Abstract

Coal is a critical input for power, fertilizer, iron and steel (I&S) and the cement sector. At times up to 75 per cent of the power generated in India is coal fired. 1

CEA (Central Electricity Authority), Department of Power, Government of India. Retrieved on 22 January 2015 from

Indian Scenario

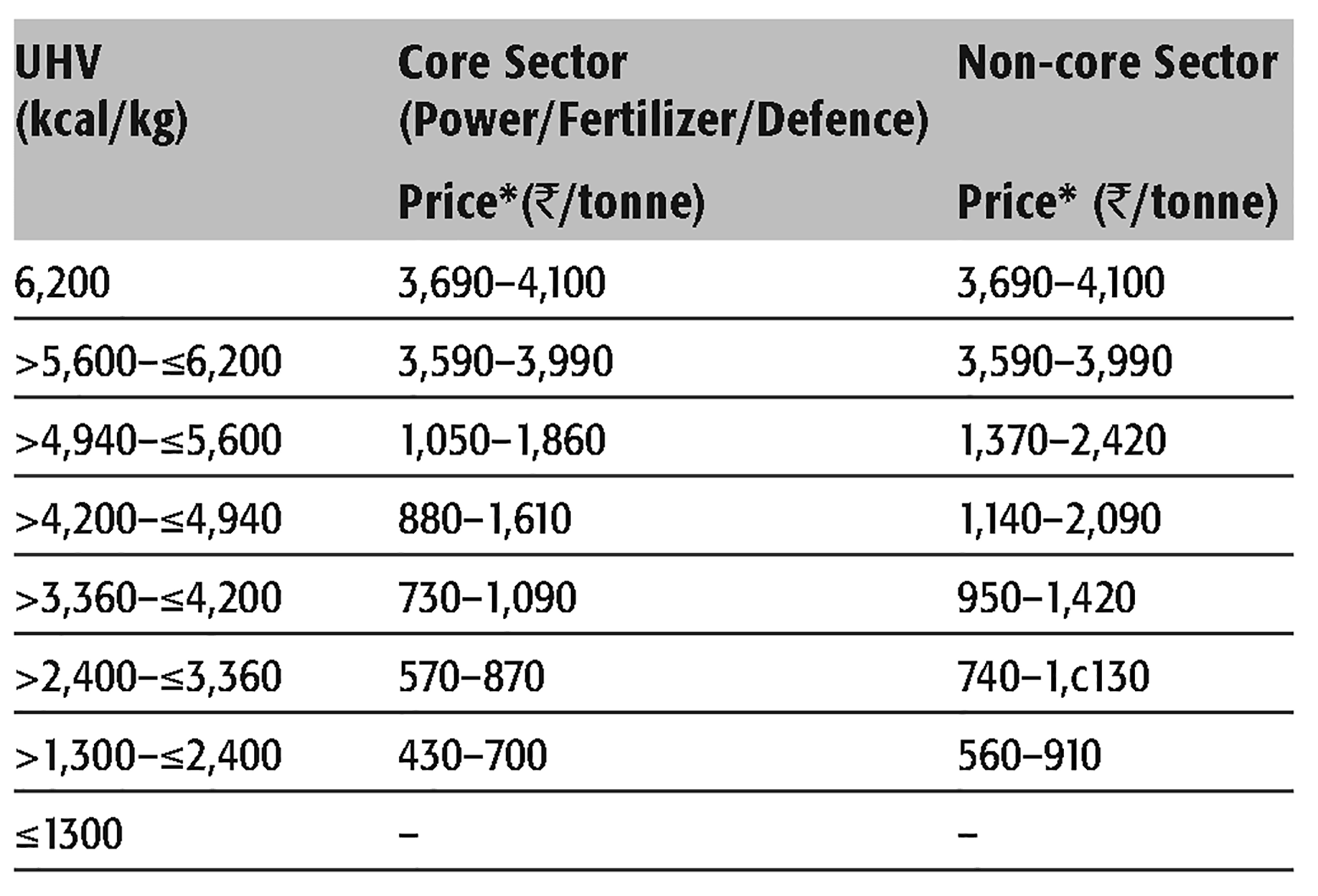

In India, coal is sold on the basis of grades, first conceived in the wake of World War I in 1917. Since nationalization, coal gradation and coal pricing have been controlled by the Union Ministry of Coal (MOC) and/or Coal India Ltd (CIL). Till 31 December 2011, non-coking coal grades used to be dependent on Useful Heat Value (UHV) expressed in kcal/kg as shown in Table 1. UHV took into account the heat trapped in ash (A) produced by burning the coal and the heat lost in removing the moisture (M) while burning the coal. Equal importance was assigned to the heat loss arising out of ash and moisture contents.

For coal with high moisture content:

For coal with low moisture and low volatile matter (VM) content:

The value of 8,900 kcal/kg adopted as the upper limit in Equations 1 and 2, represented the maximum heat value of Indian coal determined on pure coal basis.

UHV–Grade Based Non-coking Coal Pricing (2009)

*The ranges cover the prices for different subsidiaries of CIL

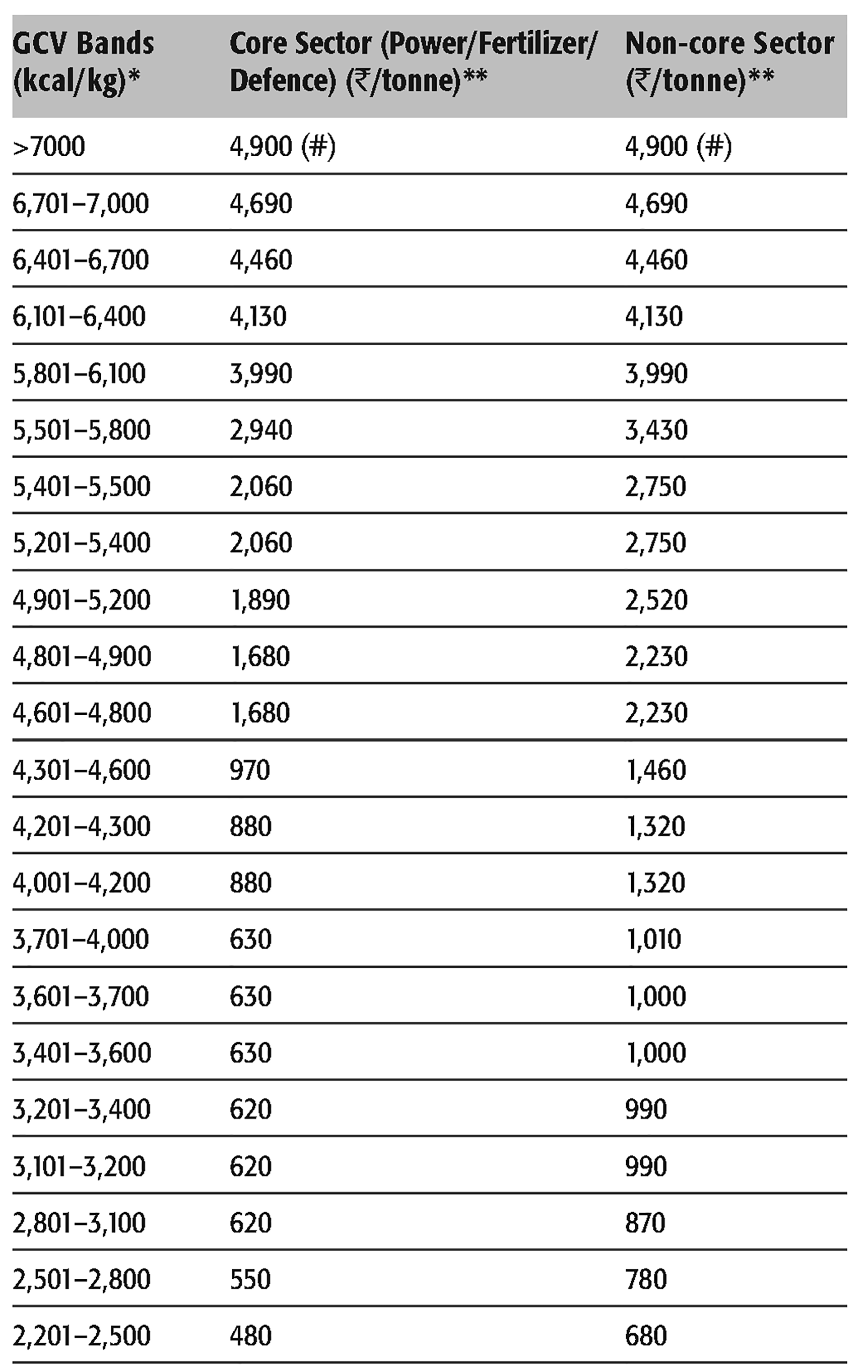

For over a decade and a half, UHV linked grade-based wide band pricing system was considered outdated. It was also felt that principally this system contributed to domestic coal being priced at 50–65 per cent cheaper than the international price till 1 January 2012. Since then, a new grade-based pricing system has been put into effect. The new grades are dependent on heat value of coal, commonly represented by Gross Calorific Value (GCV), measured and expressed in kcal/kg. Grades are uniformly spaced at an interval of 300 kcal/kg as given in Table 2. The new pricing was aimed at making the pricing system more scientific and rational while encouraging quality assurance. Possibly, all these three attributes brought the Indian coal prices on par with international coal prices. Under the new system, any coal with a GCV of less than 2,201 kcal/kg is considered as ungraded coal and cannot be sold per se. The evolution of coal pricing system in India has recently been discussed elsewhere (Bhattacharya & Tiwari, 2014). Non-coking coal known in international nomenclature as thermal coal because of its intrinsic heat value is, however, priced in a rather elaborate manner in all major coal producing countries. The same has been briefly discussed hereafter.

Run of Mine GCV-based Non-coking Coal Price

*At 5% moisture level

**Indicates mine–head prices, excluding various duties and other charges

(#) Through a subsequent notification price for the GCV exceeding 7,000 kcal/kg, has been notified to increase by ₹150/– per tonne over and above the price applicable for GCV band exceeding 6,700 but not exceeding 7,000 kcal/kg, for increase in GCV by every 100 kcal/kg or part thereof. Prices of all other grades were downwardly revised.

International Thermal Coal Pricing System

Thermal coal pricing is considered to be relatively straightforward because coal used specifically for combustion derives its value from its net heat content, with some allowance made for pollutant content, for example, sulphur, nitrogen, etc., and detrimental ash effects, for example, sodium, sulphur, ash fusion, etc. Apart from such allowances which are country-spe cific, coal cost on as delivered basis irrespective of the countries usually includes the following:

Pithead costs: labour cost, production cost, royalty and capital cost Transportation costs: railing, sea freight, road transportation, etc. Port costs (whenever involved) Retail profit margins Taxes and levies.

Country-specific allowances depend on the characteristics of the coal, indigenous or imported, consumed in the respective countries. By virtue of the specifics of the coal formation process, the US, Canadian and European coal, for example, is high in sulphur, but relatively low in nitrogen. In case of India, it is just the other way. Coal in India is of very high ash content and has difficult cleaning characteristics (for ash reduction purpose). The US, Canadian and European coal has relatively low ash content. The US and European coal is easy to clean, though most of the Canadian coal is not. Virtually, therefore, every country has its own unique pricing structure. It has at least two cost components: coal quality parameters and market parameters which depend to a great extent upon the origin of the coal and environmental legislation and supply–demand laws, respectively. The coal pricing mechanism of three countries, Poland, Indonesia and Japan has been discussed hereafter in detail.

Poland

In India, coal prices were de-regulated by the Ministry of Coal (MOC), Government of India (GOI) through the years 1996–2000. It would therefore be interesting to examine Poland's coal pricing mechanism as the country transitioned, about two and a half decades ago, from a centrally controlled state-regulated planned economy to a free market one. The energy policy of Poland is similar to those of other countries (Ney et al., 2004):

To provide energy security to the country To protect the environment from the harmful effects of power generation To provide electricity to the end-users at the minimum possible price.

Among the European countries, Poland is a major coal producer and consumer. Approximately, 97 per cent of the power produced in Poland is coal-fired. That required a coal production of 41 Mt in the year 1993 (Ney et al., 2004). In subsequent years, the production declined. In the same year, about 71 per cent of the power generated in India was contributed by coal-fired plants, the highest share in the last five decades. The corresponding coal requirement was about four times the figure for Poland (MOC, 1994; MOP, 1994).

The coal price reforms in Poland originated essentially from the country's commitment to all major environmental treaties beginning with the Geneva Convention on Trans-boundary Air Pollution (1979) and including UNFCC (Rio de Janeiro, 1992) and the Kyoto Protocol (1997). All these documents were signed by Poland and later ratified. The first step towards price reform was the gazette notification of the Ministry of Environment, Government of Poland in the year 1990, setting for the first time emission limits for all energy producers (Ney et al., 2004).

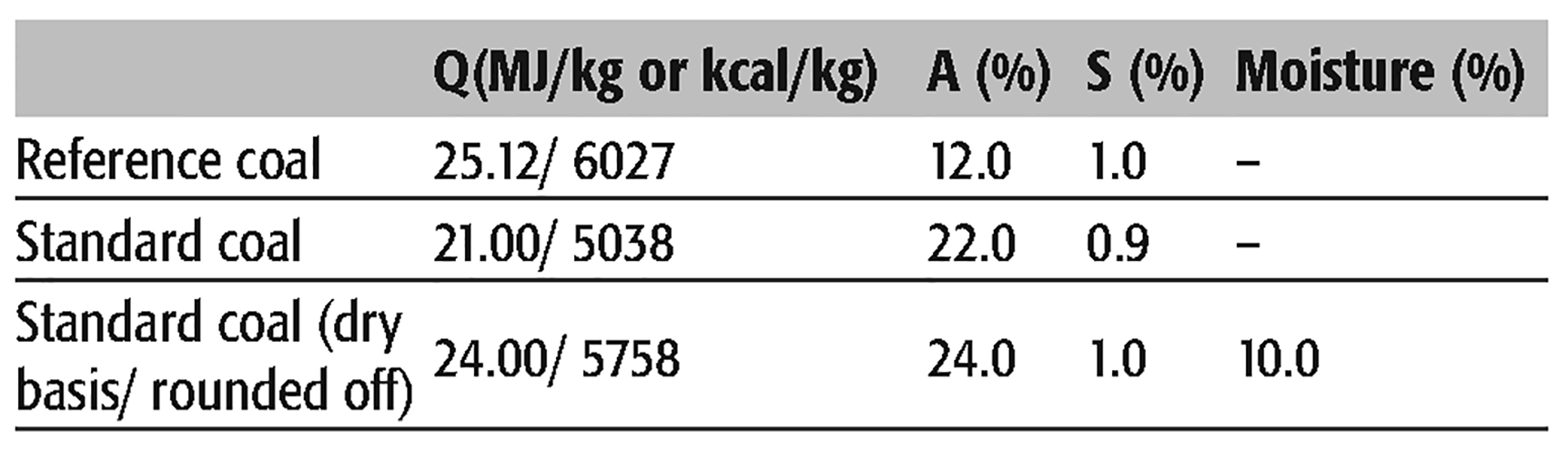

Polish coal pricing structure (Gawlik et al., 2006) links price with coal quality using a pricing formula developed by the Polish Academy of Sciences, put into force by the Ministry of Finance. The price of steam coal consumed primarily by the utilities is essentially a function of four quality parameters: heat value (utility), ash + sulphur (nuisance) and moisture (heat/ freight loss) (Equation 3).

Quality Parameters of Steam Coal in Poland

The formula was derived from the observed dependencies between quality and price as existed in the international coal trade in the 1980s and from similar relationships. Changes of the coal quality are measured in relation to that of the ‘reference’ coal (Table 3). Standard practice in international trading of coal is to limit the sulphur content to 1 per cent or less. Similarly, moisture content of 10 per cent or less has no effect on price; its increase by 1 per cent results in corresponding reduction in coal price by 1 per cent; 10 per cent is the typical moisture content of internationally traded coal.

Three ash content ranges were applied: I–from 0 to 12 per cent A(Wa = 1); II–from 12.1 to 21 per cent A and III– > 21 per cent. For the third range, Wa = 0.8 and that means the coal prices were 20 per cent lower for coals with high ash content. These ranges were introduced to promote coal cleaning. For coal of intermediate range, 1 per cent decrease in ash content resulted in 2 per cent improvement in price. The increase in price was designed to compensate for the loss of combustibles to rejects during coal cleaning and the cost of cleaning. Coefficients characterizing the standard coal embedded in the price equations might change; in fact, they do change depending upon the quantitative and qualitative inventory of coal. Coefficients characterizing the market element might also change.

Moisture content in delivered coal had always been a bone of contention in the producer–supplier–transporter–user chain. For a consignment of 100 tonnes, 1 per cent additional moisture means you pay for 100 tonnes but receive 99 tonnes. In India, moisture content is invariably a matter of dispute between CIL and the power plants. The same was the case in Poland at the time of the coal price reform. Maximum resistance to the introduction of Equation 3) was on account of moisture content, which usually was at the level of 12–15 per cent. Within a couple of years of introduction of the new pricing system, it was observed that even after wet cleaning (to reduce ash and sulphur), the coal producers could stick to the 10 per cent moisture level stipulated for standard coal (Table 3). It appears to have been achieved by technological upgradation and by introducing competition. Subsequently, moisture component in Equation 3) (indicated in bold) was removed and for standard coal moisture content was reduced from 10 per cent to 8 per cent (Gawlik et al., 2006).

Indonesia

Indonesia, a major exporter of coal to India, has introduced a benchmark pricing mechanism for its coal including steam coal since February 2010 for the domestic supplies as well the export market. The pricing is transparent and is done using four internationally acceptable coal indices to generate monthly Indonesian coal reference prices for about 62 types of coal, including 8 types of benchmark qualities. Different methods are used to determine the benchmark prices. The Directorate General of Minerals and Coal (DGMC) determines separate benchmark prices for thermal, metallurgical and low-rank and therefore inferior grade coal on monthly basis (Khambat, 2011). The benchmark price for thermal coal is determined using a formula that refers to the average coal prices based on local and international market indices. As a system, the government will determine the Coal Price Reference (Harga Batubara Acuan or HBA) by averaging the calorific (heat) value of coal in four coal price indices, namely:

Newcastle Coal Index (NEX) Global Coal Index (GC) Platts Indonesia Coal Index (ICI).

The first two indices represent international prices, while the last two indices represent local coal prices. The prices are calculated on US$ per tonne basis. Each coal category has a weight of 25 per cent (Equation 4). The coal category is divided based on coal quality, which is set at 6,322 kcal/kg on as received basis (ARB), moisture content at 8 per cent (ARB), sulphur content at 0.8 per cent (ARB), and ash content at 15 per cent (ARB).

After determining the HBA, the benchmark coal price (HPB) is calculated by a well-defined pricing formula. Thus calculated price imposes penalty for high sulphur (emission), moisture (heat/freight loss) and ash to account for the particulate emissions and for disposal cum storage of ash. There are eight benchmark prices category, representing the quality of the coal, ranging from 4,200 to 7,000 kcal/kg on gross as received basis (GAR). For coal other than the eight classes of HPB, prices are determined by interpolation approaches (Maydin et al., 2012). To avoid any dispute, conversion of coal calorific value from GAR to ADB (as dried basis) is done by using the following equation:

KGAR = Coal calorific value in GAR condition (gross as received)

KADB = Coal calorific value in ADB condition

TM = Total moisture

M = Moisture

Japan

Japan is heavily dependent on coal import and relies almost entirely on imported fuels and domestically produced nuclear power. Post Fukushima, imported coal dependence is increasing on year to year basis. About 14 per cent of the total thermal coal import in the year 2011 was made by Japan. Till about the middle of 1980s, price models based on empirical relationship (Equations 6–7) were used. With updating of the data base, the constants embedded in the relationship kept on changing on year to year basis. The models, for the fiscal year 1982, represent the import coal prices in Japan for thermal coal and anthracite, respectively (Equations 6–7).

where, FOBT usually means free on board, trimmed indicating the loaded weight ready to sail; HGI is a measure of softness of coal (softer coal, lesser generation cost); SZ is size; T is term of contract; S is sulphur content; kcal is heat content; and PR is cost of production dummy based on the size of mine (Osborne, 1988).

Since the second half of the 1980s, coal prices to the power utilities were decided by negotiations carried out between a ‘prime negotiator’ representing the buyer and the seller, and different Australian companies. The prime negotiator from each side was usually the biggest buyer and supplier (Sugiyama, 2000). For example, Chubu Electric had been the negotiator on behalf of the Japanese Power Utilities, and Drayton, Ulan and MIM as the biggest suppliers to Chubu were the lead negotiators from the Australian side. The prices decided at these negotiations had then flowed on to other Australian suppliers. This system was referred to as the ‘Benchmark Pricing system’ and it had contributed to the stabilization of coal trade for both producing and consuming countries.

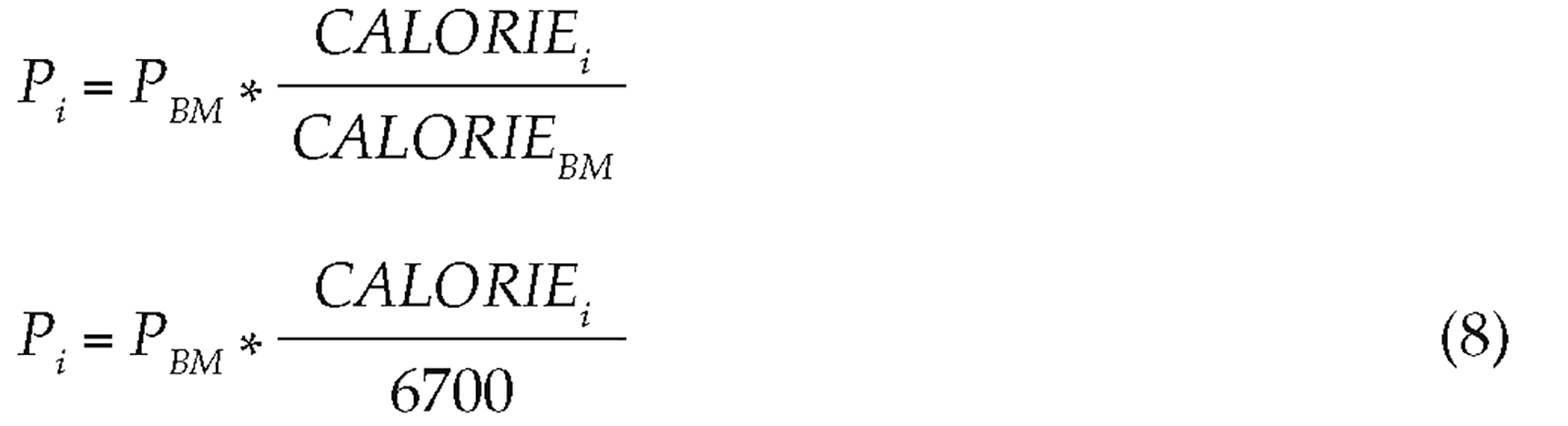

Various study groups had conducted a number of investigations with the objective to derive quality-based pricing formula, based on Australia's coal export database. As part of the exercise, quantification was made of the extent to which coal quality characteristics influence coal import prices in Japan. In general, the approach adopted was to adjust the coal prices (P) relative to the benchmark price (PBM) in proportion to the extent to which its calorific value (CALORIE) exceeded (Equation 8) the benchmark calorific value of 6,700 kcal/kg on gross air dried basis (Lindsay, Sally & Simon, 1997), provided the other quality parameters were within the limit stipulated by environmental and other (if any) agencies.

where, ‘i’ is for thermal coal shipments to Japan's electricity sector only. Equation 8) is transformed to Equation 9) by taking natural logarithms (ln) of both sides. That formed the basis for the empirical price equation for coal exports to Japan's power sector. Buying and selling were usually through long-term contracts.

The coefficient for ln CALORIEi is unity, implying that 1 per cent increase in calorific value results in a corresponding 1 per cent increase in the actual price of coal. Separate equations were formulated for thermal coal imports for other users, for example, heating, paper,

DRI, etc., based on the following general relationship.

Since the fiscal 1998, utilities had negotiated individually based on reference prices instead of benchmark prices. Negotiations are conducted between a utility and a shipper, using the first contract price agreed each year as a reference price (Productivity Commission, 1998). That does not provide a benchmark price per se but plays an important role as a price indicator. In the year 1999, for example, the Chubu Electric Power Company signed the first coal purchase contract of the year at $29.95/tonne. This reference price for the fiscal 1999 was 13.2 per cent (or $3.15/tonne) lower than that for the preceding year set at $34.50/tonne via long-term price contracts made through the earlier system.

South Africa

South African coal mining industry is passing through a transitional phase. Historically, it had served three main markets. The majority of clean coal, which is produced by cleaning, that is, processing the Run-of-Mine (ROM) coal, directly obtained from the mine, is exported. Typical qualities of this clean coal are . 12.5 per cent ash and calorific value (CV) = 6,000 kcal/kg on Net-as-Received (NAR) basis. A small fraction of similar quality coal, but closely sized into the traditionally named Nuts, Peas and Beans, is sold on the inland market to a variety of industrial and domestic consumers. A third component in the saleable products is the so-called middlings (intermediate) fraction, which varies in CV between 4,300 and 5,500 kcal/kg and is sold to the state-owned power monopoly Eskom. More than 90 per cent of the power produced in South Africa is coal-fired. With the recent trend of increased share of the mining and cleaning of poorer quality coal, relative proportion of the three markets is undergoing a change with no change in the quality specs for all the three markets (McMillan, 2006). Pricing is different for each delivered segment (Eskom, domestic and export) and often the three different markets have an inter-related relationship at specific time intervals. The relationship between the different markets and its pricing were not as strongly defined historically as it has converged over the last few years. Although Eskom and export products have completely different product specifications, many mines produce both these products, and pricing is often calculated on a cost sharing basis. Besides CV, ash and volatile matter contents, abrasive index plays an important role in price fixation. Higher the abrasive index, shorter is the life of the equipment coming in contact with coal. Among other quality parameters, size of the coal, moisture and sulphur content are limited to certain mandated values (Melanie, 2009).

United Kingdom

Higher the ash content in coal, more is the consumption of coal to produce unit energy, because heat is wasted in producing ash. In the United Kingdom, though coal used in thermal power plants is of significantly lower ash content (compared to India), coal price consists among others of ash penalty. Ash penalty includes a specific component for the smoke nuisance value, thus incorporating an incentive to produce or supply lower ash coal. Penalty system is also applied to the users. Every power plant pays the government a tax of 8 pounds (approximately ₹824) per tonne for ash disposal, known as landfill tax. This new rate came into effect in the year 2010 and is expected to increase over the years. This is in addition to the disposal cost (Landfill Tax, 2014). On the other hand, if the construction industry uses, instead of ash, any material derived from nature such as soil, sand, gravel, etc., it has to pay a tax of about half the landfill tax. This tax is in addition to the actual price of the natural material. All these penalties were introduced about two decades ago.

United States

The model of the US coal market developed for the CPS (Coal Production Sub-module) recognizes that prices in a competitive market are a function of factors that affect either the supply or the demand for coal (EIA, 2001). The general form of the model is that a competitive market converges towards equilibrium, where the quantity supplied equals the quantity demanded for region i and mining type j in year t:

In this equality, Qi,j,t represents the long-run equilibrium between supply and demand for coal in a competitive market.

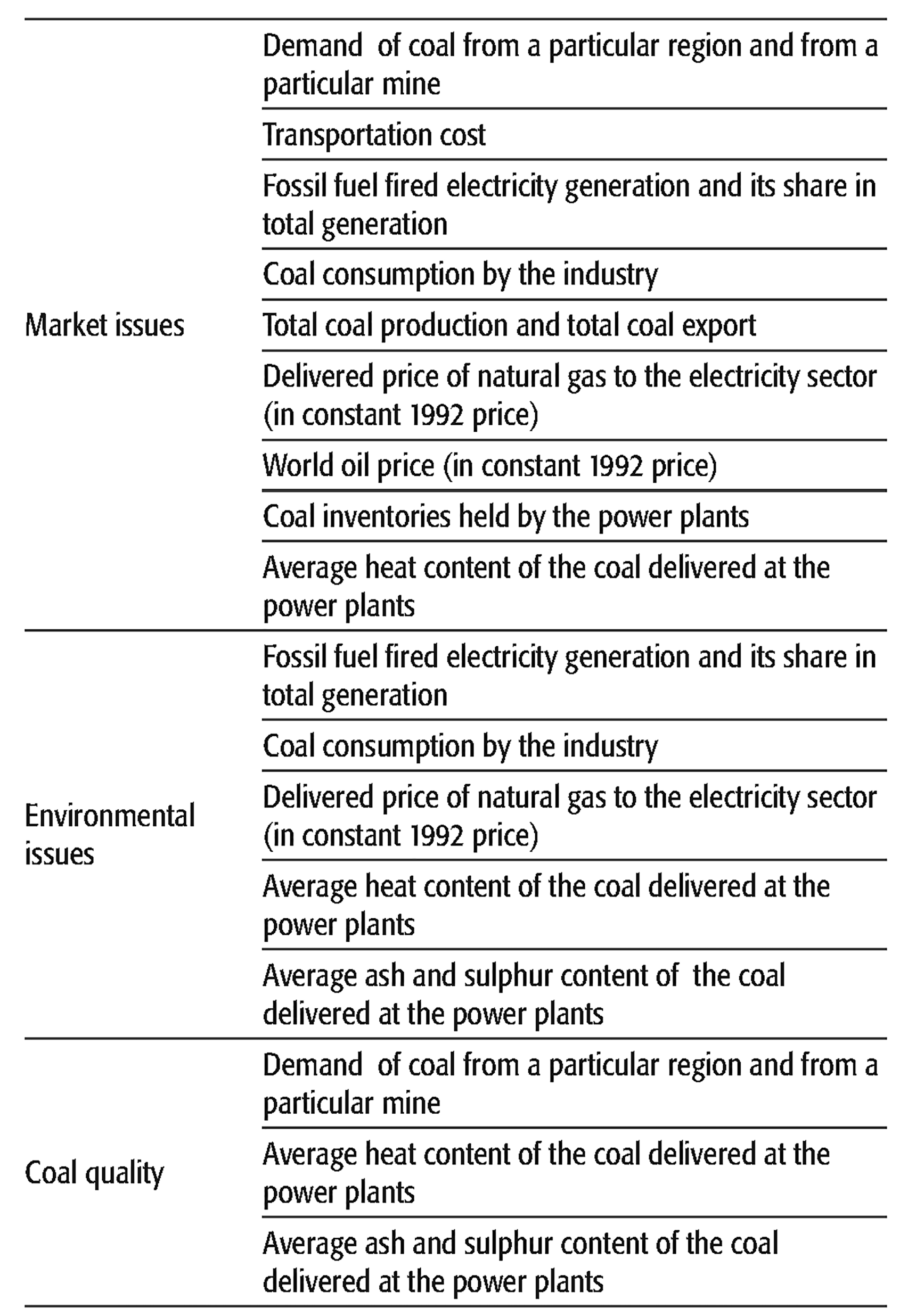

The factors which affect QD on year to year basis include three distinct groups, related to market, to environmental legislation and to coal quality (characteristics). These groups are interrelated. Average heat content of the coal delivered at the power plants, needs to address all the three issues (Table 4). Average ash and sulphur content of the coal delivered at the power plants need to address both environmental and coal quality issues. Similarly, demand of coal from a particular region and from a particular mine is reflective of the market while addressing the coal quality concerns.

The factors which affect QS on year to year basis appear to be essentially controlled by market issues:

Quantum of coal supplied from a particular region and from a particular mine Average pithead price of coal thus supplied (in constant 1992 price) Annual coal production capacity of that particular mine from that particular region and its average annual capacity utilization Labour productivity Wages Mining cost, both operational and maintenance Average industrial price of electricity and that of (ultra-low sulphur) diesel oil Various unaccounted factors A Summary of Factors affecting Demand in US Coal Market

In recent years, after the Pacific Coast Action Plan on Climate and Energy initiative was put into place, the US coal-fired power plants in right earnest started using low ash ROM coal or cleaned coal. Under this initiative, every thermal power plant is heavily penalized, for emission of every additional tonne of CO2, beyond the prescribed limit. That had affected the price. Sulphur content of coal was taken care of by juxtaposing it to ultra-low sulphur diesel oil.

Russia

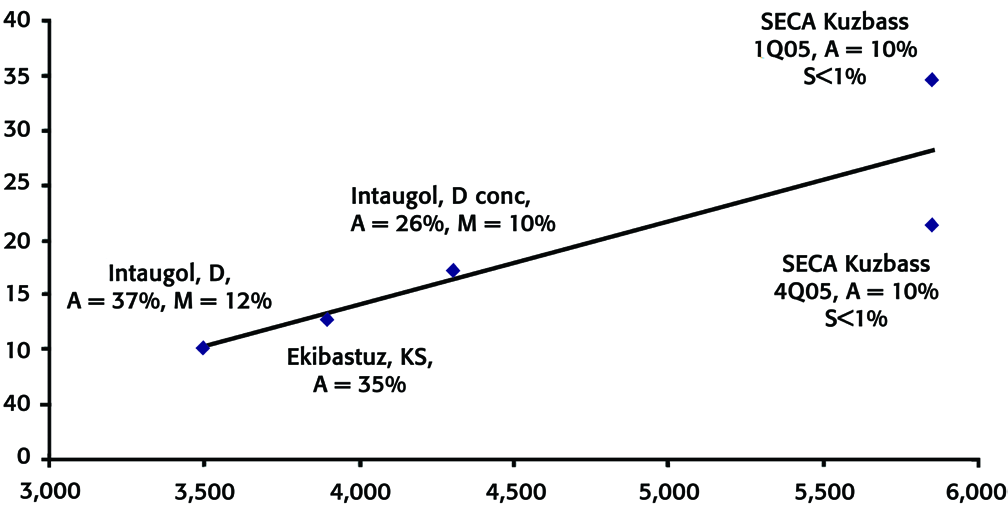

Coal pricing in Russia is done at two different levels: for domestic market and for export market. Theoretically speaking, the price for steam (non-coking) coal is proportionate to its calorific value. While this is usually the case, prices are often adjusted at a much lower level for other factors such as ash, sulphur, and in some isolated cases even for phosphorous content. Typical examples are tight-regulatory markets of the US and Western Europe. The case is however different with Russia owing to liberal pollution control norms. Coal price in domestic market is controlled by the Russian system of classification which does not ordinarily take into account ash and sulphur content. These are the characteristic values which determine whether the coal can be exported or not (Yakubov, 2006). Figure 1 shows that the price of coal which can be consumed only on the domestic market does not depend significantly on sulphur and ash content, with good coefficient of correlation. The same curve however does not really fit in the Standard European Coal Agreement (SECA) export coal parameters, where price is essentially arrived at on case-to-case basis. The most important issue for the Russian steam coal is whether it meets the quality requirements of the SECA and thus can be exported to Western Europe and Asia. Effectively, high quality steam coal is a global commodity with industry-wide standardized contracts and transparent market pricing.

The following properties of a steam coal significantly affect Russian thermal coal prices:

Calorific value (measured usually on the ash-free basis) is the core factor affecting price. It may reach 7,000 kcal/kg for high quality coal while the usual range of hard steam coal comes to some 3,500–6,500 kcal/kg. According to SECA, calorific value of standardized high-grade steam coal must exceed 5,800 kcal/kg. Ash content is another parameter having a significant effect on steam coal prices. It may reach as much as 40 per cent, Ekibastuz coal from Northern Kazakhstan being a glaring example. SECA stipulates that ash content must be below 10 per cent (15 per cent in the UK of dry weight). Sulphur content may significantly discount coal price. SECA requires sulphur below 1 per cent. For instance, Rostov based coal miner Gukovugol can export only a quarter of its output due to high sulphur content in its anthracites (a variety of coal). In Russia, since excessive coal moisture results in transportation difficulties during the winter, besides the deterioration in power plant thermal efficiency, moisture content might also affect the coal price.

China

Historically, coal pricing in China can be divided into a planned-economy period and a market-economy era (Peng, 2011; Zhao, Che, & Zhao, 2012). Prior to 1985, domestic coal price was controlled by the state. Beginning in the year 1993, coal pricing opened up gradually and started carrying a double-track price: planned price and market price. ‘Electric coal’ for power plants was under the dual-price system of ‘planned coal’ and ‘market coal’. ‘Planned coal’ is broadly equivalent to the coal linkage system practised in India under the supervision of the union government. ‘Market coal’ segment, wherein a power plant can buy coal from open market in exigency, is absent in India. On January 1, 2002, the state guided price was abolished and ‘electric coal’ reflected only the market price. However, in order to control abnormal fluctuations in price, the state continues to intervene from time to time with the dynamic coal price. Besides production cost and labour cost, the total cost of coal production includes resource cost, environment cost, sustainable development cost and safety cost.

‘Resource cost’ consists of resource tax, resource compensation fee, mining right fee, etc. In order to strengthen macroeconomic control, the state gradually raised the level of the coal resource tax in recent years. It varies from place to place and is in the range of ₹25–50 per tonne. Since mining leads to depletion of natural resources, the country levies a resource compensation fee for mining rights. To encourage efficient mining, it refers to the ratio of coal output to coal reserves in a certain area and is set at 1 per cent of the coal sales receipt. Mining right fee includes property rights and exploitation rights. Since the mineral resources belong to the nation, mining rights of new mineral resources can only be gained competitively by bidding and auction.

Since the year 2006, a company engaged in the mining of mineral resources must deposit the ‘environment cost’ and fulfil the duty of restoration of ecology. The government ensures that the fund generated is used for the assigned purpose. It adds up to the coal price. The level of ‘environment cost’ varies and is set as a percentage of sales income. In Shanxi province with the largest coal output, the environment cost is approximately ₹80 per tonne. The ‘sustainable development cost’ was first experimented in Shanxi province and was later extended to other parts of China. The standard rate is about ₹250 per tonne though it varies for different types of coal and the tonnages of coal consumed. The payment realized from coal companies is ordinarily used to solve regional ecological/environmental problems. Regulatory bodies ensure that large and medium coal mines pay ₹30–80 (1Yuan = ₹10) or more and the small coal mines pay ₹60–100 or less per tonne of coal sold as ‘safety cost’.

International Coal Price-Setting Mechanisms: A Summary

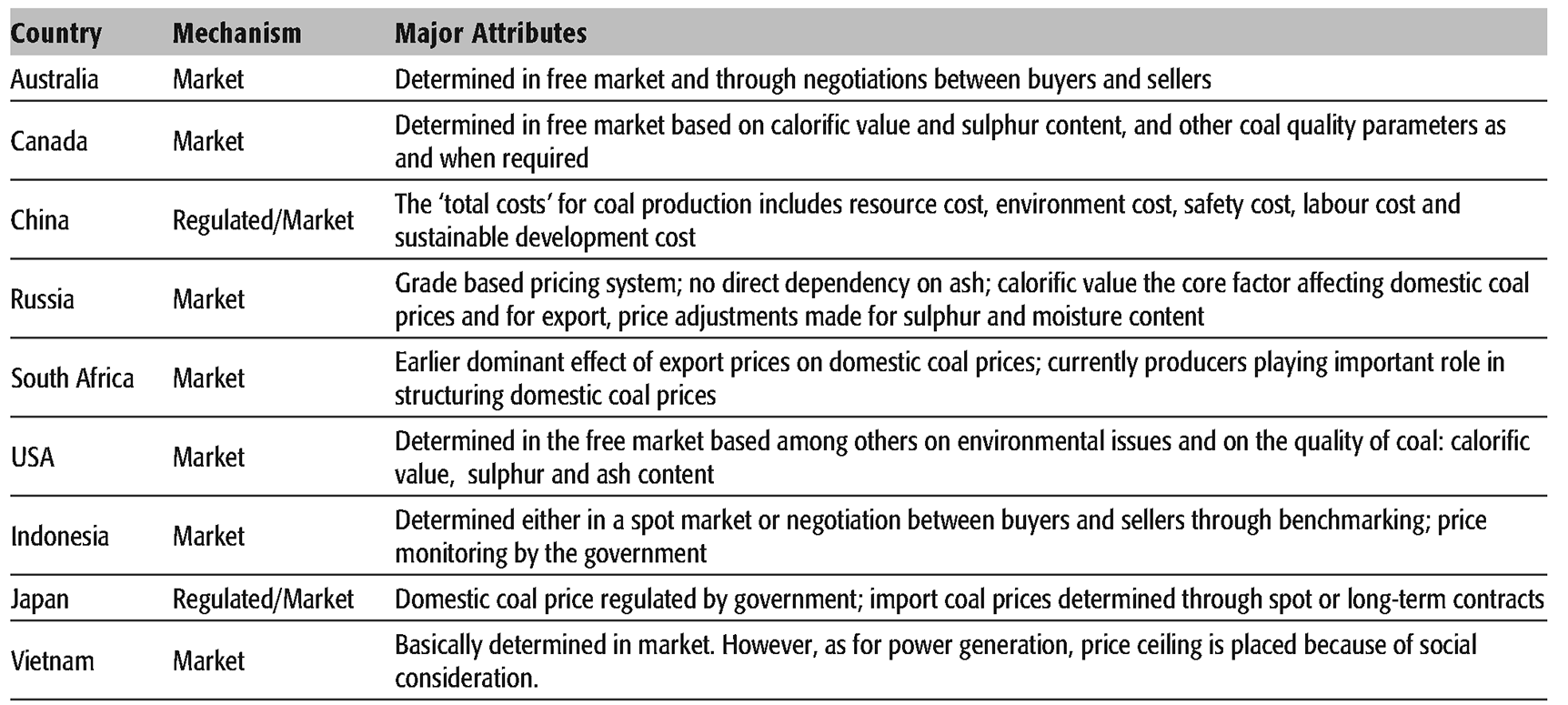

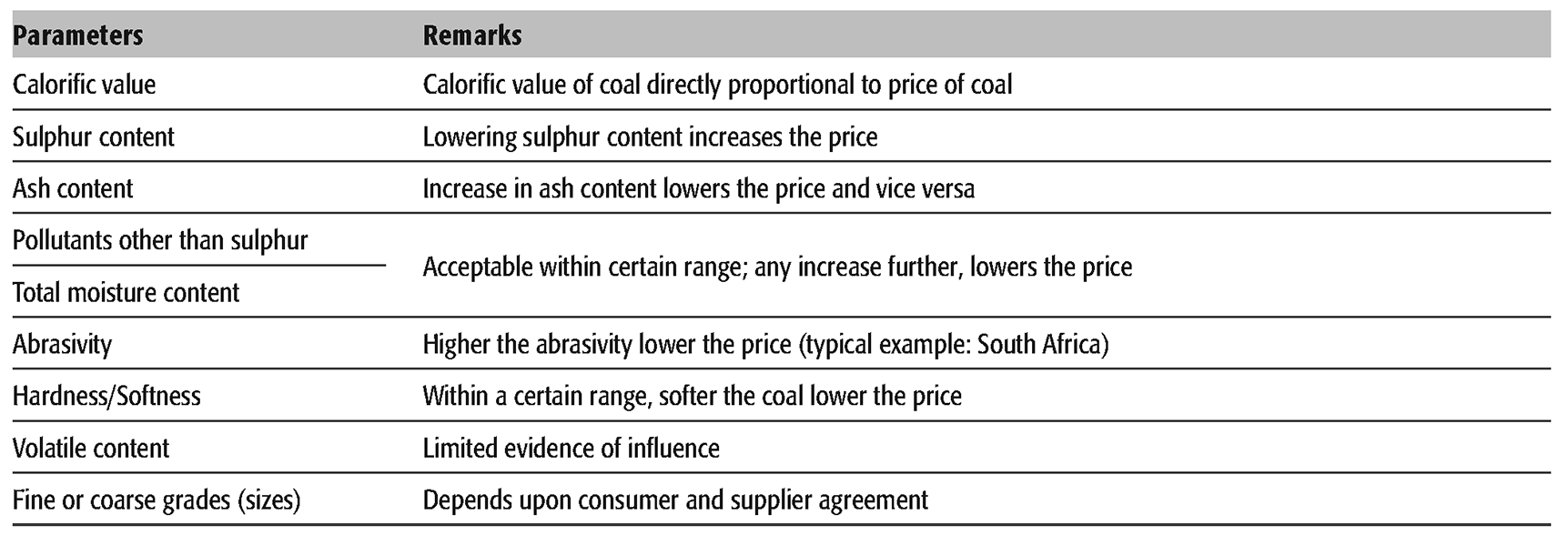

Non-coking coal pricing systems adopted in different countries have been discussed here and a summary thereof is presented in Table 5. Pricing mechanisms of three unique country cases, Poland, Russia and China, all however relevant for India, are noteworthy. The domestic markets or international trade, a standardization of coal quality parameters is in practice, the primary one being calorific value, its basic commercial property. The final price paid for the coal is also determined by other such properties which may affect commercial use, various market issues, and environmental conditions. Table 6 shows the generalized relationship between quality parameters and thermal coal prices for the countries listed in Table 5.

Summary of Coal Pricing Mechanisms of Various Countries

Generalized Relationship between Quality Parameters and Thermal Coal Prices

UHV–Grade Based Non-coking Coal Pricing as in the Year 2009

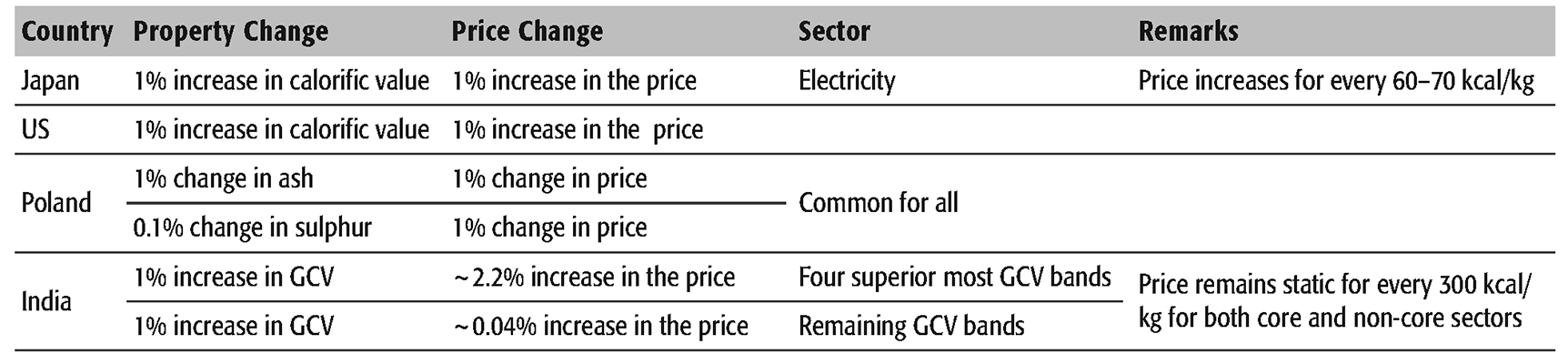

Table 7 shows a comparison of how across the world property change affects the change in coal price. The figures provided for India have been calculated on the basis of Table 1. Price change with respect to positive or negative changes in the attributives of coal appears to be softest in the coal pricing system in India because of the large width of the GCV bands.

Lessons For India

Non-coking coal in India is currently sold on the basis of grades. Grades are dependent on heat value of coal, expressed by GCV with no penalty for ash and moisture. After all higher the GCV lesser is the tonnage of coal required to produce heat to generate 1MW of power. In addition, lower the ash lesser is the tonnage of coal required to produce 1MW of power. Switchover from UHV to GCV based pricing system in itself is an improvement. Continuing the development further, drawing on international experience on non-coking coal pricing and taking into account specifics of Indian coal scenario, a new pricing system based on a holistic approach needs to be developed. A system that would be well defined and well structured so as to include the market reality, resource position of coal both in short and long term, quality parameters of the coal supplied and coal sector sustainability issues to address the different externalities associated with coal production, supply and consumption in India. Two major points, penalty on ash and moisture are discussed here. Other points have been deliberated upon elsewhere (Bhattacharya, 2010; Bhattacharya & Tiwari, 2013).

Penalty on high ash content is very important. Except China, all major coal producing countries burn 10–20 per cent ash coal for power generation. More than 60 per cent of the coal burnt in China has an ash of 30 per cent or less. The corresponding range for India is 25–45 per cent, mostly at the higher end. NTPC loses at least ₹11 billion annually because of stones, boulders, and other non-combustibles present in coal. According to NTPC estimates, coal consisting 36 per cent of the waste travels on an average 600 km from its source to the company's power plants. 2

Economic Times. Retrieved April 2014 from http://articles.economictimes.indiatimes.com/2013-04-03/news/38248567_1_coal-india-ltd-gross-calorific-value-domestic-coal

GCV based pricing therefore, creates an incentive to disregard the environmental and social license issues associated with the burning of high ash coal. The coal pricing system needs to take these issues into account. A cost component if embedded in the price could be recovered from the sales realized and later transferred, for example, to an independent agency or to governmental agencies for addressing the environmental and social license issues. That kind of approach would enhance the sustainability of coal-fired power generation, so vital for India. Mere solar power subsidy embedded in coal price is not adequate.

Relative Merits of Using Coal with only 10 per cent less Ash (cost basis: 2000)

Variation in GCV (kcal/kg) at Approximately Similar Ash (%) at 5 per cent Equilibrated Moisture

India is federal in nature. The Constitution of the country has three schedules of subjects of governance: union, state and concurrent. Power is in concurrent list. Till about a decade ago, states played the most important role in power generation. Even now the states contribute about 37 per cent and the central sector about 27 per cent of the total power generated in the country. To set up a thermal power plant, the primary requirement is of:

Land to locate the plant, township and to dispose of the fly ash Coal to burn to produce the heat Water to produce the steam, and then electricity Air to emit

Out of this, a state government in the union of India has no control over coal, the only raw material required. It is the union which decides everything about coal including the linkage, that is, the coal supply chain, from mine to power plant.

To open a coal mine in India, clearances, fairly large in number, are required in two stages. Stage I essentially involves clearance in principle involving MOEF and state government for land acquisition, pollution clearance, etc. Stage II involves the factual clearances, where most cumbersome are forest clearance from MOEF involving both union and state, though dominated by the former and land acquisition, a fully state subject. So complex is the reserve to consumption coal chain in India. There are multiple stakeholders, sometimes with conflicting interests. Coal producing states (precisely areas) suffer irreversible short-term and long-term damages. Worse is the case with the states producing pithead power.

Price reform has never been an easy task, howsoever rational it might be. A switchover from UHV to GCV based pricing system took more than a decade with acrimonious debate, essentially between the two ministries of union government, coal and power. A small country, Poland, took almost a decade to reform its coal pricing policy because of differences in opinion between the ministries of environment, power, steel and coal. Ultimately, the Ministry of Finance had to intervene and issue the price notification, that too under a mandate from the European Union (Ney et al., 2004). A new pricing system based on a holistic approach needs to be developed for the non-coking coal of India. Otherwise, the coal sector reforms would remain incomplete.