Abstract

The finance literature has analysed several aspects of the IPO market, namely, hot issue market, initial under-pricing, and long-run underperformance. Among them, findings of long-run underperformance are particularly significant as it indicates that investors incur losses on a perpetual basis by investing in a portfolio of IPO firms. According to the OECD (2019), during 2009–2019, the number of IPO issuances by non-financial firms in India were the third-highest globally. In the case of India, only a few studies have investigated the long-run performance of IPO firms. Accordingly, the present study fills a void in this arena. The study, along with the conventional event study techniques, deploys the Fama-French Five-Factor model for analysis of long-run underperformance. The study estimates investment and profitbility factors for India following the methodology illustrated by Fama-French (2015). The study finds that long-run underperformance by the IPO firms is not absolute but specific to the sample and methodology used for analysis. It also finds that underperformance is prevalent in high IPO volume years. The regression results for IPO firms as portfolios in the capital asset pricing framework do not show any long-run underperformance. This finding supports the conclusion that the long-run underperformance by IPOs reported in the previous studies results suffers from sample and methodology bias. The analyses in the five-factor framework show the plausibility of higher investment by IPO firms resulting in lower market return. IPO firms make above-industry-average capital expenditure, and their profitability converges with the industry after issue.

Keywords

Financial anomalies are empirical findings that prove that several market outcomes are inconsistent with asset pricing theories (Schwert, 2003). They indicate the presence of profit-making opportunities through arbitrage, implying the existence of market inefficiencies. The finance literature has analysed several aspects of the IPO market, namely, hot issue market, initial under-pricing, and long-run underperformance (Brav et al., 2000; Gompers & Lerner, 2003; Helwege & Liang, 2004; Loughran & Ritter, 1995; Lyandres et al., 2008; Pástor & Veronesi, 2005; Ritter, 1991). Among them, findings of long-run underperformance are particularly significant as it indicates that investors incur losses on a perpetual basis by investing in a portfolio of IPO firms.

Contrary to the animated academic debate on the anomalous behaviour of the IPOs, these are vital instruments for mobilizing risk capital for firms, enhancing liquidity for the promoters, and providing an exit route for large investors. India has a large IPO market. According to the OECD (2019), during 2009–2019, the number of IPO issuances by non-financial firms in India were the third-highest globally after the Peoples’s Republic of China and the United States of America. Therefore, various facets of the IPO market need to be analysed from time to time. In the case of India, a limited number of studies have investigated the long-run performance of IPO firms (Kohli, 2009; Sahoo & Rajib, 2010). However, these studies have primarily used a firm-specific event study framework; therefore, they do not control market-wide systematic risk 1 . Hence, existing studies on India do not test for asset pricing models and market efficiency hypotheses. Therefore, existing IPO literature has a void, which this study attempts to fill. For this, along with the conventional event study techniques, we deploy the Fama-French Five-Factor model.

The present study has two primary goals: a) to test the long-run market performance of an average Indian IPO firm vis-à-vis benchmark indices of the Indian stock market following event study methods and the capital asset pricing models, and b) to examine the possible impact of higher investment and lower profitability on the post-issue performance of IPO firms. Therefore, the present study examines the performance of an investment in a portfolio of IPOs as a long-term investment strategy and the efficiency of price discovery in India.

Our univariate analysis finds that a median IPO firm gives lower returns vis-à-vis benchmark indices in the long run. However, we also find that this underperformance is not absolute but specific to the sample and methodology used for analysis. We find that underperformance is in high IPO volume years. Our regression results for IPO firms as portfolios in the capital asset pricing framework do not show any long-run underperformance. This finding supports our conclusion that the long-run underperformance by IPOs reported in the previous studies results from sample and methodology bias. Our analyses in the five-factor framework show the plausibility of higher investment by IPO firms results in lower market return. IPO firms make above-industry-average capital expenditure, and their profitability converges with the industry after issue (Shukla & Shaw, 2018). Therefore, the market penalizes firms for underachieving pre-issue operational performance. Accordingly, we infer that while making a generalized conclusion about IPO firms as a class of financial market anomaly, one needs to be careful.

The present study makes three key contributions to the extant literature: (a) despite India’s thriving IPO market, studies related to India and emerging markets are limited; thus, this study provides new insights into the context of emerging markets; (b) the Indian capital market has witnessed a spate of regulatory changes, analysis of IPOs in this study provides an empirical test about the performance of an essential segment of the Indian capital market; and (c) furthermore, to the best of our knowledge, this is the first study to employ the Fama-French five-factor model—augmented by investment and profitability factors derived using accounting data—for the long-run market performance of IPOs in India. Therefore, this study offers new insights into empirical literature.

