Abstract

We extend beyond conventional mean-to-mean effects to examine how fundamental variables impact the entire distribution of electricity spot prices in the Australian National Electricity Market. Employing quantile regression models, we demonstrate that variable renewable energy (VRE) generation effectively lowers spot prices at lower quantiles when electricity is relatively inexpensive. However, its role in reducing prices is marginal or negligible at higher quantiles when electricity becomes more costly. High gas prices persist as a significant market challenge, with marginal increases causing price surges at the tails of the price distribution. Analysis of the 2022 energy crisis shows the limited capability of VRE and interconnectors to counteract high gas and coal prices, along with opportunistic hydro generators. The findings underscore the need for policies promoting further renewable energy adoption, a reassessment of the role of gas generation, and strategies to enhance energy market resilience.

Keywords

1. Introduction

The energy industry in Australia is experiencing a seismic shift as traditional coal-fired power plants near the end of their operational life and give way to significant investment in variable renewable energy (VRE) projects. This transition is unfolding at an unprecedented rate, with over half of the investment commitments in the National Electricity Market’s (NEM) history, amounting to 31,487 MW, taking place from 2016 to 2021. This represents approximately 51% (15,939 MW) of the total commitments (Gilmore et al. 2024; Simshauser and Gilmore 2020, 2022). As the NEM transitions, instances of both extremely high and low prices have increasingly become a common feature of the market (Mwampashi et al. 2021; Rai and Nunn 2020). Thus, comprehending the influence of price fundamentals on the distribution of spot prices is important to energy stakeholders in understanding how the ongoing transition from fossil fuels to renewables shapes not only the averages but also the extremes of electricity prices. For generators, for instance, extremely low prices can threaten their profitability, while for retailers and consumers, price spikes can lead to significant financial strain. By understanding the extremes of price distribution, generators can better strategize for these impactful events. For those engaging in trading or hedging activities, understanding the price distribution and potential extremes is key for assessing price risk and developing hedging strategies.

This study assesses the impact of electricity price fundamentals on the distribution of spot prices in the NEM. We consider several key drivers of spot prices across five NEM regional markets: VRE generation, hydro generation, electricity demand, fossil-fuel prices, and interconnector flows. We employ the quantile regression model introduced by Koenker and Bassett (1978) to scrutinize the sensitivity of price distribution to its determinants across various quantiles. Quantile regression can capture the quantile-specific dynamics and heterogeneity in the data, making it a more robust method for modeling the complex and dynamic behavior of electricity prices, and allowing direct assessment of the risks faced by consumers or producers of electricity.

We find that the impact of wind and solar generation on electricity prices varies across price distributions and states. Our findings show that in most states an increase in VRE (wind and solar) generation primarily leads to substantial decrease in electricity prices when electricity is relatively cheap (low quantiles). However, when electricity is comparatively expensive (high quantiles), the increase in VRE typically plays a marginal/no role in reducing electricity prices, with the notable exception of South Australia, a state characterized by high VRE penetration.

The impact of gas generation on electricity prices is more noticeable in the lower and intermediate quantiles (when electricity is relatively inexpensive) in New South Wales and Queensland. This effect diminishes with the quantiles. Conversely, in Victoria and South Australia, a rise in gas prices significantly impacts the highest quantiles (when electricity is costly). While the integration of VRE sources has led to a decline in the role of gas-fired power generation in setting spot prices, their impact on electricity pricing remains significant. For example, between 2014 and 2021, gas-fired generators accounted for a mere 12% of total power generation, yet their direct and indirect influence affected electricity prices for approximately 75% of overall energy production (Boston Consulting Group, 2022).

We also find that an increase in hydro generation (which usually sets bid prices slightly below those of price-setting gas generators) exerts relatively lower positive pressure on spot prices at the lower quantiles and stronger positive pressure on the higher quantiles. An increase in electricity demand affects the extremes of the electricity price distribution more than the intermediate quantiles.

In our comparative analysis of the factors influencing electricity prices, we find that gas prices remain the most dominant. At the lower quantiles, the negative effect of wind and solar generation exceeds the positive effect of gas prices; however, this effect reverses at higher quartiles. Regarding the magnitude of the positive impact from fundamental factors, gas prices and electricity demand take the lead, followed by hydro generation. Consequently, the combined positive effect of these variables outweighs the negative impact of VRE and, where relevant, the negative pressure from interconnector flows.

Furthermore, we investigate the impact of a recent shock to the NEM, which resulted from soaring coal and gas prices—driven by substantial supply disruptions in international markets due to Russia’s invasion of Ukraine and ultimately triggering an unprecedented nine-day suspension of the NEM in June 2022. We demonstrate that gas prices have a significant impact on spot prices during the energy crisis period, particularly in the lowest and intermediate quantiles. However, the magnitude of the impact is considerably larger than the average effects observed over the entire sample period. The influence of VRE generation, which could help ease upward pressure on electricity prices, is relatively small in comparison. However, in South Australia, an increase in VRE generation during the energy crisis period exerts significant downward pressure across all quantiles. We observe that this effect is generally greater than the positive pressure resulting from high gas prices.

Our study contributes to the literature in several dimensions. First, we present the first empirical analysis that examines the variation in the impact of fundamental variables across the distribution of electricity prices in the NEM. This complements earlier studies that primarily centered on the mean of electricity prices (Abban and Hasan 2021; Csereklyei et al. 2019; Mwampashi et al. 2021; Mwampashi et al. 2022). Furthermore, we investigate how fundamental variables influence price distribution amid the 2022 energy crisis. In doing so, we augment recent research, such as Nelson et al. (2023) and Simshauser (2023), that leverages this crisis to shape energy policies in Australia. Second, using consistent units of measurement for all variables allows for comparisons of the magnitude of their impact on spot prices within and across states. Previous studies in the NEM, such as Csereklyei et al. (2019), Mwampashi et al. (2021), Abban and Hasan (2021), and Mwampashi et al. (2022) run their analysis with predictor variables expressed in different units, for instance, gas prices (A$/GJ) and generation variables (MWh or GWh). Such measurement unit inconsistencies limit comparison analysis to determine the key factor(s) driving the dynamics of electricity prices in the NEM. Finally, the study supplements research such as Westgaard et al. (2021) and Hagfors et al. (2016) by rationalizing the counterintuitive effects observed therein. For instance, Westgaard et al. (2021) find that certain variables such as VRE, load, and gas and greenhouse gas (GHG) allowance price exhibit both negative and positive impacts on electricity prices, the phenomenon described in their analysis as both “hard” and “perplexing” to interpret. Our analysis aims to elucidate the reasons behind these mixed effects, focusing on the counterintuitive effects.

Our research highlights key policy implications for the energy sector, emphasizing the need for a balanced energy portfolio in the NEM that integrates cost-effective, fuel-efficient, and flexible technologies to complement VRE generation sources. Our findings show the significant impact of gas prices on increasing electricity prices, suggesting that these prices are likely to remain high and volatile. It is therefore important to develop a diverse and cost-effective energy infrastructure that incorporates short- and long-duration energy storage, as well as zero-emission fuel turbines, to ensure the affordability of electricity for consumers (Nelson et al. 2023). Moreover, the analysis of the 2022 energy crisis demonstrated that despite the substantial growth of renewables in recent years, they were insufficient to counteract the high prices resulting from reduced fossil fuel generation. This underscores the need for comprehensive regulatory frameworks and robust energy security measures to prevent future disruptions in the NEM. Policymakers and regulators must ensure sufficient available supply, timely development of renewable generation, and firming capacity as coal plants become uneconomical to operate and VRE generation continues to grow. Investing in new firming technologies and guaranteeing replacement capacity to secure the NEM’s energy supply are essential steps toward achieving long-term energy security through the accelerated uptake of energy efficiency, renewables, and low-emission fuels.

The paper is organized as follows. Section 2 details the data and model, while Section 3 discusses the effects of electricity price fundamentals on electricity price distribution. Section 4 examines the impact of the 2022 energy crisis on price distribution, and Section 5 presents concluding remarks and policy implications.

2. Data and Methods

2.1. Data and Preliminary Analysis

We analyze the five NEM regional market jurisdictions of NSW, QLD, SA, TAS, and VIC over a sample period of twelve years from 1st January 2011 to 31st December 2022. We use thirty-minute intraday data from a combination of sources: five-minute wholesale electricity spot prices (A$/MWh), supply and demand (MW), and availability (MW) data 1 from the NEM via NEOpoint, gas price (A$/GJ) data for NSW, SA, and VIC from the Short-term Trading Market (STTM), four-hour gas price data for VIC from the Declared Wholesale Gas Market (DWGM), and Australia’s ($) monthly coal price data from the World Bank (AEMO 2023a, 2023b; NEOpoint 2023; World Bank 2023).

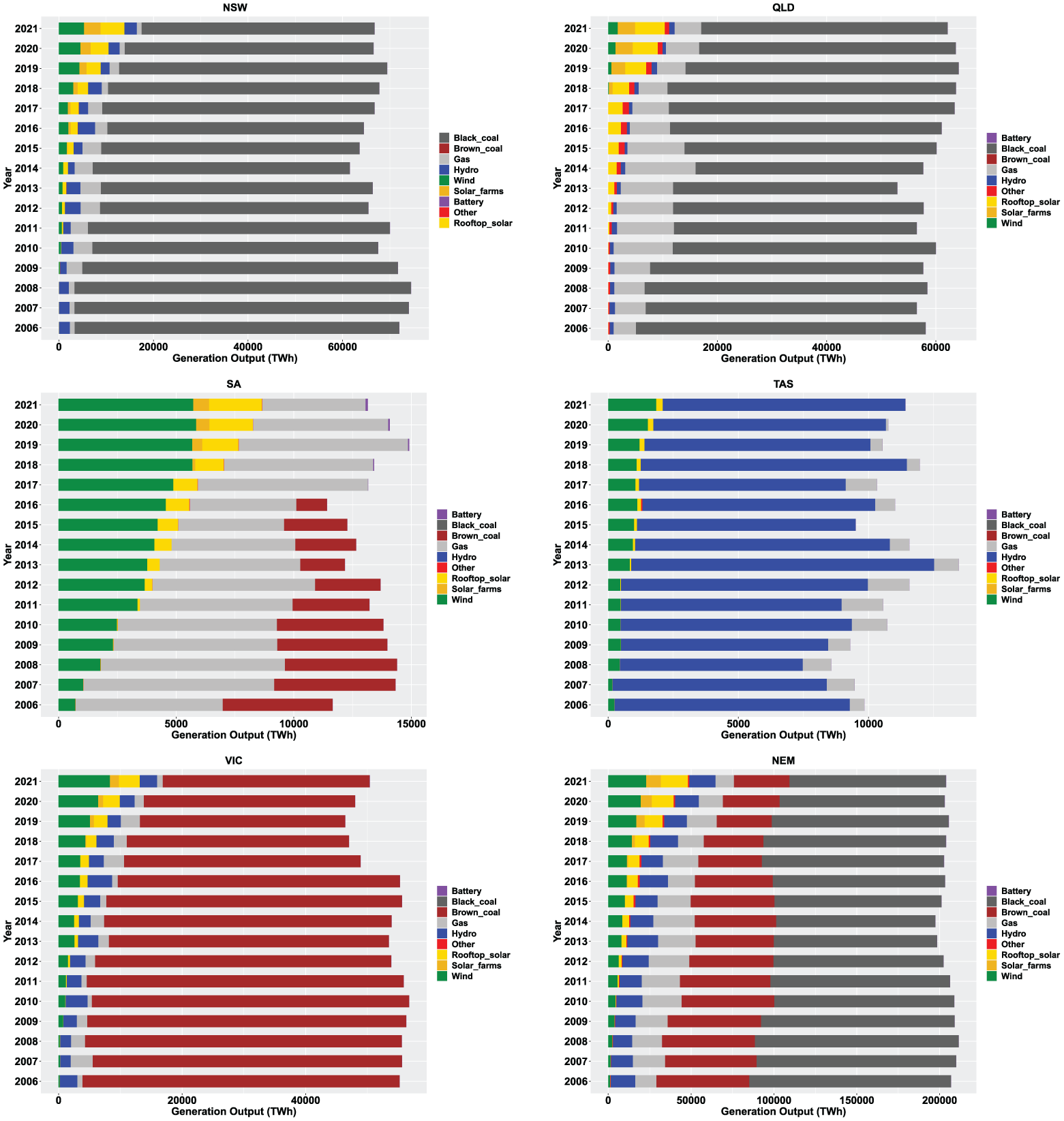

The NEM electricity mix encompasses a blend of fossil fuel and renewable energy sources. Figure 1 illustrates changes in electricity generation by fuel source in the NEM over time. Despite coal-fired generation remaining dominant, recent years have witnessed substantial investments in VRE generation. 2 To address the intermittency issues associated with VRE, flexible technologies such as batteries are increasingly being integrated into the NEM generating mix. The contribution of battery generation, however, remains limited, accounting for less than 1% of the overall generation output.

Electricity generation by fuel source in the NEM from 2006 to 2021.

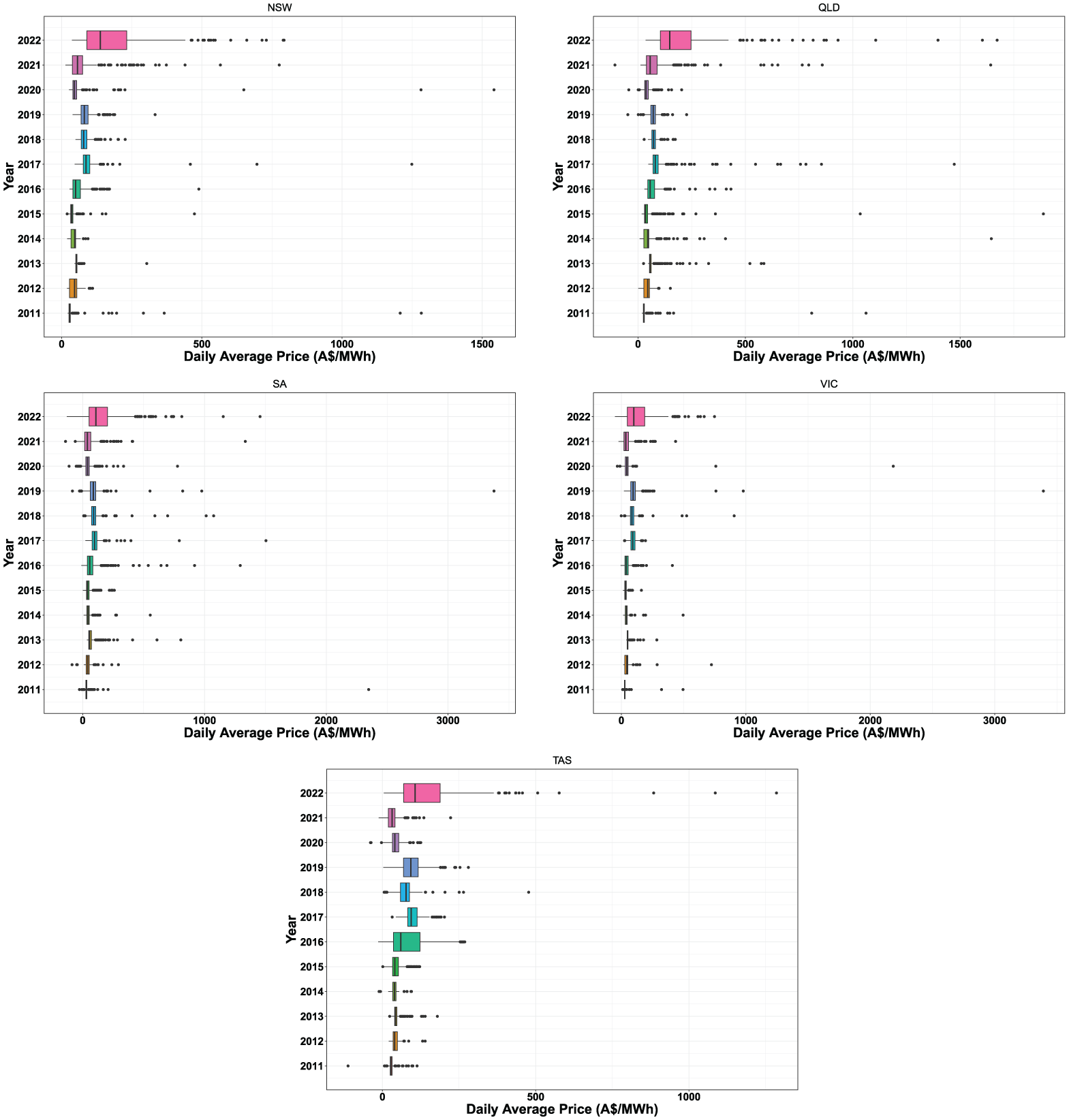

Figure 2 plots the distribution of electricity prices, and Table A3 in Appendix A provides descriptive statistics of spot prices and their determinants over the same time period. Electricity prices generally increase over the years across the NEM. We also observe that high price spikes characterized spot prices, accounting for a large portion of extreme price movements and a high degree of volatility in the market. 3 The Jarque-Bera (JB) test highlights the presence of strong asymmetry and heavy tails in the distribution. In fact, the NEM is known for its extreme price volatility, with the highest market price caps compared to any other market globally. 4 Price spikes remain relatively stable in frequency over the years (see Figure 2). However, the spread of mid-tier prices has widened over time, especially after 2015/2016, showing an increase in price volatility in the (A$ 0/MWh–A$300/MWh) range. The year 2022 stands out as a year of particular interest, where we observe a noticeable increase in the spread of mid-tier prices. This phenomenon likely reflects disorderly bidding behavior that resulted in the temporary suspension of the NEM in 2022.

Distribution and variability of daily average electricity prices over the course of twelve years from 2011 to 2022.

2.2. Relation Between Spot Prices and Their Fundamentals

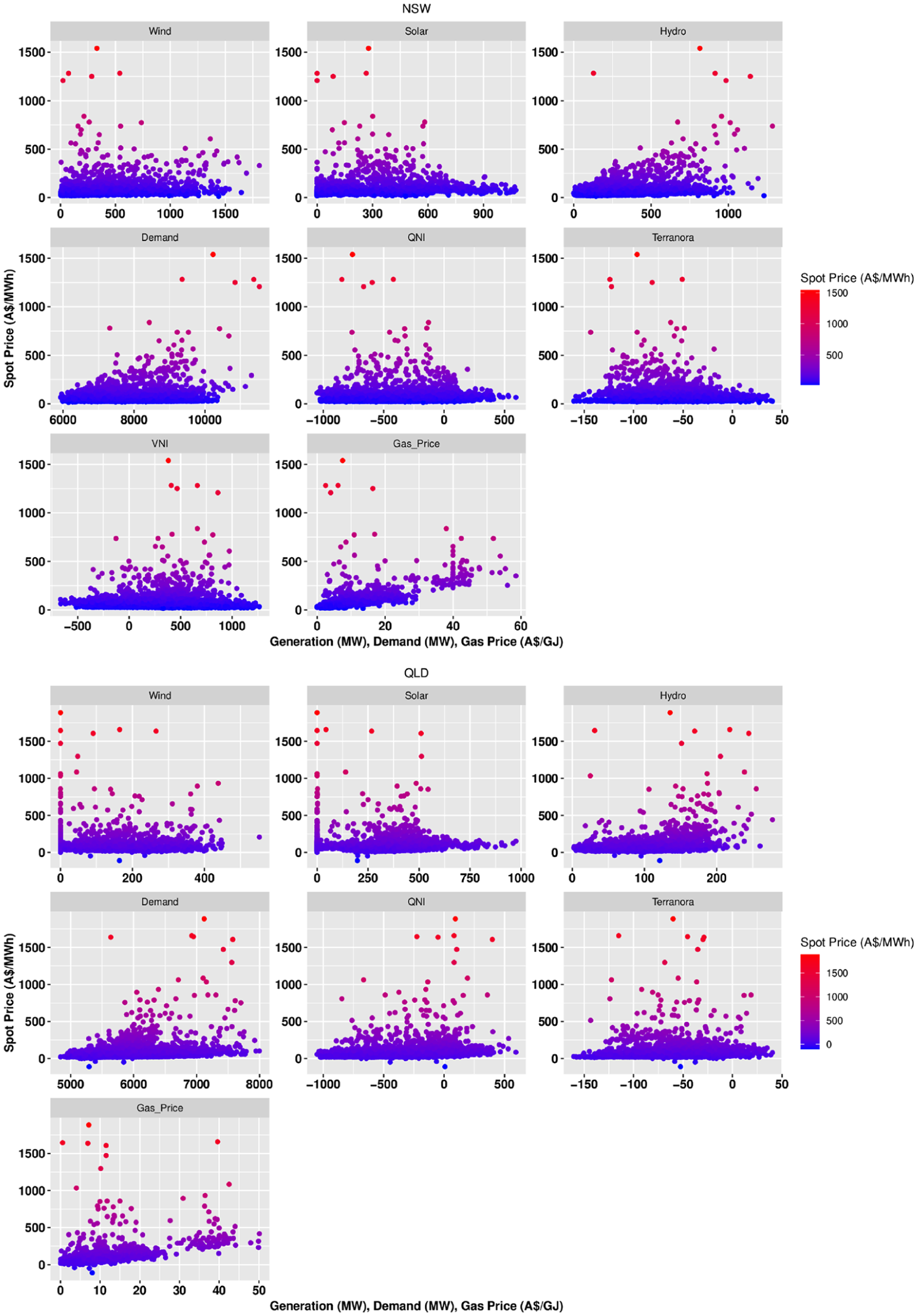

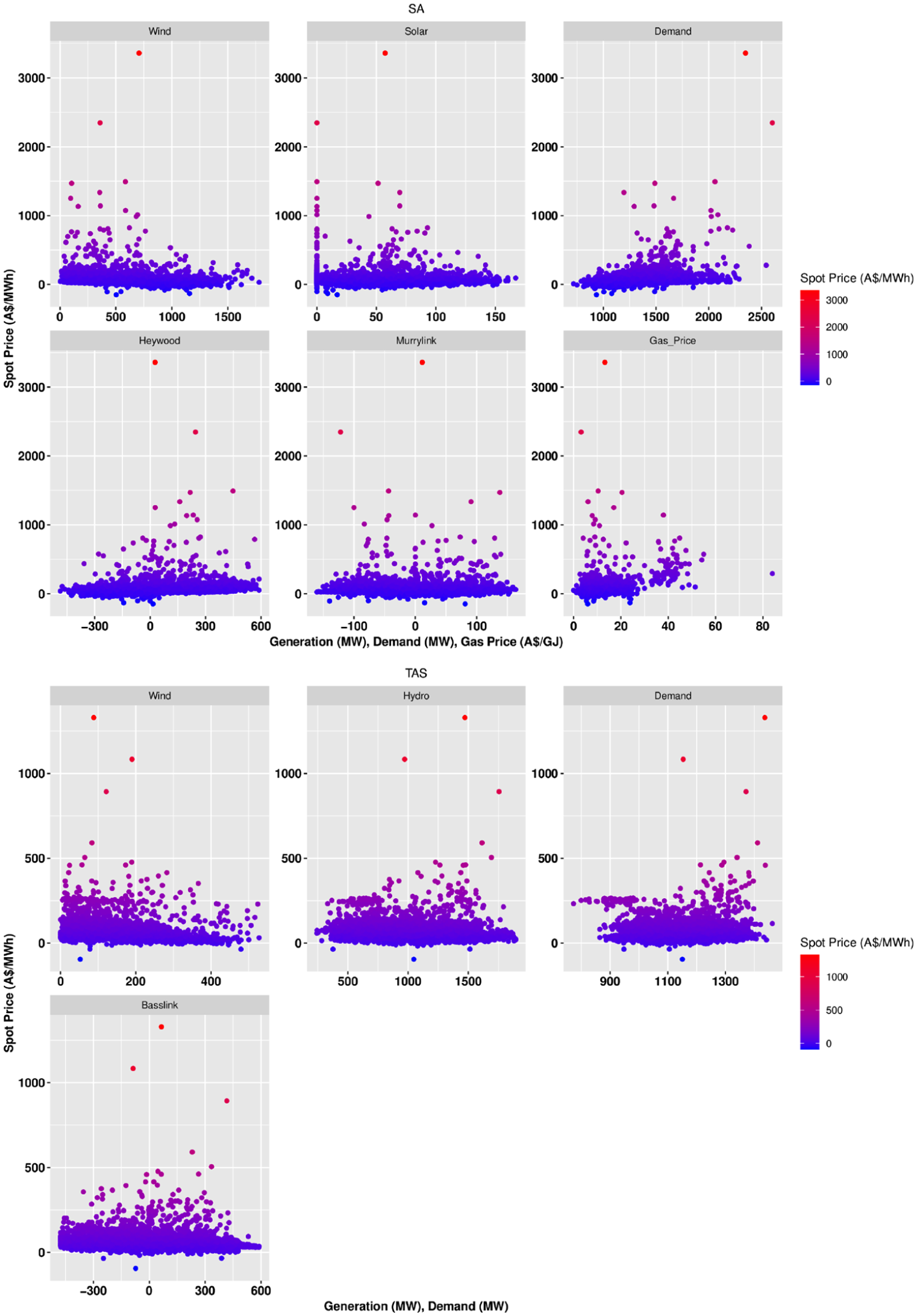

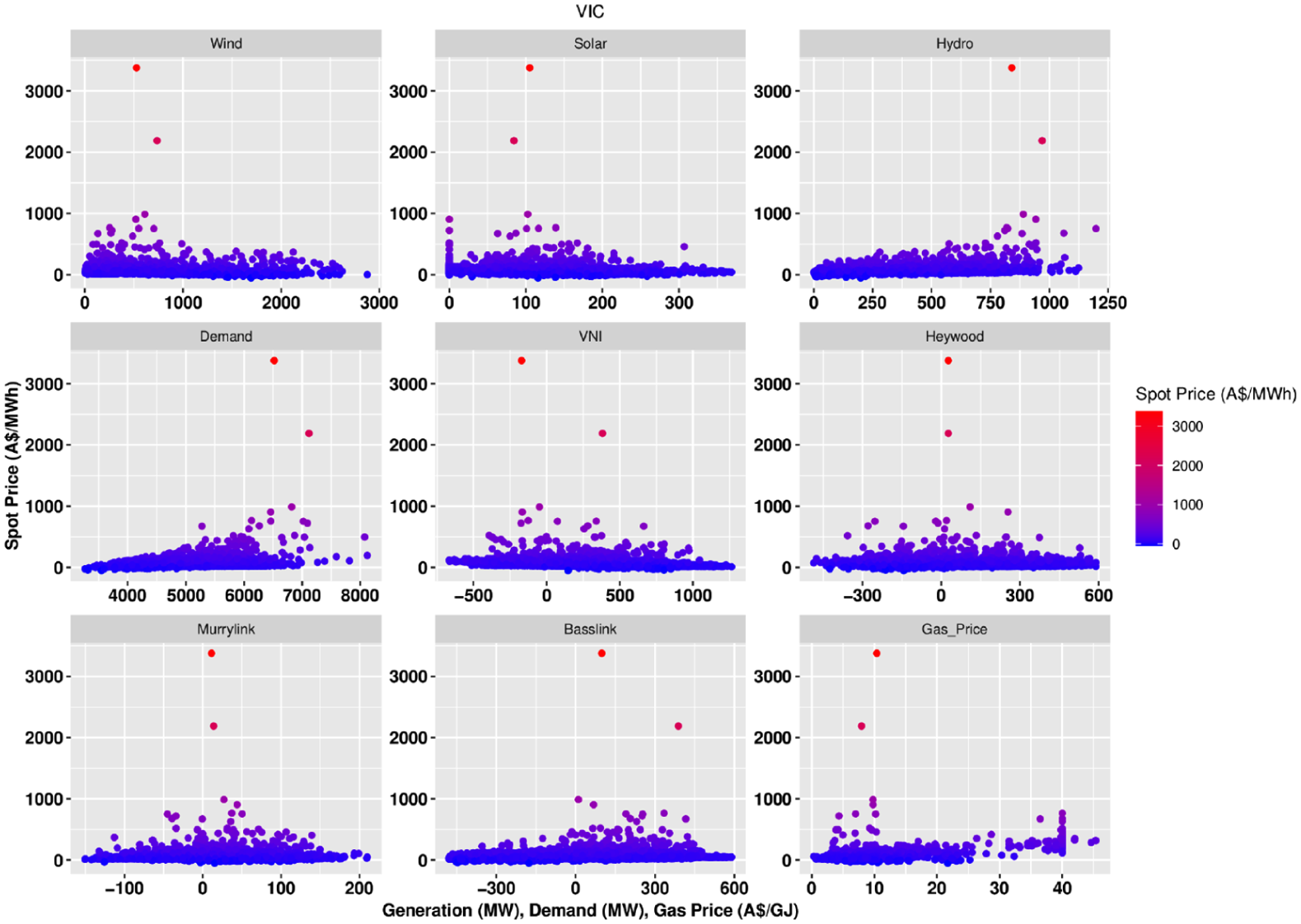

We present scatter plots in Figures 3 to 5 to gain insight into the relationship between spot prices and their driving factors in the NEM. We examine several key variables that impact spot prices, including VRE generation, hydro generation, electricity demand, fossil-fuel prices, and inter-connector flows. The literature suggests that these factors play important role in determining electricity prices in the NEM (Abban and Hasan 2021; Csereklyei et al. 2019; Mwampashi et al. 2021; Mwampashi et al. 2022).

The correlation between spot prices and their determinants in New South Wales and Queensland.

The correlation between spot prices and their determinants in South Australia and Tasmania.

The correlation between spot prices and their determinants in Victoria.

We observe a general negative correlation between wind and solar generation and spot prices, while demand, gas prices, and hydro generation exhibit a positive relation with spot prices. However, a closer examination demonstrates that these drivers’ relation with spot prices is complex and non-linear. Visual inspection suggests that price sensitivity to VRE generation is more noticeable in the lower and intermediate generation values, while hydro and demand exhibit greater sensitivity in the intermediate to upper values. Also, spot prices seem more responsive to gas prices within the low to intermediate values. These observations provide evidence for a non-linear relationship between spot prices and their underlying variables. Indeed, the non-linearity of the merit order curve translates to the non-linear relationship between spot prices and their fundamentals (Hagfors et al. 2016; Westgaard et al. 2021).

2.3. The Quantile Regression Models

We apply quantile regression models to examine the effect of fundamental factors on the distribution of spot electricity prices in the NEM. We assume that the

where

Given the distribution of

It is worth noting that, the application of the quantile regression model is informed by the main objective of this analysis, which is to understanding how various factors impact the distribution of electricity spot prices. It might be tempting to use hour-by-hour regression to address this object and align certain times of day with the tails due to their routine deviation from the norm (like high demand and prices in the morning and evening). However, the effects during these times don’t necessarily represent the “extreme” values that are important in a statistical analysis of tails—prices that occur at the outermost quantiles (e.g., the top 5% or bottom 5% of all prices observed). 6 The quantile regression approach allows for a direct examination of how various factors influence prices at the specific quantiles that represent these extremes and ensures that the analysis is not constrained to specific hours but rather incorporate all times and captures extremes that may occur due to unpredictable events (Uribe and Guillen 2020).

Our choice of method is also influenced by the statistical properties of the model, which are more robust compared to those of a linear regression model, for example. The quantile regression approach accounts for the asymmetric effects of explanatory variables on different parts of the conditional distribution. This is especially important in the Australian electricity market where extreme spot prices are a common feature (Mwampashi et al. 2021; Mwampashi et al. 2022). Unlike linear regression models, quantile regression is semi-parametric and requires minimal distributional assumptions, allowing for a more pragmatic approach in modeling complex dynamics in the electricity market (Clements et al. 2017; Hagfors et al. 2016; Maciejowska 2020; Uribe and Guillen 2020; Westgaard et al. 2021; Xu and Lin 2023). Furthermore, quantile regression models are well suited in situations where the error structure is heterogeneous and a Gaussian distribution does not accurately describe errors (Uribe and Guillen 2020). These properties make quantile regression a more robust model for modeling electricity prices compared to linear regression counterparts.

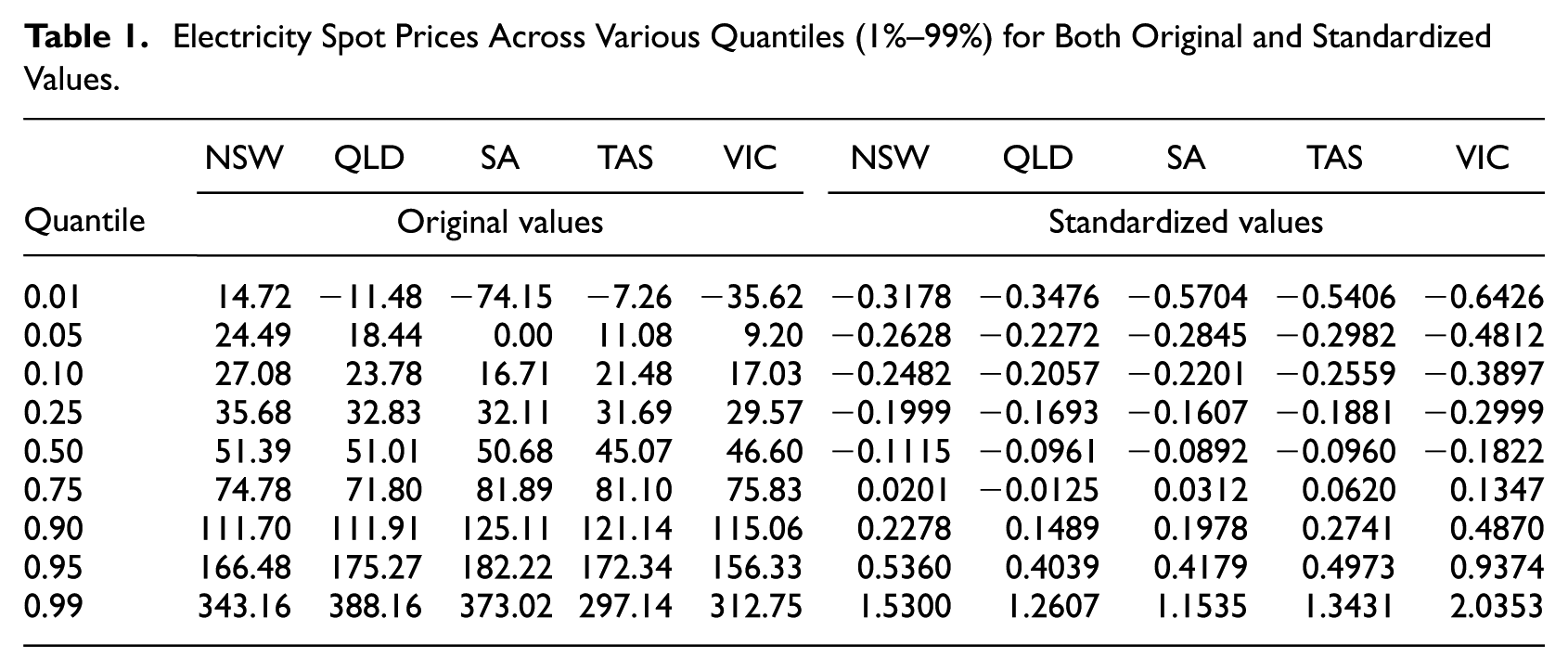

We aim to examine the impact of fundamentals on the distribution of spot prices and compare their effects. To achieve this, we standardize both independent and dependent variables before implementing our models. We select specific quantiles

Electricity Spot Prices Across Various Quantiles (1%–99%) for Both Original and Standardized Values.

To ensure the validity of our models, we conduct several tests: the JB, Dickey-Fuller (ADF), and variance inflation factors (VIFs) tests (see 6.1), which all confirm the suitability of the proposed models.

One of the econometric challenges often encountered in regression models is addressing the endogeneity problem. In the context of the NEM, this issue has been extensively documented by Forrest and MacGill (2013), Csereklyei et al. (2019), Mwampashi et al. (2021), and Mwampashi et al. (2022). From these collective analyses, it can be inferred that most variables—particularly solar and wind generation, fossil-fuel prices, and electricity demand—are determined exogenously. This allows us to establish a unidirectional causal relationship between generator output levels or fossil-fuel prices and spot market prices. One potential exception is hydro generation, which may raise concerns about reverse causality, as hydro generators tend to adjust their output in response to market conditions during peak demand periods. However, the strategic behavior of hydro generators is driven by factors external to short-term price fluctuations for three primary reasons. First, hydro generation is influenced by the opportunity cost of water and reservoir management strategies, which are forward-looking and tied to expected market prices rather than immediate price movements. Second, hydro generators engage in “shadow pricing,” aligning their bids with gas plants that typically set prices during peak periods, which reduces the likelihood of short-term price feedback affecting hydro output. Third, natural constraints such as water inflows and reservoir levels, which are entirely exogenous to the electricity market, determine the timing of hydro generation.

3. The Impact on Electricity Price Distribution

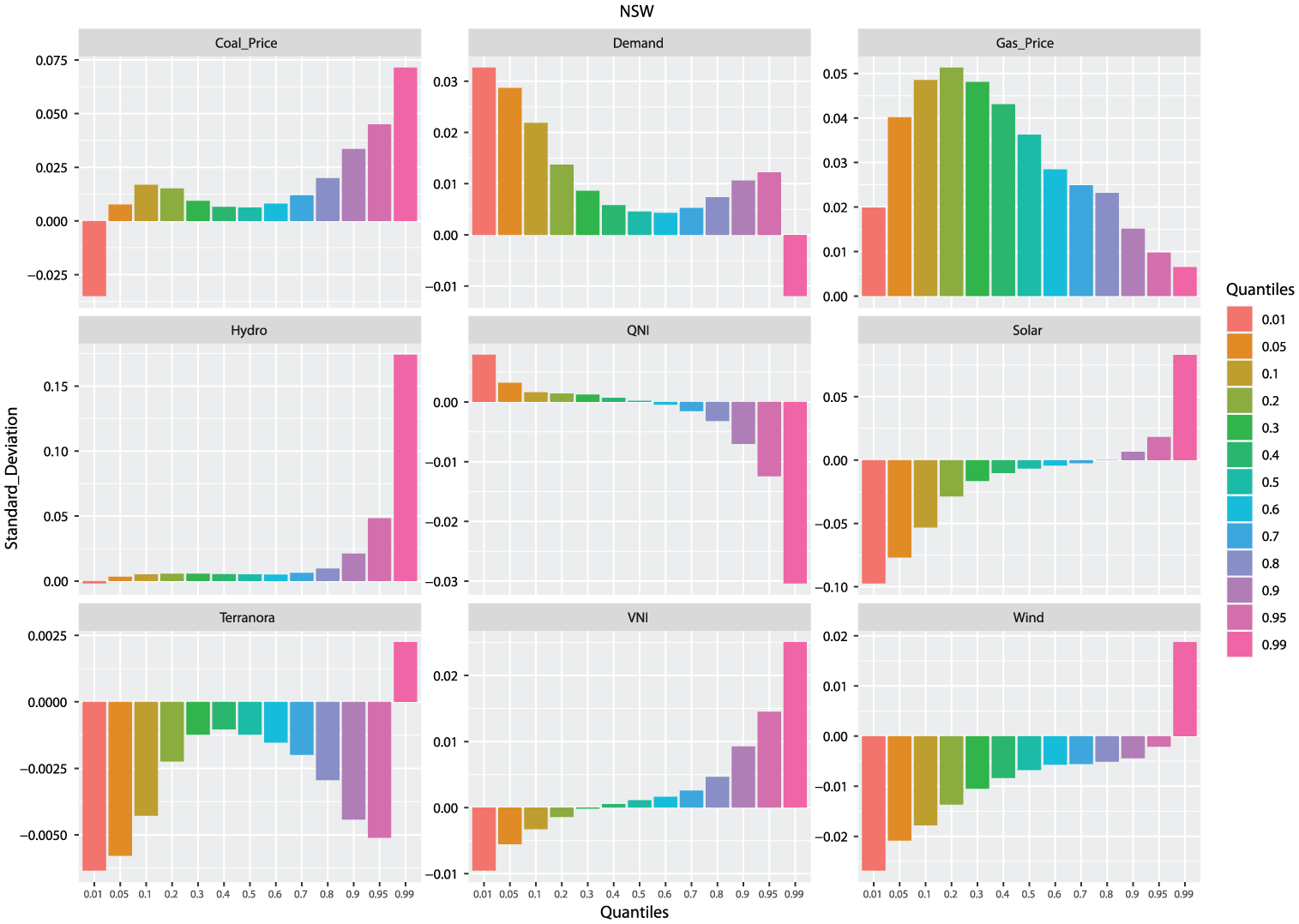

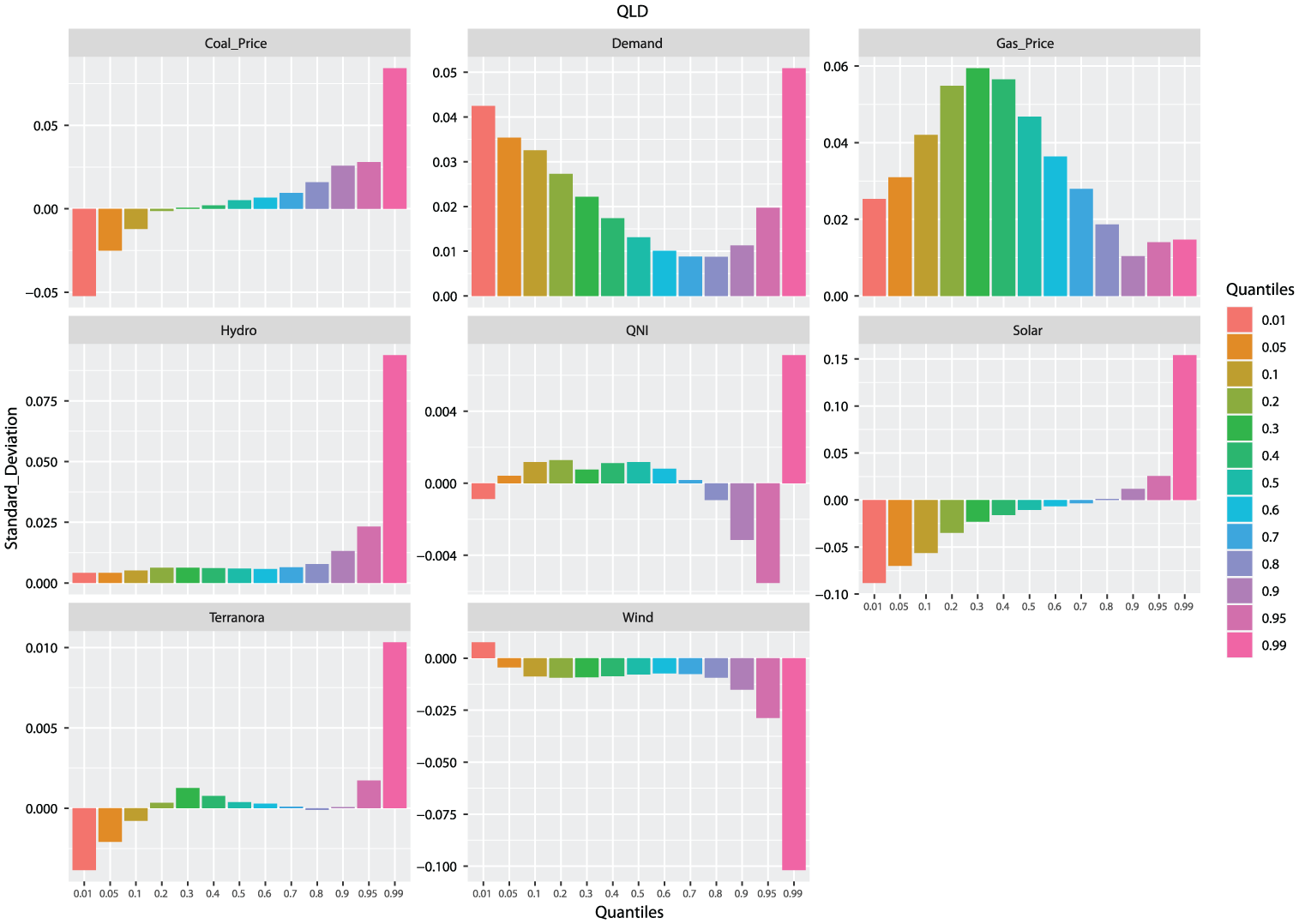

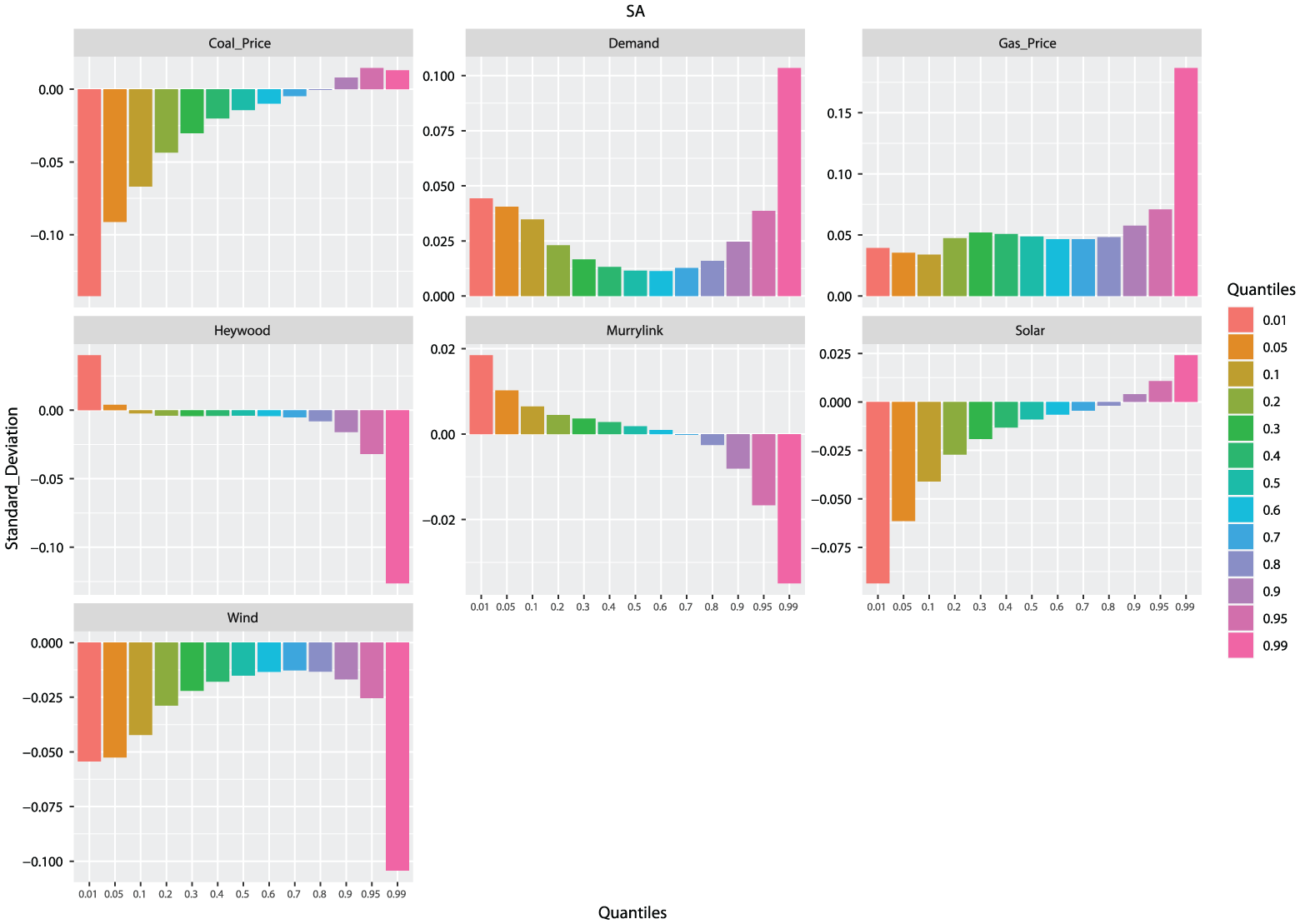

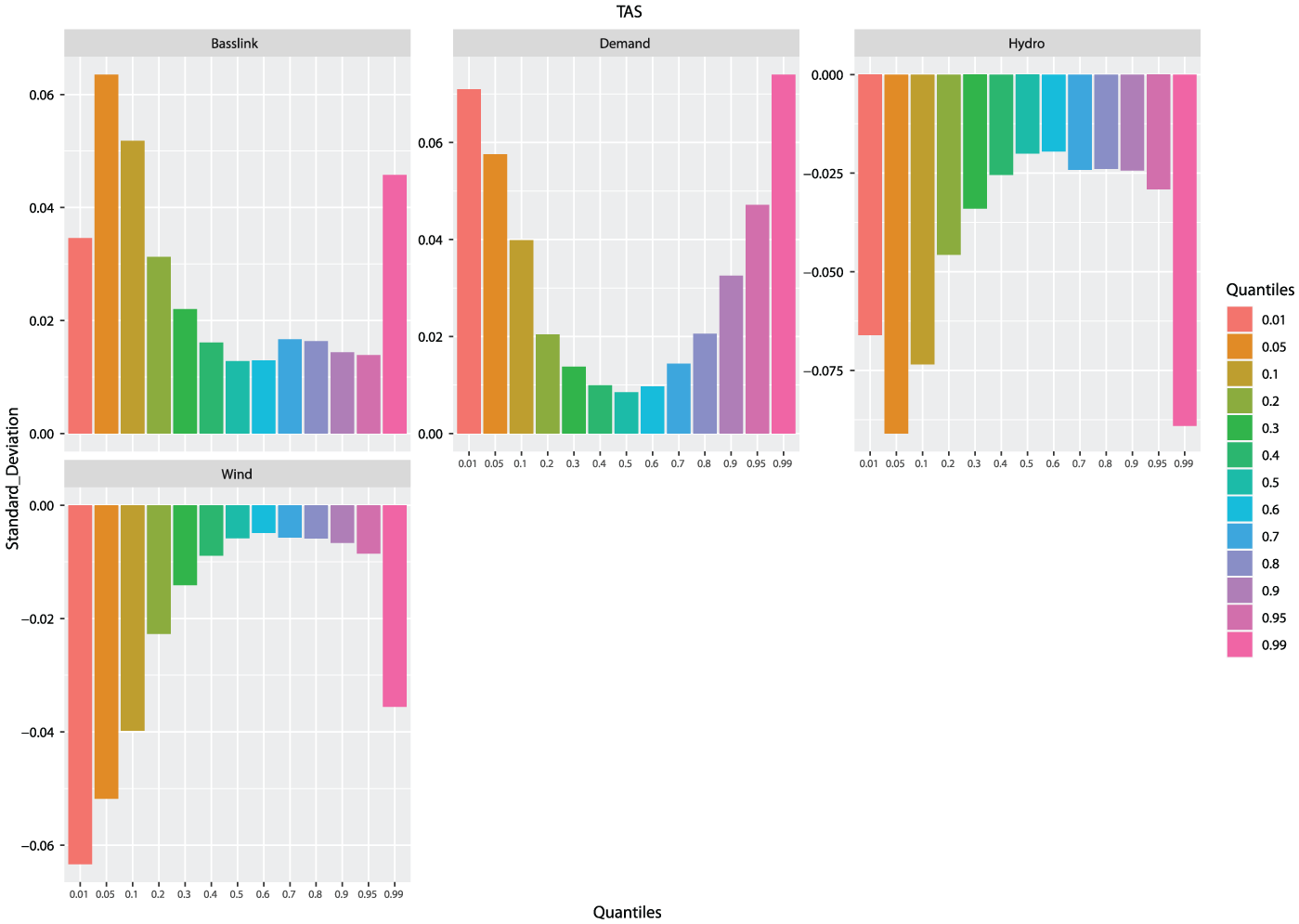

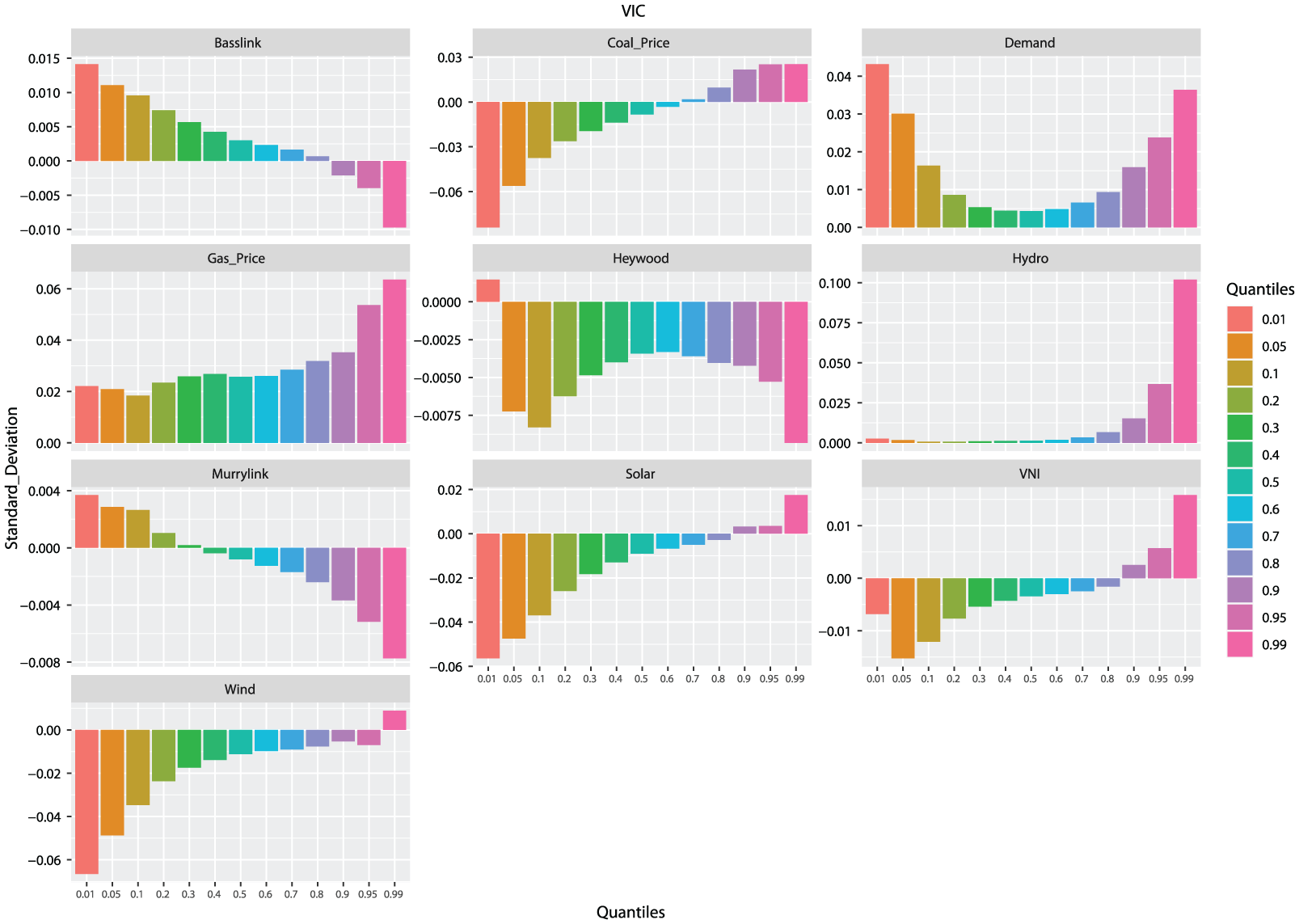

Tables 2 through 6 present the estimated coefficients of electricity price fundamentals’ effect on spot price distribution in the NEM, 8 while Figures 6 to 10 depict the relationships between the variables and their effects on electricity price distribution.

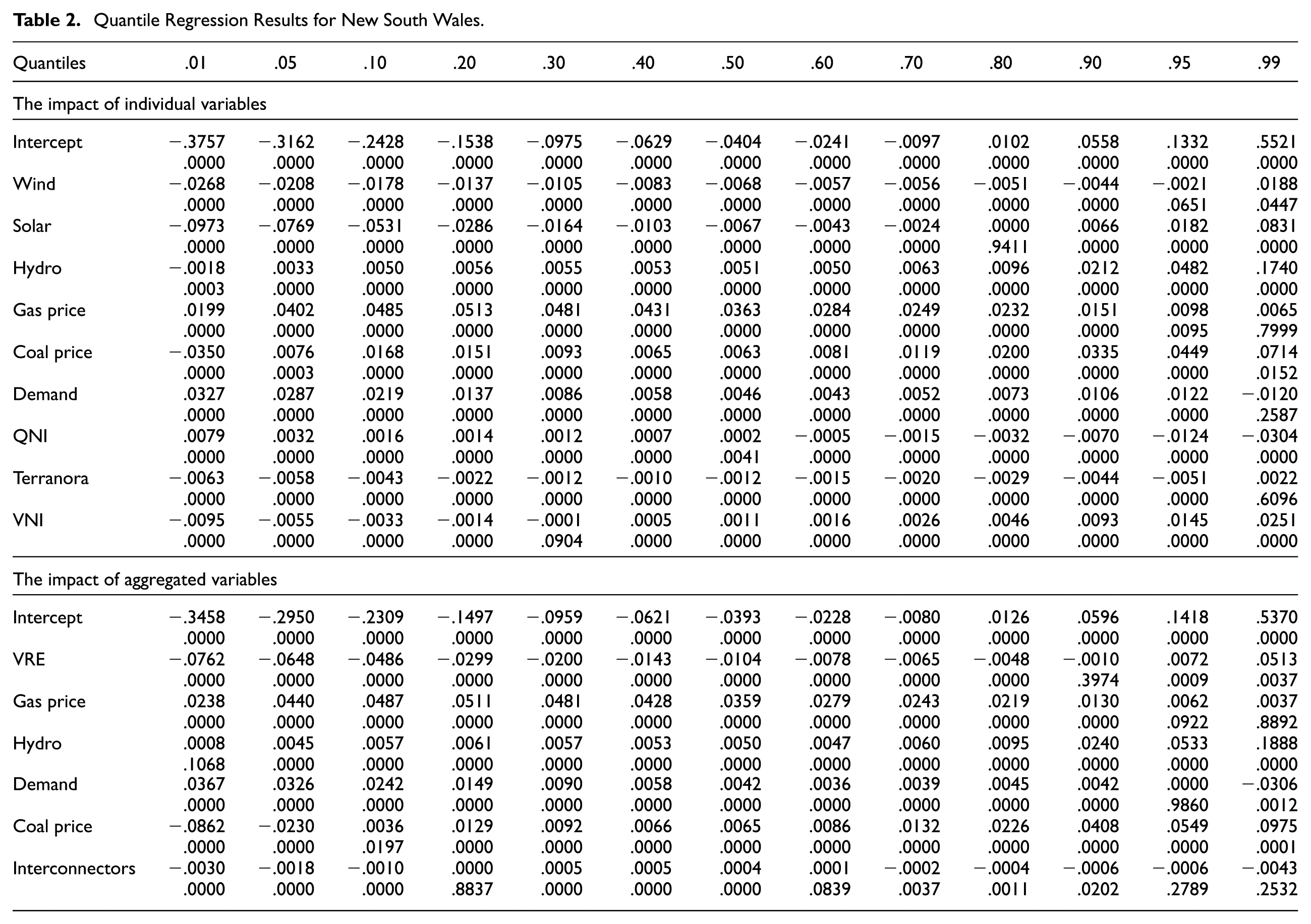

Quantile Regression Results for New South Wales.

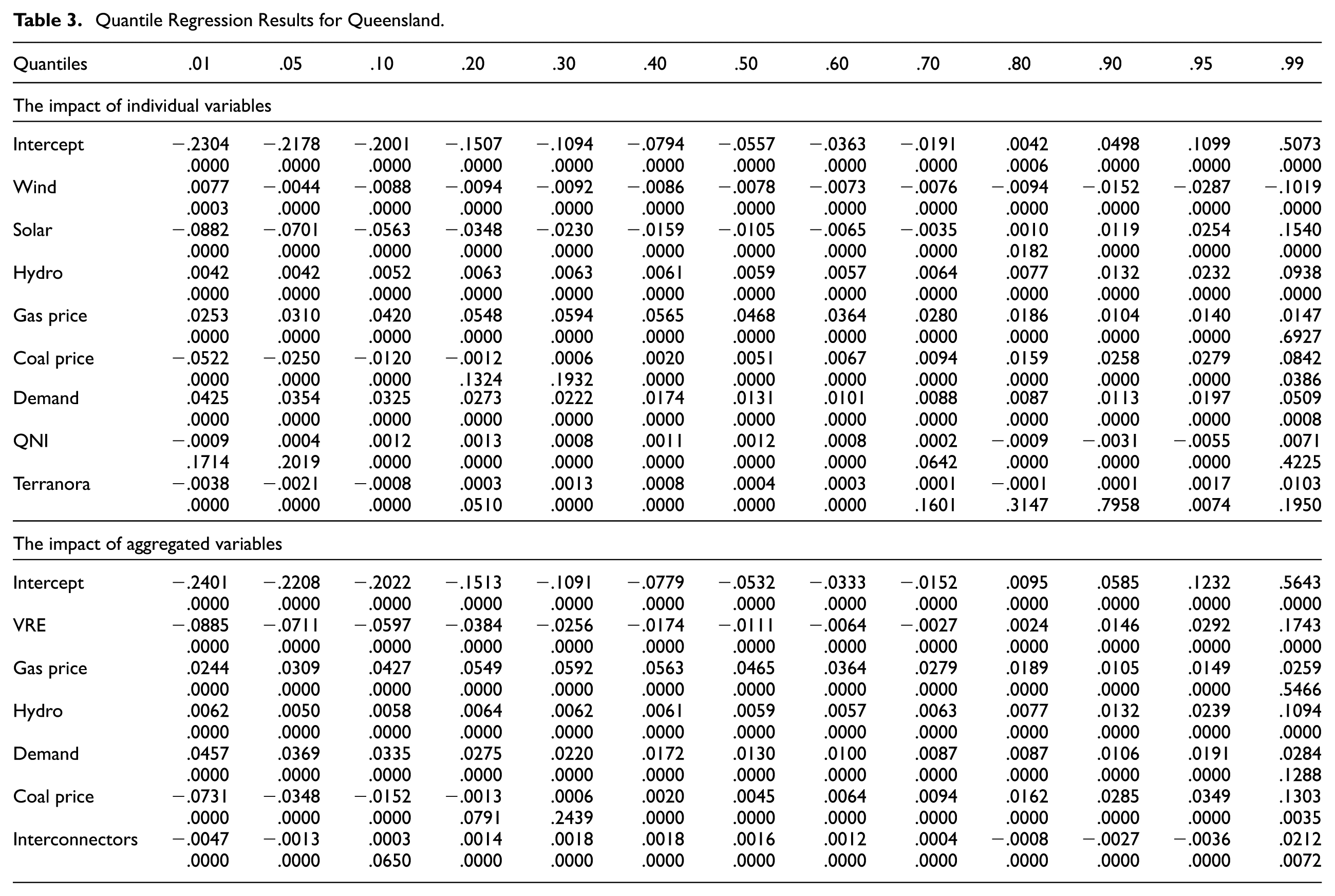

Quantile Regression Results for Queensland.

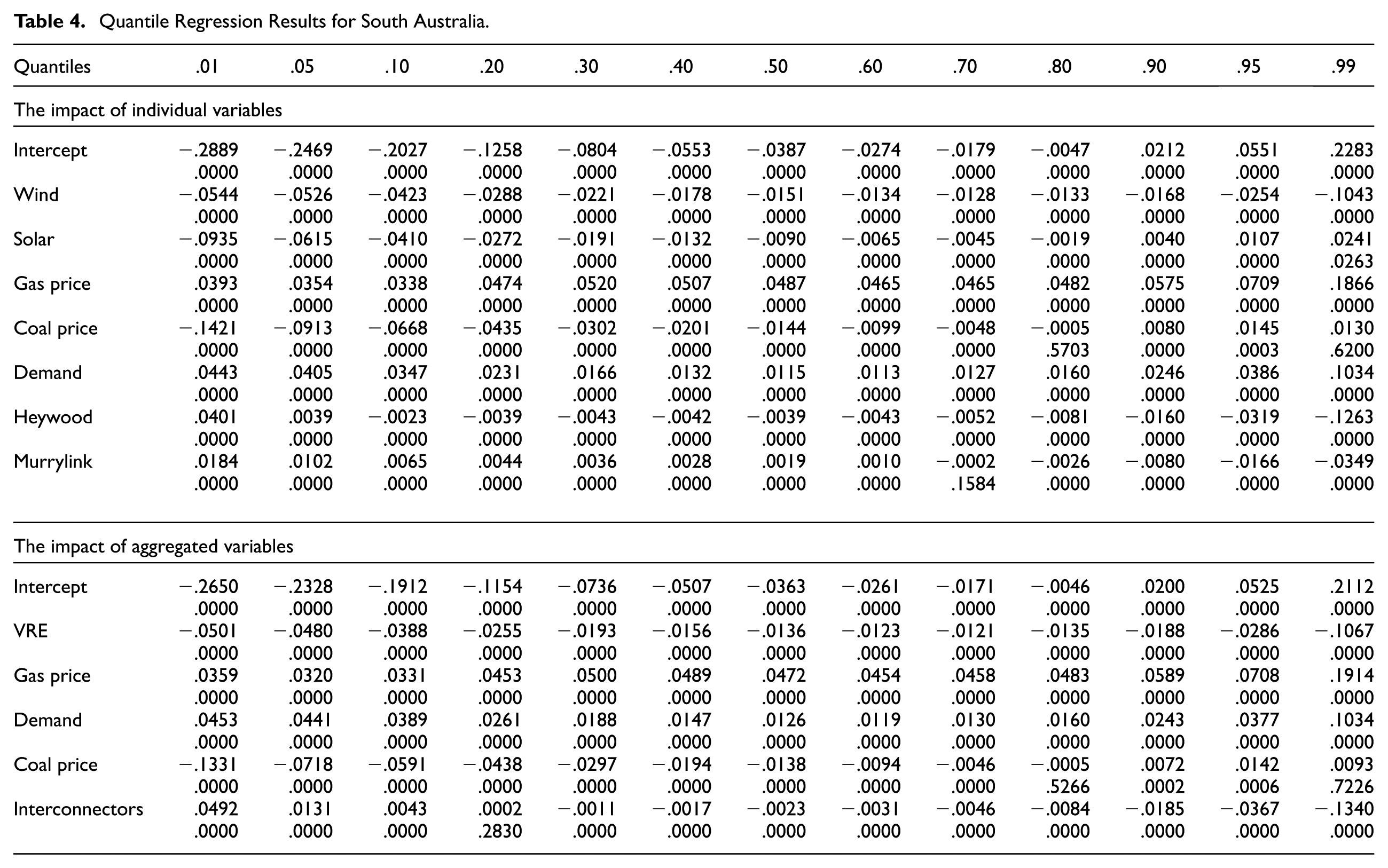

Quantile Regression Results for South Australia.

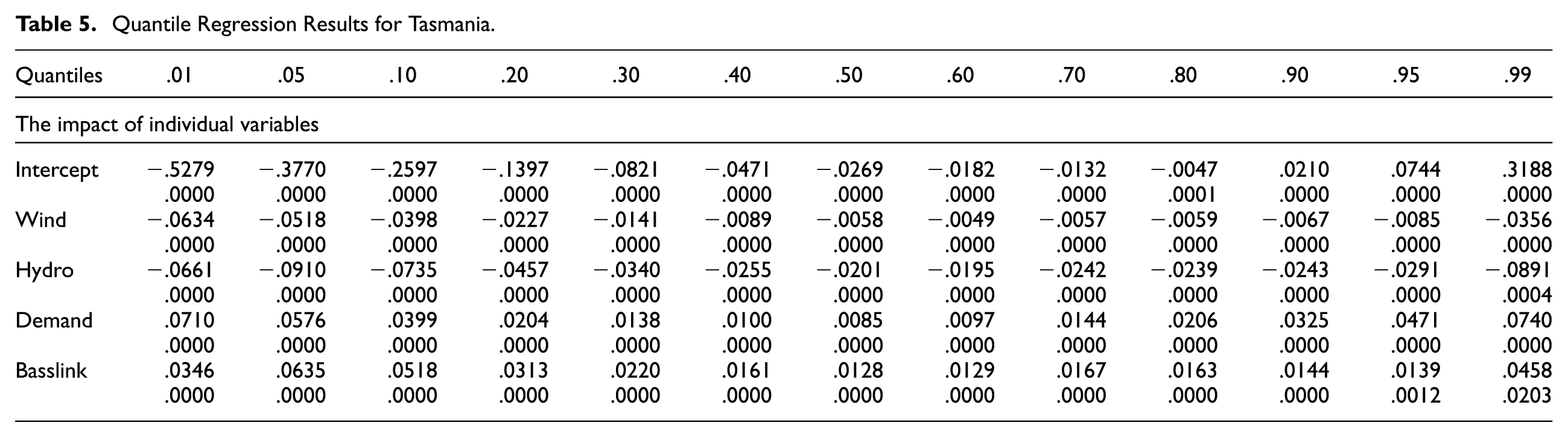

Quantile Regression Results for Tasmania.

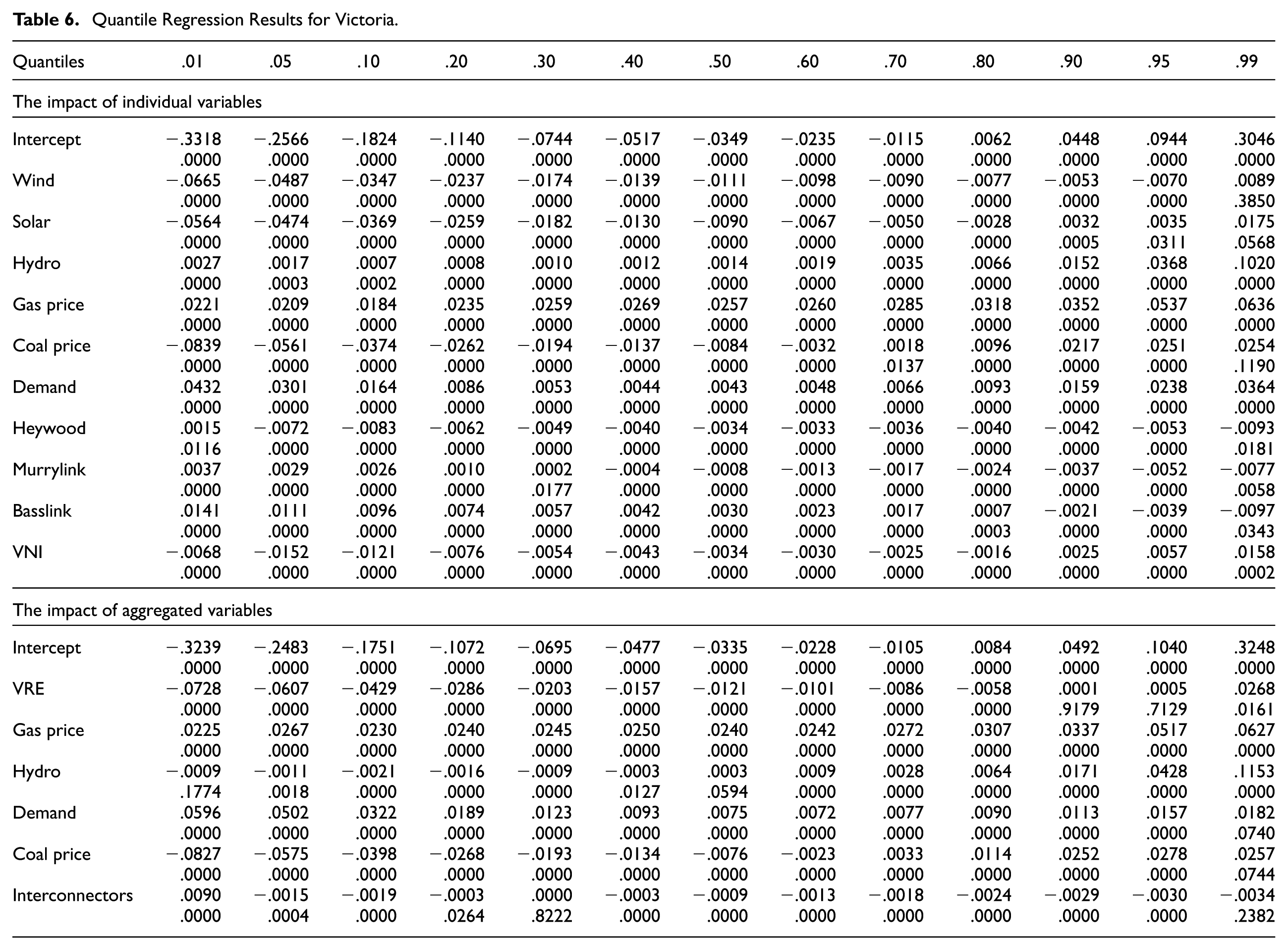

Quantile Regression Results for Victoria.

Quantile regression results for New South Wales.

Quantile regression results for Queensland.

Quantile regression results for South Australia.

Quantile regression results for Tasmania.

Quantile regression results for Victoria.

3.1. Wind and Solar Generation

We find that wind and solar generation exhibit varying effects across quantiles and states (see the top panel of Tables 2–6, and Figures 6–10). An increase in solar generation tends to have a strong negative effect on spot prices in the lowest quantile (1% quantile), which decreases with the quantiles until the 70% quantile in NSW and QLD, and the 80% quantile in SA and VIC, respectively, where the effect reverses. Wind generation exhibits a slightly different pattern. In NSW and VIC, wind generation impacts spot prices negatively up until the 95% quantile, where the effect reverses. However, in SA, TAS, and QLD, wind generation exhibits a negative impact across the entire distribution of electricity prices (with a slight exception of QLD). A more pronounced effect is observable in the highest (99%) quantile, where an increase in wind generation by 1 standard deviation in SA is associated with a reduction in spot prices by 0.05 and 0.10 standard deviations in the 1% and 99% quantiles, respectively.

When considering VRE—aggregated wind and solar generation (see the bottom panel of Tables 2–6, and 5.4), we find a similar impact across states, with the exception of SA. The effect of VRE is most pronounced in the lowest quantiles and decreases with the quantiles until the effect reverses in the 70%, 80%, and 90% quantiles in QLD, VIC, and NSW, respectively. In SA, a region with the highest VRE penetration rates, the impact of VRE is negative across all quantiles, with a slightly strong impact in the lowest quantiles than in the highest quantiles.

These results indicate that the concurrent increase of both wind and solar generation causes strong negative effects on electricity prices when electricity is relatively cheap. However, when electricity is relatively expensive, the increase in VRE generally does not play a role in reducing prices, with the exception of SA. Furthermore, wind generation has greater potential to reduce electricity prices when they are high, compared to solar generation, which likely reflects the differences in their generation profiles (Mwampashi et al. 2022). Wind generation is more distributed throughout the day and can reduce peak prices, whereas solar generation is more concentrated during the day, a period where demand and spot prices are relatively low—thus pushing prices further down. However, solar generation plays little if no role in reducing prices during peak periods.

Generally, the findings regarding the impact of price fundamentals on the spot price in the 50% quantiles collaborate with earlier studies in the NEM, such as Csereklyei et al. (2021), Mwampashi et al. (2021), Abban and Hasan (2021), and Mwampashi et al. (2022). Other studies, such as Maciejowska (2020), show that the negative impact of wind generation is more pronounced in the low quantiles of prices. In contrast, solar generation strongly impacts high quantiles of spot prices. Westgaard et al. (2021) observes a similar pattern for solar generation. However, wind production shows inconsistent effects. The primary determinant that potentially influences the differences in the effects of wind and solar generation across quantiles between previous and our current study is the correlation between wind and solar generation profiles and electricity demand (Rai and Nunn 2020). Specifically, wind and solar generation tend to exert a strong negative effect on spot prices if they correlate well with electricity demand, especially during peak periods.

3.2. Gas and Coal Prices

We find differences in the effect of gas prices across the distribution of spot prices and between states. In NSW and QLD, an increase in gas prices positively impacts spot prices more strongly in the lower and intermediate quantiles, between the 10% and 40% (inclusive) quantiles. For instance, an increase in gas prices by 1 standard deviation in QLD is associated with a 0.03 and 0.01 standard deviation electricity price increment in the 1% and 95% quantiles, respectively, compared to a 0.06 standard deviation increment in the 30% quantile. Conversely, in VIC and SA, the positive impact of gas prices on spot prices is more pronounced in the highest quantile, with the highest impact observed at the 99% quantile. Coal prices do not consistently impact the distribution of spot prices. 9 At the lowest quantiles, an increase in coal prices is negatively correlated with spot prices. These negative effects persist up until the 5%, 20%, 80%, and 60% quantiles in NSW, QLD, SA, and VIC, respectively and then reverse thereafter. We provide further discussion of these findings in subsection 3.4.

Our findings suggest that an increase in gas prices tends to increase electricity prices more substantially when electricity is relatively cheap in NSW and QLD, while in VIC and SA, gas prices tend to exert substantial upward pressure on spot prices when electricity is expensive. An increase in coal prices also tends to exert moderate upward pressure on spot prices at times when electricity is expensive. Overall, the present findings align with previous research that finds a positive correlation between gas prices and spot electricity prices in the NEM (Abban and Hasan 2021; Csereklyei et al. 2021; Mwampashi et al. 2021; Mwampashi et al. 2022). In line with our findings, studies in other markets, such as Westgaard et al. (2021), show that natural gas prices tend to drive up spot prices, especially at higher quantiles.

3.3. Demand, Hydro, and Interconnectors

The impact of electricity demand on the distribution of electricity prices is consistent across states in the NEM. An increase in electricity demand has a greater impact on the tails of the distribution compared to the intermediate quantiles. 10 However, in NSW, the impact is relatively more pronounced in the lowest quantile than in the highest quantiles. In QLD and SA, we see the opposite effect, whereas, in TAS and VIC, the impact is almost equal in the 1% and 99% quantiles. These findings align with Hagfors et al. (2016) and Westgaard et al. (2021). Specifically, Westgaard et al. (2021) notes that the positive influence of demand forecast and load on electricity prices is more pronounced at the upper quantiles of the price distribution.

These findings and those in subsections 3.1 and 3.2 offer some insights on a question posed by Hirschhorn and Brijs (2022)—whether electricity prices will ever be free. While electricity prices may be free at certain times, it is important to remember that this is not a universal phenomenon and that costs during periods of high demand continue to be significant despite increasing penetration of VRE generation (see subsection 3.5 for further discussion).

The impact of hydro generation on electricity prices is generally consistent across the NEM, with the exception of TAS. In general, an increase in hydro generation is associated with a positive impact on spot prices at the lower quantiles, the effect which increases with quantiles—a larger positive impact on spot prices at the 99% quantile. For example, in VIC, an increment of 1 standard deviation in the hydro generation is associated with an (almost) negligible positive increment in spot price at the 1% quantile, whereas at the upper (99%) quantile, an increase in hydro generation exhibits upward pressure on spot prices by around 0.10 standard deviation. TAS, a hydro-rich state, is the only market in which an increase in hydro generation exerts downward pressure on spot prices. This impact is more pronounced at the lower and highest quantiles and relatively low in the intermediate quantiles.

We also observe variations in the impact of interconnector flows on the distribution of electricity prices. For instance, the Terranora and Basslink interconnectors in NSW and TAS, respectively exert more negative pressure on the lower and upper quantiles, whereas the QNI in NSW and the Heywood and Murraylink interconnectors in SA are negatively associated with spot prices in the upper quantiles. In VIC, the Heywood interconnector is particularly noteworthy, generally exhibiting a negative impact across the quantiles with a strong impact observed in the lower and upper quantiles. The impact of other interconnectors, such as Murraylink and VNI, varies. Murraylink exhibits a strong negative impact in upper quantiles, and VNI exhibits a strong impact in lower quantiles of electricity prices.

Our results suggest that electricity demand imposes positive pressures when electricity is relatively cheap and relatively expensive, while at times when electricity is modestly expensive, its impact tends to be low. When electricity is relatively expensive, an increase in hydro generation tends to make electricity prices even higher. The interconnections across the NEM, especially from states with cheap electricity due to high renewables such as SA, have the potential to lower prices in neighboring regions, such as, VIC.

3.4. Rationalizing Counter-intuitive Effects

Several observed effects in subsections 3.1 and 3.3 may appear counterintuitive. For example, our findings suggest that an increase in renewables (wind, solar, and hydro) are positively correlated with spot prices, while coal generation is negatively correlated with spot prices, in some quantiles. We account for the observed counterintutive effects to the way electricity prices are set in the NEM and strategic bidding practices of some generators. 11

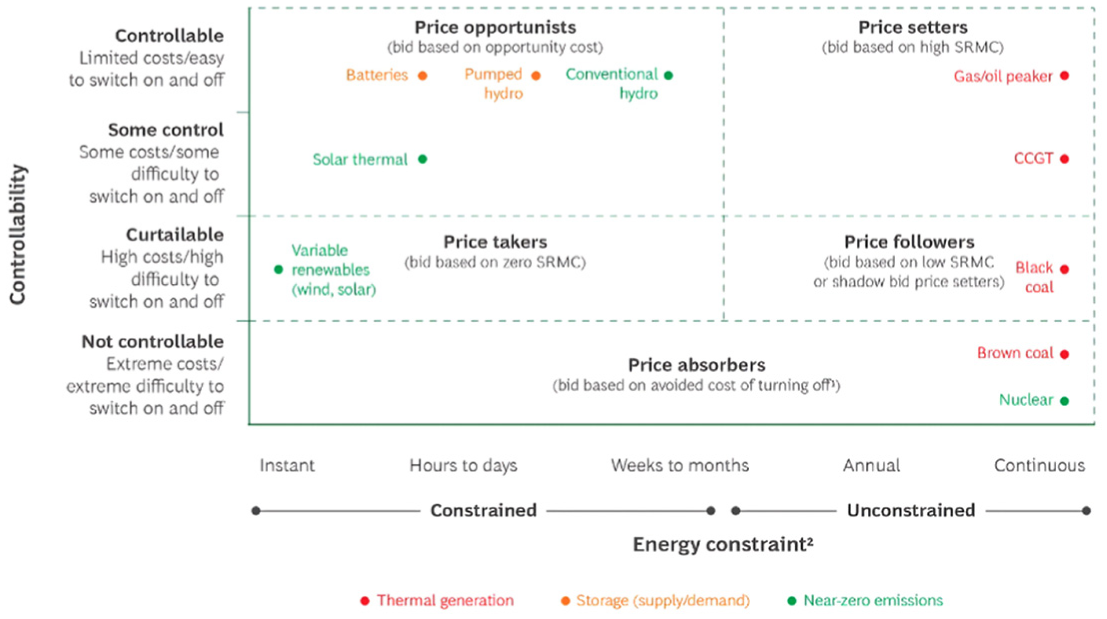

To better clarify the counterintutive effects it important to understand the roles of generators in setting prices in the NEM. We categorize the generators into three groups according to their pricing roles in the NEM: price setters, price opportunists, and price followers (see Boston Consulting Group, 2022; Nolan et al. 2022 for further discussion). Price setters directly set the price when they are the last needed to meet demand, and they also indirectly influence the price through the bidding strategies of other generators, who use the price setters’ bids as a reference. Gas-fired mid-merit and peaking generators, which adjust their output to match demand throughout the day, typically set the wholesale spot price. Thus, changes in gas prices impact electricity prices either directly by increasing gas generation costs or indirectly through the bidding strategies of other generators that use price setters’ bids as reference prices. Price opportunists include generators such as hydro plants and energy storage facilities, which have limits on how much energy they can produce. They bid based on the opportunity cost of using their energy later, generally setting their prices just under the main price setters, influenced by the latter’s fuel costs. Price followers typically have limited flexibility and are not energy-limited. They usually price their bids according to their SRMC, but sometimes they engage in shadow bidding—aligning their bids with the SRMC of higher-priced technologies to increase revenue when they become the marginal generator. Figure 11 summarizes generator roles in market pricing—price setters, price opportunists, price followers, and price absorbers. Our discussion to each counterintuitive effect are detailed in the following subsections.

Generator roles in market pricing—price setters, price opportunists, price followers, and price absorbers.

3.4.1. Wind and Solar Generation

Despite the increasing role of wind and solar generation in setting spot prices in the NEM, their impact is more pronounced during low-demand periods during the day. During peak periods, both in the morning and evening, solar generation and, to a lesser extent, wind generation is typically low, leading to spot prices equaling the dispatch cost of marginal generators, such as natural gas or coal. 12 Gas generators, however, tends to set high electricity prices, reflecting both their higher fuel cost and generators’ strategic bidding behavior.

Therefore, the observed effects can be explained by the fact that when renewables are available but not adequate, they fail to push more expensive generators out of the merit order, especially during peak times. This scenario leads to situations where renewables are technically contributing to the energy mix but are not enough to lower the price. Instead, they are part of a mix that includes high-cost generators setting the market price. Even marginal increases in wind and solar generation can coincide with prices set by more expensive technologies if the increase in renewable generation does not correspond with peak demand periods or if it does not reach a threshold necessary to shift the merit order significantly. Thus, even as renewable capacity increases, if this capacity does not align perfectly with demand profiles or exceeds the capacity of gas plants to meet peak loads, it will result in higher prices. Since all generators receive the price set by the most expensive necessary unit, an increase in renewable generation that does not displace these units leads to renewables receiving a higher price per the market, influencing the regression model to show a positive correlation between renewable generation and higher prices in these quantiles. 13

3.4.2. Hydro Generation

To understand the positive correlation between hydro generation and spot prices, it’s important to highlight the strategic behavior of hydro generators. Hydro plants often decide when to generate electricity based on the value of the water in their reservoirs, not just the cost of running the plant. 14 In the NEM, flexible generators with high fuel costs are considered capacity providers (e.g., open-cycle gas turbines). These flexible generators are available to quickly provide electricity when needed, rather than providing low-cost electricity at all times. Hydro generators are also highly flexible generators that tend to act more as capacity providers due to constrained energy supply—finite water availability (Hydro Tasmania 2019). This means they tend to generate electricity during times when they can get the highest prices for it—usually during peak demand periods when prices are higher. Hydro plants manage their stored water to make sure they’re making the most money possible, especially during these peak times. This strategic approach can explain why there is a positive correlation between hydro generation and higher spot prices, even if hydro power is generally cheaper to produce compared to gas.

It’s also important to note that gas plants often set the market price during peak demand periods because they are usually the marginal generator. Since hydro generators get paid the same market price that the gas plants set, they benefit from operating during these high-price times. Furthermore, a study by Nolan et al. (2022) demonstrates that when hydro plants set prices, they often follow the pricing patterns of gas power plants, a strategy known in Australia as “shadow pricing.” These strategic behavior by hydro plants, considering both the opportunity cost of stored water and market conditions, helps to explain the observed the observed effects in the high quantiles of the electricity prices. 15

3.4.3. Coal Prices

Coal-fired power stations are typically designed for steady, continuous operation and do not easily ramp down due to technical constraints and economic reasons. This means they often continue generating power regardless of fluctuations in demand or increases in renewable energy supply. In lower quantiles, where demand is minimal and renewable output is sufficient, coal’s continuous operation can lead to oversupply, pushing prices down. This effect is magnified when coal continues to generate power even when not needed, due to its inflexibility and low marginal costs (Mwampashi et al. 2021). 16 Since renewable energy generators often set prices during these periods, this results in a negative correlation between coal prices and spot prices during these times. The reason we observe varying effects across the quantiles is because coal does not operate exclusively during low or negative price periods. Indeed we observe the negative correlation shifts from low quantiles to mid quantiles and eventually turns positive in high quantiles when demand is high and coal generators set prices. 17

In general, the role of VRE and hydro in shaping the NEM continues to depend on gas prices. Despite the significant increase in wind and solar generation in recent years, their impact on reducing prices during peak periods remains negligible, particularly due to high gas prices.

3.5. Comparative Analysis

The findings presented in Tables 2 through 6, and 5.4 suggest that both wind and solar power generation contribute to a decrease in spot prices in the lower quantiles, with solar generation exhibiting a substantial negative impact on spot prices compared to wind generation. To illustrate, in the 1% quantile in QLD, a 1 standard deviation increase in solar generation correlates with a decrease of 0.09 standard deviations in spot prices. By contrast, an equivalent increase in wind power generation corresponds with a modest decline of 0.01 standard deviations in spot prices. These findings concur with Mwampashi et al. (2022) and can be accounted to the fact that solar generation tends to correlate more with electricity demand (both peak in the summer). Thus, an increase in solar generation significantly impact electricity prices during this season than wind generation. Nevertheless, solar generation does not contribute significantly to easing price pressure in the higher quantiles.

The results in the bottom panel of Tables 2 through 6, and 5.4 suggest further that the negative impact of VRE exceeds the positive impact of gas prices in the lower quantiles. However, as the quantiles increase, the positive impact of gas prices becomes more significant than the negative impact of VRE. However, in the higher quantiles, both VRE and gas generation tends to affect spot electricity in the same direction due to the reasons discussed in subsection 3.4.

Considering all price fundamentals, except coal, suggests that gas prices and electricity demand exert considerable upward pressure on spot prices in the NEM, followed by hydro generation. The impact of interconnectors is inconsistent across the quantiles. However, when negative, their combined effects with those of wind and solar generation still exhibit slightly negative impacts on spot prices compared to the positive pressure resulting from gas prices, hydro generation, and electricity demand.

To conclude, both domestic and international pressure on gas prices may continue to have a significant impact on electricity prices in the NEM, especially given that wind and solar generation are still at low levels.

4. The 2022 Energy Crisis in the NEM

The NEM saw record-breaking average spot prices in the second quarter of 2022, reaching unprecedented levels in its more than two decade history. Primarily, a potent mixture of four key elements were behind extreme market dynamics: soaring gas prices, elevated coal prices, high operational demand, and widespread generator unavailability (AER 2022; Tan et al. 2023). Due to this shock, wholesale prices tripled, increasing from $75/MWh in 2021 to $225/MWh in 2022 (Simshauser 2023). Elevated, sustained prices led to the implementation of the administered price cap (APC), which effectively capped prices to A$300/MWh when cumulative spot prices surpassed the cumulative price threshold (CPT), see Figure A2. High fuel costs, combined with the introduction of the APC, resulted in multiple power generators withdrawing their capacity from the market, contributing to a severe supply shortage. Ultimately, AEMO suspended market operations on June 15, 2022, as it became unfeasible to comply with the NER (ACCC 2022; AER 2022). This suspension marked only the second occurrence in the NEM’s history, with the first being a brief two-hour interruption in 2001 due to a technological issue.

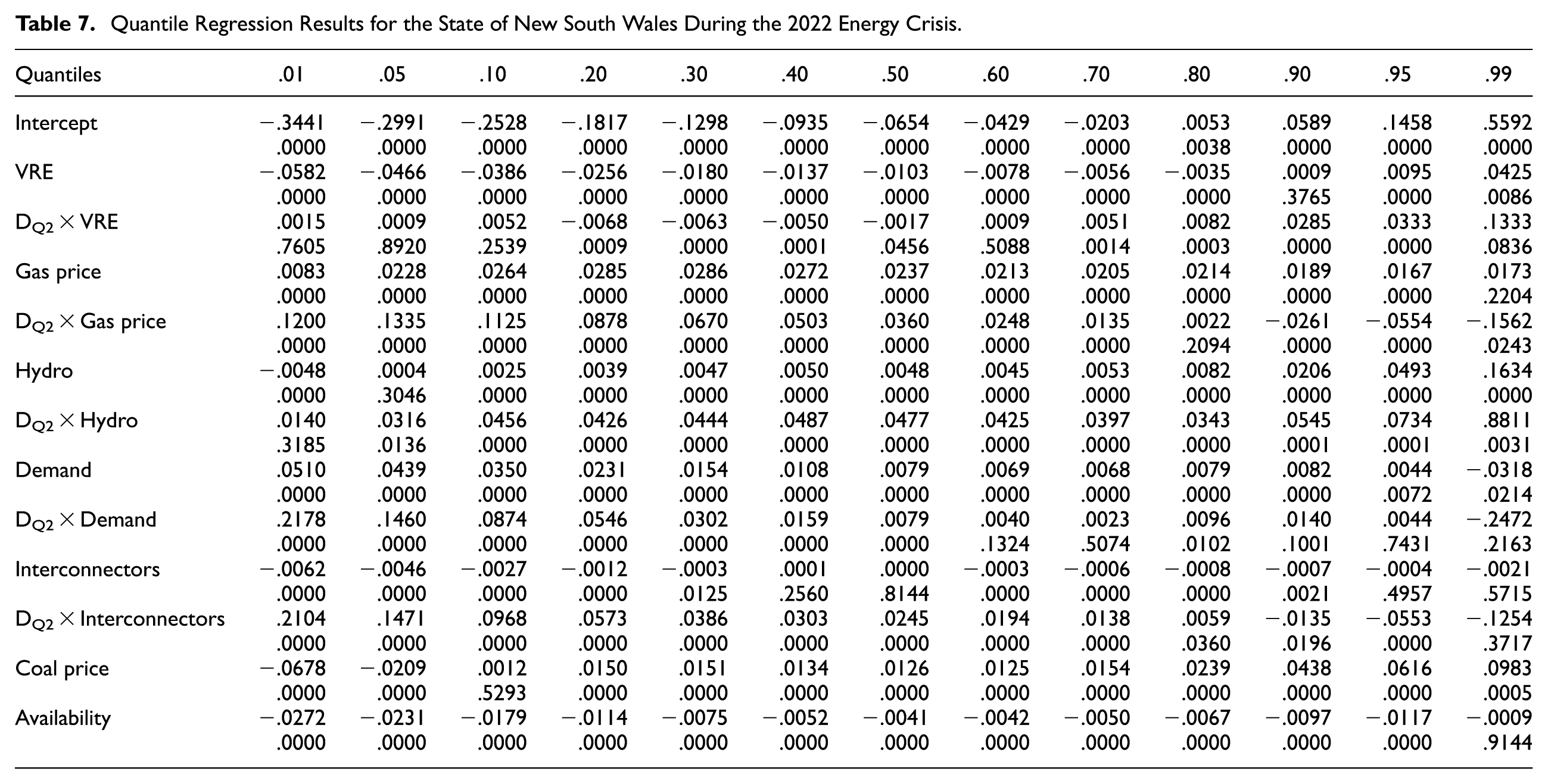

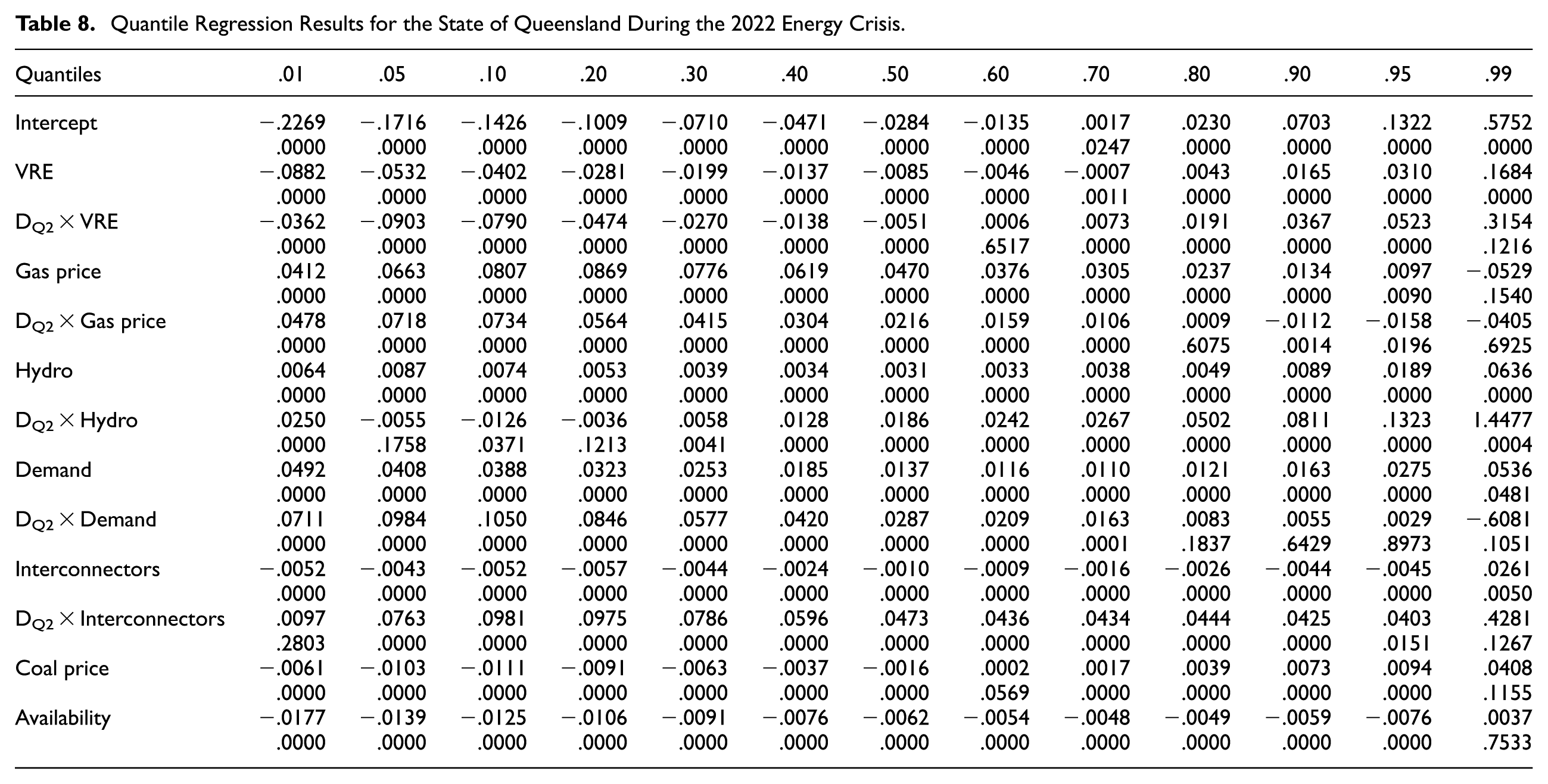

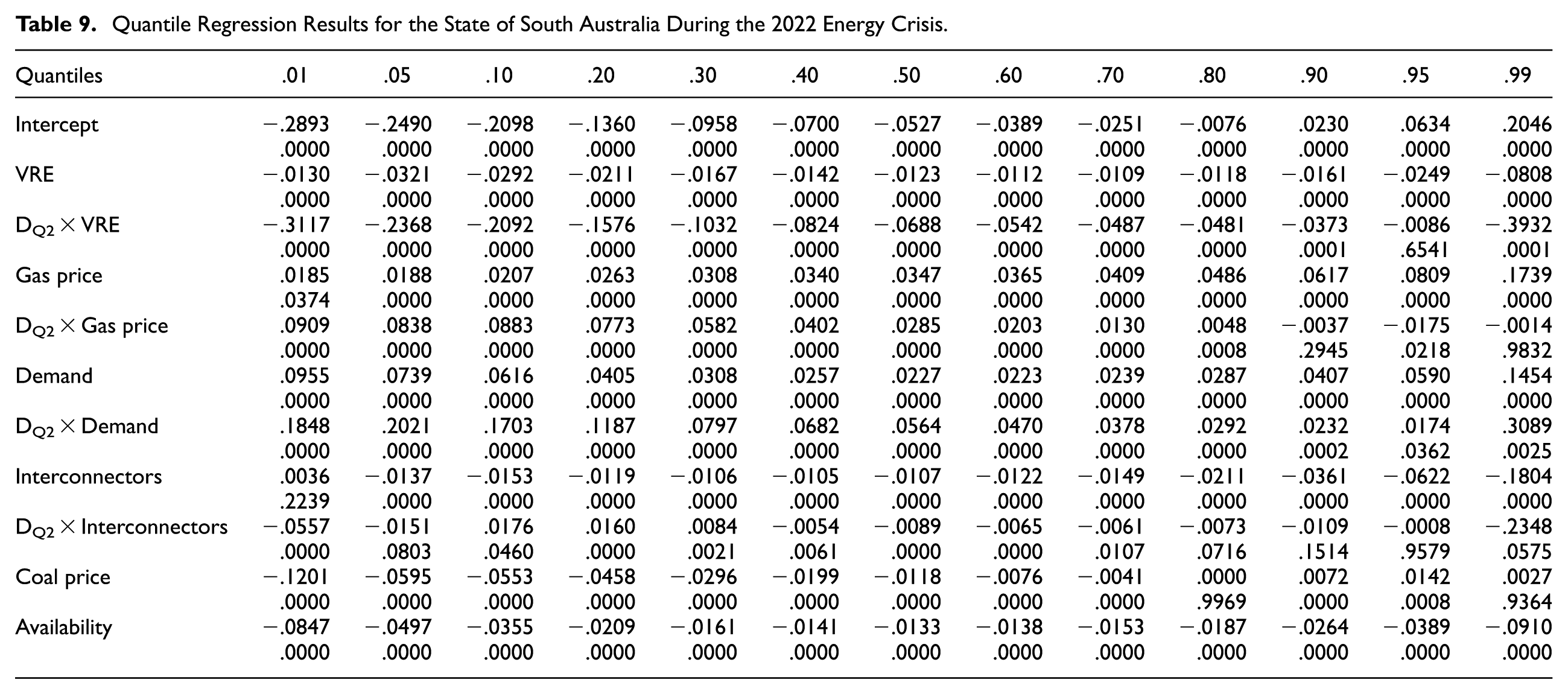

Tables 7 to 11 present estimates of price fundamentals in the distribution of spot prices during the 2022 energy crisis (hereafter referred to as the “energy crisis”) in the NEM. To capture the impact of this event, we employ a dummy variable,

Quantile Regression Results for the State of New South Wales During the 2022 Energy Crisis.

Quantile Regression Results for the State of Queensland During the 2022 Energy Crisis.

Quantile Regression Results for the State of South Australia During the 2022 Energy Crisis.

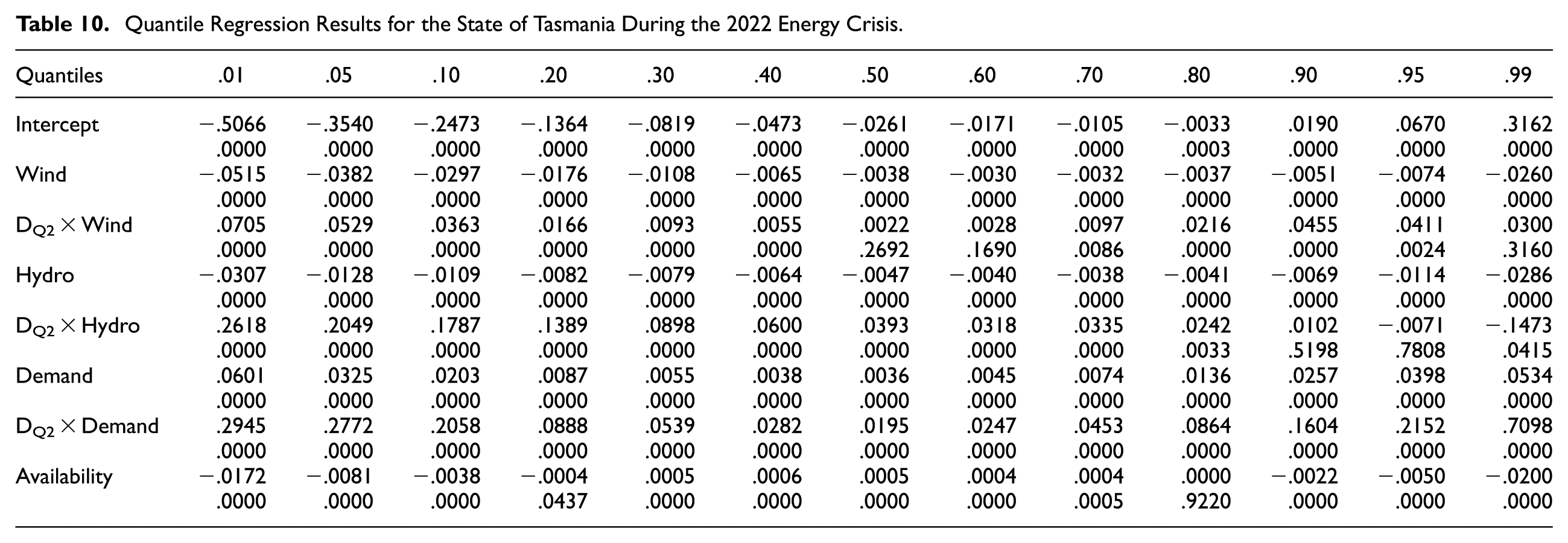

Quantile Regression Results for the State of Tasmania During the 2022 Energy Crisis.

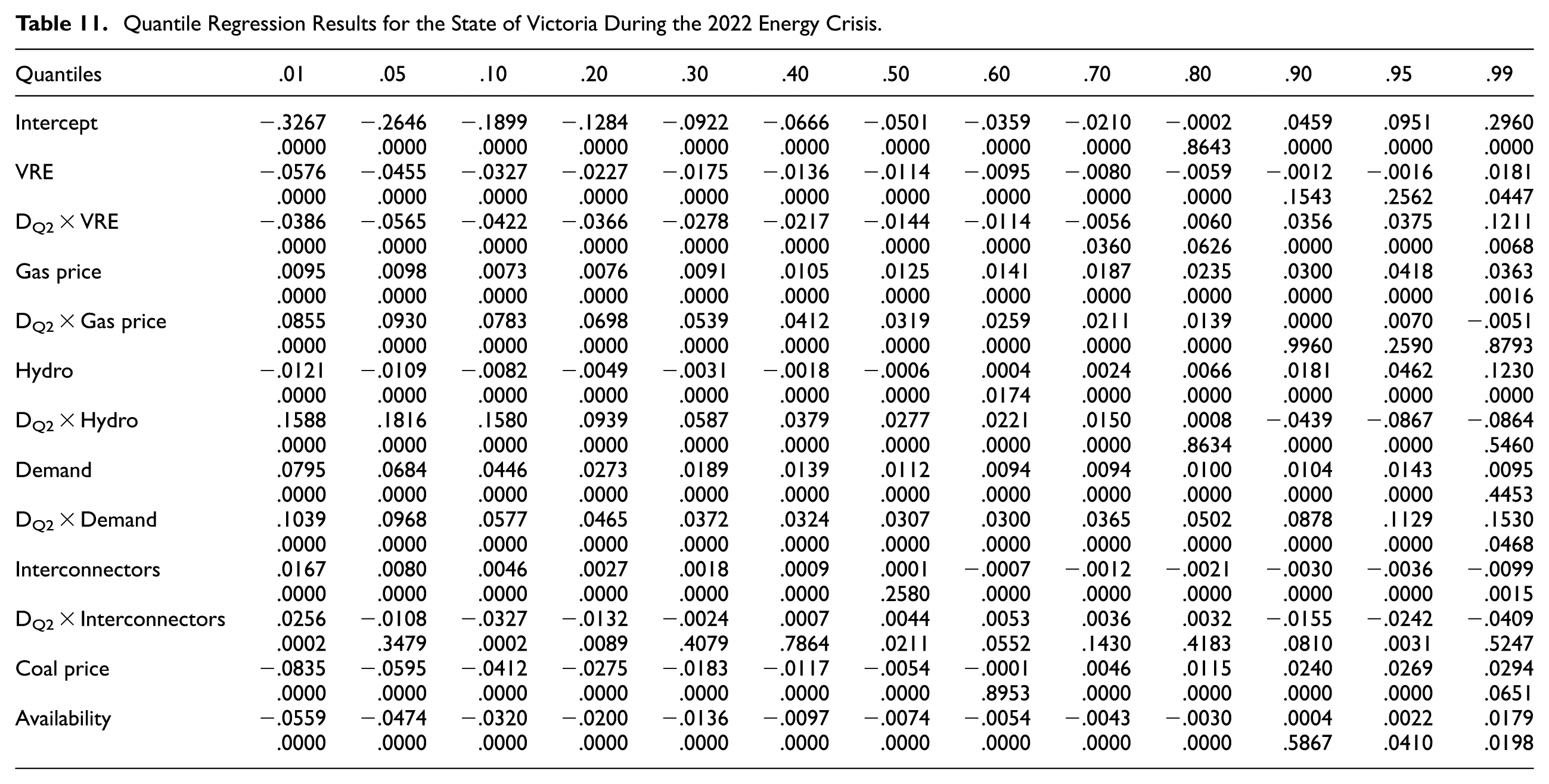

Quantile Regression Results for the State of Victoria During the 2022 Energy Crisis.

We find that gas prices exhibit a significant impact on spot prices during the crisis period, especially in the lower and intermediate quantiles (1%–30%), with the effects decreasing with the quantiles. When considering the lower quantiles, this impact is most pronounced in NSW and QLD, followed by SA and VIC. In NSW and QLD, a 1 standard deviation increase in gas prices positively impacts spot prices by 0.16 and 0.14, and 0.14 and 0.15 standard deviations in the 5% and 10% quantiles, respectively, during the energy crisis period. VIC and SA exhibit a slightly smaller impact of approximately 0.10 to 0.11 standard deviation in the 1% and 10% quantiles. 19 The second quarter of 2022 saw a significant rise in electricity prices, with extended high spot prices accounting for much of the increase. Indeed, across all price-setting technologies (thermal, hydro, and battery), the average marginal prices were higher in 2022 than those of the previous three quarters (ACCC 2022).

Although the impact of gas prices is relatively more pronounced in NSW, we find that the impact of VRE is relatively smaller. This suggests that VRE is still not in a position to counteract the impact of high gas prices in the NEM. Specifically, we observe that an increase in VRE is associated with a slight price decrease of around 0.05 and 0.03 standard deviations in the 5% and 10% quantiles, respectively. However, in QLD, the increase in VRE generation exerts a downward pressure on spot prices at a magnitude relatively close to that at which gas generation exerts an upward pressure on spot electricity prices. This negative pressure decreases with the quantiles, whereas the positive pressure of gas price increases with the quantiles. SA is exceptional, where the increase in VRE generation during the energy crisis period exerts substantial downward pressure on spot prices. This impact is higher than the positive pressure resulting from high gas prices, particularly in the 1% to 90% quantiles of electricity prices. The impact of VRE in VIC during the crisis period is relatively small, with the negative pressure resulting from VRE being smaller than the positive pressure resulting from gas prices in almost all quantiles of spot prices. While our analysis in Section 3.1 indicates a negative effect of wind generation across the distribution of electricity prices, this is not the case during the energy crisis period, where its impact appears to be negligible (with a slightly exception of the 20%–60% quantiles).

We also observe that other variables, such as hydro generation and demand, generally exhibit substantial upward pressure on spot prices during the crisis period across quantiles of spot prices. Demand significantly affects spot prices in VIC and SA across both lower and higher quantiles, while in QLD and NSW, the pronounced effects are mainly observed in the lower quantiles. Hydro generation substantially positively impacts spot prices in the two regions of NSW and QLD in the highest quantile during the crisis period. The impact in other regions is relatively small, with hydro contributing to reducing high price pressure in TAS and slightly in higher quantiles in VIC. The role of interconnectors varies but generally exhibits a marginal contribution to reducing spot prices in the tails of the spot prices.

Our analysis shows that gas prices and electricity demand play a significant role in driving spot price during the 2022 energy crisis in the NEM, particularly in the lower quantiles of electricity prices. While the increase in VRE generation plays a role in reducing spot prices, its impact remains marginal, especially in regions with low to moderate generation levels.

5. Conclusions and Policy Implications

5.1. Conclusions

This study presents a comprehensive examination of the impact of electricity price fundamentals on the distribution of spot prices in Australia’s NEM. It offers the first analysis to investigate the impact of fundamental variables on an entire distribution of electricity prices. We demonstrate that both wind and solar generation negatively affects the lower quantiles of electricity prices. However, their impact on higher quantiles is generally marginal or non-existent, with the notable exception of South Australia, a state with high VRE penetration. A combination of wind and solar generation plays a minimal or no role in reducing electricity prices, when electricity is relatively expansive, compared to when it is relatively cheap. Gas prices remain the most dominant factor in shaping electricity prices, with the combined positive effect of gas prices, electricity demand, and hydro generation outweighing the negative impact of VRE and the negative pressure from interconnector flows.

5.2. Policy Implications

The mixed impact of the fundamental variables across the distribution of electricity prices entail several policy implications for the energy sector.

5.2.1. Incentivizing Further Adoption of Renewable Energy

The fact that VRE exhibits the minimal impact of VRE generation on higher quantiles, which typically correspond to peak demand periods or scarcity of supply, provides a strong need for adopting additional renewable energy policies to encourage the uptake of renewable energy sources in the NEM. There is also a need for governments and electricity market designers to develop a diverse and least-cost optimal mix of renewable technologies with varied designs and locations to ensure their output correlates effectively with current and projected demand. Furthermore, policies should address challenges associated with integrating renewable energy sources into power grids, such as updating grid infrastructure, improving forecasting techniques for VRE, and addressing regulatory or market barriers to VRE integration.

5.2.2. Re-examining the Role of Gas Generation

During periods of high gas prices, spot electricity prices can surge, potentially reaching or exceeding the A$300/MWh cap. This underscores the importance of financial instruments like the “A$300 cap” swap contract as a risk management tool for end consumers, providing budget certainty and mitigating exposure to high spot price swings. However, repeated breaches of the A$300 cap due to high gas generation might increase the demand and cost of these swap contracts, potentially increasing the overall cost of electricity for end consumers if these increased insurance costs are passed down to them. As the overall benefits of renewables depend on the cost of supplemental generators, such as gas generation, integrating relatively low-cost energy sources becomes increasingly important for maintaining electricity affordability in the NEM. Generally, a cost-effective approach to complement renewable energy sources in the NEM involves incorporating a mix of short- and long-duration energy storage, supplemented by zero-emission fuel turbines and demand response mechanisms (Nelson et al. 2023).

5.2.3. Improve Energy Market Resilience

Our examination of the 2022 energy crisis underscores the necessity for comprehensive regulatory frameworks and energy security measures to alleviate the risks and consequences of future disruptions in the NEM due to external shocks. During the crisis, when coal prices soared, and many coal plants went offline, gas generation and opportunity cost hydro played significant roles in determining electricity prices in the NEM. This event serves as an essential reminder for policymakers and energy regulators to guarantee sufficient available supply as most coal plants become uneconomical to operate near the end of their economic life, and VRE generation continues to grow. Robust policy measures must be implemented to ensure that the decommissioning of coal-fired generators aligns with the timely development of adequate renewable generation and firming capacity. Investing in optimal new firming technologies to complement the rapidly growing VRE generation and guaranteeing replacement capacity that can be deployed immediately when existing capacity fails are important steps toward securing the NEM’s energy supply (Nelson et al. 2023).

Footnotes

6. Appendix A

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

1

We include the “availability” data to capture the decrease in available generation capacity during the second quarter of 2022, where several factors resulted in significantly lower output, especially from coal-fired generators. At its peak on 13 June, the volume of generation capacity offline due to planned and unplanned outages was 6.4 GW, corresponding to 29% of the total coal-fired power plant capacity registered in the NEM (![]() ).

).

2

Changes in total generations from year to year, as observed in Figure 1, primarily result from changes in the generation landscape observed in the NEM over the past decade, especially due to the transition from centralized fossil fuel generation to VRE as well as the dynamics of the interconnectors flows. For instance, SA lost all of its coal plant generating units over the period 2012 to 2016 (![]() ). The reduction in supply caused by substantial exits of coal-fired plants has been complemented by a significant increase in VRE generation in the recent years.

). The reduction in supply caused by substantial exits of coal-fired plants has been complemented by a significant increase in VRE generation in the recent years.

3

The decrease in supply due to the retirements of coal-fired plants, coupled with the lack of new “dispatchable” plants entering the market, significantly high gas and coal fuel costs, and the introduction and repeal of a carbon pricing mechanism, have been the primary drivers of the rise in spot prices and volatility in the NEM over the last decade (Mwampashi et al. 2021; Rai and Nunn 2020; Simshauser and Gilmore 2022; ![]() ). Despite the substantial increase in VRE penetration, its effect was generally not sufficient to offset the high prices observed during 2016 to 2019 period, as evidenced by the minimal contribution of low and negative spot prices to overall average price levels.

). Despite the substantial increase in VRE penetration, its effect was generally not sufficient to offset the high prices observed during 2016 to 2019 period, as evidenced by the minimal contribution of low and negative spot prices to overall average price levels.

4

In the NEM, the market price cap (MPC, also known as the value of lost load) is A$15,500/MWh compared to Euro 3,000/MWh in Europe—approx. A$4,620.32/MWh: Exchange rate 1 Euro = A$1.54 (Boston Consulting Group, 2022). Typically, prices range between A$30 and 100/MWh. However, during periods of excess supply, prices can plummet to the market price floor (MPF), −A$1,000/MWh. Conversely, during times of scarcity, prices can surge up to the market price cap of A$15,100/MWh (![]() ).

).

5

Intraday data are characterized by a high degree of seasonality, namely intraday, daily, monthly, and yearly (see ![]() for further discussion). The indicator variable

for further discussion). The indicator variable

6

Morning and evening hours in hour-to-hour analysis are specific times of the day, not necessarily related to the statistical distribution of prices. Prices could be routinely high or low during these times but don’t necessarily capture the unpredictability or the extremities associated with the true statistical tails (like those caused by unforeseen outages or sudden demand surges).

7

The 99% quantile, or the 99th percentile, is a value below which 99% of the observations may be found. The fact that this value aligns closely with the A$300/MWh cap for swap contracts is of significant interest. It implies that the cap is set just above the price level that is exceeded 1% of the time, providing protection against extreme price events. Note that the standard cap contract commonly traded in the NEM is the “A$300 cap,” which serves as a hedge against spot prices above A$300/MWh (AEMC 2023a).

8

The top panels of Tables 2 to ![]() show the impact of individual variables, and the bottom panels shows the impact of aggregated variables. The coefficients for each variable in the model are displayed, along with their corresponding p-values. Full results tables, which include dummy variables, can be provided for a more in-depth analysis upon request.

show the impact of individual variables, and the bottom panels shows the impact of aggregated variables. The coefficients for each variable in the model are displayed, along with their corresponding p-values. Full results tables, which include dummy variables, can be provided for a more in-depth analysis upon request.

9

As noted in Table A3 in ![]() , coal price data is available only monthly, requiring replication of values to align with the high-frequency analysis. Including these values aims to reduce potential endogeneity bias. Consequently, the estimated coefficient may not accurately represent the true effect, given the assumptions made.

, coal price data is available only monthly, requiring replication of values to align with the high-frequency analysis. Including these values aims to reduce potential endogeneity bias. Consequently, the estimated coefficient may not accurately represent the true effect, given the assumptions made.

10

The finding that demand has a higher impact on electricity prices, particularly when they are high, suggests that the supply curves in Australia’s energy markets are S-shaped. Operators of coal power plants may offer prices below marginal costs, including negative prices, just to stay online. This occurs due to the inflexibility of coal plants and their high start-up costs.

11

Generation plants submit bids every five minutes indicating the lowest price they are willing to accept to produce electricity. These bids are supposed to represent the plant’s short-run marginal cost (SRMC). The system uses a merit order to dispatch plants, starting with the lowest bidders and adding higher-priced plants until the demand is met. The market price of electricity is set by the highest bid among the generators needed to meet demand. Every dispatched generator is paid this market price, which for some means earning significantly more than their SRMC, thereby providing a return on their investment (![]() ).

).

12

Despite the interconnected nature of the regional markets, there remains an issue of coinciding minimum supply and maximum demand. Around 7 pm (EST), particularly in TAS and VIC, wind output is at its lowest, solar output is near its minimum, and the NEM experiences maximum demand. Also, there is a considerable variation across different seasons (![]() ).

).

13

The observed positive impact of solar generation on spot electricity prices, especially during the evening when solar generation is down due to the higher marginal costs of generation associated with fast start-up and flexible plants—and ramping costs associated with coal-fired power plants aligns with several findings, including Bushnell and Novan (2021) in California’s electricity market, Mountain et al. (2018) and Mwampashi et al. (2022) in Australia (NEM), Jha and Leslie (2020) in Australia (Wholesale Electricity Market (WEM)), and ![]() in Israeli electricity market.

in Israeli electricity market.

14

Empirically, we use the aggregated regional output from run-of-river and pumped hydro plants. However, we acknowledge that the two types of plants can have different impacts on prices.

15

16

In Australia, the dramatic increase in rooftop generation is exerting substantial downward pressure on grid electricity prices in the middle of the day, which has resulted in very low or even negative prices when the sun is at its peak. The frequency and magnitude of these negative prices have also increased over time, with supply often exceeding demand (Mwampashi et al. 2021; ![]() ).

).

17

It worth acknowledging that these results could be influenced by a single value for the entire month assumption highlighted in Footnote 9. However, we believe that multicollinearity does not significantly influence our findings. Overall, we found no evidence of significant strong correlation between variables (please see 6.1 for further discussion).

18

To estimate the impact of fundamental variables during the energy crisis in Tables 7 to ![]() , we need to consider the coefficients of these variables and their interaction terms. For instance, given the coefficients for VRE and

, we need to consider the coefficients of these variables and their interaction terms. For instance, given the coefficients for VRE and

19

In SA, the impact is the least pronounced among all three regions, even though the region relies heavily on gas generation. This observation, however, does not apply to the 99% quantile, wherein a substantial impact—approximately 0.17 standard deviations—is observed for each standard deviation increase in gas prices. This outcome can be attributed to the dominance of high wind and solar generation, which is greater in SA than in any other state within the NEM.