Abstract

Executive Summary

The future trading has been held responsible by certain political and interest groups of enhancing speculative trading activities and causing volatility in the spot market, thereby further spiralling up inflation. This study examines the effect of future of trading activity on spot market volatility. The study first determined the Granger causal relationship between unexpected future trading volume and spot market volatility. It then examined the Granger causal relationship between unexpected open interest and spot market volatility. The spot volatility and liquidity was modelled using EGARCH and unexpected trading volume. The expected trading volume and open interest was calculated by using the 21-day moving average, and the difference between actual and expected component was treated as the unexpected trading volume and unexpected open interest. Empirical results confirm that for chickpeas (channa), cluster bean (guar seed), pepper, refined soy oil, and wheat, the future (unexpected) liquidity leads spot market volatility. The causal relationship implies that trading volume, which is a proxy for speculators and day traders, is dominant in the future market and leads volatility in the spot market. The results are in conformity with earlier empirical findings —Yang, Balyeat and Leathan (2005) and Nath and Lingareddy (2008)—that future trading destabilizes the spot market for agricultural commodities.

Results show that there is no causal relationship between future open interest and spot volatility for all commodities except refined soy oil and wheat. The findings imply that open interest, which is a proxy of hedging activity, is leading to volatility in spot market for refined soy oil and wheat. The results are in conformity to earlier empirical studies that there is a weak causal feedback between future unexpected open interest and volatility in spot market (Yang et al., 2005). For chickpeas (channa), the increase in volatility in the spot market increases trading activity in the future market. The findings are contrary to earlier empirical evidence (Chatrath, Ramchander, & Song, 1996; Yang et al., 2005) that increase in spot volatility reduces future trading activity. However, they are in conformity to Chen, Cuny and Haugen (1995) that increase in spot volatility increases future open interest. The results reveal that the future market has been unable to engage sufficient hedging activity. Thereby, a causal relationship exists only for future trading volume and spot volatility, and not for future open interest and spot volatility.

The results have major implications for policymakers, investment managers, and for researchers as well. The study contributes to literature on price discovery, spillovers, and price destabilization for Indian commodity markets.

Trading in agricultural derivatives has been a contentious issue for a long time. Researchers, regulators, producers, and investors have debated over its existence, structure, and operation. Wide fluctuations in the prices of agricultural derivatives have a deep economic and social impact on the lives of farmers. The agricultural derivative market was set up to provide a market mechanism for price discovery 1

According to Yang and Leatham (1999), ‘In a static sense, price discovery implies the existence of equilibrium prices. In a dynamic sense, the price discovery process describes how information is transmitted across the markets.’

Prior to 2000, the commodities derivative markets saw a series of ban on trading in agricultural commodities. National Agricultural Policy (NAP) (2000) supported risk management and price discovery of agricultural commodities through future trading. In 2003, trading on commodity derivative exchanges got a fresh start and volumes on future markets revived. However, under political pressure and in an attempt to control rising inflation, trading was banned on certain commodities in 2007–2008. The government formed the Sen Committee in 2008 which concluded that there was no statistical evidence that future trading caused spot market destabilization. 2

Destabilization is the volatility in one market caused from speculative trading activity in another.

In financial literature, the effect of future trading on spot price destabilization has been continuously debated for various markets throughout the world. Mallikarjunappa and Afsal (2008) investigated the impact of introduction of futures trading (CNX Bank Nifty Index) and found that the market volatility had increased post introduction of future trading. Some researchers argue that commodity trading in future market has escalated the volatility of spot market by attracting uninformed traders with their high degree of leverage (Nath & Lingareddy, 2008). Also, future market could cause distortions in the spot market as it can attract a significant amount of new hedge trading without attracting enough speculation to permit effective risk transfer (Figlewski, 1981). The pressures created in the future markets could spill over to spot markets where the dealers and other market makers end up bearing the risk transferred through both the spot and the future market. According to Yang et al. (2005), unexpected futures trading volume uni-directionally causes spot price volatility for most of the commodities. In the context of the Indian commodities market, research findings of Nath and Lingareddy (2008) state that the futures market has not helped in reducing cyclical/seasonal fluctuations in the spot market. Also, future trading has led to an increase in volatility in the spot market for some of the commodities.

However, other researchers have claimed that futures market helps to spread risk from those hedging cash positions to professional speculators who are more than willing to take the risk to make speculative gains (Bessembinder & Seguin, 1992, 1993). Bessembinder and Seguin (1992) report evidence that introduction of futures trading has caused a decline in equity volatility. Kasman and Kasman (2008) have found that the introduction of futures trading has led to stability in the Turkish stock markets. According to Figlewski (1981), although future trading has led to an increase in spot price volatility for Ginnie Mae (GNMA) securities, the instable spot market could increase hedging activity in the futures market. The study suggests existence of reverse causation.

Apart from liquidity, 3

Liquidity is the quantity of contracts bought and sold.

Open interest is the total number of future contracts that are not closed or delivered on a particular day.

Some research studies hold a contrarian view that open interest leads to an increase in spot price volatility. Chen et al. (1995) have modelled the differences between holding stock and future contract on the basis of investor preference for idiosyncratic benefits from holding stock. The study has shown that an increase in volatility increases with the open interest.

Although market depth has a significant relationship with price volatility, it has not been examined frequently. This research study focuses on the role of future trading activity in destabilizing and enhancing depth of spot markets. It also examines lead–lag relationship between spot volatility and open interest. There has been considerable research on effect of future trading on spot price volatility in financial asset market. But limited empirical evidence is available on lead–lag relationship between future trading and spot market destabilization in agricultural commodity markets. The study also investigates the interesting research question of spot trading causing future market destabilization. Any existence of future market destabilization shall have serious implications for the functioning and regulatory mechanism of the commodity trading. Therefore, this study focuses on causal relationships between trading activity variables and volatility of spot markets.

DATA SOURCE

The data consists of daily closing spot prices and future prices, spot trading volume, future trading volume, and future open interest for eight commodities chickpeas (channa), cluster bean (guar seed), cotton (kapas), soya bean, pepper, potato, refined soy oil, and wheat. The data has been compiled from National Commodity & Derivative Exchange Limited (NCDEX), and the data source, and beginning and ending dates have been presented in Tables 1 and 2. The daily spot and future prices are converted to spot return ln(Pst/Pst – 1) and future return ln(Pft/Pft – 1) series for further analysis. Trading volume is used as a proxy for liquidity and the open interest is used as a measure of depth in future markets.

