Abstract

Executive Summary

Capital market uses financial information with high disclosure quality, and this information can influence capital market decision-making. Corporate governance research shows that ownership structure can influence financial reporting quality, and thus play an effective role in capital market decision-making.

The main purpose of the current study is to examine the impact of ownership structure and disclosure quality on the information asymmetry phenomenon among the listed companies on the Tehran Stock Exchange (TSE). Ownership structure (including ownership concentration and institutional ownership) and disclosure quality (including reliability and timeliness) are considered as independent variables, and their impact is examined on the dependent variable (information asymmetry). Consistent with extant literature, bid-ask spread is used as a proxy variable for information asymmetry.

The statistical results, based on data collected from 102 listed companies on the TSE during 2007–2014, revealed positive impact of ownership structure and negative impact of disclosure quality on information asymmetry. These results show that information asymmetry is less in firms that published more reliable and timely information, and is more in firms with more concentrated ownership structure, higher institutional ownership, and lower disclosure quality. In other words, reliability and timeliness of information have a positive role in stock price identification and close-up views of the buyer and seller in TSE.

Findings of this article can assist accounting researchers and theoreticians in comparing real world facts with hypotheses developed with respect to ownership structure, disclosure quality, and information asymmetry. By increasing transparency in the capital markets, market participants, decision-makers, financial analysts, and potential investors are aided in their analysis of plans for investments in financial assets.

Keywords

Disclosure is essential to market efficiency. Firms disclose their information via legal financial reports including financial statements, notes to the financial statements, management discussion and analysis, and other legal reporting systems. In addition, some firms make voluntary disclosures such as management forecasts and additional information disseminated in press. Demand for financial reports and disclosure is mainly due to information asymmetry and agency problems between management and external users (Jiang, Habib, & Baiding, 2011).

Information asymmetry and agency problem lead to inefficient allocation of resources in the capital market. Therefore, efficient contracts between agents and principals are used to solve these problems and increase agent’s incentive for disclosure of information. As a result of this process, misevaluation of the firm is reduced and conflicting interests are tuned to be congruent. Environmental and economic factors along with financial characteristics of companies impede information asymmetry and agency problems to be solved completely (Jensen & Meckling, 1976). Accounting disclosures under uncertain (risky) situations are essential for investors. So, firms attempt to make high-quality disclosures to attain investors’ trust and reduce their uncertainty.

A key challenge for well-developed markets is optimal allocation of savings to existing investment opportunities. Usually, there are many firms and entrepreneurs who are willing to attract resources for purposes of applying their business ideas. While both investors and practitioners are willing to operate business activities, matching resources to investment opportunities in business sector is highly complicated for two reasons. First, managers have a better knowledge about the value of investment opportunities than the depositors, and also, they have more incentive to overstate the value of their firms. Therefore, investors face information asymmetry problem when deciding on investment in firms. Second, after depositors (investors) have invested their money in a firm, managers have an incentive to use their investment in an inappropriate way, so that the agency problem appears (Beyer et al., 2010; Healy & Palepu, 2001).

Accounting information (including accounting disclosures) plays important roles in well-developed capital markets. First, accounting information enables those providing firm’s capital (including shareholders’ and creditors’) to evaluate potential return for investment opportunities (valuating or ex-ante role of accounting information). Second, accounting information enables those providing firm’s capital to monitor the usage of contributed capital to the firm (stewardship or ex-post role of accounting information). Generally, agency problems and information asymmetry constrain optimal allocation of resources in capital markets (Beyer et al., 2010). Accounting disclosure is a good mechanism to facilitate safe transmission of information between management and investors, which play an important role in mitigating information asymmetry (Healy & Palepu, 2001).

Capital structure is among the important factors affecting information asymmetry and agency problem. Some theoreticians believe that, according to active monitoring hypothesis (Demiralp et al., 2011), existence of institutional investors among shareholders of the firm (ownership concentration) can reduce information asymmetry and in turn mitigate agency costs, mainly due to the monitoring role of these types of investors. On the other hand, based on self-interest hypothesis (Statman, 2011), the institutional investors have more incentive to access private information about the firm for their trading purposes. In this situation, these investors are less interested in monitoring firm’s activities and more interested in disclosure by the firm and, therefore, are likely to increase information asymmetry and in turn increase agency problems (Jiang et al., 2011).

In this backdrop, the main problem to be addressed in this article is the impact of capital structure (including ownership concentration and institutional ownership) and disclosure quality (including reliability and timeliness of disclosure) on information asymmetry.

Literature Review

Botosan (1997) found a negative relation between the level of disclosure index and information asymmetry among manufacturing companies with less analyst coverage in the security market. Lang and Lundholm (2000) argued that disclosure of corporate governance and information about capital structure reduced information asymmetry. So, shareholders could more effectively monitor management actions.

