Abstract

Speculative trading in energy and commodity markets has been blamed for increased volatility, price distortions, and market inefficiency, with negative effects on the real economy. We take a new approach to investigate the impact of speculative trading using macroeconomic announcements and high-frequency data. We study the impact of twenty-six macroeconomic announcement releases on energy commodities (crude oil, natural gas) as our baseline case, which we contrast with metals (gold, silver, copper, and palladium). We find that increased speculative trading lessens the impact of macroeconomic surprises on futures markets, as measured by price drift, volatility, and bid-ask spreads. Our full-sample results show that increased trading by speculators improves liquidity and price discovery, while reducing volatility. We document a damping effect on volatility that is stronger for procyclical commodities such as crude oil and natural gas than for precious metals such as gold, which is a safe haven. In sub-sample analysis where we separate the effects of money managers and swap dealers, we find that the positive effects that we document are driven by money managers. Since traditional market participants prefer stability, our results suggest a beneficial impact of increased trading and speculation.

Keywords

1. Introduction

The appeal of energy and other commodities as an asset class has grown since the Commodity Futures Modernization Act of 2000 (CFMA). By partially deregulating derivatives, the CFMA has made it easier to trade commodity futures contracts for investment purposes. Rather than invest in physicals or in shares of commodity-linked firms, investors can use futures to gain exposure to “commodity beta” (Boons et al. 2014). This evolution is particularly relevant for energy markets, where futures trading volume has grown tremendously. For instance, the total trading volume of commodity derivatives was 137.3 bn contracts in 2023, which is 64% more than in 2022 (Futures Industry Association, 2024). An important reason for this trend is that commodities have periodically benefited from bull cycles (most notably in 2004–2008), attracting a growing number of speculators and institutional investors. As a result, the commodities asset class has become an important but volatile revenue source for trading firms and investment banks. Three firms, Goldman Sachs, Citi, and Macquarie earned together $20 bn from commodities trading in 2022, much of it from energy-related contracts. 1

Is the presence of more financial investors harmful to traditional market participants, such as hedgers? While many think so, the evidence is unclear. The idea that poorly informed investors can disrupt markets has a long history (Shleifer and Summers 1990) and has been revived in a recent theoretical literature on financialization (Basak and Pavlova 2016; Goldstein and Yang 2022). These papers are motivated by the commodity price run-up of 2004 to 2008, which occurred shortly after the CFMA was passed (Domanski and Heath 2007). Critics argue that the activities of financial investors, who are not directly involved in producing or processing commodities, can distort prices and increase volatility. 2 These critics claim that energy and commodity markets have become more sensitive to financial market fluctuations, and less to supply and demand fundamentals. Energy futures markets have attracted attention due to the popular perception that large price swings affect the real economy (e.g., through higher gasoline and heating costs) (Cheng and Xiong 2014). Research, however, generally does not support this claim (Baumeister and Kilian 2014). Whether or not these fears are justified, policymakers have taken notice and the CFTC has progressively implemented rule changes such as new position limits.

A large empirical literature debates the causes of periodic price and volatility run-ups in commodity and energy markets. Researchers emphasize the importance of differentiating between speculative traders and passive investors (e.g., index traders). The latter category of traders is more recent and trades energy and commodity contracts for diversification purposes rather than for speculative profit. While Singleton (2014) suggests that financial investors may be to blame for higher energy prices, Kilian and Murphy (2014) use a structural model to show that speculation can be ruled out as a cause of the oil price surge during 2003 to 2008 – even though speculative demand played a role in previous oil price spikes. Further evidence against the hypothesis that index traders are responsible for the sharp increase in commodity prices is provided by Irwin and Sanders (2011, 2012). In a different strand of the literature, Büyükşahin and Harris (2011) use Granger causality tests and daily data to investigate whether speculators increase crude oil futures prices. They find little evidence to support that claim. Also using daily position-level data, Brunetti et al. (2016) show that speculators reduce price volatility in commodity and energy markets. Reviewing this early literature, Fattouh et al. (2013) conclude that speculation is unlikely to explain the commodity and energy bull cycle of 2004 to 2008.

Recent research provides new theoretical grounds to establish how trading activity could affect energy and commodity prices (Basak and Pavlova 2016; Goldstein and Yang 2022). The subsequent empirical literature, however, does not reach a consensus. Henderson et al. (2015) use data on commodity-linked notes to show that uninformed trading flows affect commodity prices, but Ready and Ready (2022) argue that the economic magnitude of this effect is too small to matter. Other recent papers find instances of futures price overshooting, reversals, and greater noise in markets (Da et al. 2024). They also find that commodities seem to display higher correlations with equities and with each other (Kang et al. 2023).

Thus, our main contribution is to provide sharply identified evidence on the impact of speculative trading on energy (crude oil and natural gas) and metal markets (gold, silver, copper, and palladium), with additional evidence on sub-categories of traders. We focus on speculation rather than financialization, which has been linked to the trading activities of passive (index) traders (Tang and Xiong 2012). Specifically, our paper investigates the impact of speculative trading of sub-categories of non-commercial traders. Our rationale is that speculative trading is likely to reflect informed trades, which is our focus, in contrast to index traders who are considered uninformed. Energy commodities serve as our baseline case due to their economic importance and high trading volumes, while metals offer a useful comparison, particularly as gold is perceived as a safe-haven asset. We use high-frequency (five-minute) data to measure the instantaneous reaction of commodity futures returns, volatility, and bid-ask spreads to the surprise component in macroeconomic announcement releases (Andersen et al. 2007; Kurov et al. 2019). The data runs from April 4th, 2007, to February 11th, 2024. Our framework also accounts for the time-varying intensity of speculative trading activity. This study builds on Kilian and Vega (2011), who find no evidence, at a daily frequency, that energy prices react to macroeconomic announcements. By using intraday data, we can better identify the impact of specific macro surprises. We also avoid a common criticism of event study methods, namely that using daily frequency data may reduce the power of statistical tests and could lead the researcher to misattribute the effect of a specific announcement, as other market events occur the same day (Kothari and Warner 2007).

We find evidence of beneficial effects (price stability and market efficiency) from increased trading activity in energy and commodity markets. Our first finding is a damping effect on price reactions: while macro surprises generate a positive abnormal return for good news (and negative for bad news), the magnitude of this reaction is significantly weaker when speculative trading is higher. Second, we find a similar damping effect on volatility reactions. While all surprises (good or bad) generate a volatility increase, this reaction is lessened when the futures market shows more speculative trading. Third, we document lower bid-ask spreads when speculative trading is higher, controlling for the surprise environment. Fourth and last, these beneficial effects are linked to the trading activities of money managers. In contrast, increased trading by swap dealers appears to have an amplifying effect on reactions to macro surprises. These new insights are made possible by investigating this issue using a new angle, namely their sensitivity to macroeconomic surprises, and with high-frequency data. Our findings have important implications for energy market investment and regulation, and to the broader debate about speculation in energy and commodity markets.

By investigating a broad range of traders in energy and commodity markets, our findings also extend the work of Brunetti et al. (2016). They find that financial investors, especially money managers and hedge funds, help commodity markets by supplying liquidity, reducing volatility, and generally improving market efficiency. Moreover, our results relate to Cheng et al. (2015) who show that financial investors, being better informed about markets, contribute to price discovery and liquidity. This is particularly relevant for energy markets, where accurate price discovery is crucial for physical market participants and investors. Thus, speculative traders help markets by distributing and assimilating new information into prices. These insights are valuable given the ongoing energy transition and the importance of efficient price discovery in energy markets. Two papers are probably closest to ours. First, Brunetti et al. (2016) who find that hedge funds add liquidity to commodity markets, resulting in more efficient prices and lower volatility. They argue that it is merchant positions (i.e., hedgers) that are linked to greater volatility, and that the presence of hedge funds allows for faster and more efficient price discovery. Second, using daily data, Kilian and Vega (2011) study how energy prices react to macroeconomic announcements. Our paper extends this work to high frequency data.

2. Background

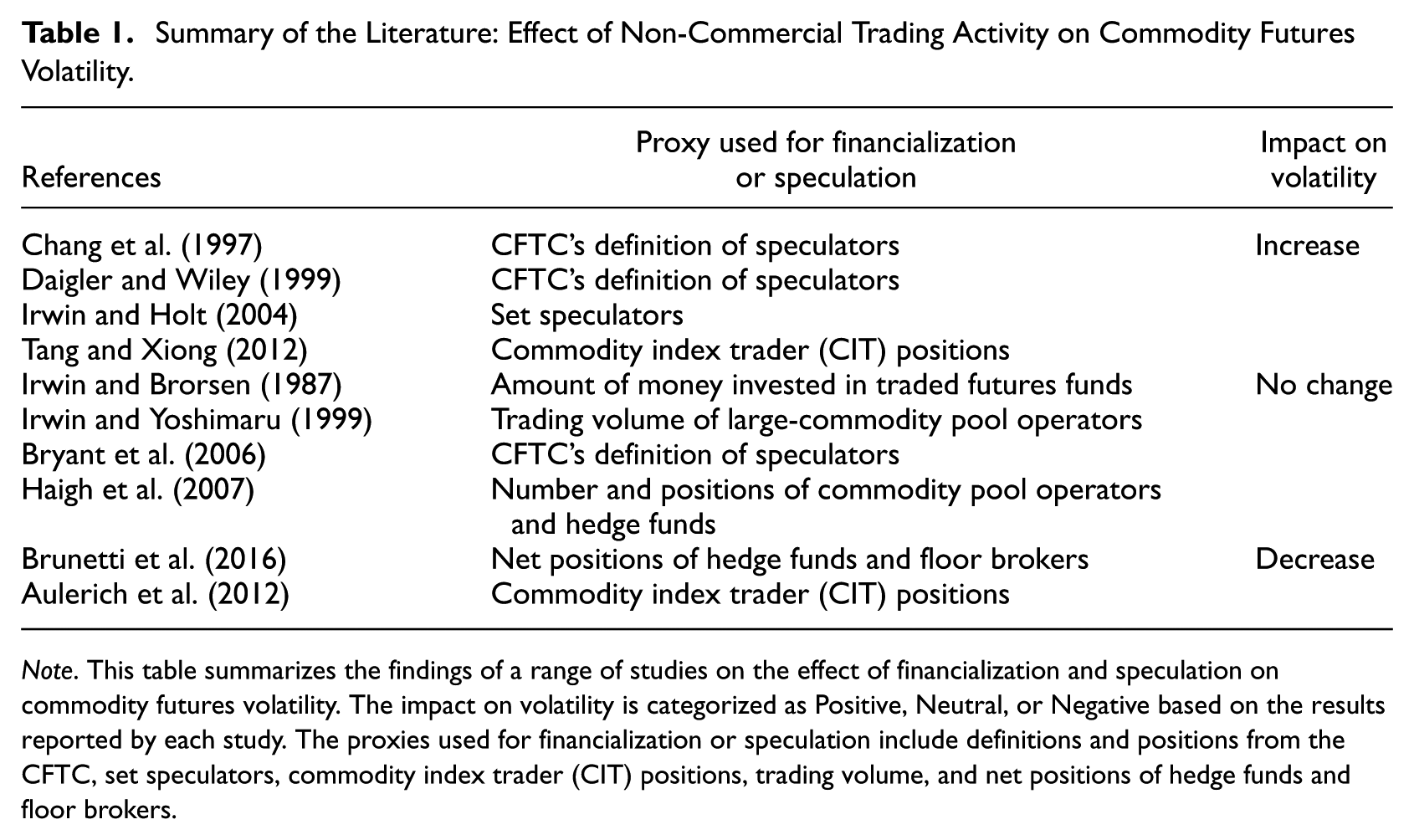

Price discovery in commodity markets occurs mainly in futures markets and is affected by informational frictions around supply and demand. Thus, risk sharing and information discovery represent a potential channel for financial investors to generate distortions in energy and commodity markets (Cheng and Xiong 2014). In their model, Basak and Pavlova (2016) predict that the increased presence of financial actors can increase commodity futures volatility, as well as correlations between commodity and equity returns. Goldstein and Yang (2022) also argue that under some conditions, a greater presence of financial investors can be harmful to commodity markets. Theory shows how a change in the participant mix in commodity markets could generate undesirable distortions, but the empirical literature is far from settled (see Table 1). Singleton (2014) argues that trading activity by financial investors creates informational frictions, leading commodity prices to become more volatile and to diverge from their fundamental values. Using a no-arbitrage argument, however, Hamilton and Wu (2014) show that the positions of commodity traders included in index funds cannot be used to achieve excess returns in futures markets. Ready and Ready (2022) show that while index traders do have a positive price impact, it is much too small to explain the apparent price distortions or bull cycles observed since 2004. In addition, financial investors do not have a uniform impact on market liquidity. Investors affect liquidity risk by either providing liquidity to meet the hedging needs of other traders or consuming liquidity when they trade for their own needs (Kang et al. 2020b). Indeed, Brunetti and Reiffen (2014) show using data on commodity trader positions that index traders provide insurance against price risk.

Summary of the Literature: Effect of Non-Commercial Trading Activity on Commodity Futures Volatility.

Note. This table summarizes the findings of a range of studies on the effect of financialization and speculation on commodity futures volatility. The impact on volatility is categorized as Positive, Neutral, or Negative based on the results reported by each study. The proxies used for financialization or speculation include definitions and positions from the CFTC, set speculators, commodity index trader (CIT) positions, trading volume, and net positions of hedge funds and floor brokers.

2.1. Macroeconomic Announcements

Surprises in macroeconomic announcements affect financial markets, whether in stocks (Scholtus et al. 2014) or in bonds (Fleming and Remolona 1997). In a key study, Balduzzi et al. (2001) find that seventeen public news releases affect bond prices, trading volume, and bid-ask spreads. Karali and Ramirez (2014) show that energy futures markets exhibit asymmetric responses to macroeconomic news, with significant volatility spillovers between natural gas and crude oil markets. Cao et al. (2024) document a time-varying relationship between U.S. monetary policy and crude oil prices, finding that unexpected oil price increases can push monetary policy from expansionary to restrictive stance. Kang et al. (2020a) further show that after 2004, short-term oil price volatility is driven by industrial production, term spreads, and credit spreads, along with traditional market factors.

The literature on commodity-specific announcements is smaller and less conclusive. Hollstein et al. (2020) look at how different economic variables affect the term structure of commodity futures volatility. They show that speculation and jobs-related macro variables have the largest impact on volatility. Zhu et al. (2022) further show that stock market anomalies can be explained to some extent by oil price shocks, separately from the effect of other macroeconomic variables and investor sentiment. While the literature finds a clear impact of macroeconomic announcements on stock and bond prices, there is no clear answer as to whether they affect commodity futures prices, or whether increased trading by financial participants accentuates these reactions. This issue is especially relevant for energy markets, given their macroeconomic importance. Our research provides new insights by using high-frequency data, expanding the set of announcements, and considering a time-varying measure of speculative trading intensity to capture trading activities for each of the commodities in the sample.

3. Data

We now present a detailed description of our data. Since this paper relies on several types of data, we describe: (i) how to obtain the macroeconomic announcement surprises, (ii) the commodity futures data, and (iii) how to capture speculative trading activity.

3.1. Data on Macroeconomic Announcements

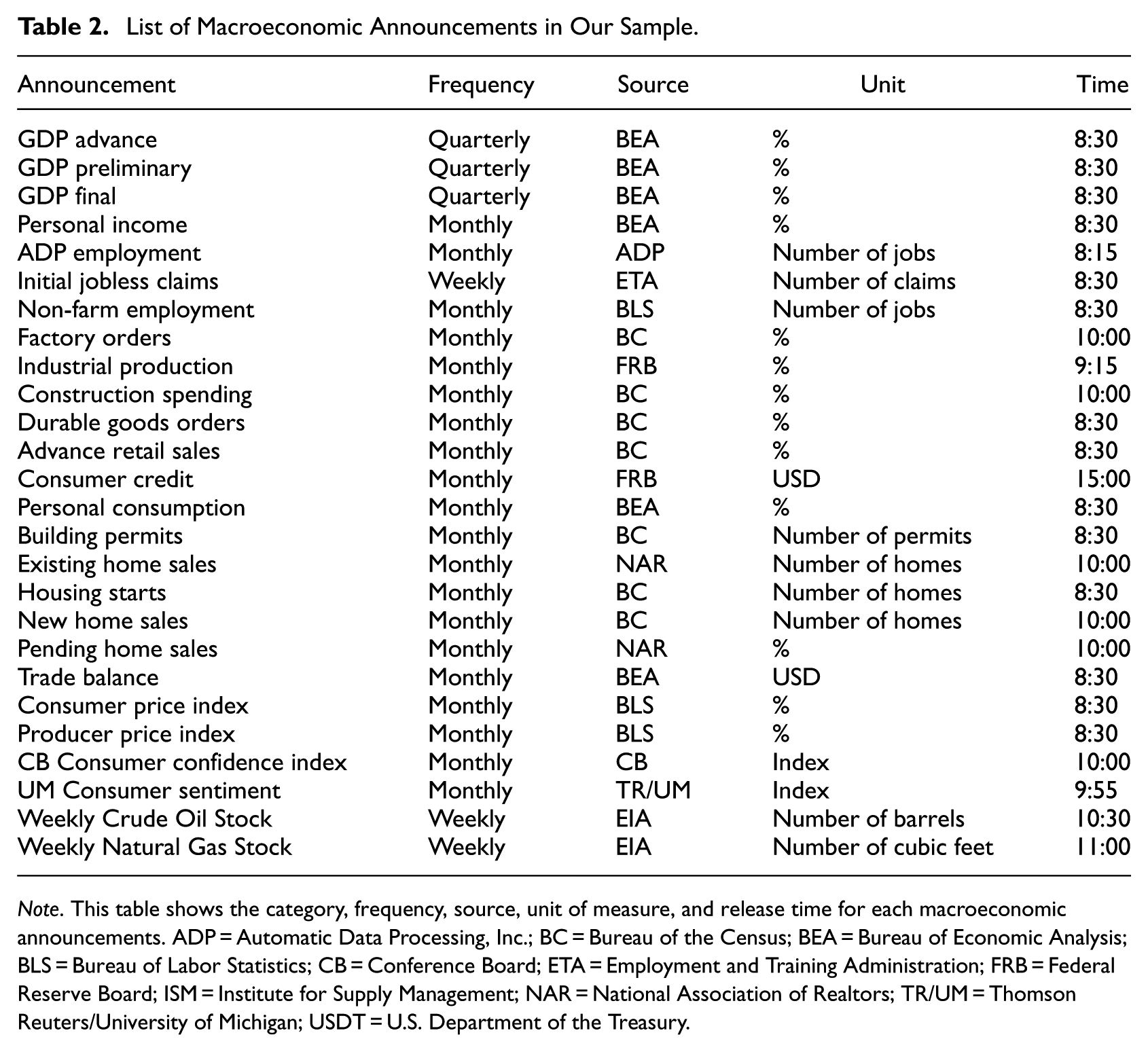

The macroeconomic announcement release data are obtained from Bloomberg and Refinitiv Eikon. We collect information on twenty-two announcements that are standard to the literature (see e.g., Andersen et al. 2003). Our sample for macroeconomic announcements is matched to our high-frequency data and therefore runs from April 2nd, 2007 to February 11th, 2024. The announcements belong to ten categories: Income, Employment, Industrial Activity, Investment, Consumption, Housing Sector, Government, Net Exports, Inflation, and Forward-looking. Most of the announcements are released on a monthly basis. Table 2 summarizes the announcements and provides more detail such as the number of observations, release frequency, source, unit of measure, and time of release. Bloomberg provides analyst forecasts for all announcements, as well as the actual value of the announcement release. For all announcements except the Consumer Price Index and Initial Jobless Claims releases, a positive surprise will be interpreted by investors as signaling a strong economy (Fleming and Remolona 1997). In addition, we include energy sector-specific announcements published by the U.S. Energy Information Administration. The first is the weekly crude oil storage report, which provides an update on the quantity of crude oil held in storage in the U.S. The second is the weekly natural gas storage report. We do not include OPEC announcements, as they cannot be reliably used in a high-frequency econometric design (Känzig 2021) (Table 2). 3

List of Macroeconomic Announcements in Our Sample.

Note. This table shows the category, frequency, source, unit of measure, and release time for each macroeconomic announcements. ADP = Automatic Data Processing, Inc.; BC = Bureau of the Census; BEA = Bureau of Economic Analysis; BLS = Bureau of Labor Statistics; CB = Conference Board; ETA = Employment and Training Administration; FRB = Federal Reserve Board; ISM = Institute for Supply Management; NAR = National Association of Realtors; TR/UM = Thomson Reuters/University of Michigan; USDT = U.S. Department of the Treasury.

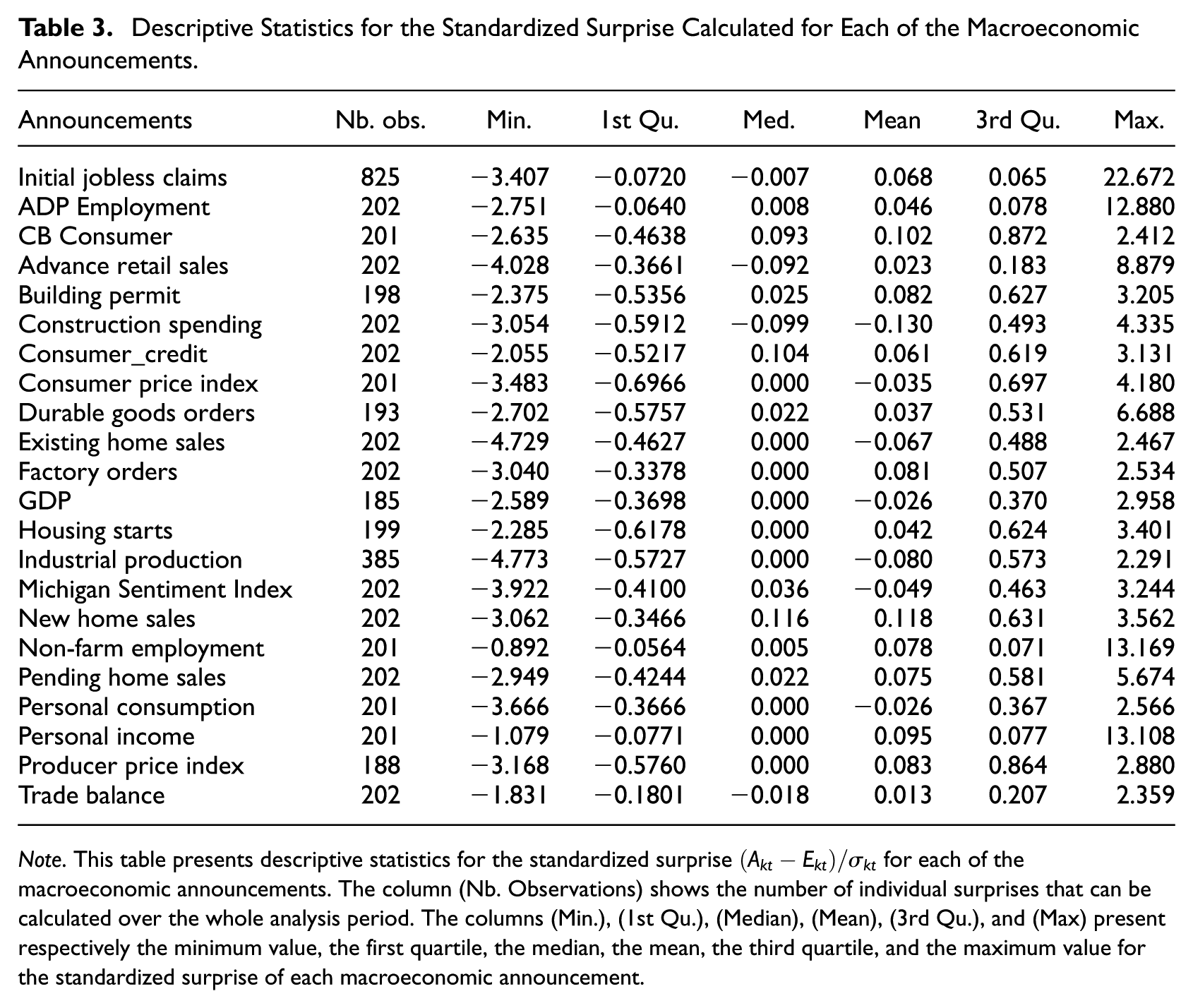

It is common practice in this literature to use the standardized surprise of an announcement rather than its realized value to quantify the unexpected component of the release. To calculate surprises, we follow Balduzzi et al. (2001). Let

The sample period is used to compute

Descriptive Statistics for the Standardized Surprise Calculated for Each of the Macroeconomic Announcements.

Note. This table presents descriptive statistics for the standardized surprise

3.2. Commodity Futures Price Data

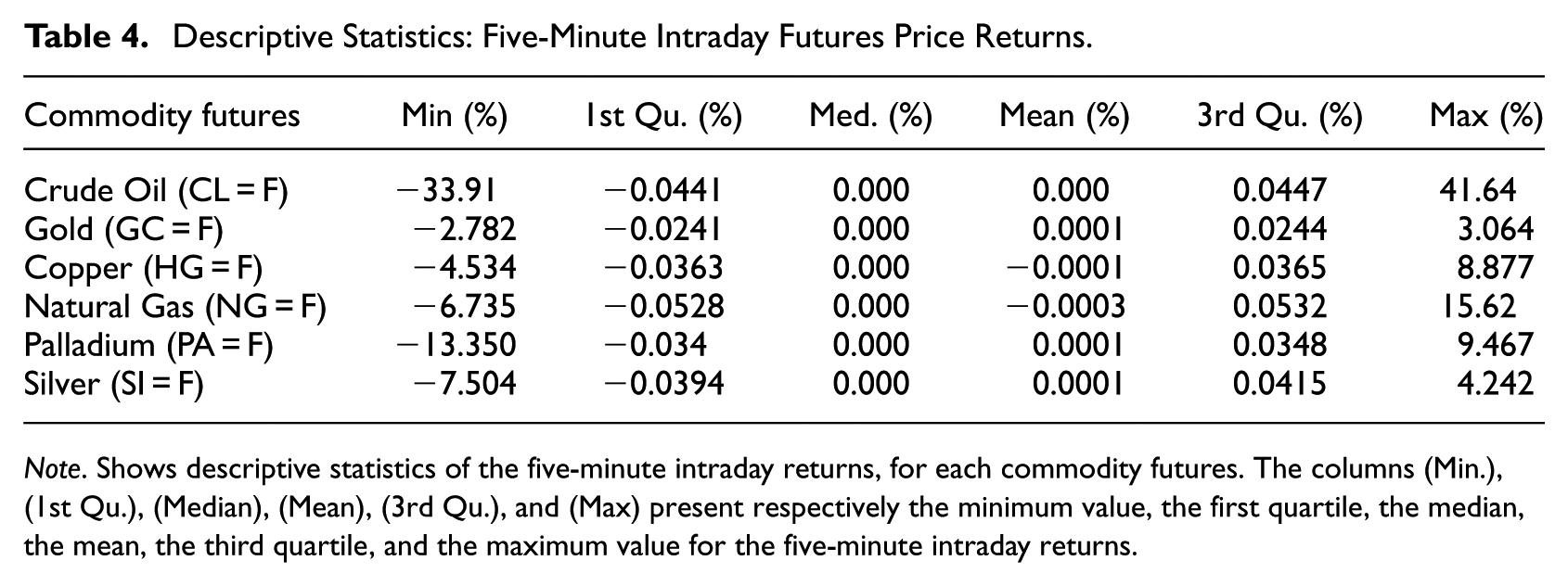

For intraday data on commodity futures prices, we use Barchart’s API. 5 Our dataset for prices contains some of the most economically significant commodity futures contracts traded in the U.S. We use a high-frequency price series that runs from April 2nd, 2007 to February 11, 2024. Among these contracts, crude oil and natural gas are pro-cyclical, while gold and silver behave as safe havens. High-grade copper and palladium are industrial metals used in the manufacturing of consumer products.

For each of the commodities in our sample, price returns

Descriptive statistics for the five-minute log returns are presented in Table 4. The most extreme outlier observations belong to crude oil, while gold has the fewest outliers. 6

Descriptive Statistics: Five-Minute Intraday Futures Price Returns.

Note. Shows descriptive statistics of the five-minute intraday returns, for each commodity futures. The columns (Min.), (1st Qu.), (Median), (Mean), (3rd Qu.), and (Max) present respectively the minimum value, the first quartile, the median, the mean, the third quartile, and the maximum value for the five-minute intraday returns.

3.3. Measures of Speculative Trading Activity and Trader Categories

The index of speculative trading is constructed using data in the Commitment of Traders (CoT) Report published weekly by the Commodity Futures Trading Commission (CFTC). The data provided by the CFTC includes the number of positions held by different types of participants in commodity markets. The CFTC separates trader types as follows: Commercials refer to trader-reported futures positions which the trader claims are used for hedging purposes, while Non-Commercials is obtained by subtracting the total long and short commercial positions from the total open interest.

7

We use the following information presented in the

The specific measure we use follows Hedegaard (2011), who suggests an index of speculative activity computed as the ratio of net long speculative positions over total open interest (

In addition to computing

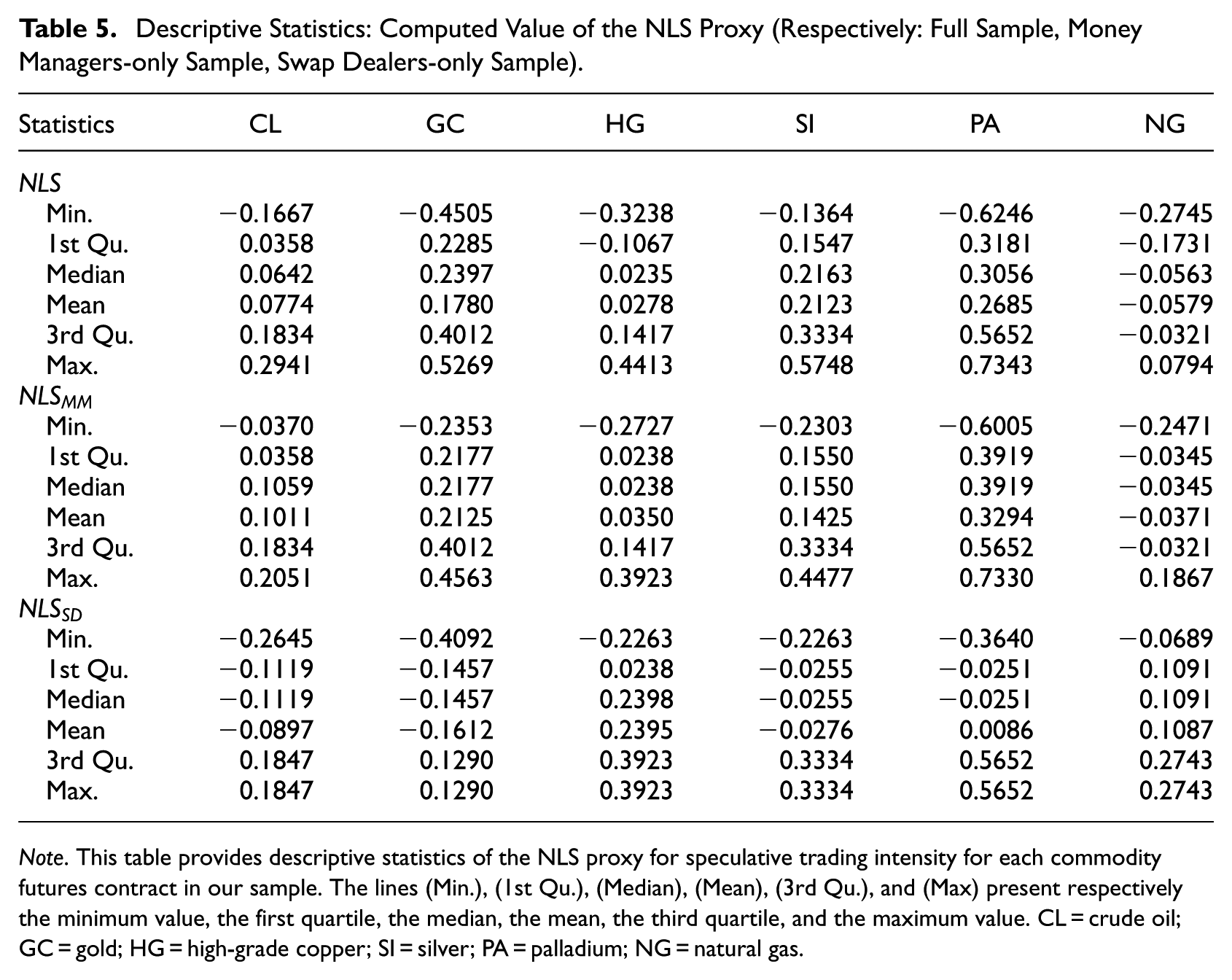

Descriptive Statistics: Computed Value of the NLS Proxy (Respectively: Full Sample, Money Managers-only Sample, Swap Dealers-only Sample).

Note. This table provides descriptive statistics of the NLS proxy for speculative trading intensity for each commodity futures contract in our sample. The lines (Min.), (1st Qu.), (Median), (Mean), (3rd Qu.), and (Max) present respectively the minimum value, the first quartile, the median, the mean, the third quartile, and the maximum value. CL = crude oil; GC = gold; HG = high-grade copper; SI = silver; PA = palladium; NG = natural gas.

4. Econometric Framework and Methods

4.1. Modeling the Impact of Surprises on Returns

Our high-frequency regression model is based on Kurov et al. (2019). 11 We run the following regression using the specification in equation (4):

where

After obtaining

4.2. Modeling the Impact of Surprises on Volatility

To estimate the volatility equation, we use a GARCH specification, as it is well known that the variance of commodity futures returns displays time variation and clustering (see e.g., Brunetti and Reiffen 2014). We specify a GARCH (1,1) model and extend the equation by including our NLS speculative intensity proxy as well as the macroeconomic news surprise variables. First, we estimate the mean equation (6):

Then, we estimate the following equation for conditional variance:

where

4.3 Modeling the impact on bid-ask spreads

Speculative trading could make markets more efficient by improving information. We test this hypothesis by measuring the effect of macro surprises on the futures price bid-ask spread in high-frequency regressions. The bid-ask spread is widely recognized as a measure of market efficiency. A narrower spread suggests less uncertainty about the asset’s true value and reflects lower transaction costs, improved liquidity, and lower information asymmetry (Roll 1984). Furthermore, Chordia et al. (2008) show that the bid-ask spread is an indicator of market quality and market efficiency. Since a smaller spread is associated with a more efficient price discovery process, an increase in the quality of market information should decrease the spread. Therefore, we estimate the following equation, where the relative bid-ask spread is defined as

In equation (8),

5. Results

5.1. The Impact of Surprises on Cumulative Abnormal Returns

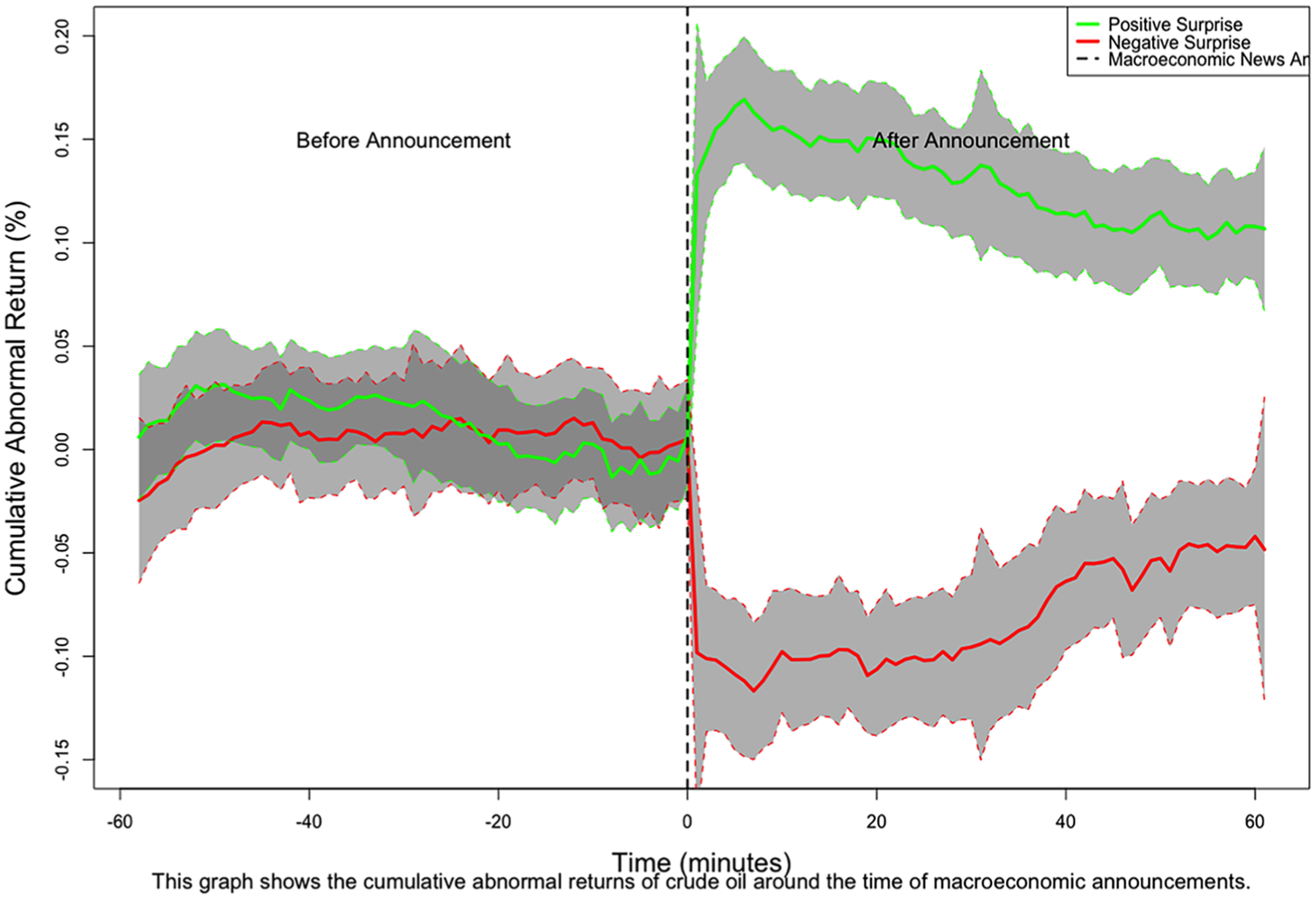

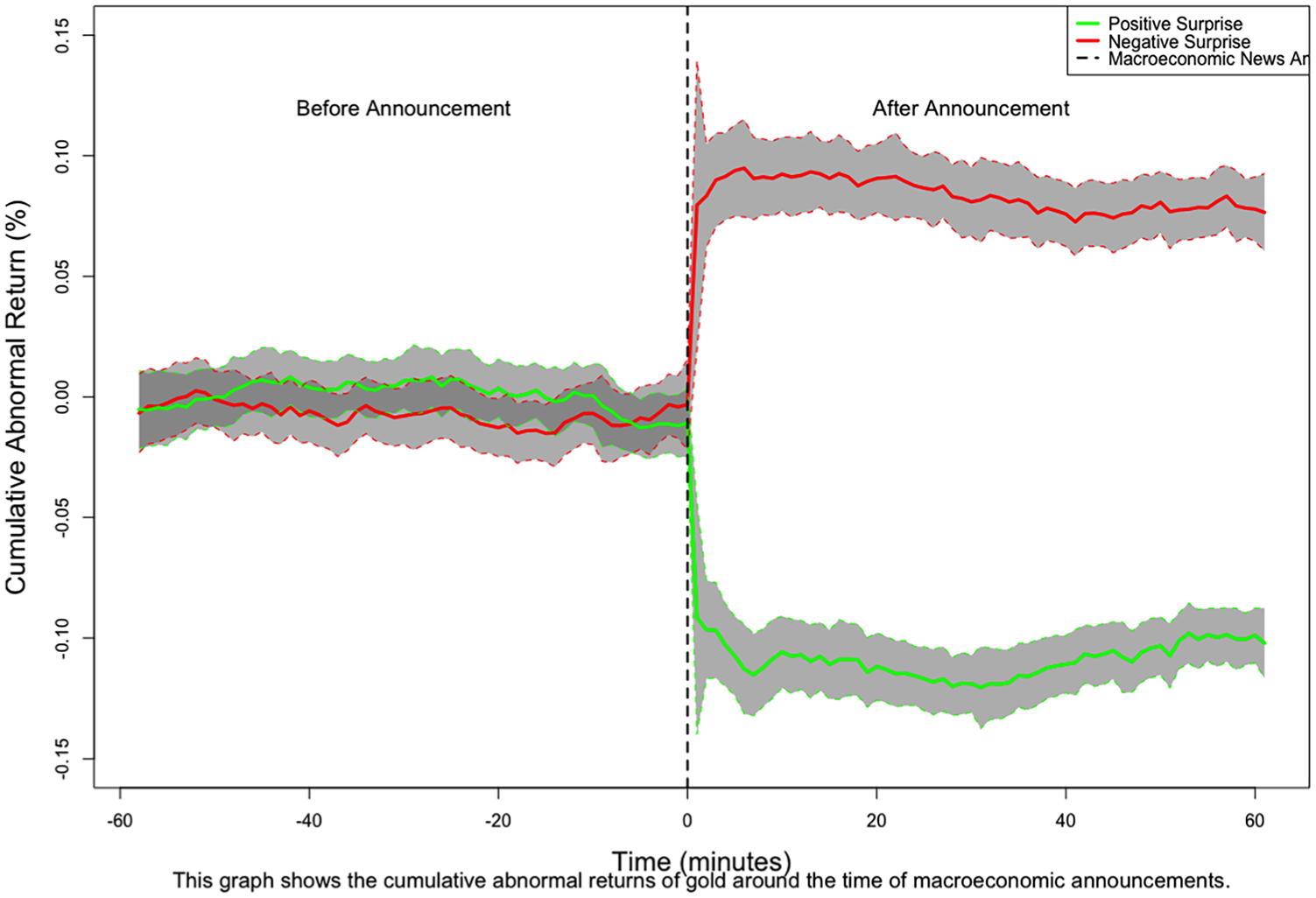

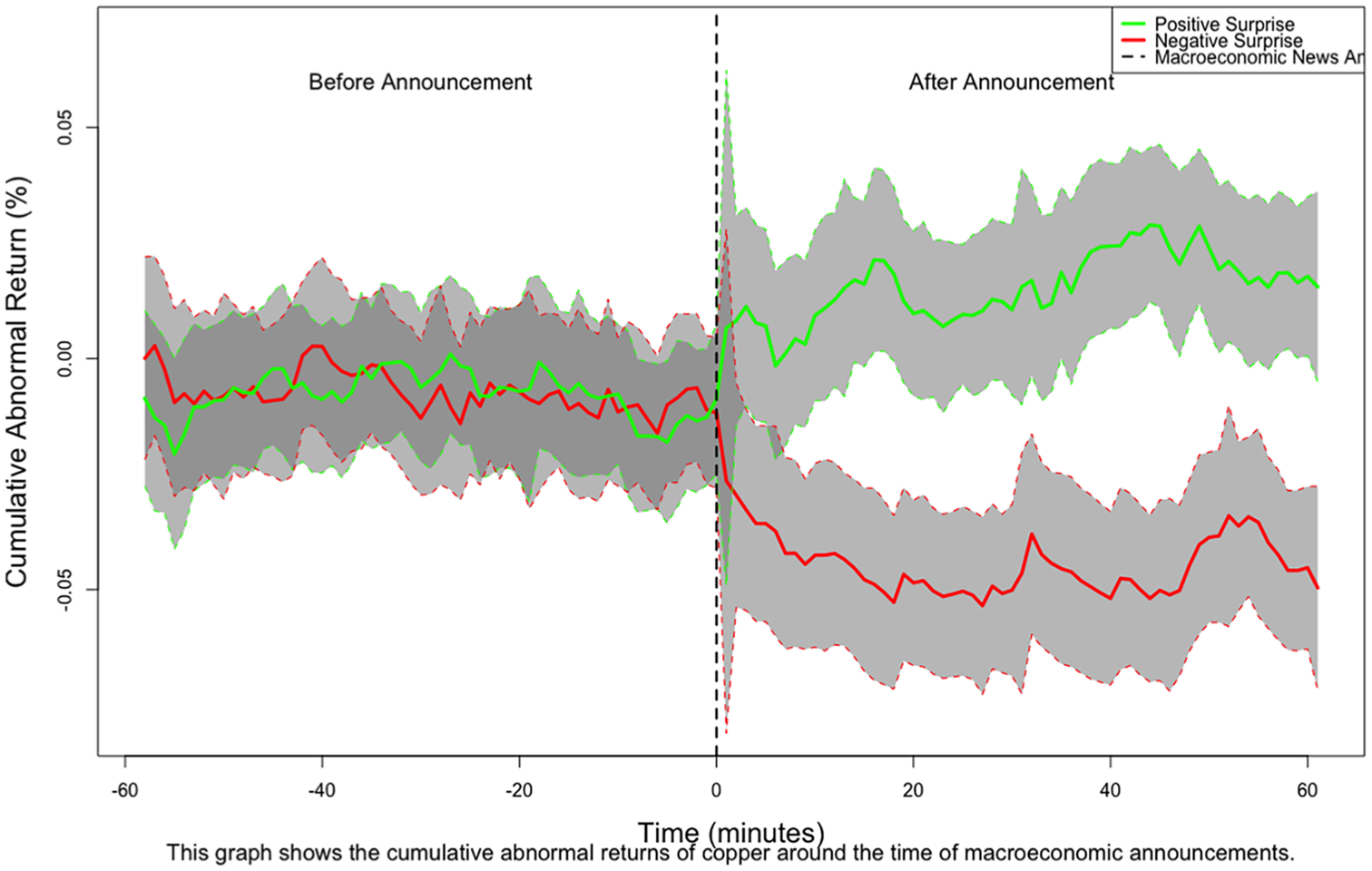

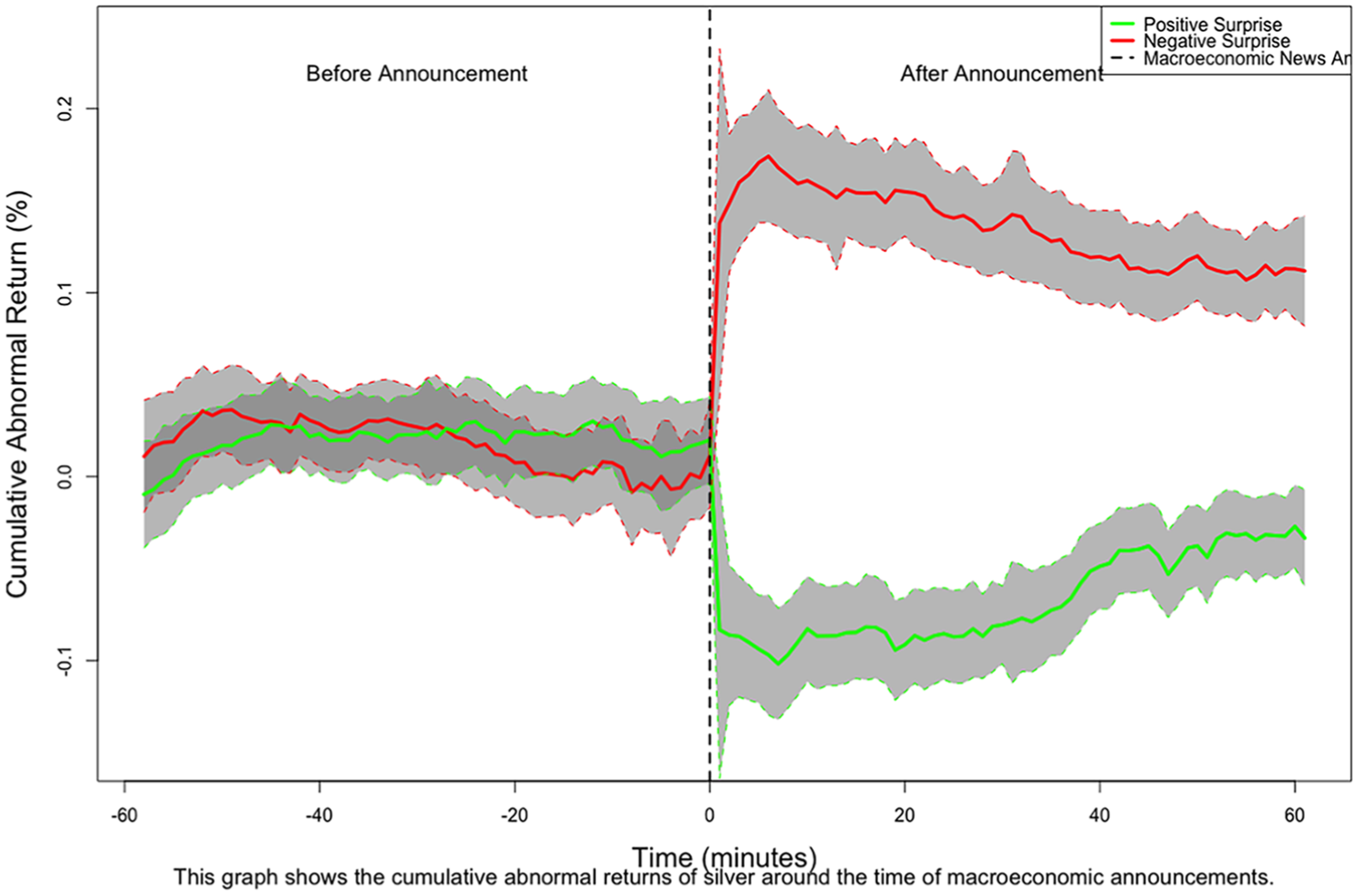

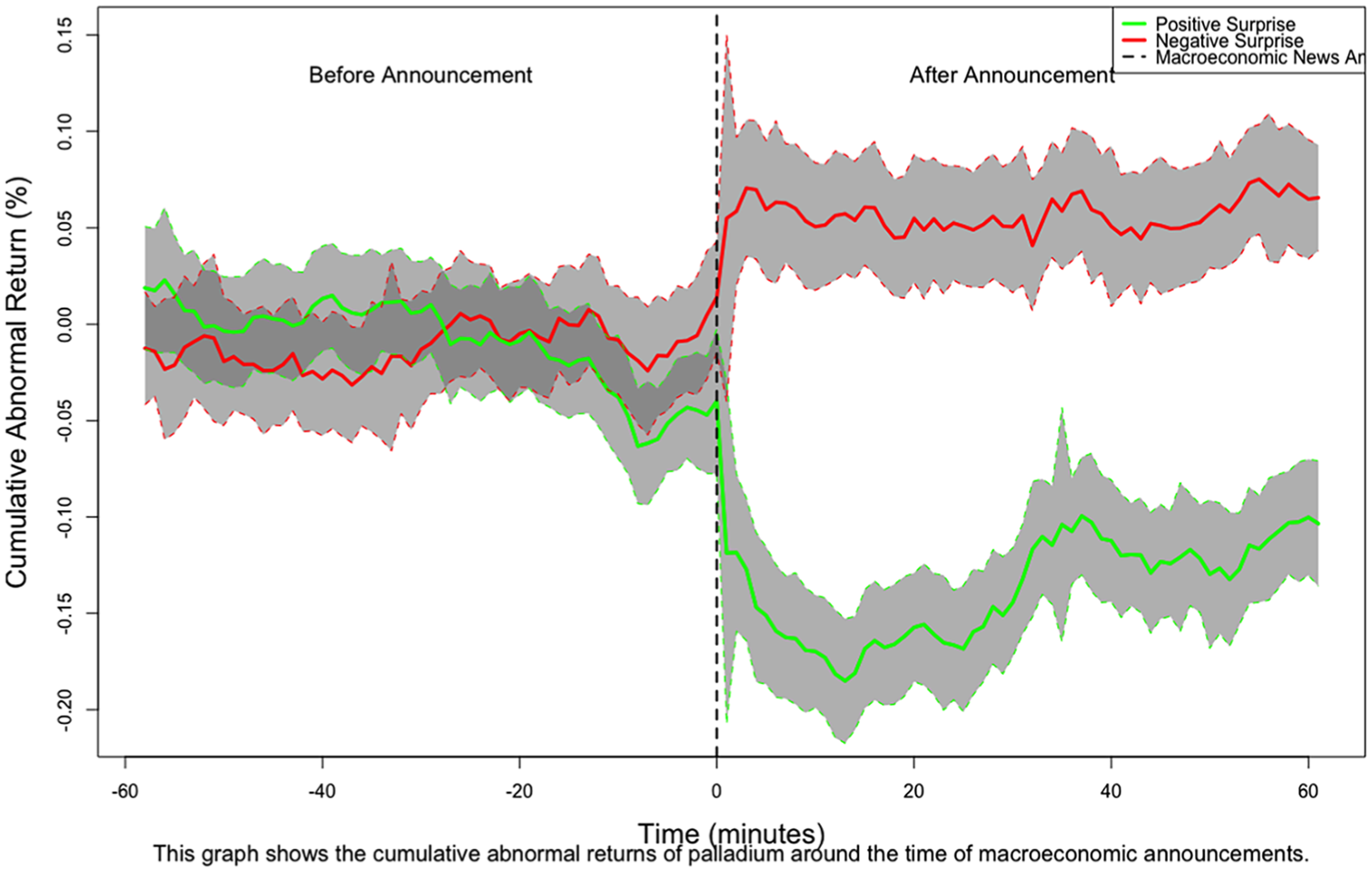

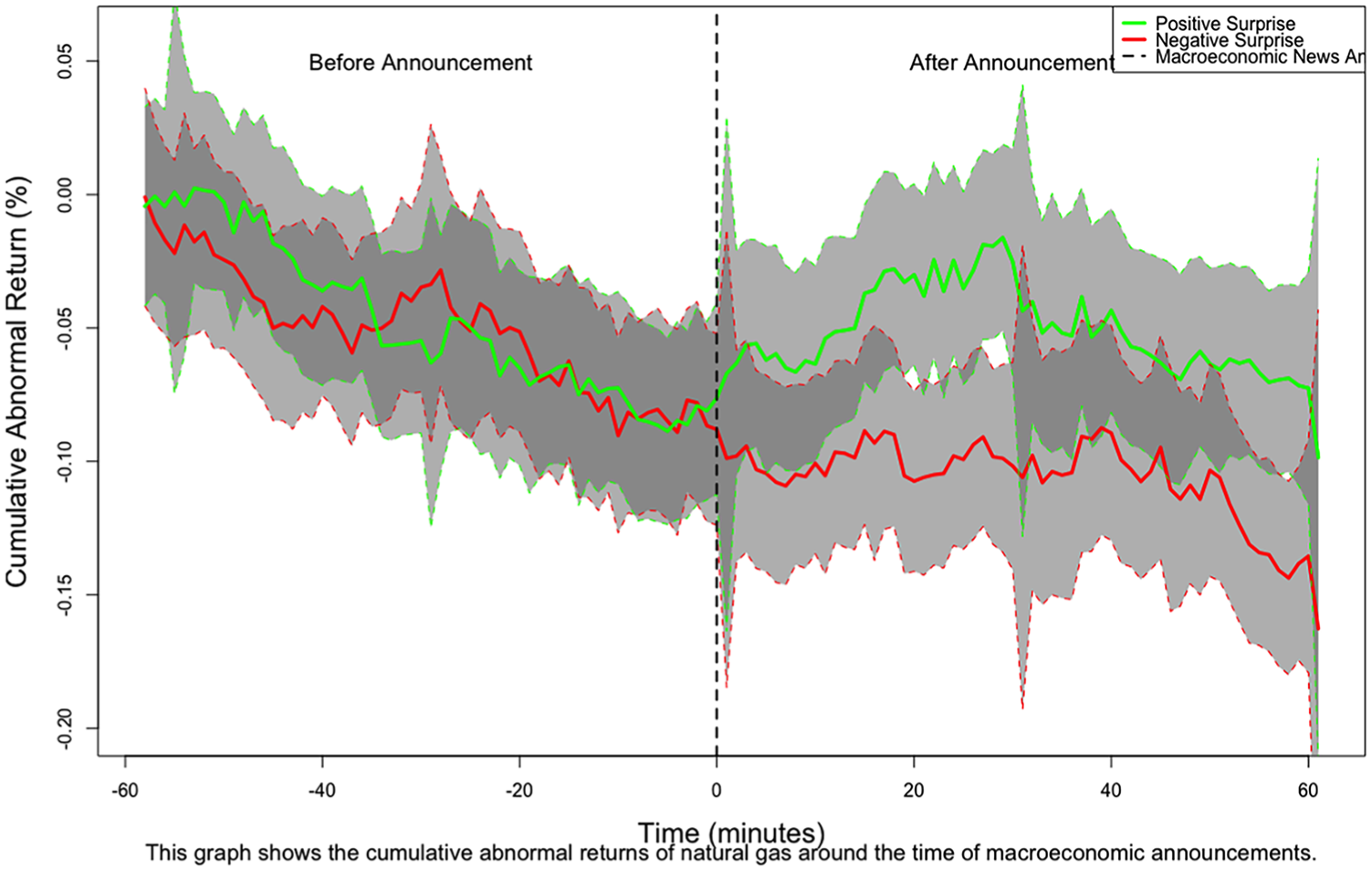

We begin by documenting the impact of macroeconomic announcement surprises on commodity futures returns. The impact of surprises is shown in the following graphs of high-frequency cumulative abnormal returns (CARs). Figures 1 to 6 show CARs for each commodity as measured over a window of sixty minutes before to sixty minutes after a macroeconomic announcement release. The figures are constructed similarly to those shown in Kurov et al. (2019). The magnitude of the CARs after announcement releases is comparable to those shown in their paper for stock index and Treasury futures. Unlike them, however, we do not see evidence of a pre-announcement drift.

Cumulative abnormal return of crude oil sixty minutes before and after macroeconomic announcements.

Cumulative abnormal return of gold sixty minutes before and after macroeconomic announcements.

Cumulative abnormal return of copper sixty minutes before and after macroeconomic announcements.

Cumulative abnormal return of silver sixty minutes before and after macroeconomic announcements.

Cumulative abnormal return of palladium sixty minutes before and after macroeconomic announcements.

Cumulative abnormal return of natural gas sixty minutes before and after macroeconomic announcements.

A red line denotes the average CAR for announcement releases that are seen as negative surprises (i.e., worse than anticipated news), while a green line denotes the average CAR for positive surprises. For brevity, we discuss only the CARs for crude oil and gold, as they are representative of pro-cyclical energy markets and safe haven assets. Figure 1 shows the average CAR for crude oil futures. The CAR increases following a positive surprise and decreases following a negative one, confirming that crude oil is a pro-cyclical commodity. In contrast, Figure 2 shows that gold futures react in the opposite manner. The red line indicates that CAR is positive after bad news, while the green line shows that CAR is negative after good news.

5.2. Macroeconomic Surprises, Speculative Trading Activity and Futures Returns

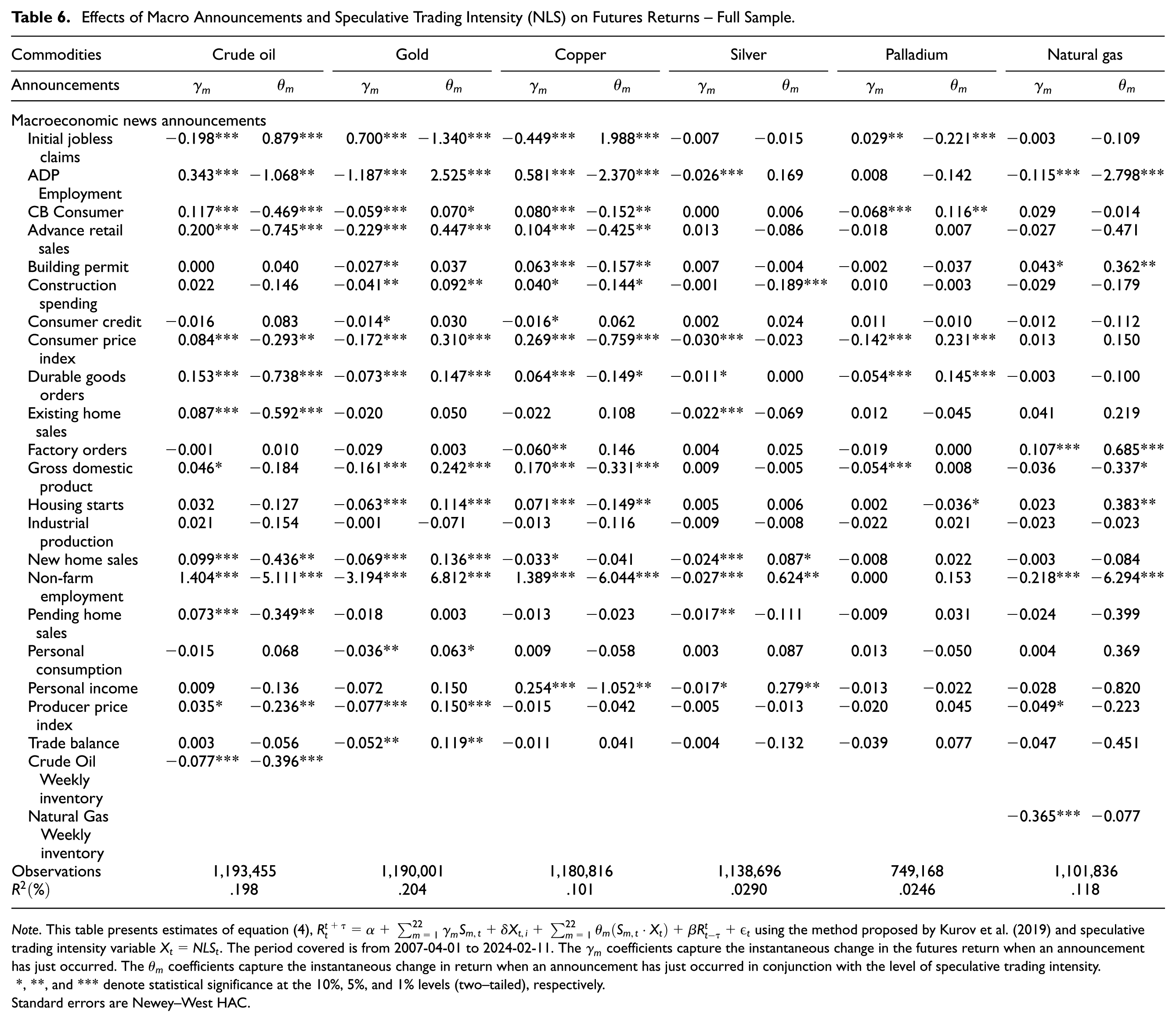

Table 6 presents the results of high-frequency regressions that explain commodity futures returns immediately after a macroeconomic announcement release. Our discussion focuses on coefficients that are statistically significant at the 5 percent level.

12

We begin with energy commodities, which serve as our baseline case. The

Effects of Macro Announcements and Speculative Trading Intensity (NLS) on Futures Returns – Full Sample.

Note. This table presents estimates of equation (4),

Effects of Macro Announcements and Speculative Trading Intensity (NLS) on Futures Conditional Variance – Full Sample.

Note. This table presents estimates of equation (7) using the speculative trading intensity variable

In the case of natural gas futures, we find that the results across announcements are less frequently significant. Increased speculative trading tends to increase the magnitude of the surprise’s effects, when the results are significant. An exception is the natural gas market-specific announcement release (inventories), for which the coefficient is negative but not significant. Overall for natural gas futures, we do not find as much support that speculative trading dampens the effect of macroeconomic announcements on returns. The reason why the results for natural gas futures are less conclusive is most likely that this futures contract displays greater volatility, that it has a lower trading volume (Irwin and Sanders 2012), and it has less speculative trading activity (thus, fewer informed traders) (Büyükşahin and Robe 2014).

Copper is a pro-cyclical, industrial commodity, so it is expected that the results for copper futures should resemble those for crude oil. The results are highly significant for many announcements. If we look at announcements such as ADP Employment and CB Consumer Confidence, which are “good news,” the

Gold is considered to be a safe haven asset (Baur and Lucey 2010). Therefore, it is expected that the reaction of gold futures returns to macro surprises will be the opposite to what we have found for crude oil, natural gas, and copper. This is indeed what we find: gold futures returns are lower after “good news” and higher after “bad news.” These results support the idea that energy commodities are pro-cyclical, while gold is a safe haven asset. In particular, the positive

The last two commodities in our sample, silver and palladium futures, behave more like gold futures. We find that for Initial Jobless Claims for palladium and ADP Employment in silver, significant

5.3. Macroeconomic Surprises, Speculative Trading, and Volatility

Table 7 presents regression results to explain the conditional variance of high-frequency commodity futures returns after macroeconomic announcements. We first examine our baseline assets, energy commodities, as volatility in energy markets is of particular concern given their economic importance and direct impact on consumer prices. For crude oil, macroeconomic surprises generally lead to an increase in conditional variance, as the

Comparing these results with those for other commodities, we find that gold, copper, silver, and palladium also show positive

Therefore, our findings highlight the valuable role of speculative traders in reducing volatility, particularly in crude oil futures markets, where price stability has important implications for the broader economy. While macroeconomic news tends to increase volatility across commodity markets, the damping effect of speculative trading appears strongest in energy markets. We show that this relationship is consistent across different types of announcements and remains robust when controlling for various market conditions.

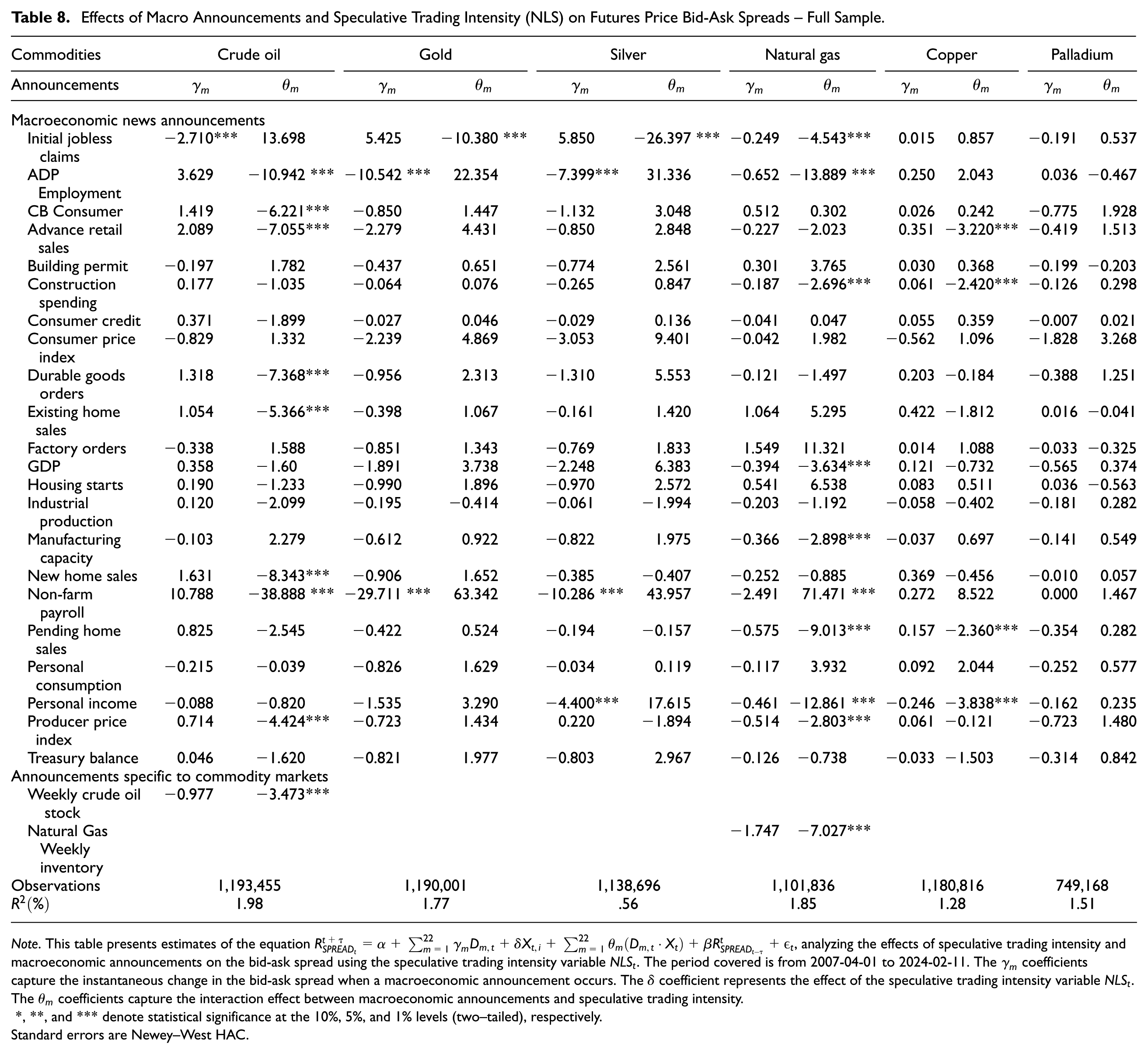

5.4. Macroeconomic Surprises, Speculation, and Bid-Ask Spreads

Table 8 shows our results for the impact of macroeconomic surprises and speculative trading intensity on futures prices bid-ask spreads. This empirical analysis provides a test of informational efficiency. We first focus on energy markets. In the bid-ask spread regressions, the

Effects of Macro Announcements and Speculative Trading Intensity (NLS) on Futures Price Bid-Ask Spreads – Full Sample.

Note. This table presents estimates of the equation

Comparing these results to those obtained for the other commodities in our sample, we find that the results for

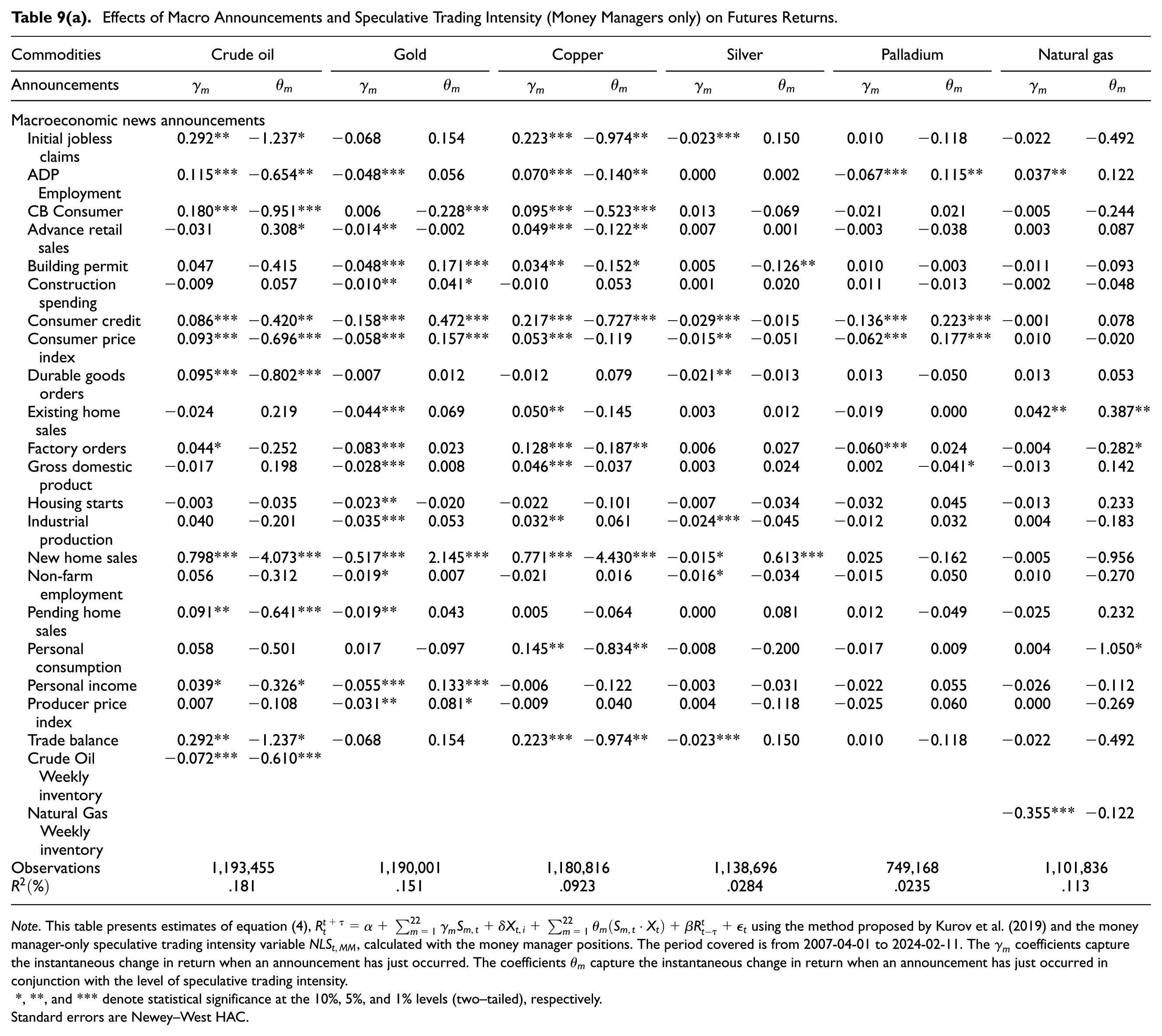

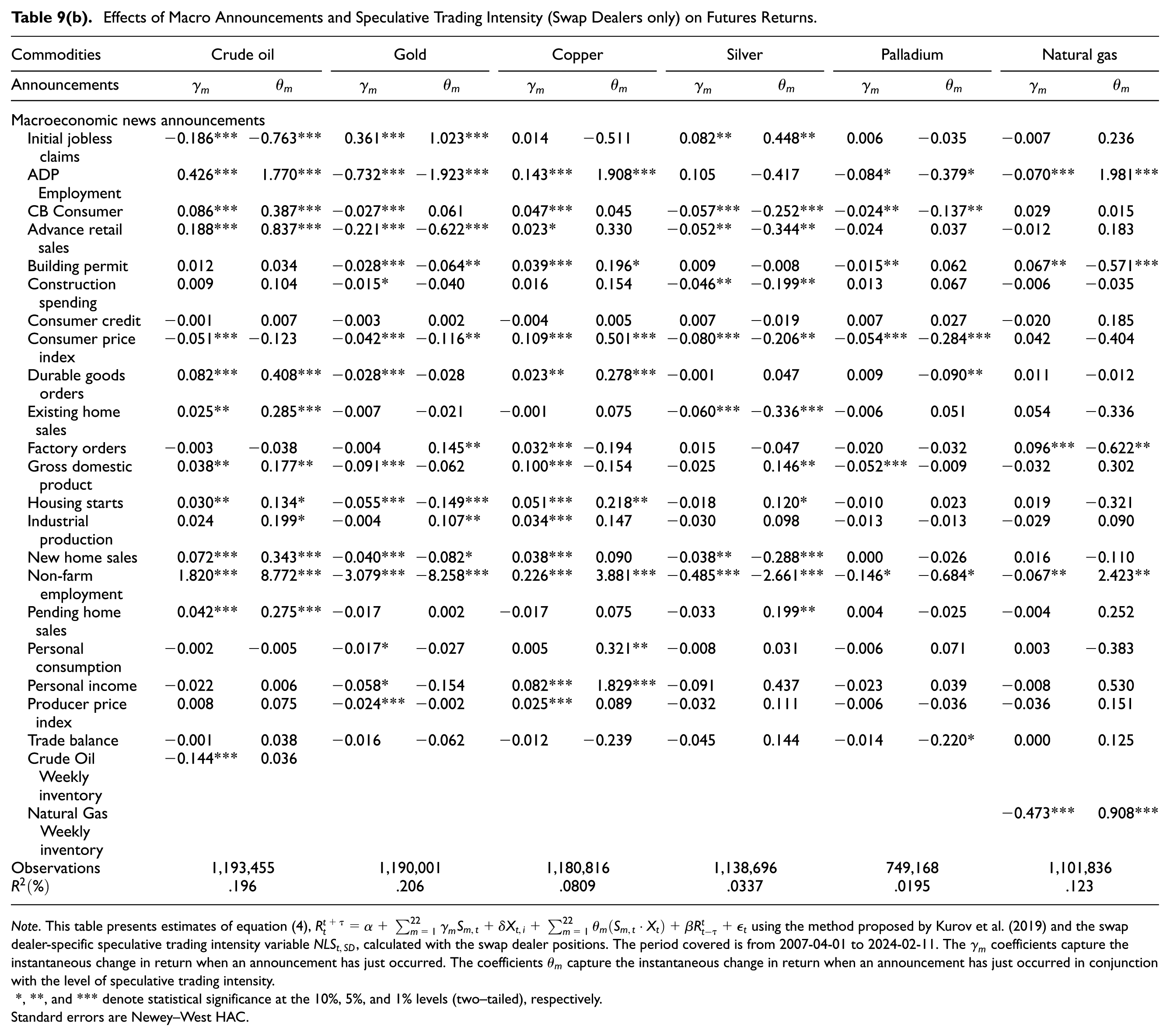

5.5. Differences in Results According to Trader Type

To investigate whether differences in trader type are relevant in explaining our findings, we provide disaggregated results in this section. To this end, we estimate equations (6) to (8) for two categories of Non-Commercial traders, namely, swap dealers (SD) and money managers (MM). For each of the two, the CFTC reports the number of long and short positions in their disaggregated Commitment of Traders (COT) reports. We compute the NLS index for each trader category over time, allowing us to separately quantify the intensity of trading activity by money managers and swap dealers.

First, we examine the returns equation for money manager positions, as shown in Table 9(a). Increased trading activity by money managers has the same effect as in our baseline results. If we consider crude oil futures, for example, the

Effects of Macro Announcements and Speculative Trading Intensity (Money Managers only) on Futures Returns.

Note. This table presents estimates of equation (4),

Effects of Macro Announcements and Speculative Trading Intensity (Swap Dealers only) on Futures Returns.

Note. This table presents estimates of equation (4),

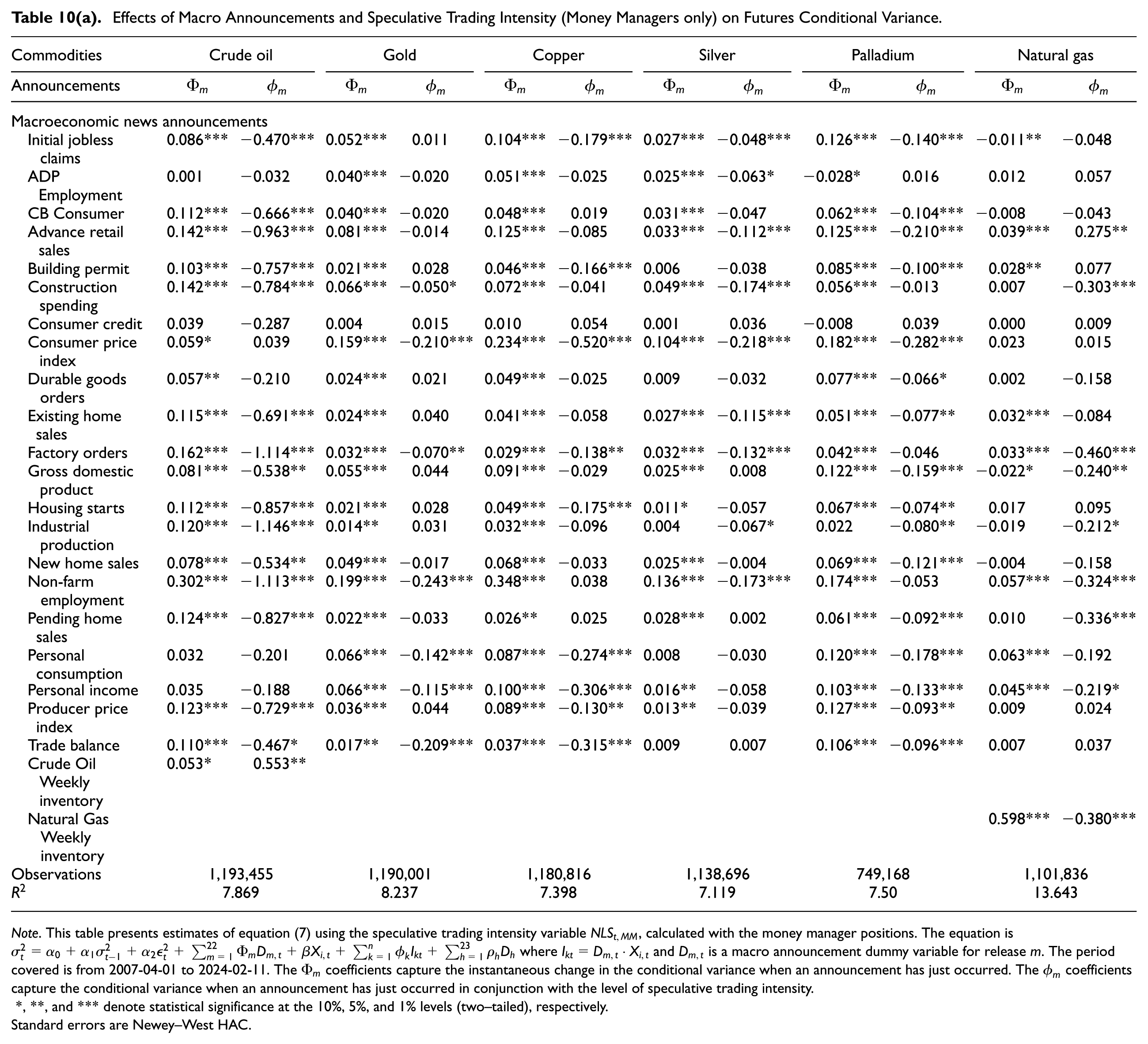

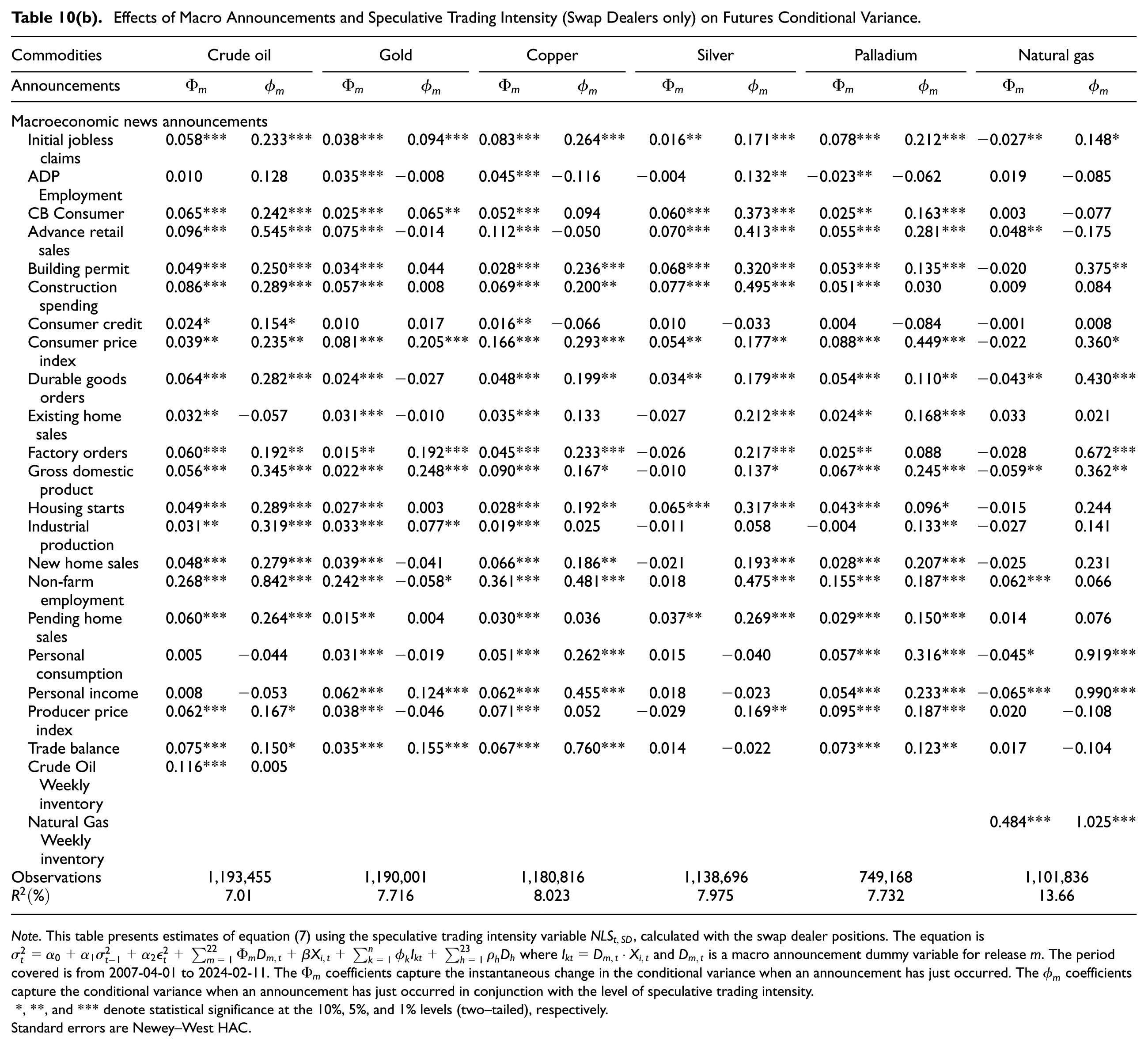

Table 10(a) and 10(b) show our disaggregated results for the variance equation using sample data for money managers and swap dealers, respectively. The money manager results are similar to what we find in the aggregate sample, namely that both good and bad surprises increase volatility (as shown by

Effects of Macro Announcements and Speculative Trading Intensity (Money Managers only) on Futures Conditional Variance.

Note. This table presents estimates of equation (7) using the speculative trading intensity variable

Effects of Macro Announcements and Speculative Trading Intensity (Swap Dealers only) on Futures Conditional Variance.

Note. This table presents estimates of equation (7) using the speculative trading intensity variable

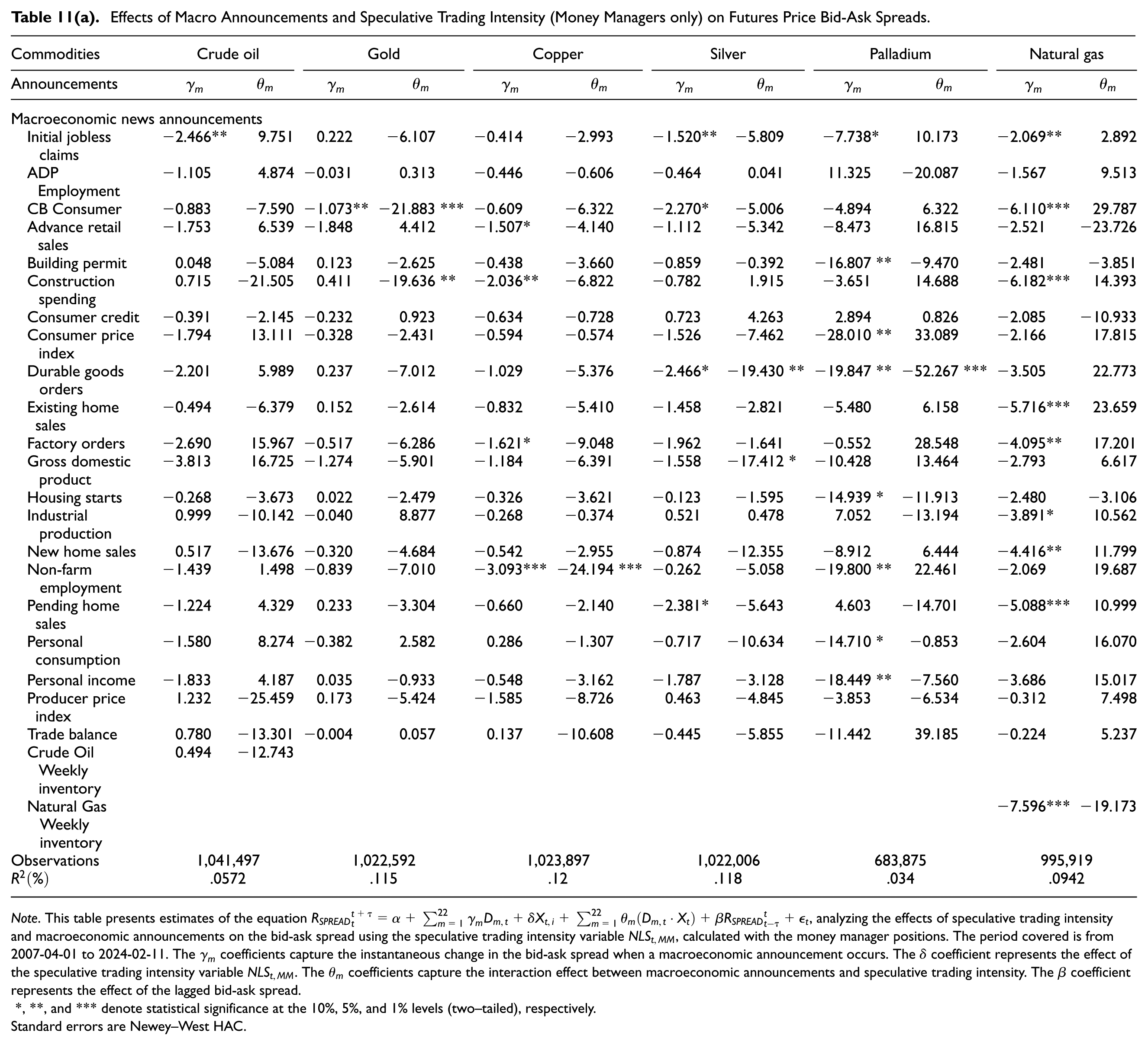

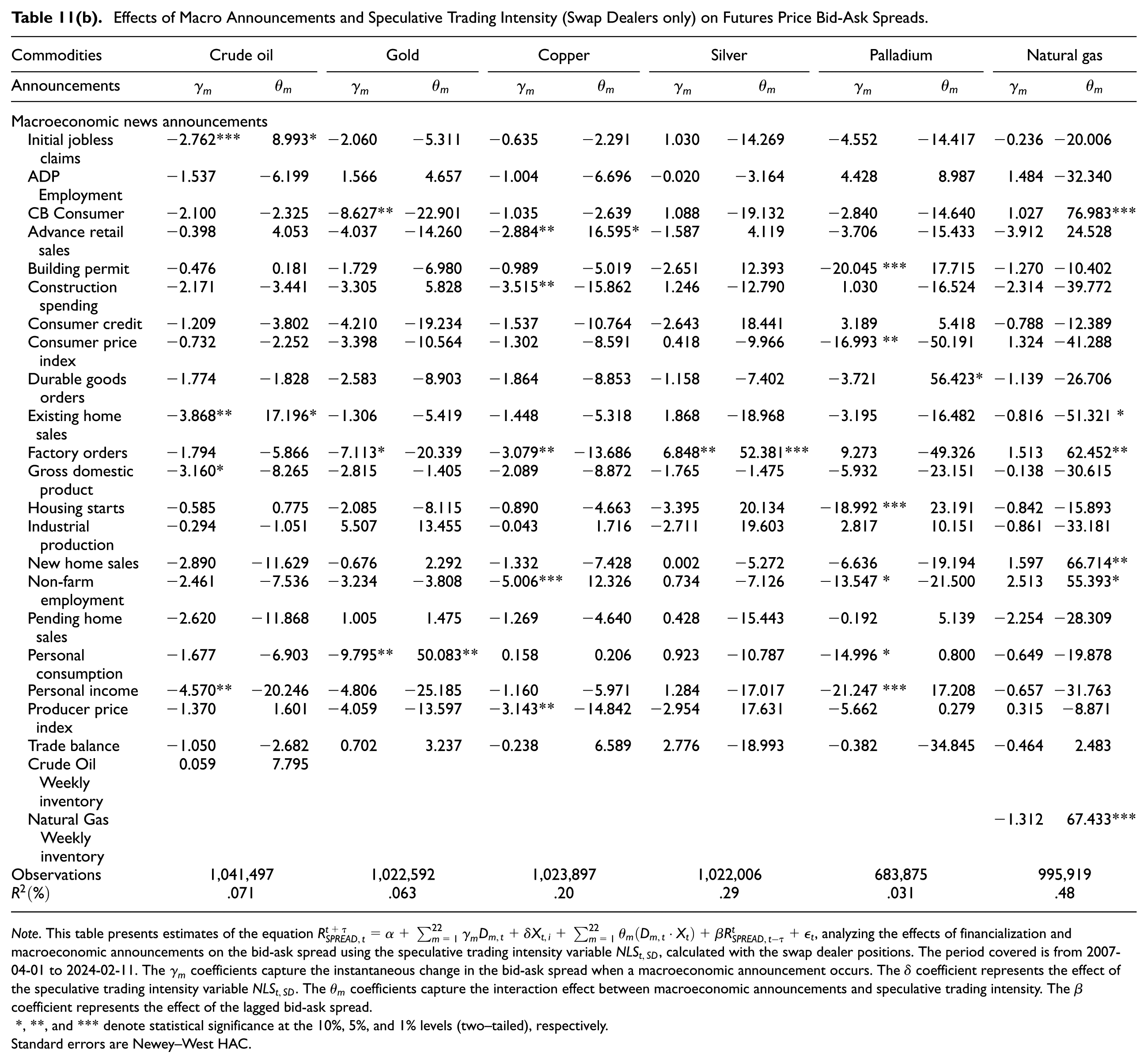

Lastly, we examine whether the effects on bid-ask spreads differ between trader types. Table 11(a) presents the results for money managers. As the

Effects of Macro Announcements and Speculative Trading Intensity (Money Managers only) on Futures Price Bid-Ask Spreads.

Note. This table presents estimates of the equation

Effects of Macro Announcements and Speculative Trading Intensity (Swap Dealers only) on Futures Price Bid-Ask Spreads.

Note. This table presents estimates of the equation

6. Discussion and Implications

Our findings contribute new insights to an unsettled literature on the impact of different types of financial participants in energy and commodity markets (Ready and Ready 2022). In addition to being an important alternative asset class, energy commodities are central to economic activity, while energy futures trading is important for price stability. Being closely related to macroeconomic risk (Cheng et al. 2015), energy commodities therefore play a key role in macro-finance. By taking a novel angle of high-frequency market reactions to macroeconomic surprises, our results contribute a more nuanced picture of the impact of speculative trading and help to reconcile previous findings in the literature.

Goldstein and Yang (2022) develop a theoretical model to examine how financial traders improve information transmission between futures and spot markets. They show how market efficiency should benefit from the presence of informed financial traders, whose actions lead to increases in pricing transparency and to lower information asymmetry. Our empirical results provide support for this model. We show that increased speculative trading activity lowers bid-ask spreads after a macro news release, in addition to reducing the magnitude of price and volatility reactions to macro surprises. This improvement in informational efficiency is especially valuable in energy markets, where price discovery has direct implications for industrial users and consumers. We find that this effect is driven by money managers. In addition, our results point to smaller, negative effects linked to swap dealers. The difference between the two sets of disaggregated empirical results can be explained by the fact that they trade for different purposes. Money managers aim to make a profit based on information, while swap dealers are intermediaries who, while perhaps informed, primarily provide services to customers such as institutional investors, in addition to hedging their swap positions. In line with this interpretation, our results also build on Fishe and Smith (2012), who show that some financial traders (e.g., money managers) are better informed than others in commodity markets.

Our findings also extend and build on the results of an earlier empirical literature that uses daily-level data. This literature includes Brunetti et al. (2016) who find that speculative traders, especially money managers and hedge funds, are helpful to energy and commodity markets, as well as Büyükşahin and Harris (2011) and Alquist and Gervais (2013) who show that the futures positions of financial firms such as hedge funds do not predict next-day changes in crude oil prices. Moreover, our results relate to Cheng et al. (2015) who show that financial investors, being better informed about markets, contribute to price discovery and liquidity. The key message is therefore that speculative trading is helpful to markets by distributing and assimilating new information into prices. The findings shown in this paper have important implications for energy markets regulation and policy. First, they suggest that attempts to limit speculative trading in energy markets could, in fact, increase price volatility and reduce informational efficiency and price discovery. Second, they indicate that different types of financial participants have distinct effects on market quality, suggesting that regulatory frameworks should pay careful attention to market composition. Third, they highlight the importance of maintaining a robust price discovery mechanism in energy markets, given their crucial role in the economy.

7. Conclusion

This paper investigates the impact of speculative trading on the real economy and energy markets through a new angle, namely high-frequency surprises in macroeconomic announcement releases, which allows for better-identified effects. We empirically test whether increased speculative trading activity amplifies or dampens the impact of macro surprises on prices and volatility in commodity futures markets. Our results suggest that increased speculative trading activity has beneficial effects for energy and commodity markets. This is accomplished by reducing volatility and improving price discovery, as indeed price stability and efficient price discovery are crucial for market participants and the broader economy. We find that a greater intensity of speculative trading does not amplify the effects of macro announcement surprises on prices or volatility. On the contrary, an increase in speculative trading in a given commodity has a damping effect: prices and volatility react less to macro surprises when speculative trading is higher. This stabilizing effect of speculation is especially valuable to energy markets, where price volatility can have significant economic consequences.

What is more, our findings are consistent with information diffusion economic arguments. Our analysis of bid-ask spreads in futures contracts further confirms that speculative trading tends to improve market efficiency. Our results show that these effects are mostly linked to the trading activities of money managers rather than swap dealers. Thus, we contribute to a literature that emphasizes how non-commercial market participants such as money managers are beneficial to commodity markets by supplying liquidity, reducing volatility, and generally improving market efficiency. This finding is particularly relevant for energy markets, which have seen substantial increases in trading volume and complexity.

Our findings have important implications for energy market regulation and policy. The damping effect on volatility shocks documented in this paper implies that speculative traders contribute to market stability, which is essential for energy security and economic planning. This stability could also facilitate investment in energy infrastructure and support the ongoing energy transition. By lowering the magnitude of volatility shocks, and thus reducing the real option value of delaying investments, our findings suggest that a greater involvement by speculative traders may also help with sustainability efforts to finance a green energy transition, alongside other instruments such as green bonds and portfolio screens for sustainable investments. Looking forward, our results suggest several promising avenues for future research in energy markets. First, the role of financial investors (speculators as well as passive investors) in facilitating the energy transition warrants further investigation. Second, the connection between speculative trading and energy market regulation remains an important area for study, given that we find different impacts for money managers and swap dealers. Finally, the impact on energy price discovery of new trading technologies and market participants is an emerging research frontier. These questions are particularly relevant given the increasing importance of energy markets in addressing climate uncertainty and in ensuring economic stability.

Supplemental Material

sj-pdf-1-enj-10.1177_01956574251369707 – Supplemental material for Speculative Trading in Energy Markets: Evidence from Macroeconomic Surprises

Supplemental material, sj-pdf-1-enj-10.1177_01956574251369707 for Speculative Trading in Energy Markets: Evidence from Macroeconomic Surprises by Simon-Pierre Boucher, Marie-Hélène Gagnon and Gabriel J. Power in The Energy Journal

Supplemental Material

sj-pdf-2-enj-10.1177_01956574251369707 – Supplemental material for Speculative Trading in Energy Markets: Evidence from Macroeconomic Surprises

Supplemental material, sj-pdf-2-enj-10.1177_01956574251369707 for Speculative Trading in Energy Markets: Evidence from Macroeconomic Surprises by Simon-Pierre Boucher, Marie-Hélène Gagnon and Gabriel J. Power in The Energy Journal

Supplemental Material

sj-pdf-3-enj-10.1177_01956574251369707 – Supplemental material for Speculative Trading in Energy Markets: Evidence from Macroeconomic Surprises

Supplemental material, sj-pdf-3-enj-10.1177_01956574251369707 for Speculative Trading in Energy Markets: Evidence from Macroeconomic Surprises by Simon-Pierre Boucher, Marie-Hélène Gagnon and Gabriel J. Power in The Energy Journal

Footnotes

Acknowledgements

The authors thank participants at seminars at Humboldt University Berlin, South Dakota State University (Ness School), University of Illinois, Urbana-Champaign (ACE), and at meetings of the Commodity & Energy Markets Association (2021),World Finance & Banking Association (2021), Société canadienne de sciences économiques (2022), 4th Ethical Finance and Sustainability (EFS) conference (2022), and Multinational Finance Society (2022). The authors also thank the editor George Filis, two anonymous referees, as well as Jocelyn Grira, Joseph Marks, Alessandro Melone (discussants) and Scott Irwin, Michel Robe, and Zhiguang Wang.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: For financial support, the authors thank the Social Sciences and Humanities Research Council and the Chaire Industrielle-Alliance Groupe financier. Any remaining errors are ours alone.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

1

Sources: The Financial Times, Bloomberg, S&P Global and Euronews.

2

A high-profile example is Masters (2009), who testified before the U.S. Congress in 2008 and before the CFTC in 2009 about “Ending excessive speculation in commodity markets.” While his argument is not supported by empirical evidence, as shown by ![]() , the Masters hypothesis reflects beliefs held at the time by many market participants.

, the Masters hypothesis reflects beliefs held at the time by many market participants.

3

There are a few issues with the OPEC announcements: First, they are not released at a specific time. Second, it is impossible to know precisely when a given OPEC announcement was made available to investors. Third, OPEC’s influence has weakened since the 1980s.

4

The literature argues that measuring

6

7

The CFTC defines commercial traders as participants in commodity markets who primarily use futures contracts to hedge their business activities (e.g., buying or selling commodities). All traders who are not classified as Commercial are automatically classified as Non-Commercial traders. To obtain the number of long positions held by Non-Commercial traders, we subtract the total long Commercial positions from the total open interest. For the number of short positions held by Non-Commercial traders, we subtract the total short Commercial Positions from the total open interest.

8

In an earlier draft, we also reported results based on two alternative proxies as well as a proxy constructed using principal component analysis. The alternative proxies are Working’s ![]() ). These results, which are available upon request, are consistent with our main findings and do not change the paper’s implications.

). These results, which are available upon request, are consistent with our main findings and do not change the paper’s implications.

10

This category is also called “Managed money.” The CFTC writes that they are “registered commodity trading advisor (CTA); a registered commodity pool operator (CPO); or an unregistered fund identified by CFTC.” There is some overlap between Money managers and hedge funds, but they are distinct.

11

12

In an earlier draft, we also reported results for different sub-periods, such as the Zero Lower Bound period, the 2008 to 2010 financial crisis and Great Recession, and the COVID-19 period. These results do not materially affect our findings or conclusions, and they are available upon request.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.