Data Source

Beginning and Ending Dates for Data Collection

RELATIONSHIP BETWEEN FUTURE LIQUIDITY AND SPOT VOLATILITY

The analysis has been performed in two parts. While the first part deals with the causal relationship between future unexpected trading activity and spot volatility, the second part deals with causality between unexpected open interest and spot volatility.

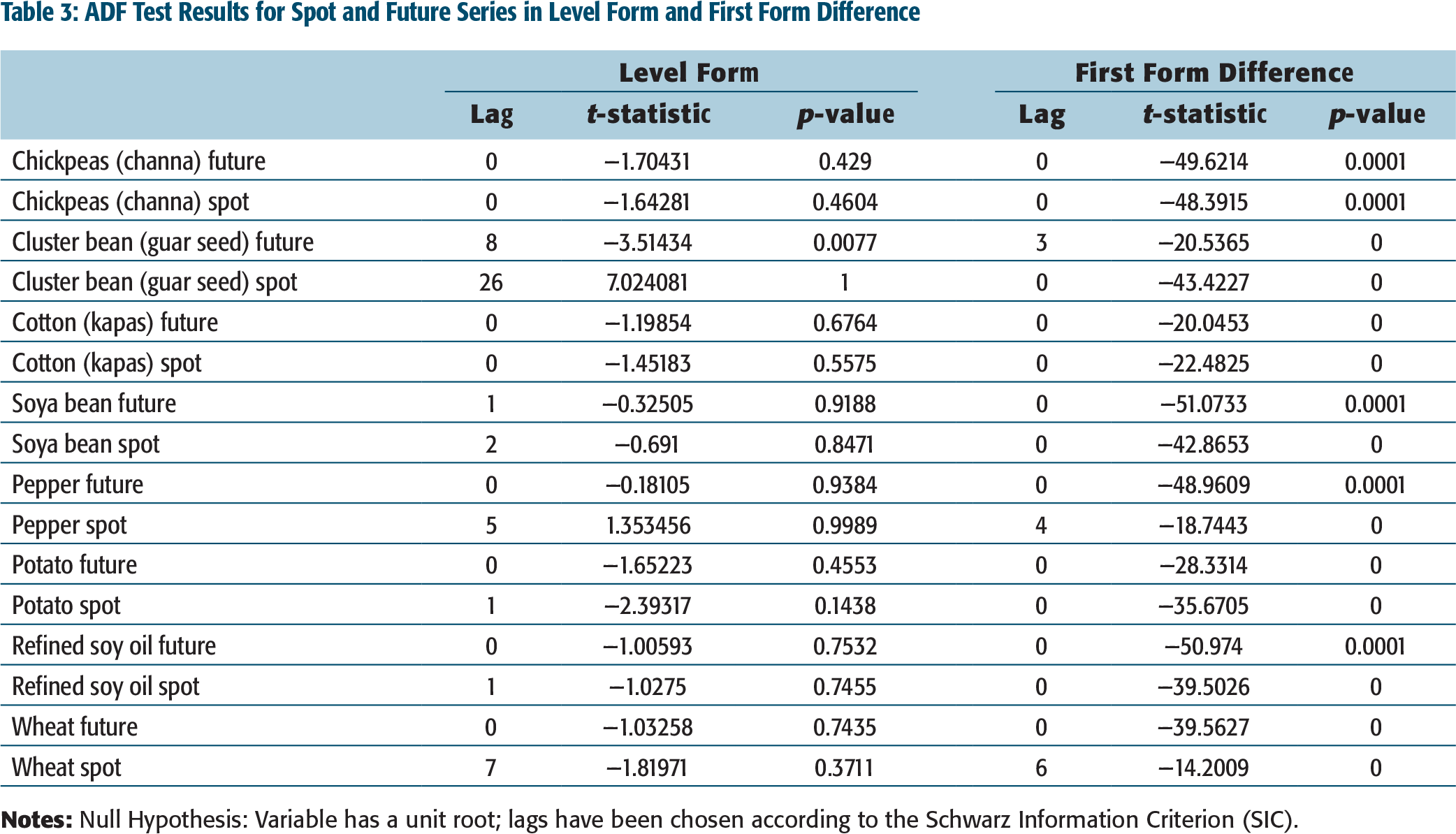

To model volatility, the future and spot price series are tested for stationarity. The order of integration of the spot price ln(Pst) and future price ln(Pft) series is examined using Augmented Dickey–Fuller (ADF) test. 5

ADF test is applied on the following regression model:

ADF Test Results for Spot and Future Series in Level Form and First Form Difference

The study models volatility as conditional on time because of presence of heteroscedastic error terms (Bala & Premaratne, 2003; Booth, Martikainen, & Tse, 1997; Sehgal, Rajput, & Desting, 2013; Silvapule & Moosa, 1999; Yang et al., 2005). The error terms of asset returns show unequal variances which may be autoregressive over a period of time. The autoregressive conditional heteroskedasticity (ARCH) model portrays volatility as the clustering of large shocks to the dependent variable. Bollerslev (1986) further extended the variance model to include not just the past squared error terms but also the past conditional variances. However, the generalized autoregressive conditional heteroskedasticity (GARCH) model suffers from certain shortcomings like the inherent assumptions that positive and negative error terms have symmetric effect on volatility. Also, the GARCH model imposes restriction of positive coefficients. It has been empirically documented that volatility transmission are asymmetric and spillovers are more pronounced for bad news than good news (Booth et al., 1997). Exponential generalized autoregressive conditional heteroskedasticity (EGARCH) introduced by Nelson (1991) overcomes these shortcomings, and the model captures asymmetric impact of shocks. Hsieh (1993) discusses that the EGARCH model is preferable to ARCH model and GARCH model for two primary reasons. The first being, the conditional variance of an EGARCH model responds differently to a rise and a fall in the variance, whereas ARCH and GARCH models impose a symmetric response. Second, the EGARCH model does not impose any constraint on the coefficients for non-negativity of the variance. The model envisages fall in prices as more influential for predicting volatility than rise in prices. It is represented as follows:

The above equation allows to have positive and negative values, and they impact volatility differently.

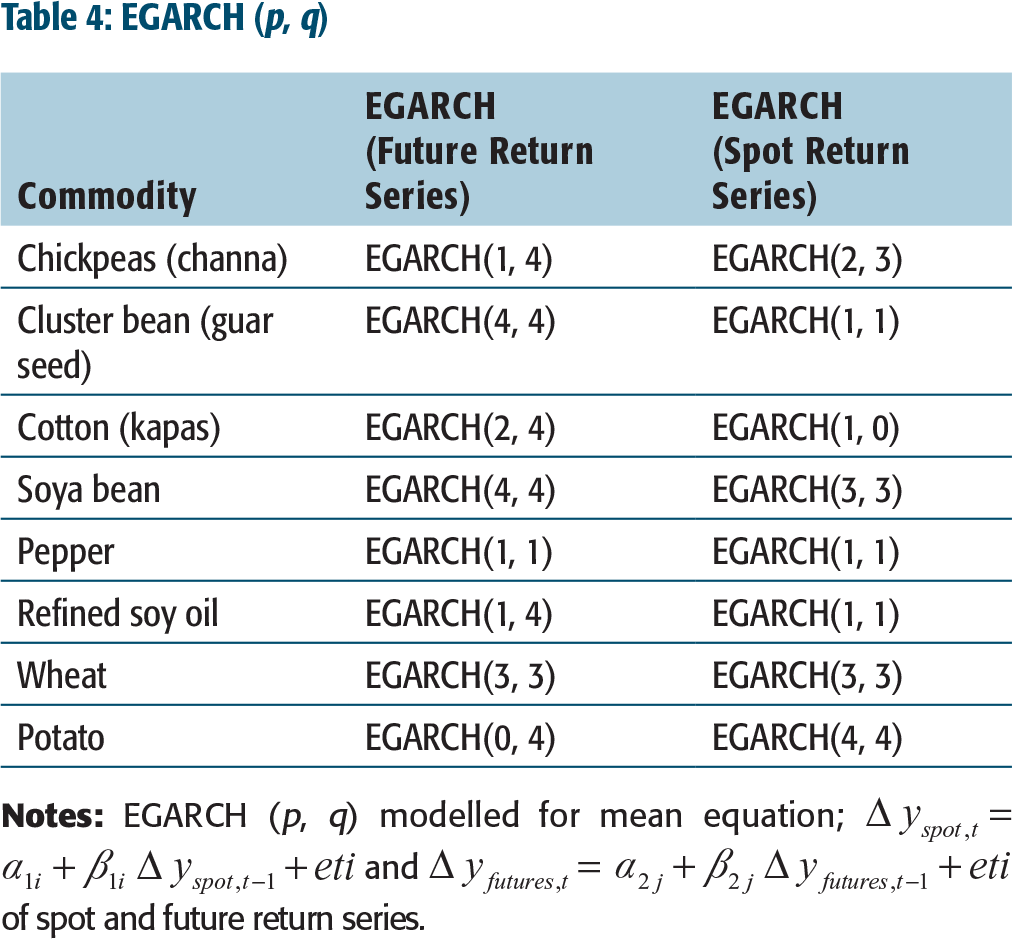

The study models EGARCH (p, q) for the following spot and future mean equation:

EGARCH (p, q)

Bessembinder and Seguin (1992) and Yang et al. (2005) used a 21-day moving average of trading volume and open interest to build expected trading volume and open interest. We experimented with and investigated alternate volume decomposition, including 14-days, 21-days, and 42-days moving average. Our conclusions were robust to these alternatives. We report the results of 21-days moving average as it captures the information of monthly volume. The difference between actual and expected component is the unexpected trading volume and the unexpected open interest. The unexpected components are calculated to analyse the relationship between spot volatility and trading activity. The unexpected components are interpreted as daily trading volume shock and daily open interest shock. The impact of an unexpected volume shock is 2–13 times greater than the change in expected volume on volatility for commodity future market in the US (Bessembinder & Seguin, 1993). The present study examines the lead–lag behaviour of unexpected futures trading volume and conditional return variances using Granger (1969) causality. Granger (1969) examines whether the past values of dependent variable (y) and the lagged values of independent variable (x) can improve the explanation for the current variable (y). When the test examines the statement ‘x Granger-causes y’, it only implies the precedence of information content and not the effect or result. The following specifications are used for the Granger causality test:

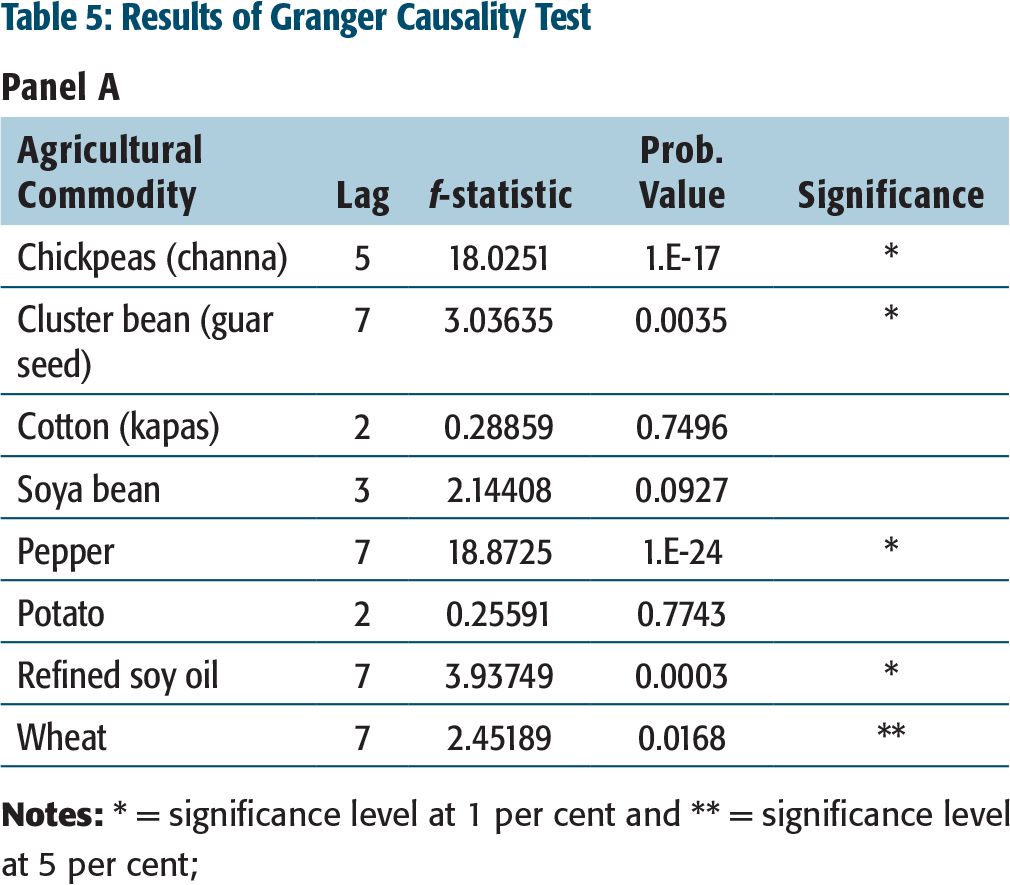

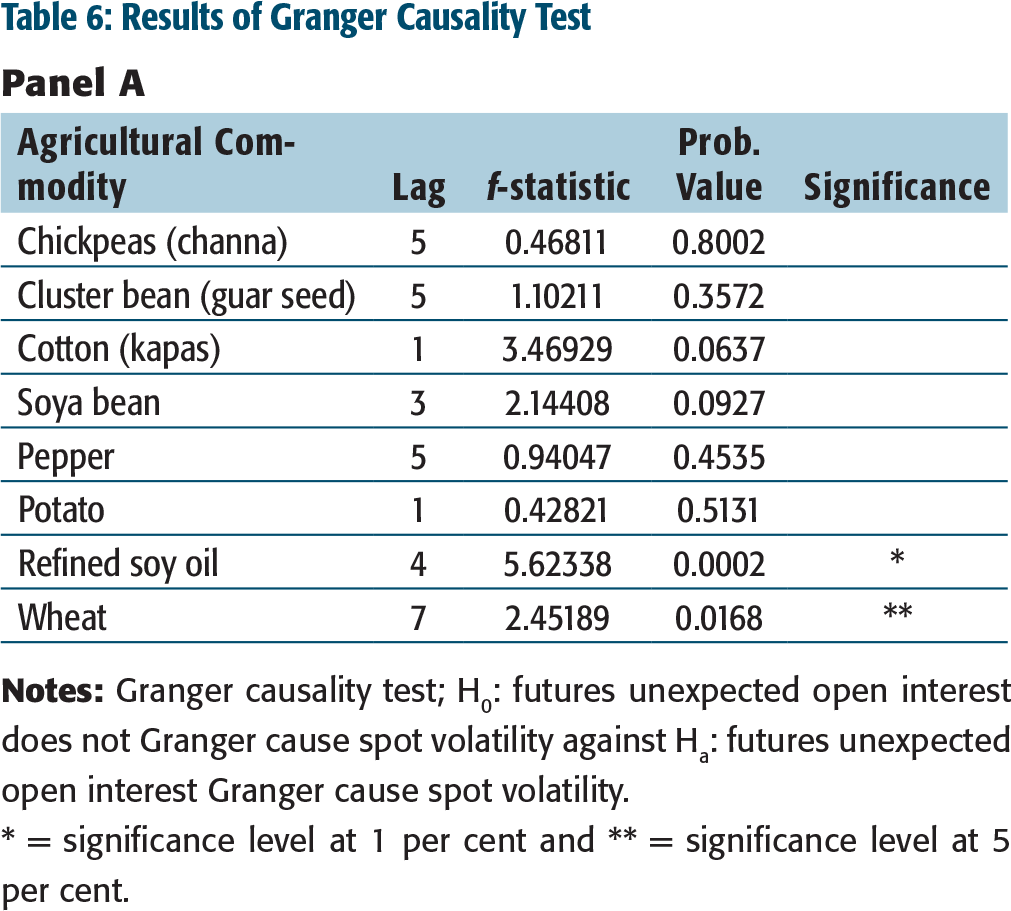

Results of Granger Causality Test

H0: futures unexpected trading volume does not Granger cause spot volatility against Ha: futures unexpected trading volume Granger cause spot volatility.

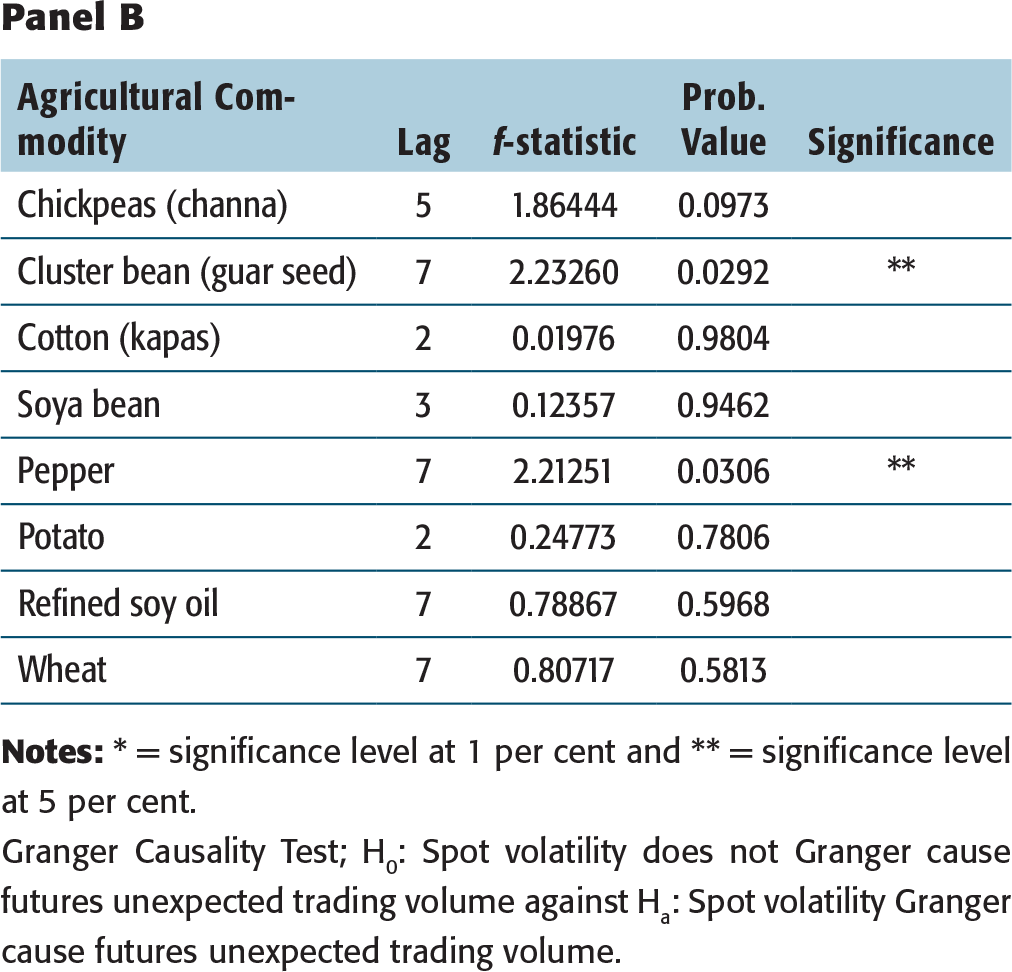

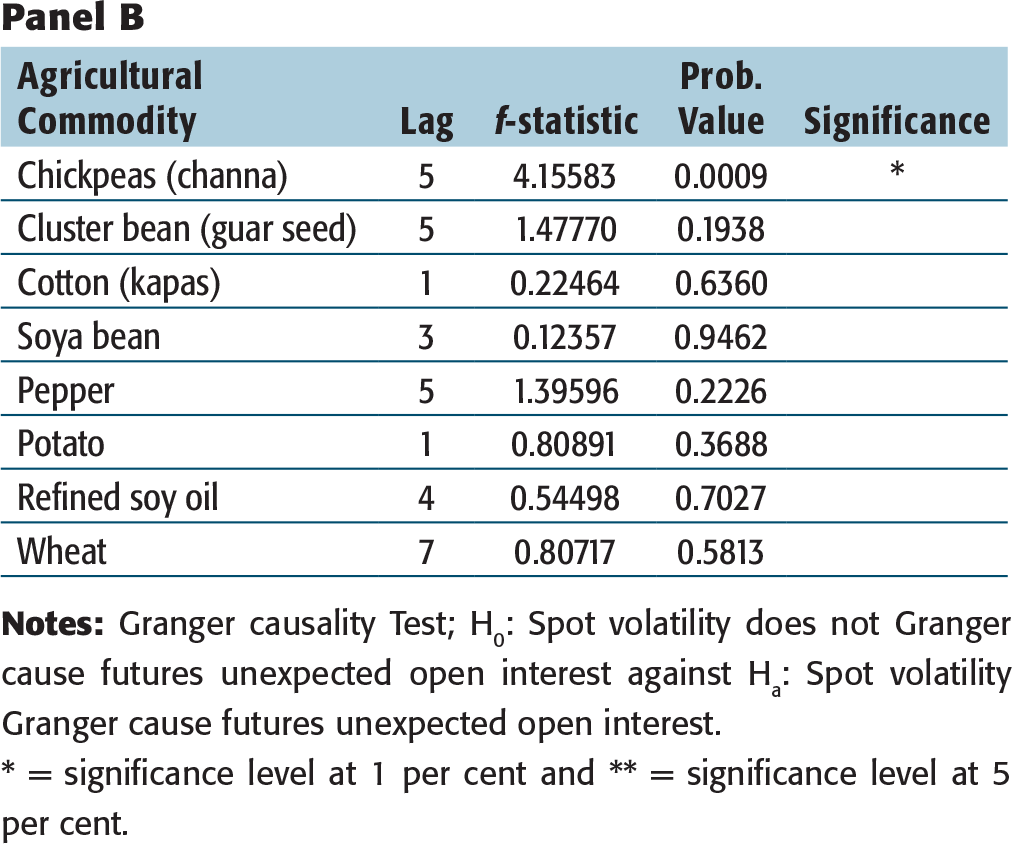

Panel B

Granger Causality Test; H0: Spot volatility does not Granger cause futures unexpected trading volume against Ha: Spot volatility Granger cause futures unexpected trading volume.

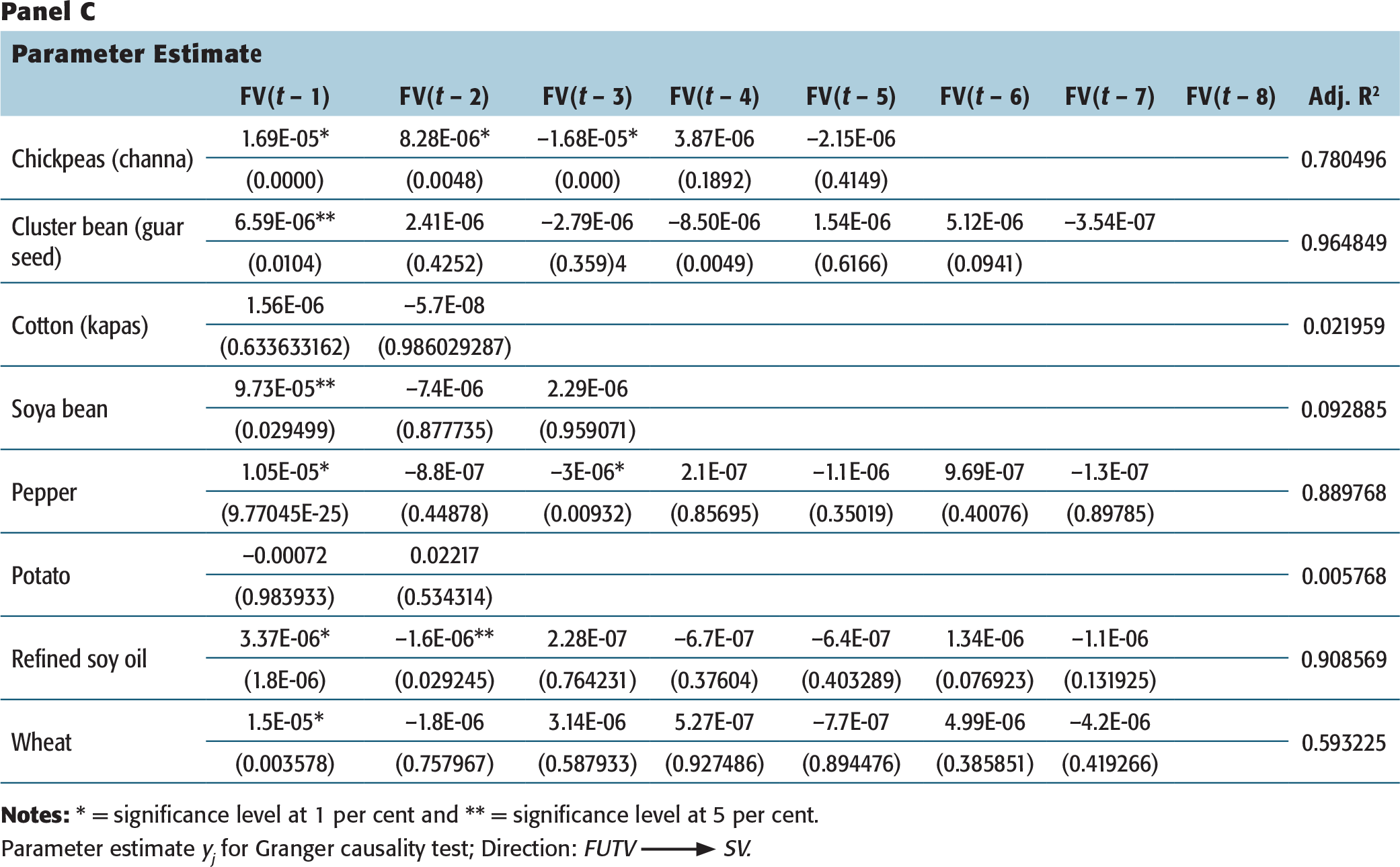

(channa), cluster bean (guar seed), pepper, refined soy oil, and wheat have significant lead–lag behaviour between spot and futures market. For all the five commodities, unexpected futures trading activity leads spot market volatility. Our results show that the unexpected trading activity of future Granger causes spot volatility. They also show that for all the five agricultural commodities, 1-day lagged values of future (unexpected) liquidity increases volatility in the spot market. The 2-day lag of future trading activity is insignificant for all the commodities except chickpeas (channa) and refined soy oil. The chickpeas (channa) 2-day lag futures trading activity has a significant positive impact on spot volatility, whereas refined soy oil has a significant negative impact on spot volatility. Also, 3-day lag of future trading activity for chickpeas (channa) and pepper, and 4-day lag for cluster bean (guar seed) have significant negative impact on spot market volatility. The negative coefficient shows that for every percentage increase in future unexpected trading activity, the volatility in spot market would decrease. The results show that lagged information stabilizes the market, whereas more recent information makes spot markets volatile. The findings are consistent with earlier empirical studies that futures trading activity destabilizes spot markets Nath and Lingareddy (2008).Panel C

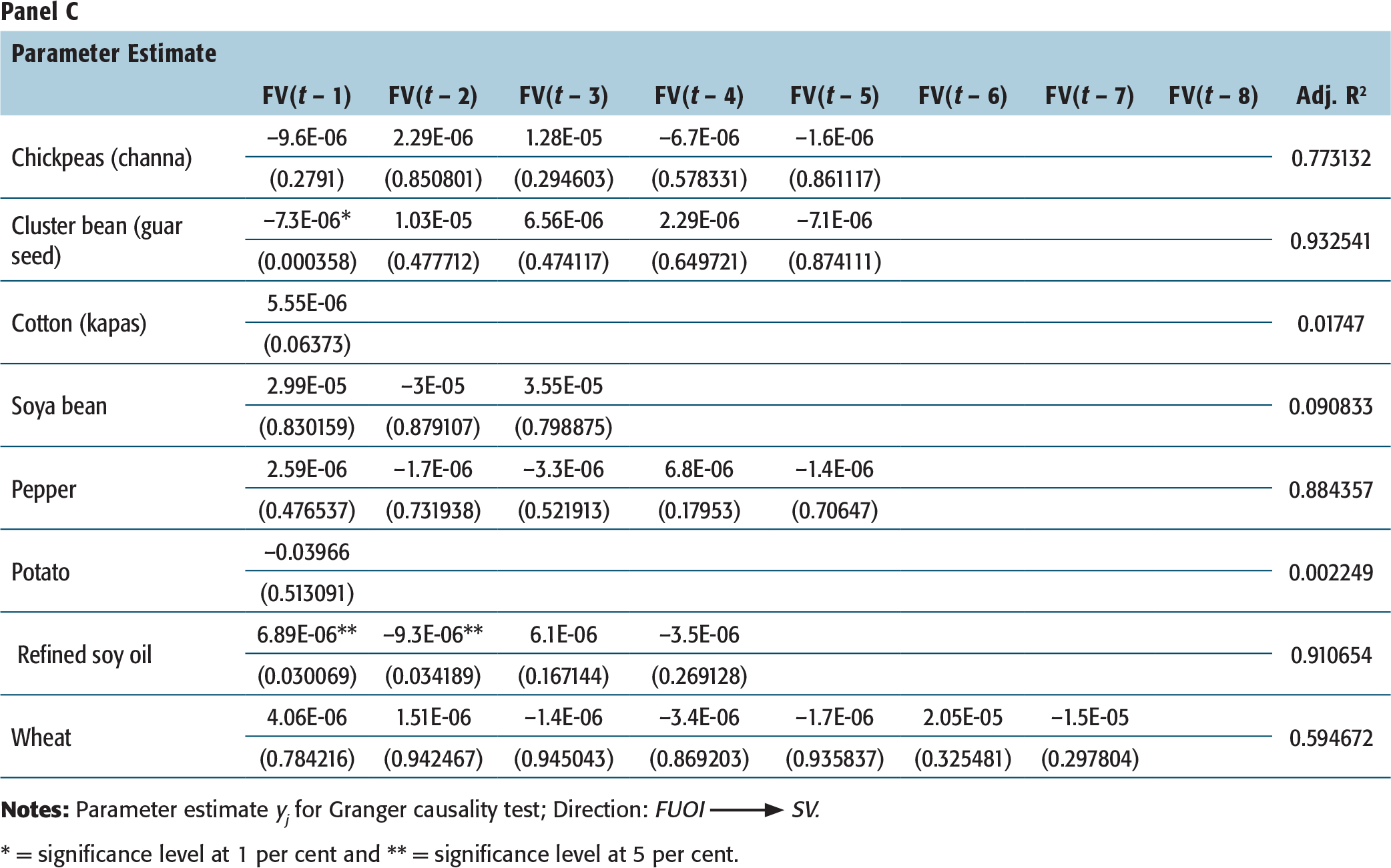

Parameter estimate yj for Granger causality test; Direction: FUTV SV.

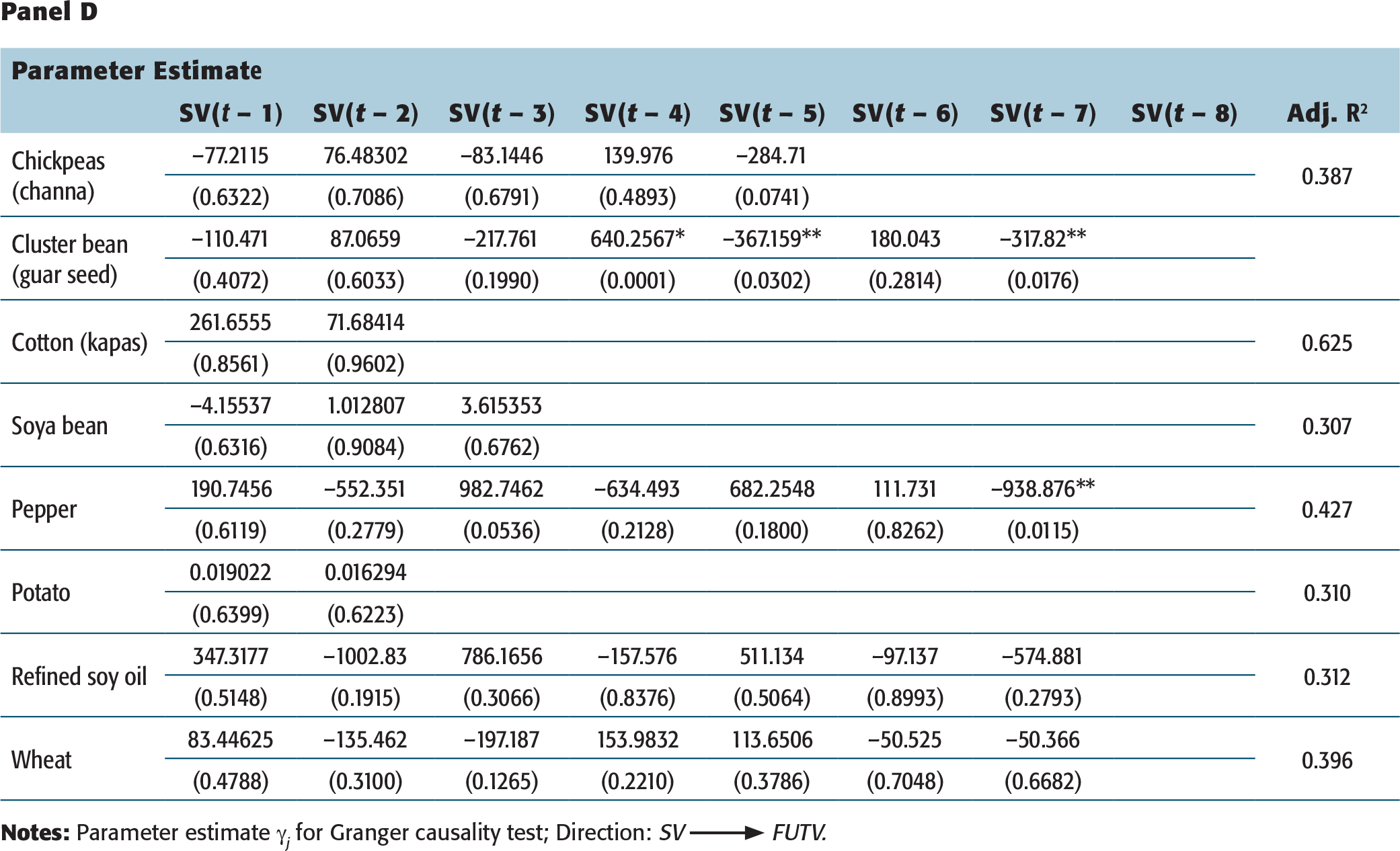

Panel D

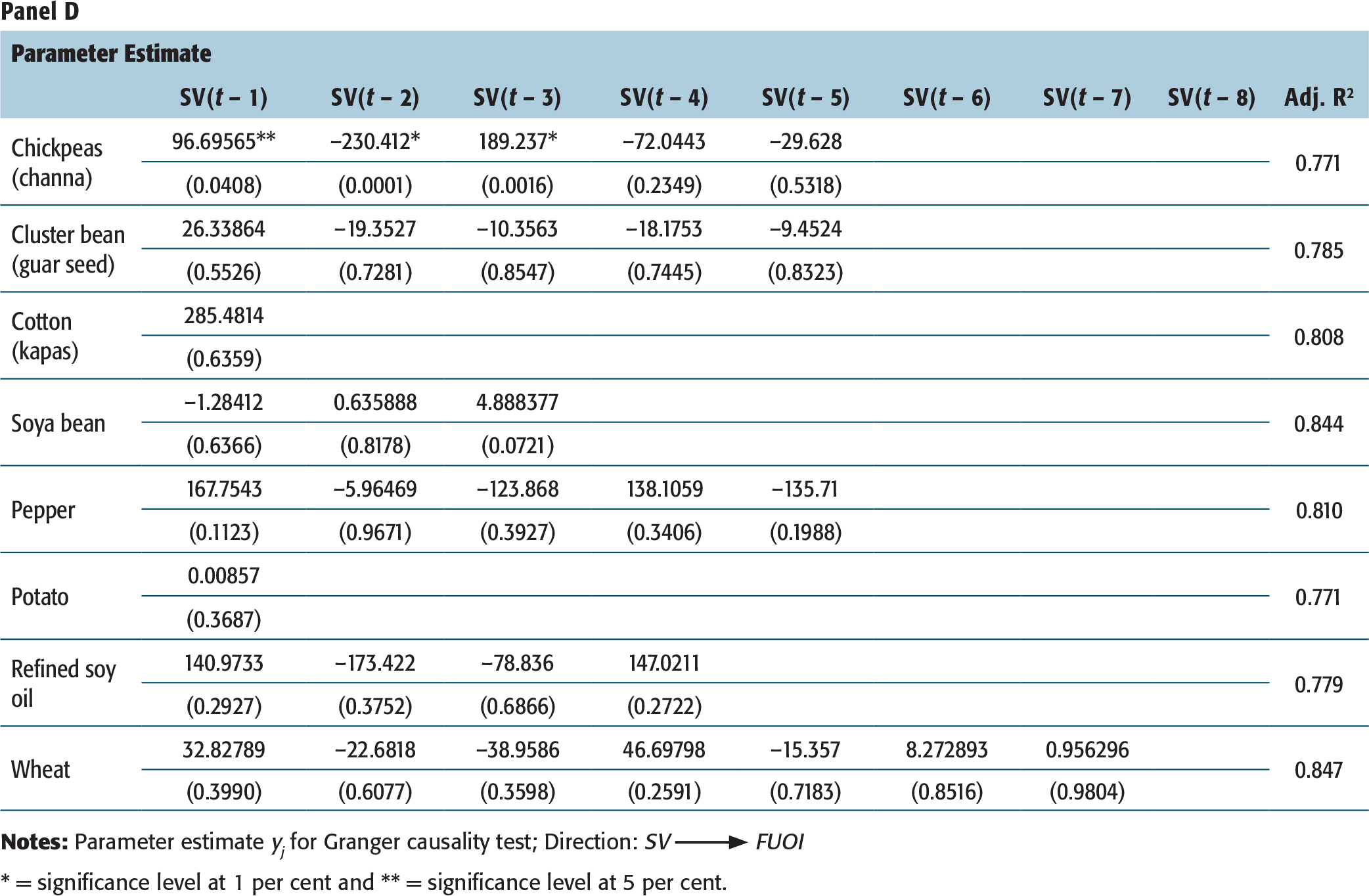

There is a significant bivariate causal relationship in two commodities—cluster bean (guar seed) and pepper—that is, spot market volatility Granger causes future unexpected trading activity and vice versa. The information transformation is more significant from future markets to spot markets. There is existence of reverse causality, and spot market volatility leads future unexpected trading activity. The 4-day lag spot volatility of cluster bean (guar seed) increases future unexpected trading volume, whereas a 7-day lag spot volatility of cluster bean (guar seed) and pepper significantly lead to a decrease in future unexpected trading volume.

RELATIONSHIP BETWEEN DEPTH IN THE FUTURE MARKET AND SPOT VOLATILITY

Very few research studies have examined the lead–lag behaviour between future market depth and spot volatility (Bessembinder & Seguin, 1992, 1993; Chen et al., 1995; Yang et al., 2005). The analysis of open interest (proxy for market depth) becomes important for two reasons. First, a lot of speculators being day traders would close their positions for the day, whereas open interest at the close of the day reflects primary hedging activity. Second, market depth also depends on the willingness and ability of traders to take risk. An unexpected change in the open interest is a close proxy for willingness of future traders to take risk.

To examine the Granger causal relation between unexpected open interest and the conditional variance of spot market, the following equation has been used:

The hedging activity in future market should reduce spot volatility. However, the results show that traders in the future markets in refined soy oil and wheat have seen increased volatility in the spot market attracting speculators, which means that they have been unable to attract hedging activity. For all the other commodities, the study shows that future unexpected open interest which primarily reflects hedging activity does not lead to increase in spot volatility. Findings also show that spot volatility in chickpeas (channa) market Granger causes future unexpected open interest. The 1-day and 3-day lag of spot volatility increase future unexpected open interest, whereas 2-day lag of spot volatility reduces future trading activity. The information gets generated in the spot market which is then reflected in the trading activity of future market.

Results of Granger Causality Test

* = significance level at 1 per cent and ** = significance level at 5 per cent.

Panel B

* = significance level at 1 per cent and ** = significance level at 5 per cent.

SUMMARY AND CONCLUSION

There is no consensus on the future trading activity destabilizing spot markets or enhancing the depth of the asset market. Moreover, the role of open interest in destabilizing or enhancing depth in spot markets is relatively unexplored. This article studies the Granger causal relationship between future unexpected trading volume and spot volatility. It also explores the Granger causal relation between future unexpected open interest and spot volatility for agricultural commodities in the Indian context.

Empirical results confirm that for most of the commodities, there is a significant lead–lag relationship between future unexpected trading volume and spot volatility. The five agricultural commodities include chickpeas (channa), cluster bean (guar seed), pepper, refined soy oil, and wheat, for which the future (unexpected) liquidity leads spot market volatility. The causal relationship implies that trading volume, which is a proxy for speculators and day traders, is dominant in the future market and leads volatility in the spot market. The results are in conformity with earlier empirical findings of Yang et al. (2005) and Nath and Lingareddy (2008), concluding that the future trading destabilizes the spot market for agricultural commodities.

Panel C

* = significance level at 1 per cent and ** = significance level at 5 per cent.

Panel D

* = significance level at 1 per cent and ** = significance level at 5 per cent.

Apart from examining agricultural commodity markets for price discovery and spillovers, the efficacy of price formation in these markets further extends to spot price destabilization.6 Certain interest groups have accused future trading of enhancing speculative trading activities and causing volatility in the spot market, thereby further spiralling up inflation. However, research shows that future trading activity has improved the speed and quality of information flow to the spot market (Antoniou & Holmes, 1995). Figlewski (1981) explains that futures markets spread risk among a large number of investors and transfers it from those hedging spot position to professional speculators. This reduces the risk premium attached to the spot market. Also, future markets enhance informational efficiency as trading takes place on a transparent platform by specialists. Therefore, some research studies have documented that trading in futures reduces volatility in the spot market and enhances market depth (Bessembinder & Seguin, 1992; Figlewski, 1981; Kasman & Kasman, 2008). Whereas other empirical studies suggest that trading in futures has destabilized the spot market (Nath & Lingareddy, 2008; Yang et al., 2005). Indian studies have also advocated that commodity futures markets burdened with government controls and price regulations such as minimum support price, interstate taxes, infrastructure shortcomings for storage and warehousing, etc., fail to perform the function of price formation (Sen, 2008). The present study investigates whether the future trading activity enhances depth or destabilizes the spot market. It applies Granger causality test to examine lead–lag behaviour between future trading activity and spot volatility.

This study contributes to the literature on information transmission for Indian market. The results can be used by policymakers and government agencies to analyse the role of future markets in destabilizing spot market. The future unexpected trading volume increases volatility in the spot market for almost all commodities, thereby destabilizing the spot market. To deepen the markets, the government needs to encourage participation of hedgers in the future market. The government needs to promote hedging activity in the future market with better infrastructure facilities such as low storage costs, warehouse receipts, and electronic spot exchange for better information symmetry. The farmers can be encouraged for greater participation in future market by introduction of commodity options. Commodity options provide direct benefits to farmers. The investors can analyse volatility and liquidity transmission across spot and future markets. These transmissions can be used to estimate the risk associated with agricultural commodities and develop various hedging techniques.