The study has been divided into seven sections. The next section covers key reforms carried out in the Indian capital market after 1990. It also briefly outlines the importance of the Indian IPO market in the global equity market. We then cover theoretical underpinnings and the literature survey and outline data sources and research methodology. The subsequent section discusses descriptive statistics. We then outline the post-issue long-run market performance following the event study framework. The long-run performance using various asset pricing models is analysed. Finally, the last section concludes the study.

IMPORTANCE OF THE INDIAN IPO MARKET IN THE GLOBAL IPO MARKET

The year 1990 is known as a point of inflexion in the economic history of India (Acharya, 2019; Tyagi, 2017). The economic reforms assigned greater responsibility to the market-based financial system to allocate productive resources efficiently. The most crucial reform measure undertaken in the early 1990s was repealing the Capital Issues (Control) Act 1947, which paved the way for market-determined pricing of primary capital issues. Over the years, policymakers took several measures to strengthen equity market infrastructure, replacing the open outcry system with screen-based online order-matching trading platforms; strengthening the settlement system with the establishment of depositories; shortening the settlement cycle and introduction of electronic funds transfer facilities.

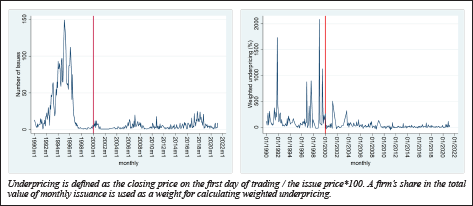

The reforms in the Indian capital market have not followed a linear path. Regulators and policymakers have had their fair share of learning and redesigning. For example, during the initial years of primary capital market liberalization, that is, 1990–1996, the IPO market witnessed a large volume of equity issuances by firms with weaker fundamentals or ‘fly-by-night’ entrepreneurs (Agarwalla et al., 2013). This led to several new reforms in the late 1990s and early 2000s, namely, financial data reporting norms, guidelines for pricing the issue, the lock-in period, and vetting of draft red herring prospectus by the market regulator. Additionally, introducing the book-building process for IPOs in 1999 brought further maturity in the primary equity market. Reforms carried out after 1996–2000 brought maturity in the Indian capital market and instilled a distinct structural break in the functioning of the IPO market after the year 2000. Marisetty and Subrahmanyam (2010) divided the journey of reforms in the Indian market from 1990 into three distinct phases: (a) the immediate post-liberalization regime (1990–1995); (b) the initial regulated regime (1996–2000); and (c) the reformed regulated regime (post-2001). After these reforms, the Indian market recorded a lower volume of IPOs and a decline in initial under pricing (Figure 1). Thereby, anomalies of the hot issue market and initial under pricing were resolved significantly.

According to Ernst and Young (2018) and the OECD, the Indian IPO market is one of the fastest-growing markets globally. The institutional ownership of the listed firms in India is only marginally behind those in Japan and Chinese Taipei (OECD, 2017, 2018). Equity investment by foreign institutional investors has been consistently rising in the Indian equity market. Their participation is expected to rise further in the medium to longer term. However, relative to the USA and other advanced economies, the Indian market is still characterized by weak legal institutions, higher information asymmetry, weaker market discipline, and poor corporate governance. We believe that structural reforms and the rapidly growing size of the capital market are two critical aspects of why the Indian IPO market needs to be studied separately from advanced economies.

THEORETICAL UNDERPINNINGS AND SURVEY OF LITERATURE

The Empirical Literature on Long-run Underperformance by IPOs

The empirical literature on IPOs is primarily on the United States of America’s experience, where, commonly, IPO firms underperform vis-à-vis already listed firms. Ritter (1991) found that in the long run, IPO firms significantly underperform vis-à-vis a set of companies matched by size and industry. The underperformance is among younger growth firms. He concludes that this phenomenon is more consistent with a scenario of firms going public when investors are irrationally over-optimistic about the future potential of specific industries (Shiller, 1990) and termed it as a ‘fad’ explanation. Loughran and Ritter (1995) revisited IPO market performance and the performance of seasoned equity firms. They found that IPO and seasoned equity firms give lower returns than market benchmarks and matched firms. The low returns of these firms are only partially explained by the book-to-market ratio of firms.

