Abstract

Executive Summary

This article examines the differential impact of ownership on the relative importance of corporate headquarters, industry, and business units on the performance of business units of firms in India. Different sets of owners have diverse objectives due to which there are variations in strategic choices resulting in the variance in performance of firms. This article first examines the extent to which variance in business unit performance can be attributed to ownership. It subsequently evaluates the relative importance of industry, corporate headquarters, and business units in explaining business unit performance variance of domestic firms and MNEs. The analysis for this article is based on a unique hand-collated database that contains details of the business units of domestic firms and MNEs operating in India. These details include business unit performance as well as the industry affiliation of the business unit. The article leverages multilevel analysis to understand the relative importance of the various effects. This analysis helps to know the magnitude of the various effects as well as their statistical significance. The results indicate that ownership is a significant institutional variable that explains business unit performance. An examination of the magnitudes of the effects also suggest that business unit effects and corporate effects are more important than industry effects in explaining business unit performance of firms operating in India. The magnitude of the business unit effects is greater than the corporate effects in the case of domestic firms. In the case of the MNE affiliates, although the magnitude of the corporate effects are greater than the business unit effects, this difference is not statistically significant. Overall, these results reinforce other empirical results that establish the importance of firm resources and capabilities in influencing firm performance as compared to the industry structure. These results are significant because in the Indian context, although studies have so far evaluated firm performance, they have not disaggregated the business unit and corporate headquarters effects. This article aligns the study of performance variance of Indian firms with those conducted across the globe and helps to compare how the relative importance of various effects vary. It makes an important contribution by including ownership in the study of business unit performance variance of Indian firms.

One of the longstanding and important debates in strategy literature has been on the relative importance of the industry structure and the firm’s resources and capabilities in influencing firm performance (Hawawini, Subramanian, & Verdin, 2003; Majumdar & Bhattacharjee, 2014; Misangyi, Elms, Greckhamer, & Lepine, 2006; Rumelt, 1991; Schmalensee, 1985). Researchers have found that the relative importance of industry, corporate, and business unit effects vary depending on the broad economic sector in which a company is participating, or the country in which the corporation is operating (Fitza, Matusik, & Mosakowski, 2009; Makino, Isobe, & Chan, 2004; McGahan & Porter, 1997; McGahan & Victer, 2010; Tong, Alessandri, Reuer, & Chintakananda, 2008). While this research has taken us a long way in understanding the effects of internal and external factors on performance variance of a firm, our understanding of how generalizable those findings are across various ownership categories are scarce. We intend to fill this gap by situating our study on multibusiness firms from Indian corporate landscape, an important big emerging market that has embraced pro-market reforms recently and become an attractive battlefield for foreign multinationals (MNEs) and vibrant domestic firms.

Different categories of owners have diverse ‘objective functions’ and this diversity gives rise to variance in their competitiveness, strategic choices and performance outcomes (Anderson & Reeb, 2003; Chacar & Vissa, 2005; Douma, George, & Kabir, 2006; Fitza et al., 2009; Woidtke, 2002). The differences in identities and attributes of persons in control of the firm result in a variety of relationships, those between the organization and the external environment, as well as the intra-organizational relationships (Heugens, Van Essen, & van Oosterhout, 2009; Pedersen & Thomsen, 2003). This also gives rise to differential resource endowments across organizations, intra-firm power relationships, and administrative structures that govern the intra-organizational relationships (Salancik & Pfeffer, 1980). While MNE subsidiaries rely on resources such as new products, technologies and managerial talent imparted by the corporate parent to overcome liability of foreignness (Zaheer, 1995) in the host country, domestic firms seek advantages from their knowledge of the local institutions, customer insights, and managerial capabilities. In this study, we seek to examine how ownership—foreign or domestic—determine the varying degrees of parenting advantage that different organizations possess in an important emerging economy (EE) like India.

We chose India as it has emerged as one of the largest and fastest growing economies in the world. After the deregulation, privatization and economic liberalization in the nineties, it has become an attractive destination for foreign direct investments. While diversity in knowledge sources, superior technology, and proven product-country image provide advantages to the MNEs; lack of local knowledge, networks and understanding of complex government, and native institutions create impediments to the survival and success of these multinationals.

The experience of a leading multinational consumer goods company illustrates the challenge: its revenue in India has grown by 7 percent compounded annually in the past seven years—almost twice the rate of the parent company in the same period. Nevertheless, the company’s growth rate in India is only about half that of the sector. (Choudhary, Kshirsagar, & Narayanan, 2012)

In the meanwhile, increasing competition in domestic markets (Dau, 2012) has motivated a great number of Indian domestic firms to transform themselves into emerging multinationals by successfully upgrading their skills and capabilities (Gubbi, Aulakh, Ray, Sarkar, & Chittoor, 2010). Therefore, studying the locus of performance bestows on us an understanding of how the differential resources and capabilities of the business unit, corporate parent, and industry factors contribute to the heterogeneity in firms. We believe that such an analysis would be an important addition to the strategic management literature.

We adopt the multilevel analysis to study the relative importance of the industry, corporate and business segments in explaining the variance in segment performance (Majumdar & Bhattacharjee, 2014). Multi-level analysis provides the advantages of using continuous variables even while teasing out the inherent multilevel or nested nature of business segment performance, without the disadvantages of the earlier techniques (Hough, 2006; Misangyi et al., 2006). We apply the multilevel analysis on a sample of 24,448 segment-year observations with varied number of segments both across time and corporates, spanning 2,121 corporations, and 72 industry classifications for the time period 2002–2013 to study impact of ownership on magnitudes and importance of various effects.

