Abstract

Executive Summary

In the past decade, farm loan waivers have become a policy instrument to alleviate the financial distress of farmers. Despite agreement on the theoretical rationale for such debt forgiveness and its deep contextual relevance, many fear that in the long run, loan waivers might vitiate the repayment culture in the farm sector and undermine the financial status of banks. At present, critiques of large-scale loan waivers rest on limited evidence. This article reviews and synthesizes existing research and available data on the implications of loan waivers, especially for the flow of credit to farmers from banks. On most of the issues, such as farmer well-being and repayment culture, there seems to be mixed evidence on the consequences of debt waivers. Credible evidence on macroeconomic implications is limited, mainly on account of methodological challenges. This article concludes that even if loan waivers are an inappropriate strategy to support farm incomes in sustainable ways, the wide-ranging negative impacts on the formal banking sector are perhaps overstated. A more fruitful approach would be to focus on whether loan waivers can be designed to reduce the possible negative consequences for the formal banking system as well as for macroeconomic system. The article identifies three possible instruments—loan insurance products that will help banks cope with the consequences of large-scale defaults. Second, to explore the creation of a distress fund that will cushion state finances, should there be a need for debt waivers. Third, it would be useful to consider the operation of debt relief commissions to have an ongoing process for debt waivers.

Since April 2019, there has been a spate of announcements by different state governments in India on waiving farm loans for indebted farmers. The current wave of loan waivers is regarded as populist as well as an implicit acknowledgement of the pervasive farm distress cumulating over the past 2 years. It appears that farm loan waivers as a policy lever are here to stay. Although originally intended as a one-off instrument—a solution to an exceptional circumstance—the past decade has seen loan waivers become a routine instrument in supporting the agricultural sector. This is, in part, because the deep structural constraints of Indian agriculture remain unaddressed and, in part, because there have been several weather-related shocks in large parts of the country in recent years. In this context, it is important to assess the implications of loan waivers for the credit ecosystem. There is an acknowledgement today that given the extent of farm distress and the somewhat limited options available in the short run, loan waivers are justifiable in the interests of farmer welfare—and some even contend that it does not go far enough; at the same time, loan waivers are deemed to have several associated problems and limitations that provoke a pause. Indeed, there is a popular perception that debt waiver is often used as an instrument of political economy, to appease various interest groups and serve limited purpose, doing more harm than good. This article offers a synthesis of existing evidence and a narrative review of existing debates, with a special focus on understanding the implications of loan waivers on the flow of credit to farmers, especially from the banking sector.

A key hurdle in assessing the implications of farm loan waivers is the challenge of establishing clear causal links between the waiver itself and the presumed consequences of waivers. Existing evidence is mostly based on surveys that allow us to assess impacts at the farm household level, but the larger macroeconomic consequences for the formal credit ecosystem remain under-researched and somewhat elusive. Several loan waiver schemes have been announced but are yet to be implemented and it is hard to anticipate the full range of consequences; that said, loan waivers from the past give us a limited sense of whether the anticipated consequences have supporting evidence or not.

THE RATIONALE AND ITS CAVEATS

The overarching rationale for a debt waiver is that sometimes viable economic units face endogenous credit constraints or thresholds of debt that are so large that they are unable to secure more credit, even though the net payoffs to doing so might be positive (Myers, 1977). Debt forgiveness is proposed as one way to overcome such a debt overhang; while it involves some costs, it allows viable units to survive by allowing them to borrow (Krugman, 1988; Sachs, 1989).

In the Indian context, loan waivers resolve a debt overhang problem that allows farmers to continue accessing credit from formal credit institutions, in a situation of pervasive credit constraints—where the next best alternative might be loans at usurious interest rates from informal sources. This would allow farmers to continue their farming operations as well as protect their existing consumption levels or assets. When the risk of default is high especially due to catastrophic systemic risks faced by a large proportion of borrowers, such loan waivers help borrowers recover and enable creditors to avoid widespread defaults and return to ‘business as usual’.

In addition to the micro-theoretic rationale of keeping potentially viable farmers in business, there is also a contextual rationale. Evidence suggests that returns from agriculture are barely adequate to cover costs of cultivation and consumption expenditure, especially for those with landholdings less than a hectare (Bakshi & Modak, 2017; NAFIS, 2017). This is evident from both nationally representative surveys as well as village studies. Low productivity, a combination of low prices and increasing costs, limits the profitability of agriculture, especially for small and marginal farmers. Apart from these structural problems, farmers also face significant risks—both systemic (or covariate) risks and idiosyncratic risks. Despite several initiatives, reliable instruments of insurance are not available to farmers. For example, there is widespread agreement that crop insurance has by and large failed most farmers. Existing studies suggest unfulfilled/pending claims, exclusion of small and marginal farmers, poor uptake, awareness, and so on (see Comptroller and Auditor General of India [CAG], 2017, for example). Even internationally, a long-held view is that crop insurance is not often the most cost effective approach for governments (See Hazell, 1992, for instance). In this context, farmers rely overwhelmingly on credit, especially informal credit, to tide over short-term shocks to their income stream. For those who are unable to supplement farm income or bear the losses through other non-farm sources of income, debt becomes crucial to enable them to tide over bad years.

The government has, in the past, attempted to regulate even private money lending. Even in the colonial period, and continuing after Independence, several states passed legislation to oversee and regulate moneylending. These have been mostly unsuccessful. Governments have frequently attempted to provide relief via debt swap and rescheduling of repayments of loans to private moneylenders. For example, in 1975 there was an attempt to tackle the debt burden in informal credit by way of a general moratorium on moneylenders’ debt, similar attempts to ban bonded labour consequent to non-payment of debt, and so on. In an effort to ameliorate the suffering of debt-ridden farmers, the Andhra Pradesh Legislative Assembly passed the A.P. Farmers Agricultural Debts (Moratorium) Act 2004 on 21 June 2004, which provides for declaring a six-month moratorium on repayment of loans from private moneylenders. Each of these has barely had any success. Existing accounts of the relationship between indebtedness and farmer suicides (Mishra, 2006, for example) suggest the need for some measure of relief for farmers. The case for debt waivers thus assumes significance in the context of the very limited impact of alternative measures to ease farmer indebtedness.

While other policy instruments such as relief payments do exist in the case of extreme events such as drought or floods, given the range of risks including price and other yield risks, farm distress could be widespread even in the absence of extreme events. From the farmer’s point of view, if farm incomes are such that it undermines their ability to repay loans to creditors, there is a high risk of default. This may result in farmers losing any collateral that they used to obtain the loan and also prevents future credit access on the basis of their loan default record. In the Indian context, given the dependence of farmers on credit for their routine operations, this could potentially have disastrous consequences. The main objective of farm loan waivers in this case is to alleviate farm distress, particularly when shared shocks affect farmer incomes.

From the point of view of lenders, farm loan waivers are based on the idea that in an economy that is credit constrained, unpaid loans clog the pipeline of formal sector credit flow that, in turn, hampers the ability of the formal sector to continue its lending operations. Farm loan waivers in this context help de-clog the credit lines and enable creditors to infuse credit into the sector in stress. This makes it different from other forms of direct relief payments that might not have a similar impact on the credit flows. In principle, a one-time loan waiver is supposed to get the system back on track and move forward thereon.

Not all debt waiver schemes are the same and can be quite different from one another in design. For instance, debt waivers can be targeted, restricted to certain sections of the farming community (smallholders), certain lenders (cooperative or commercial banks) and involve caps on the extent of waiver (just the interest component or the principal, or even relief, which entails forgiving a part of the principal). In India, there have been two major nation-wide loan waivers (in 1989–1990 and 2008–2009). Most of the recent debt waiver schemes have been state-level initiatives. These have ranged from moratorium on interest payments to debt relief and debt waivers. In a typical loan waiver, banks or lenders would, backed by a state guarantee, waive loans of their borrowers as per prescribed guidelines or eligibility criteria. The state would compensate these lenders, typically staggering this over a few years. The compensation, when delayed is often paid out to creditors with an interest rate component and the state governments typically fund these through borrowings to the extent that revenues are not adequate to cover these commitments. Debt waivers thus involve several stakeholders, each of which can have a bearing on the formal credit ecosystem.

However, as is evident, implementing farm loan waivers have complex financial ramifications for several parties, especially if the agricultural sector is exposed to repeated shocks. Furthermore, not only is it the case that there could be unanticipated consequences; when farm loan waivers are declared frequently, the anticipation of such waivers could lead to perverse consequences, coming in part from a set of expectations that build around borrowers that such waivers are likely to occur (EPWRF, 2008). These latter set of concerns are best represented in this much-quoted statement by the then Governor of the Reserve Bank of India

I think it (farm loan waiver) undermines an honest credit culture, it impacts credit discipline, it blunts incentives for future borrowers to repay, in other words, waivers engender moral hazard. It also entails at the end of the day transfer from taxpayers to borrowers. If on account of this, overall Government borrowing goes up, yields on Government bonds also are impacted. Thereafter it can also lead to the crowding out of private borrowers as higher government borrowing can lead to an increase in cost of borrowing for others. I think we need to create a consensus such that loan waiver promises are eschewed, otherwise sub-sovereign fiscal challenges in this context could eventually affect the national balance sheet. (Press Conference, 6 April 2017; See also Patel, 2017)

Whether or not these fears are well founded is the subject of the article.

HISTORY OF FARM LOAN WAIVERS IN INDIA

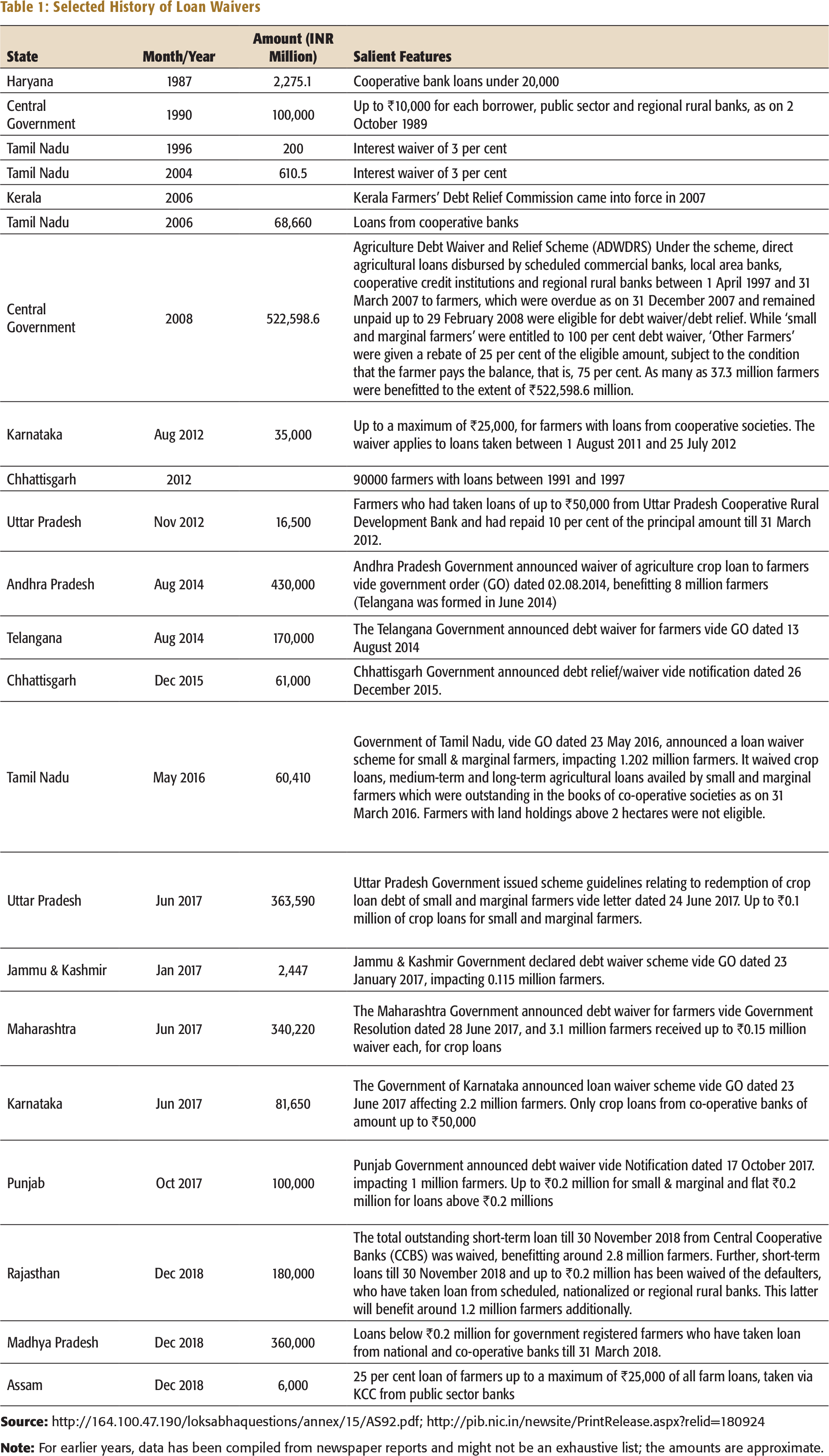

Selected History of Loan Waivers

Loan waivers often seem to be an intervention that affects the entire farming community, but it is well known that the beneficiaries are often only those who are already able to access credit offered by banks, typically, the better off farmers. There is therefore an inherent bias against informal sector borrowers (Ramakumar, 2013). In scope, the ADWDRS, 2008–2009, a nationwide loan waiver, reached only an estimated ₹30.1 million, with an additional 6.8 million benefitting from relief. Compared to an estimate of 117.6 million operational holdings in 2010 (owned individually, jointly or by institutions) that were below 2 hectares, it is clear that less than a third of small and marginal farmers found relief. In the context of the ADWDRS 2008–2009, it was noted that states with high proportion of indebted farmers also had high share of informal loans—their exclusion exacerbated inequalities across farmers. The implementation of many loan waiver schemes also left a lot to be desired (CAG Report, 2014, Government of India, 2014). A performance audit of the ADWDRS 2008 suggests that several non-eligible beneficiaries obtained waivers and relief while several eligible people did not obtain these waivers or relief. Out of 9,334 accounts audited in nine states, 13.46 per cent were found to be eligible but not identified as such by the banks and hence did not obtain benefits. Out of the 80,299 accounts, in 8.5 per cent of the cases, the beneficiary was not eligible for waiver or relief, as per the rules nevertheless benefitted from this. This suggests that given the extent violation of the norms, studies that focus on comparing welfare impacts of beneficiaries and non-beneficiaries are complicated. It suggests at the same time that given the limited reach, especially targeting relatively smaller borrowers, the macroeconomic and fiscal implications would be somewhat limited as opposed to a loan waiver that covered all farmers.

IMPACT OF LOAN WAIVERS: ASSESSING ASSESSMENTS

Impacts on Farmers on Well-being and Repayment Capacity

There is little doubt that loan waivers benefit farmers, although in what forms these benefits manifest is open to question. In the short term, this implicit transfer releases a liquidity constraint and enables farmers to protect their consumption and input expenditures in farming operations. 1

Robert (2012) report that beneficiaries are happier and face less stress, although there are also negative feelings of benefitting from loan waivers.

It appears that the impacts could be heterogeneous across beneficiaries. Mukherjee, Subramanian, and Tantri (2017) show that the debt waiver engenders costs when it is directed to non-distressed borrowers, but generates substantial benefits when it is directed to distressed borrowers. They find that the default rate of distressed (drought-related) waiver beneficiaries is lower by 16–22 per cent when compared to distressed non-beneficiaries. It can protect and smoothen consumption expenditure too.

Kanz (2016) in his primary household survey in Gujarat finds that debt relief does not increase investment. Beneficiary households of ADWDRS reduced their agricultural investment by between 14 and 24 per cent relative to non-beneficiary households. He also finds that debt relief does not increase the productivity. Households witnessed a decline of between 13 and 19 per cent in revenue per acre relative to non-beneficiary households, indicating a loss of productivity.

Is There Erosion of Credit Discipline?

Although debt waivers strengthen the repayment capacity of the farmer in the short run, there seems to be consistent evidence that credit discipline does indeed erode following a loan waiver. De and Tantri (2013) highlight the problem of loan waivers leading to strategic defaults. If debtors expect future debts to be waived off, their incentive to repay future loans reduces. They report that full waiver beneficiaries (ADWDRS) delayed loan repayment by 22 days on an average; partial waiver beneficiaries delayed by 25 days on an average (number of days outstanding). Non-beneficiaries delayed the most, by 197 days on an average, in anticipation of a waiver. Gine and Kanz (2017) finds that the ADWDRS 2008 led to a degradation of credit discipline among farmers and 1 standard deviation increase in bailout exposure leads to a 52 per cent increase in the probability that a district experiences an increase in the share of non-performing loans. Chakraborty and Gupta (2017b) find that in Uttar Pradesh, repayment rates fell by 15–25 per cent after implementation of Uttar Pradesh Rin Maafi Yojana 2017. Subjective perceptions of borrowers also reveal these concerns. For example, Jain and Raju (2011) find that the intentions to repay loans among non-beneficiary farmers reduced drastically after announcement. Before announcement of ADWDRS, nearly 90 per cent non-beneficiary farmers intended to repay their loans, but after the announcement, only 3 per cent were inclined to repay their future loans. 2

The interest subvention scheme was introduced precisely to tackle this issue. The recoveries reported in this paper have looked different in its absence.

Is there Formal Sector Credit Rationing or Informalization of Credit Post-Waiver?

In principle, a debt waiver, by clearing the creditor’s books off non-performing assets (NPAs) of loans that have a high probability of default and most likely defaulted, the creditor would be able to free up resources to lend out a fresh round of loans. One key motivation of loan waivers is to ensure that farmers can continue to rely on formal sources of credit, in this case, banks. Yet, it seems that debt waivers lead to perverse consequences, where there is greater formal sector credit rationing. It must be noted here that by formal credit, the reference is to the banking sector rather than the micro-finance institutions (MFIs) and non-banking financial companies (NBFCs), which have an increasing presence in the agricultural credit landscape. One reason put forth is that because the waiver is staggered, lenders do not have the liquidity immediately post-waiver to be able to issue fresh loans. The other reason is that the formal sector consequent to waiver often attracts new borrowers especially from the small and marginal category in anticipation of new loans. To the extent that these new borrowers do not strategically default on loan repayments, this can be a positive outcome. But banks might scale down lending in fear of these perverse consequences. One would expect that these effects vary across the types of lending institutions, that is, between private and public sector banks and cooperative banks.

Studies that use survey data and secondary data both find evidence on formal credit rationing post-waiver. For example, Gine and Kanz (2017) found that a standard deviation increase of 1 in the share of credit waived under ADWDRS led to a 4–6 per cent decline in the number of new loans and a 14–16 per cent decline in the amount of post-programme lending. One and a half years after debt relief under ADWDRS, formal sector debt among households that benefited from unconditional debt relief declined by 8–10 per cent compared to households in the control group. Over the same period, their relative reliance on informal credit increased by 5–6 per cent. Districts with higher programme exposure (than median) got only 36 paisa and those with lower exposure got ₹4 of new lending per rupee debt waived. Similarly, a National Institute of Bank Management (NIBM) Report (2011) on ADWDRS notes that for the branches surveyed as part of the study, among borrowers whose loan accounts were closed on account of ADWDRS, the percentage of borrowers who could receive fresh loans from the respective branch were only 18 per cent for cooperatives, 71 per cent for Regional Rural Banks (RRBs), and 81 per cent for commercial banks.

However, some find that this impact is short-lived and the differences even out as the credit flow recovers. Raj and Edwin (2018) use transaction level data of agricultural credit given to all farmers for 3 years 2015–2016, 2016–2017, and 2017–2018 (up to 15 December 2017) from 22 Primary Agricultural Cooperative Credit Societies (PACCS) in seven districts of Tamil Nadu to study the loan waiver of 2016. They find that in the short term, the probability of obtaining credit post-waiver is higher for non-beneficiary farmers relative to beneficiary farmers around the eligibility cut-off of 5 hectares. They attribute these to several reasons (a) the time taken to verify the eligible farmer accounts which delayed the sanction of new loans to beneficiary farmers in the year of implementation of the debt waiver; (b) non-beneficiary farmers being encouraged to make prompt repayment of crop loans to avail full interest relief with the promise of new loans. They find, however, that these impacts do not last beyond the year.

In contrast, Hoda and Tewary (2015) claim that debt waivers affected rural credit with defaults of such a high magnitude that it took the banks several years to recover from its impact (Report on Task Force of Rural Co-operative Credit Institutions, 2006). Although the scheme was implemented during 1990–1991, the real impact may have been felt from November 1989 itself when various political parties started making promises that they would write off agricultural loans if they returned to power. Shylendra and Singh (1994) found that the loan recovery of Primary Agricultural Credit Society (PACS) in Karnataka fell from 74.9 per cent in 1987–1988 to 41.1 per cent in 1991–1992. One impact that is harder to gauge and worth studying is the phenomenon of borrowers switching accounts to nationalized banks in anticipation of loan waivers since there is a fear that the waiver may not be extended to private banks. There is anecdotal evidence that this might be happening (Kasbekar, 2008).

Implications for the Banks

In most loan waivers thus far, the credit agency tends to be either the scheduled commercial banks or cooperative banks. To the extent that in the absence of a waiver, they would have had to absorb defaults. Such waivers could enhance the profitability or limit the losses of the lender. A NIBM Report (2011) on ADWDRS noted that profits of cooperatives and commercial banks increased in 2008–2009 and of RRBs in 2009–2010. The study identifies agricultural NPA recovery as the most important reason for this. At the same time, this is a one-time increase in profitability and it is unclear whether these translate to a profit stream for these institutions, beyond the year of loan waiver. If a key objective of the loan waiver is to clear the books of the lenders off their NPAs, it appears that the waivers did their job.

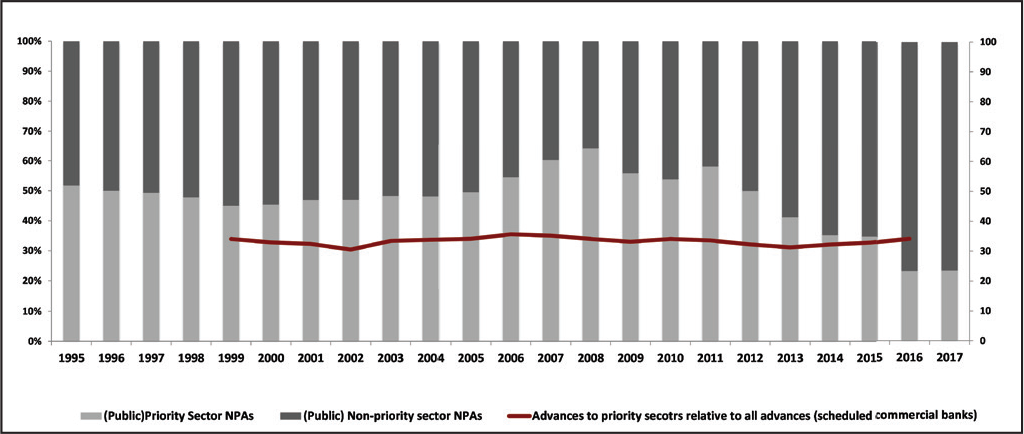

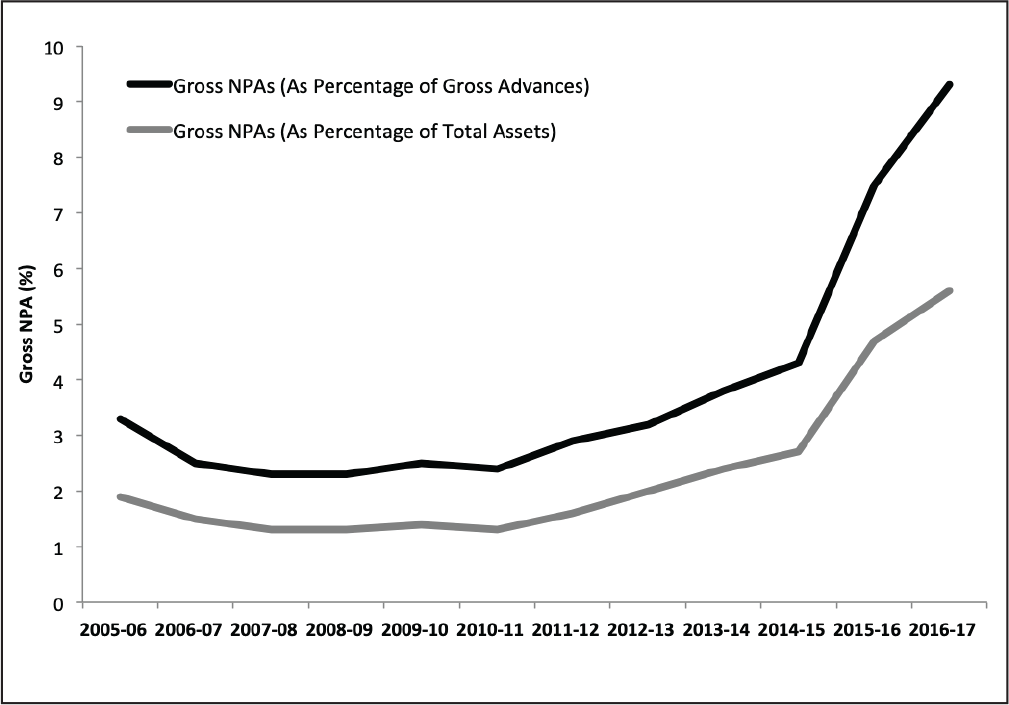

Nevertheless, one would want to track the behaviour of the NPAs over time. If debt waivers vitiate the repayment culture, lenders would register a disproportionate increase in NPAs in the agricultural sector. This is a concern that has been raised by few scholars (Rath, 2008; Vaidyanathan, 2008). As it turns out, while the NPAs have been on the rise, it is not clear that this is driven by the 2008–2009 debt waiver, nor is it the case that agricultural NPAs have risen relative to those in other sectors. As Chandrasekhar and Ghosh (2018) note that when compared to total advances, there is no dramatic change in the share of priority sector lending or agricultural advances, in the past decade. In fact, the NPAs in the non-priority sectors account for an overwhelmingly increasing share of all NPAs. Figure 1 shows that NPAs are rising, and at the same time, NPAs in the priority sector, relative to the non-priority sector for public sector banks and the proportion of priority sector advances for all scheduled commercial banks (Figure 2).

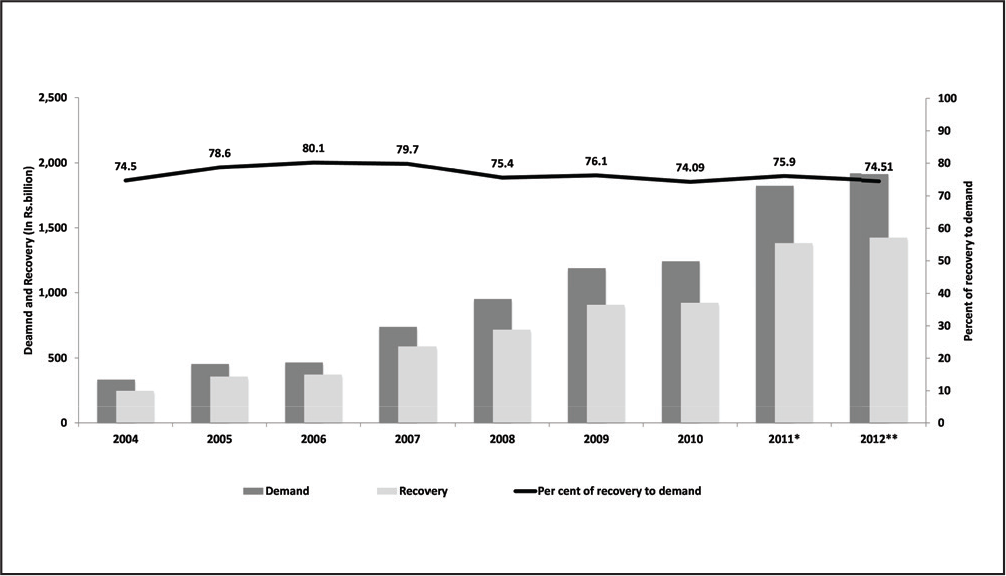

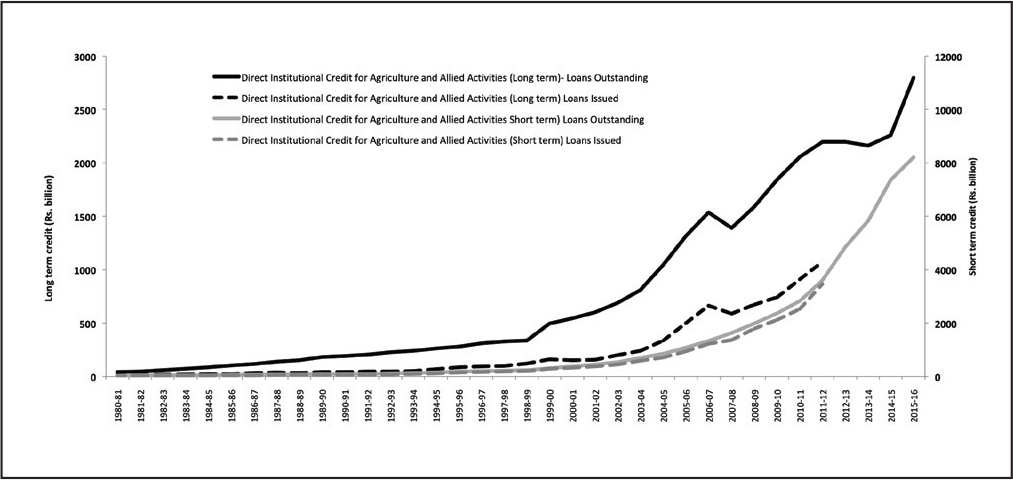

Trends in loans issued too suggest a dent in the immediate aftermath of the debt waiver but returns to the trend within 2 years of the 2008–2009 waiver (Figure 3). Recovery rates too suggest no dramatic decline (Figure 4). This is not to suggest that no impacts exist; but the impact may be rather limited in scale and does not necessarily reflect or negatively impact key indicators at the macro level.

Implications for Government Finances

A key concern for the larger macroeconomic context has been the burden that loan waivers would place on government finances. To a large extent, the implications of the loan waiver depend on how states finance these and how they structure the absorption of the costs into the budget. On the one hand, borrowing to cover the cost of farm loan waivers or cutting back on other expenditure could crowd out potentially critical farm investments that have the capacity to benefit the farming community in the longer run. On the other hand, when the government relies on it, it could also impact the inflation rates via increasing the fiscal deficit of the states. Further, considering that the loan waivers often are spread over several years, the impact of a single farm loan waiver could have ramifications beyond the current fiscal year. For example, in AP, Telangana, and Tamil Nadu, the benefits of the debt waiver in these states were given to the farmers in the year of implementation, but the reimbursements to the lending institutions by the state governments are being done in a phased manner, over a five-year period for Andhra Pradesh and Tamil Nadu. Telangana has completed its reimbursement by 2017–2018. As one would expect, evidence on these aspects is very hard to establish, nor is the existing evidence conclusive and indeed given the diversity of states implementing these loan waivers, the consequences for state fiscal deficit could be heterogeneous.

Not all the states that have announced waivers are in a precarious fiscal state, though the burden on state finances is a significant cause for concern. Phadnis and Goswamy (2019) observed that out of the nine loan waivers that were announced prior to 2016, seven were introduced by states that had lower debt/GSDP (Gross State Domestic Product) ratios than the all-India state average. The only two states (Uttar Pradesh in 2012 and Kerala in 2006) that had higher debt ratios presented waivers of very low size (<1% of state budget). The trend seems to have changed post-2016. First, a higher proportion of the seven waiver-announcing states fell in the higher debt category (3 out of 7). Second, the three states with high debt have introduced large waivers ranging from 8.5 to 12 per cent of the state budget. Suhag and Tiwari (2018) estimate that the contribution to fiscal deficit ranges between 0.1 and 0.9 percentage points for the eight states that have announced loan waivers since 2014–2015. Four of them have an average fiscal deficit of below 3 per cent even after accounting for loan waivers. 3

Whether it is in terms of fiscal deficit, NPAs, or fresh loans, it is apparent that there is considerable diversity of experience across states. This is an area that deserves further research.

The Reserve Bank of India has stated that past waivers had an enduring impact on market borrowings (Reserve Bank of India [RBI], 2018). If overall government borrowing increases, the RBI cautions, yields on state development loans (SDL) firm up, posing higher interest burden for the states in future. Observers note that this can also crowd out private borrowers, if it is the case that there is a limited pool of investible resources, since the general cost of borrowing increases for everyone as the government begins to borrow. Thus, state government farm loan waivers have the potential to crowd out corporate borrowings if financed through SDL issuance.

Depending on possible sources of financing, the additional burden including (a) additional market borrowing and (b) pruning of wasteful expenditure, this may result in an increase in the consolidated gross fiscal deficit/gross domestic product (GFD/GDP) ratio of the states by about 20–40 basis points (bps). Higher fiscal deficits per se can lead to an increase in inflation expectations and actual inflation.

In general, theoretical concerns are empirically hard to validate. Tracking the source of public finance for loan waivers is perhaps futile, given the fungibility of funds even for governments. Thus, even if empirical work attempts to relate loan waivers to fiscal consequences for state governments, they cannot credibly identify the channels or causal chain through which these consequences materialize. Mitra, Bhattacharyya, John, Manna, and George (2017) study estimates that the aggregate GFD/GDP ratio of the states could increase by about 20–40 bps on account of recent loan waivers. This would, in turn, lead to increased cost of borrowing and negatively affect capital expenditure. The RBI Report on State Finances (2018) speculates that the decline in capital outlay growth during 2017–2018 in some waiver granting states is a pointer to the likely impact of the waiver on developmental expenditure. This could also crowd out private investment. There are also concerns regarding the consequences for inflation in the economy. Mitra et al. (2017) estimate that if the combined fiscal deficit for 2017–2018 goes up by 40 basis points on account of farm loan waivers, with the budgeted combined fiscal deficit at 5.9 per cent for 2017–2018 and inflationary momentum remaining benign, ceteris paribus, this may lead to around 20 basis points permanent increase in inflation, starting in 2017–2018.

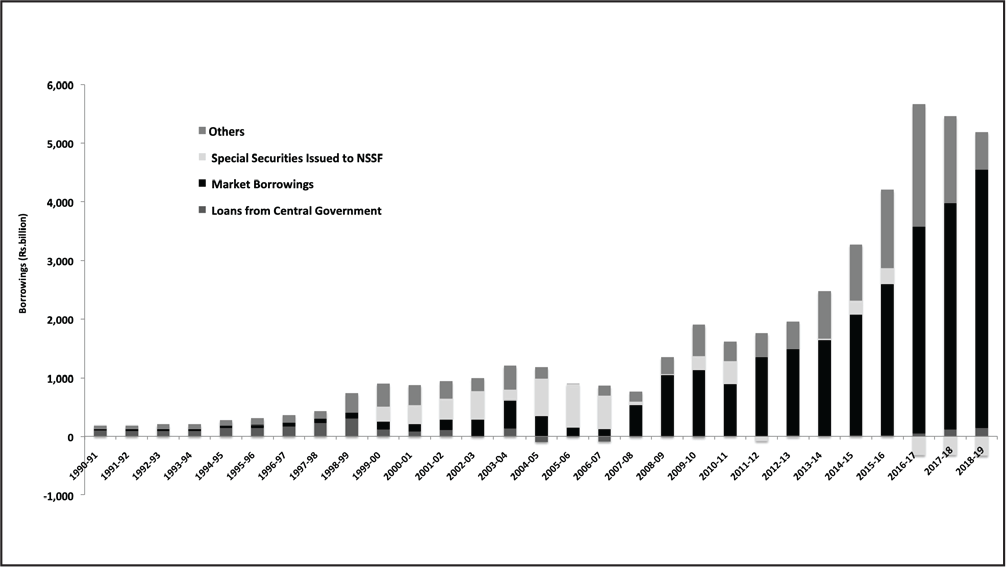

It does seem to be the case that states have increasingly resorted to market borrowings to cover their fiscal deficits (Figure 5). While it is hard to attribute this to loan waivers, to the extent that these waivers drive states to borrow from markets, its attendant consequences are noteworthy.

CONCLUDING REMARKS

It is apparent that despite growing literature, there is no unequivocal evidence on the consequences of loan waivers for different stakeholders. In this section, we identify areas where further research would be useful and reflect on the way forward.

Existing evidence seems restricted to assessing the short-term consequences of a single loan waiver. However, one critical gap continues to exist. There is perhaps no study or survey that assesses the implication of repeated loan waivers to the same set of beneficiaries. Tracking such a sample over a period of time would provide us with much needed insights into the potential sustained negative consequences of loan waivers for repayment culture. Another aspect that requires attention is the response of state governments in funding strategies vis-a-vis loan waivers. Do they invariably fund these by reducing capital expenditure allocations and if yes, from which sectors are these funds diverted? If indeed this is the case, what are the consequences of such reallocation? The article also presented indicative evidence based on economy-wide data to uncover potential impacts of nationwide large-scale waivers. Overall, while there is reason to believe that there might be adverse consequences in terms of the burden on state finances and its consequences, existing evidence is fairly mixed. Further research would be essential on the macroeconomic consequences of loan waivers, where rigorous research is all but absent.

The debates on farm waiver have been so far on whether or not these waivers should be implemented, on whether these should be ‘off the table’, so to speak. 4

Some oppose the idea of farm loan waiver, while others suggest that it should not be a poll promise without necessarily commenting on whether farm loan waivers can be a credible and useful policy instrument.

There is also a view that farm loan waivers are undesirable. However, it neglects the fact that large defaults for industries and businesses are routinely written off. Furthermore, the scale of the latter is much larger than for the farming sector. In that sense, farm loan waivers are perhaps less pernicious to the fiscal health of the country. Indeed, it can be argued that the use of loan waivers as a political instrument to address specific interest groups is not per se a problem if such loan waivers fill an important lacuna in the set of coping strategies that farmers access.

Notwithstanding these arguments, a more fruitful approach would be to focus on whether loan waivers can be designed to reduce the possible negative consequences for the formal banking system as well as for macroeconomic system. In terms of policy, a question arises: Is there an optimal way to design debt relief? We reflect on several possible approaches, not necessarily mutually exclusive.

In the context of a move to direct payments, it is important to note that whereas direct payments and disaster relief payments might have a similar welfare impact on farmers, debt relief has two features that the former do not. It helps banks to not only clear their books of non-recoverable loans but also allow farmers to restart with a clean slate. At this time, the only recourse banks have to recovering loans in the case of widespread defaults in the face of covariate shocks (especially weather related) is via a first charge on insurance payouts. 5

Sen (2017) notes that loans are compulsorily insured by the Agricultural Insurance Corporation (AIC), although it is neither based on actuarial principles nor is the AIC adequately capitalized. In the event of defaults, liabilities are backstopped by the Central Government through budgetary support.

Another instrument would be to form an agriculture distress or crisis fund, not unlike the price stabilization fund. 6

http://pib.nic.in/newsite/PrintRelease.aspx?relid=160050

Perhaps a more difficult alternative, mainly because it would involve political persuasion, is to move to a model based on the Kerala Farmers’ Debt Relief Commission or Ombudsman to mediate and assess cases for the award of moratoria, waiver, and relief as also debt restructuring on a continuous basis. A related approach that is linked to the previous one is to leverage the Bankruptcy Insolvency code (Satija, 2019)—this approach is operationally not different from the Kerala Debt Relief Commission but takes advantage of existing laws to do so. The challenge would be that the number of cases that would be dealt with as also the time and costs of running a system nationwide.

Until such time that the larger structural issues in Indian agriculture are resolved and in the face of persistent and impending climactic risks that farmers would continue to face, it would be prudent to retain debt waiver and relief as an additional policy instrument.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

FUNDING

The author(s) received no financial support for the research, authorship, and/or publication of this article.