However, using Fama and French’s Three-Factor model (1993), Brav and Gompers (1997) found that IPO firm’s long-run underperformance is concentrated only in non-venture-backed small-sized high valuation firms. Furthermore, they stated that underperformance is not unique to IPO firms; instead, all low book-to-market ratio firms underperform. According to them, in the smaller firms, predominantly individual investors hold equity, and cannot devote adequate resources on analysis; therefore, there is a high degree of information asymmetry. Interestingly, they find that institutional investors are not hurt significantly by the underperformance of this type of IPOs. Brav et al. (2000) and Gompers and Lerner (2003) also reached a similar conclusion of no definite evidence of underperformance with different samples and time horizons.

Researchers in other countries have tried to reproduce the results of the US studies. Levis (1993) and Gregory et al. (2010) tested abnormal returns by IPO firms in the United Kingdom. They generally accept the conclusions of Ritter (1991). Lee et al. (1996) studied IPO firms in Singapore. After adjusting for risk and size, they found that the initial return of IPO firms is not significantly different from standard market return and long-run average returns are insignificantly different from an efficient market expectation. Thomadakis et al. (2012), in a study relating to the long-term performance of Greek IPOs, found long-run over-performance. Zarafat and Vejzagic (2014) find that Malaysian IPO firms underperform in the long run; however, underperformance is not statistically significant. Hence, the cross-country literature does not support uni-directional long-run underperformance by the IPOs.

The Long-run Performance of Initial Public Offerings in India

Despite a vibrant IPO market, we do not find many studies analysing the long-run performance of IPOs in India. The existing studies also have used smaller time windows and sector-specific samples for the analysis. Besides, the Indian studies have mainly relied on the financial anomalies argument for analysing long-run performance. Generally, these studies have calculated long-run performance relative to a benchmark and broader market indices using buy-and-hold abnormal return, cumulative abnormal return, and wealth relatives. Except for Ghosh (2007), who uses the capital asset pricing model and the Fama-French Three-Factor model to examine the cross-sectional return of IPO firms, other authors use firm-specific attributes to explain the market underperformance of IPOs. For example, Sahoo and Rajib (2010) found that IPO firms have pronounced underperformance in the first year of listing (i.e., initial 12 months) followed by outperformance in the subsequent years. However, this study covers a short period, therefore, suffers from a sample bias. Moreover, in the initial period of their research, the IPO market was recording an uptrend; the broader equity market attained a peak after the terminal year of the study; thus, their results are not unbiased.

Ghosh (2005) finds that commercial banks’ IPOs do not underperform in the long run as sectoral regulation eliminates any window dressing before issue. However, his analysis pertains to commercial banks only; therefore, it cannot be generalized. Marisetty and Subrahmanyam (2008) analyse the impact of ownership on post-issue performance. They do not find any meaningful difference in the performance of issue firms emanating due to differential ownership of firms. Kohli (2009) concludes that since IPO firms underperform vis-à-vis benchmarks, the capital market makes an inefficient allocation of resources compared with the banking system in India. Indian studies have concluded multiple firm-specific factors, namely, firm size, issue size, initial return, market conditions, and so on, as possible explanations for relative market underperformance. Hence, these studies do not attempt to systematically analyse this problem. Though Ghosh (2007) uses a capital asset pricing framework to analyse IPO firms’ performance, a problem with that study is that it only analyses cross-sectional return. Therefore, none of the Indian studies analyse long-run IPO performance as an investible portfolio. In real life, investors follow different portfolio-based investment strategies. In the case of IPOs also, it is appropriate to assume that investors follow a strategy of investing in a portfolio of IPO firms (Pástor & Veronesi, 2005). Therefore, only a cross-sectional analysis may not appropriate. Accordingly, we need to analyse the long-run performance of IPO firms as a portfolio in the capital asset pricing framework.

The Theoretical Underpinning of Long-run Underperformance

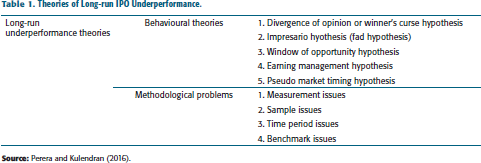

Generally speaking, for explaining long-run underperformance, the empirical literature has primarily relied on two strands of literature: first financial anomaly literature, which rejects standard asset pricing models and argues that capital markets are inherently inefficient and IPO underperformance is a reflection of such inefficiency, and second, market efficiency hypothesis that consistently maintains that financial anomalies, namely, IPO underperformance, are an outcome of biases in the measurement of long-run return (Perera & Kulendran, 2016) (Table 1). In this regard, we briefly discuss financial anomaly literature, followed by a discussion on the recent evolution in asset pricing models.

