Abstract

Benford’s Law is viewed as an interesting phenomenon for studying naturally occurring digits. Benford discovered that naturally occurring numbers tend to follow a specified logarithmic probability distribution function. Benford’s Law, specifically in the field of accounting and finance, has been used as a tool to detect patterns in reported earnings. Its applications include detecting dubious digits in forensic accounting, detecting possible financial irregularities, and detecting fraud in accounting data.

Benford derived the logarithmic expression for the probability distribution function.

Where P (d) is the probability of a number having the first non-zero-digit d and log n is logarithmic to the base 10.

The current study attempts to validate Benford’s Law on data obtained from financial statements of two categories of companies that have been identified a priori. One category is of suspected shell companies and the other one is of the genuine companies. For carrying out research, all the listed companies on CNX 500 Index of National Stock Exchange (NSE) of India and a list of 331 suspected shell companies declared by Securities and Exchange Board of India (SEBI) constituted population of the study. The study includes analysis of both first digit and second digit of 301 companies over a period of 10 years. Deviation measures such as Kolmogorov–Smirnov (KS) statistics and mean absolute deviation (MAD) are used for the purpose of analysis. Findings of the study conclusively prove the validity of Benford’s Law for financial data disclosures in India. Second digit of financial data has the potency to provide better discrimination between genuine financial data and concocted data. Data pooling across the years augments the ability to Benford’s Law to segregate genuine financial data sets from fudged data sets.

where P(d) is the probability of a number having the first non-zero-digit d and log n is logarithmic to the base 10.

The defining characteristic of Benford’s Law is that it is observable only in naturally occurring numbers, not in numbers that are artificially concocted (Kumar & Bhattacharya, 2007). Benford’s Law applies to almost all natural numbers (Nigrini, 1999), but does not apply to assigned numbers (Bradley & Farnsworth, 2009). The law has been used for finding out the level of error in financial statements disclosed by the companies. With the help of numerical methods, it was disclosed that error-free financial statements tend to follow Benford’s Law (Amiram et al., 2015). Previously, financial irregularities have been detected with the help of Benford’s Law. Documented evidence suggests that managers of Japanese firms tend to engage in manipulative activities of rounding earnings numbers (Skousen et al., 2004). Similarly, managerial intervention in the capital allocation process is proven in the German Banking Industry (El Mouaaouy & Riepe, 2018). Departure from Benford’s Law has been determined as a significant predictor for bank failures (Alali & Romero, 2013). Disclosed remuneration of managers of the publicly listed companies in the USA have been found to largely follow the law (Mukherjee, 2018).

The present study attempts to evaluate the efficacy of Benford’s Law in the context of discriminating between shell companies and genuine companies. We used both first and second-digit distributions for assessing the conformance of financial statement data with Benford’s Law. Majority of the Benford Law based studies, regarding intentional/unintentional financial statements errors, are from developed countries such as the USA (Alali & Romero, 2013; Bradley & Farnsworth, 2009), Japan (Skousen et al., 2004), and European countries such as Germany (El Mouaaouy & Riepe, 2018; Ullmann & Watrin, 2017) and Spain (Badal-Valero et al., 2018). To our knowledge, there are no studies in the existing literature that have attempted to compare shell and genuine companies with the help of Benford’s Law. This is a first of its kind study aimed at evaluating the efficacy of Benford’s Law in identifying shell companies.

BACKGROUND OF THE STUDY

Prior Literature on Benford’s Law

Natural numbers carry an unexpected quality not found in assigned/concocted numbers. Benford’s Law can be used to segregate natural numbers from concocted numbers. Financials can provide vital clues regarding the nature of the firm and unlawful practices (Ravenda et al., 2018). Benford’s Law is helpful in detecting the cases where fictional numbers are involved or at least can be used as a signal to audit more (Nigrini, 2018).

Benford’s Law of the expected frequency of naturally occurring leading digits (Nigrini & Mittermaier, 1997) is widely used and discussed in the financial accounting, auditing, and fraud detection literature (Diekmann & Jann, 2010; Rauch et al., 2011; Tödter, 2009). The law was introduced to auditing literature by Nigrini and Mittermaier (1997) with a goal to detect fraud. Benford’s Law was also applied in finance literature (Dorfleitner & Klein, 2009; Kalaichelvan & Kai Jie Shawn, 2012) and detecting tax irregularities. Specifically, in the field of accounting and finance, Benford’s Law has been used as a tool to detect patterns in reported earnings (Skousen et al., 2004). Other applications include detecting dubious digits in forensic accounting (Kumar & Bhattacharya, 2007), detecting possible financial irregularities (Amiram et al., 2015), investigating the characteristics of failed US commercial banks (Alali & Romero, 2013), and detecting fraud in accounting data (Badal-Valero et al., 2018). Non-conformance to Benford’s Law is termed as an indicator of poor internal and disclosure control resulting in poor quality financial data. Advantages of applying Benford’s Law for fraud detection include ease of implementation, low cost, and applicability to large databases (Kovalerchuk et al., 2007).

At the same time, the statistical evidence of non-conformity to Benford’s Law should not be considered conclusive, but it should be regarded as one of several investigation tools that can be utilized by a forensic accountant to detect fraud (Kumar & Bhattacharya, 2007). Apart from accounting-based studies, the law has been used for finding errors and frauds in scientific publications (Diekmann & Jann, 2010) and scientometric data (Campanario & Coslado, 2011).

Shell Companies

Fast-paced development in the emerging economies often accompanies the chances of manipulation and misrepresentation on the part of various stakeholders. Shell company is a corporate entity without active business operations. Shell companies are usually incorporated with the intention of evading law to undertake illegal money laundering and related activities. It is interesting to note that shell companies are usually listed on the stock exchange and are not illegal inherently. However, a large number of shell companies are deliberate financial arrangements created to promote start-ups or illegal activities such as tax evasion (Obermayer & Obermaier, 2016; Sharman, 2017), bankruptcy frauds, fake service schemes, market manipulation, money laundering for terrorist activities, and drug trafficking (Cooley et al., 2018). There are several instances where private firms go public via a reverse merger with the help of shell companies, therefore, avoiding the fundraising process (Floros & Sapp, 2011). As a part of the shadow economy, such firms lead to black money transactions (Jancsics, 2017). Black money transactions hinder the implementation of development initiatives and render policy interventions ineffective. On account of increased financial reporting frauds, the regulators in the developing countries have initiated a range of reforms (Nyamori et al., 2017). Fight against such illegal activities and black money has been on in India for quite some time. The incumbent Union Government has launched many initiatives to curb the menace of black money and money laundering activities. Digitization has been providing a helping hand to this cause. Shell companies play a detrimental role to the tax systems and growth of an economy. Therefore, it is important to identify and curtail such illegal activities on the part of shell companies.

The Relevance of Benford’s Law to the Study

Previously attempts have been made to identify the fraudulent financial statements using statistical analysis (Jones et al., 2008, MacCarthy et al., 2017) such as Beneish M-score (Beneish, 1999) and anomaly detection (Luna et al., 2018; Stack, 2015). But the need for improved and alternative methods has also been expressed in the literature (Aris et al., 2015). As shell companies do not undertake business operations, these are likely to present concocted financial statements. Benford’s Law can be used to identify such fraudulent financial data disclosures. It is tough to fabricate data conforming Benford’s Law (Bolton & Hand, 2002). Based on conformance to Benford’s Law, the comparison of shell companies with genuine companies can reveal the potential of the said law in discriminating between the two types. The present study attempts to compare the suspected shell companies with genuine companies for checking the efficacy and validity of Benford’s Law in the given context. Given the list of suspected shell companies, the information on the typology of such companies was available a priori.

METHODOLOGY

The study considers companies from two contrasting groups. The first group consists of the suspected shell companies, and the second group consists of non-shell companies, that is, expected to be the genuine companies. It can be safely presumed that naturally occurring data is available from financial statements of non-shell companies. On the other hand, data of financial statements from the suspected shell companies is expected to be concocted as these companies do not have real business transactions. For carrying out research, all the listed companies on CNX 500 Index of National Stock Exchange (NSE) of India and a list of 331 suspected shell companies declared by Securities and Exchange Board of India (SEBI) constituted the population of the study. NSE is the largest stock exchange of India, having a total market capitalization of more than US$1.41 trillion with 1,696 number of listings. The S&P CNX 500 is India’s first broad-based stock market index of the Indian stock market and represents 95.20 per cent of free-float market capitalization of all stocks listed on NSE. SEBI is the regulator of the securities market in India. SEBI vide letter no. SEBI/HO/ISD/OW/P/2017/18183 dated 7 August 2017 declared a list of 331 suspected shell companies identified by Ministry of Corporate Affairs, Government of India. SEBI curtailed trading in these companies and investors were allowed to make only one transaction per month. Using the simple random sampling technique, 151 companies from the list of CNX 500 Index and 150 companies from the list of 331 shell companies were included in the sample. Average net sale of selected non-shell companies is ₹ 64.90 billion with a standard deviation of ₹ 226.51 billion. Average profit after tax (PAT) of selected non-shell companies is ₹ 7.11 billion with a standard deviation of ₹ 22.54 billion. On the other hand, the average net sale of selected shell companies is ₹ 627.52 million with a standard deviation of ₹ 1837.40 million. Average PAT of selected shell companies is ₹ 42.32 million with a standard deviation of ₹ 332.33 million.

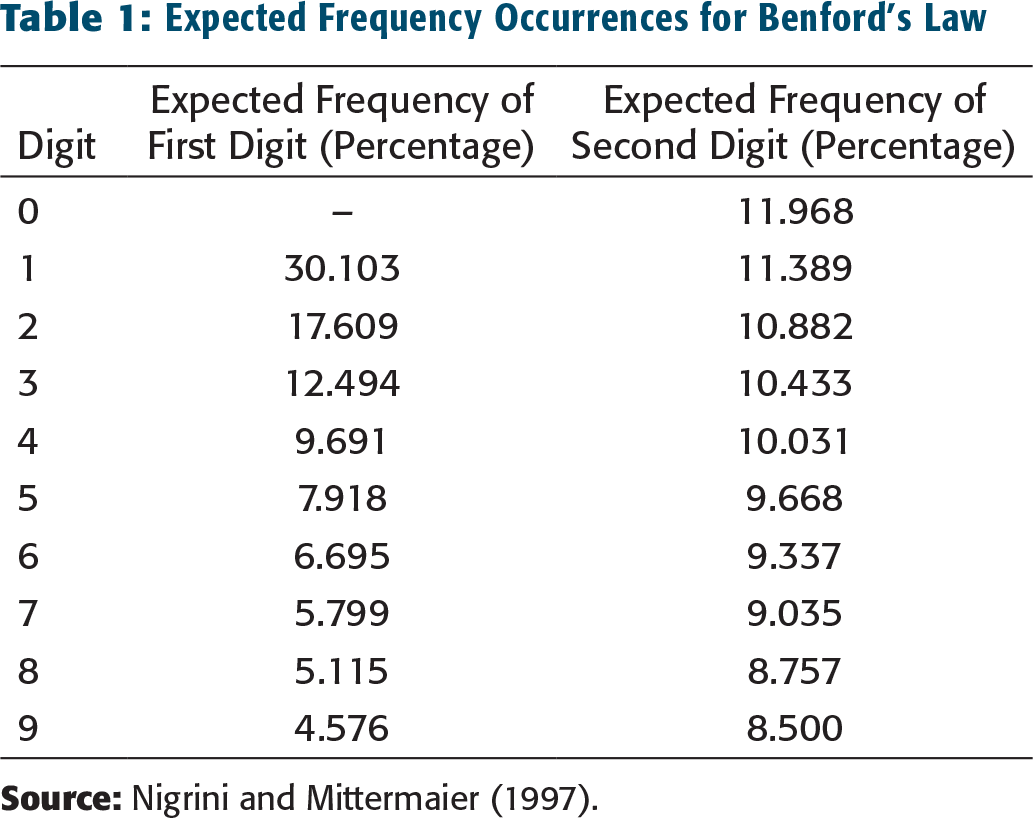

Expected Frequency Occurrences for Benford’s Law

KS statistics are computed from the distributions to test the conformity of the sample to Benford’s Law. KS statistic is calculated as follows:

where AD is the empirical frequency of actual digit, and ED is the expected frequency of the digit as per Benford’s distribution. For example, AD1 is the actual frequency of digit 1, and ED1 is the expected frequency of digit 1 as per Benford’s Law. To test the conformity of a given distribution to Benford’s distribution at the 5% level based on the KS statistic, the test value is calculated as 1.36/√N, where N is the total number of occurrences. For analysis, data sets with KS value of more than the critical value (at 5% level) are considered as cases of non-conformity.

Use of MAD is also prevalent in the literature related to Benford’s Law (Amiram et al., 2015). The MAD statistic is calculated as follows:

where K is the number of leading digits being analysed.

It is important to note that MAD-based evaluation at the most provides relative measurement and does not have any critical value (as in the case of KS statistic). Statistical tools such as chi-square test for association, phi-coefficient for the strength of association, and t-test for difference of means are used for analysis.

FINDINGS

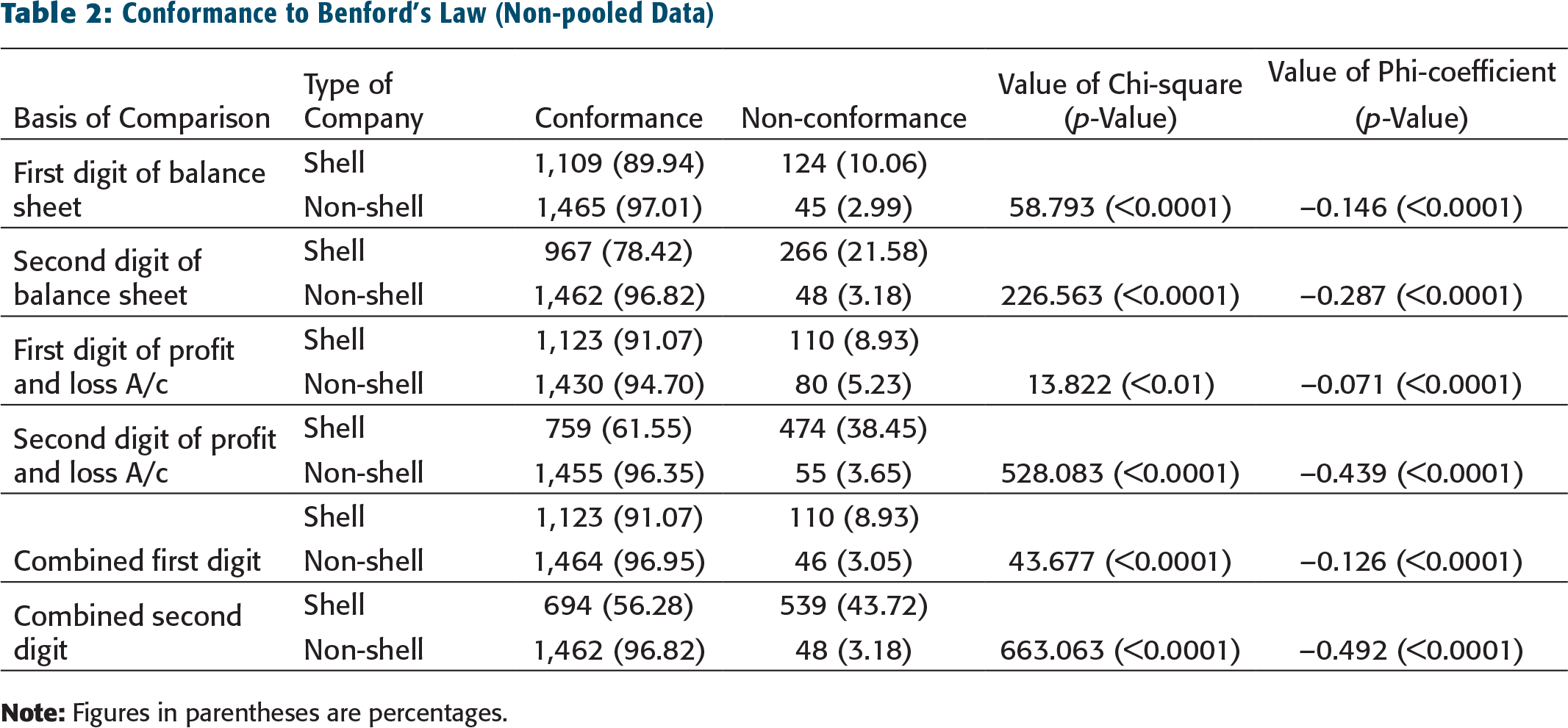

Conformity to Benfords’s law is checked for non-pooled data by calculating KS statistics for 2,743 data sets. Out of these data sets, 1,233 data sets are from suspected shell companies, while 1,510 data sets are from non-shell companies. Data sets with higher KS statistics value than the critical value at 5 per cent level are labelled as showing non-conformance.

Conformance to Benford’s Law (Non-pooled Data)

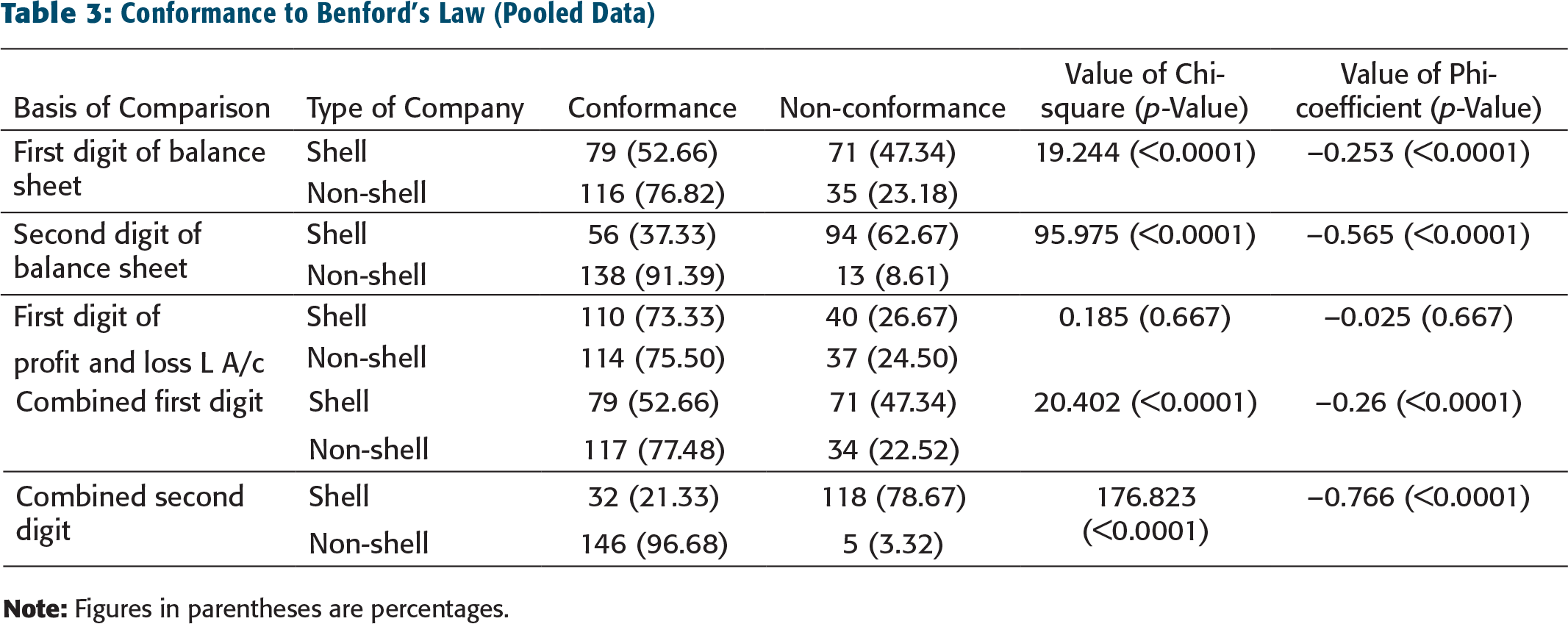

Conformance to Benford’s Law (Pooled Data)

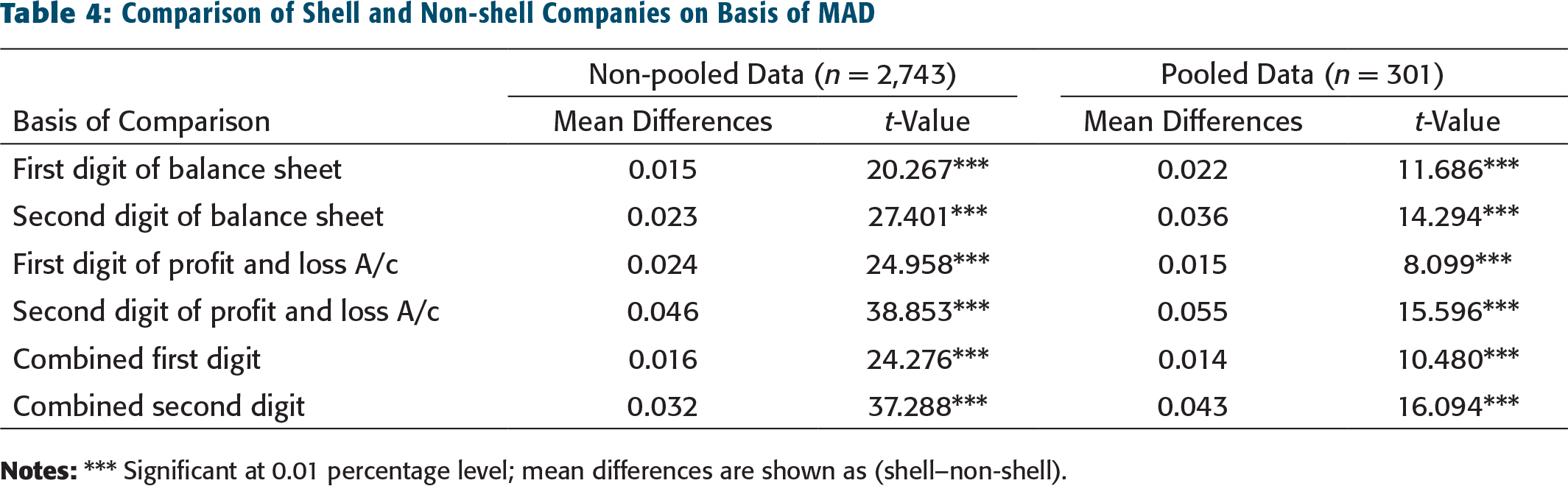

Comparison of Shell and Non-shell Companies on Basis of MAD

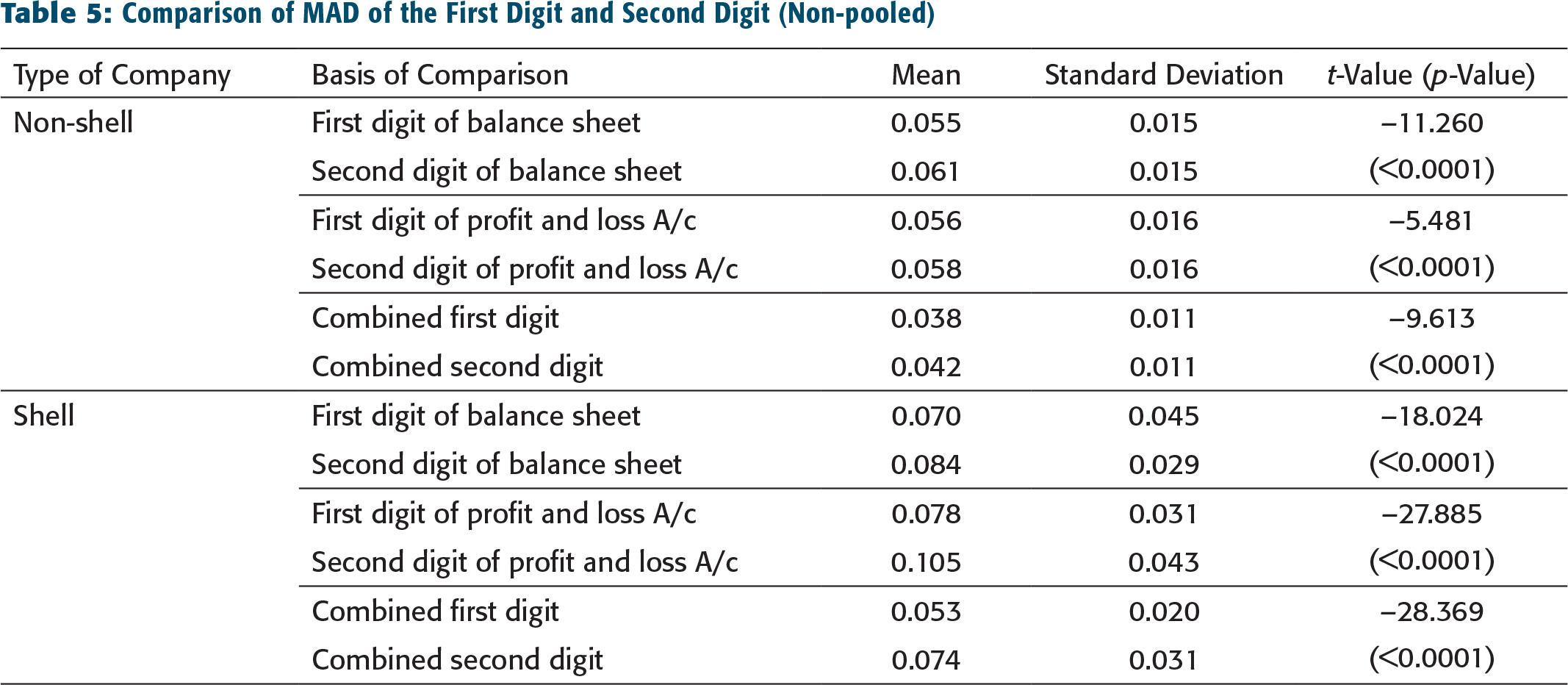

It makes an interesting observation to compare the results for the first digit and second digit of financial statements. Table 5 presents the results of the comparison of first digit data and second digit data for non-pooled data on the basis of MAD. MAD for the second digit is significantly higher as compared to that of the first digit for all instances in case of non-shell companies. There is significantly higher MAD for the second digit in case of the suspected shell companies. The ratio of average MAD of the second digit to the first digit indicates a relatively lesser variation of MAD between the first digit and second digit for non-shell companies (1.109, 1.035, and 1.105) for balance sheet, profit and loss account, and combined data as compared to shell companies (1.200, 1.346, and 1.396).

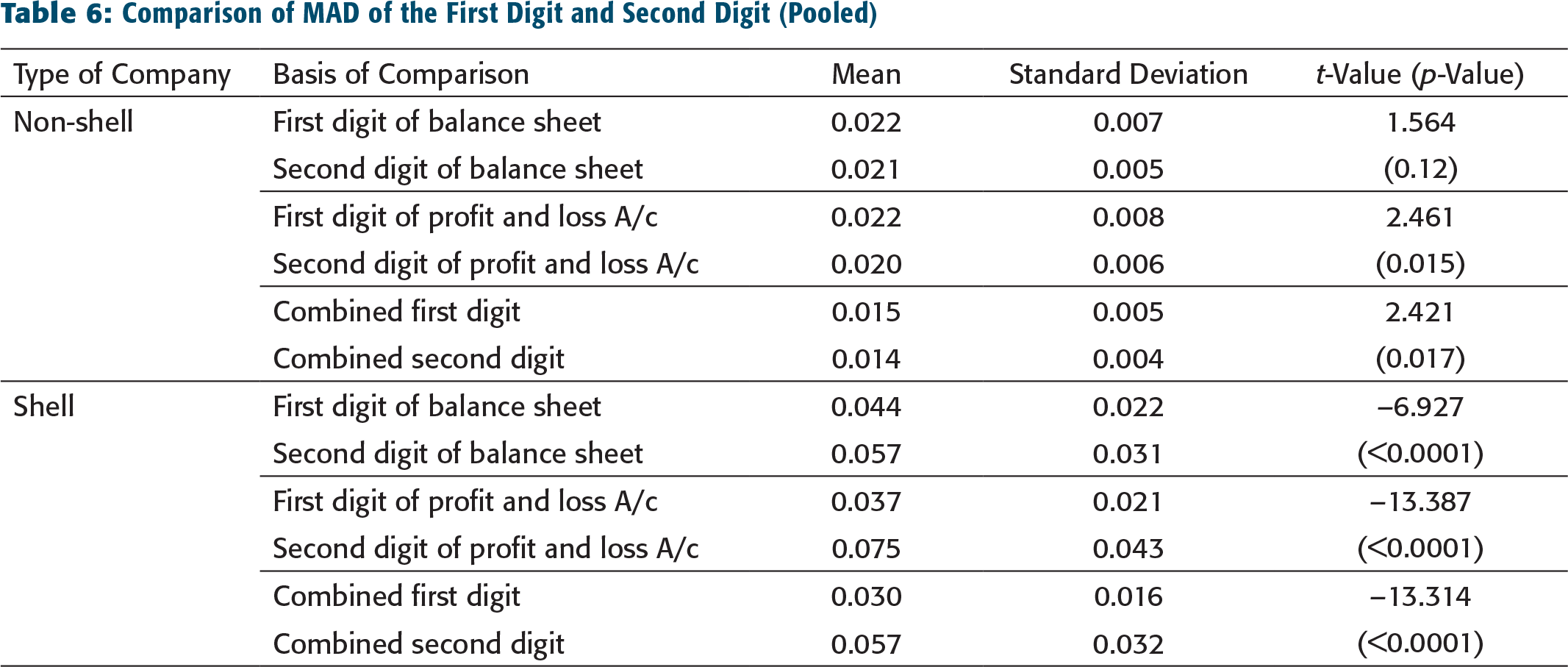

Table 6 shows the comparison of MAD for the first and second digit for pooled data. For non-shell companies, there is no significant difference between the average MAD between the first and second digit of balance sheet at 5 per cent level of significance. There is a significant (p = 0.015) lower MAD for the second digit of income profit and loss account as compared to the first digit. A similar pattern is there for the first digit of combined data (p = 0.017). Findings for the suspected shell companies exhibit an opposite pattern.

