Abstract

Saudi Arabia, the world’s largest oil exporter, aims to reach net zero emissions (NZE) by 2060 and heads to a drastic transformation of its energy sector amid a changing international oil market. This paper presents least-cost NZE trajectories for Saudi Arabia, consistent with alternative international oil prices and availability of carbon capture solutions. We use a hybrid forward-looking general equilibrium model where current and future mitigation technologies are represented explicitly. The results show that domestic price reforms alone can cut emissions by 13 percent to 27 percent below a baseline no-policy scenario by 2060. Lower international oil prices reduce the opportunity cost of fossil fuels and increase the implicit CO2 price needed to reach NZE. Along with energy efficiency, renewables and clean hydrogen; NZE would need to rely on a large deployment of carbon capture technologies, whose scalability is still uncertain. In NZE, direct air capture (DAC) would need to offset residual emissions and would become a large consumer of electricity and gas. The massive energy sector investments needed for NZE tend to crowd out non-energy investments. In NZE, the GDP is 3 percent to 10 percent below the baseline, depending on whether the international oil price is high or low and on the scale of carbon capture availability.

1. Introduction

Saudi Arabia announced in 2021 its goal to reach net zero emissions (NZE) of greenhouse gas (GHG) by 2060 (SMEGI 2022). This objective is particularly challenging because it requires a full restructuring of the county’s large energy sector with costly investments that may weight on economic development. Therefore, it is crucial to assess potential least-cost net zero pathways for Saudi Arabia, what policies could help to achieve them, and what could be the consequences for the entire economy. Moreover, the transition to net zero will occur in a global context of energy market transformation that will affect oil prices. Given the importance of oil export revenue in Saudi Arabia (59% of fiscal revenue in 2021), assessing how international oil prices may influence least-cost net zero policies is essential. Last, but not least, achieving net-zero emissions will require carbon capture and carbon removal technologies, which have not yet been deployed at scale. Understanding the role these technologies will play and how their availability will impact the cost of reaching net zero is essential.

This paper investigates possible economic consequences of NZE policies in Saudi Arabia. We use a new hybrid forward-looking general equilibrium model of the Saudi economy, which explicitly represents energy-intensive technologies and administered energy prices (prices of energy that are set by the government). Based on various scenario simulations, we address two types of issues. First, we are interested in the shape of the least-cost energy transition for given technological assumptions. What could be the NZE energy mix? What can be the role of carbon capture technologies? What implicit (shadow) carbon price would be needed? What could be the cost for the energy sector and the effects on the rest of the economy? Second, we seek to understand the role of international oil prices during the transition. How may international oil prices influence the least-cost policies? How large is the effect of lower oil prices compared with the effect of a domestic net zero policy?

The economic impacts of the energy transition may differ significantly between oil-importing and oil-exporting countries. In oil-importing countries, the cost of mitigation may be relatively limited, as low-carbon policies combined with economy-wide green stimulus and structural reforms can potentially increase economic growth. In contrast, oil-exporting countries would face more challenges due to unfavorable developments in international energy markets, which can negatively impact their trade (OECD 2017). Studies have highlighted the economic challenges fossil-fuel exporters and Gulf Cooperation Council (GCC) countries will face in achieving their energy transition (Mirzoev et al. 2020; Peszko et al. 2020). Recent macroeconomic assessments of net zero scenarios have shown higher economic costs for oil exporters than for other economies (Chateau, Jaumotte and Schwerhoff 2022; Jaumotte, Liu and McKibbin 2021), but provide little insight into the underlying transformation of the energy sectors. Some studies have presented consistent assessments of energy and macroeconomic pathways toward net zero emissions for advanced energy-exporting economies (e.g., Adams [2021] for Australia). But thus far, to the best of our knowledge, there has been no assessment of the economy-wide implications of net zero for an energy-exporting emerging economy like Saudi Arabia.

This paper contributes to the modeling literature about the energy transition in oil-exporting emerging countries in four ways. First, it fills an important gap by providing for Saudi Arabia—the world’s largest oil exporter—a model-based long-term baseline of CO2 emissions rooted in a structured energy economy storyline. Second, it is the first study to provide a general equilibrium assessment of a net zero scenario for an energy-exporting emerging economy. Third, it investigates explicitly how international oil prices influence least-cost net zero policies. Last, this work introduces a new dynamic forward-looking hybrid top-down bottom-up general equilibrium model of Saudi Arabia. Unlike standard CGEs, which rely entirely on aggregated macroeconomic functions and assumptions about various elasticities. The model explicitly represents the substitution and mitigation options based on technical parameters. However, besides these contributions, it is important to note that this article only considers the cost of the energy transition, regardless of the obvious positive impacts in terms of reduction in climate-related damages.

The article is structured as follows. In the second section, we present contextual elements about Saudi Arabia’s net zero policies and review the related modeling literature. In the third section, we introduce the modeling framework. The fourth section describes the baseline scenario and introduces scenarios that combine energy policies in Saudi Arabia and alternative international oil prices. The fifth section presents the main simulation results, describing the effects of the policies on the energy sector and economic activity. It also highlights how international oil prices influence the net zero pathway of the energy sector and the overall economic performance. The last section concludes.

2. Net Zero Scenarios in Saudi Arabia: Context and Related Literature

In the context of its pledge to achieve carbon neutrality by 2060, Saudi Arabia reaffirmed its commitment to the Paris Agreement. In the 2021 update of its nationally determined commitment (NDC), the country states it aims at “reducing, avoiding, and removing GHG emissions by 278million tons (Mt) of CO2 equivalent annually by 2030.” 1 Saudi Arabia has put in place a series of initiatives to achieve its NDC objective and prepare for the transition to net zero.

Initiatives in the power sector aim to increase the share of renewable energy to 50 percent of the electricity mix while phasing out the use of liquid fuels. Measures are also in place to improve energy efficiency in the building and transportation sectors (Belaïd and Massié 2023), and to foster carbon removal by planting 650million trees in the Kingdom by 2030 (SMEGI 2022). Moreover, an aspect of net zero strategies specific to Saudi Arabia and the GCC region is the key role given to clean (green and blue) hydrogen and carbon capture and storage (CCS) technologies. For instance, the country plans to ramp up carbon capture to 44 Mt of CO2 by 2035 (SMEGI 2022). There are multiple reasons why carbon capture is so important in Saudi Arabia’s energy transition. First, in the power sector, gas with CCS can be a suitable complement to non-dispatchable renewable technologies. Moreover, the country has large refining, petrochemicals and cement sectors. These sectors are a source of very high process emissions 2 which, unlike emissions from combustion, cannot be abated through fuel switching and energy efficiency improvements. In addition, CCS is necessary for developing blue hydrogen, which would give value to domestic gas reserves and serve as a feedstock in the petrochemical sector. Furthermore, given that some emissions may remain unabated, and the limited potential for natural carbon sinks (e.g., afforestation) in Saudi Arabia, direct air capture (DAC) is a technology option that will be needed to reach net zero. Lastly, Saudi Arabia possesses a very large potential for CO2 storage, thanks to its favorable geology and abundant saline aquifers (Ye et al. 2023).

The deployment of all the technologies needed to meet the net zero objective will require costly investments, and households and businesses may face an increase in energy expenditure. Exporting firms will have to preserve their price competitiveness while complying with stringent environmental regulations. Moreover, the transformations in Saudi Arabia’s energy sector will play out within a context where other countries implement net zero policies, with possible consequences on the global oil market. Widespread adoption of net zero policies may exert downward pressure on oil prices and impact the economies of Saudi Arabia and other oil exporters. The Kingdom may have to adjust to the context of lower oil revenue while having, at the same time, to pay a high cost for restructuring its energy system. However, the new energy landscape may also create new opportunities. Hydrogen, for instance, may help build new competitive advantages for Saudi Arabia in global energy markets. Assessing the costs and opportunities of net zero requires a quantification combining various technology options with a representation of possible future socioeconomic developments in the Kingdom.

There have been several modeling assessments of the consequences of domestic energy policies in Saudi Arabia, but mostly focused on domestic price reforms. Matar et al. (2015) develop a detailed partial equilibrium model of the energy-intensive sectors to investigate administered price reforms and their consequences on oil export revenue. Soummane, Ghersi and Lecocq (2022) simulate price reforms combined with structural policies using a CGE model and stress how they can offset the negative effects of lower international oil prices. Blazquez et al. (2020) use a dynamic stochastic general equilibrium model to represent the macroeconomic effects of energy price reforms. Durand-Lasserve et al. (2023) represent the impacts of price reforms both on the energy sector and on the rest of the economy.

However, thus far, there have been only very partial assessments of the consequences of decarbonization policies for Saudi Arabia or even for a GCC country. Using a linear programming (LP) model adjusted to Saudi Arabia, Alshammari and Sarathy (2017) study pathways to reduce CO2 emissions by 80 percent in the power sector. They find that CCUS plays a key role in mitigation before renewable technologies are deployed at full scale. Their result is at odds with the literature on least-cost mitigation policies, which generally finds that relatively cheap renewable technology is deployed before CCS, which is relatively expensive. Alshammari and Sarathy (2017) stress that beyond a certain threshold of international oil prices, the oil sector would be willing to pay a high price for CO2 to increase enhanced oil recovery. Their approach, nevertheless, has important limitations. In particular, given that the oil supply in Saudi Arabia is primarily driven by policies within OPEC, there is no reason why higher oil prices should stimulate a massive boost of oil production through enhanced oil recovery. Al-Sinan, Bubshait and Alamri (2023) explore long-term CO2 emission pathways based on expert judgments and a series of separated calculations. They assess the impact on emissions of various policy initiatives that are to be fulfilled by 2030. The authors find that if continued beyond 2030, the initiatives would lead to almost net zero GHG emissions by 2060. However, due to the lack of an integrated modeling framework, their results are more of a narrative than a proper quantification.

There have been only two modeling assessments of a net zero trajectory for a GCC country. The first one, performed by Babonneau, Benlahrech and Haurie (2022), is based on a bottom-up LP model of energy sectors and simulates net zero emission pathways in Qatar. They highlight the possible role of renewable and direct air capture technologies. Once net zero is achieved, they envisage that Qatar will further remove carbon from the atmosphere via DAC and receive offset payments from the rest of the world. The article is particularly interesting because it covers emissions from the entire energy system, while it also shows the influence of DAC on gas and electricity demand. However, the assumption unerlying the adjustment in the oil and gas revenue is strong because the scenarios assume changes in export volumes, not export prices. Therefore, the adjustment of domestic energy technologies does not reflect changes in international energy prices. Moreover, their model does not represent administered prices and the impact of price deregulation. In addition, there is little discussion on whether the carbon offset price scenarios that are used are plausible. The second modeling assessment of net zero, conducted by Kamboj et al. (2024), focuses on Saudi Arabia and utilizes a version of the GCAM partial equilibrium integrated assessment model. The study highlights the critical role of DAC, which is projected to remove more than 370 Mt of CO2 by 2060—equivalent to approximately two-thirds of Saudi Arabia’s CO2 emissions in 2019 (Crippa et al. 2024). However, the study offers limited discussion on the implications of such a level of DAC deployment for the energy system and the associated investment requirements. Furthermore, the article provides little insight into the impact of price deregulation or about the CO2 price necessary to achieve net-zero emissions. It also overlooks a key challenge: the effect of changes in international oil prices on Saudi Arabia’s energy transition. Finally, due to the partial equilibrium nature of the model, the study does not assess the broader macroeconomic impacts of the net-zero transformation.

3. Model Description

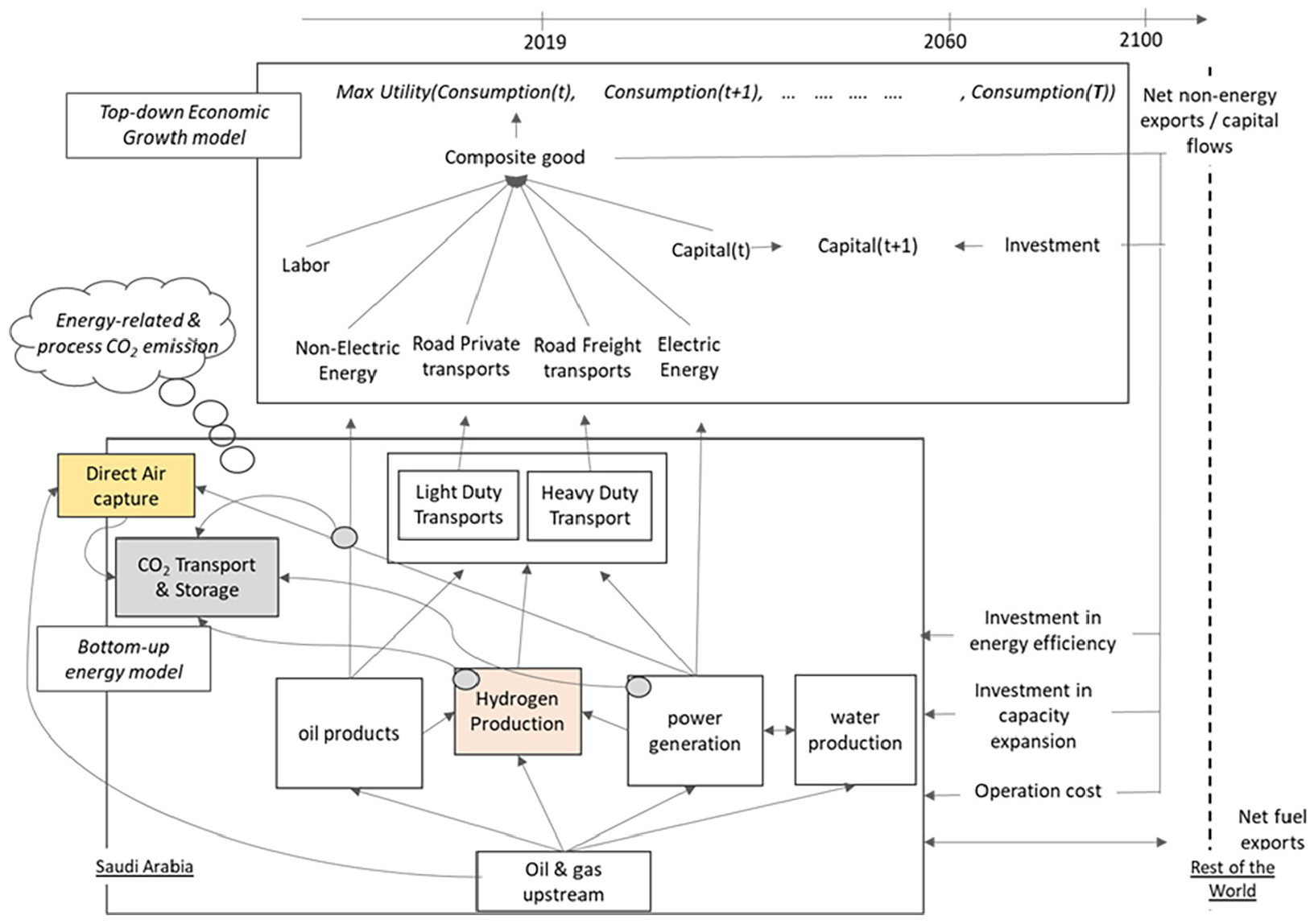

We have developed a new energy economy model to represent least-cost net zero pathways for Saudi Arabia (Figure 1). It belongs to the family of hybrid forward-looking general equilibrium models such as MERGE (Manne, Mendelsohn and Richels 1995), WITCH (Bosetti et al. 2006), or REMIND (Leimbach et al. 2010). It represents Saudi Arabia as an open economy and includes the most prominent features of the Kingdom’s energy system. The model is hybrid because it combines a top-down representation of macroeconomic variables and aggregated energy service demands—modeled using an aggregated CES production function—with a bottom-up representation of energy service supply technologies defined by their physical characteristics. 3

Schematic view of the model.

The top-down part of the model represents the substitutions between capital, labor, and very aggregated categories of energy services. Unlike standard CGE models, which entirely rely on CES functions, even for representing energy technologies, we use the CES function only at the top level of aggregation. The bottom-up part of the model disaggregates energy services into explicit technologies characterized by their technical coefficients and investment in operation and maintenance costs (see details in Supplemental Appendix A sections 4–6). It is a linear activity system that allows the capture of radical technological shifts, including the complete phase-out of certain technologies. Note that the representation per technology in the bottom-up model is an advantage over the standard CGE models which entirely rely on CES functions, even for representing technology substitution. The CGE models can represent endogenous shifts between technologies as far as they were part of the base year energy mix (e.g., heavy fuel to gas power generation). In contrast, the bottom-up representation of the energy system accommodates the endogenous ramp-up of technologies that were not present in the base year energy mix, either because of price distortions (e.g., solar PV because of low administered fuels prices for electricity producers), or because of currently insufficient price incentives, limited scalability and high initial cost (such as for carbon capture and hydrogen). Additionally, the bottom-up formulation provides a clear representation of the planning implications of the model results, including capital expenditure, capacity expansion, and path dependency.

The aim of the hybrid model is to make a link between the energy system and the rest of the economy, not to outperform other types of models in terms of resolution. For instance, for the non-energy sectors, the hybrid model does not have the sectoral granularity of the pure CGE models. Similarly, it does not have the very high level of technological details that are found in pure bottom-up models such as TIMES (Loulou et al. 2016). There are also limitations to the modeling approach that are inherent to dealing with a long-term horizon. We will focus here on the main ones. The calibration of the time-varying coefficients of the CES function in the top-down part of the model reflects the implicit assumption that there will be no major shift in preferences and in economic structure if there are no changes in policy (see Supplemental Appendix A, section 7.2). It is reflected in the baseline scenario, which does not show disruptive change (Table 1). In addition, as with any model with technology details, we need to rely on a large number of assumptions about the various technologies. When doing scenarios with very ambitious decarbonization targets, like net zero, the assumptions about backstop-type technologies, such as CCS in our model, are very important. This is why we consider alternative scenarios, with high or low availability of CCS technologies.

Main Characteristics of the Baseline Scenario.

Source. Author’s calculations.

SAR = Saudi Riyal, 1 USD = 3.75 SAR.

Including remittances.

Primary energy intensity of the non-oil sector.

CO2 intensity of primary energy consumption.

In Saudi Arabia, the domestic energy prices are set by the government. Energy price deregulation that would let domestic prices adjust to the international prices is a key policy option for energy conservation and emissions mitigation. To be policy relevant, the representation of the energy system needs to accommodate both administered energy prices (i.e., prices set by the government) and deregulated energy prices (i.e., market-clearing prices). To do so, our model is formulated and solved as a Mixed Complementarity Problem (MCP). However, the MCP formulation is tedious, and we prefer here, for simplicity, to give the nonlinear programming formulation. Note also that we insist here on the key mechanisms only. Equations (1) to (6) below present the top-down part of the model, showing the aggregated functions that define the demand for aggregate energy services. The description of the bottom-up model, which shows how energy services are met by explicit energy technologies, would be too long for the main text of the articles. But the details can be found in Supplemental Appendix A. Note that the GAMS code of the model is available from the author upon request.

A representative household maximizes an intertemporal welfare function

where

The domestic demand corresponds to consumption,

The composite good XA is an Armington aggregate of goods

The domestic economy produces an aggregate output

The composite output

with:

At each period, the input mix can be adjusted in the new vintage of equipment only. The proportion of inputs is fixed in the older vintages, which decay at an annual rate,

Products

As said earlier, the energy supply is represented with a bottom-up linear activity model which contains explicit technologies. For simplicity, we give here a high-level algebraic representation. The reader can refer to Supplemental Appendix A sections 4 to 6 for a complete description of each equation of the bottom-up energy model.

First, the bottom-up model supplies energy services (denoted by the superscript bu) that meet the input demands from the top-down part of the model:

The bottom-up model also determines the quantities of energy commodities that are imported and exported. An outcome of the bottom-up model is a trajectory of energy-intensive services and energy commodity imports and exports. Now, we can define the feasible set of activities in the bottom-up model that allows the fulfillment of a given outcome. The feasible set is the set of

where the supplies of energy-intensive services (

where costet represents the sum of all CAPEX and non-energy OPEX associated with each operation and investment decision in the energy sector. The total cost for the energy sector is a claim on the demand for domestic goods, as shown in equation (1). Welfare maximization implies that, for a given demand for energy services in the top-down model, the energy system cost is minimized. Increasing energy imports or reducing energy exports would reduce energy costs ECOSTt and could increase welfare by increasing the quantity of Armington goods that can be consumed in equation (1).

However, as a closure rule we impose that in our model the current account balance CAB in equation (5) is fixed. If net energy exports decrease, net exports of non-energy goods (PX.XX–PM.XM) need to increase. As a result, domestic demand XA in equation (1) will decrease. Therefore, changing net energy exports will also tend to reduce welfare. The adjustment of the real exchange rate—which determines the trade competitiveness of the non-oil sector—ensures that the current account balance remains fixed. Specifically, if the oil export revenue increases, there is a real exchange appreciation and the non-oil export revenue decreases. Therefore, the model represents the Dutch disease effect.

Moreover, at the welfare optimum, the marginal benefit of consuming an energy commodity domestically must be equal to the marginal benefit of the revenue generated by exporting this commodity. In other words, if a commodity is exported, its price for domestic consumers needs to align with its export price. The export price is here the opportunity cost of the commodity. 4 Note that, in the baseline scenario, the domestic prices are administered and that they cannot adjust to the opportunity cost. Therefore, in the baseline scenario, the welfare is not maximized. In our model, welfare maximization requires that the domestic commodity prices are deregulated.

4. The Baseline and the Policy Scenarios

The baseline scenario projects the Saudi economy at the horizon of 2060 assuming that there are no stringent domestic and global climate policies. In the Kingdom, domestic energy prices remain administered and relatively low—at their 2019 value—and there is no emission mitigation policy. At the global level, because of the absence of stringent climate policy, world oil demand and price remain high. More precisely, the oil price converges to USD 95 per barrel in the long run, as projected in IEA (2022) Stated Policies Scenarios (STEPS). 5 The energy economy baseline trajectory is summarized in Table 1. The methods and the assumptions that have served to build this baseline are described in Supplemental Appendix A. Note that, in this baseline scenario with limited global mitigation efforts, climate change would negatively impact the Saudi economy. However, we do not model climate-related damages or their economic consequences in the baseline scenario or in any of the scenarios presented in this paper.

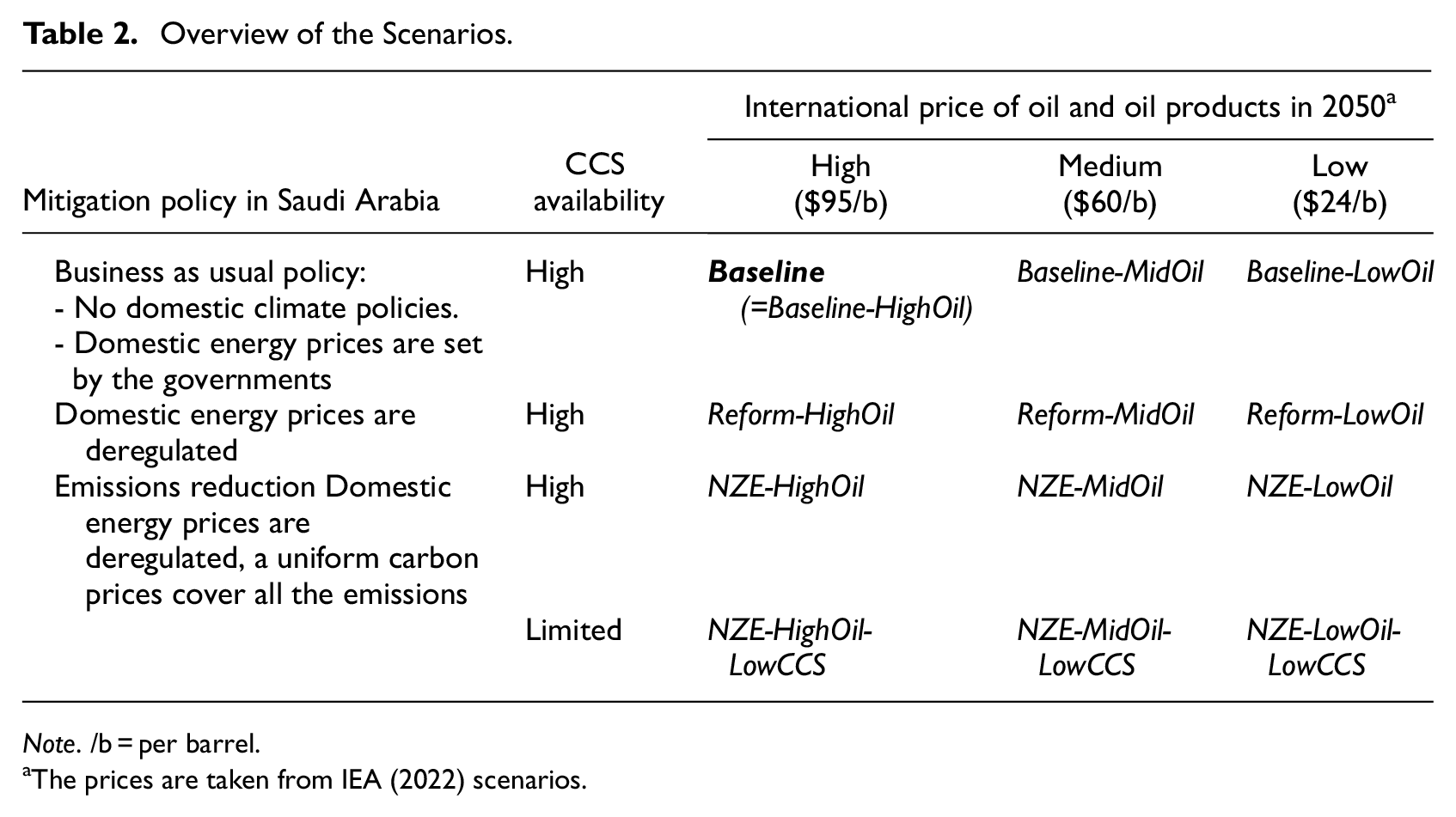

To illustrate the influence of the international oil price on Saudi Arabia’s energy transition, we define alternative scenarios around the baseline along two dimensions: (i) the domestic energy or emission mitigation policy, and (ii) the international oil price trajectory. The first row of Table 2 corresponds to the scenarios with no mitigation action and no price reform in Saudi Arabia. 6 We find on this line the baseline scenario 7 explained above, where the oil price is USD 95 per barrel in the long run—as in the IEA’s (2022) STEPS scenario—and where there is no domestic mitigation action. The other scenarios—Baseline-MidOil and Baseline-LowOil—feature lower international prices of USD 60 and USD 24 per barrel in 2050 based on IEA’s (2022) Announced Pledges and NZE scenarios respectively. Note that the Baseline-LowOil scenario represents what would happen if Saudi Arabia were flying solo, having no climate policies while the other countries do.

Overview of the Scenarios.

Note. /b = per barrel.

The prices are taken from IEA (2022) scenarios.

In the second line of Table 2, we represent scenarios of price reforms where the Saudi government lets domestic energy prices adjust to market conditions. Energy producers who can export their commodities will consider the opportunity cost of not selling at the international price. They will ultimately adjust the domestic prices to the international level, and domestic energy consumers will adjust their demands. We consider, again, three different oil prices to assess how oil prices influence the emissions, energy sector, and economic outcomes of price reforms.

Policies other than price reforms will be needed to decarbonize the economy and to reach NZE. Therefore, we introduce scenarios with a domestic net zero policy (third line of Table 2) where the price deregulation is accompanied by a cap and trade system that covers CO2 emissions from energy combustion and industrial processes. The cap corresponds to an exogenous quantity of emissions allowances that are distributed every year and that are gradually decreased, until reaching net zero by 2060. To allow for some flexibility and to represent policies that minimize the intertemporal mitigation cost, we allow for the banking of emission permits. If, at some periods, the emissions are below the cap, allowances in excess can be saved and used to exceed the cap in subsequent periods.

As previously, we examine the results of the net zero policy under the three different oil prices mentioned above. The scenario NZE-LowOil—with decarbonization and low oil price—corresponds to a global net zero policy where Saudi Arabia and all the other countries of the world would implement net zero policies. The scenario with decarbonization and high international oil price (NZE-HighOil) corresponds to a situation where Saudi Arabia would be a single climate leader, implementing net zero on its own, while other countries would have very limited climate policies. This scenario is implausible. However, it is useful because it serves to disentangle the “pure effects” of the net zero policy (i.e., the effects due to the domestic net zero policy only), from the “pure effects” due to a lower international oil price.

Achieving net zero will require deploying carbon capture technologies on a large scale to address residual emissions. The availability of these technologies will significantly impact the pathways to achieving net zero. However, there is precisely a lot of uncertainty about carbon capture technologies, because they have never been deployed at scale. Therefore, it is crucial to assess the least-cost options under scenarios of limited carbon capture availability. Specifically, we constrain the total amount of CO2 captured across all sources, including power generation (using gas with CCS), blue hydrogen production, industrial processes in the petrochemical and cement sectors, and DAC. The fourth row of Table 2 represents net zero scenarios where carbon capture availability is capped at 250 Mt per year by 2060. This limit is close to the minimum level of capture required to maintain the feasibility of the Net Zero 2060 target.

The oil prices are predetermined in all scenarios as if they were not affected by Saudi Arabia’s actions. This is a limitation of our approach, given that as the world’s largest oil exporter and a core OPEC member, Saudi Arabia has historically influenced international oil prices. However, analyzing how Saudi Arabia’s decisions might exactly affect oil prices around low, medium, and high price levels would have required broadening the paper’s scope and shifting its focus away from the core issue of NZE in the Kingdom. For simplicity, we opted to base our analysis on three exogenous oil price scenarios derived from IEA (2022) which is a clearly identifiable source.

In all the scenarios, the international oil prices remain well below Saudi Arabia’s production cost, which is around $8 per barrel in the model (based on data released in Aramco [2020]). Moreover, crude oil production is limited to 10.3 million barrels per day (mb/d). This level corresponds to an estimated 11.8 mb/d crude oil production capacity as of 2019, minus a spare capacity of 1.5 mb/d, in line with the historical levels (see Supplemental Appendix A, Table 5). In other words, we do not let oil production significantly expand in any of the scenarios. Given that oil production reaches the same upper limit in all the scenarios, oil export revenues only vary depending on international prices and domestic consumption levels (with lower domestic consumption leading to higher exports). One can argue that lower oil prices should lead Saudi Arabia to reduce its oil production. However, given its low oil production cost Saudi Arabia is one of the world’s producers whose output should be least impacted by a drop in oil price. Finally, as mentioned in the paragraph above, we did not try to assess how Saudi Arabia would adjust its production to the international price. It is worth noting, though, that among the various scenarios, those with lower oil prices would probably imply a higher global market share for Saudi Arabia.

5. Results

First, we present the emissions trajectories and energy mix in the baseline, the price reform, and the net zero scenarios. Then, we show the implication of the various scenarios on energy system costs and energy export revenues and discuss the contribution of clean hydrogen exports. Finally, we explain possible macroeconomic impacts, seeking to differentiate the effect of the domestic mitigation bill from the effect of changes in international oil prices.

5.1. Emissions and Energy Mix

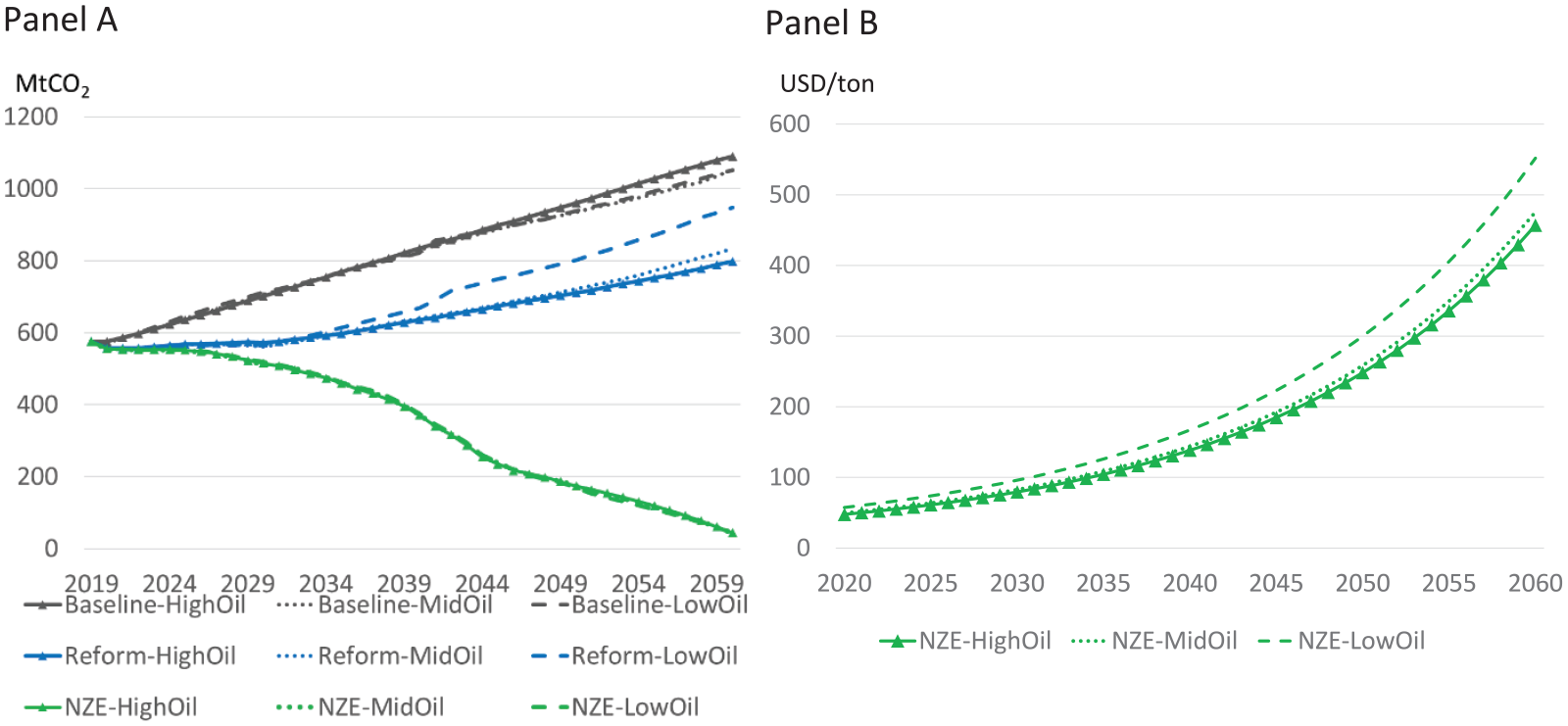

In the three baseline scenarios, CO2 emissions almost double over the model’s horizon and reach around 1.1 Giga tons (Gt) by 2060 (see the black lines on Figure 2 panel A). The emissions trajectories are very similar because final consumers face the same administered energy prices in the three scenarios. The slight difference that we see comes from macroeconomic activity feedback (see Figure 12). Price reforms reduce CO2 emissions compared with the baseline scenarios by 20 percent in 2030. In the longer run the oil price influences the emissions trajectories. Lower international prices involve less upward adjustment of domestic prices, less energy conservation, and more CO2 emissions. Price deregulation in the context of high oil prices (scenario Reform-HighOil) leads in 2060 to a 27 percent reduction in CO2 emissions compared with the baseline. The reduction is only 13 percent if low oil prices prevail (scenario Reform-LowOil).

Saudi Arabia net CO2 emissions and CO2 shadow prices.

In the net zero scenarios (green lines in Figure 2, panel A), whatever the oil price is, CO2 emissions follow the same path which is close to the maximum abatement potential. By 2030, CO2 emissions trajectories compatible with net zero are around 185 Million tons (Mt) below the baseline. Nevertheless, emissions are still above the current NDC target of Saudi Arabia, which pledges to reduce GHG emissions by 278 Mt CO2eq in 2030 compared with a baseline. Hence our results suggest that the NDC emissions reduction objective may be too ambitious compared with what is needed to reach net zero, and also extremely difficult to realize. 8

Our results show that the oil price influences the CO2 shadow price (See Figure 2, panel B) needed to incentivize the net zero transformation. In contexts of high and medium international oil prices (NZE-HighOil and NZE-MidOil), the CO2 price starts at around USD 50 per ton and reaches around USD 250 per ton by 2050. A low international oil price (NZE-LowOil) leads to a carbon price that increases from around USD 60 in 2020 to USD 300 per ton in 2050. The opportunity cost of oil, which directly relates to the international oil price, is an important incentive for reducing liquid fuel consumption and emissions during the first years of the projections. If the international oil price is lower, so is its opportunity cost. Therefore, a higher carbon price is needed to discourage the use of oil products and to encourage low-emission technologies. This is why the carbon price is higher in the NZE-LowOil scenario, despite lower economic activity (see non-energy output on Figure 12 panels D). In the net zero scenarios, the carbon price grows at the same rate as the interest rate of the economy, which is around 5 percent. Least-cost emission abatement implies that the marginal abatement cost is constant in discounted value. From an emission permit market perspective, it means that in early periods, emissions were lower than the number of allowances distributed, and that emissions allowances were banked. In the case of limited availability of carbon capture, the CO2 prices required for decarbonization are much higher, they start above USD 80 per ton and reach 440 to 500 USD per ton by 2050 (see Supplemental Appendix B, Figure 3).

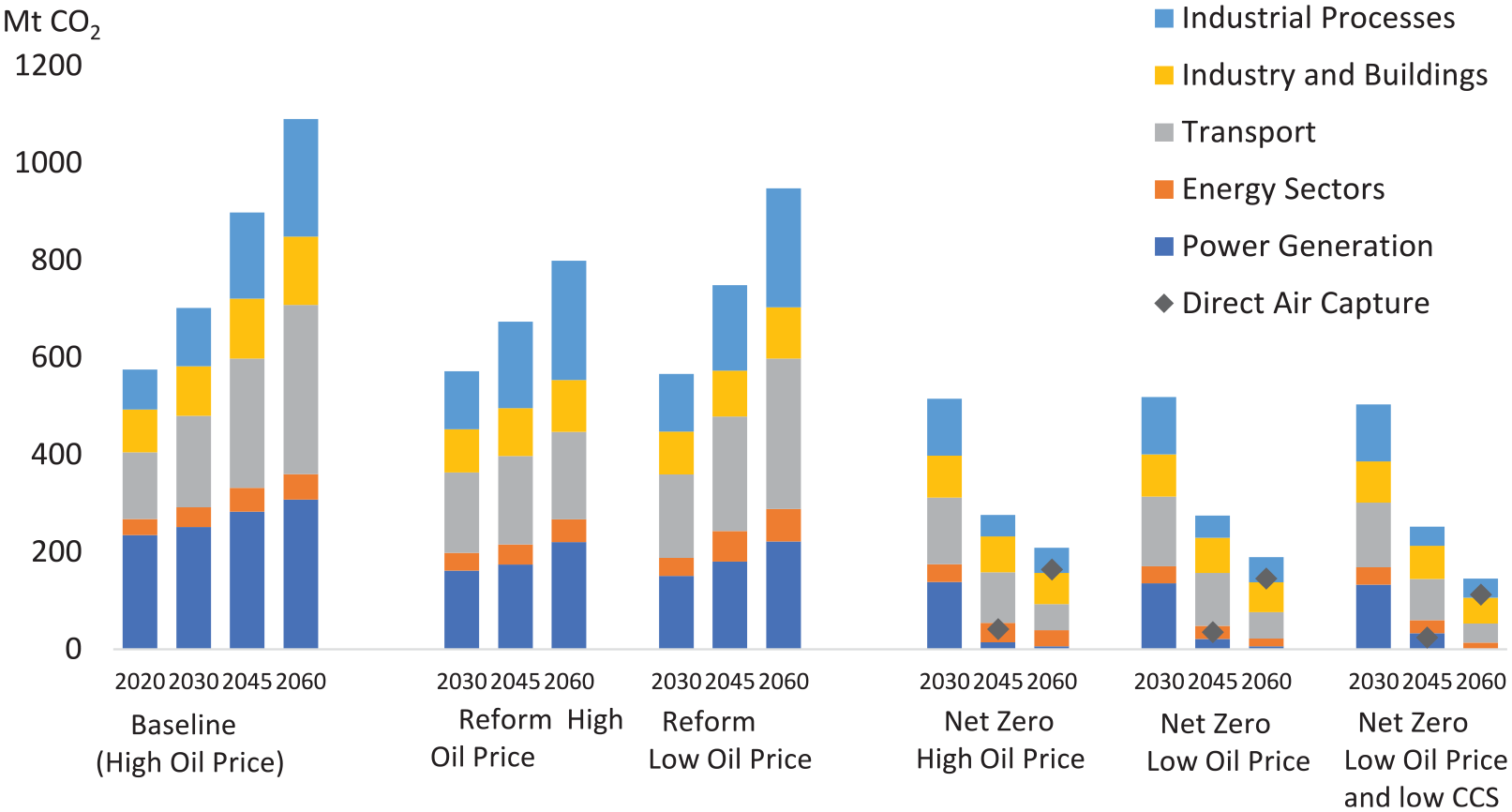

In the price reform scenarios, CO2 emissions still increase in all sectors (Figure 3). We also see that a price reform leads to the same emissions in the power sector, whether the oil price is high or low. However, the price reform mitigates more transportation emissions if the oil prices are high. In the case of low international oil prices, the adjustment of relative transportation fuel prices due to the price reform is not sufficient to simulate energy saving and fuel switching. In the case of the net zero emissions scenarios, the decarbonization pathways are the same regardless of the oil price. The electricity sector is totally decarbonized, and emissions decrease for all the sources represented. Process emissions are reduced compared with the baseline due to carbon capture, the substitution of blue for grey hydrogen, and the adoption of low-emitting processes in the cement industry. By 2060, around 200 Mt of CO2 are emitted in the net zero scenarios. The abatement of these remaining emissions is extremely costly. Around 160 Mt are abated using DAC. The remaining 40 Mt of CO2 are covered by emissions permits that have been banked over the early periods when emissions were lower than the cap, and permits were saved to be used in later periods. DAC starts being massively deployed by the mid-2040s. DAC runs using electricity that is already carbon neutral and natural gas that is made available as more power generation comes from nuclear and renewable and less from gas. Note that our 160 Mt of CO2 captured with DAC in 2060 is high, but significantly below the 370 Mt found by Kamboj et al. (2024) for the same period. Moreover, if assuming a lower availability of carbon capture options, as in scenario NZE-LowOil-LowCCS, DAC is reduced to 110million Mt of CO2 by 2060 and more mitigation is needed to reach Net Zero.

Sectoral CO2 emission pathways in selected scenarios.

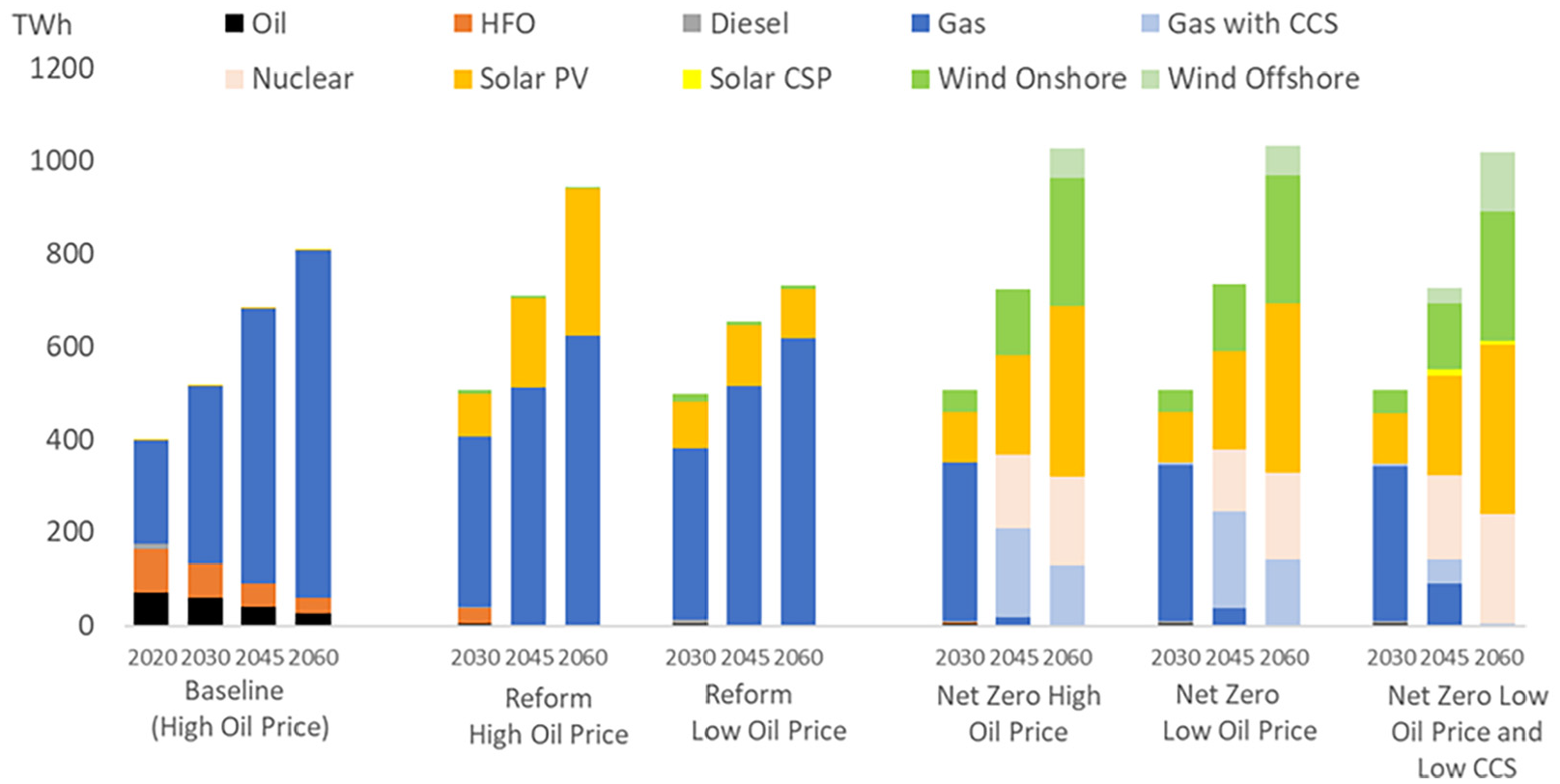

The price reforms and, to a greater extent, the net zero policy, lead to a considerable transformation of the electricity mix (Figure 4). In the baseline scenario, the electricity mix is dominated by gas, which has a price administered and set below marginal production cost. Liquid-fired generation persists because, due to low administered liquid fuel prices, existing liquid-powered capacities are operated until the end of their lifetime. Price reforms accelerate the phase-out of liquids in the power sector because their opportunity cost becomes too high, even in the case where the international oil price is low. Therefore, our results show that the policies to phase out the liquid in power generation are cost-effective whether the oil price is high or low. In addition, because price reforms increase gas prices, solar and wind generation are competitive and ramp up quickly. In the long run, in the price reform scenarios, electricity is supplied by solar PV and natural gas. Importantly, in the case of higher oil prices, there is greater electricity demand. The reason is that if the oil price is high, the electricity price decreases relative to other energy carriers, and there is more electrification of demand.

Electricity mix in selected scenarios.

Figure 4 also shows that total power generation is greater in the net zero scenario than in the baseline. Moreover, in the net zero scenarios, the electricity mix is not affected by the oil price. The least-cost pathways for net zero are based on electrifying demand and decarbonizing power generation. In addition, the need to fuel DAC facilities to reach net zero increases the total electricity demand. Electricity generation is almost carbon neutral by 2045. Unabated gas generation is phased out, with no investments in new units, alongside a large deployment of solar and wind technologies. By the 2040s, gas with CCS and nuclear capacities expand. Finally, in 2060, power generation comes entirely from solar, wind, nuclear, and CCS technologies. Wind plays an important role due to its good load-carrying capability factor compared with solar PV, which limits the need for utility-scale battery storage. However, the electric system still requires around 60 GWof battery capacity by 2060 (see Supplemental Appendix B, Figure 4). When restricting the use of CCS, as in scenarios NZE-LowOil-LowCCS (right of Figure 4), there is no gas with CCS in power generation; this absence is compensated for by more generation with nuclear and wind offshore technologies. Due to the greater share of renewables, there is an additional 5GW of battery needed for the power system. Interestingly, when restricted, carbon capture remains largely utilized in DAC (Figure 3) but is absent in power generation (Figure 4). Gas with CCS in power generation represents a relatively low-cost abatement option compared to DAC, so it might be expected that reducing total capture would primarily impact DAC. However, capture in power generation is more significantly affected than DAC because it competes with relatively inexpensive renewable power generation technologies.

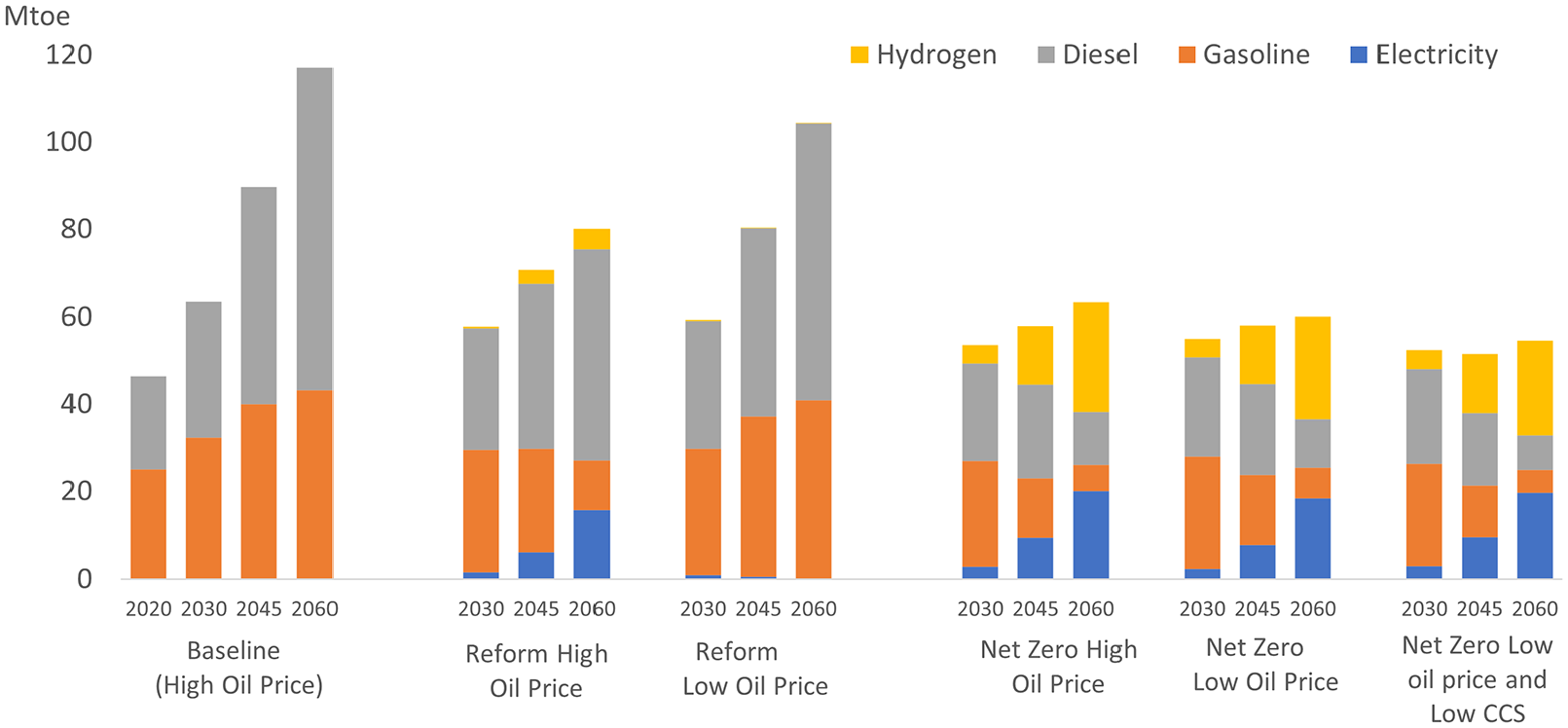

In the baseline, transportation fuel demand grows quickly (Figure 5), driven by non-oil GDP and population. Light-duty vehicles entirely rely on gasoline, the administered price of which is close to the international level. Heavy-duty vehicles entirely rely on diesel, the administered price of which is very low. Price deregulation has a significant impact on energy consumption in transportation. The upward price adjustment reduces demand for diesel, even in a situation where the international price is low. Moreover, with a high oil price, the opportunity cost of gasoline and diesel is high, and it encourages the penetration of electric vehicles. However, if the price reform happens in a context of low oil price, the opportunity cost of liquids is too low to encourage fuel switching. In the net zero scenarios, we see a much slower growth of transportation fuel demand, as well as a change in the fuel mix that increases the energy density of fuel (with more electricity and hydrogen). In 2060, the demand for liquid fuel is reduced by more than 60 percent compared with 2020, and hydrogen and electricity represent more than 70 percent of the mix. When carbon capture is restricted (right of Figure 5), the demand for transportation fuels decreases even further. The high CO2 prices reduce gasoline demand, and the limited production of blue hydrogen hinders the adoption of fuel-cell vehicles. Additionally, electricity becomes more costly without gas with CCS generation, and it impacts EV adoption negatively. In any case, the fuel switching, which is needed early on to achieve net zero, cannot be achieved with price deregulation if the international oil price is low. Therefore, reaching net zero in a context of low international oil prices will require a higher CO2 price, as Figure 2 showed.

Energy consumption in transportation.

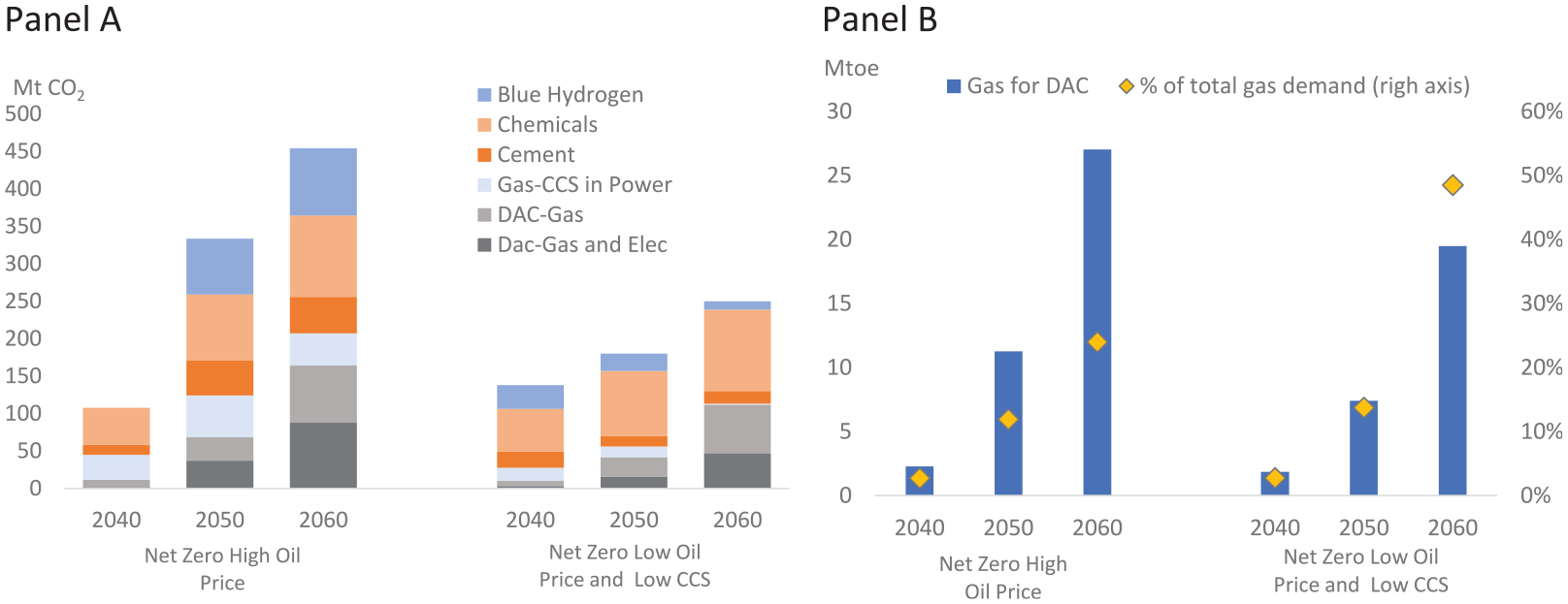

The net-zero scenarios require considerable carbon capture and storage by 2060. This is illustrated in scenario NZE-HighOil in Figure 6, which assumes no upper bound on total carbon capture. As early as 2040, almost 110 Mt of CO2 are captured, coming from capture in industry and gas CCS in power generation (Panel A). Carbon captured in industry keeps on growing over the model horizon. By 2050, blue hydrogen and DAC contribute to increasing the total capture, which reaches 450 Mt by 2060. This large number implies the construction of a considerable transportation and storage infrastructure in the net zero scenario. Moreover, to capture around 160 Mt of CO2 by 2060, the DAC sector consumes considerable quantities of energy; for instance, it is responsible for around 25 percent of the primary gas demand (Figure 6, panel B).

Carbon capture in net zero scenarios.

When restricting the availability of carbon capture to 250 Mt by 2060 as in scenario NZE-LowOil-LowCCS, in Figure 6, we see that by 2060, CO2 will be captured in DAC and in industry. There is no blue hydrogen production, and no CCS in power generation. Interestingly, DAC, which is a costly technology, still removes around 110 mt of CO2. DAC is preferred over blue hydrogen and gas CCS, which are, in principle, decarbonization options with a lower cost. The explanation is that DAC appears to be necessary to abate residual emissions. On the contrary, blue hydrogen has alternatives, which are green hydrogen and more electrification in transport; while CCS in power generation can be replaced with renewables. Last, note that when we restrict the availability of carbon capture, the net zero trajectories leads to a drop in gas consumption (see Supplemental Appendix B, Figure 5), and up to 50 percent of primary gas demand comes from DAC (Figure 6, Panel B).

5.2. Decarbonization Cost, Oil, and Hydrogen Exports Revenue

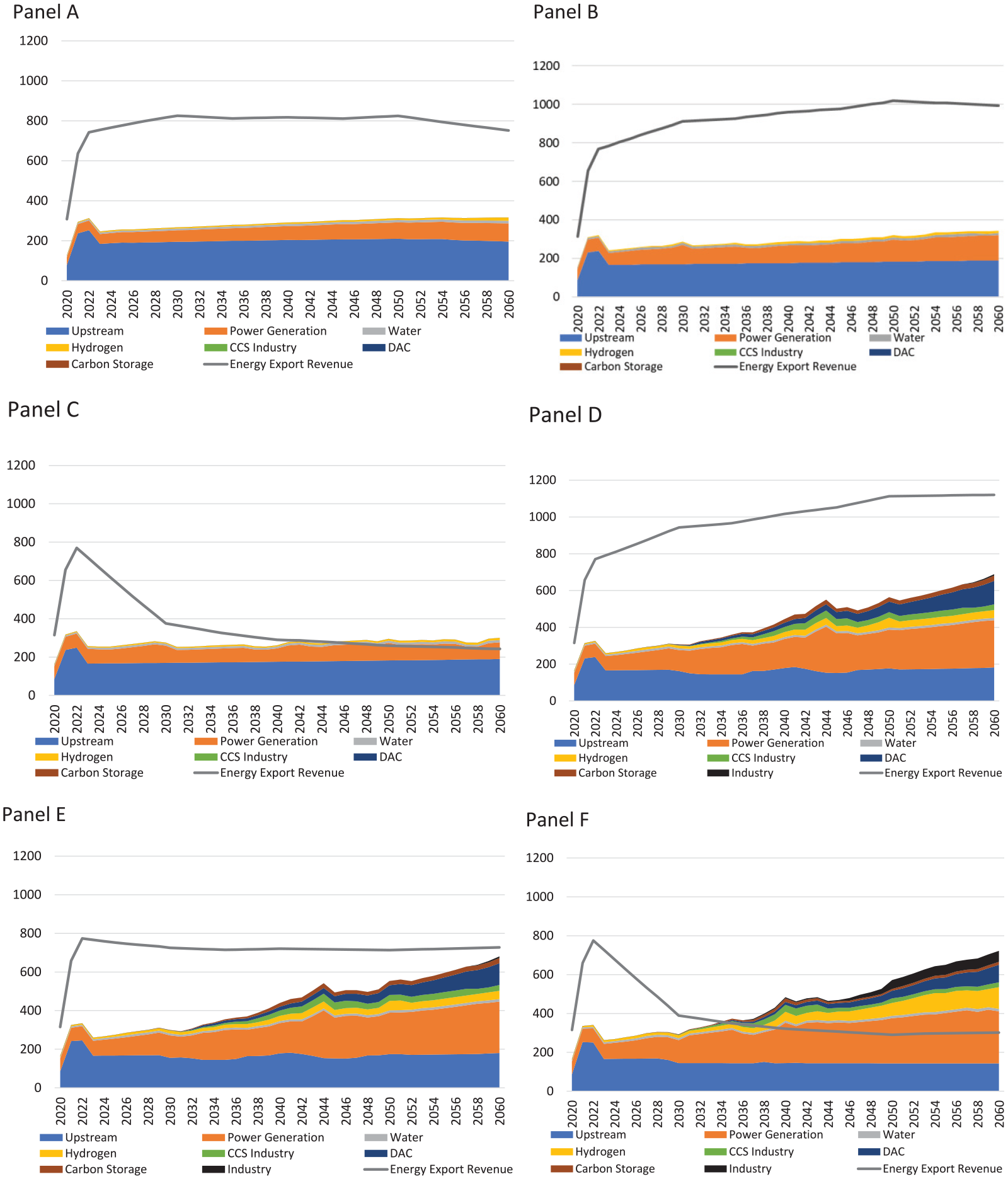

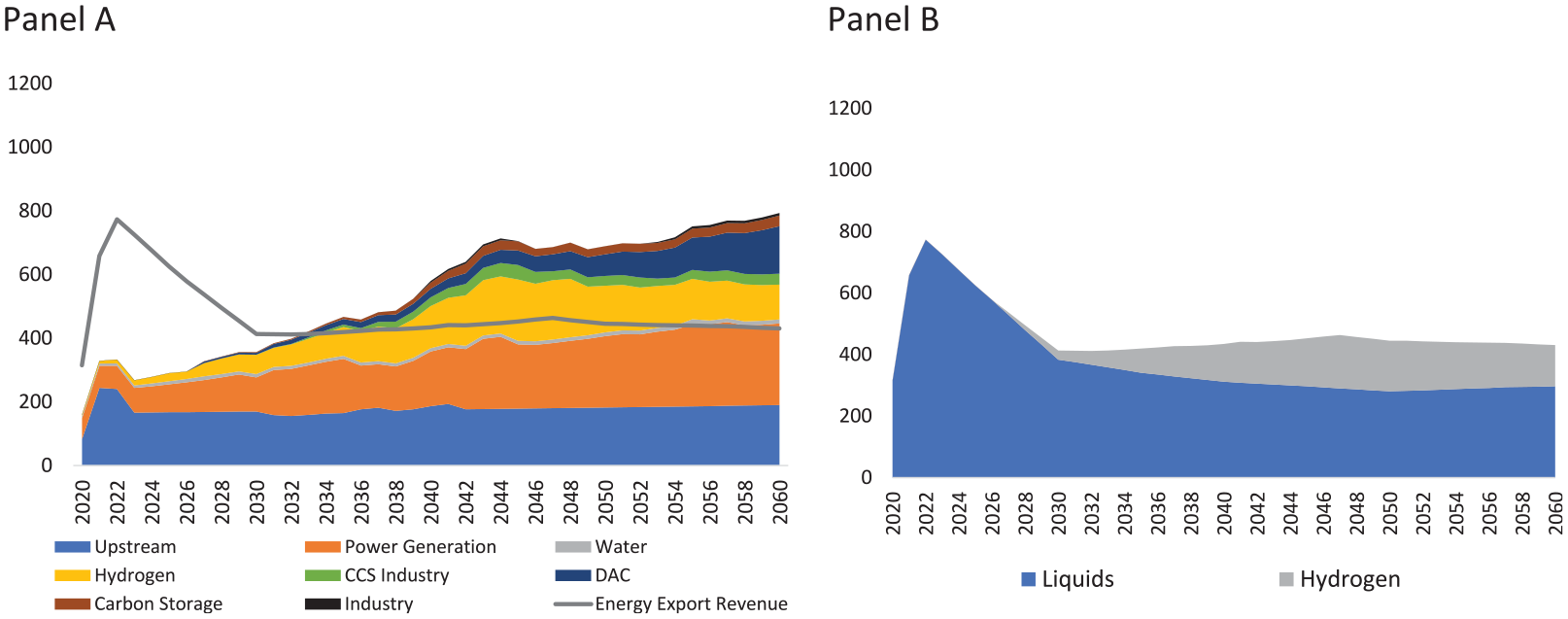

The net-zero scenarios require costly investments to mitigate domestic emissions and to expand carbon capture technologies, including DAC. At the same time, the energy export revenue will be impacted by the variations in international oil prices. Therefore, Saudi Arabia may be in a situation where it needs to fund considerable investments to achieve its net zero objective while simultaneously facing a decrease in hydrocarbon revenue. Figure 7 summarizes the expenditure needed in the energy sectors and compares the total with the energy export revenue. On the expenditure side, we include all the CAPEX and non-energy OPEX to reflect the purchase of equipment for energy production, transformation, and consumption. Moreover, we have included the expenditure of the upstream, power, water, and hydrogen sectors. We have also added equipment that relates to carbon capture and storage. We represent the energy export revenue on the same graphs with a line. The energy exports correspond to crude oil and oil products.

Energy system costs and energy export revenue (2019 SAR per year).

In the baseline scenario (Figure 7, panel A), the energy exports revenue stagnates and then decreases in the long run. This occurs because, as explained in Section 4, we have strictly limited oil production in Saudi Arabia accross the entire model horizon and in all the scenarios. At the same time, because of the low administered fuel prices, domestic consumption of liquids continues to increase and erodes oil export revenue. However, these revenues remain way above energy system costs (the stacked areas), showing that the energy sector is still a considerable net source of revenue by 2060. In the case of price reform with high international prices (Figure 7, panel B), the net revenue of the energy sector is greater than in the baseline. Thanks to energy conservation induced by the upward adjustment of domestic prices, more liquids are available for export. The energy export revenue is around 30 percent higher than in the baseline scenario and keeps increasing until 2050. However, a very low international oil price environment would lead to an accelerated decrease of the net energy sector revenue, which would ultimately become negative by 2045, despite the price reform (Figure 7, panel C).

The scenarios with decarbonization (Figure 6, panels D–F) imply very high energy system costs. Expenditure in the power sector starts increasing from the first years of the time horizon. Decarbonizing the energy sector requires the early decommissioning some gas generation capacities without CCS and the deployment of renewables, CCS, and nuclear technologies that are capital-intensive. Moreover, these new investments need to match a power demand that is greater because of the electrification of energy consumption, particularly in transportation. Last, carbon capture, and in particular DAC equipment, represents a considerable cost, especially after 2050. When carbon capture is restricted, as in Panel F, the transition is even more expensive because technologies that are more expensive than CCS need to be ramped up. With less capture available, mitigation required more process emission reduction by clinker substitution in the cement sector, which has a very high cost. In addition, large spending is needed to ramp up green hydrogen production with dedicated hydrogen production capacity.

Finally, in the net zero scenarios, the total energy system cost is multiplied by around 2.4 between the early 2020s and 2060, whereas it increases by less than 10 percent in the baseline scenarios. In the very hypothetical scenario with net zero and high international oil price, the net revenue of the energy sector remains largely positive, even in 2060. In this scenario, despite all the expenditure needed to upgrade the energy sector to net zero, the high international oil price maintains energy export revenues, which remain 50 percent greater than the energy system costs. But as already mentioned, it is unlikely that Saudi Arabia’s energy transition will happen in such a high oil price world. Assuming a lower oil price gives a different picture. In the net zero scenario with a medium oil price, in 2060 the energy export revenue just covers the energy system cost (Panel E), and if the oil price is low, the energy system costmay exceed the oil revenue as soon as 2035 (Panel F).

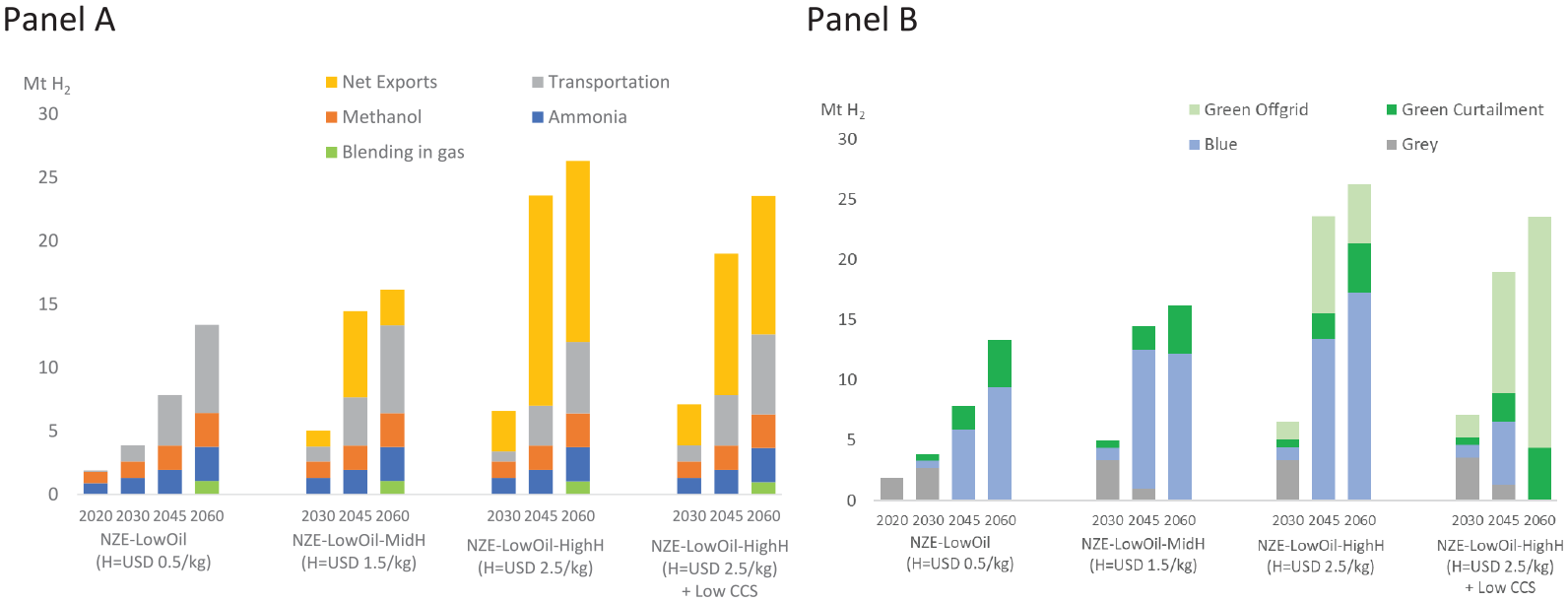

An international clean hydrogen market could emerge with the global energy transition (IRENA 2022). Saudi Arabia has a large potential for clean hydrogen (blue and green) production. Clean hydrogen exports may offset part of the losses in oil revenue due to lower oil prices. In all the scenarios explored thus far, we assumed an international free on board (FOB) price of hydrogen of USD 0.5 per kg. This price, which is very low, does not trigger hydrogen exports, and therefore we find that all the hydrogen produced is consumed domestically (Figure 8, Panel A, scenario NZE-LowOil). Here, we investigate whether higher international hydrogen prices could trigger enough hydrogen exports revenue to offset losses in oil exports revenue. We do additional scenarios with higher hydrogen prices assumptions. First, we assume a free on board (FOB) price of hydrogen of USD 1.5 per ton. This price is roughly in line with Hostert (2022) and DNV (2022), who project a delivery hydrogen price of around USD 2.5 per kg for importing regions by 2050; and with IRENA (2022) who consider a hydrogen transportation cost of around USD 1 per kg for the same year. Second, we assume a higher FOB price of hydrogen of USD 2.5 per kg.This price is very high compared with existing projections, and it will serve to provide a highly optimistic assessment of hydrogen exports revenue.

Sensitivity of hydrogen supply and demand to hydrogen price in the NZE-LowOil scenario.

For prices of USD 1.5 per kg and above, Saudi Arabia begins exporting hydrogen by 2030 (Figure 8, scenario NZE-LowOil-MidH). However, its exports peak in subsequent periods, due to high domestic demand for clean hydrogen, driven by the decarbonization of transportation and the replacement of grey hydrogen feedstocks in industries. Blue hydrogen emerges as the most competitive technology for clean hydrogen production, thanks to the large volumes of gas available following the shift to renewable energy in power generation. Additional hydrogen production comes from curtailed renewable electricity.

When increasing the hydrogen price to USD 2.5 per kg (Figure 8, scenario NZE-LowOil-HigH), we see that more hydrogen production is directed to exports, which surpass domestic consumption. High export prices of hydrogen tend to reduce its use in the domestic transportation sector compared with other NZE scenarios. Supply is ramped up through to greater volumes of blue hydrogen, although production becomes constrained by gas availability by the end of the planning horizon. Furthermore, the quantity of electricity curtailed depends on residual electricity demand and cannot be extended to meet higher hydrogen demand. As a result, dedicated off-grid hydrogen production starts to emerge to meet the demand for export and domestic use. This scenario with high hydrogen exports is heavily dependent on the scalability of the carbon capture technologies used in blue hydrogen production. Therefore, we consider a last scenario where the hydrogen price is high and CCS availability is limited (scenario NZE-LowOil-HighH+LowCCS, in Figure 8). In this case, because blue hydrogen is restricted, green off-grid hydrogen becomes the dominant production technology. However, due to its high cost, it cannot support hydrogen exports to the same extent as scenarios NZE-LowOil-HigH where blue hydrogen could be scaled up.

The exports of hydrogen brings additional revenue to Saudi Arabia. However, even in our most favorable scenario, where hydrogen price is as high as USD 2.5 per kg and CCS can be deployed at a large scale (scenario NZE-LowOil-HigH), hydrogen exports can only very partially offset a possible decline in oil revenue (Figure 9 Panel B). Moreover, the development of hydrogen exports requires considerable spending to increase production capacity. Expenditure to increase hydrogen supply is, around 2040, equivalent to the expenditure in the power sector (Figure 9, Panel A).

Energy system costs and export revenue in NZE-LowOil scenario with hydrogen at USD 2.5/kg.

5.3. Macroeconomic Effects of Mitigation Cost and Variations in International Oil Prices

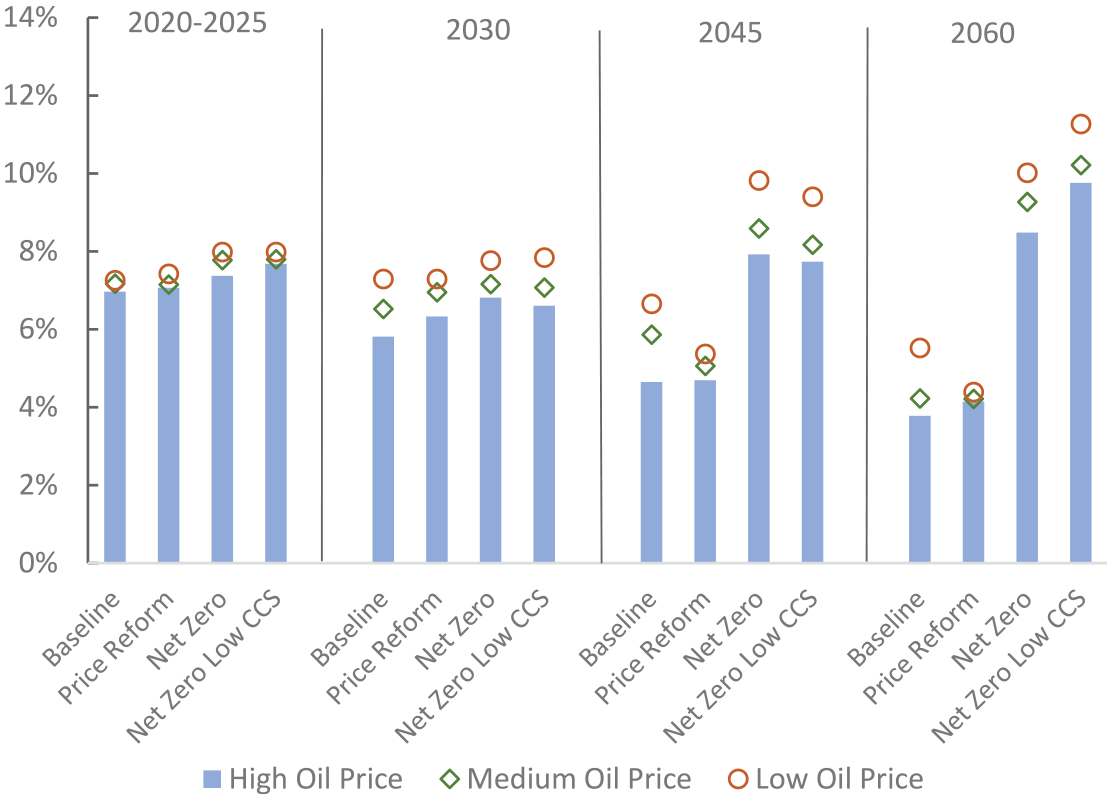

In the baseline and price reform scenarios, the share of energy expenditure (energy system CAPEX and non-energy OPEX as defined in section 5.2) in GDP decreases in the long run: from between 7 percent and 8 percent in the early 2020s to between 4 percent and 7 percent by 2060. This decrease comes from the technological improvements and from the gains in energy efficiency that were assumed in the baseline. Another reason is that without an implicit price of carbon, the energy mix in the baseline and in the price reform scenarios can rely on low-cost carbon-intensive technology options. In contrast, in the net zero policy scenarios, the share of energy expenditure in GDP increases to reach 9 to 12 percent by 2060 (Figure 10). The implicit price of carbon leads to the adoption of technologies that are way more expensive than those adopted in the baseline.

Energy system costs as percentage of GDP in the various scenarios.

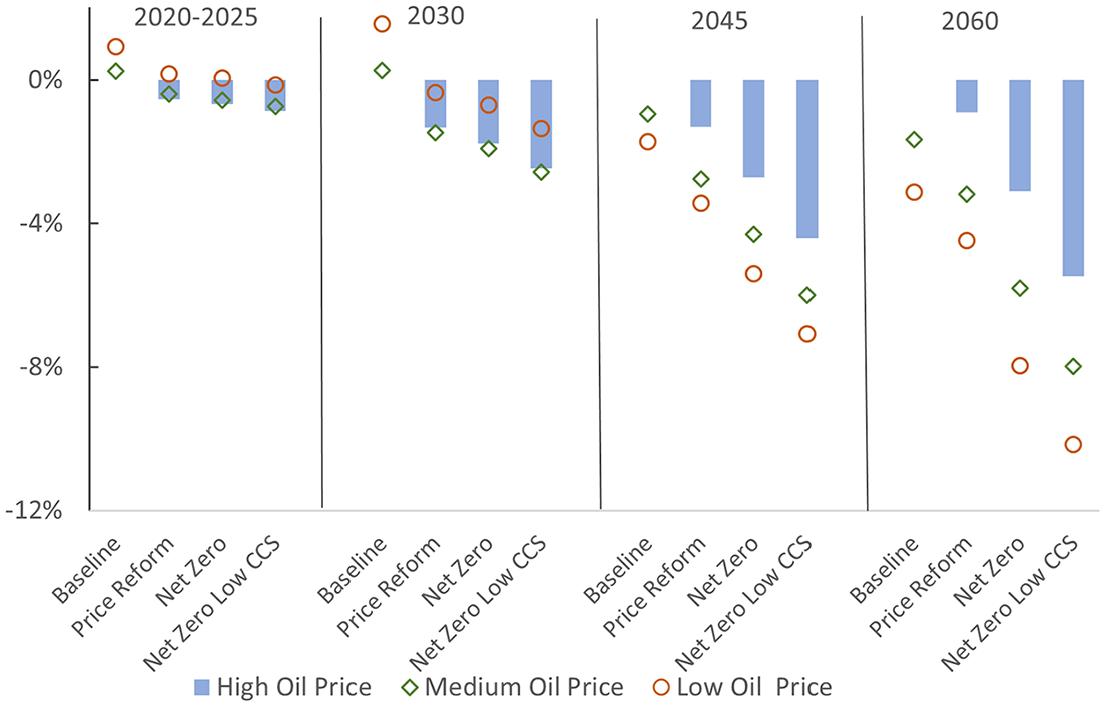

The net-zero policy has a significant impact on real GDP. Figure 11 shows that by 2060, the net zero policy can reduce real GDP by around 3 percent compared with the baseline if the international oil price remains high and if CCS is available on a large scale; and up to 10 percent if the oil price is low and if there is less possibility to deploy CCS. Net zero policies have three distinct effects that are all detrimental to non-oil GDP. First, the greater energy system expenditure that is needed for decarbonization crowds out domestic demand and non-energy investments, leading to a lower non-energy output. Second, the net zero policy raises the supply cost of the energy services, which leads to an inflationary effect. The real exchange rate increases and reduces the trade competitiveness of the non-oil sector which, as a result, produces less. Third, the net-zero policy creates a Dutch disease effect. Domestic mitigation reduces the domestic consumption of crude and oil products and increase their exports. Oil revenue inflows increase. As a result, the real exchange rate appreciates further, which further harms the trade competitiveness of the non-oil sector. Note that the price deregulation scenarios also increase the export of fossil fuels and lead to the same type of Dutch disease effect as net zero scenarios, with a negative impact on GDP. Lower international prices of oil tend to mitigate temporarily the effect of the Dutch disease. They limit the oil revenue inflows and keep the real exchange rate at a low level. As Figure 11 shows, paradoxically, in the medium run (until 2030), lower oil prices are associated with a greater GDP. However, in the longer run (after 2030), lower oil prices depress domestic consumption and investment in the non-energy sectors and lead to worse real GDP outcomes.

Real GDP in the various scenarios as percentage deviation from the baseline.

We also see in Figure 11 that CCS availability can help mitigate the GDP impact of decarbonization. Achieving NZE costs an additional 2 percent of GDP in 2060 when only limited CCS is available (Scenarios Net Zero Low CCS in Figure 10). This effect of CCS availability on GDP may seem high considering that the incremental energy system cost due to the limitation in CCS is only 1 percent of GDP (Figure 10). One of the explanations is that if there is less CCS availability, the assest value of the vast domestic gas reserves shrinks. More precisely, it is the large CCS availability that givesprospects to domestic gas demand for decarbonization: in power generation with CCS, in blue hydrogen production, and in DAC. If there is less CCS availiabilty, only a small portion of the gas reserves can be used in the energy transition. As a result, gas production drops (Supplemental Appendix B, Figure 5), negatively impacting total GDP growth.

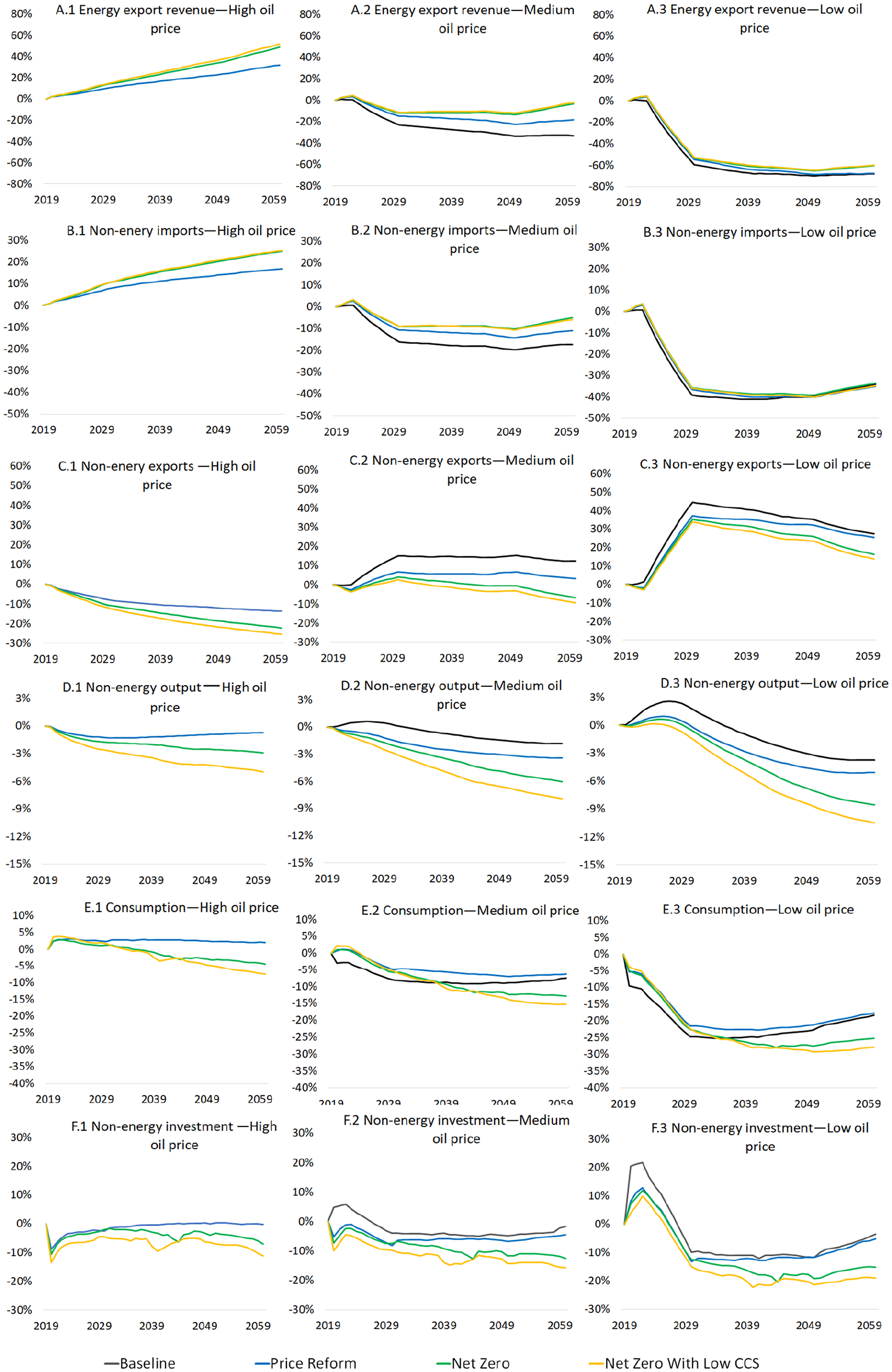

We plot the key macroeconomic variables in Figure 12. All the results are represented as deviations from the baseline scenario. The left side quadrants show the responses of variables when the international oil price is high. The quadrants in the middle and the right represent the responses when the oil price is medium and low. For each price level, we examine the impact of keeping the domestic policies as of today (baseline, in black lines), reforming energy prices (blue lines), and achieving net zero (green Lines). We also include (orange line) the scenario where the net zero is achieved with limited availability of CCS.

Key macroeconomic indicators as percentage deviation from the baseline.

First, let us examine the left quadrants of Figure 12 to understand the effects of price reforms and net zero policies if the international oil price remains high. Both policies increase energy savings and, therefore, energy export revenue (panel A.1). This positive revenue shock gives way to an appreciation of the real exchange rate that deteriorates the non-oil trade balance. Non-energy imports increase (panel B.1) and non-energy exports decrease (panel C.1). Finally, the non-energy output decreases (panel D.1). The decrease is more pronounced in the case of the net zero policy because the high domestic decarbonization bill crowds out non-energy investment (panel F.1). In the price reform scenarios, the reduction in price distortions leads to an increase in consumption (blue line on panel E.1). Overall, in both the price reform and the net zero scenarios, the higher real exchange rate has a positive influence on consumption. However, in the net zero scenario, the increase in energy system cost crowds out consumption, which, after an initial rise, slides below the baseline (panel E.1). Higher energy prices, as well as exchange rate appreciation, reduce investment over the first periods of the time horizon (panel F.1). Moreover, we see that, in the net zero scenario, the crowding out effect on non-energy investment worsens gradually, following the increase in the domestic decarbonization bill.

The middle and right-side quadrants illustrate the adjustment mechanisms in cases of lower international oil prices. As seen previously, net zero policies, and, to a lesser extent price reforms, increase non-energy exports (panels C.2 and C.3). This, in turn, affects non-oil output. In the medium run, lower oil prices stimulate non-energy output (before 2030, the black line on D.3 is above the black line of D.2, and both are above the baseline). However, in the longer run, they depress non-oil output (after 2030, the black line of D.2 is above the black line of D.3 before they both slide down below the baseline). In the long run, total output is negatively affected by lower international oil prices (Figure 12, panels E). However, in the short run, as lower energy export revenue improves the non-energy trade balance, there is a positive effect on output. In the case of price deregulation with low international oil prices, over the first periods, output is higher than in the baseline scenario. Nevertheless, with time, output decreases, because of the reduction in domestic demand and non-energy investment. Over the first time periods of the scenarios with the low oil price, investment tends to be higher than in the reference scenario. However, in the longer run, non-energy investment is negatively affected by lower domestic demand and crowded out by the considerable increase in energy system costs (panels F.2 and F.3). The limited availability of CCS (orange lines in Figure 12) exacerbates the negative impact of the net zero on the domestic economy. Without CCS, the high CO2 price increases the cost of energy services. Given the complementarity of capital with energy, investment is further depressed (Panels F), which has negative consequences on output (Panel D).

To conclude this section on macroeconomic impacts, it is important to note that the closure rule we have chosen, with the fixed current account balance and the endogenous real exchange rate, tends to exaggerate the adjustment that occurs through consumption. Assuming a fixed current account balance is restrictive but necessary. In general, a decrease in oil export revenue leads to a deterioration of the current account balance. Hence, the shocks resulting from domestic or global decarbonization would probably be absorbed more smoothly by domestic demand than shown by our simulations. However, large current account surpluses or deficits cannot persist indefinitely, and our closure rule was specifically designed to preclude permanent imbalances.

6. Conclusions

We used a forward-looking hybrid general equilibrium model to project possible net zero emission pathways for Saudi Arabia at horizon 2060 under alternative international oil price environments. Our net zero scenarios show a drastic transformation of the energy sector. Power generation becomes almost carbon neutral by 2045 thanks to renewable, gas with CCS, and nuclear. Electricity and clean hydrogen represent two-thirds of the energy consumption of the transportation sector by 2060. Abatement in industry occurs due to fuel switching, clean hydrogen, and a large deployment of CCS. However, substantial unabated emissions remain, and DAC ramps up after 2040. By 2060, 110 to 160 Mt of CO2 are captured with DAC, the equivalent of 20 to 33 percent of the CO2 emissions of 2019. As a result, DAC emerges as a large sector for energy demand. By 2060, it accounts for 25 to 50 percent of the primary gas demand.

The implicit carbon price that incentivizes net zero increases from USD 50 to 60 per ton in the first years of the model to USD 250 to 300 per ton by 2050 if we assume CCS technologies are widely available. This CO2 price varies when we change our exogenous oil price assumptions. A lower oil price reduces the opportunity cost of using oil domestically and increases the implicit price of carbon needed to incentivize emissions reductions. Taking more conservative assumptions about the availability of carbon capture technologies leads to higher CO2 prices, starting around USD 80 per ton and reaching USD 440 to 500 by 2050.

In the NZE scenarios, the share of energy system costs in GDP increases, from 7-8 percent in the first years of the model horizon to around 9-12 percent by 2060. In addition, we find that if the NZE has to be implemented in a low international oil price environment, the energy system cost may eventually exceed the oil export revenue. Moreover, our results suggest that clean hydrogen exports revenues are not significant unless we assume future hydrogen prices above the current mainstream institutional projections.

The model’s results show the possible macroeconomic impacts of the scenarios of net zero. Real GDP is around 3 percent below the baseline by 2060. The gap reaches 8 percent if we assume that the net zero policy occurs in the context of very low international oil prices, and 10 percent if CCS availability is limited. Moreover, we find significantly greater negative effects on household consumption. The results also show the importance of price reforms to improve welfare, even though the gains from the reform are less important in a low oil price context.

The results provide several policy insights that can inform Saudi Arabia’s net zero strategy. They show that in the medium term, existing and announced policy initiatives are aligned with the net-zero targets. The announced 2030 target of 50 percent of renewable and liquid displacements in the power sector is roughly on the trajectory of our net-zero least-cost pathways, whatever international oil price we assume. The support for carbon capture projects is consistent with the need to abate emissions from the energy-intensive sectors to develop CCS in power generation and DAC. Given the size of the required carbon capture infrastructure, the results highlight the importance of developing a sizable industry that can be scaled up and benefit from learning by doing. Price deregulation policies can play an important role in mitigating emissions, but the results show that they are not sufficient, especially if the international oil price is low. Specific carbon mitigation actions are needed and the policies will have to be coordinated through a shadow price of carbon that harmonizes the incentives in the energy sector. This price would have to be linked to the international oil price. Moreover, we find that the current NDCs of reducing GHG emissions by 278 Mt CO2-eq by 2030 relative to a baseline may be considered highly ambitious, very difficult to achieve, and corresponds to an emission pathway below what is required to reach net zero. The NDCs may be reformulated with an updated GHG abatement target and possibly an assessment of the baseline emissions to evaluate the progress toward reducing, avoiding, and removing GHG emissions and the alignment of the current policy efforts.

The results also provide insights into how Saudi Arabia can smoothly overcome the double challenge of investing in energy transition technologies and facing changes in oil export revenue. Several policy options need to be envisaged to mitigate the cost and to shelter households and firms from high energy prices. First, Saudi Arabia can use offsets to reduce the domestic cost of mitigation. Nature-based solutions in the Middle East, and beyond can serve this purpose, but more options can be envisaged. These offsets could be available at costs many times below the cost of abatement with DAC and they would significantly reduce the mitigation bill paid by Saudi Arabia. However, the country also needs to continue supporting the development of all the technology options that can reduce net emissions, especially carbon capture. Moreover, diversification within and beyond the energy sector will be essential to mitigate the cost of the transition for the economy. Hydrogen may generate revenue, but only in favorable market configurations, and costly investment will need to be backed by guarantees on the security of demand. Moreover, the scale of the net zero transformation is so important that it will stimulate certain activities. Sectors such as clean construction, building retrofitting, energy efficient material, renewable and carbon capture equipment, and critical minerals mining and processing will become particularly strategically important to reap new opportunities created by net zero. Industrial policies can support these sectors with targeted policy packages. The structure of the economy will also need to continue the adjustment toward improving the competitiveness of the non-oil sectors. Finally, budget policies must play a role by smoothing the cost of the energy transition.

Supplemental Material

sj-docx-1-enj-10.1177_01956574251340006 – Supplemental material for Net Zero Emissions in Saudi Arabia by 2060: Least-Cost Pathways, Influence of International Oil Price, and Economic Consequences

Supplemental material, sj-docx-1-enj-10.1177_01956574251340006 for Net Zero Emissions in Saudi Arabia by 2060: Least-Cost Pathways, Influence of International Oil Price, and Economic Consequences by Olivier Durand-Lasserve in The Energy Journal

Supplemental Material

sj-docx-2-enj-10.1177_01956574251340006 – Supplemental material for Net Zero Emissions in Saudi Arabia by 2060: Least-Cost Pathways, Influence of International Oil Price, and Economic Consequences

Supplemental material, sj-docx-2-enj-10.1177_01956574251340006 for Net Zero Emissions in Saudi Arabia by 2060: Least-Cost Pathways, Influence of International Oil Price, and Economic Consequences by Olivier Durand-Lasserve in The Energy Journal

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

2

3

4

Here, the opportunity cost is the export price because we assume no response of international energy prices to changes in energy exports. The international oil prices used in the model are exogenous and they are defined with the scenarios in Table 2. See ![]() for a generalization of the notion of opportunity cost to cases where the international price responds to exports.

for a generalization of the notion of opportunity cost to cases where the international price responds to exports.

5

The international oil price trajectories of IEA (2022) are shown in ![]() .

.

6

The only policy susceptible to limiting emissions is the ban on investment in liquid-fired power plants and in thermal desalination. These policies are active in all the scenarios.

7

8

The comparison between our model’s results and the NDC objective of reducing GHG emissions by 278 Mt CO2eq in 2030 compared with a baseline is not straightforward though. The NDC covers mitigation in all GHGs and, potentially, the nature-based solutions. Our model covers CO2 emissions only. However, thanks to a few side calculations we find that our reduction of 185 Mt in CO2 emissions is very unlikely to be enough to reduce GHG emissions by 278 Mt CO2eq. Reaching 278 Mt would require reducing net non-CO2 GHG emissions by 93 (278−185) Mt CO2eq thanks to (i) non-CO2 GHG emissions mitigation and (ii) carbon removal with nature-based solutions. First, abating 93 Mt CO2eq of non-CO2 GHGs by 2030 would require a 60 percent reduction in non-CO2 GHGs emissions compared with their baseline level (which is 160 Mt in 2030 as Table 1 shows). Second, back-of-the-envelop calculations show (assuming that a mature tree captures 22 kg of CO2 per year [EEA 2012]), that the plantation of 650 million trees by 2030 as planned in (![]() ) would not lead to the capture of more than 14.5 Mt of CO2 per year.

) would not lead to the capture of more than 14.5 Mt of CO2 per year.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.