Abstract

Keywords

Anil Rai Gupta, the son of the founder of Havells, Qimat Rai Gupta, was proud of the strong foundation of the Havells brand. While he was aware of the extraordinary accomplishments of his father, he was also mindful of strong competitors in several product categories that posed considerable threat for the diversified Havells brand. The economic slowdown had a deep impact on the industrial growth in the Indian economy and this impacted the growth rate of Havells.

About Havells

1

Details of all milestones from the inception to present are retrieved from: http://www.havells.com/milestones.aspx

Details of all milestones from the inception to present are retrieved from: http://www.havells.com/milestones.aspx

Havells was a $1.3 billion fast moving electrical goods (FMEG) company with a strong global footprint. 2

Information released by the company in February 2014. Retrieved from: http://www.havells.com/Admin/SiteMedia/CompanyPdfs/February%202014%20Presentation.pdf

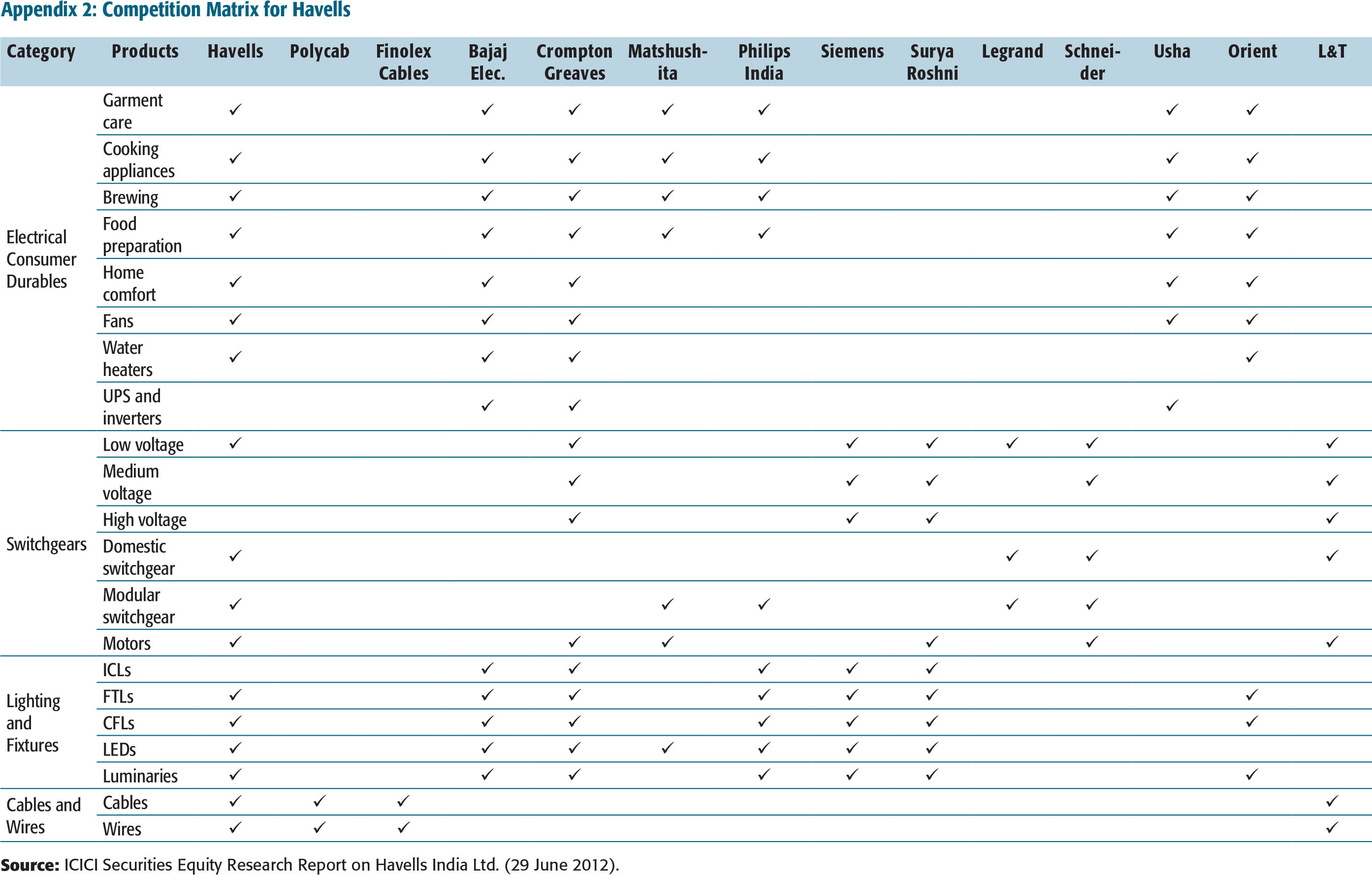

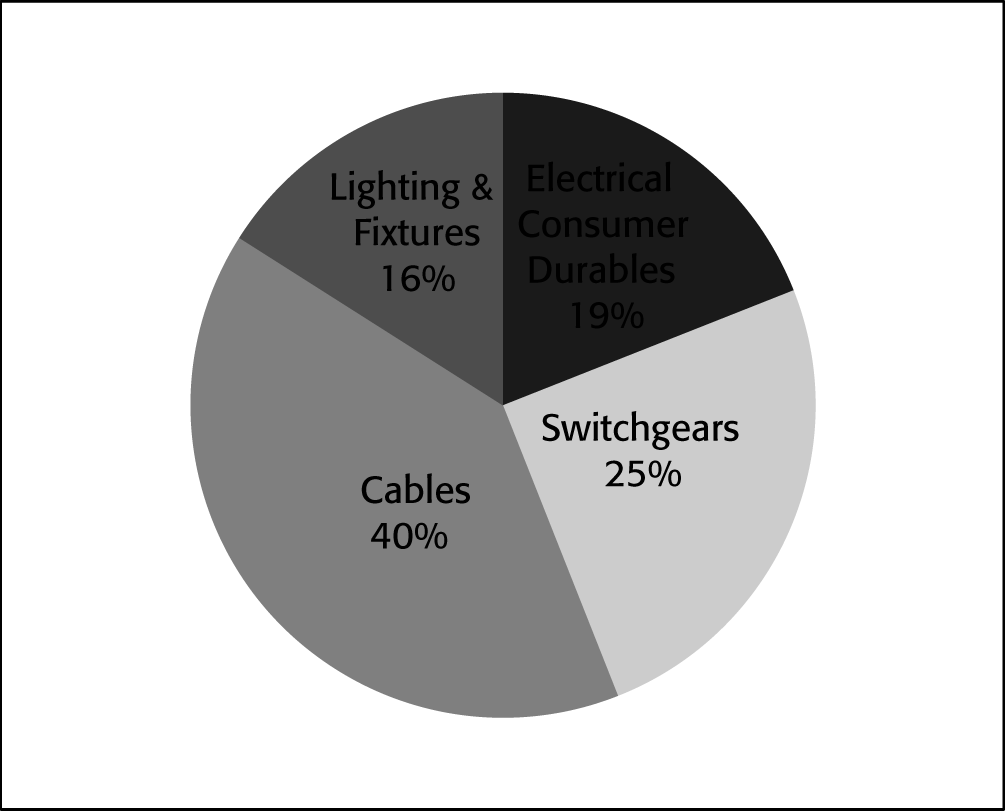

Havells operated in both industrial as well as consumer markets. Its product range comprised four broad categories—switchgears, cables, lighting and fixtures, and electrical consumer durables (ECDs) (see Exhibit 1). The portfolio of Havells included products such as industrial and domestic circuit protection switchgears, cables and wires, motors, fans, power capacitors, compact fluorescent lamps (CFLs), luminaries for domestic, commercial and industrial applications, modular switches, water heaters and domestic appliances covering the entire gamut of household, commercial and industrial needs. The company had 11 state-of-the-art manufacturing units located in India and 7 located in Europe, Latin America, Africa and China. Havells owned several well-known brands such as Havells, Crabtree, Standard, Sylvania, Concord and Lumiance. It acquired several international certifications such as CSA, KEMA, CB, CE, ASTA, CPA, SEMKO, SIRIUM (Malaysia), SPRING (Singapore), TSE (Turkey), SNI (Indonesia) and EDD (Bahrain) for various products.

Competition Matrix for Havells

Over a period of time, Havells moved from being a predominantly industrial brand to a consumer brand. It consistently invested in branding and distribution in order to build a consumer brand in the FMEG business. It also invested in setting up world-class manufacturing facilities. Most of the products of the company, including components, were manufactured in-house to adhere to strict quality standards, which was the hallmark of the Havells brand. The corporate brand stood for quality and innovation across all product verticals. The founder’s lineage ensured that the company always focused on building strong, strategic partnerships with its channel intermediaries.

Anil Rai Gupta pronounced the reason for Havells’ transition to a consumer brand:

We wanted to keep a balance in the company. We were too focused on the industry (industrial market) which was largely dependent on government policies. So, if there was a downturn in the economy, industry (industrial market) was the first to get impacted. We, therefore, thought of slowly moving into the consumer space as well. And we always had a brand mindset which typically worked more with consumer goods than industrial goods. So, for us, it was a natural way of moving into consumer products. Even our advertisements started promoting products that were very drab in nature. Nobody really thought of branding or promoting an MCB or an RCCB. But we did that. So, the intent clearly was to push this brand more and more towards consumers, and reach out to them directly. As the company transformed from being an industrial brand to supplying products for consumer markets, it introduced products such as CFLs, fans, modular switches for domestic usage, luminaries, water heaters and domestic appliances. It advertised extensively to target the consumer market. The company also started its exclusive stores called ‘Havells Galaxy’ that were the flagship stores of the brand. These stores showcased the entire consumer product range of Havells.

Havells was an ambitious, yet a conservative group. Its policies were guided by better profitability, free cash flow and superior return to its shareholders. 3

For full information about the financials of Havells, please refer to http://www.havells.com/InvestorSection.aspx

For updated results for FY 2013–2014, refer to http://www.havells.com/Admin/SiteMedia/Investor-Section/PublishedReport/Havells%20Financial%20Results%20FY%2014.pdf

For audited financial results for the financial year 2013–2014, please refer to http://www.havells.com/Admin/SiteMedia/Investor-Section/InformationUpdate/Havells%20Information%20Update%20FY14.pdf

An Entrepreneurial Success Story

6

Retrieved from: http://www.havells.com/chairman-profile.aspx; http://www.havells.com/ediaimage/754239713754239713754239713754239713.pdf

Retrieved from: http://www.havells.com/chairman-profile.aspx; http://www.havells.com/ediaimage/754239713754239713754239713754239713.pdf

The journey of Havells was the stunning entrepreneurial success story of its founder, Qimat Rai Gupta, who quit his teaching job in a school in the north Indian state of Punjab and came to Delhi in the year 1958. He started an electrical goods trading company in Bhagirath Palace 7

This is the wholesale market for electrical goods in Delhi.

In 1992, Qimat Rai Gupta’s son, Anil Rai Gupta, joined the family business as the Joint Managing Director and in 1995, his cousin, Ameet Gupta, joined as the Director of the company. Even though they belonged to the next generation, there was no friction between them, as Qimat Rai Gupta was well-versed with the changing trends in the business environment.

In 2000, the company acquired a stake in Duke Amics Electronics (P) Ltd. to manufacture electronic meters. It also acquired a controlling stake in Standard Electricals Ltd., which became a 100 per cent subsidiary in 2002. In 2001, the company consolidated its business by merging ECS limited with the MCCB business of Crabtree. The company further diversified its business and moved into consumer products such as CFLs and fans in the year 2003. Brand extensions of the Havells corporate brand name into other product categories brought in growth for the company. By 2005, the company had set up more manufacturing units for several products in other parts of India such as Faridabad, Baddi, Noida and Haridwar. Havells set up a research and development (R&D) unit in Noida in the year 2005. In 2006, Crabtree India merged with Havells India. Havells became the first company to obtain an Indian Standards Index (ISI) certification for its CFL range. In this year, the company also initiated several CSR activities, such as participation in the mid-day meal programme of the Government of India.

2007 was the watershed year for Havells, as it acquired the lighting business of the German major SLI Sylvania for $300 million. This was the largest acquisition by an Indian electrical company. With this acquisition, Havells became the fourth largest global player in the lighting business after Philips, Osram and General Electric (GE).

By the end of 2008, the company had forayed into the electrical motors business. Havells set up the largest plant for electrical motors in Neemrana, Rajasthan. After 2008, the company set up several manufacturing plants and expanded aggressively into the domestic appliance business.

Philosophy of the Founder

Qimat Rai Gupta thought that it was important to evolve over time. He strongly believed in the power of his employees and channel intermediaries. If these two groups supported him, the company could succeed. Dealers and employees were always the fulcrum of Havells’ strategy. He also believed that with a shift in preferences, consumers were willing to pay more for quality products. The Chairman, Qimat Rai Gupta, wanted to build a strong corporate brand that could help the company tide over difficult times besides providing an unbeatable competitive advantage. He also believed in the power of constant and sometimes drastic innovation.

Every morning, the Chairman held meetings with the key people in the company to discuss the current direction of the company and plan its future initiatives. He believed in a participative management style, deviating from the usual family business practices, as the company was run by a professional management team. These meetings helped in nimble decision-making, which was critical for a company as large as Havells.

Acquisition of Sylvania and Realizing Global Ambitions

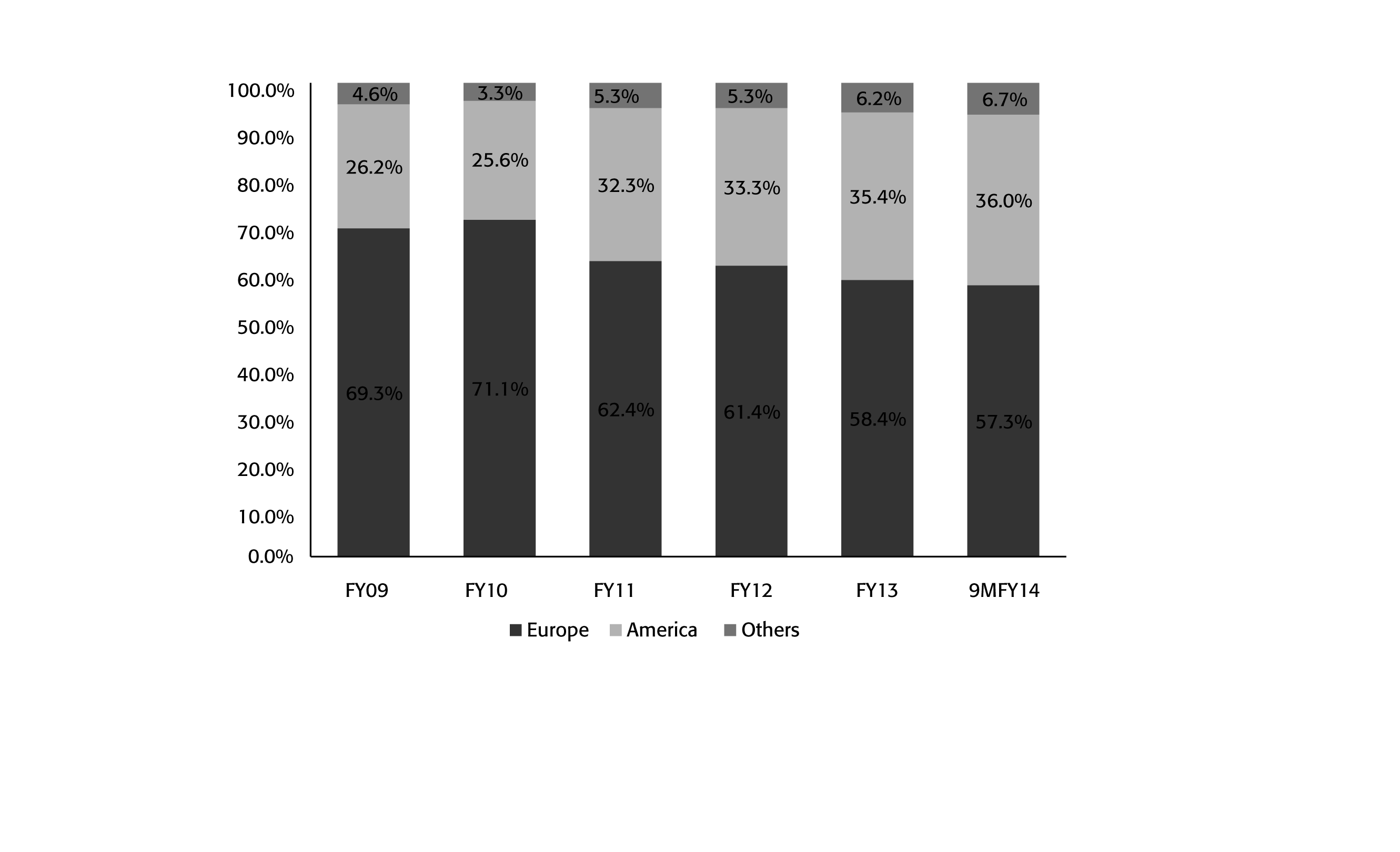

While Havells was a company known for its electrical switches, MCBs and flexible cables, Sylvania was well known for lighting and fixtures. Therefore, for Havells, synergy existed in acquisition. With the acquisition of Sylvania, Havells transcended from a predominantly India-based company to a global company, with operations in more than 50 countries. The Sylvania acquisition resulted in a drastic increase in the scale of operations for Havells. Sylvania had more than 20,000 dealers in Latin America, Europe, Africa and Asia, 8

In Mexico, United States, Australia and New Zealand, however, Sylvania’s business had been sold to Osram, which in turn had sold it to a consortium of three private equity firms—DDG Capital, JP Morgan and Subros.

The Sylvania acquisition was done for several reasons—firstly, as a company, we had a global aspiration—we wanted to send this brand world over. Secondly, we had bought a company which exactly matched what we really wanted. The foundation of Havells had three pillars—the brand, the manufacturing set-up and the distribution set-up. Sylvania was all of this—a 100-year old brand with an extensive distribution network and great manufacturing capability. If we hadn’t acquired Sylvania, we would have taken 40 years to go global. Sylvania had presence in 50 countries and had 90 offices. We couldn’t have got this scale otherwise; so, it was a natural choice—when Sylvania was offered to us, we took it up.

Havells Sylvania decided to focus on technologies such as CFL and light-emitting diode (LED) that were still evolving at that time. These technologies addressed the core issues of energy conservation and environmental preservation. These technologies had a huge demand in the European market 9

European demand for energy-efficient lighting was $930 million in the year 2007, out of which the demand for CFL was $883 million. This market was expected to reach $1.4 billion by the year 2014.