Table 6 shows significant higher MAD for the second digit as compared to the first digit for balance sheet, profit and loss account, and combined data. Ratios of average MAD of the second digit to the first digit throw up an interesting pattern in case of pooled data. There is a relatively lower variation for non-shell companies (0.954, 0.909, and 0.933) for balance sheet, profit and loss account, and combined data as compared to that of suspected shell companies (1.295, 2.027, and 1.900).

DISCUSSION

Comparison of MAD of the First Digit and Second Digit (Non-pooled)

Comparison of MAD of the First Digit and Second Digit (Pooled)

Second, the comparison of first digit results and second digit results provides an exciting insight regarding the use of Benford’s Law. For non-shell companies, there is an increase in the degree of conformity for the second digit as compared to the first digit. On the other hand, a decrease in the degree of conformity is there for shell companies for the second digit. Previously researches have also advocated relatively higher efficacy of second digit analysis (Diekmann, 2007; Durtschi et al., 2004). Pooled data exhibits higher discriminatory power of Benford’s Law as values of phi-coefficient are higher in case of pooled data as compared to year-wise data, only with the exception of the first digit of profit and loss account. Third, the ratios of mean value of MAD for second digit and first digit are different for non-shell companies and shell companies in pooled data analysis as compared to analysis based on individual years. The finding indicates that combined financial statements data for the second digit, pooled over the years, provides a maximum enhancement to discriminatory power of Benford’s Law.

It is evident from the findings that although in small fractions, non-shell companies also failed the test of conformity. On the other hand, a small fraction of suspected shell companies exhibited conformity. This finding is supported by previous studies arguing that Benford’s Law does not have the absolute power to segregate naturally occurring data from managed data (Diekmann & Jann, 2010; Goodman, 2016; Kovalerchuk et al., 2007). At best, Benford’s Law can be used as a part of a set of tools for segregating natural data occurrences and cooked data as in itself Benford’s Law may fail to identify fudged financial data in a precise manner.

IMPLICATIONS

Conformance of a data set to Benford’s Law is suggestive of naturally occurring financial data devoid of any manipulation. Benford’s Law can be effectively used for identifying shell companies on account of their non-conformance. Also, this law can be useful for making an assessment of internal and disclosure controls in the organization. Better internal and disclosure controls assure a better quality of financials. Practitioners and firms involved in forensic auditing can expect better results from the second digit as compared to the first digit. Benford’s Law is known for quite a while, and there is a possibility that to ensure conformity, data manipulators have started taking care of the first digit. But the findings of the study indicate that second digit and pooled data are more suitable for detecting the possibility of manipulation. Findings of the study also throw some caveats regarding use of Benford’s Law. Despite the validity of Benford’s Law with considerable discriminatory power, it cannot be taken as an absolute tool for segregating natural data disclosures and intentional data disclosures. Therefore, this law can be used for flagging the suspect companies for further investigation and analysis.

CONCLUSION AND LIMITATIONS

The present study is aimed at evaluating the efficacy of Benford’s Law in discriminating between a shell and genuine companies in the Indian context. We employed both first and second-digit analyses for determining the conformance of financial statement data using measures such as KS statistics and MAD. Findings of the study conclusively prove the efficacy of Benford’s Law for flagging suspected shell companies. There is a significant difference in conformance to Benford’s Law between shell companies and genuine companies. The second digit of financial data has the potency to provide better discrimination between genuine financial data and concocted data. Data pooling across the years further enhances this potency. The present study is based on secondary data, and its implications are limited by the accuracy of the data. Further research can be undertaken to test the efficacy of discriminatory power of Benford’s Law, through the second digit and pooled data, both in developing and developed countries. Also, apart from financial statements, research can be undertaken for finding out tax evasion and fraudulent international transactions. Research efforts may focus on building classification-based data mining models for identifying shell companies. Further, attempts can be made for identifying shell companies based on transaction patterns and related anomalies.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship, and/or publication of this article.

e-mail:

e-mail: