Abstract

With nearly 250 million internet and 173 million smartphone users, the Indian online industry touched US$13.5 billion (INR 865 billion) in 2014 (Bhargava, 2015; Bose, 2015; Vardhan 2014). After the acquisition of online fashion store Myntra by Flipkart in May 2014, Ola created ripples in the Indian taxi industry on 2 March 2015. It acquired its competitor TaxiForSure (TFS) for US$200 million (INR 12.8 billion) (The Financial Express 2015). Toeing Flipkartís initial strategy of retaining Myntra, Ola declared that TaxiForSure would continue as a separate entity. In the words of Bhavish Aggarwal, CEO, Ola:

Ola and TaxiForSure share the same vision of revolutionizing urban mobility. TaxiForSure has a great team and they have built a very exciting business in a short time. Thereís a lot of complementary value in the strategy TaxiForSure has followed. I look forward to working with them towards realizing our common vision. (The Financial Express 2015)

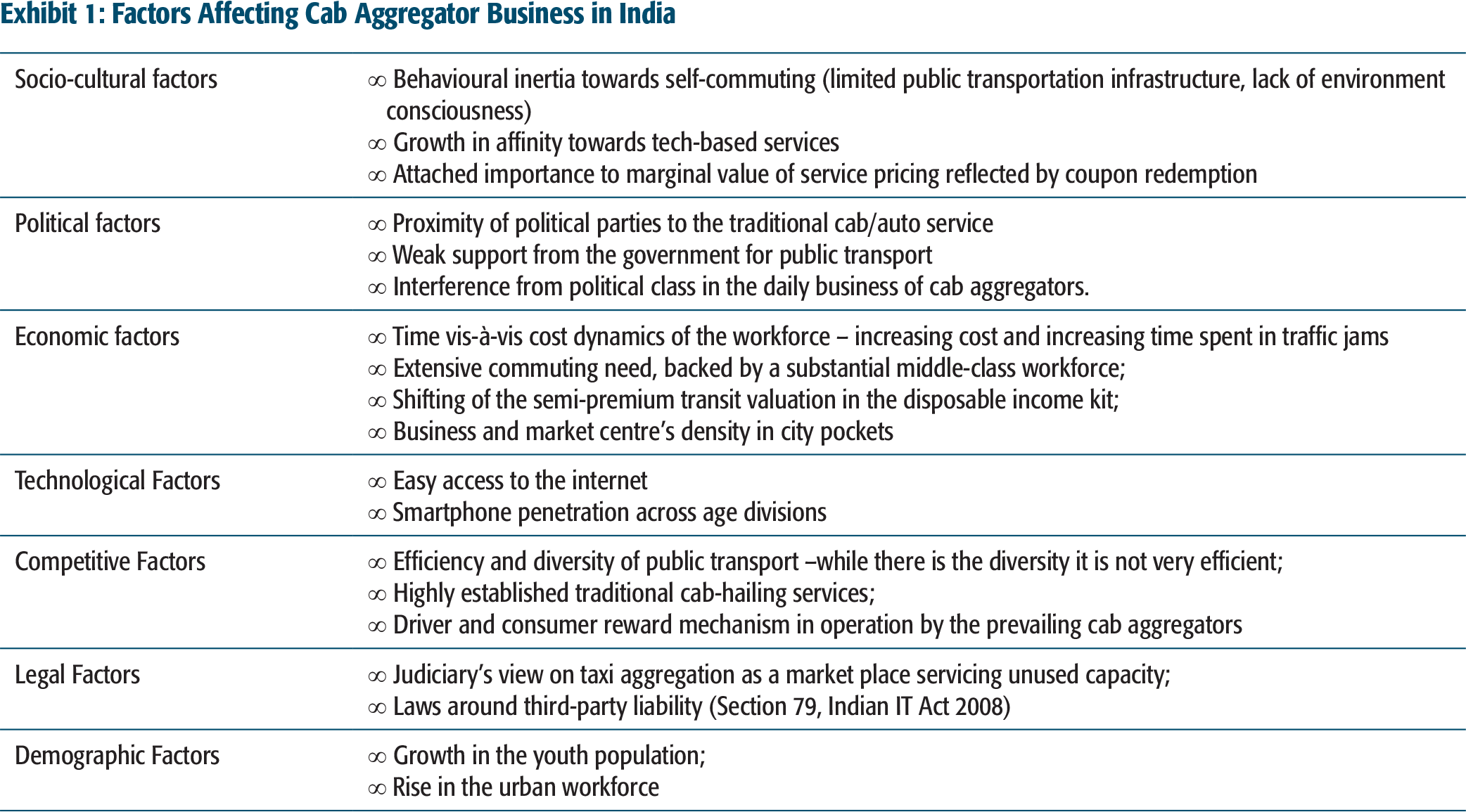

Factors Affecting Cab Aggregator Business in India

ABOUT OLA

Facing unpleasant experiences with the local cab services was a universal pain point for taxi users in India. Bhavish Aggarwal and Ankit Bhati, alumni of the Indian Institute of Technology Bombay, India, saw a huge market opportunity in the highly fragmented taxi industry (Gupta, 2015). In 2011, they founded ANI Technologies Private Limited that operated Ola as an aggregation-based business model (Prabhakar, 2015). This pioneering model sought to bring a structural change in the taxi booking space as against the conventional taxi service providers that existed in the market. According to Aggarwal:

We donít own a single car. Every car that we have in the Ola fleet is owned by a micro-entrepreneur, a driver or an operator. Ola is merely a technology platform that enables operators to generate additional revenue streams, and at the same time delivers good customer experience. (Prabhakar, 2015).

Since the model focused on customer experience, customer adoption was not a big challenge. The company commenced its operations providing place-to-place services within towns. Besides charging on an hourly basis, it also undertook reservations for outstation travel.

However, sourcing taxis for Ola proved to be quite difficult. The big challenge for the company was to convince independent cab drivers and owners to join Ola. It worked on an income allocation model with operators/drivers. Contingent on the type and size of the business, cab drivers were expected to pay between 7ñ10 per cent of every deal to the company (Prabhakar, 2015).

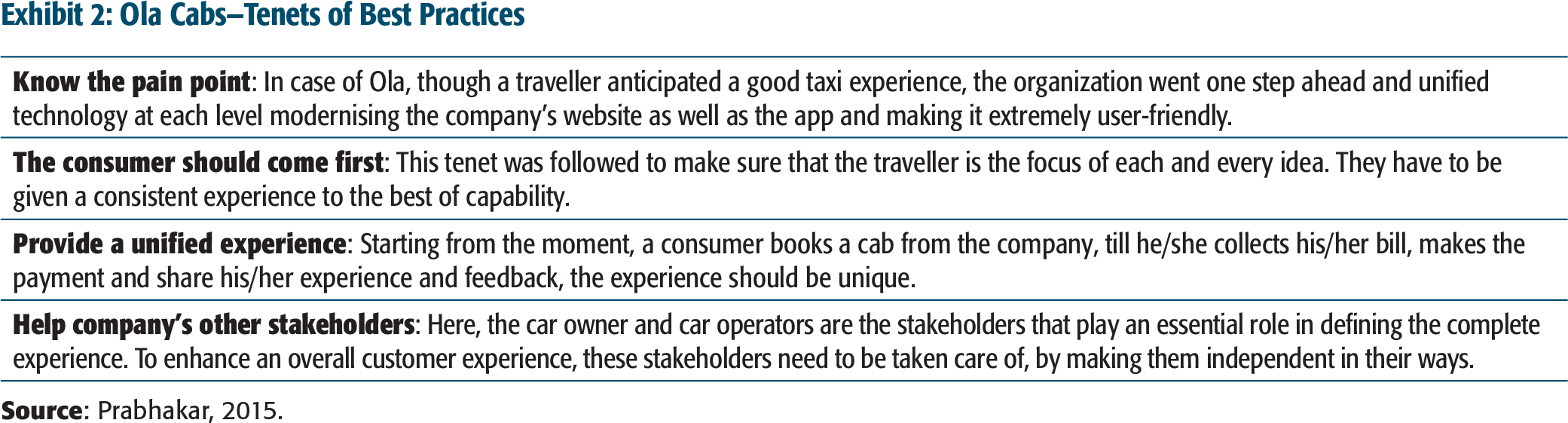

Exhibit 2: Ola Cabs—Tenets of Best Practices

For making the journey an experience in itself, Ola didnít seek a destination from its customers. Its goal was to ensure that the customerís journey was an experience, and this had nothing to do with the distance travelled. The companyís policy specifically noted that Ola drivers would never say no to customers. Once a booking was made, the driver had to serve them. In case a driver wanted to halt the ride for some time, he had the liberty to switch off the global positioning satellite (GPS). The company included an ëSOS button and emergency contactsí in January 2015 to add new personal safety features. Focusing on its customers, the company ran advertisements on radio and other mass media. It also interacted with them on social media to create its brand value. Ola accelerated its branding activities only when it launched its services in a new city (Prabhakar, 2015).

By April 2012, the company had raised initial financing of about US$5 million (INR 32.1 million) from Tiger Global Management. It further raised US$20 million (INR 128.2 million) through the second round from the existing investors in November 2013 (Prabhakar, 2015). By January 2015, Ola had 60,000 cabs in 52 Indian cities. Of these, 34 cities were added in the last three months. This reflected the pace of the companyís expansion. It had also aggressively planned to touch 200 cities by the end of 2015 (Prabhakar, 2015). The companyís revenues had grown by 40 per cent month-on-month in January 2015 (Rai, 2015). By mid-March 2015, Ola increased its operation to 67 cities and had received about US$277 million (INR 17.7 billion) in funding. The majority of these were smaller Indian cities, where Ola was the first mover (Bose, 2015). In the cities of Bangalore, Chennai, Ahmedabad, Pune, Delhi, and Hyderabad, the company also offered the booking of three-wheeler auto-rickshaws to grab a larger market share among middle-class India (Prabhakar, 2015; Track.in, 2015).

ABOUT TFS

Sensing the absolute dearth of taxi services in the country and to address the urban commuting challenges, Raghunandan G. and Aprameya Radhakrishna started Bangalore-based Serendipity Infolabs Private Limited in 2011. TFS operated under its aegis. To achieve its vision, TFS maintained a network of over 15,000 drivers, 500 operators and a fleet of cabs that included hatchbacks, sedans, SUVs, and luxury cars. The company had also launched Nano (the small car of 624cc from Tata Motors Ltd) and auto-rickshaw (three-wheeler) services. From a humble beginning in a 100 square feet garage-equivalent room, the company had grown and moved into an office space of 19,000 square feet in 2015 with a team of 1,700 employees.

By offering safe, easy, economical, and convenient travel options, TFS had emerged to be one among the fastest-growing taxi aggregators in the country. The company differentiated itself from the competitors with its asset-light business model. TFS partnered with different taxi operators, who worked with drivers. The marketing strategy aimed at incessantly increasing the customer delight quotient. With cutting-edge technology, the company endeavoured to extend the overall experience to customers, right from the point they booked a ride till they got off the vehicle. Besides training the drivers for driving, the companyís driver finishing school also taught them the ways to conduct with customers and manage technology.

Besides the initial funding of US$4 million (INR 25.6 million) from investors in June 2013, TFS further raised a total of US$40 million (INR 256 million) in two rounds in 2014. From a three-city presence in 2011, the companyís grew to 40 cities in four years and had plans to scale up. In the financial year 2012ñ2013, the company had a net revenue of INR 1

INR: Indian National Rupee

THE INDIAN TAXI MARKET

Taxis in India were known for being unsteady vehicles, with tampered meters, untrustworthy drivers, and awful service. Taxi rides were marred by frequent arguments with drivers over routes, payments, and behaviour. Nearly 95 per cent of the market in terms of a number of vehicles was unorganized, which made it difficult to estimate the number of taxis in India. It was estimated to be anywhere between 500,000 and one million (Knowledge@Wharton, 2013). Largely unorganized, most of the players had as few as one, two or three cars. A typical operator owned a fleet of 2ñ50 vehicles and had a presence in one or two cities (Gore, 2015). The sector included street taxis, radio taxis and cars on hire, besides dedicated fleets exclusively used by corporates. There was no predictability of business for these taxis. With only 2 per cent of 1.3 billion Indians owning cars, taxis emerged as the most needed amenity (Jetley, 2014). Travellers faced inadequate information and assurance regarding the availability of cabs. Adding to their woes was lack of standardization in quality of service as well as transparency in pricing (Knowledge@Wharton, 2013).

