Abstract

Keywords

INTRODUCTION

Hegde was a career banker, and Nishtala had worked in the manufacturing sector. They had worked together in Fullerton, a large non-banking finance company backed by Temasek group of Singapore. At Fullerton, they created and led the microfinance business. Fullerton also offered financial services to micro, small and medium enterprises (MSMEs).

The microfinance institutions (MFIs) segment was getting cluttered, with multiple players operating on similar models. While there was much bullishness in the microfinance segment with one of the largest MFIs—SKS Microfinance—announcing the public offering in March 2010, there was also a sense that the microfinance market was overheating, particularly in the southern state of (then undivided) Andhra Pradesh with too many institutions chasing the same set of clients leading to overindebtedness driven by mindless growth.

At the same time, Hegde and Nishtala sensed an opportunity to work solely in the MSME sector because the market was large enough to warrant a dedicated organization. They quit Fullerton and set up Vistaar Finance, with operations in Karnataka and Tamil Nadu in April 2010, with an initial capital of `150 million. By October 2010, this decision made by Hegde and Nishtala was vindicated when there were a series of microfinance client suicides in (the then undivided) Andhra Pradesh. The state government clamped down on MFI through an ordinance followed by a very stringent law that heavily restricted the operations of MFI (Government of Andhra Pradesh, 2010).

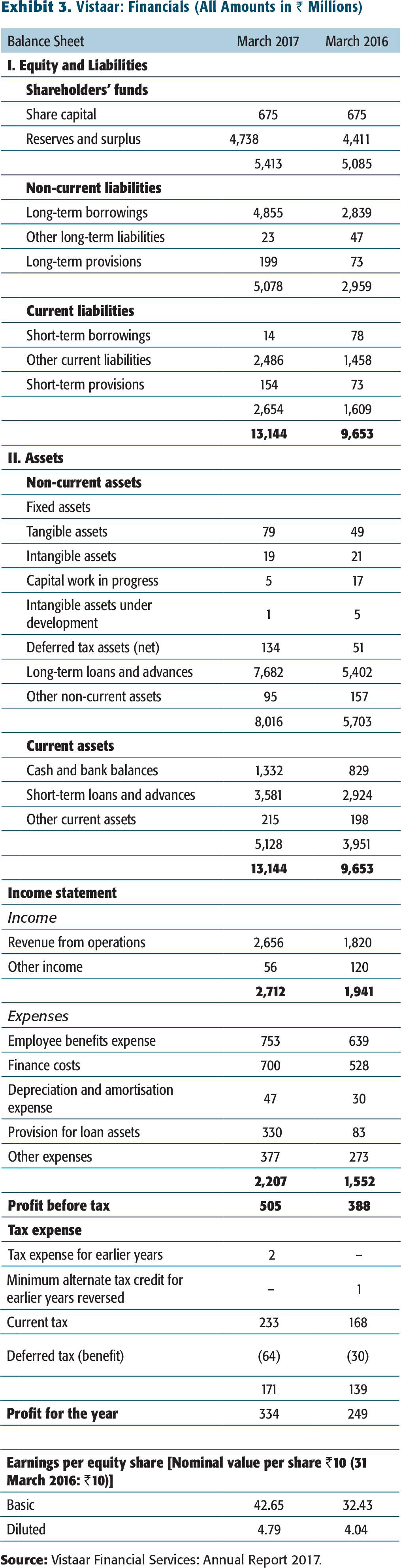

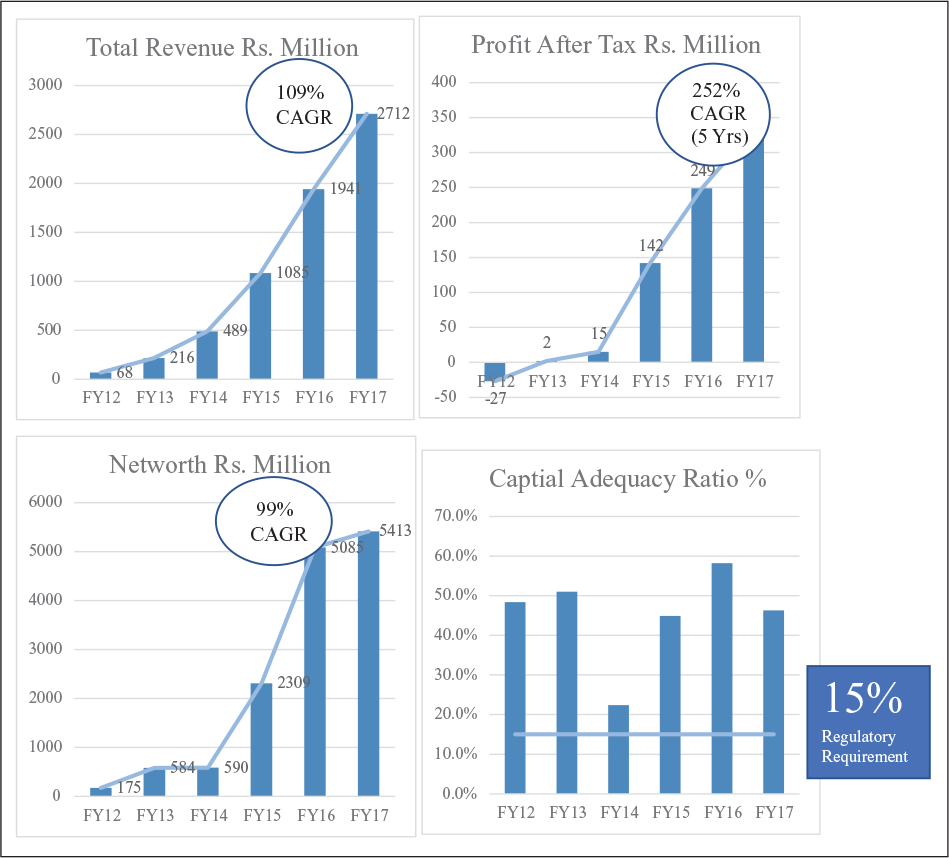

Vistaar Finance offered a range of financial services to small businesses. For Vistaar, the business model (explained in detail in the following sections) was effective, and the growth had been impressive. The year 2016–2017 had been remarkable despite the general slowdown in the MSME space following the demonetization announcement made by the Prime Minister on 8 November 2016. The topline and bottomline had grown, indicating that the Vistaar model was robust (see Exhibit 3 for financial statements).

Around the same time, the Indian banking system was opening up. In April 2014, the Reserve Bank of India (RBI) issued two new bank licences representing two ends of the financial world. One to Bandhan, the largest MFI, and the other to IDFC, an infrastructure financing major. They were chosen from a list of 25 aspirants. Although the inclusion of Bandhan was seen as a wild card entry, there was hope that more licences could be issued to similar institutions. Thereafter, the application process for small finance banks (SFB) (RBI, 2014) opened in November 2014. RBI received 72 applications for SFBs. After scrutiny, RBI granted in-principle licences to 10 SFBs. By the end of 2017, most had started operations. They were expected to offer half of their portfolio in loan sizes less than ₹2.5 million and deploy 75 per cent of their book compulsorily into priority sector. In August 2016, the RBI issued guidelines opening applications for a banking licence on-tap (RBI, 2016). Based on these guidelines, Vistaar was eligible to apply for a bank licence in 2020.

It was in this context that Vistaar’s top management was brainstorming on the dilemma of the growth path for Vistaar.

MSME OPPORTUNITIES AND CHALLENGES

From their experience, Brahmanand Hegde and Ramakrishna Nishtala knew the potential and the challenges of the MSME sector. It needed innovative and unconventional solutions for the lending model to be profitable and trustworthy. MSMEs had been unbanked largely because the past efforts were unsuccessful and non-profitable. There were manifold reasons for the lack of growth in the MSME sector. Phansalkar, based on an extensive consulting experience (Phansalkar, 2002), identified eight important mistakes that the small-scale sector commonly made:

Excessive or exclusive dependence on the buyer; Expanding fixed assets before providing for working capital; Borrowing in the cash market to increase stock; Doing informal business; Spawning firms; Marketing myopia or the inability to look at the needs of customers; Hiring employees for reasons other than competence and Unrealistic project planning.

These mistakes represented an opportunity for an organization like Vistaar. They aspired to move the businesses from the informal sector to the formal sector. This was a challenge especially because a substantial part of the transactions was in cash, and the records did not reflect the risks and profitability. Moreover, the small ticket size of the loan and the time required for loan assessment did not promise great yields. It was almost impossible to assess the risk of this category of borrowers using the mainstream financial metrics. The non-performing assets (NPA) in this segment were very high, and therefore, the benchmarks were stacked against any entrepreneur foraying into this segment, though it seemed to hold out a great opportunity.

However, despite these odds, this underserved segment looked like a great opportunity for Vistaar. The main belief of Vistaar was that ‘small businesses make a big economy’. Therefore, the goal was to be a catalyst to the underserved MSME segment so that they could achieve greater economic and social well-being (Vistaar Finance, 2016).

MSME SECTOR IN INDIA

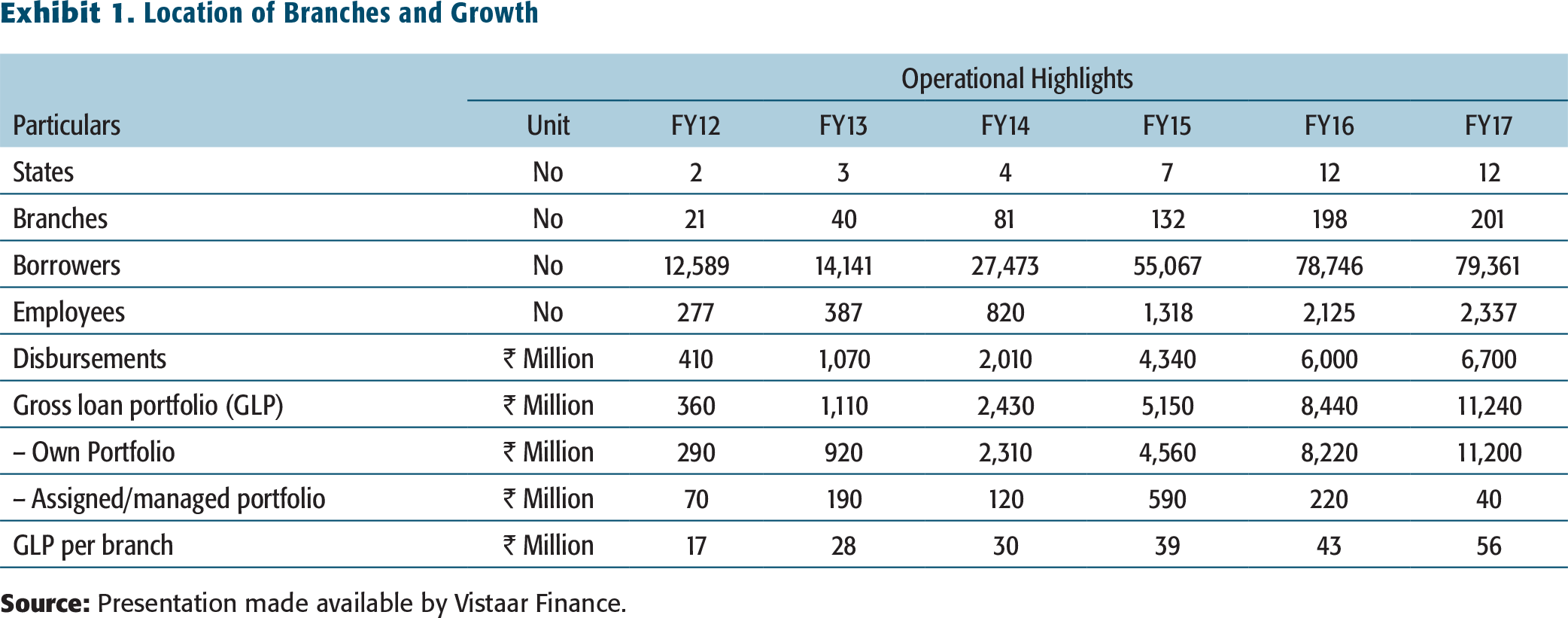

Location of Branches and Growth

Yet the level of access and awareness about the financial system remained low in this sector. The total demand for capital (debt and equity combined) was US$650 billion, but there was a gap of US$418 billion (roughly two-thirds of total demand) in the MSME sector (Intellecap, 2016). This was just among registered entities. Another report claimed that 93 per cent of microenterprises had no access to the financial system (Ernst & Young, 2016). Extensive research showed that financial inclusion of the MSME sector is of great importance for India’s economic development.

With the growth in the MSME sector, the opportunity for the financial sector was enormous. Many players were getting ready to serve the unbanked. A good number of these started with loans to individuals. Vistaar was unique in focusing their energies only on enterprises and entrepreneurs.

FUNDING LANDSCAPE

Although there were directives from the RBI that there should be dedicated credit lines for the MSME sector in the priority sector lending norms, it was not sharply mandated. An overall shortfall in the priority sector lending targets (other than the mandatory 18% of the adjusted net bank credit to agriculture) was to be invested in Small Industries Development Bank of India (SIDBI) bonds. SIDBI worked as an umbrella organization for the MSME sector not only providing refinance but also creating ecosystem institutions, such as the small and medium enterprises rating agency, credit guarantee trust for small and medium enterprises and a venture fund. However, this market was large, and the formal sector did not take advantage of the opportunities provided by the sector.

In 2014, RBI set up an internal working group to revise the priority sector lending norms. Based on the report submitted by the working group, RBI changed the targets and definitions, making it mandatory for all banks to focus on at least a part of their portfolio to the MSME sector and in particular to the microenterprises (Intellecap, 2016).

VISTAAR MODEL

Vistaar had seen good growth in 6 years with numerous rounds of capital infusion including ₹2.5 billion in 2015, which was the largest and the most recent. In 2016, Vistaar operated 201 branches across 12 states. As of FY 2016, it had 78,000 active borrowers, of which three-quarters were women entrepreneurs. About 97 per cent of customers were from rural and semi-urban areas. Exhibit 1 shows the spread of Vistaar branches and growth.

Target Market

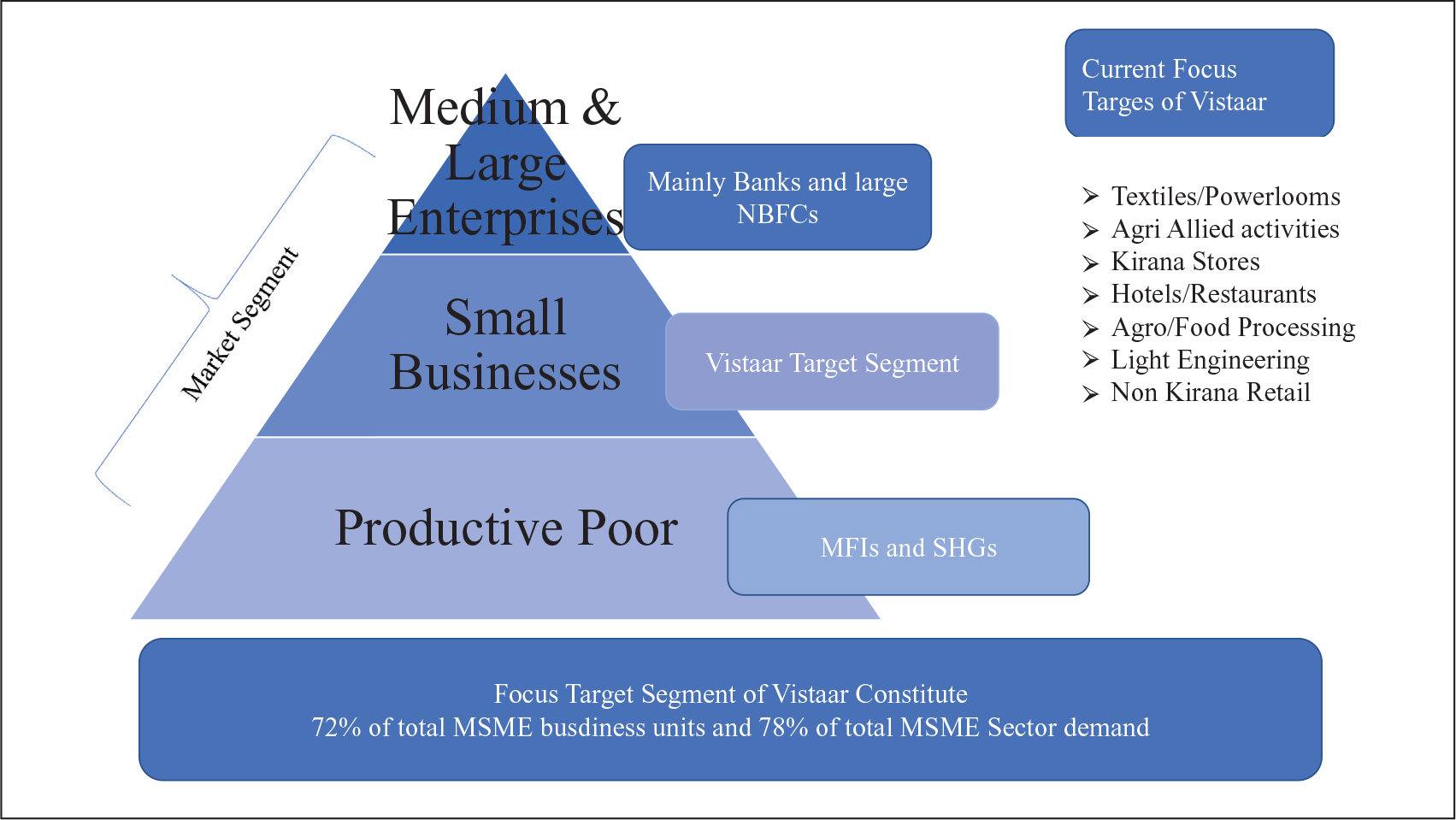

The company’s business model was unique. It built on the fact that in case of MSMEs, what you see is what you do not get; there was opacity in the operations because this segment operated at the axis between the formal and the informal sector. A large part of the transactions could be unaccounted, making traditional assessment models and cash flow-based lending models irrelevant. While Vistaar was a formal company, their credit assessment models had to necessarily account for other non-financial parameters that operated as surrogates for client behaviour and orientation that indicated both the ability and willingness to pay back the loans. This involved intimately understanding every segment that their borrowers operated in. At the heart of the business model was a unique credit approval process. Vistaar’s target market was a combination of applicants’ geographic proximity to Vistaar branches, business segment and size.

The specific business segments that Vistaar covered were:

Textiles/Powerlooms Agriculture-allied activities Kirana stores (small grocery stores) Hotels/Restaurants Agro/Food processing Light engineering Non-kirana retail

The internal estimates showed that these segments covered 80 per cent of MSME businesses in the country. Each branch served customers in a radius of 30 km. The customer base was widened by opening new branches. Vistaar was focusing on MSMEs segment, and being a pioneer was advantageous, both on the capabilities and on the customers’ portfolio. Exhibit 2 gives the slicing of the MSME segment as per Vistaar’s vision.

Unique Loan Approval Process

Vistaar managed to be successful in the MSME segment because of its unique credit appraisal process. Assessing the income, ability, intention, business sustainability and credit behaviour of the customers was the main challenge. Usually, there were no official papers providing proof of transactions, and all businesses mostly operated on cash payments. Vistaar managed to keep its NPA at an acceptable level (just 2.23%) because of its deep knowledge of customers’ businesses.

The credit appraisal process was well-structured and well-defined. There was a good understanding of the ecosystem in which the customer operated. While one could understand the macroeconomic risks, there were sub-risks which were not firm specific, but possibly geographical cluster specific or specific to the value chains. This assessment started with the formation of sector committees comprising product and credit experts. These committees were tasked with understanding and analysing a particular business/industry in depth and built guidelines pertaining to metrics, such as cash flows, cost structure, average stock values, and so on, and defined standards for each segment.

At the customer level, Vistaar staff members personally met and evaluated each customer in an unconventional way that included not only reviewing official documents but also informal accounting papers and internal reports. A typical example would be the analysis of Red Book (Chopdi), maintained by most North Indian businesses that record their accounts in single entry format where the year to reckon is from Diwali to Diwali—the new year as per the traditions and the lunar calendar. The real value of inventory was also directly assessed by Vistaar staff.

The next step was to interview all stakeholders, such as suppliers, customers and neighbours, in an attempt to understand the applicant better and gauge the willingness to pay as per the customer’s character. The interview process also helped the customer to see Vistaar as being connected with the local community which could put the customer in a negative light, in case of a default.

The customers adhered to the loan terms because of the collateral. Usually, the collaterals had low fungibility and recovery value and did not reduce default risk. But the role of collaterals was as a means of moral suasion. It was true that Vistaar could recover financially to an extent from the collateral, but if the customer lost the property, then everything was lost. The design was that fear should dissuade the customers from defaulting.

Finally, collection was a critical challenge. Customers often dealt only in cash and had limited or no history of transactions with the banks. There was no group liability. Vistaar used a three-pronged approach:

Using collateral as a moral suasion at the time of approval. Close intercommunity relationships with the borrower community, created social pressure to repay. Show a credit literacy video that explained the benefit of on-time repayment, credit bureau record and importance of credit history. This helped to sensitize every customer on good repayment behaviour.

PRODUCTS

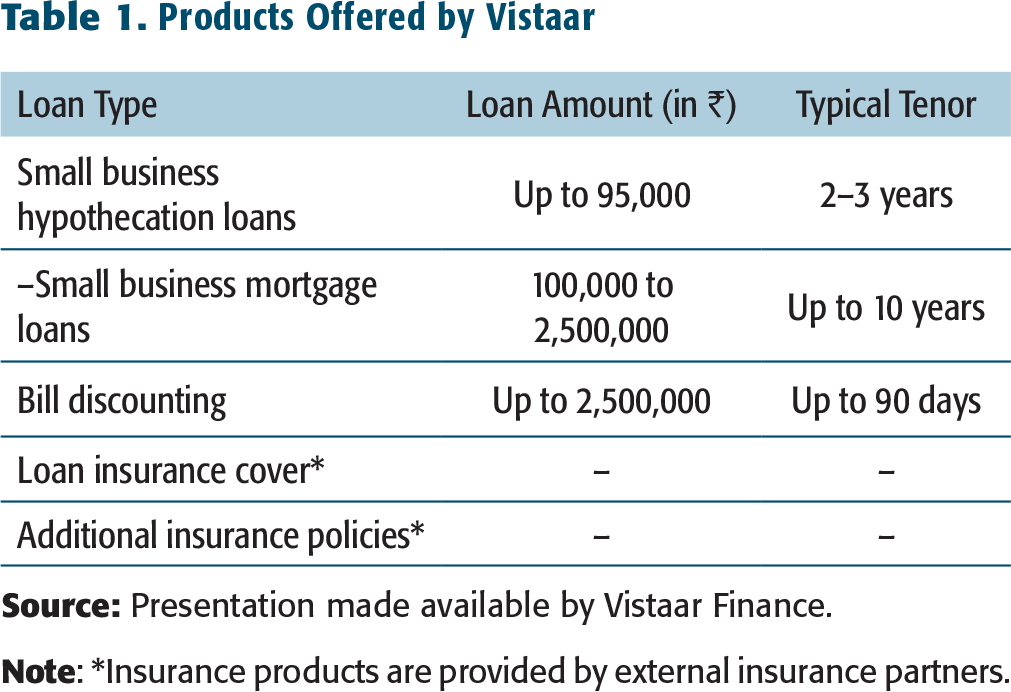

Products Offered by Vistaar

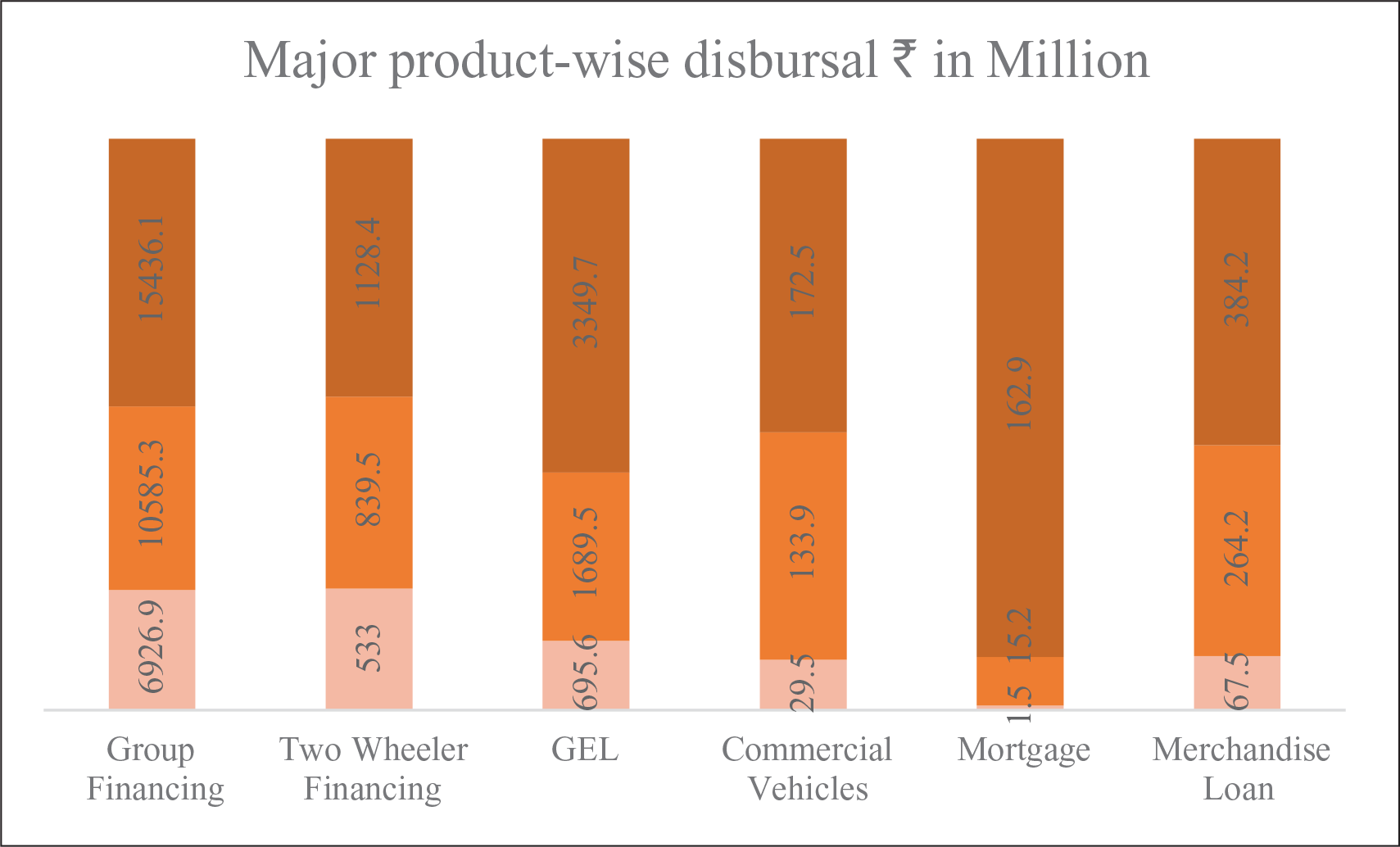

When Vistaar was founded, the majority of the portfolio was unsecured loans. However, the mortgage loan became popular and turned out to occupy a larger part of the portfolio. This helped Vistaar to de-risk the portfolio. Vistaar targeted to keep only about 20 per cent of the loan book as unsecured debt. In addition, Vistaar introduced a home loan product exclusive to Vistaar customers which would deepen the existing portfolio.

FINANCIAL PERFORMANCE

Vistaar: Financials (All Amounts in ₹ Millions)

CUSTOMER IMPACT

Vistaar support played a key role in increasing the profitability of the clients’ business. The businesses saw increased revenues through widening of product offerings and stocks (for stores), increased production capacity (small factories like power looms) and renovation and refurbishment of facilities (for small hotels and guest houses). The understanding of the business allowed Vistaar to provide for the real needs of each customer. It was able to make an impact in a way that made a difference to the customers. Some customers’ success stories are documented on the website (Vistaar Finance, n.d.).

CHANGES IN THE CONTEXT: THE LAUNCH OF MUDRA AND PMMY MUDRA AND PMMY

The thrust to expand banking services to the informal and small-scale enterprises was two-pronged and led by the government and RBI. In a surprise announcement, the Finance Minister, in his 2015 budget, announced the setting up of Micro Units Development and Refinance Agency (MUDRA) Bank.

While it was initially announced as a separate bank, it was established as a non-banking financial company (NBFC) and a subsidiary of SIDBI (Sriram, 2016). Along with the Pradhan Mantri Mudra Yojana (PMMY), MUDRA sought to bolster the activities of the MSME lenders in the country by providing financial, regulatory and technical support. Although both MUDRA and PMMY took off quickly, some doubts on the institution’s raison d’₹tre persisted. There were already banks and non banking financial institutions operating in the market with refinance from SIDBI. In addition there was a credit guarantee scheme that was operating effectively. In the light of these, the additional value of the new institutions and schemes were questionable.

Hegde believed that MUDRA was valuable to the ecosystem as a whole. However, Vistaar had not applied for any financial assistance from MUDRA. There was divergence in the objectives of MUDRA and Vistaar. Vistaar, while serving the underserved, was still a rent-seeking and profit-making organization. This meant that the pricing depended on the risk profile of the borrower rather than the business size. The safety of the loan was also defined by the collateral. The refinance from MUDRA would cap the pricing at a predefined annualized interest rate. While this was good for the ecosystem to enhance the acceptability of underserved customers, it did not help the business cause of Vistaar.

At the same time, Vistaar could not ignore the developments in the ecosystem. MUDRA was funding MFIs. Some of the MFIs were moving into individual loans for micro entrepreneurs. The limits per loan in the urban areas under the definition of microfinance had been enhanced, and MFIs were also free to lend up to 15 per cent of their portfolio to non-MFI sector. Older institutions like Fullerton and Indiabulls were active, and new institutions like Veritas were being set up. Some of the MFIs had become SFBs entering straight into the microenterprise sector.

So while opportunities were opening up for Vistaar, there were challenges too. Vistaar did not qualify for the SFB licence conditions of having a 10-year track record. But, at this point, Vistaar had to decide if they would be ready to apply for a licence when they qualified. With the licence for universal banks being available on-tap, there was an expectation that even SFB licences would be available on-tap. Any institution could apply for a licence if it believed that it qualified for becoming bank as per the specified guidelines. If Vistaar decided to choose this option, then the capitalization and operations would have to move in conformity with the requirements of an application while ensuring a smooth transition.

OTHER PLAYERS IN THE ECOSYSTEM

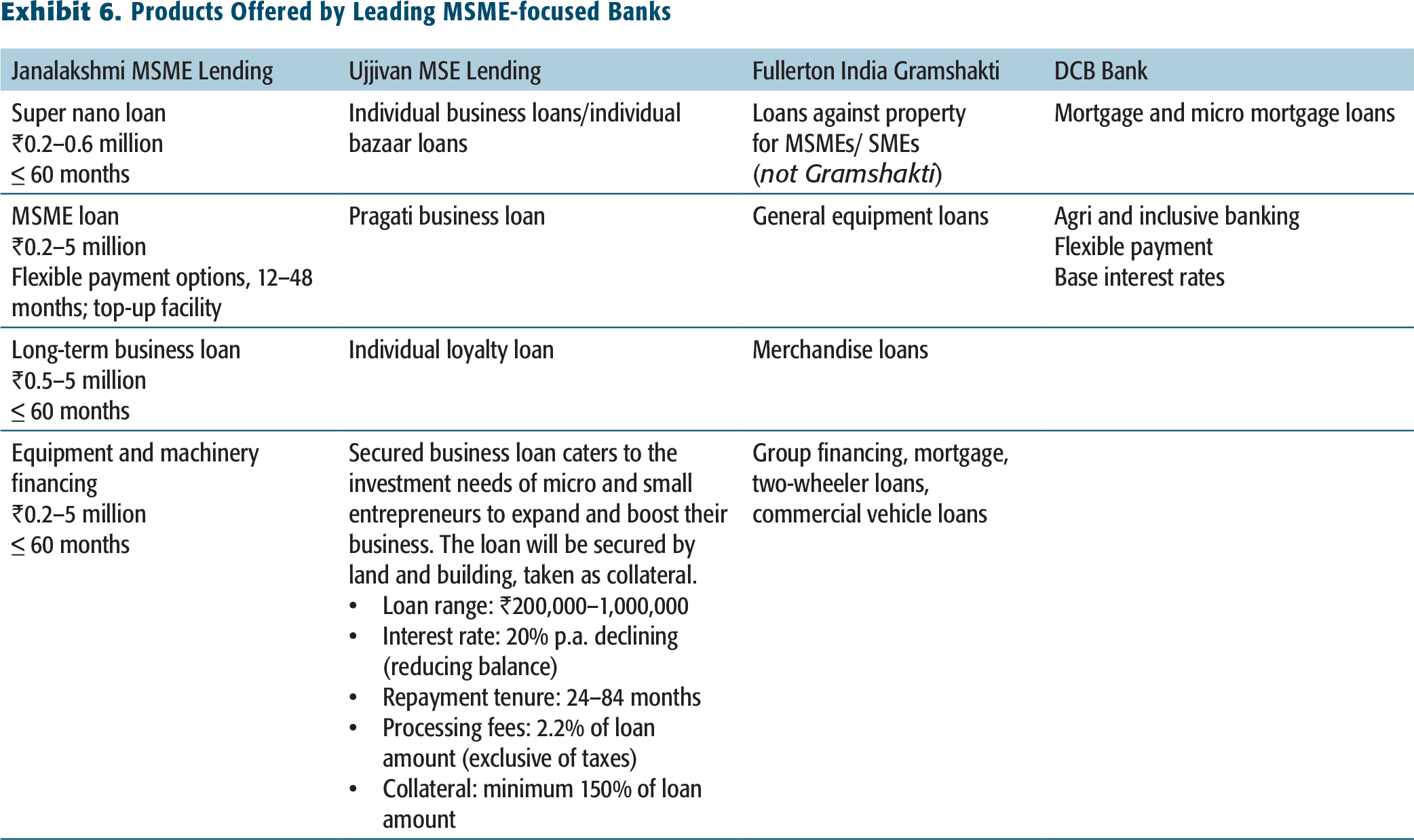

While there were many players in the sector, some were significant competitors of Vistaar. Ujjivan and Janalakshmi were MFIs that had recently become SFBs; they were headquartered in Bengaluru and had a very strong network in the geographies that Vistaar operated. Fullerton and DCB Bank were functionally competing with Vistaar. Bajaj Finance had its unique niche; AU SFB had growth potential and RBL Bank offered interesting products. Broadly speaking, the activities of these organizations with respect to MSMEs could be placed on a spectrum. On one end of this spectrum was the following operational set-up: targeted products designed specifically for small business owners, marketed through a dedicated MSME channel. This was typified by Janalakshmi. On the other end was a range of financial products of varying flexibility that could cut across retail, corporate and MSME lending, depending on the particular needs of each applicant. This was typified by Fullerton. Vistaar distinctly belonged to the former category. Details about the competitors are provided in Exhibit 5.

Details About Competitors

VISTAAR’S RESPONSE TO COMPETITION

With the increasing competition, Vistaar evolved a three-pronged strategy to compete in the market place and retain their position and grow the market share. These were:

Technology: They were rapidly digitizing all the processes and building artificial intelligence systems that replaced the manual processes which would increase efficiency and reduce operational risk.

Internal training processes built medium- and long-term employee capability and laid out career road map to retain the best employees. Investing in employees built their stickiness with the company.

Credit scoring algorithms would be increasingly used. Vistaar had more data than other players on MSMEs which could help it to assess customers in an objective way by setting parameters. As data increased, the model would be more reliable, putting Vistaar ahead of the curve.

Products Offered by Leading MSME-focused Banks

With increasing competition, Vistaar saw the introduction of innovative technologic solutions in the process as a fundamental source of advantage. There were different measures that were in the development phase. Vistaar was introducing tablets as an exclusive device to carry out and register transactions and planned to use this across all branches. This solution made processes efficient and effective in terms of time and transparency. It also reduced costs.

Vistaar was also planning to set up an internal data analytics department. The new department would mine the vast and exclusive data recorded since Vistaar’s inception. The insights from this could help Vistaar build new products and satisfy customers’ needs. Vistaar could use the data to better assess the customers’ ability to pay and would be able to deepen its current customers’ portfolio, while being aware of the risk profile of each business.

The last initiative of Vistaar, but not widely used, was a psychometric test to be administered on applicants, which was being developed in partnership with a partner specializing in analysing borrower behaviour.

Vistaar was a successful example of proactive entrepreneurship, an institution that decided to take up the challenge of tapping an unserved segment in an innovative way and did so profitably. However, there were also concerns on whether it was possible for technology to effectively substitute a direct human relationship.

It was in this context that the promoters were contemplating the growth path for Vistaar. Should they remain a specialized MSME financing enterprise, with their own internal models that would help them (as it has in the past) to continue servicing the existing and new customers or should they look at changing their model to go closer to the mainstream models—while retaining the knowledge-based uniqueness—and move towards cutting the costs on the liabilities side by becoming a bank. While there were advantages in preparing to be a bank, there were also significant compliance and business model restrictions. Hegde and Nishtala were looking at the next decade and the type of growth they should be targeting, given that many more SFBs were around and that there was MUDRA and PMMY in the ecosystem. They had to explore not only their own growth strategy but also figure out how they could use the developments in the ecosystem for their own growth.

DECLARATION OF CONFLICTING INTERESTS

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

FUNDING

The author(s) received no financial support for the research, authorship, and/or publication of this article.