Abstract

Executive Summary

Over the last decade, efforts have been made to improve the quality of financial reporting and corporate governance standards prevailing in emerging markets. Even after 20 years of globalization, emerging markets continue to trade as a separate class (Bekaert & Harvey, 2014). On account of a weak regulatory environment, firm-specific information asymmetry is expected to be on the higher side as compared to developed markets. In such an environment, any factors which mitigate information asymmetry may help improve efficiency of information providers such as equity research analysts. The role of equity research analysts is to process financial information and provide estimates which may be used by investors to make informed investment decisions. This study investigates whether the factors which mitigate firm-specific information asymmetry improve analyst target price accuracy in India.

We expect sophisticated financial intermediaries such as equity research analysts to produce more accurate target price forecasts for firms with higher frequency of corporate announcements, higher analyst coverage, and higher foreign institutional holdings. Past research suggests that these three factors reduce information asymmetry and this reduction could possibly help analysts produce superior results.

Our results show that higher frequency of corporate announcements creates short-term noise which reduces target price accuracy at the end of one-year forecast horizon. Our findings reveal that higher analyst coverage leads to better flow of firm-specific private information and improves target price accuracy anytime during or at the end of one year. We report that higher foreign institutional holding possibly improves stock liquidity, attracting more traders, which eventually leads to better target price accuracy at the end of forecast horizon. Our key finding is that there is a reduction in firm-specific information asymmetry due to the presence of more number of analysts and higher percentage of institutional holding.

Keywords

A target price forecast offers the most direct investment advice to investors, as it is the analyst’s prediction of the firm’s stock price over the next 12 months. Ramnath, Rock and Shane (2008) observe that firm-specific information available in financial markets is used by analysts to derive their outputs including target price forecasts. In essence, analysts process and evaluate firm-specific information and produce an expected target price for a firm. Recent studies support the suggestion that the quality of financial reporting by a firm helps analysts produce superior target price forecasts. For example, Bilinski, Lyssicmachou and Walker (2012) find that target price accuracy of analysts is affected by the quality of financial reporting, enforcement of accounting standards, and the level of promoter ownership prevailing at a country level. On similar lines, Kerl and Ohlert (2015) find that star analysts with superior stock picking abilities perform better in countries with better country-level corporate governance. In developed markets like the US, the Securities and Exchange Commission (SEC) has proposed and implemented policies on corporate disclosures in an attempt to improve the flow of information to financial intermediaries such as security analysts. Regulation Fair Disclosure, 1

Securities and Exchange Commission, regulator in the US, has approved a set of fair disclosure rules through Regulation FD which provides that when an issuer discloses material non-public information to certain individuals or entities generally, securities market professionals, such as stock analysts, or holders of the issuer’s securities who may well trade on the basis of the information, the issuer must make public disclosure of that information.

An act passed by U.S. Congress in 2002 to protect investors from the possibility of fraudulent accounting activities by corporations after the wake of scandals involving large corporations like Enron, Tyco, etc.

However, emerging markets continue to suffer from weak legal and regulatory framework which impairs the quality of information flowing in the system. This, despite the fact that regulators in emerging markets have taken steps to improve disclosure norms (e.g., Clause 49 in India, Capital Markets and Services (Amendment) Act 2012 in Malaysia). In such a dynamic emerging market environment, the quality of financial information provided through regulatory channels is inferior. This makes the role of other factors which mitigate information asymmetry critical. This article evaluates whether these other factors improve an analyst’s accuracy with target price forecasts in an emerging economy context.

Our results reveal that analysts have superior short-term target price accuracy with firms having higher analyst coverage. We report that target price accuracy at the end of the forecast horizon of one year improves when target price forecasts are issued on firms having higher analyst coverage and higher foreign institutional holding. This implies that reduction in information asymmetry has a significant impact on target price accuracy of analysts. However, we find that a firm’s effort to convey information to market participants through higher frequency of corporate announcements creates short-term noise for analysts and reduces analyst target price accuracy at the end of the forecast horizon of one year. Our key finding is that reduction in firm-specific information asymmetry, due to the involvement of informed market participants such as equity research analysts and institutional investors, is more beneficial to analysts than the efforts put by a firm to reduce firm-specific information asymmetry in an emerging market environment.

LITERATURE REVIEW

With the advent of globalization, emerging markets have attracted considerable investments over the past 20 years. In 1998, Morgan Stanley Capital International (MSCI) emerging market index represented less than 1 per cent of global market capitalization, and now in 2017, the index represents almost 10 per cent of global market capitalization. 3

Retrieved 18 July 2017 from https://www.msci.com/emerging-markets

Even though emerging markets are quite different from developed markets, there is not much research conducted on the role of analysts in emerging markets. Some emerging markets offer an interesting background for research related to capital markets. For example, Bombay Stock Exchange has a total of 5,355 companies listed, which is the highest in the world (Bombay Stock Exchange, 2014). Considering the width of equity markets and the volatile nature of stocks in India, the role of analysts as information providers becomes important for investors. However, analyst performance in India has received considerably less scrutiny, and this study attempts to measure analyst performance with target price forecasts in India.

India, as an emerging market, offers an interesting backdrop to investigate the impact of flow of information on financial intermediaries such as security analysts. The regulator in India, Securities and Exchange Board of India (SEBI), implemented Clause 49 4

Clause 49 of the SEBI guidelines (2001) on corporate governance as amended on 29 October 2004 has made major changes in the definition of independent directors, strengthening the responsibilities of audit committees, improving quality of financial disclosures, including those relating to related party transactions, and proceeds from public/rights/preferential issues, requiring boards to adopt formal code of conduct, requiring CEO/CFO certification of financial statements and for improving disclosures to shareholders.

ICAI-AS18: This standard should be applied in reporting related party relationships and transactions between a reporting enterprise and its related parties. The requirements of this standard apply to the financial statements of each reporting enterprise as also to consolidate financial statements presented by a holding company.