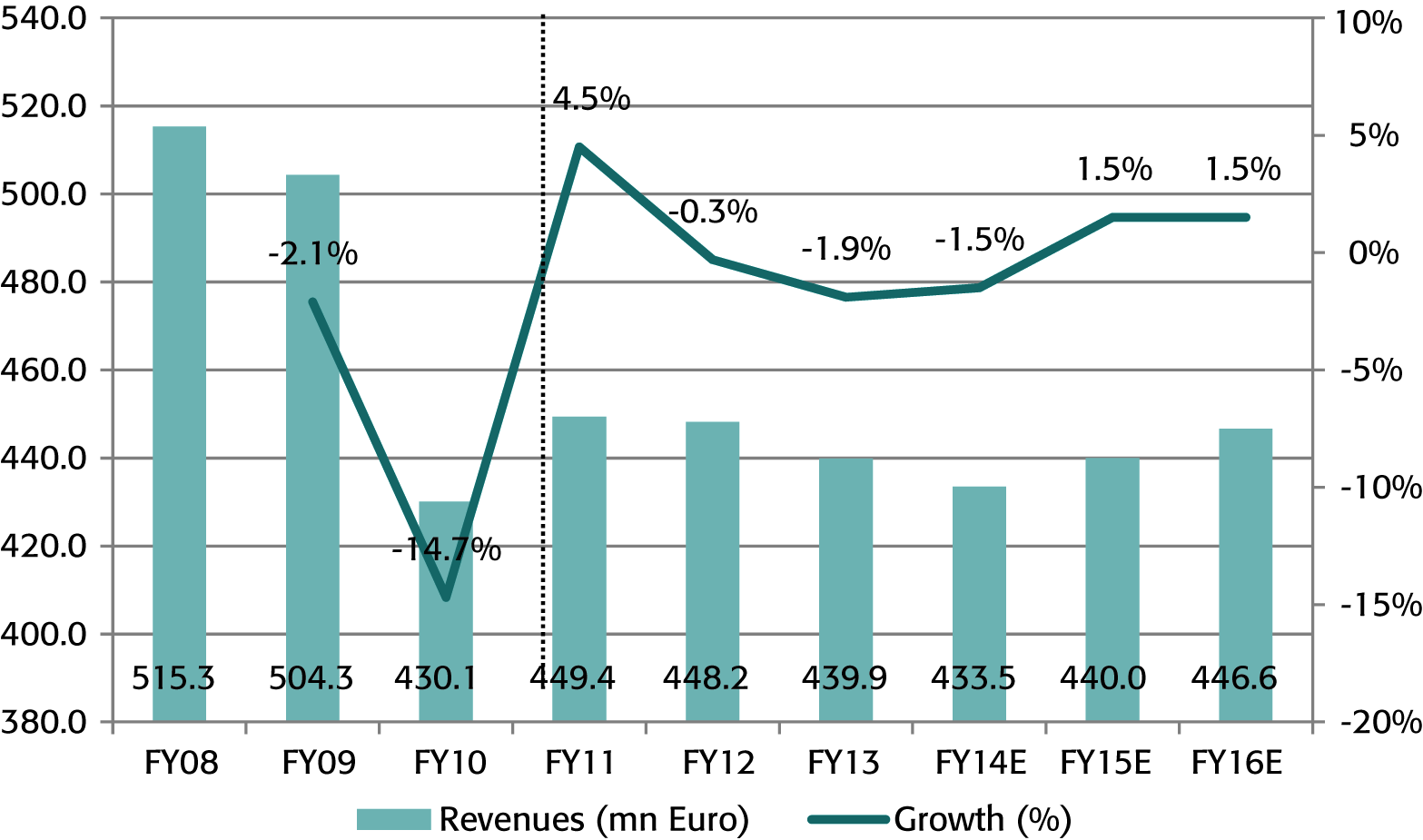

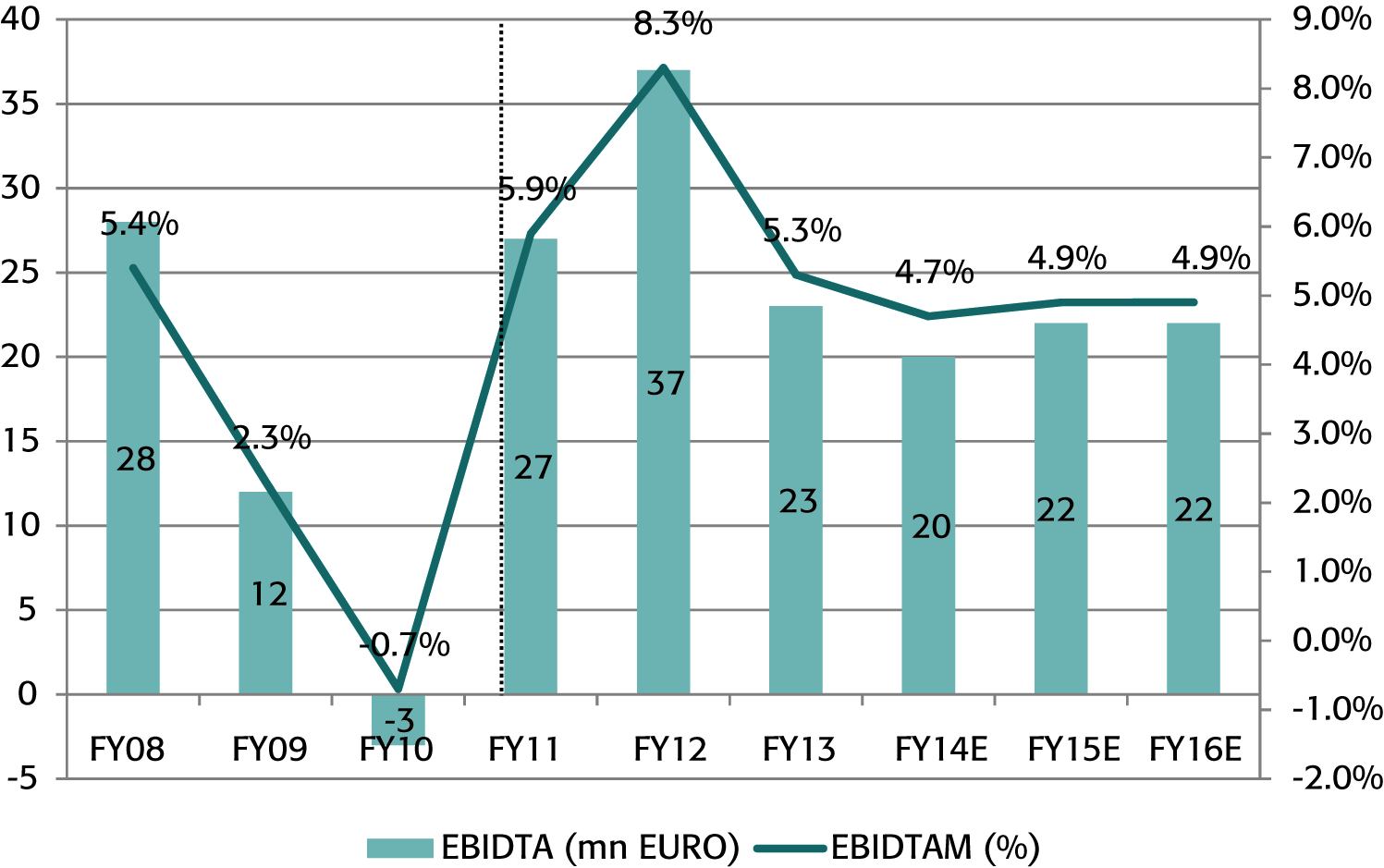

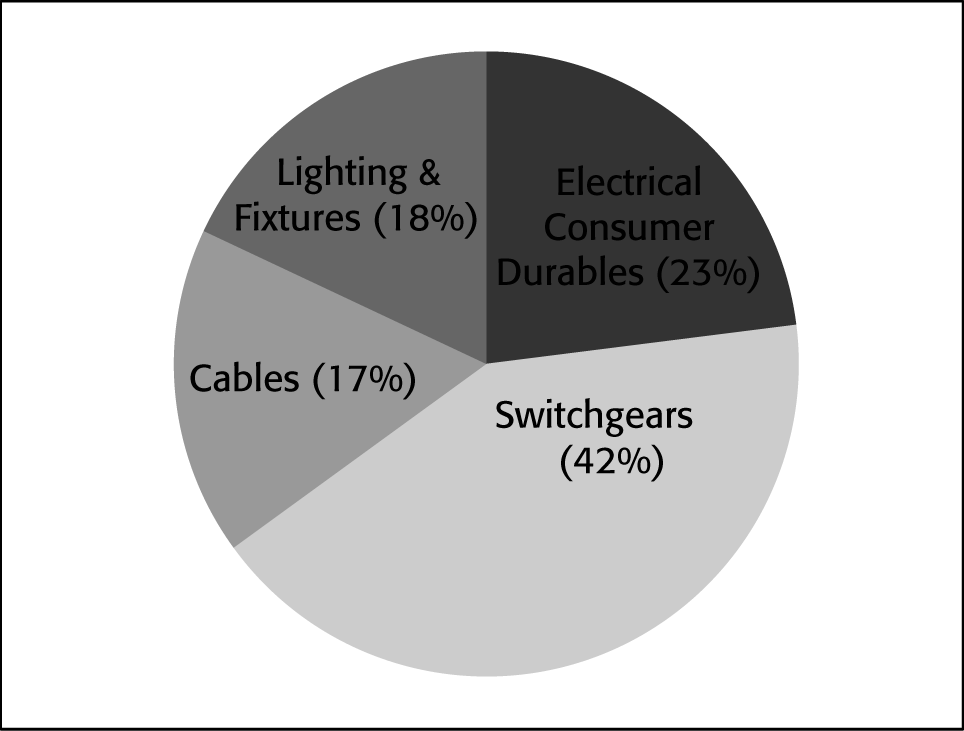

Sylvania was primarily present in the European and American markets (see Exhibit 2). In the year 2008, a year after the acquisition, the losses at Sylvania had increased and there were fears that the Sylvania acquisition could ruin the entire group’s prospects. However, Qimat Rai Gupta refused to give up. A success in this venture meant that Havells could achieve its grand global ambitions. A majority of sales for Sylvania came from Europe. Due to the global economic slowdown, the European market remained sluggish from 2008 onwards. The tough times for Sylvania lasted through the years 2009 and 2010. In the year 2011, Havells was able to turnaround the brand. The brand did better in FY 2012–2013 (see Exhibits 3(a) and Exhibit 3(b)). In Europe, the company had intensified distribution and broadened its product mix to improve the performance of Sylvania. This helped the company to increase the market share for Sylvania in the European market. Both in America and Europe, Sylvania started gaining market share over its rivals. In 2013, Havells Sylvania contributed to around 42 per cent of Havells’ global revenues and 39 per cent of its operating profits.

Transition of Havells From Industrial to Consumer Brand

From 2004 onwards, Havells started the transition from being a predominantly industrial brand to becoming a consumer brand. Havells was positioned as a premium brand that laid emphasis on innovation, product quality and service. The company was focused on being both consumer and dealer centric.

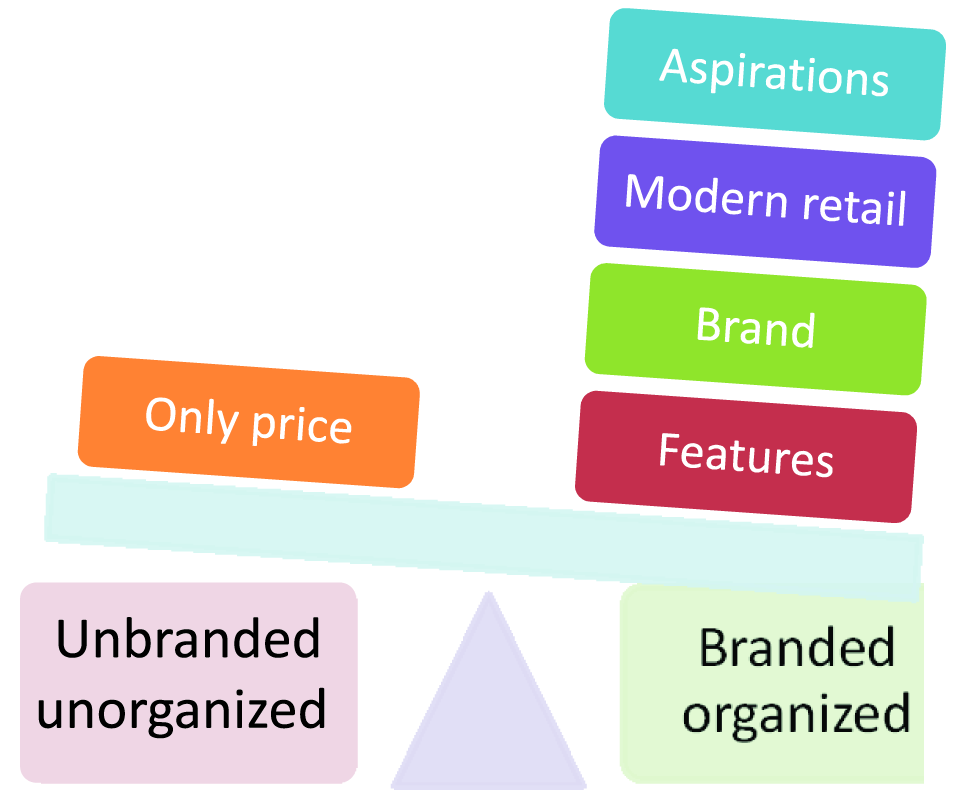

The transition of Havells into a consumer brand was aided by a paradigm shift in consumer buying behaviour in the Indian market (see Exhibit 4). Consumer purchases were increasingly being driven by aspiration. Consumers preferred branded products over unbranded products. Consequently, the organized market gained more prominence as compared to the unorganized market. This resulted in vast growth opportunities for branded electrical consumer products. Anil Rai Gupta said: ‘We saw the unorganized market shrinking very, very fast. So, whatever we did in terms of promotion and distribution benefited all the organized players, which was fine.’

Developments in the macro-environment such as the growth of the housing sector 10

According to Cushman & Wakefield, there will be demand for 12 million new houses between 2013 and 2017

For detailed analysis, please refer to http://www.ficci.com/Sedocument/20218/Power-Report2013.pdf

According to the Central Electricity Authority, India faced a peak electricity shortage of 12,000 MW in 2012–2013.

Involvement levels also increased due to the increasing engagement and usage experiences of consumers. Branding along with high product quality emerged as key differentiators for the entire Havells portfolio. As the company transitioned from an industrial brand to a consumer brand, it was felt that the brand awareness and preference of Havells should be increased.

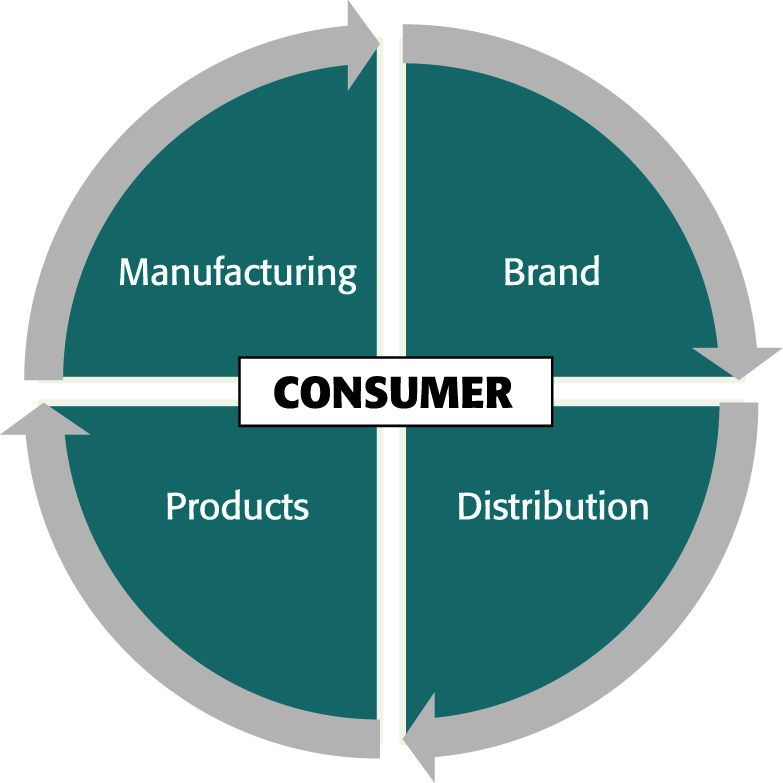

Havells focused on four key areas to transform the hitherto industrial business into a consumer brand—manufacturing, product innovation, distribution, branding and advertising (see Exhibit 5). Sustained investments in these key areas helped build brand equity for Havells.

Manufacturing and Innovation

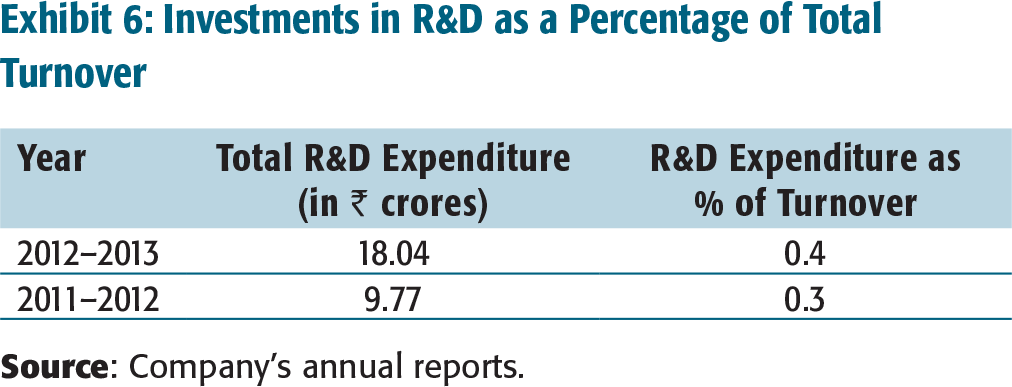

Havells India limited (HIL) was listed on the Indian stock exchange in the year 1993. Thereafter, the company faced a lot of competition from low-cost Chinese manufacturers. The company sourced technology from small and medium firms from Germany. Many of these firms also closed down due to the Chinese onslaught. Therefore, Havells started developing in-house technology and opened four R&D centres between 1993 and 1998. After the liberalization, competition for Havells came from both multinationals and Chinese companies. That is when Havells started investing heavily in R&D and manufacturing. It had a strong manufacturing base, backed by sustained investments in R&D 13

Havells had 11 state-of-the-art manufacturing units in India located at Haridwar, Baddi, Noida, Faridabad, Alwar and Neemrana, and 6 state-of-the-art manufacturing plants located across Europe, Latin America and Africa—for details refer to: http://www.havells.com/havells-network.aspx

Investments in R&D as a Percentage of Total Turnover

The innovation centre of the (Qimat Rai Gupta) QRG Group was located in Noida, India. The centre provided theoretical and experimental foundations for all aspects of electrical engineering. The primary desired outcome of the innovation process was to make better products for customers that were safer. Quality was the hallmark of the QRG group.

Havells connected its entire operations including dealers, branches, manufacturing facilities and management information systems by investing heavily in information technology. The company’s service portal was also linked to its plants so that all complaints and resolutions were recorded formally in order to facilitate suitable changes in manufacturing (Mallya, 2013). This increased efficiency and margins for the company. It also led to increased dealer and vendor satisfaction.

The company also believed in offering its customers best services at their doorstep. Anil Rai Gupta said:

We gave service at the consumer’s doorstep. If the customer had a `700–1,000 dry iron that had developed a problem, the Havells representative would come to the house, rectify the appliance and deliver it back. That’s the amount of convenience we offered across all products. No other company offered their services at the customer’s doorstep. They told the customer to call their helpline and the actual service took a lot of time. For small ticket items, the customer was expected to go to the service centre and leave his appliance for many days. In some cases, our service cost was higher than the cost of the product itself. But we were ready to take that (kind of cost). The biggest of the multinationals gave such services only for high-cost items, for example, a geyser, which cost `8,000–10,000, and not on a ` 500 iron or a ` 1,200 CFL or a ` 50 switch.

Although all the products of Havells were built to be better, safer and smarter than the competitors’, the main aim of the company was to win customer confidence. The services offered by Havells were different for industrial markets as compared to consumer markets, as Anil Rai Gupta remarked:

On the industrial products side, the service backup was extremely critical because due to the failure of any of our product, the customer’s factory or business could stop. And that would mean a huge loss. So, we had to give confidence to our customers that with our products, there would be no downtime. Their businesses were running on our products 24 hours, and we had to be sure that if there was any problem, we replaced the product quickly or did whatever it took to make sure that there was minimum downtime. That was really important in the industrial market.

Distribution

Qimat Rai Gupta’s foundations as a trader made him understand the innate needs of the channel members of Havells. He also understood that the channel members could catapult the brand to great heights if the company considered them to be their strategic partners. Anil Rai Gupta said:

The chairman himself was a dealer and so he understood the difficulties faced by this community. Most of the dealers were not very well educated. And also, this was not a typical business, so banks did not fund them. As the dealers were typical businessmen, they did not think of saving for their future. Whatever money came in, they ploughed it back into their business. In most of the cases, it was a one-man army. So, Havells started looking at these businesses differently—if it were me instead of him, what would I have done? And that was when we did many things for them. For instance, we organized funding for them from the banks and acted as guarantors for them. We offered them health insurance worth ` 5 lakh by asking them to pay a token money of ` 1, because my father believed that nothing should be given away free. So, those guys who owned small shops earlier grew with the company and now own large, palatial houses. My father said that if they grew, we would also grow. We put a lot at stake so that our dealers stood by us in good and bad times. These things built emotional associations with them. This was a key differentiator. No other competitor had done this in the market, and these dealers never left us.

Therefore, the company valued its relationship with its dealers immensely. Its channel policy aimed at creating sustainable relationship with the channel intermediaries through consistent policies, transparency and growth initiatives.

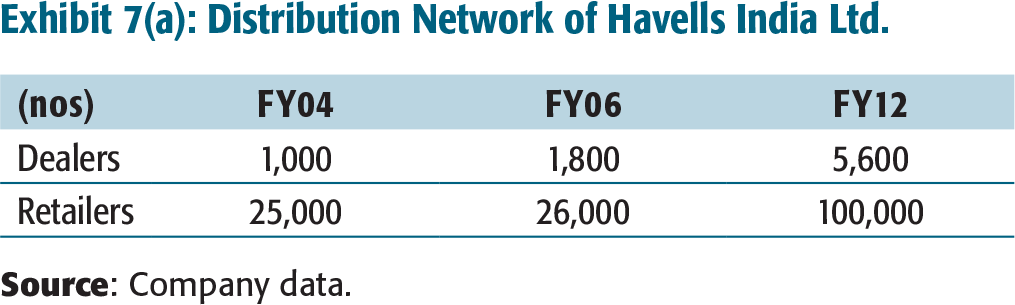

Distribution Network of Havells India Ltd.

We are not even present in 50 per cent of the country today. And our competitors’ presence is only 10 per cent. We may be covering some of these retailers in smaller towns, cities and rural areas using dealers or distributors. In fact, our brand is being demanded in a lot of areas but we are not available there. Therefore, our job is to reach out to more and more consumers by going to these geographies and creating a set-up there. That will give us a lot of advantage.

Havells had decided to concentrate on the Tier II and Tier III towns in the future. The company planned to increase its distribution presence in two stages for the cities and towns with populations of less than 1 lakh—it planned to cover all cities by the end of 2013, and by the next year, it planned to cover all such towns with populations of less than 50,000. It had specific coverage plans for different states. For instance, as Uttar Pradesh was a huge market for Havells, contributing about 12 per cent of its overall revenues, the company planned to increase its dealership network to 600 from the current number of 150.

An important part of the distribution network of Havells was its flagship Galaxy stores. Anil Rai Gupta briefed:

A Galaxy store was a one-stop shop for all Havells’ products. So, whatever we made, irrespective of whether it sold in that area or not, it was showcased in the Galaxy store. It was like an advertisement for us. It was also about how a consumer had a look and feel of the product. Today, a customer was not only me, it was the entire family. For instance, when a house was being constructed or bought, it was a family decision to go for X or Y brand of electricals. Now, women were equally important in the house and they were taking the decisions. But these women were not going to be able to go to these crowded and cluttered wholesale markets. So, we had to create an atmosphere where a family would want to take their kids as well.

All Galaxy stores were exclusive franchisees of Havells. Most of the Galaxy dealers had been with Havells for a long time. Others had previously dealt in multi-branded outlets. The look and the feel of the Galaxy stores were decided by the company. The company took decisions about products and innovations that were kept in the Galaxy stores and also trained the employees engaged in these stores. In fact, these stores provided a tremendous brand-building exercise for the company. The number of Galaxy showrooms was to be doubled from the existing 210 to 400, covering 250 towns instead of the earlier 130 towns. Galaxy stores contributed to 12 per cent of Havells’ revenues (excluding its cable business). They were critical for high quality brand visibility and direct consumer engagement.

Havells gave lucrative dealer incentives. The company had also initiated the ‘Power Plus’ programme for electricians and dealers. The company had an existing database of 10,000 dealers and 30,000 electricians under this programme. Dealers and electricians got points on each purchase of Havells’ products that could be redeemed against attractive products.

Branding and Advertising

In the consumer market, Havells used the advertising route to position its brand and create a strong brand preference. The Havells account was handled by Lowe and the media buying arm was Group M. Most of the advertisements were featured during cricket matches, as Havells found that decisions about electrical products were made by men in a household. As cricket was the favourite sport watched by many Indian men, advertisement inserts were usually given during popular cricket series. Chunks of the advertising budget were used in buying space during popular cricket tournaments such as the T20 World Cup, which garner high TRPs. 14

TRP is Television Rating Point. It measures the reach and, therefore the popularity of a programme. Higher TRPs indicate higher reach, and therefore higher popularity. Programmes with high TRPs had higher advertising rates.

Before 2005, we were dealing in products that were behind the doors. Industrial products, or for that matter even consumer products like an MCB or RCCB, or switches were not glamourized. Customers never bothered to pick up a particular brand of MCB or a switch and women were not a part of the decision-making at all. Men watched cricket, and therefore cricket was our natural choice for running our advertising campaign. It was in 2011, when we launched our home appliances that we started shifting our cricket advertising slowly to non-cricket advertising because women also became a part of target audience for these products.

Decisions about products like fans, switches, circuit breakers, etc., were not made very often. However, advertisements were frequently repeated to reinforce the brand through continuous engagement with end users. Anil Rai Gupta explained the purpose of the sustained Havells campaign:

The intent was to make customers aware that while these products (electrical products) were life-threatening products in some sense—a short circuit can be fatal—nobody knew what this product was all about. Till 2005, when we started advertising MCBs, fuses existed in the market. Consumers had to change fuses by taking them out, rewire and put them back. That is when we slowly started educating customers that these were critical products for their own safety, and when they could buy houses worth lakhs, why couldn’t they invest ` 10,000–15,000 in getting the basic MCBs? So, the intention was to educate customers that their dependence on the electrician should not be so high that they followed his advice blindly. The humour appeal in the campaigns made it easier for the customers to understand what we wanted to tell them.

The shock laga (got an electric shock) campaign signified the transition of Havells from an industrial to a consumer brand. Other campaigns included flower like idlis (for its idli maker), wires that don’t catch fire and mere fans hamesha mere saath rahenge (my fans will always remain with me—a campaign that featured the yesteryear superstar Rajesh Khanna). Recently, the company had used the theme of Respect for women for advertisements for its domestic appliance range. 15

The advertisements can be seen by using the link: http://www.havells.com/TvAds.aspx

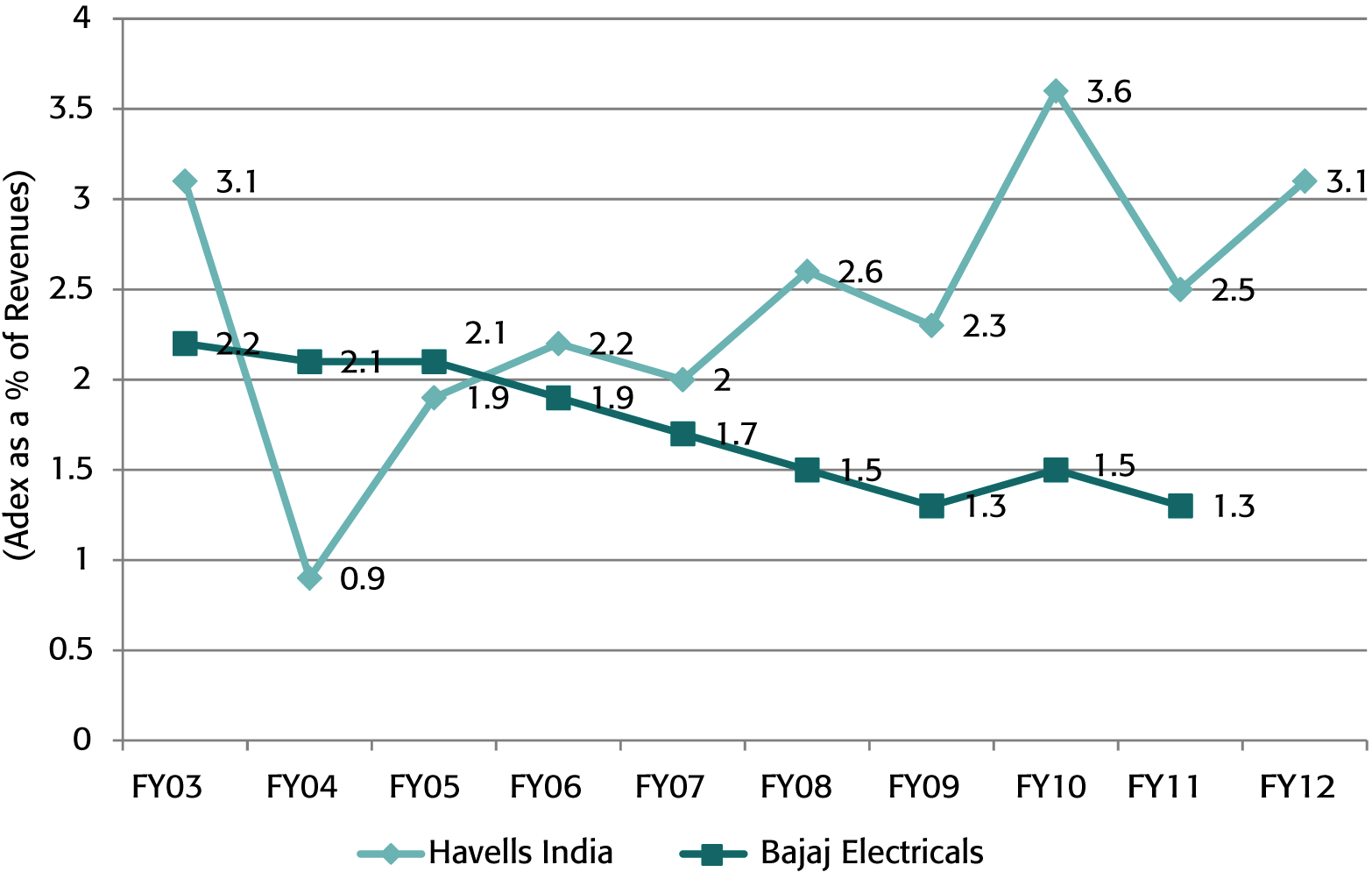

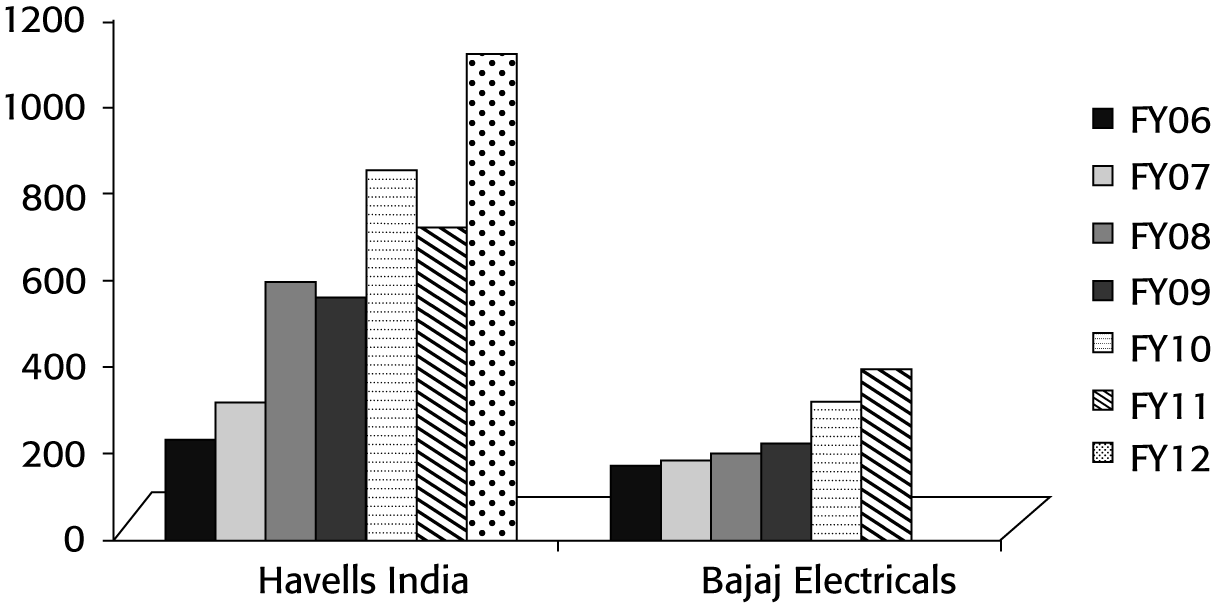

Many companies had decided to cut back on ad spend due to the onset of recession. However, Havells increased its advertising expenditure and emphasized on the consumer benefit of shock prevention. The campaign displayed high repetition of advertisements, and the decibel levels for a campaign by an electrical goods company matched that of telecom companies in the Indian market. Havells had decided to benchmark its branding activities with those of other FMCG majors, particularly in terms of the advertising spend. Havells spent much more on advertising as compared to its competitors. In many product categories where there was not much differentiation, Havells’ branding exercise helped it in achieving high growth and market share. This was a highly unconventional move, as no other player before Havells had invested in advertising aimed directly at the end consumer for FMEG products (see Exhibit 8(a) and Exhibit 8(b)).

BRAND PORTFOLIO

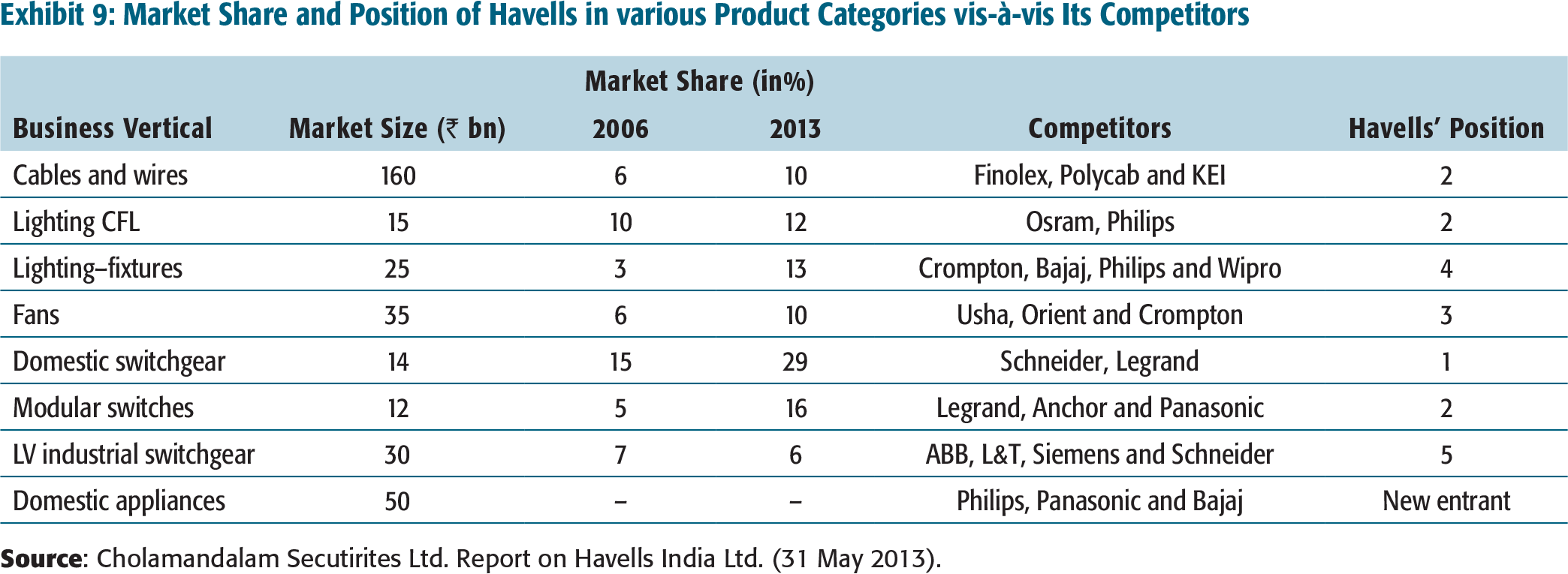

Havells was a diversified company having 17 product verticals. Each vertical had a different set of competitors (see Exhibit 9). Havells constantly identified market gaps to evaluate and expand the existing product categories. The company never hesitated to enter categories that had well-entrenched competitors, such as ECDs, water motors and hand pumps. Anil Rai Gupta noted:

The company had business heads and product heads. Similarly, at the branch level, there were branch heads, product heads and then there were teams under the product heads which were working on their own brands or products. Those people tracked competition. There were some central divisions, like marketing and communications, which catered to the entire Indian market. We chose and defined support to products and categories depending on certain factors. If, say, the festive season was coming, domestic appliances sold the most during this time, and we pushed it. And during summer, we pushed more fans. However, all products were not seasonal, for example, the MCBs. Therefore, the general ads, including the ‘shock laga’ ad, were aired continuously.

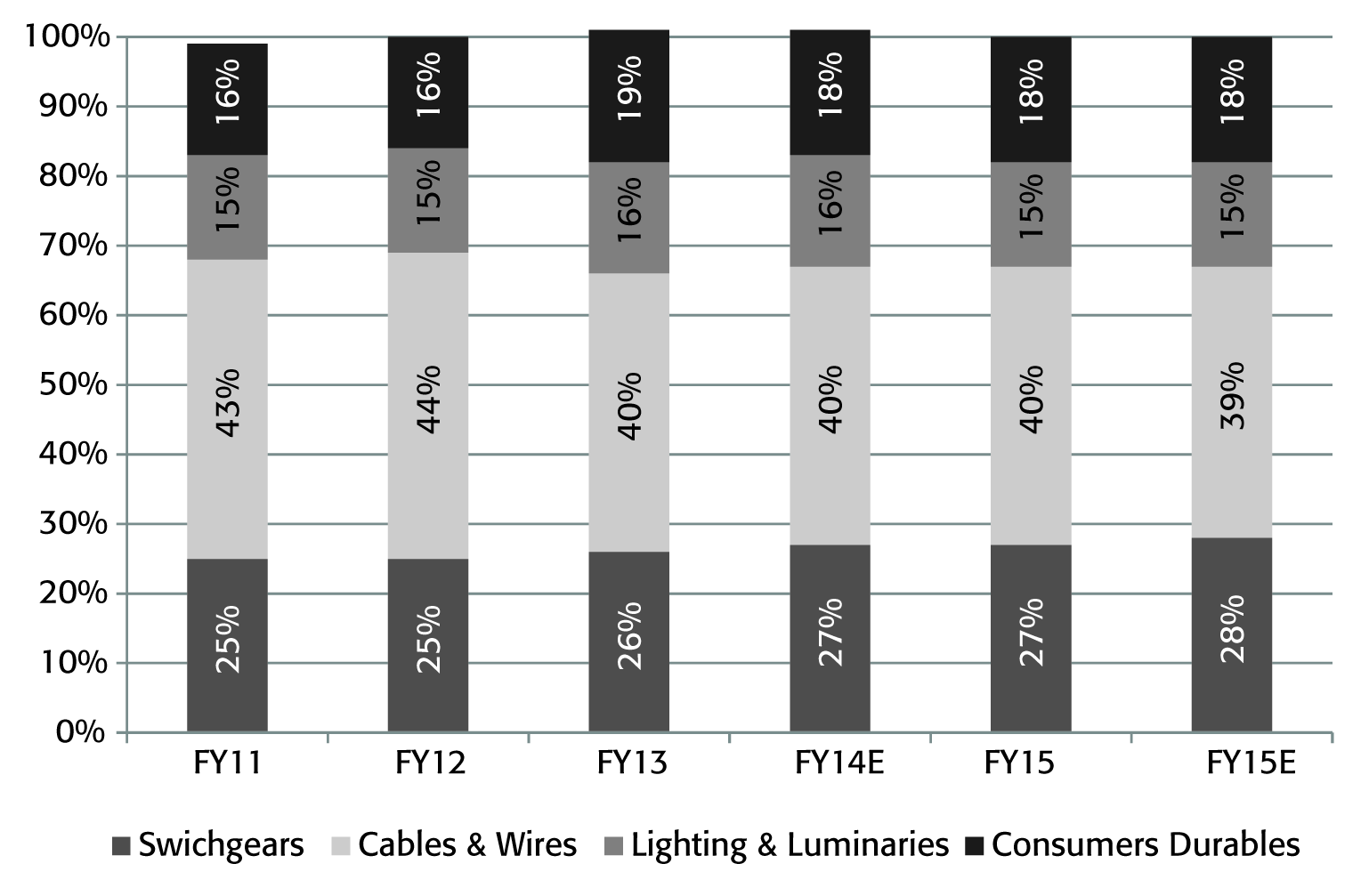

Havells operated in verticals that were commoditized by nature. Except the consumer durables business, all the other product verticals of Havells were traditionally B2B businesses. 16

B2B business: Products or services manufactured by one firm and sold to another, for example, switchgears were essentially industrial products.

Retrieved from http://www.havells.com/Admin/SiteMedia/CompanyPdfs/Sustainable-Value.pdf

Market Share and Position of Havells in various Product Categories vis-à-vis Its Competitors

Switchgears

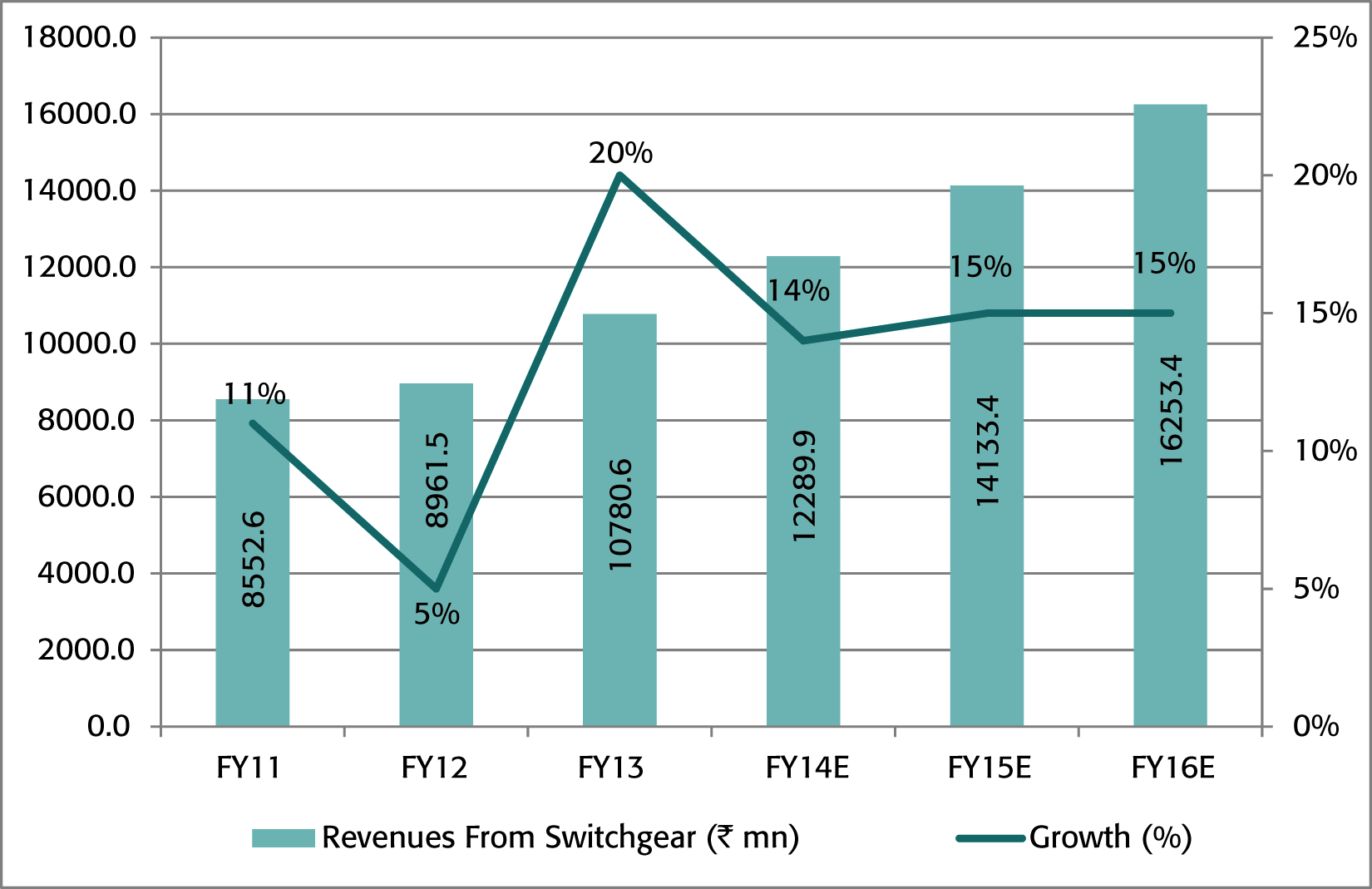

The switchgear market in India was valued at ` 135 billion in 2013 and was expected to grow at 10 per cent for the next 4–5 years (Exhibit 11). Low voltage switchgears, which accounted for more than 55 per cent of the market, had a higher share of unorganized players.

The domestic switchgear market was dominated by few organized players and hence had low competition. Havells offered a discount of 30–40 per cent to dealers as compared to 40–55 per cent by the competitors. The product range of Havells comprised MCB, RCCB, changeover switch and distribution board. The modular switches segment saw the presence of many local players along with a few dominant organized players. Havells offered discounts between 30 and 55 per cent and dealers got a margin of 5–7 per cent. The Crabtree brand of Havells was prominent in this market. Customers were switching from unorganized to organized markets at a fast pace due to higher safety and aesthetic appeal of the branded products. Havells targeted different segments with its brands Crabtree, Standard and Reo.

In the switchgear market, the main competitors of Havells were Legrand, Anchor and Schneider. Legrand was positioned as a premium brand in the switchgear market. The premium positioning of Legrand reflected the transition of the customer from being price conscious to being value conscious. The products of Legrand (MCBs and switches) were priced higher than all the other brands in the market, and the company justified it on the basis of the entire package of product, service and support. The distribution of Legrand was also more exclusive compared to Havells. Legrand appointed authorized dealers in each city who were responsible for driving sales at their own end. Anchor operated mainly in the low-voltage switchgear market and positioned its brand at the popular end of the market. It had also introduced products such as distribution boards, mini-MCBs, MCBs, RCCBs and isolators. Schneider had acquired the Luminous Power brand in 2011. The Luminous brand sold switches and switchgears, while the Schneider brand sold the higher end sockets, distribution boards and modular switches for homes and businesses. Schneider mostly concentrated on the medium-voltage switchgear market.

In the industrial switchgear segment, there were few organized players and low competition. Industrial customers had strong brand preference due to safety features and high technology. The market share of Havells had dropped in this segment, as its positioning was not strong. The product range of Havells was limited as compared to competitors, as was the brand recall. However, the margins were around 35 per cent. The main competitors were ABB, Schneider, L&T and Siemens.

Cables and Wires

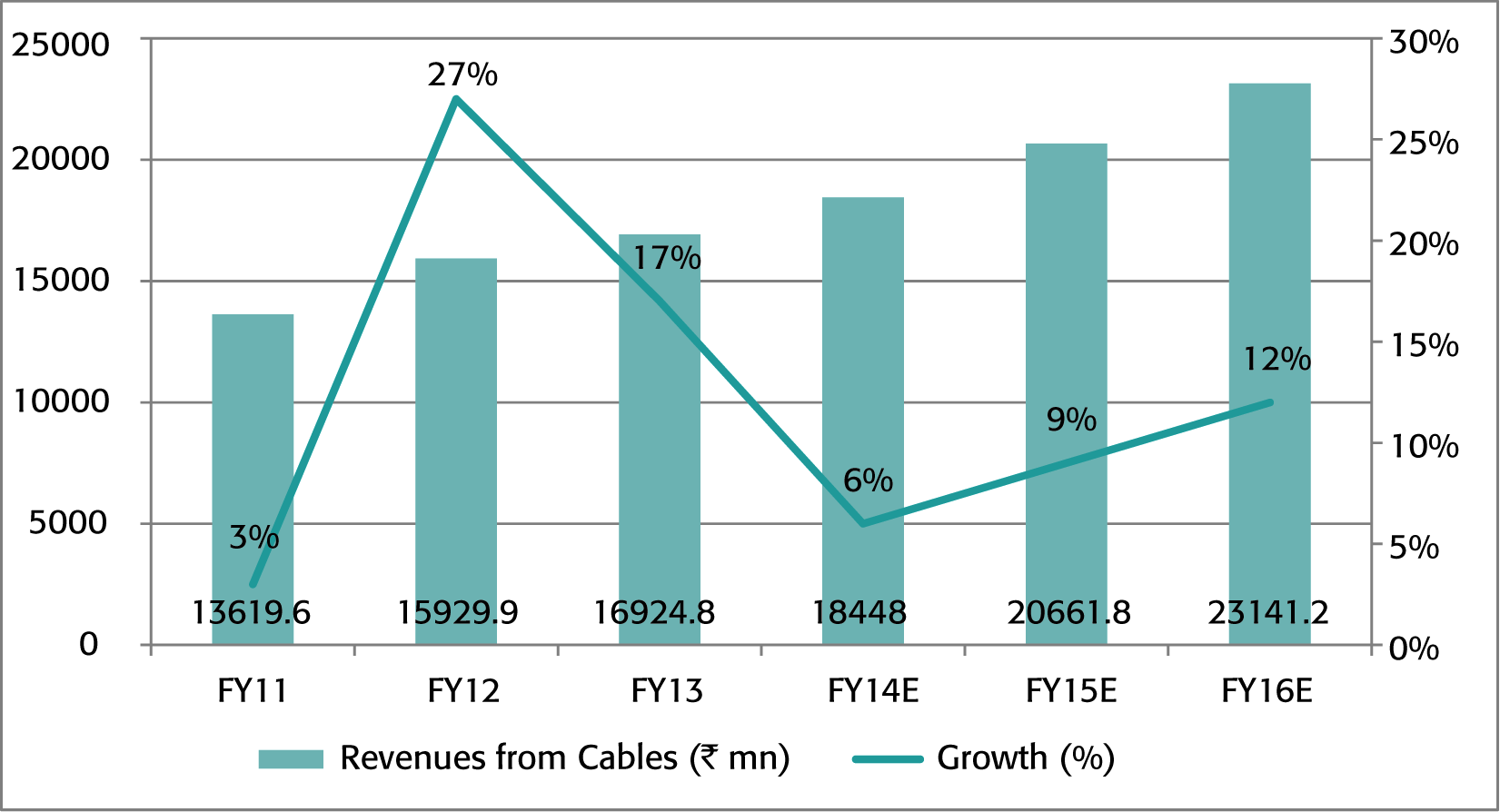

The cables and wires market comprised nearly 40 per cent of the entire electrical industry and was growing at the rate of nearly 15 per cent for the last few years due to growth in the power, infrastructure and communication industries (Exhibit 12). The market was divided into four segments—house wires, low-tension wiring, high-tension wiring and extra-high-voltage wiring. The market was highly fragmented, characterized by commoditization. Cables were volume driven and dealers were not brand conscious, whereas in the wires segment, brand consciousness existed. Cables were largely targeted at institutional buyers, while in the wires market, institutional buyers and dealers had a share of around 50 per cent each. The market was highly regional and each player had a regional stronghold that was difficult to break. Prices were very volatile in this market due to changes in the prices of copper and aluminium. The target segments included architects, contractors, engineers and builders.

In the industrial and domestic cable markets, Havells was ranked third. It was more prominent in the wires market, as customers were brand conscious. Havells charged premium price in the wires market owing to better product quality. Advertising emphasizing safety in wires was aimed at end consumers.

Its main competitors were Anchor Electricals, Finolex cables, Polycab, V-Guard and KEI. Anchor Electricals was primarily a switchgear company that diversified into other categories such as cables and wires in a bid to reduce its dependence on one vertical. The brand positioned itself on the safety plank, as its cables and wires were more than 100 per cent conductible. Finolex operated in the electrical and communications cable markets. The brand shifted from a commodity player to brand building, which enabled it to create consumer pull. Finolex was also able to exercise greater control over trade, as a stronger brand enabled it to receive advance payments from the channel intermediaries, which was difficult in the commoditized scenario (Panchal & Palande, 2014). Polycab was a competitor in the wires market and positioned its wires on the safety and savings plank. The advertising campaign for Polycab sought to increase the involvement level of customers towards wires and make them brand conscious. 18

‘Polycab rides on humor to make “safety” and “saving” promise.’Campaign India. Retrieved from http://www.campaignindia.in/Video/337819,polycab-rides-on-humour-to-make-safety-and-saving-promise.aspx

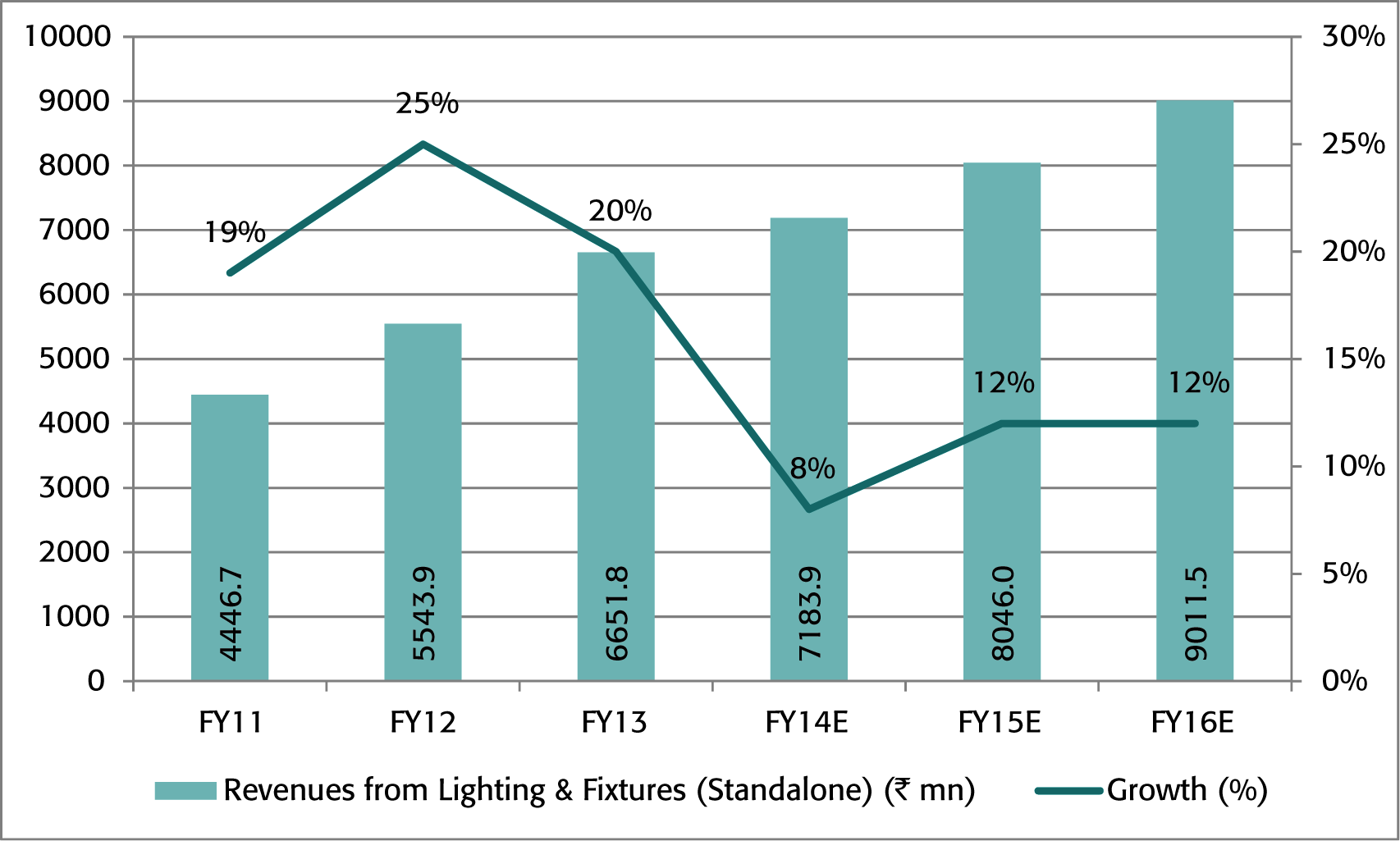

Lighting and Fixtures

The lighting market comprised commercial lighting, areas lighting, road lighting, luminance, consumer lighting and home décor. CFL and LED were new technologies in the lighting market. The lighting market was highly competitive and was slowly shifting from an unorganized to an organized market. (For growth of lighting market, see Exhibit 13.) Chinese products were a major threat for branded players. Pricing and branding were the key differentiators in this market. The market saw several innovations from lamps to tubes to CFL and more recently, the LED technology. Government initiatives led the replacement of the CFL technology with LED. Havells was strong in consumer lighting due to aggressive branding. All the organized players straddled the entire product line. Service was an extremely important choice criterion in this market, and this was the strength of the Havells brand.

In the lighting business, Havells held the second position in the CFL market. The main competitors were Philips and Osram. It held the fourth position in the luminaries 19

Luminaries comprised of area lighting, commercial lighting, road lighting and luminance.

The LED market was the future for the lighting industry in India. The public sector, street lighting, commercial and industrial segments accounted for nearly 95 per cent of the LED market. The street lighting accounted for about 65 per cent of the LED market. Philips held the highest market share followed by Osram.

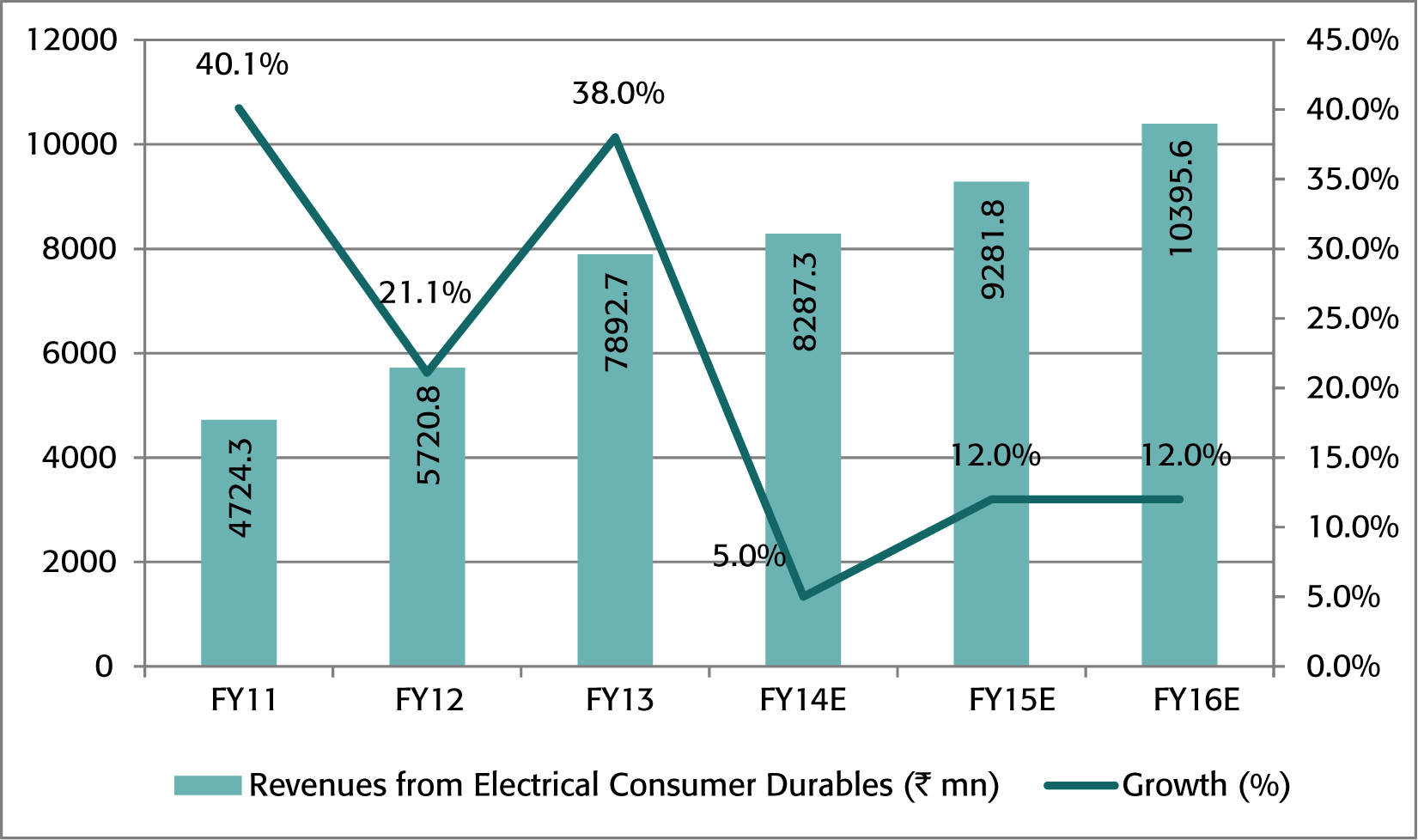

Electrical Consumer Durables

Havells’ foray into the ECDs market signified its transition into a consumer brand. A volatile industrial market prompted this move. Various products in the Havells portfolio in the ECD business included fans, motors, home pumps and domestic appliances dealing in garment care, such as electric iron; brewing, such as espresso coffee machine; cooking, such as toasters and ovens; food preparation, such as hand blenders, juicers and mixers and home comfort, such as water heaters (For revenue and growth of ECD, see Exhibit 14).

In the ECDs market, Havells was ranked third in the market for fans. Its main competitors were Crompton Greaves, Usha, Bajaj Electricals and Orient. The fan market in India was equally divided between the organized and unorganized market, although consumer preference for branded fans had gravitated the market towards the former. There was a high demand for non-decorative fans, although decorative fans were growing in popularity. Havells was the first company to launch decorative fans in 2003. Customers preferred warranties in the fan market. The product range of Havells included ceiling fans, table fans, high speed fans and air circulators, besides decorative fans. Havells adopted a twin-brand strategy for its fan market under the brand names Havells and Standard. Both brands were positioned as premium brands, although the Havells brand catered to the mid-market segment as well (The Hindu, 12 February 2014).

There was an intense competition among Orient, Havells and Crompton Greaves in the premium ceiling fans segment. Usha also planned to introduce several new models in the same segment. In the industrial fans market, competition existed among Havells, Bajaj and Crompton Greaves. In the table fans segment, Havells’ main rival was Orient. Bajaj and Havells intensified their distribution network. Bajaj also increased loyalty programmes for its retailers, for instance, by giving them more margins and increasing their credit periods. Orient increased its investment in promotional activities. All the companies focused more on the Tier III cities and the rural markets to enhance their market shares (Bhattacharjee, 2013). 20

http://www.keynoteindia.net/document-hosting/research/044_HavellsIndia_InitiatingCoverage.pdf

http://www.livemint.com/Companies/TUiQ4R7WC6PScb45Pya46K/Bajaj-Electricals-decides-to-focus-on-export-rural-markets.html

http://www.thehindubusinessline.com/portfolio/firm-calls/havells-india-invest/article6492010.ece

The domestic appliance market was highly competitive and was shifting from an unorganized to an organized market at a fast pace. There were a huge variety of products and brands that customers could choose from. There were different customer segments that were sensitive to price or quality. Dealer margins were usually low (between 2 and 5%). Havells leveraged its premium image and intensive distribution network. Customer preferred brands that had a large portfolio and offered prompt services.

Havells was a relatively new entrant in the domestic appliances business. It invested in product innovations. The existing brand network strengths were leveraged for the success of the new launches.

The leading players in this category were Philips, TTK Prestige and Bajaj. Philips positioned itself as an innovation-led company that introduced new products in the Indian market every year. The company felt that customers were willing to pay more for smart features and innovations (Taurani, 2014). TTK Prestige positioned itself as the total kitchen solutions provider, offering safety, durability and convenience to the customer (The Hindu, 29 September 2012). The brand had high recall value and had built an intensive distribution network over time. It had expanded its product portfolio from being a single-product company to a diversified one. Bajaj established itself as one of the leading players in the domestic appliance market through constant innovations in products and processes. It set up exclusive retail outlets called ‘Bajaj World’ across India to enable the brand to have higher visibility. Bajaj offered strong after sales service to its customers. The company launched its premium range of products under the brand name Bajaj Platini and also distributed and serviced the Morphy Richards brand in the Indian market. The company believed that the potent combination of innovation, manufacturing, distribution and advertising gave it an edge in the intensely competitive electrical appliances market. 23

Leveraging the legacy of ‘Bajaj’ to inspire trust. Retrieved from http://www.campaignindia.in/Article/354854,leveraging-the-legacy-of-8216bajaj8217-to-inspire-trust.aspx

Havells launched monoblock pumps targeted at home and commercial establishments in the second half of 2013, and planned to expand its water pumps portfolio.

COMPETITION

Competition came from different companies in various verticals that Havells operated in (Appendix 2). For instance, in cables, its competitor was Finolex; in fans, its main competitors were Crompton Greaves, Orient and Khaitan; in home electricals, the main competitor was Bajaj; and in lighting, competition was from Philips, Osram and Wipro. Havells competed simultaneously with industrial equipment majors such as L&T and ABB, and Bajaj and Philips due to its diverse portfolio. Although Havells positioned itself as a premium brand in all the product verticals it operated in, this did not come at the cost of growth.

Havells succeeded in these diverse product lines, as it was able to spot gaps in each and exploited them. For instance, although Finolex was a strong player in the cables and wires business, it never really built a strong brand, and thus customer perceptions of commoditization of the category remained. Brands like Orient and Khaitan also became complacent with their existing market shares in the fan market, allowing Havells to enter this category aggressively. Crompton and Bajaj diversified into engineering projects expecting higher returns, as India was witnessing an infrastructure boom. However, infrastructure projects were capital intensive, there were many delays in execution and cost escalations were a regular feature. Under these conditions, the company’s returns on capital employed were usually lesser than anticipated. Therefore, Havells consciously decided to stay away from the infrastructure sector. Philips and Osram were multinationals that could not be nimble-footed due to control from their headquarters, while for Wipro, lighting was a marginal business. Therefore, despite the presence of many strong brands, Havells could still establish itself as a strong player across diverse verticals.

Schneider Electric was another competitor that entered the retail market from serving only industrial markets, much like Havells. Earlier, the company had a network of large wholesale dealers who sold to contractors and dealers. It acquired Luminous in a bid to enter the retail market. This gave them access to over 25,000 retail outlets and a large product portfolio including inverters, fans and batteries. The company also competed in the switch and switchgear market. And like Havells, the company opened flagship stores called ‘Schneider Electric’ where it placed its premium offerings that were sold to retail customers and small- and medium-sized enterprises. And Luminous stores sold its popular products in verticals such as fans, batteries, switches, invertors and MCBs. Schneider was second in the switchgear market and was Havells’ closest competitor along with Legrand. The company operated in different channels and used different brand names for the popular and premium markets.

LAUNCH OF REO AND INITIAL FEEDBACK

Havells launched new products for the C-class towns to penetrate deeper into the Indian market. In the last quarter of 2012, the company launched Reo, its first range of low-priced electric switches targeted at C-class towns 24

Cities and towns in India were classified on the basis of the Census of India 2001 into categories A, B and C. This classification is used for calculating various permissible allowances for employees in the Government of India.

Anchor Panasonic was the leader. We moved into this space to achieve some market share. The problem was that our brand name had reached deep, although our products had not. Consumers in these markets did not switch to a modular switch easily. They could buy a better switch, but for that they had to replace the entire switch board. So, they could shift to a better product, and we gave them Reo. From a retailer’s perspective also, this was better, as he could stock 20 switches in his outlet. Havells could not penetrate these markets using mixies or geysers because retailers refused to keep stock of these products as they were slow moving. So, penetration was easier using CFLs or switches, and once they knew that Havells’ products were in demand, they were more amenable to stocking geysers or mixies. The sale of low-priced products gave them confidence about Havells.

The brand was initially launched in three states of India—Uttar Pradesh, West Bengal and Bihar—and was later rolled out in 12 other states. The company planned to make Reo a national brand by the end of 2013. This was the first low-priced brand launched by Havells. The company traditionally sold premium products for the brand conscious consumers in urban markets. According to Anil Rai Gupta:

Even Reo was premium as compared to other competitors. The material and safety features in Reo were the same as in the premium switches. So, for the popular category, this was like a modular switch. Apart from the fact that it did not have an outer blade and that its screws were visible, everything else about Reo was almost the same as a premium switch from Havells.

The company’s plan with Reo was to enter a market that had long-term potential demand. This was synchronous with its strategy of creating new categories in the domestic market that could be scaled up to ` 500 crore businesses in the next three years. The diversification into various segments was important to insulate the overall business from the business cycles and achieve consistent growth.

Reo was also important for Havells to test grounds in the hitherto unexplored small towns and rural markets of India. If Reo did well, other products of Havells could also be launched in these markets. Reo used the dealer route to reach the rural hinterland. The initial response for the Reo brand was very good. The company gathered that even though the Havells brand sold for a premium, it still was demanded in the C class towns and rural markets primarily due to higher quality. The company expected the rural market to register high growth in the coming years.

However, over a period of time, the company was finding it difficult to scale up Reo because of its refusal to charge lower margins. Charging high margins made it difficult for Havells to push Reo among retailers. Competitors like Anchor were providing longer credit periods because of which retailers were willing to stock up higher inventory of Anchor switches. Anchor switches were also priced lower and the company had a wider product range as compared to Havells. Anchor had 40 per cent market share in the low-cost switches and was the market leader. Havells decided to continue with its existing strategy due to the potential opportunity in the Tier II and Tier III cities. It also had to intensify its reach in Tier II and Tier III towns, particularly in west and south India, to increase its market share in these cities. There were conflicting opinions among analysts about whether Havells’ strategy of selling low-cost switches was synchronous with its positioning (Business Standard, 29 September 2013). Havells was sure that it would never lower prices to match competition, thus retaining their premium image even in the low-cost switch market. The company was sure that customers would realize the superior value of its products, and upgrade even in these markets.

THE FUTURE

Havells decided to focus more on its consumer business for sustained growth and future leadership in the Indian market. It planned to gravitate further towards the consumer branded market.

The key drivers for higher growth were to be brand promotion, distribution penetration, innovation, manufacturing, services and product expansion. Havells predicted that the domestic market would continue to grow at 15–20 per cent and register profits of 12–13 per cent for the next two years for the company. The company also planned the introduction of new products for the Indian market, particularly in the switches and sockets segment.

As Anil Rai Gupta reflected on the long, fulfilling journey of his father, he was extremely satisfied by the transformation of the business into a consumer-faced organization that was less volatile. In the long run, this was a good move. Competition was a concern, as was the economic downturn. Other thoughts were related to the growth and diversification of the business.