Noravesh and Ebrahimi (2005) examined the relationships between shareholder composition, information asymmetry, and usefulness of performance measures. Their purpose was to provide evidence on the role of institutional investors in reducing information asymmetry among firms listed on the Tehran Stock Exchange (TSE). Their results showed that firms with more institutional investors provided more information about future earnings compared to firms with less institutional investors.

Beeks and Brown (2006) suggested that firms with more concentrated ownership structure made better accounting disclosures which reduced information asymmetry. LaFond and Watts (2008) showed that firms with more investment opportunities had lower financial reporting quality and were more likely to have lower level of accounting disclosures. Conversely, during the finalization of investment projects, when the firms’ potential for future growth is lower, information asymmetry could reduce and, therefore, the quality of financial reporting could improve.

Hasas and Bazazzadeh (2008) examined the relation between institutional investors and firms’ value; their findings, consistent with active monitoring hypothesis, showed a significant positive relation between the level of institutional ownership and value of the firm. Nevertheless, their other findings, contrary to the interest convergence hypothesis, did not prove any significant relation between institutional ownership concentration and value of the firm.

Khlif and Souissi (2010) found a positive relation between profitability of the firm and information asymmetry. Jiang et al. (2011) examined the impact of ownership concentration and discretionary disclosure on information asymmetry among New Zealand firms. Their findings showed a positive impact of ownership concentration along with a negative impact of discretionary disclosure on information asymmetry. Reeb and Zhao (2013) tested the relationships between education, experience, and communication among board members, disclosure quality, and information asymmetry. Their findings prove an inverse relation between education, experience and communication among board members and information asymmetry.

Etamadi, Amirkhani, and Rezaei (2011) studied the value relevance of disclosure with respect to information asymmetry. Their study revealed that disclosures made via financial reports had information content about future earnings, and investors used this information for purposes of their decision-making. Osta (2011), in his study on relationship between ownership structure and earnings management, suggested that differences in ownership structure could justify earnings management. In other words, his study showed a significant negative relation between institutional ownership, management ownership, and earnings management, but a significant positive relation between company ownership and earnings management. Rahimian, Hemati, and Soleymanifard (2012) studied the impact of earnings quality on information asymmetry among the firms listed on TSE. Their study provided evidence on negative impact of earnings quality on information asymmetry of firms.

Dai, Kong, and Wang (2013) investigated how information asymmetry and mutual fund ownership affected the listed companies’ earnings management. The outcomes of the study showed that reducing information asymmetry improved firms’ earnings management behaviour. Further, they also found that compared to the short-term mutual funds, the long-term mutual funds promoted earnings quality more by adopting a monitoring role.

Han, Jin, and Kang (2013), by measuring information precision, observed that managerial ownership was positively associated with financial analysts’ public and private information precisions, largely consistent with the alignment view of managerial equity ownership.

Kosaiyakanont (2013) examined the importance of financial analysts as information intermediaries in the emerging capital market of Thailand. The findings provided evidence that more analysts following a company mitigated information asymmetry among investors and led to improved stock market liquidity in Thailand’s emerging capital market, similar to the role they had been found to play in developed markets.

Uyar, Kilic, and Bayyurt (2013) investigated the factors that impacted the voluntary information disclosure level of Turkish companies. The findings revealed an association between the voluntary information disclosure level and the variables such as firm size, auditing firm size, proportion of independent directors on the board, institutional/corporate ownership, and corporate governance.

Niléhn and Thoresson (2014, p. 47) studied the variables affecting the extent of corporate voluntary information in Sweden. The findings showed asymmetric information and agency costs as important determinants of the extent of strategic corporate information, that is, voluntary information, in Swedish companies. Larger firms seemed to reduce agency costs and narrowed the information asymmetry by increasing the level of information disclosed.

Ali (2014) investigated the impact of ownership structure on corporate voluntary disclosure in Tunisia. The results showed that the level of voluntary disclosure was negatively significantly related to the blockholder ownership and family ownership, while it was positively related to the proportion of institutional investor ownership and firm performance.

Boubaker, Hamrouni, and Liang (2015) examined the relative performance of several corporate governance factors, specifically the characteristics of board of directors, managerial ownership, and voluntary disclosure, in improving firm information environments based on a B-convex method on a sample of 70 non-financial French-listed firms, belonging to the SBF 120 index. The results of the study showed that 68.57 per cent of the sample firms were located on the efficiency frontier. Corporate governance practices appeared to serve as effective monitoring for the top executives of these firms, which reduced information asymmetry between insiders and outsiders, thereby improving the information environment.

Satta, Parola, Profumo, and Penco (2015) studied the explanatory power of corporate governance issues, such as ownership structure and board composition, as potential determinants of communication quality. The results showed that a diffuse ownership along with the existence of an audit committee was associated with increased qualitative levels of voluntary disclosure, while managerial ownership, board size, and the number of board committees presented a negative relation to disclosure. Moreover, institutional investors’ ownership and the presence of independent directors were not related to disclosure quality.

Albawwat and Yazis Ali Basah (2015) studied the relationship between characteristics of corporate governance and structure of ownership on voluntary disclosure in interim financial reports during 2009–2013. A substantial degree of voluntary disclosure was demonstrated in high-level corporate governance awareness and implementation in Jordan. Specifically, the factors of board compensation, audit firm size, and government ownership significantly impacted voluntary disclosure.

Hypotheses Development

Agency problems and information asymmetry limit optimal allocation of resources in capital markets (Beyer et al., 2010). Accounting disclosure is a mechanism which facilitates safe transmission of information between management and investors, and plays an important role in mitigating information asymmetry (Healy & Palepu, 2001). Based on these concepts, the first and second hypotheses are developed as follows:

H1: There is a significant relation between timeliness of disclosures and information asymmetry.

H2: There is a significant relation between reliability of disclosures and information asymmetry.

According to the active monitoring hypothesis, existence of institutional investors and major investors among shareholders of the firm (ownership concentration) can reduce information asymmetry and in turn mitigate agency costs, mainly due to the monitoring role of these investors. On the other hand, based on self-interest hypothesis, institutional investors and major investors have more incentive for accessing private information about the firm for their trading purposes. In this situation, these investors are less interested in monitoring firm’s activities and more interested in disclosure by the firm and, therefore, are likely to increase information asymmetry and in turn increase agency problems (Jiang et al., 2011). Based on this, the third and fourth hypotheses are as follows:

H3: There is a significant relation between ownership concentration and information asymmetry.

H4: There is a significant relation between institutional ownership and information asymmetry.

Methodology

The current study is considered as a semi-experimental study. An inductive method was applied on the ex-post data (using historical data), and correlation analysis was used for the statistical analysis. The initial sample included data from all the firms listed on TSE during the years 2007–2014. The firms that did not meet any of the following conditions were omitted:

Availability of necessary data for measuring the variables Listed at least from 2006 on TSE, and continued to be listed till 2014. Fiscal year ended March 21 every year (end of calendar year in Iran). Did not operate as financial intermediaries.

Considering the above conditions, the final sample included 102 firms (510 firm-years). The required data for the study were collected using Iranian databases including Rahavard Novin, firms’ prospectuses, and their audited financial statements. The statistical analysis used EViews and SPSS software, and the hypotheses were tested using t-student statistic at the significance level of 95 per cent.

The Model

Following Jiang et al. (2011), the first and second hypotheses were tested using Model 1:

Model 1

SPREAD it = β0 + β1Timeliness it + β2Reliability it +β3Size it + β4Trading volume it + β5Stock price it + ε i,t

Consistent with Jiang et al. (2011), the following regression model was used for testing the third and fourth hypotheses:

Model 2

SPREAD it = β0 + β1Concentration it + β2Insown it +β3Size it + β4Trading volume it + β5Stock price it + ε i,t

Dependent Variable

SPREAD = information asymmetry measured as bid-ask spread for firm i in year t.

Independent Variables

Timeliness = proxy variable for measurement of timeliness of disclosures.

In this article, timeliness of disclosures was measured using corporate disclosure scores published by the Iranian Securities and Exchange Committee (SEC). Information dissemination scores for the firms were calculated based on their reporting characteristics such as reliability and timeliness of their reporting.

Reliability = proxy variable for measurement of reliability of disclosures.

In this article, reliability of disclosures was measured using corporate disclosure scores published by the Iranian SEC. Information dissemination scores for the firms were calculated based on their reporting characteristics such as reliability and timeliness of their reporting.

Concentration = proxy variable for ownership concentration. By ownership concentration, we mean percentage of shares owed by main owners. Shareholders owning more than 5 per cent of all outstanding shares at the end of the year were classified as the main owners.

InsOwn = percentage of shares held by governmental organizations and other public companies.

Control Variables

Size = measured as logarithm of total assets at the end of the year.

Trading volume = measured as total number of shares traded during the year.

Stock price = measured as closing price of firm’s stock at the year end,

Findings

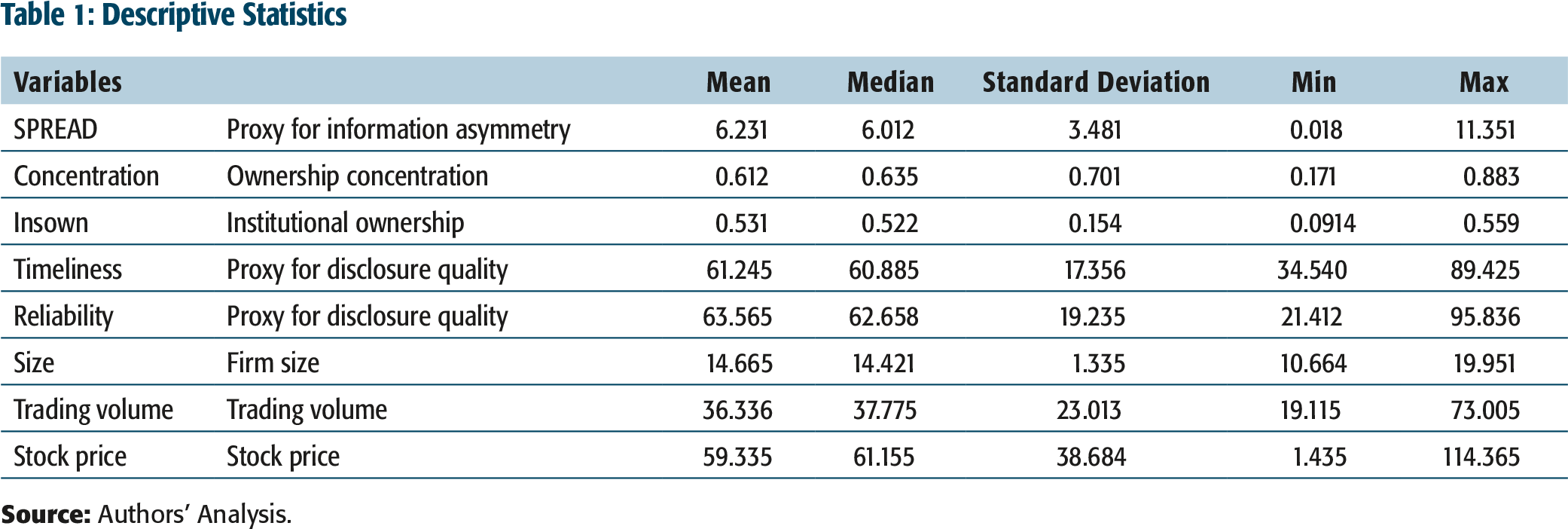

Descriptive Statistics

Descriptive statistics of independent, dependent, and control variables for data from the 102 sample firms, including mean, median, standard deviation, minimum, and maximum are presented in Table 1.

Determination of an Appropriate Model for Regression Estimation

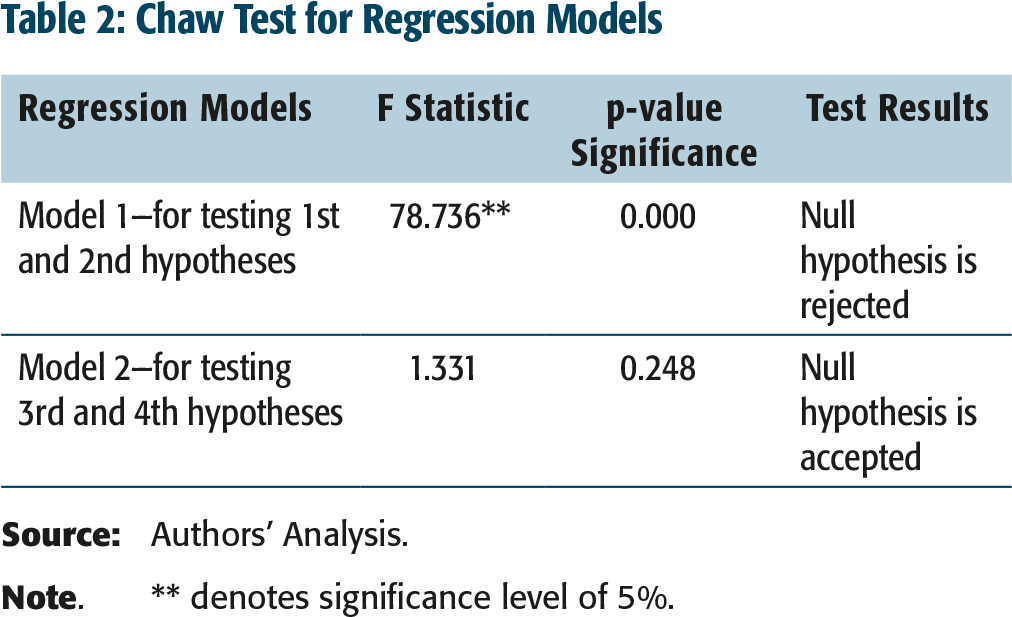

Chaw Test

Results from F-test for regression models used in this study are shown in Table 2.