From our literature review, we infer that stock price of a firm with better disclosure quality and quantity is easier to predict. This article investigates if reduction in information asymmetry through certain market factors helps equity research analysts. We first dwell on the question of whether reduction of information has helped equity research analysts in financial markets, and then focus on how to measure factors mitigating information asymmetry in emerging markets. Past literature provides numerous motives to expect quality of information to have an effect on the accuracy of financial analysts’ forecasts.

Barker and Imam (2008) are of the opinion that analysts depend on accounting information to develop earnings forecasts. Earlier studies (Healy, Hutton, & Palepu, 1999; Williams, 1996) have shown that the quality of reporting by a firm is an important factor in determining the usefulness of financial information. Salerno (2014) finds that the quality of financial information has a direct association with analyst earnings accuracy, and accuracy is higher, when quality of financial reporting by firms is higher. Bhattacharya, Desai and Venkataraman (2013) evaluate the impact of poor earnings quality on information asymmetry, and find that innate and discretionary components of earnings quality play a significant role in creating information asymmetry. Since emerging markets are typically plagued with poor quality of financial reporting, the probability of existence of information asymmetry is higher, and this in turn may negatively affect the performance of analysts working in emerging markets. Ang and Ma (1999) in a study to evaluate the importance of firm transparency for analysts in Chinese stock markets find that analysts have higher forecast errors and overestimate earnings for Chinese stocks as compared to several developed and developing Asian–Pacific markets. The findings from their study suggest that analysts are inclined to have better accuracy with firms having lower information asymmetry and more transparency.

With this background, we set out to explore if reduction in information asymmetry helps analysts working in an emerging market environment plagued with a poor regulatory framework. Specifically, we investigate whether factors which mitigate firm-specific information asymmetry improve the accuracy of target price forecasts. A few studies have addressed the impact of higher level of firm disclosures on target price accuracy, which is the main focus of this study. For example, Cho (2014) finds that analysts’ failure to incorporate accrual component of earnings leads to lower target price performance. However, there are hardly any studies which have investigated whether reduction in firm-specific information asymmetry improves target price accuracy of analysts in an emerging market environment.

HYPOTHESIS DEVELOPMENT

Academic studies have evaluated various factors which help reduce information asymmetry with respect to a firm. Our research focuses on three such factors namely frequency of corporate announcements by the firm, foreign institutional shareholding in the firm, and analyst coverage of the firm. In our opinion, these variables are relevant with respect to analyst performance in emerging markets like India.

Theory suggests that higher level of information disclosures has the potential of reducing information asymmetry between stakeholders and firm managers. Many studies (Bowen, Davis, & Matsumoto, 2002; Diamond & Verrecchia, 1991; Frankel, Johnson, & Skinner, 1999) have corroborated this. Brown and Hillegeist (2007) show that the level of information asymmetry of a firm is negatively associated with the information quality in the firm’s annual report and the investor relations activities taken up by the firm. Sankaraguruswamy, Shen and Yamada (2013) find that firm-specific degree of information asymmetry is lower, when firms have more frequent press releases. Earlier studies show that a firm’s frequency of information release is negatively associated with information asymmetry. This suggests that analysts may have higher target price accuracy with firm’s having lower information asymmetry on account of higher frequency of information release. We frame our first hypothesis:

H1: Analysts will have higher target price accuracy with firms having higher frequency of corporate announcements.

Analysts express their outlook on firms or forecast based on the information provided by the firms. Kerl (2011) detected that such research reports supplied by the analysts form significant sources of private information for all the participants in the capital market. Researchers (Chan & Hameed, 2006; Sun, 2009; Yu, 2008) ascertained the role of high analyst coverage in establishing an efficient corporate governance environment in capital markets. Specifically, Chang, Dasgupta and Hilary (2006) identify analyst coverage as one of the factors which mitigate information asymmetry in financial markets. Lang, Lins and Miller (2003) report that an increase in the number of analysts following a firm is directly associated with higher firm valuations, particularly for firms likely to face governance problems. Chan and Hameed (2006) find that higher analyst following leads higher stock price synchronicity, which we feel should help analysts make more accurate target price predictions. From these studies, we infer our second hypothesis as:

H2: Analysts will have higher target price accuracy with firms having higher analyst following.

Bekaert and Harvey (1998) have investigated the impact of foreign flows on emerging markets, and their findings show that foreign portfolio investments in emerging equity markets reflect deep changes in the functioning of emerging equity markets. Research suggests that foreign institutional investors may reduce information asymmetry in equity markets. Jiang and Kim (2004) report that foreign institutional investors are more efficient at processing public information and are also attracted to firms with low information asymmetry in Japan. Choi, Lam, Sami and Zhou (2013) find that foreign equity investors have positive effect on the local markets information environment, thereby reducing information asymmetry. These studies suggest that the presence of foreign investors reduces information asymmetry, which in turn should help equity research analysts in processing information more efficiently with higher accuracy in forecasts. We frame our third hypothesis:

H3: Analysts will have higher target price accuracy with firms having higher foreign institutional shareholding.

RESEARCH METHODOLOGY

Data set

Equity research reports (with clear mention of target price were collected from Thomson First Call, 6

Thomson First Call is a leading distributor of brokerage-firm research and analyst forecasts to institutional investors worldwide.

CNX 100 index represents 78.6% of free float market capitalization on NSE, India.

We have excluded the buy side analyst information as they are distributed only to limited audience.