Theories of Long-run IPO Underperformance.

Financial Anomaly Argument

According to the financial anomaly literature, IPO underperformance could result from three related problems, that is, the winner’s curse, the window of opportunity, and the earning management problem. Winner’s curse relies on behavioural finance theories to show that economic agents make systematic errors in their decisions (Ritter, 2003). Contrary to the winner’s curse hypothesis, the window of opportunity hypothesis explains long-run underperformance resulting from a speculation bubble known as the investment fads (Shiller, 2014), whereby markets are characterized by very high investor enthusiasm. Under this situation, issuers with weak fundamentals exploit this phenomenon and bring their issues around the peak of the fad. Once the fad is over, investors suffer losses. The earnings management hypothesis argues that IPO firms show higher operating performance by managing their accrual income over cash flows throughout the IPO process. As a result, post-issue actual earnings are revealed to investors, bringing down prices after issue (Teoh et al., 1998). A common thread in all financial anomalies hypotheses is that capital markets are inherently inefficient.

Contrary to behavioural conjectures, the market efficiency arguments explain that financial anomalies are chance outcomes. Overreaction and under-reaction to information are equally likely (Fama, 1998), and the use of appropriate methodology manifests in the disappearance of anomalies.

Investment and Profitability Hypothesis

Lyandres et al., (2008) found that as compared with established firms, issue firms over-invest and thereby achieve lower returns after issue. The investment hypothesis claims that issuing firm is less risky as a potential growth opportunity is transformed into an asset, which reduces risk and expected return. Fama-French (2015) provides a more formal explanation for using investment and profitability factors as additional factors in the extended asset pricing model. The new version is known as the Fama-French Five-Factor model. The empirical literature indicates that the five-factor model outperforms the three-factor model in explanatory power to elucidate various financial market irregularities (Nichol & Dowling, 2014; Wang et al., 2015; Zhang, 2017).

A Model for the Relationship Between Investment, Profitability and Expected Stock Return

Fama and French (2015), using a simple dividend discount model (DDM), showed a relationship between investment, profitability, and expected return. At time t, price of a share of a company, Mt is given by

where,

Here, Yt+τ is total equity earnings for period t+τ and dBt+τ is the change in total book value of equity or fresh investment by firms. It can be alternatively be written as:

In equation (3), everything else constant except the current value of the stock Mt, and the expected stock return [r], then a lower value of Mt/Bt implies a higher expected return. Alternatively, fix everything except expected future earnings and expected stock return, then a higher expected earning leads to higher stock return and; a higher growth in value of book equity Bt (or real investment) implies a lower expected return. The above analysis provides a basis for including investment and profitability factors in the Fama-French Factor Models (4).

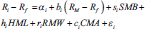

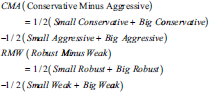

In the above, RM-Rf is market risk premium, that is, excess market return over the risk-free rate (Rf), and Ri-Rf, the excess return of an asset over the risk-free rate. A statistically significant α with negative [positive] coefficients suggest underperformance [outperformance] in the portfolio unexplained by the risk premium. SMB is the difference between returns of ‘small’ and ‘big’ stock portfolios, while HML is the difference between returns of firms with a ‘high’ book-to-price ratio and firms with a ‘low’ book-to-price ratio. 2 CMA and RMW are investment and profitability factors, respectively (the formation methodology of these factors is in the next section).

DATA AND METHODOLOGY

Data

Our study uses the data from Prowess, managed by the Centre for Monitoring the Indian Economy (CMIE). The sample consists of firms that underwent IPO from 1 January 2000 to 31 March 2015, on the Indian exchanges 3 . We analyse the market return of IPO firms for 36 months after listing. Accordingly, we have used market data up to March 2018. A firm has been included in our sample if it has a minimum of 36 months of market data. We calculated the monthly return using month-end stock prices after adjusting for stock splits, bonuses, and other financial events other than a declaration of dividends.