Descriptive Statistics

Chaw Test for Regression Models

For Model 1 used to test the first and second hypotheses, considering the significance of Chaw’s test results, null hypothesis (which says that using pool model is more appropriate) is rejected. In other words, due to existing singular or group effects, panel data method should be used for regression estimation. In the following section, results of Hausman test to determine whether the panel data is random effect or fixed effect are described.

For Model 2 used to test the third and fourth hypotheses, considering the significance of Chaw’s test results, null hypothesis (which says that using pool model is more appropriate) is accepted. In other words, since there are no singular or group effects, pool data method should be used for regression estimation so that there is no need to perform Hausman test.

Hausman Test

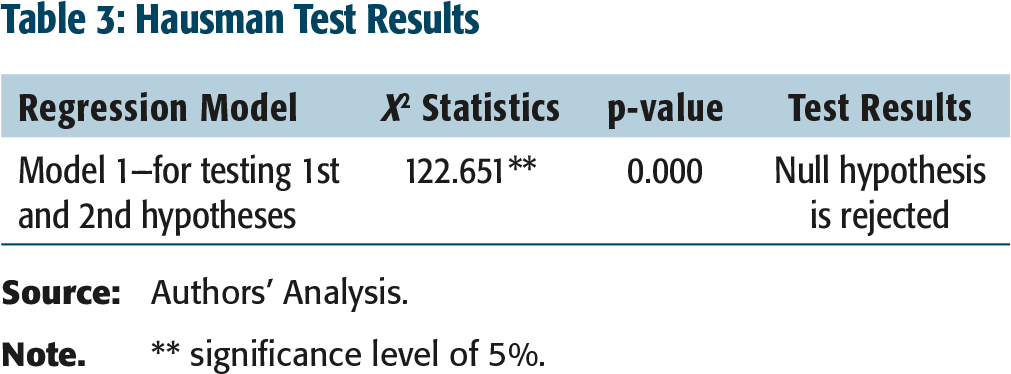

After constants are determined (not to be the same for different years), there is a need to find an appropriate method (fixed effects or random effects) for regression estimation purposes. In this article, Hausman test was used to test the null hypothesis, that is, random effect estimation is consistent against alternative hypothesis, arguing that random effect estimation is inconsistent.

The results from Hausman test for Model 1 used to test the first and second hypotheses are presented in Table 3. The Hausman test output shows that X2 statistic for the said model equals to 122.651, which is significant at 5 per cent level, and leads to the disapproval of null hypothesis; thus, considering this result, panel data with fixed effects was used for the estimation of Model 1 to test the first and second hypotheses.

Hausman Test Results

Testing Classic Assumptions for Regression Estimation

Before the estimation of any regression model, the classic assumptions behind the linear regression models were tested. These tests and their results are discussed in the next section.

Normality of Independent Variable Distribution

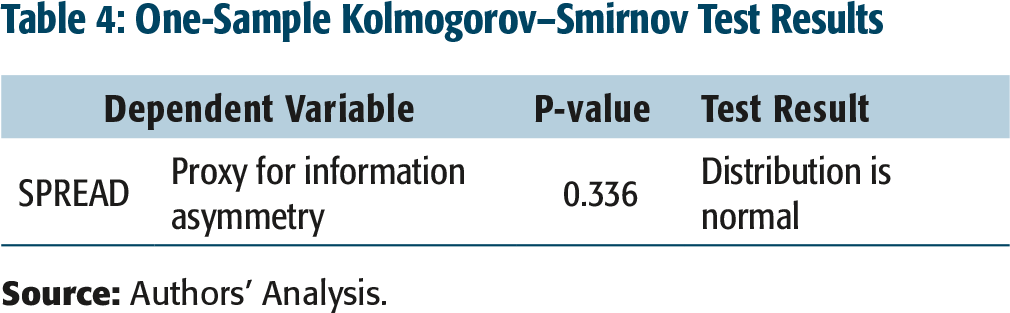

The Kolmogorov–Smirnov test was used to determine whether the distribution of independent variables was normal, results of which are presented in Table 4. Since the significance level calculated in the Kolmogorov–Smirnov test is more than 5 per cent (0.586), as presented in Table 4, null hypothesis for this test is rejected and, therefore, we can conclude that the distribution of SPREAD (independent variable) is normal.

One-Sample Kolmogorov–Smirnov Test Results

Residuals’ Autocorrelation

The Durbin–Watson statistic was used to test the presence of autocorrelation in the residuals. This statistic is generally used to test the following hypotheses in this respect:

H0 = There is no significant autocorrelation in the residuals

H1 = There is a significant autocorrelation in the residuals

If the Durbin–Watson statistic is between 1.5 and 2.5, then the null hypothesis (no autocorrelation between residuals) is accepted; else, the alternative hypothesis is accepted.

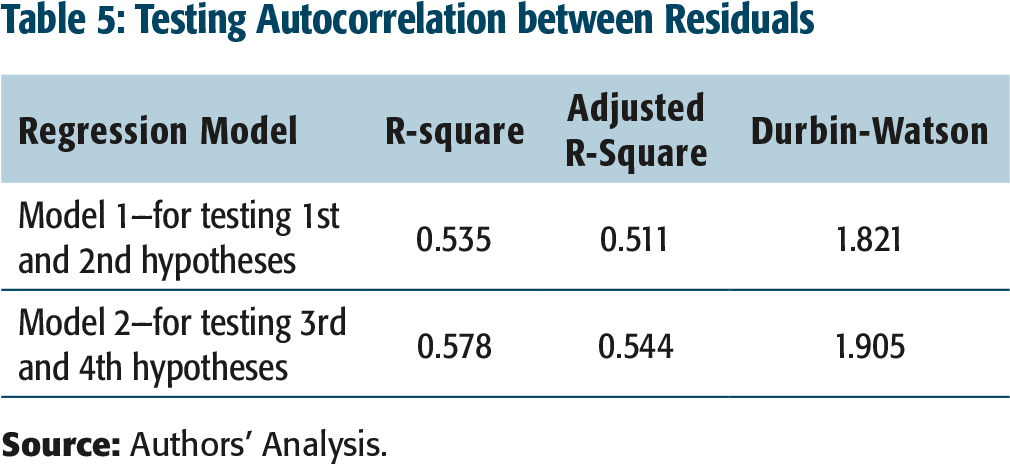

Durbin–Watson statistic, R-square, and adjusted R-square for both the models used in this article are shown in Table 5.

Testing Autocorrelation between Residuals

As shown in Table 5, Durbin–Watson statistic for both the models is between 1.5 and 2.5. Therefore, the null hypothesis, that there is no significant autocorrelation in the residuals, is accepted.

After testing the classic assumptions for regression models, the results from the estimation of the regression models and the test of the main research hypotheses are discussed in the following section.

Testing Research Hypotheses

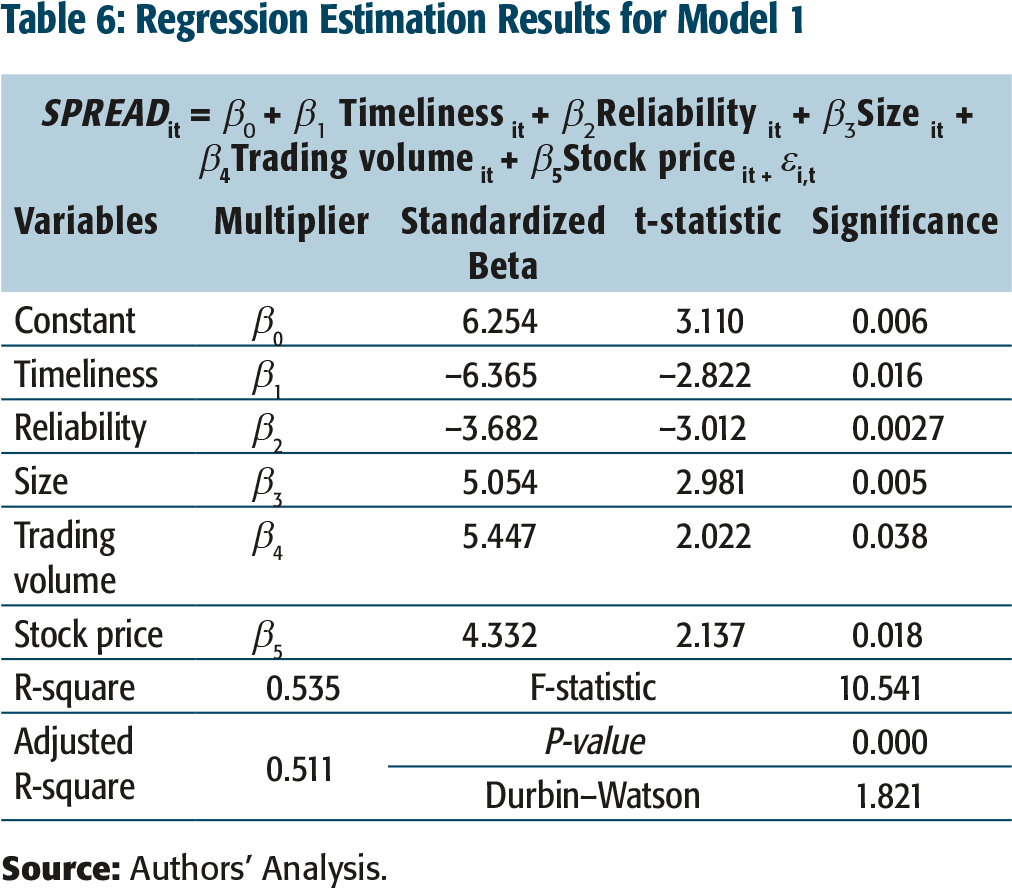

The results of estimation of regression Model 1 used to test the first and second hypotheses are presented in Table 6. As shown in Table 6, F-statistic for Model 1 is 10.541 which proves that goodness of fit for this model is of appropriate level. Also, estimated R-square and adjusted R-square for Model 1 are 53.5 per cent and 51.1 per cent, respectively. Based on this, therefore, it can be concluded that explanatory variables used in the regression Model 1 can explain only 53.5 per cent of the changes in information asymmetry.

Regression Estimation Results for Model 1

It should be noted that the positive (negative) sign of figures presented in Standardized Beta column shows the direct (reverse) impact of each variable on information asymmetry of the sample firms.

H1: There is a significant relation between timeliness of disclosures and information asymmetry.

As shown in Table 6, timeliness of disclosures is significant at 5 per cent (sig. = 0.016); also, the absolute value of t-student statistic for this variable is –2.822, which proves that it is significant at 5 per cent level. Therefore, at 95 per cent level of confidence, the first research hypothesis that there is a significant relation between timeliness of disclosures and information asymmetry is accepted.

H2: There is a significant relation between reliability of disclosures and information asymmetry.

As shown in Table 6, reliability of disclosures is significant at 5 per cent (sig. = 0.0027); also, the absolute value of t-student statistic for this variable is –3.012, which proves that it is significant at 5 per cent level. Therefore, at 95 per cent level of confidence, the second research hypothesis, that there is a significant relation between reliability of disclosures and information asymmetry, is accepted.

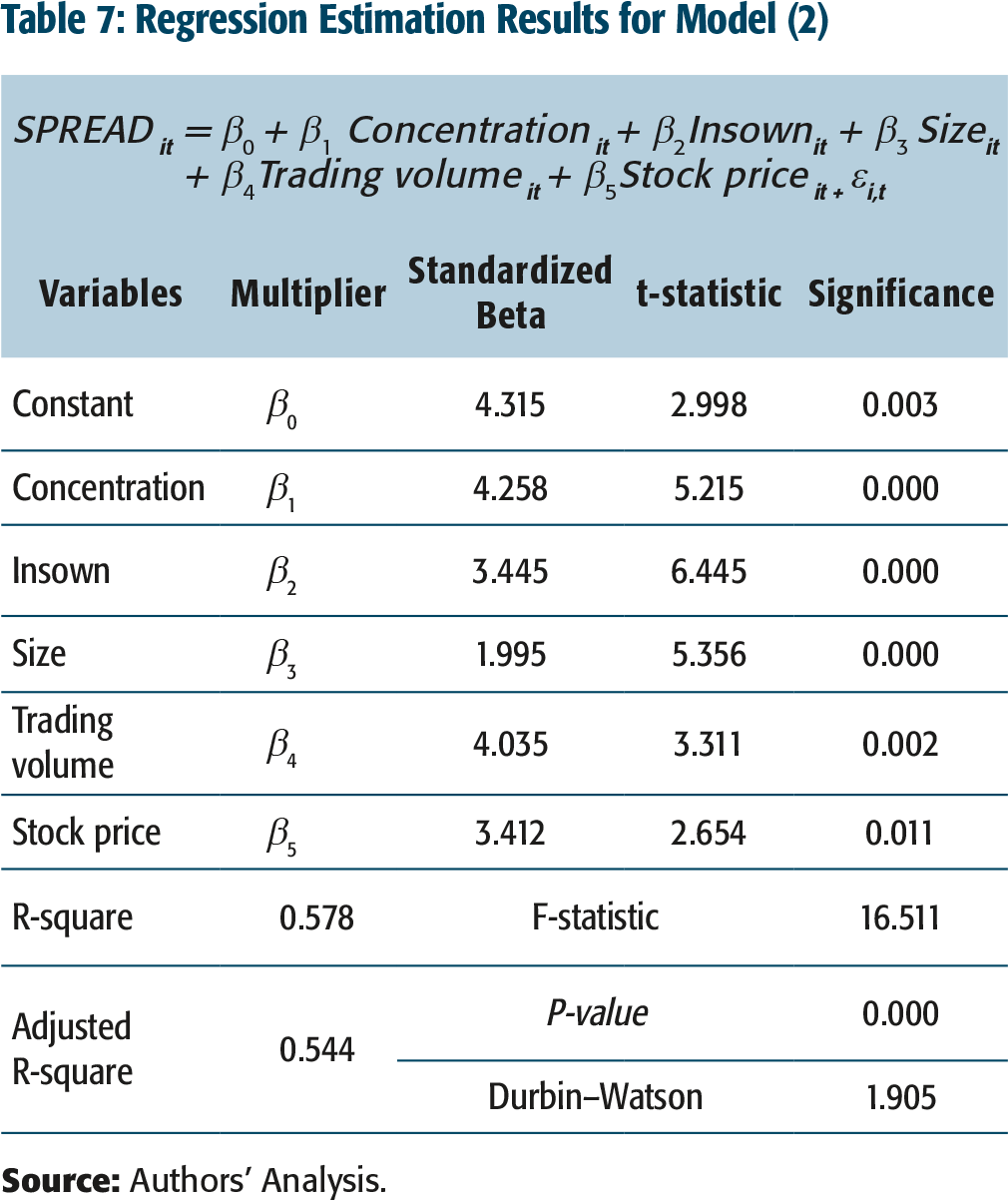

Results from the estimation of regression Model 2 used to test the third and fourth hypotheses are presented in Table 7. As shown in this table, F-statistic for Model 2 is 16.511, which proves that goodness of fit for this model is of appropriate level. Also, estimated R-square and adjusted R-square for Model 1 are 57.8 per cent and 54.4 per cent, respectively. Based on this, therefore, it can be concluded that explanatory variables used in the regression Model 2 can explain only 57.8 per cent of the changes in information asymmetry. It should be noted that positive (negative) sign of figures presented in Standardized Beta column shows the direct (reverse) impact of each of the variables on information asymmetry of the sample firms.

Regression Estimation Results for Model (2)

H3: There is a significant relation between ownership concentration and information asymmetry.

As shown in Table 7, ownership concentration is significant at 5 per cent (sig. = 0.000); also, the absolute value of t-student statistic for this variable (5.215) is higher than the relative value from t-student table at the same degree of freedom, which proves that it is significant at 5 per cent level. Therefore, at 95 per cent level of confidence, the third research hypothesis that there is a significant relation between ownership concentration and information asymmetry is accepted. Moreover, positive sign of standardized beta estimated for ownership concentration (4.258) in the regression Model 2 can be considered as its positive (direct) impact on information asymmetry.

H4: There is a significant relation between institutional ownership and information asymmetry.

As shown in Table 7, institutional ownership is significant at 5 per cent (sig. = 0.000); also, the absolute value of t-student statistic for this variable (6.445) is higher than the relative value from t-student table at the same degree of freedom, which proves that it is significant at 5 per cent level. Therefore, at 95 per cent level of confidence, the fourth research hypothesis that there is a significant relation between institutional ownership and information asymmetry is accepted. Moreover, the positive sign of standardized beta estimated for institutional ownership (3.445) in the regression Model 2 can be considered as its positive (direct) impact on information asymmetry.

Conclusion

Accounting information (including accounting disclosures) plays an important role in well-developed capital markets. First, accounting information enables those providing firm’s capital (including shareholders and creditors) to evaluate potential return for investment opportunities (valuating or ex-ante role of accounting information). Second, accounting information enables those providing firm’s capital to monitor usage of contributed capital to the firm (stewardship or ex-post role of accounting information). Generally, agency problems and information asymmetry constrain optimal allocation of resources in capital markets (Beyer et al., 2010). Accounting disclosure is a good mechanism to facilitate safe transmission of information between management and investors, which plays an important role in mitigating information asymmetry (Healy & Palepu, 2001).

Capital structure is among the important factors affecting information asymmetry and agency problem. Some theoreticians believe that according to active monitoring hypothesis, existence of institutional investors and main investors among shareholders of the firm (ownership concentration) can reduce information asymmetry and in turn mitigate agency costs, mainly due to the monitoring role of these types of investors. On the other hand, based on self-interest hypothesis, institutional investors and main investors have more incentive to access private information about the firm for their trading purposes. In this situation, these investors are less interested in monitoring firm’s activities and more interested in disclosure by the firm, and, therefore, are likely to increase information asymmetry, in turn increasing the agency problems (Jiang et al., 2011).

Statistical results derived from the analysis of data from 102 selected firms during the period 2007–2014 show positive (direct) and negative (reverse) impacts of ownership structure and disclosure quality on information asymmetry, respectively. These findings suggest that information asymmetry is more in firms which have major investors, higher level of institutional ownership, and lower disclosure quality compared to other firms. Overall, the findings are consistent with the self-interest hypothesis.