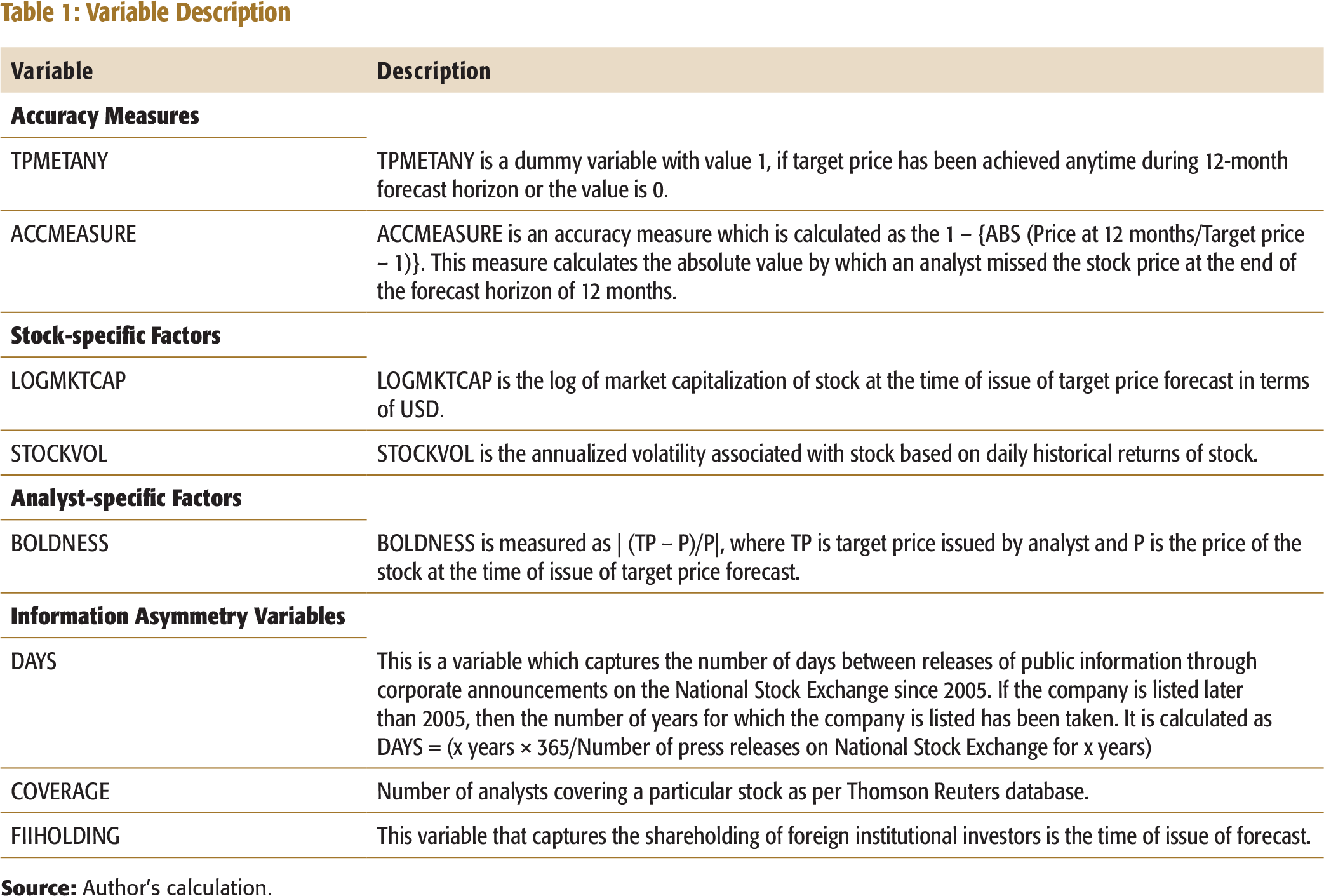

Measures of Analyst Target Price Accuracy

Analysts primarily have three outputs from equity research reports: earnings forecasts, recommendations, and target price forecasts (Asquith, Mikhail, & Au, 2005). From an investor’s perspective, target price forecasts offer most direct investment advice on the future expectation from stock prices (Bilinski, Lyssimachou, & Walker, 2012). It is expected that factors which mitigate information asymmetry improve target price accuracy for analysts. We created two variables: TPMETANY and ACCMEASURE, which evaluated two different aspects of target price performance. Analysts typically issue target price forecasts with a 12-month forecast horizon, and these two measures assessed analyst performance with respect to the forecast horizon. First, we used TPMETANY to measure analyst performance at any point of time during the forecast horizon of 12 months. This variable takes a value of 1, if a target price is met during the 12-month horizon, otherwise the value is 0. It can be observed that TPMETANY is a short-term measure of analyst accuracy with target price forecasts. The second measure ACCMEASURE evaluated analyst performance at the end of forecast horizon. The measure has been used by Kerl (2011) in his study on target price accuracy of analyst’s in German stock market. ACCMEASURE estimates the absolute forecast error at the end of the forecast horizon of 12 months. ACCMEASURE is calculated as follows:

ACCMEASURE = 1 – {ABSOLUTE (Stock price at 12 months/Target price) – 1}

To explain the variable, assume that an analyst has issued a target price of ₹453 on a stock with a one-year forecast horizon. At the end of the forecast horizon, the stock price turns out to be ₹294. The absolute forecast error (294/453–1) would be 35 per cent and the ACCMEASURE would give a value of 65per cent.

Independent Variables Used in This Study

Based on the three hypotheses discussed earlier, independent variables were created for the regression analysis. The variable DAYS captures the number of days between corporate announcements 9

Corporate announcements include release of financial information, outcome of board meeting, press release, data on allotment of securities, transcripts of analyst meetings, news verification, and other firm-specific information released by the firm on NSE.

For stocks in our sample, data on corporate announcements has been collected from National Stock Exchange (NSE), India. Data on corporate announcements was available on NSE from 2004 onwards; hence, this makes the value of x as 11 years in most cases. For companies which were listed after 2004, we have taken the exact number of years for which the company has been listed. For example, if a company has been listed since 2004, we have taken the number of years as 11 (between 2004 and 2014). Now, if the company has released 300 corporate announcements between 2004 and 2014, then we get the frequency of information release as 13.4 days (11 × 365/300). Based on our literature review, we expect analysts to have higher TPMETANY and ACCMEASURE for firms having lesser number of days between corporate announcements, that is, lesser days between corporate announcements means higher frequency of corporate announcements.

The second variable, COVERAGE captured the number of analysts following a firm. The requisite data on analyst coverage was extracted from Thomson Reuters database, which provides information on the number of analysts covering a particular firm. Our expectation based on earlier studies is that analysts will have higher TPMETANY and ACCMEASURE for firms having higher number of analyst following.