Abnormal returns are calculated using the adjusted closing prices of benchmark indices such as BSE Sensex, BSE 500, NSE Nifty, and NSE 500. Yields of three months treasury bills are used as the risk-free rate. Data of market factor, size factor, and valuation factor are from Agarwalla et al. (2013). Investment and profitability factors are estimated following Fama and French (2015).

Measurement of Long-run Abnormal Return and Related Statistical Issues

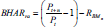

Following Lyon et al. (1999) and Schwert (2003), we measure the long-run performance of IPO firms using 36 months buy and hold abnormal return (BHAR) and cumulative abnormal return (CAR)

4

. The n period risk-adjusted total stock return or risk-adjusted BHAR is defined as (eq. 5)

Here, Pt+n is closing price after n months and Pt is the closing price at the tth period and RBM is the return of the benchmark index for the same period. Using the method of Ritter (1991), Brav and Gompers (1997), and Lyandres et al. (2008), we define CAR as (eq. 6).

The CAR of a firm after s months of IPO is defined as a summation of average benchmark adjusted returns. These measures can also be weighted by using suitable weight for size and other firm-related attributes.

Formation of Investment and Profitability Factor

Following Fama and French (2015), we construct the investment and profitability factors. Fama and French (2015), and Hou et al. (2015) use change in a firm’s total asset during periods t and t−1 as a proxy for investment. For profitability, Fama and French (2015) have used return on asset (ROA) [ratio of operating profit with the total asset at t−1] as a proxy. Besides, researchers have made economy-specific adjustments to incorporate local realities in factors (Chiah et al., 2016). Accordingly, we dropped smaller market capitalization firms cumulatively representing less than 5% of the total market capitalization. During the study period (2000–2018), there were 5,963 listed firms, after applying filter for small market capitalization firms, we are left with 1,392 firms. The remaining firms are divided into two equal parts based on size and three parts (30 : 40 : 30) using investment rate and profitability. In line with Agarwalla et al. (2013), factor portfolios are adjusted in September every year. Formation of profitability and investment factors is done using two X three sort of size and profitability, and size and investment variables.

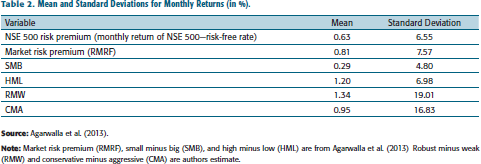

Mean andStandard Deviations for Monthly Returns (in %).

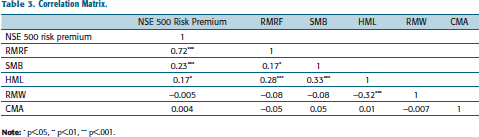

Correlation Matrix.

Regression Test for all Factors.

DESCRIPTIVE STATISTICS

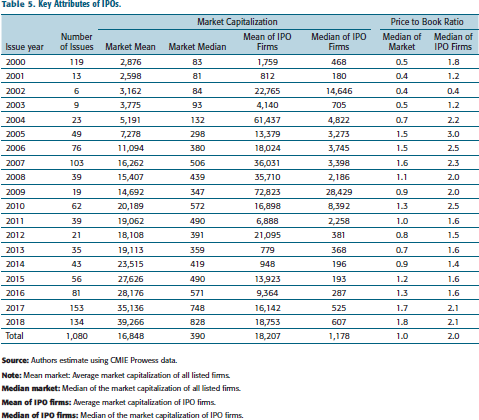

Key Attributes of IPOs.

The median size of an IPO firm was larger than that of a median listed firm in India till 2012 when BSE and NSE launched dedicated platforms for small and medium enterprises. Even the mean size of IPO firms is larger than the market mean size, indicating a relatively larger size of issue firms in India. The larger ‘firms’ size of IPOs probably reflects strict entry regulations framed by the SEBI to deter poor quality firms from mobilizing resources from the Indian capital market after exuberance in the 1990s. However, price to book (PB) ratios of IPO firms are generally higher than the average firm listed at BSE and NSE (Table 5). From a higher PB ratio, we could infer that these companies promised to give a higher return at the time of the issue.

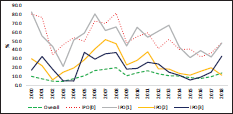

The frequency distribution of Indian IPO firms in terms of annual investments reveals that Indian firms make significant investments in productive assets (Shukla & Shaw, 2018). The higher investment by IPO firms indicates the presence of positive net present value opportunities with firms. This also demonstrates that investing firms convert their growth opportunities in assets after issue (Carlson et al., 2006; Cochrane, 1991). However, as growth opportunities shrink in the subsequent years, firms’ investment growth in physical assets declines and converges with industry averages (Figure 2).