We find that across the various firms in India that report results for business segments, ownership of the firm is important in explaining firm performance heterogeneity. While the magnitude is lower than that of industry effects, the difference between the two is not significant. Examining the relative importance of the various effects across Indian domestic firms and MNE affiliates, we find that the prominence of the corporate headquarters is not always true and is contingent upon the ownership of the firm. We find that the corporate effects are greater than industry effects in MNE affiliates, and they are not smaller than business unit effects, whereas business unit effects explain greater performance variance of domestic firms. We argue that the degree to which the business unit sources its technologies, new products, and market information from the corporate headquarters and the external environment that it is situated in could contribute to the relative importance of corporate and business unit effects.

THEORY AND HYPOTHESES

Ownership influences the firm in myriad ways. Owners set up objectives for the firm congruent with their identities, traits, and characteristics (Hautz, Mayer, & Stadler, 2013). They endow the firm with resources and offer opportunities for further enhancement through their membership of various networks (Gómez-Mejia, Cruz, Berrone, & De Castro, 2011). For instance, there are huge differences in ownership advantages between foreign MNE affiliates and domestic home-grown firms. Foreign MNE affiliates enjoy ownership advantages related to technology (patents, R&D facilities, and new product development), marketing and management skills, expertise in managing oligopolistic industries and co-ordinating geographically dispersed business activities (Dunning, 1993). In a parallel literature on EE firms, scholars argue that these firms can benefit from their in-depth understanding of customer psyche, disproportionate access to managerial talent, non-economic assets such as political and business networks, and organizational structures that are optimized for working in markets with less or no formal institutions (Guillén & García-Canal, 2009). Furthermore, the objectives and resource positions of the firm vis-à-vis its competitors are reflected in the governance of the firm through the constraints imposed by the owners on the managers of the firm (Anderson & Reeb, 2003; Salancik & Pfeffer, 1980). State-owned enterprises, that is, firms controlled by governments, face multiple and conflicting objectives associated with economic (Stiglitz, 1986), sociological (Doyle, 1963) and political (Millward, 2011) benefits for the state. As a result, they have different ownership priorities compared to stand-alone private firms. In this article, we evaluate how ownership influences the relative importance of corporate and business strategy in explaining performance heterogeneity of domestic and foreign firms. The only notable study in this area is by Xia and Walker (2015) in the Chinese context, wherein they emphasize on analysing the interaction between ownership and region effects. In this article, we differ from this line of reasoning by evaluating ‘stylized facts’ pertaining to how ownership influences firms’ adoption of elements of either corporate or business strategy or relies on industry factors for their performance. To do so, we first evaluate if ownership effects are significant in the Indian context, and then analyse the relative importance of corporate, business unit, and industry effects of domestic and foreign firms. Next, we discuss the ownership effects of each of the major ownership categories of Indian businesses.

Government Ownership

Governments have invested in or established corporations for a number of reasons including addressing issues of market failure due to inadequate private capital, need for public control over scarce and valuable resources of national interest such as oil and energy, regional development, or redistribution. The persistence of these organizations has been attributed to organizational inertia and perpetuation of the interests of the ruling elite (Goldeng, Grünfeld, & Benito, 2008). Since such firms’ objectives are not explicitly oriented towards profit maximization, a number of principal–agent conflicts arise. In the past, these firms were shielded from competition, because they were either natural monopolies, or participation by the private sector was highly regulated, or the size of the private sector was smaller as compared to the public sector. Scholars have argued that since managerial incentives are not aligned with the performance of the firm and the other external mechanisms that could influence managerial behaviour, such as markets for managers, corporate control, and capital are not efficient, on an average, performance of government-owned or -controlled firms should be lesser than private firms. Moreover, these firms also suffer from inadequate monitoring due to incomplete adoption of corporate governance norms, and the presence of politicians as the mediators between the owners (electorate) and the managers of these firms (Cuervo & Villalonga, 2000). Therefore, we argue that the nature and essence of ownership advantages are quite different in these firms and hence these firms should be studied separately from other privately owned firms.

Private Ownership

India has historically been a mixed economy, where, although the state-owned or -controlled enterprises played a significant role in the economic activities of the country, the private sector was also encouraged to invest in certain industrial sectors and compete with the government-owned or -controlled firms (Bhagwati, 1993). With the reforms enacted by successive regimes in the country, private-sector firms not only have greater economic freedom to invest in industries that were previously restricted to them but also access to the resources that were otherwise controlled (Jalan, 2005). Private-sector firms in India are either family controlled, or have widely dispersed shareholding. These firms are organized either in the form of business groups or individual stand-alone firms (Douma et al., 2006). The identity of the private owner and the form of organization influence the resource endowments and governance of the firm. Family-controlled firms accord greater importance to affect related objectives as compared to other categories of owners (Gómez-Mejia, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007). They possess patient capital and are more likely to encourage investments that enable the firm to be passed on to the next generation in the family (Breton-Miller & Miller, 2006). This, hence, impacts the degree to which the firm is willing to lose control in order to gain external resources including financial, technological, and managerial.

Organizational forms evolve in response to market failures. The business groups in India are the outcome of the internalization of market failures for capital or labour. Business groups facilitate access to technology, as well as greater access to external networks that facilitate interaction with other important stakeholders such as the regulators and government agencies (Khanna & Palepu, 2000; Khanna & Rivkin, 2001; Manikandan & Ramachandran, 2015; Ramachandran, Manikandan, & Pant, 2013). Firms that are not affiliated to any business groups need to develop their own sources of technology from the ground up, as well as, rely on knowledge spillovers from domestic and foreign competitors (Kumaraswamy, Mudambi, Saranga, & Tripathy, 2012). Thus, variations in ownership and organizational form affect the knowledge bases of the firm, its relationships with various stakeholders, and access to various networks that result in performance heterogeneity.

Foreign Ownership

The launch of pro-market reforms in 1991 also eased entry of multinational firms (MNEs) into the Indian markets as compared to the command and control regime (Panagariya, 2010). There are multiple factors that affect firm performance in host countries. According to the OLI paradigm (Dunning, 1988), firm-specific advantages that accumulate over time are a result of market failures, and often result in accumulation of intangible assets (Bellak, 2004). The advantages due to market imperfections stem from the market power that MNEs enjoy through their strategic behaviour including collusion, oligopolistic reaction, and multimarket contact, especially important in case of imperfect competition in industries where markets are dominated by few firms (Bellak, 2004; Caves, 1996; Fuentelsaz & Gómez, 2006). Accumulation of intangible assets results in the superior performance of MNEs in the host country through the economies of scope, and through the rent-yielding, knowledge-based advantages that can be exploited at low marginal costs.

There are many factors that influence MNE performance, especially those related to liability of foreignness (Zaheer, 1995), liability of outsidership (Johanson & Vahlne, 2009), and distance between the home country and host country (Ghemawat, 2001). While diversity in knowledge sources, superior technology, and proven products provide advantages to the MNE in the host countries, lack of local knowledge, networks and understanding of institutions specific to the host country are likely to act as barriers to the performance of the firm (Luo, 2003). Moreover, since MNEs derive competitive advantage in the host countries from firm-specific advantages and governance practices and these are not uniform across all MNEs, it leads to MNE performance heterogeneity. MNE performance is also influenced by the nature of interaction (e.g., degree of autonomy) between the headquarters and host country affiliates (Ambos & Birkinshaw, 2010). Empirical evidence on the performance of MNEs in EEs is hence mixed, with some studies that claim a positive linear relationship between MNE characteristics and performance and others that posit curvilinear relationships. Douma et al. (2006) find positive relationship between foreign ownership and firm performance but Konings (2001) finds that this relationship is not uniform in Eastern European countries.

From our discussion based on literature thus far, we can clearly expect that ownership explains a significant percentage of performance variance of Indian firms. We hence, reiterate the following:

H1: Firms’ ownership type explains a significant percentage of variation in firms’ business unit performance variance.

Corporate Effects

Management of multiple activities in multiple locations is a complex task for corporations. It is typically achieved using multi-divisional structures comprising of divisions and subsidiaries (Chandler, 1991). The corporate headquarters coordinate between various divisions and subsidiaries. In the case of foreign subsidiaries, MNC headquarters whether global or regional, coordinate between the various foreign affiliates. Corporate headquarters play multiple roles in the organizational hierarchy that can be categorized as the value-creating or the entrepreneurial role and the loss prevention or administrative roles (Chandler, 1991; Menz, Kunisch, & Collis, 2015). They also have additional roles of parenting the business units or subsidiaries (Goold & Campbell, 2002), loss prevention to reduce the opportunistic behaviour of various business units, and minimize the agency costs due to delegation of decision-making authority (Bowman & Helfat, 2001; Eisenhardt, 1985). They are further important in the organization for their legal and compliance functions, which they achieve by representing the divisions or subsidiaries to external stakeholders and ensuring conformance to regulatory requirements; and increasingly, in providing shared services where scale economies are feasible (Menz et al., 2015). Corporate strategy, hence, has a significant role to play in firm performance regardless of whether the firm is a multi-business one or otherwise.

Business Unit Effects

Business units are the ‘quasi-autonomous’ operating entities of a firm that actually constitute the industry (Brush, Bromiley, & Hendrickx, 1999). In order to manage the complexities of a multi-business firm, firm activities are grouped along product or industry lines such that firms can realize economies of scale and scope as well as information-processing efficiency (Chandler, 1991). The aggregate of the performance of the business units after accounting for the corporate cost centres results in the firm performance (Brush et al., 1999). Hence, scholars have long advocated that studies examining performance variance should examine the business unit performance variance rather than firm performance (Rumelt, 1991). Scholars have also long argued that business units explain the greatest percentage of business unit performance variance, since it is the valuable, rare and inimitable resources and capabilities available to the business unit that aid the business unit in achieving superior performance that in turn translates to firm performance (McGahan & Porter, 2002).

Relative Importance of Effects

Empirical evidence indicates that corporate effects are significant in explaining performance variance. While initial studies (McGahan & Porter, 1997; Rumelt, 1991; Schmalensee, 1985) suggested that corporate effects were either insignificant or smaller as compared to industry effects, subsequent studies revealed that corporate effects were at least as important as industry effects (Misangyi et al., 2006), if not more important in explaining performance variance (Bowman & Helfat, 2001; Brush et al., 1999; Hough, 2006; Roquebert, Phillips, & Westfall, 1996). The consensus from the studies of performance variance until date is that business unit effects explain the greatest percentage of performance variance, followed by corporate effects and industry effects. Barring McGahan & Porter (2002), there are, however, few studies that have examined the contingencies under which the order of importance changes. In this article, we examine how the impact of ownership on the relative order of effects also explains performance variance.

Relative Importance of Effects for MNE Affiliates

According to the knowledge-based view of the firm, firms can be envisaged as ‘social communities that specialize in the creation and internal transfer of knowledge’ (Kogut & Zander, 1993). While this definition holds true for firms regardless of ownership, there are differences in the capabilities and routines developed by MNEs and domestic firms (Grant, 1996). The sources of knowledge for the MNEs are more diverse as compared to the firms operating in a single geography. Further, they develop capabilities and routines including managerial capacity within the firm that can absorb knowledge from these diverse sources and facilitate knowledge transfer from the affiliate to headquarters and headquarters to affiliates (Birkinshaw & Morrison, 1995). For the domestic firms, the knowledge sources are likely to be restricted to those developed in-house or from peer firms possibly resulting in a lower stock of knowledge as compared to the MNEs. This argument is often used to ease entry barriers and liberalize trade restrictions.

Foreign affiliates of MNEs have hence, two main dependencies. First, they are dependent on the corporate-parent to provide access to products, technology, and especially in the early stages, managerial talent. Second, they are dependent on the host country to provide infrastructure, inputs for production such as land and labour, insights into the customer, and facilitate its logistics, sales and distribution. Apart from these, the foreign affiliate also needs to adapt to the regulatory environment and competition in the host country. In EEs, the regulatory environment is marked by weak institutional mechanisms, ambiguity in legal enforcement, and uncertainty (Luo, 2003; Meyer & Peng, 2005). There is a certain degree of flexibility and responsiveness that needs to be built in to the interactions between the foreign affiliate and the host country environment, and, it is the strong relationship between the corporate-parent and the affiliate developed to transfer knowledge, capital, and other resources and processes including managerial that help it to reduce its dependence on the host country environment. According to the resource-dependence theory (Hillman, Withers, & Collins, 2009; Mudambi & Pedersen, 2007), in situations of unequal power arrangements, especially due to unequal control of resources that could help cope with environmental contingencies, the social actors with control over resources influence the actions of the organizations. Since the corporate-parent controls the resources that are critical to the functioning of the foreign affiliate in an uncertain environment, it is the corporate-parent that is in a position to influence the foreign affiliate’s decisions and actions.

Post the economic reforms initiated in 1991 in India, increasing number of industries are getting deregulated. The government is decreasing its intervention in markets by picking winners. Economic actors are gaining increasing agency, and markets are becoming contestable (Majumdar & Bhattacharjee, 2014). MNEs, hence, have greater freedom to choose the industries in which they want to operate. They also face lesser risks of expropriation (Rodrik, 2007). In conditions where forces distorting the markets are weaker, competing entities are likely to generate normal returns. Firms can fail in high-profit industries and succeed in low-profit industries due to their competitive advantages. When the entity possesses resources and capabilities that are rare, inimitable, valuable and non-substitutable, it can possess competitive advantage, irrespective of the industry (Barney, Ketchen, & Wright, 2011; Majumdar & Bhattacharjee, 2014). For MNE affiliates, the corporate parent provides these advantages in the form of technology, products and managerial capabilities. Empirical evidence from variance decomposition studies also suggests that corporate effects are greater as compared to industry effects (Majumdar & Bhattachejee, 2014; Roquebert et al., 1996).

We, hence, contend that because the corporate headquarters are responsible for some of the key strategic choices that impact the firm performance, such as diversification, internationalization, and investments in R&D, and it is the repository of capabilities, such as the ability to transfer technology, products and managerial talent:

Relative Importance of Effects for Domestic Home-grown Firms

Business units are the entities within a corporation that actually compete in the industry (Brush et al., 1999; Rumelt, 1991). While MNE affiliates possess advantages bestowed by the corporate parent in terms of superior technology, and products, they are unlikely to possess market information due to liability of foreignness (Zaheer, 1995). In contrast, since domestic firms are embedded in the fabric of the society in which they operate, they possess superior market information. They are hence, likely to have better market intelligence, knowledge of demographics, and hence, demand. In an EE like India, corporate functions like technological prowess and sophistication of products is still evolving. While the corporate headquarters collates and synthesizes market information provided by various business units, the chief repositories of the information are the business units. Further, since the business units of the firm have repeated interactions with the retailers, suppliers, customers, employment agencies, and other societal stakeholders where they operate, they are more likely to develop trust with these entities, acquire fine-grained information otherwise not available, and develop joint problem-solving arrangements that allow coordination and resolution of disputes without seeking legal recourse at all times (Uzzi, 1996; Uzzi & Lancaster, 2003).

Since the business units compete in the marketplace, they are likely to have greater competition-scanning capabilities. They are also likely to be better able to judge which of the resource configurations are likely to give them an advantage in the marketplace. Firms use indirect learning mechanisms such as reverse engineering, technology licensing, and recruitment of trained personnel from competitor MNEs to compete in the marketplace (Kumaraswamy et al., 2012; Li, Chen, & Shapiro, 2010; Liu, Lu, Filatotchev, Buck, & Wright, 2010). These activities are highly specific to the business unit of the firm rather than the corporate as a whole. While the corporate headquarters play a role in developing the organizational climate that fosters such learning activities, it is the business units that are the repositories of the outcomes of the learning process, and they integrate this learning to their business activities (Bowman & Helfat, 2001). Evidence from studies of variance decomposition of business unit performance also suggests that business unit effects are more important as compared to corporate and industry effects (Brush et al., 1999; Hough, 2006). We, hence, argue that the resources and capabilities that reside with the business unit have a greater effect on the business unit profitability as compared to the corporate headquarters or the industry structures.

METHODS

In this study, we emphasize methods that document relationships without specifying causality and thus, produce stylized facts for further research (McGahan and Porter, 2002; Schmalensee, 1985; Xia & Walker, 2015). We first analyse the relative contribution of ownership type to performance variance and then evaluate how the relative importance of business unit, corporate and industry effects changes with ownership type. One of the unique aspects of our study is that we analyse the business unit performance and thus disaggregate firm effects between corporate and business unit effects, in line with other studies using data from developed countries.

Data and Sample

We collect business unit-related data 1

We use the term ‘business unit’ and ‘business segment’ interchangeably in this study, in line with established literature like Roquebert et al. (1999). Business segments are composites of those business units whose accounting data can be aggregated meaningfully and reported in annual reports.

AS 17 of the Institute of Chartered Accountants of India mandates segment reporting by all listed firms and firms with turnover greater than Rs 500 million with effect from 1 April 2001.

NIC in India stands for National Industrial Classification, the equivalent of SIC in the USA—prepared by the Central Statistical Organizations, Ministry of Statistics and Programme Implementation, Government of India.

We discarded business segments described as ‘others’, since they are usually a residual to aggregate business units that might actually compete in different industries or cannot be meaningfully combined with other business segments of firms (McGahan & Porter, 1997). In accordance with prior studies, since the bases of profitability of financial firms are distinct from other firms, we excluded them and segments with no primary industry classification (McGahan & Porter, 1997, 2002). If observations in our database had missing information pertaining to key variables, we omitted such observations. In order to exclude observations that do not contribute to the profitability of the firm over time, we discarded segments with less than rupees five million in assets or those whose profitability exceeded 300 per cent or was less than –300 per cent, since they are often created for the spinoff of business units (Chari & David, 2012; McGahan & Porter, 1997). We did not modify the dependent variable observations in any other manner.

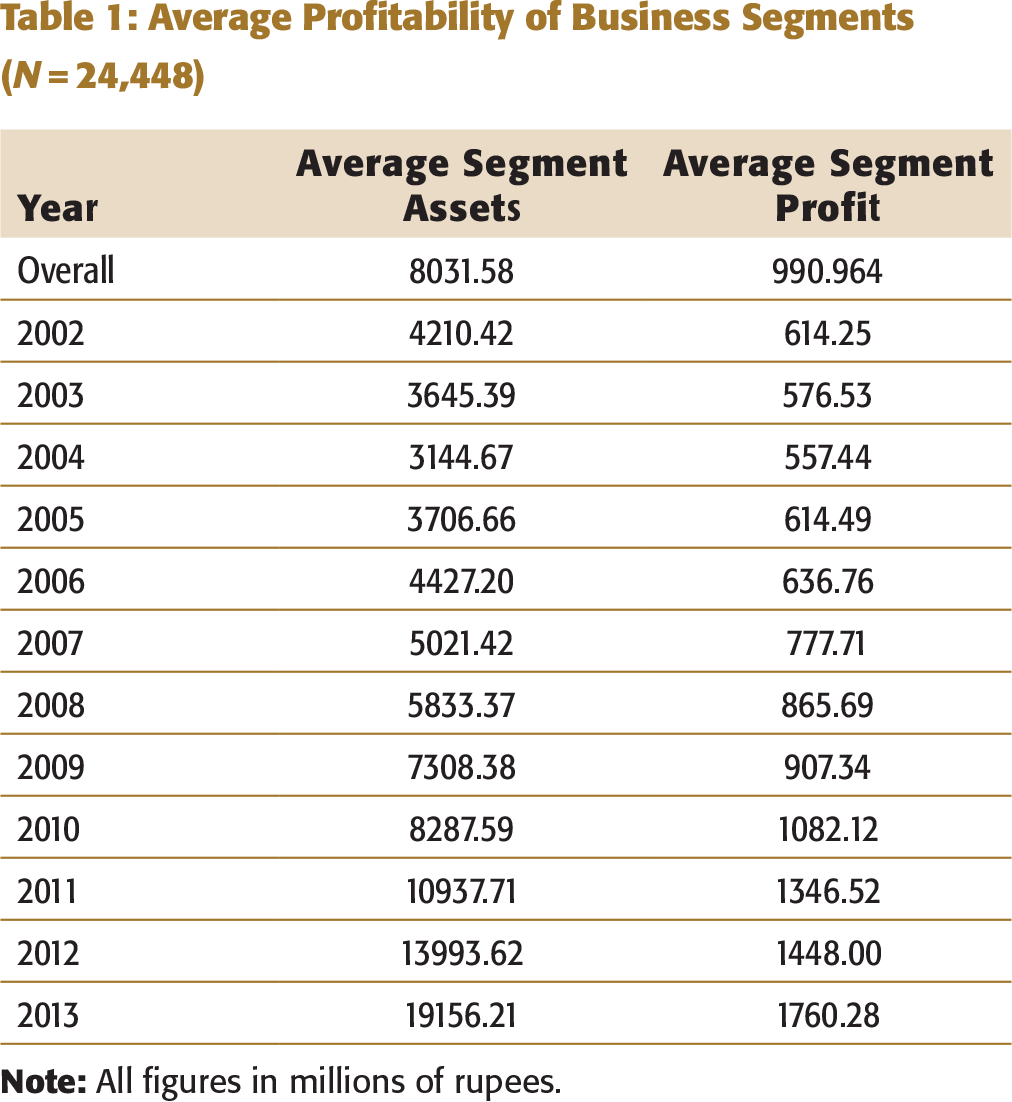

Our data set consists of 24,448 segment-year observations. These observations are nested within 2,754 business-segments, which are, in turn, nested within 2,121 corporations, two broad ownership categories, and cross-classified across 72 industry classifications. We utilize the ownership categorization provided by the Prowess database. The split of observations based on the ownership of the firm into foreign and domestic firms leads to 1,744 segment-year observations for MNE affiliates and 20,798 segment-year observations for domestic firms. While studying the relative importance of corporate and business unit effects in domestic firms, we only include the for-profit firms since the objectives of firms controlled by the government, either in the form of majority ownership, or joint venture or cooperatives are different from the for-profit firms (Boix, 2001; Heath & Norman, 2004). Due to the differences in objectives, the profitability of such firms might be influenced by factors other than firm characteristics and hence, we exclude them from this model. We define industry at the two-digit level, a widespread practice in published research on Indian firms (Lamin, 2013). Our data set consists of both diversified and undiversified firms.

Of the total 24,448 observations in our data set, the maximum of 9.36 per cent are from the manufacturers of chemicals and chemical products, 7.82 per cent from electricity, gas, steam, and air conditioning supply industry, 7.18 per cent from food processing industry, 5.20 per cent from the basic metals industry.

Average Profitability of Business Segments (N = 24,448)

Model Estimation

We decompose the business unit performance variance into components related to ownership, corporate, industry, and business unit effects. We use the multilevel analysis to examine the relative importance of the industry, corporate and business unit effects in explaining business unit performance. In this line of inquiry, many techniques have been used (Brush et al., 1999; McGahan & Porter, 2002; Rumelt, 1991), including, variance component analysis (VCA), nested analysis of variance (ANOVA) models, and two-stage least squares (2SLS). Although VCA has been used in previous studies (Roquebert et al., 1996; Rumelt, 1991), Hough (2006) has argued that this method might produce unreliable variance estimates or underestimate the true importance of an effect—or in some instances, even produce negative estimates. The estimates from the ANOVA analysis are based on the assumption of independent errors across categories, but the nesting of business units within the corporate headquarters leads to collinearity between corporate and business segment dummies (Bowman & Helfat, 2001), thereby violating the independent error assumptions.

Multi-level analysis addresses the disadvantages of VCA, nested ANOVA, and 2SLS even as it retains advantages like use of continuous predictor variables. The null or fully unconditional model where there are no predictor variables at any level is equivalent to the variance components model, but the estimation technique ensures that negative variances are not produced (Hough, 2006; Misangyi et al., 2006).

We follow Hough (2006) and Leckie (2013), to visualize business unit performance of MNEs and domestic firms as a three-level model with years at level one nested within business units at level two that are nested within the cross-classification of corporations and industries at level three, and in the case of analysing the ownership effects, the ownership category at level four. The following generalized equation represents SRoA as a grand mean with random effects for owner h, industry k, corporation j, business unit i, and time t represented by

In the case of MNE subsidiaries and domestic firms, the following model is used:

Variance partition coefficients are used to estimate the observed variance explained by each level of the hierarchy in the model (Leckie, 2013). We use the restricted maximum likelihood (REML) approach (Chang & Hong, 2002; Majumdar & Bhattacharjee, 2014). This method provides robust results even if there are fluctuations in sampling. Further, it allows us to make inferences about the estimation of the contribution that each factor makes to the overall performance variance, absolute and relative values of the variance components, as well as hypotheses testing. While testing the hypotheses, we evaluate if the variance associated with each of the effect is greater than zero and further analyse their relative importance.

General linear approaches like components of variances or ANOVA are limited by their inability to account for the interactions between the firm, industry, and group effects (Hough, 2006; Misangyi et al., 2006). The REML approach helps us through the nesting and cross-classification of effects to arrive at robust estimates of variance components.

RESULTS

Multilevel Analysis of Business Unit Performance

Summary Results of Inter-size Difference Tests

Tests of Significance

Using multilevel analysis, in addition to comparing the magnitudes of the various effects that could explain performance variance, we also test the significance of these effects, whether these effects are greater than zero. One of challenges in this testing has been due to the null hypothesis of the effect being zero, placing the true value of the parameter on the boundary of the parameter space (Snijders & Bosker, 2012). The REML method of computing standard error estimates helps in overcoming this issue (Rao, 1997).

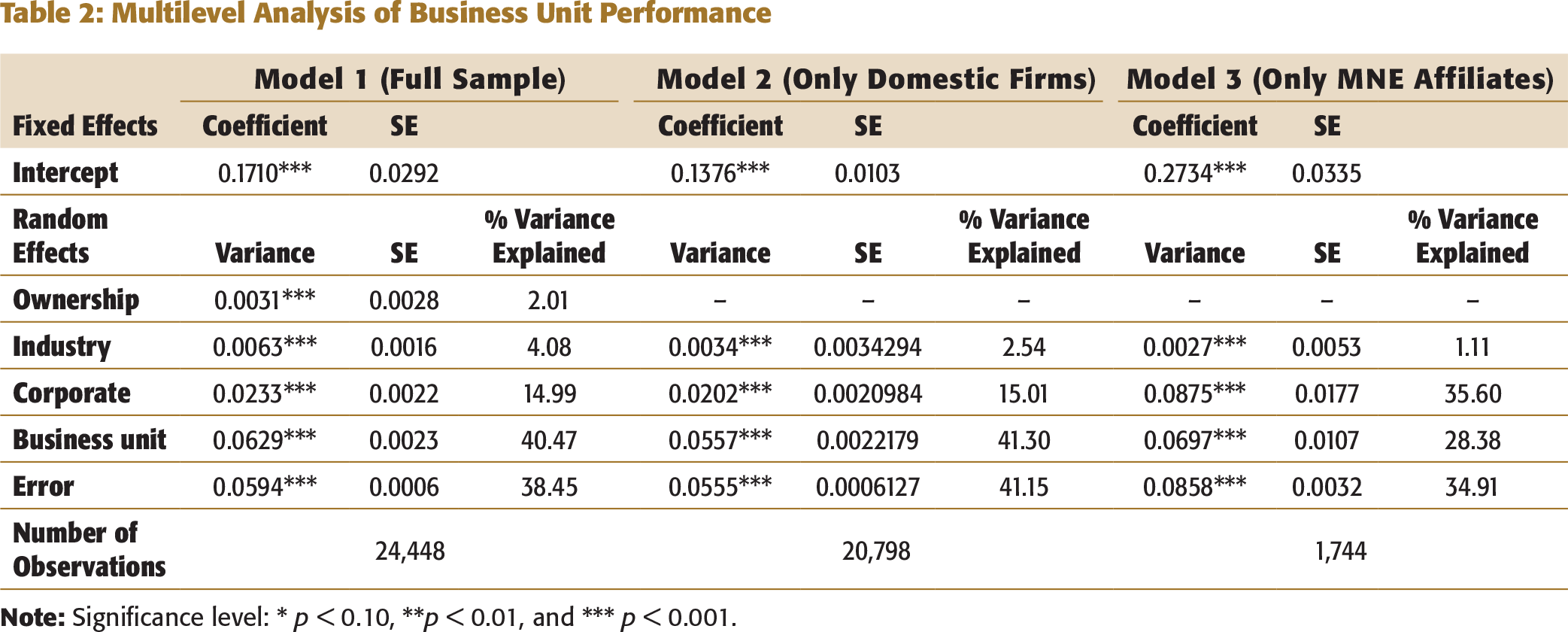

The tests of these hypotheses are summarized in Table 2. We find that all for the effects, ownership, business unit, corporate, and industry, we reject the null hypotheses

Comparison of Magnitudes

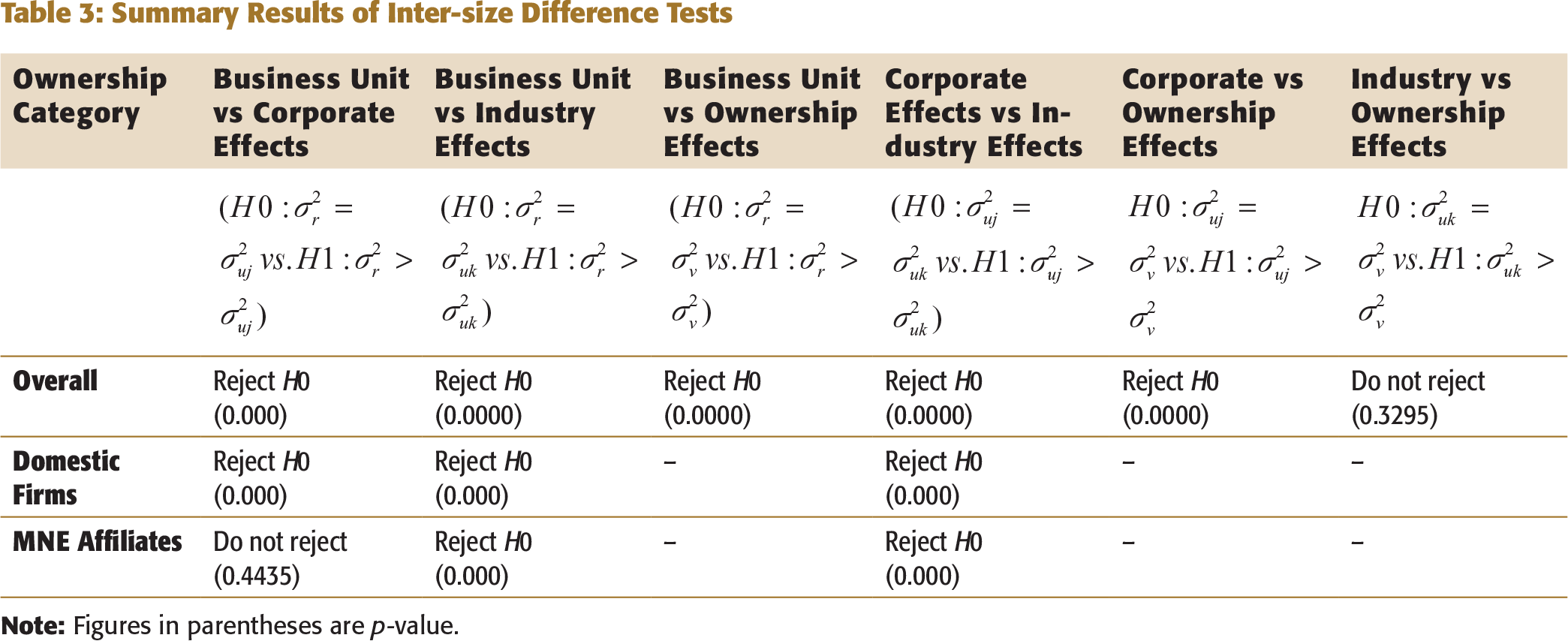

We compare the magnitudes of the various effects to evaluate their relative importance. The results of the tests are summarized in Table 3. We test for the null hypothesis that the magnitudes of effects are equal to each other. Testing for ownership effects, we find that we cannot reject the null hypothesis of equality between the ownership and industry effects. However, we find that we can reject the null hypothesis of equality between the various effects in all the cases.

Examining the tests of equality for various effects for MNE affiliates, we find that while industry effects explain the least performance variance, we cannot reject the null hypothesis of equality between corporate and business unit effects. However, corporate effects explain 35.60 per cent as compared to 28.38 per cent by business unit effects, although the difference in magnitude is not statistically significant. Overall, our results support H2a by highlighting that corporate effects are greater in magnitude as compared to industry effects and this difference is significant. Though such is true when compared with business unit effects, the difference is not statistically significant; thereby our results do not support H2b. Testing for the order of effects for domestic firms, we find that we can reject the null hypothesis of equality between various effects. This establishes that for domestic firms, business unit effects explain the greatest percentage of total performance variance, followed by corporate effects and industry effects explain the least variance. We thus, find support for both H3a and H3b.

DISCUSSION AND CONCLUSION

In this article, we evaluate the effect of ownership on the impact that the corporate headquarters has on the business unit profitability variance. We utilize multilevel analysis to model the hierarchical relationship between the ownership, corporate, industry, and segment effects allowing for the cross-classification between the corporate and industry effects. It allows us to use continuous variables and categorical predictors with a complex error structure allowing us to overcome the limitations of the VCA and nested ANOVA. By using the multilevel analysis, we also respond to the call by scholars in the area of international business to improve the accuracy of models with respect to context and lower level-effects (Peterson, Arregle, & Martin, 2012).

We find full support for two of our hypotheses, and partial support for the third. We find further empirical evidence for the significance of ownership effects for firms operating in India. We also find that the relative importance of corporate and business unit effects changes with ownership. We find only partial support for corporate effects explaining the greatest percentage for MNE affiliates’ performance variance, while establishing that business unit effects explain the greatest percentage of business unit performance variance for domestic firms.

Our study contributes a few insights into the impact of the ownership on the way firms are organized. While the finding that ownership effects are significant have been explored in other studies, notably Douma et al. (2006), these studies broadly distinguish between private Indian firms and MNEs. By including other ownership categories, we take a more comprehensive look at the different ownership categories, including public sector firms. Our finding of significant ownership effects indicates that these other ownership categories also need to be factored in while studying causal relationships between ownership and performance.

We also find support for our contention that the relative importance of corporate and business unit effects is not the same at all times and ownership is one of the factors that influences the relative importance. Studies of Indian firms thus far have not distinguished between the single- and multi-business firms. While the business strategy in the single-business firm cannot be distinguished from the corporate strategy, in multi-business firms, there is a clear distinction between the two. Business units are responsible for the market information and production activities of the firm. They determine the sources of competitive advantage through an understanding of the firms’ resource configurations and whether it lies in cost or differentiation advantages. Business units are competing in the market place. They have the information required to analyse the changes in the industry structure, competitors or the resources available. They have information on the changes in technology and the likely impact on firms. The importance of the business units is high in instances where they can assess the changes in the environment and respond to the changes.

However, due to liability of foreignness (Kostova & Zaheer, 1999; Zaheer, 1995), business units of MNEs cannot readily access some of the sources of information and some of the competitive responses are restricted to them. Where the role of corporate headquarters in determining performance of the foreign affiliates is increasingly gaining attention (Luo, 2003), especially in terms of knowledge accumulation and dissemination, the high corporate effects also denote the power residing with it. In EE countries like India, where there is still uncertainty and dynamism in terms of the external environment of the firm, MNEs would attempt to protect their intellectual property and production processes by concentrating information in the headquarters rather than give autonomy to the affiliates.

The contingent effects of ownership on relative importance of corporate headquarters and business unit effects has implications for the degree of decentralization within the organization, and the relative importance of corporate initiatives like diversification as against business strategies such as product differentiation and new product introductions. These results suggest that investigation of causal relationships along these dimensions would yield richer insights on determinants of performance of Indian firms.

While we make many contributions, our study is not without limitations that open up further avenues for research. This study does not establish causal relationships between the constructs of interest. The role of different ownership types such as business groups and state-owned enterprises and their influence on performance, organization structuring, and diversification decisions especially in the domestic context are worth pursuing. These are an important facet of Indian business and our results demonstrate that heterogeneity in corporate strategies adopted by firms are influenced by ownership of the firm. Further, family businesses are an important constituent of Indian economy, hence we urge future researchers to take such diverse ownership categories to take into account and enrich the literature. Notwithstanding the limitations, we have thrown some probing light on the importance of ownership structure in explaining business unit performance variance in India and covered significant theoretical and empirical ground with a hope to spark more research in the future.

ACKNOWLEDGEMENT

We are grateful to Professor Sougata Ray for his insightful comments on earlier versions of this manuscript.

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship, and/or publication of this article.