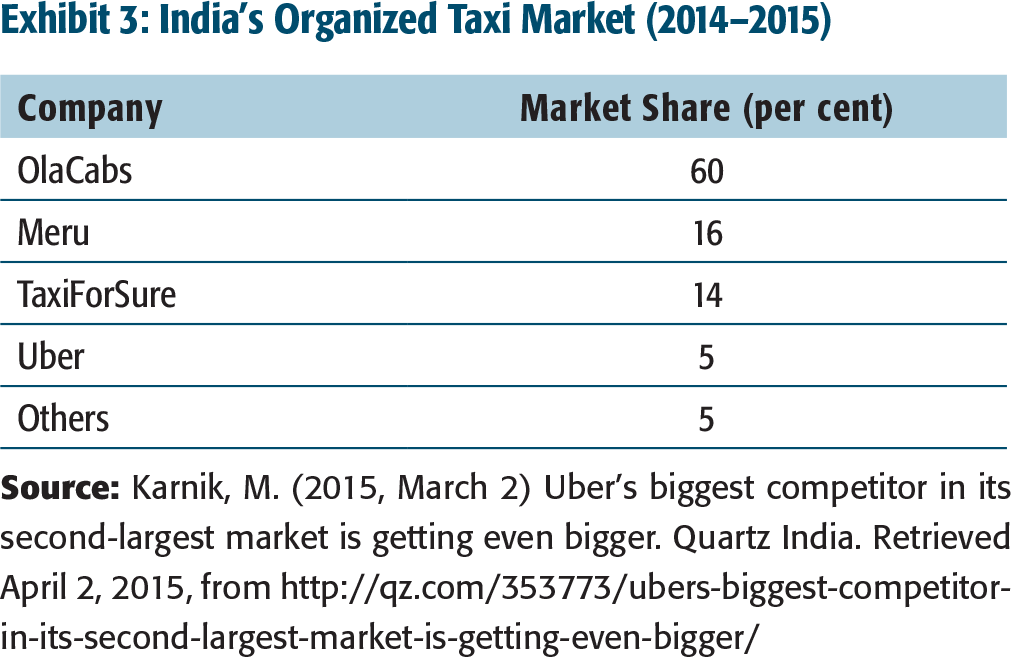

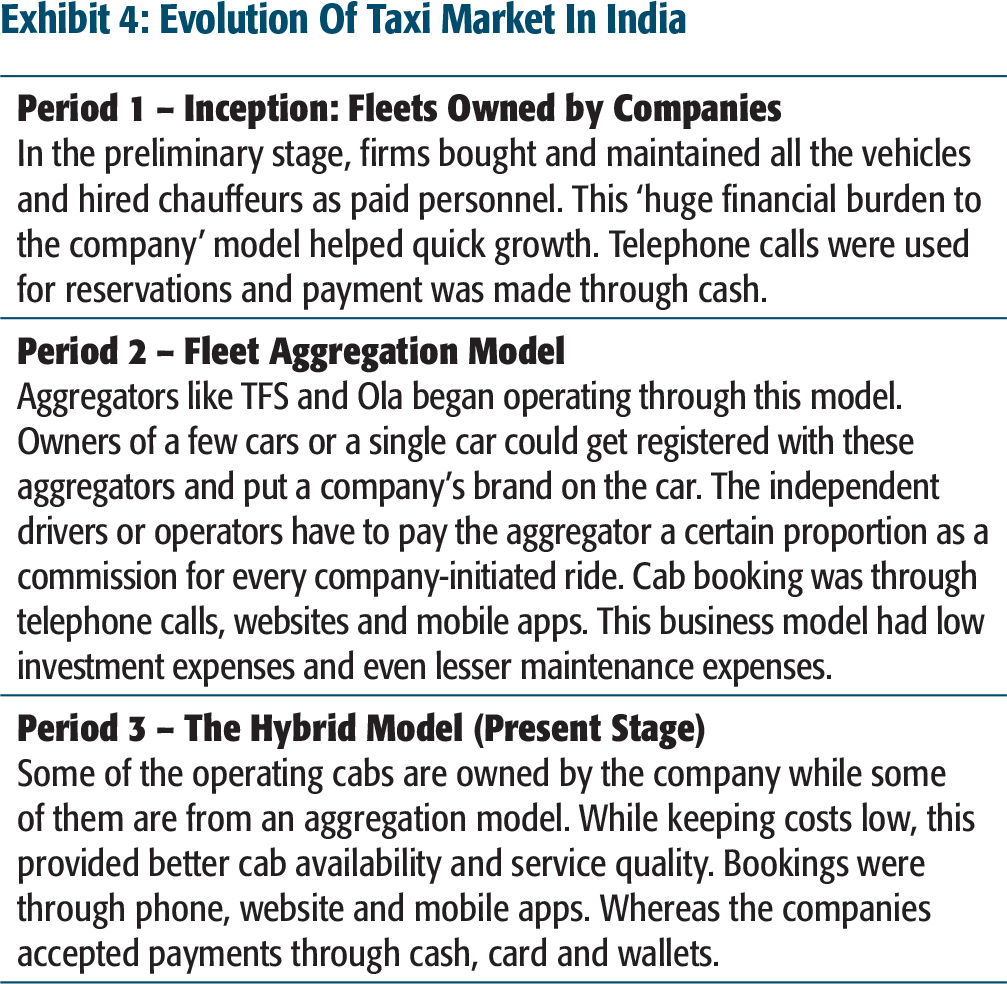

In 2001, Mega Cabs and Fast Track Taxi started with small fleets. GPS-linked, electronically-metered cabs brought a welcome reprieve in 2006 (Utkarsh, 2014). After this, players such as Meru Cabs, Easy Cabs, and Savaari entered the market. This lead to several players in the Indian taxi space vying for more market share (Utkarsh, 2014). Post the 2008 period, the industry witnessed extraordinary growth. By 2014, aggregators such as Ola, Uber and TFS had conquered 3ñ4 per cent of the entire taxi market in India and had a significant prospect of growing exponentially (Utkarsh, 2014; see Exhibit 3). Though these aggregators had started years later than the traditional radio cabs such as Meru and Mega Cabs, the former had already started eclipsing radio cabs in terms of cities being covered, fleet size, services offered, and pricing (Jetley, 2014). By 2020, together these organized players were projected to have 15 per cent of this market (Kumar, 2015). The taxi market in India had evolved in three distinct phases (see Exhibit 4).

To cater to the demand of cheap taxies, operators came out with smaller cars that were more economical than the traditional taxis and radio cabs. In this category, Meru launched ëGenieí in Bengaluru and Hyderabad, the two most emerging corporate towns in India (Ghosh, 2015).

India’s Organized Taxi Market (2014–2015)

Evolution Of Taxi Market In India

Estimated to be around INR480 billion (US$8 billion), the taxi market was projected to grow at 17ñ20 per cent annually. Investments through venture capitalists to the tune of INR24 billion (US$400 million) had been made into these companies (Ghosh, 2015). To focus on its expansion, Ola, at a valuation of over US$1 billion (INR 64.1 billion), had raised over US$210 million (INR 13.4 billion)from Softbank. TFS had also raised US$30 million (INR 192 million) in 2014. With over US$1.5 billion (INR 96.1 billion) to charge its worldwide growth, Uber had committed to invest nearly US$400 million (INR 25.6 billion) to develop and stimulate its app-based cab services in India (Utkarsh, 2014).

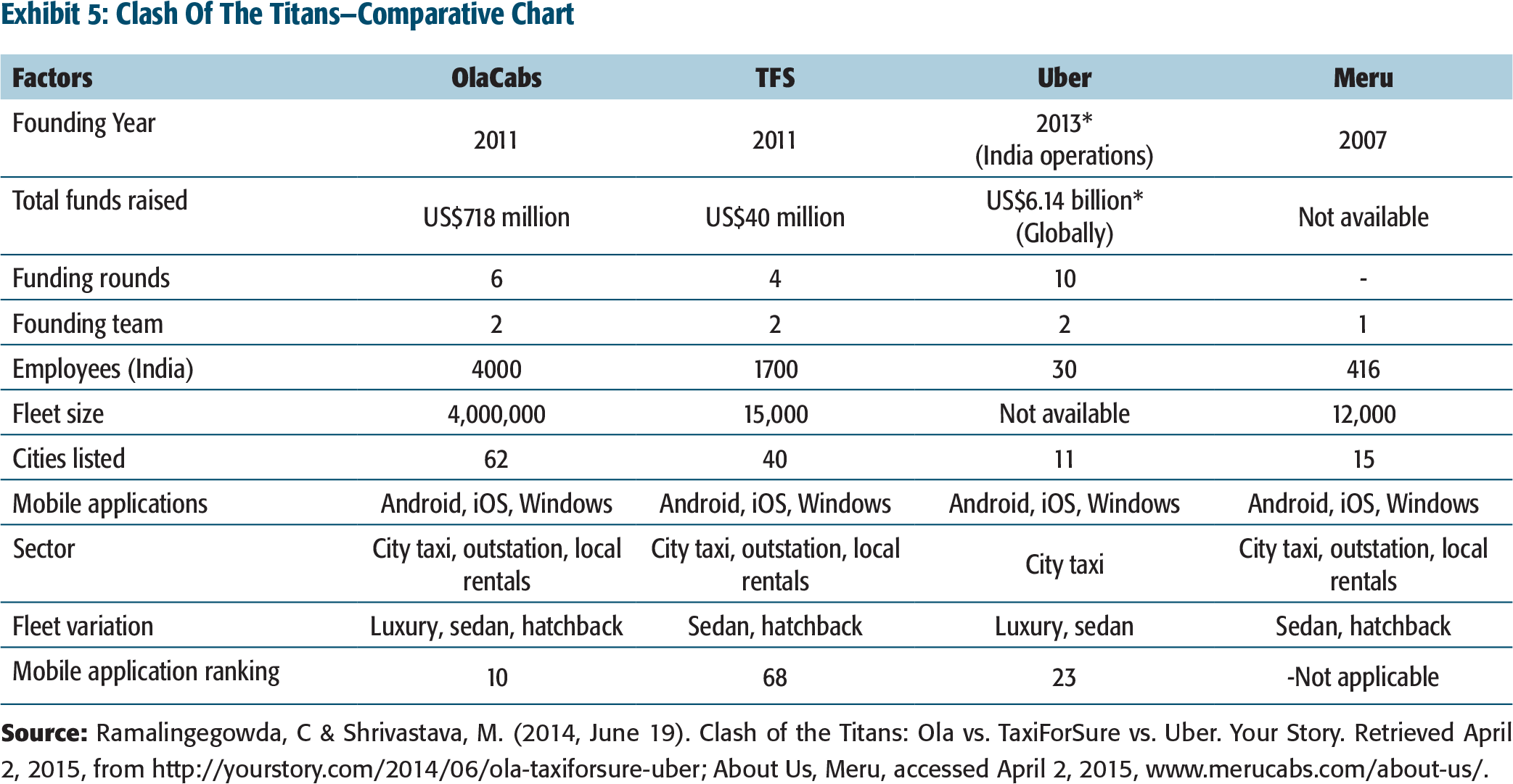

Refer Exhibit 5 for a comparative profile of four major players. The descriptions of Meru and Uber are as follows:

Meru

Meru, one of the earliest companies, was a pioneer in introducing ëmetered radio cabsí in India. Launched in Mumbai in April 2007, it grew at a rapid pace by acquiring a number of cars as well as spreading its geographical presence (Meru. n. d.). The company had a fleet of more than 6,000 cabs across seven cities. It was known for a hassle-free travel in a well-furnished, air-conditioned on-call taxi that was easily accessible 24/7. An electronic receipt after the journey assured the customers of genuine billing. By devising systems, processes and technologies, that provided a reliable interface, Meru focused on delivering consistent taxi services through multiple touch points (Meru. n. d.) The company achieved recognition by becoming the third largest ëradio taxiícompany in the world for undertaking more than 20,000 journeys per day (Meru. n. d.). In the financial year 2013ñ2014, Meru generated revenues of INR4.5 billion (US$70.95 million) and expected to touch INR6 billion (US$94.61 million) in the next year (PTI, 2014).

Uber

Clash Of The Titans—Comparative Chart

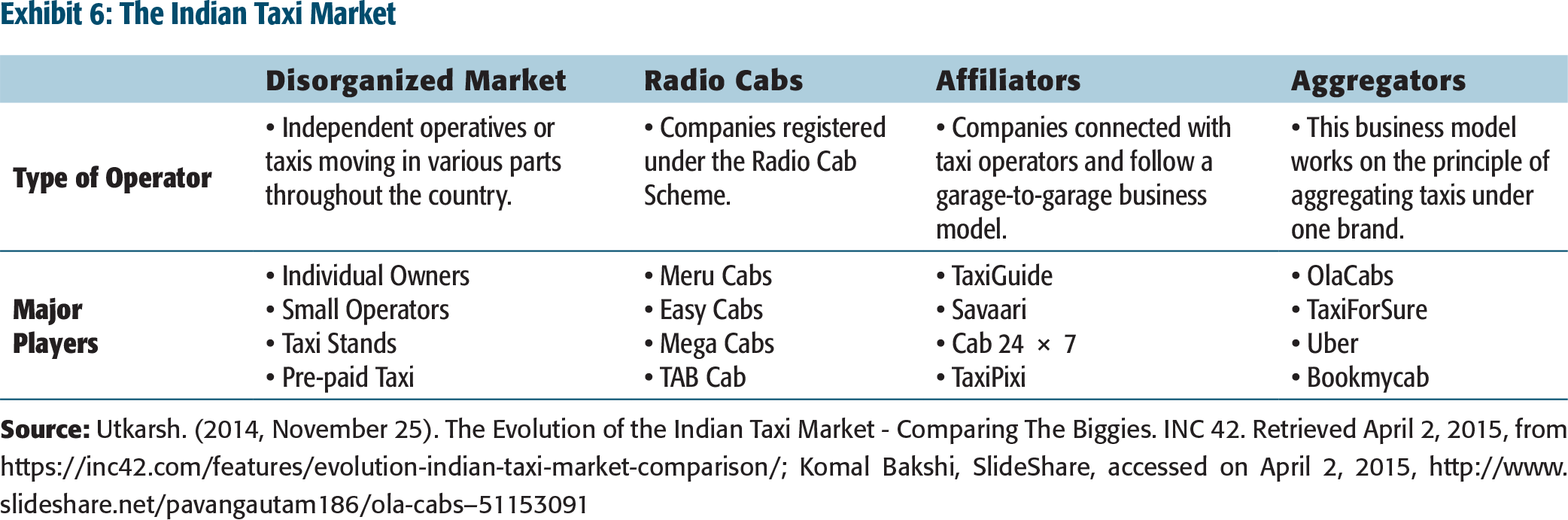

The Indian Taxi Market

BUSINESS MODEL OF THE AGGREGATORS

Contrary to a traditional taxi/cab rental companies that owned their cars, businesses based on an aggregator model such as Ola, TFS, and BookMyCab had adopted an asset-light model (see Exhibit 6). In the words of Avinash Gupta, co-founder of Mumbai-based BookMyCab, ëOwning cars is a very capital intensive business and difficult to scale beyond a point. The aggregator model is asset-light and therefore requires less capitalí (Knowledge@Wharton, 2013)

The aggregator maintained a system of associatesóeither chauffeurs who possessed and drove a solo car or cab operators who had a fleet of vehicles that were driven by chauffeurs. For communication and metering, each automobile in the aggregatorís system was fixed with a GPS device that was integrated with the companyís IT system (Knowledge@Wharton, 2013).

Uberís entry in India changed the game of the taxi business. It was no longer about getting most customers, but about getting more customers on the mobile phone. A study had found that booking a cab via mobile app costs 6 per cent lesser than via call centre. Ola and TFS followed the game (Shah, 2014).

THE TAKEOVER PROCESS

In August 2014, Ola reduced ride charges for Ola Mini by 25 per cent. This reduction in the tariff from INR13 (US$0.20) to INR10 (US$0.16) per kilometre made taxicabs more economical than travelling in an auto-rickshaw. For its sedan, the company reduced the tariff from INR16 (US$0.25) to INR13 (US$0.20) per kilometre. Ola carved a separate plan for its drivers. With a new weekly bonus system, drivers could earn as much as INR8,000 (US$125.73), if they made more than 30 trips in a week. Later, in September 2014, Ola modified its incentive system for drivers and gave incentives daily. Drivers completing five tours in a day got an additional amount of INR500 (US$7.86). The drivers received INR800 (US$12.57) and INR1,200 (US$18.86) for seven and ten trips, respectively. In this aggressive promotional spree, it also launched a new service known as Ola Wallet for its customers. Travellers received 100 per cent cashback on their first recharge.

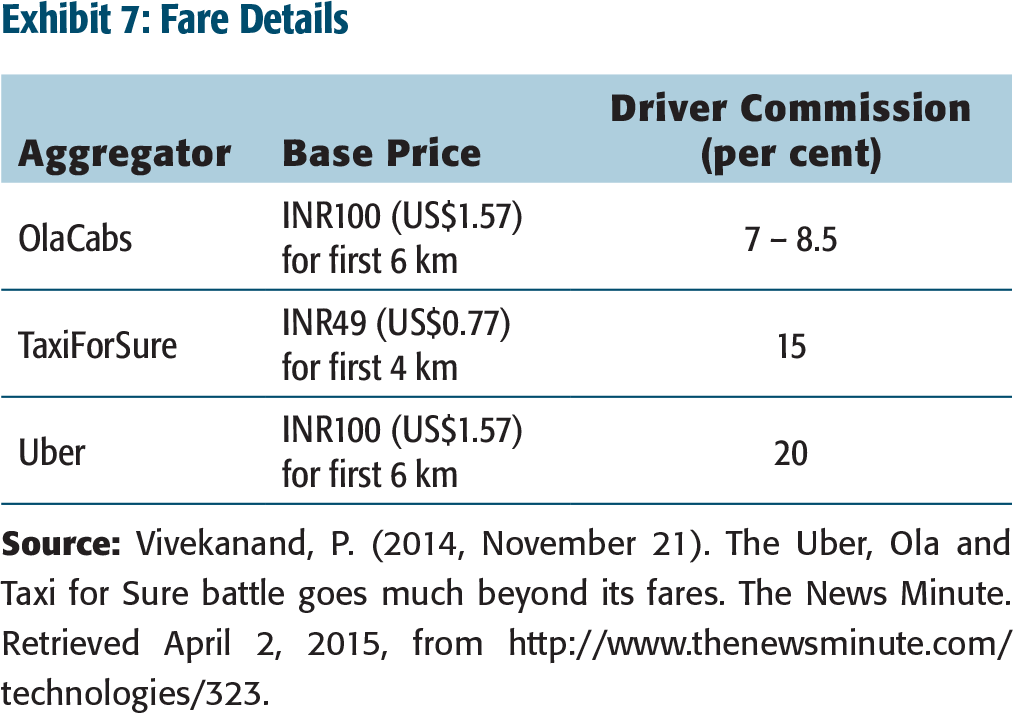

Fare Details

In the meanwhile, Ola had raised INR2.5 billion (US$39.42 million) in funding and was investing in getting more consumers and drivers on board. The founders of TFS took Olaís drastic fare reduction to be ëan aberration that would slowly come back to the groundí. With the backing of US$210 million raised from Japanís SoftBank in October 2014, Ola didnít step back and continued the aggressive price war.

To counter Olaís aggressive strategy, TFS had to raise money very quickly. In the world of start-ups, the larger the difference between two firms, the more difficult it is to raise capital for the smaller start-up. TFS was able to raise about US$50 million from Accel, Helion Venture Partners and Bessemer Venture Partners. Later, it received an additional capital of US$30 million in August 2014. With US$210 million in its hand, Ola had huge chances of outrunning TFS. But with US$8ñ10 million left in the bank, TFS needed big capital and had to enter the financial market to raise an additional round of funds. This time it needed a bigger amount.

With this goal, Raghunandan, co-founder, TFS left for USA in December 2014. Upon landing there, he came to know of an incident that had just taken place in Delhi. An Uber cab driver had molested a 26-year-old lady commuter. It had ominous consequences for the cab industry in India. Widespread anger led to the buzz that all radio cab aggregator companies would be barred from operating. Many Indian states were considering a ban. For investors, there was a dilemma as the regulation was a top priority. Any more investment in such precarious situation was beyond question. For TFS raising funds had become nearly impossible.

In January 2015, with a meagre amount of capital left, and no time, TFS was in trouble. It had less than US$2 million in hand, which would have lasted for another six weeks. On 10 January 2015, Accel Indiaís partners approached TFS founders with Olaís interest in the company. Anand Daniel, Partner in Accel India said, ëSo why donít you guys consider this? It is something we can explore.í

TFS was already in talks with Uber. However, the deal failed due to issues related to personnel at TFS. Globally, Uber had only 848 employees on its rolls, while TFS had 1,700 in India. Finalization of a deal with Uber would have led to 90 per cent of TFS staff losing their jobs. This was not acceptable to TFS founders.

On the other, Aggarwal, CEO Ola, agreed to the terms and ensured that none of the employees of TFS would lose their job. He also committed that Ola would continue to work with operators of TFS. Finally, Ola acquired TFS by paying INR12 billion (US$200 million) in cash and stock.

The nascent Indian taxi aggregation industry witnessed its first major consolidation on 2 March 2015.

THE DILEMMA

Immediately after the acquisition, Ola announced that TFS would operate as a separate entity and the brand would not be dissolved. According to Sumchit Anand, MD, Acquisory Consulting India,

The complete online industry was grounded heavily on marketing for the creation of brands and promotional activities. Therefore, the assessment of a firm when it gets acquired is not just for the business it does, but also for the brandís value. One of the main motives for firms to maintain the brand identity of the acquired firm under their aegis was to have the brand positioning intact. This would allow the parent company to gain dividends of hard work, resources and millions of dollars already spent on them. An added benefit of maintaining two separate profit and loss accounts could be that the acquiring company can keep a tab on how its acquisition is doing.

Immediately after the acquisition, Ola and TFS maintained the position that the two companies would continue to operate as individual entities. Analysts, however, were of the opinion that it would be more sensible for the companies to merge soon. As per Yugal Joshi, Practice Director, Everest Group, ëOla and TFS are doing more or less the same thing. So it would make most sense for them to merge as one entity.í

Industry experts also pointed out the issues, challenges and difficulties associated with the integration of the companies, particularly in the area of technical plug-ins of teams. Anand said, ëMaking an acquisition is easy but integration is a bigger challenge. There are cultural challenges and differences in ethos and even in go-to-market strategies. So, it is not easy to merge two young companies.í

THE ROAD AHEAD

This consolidation in an online taxi aggregation industry had varied implications for different stakeholdersóinvestors, customers, and competitors. For investors, it was good news as it offered an exit route for them in an industry that was years away from an initial public offer. The taxi market had enormous space for progression and unlikely to reach full capacity in the near future. Although there was a decent possibility for development in tier 2 cities, metros were still the primary market for all the taxi operators. This was expected to lead to more price wars and fleet variations.

To satisfy the price-conscious Indian consumers and to compete against other forms of public conveyance, more low-cost options were expected to be introduced. Already Ola Auto, Ola Nano and UberGo had been launched. Service guarantee and superiority, and accessibility were expected to materialize as the enduring differentiators. Sharing rides with other travellers was scheduled to happen in the next few years and reduce costs even more for the travellers as well as the cab companies. Few small ride-sharing start-ups such as PoolCircle, Zify, Ridingo, LetsRide and Rocket Internetís Tripda had already entered the market competing with the cab aggregators.

Expecting to sustain leadership in Indiaís online taxi aggregator market, Ola needed to re-strategize its orientation and operations. Also, needed were strategies for acquiring new customers, to amplify marketing efforts for both, and to achieve price parity if they sold common products on both sites. The core issue remainedówhether TFS should be merged into Ola or should it continue as a separate entity to cater to different market segments.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The author received no financial support for the research, authorship and/or publication of this article.