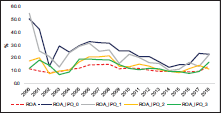

The presence of attractive investment opportunities with issue firms is confirmed with a higher return on assets reported by these firms vis-à-vis the industry average. IPO firms start at a very high return. Higher investment during and after the issue period reduces the expected return for issue firms. In other words, these firms are unable to convert their issue year investments in profit, and their relative performance corrects sharply converging with the industry average (Figure 3). The decline in profitability of these firms reflects the inability of these firms to exploit their new investments (Shukla & Shaw, 2018).

POST-ISSUE PERFORMANCE

As mentioned in the methodology section, following Loughran and Ritter (1995), Gompers and Lerner (2003), and Sahoo and Rajib (2010), we estimate CAR and BHAR for IPO firms adjusted for benchmark indices. Further, to assess possible industry effects on the long-run performance of IPO firms, we calculate CAR and BHAR for all firms, for only non-financial firms, for only manufacturing firms, and for other firms (i.e., non-financial and non-manufacturing firms).

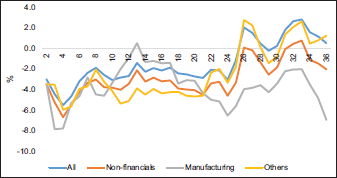

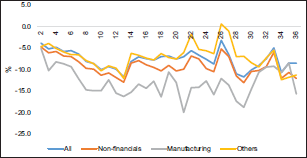

The mean CAR of IPO firms is negative in the first twenty-four months; however, it turned positive after the twenty-fifth month onwards (Figure 4). On the other hand, the mean CAR of manufacturing firms is negative for almost all months. As against the mean CAR, the median CAR of firms from all industries is significantly negative, reflecting sharp underperformance by most firms (Figure 5). However, this also indicates that some IPO firms show very high outperformance.

Compared to event month-wise abnormal return, IPO firms’ calendar year basis performance displays a very different picture. These firms exhibit very sharp underperformance and outperformance based on the year of an issue. In certain issue years, particularly in high volume years, we observe sharp underperformance, while in other years, a sizable outperformance is observed. This suggests that underperformance or outperformance by IPOs is not absolute in India, contrary to the generally observed experience in the US market.

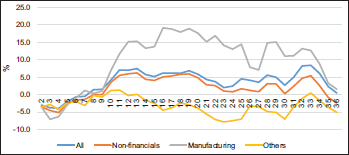

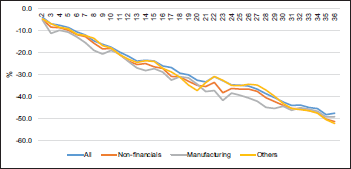

The movement of mean BHAR is similar to mean CAR (Figure 6). However, in contrast to the above, the median BHAR of all classes of firms shows a very stark underperformance (Figure 7). The sharp underperformance of median IPO firm vis-à-vis benchmark indices is in line with global literature.

Standard measures of long-run post-issue abnormal return of the Indian IPO firms show that, like their global peers, IPO firms in India also record severe long-run underperformance when analysed in the event study framework. This outcome is closer to the findings of financial anomaly literature, that is, investment fad (Shiller, 1990) and window of opportunity (Loughran & Ritter, 1995) debate. However, the issue-year-wise analysis also favours arguments of pseudo-market timing hypothesis (Schultz, 2003).

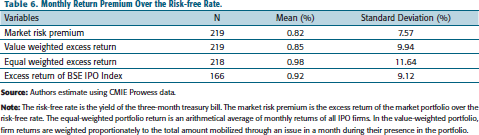

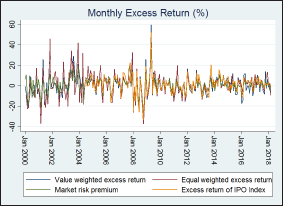

Monthly Return Premium Over the Risk-free Rate.

Monthly returns of all these portfolios display a very high degree of co-movement with broader market returns (Figure 8). The analysis presented here shows that long-run underperformance by issue firms in the US literature is based on somewhat specific samples. Accordingly, we need to perform calendar-time factor regressions following Fama and French (2015) and Lyandres et al. (2008). In the next section, we perform two separate regression analyses, first at the firm level and then at an aggregate portfolio level.