Third, we created a variable FIIHOLDING which measured the foreign institutional holding in the firm at the time when the forecast was issued. Our literature review suggests that analysts will have higher TPMETANY and ACCMEASURE for firms having higher foreign institutional holding.

Control Variables

Variable Description

REGRESSION EQUATIONS

We investigated the determinants of target price accuracy based on a multivariate regression substructure. This study has proposed TPMETANY and ACCMEASURE as the main dependent variables and independent variables, including DAYS, COVERAGE, and FIIHOLDING with control variables. Greene (2003) demonstrated the use of logit regression when the dependent variable is a dummy variable. For our short-term measure, TPMETANY, we established logit regression equations to test our three hypotheses which is as follows:

For our second measure, ACCMEASURE, we used ordinary least squares regression (OLS). The equation to test all three hypotheses with ACCMEASURE as dependent variable is as follows:

Our regression estimates are expected to provide results for the three hypotheses twice: one for short-term accuracy and the other for accuracy at the end of the forecast horizon.

FINDINGS

Descriptive Statistics

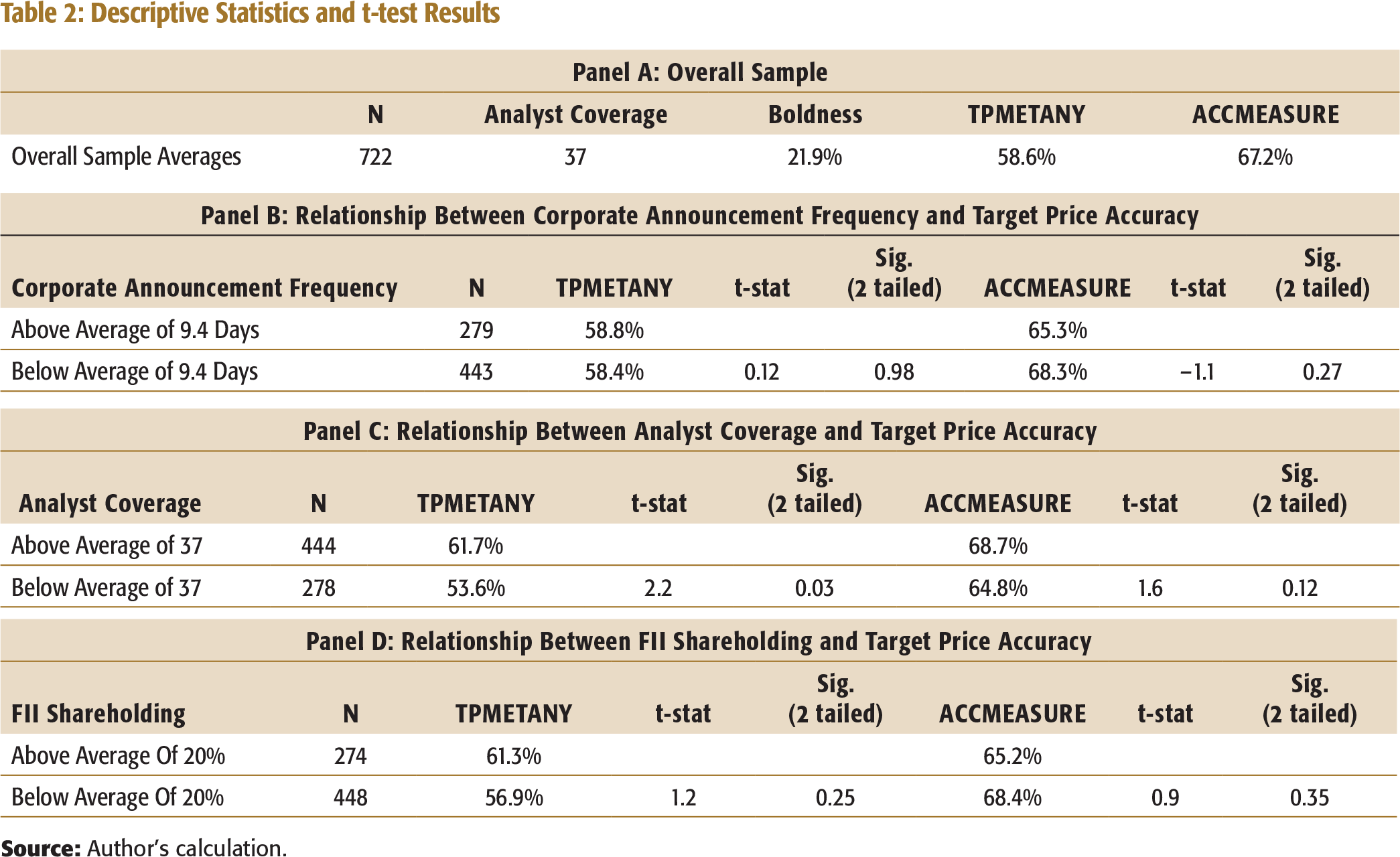

Descriptive statistics associated with our main variables of study are presented in Table 2. Panel A in Table 2 provides results associated with the overall sample. The mean analyst following for the sample firms is 37. The results indicate that the highest number of analysts following a particular company is 56 and the least number is 5. Overall, analysts expect 21.9 per cent movement in share price from current level of stock prices. With respect to performance, we find that analysts meet their target price forecasts with 57.1 per cent accuracy, when measuring analyst performance using TPMETANY. Bradshaw, Brown and Huang (2013) find that analysts have accuracy of 64 per cent for TPMETANY. On our other measure, ACCMEASURE, we find that analysts meet their target price forecasts with 67.2 per cent accuracy. On the same measure, Kerl (2011) reports analyst accuracy of 67.4 per cent in German markets. It can be observed that results on target price performance from India are comparable with results from the US and Germany.

Panel B in Table 2 shows descriptive statistics and t-test results on the relationship between the frequency of corporate announcements and analyst performance. We find that Indian companies make a corporate announcement on NSE every 9 days. For companies which have above average frequency of corporate announcement, TPMETANY is 58.8 per cent and ACCMEASURE is 65.3 per cent. This can be compared with analyst performance for companies having below average frequency of corporate announcement, where TPMETANY is 58.4 per cent and ACCMEASURE is 68.3 per cent. The independent sample t-test reveals that there is no association between TPMETANY and DAYS (t-stat = 0.12, p = 0.98) as well as between ACCMEASURE and DAYS (t-stat = –1.1, p = 0.27). Results suggest that analysts’ performance is not affected by the frequency of corporate announcements.

Panel C in Table 2 presents descriptive statistics and t-test results, exploring the relationship between analyst coverage and target price accuracy. When number of analysts covering a company is more than the average of 37, TPMETANY is 53.6 per cent and ACCMEASURE is 68.7 per cent, while TPMETANY is 53.6 per cent and ACCMEASURE is 64.8 per cent, when the number of analysts covering a company is less than the average of 37. Independent sample t-test results show that there is a significant association between TPMETANY and COVERAGE (t-stat = 2.2, significant at 5% level), while independent sample t-test results show that there is no significant association between ACCMEASURE and COVERAGE (t-stat = 1.7, p = 0.12). Put together, descriptive statistics and independent sample t-test results show that analysts have better short-term performance with companies having higher analyst following or coverage.

Panel D in Table 2 shows descriptive statistics and independent sample t-test results to investigate the relationship between foreign institutional holding in a firm and target price accuracy. When foreign institutional holding is above the average of 20 per cent, TPMETANY is 61.3 per cent and ACCMEASURE is 65.2 per cent. When the foreign institutional holding is below average of 20 per cent, TPMETANY is 56.9 per cent and ACCMEASURE is 68.4 per cent. Independent sample t-test results show that there is no association between TPMETANY and FIIHOLDING (t-stat = 1.2, p = 0.25), and ACCMEASURE and FIIHOLDING (t-stat = 0.9, p = 0.35).

Descriptive Statistics and t-test Results

Correlation Table and Variance Inflation Factor Analysis

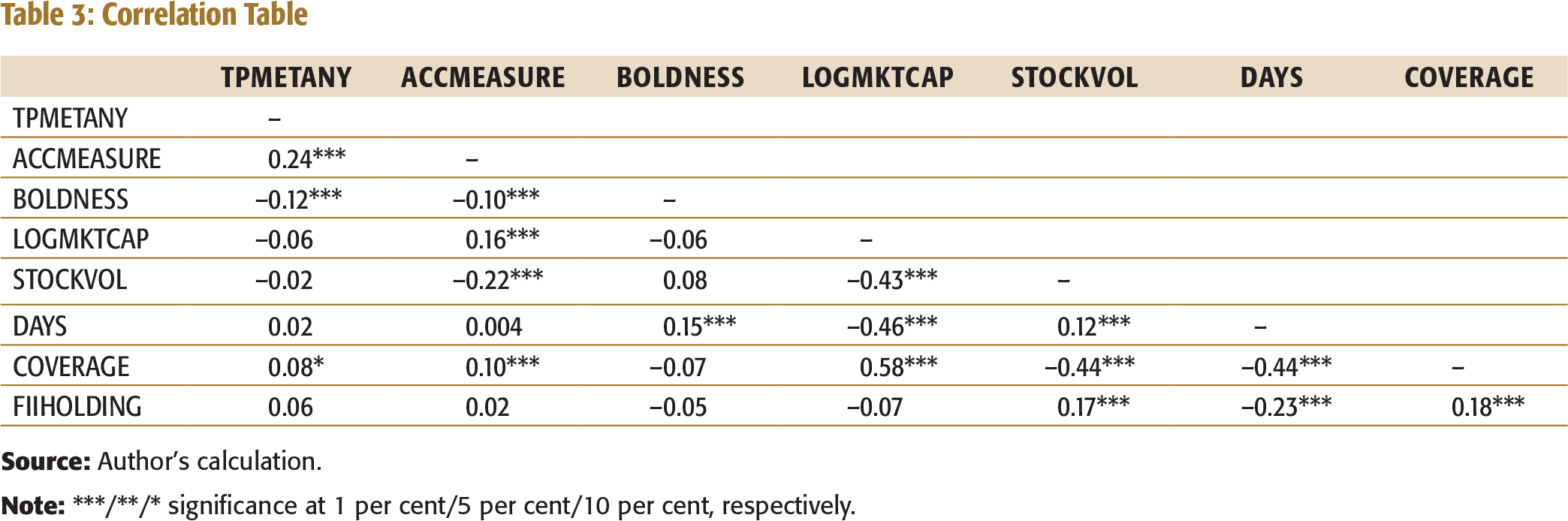

Table 3 presents the correlation data which explains the relationship between measures of target price performance, factors mitigating information asymmetry, and other variables used in this study. The results show that TPMETANY and ACCMEASURE are significantly and positively correlated (0.24, significant at 1% level). This also suggests that TPMETANY and ACCMEASURE capture different aspects of target price performance. TPMETANY is positively associated with COVERAGE (0.08, significant at 10% level), suggesting that there is a relatively weak correlation between short-term analyst performance. ACCMEASURE is positively and significantly correlated with COVERAGE (0.10, significant at 1% level). This implies that analysts have better analyst performance at the end of the forecast horizon for firms having higher analyst following. We find no significant correlation between our measures of target price performance and DAYS and FIIHOLDING.

COVERAGE and DAYS are negatively and significantly correlated (–0.44, significant at 1% level), suggesting that firms with higher analyst coverage have lesser days between corporate announcements. Also, there is a significant and negative correlation between FIIHOLDING and DAYS (–0.23, significant at 1% level), suggesting that foreign investors prefer to invest in firms which have lesser number of days between corporate announcements. COVERAGE and FIIHOLDING (0.18, significant at 1% level) are positively correlated, suggesting that foreign investors prefer to invest in firms which have higher analyst following.

Since the correlation between three independent variables DAYS, COVERAGE, and FIIHOLDING is on the higher side, there could be issues of multicollinearity. To put it in perspective, there could be cases where analyst coverage is higher for stocks having higher FII holding. Or it is also possible that analyst coverage and FII holding is higher for stocks releasing information more frequently. The key problem with multicollinearity is that it results in unstable parameter estimates, leading to distortion of relationship between independent variables on dependent variables. Also, multicollinearity could lead to less reliable probability values in multiple regression analysis.

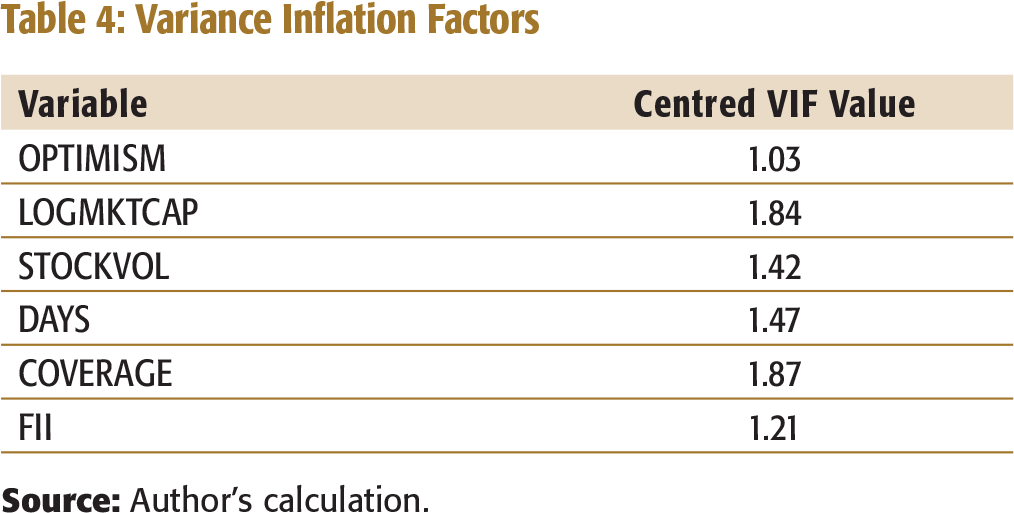

To test for multicollinearity, a variance inflation factor (VIF) test was conducted. VIF test measures the degree to the extent that the variance of the OLS estimator is inflated or affected on account of issues related to collinearity. Academicians have used VIF as an indicator of multicollinearity. It is suggested that if the VIF variables exceed 10, then the variable is said to be highly collinear (Gujarati, 2003). Table 4 presents results from the VIF test. The results show that the VIF value does not exceed 5 in any of the cases, and thus the issue of multicollinearity does not exist.

Correlation Table

Variance Inflation Factors

With respect to correlation of other variables with our three measures of interest, we find that BOLDNESS and DAYS are positively and significantly correlated (0.15, significant at 1% level), indicating that analysts may deviate more from current market prices for companies which communicate less frequently with shareholders. Our correlation table shows that LOGMKTCAP and DAYS are negatively and significantly correlated (–0.46, significant at 1% level), suggesting that smaller firms have higher number of days between corporate announcements, that is, smaller firms release information less frequently. LOGMKTCAP is also positively and significantly correlated with COVERAGE (0.58, significant at 1% level), suggesting that number of analysts following a firm is higher for larger firms. STOCKVOL is positively correlated with DAYS (0.12, significant at 1% level), suggesting that stock volatility is higher for firms which have more number of days between corporate announcements. STOCKVOL is negatively correlated with COVERAGE (–0.44, significant at 1% level), suggesting that analyst coverage is higher for stocks having lower volatility. There is positive and significant correlation between STOCKVOL and FIIHOLDING (0.17, significant at 1% level), suggesting that stocks which have higher foreign institutional holding tend to be more volatile.

Logit and Ordinary Least Squares Regression Results

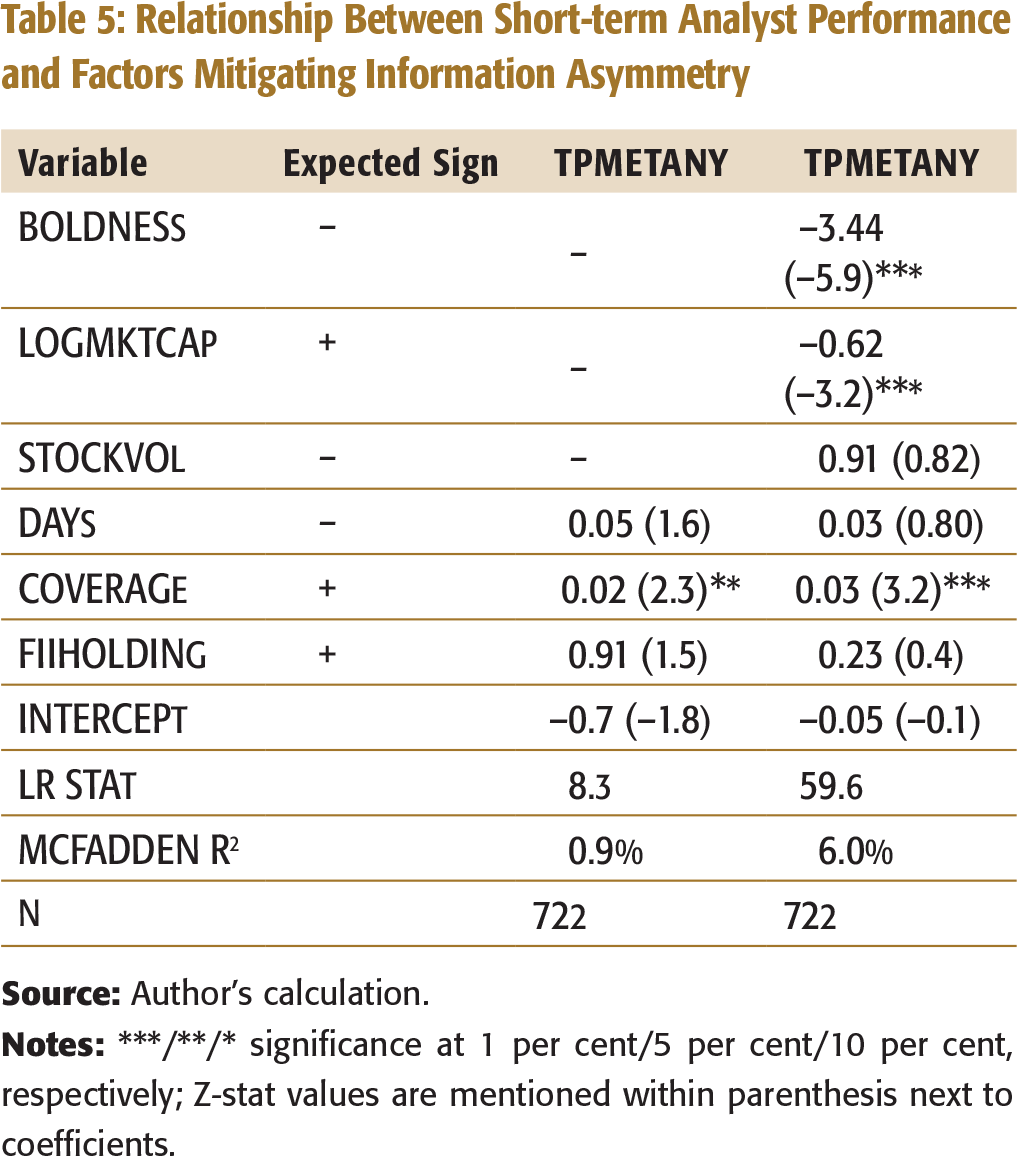

Relationship Between Short-term Analyst Performance and Factors Mitigating Information Asymmetry

This table presents results from logit regression of TPMETANY on factors mitigating information asymmetry, including DAYS, COVERAGE, and FIIHOLDING, without and within the presence of BOLDNESS, LOGMKTCAP, and STOCKVOL as control variables. All variables are defined in Table 1.

Our results from Table 5 show that there is no association between short-term target price accuracy of analyst and the number days between corporate announcements. We had hypothesized that analyst accuracy would improve with firms releasing information on a frequent basis, but our results do not support the hypothesis. For short-term target price accuracy, we reject the hypothesis 1. Our results from Table 5 show that analysts have significantly better short-term target price accuracy with firms having high number of analysts following or coverage. We accept hypothesis 2 and report that analysts have better short-term accuracy with firms having higher analyst coverage. Our third hypothesis was to test the relationship between target price accuracy and foreign institutional holding in a firm. Our results show that short-term target price accuracy has no association with foreign institutional holding in a firm. We reject hypothesis 3 for short-term target price accuracy measure.

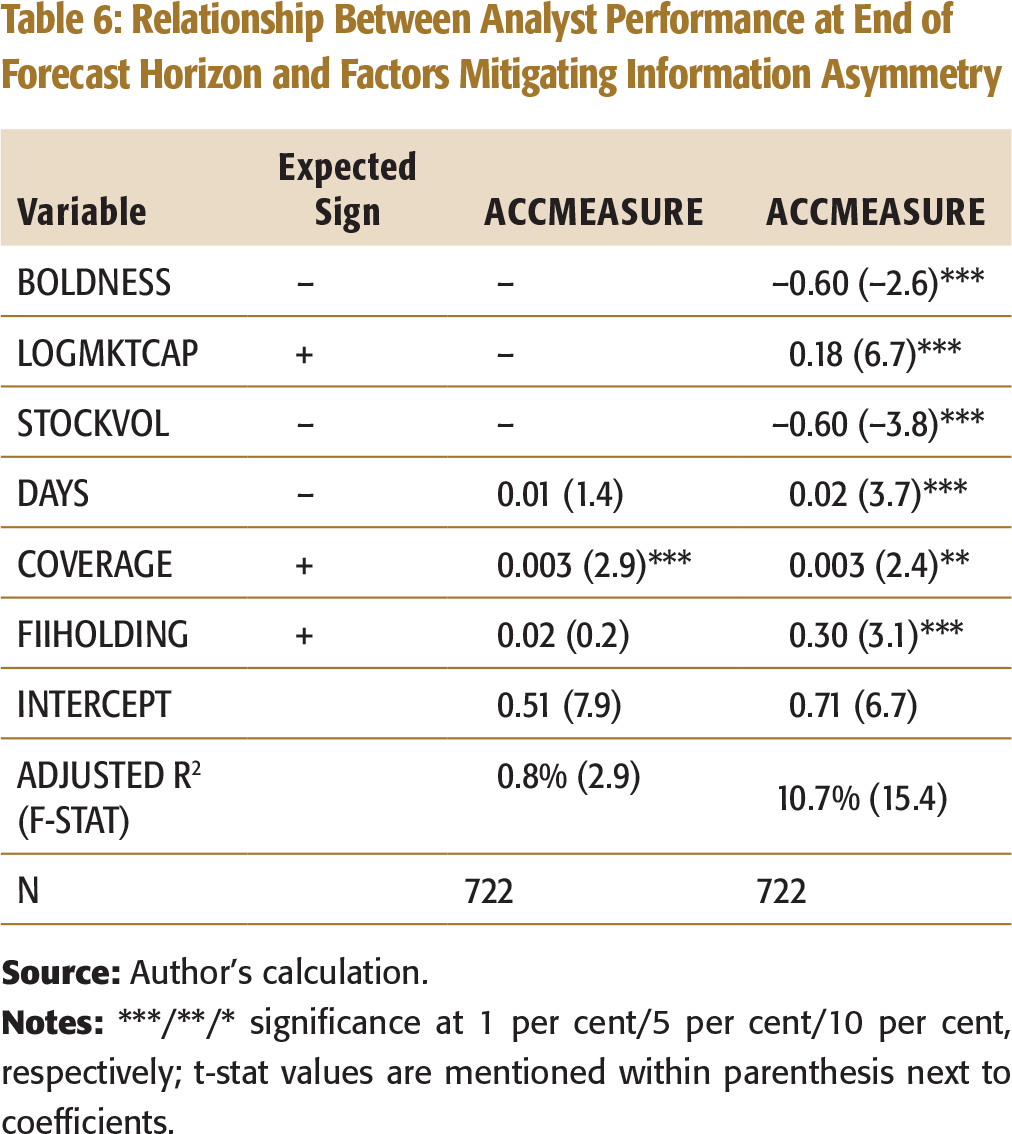

Relationship Between Analyst Performance at End of Forecast Horizon and Factors Mitigating Information Asymmetry

This table presents results from OLS regression of ACCMEASURE on factors which mitigate information asymmetry, including DAYS, COVERAGE, and FIIHOLDING. BOLDNESS, LOGMKTCAP, and STOCKVOL are used as control variables. All variables are defined in Table 1.

It must be noted that in the regression results from Table 5 and Table 6, the introduction of control variables significantly improved the predictive ability of the model. Earlier research has shown that the three control variables, including market capitalization (Kerl, 2011), stock volatility (Demirakos, Strong, & Walker, 2010), and analyst boldness (Demirakos, Strong, & Walker, 2010) have a significant association with target price accuracy and our results further confirm these findings in an Indian context. The improvement in predictive ability after introduction of these control variables implies that the impact of information-related variables used in this study (DAYS, COVERAGE, and FIIHOLDING) is lesser than firm specific (market capitalization, firm size) and analyst specific (boldness) on analyst accuracy.

We hypothesized that analyst target price at end of forecast horizon will improve for firms having lesser number of days between corporate announcements. However, our results, contrary to our expectations, show that target price accuracy at the end of forecast horizon is more for firms which disclose less and have more number of days between announcements. We, therefore, reject hypothesis 1, when target price accuracy is measured at the end of the forecast horizon. Our second hypothesis was to test if target price accuracy of analysts is higher, when analyst issue target price forecasts on firms which are followed by higher number of analysts. Our results show that there is significant and positive association between target price accuracy at the end of forecast horizon and the number of analysts following a firm. Therefore, we accept hypothesis 2, when target price accuracy is measured at the end of the forecast horizon. Our third hypothesis was to test if analyst performance is superior with firm’s having higher foreign institutional holding, and our results for OLS confirm this. We accept hypothesis 3, when analyst performance is measured at the end of forecast horizon.

INTERPRETING THE RESULTS

Regression results associated with the variable DAYS show that frequency of corporate announcements has no impact on short-term target price accuracy. However, unexpectedly, we find that analysts produce superior target price forecasts for firms which make lesser corporate announcements. Frost, Gordon and Pownall (2008) find that firms in emerging markets pick and choose among alternatives such as the level of transparency of annual report, voluntary dissemination of information through websites to enhance their financial reporting, and disclosure quality. They contend that emerging market firms do not make conscious effort to migrate from low quality information to high quality information on all parameters, and are selective in their approach towards improving quality of information provided to stakeholders. With respect to emerging markets, Claessens and Yurtoglu (2013) report that voluntary and market corporate governance mechanisms have lesser impact in emerging markets where the overall corporate governance is weak. We believe that higher frequency of corporate announcements creates short-term noise on account of poor quality of financial reporting, and this reduces analyst accuracy at the end of the forecast horizon.

Results associated with COVERAGE show that analysts have significantly superior target price accuracy anytime during or at the end of the forecast horizon with firms which have higher number of analyst coverage. Healy and Palepu (2001) find that analysts act as information intermediaries and are involved in production of private information which helps detect any mismanagement by a firm’s manager. Also, Schutte and Unlu (2009) suggest that the noise associated with stock price fluctuations is reduced, when analyst coverage is higher. Yu (2008) finds that firms with higher analyst coverage have lesser earnings management, suggesting that analysts process private information which the management of a firm may not release. The higher flow of private information possibly helps analysts predict share prices more accurately in the short term and at the end of forecast horizon for firms. We believe that this higher flow of private information is more relevant in an emerging market like India where a weak regulatory and institutional framework reduces the quality of information flowing to all stakeholders in a firm. In fact, Hope (2003) reports that analysts are more accurate in countries which have high quality accounting disclosures and enforcements of accounting standards.

Results associated with our third variable of interest, foreign institutional holding (FII), show that analysts have superior target price accuracy at the end of the forecast horizon with firms which have higher foreign institutional holding. Huang and Shiu (2005), and Richards (2005) report that buying by foreign institutional investors in emerging markets is generally considered as a positive signal by markets participants, and this attracts uninformed traders and improves stock liquidity. In this regard, Prasanna and Menon (2012) report that the presence of foreign institutional investors improves liquidity of stocks trading in emerging markets like India. Higher liquidity is typically associated with more efficient price discovery, and the financial system as a whole benefits from liquidity (Wuyts, 2007). We suggest that this higher foreign holding improves liquidity in stocks, which in turn helps produce superior target price forecasts at the end of the forecast horizon.

CONCLUSION

In this study, we investigate whether factors mitigating firm-specific information asymmetry in an emerging market improve target price accuracy of analysts. We use frequency of corporate announcements by a firm, analyst coverage of a firm, and foreign institutional holding in a firm as factors which could reduce information asymmetry in emerging markets, and help analysts achieved superior target price results. Our results show that higher analyst coverage improves analyst accuracy in the short term and at the end of forecast horizon, while higher foreign institutional hold improves target price accuracy at the end of the forecast horizon. With respect to frequency of corporate announcements, we find that higher frequency of corporate announcements creates short-term noise and reduces target price accuracy of analysts. An extension of this study would be to investigate if factors which mitigate information asymmetry can possibly help unsophisticated investors by providing abnormal returns. A limitation of our study is that it is a market-centric study based on Indian equity research reports, and a more detailed study including data from other emerging markets would possibly provide deeper insights into the impact of factors which mitigate information asymmetry on analyst performance.