Abstract

There is currently an intense debate in Europe on the allocation of transmission capacity in the internal electricity market. In this context, the concept of market-based re-dispatch has regained considerable attention, as a candidate design to reconcile the zonal organization of the market with a pricing system that supports efficient real-time dispatch. In this paper, we study the problem of capacity expansion under zonal pricing with market-based re-dispatch. We propose a formulation of the problem as a mixed linear complementarity problem and analyze the existence and efficiency of solutions, both from a theoretical and empirical perspective. We find that zonal pricing with market-based re-dispatch leads to large efficiency losses. Moreover, although there exist theoretical conditions under which the efficiency of the design could be improved by means of regulatory interventions, the strictness of these conditions renders their practical implementation difficult and, therefore, the full recovery of the efficiency unlikely.

1. Introduction

1.1. Motivation

The debate between nodal and zonal pricing is an old story in the evolution of the U.S. power system. In their three-phase review of the history of the process, Hobbs and Oren (2019) note, almost in passing, that the subject had been settled in the first phase, namely after the California experience: the zonal system had fundamental flaws that the nodal system avoided. The Texas experience came a bit later but confirmed the observation (Triolo and Wolak 2021). The situation is quite different in Europe: a recent report (ACER 2022) issued in response to criticisms against the high prices observed in the power market in the end of 2021 (i.e., well before the perturbations on the gas market induced by the events in Ukraine) argues that the current European (zonal) system is functioning properly, but that one might consider some improvements, among which a reduction of the size of the zones. In particular, the nodal system is mentioned as an example of this reduction (ACER 2022, 27). This difference between the U.S. and EU points of view after so many years of theory and experience on a subject that looks purely technical is strange and must have some fundamental explanation. It cannot be a misunderstanding of the nodal system, which had been described in the French literature as early as Boiteux and Stasi (1952). But institutions suggest a possible reason for divergent points of view. The restructuring of the power system in Europe was part of the integration of sectoral markets that created the internal market in 1992, with delays expected in “difficult sectors,” electricity being one of them. It suffices to note, here, that a nodal model in an integrated European market would have merged national systems and interconnections into a new supranational model where all components of national networks would be placed on the same footing. Conversely, the coupling of the zonal national systems maintained their individuality and developed a framework facilitating exchanges between them through interconnections. In other words, the nodal system in the internal EU market would have had a supranational flavor that the zonal system was thought to be able to bypass.

As a consequence of the institutional barriers, the EU internal electricity market developed in general at a slower pace than their U.S. counterparts. This can be observed for instance in how the EU market has been organized originally around the day-ahead market, which has, until recently, been viewed as the spot market. Re-dispatching and balancing are instead seen as services used to maintain as much as possible the day-ahead positions. Continuous efforts have been made to gradually improve on this basic design with, for instance, the development of platforms to coordinate the activation of balancing capacity (MARI and PICASSO) or the efforts to integrate more precise scarcity pricing. There is, however, an intrinsic limit to these improvements, which is that the exact conditions under which electricity trading takes place are known only in real time. Therefore, as argued in Harvey and Hogan (2022), “Any pricing system that sets prices that are inconsistent with the real-time dispatch necessarily requires discriminatory pricing, limits on access, constrained-on and –off payments, or reliance on command and control to maintain reliability.” With the increasing integration of renewable resources and distributed energy resources, which bring more variation and uncertainty in the grid, the reliance on these ad-hoc measures becomes increasingly complicated. In this context, market-based re-dispatch represents a seemingly appealing modification to the European design, introducing a pricing system that is closer to the real-time dispatch without completely questioning the zonal organization. Market-based re-dispatch draws indeed more and more interest among EU market design discussions, as witnessed by the fact that it is now the default option in the regulation (European Parliament, Council of the European Union 2019).

At the same time, there has recently been an increasing interest in local flexibility markets, for which a certain number of pilots are emerging all over the continent (Frontier Economics and ENTSO-E 2021). It is interesting to note that the primary use of these local flexibility markets is congestion management, as revealed in a poll of Nordic DSOs (Hackett et al. 2021). Therefore, most of these initiatives work on the principle of locational pricing, which implies that opportunities exist for inc-dec gaming.

In times of energy transition, it is therefore crucial to understand the relationship between power generation investment and a short-term market design based on zonal pricing followed by market-based re-dispatch. Our interest in this paper is to analyze this question from a computational perspective, by proposing a model of a long-term competitive equilibrium under this design. Along with the development of the model, we propose a solution methodology that enables the computation of an equilibrium on large-scale instances, and apply it on a realistic instance tailored to the Central Western European network.

1.2. Related Literature

There is an existing stream of literature centered on the quantitative analysis of zonal pricing with market-based re-dispatch. In the early days of the discussions on market-based congestion management in Europe, De Vries and Hakvoort (2002) analyzed five different designs among which uniform pricing followed by market-based re-dispatch, which was then referred to as countertrading. The authors proposed a stylized two-node one-zone example and concluded that, in theory, countertrading is efficient in the short term. The model does not account for inc-dec gaming, which is an important aspect in market-based re-dispatch. Potential inefficiencies stemming from deviations from this idealized setting analyzed in the paper are discussed qualitatively in the work of De Vries and Hakvoort (2002).

One situation that could be associated to inefficiencies in market-based re-dispatch in the short term takes place when the TSO does not act as a price-taker in the re-dispatch market. This situation is analyzed by Grimm et al. (2018) under the assumption of absence of inc-dec gaming. The authors show, on an illustrative example, that, in this case, the outcome could be inefficient.

An important drawback of re-dispatch markets is that they offer the possibility to market participants to engage in arbitrage between the zonal and re-dispatch price, the so-called inc-dec game. This leads to a distortion of long-run investment incentives as well as the extraction of short-term rents by those exercising the gaming strategy for essentially offering nothing to the system. This situation is analyzed quantitatively in Holmberg and Lazarczyk (2015). The authors show that inc-dec gaming is an arbitrage strategy that also occurs under perfect competition. They conclude that, under certain restrictive assumptions, zonal pricing followed by market-based re-dispatch is efficient in the short term, and the outcomes only differ by a redistribution of the welfare.

More recently, Hirth and Schlecht (2020) proposed a simple model on a two-node one-zone example in order to analyze inc-dec gaming. The authors emphasize that the design leads to undue arbitrage opportunities for market participants, even when they cannot exercise market power. The authors further discuss the conditions under which this arbitrage is exacerbated or can be mitigated.

Our work also relates to an emerging stream of literature on the study of the impact of locational instruments in zonal markets from a quantitative perspective. The first paper that tackles this problem quantitatively is Grimm et al. (2019). The authors propose a tri-level model of the long-run equilibrium of zonal pricing with cost-based re-dispatch. The tri-level structure aims at representing the sequential nature of the problem: grid investment by the TSO, capacity investment by private firms and re-dispatching in the short term by the TSO. A simplified spatially differentiated capacity signal based on average nodal prices is then added to the model. The authors find that, although it influences the location of investment, the introduction of a well-calibrated capacity signal only slightly improves welfare, as the signal fails to also impact the operational efficiency of the system. Schmidt and Zinke (2020) study the impact of uniform pricing in Germany on the siting of wind generation. They find that nodal pricing, by incentivizing the siting of investment closer to load centers and thereby reducing wind curtailment, has a positive effect on welfare. The paper also investigates the restoration of a locational component to the uniform price through capacity-based latitude-dependent connection charges. However, the authors find that these simplified locational instruments are not adequate for mitigating the inefficiencies associated to uniform pricing. Finally, Eicke (2021) proposes a model for quantifying the optimal capacity-based locational signal for restoring the efficiency of investment in zonal pricing with cost-based re-dispatch. Unlike the two papers previously cited, this paper is the first to consider a technology-differentiated signal. The author shows that differentiating by technology is a necessary condition for restoring the efficiency of nodal pricing. They find that, although locational capacity signals have a significant cost-saving potential, they do not lead to a full recovery of the efficiency of nodal pricing.

1.3. Contributions

This paper contributes to the existing literature in the following ways:

Our main contribution is to propose a model that internalizes the investment decisions of private firms in generating capacity in a zonal market design with market-based re-dispatch. We show how the loss of efficiency of this design originates from its mathematical formulation and formally establish the existence of a resulting equilibrium.

Based on this modeling framework, we discuss the theoretical conditions under which the long-run efficiency of nodal pricing can be recovered in a zonal pricing market with market-based re-dispatch.

We show how to integrate market monitoring considerations in the analysis of the long-term equilibrium by imposing limitations on the deviation from truthful bidding for market participants.

Finally, we provide simulations of the long-term equilibrium in zonal pricing followed by market-based re-dispatch on a large-scale instance of the Central Western European (CWE) network area and compare its efficiency to nodal and zonal pricing benchmark designs.

1.4. Organization of the Paper

The paper is organized as follows: we start, in section 2, by presenting our model of zonal pricing with market-based re-dispatch in the short term. Then, section 3 extends the model to the case of the long-term equilibrium and discusses how the integration of long-term considerations leads to a loss of efficiency of the design. In section 4, we analyze how efficiency can be restored by means of additional market instruments. Section 5 extends our model to incorporate an endogenous representation of market monitoring that limits zonal-nodal arbitrage. Finally, in section 6, we present the results of our case-study before discussing some concluding remarks in section 7.

2. Short-term Equilibrium

2.1. Model

We start by presenting a simple model of zonal pricing followed by market-based re-dispatch (abbreviated MBR hereafter) in the short term, that is, when investment decisions in generation capacity are ignored. The re-dispatch problem that we consider in this paper is an economic dispatch with nodal transmission constraints and pay-as-cleared settlements. We model the economic equilibrium on the electricity market as a Nash equilibrium between three types of agents: a single TSO, the producers, and a Walrasian auctioneer that enforces market clearing conditions (i.e., a power exchange). In order to focus on the impacts of MBR on the short and long-term equilibria, we adopt a set of simplifying assumptions that allow us to isolate the effects related to this congestion management policy. In particular, we assume that the market is perfectly competitive and we model the agents as price takers. This implies that we ignore market power. Although real markets deviate from the situation of perfect competition, our view is that it remains essential to understand the performance of market designs under perfect competition, as it is unlikely that identified inefficiencies will disappear in imperfectly competitive markets. The assumption of perfect competition allows us to keep the models transparent and tractable.

Note that absence of market power also forces us to question the terminology of “inc-dec gaming.” Indeed, the market design that we analyze in this paper modifies the opportunity cost of participants in the zonal market with the introduction of the subsequent re-dispatch market. This means that their cost is now an opportunity cost which differs from their marginal production cost. In our setting, participants would thus still bid at cost, whereas inc-dec gaming suggest some kind of strategic behavior due to market power. Therefore, in order to avoid any confusion, we refrain from using the terminology “inc-dec gaming” and, instead, refer to

In addition, we assume that the profit-maximizing problems of all agents are linear and that there are no intertemporal operating constraints: in the short run, all periods are independent. We consider that producers can invest in generation capacity in a continuous way, and we ignore transmission capacity expansion, for which the continuity assumption would be unrealistic.

Electricity demand is assumed to be known and inelastic. We make this assumption in order to keep the equations and the theoretical analysis as simple as possible, but we note that our model, as well as the theoretical results, naturally extend to the case of active demand-side participation. The logic is that consumers can also engage in price arbitrage between the two sequential markets, in a symmetrical way as the behavior of the producers. This is formally shown in Appendix B, where we discuss extensions of our model to different types of market participants, including active consumers. We also show that the results of the paper naturally extend to these different cases.

Finally, our model is deterministic and we assume perfect foresight. This implies in particular that market participants are able to perfectly anticipate the subsequent re-dispatch price when bidding in the zonal market. We note that this is a strong assumption that is not likely to be verified in practice. As noted in Hirth and Schlecht (2020), exercising price arbitrage would expose market participants to risk, which would probably limit the degree to which participants would be willing to exercise this arbitrage if risk aversion is taken into account. In the present paper, we abstract from uncertainty considerations to keep the model transparent, computationally tractable and absent of additional considerations regarding risk aversion and the forecasting abilities of agents. The endogenous modeling of uncertainty in the context of market-based re-dispatch is relegated to future research. Note that the perfect foresight assumption also allows us to omit N-1 security constraints in the representation of transmission capacity.

We now proceed to the sequential description of the profit-maximizing problems of each agent under our set of assumptions.

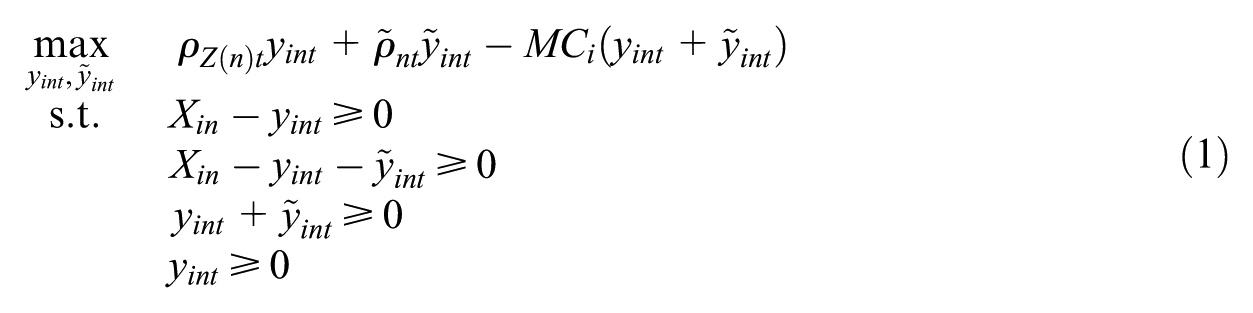

Producers

The producers with technology

The constraints of problem (1) ensures that the quantities cleared in both the zonal and re-dispatch markets are physically feasible. 1 Note that here, again, we use a basic producer model to keep the equations and the theoretical analysis as simple as possible. However, it should be noted that the results that we present in this paper are robust to the specific representation of market participants. In particular, under the assumptions of absence of market power and perfect information, the results naturally extend to renewable resources and storage units. The reader is referred to Appendix B for a formal discussion of the extension of our model to the case of renewable and storage resources.

We split the description of the TSO problems in the zonal and re-dispatch markets in the interest of clarity. As the two problems are completely independent, this can be done without loss of generality.

TSO in the Zonal Market

The TSO maximizes its profit from the transmission of electricity given the zonal prices by controlling the net position of each zone (

where

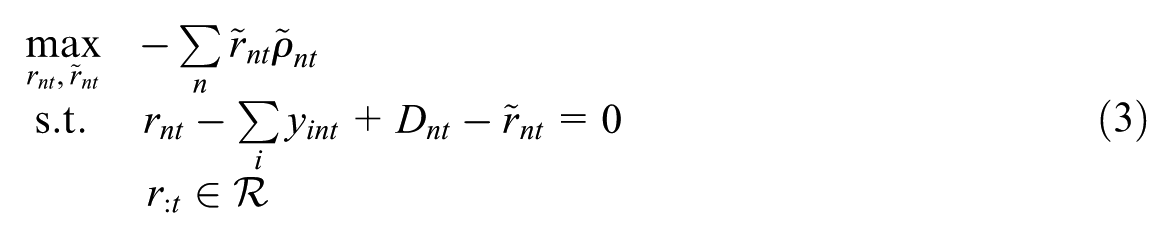

TSO in Re-dispatch Market

In the re-dispatch market, the TSO has to buy re-dispatch resources (

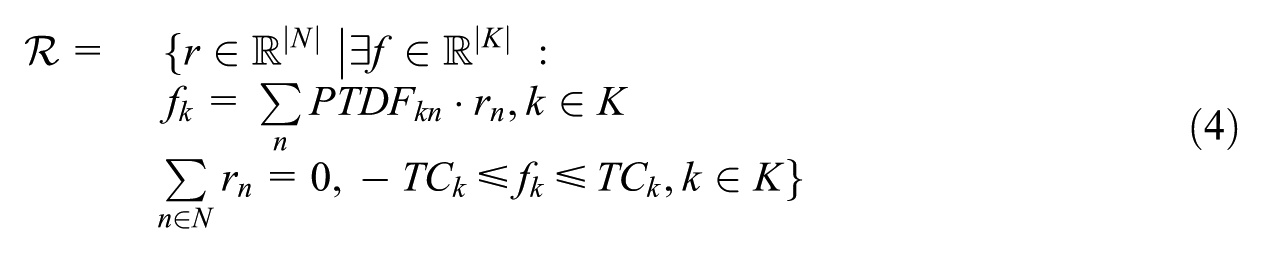

Note the fundamental difference between the formulations of the zonal market and nodal re-dispatch market: whereas the zonal market only imposes constraints on the zonal net positions

where

Auctioneer in the Zonal Market

In the zonal market, the auctioneer determines zonal prices while ensuring that the market clears in every zone of the network. This function can be represented as a profit-maximizing problem for zone

Auctioneer in the Re-dispatch Market

Similarly, the auctioneer of the re-dispatch market ensures the TSO’s demand for re-dispatch resources matches its supply from market participants.

It is important to note that the right solution concept for this game is that of a generalized Nash equilibrium (GNE). Indeed, the feasible set of the TSO in the re-dispatch market, as described in Problem (3), is based on the nodal net injections in the physical dispatch that depend on the production in the zonal market. This implies that it is not equivalent to a single optimization problem. Nevertheless, the equilibrium can still be formulated as a single problem in the form of a mixed linear complementarity problem (MLCP).

Equivalent MLCP

The equivalent MLCP can be obtained by aggregating the KKT optimality conditions (which are necessary and sufficient for linear programs) of the profit-maximizing problem of every agent. Using Greek letters for denoting dual variables for each constraint, we obtain the following MLCP:

where we define

and

which are well-defined as both

This MLCP formalizes the short-term equilibrium in markets with zonal pricing and MBR, such as the one that is described on a simple one-zone two-node network in Hirth and Schlecht (2020). It can thus be used to characterize and represent quantitatively the so-called inc-dec game in perfect competition, which is in reality an arbitrage between the zonal and re-dispatch market.

In the short term, although the equilibrium cannot be formulated as a single LP, a further simplification of the MLCP can be obtained by observing that the part of the problem that relates to the re-dispatch market is independent of the part that relates to the zonal market. More precisely, let us consider the MLCP obtained by isolating the equations related to the re-dispatch problem only, that is, the MLCP made of equations (7b), (7d), (7e), (7h), (7i), (7j), (7k), and (7m). If we denote by

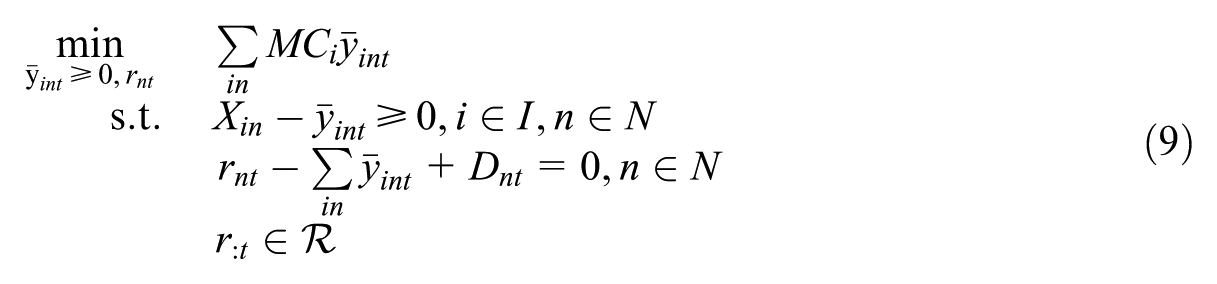

Problem (8) fully characterizes the solution to problem (7) for the variables associated to the re-dispatch market, that is, the variables denoted with the tilde. Observe that MLCP (8) is exactly the set of KKT conditions of the nodal economic dispatch problem:

This means that the physical dispatch, obtained after the re-dispatch market, corresponds to the optimal solution of the nodal economic dispatch.

Now, let us look in further detail at the MLCP obtained by isolating the equations related to the zonal market, that is, the MLCP made of equations (7a), (7c), (7f), (7g), and (7l). Equation (7b) implies that

Accounting for this simplification, we get that MLCP (7a), (7c), (7f), (7g), (7l) is exactly the set of KKT conditions of the following optimization problem:

That is, the zonal part of the problem corresponds to a zonal economic dispatch problem where the marginal cost of technology

The decomposition between the zonal and re-dispatch parts of the problem that we have just highlighted has two important implications in the short term regarding (i) the solution methodology for solving the equilibrium, that we discuss in section 2.2 and (ii) the efficiency of the equilibrium, that we discuss in section 2.3.

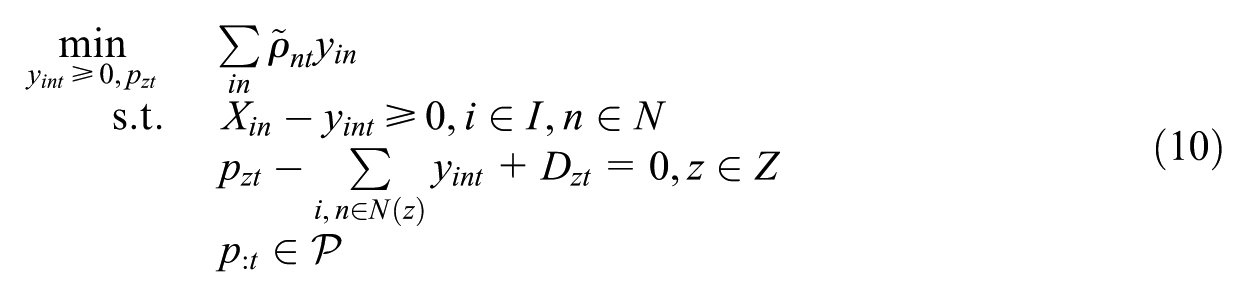

2.2. Solution Methodology

The decomposition between the zonal and re-dispatch parts reveals a simple two-step solution methodology for obtaining an equilibrium of zonal pricing followed by MBR in the short term, that we present in Algorithm 1. Note that this is implicitly the methodology that is used by Hirth and Schlecht (2020) to identify an equilibrium in their illustrative example: they assume that the opportunity cost of bidding in the zonal market corresponds to the nodal prices and then check that the assumed prices on the re-dispatch market turn out to be correct.

2.3. Efficiency

A second implication of the decomposition of the problem between the zonal and re-dispatch parts is the efficiency of the design in the short term. A design is efficient if it leads to the same total cost as the centralized optimization problem, which, in our case, corresponds to the nodal economic dispatch problem introduced in equation (9). The efficiency result is formalized in Proposition 1.

The proofs of all propositions of this paper are provided in Appendix A.

Our model assumes implicitly that there is no irrevocable decision with respect to the outcome of the zonal pricing auction. This is a crucial assumption for Proposition 1 to hold. In particular, we assume that there is no unit commitment decision made based on the zonal auction and that the zonal net positions cleared in the zonal auction are not firm and can be freely modified during the re-dispatch phase, which implies that the TSOs coordinate perfectly, which includes resorting to cross-border re-dispatch. 4

Proposition 1 should be seen as closely related to Proposition 4 of Holmberg and Lazarczyk (2015) which also states that zonal pricing with MBR is efficient in the short run under a slightly different framework and assumptions. In particular, Holmberg and Lazarczyk (2015) assume that the TSO sets the inter-zonal flows to their level in the efficient dispatch. This assumption is related to our assumption of perfect TSO coordination in the re-dispatch stage: both assumptions imply that the efficient dispatch can be recovered during the re-dispatch stage.

2.4. Results on an Illustrative Example

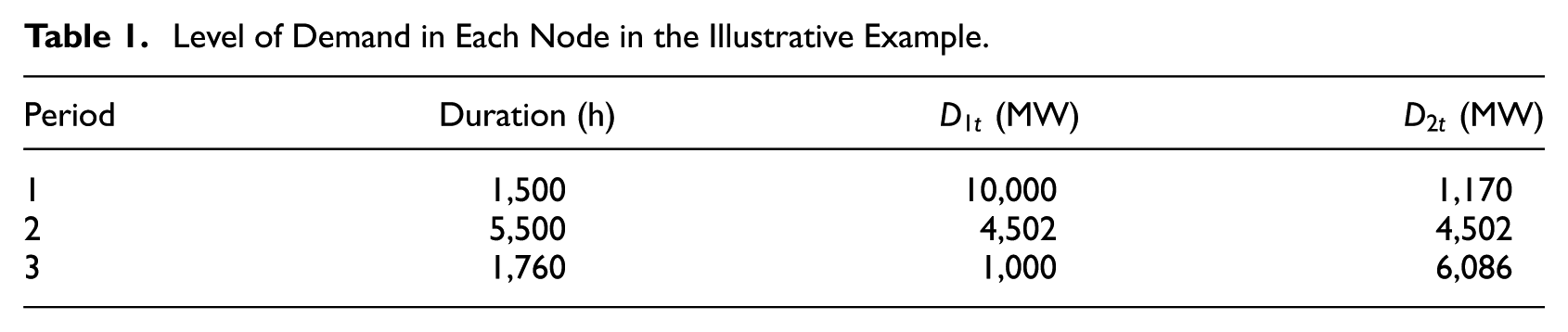

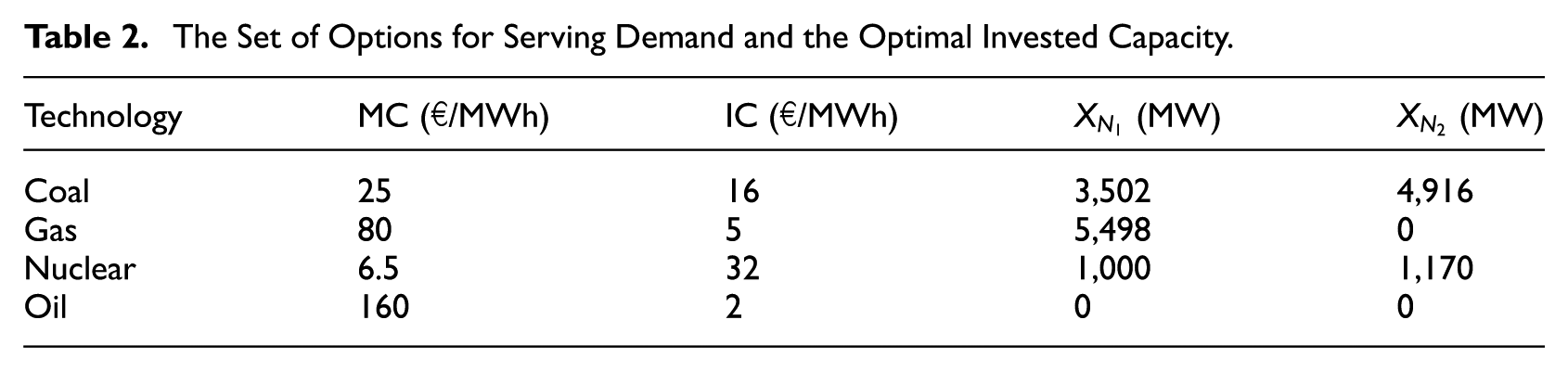

In order to illustrate our model, we present in this section its results on a small example. We use the simplest possible network configuration that can be used to illustrate a zonal design: two nodes linked by a fictitious line of 0 MW of capacity, grouped into a single zone. We assume that the one-year time horizon is divided into three periods of different duration in which the demand is constant in both nodes. The duration of the period as well as the level of the demand in each period and in each node is displayed in Table 1. Finally, we assume that there are four technologies available for serving the demand, with constant marginal and investment costs, as shown in Table 2. In the short-term equilibrium, the capacities need to be fixed. We assume that they are fixed at the level that is indicated in Table 2. 5 As the transmission line in our example is purely fictitious, the two nodes can be seen as completely independent and the nodal solution can be easily obtained using, for instance, the screening curve method (Stoft 2002) on both nodes. The optimal investment is also shown in Table 2. Using these levels of capacity, one can apply Algorithm 1 to solve for the short-term equilibrium in zonal pricing with MBR.

Level of Demand in Each Node in the Illustrative Example.

The Set of Options for Serving Demand and the Optimal Invested Capacity.

From a qualitative point of view, there are two types of zonal-nodal arbitrage behaviors that can be exercised by producers, depending on whether they expect to be re-dispatched up or down.

The units that will be re-dispatched up in the nodal market (also called constrained-on units) anticipate a higher re-dispatch price than the zonal price. For these resources, it is preferable not to be cleared in the zonal market at all, and sell all their production in the re-dispatch market. As there exists a subsequent market on which they can trade, their opportunity cost is the re-dispatch price that they anticipate, and they have no incentive to bid at a different price than the re-dispatch price in the zonal market.

In a symmetric way, the units that will be re-dispatched down (the constrained-off units) anticipate a lower price in the re-dispatch market. For them, it is preferable to sell all their production in the zonal market at a high price and buy it back in the re-dispatch market at a lower price. Again, knowing that a subsequent market with a different price is coming, their opportunity cost becomes the re-dispatch price, and bidding at the anticipated re-dispatch price becomes their optimal strategy.

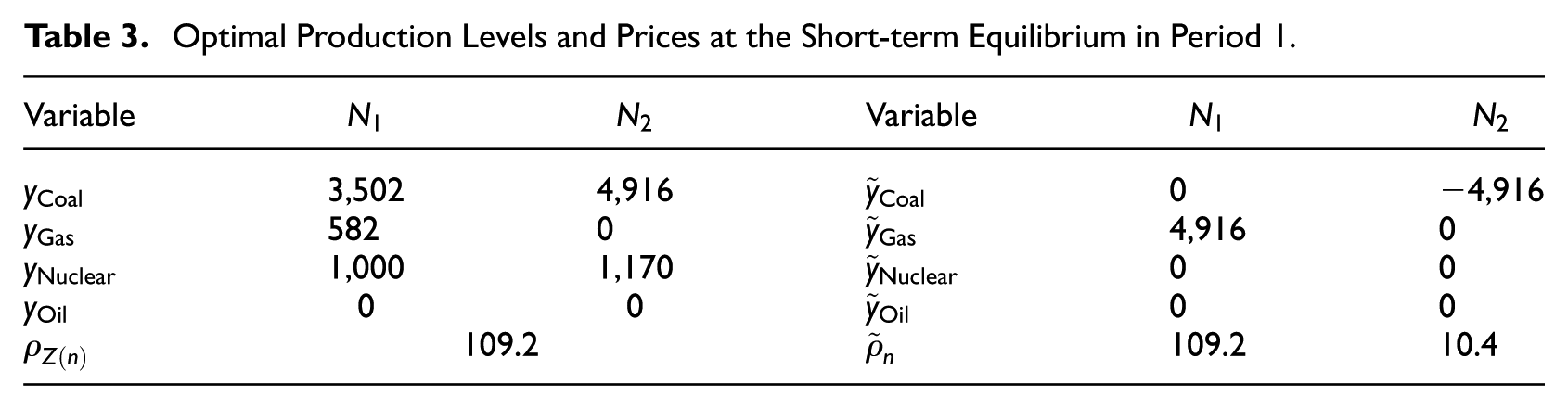

Our illustrative example is a prime example of these two types of arbitrage behaviors. Let us first focus on the results for period 1. The optimal levels of production and prices for this period are shown in Table 3. Here, the Coal unit in

Optimal Production Levels and Prices at the Short-term Equilibrium in Period 1.

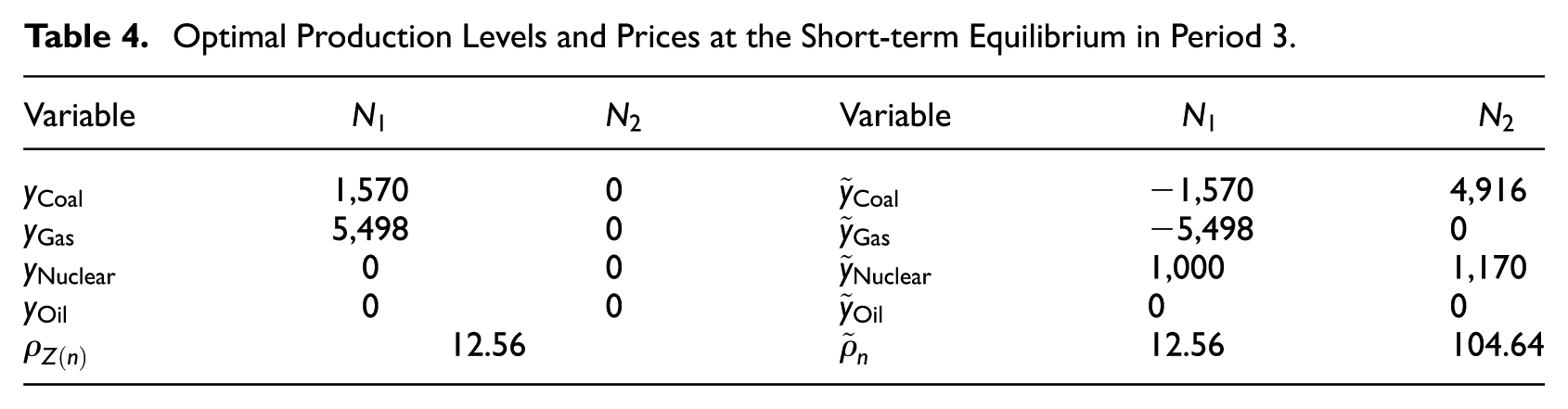

Let us now have a look at the results in period 3, shown in Table 4. Here, the Coal and Nuclear units in Node

Optimal Production Levels and Prices at the Short-term Equilibrium in Period 3.

After the re-dispatch market, nevertheless, the optimal production mix is recovered. The short-term welfare is thus equal to that of the nodal design and the two policies differ only in terms of the allocation of surplus between the different agents. The situation is different in the long term, which is the focus of the next section of this paper.

3. Long-term Equilibrium

3.1. Model

As discussed in past literature (Hirth and Schlecht 2020; Holmberg and Lazarczyk 2015), although efficient under certain conditions in the short term, zonal pricing with MBR distorts the investment signal and, therefore, leads to inefficiencies in the long term. Our goal in this section is to capture these inefficiencies in our model by formulating the long-term equilibrium of zonal pricing with MBR. In order to account for investment in generation capacity, we introduce variable

This problem is the counterpart of equation (9) in the long-term case.

We now turn to the long-term model of zonal pricing with MBR. In perfect competition, investment will be made in technology

Moreover, the investment in capacity modifies the capacity limits in the zonal and re-dispatch markets in the following way:

The MLCP consisting of equations (12), (13), (14), (7a), (7b), (7e) to (7m), with all short-term variables indexed by time period, models the long-term equilibrium of zonal pricing with MBR.

Crucially, the investment condition represented in equation (12) now links together the two parts of the problem related to the zonal market (through variables

Note that condition

Another important question is that of the uniqueness of solutions. However, the loss of equivalence with a single optimization problem implies that less can be guaranteed. One can nevertheless show that for almost all parameter data, the long-run equilibrium has a finite and odd number of solutions. This claim can be proved using the formalism of homotopy theory, following Bidard (2012). The reader is referred to Appendix C for a more thorough discussion of the uniqueness of solutions to the investment problem.

3.2. Results on the Illustrative Example

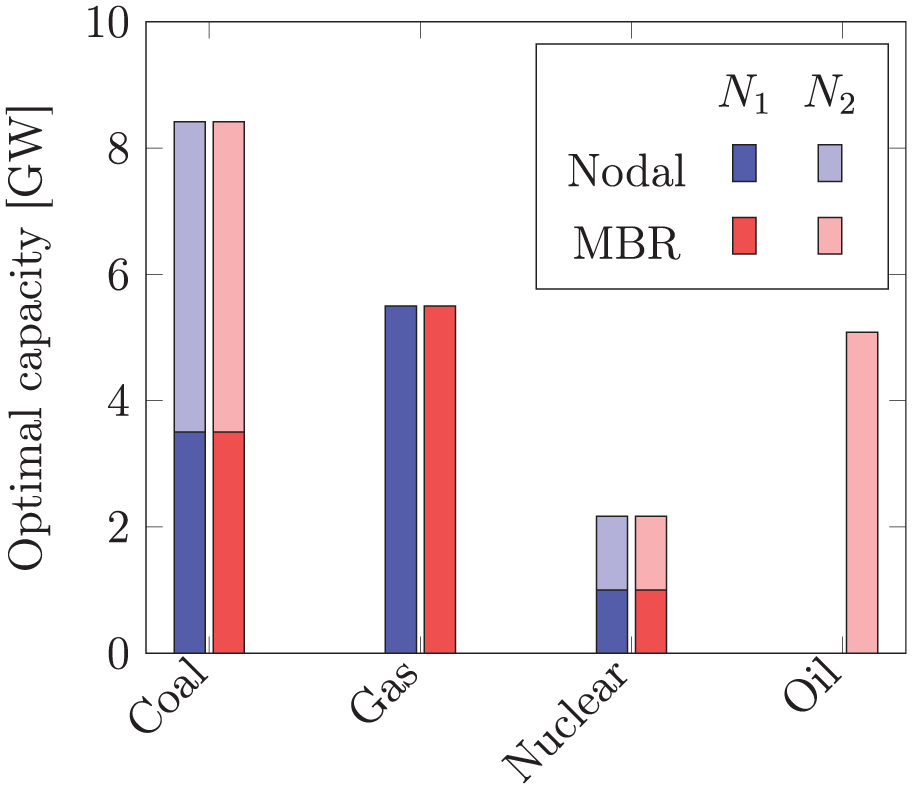

In this section, we illustrate the results of our long-term model on the same example as the one used for the short-term model. Contrary to the short-term case, however, we do not assume any existing capacity. We solve the MLCP using a simple splitting method, that is also used for the case study presented in section 6, and refer the reader to section 6.2 for more details on the solution methodology. Figure 1 shows the optimal capacity mix in both nodal pricing and zonal pricing with MBR. We observe that the optimal mixes are almost perfectly equivalent, with the notable exception that zonal pricing with MBR leads to an additional investment of around 5 GW of Oil capacity in node

Optimal capacity mix in the long-term equilibrium of the illustrative example for both nodal pricing and zonal pricing with MBR.

In the next section, we discuss whether zonal pricing with MBR can be modified in order to restore its efficiency.

4. Restoring Efficiency

In the previous section, we present a model that captures the inefficiencies of zonal pricing with MBR and illustrates these inefficiencies on a simple example. We now investigate whether these inefficiencies can be corrected by modifying the design.

One might first think that removing the asset-backed arbitrage constraint could improve efficiency, as this would eliminate the incentive to invest in ghost plants. They are indeed the source of inefficiencies, as discussed in section 3.2. This would, however, not solve the inc-dec problem. Removing the asset-backed arbitrage constraint is equivalent to allowing pure virtual trade, that is, allowing the participation of purely financial agents who exploit arbitrage opportunities. In this case, there would not exist any equilibrium, as zonal and re-dispatch prices could never perfectly converge. Virtual bidders would thus theoretically be able to extract infinite arbitrage rents.

Instead, we argue that, from a technical point of view, there are two ways to understand the loss of efficiency, and each is associated to a possible modification of the design for restoring efficiency. The first way to understand the loss of efficiency is to observe that the production decision of the producers imposes an externality on the decision set of the TSO, which leads to a market failure. We can therefore resort to the classical theory of Pigouvian taxation in order to understand how efficiency can be restored. Another viewpoint that can be adopted is one in which the loss of efficiency is seen as resulting from the interdependence of the zonal and the re-dispatch markets, as we discuss in section 3.1. A disconnection between the two can be imposed through an additional market instrument. These two ways of recovering efficiency are discussed successively in the remainder of this section.

4.1. Pigouvian Taxation

A Pigouvian tax, named after Pigou (1932), is a well-known way to correct market failures due to externalities. The idea is to force the agent that causes an externality to internalize it, by imposing a tax exactly equal to the marginal cost of the externality at the optimal solution. In our problem, the externality comes from the following constraint in the TSO’s problem:

Following the Pigouvian theory, efficiency can thus be restored by adding

The first term corresponds exactly to the nodal profit for the nodal physical dispatch

where

with

In words,

In that case, however, one can also observe that the zonal market loses its meaning: there is always an equilibrium solution with a zonal price of 0€/MWh. Indeed, the second term of equation (15) then vanishes, and the total profit of the producers is exactly the nodal profit for the nodal physical dispatch.

4.2. Locational Capacity Market

As we mention in section 3.1, the loss of efficiency can also be viewed as resulting from the interdependence between the zonal and re-dispatch markets. This is done through the investment condition, that we recall here:

In this section, we argue that the efficiency of nodal pricing can be recovered by introduction a locational capacity market. The introduction of a capacity price

The capacity market clearing condition reads

where

In Proposition 3, we show that these conditions can be considerably weakened: the efficiency is guaranteed to be recovered even in the case where the locational capacity price is not differentiated per technology and is forced to be positive. 6

The intuition behind Proposition 3 is that, as all market participants have the same opportunity cost when participating to the zonal market, they will earn the same margin. Consequently, there exists a non-negative capacity charge, uniform for all units at the same location, that will cancel out the profits made by the participants through the zonal-nodal arbitrage, which restores efficiency.

The crucial point for this result to hold is thus the fundamental observation that all market participants have the incentive to bid the anticipated re-dispatch price in the zonal market. This is what we prove formally in Proposition 3. As it turns out, under the assumptions of absence of market power and perfect information, this is a robust result that does not depend on the specific representation of market participants used in this paper. We discuss this further in Appendix B.

5. Market Monitoring via Price Cap and Price Floor

As we discuss in section 2, zonal pricing with MBR incentivizes market participants to deviate from truthful bidding in the zonal market, even in the absence of market power. We have seen that the results of the zonal market can be found by solving the modified zonal economic dispatch problem given by model (10), where the marginal cost of participants has been replaced by the expected re-dispatch price at their location, which corresponds to their opportunity cost. In this case, their opportunity cost can be interpreted as the price bid that rational price-taking agents would submit in the market, as we argue in Footnote 3. In practice, however, such a deviation from truthful bidding could catch the attention of the regulator, which would have the opportunity to intervene to prevent such a behavior. Closer market monitoring is indeed sometimes suggested as a solution for improved efficiency in this context (Cramton 2022).

Our interest in the present section is to integrate market monitoring in our model of zonal pricing with MBR. For this purpose, we assume that market participants submit a bid in the zonal market that corresponds to a weighted average of their marginal cost and the anticipated re-dispatch price, that is,

Following the developments in section 2, we know that the MLCP (7), corresponding to the short-term equilibrium of zonal pricing followed by MBR, can equivalently be written, by means of a change of variables, as:

where equations (8a) to (8e) correspond to the complementarity conditions of the nodal economic dispatch, that define the re-dispatch price

Interestingly, letting

Note that problem (21) is not equivalent to the nodal capacity expansion problem, due to the additional term in the objective, which leads to double counting the zonal production cost. MBR without anticipation is thus in general associated to a loss of efficiency in the long term, as we also verify empirically in the case study, presented in the next section.

6. Case Study: Central Western Europe

In this section, we present simulation results for a reduced instance of the Central Western European network area.

6.1. Data

We use the same dataset as in Lété et al. (2022). The area consists of six countries (Austria, Belgium, Germany, France, Luxembourg, and the Netherlands) grouped into five bidding zones, Germany and Luxembourg forming one single zone. Our network is a reduced version of the CWE transmission grid, originally based on the European grid model of Hutcheon and Bialek (2013). Our time series data (hourly demand, solar and wind production in each country) are obtained from the ENSTO-E Transparency Platform for the year 2018. The generation data is obtained from Open Power System Data (2020). Our dataset includes a total of 892 non-renewable units. The models that we use for the case study are generalized versions of the models presented in sections 2 and 3. In the models of the CWE case study, we also consider revenues from reserve provision, where reserve is assumed to be cleared simultaneously with energy. We also consider fixed operating and maintenance costs. Units that cannot cover their fixed costs are decommissioned. We assume that investment is possible in three different technologies, similarly to Ambrosius et al. (2020): CCGT units, OCGT units and Combined Heat and Power CCGT units. Our cost data is sourced from Ambrosius et al. (2020). Wind and solar expansion are accounted for in an exogenous way. Based on the exogenous renewable production, we build a net load duration curve, that we discretize into twenty time periods, in order to obtain a tractable model. The capacity expansion model is then run on a single representative year with twenty types of hours. Load, renewable capacity and existing generators are calibrated for their expected value on future year 2035. The reader is referred to Lété et al. (2022) for more details on the dataset, including specific values for the different costs used in the case study.

6.2. Algorithmic Remarks

As we mention in section 3, the long-term equilibrium of zonal pricing with MBR corresponds to a GNE. The GNE property originates in the imperfect nature of the market as the impacts of the production decisions in the zonal market on the feasibility set of the TSO are not internalized by the producers. From a mathematical point of view, this results in the breaking of the equivalence between the MLCP that aggregates the KKT optimality conditions at equilibrium of each type of agent and the LP that maximizes welfare. However, although the equivalence does not hold, this reasoning suggests a way to leverage this structure algorithmically by resorting to a splitting algorithm. We describe below a basic splitting algorithm for solving the

Step 0. Initialization. Let

Step 1. General iteration. Given

and let

Step 2. Test for termination. If

In our case, a natural choice for matrix

This is the methodology that we use for solving for the GNE corresponding to the long-term MLCP. We note however that we have no guarantee of convergence for this algorithm on our problem and that we observe empirically that convergence is sensitive to the starting point.

6.3. Analysis of the Results

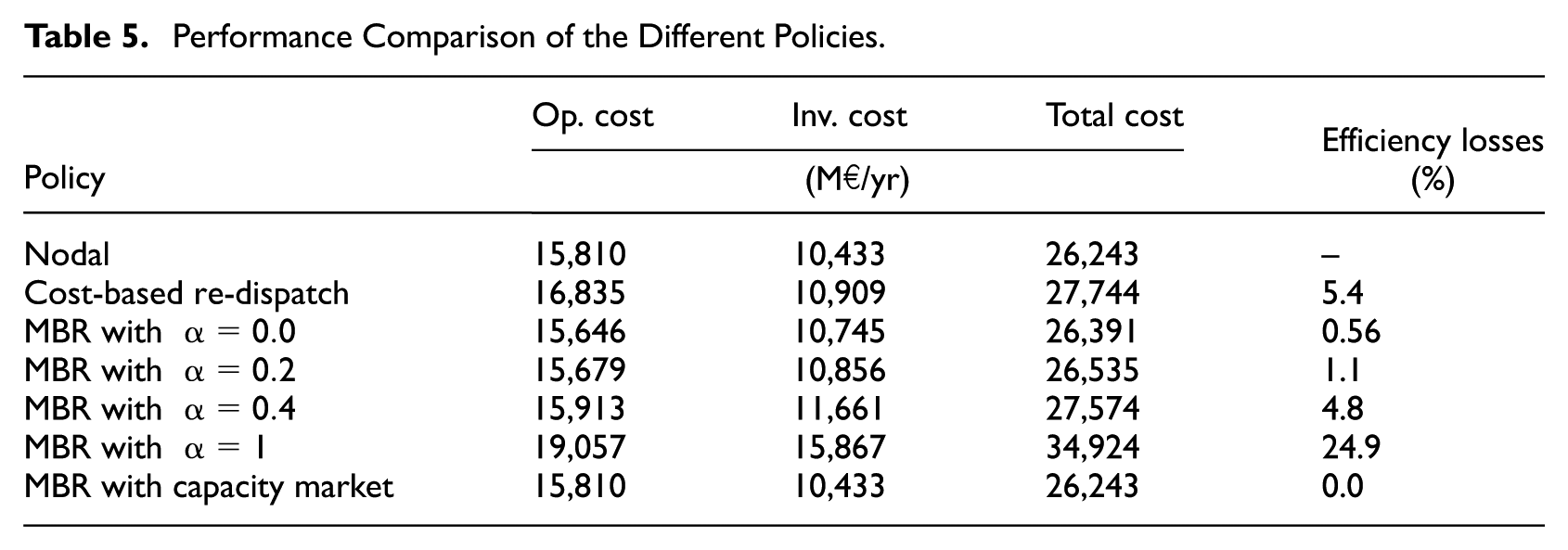

We benchmark the results of zonal pricing with MBR against two other policies: nodal pricing and zonal pricing with cost-based re-dispatch, which ensures that the re-dispatch phase is revenue-neutral for the producers. This policy also leads to inefficiencies in the long term due to the incorrect investment signal that zonal prices represent, as discussed in further detail in Lété et al. (2022). Table 5 presents the performance in terms of total operational and investment costs of the different policies. We observe that, in the long run, zonal pricing followed by MBR is significantly more costly than the nodal pricing benchmark.

7

When

Performance Comparison of the Different Policies.

Still in the case with

According to our results, market monitoring has a very significant influence on the efficiency of zonal pricing with MBR. In the theoretical case of perfect market monitoring, that is, in the case of no anticipation of the re-dispatch by market participants, the efficiency of nodal pricing is almost recovered. The efficiency gap remains small with a close monitoring corresponding to

Note that these results have been obtained under the assumption of inelastic demand. As we note in section 2.1, in practice, consumers could also engage in price arbitrage between the zonal and re-dispatch market. Empirically, the results that we obtain here are thus conservative, and active consumers engaging in price arbitrage can only make things worse. This reinforces our conclusion regarding the inefficiency of the design.

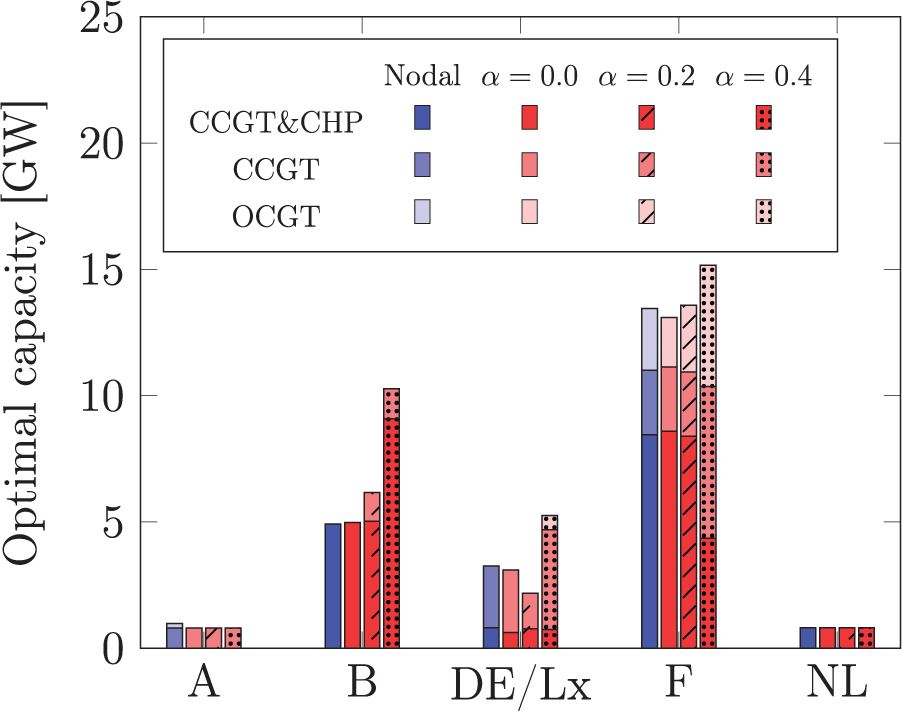

Figure 2 presents the optimal investment in the three candidate technologies for the five CWE bidding zones. One observes that the main difference between the nodal pricing and MBR policies is that zonal pricing with MBR tends to over-invest, especially in technologies with lower investment cost like CCGT and OCGT. This is particularly visible in the case with

Optimal capacity in the long-term equilibrium in nodal pricing and zonal pricing with MBR, decomposed by bidding zone.

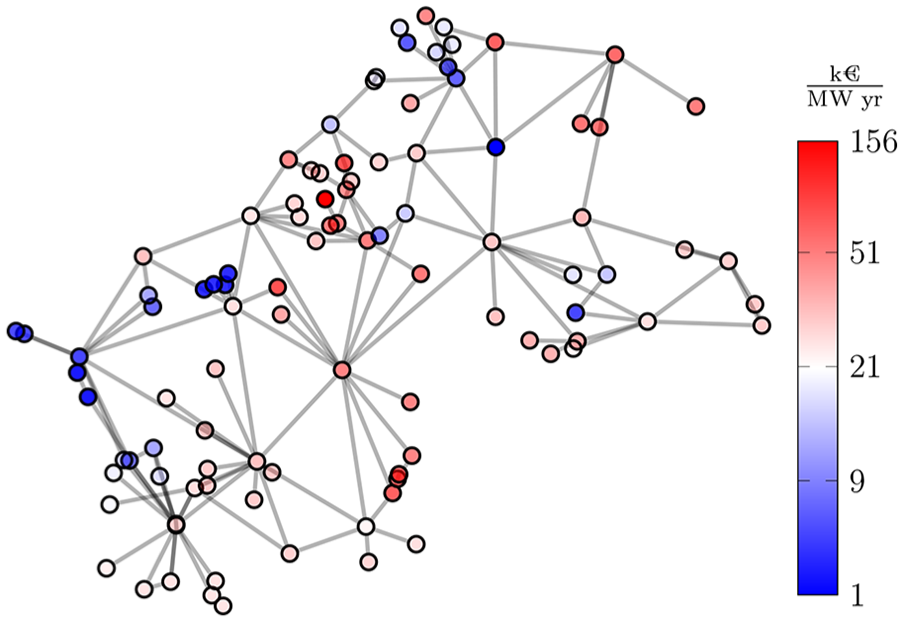

Although their total costs are similar with intermediate monitoring, the MBR policy has a notable advantage over zonal pricing with cost-based re-dispatch: its efficiency can be restored when it is combined with a locational capacity market, as discussed theoretically in section 4.2 and confirmed here empirically. In this section, we are also interested in analyzing the conditions under which the efficiency of zonal pricing with MBR could be restored. Figure 3 presents the magnitude of the optimal capacity price under this policy for each node of the network.

Spatial distribution of the optimal capacity price.

We observe large differences between the different values of the optimal capacity price. In particular, although the large majority of the charges are below 50k€/MW, one node at the border between Belgium and France receives a value of more than 150k€/MW. This large value can be explained by the fact that it is only connected to nodes in France while it belongs to the Belgian bidding zone. For this reason, it exhibits a large difference between its zonal and nodal price which makes it particularly prone to arbitrage.

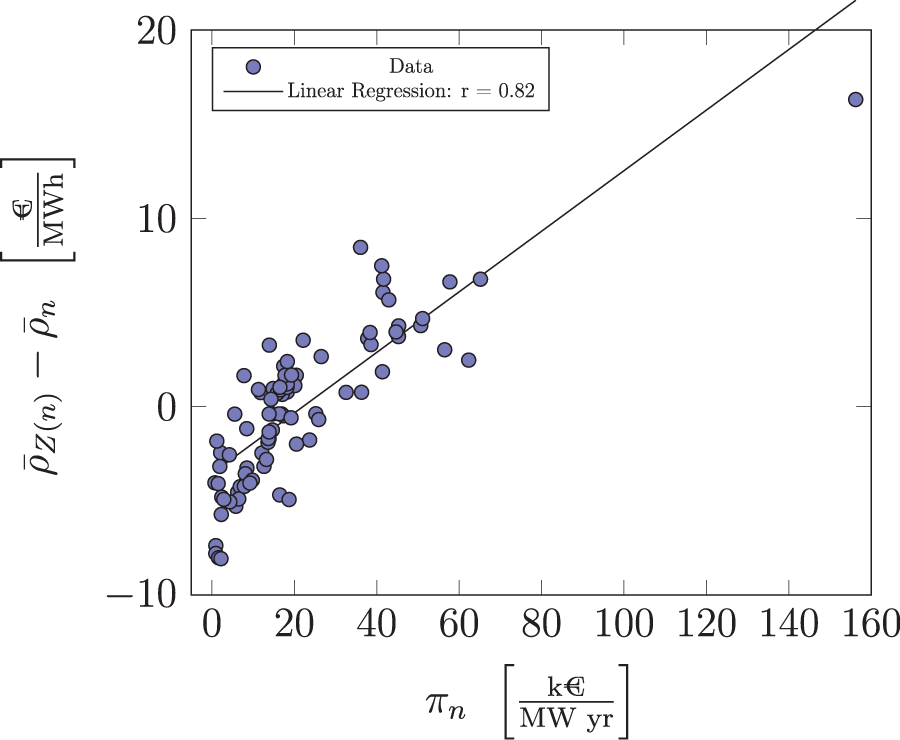

To confirm this intuition, we plot, in Figure 4, the difference between average zonal and nodal prices as a function of the optimal capacity price. Clearly, there is a high correlation between the difference of average nodal and zonal prices in a location and the value of the optimal capacity price needed to restore the efficiency of MBR, which suggests that this difference is the main driver for the inefficiency.

Difference between the average zonal and nodal prices as a function of the optimal capacity price.

7. Conclusion

As the integration of renewable energy and distributed energy resources increases uncertainty and variability in the electricity grid, it becomes more and more important to evolve toward a pricing system that is consistent with real-time dispatch. For different reasons driven by institutional concerns, the European market has been organized around the concept of zonal pricing. Instead, locational marginal pricing, which proved efficient in various markets around the world, has so far been dismissed. In this context, it appears tempting for EU stakeholders and legislators to rely increasingly on market-based re-dispatch, which is seen as being able to reconcile a pricing system that supports real-time dispatch with the zonal organization of the market. This is for instance witnessed in the recast of the electricity regulation which makes market-based re-dispatch the default rule (European Parliament, Council of the European Union 2019). It is well known that zonal pricing followed by MBR incentivizes market participants to deviate from bidding at marginal cost, even in the absence of market power. Existing literature has studied the problem in the short term (De Vries and Hakvoort 2002; Hirth and Schlecht 2020; Holmberg and Lazarczyk 2015). In this paper, we prove formally that under a series of strong assumptions (perfect foresight and absence of irrevocable decisions based on the zonal market), zonal pricing with MBR is efficient in the short term. These assumptions, however, are known not to hold in practice. Indeed, many resources must be committed in the day-ahead stage, based on the results of the zonal market, which leads to inefficiencies in the short run (Aravena et al. 2021).

In the long run, new types of inefficiencies manifest, even under the series of strong assumptions mentioned above. In times of energy transition, it is therefore crucial to understand how MBR impacts the long-term equilibrium, both theoretically and quantitatively.

In this paper, we propose a long-term equilibrium model of zonal pricing followed by MBR. We show how inefficiencies in the long run originate from the mathematical structure of the problem, with investment conditions coupling the zonal and nodal parts of the problem. We then discuss the conditions under which efficiency can be restored under this design as well as the impact of market monitoring on efficiency. Finally, we propose a case study on a large-scale instance representing Central Western Europe and compare MBR with nodal and zonal pricing benchmarks.

We find that zonal pricing followed by MBR is associated with significant efficiency losses, due to the fact that it incentivizes over-investment in technologies with low investment cost. This confirms the intuition discussed in Hirth and Schlecht (2020), that predicts investment in so-called “ghost plants” under this design. Our results also confirm that efficiency can be restored by introducing an additional locational capacity market, as proven theoretically in the paper. We find, however, that recovering efficiency is only possible under large deviations in capacity charges among locations, hindering the practicability of an efficient implementation. Finally, the case study highlights that market monitoring has an important impact on the results. Although efficiency can be kept close to that of nodal pricing under close monitoring, it quickly deteriorates when monitoring is relaxed.

The present work has focused on the efficiency of MBR in the best case, and has omitted the impact of uncertainty. In particular, we have assumed that market participants are able to perfectly predict re-dispatch when participating in the day-ahead market. Based on our modeling framework, it would be possible to relax this assumption by considering uncertainty in the re-dispatch price. This would make for an interesting extension to the present work, which would allow us to account for risk considerations. Moreover, an important argument for evolving toward MBR relates to the difficulty of evaluating correct compensation for re-dispatched resources in cost-based re-dispatch in a system with significant penetration of demand response and storage. Future work will build on the modeling framework presented in this paper in order to assess the impacts of MBR in systems with an increasing deployment of these types of resources.

Footnotes

Appendix A

Appendix B

Appendix C

Appendix D

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The work has received funding from the European Research Council (ERC) under the European Unions Horizon 2020 research and innovation programme (grant agreement No. 850540). Quentin Lété was a Research Fellow of the Fonds de la Recherche Scientifique – FNRS.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

1

Note that this prevents financial arbitrage, following the assumption of ![]() Using the terminology of Hirth and Schlecht (2020), our model is thus based on asset-backed arbitrage which implies that participants can only bid quantities that they would be able to physically produce in both the zonal and the re-dispatch markets.

Using the terminology of Hirth and Schlecht (2020), our model is thus based on asset-backed arbitrage which implies that participants can only bid quantities that they would be able to physically produce in both the zonal and the re-dispatch markets.

2

The separation between the TSO and the market operator follows the organization of the European market. In practice, the optimality conditions of (2) are directly added to the market clearing algorithm. In the case of the European electricity market, therefore, KKT conditions of (2) correspond to the network equilibrium conditions that are part of Euphemia, the algorithm that clears the zonal day-ahead market.

3

This observation is important, as it reveals the bidding behavior that a rational fringe agent would have in this setting. Indeed, the interest of an agent in this market is to bid

4

Note that although this condition is not fully respected in the current European practice, there is an ongoing effort toward improving cross-border coordination. Indeed, the European Commission guidelines now state that TSOs should develop a common methodology for coordinated re-dispatch and countertrading (![]() , Art. 35, §1).

, Art. 35, §1).

5

6

The weakening of the conditions for recovery of efficiency obtained in Proposition 3 is particularly important as it allows to connect the design to existing initiatives in Europe. As discussed in details in ![]() , Great Britain, Ireland and Sweden all implement capacity-based instruments that are differentiated among locations, but none of them are differentiated among technologies. These instruments are not market-based. There is a capacity market in France, but it has no spatial differentiation. However, as discussed in Eicke et al. (2020), France has recently implemented a specific tender to build new capacity in Brittany that was facing adequacy issues. This particular capacity tender thus had explicit spatial differentiation. Moreover, many countries impose a connection charge to new capacities. This shows that a locational capacity market that determines a capacity charge would share many characteristics with existing instruments in different European countries.

, Great Britain, Ireland and Sweden all implement capacity-based instruments that are differentiated among locations, but none of them are differentiated among technologies. These instruments are not market-based. There is a capacity market in France, but it has no spatial differentiation. However, as discussed in Eicke et al. (2020), France has recently implemented a specific tender to build new capacity in Brittany that was facing adequacy issues. This particular capacity tender thus had explicit spatial differentiation. Moreover, many countries impose a connection charge to new capacities. This shows that a locational capacity market that determines a capacity charge would share many characteristics with existing instruments in different European countries.

7

Note that caution must be exercised when interpreting the efficiency results, in view of the potential non-uniqueness of equilibria that is discussed in ![]() . The results presented here relate to the equilibrium found by the splitting algorithm, but we cannot exclude the existence of other, perhaps more efficient, equilibria.

. The results presented here relate to the equilibrium found by the splitting algorithm, but we cannot exclude the existence of other, perhaps more efficient, equilibria.