FACTOR REGRESSIONS IN FAMA-FRENCH THREE-FACTOR AND FIVE-FACTOR FRAMEWORK

Analysis of the previous section suggests that there are long-run underperformance by IPO firms vis-à-vis benchmark indices when performance is analysed at the firm level following certain methodologies. Nonetheless, the above analysis does not throw any light on whether the return offered by the IPO firms is commensurate with asset pricing models or not. Therefore, we perform two separate regression analyses, firm-level, and portfolio-level, in the asset pricing framework as discussed the third section (eq. 4).

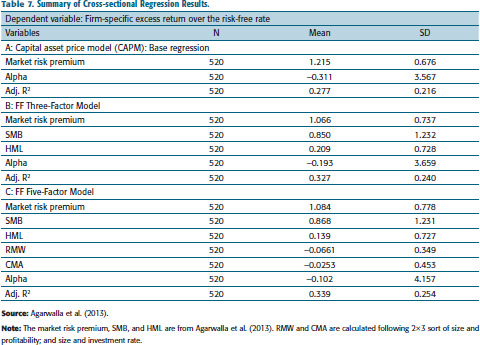

Firm-Level Analysis

Summary of Cross-sectional Regression Results.

The firm-level regression analysis shows that there is underperformance in IPO firms vis-à-vis the broader market. We also find that as we include more factors to account for systematic risk, the size of underperformance declines. After showing underperformance at the firm level and relevance of investment and profitability factors for IPO firms, we analyse portfolios formed of IPO firms on an equal-weight and value-weight basis.

Portfolio Analysis

For portfolio analysis, we form two sets of portfolios, an equal-weighted and a value-weighted. An equal-weighted portfolio is created using a simple average of monthly returns of all IPO firms for 36 months. On the other hand, the value-weighted portfolio was formed using the issue amount by the issuing firm during the month as a weight. Accordingly, weights of the value-weighted portfolio are adjusted when either a new firm makes an issue or an existing firm completes 36 months and therefore is dropped from the portfolio. Hence, weights of portfolios are adjusted every time a new firm comes with an issue, or an existing firm leaves it.

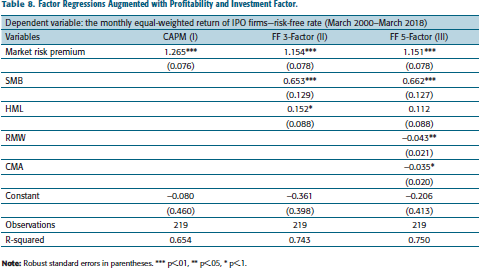

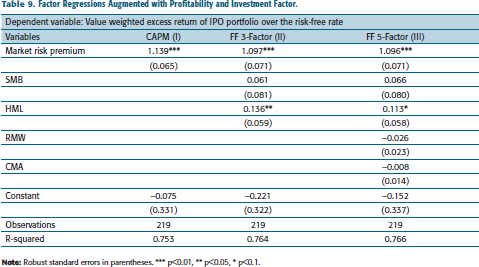

The equal-weighted and value-weighted monthly excess returns of portfolios of IPO firms are regressed over market risk premium in a baseline case, that is, capital asset pricing model. Subsequently, the baseline model is augmented by size, valuation, investment, and profitability factors, respectively (Cooper et al., 2008; Fama & French, 2015; Lyandres et al., 2008; Titman et al., 2004) (Table 8).

Factor Regressions Augmented with Profitability and Investment Factor.

