several cross-functional connections in the form of committees, for example, grievance redressal committee (Exhibit 5). This committee exists at the corporate level and is part of a broader wing named Service Recovery (HDFC Life, n.d.b). Several touchpoints exist for customers, both as regards general policy servicing and for reporting complaints (Exhibit 4, Panel B). Specifically, under the grievance handling mechanism also, customers can approach physically through branches, via email at

VIVEK’S ORDEAL

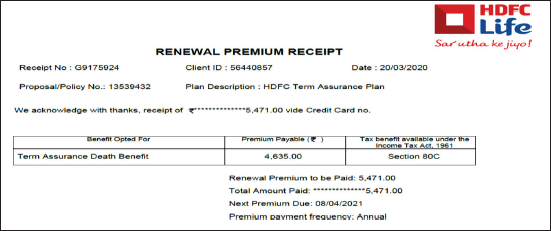

It was 19 March 2020, when Vivek was reminded of the approaching due date of premium payment for his term cover by his smartphone reminder. He paid the premium in advance, as every year, directly on the HDFC Life website without using any intermediary platforms. He immediately received a mail acknowledging the payment. Two days later, he received the formal premium payment receipt (Exhibit 6). To Vivek, it marked the end of his obligation till the next year.

Formal Premium Payment Receipt Mail.

Naturally, he was taken aback when, on Wednesday, 15 July 2020, he received a call from an HDFC Life executive requesting him to pay the premium, now overdue. Vivek nevertheless took it as an overzealous attempt to pursue premium payments. He informed about having paid sometime in March and requested the executive to verify from the system. She cited an inability to do the same instantly and promised to revert the next day.

On Friday, though Vivek did not receive the committed call, he thought of checking the ‘My Account’ section on the HDFC Life website, just for reassurance. As he logged in, he was astonished to see his policy’s status mentioned as Contract Lapsed since 08/04/2020, the due date of his premium. This was despite the recognition of the payment transaction made on 19 March 2020 in the payment history link. Unable to understand this contradiction, he decided to check his account through which the payment was made. Though it duly showed a debit of the premium amount on 19 March 2020, it also showed a credit entry of the same amount on 16 April 2020 (Exhibit 7).

Partial Bank Statement.

The bank statement had confused him further. Vivek had neither requested for any refund of premium nor received any communication regarding the same from HDFC Life. Even otherwise, do the insurers’ refund premiums, even if asked? Further, his cover was lying suspended for about three months, without notice to him. Vivek thought of the various ramifications this unilateral action could have caused. What could have been the legal validity of the claim had it, unfortunately, needed to be raised? He was afraid that HDFC Life would have simply rejected such a claim, and his family could perhaps have been able to do nothing. Though these questions were hypothetical, Vivek could not avoid thinking about them.

Vivek decided to write to the insurer. Though email to the service team was expected as the first stage of representation, he marked the correspondence additionally to the grievance redressal officer (Exhibit 8). Further, given the sufficiency of the time already elapsed and the criticality of the issue as perceived by him, Vivek complained with the IRDAI vide IGMS (Exhibit 9).

Vivek’s Correspondence Dated 17 July 2020.

Vivek’s Complaint Docket Dated 17 July 2020, to IGMS IRDAI.

An auto-reply the next day gave him a reference number, ‘HDFCSL=006-664-956’ for the issue. On Sunday, he received another email (Exhibit 10). Vivek was offered an apology and requested for a few days to resolve the concern. Surprisingly, this communication gave the issue a different reference number, ‘HDFCSL=006-664-910’.

Reply from HDFC Life Dated 19 July 2020

Week 2

On Tuesday, he received another email (Exhibit 11). For the first time, a commitment was given to share an online payment link without extra charges. There was no mention of why the premium was refunded or even if it was refunded at all. Things seemed to be on the right track when he received the committed payment link on Thursday. The correspondence (Exhibit 12) explicitly mentioned that the late charges were waived off.

Reply by HDFC Life Dated 21 July 2020.

The Mail with the Payment Link Received from HDFC Life Dated 23 July 2020.

Vivek went on to pay through the received link. However, against the commitment, the payment link demanded ₹5,592 instead of the actual premium amount of ₹5,471. Though Vivek felt angry, he decided against further escalation. While he wrote back (Exhibit 13), Vivek received a telephonic call from the same executive who called on July 15 and was instrumental in beginning this episode. Whereas her call came a good seven days later than commitment, Vivek still expected to hear something about the ongoing correspondence. Instead, she repeated the same request of premium payment, citing it as long overdue. Though Vivek got frustrated momentarily, he realized that she was just a cog in the wheel. Accordingly, he reminded her of the commitment of reverting with details, the other time they had talked. She had expectedly forgotten everything and instead asked Vivek to drop a mail to customer service. Sensing that both could realize nothing from the interaction, they disconnected the call.

Vivek’s Reply Against the Received Payment Link, Dated 23 July 2020.

Repeated lapses by the insurer prompted him to escalate the issue further. Since Vivek already had an open grievance with IRDAI for around a week, he visited the Centralized Public Grievance Redress and Monitoring System (CPGRAMS) of the Department of Administrative Reforms & Public Grievances (CPGRAMS, n.d.), Govt. of India, and logged his complaint against the insurer (Exhibit 14). Things took a further reversal on Friday when a mail from HDFC Life (Exhibit 15) declared that online payment would be with late charges only. It further belied the earlier commitment made multiple times. Vivek was thoroughly annoyed now and sent a strongly worded reply (Exhibit 16).

Complaint Booked by Vivek on CPGRAMS Portal, Government of India.

Reply from HDFC Life Dated 24 July 2020

Vivek’s Mail Dated 24 July 2020.

Week 3

After an uneventful weekend, Vivek received another mail on Monday, 27 July (Exhibit 17). Though it again quoted a new reference number (the third in aggregate, so far), it at least acknowledged that payment was refunded due to technical error. HDFC Life had taken 10 days since his initial request and more than 4 months since the actual payment for this realization. Further, the issue of the surcharge for repayment was ignored. Vivek felt betrayed as all the 10 days of several interactions stood disregarded. The same message communicated to him was also used as proof of having provided the resolution, and his complaints at IGMS (IRDAI) and CPGRAMS were closed. Though there was no actual or even partial resolution, Vivek could not find any effort to check the resolution claim’s veracity.

Reply of HDFC Life Dated 27 July 2020 (Used for Closing the IGMS Docket).

Having no alternative, he wrote again to HDFC Life (Exhibit 18), this time to escalation1@hdfclife.com, as per the sequence recommended by HDFC Life’s internal grievance mechanism. Further, Vivek reopened and escalated the IGMS docket no. 07-20-008196 and raised a fresh CPGRAMS complaint (docket no. DEAID/E/2020/04586) since the system did not give any option of reopening a closed docket. Further, he provided detailed feedback to CPGRAMS for the wrongly closed docket. At this stage, he found an issue with the whole system. Somehow his grievance had transcended the insurer. IRDAI had acted merely as a postman between him and the insurer, ignoring the merit of the claimed resolution(s). Let alone the substantive issues, even the procedural requirements like conveyance of ombudsman information were not met in the reply. While Vivek strongly believed that he was wronged, he had only asked for the opportunity to pay the original premium and his right of immediate policy revival. He wondered how his request could be considered unjustified.

Vivek’s Mail Dated 27 July 2020.

His ongoing encounter took a truly material turn on Thursday when he received two emails from HDFC Life. Whereas the first one (see Exhibit 19) informed that work was in progress and sought additional time, the second email (see Exhibit 20) claimed to have already resolved the issue once again. The second correspondence gave Vivek a strict timeline of 48 hours to pay again through an online link, which surprisingly was nowhere to be seen. Further, HDFC Life used this correspondence as a resolution to close the IGMS escalated complaint and the CPGRAMS second complaint DEAID/E/2020/04586. When the premium payment link was still not available, payment had yet not been made again, and the policy was still in an unauthorizedly lapsed state for no fault of his, Vivek wondered, whether and how could this be claimed as a resolution?

First Reply Email of HDFC Life Dated 30 July 2020.

Second Reply Email of HDFC Life Dated 30 July 2020 (This Message Also Used as Proof for Closing the Escalated Docket at IRDAI IGMS and the Second CPGRAMS Complaint).

In the absence of the promised payment link and with the 48-hour deadline looming on him, Vivek had no option but to write back (Exhibit 21). He presented another request against successive false closures at IGMS IRDAI, vide docket no. 07-20-014772, as the system did not allow a second reopening or escalation. Similarly, he raised the third complaint at CPGRAMS vide docket no. DEAID/E/2020/04657. Later in the evening, he received another mail (Exhibit 22), requesting him to wait for up to a day for the payment link. Vivek could not understand the hurry of inappropriately closing the complaint when the payment link needed time to be shared. At the insurer’s end, no one seemed to be bothered about the arbitrary change of his policy status to contract lapsed state. Later in the night, Vivek received a payment link via SMS on the registered mobile number. Finally, finding the demanded amount to be without surcharge, he paid within 15 minutes and decided to send a payment intimation mail (Exhibit 23). Specifically, his point was the revival of the policy from the undeserved lapsed status on priority. He had already had enough of this.

Vivek’s Mail Dated 30 July 2020, Against the Non-availability of Payment Link.

Reply of HDFC Life Dated 30 July 2020, Advising to Wait for the Payment Link.

Vivek’s Mail Dated 30 July 2020, Intimating the Payment of Premium.

On Friday, Vivek received another mail (Exhibit 24) confirming premium receipt and committing a timely revival. Finally, he felt that his troubles might finally be over. However, his expectations were again belied on Sunday. Instead of getting the policy revival update, he was asked for personal health statement(s) as a pre-condition for policy revival (Exhibit 25). Further, this correspondence again quoted a new reference number for his continued grievance (fourth so far). Though Vivek had nothing to hide regarding his health particulars, he found the instruction hegemonic, unethical, and unprofessional. Had this information been sought from all policyholders or only for lapsed policies? Even if it was done for lapsed policies only, should it be asked from him, given the peculiar circumstances of his case, when HDFC Life itself wrongly refunded the paid premium? Third, even if this additional requirement was deemed relevant in his case, was it ethical to have raised the demand after receiving the payment? Though Vivek was tired of this ordeal, he again mustered the will to write back (Exhibit 26).

Reply Email of HDFC Life Dated 31 July 2020, Confirming Receipt of Premium.

An Email of HDFC Life Dated 2 August 2020, Seeking Additional Requirements.

Vivek’s Mail Dated 2 August 2020, Objecting to the Fresh Set of Requirements.

Week 4

Vivek received further correspondence on Monday (Exhibit 27), asking for a deposit of ₹121 as balance payment to revive the policy. He had already received an SMS to this effect on Saturday and had checked his account section on the website, wherein a service request number 1-46850253278 existed to this effect. This action countered HDFC Life’s claim of waiving this penal amount as a service gesture (Exhibit 20). However, his ability to get surprised was now profoundly inhibited, having seen so much over the past few days. Vivek decided against writing further, since he had already objected to this service request in his mail sent on Sunday.

An Email from HDFC Life Dated 3 August 2020, Seeking Additional Payment.

On Wednesday, Vivek was requested to ignore the messages demanding interest (Exhibit 28). There was no mention of the requirement of forms and documents raised on Sunday. Even in raising late fee/interest charges, Vivek failed to understand why could not the system recognize the need not to send these messages? If he was to ignore some messages, how could he get to know which ones to accede to and which ones to ignore? The next day, Vivek received a telephonic call from the service recovery team, informing that the policy has finally been revived, and a mail to this effect has also been sent to him (Exhibit 29). HDFC Life used this mail as evidence for closing the second IGMS complaint (docket no. 07-20-014772). As he logged onto the HDFC Life website, hoping to see a corrected picture, he still found his policy to be contract lapsed. Further, the system still displayed a pending service request demanding the late fee/interest. He clicked the snapshots of the ‘My Account’ section and wrote back (Exhibit 30). Unsurprisingly, he again received a reply (Exhibit 31), requesting him to wait for one day for the changes to take effect. He could not fathom their urgency of making repeated claims of resolution when things were almost always still in process.

An Email from HDFC Life Dated 5 August 2020, Requesting Vivek to Ignore Their Messages.

An Email from HDFC Life Dated 6 August 2020, Confirming Resolution.

Vivek’s Email Dated 6 August 2020.

An Email from HDFC Life Dated 6 August 2020, Asking for Further Time.

The next day, he could check that his policy status had been updated. His persistent fight for a fair resolution had achieved finality. Nevertheless, he was not happy. His thoughts wandered to whether the result was fair at all. Did the underlying issue justify the kind of effort he had to put in? Was it a matter of only the monetary penalty of ₹121? Can a system that provides a resolution only after transcending triviality to the level of unimaginable complexity be termed as fair? Is it an intended strategy of the mighty to digress the attention of the weak from key issues?

The more Vivek thought, the more convinced he became that the battle was still not won. Throughout this tale, he was troubled more by the way his issue was handled and much lesser by the initial technical failure. His concern was that HDFC Life could still not learn anything from this episode. If that is the case, many like him will face preventable inconvenience again. He resolved to make a detailed representation to HDFC Life, presenting the complete chronology of the dispute. Further, he decided to raise a demand for compensation as a strong message to the insurer. Vivek was moving into personally unchartered territory and had little hope of a positive outcome from the insurer. While having such apprehensions, Vivek simultaneously thought of his choices in the event of no response. He remembered Mahatma Gandhi’s words, ‘Be the change that you wish to see in the world.’ While he thought of this imperative of initiative, many forces were holding him back. Having crossed a river, he was staring at a vast expanse that could very well be an ocean.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship, and/or publication of this article.

e-mail:

e-mail: