Abstract

Executive Summary

The study highlights the need for measures to accelerate the pace of the business correspondent (BC) model for financial inclusion in India. The financial analysis of the existing BCs with the existing products and services in practice shows a very diffusive break-even (more than 7 years). The occurrence of such a long-term break-even point can be a potential threat to the sustainability of new and struggling entrepreneurs like a Customer Service Point (CSP). A CSP agent runs a kiosk of a certain bank in a rural context, functioning like a BC between the bank and the beneficiaries. The primary investigation found that high cost and low volume of transaction at the CSP points are two major causes of the long break-even. In this context, the study revisited the constructs related to cost structure, market outreach, market potential and commission structure for channellizing respective banking and non-banking products. The major categories of products include (a) banking operation, (b) loan and over-draft, and (c) social security schemes. In search of a solution, the study adopts a non-random stratified sampling technique with a semi-structured interview process to collect the data from different stakeholders in the BC operation. To develop an economically viable BC model, the researchers use a standard financial modelling technique. In contrast to the existing kiosk model of CSP operation, the study found that while applying the new model a CSP agent takes three years to break-even under the same condition as that of the existing model. The study can also be applied in the domain of bottom of the pyramid (BOP) marketing by treating to create value among the low-income customers and business partners like CSPs. This research can further be extended to investigate the viability of the BC model from the banks’ return on investment perspective.

Access to finance by every section of the society is a prerequisite for achieving inclusive growth in any economy. The World Bank–Universal Financial Access (UFA) 2020 Overview (The World Bank, 2018) on financial exclusion depicts that India stands at 20.6 per cent of the world’s two billion unbanked population, followed by China (11.6%) and Pakistan (5.2%) in the Asian region. Further, the World Bank Findex (The World Bank, 2014) survey shows that out of 1.2 billion Indian population, only 53 per cent of Indians are financially included. To make progress in financial inclusion, historically, Indian banks have favoured expanding their number of brick-and-mortar branches over deploying branchless technology. The banks have relied on business correspondents (BCs; i.e., third party agents) to reach the unbanked population in remote and unbanked villages. In 2006, the Reserve Bank of India (RBI) devised the BC model (Basu, 2006). The model not only aims to provide an alternative banking channel to millions by making financial services accessible for the un-/underbanked population through a branchless banking facility but also supports the national agenda for employment generation (RBI, 2008). The corporate BCs (also known as the BC network managers [BCNM]) act as a middleman and distribute the banking products with the help of multiple Customer Service Points (CSPs) or commonly referred to as agents or Bank Mitras. These Bank Mitras are the micro- or nano-level entrepreneurs, usually small shop owners or freelancers in the rural and semi-urban areas. The CSP agents act as the retailing points for delivering the banking services at locations other than a bank branch or ATM. The CSP agents are enabled to provide a defined range of banking services at low cost, hence are instrumental in promoting financial inclusion (Mehrotra, Tiwari, Karthick, Khanna, & Khanna, 2018). As an opportunity, most of the CSP agents join this BC banking business to supplement their existing income.

The banking products for financial inclusion offer the Bank Mitras a reasonable return on their investment; and there are 1.26 lakh Bank Mitras delivering branchless banking services in different Sub Service Areas (SSA; PMJDY, 2019). An SSA consists of three to four villages having combined average population of 1,600 to 1,800 (SLBC, 2019). Besides, as on November 2019, the progress of such a huge network of branchless banking using the CSPs or the Bank Mitra network in rural India reports that there are 37.55 crore beneficiaries banked having ₹107,172.54 crore balance in their accounts (PMJDY, 2019). Moreover, the latest available data on the number of bank branches in rural areas shows an increase from 28,583 in March 2011 to 48,834 in March 2019 (RBI, 2019); while the number of branchless banking outlets (including ATMs) in rural India has risen from 34,316 in March 2010 to 547,233 and 518,742 in March 2017 and 2018, respectively (RBI, 2018, Table IV.25, p. 80). Such progress shows an impressive outreach of banking services through branchless banking.

However, the growth rate represented in these numbers do not take into account the number of CSP agents who are dormant (Kale, 2016). Moreover, a study conducted by Mehrotra et al. (2018) found that while the banking industry is employing more agents, customer growth is slowing down. One of the possible reasons could be the rise of over-the-counter (OTC) remittance transactions. It also indicates that the CSP agents are not able to generate enough customer registration or transactions. The results have a direct effect on the CSP agent return on investment and profitability. Besides, the CSP agents face a wide range of issues and challenges with respect to the product they offer, kiosk costing (fixed and operational), liquidity management, inadequate support from the banks, small profit margin, financing for working capital management, technology-related issues, marketing and communications, customer dissonance and service, low profit margin, etc. In this context, it is important to note that if the CSP agents earn more from the prior business than from the existing BC model operation, then he/she would be unwilling to commit more time since it is less profitable. While the operational process of the CSP agents holds potential, research indicates that the policy has not taken off in the way it was envisioned (ACCESS, 2014; Basu, 2006; Bhanot, Bapat, & Bera, 2012; Bihari, 2011; Kapoor, 2014; R. Pal & R. Pal, 2012; Singh et al., 2014). As a result, both the supply side (e.g., banks) as well as the demand side (e.g., beneficiaries) are struggling for smooth operational efficiency of the financial inclusion drive. Different studies envisage that the existing BC guidelines do allow just enough space for the improvement as well as a possibility for bringing a sustainable business model for the BC agents (R. Pal & R. Pal, 2012; RBI, 2015a, 2015b). Based on the multiple issues and challenges with the BC model of business operation, the study raises the research questions: Is the BC model of financial inclusion financially sustainable? Is there any scope of making the model more sustainable?

BANKING INDUSTRY AND FINANCIAL INCLUSION IN INDIA AT A GLANCE

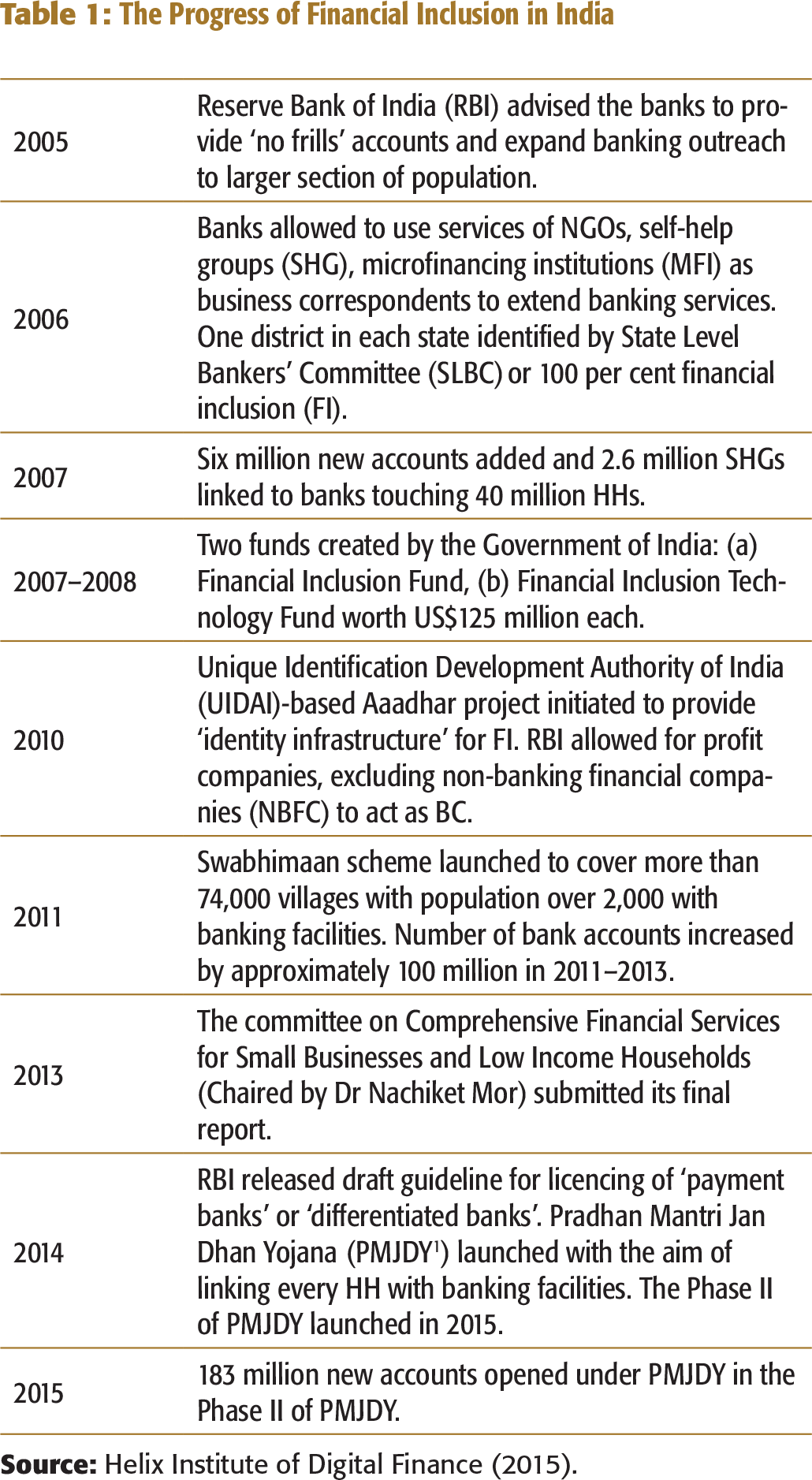

The Progress of Financial Inclusion in India

THE BUSINESS CORRESPONDENT MODEL IN INDIA

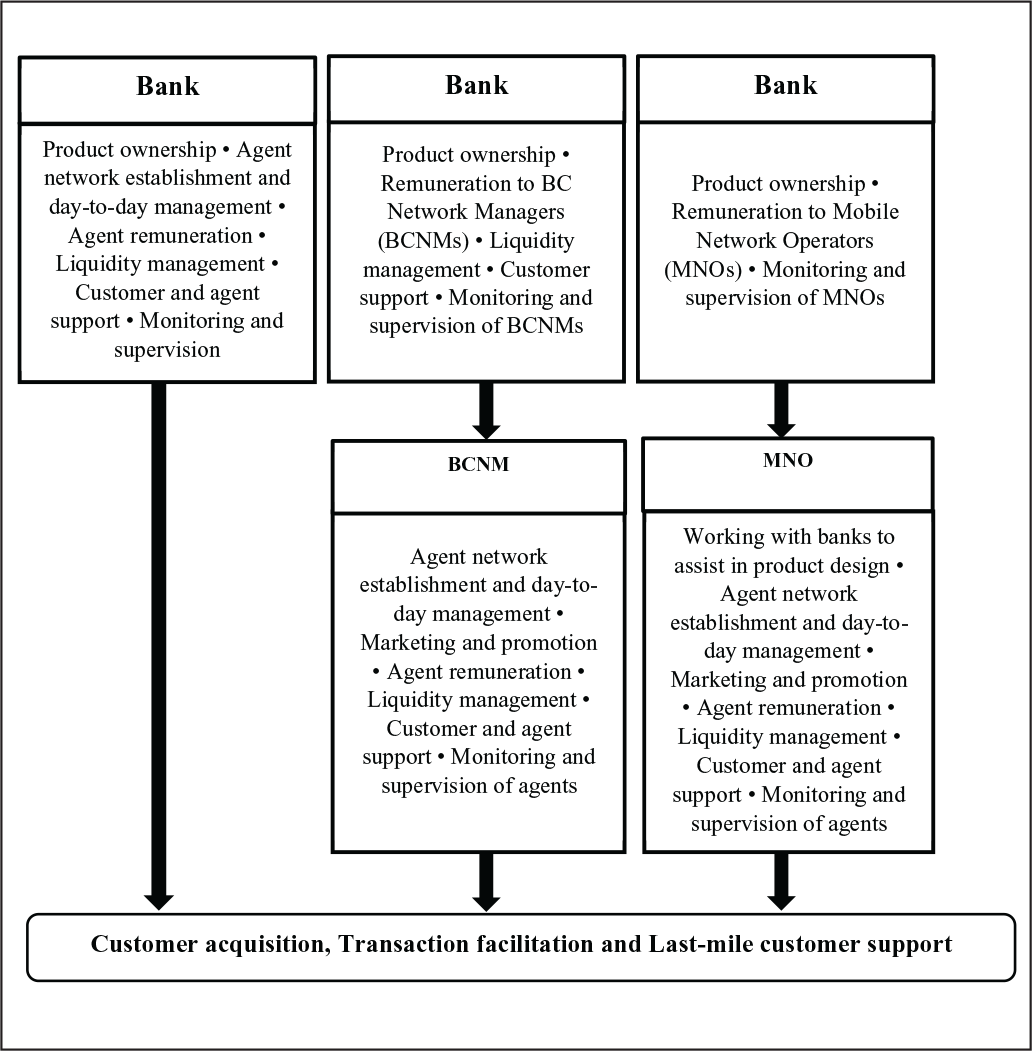

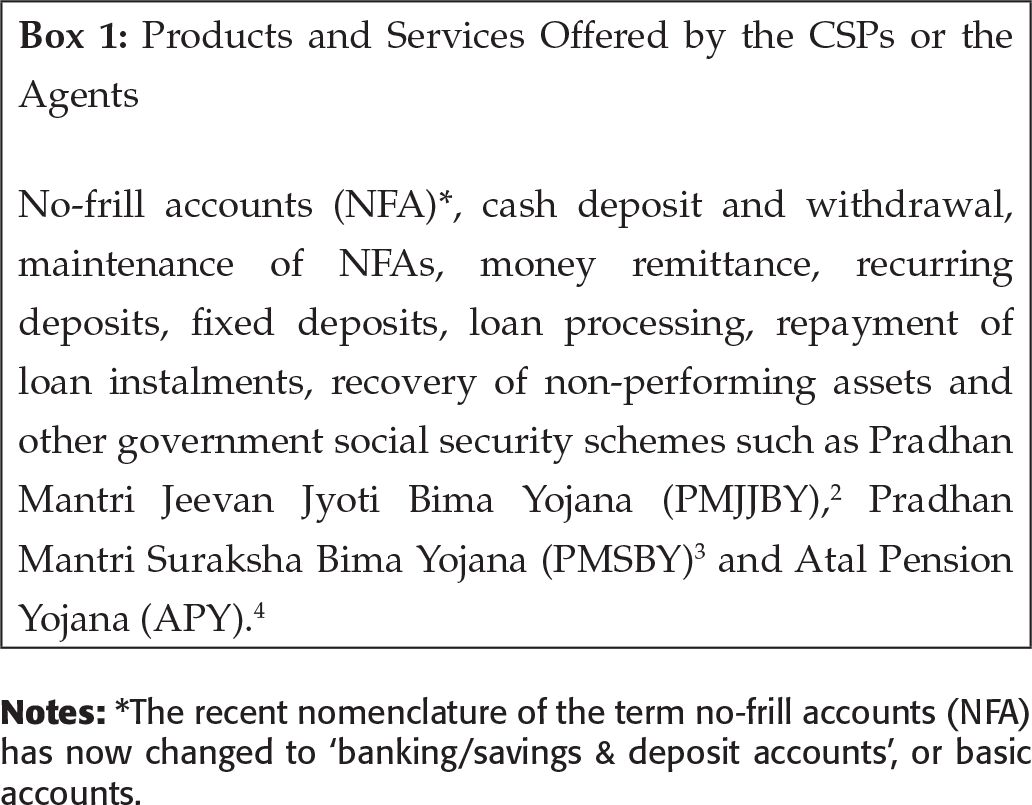

The BC model of financial inclusion depends upon the success of the CSP agents who are micro-level entrepreneurs. The study uses the Organisation for Economic Co-operation and Development (OECD) definition: Business with zero to nine employees are regarded as micro-enterprises (OECD, 2005, 2017). The micro-entrepreneurs distinguish themselves from larger small and medium enterprises (SMEs) through a deficiency of capacities such as networking, marketing, business planning, human resource and the use of IT. The deficiencies become the main hindrances to micro-entrepreneurs at all stages of development (Barnes et al., 2012; Brush, Ceru, & Blackburn, 2009; Foreman-Peck, Makepeace, & Morgan, 2011; Gherhes, Williams, Vorley, & Vasconcelos, 2016; Greenbank, 2001). The agents act as the retail point for the banks by providing banking services at locations other than a bank branch or ATM. Figure 1 and Box 1 depict an outline of three different financial inclusion model and different products and services offered by the CSPs respectively. All the three models are self-explanatory and define the roles and responsibility of the respective stakeholders.

Financial Inclusion Models in India

Products and Services Offered by the CSPs or the Agents

While statistically, the progress of financial inclusion is impressive, there has been criticism emanating from various quarters that the scheme is not delivering what it was intended to (Mukhopadhyay, 2016). Many of the CSP agents are unmotivated due to compensation schemes and lack of support from the upper channels like the banks and the BC network managers for their business viability. The effectiveness of the BC model as a channel interface between bankers and beneficiaries needs to be addressed. The study has been designed taking into consideration the background of the financial inclusion plan in India. Therefore, the aim of the study is

To investigate the business sustainability of the BC model of financial inclusion To propose a financial model for the BC agents based on commission and incentive structure of banks products

METHODOLOGY

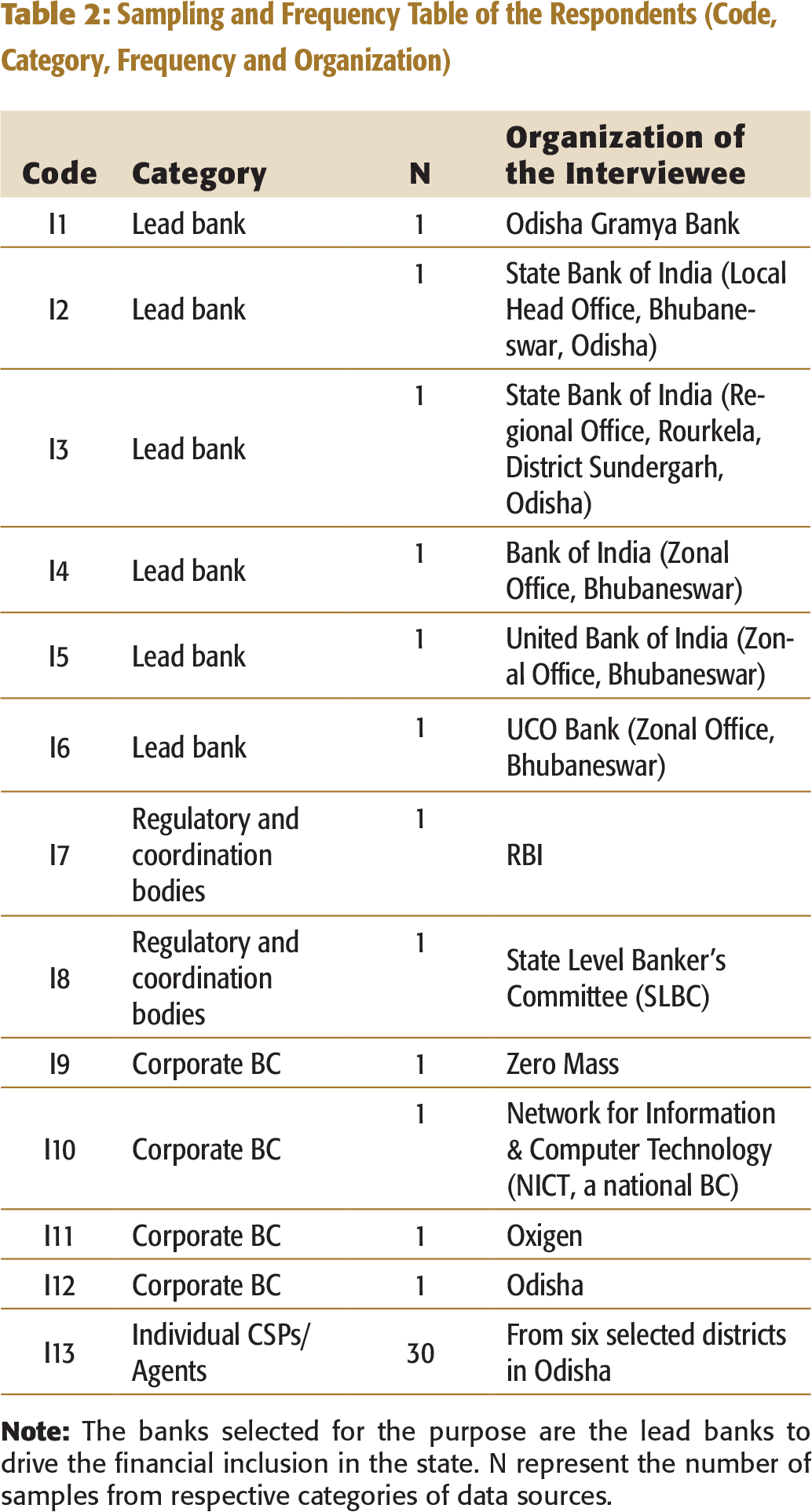

To realize the objectives, the study considers four different strata of respondents, which includes scheduled commercial banks with a lead bank 5

Lead bank: The RBI introduced the ‘Lead Bank Scheme’ towards the end of 1969. To enable banks to assume their lead role, effective and systematic manner, all districts in the country, except the metropolitan cities of India, were allotted among the public sector banks and a few private sector banks. The lead bank role is to act as a consortium leader for co-ordinating the efforts of all credit institutions in each of the allotted districts for expansion of branch banking facilities and for meeting the credit needs of the rural economy. Retrieved from https://rbi.org.in/Scripts/BS_ViewMasCirculardetails.aspx?id=9077

Sampling and Frequency Table of the Respondents (Code, Category, Frequency and Organization)

Based on the field coverage, the strata constitute six lead banks, two regulatory and coordination bodies, four corporate BCs and 30 CSPs or agents. The CSP agents are recruited from six districts of Odisha. The study adopts the random sampling approach for selecting the districts and the CSP agents. Regarding the nature of the samples, except the CSP agents, all the respondents belonged to the senior and middle management of the aforementioned stakeholders. The agents ran a CSP business either through the channel of corporate BCs or were directly appointed by the banks. The data was collected over a period of two months in May and June 2016.

DATA COLLECTION

The two objectives of the study indicate their existence with two broad categories of stakeholders. The first category links to the agents who retail the banking products and services to the end users. The second category is a list of stakeholders that are directly or indirectly involved in the decision-making process. Hence, two different sets of questionnaires were designed to extract comprehensive information from the respondents. The data were collected using a semi-structured questionnaire in a face-to-face interview. The typical profile of the respondents in the second category was that of an individual, more than 40 years old, with a banking and regulating experience in the range of 10 to 20 years and an average five years of experience in managing the financial inclusion division in their respective institutions. On the other hand, the typical first category respondents (the CSP agents) belonged to the 30- to 40-year age group, had a minimum qualification of 10+2 and a majority of them were graduates with an experience in the range of 4–8 years in the financial inclusion (FI) retail operation.

FINANCIAL MODELLING: STUDYING THE ECONOMIC VIABILITY OF THE CSPs OR THE AGENTS

Different CSP Agent Models

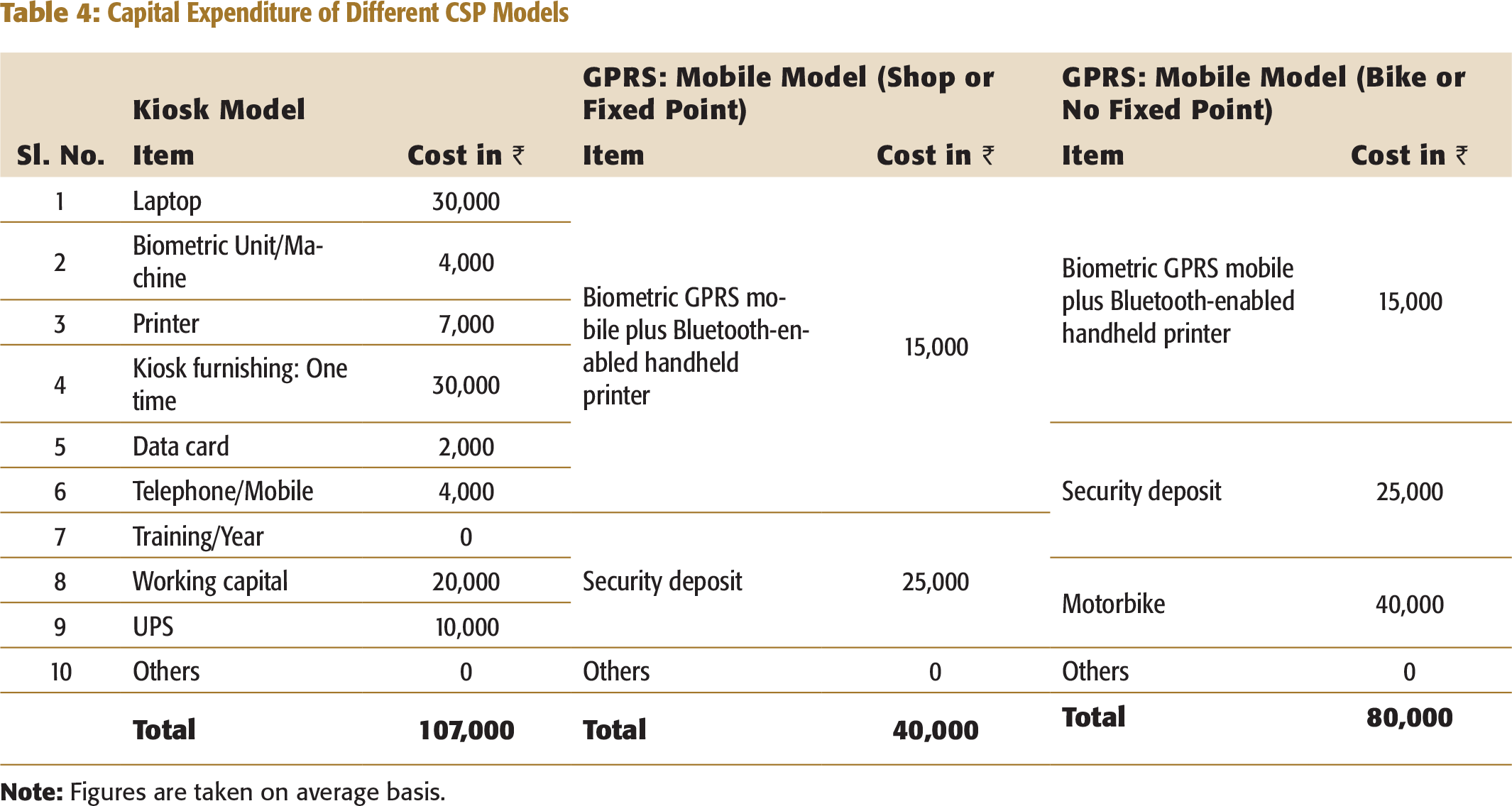

Capital Expenditure of Different CSP Models

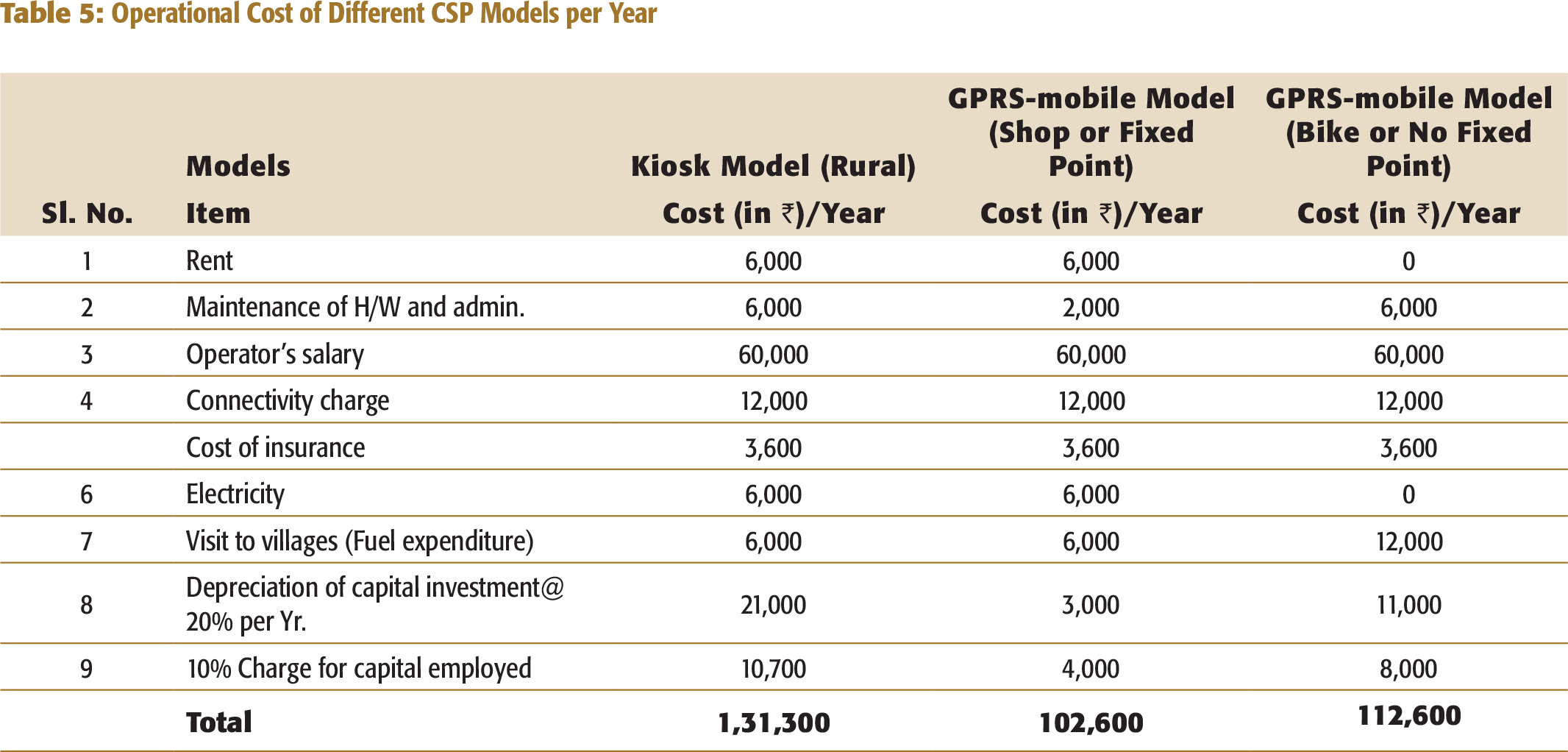

Operational Cost of Different CSP Models per Year

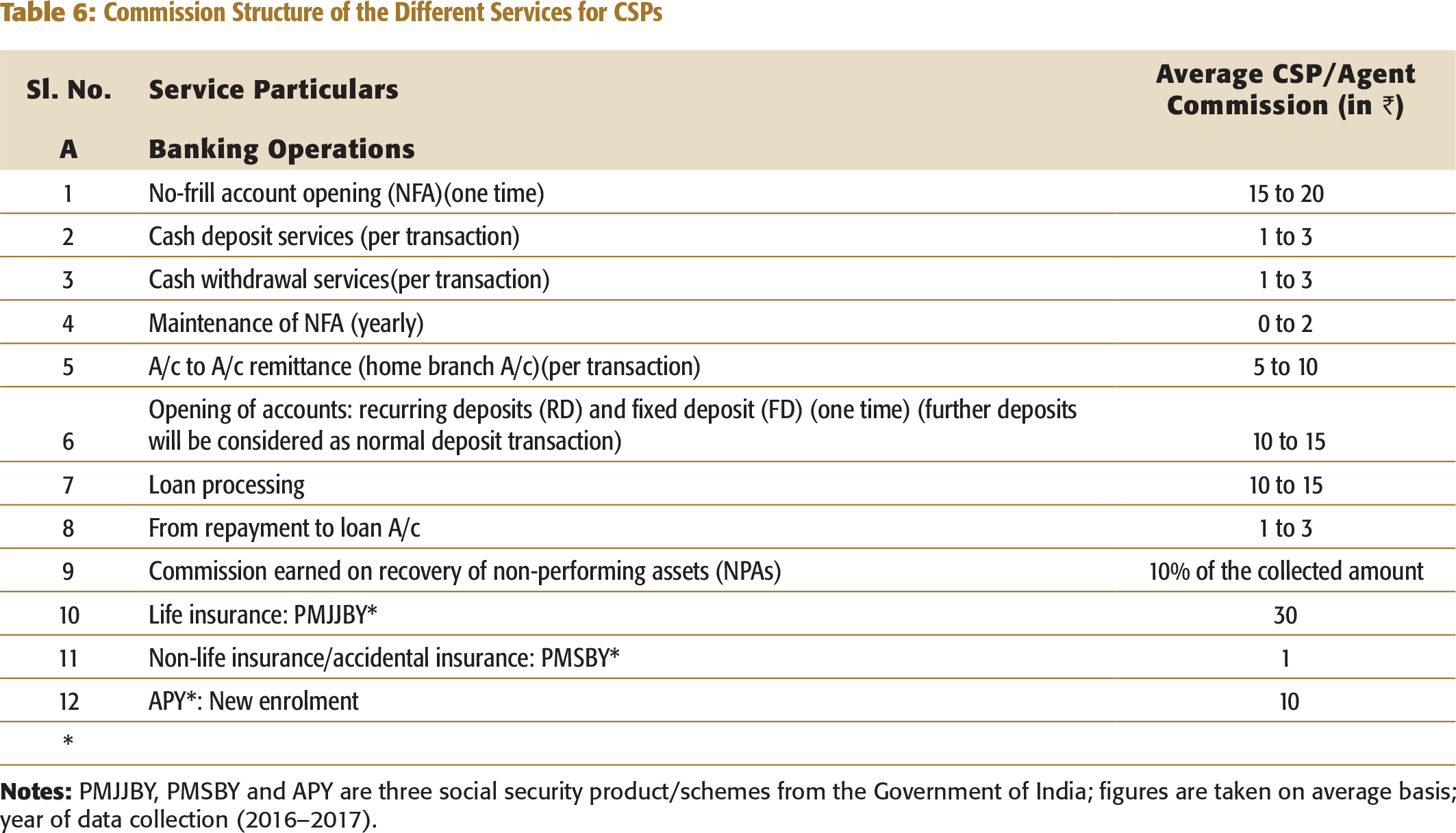

Commission Structure of the Different Services for CSPs

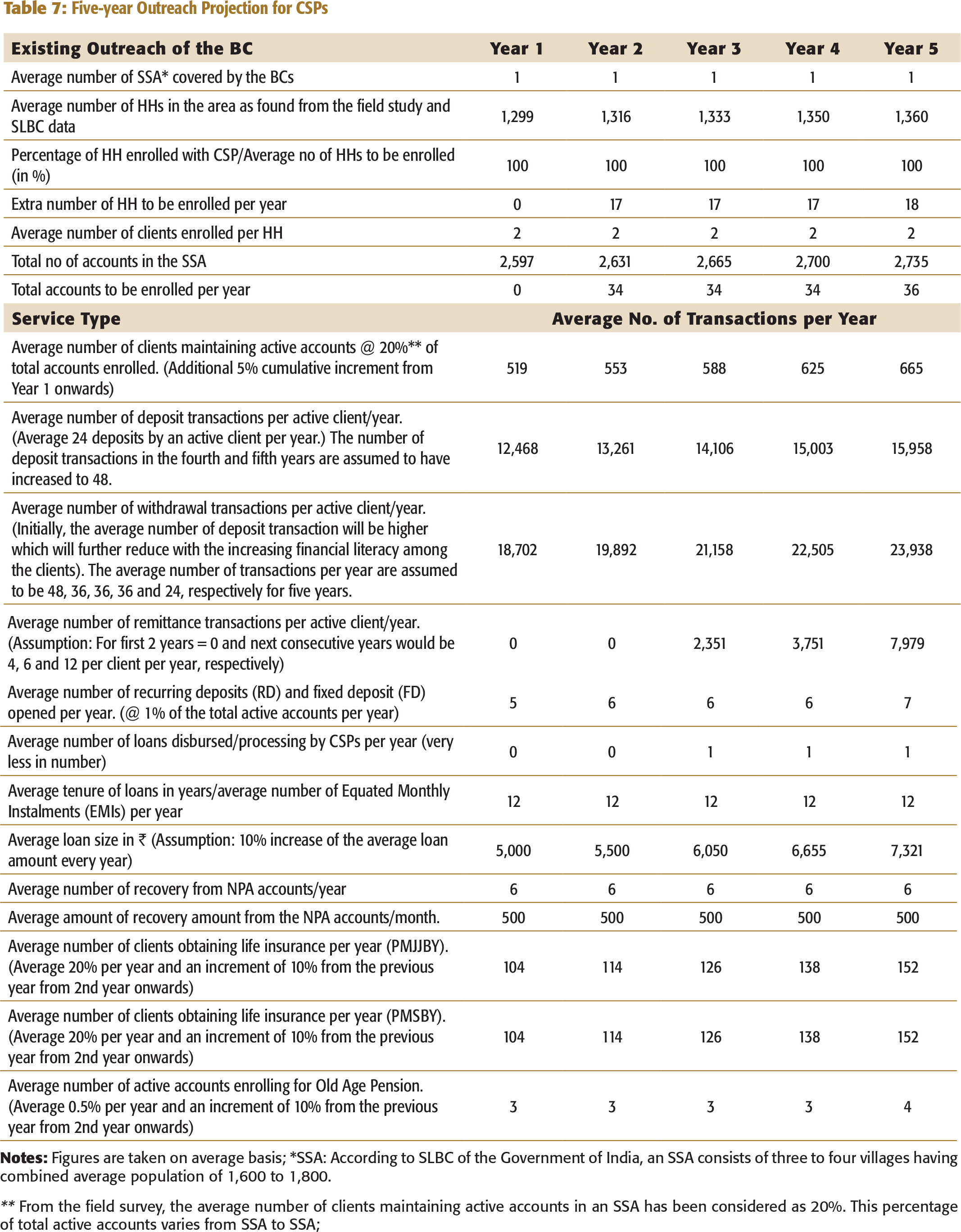

Five-year Outreach Projection for CSPs

** From the field survey, the average number of clients maintaining active accounts in an SSA has been considered as 20%. This percentage of total active accounts varies from SSA to SSA;

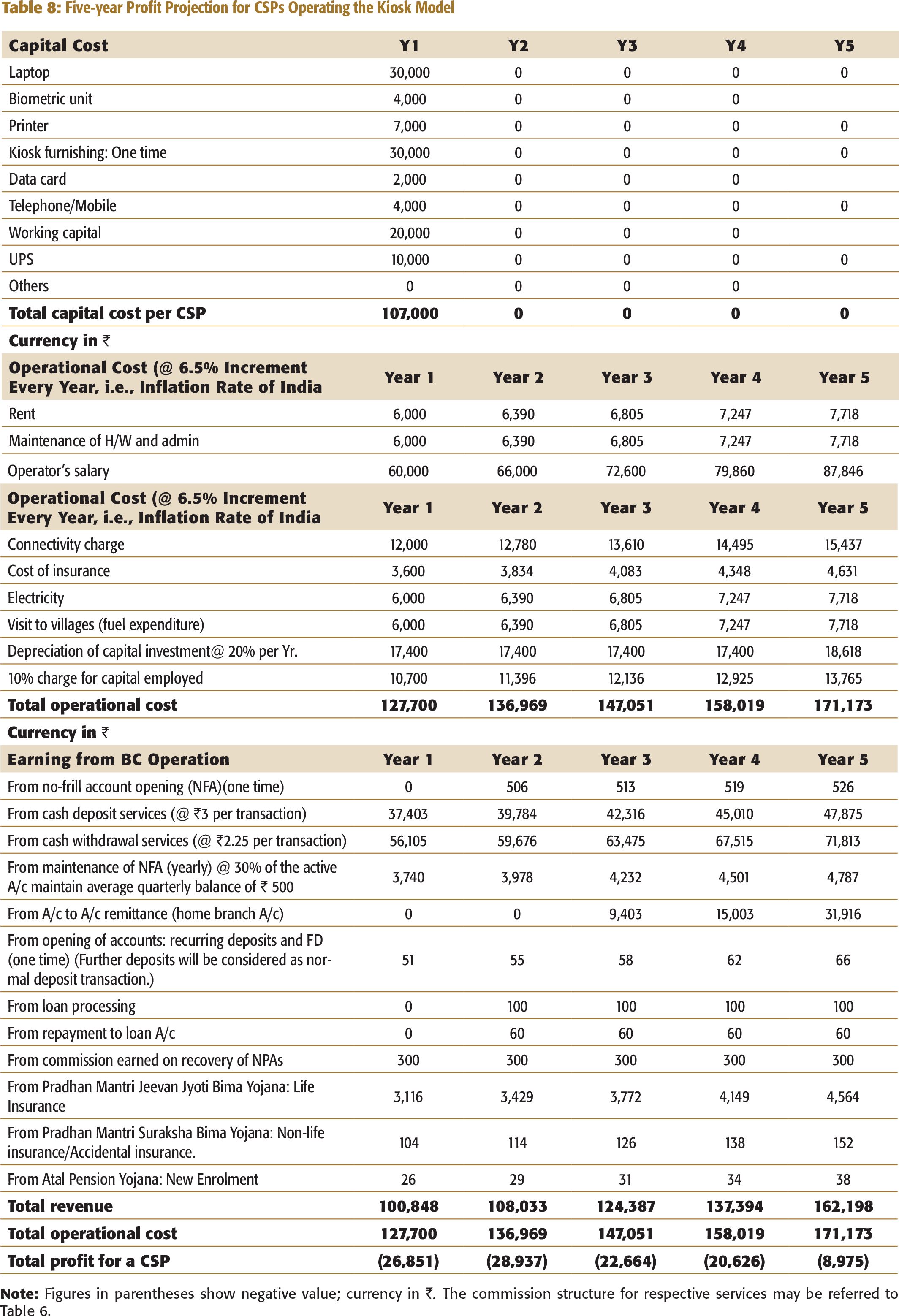

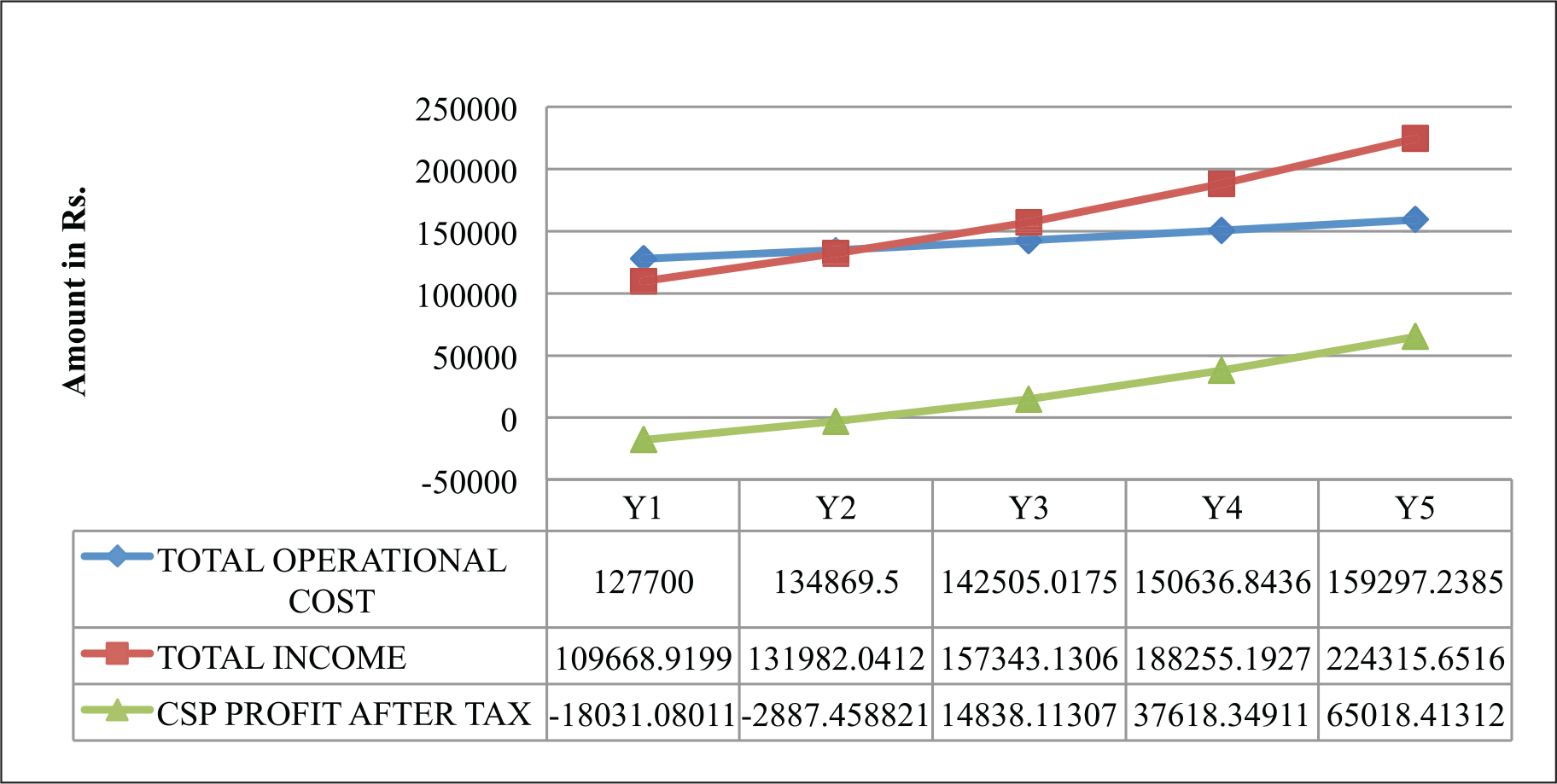

Five-year Profit Projection for CSPs Operating the Kiosk Model

Observations of the Existing BC Model Implemented by the Banks

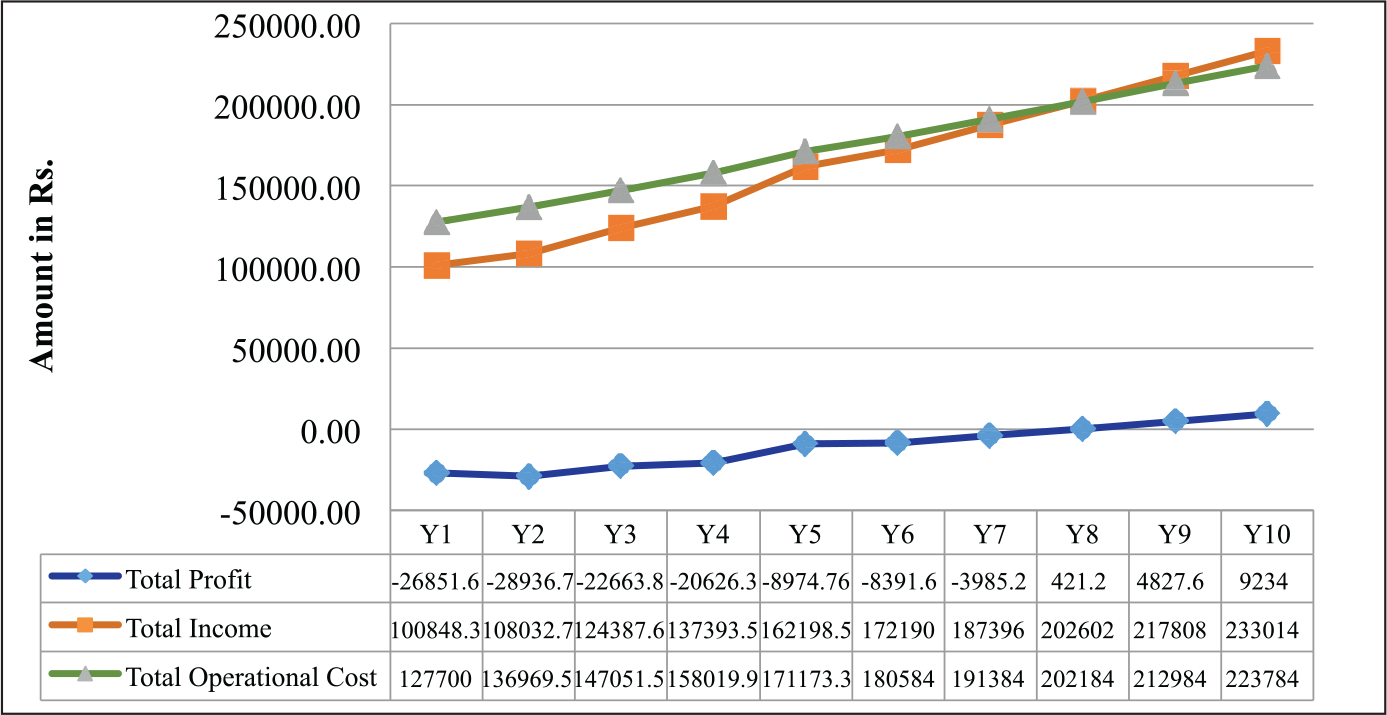

Figure 2 depicts a 10-year projection, which indicates that the CSP agents achieve their break-even point after the 7th year of business operation. The break-even has been calculated on the basis of average active accounts present in an SSA, containing 1,299 (average) number of HHs and 2,597 number of NFAs. While majority of the NFA accounts are found to be dormant, an average 20 per cent (as per the outcome of the discussion with different stakeholders) of the total NFAs in an SSA has been found to be active. This 20 per cent equals to 519 number of active accounts from a single SSA with an average of 2,597 NFAs. From the empirical data, as collected from different stakeholders, very limited banking products are offered through the CSP agents in Odisha as a part of their existing operation. Moreover, the most common services availed by the beneficiaries via the BC mode of operation are limited to only deposits, withdrawal and a few remittance services. Whereas other enlisted services with a CSP such as recovery of non-performing assets (NPA), recurring deposits, fixed deposits (short and long term), loan processing and microloan deposits are given less attention. Therefore, the present activity of the CSP agents does not result in recovery of investment made upfront.

By comparing the kiosk model with other BC models of operation, both the capital and operation cost in case of kiosk model is on the higher side (refer to Tables 4 and 5). However, because of the security and fixed-point accessibility of the CSPs, the kiosk model is popular with banks as well as the beneficiaries. However, the study estimates that in a typical rural scenario, the CSP agents, who handle an SSA, with a population of 1,600 to 1,800 receive Rs. 2,000 after meeting the obligatory expenses towards travel to the base branch, cost of electricity and connectivity, and other variable costs. This low-income perspective of the existing kiosk model at a high fixed, as well as operational cost, leads to lack of interest and motivation among the personnel handling the CSPs. Hence, there is an imperative need for the development of a new model where a CSP agent can optimize the investment. At the same time, the model should be productive for both the banks as well as the beneficiaries on a long-term basis with a minimum fixed income.

PROPOSED MODEL

In the proposed model for BCs operating the kiosk model, following assumptions have been made, taking into consideration the data collected from different stakeholders.

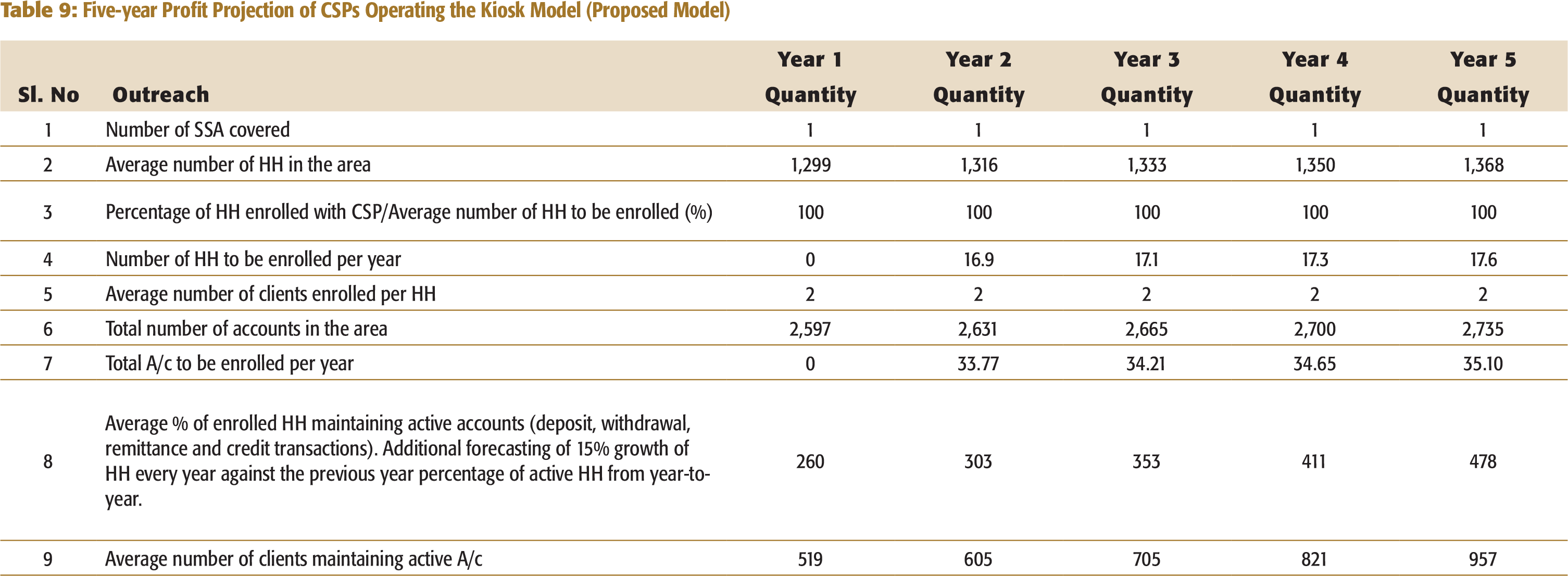

Average percentage of active clients is the same, that is, 20 per cent. Additional forecasting of 15 per cent growth of HH numbers every year against the previous year percentage of active HH from year to year. The capital and variable cost remain the same for both the existing practice and the proposed model of practice. The width of product range has been increased from the existing product basket in the kiosk model. The commission structure for different products is taken on its average, based on the data collected during the field survey. The proposed model can vary depending upon the users’ preference for decision-making by putting different data such as percentage of enrolling active accounts, commission structure, and cost structure for fixed and variable cost.

Five-year Profit Projection of CSPs Operating the Kiosk Model (Proposed Model)

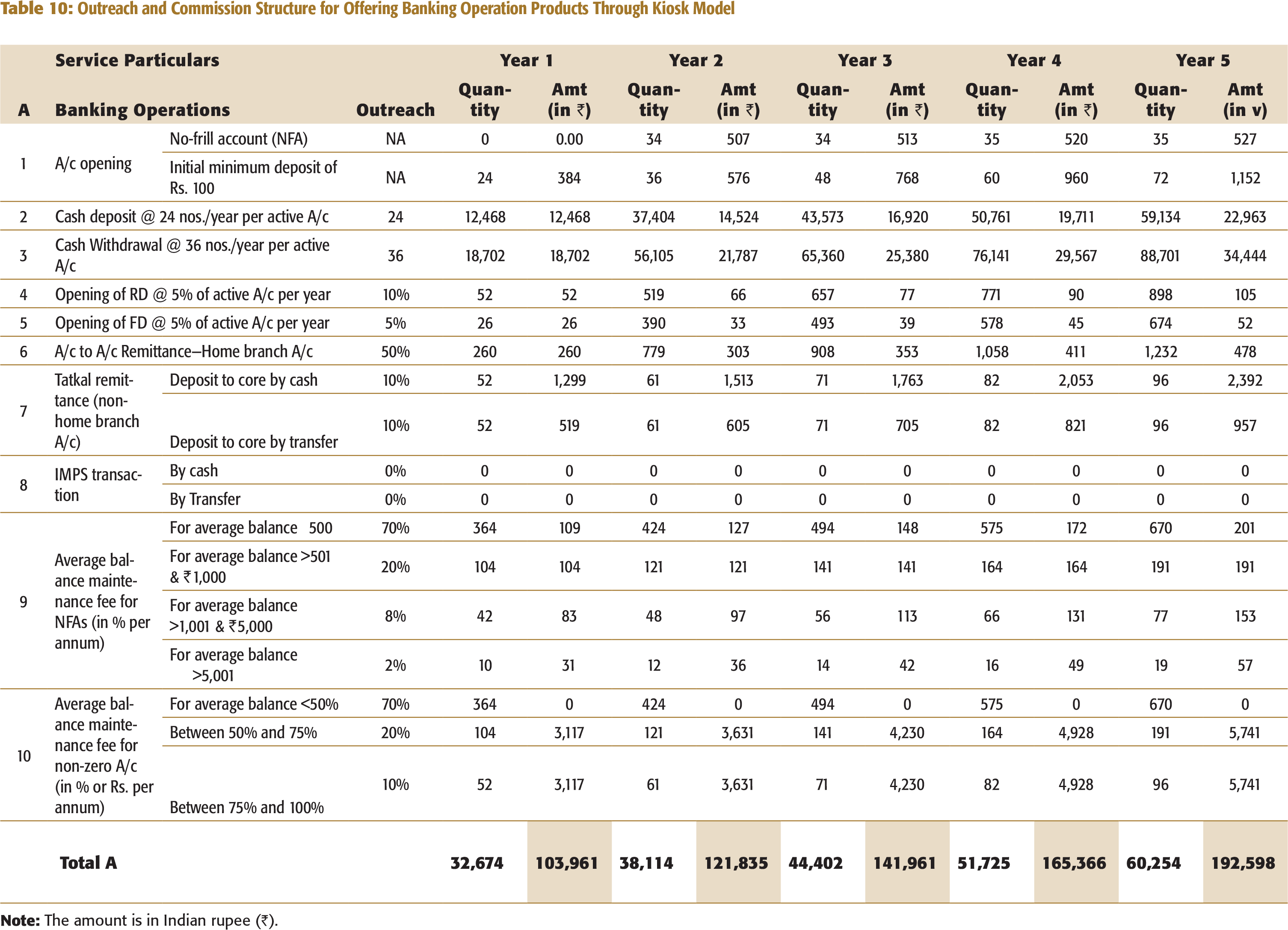

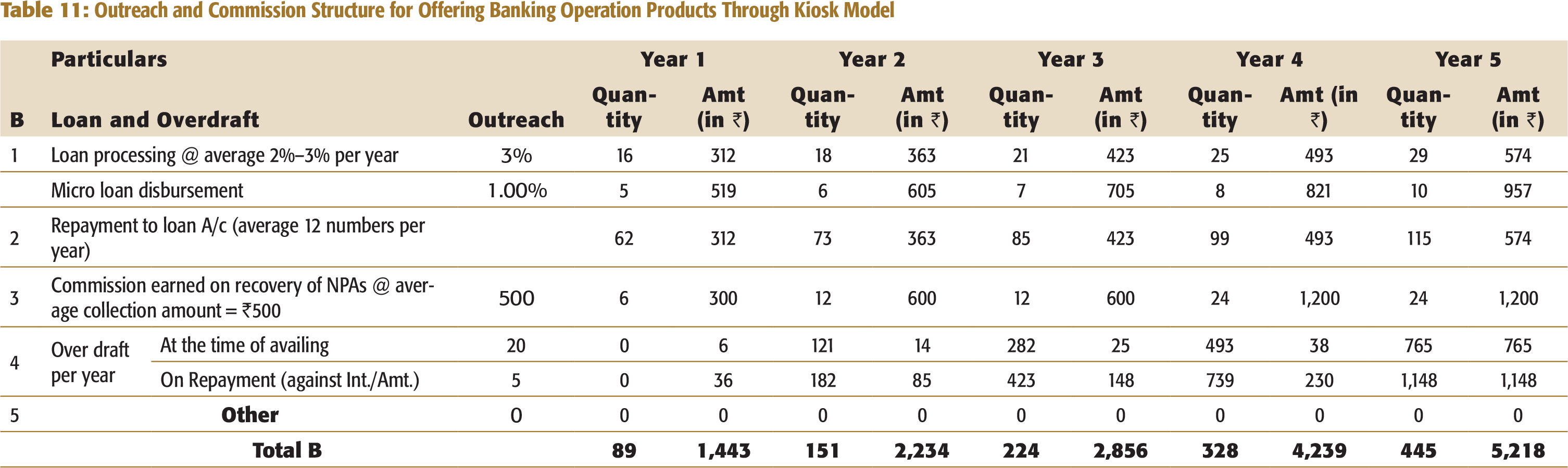

Outreach and Commission Structure for Offering Banking Operation Products Through Kiosk Model

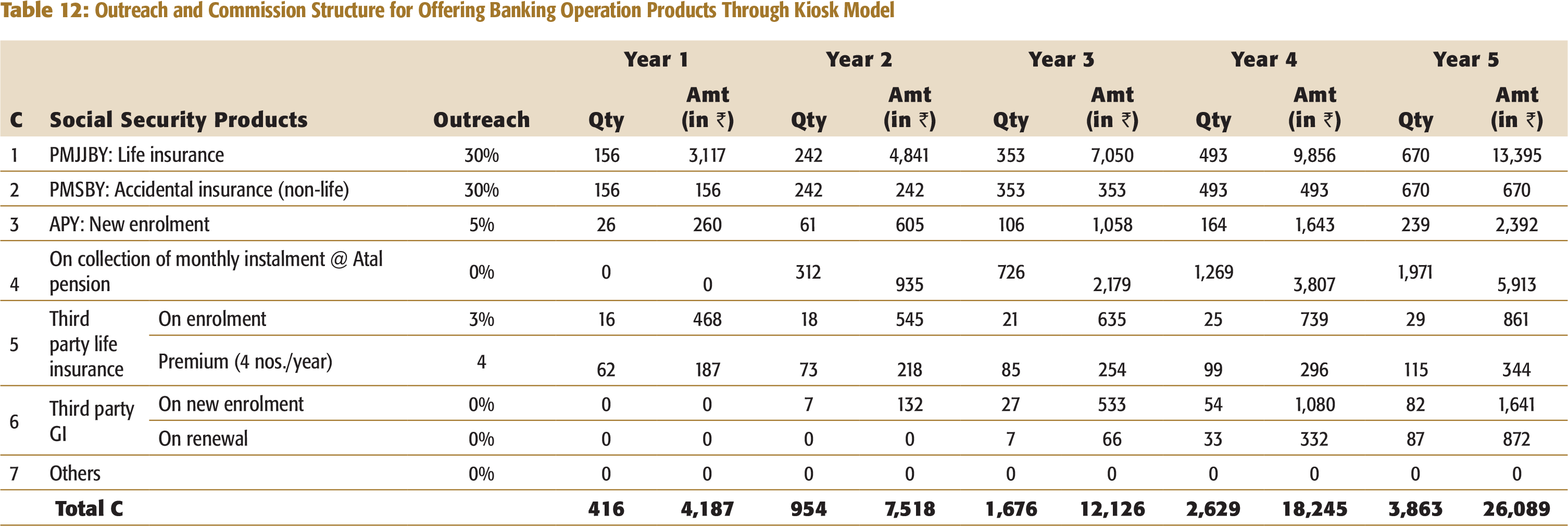

Outreach and Commission Structure for Offering Banking Operation Products Through Kiosk Model

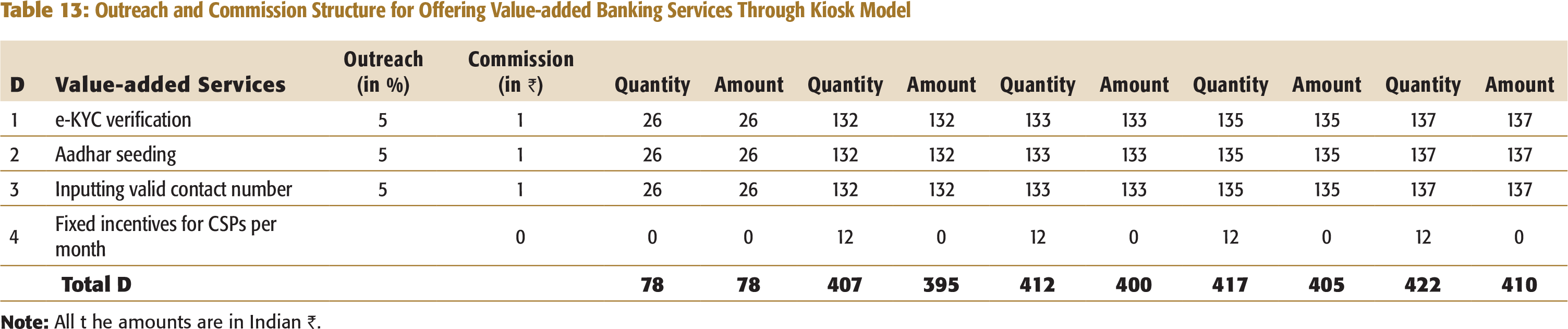

Outreach and Commission Structure for Offering Banking Operation Products Through Kiosk Model

Outreach and Commission Structure for Offering Value-added Banking Services Through Kiosk Model

Year-wise Income Analysis

FINDINGS AND RECOMMENDATIONS

Broadly, the findings from the study show that the commercial viability of the BC model from the CSP agent perspective pose a serious challenge with a threat to its very existence. At present, most of the agents operate in rural areas and struggle to generate the volume of business as well as profitability for their existence. As revealed by the outcome of the existing model as shown in Table 8 and Figure 2, a CSP agent can achieve its break-even only after seven years through the existing kiosk model of operation. The major challenges in the kiosk model are the high cost and low volume of transaction.

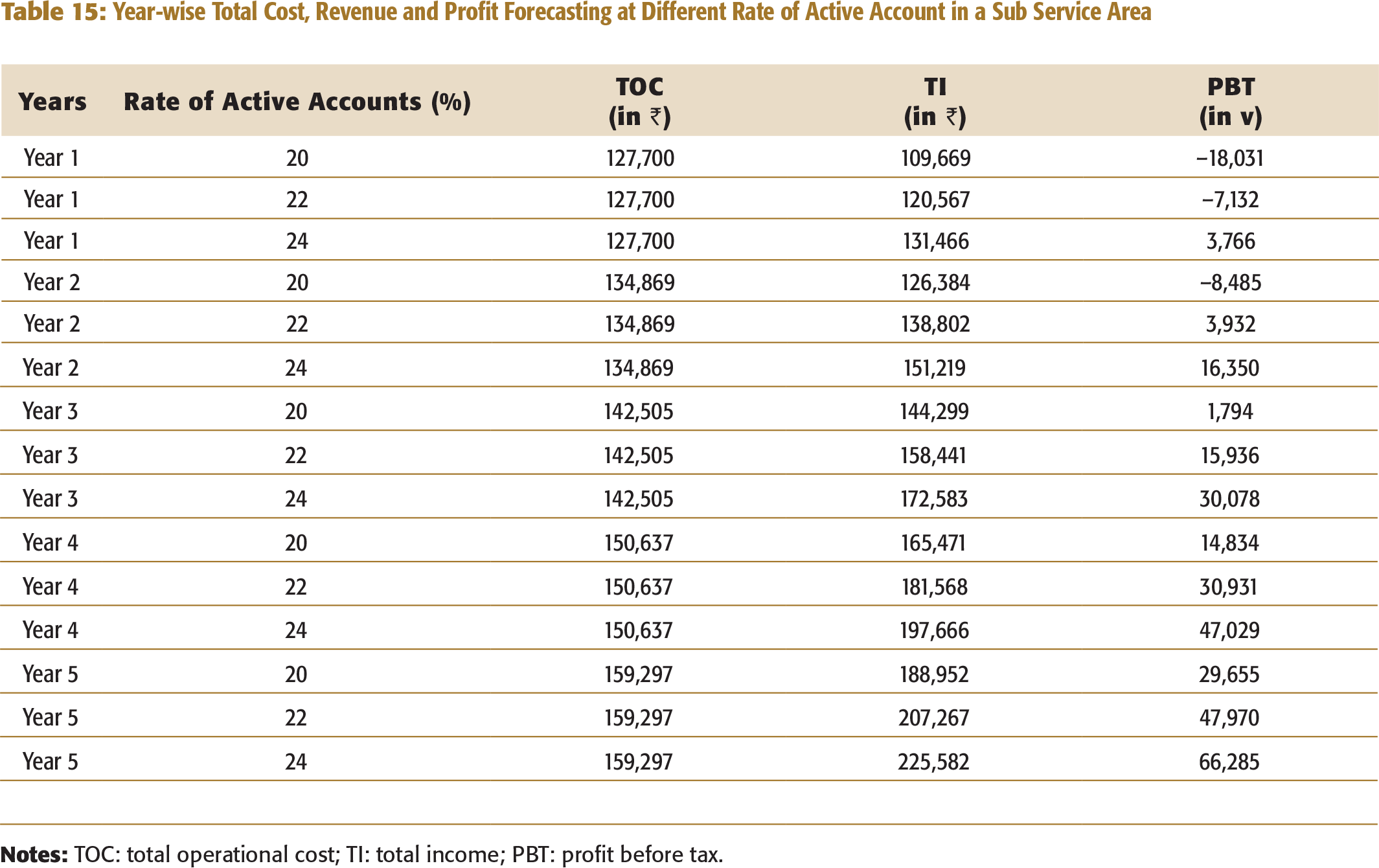

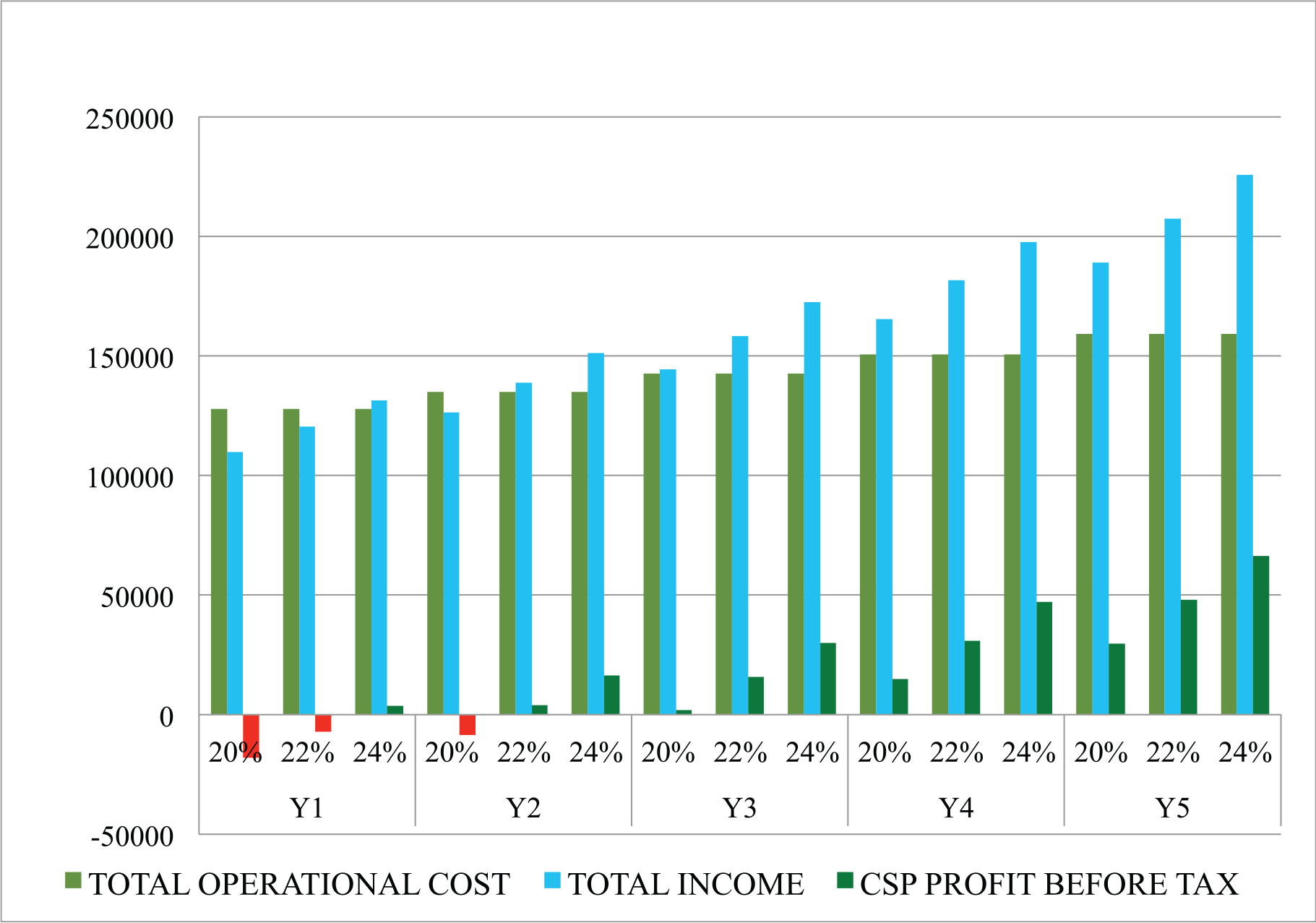

In contrast to the existing kiosk model of CSP operation—the proposed model and as depicted in Tables 9–14 and Figures 3 and 4—a CSP agent takes three years to break-even under the same condition as that of the existing model. This achievement in the proposed model is due to the increase in the product range and the outreach plan for each CSP therefore addressing the volume of transactions issue, which further contribute to the economies of scale. Moreover, as shown in Table 15, the break-even can be achieved even in the first year of the inception of the CSP when the active account coverage is increased to 24 per cent. Regarding the income-sharing pattern among the bank, corporate BC and the CSP agent, the bank normally retains 10 per cent to 20 per cent of the charges collected from the customers. The bank shares the remaining with the corporate BC. The cost of BC operation has three major components such as payment to CSP agents, the cost of technology and supervisory/managerial cost. The corporate BC usually pays 60 per cent to 75 per cent of its earning to its CSP agents. Therefore, the earnings of the CSP agents depend upon the volume of business and transaction with the beneficiaries at the designated SSAs. Therefore, until the BC model builds up enough volume such as active accounts and the number of transactions, the CSP agents in rural areas would continue to lose money, for example, more than seven years to meet the break-even (refer to Figure 2). Therefore, the challenge before the system is to keep the CSPs active until they achieve financial viability. The study identified the CSP as the weakest, as well as the most critical link in the BC chain, which needs immediate strengthening.

Year-wise Total Cost, Revenue and Profit Forecasting at Different Rate of Active Account in a Sub Service Area

To overcome the constraints and weaknesses of the BC model identified by the research team, strategic interventions by regulators, commercial banks and the CSP agents themselves is essential. There should be a concentrated effort on making the BC model more viable, sustainable and financially attractive to all stakeholders. The proposed business model, as depicted in Table 15, indicates that under optimal circumstances, with different percentage of coverage of active accounts such as 20 per cent, 22 per cent and 24 per cent, an average time period of 3 years, 2 years and 1 year, respectively, is required by the CSP agents to break-even. The challenge, therefore, is to sustain the CSP until the break-even point. Break-even has been achieved due to the increase in the product range and the outreach plan for each CSP. Therefore, it is important that at the bank level, an increase in the product range as well as restructuring the outreach plan at each SSA level be undertaken. By increasing the range of banking products, both bank as well as the CSP agents are benefited. A primary reason for the banks not offering a basket of products is the lack of confidence in the BC system. The bank feels that managing the operational risk in the form of frauds, malpractices and non-adherence to the banking system and the operational process at CSP level is a major challenge. The problem can be addressed by strengthening the systems and procedures at the CSP level with the active support of the bank. In addition to this, the CSPs, which are active at a grass root level, needs to be well informed and should be competent in facing customers. Hence, the banks, as well as the corporate BCs need to concentrate on capacity-building of CSP agents on an ongoing basis by creating separate internal facilities and programmes.

Year-wise Presentation of Income vs. Cost vs. Profit Analysis at Different Percentages of Enrolled Clients Maintaining Active Accounts per SSA

CONCLUSION

The study highlights the need for measures to accelerate the pace of the BC model with quality, accuracy and cost effectiveness to address the financial inclusion programme. This concern has been shared by the Ex-RBI Governor (Bhakta, 2016). The proposed BC model for business sustainability depicts that increasing the financial product range and inducing more coverage and improvised quality of service delivery can help the BC operation in reaching the break-even point in less duration. The model can be a beneficial tool for the lead banks in a specific region for their BC operation towards achieving the financial inclusion goal. Besides, new business opportunities for the banks may be explored through the BC channel of financial inclusion for better market penetration and new market expansion for different banking products.

This research can further be extended to investigate the viability of the BC model from the banks’ return on investment perspective. Future research can focus on both the demand and supply side of the BC operation. For instance, the understanding of different stakeholder’s perceptions about the status of financial inclusion can be a potential avenue for research from the governance perspective (Behera, Pratihari, & Mohapatra, 2013; Uzma, 2016); and macromarketing perspective for the well-being of the society as a whole (Aiyar & Venugopal, 2019). Besides, banks can engage and utilize the local network and resources of the channel members with different value co-creation activities such as the implementation of different corporate social responsibilities (CSR) initiatives in the target markets (Perez, Rodriguez, & Bosque, 2014; Perez & Bosque, 2015; Pratihari & Uzma, 2018). The efforts of the BC as an active channel member may be incentivized by the link-bank branch of the BC operation. As an outcome, a culture of trust and responsiveness may be developed among the members of the value chain, which can be a motivating factor for better productivity (Arora & Kazmi, 2012; Pratihari & Uzma, 2019). The study can also be applied in the domain of bottom of the pyramid (BOP) marketing. Whereas, the notion of BOP marketing lies with the philosophy of profitability with poverty alleviation (Jaiswal, 2008; Prahalad, 2005). In contemporary literature, the apprehension of serving the BOP and the imperatives of value creation has shifted the phenomena of BOP marketing by treating BOP as customer or the beneficiaries (BOP 1.0) to BOP as business partner (BOP 2.0) and BOP as producer (BOP 3.0) (Dembek, Sivasubramaniam, & Chmielewski, 2019), where BC operation for financial inclusion may not be an exception. The robustness of the model may be tested in a different time and geographical contexts in different economies and cross-cultural contexts. The geographical scope of the study is limited to only a representative state of India, and further investigation may be invited to test the feasibility of the CSP agents, who act as micro-level entrepreneurs in the BC model of financial inclusion in other states of India and other emerging and developing economies.

Footnotes

ACKNOWLEDGEMENT

The study is a part of the NABARD, Mumbai, sponsored project titled ‘Status of Financial Inclusion in Odisha’.

APPENDIX

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.