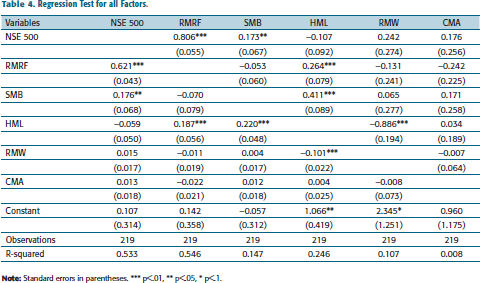

The result for our baseline CAPM, reported in column I of Table 8, indicates that the intercept term is negative but statistically not significant. This result is significantly different from the results of our firm-level regressions. Therein, we found that many firms have negative and statistically significant intercepts. The insignificance of the intercept of portfolio regression shows that portfolio formation alone cancels many risks inherent at a firm level. The coefficient of market risk premium is statistically significant and greater than one, meaning that the portfolio of IPO firms is a high-risk portfolio, as is evident in co-movement with market returns (refer to Figure 8). Market risk is, therefore, able to explain the return of issuing firms. As suggested in the pseudo-market timing hypothesis (Schultz, 2003), generally IPOs come to market when the broader market is peaking or at very high levels. In this scenario, when the market declines, issuing firms record even sharper negative returns. Therefore, an average issue firm gives a negative return, when analysed in an event study framework as generally observed in the literature. However, if issues are made at the ebb of a market cycle then issuing firms outperform the broader market. This result is in line with the findings of the fourth section, wherein we do not observe any significant underperformance by a portfolio of IPO firms formed on an issue-year basis. Another aspect is that, unlike Fama and French (1993), we find that coefficients of size and valuation factors are relatively smaller vis-à-vis reported in the US studies (Table 8, column II). In the five-factor test, we add investment and profitability factors (Table 8, column III). We find that the profitability and investment factor coefficients are negative and statistically significant. This finding is similar to the results of Lyandres et al. (2008). The value of adjusted R2 rises in all specifications. The five-factor model can explain around 75% variations in the portfolio compared to 65% in the case of baseline analysis.

Factor Regressions Augmented with Profitability and Investment Factor.

CONCLUSION

IPOs are one of the most critical capital market events. Even from a firm’s perspective, IPOs are a major structural break. In the Indian capital market, the equity segment is more prominent vis-à-vis the debt segment. In the equity segment, an IPO is a principal instrument through which new firms come to the market. Academic literature, generally for advanced economies, has pointed out that IPOs are a loss-making investment in the long run vis-à-vis already listed firms. Though the Indian IPO market is one of the largest globally, the capital market is still developing. The capital market regulator is making concerted efforts to improve corporate governance structures and enforcing legal statutes relating to the protection of minority stockholders. However, a weaker regulatory regime still symbolizes the Indian system. ‘IPOs’ long-run market underperformance is touted as an outcome of the relative price inefficiency prevalent in the Indian capital market.

We analysed the long-run market performance of the Indian IPO firms floated from April 2000 to March 2015 in the event study framework and asset pricing framework. Our analysis suggests that contrary to the US-based studies’ experience, where over a longer period, IPO firms as a portfolio generate a significantly lower return even after adjusting for systematic risks, the IPOs in India as a portfolio do not exhibit an underperformance on a systematic basis. At the firm level, we find cases of underperformance, and we also see that a median IPO firm gives a significantly lower return than a benchmark index. The fundamental explanation for this outcome is that most issues are floated when the broader market is at the financial cycle’s peak. This outcome is akin to pseudo-market hypothesis (Schultz, 2003).

We perform a host of firm-specific and portfolio-related analyses. Our event study-based analysis shows that IPO firms underperform in terms of the buy and hold abnormal return and cumulative abnormal return. Further, when we regress the monthly excess return of IPO firms in an asset pricing framework, most firms have negative intercepts. We find that the inclusion of additional systematic risk factors, namely, size, valuation, investment, and profitability, reduce intercepts’ negativity. Hence, the additional risk factors help in explaining the underperformance. Investment and profitability factors also have the right signs suggesting that IPO firms possibly over-invest and record lower profit.

We form an equal-weighted portfolio and a value-weighted portfolio of all the IPO firms during the study period. Excess returns of these portfolios are regressed over market risk premium and other Fama-French Factors. Portfolio-based regression analysis provides additional evidence that systematic risks can explain the long-run return of IPOs. The investment and profitability factors are significant with a negative sign. Therefore, in this study, we also find investment and profitability factors have additional explanatory power to explain the long-run return of the issuing firms. However, as discussed, ‘IPOs’ long-run underperformance is just one of many oft-cited anomalies. The outcome of this study encourages a newer analysis of financial anomaly behaviour.

Footnotes

ACKNOWLEDGEMENT

Authors are thankful to Professor K. Narayanan and Professor Ranjan Kumar Panda of Humanities and Social Sciences Department of the IIT Bombay for their comments on an earlier version of the article. Authors express their gratitude towards Dr Govind Prasad Samanta, Adviser, RBI for constant support.

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

DISCLAIMER

The views expressed in the article are those of the authors and do not represent the views of the institutions they belong to.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.

NOTES

e-mail:

e-mail: