Abstract

Executive Summary

The competition among the organizations is increasing continuously and there has been a rapid shift in the business process deliverance. Financial service firms are striving to improve their business processes by liaising with customers to survive and compete successfully. The literature has obstinately emphasized on the utmost importance of trust and loyalty to survive in the financial sector. This study aims to explore the role of customer knowledge management (CKM) and satisfaction as antecedents of customer trust in the retail banking sector. The causal relationships existing between CKM, satisfaction, trust, and loyalty are explored. The mediating role of customer trust in the knowledge–loyalty and satisfaction–loyalty relationships is also explored. The data has been collected randomly from 412 customers of a private bank through survey by questionnaire. The research instrument has been developed and purified through factor analysis (confirmatory factor analysis). Structural equation modelling (SEM) has been employed to examine the causal relationship and fitness of the proposed model.

The findings of the study reveal that CKM and satisfaction positively impact customer trust, and customer trust has a significant impact on loyalty. Besides, trust partially mediates the effect of knowledge and satisfaction on loyalty. The findings of the study are valuable to managers and strategists in understanding customer need in order to formulate the relevant customer loyalty programmes. However, the study focused on retail banking sector and uses data from a single bank only. Future research may evaluate the generalizability of findings across other banks as well as other nationalities. The main contribution of this study is to the loyalty literature by empirically validating the identified antecedents and demonstrating their role in managing loyalty. Furthermore, the study provides some valuable insights into the relational exchanges between variables wherein some inferences are derived from results regarding trust and loyalty.

Keywords

Rowley (2002) has argued that trust is the fundamental entity that brings the partners together in a relational system and makes them comfortable for a business transaction. Trust is built through continuous transactions and interactions (Oliver, 1999; Reichheld & Schefter, 2000) but the key determinant of trust is associated with the usage of customer information and knowledge by the business organization (Jarvenpaa, Knoll, & Lediner, 1998). Smith and Barclay (1997) have opined that customer satisfaction is an important outcome of buyer–seller relationships. Development of trust among customers is achieved through proper investment in buyer–seller relationships (Gundlach, Achrol, & Mentzer, 1995). Accordingly, Vuuren, Roberts-Lombard, and Tonder (2012) have studied trust, satisfaction, and commitment as the determinants of loyalty in service sector. However, little research has been carried out on CKM and customer satisfaction as the determinants of trust in banking sectors.

CKM is the key for nurturing customer relationships, yet banks find themselves locked out at some critical points in customer’s decision-making process (Lavender, 2004). Business information is one of the important aspects of maintaining existing and prospecting relationships with customers. A good business information solution will allow relationship managers to specify the information they require for creating a regional, national, or even global database of customers. The more knowledge a relationship manager of a bank has about its customers, greater the chance of turning a prospective customer into a client (Lavender, 2004). Given the current competitive business environment, customer loyalty is vital and a scarce resource which should be utilized such that there is long-term profitability (Fang, Chang, Ou, & Chou, 2014; Melnyk & Bijmolt, 2015). It is easier to speed up purchases from existing customers than new ones (Naidu et al., 1999). Therefore, customer loyalty is a complex phenomenon which is not only affected by a single variable but a whole set of variables pertaining to customer. In this backdrop, the study contributes to the loyalty literature by empirically validating the identified antecedents and demonstrating their role in managing loyalty which the prior studies have not yet exhibited.

OBJECTIVES

The present study has been carried out to explore the impact of CKM and customer satisfaction on customer trust and loyalty. The study also attempts to analyse the mediating role of customer trust in the relationship between knowledge management and loyalty, and customer satisfaction and loyalty.

LITERATURE REVIEW AND HYPOTHESES DEVELOPMENT

Customer information helps banks to develop strong bonds of trust and commitment with customers by taking into account honesty, reliability, fulfilment, competence, quality, credibility, and benevolence (Kantsberger & Kunz, 2010; Sirdeshmukh, Singh, & Sabol, 2002). Rowley (2002) has argued that trust can be built through proper utilization of customer knowledge and information. It was further opined that trust and loyalty are closely related to each other, as there is no loyalty without trust. Researchers have identified a dynamic relationship among customer knowledge, trust and loyalty, where trust is recognized as a key mediator in the successful relationships with customers (Doney & Cannon, 1997). Kracklauer, Mills, and Seifert (2004) have suggested that loyalty should be regarded as a combination of customer satisfaction and customer trust. In the Malaysian banking sector, Ndubisi (2007) has evaluated the relationship of four constructs (commitment, trust, conflict handling, and communication) on customer loyalty. Results of the study reveal that the four constructs have a positive impact on customer loyalty. Very few studies have shed light on customer trust as an antecedent of loyalty; and customer satisfaction and CKM as determinants of customer trust.

IMPACT OF CUSTOMER TRUST ON CUSTOMER LOYALTY

Customer loyalty is crucial for both organization and customers. A comprehensive definition of loyalty has been formulated by Oliver (1999, p. 34), ‘a deeply held commitment to rebuy or re-patronize a preferred product/service consistently in the future, thereby causing repetitive same-brand or same brand-set purchasing, despite situational influences and marketing effort having the potential to cause switching behaviour’. Customer trust influences customer loyalty, so the higher the customer trust is, the higher is the customer loyalty (Bagram, 2010; Jarvinen, 2014; Paulssen, Roulet, & Wilke, 2014). Many researchers have considered the role of trust in development of quality relationship (Dahlstrom, Nygaard, Kimasheva, & Ulvnes, 2014) along with customer satisfaction. Trust has also been conceptualized as a powerful feature of relationship management (Anderson, Lodish, & Weitz, 1987), a source of believability and honesty (Zeithaml, Barry, & Parasuraman, 1996) and a tool of communication between parties. Doney and Cannon (1997) suggested that perceived service quality has significantly positive association with trust, and trust has significantly positive relationship with loyalty. Ranaweera and Prabhu (2003) opined that trust is a stronger emotion than satisfaction and therefore better predicts loyalty. They have also argued that trust has a positive impact on retention/loyalty. Hsu (2007) has observed a positive effect of trust on loyalty thereby helping in attracting new customers and later in retaining existing ones besides influencing overall satisfaction. On the basis of evidences stated previously, the following hypothesis has been proposed:

H1: Customer trust is positively related to customer loyalty

Impact of Customer Knowledge Management on Customer Trust and Satisfaction

CKM is a valuable asset for any organization. Gathering, managing, and sharing customer knowledge can be a valuable competitive action for organizations (Murillo & Annabi, 2002). CKM refers to the firm’s understanding of current and future customer’s needs and preferences (Lee, Naylor, & Chen, 2011). CKM refers to facts, philosophies, and processes for effective handling of relationship encounters with customers and creating a positive image in the mind of customer towards the enterprise (Motowidlo, Borman, & Schmit, 1997). CKM prompts to provide customer insight, profiles, habits, contact preferences, and understanding to improve an organization’s contact with the customer, which will enhance satisfaction and loyalty among customers (Xu & Walton, 2005). Mithas, Krishnan, and Fornell (2005) have argued that CKM derives customer satisfaction by tailoring the firm’s offerings to suit customer requirements. Customer data can be used as a platform by customer relationship management (CRM) systems for communication, creating loyalty, customer service and satisfaction, trust cultivation and relationship maintenance in banks (L. K. Patwa & K. K. Patwa, 2014; Pillai, Brusco, Goldsmith, & Hofacker, 2015). Oliver (1999) has argued that trust can be developed among the customers through proper management of customer information and knowledge. The information generated by CKM system can be utilized by the bank for creating a sense of trust and commitment among customers. CKM processes enhance speed and effectiveness of a firm’s customer response (Jayachandran, Hewett, & Kaufman, 2004) which increases perceived value and decreases customer defection (Bueren, Schierholz, Kolbe, & Brenner, 2005). Peppers and Rogers (2004) have stressed that winning customer trust has become a herculean task for enterprises to build a long-lasting relationship with customers. This is possible through customer knowledge and information which provide capability to differentiate one customer from another. Deficiency in information and knowledge affects trust between the two parties. Nevertheless, the usage of customer information for the purpose of improving the value of customer relationships appears to be an area in need of development.

According to Anderson and Weitz (1989, p. 312), trust is ‘one party’s belief that its needs will be fulfilled in the future by actions undertaken by other party’. From a banking perspective, trust is important for the development of relationship between customer and bank (Hoq, Sultana, & Amin, 2010; Jan & Abdullah, 2014). The recent financial crisis has brought to light the role of customer trust in the banking industry. Interest towards the area of study has grown recently and is now considered as an essential element of the relationship development in banking sector (Yee & Yeung, 2010). Indeed, associated feeling of security is an effective means to retain existing customers and attract new ones (Behram, 2005). Bradach and Eccles (1989) have argued trust as a control mechanism that aids in emergence of positive relationships thereby suppressing uncertainty, vulnerability, and dependence. Many researchers have regarded trust as the central construct in customer loyalty and repurchase intentions (Sirdeshmukh et al., 2002). Accordingly, Morgan and Hunt (1994) consider trust critical to the studies dealing in the management of customer loyalty. They have emphasized the importance of trust in the relational exchange, since relationships characterized by trust are highly valued by both the parties. On the basis of the aforementioned evidences, following hypotheses have been proposed:

H2: CKM is positively related to customer trust

H3: CKM is positively related to customer satisfaction

H4: Customer trust mediates the effect of CKM on loyalty

Impact of Customer Satisfaction on Customer Trust

Customer satisfaction is defined as ‘the customer’s response to the evaluation of the perceived discrepancy between prior expectations and the actual performance of the product/service as perceived after its consumption’ (Tse & Wilton, 1988, p. 204). The literature regarding satisfaction and trust has revealed a mixed response towards the two concepts. One school of thought considers trust as the antecedent of satisfaction (Andaleeb, 1996; Geyskens, Steenkamp, & Kumar, 1998) while the other school of thought considers satisfaction as the determinant of trust (Ganesan, 1994; Johnson & Grayson, 2005; Pelau, 2008). Geyskens et al. (1998) on the basis of meta-analysis in a channel marketing context has suggested satisfaction as the predecessor of trust. Evidently, the present study considers satisfaction as an antecedent of trust. Johnson and Grayson (2005) have observed that the experience of a certain level of satisfaction potentially contributes to the perception of both cognitive and affective trust. Trif (2013) has observed a positive and strong association between overall customer satisfaction and customer trust. This adds to the argument that customer satisfaction and customer trust are significantly related to customer loyalty. Yap, Ramayah, Nushazelin, and Shahidan (2012) provide empirical evidence that satisfaction has a positive effect on trust and the trust in turn has a positive influence on loyalty (Bendall-Lyon & Powers, 2003; Lam & Burton, 2006). Most of the research models dealing with satisfaction or loyalty possess trust as an important determinant (Verhagen, Meents, & Yao-Hua, 2006). From a banking perspective, trust is one of the key elements in relationship development between the bank and the customer (Hoq et al., 2010). It is also regarded as one of the mediating variables and has a positive impact on customer loyalty (Ball, Coelho, & Machas, 2004). In the light of the aforementioned information as presented in the literature, the following hypotheses have been proposed:

H5: Customer satisfaction is positively related to customer trust

H6: Customer trust mediates the effect of customer satisfaction on loyalty

H7: Customer satisfaction mediates the effect of CKM on trust

PROPOSED RESEARCH MODEL

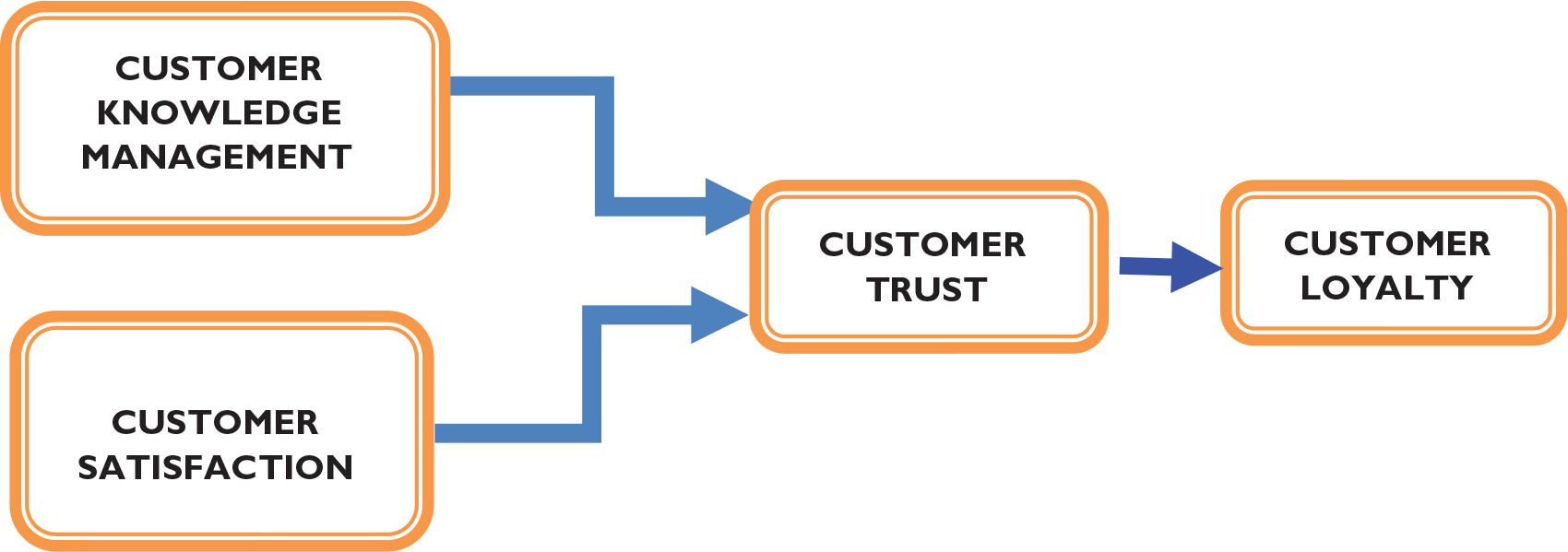

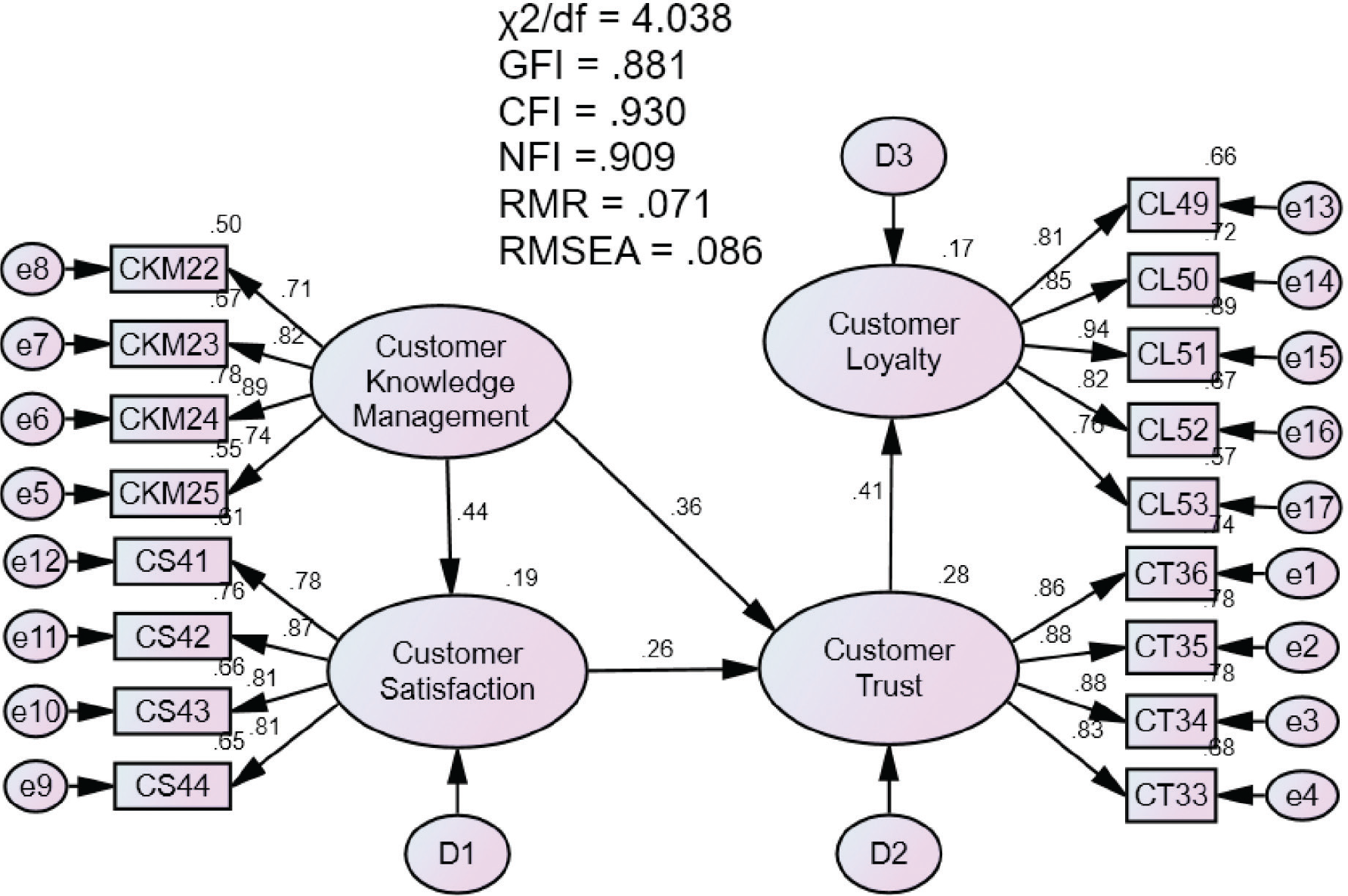

The model of the study has been developed based on the review of literature and existing research gaps. Four variables—CKM, satisfaction, trust, and loyalty have been identified. CKM and satisfaction are presumed as independent variables which can affect customer trust (intervening variable). The customer trust can affect customer loyalty which is presumed as a dependent variable. In order to test the various causal relationships between variables in the model, structural equation modelling (SEM) was employed. First, the measurement model was developed. Then, the structural model was tested and various path estimates were determined. The hypothesized relationships among the variables are depicted in proposed model (Figure 1).

Proposed Research Model

METHODOLOGY

Research Population and Sample

The study was conducted in 2015–2016 at one of the major private sector banks of India. The bank was chosen for the study as it was the first bank to implement the CRM strategy in Jammu and Kashmir. The study examines the CRM strategy and investigates whether its implementation led to improvement in the satisfaction and loyalty in bank customers. The area (geographical) of study was Jammu and Kashmir consisting of 67 branch units in the state (at the time when this study was carried). Data was collected from customers of the bank. Researchers directly approached the respondents and those not approachable were contacted via e-mail for data collection. The survey has been conducted in two divisions of the state, that is, Jammu division and Kashmir division. 1

The state of Jammu and Kashmir comprises of three geographical regions: Jammu, Kashmir, and Ladakh. This particular bank has operations only in the Jammu and Kashmir region.

Cluster sampling technique was employed for selecting the desired sample. Basically, the bank’s branch network was divided into six clusters of which two clusters were selected randomly. All the branches in these clusters were included in the study. However, since the customer volume was very high, simple random sampling was undertaken to select respondents. Therefore, cluster sampling was employed to select business units and simple random sampling was applied to select individual respondents. The sample size was determined on the basis of following assumptions:

Most researchers consider a sample size of 200–500 respondents adequate for most of management researches (Hill & Alexander, 2002; Tabachnick & Fidell, 2007). The sample size can be determined on the basis of number of items in questionnaire, that is, for each item, 5 to 10 respondents are adequate (Hair, Anderson, Tatham, & Black, 1998).

Based on these, 440 questionnaires were distributed among the customers of the bank. About 423 questionnaires were received, of which 11 were rejected as they were incomplete.

Questionnaire Development and Data Collection

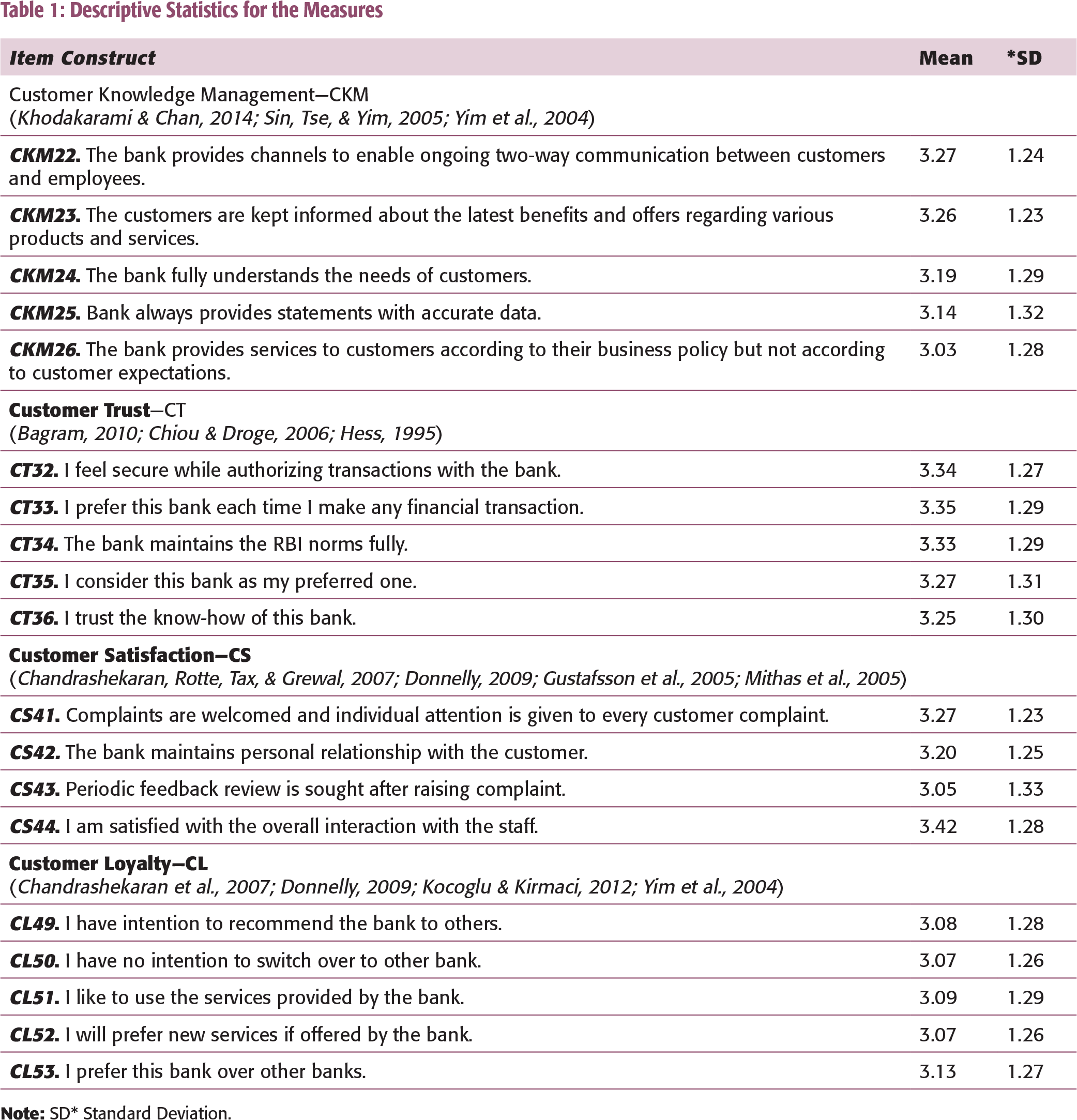

Descriptive Statistics for the Measures

Common Method Bias

Common method bias (CMB) arises when multiple constructs are measured using a common method (multiple item scales present within the same survey). When respondents are asked to give their perceptual response on two or more constructs in the same survey, it may produce a spurious correlations among the items measuring these constructs owing to response style, social desirability, and priming. These correlations are actually different from true correlation among the measured constructs (Kamakura, 2010). For this study, the Harman Single Factor Score was used to identify any bias in the measurement instrument (Harman, 1960). Exploratory factory analysis was performed to load all the items into a single factor to examine unrotated factor solution. All the items were loaded in a single factor that explains 42.23 per cent of the total variance. Since, the total variance explained by the single factor is less than 50 per cent; it suggests that CMB does not affect data and the results (Podsakoff, MacKenzie, Lee, & Podsakoff, 2003).

Confirmatory Factor Analysis (CFA)

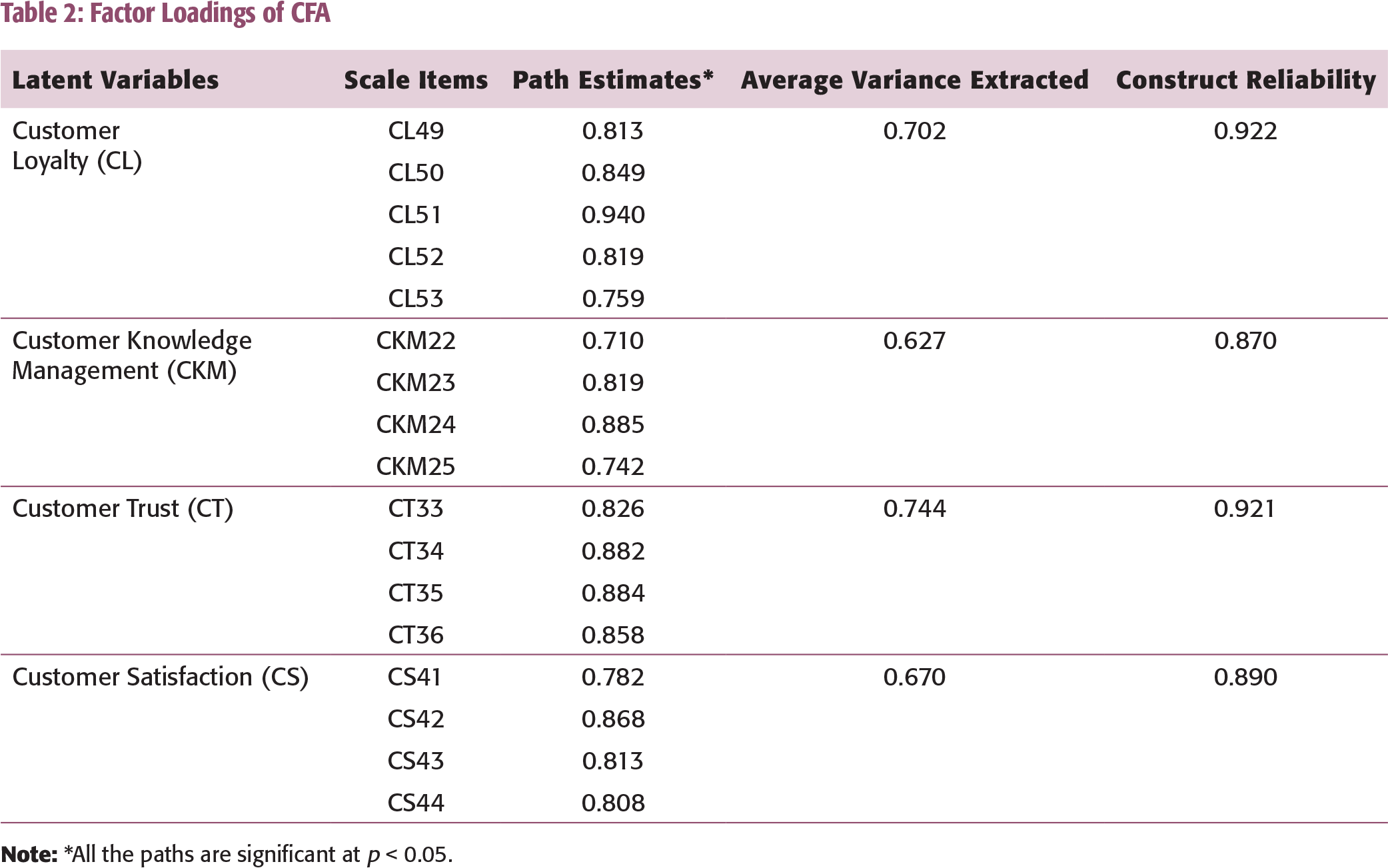

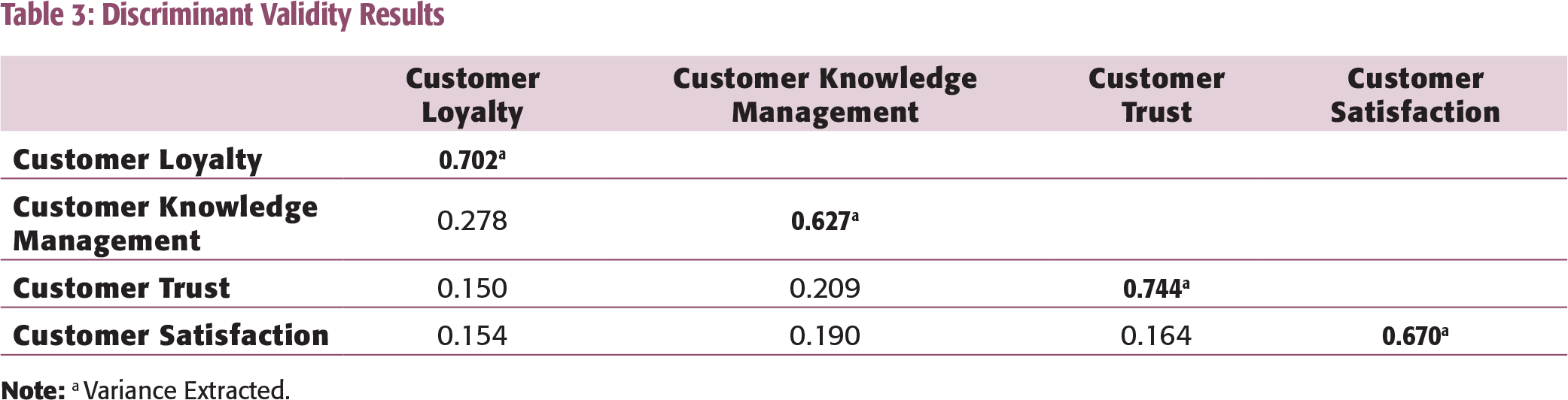

CFA was also performed to confirm the uni-dimensionality of measurements. For the assessment of CFA, various goodness and badness indices, and the model fit summary were followed (Chau, 1997). The various fit indices used for the assessment of measurement model include—χ2/df (< 2 is good and 2–5 acceptable); goodness-of-fit index (GFI > 0.90 is good and > 0.80 acceptable); normed fit index (NFI > 0.90); comparative fit index (CFI > 0.90); root mean residual (RMR < 0.10) and root mean square error of approximation (RMSEA < 0.10). Factor loadings are standardized regression weights of variables with its items. While, loadings above 0.70 are considered good, a loading above 0.60 is also acceptable (Hair et al., 1998). The significantly good loading of the items provides an evidence for convergent validity, so average variance extracted (AVE), construct reliability (CR), and discriminant validity (DV) were calculated (Table 2). Standardized loading estimates should be at least 0.5 or higher, and ideally 0.7 or higher; AVE should be 0.5 or greater to suggest adequate convergent validity; CR should be 0.7 or higher to indicate adequate convergence or internal consistency; and for DV, the square of the correlation between factors should not exceed the variance extracted (Fornell & Larcker, 1981), which indicates the degree to which measures of conceptually distinct construct differ.

Factor Loadings of CFA

Discriminant Validity Results

STRUCTURAL EQUATION MODELLING RESULTS

The various causal relationships hypothesized in the study were tested. The hypotheses test was performed using structural path modelling with customer trust and loyalty as the dependent variables, and CKM and satisfaction as independent variables (Figure 2).

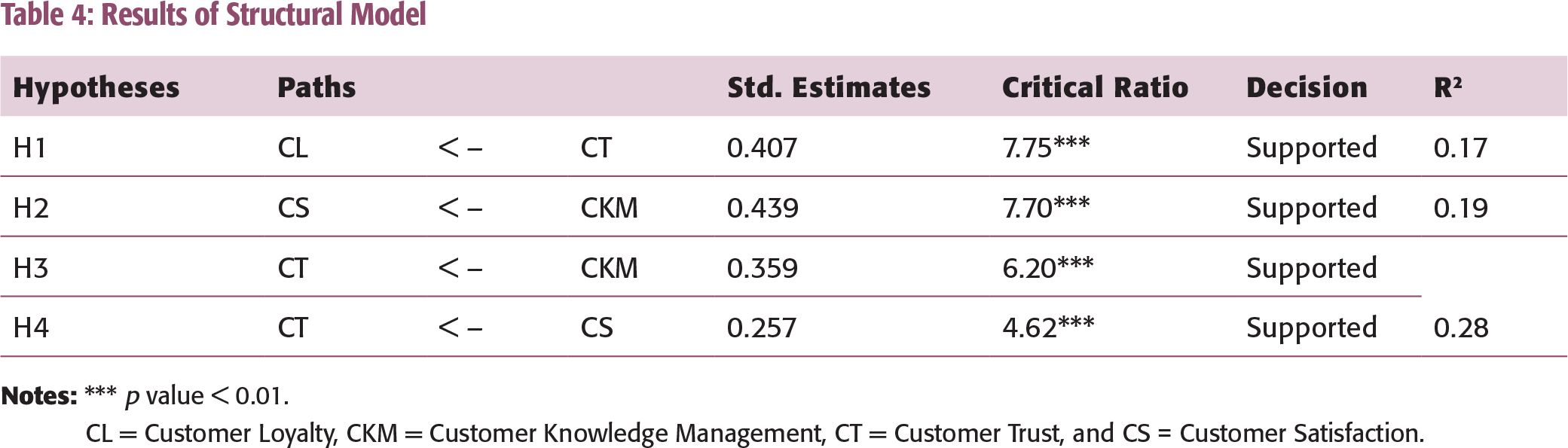

The analysis procedure for testing hypotheses requires evaluation of model summary to check whether hypothesized model fits the data and is in accordance with the proposed conceptual model. In addition, significance of the parameter estimates was evaluated through regression estimates, critical ratio, and coefficient of determination (R2). The results indicate that hypothesized model fits the observed data well (Figure 2). The fitness indices of the present model, that is, χ2/df = 4.03, GFI = 0.88, CFI = 0.93, NFI = 0.91, RMR = 0.07, and RMSEA = 0.08 shown in model summary are good and fall in the acceptable limits. Furthermore, all the structural paths were statistically significant (p < 0.05) with regression estimate above 0.20. Interestingly, all hypotheses are supported (Table 4).

Structural Model Showing Various Causal Relationships

Results of Structural Model

CL = Customer Loyalty, CKM = Customer Knowledge Management, CT = Customer Trust, and CS = Customer Satisfaction.

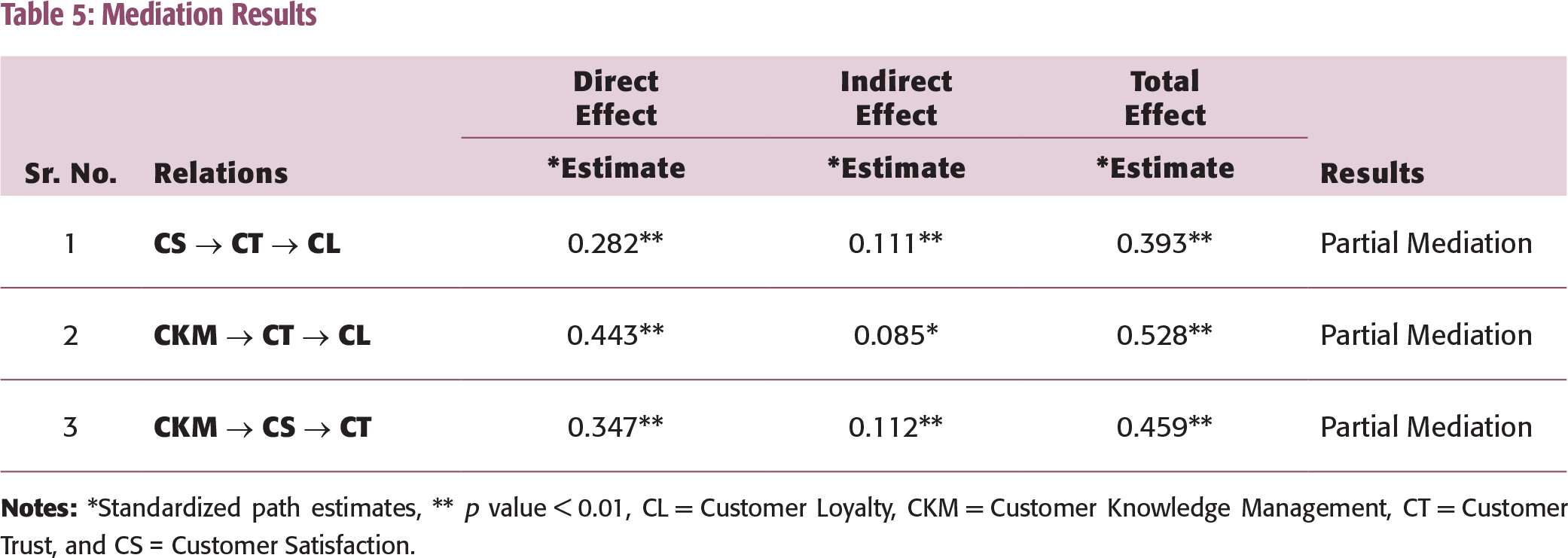

For testing the H4, H6, and H7 mediation, analysis was performed through bias-corrected percentile bootstrap with 95 per cent confidence interval to get standardized effects. However, it is imperative to note that H4, customer trust mediates the effect of CKM on loyalty was partially accepted. Detailed results of the hypotheses and other parameters are shared in Table 5. Similarly, for mediation hypothesis H6 and H7, the result of direct and indirect path estimates are summarized in Table 5. It reveals that customer trust acts as partial mediator between customer satisfaction and loyalty. And customer satisfaction partially mediates the effect of CKM on customer trust. The reason is that both customer satisfaction and CKM exerts substantial (around half of total effect) and significant indirect effect, thus suggesting partial mediation. Furthermore, the direct paths are still significant in presence of the mediator. If the direct path becomes insignificant in presence of the mediator; it is then termed as complete mediation (Hair, Black, Babin, & Anderson, 2010). In this case, Hair et al. (2010) and Kline (2011) recommended that when both direct and indirect paths are significant, standardized indirect effect be divided by standardized total effect. If the outcome is more than 50 per cent, then there is evidence of full mediation. Alternatively, if it is below 50 per cent, then it is treated as partial mediation.

Mediation Results

It was found that CKM and customer satisfaction significantly explain more of the variance in customer trust (R2 = 0.28) than customer loyalty (R2 = 0.17) and CKM explains only 19 per cent of variance in the customer satisfaction (R2 = 0.19). Customer knowledge and customer information can be used as an instrument by banks to galvanize and melds all units of the bank to build a strong corporate outlook by enhancing satisfaction, cultivating trust, building loyalty, and maintaining cordial relationship with customers (L. K. Patwa & K. K. Patwa, 2014). The findings are also in coherence to the fact that companies which do not use customer knowledge for developing and improving products or services might lose their customers to other banks. It was also revealed from the structural model that CKM is the strongest predictor of customer satisfaction, and customer trust is that predictor of customer loyalty. The finding can be justified by the fact that there could be a mediating variable between customer satisfaction and customer loyalty which strongly clubs the relationship between satisfaction and loyalty (Neal, 1999; Sirdeshmukh et al., 2002).

The study depicts that customer trust acts as a partial mediator between ‘CKM → customer loyalty’ and ‘customer satisfaction → customer loyalty’. It means the direct relationship between ‘CKM → customer loyalty’ and ‘customer satisfaction → customer loyalty’ is not completely suppressed by customer trust. Also, the link between customer trust and customer loyalty is strong. This gets support from the previous research findings of Luarn and Lin (2003). However, contrasting views are observed about satisfaction and loyalty by both business professionals and academicians (O’Malley, 1998; Ranaweera & Prabhu, 2003). Reichheld (1994) demonstrates that customers claiming to be satisfied or highly satisfied may still cease to be loyal. Contrarily, loyal customers are not necessarily the satisfied ones although satisfied customers do tend to be loyal (Castaneda, 2011; Oliver, 1999).

DISCUSSION

The study shows that CKM has a strong impact on customer trust rather than customer satisfaction. Also, mediation analysis highlighted the nominal role of trust in loyalty and presented customer trust as the precursor of customer loyalty. Thus, customer loyalty can be enhanced by the bank through proper understanding of a customer’s dynamic behaviour and maintaining the up-to-date information about customers. Building a centralized knowledge base of customer and winning the customer trust can have a synergistic impact on the customer loyalty management initiatives. Managerial competence, knowledge management, and technological innovations can add value to customer trust to enrich the cultural integrity of customer loyalty management. Furthermore, customer trust has an intermediary role between satisfaction and loyalty. However, the relationship between customer satisfaction and loyalty is controversial as satisfied customers are not always loyal. Therefore, the study puts forth the strategy that intervention of trust between customer satisfaction and loyalty is crucial. Therefore, satisfaction can lead to loyalty when customer builds trust.

Banks willing to improve their relationships with customers need constant monitoring of customer behaviour and internal processes. However, if the bank fails to deliver customer relationship capabilities to customers, it will have a negative impact on the relationship strength. It can not only transform valuable customers into non-loyal entity, but customers may develop an antagonistic viewpoint towards the bank. As a result, this could have a serious consequence for the bank’s reputation and long-term competitiveness. This gives rise to two contrasting views on customer retaliation: ‘love is blind’ versus ‘love becomes hate’. The ‘love is blind’ view argues that customers with a strong relationship are more likely to forgive a service failure, and as a result retaliates to a lesser extent than customers with a weak relationship (Grégoire & Fisher, 2006). On the other hand, ‘love becomes hate’ argues that customers who possess a strong relationship tend to retaliate more vigorously than those with a weak relationship.

Managerial Implications

In the study, an attempt has been made to provide practical advice to the bank about their current readiness of customer trust and loyalty achieved through CKM and satisfaction. The area needs continuous improvement in order to build and sustain competitiveness in an increasingly competitive banking sector which is marred by structural changes, entry of new players, and customer demands. This forces the bank to focus on certain core competencies in order to deliver better value to their customers.

The managers need to exercise some benchmarks (norms) which should be used as the basis for comparison (both at the firm level and at the industry level) with major competitors. It serves as the means to track best customer loyalty practices in banking industry and replication of these best practices in the bank. The bank should bring in best breed of CRM technology software for capturing customer knowledge and information, which is fit for the Jammu and Kashmir business environment.

Limitations

Despite the contribution of this study to the domain of CRM knowledge, the study has some limitations. It has been conducted on a single bank in the state of Jammu and Kashmir, by employing survey by questionnaire method from customers of a private sector bank in Jammu and Kashmir. This limits the external generalizability of the results.

The study was cross-sectional in nature, that is, primary data was collected at a certain point of time not for a period of time (longitudinal research) because development of trust and loyalty among customers can best be understood through longitudinal study as it does not take customers’ past behaviour into account. The data for the study covers 412 customers for assessment from Jammu and Kashmir. Although, the data is adequate for statistical analysis but for more accuracy and authenticity larger sample size could have been taken. The questionnaire used for the study was addressed to the bank customers, all the stakeholders related with banking CRM were not covered under the study.

Future Research Scope

The present research study was based on the relationship of CKM and satisfaction with the customer trust and loyalty. The empirical findings have shown that there is weak relationship between customer satisfaction and trust. This relationship need to be further explored in order to find out variables which will enrich the relationship between customer satisfaction and trust. Furthermore, the study was conducted in the state of Jammu and Kashmir on a single bank. Future research studies could replicate the current study for some other nationalities and geographical area or study different banks and even non-banking industries.