Abstract

This paper explores market participants’ incentives to exercise unilateral market power in financial transmission rights (FTR) auctions. I present a model of strategic bidding in FTR auctions that illustrates how the standard market clearing mechanism for FTR auctions facilitates cross-path competition, limiting the profitability of demand reduction. Simulation evidence suggests that this force can dramatically reduce rents from unilateral market power relative to other sources of auction revenue shortfalls, highlighting potential adverse effects from proposed market reforms such as decentralized FTR sales and bidding-path restrictions that may weaken cross-path competition.

Keywords

1. Introduction

Financial transmission rights (FTRs) are an important element of restructured electricity markets. Operators of restructured electricity markets in the United States (known as independent system operators or ISOs) collect congestion revenues of roughly $3B per year, or about 4 percent of wholesale electricity costs (Parsons 2023). FTRs are forward claims on these revenues. While many FTRs are directly allocated to energy market participants, a large share are sold in complex auctions in which participants—including financial speculators—can potentially profit from strategic behavior. A robust empirical literature has established that purely financial participants consistently earn large trading profits in FTR auctions, raising concerns that strategic distortions could be significant. 1

In this paper, I use simple economic theory to investigate the contribution of unilateral market power to so-called “auction revenue shortfalls.” Building on recent developments in the theory of imperfectly competitive financial markets (Rostek and Yoon 2023), I show that the market clearing mechanism used in FTR auctions results in significant competitive pressure even when bidding activity is thinly dispersed across individual FTRs, weakening bidders’ incentives to shade their bids. The main results suggest that in the context of a dense, real-world transmission network, rents from unilateral market power could be relatively insignificant, despite apparent market imperfections such as limited participation for individual FTRs and a lack of explicit reserve prices. Well-documented auction revenue shortfalls may reflect the intrinsic costs of holding illiquid FTRs rather than insufficient competition.

In a typical FTR auction, bidders submit downward-sloping demand schedules for quantities of transmission capacity between points (nodes) in the network. After receiving bids, the market operator allocates capacity across “paths” to maximize net revenue, subject to the constraint that the final allocation of FTRs is simultaneously feasible with respect to the physical transmission constraints of the network. 2 Due to this constraint, which is enforced to ensure that the market operator remains budget-balanced, the residual supply curves faced by each bidder depend on the strategic behavior of bidders throughout the network. Bidders compete for capacity on common transmission elements when competing for disparate FTRs, and the effective level of competition for any individual FTR can be high even if few bids are submitted on it.

Section 2 captures this intuition in a stylized model of an imperfectly competitive FTR auction. Because the market clearing mechanism used in the FTR auction generalizes the familiar uniform price auction, the well-known characterization of price impacts in uniform price auctions can be adapted to the FTR auction setting. This shows how bidders’ incentives to exercise unilateral market power depend the structure of the transmission network, which mediates the strategic interaction of bidders on different paths. In a uniform price auction, bidders’ price impacts depend on the level of competition and the concavity of rival bidders’ preferences; in the FTR auction, bidders’ price impacts depend on the level of competition and the concavity of rival bidders’ preferences on all strategically connected FTRs—those that are related via equilibrium binding constraints—with greater weight given to bidding on electrically similar FTRs. In real-world FTR auctions, nearly all FTRs will be strategically connected, suggesting that effective levels of competition are generally high except possibly in the most peripheral regions of the transmission network.

Section 3 illustrates the implications of the model numerically in the context of the same six-node test network previously analyzed in Chao et al. (2000) and Deng, Oren and Meliopoulos (2010). In this network, a “North” region with excess generation is linked to a “South” region with excess demand, resulting in congestion. Uncertainty over the level of future demand creates uncertainty over congestion, and hence FTR payouts. Risk averse speculators compete to purchase FTRs while accounting for the behavior of bidders throughout the entire transmission network. I compare the standard FTR auction to a benchmark mechanism with uniform price auctions for individual FTRs, finding that the former results in far more aggressive bidding.

Empirically validating the model is challenging because detailed information on real-world transmission networks is generally unavailable to researchers. For instance, the key object governing the extent of cross-path strategic interaction is the power transfer distribution factor (PTDF) matrix, which summarizes the structure of the transmission network. This matrix cannot be reliably constructed from publicly available information. 3 Lack of information on network constraints and the PTDF matrix precludes the use of structural methods to recover bidders’ marginal valuations (e.g., Kastl 2011), as such methods require complete knowledge of the market clearing procedure to simulate supply elasticities.

Nevertheless, the analysis provides several clear implications for potential market reforms to address auction revenue shortfalls. If market power rents are small, then auction revenue shortfalls may primarily reflect concavity in bidders’ preferences (from risk aversion, inventory costs, or other sources). Accordingly, proposed reforms that would decentralize FTR sales or prohibit bidding on certain types of FTRs could harm competition without addressing potentially more fundamental sources of underpricing. I discuss the policy implications of the analysis in greater detail in the conclusion.

1.1. Related Literature

ISOs accrue congestion revenue due to the use of locational marginal pricing (Schweppe et al. 1988). Hogan (1992) proposed that market operators issue FTRs funded with congestion revenue. Doing so enables the market operator to distribute congestion revenue among market participants in a manner that may help facilitate long-term contracting, among other potential benefits. Operators of all seven restructured energy markets in the United States issue FTRs, typically through a combination of direct allocation and auctions.

As FTR auction markets have matured, a significant empirical literature has documented that auction prices for FTRs tend to be “underpriced” relative to their ex post value (Adamson and Englander 2005; Bartholomew et al. 2003; CAISO 2016; Olmstead 2018; Opgrand et al. 2022). Some authors have emphasized the potential for risk premia to explain underpricing (e.g., Adamson and Englander 2005; Baltadounis et al. 2017; Bartholomew et al. 2003), while others have focused on private information (Leslie 2021) or cross-market effects (Opgrand et al. 2022). Relative to this literature, my primary contribution is a novel explanation for why unilateral market power specifically may contribute little to underpricing. Moreover, while one might always question the significance of market power rents on the grounds that profitable opportunities tend to attract new entrants, the explanation I offer does not rely on the assertion that entry barriers are low.

Evidence of persistent underpricing has motivated a robust policy debate in recent years, with some observers suggesting that FTR auctions should be eliminated in favor of more extensive direct allocation (CAISO 2017; Monitoring Analytics 2022; Parsons 2020) and others emphasizing that existing auction mechanisms provide important benefits due to the unique benefits of FTRs for hedging congestion risk (Bushnell, Harvey and Hobbs 2018; FERC 2022). My analysis is broadly consistent with the latter perspective, but provides insights into how specific policy proposals motivated by the former (such as bidding restrictions) may affect competition.

In order to analytically characterize market power in an FTR auction, I adapt a workhorse model of supply function competition from the literature on imperfectly competitive financial markets (Malamud and Rostek 2017; Rostek and Yoon 2023; Vives, 2008). While this approach is effective for the purpose of this paper, the use of supply function equilibria has long been considered intractable for many applications in nodal power markets (including FTR markets), leading to the use of Cournot equilibria and related approaches such as conjectured supply function equilibria (Day, Hobbs and Pang 2002). For instance, Bautista Alderete (2005) builds a model of conjectured supply function equilibria in FTR auctions. In comparison to Bautista Alderete (2005), my primary focus is the microfoundations of market power rather than computational tractability, making a supply function approach essential. Deng, Oren and Meliopoulos (2010) also study the implications of simultaneous feasibility constraints for prices in FTR auctions, but in an environment with perfectly competitive bidding and flat demands.

Imperfect competition in restructured electricity markets has attracted significant attention both theoretically (e.g., Borenstein, Bushnell and Stoft 2000; Joskow and Tirole 2000) and empirically (e.g., Borenstein, Bushnell and Wolak 2002; Hortaçsu and Puller 2008; Wolfram 1999), but relatively little work has examined market microstructure in realistic nodal power markets. One notable exception is Mercadal (2022), who extends of Hortaçsu and Puller’s (2008) empirical bidding model to the context of nodal power markets with transmission constraints. In comparison, I characterize bidders’ residual demand curves analytically, but without simplifying the transmission network to the same extent as Joskow and Tirole (2000).

More generally, Mercadal (2022) and several other authors have analyzed the role of financial participants in electricity markets (e.g., Birge et al. 2018; Jha and Wolak 2023). Notably, Ledgerwood and Pfeifenberger (2013) and Lo Prete et al. (2019) discuss the possibility that financial speculators may submit virtual day-ahead bids strategically in order to influence FTR values. I do not consider this possibility here. However, this and other forms of potential market manipulation could be relevant to observed auction revenue shortfalls.

2. Market Power in FTR Auctions

Consider a market operator (ISO) that manages a grid with

The ISO may directly allocate FTRs to market participants such as load serving entities (LSEs), sometimes in the form of auction revenue rights (ARRs). After any directly allocated FTRs

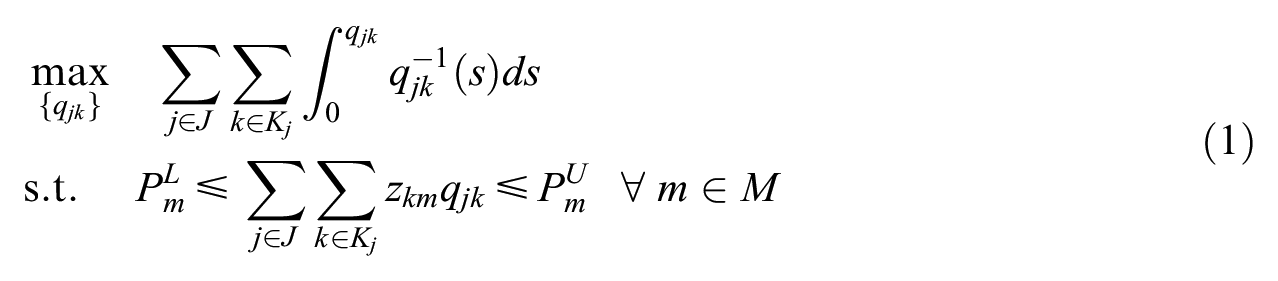

In a standard FTR auction, bidders submit downward-sloping demand schedules for FTR capacity. Suppose bidder

An allocation of FTRs which satisfies the constraints in (1) is said to be simultaneously feasible.

7

In this expression,

Lemma 1 establishes a well known fact regarding market clearing in the FTR auction. In particular, the price of FTR

The FTR auction generalizes the familiar uniform price auction. For example, in a degenerate transmission network with two nodes and a single transmission constraint

In the next section, I analyze optimal bidding in the FTR auction. Before doing so, it is helpful to introduce additional notation. In the solution to (1), let

2.1. Price Impacts Under Simultaneous Feasibility

In a uniform price auction, the market clearing price is the price that exhausts the auctioneer’s supply of the good (provided that demand exceeds supply at the reserve price). In an FTR auction, by contrast, the market clearing price is determined by the solution to (1). Bidders with market power anticipate the effects of their bids on market clearing prices, or price impacts (Rostek and Yoon 2023). In this section, I analyze bidders’ price impacts when market prices are determined according to (1).

For simplicity, suppose that bidders’ participation decisions, preferences, and the distribution of FTR payouts are common knowledge.

9

Furthermore,

where

Optimal bidding requires that the gradient of

When

In a Bayesian Nash equilibrium (BNE) of the FTR auction game with linear bid schedules, each bidder

In order to describe the cross-path strategic interactions induced by simultaneous feasibility, I introduce a notion of connectivity from graph theory.

Proposition 1 uses this definition to relate bidder

For convenience, I assume that

and

where

In a degenerate network with a single FTR and a single binding constraint, Assumption 1 is satisfied whenever there are three or more bidders, mirroring a well-known sufficient condition for the existence of an equilibrium in uniform price auctions with common information (Rostek and Yoon 2023). Assumption 1 generalizes this idea to the FTR auction, in which different bidders may submit bids on different portfolios of FTRs, and some pairs of FTRs may not be strategically connected. For example, if fewer than three bids are submitted on an FTR that is not strategically connected to any other FTR under

We can now state the main result of the paper:

where

Proofs of Proposition 1 and all other results are provided in Appendix A.

The significance of (6) is to clarify the manner in which bidder

To more clearly illustrate the unique features of FTR auctions, it is useful to restrict attention to the special case in which

While for each bidder

Proposition 1 implies that

Inspection of Proposition 1 suggests that an FTR auction produces more competitive bidding for FTR

where

Since

Even in the case of single-path bidding, there may be more than one binding constraint for some component

where

This fact can be used to establish comparative statics for the general single-path bidding case, summarized in Corollary 1 below. In a typical uniform price auction, price impacts are declining in the number of bidders. In the FTR auction, the effects of a marginal bidder are more nuanced. If the set of binding constraints were fixed in advance, then

where

Since one would expect the PTDF matrix

3. Numerical Illustration

In this section, I investigate the market design implications of the model in Section 2 by comparing equilibrium outcomes of a simulated FTR auction to equilibrium outcomes of an benchmark mechanism in which FTR capacity is sold in parallel uniform price auctions.

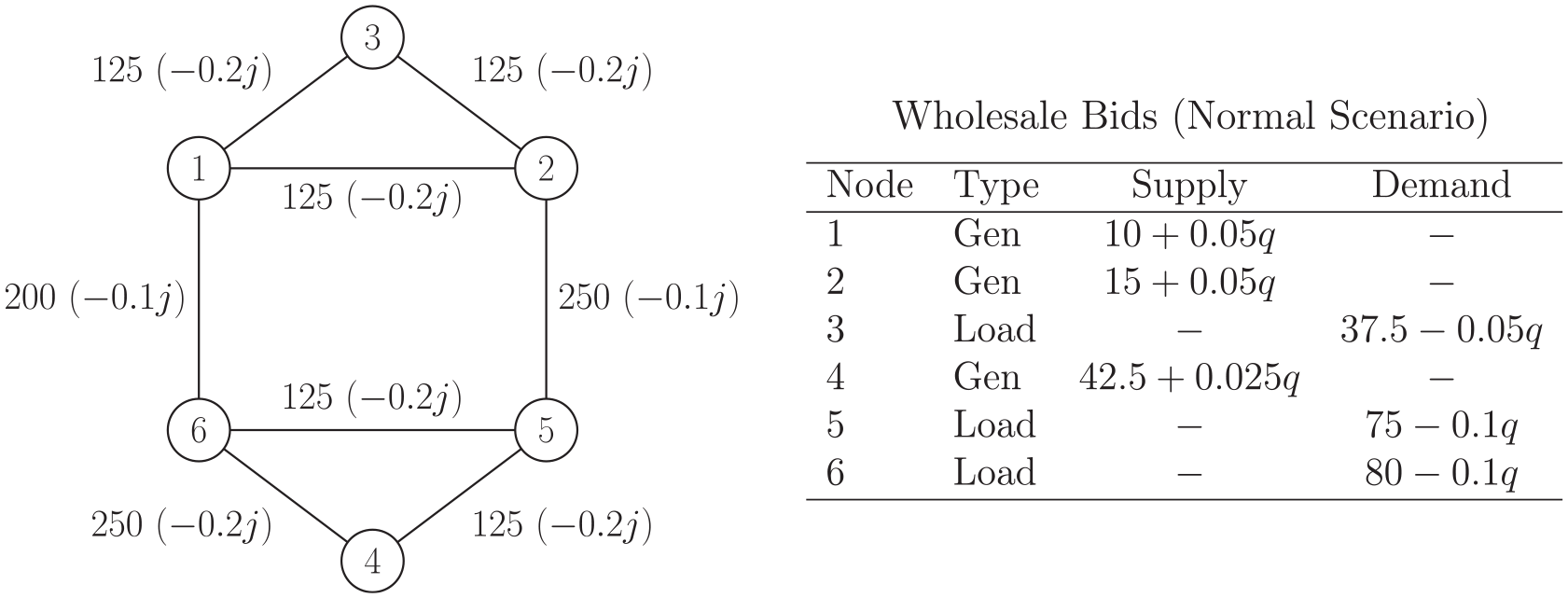

I focus on the six-node test case analyzed in Chao et al. (2000) and Deng, Oren and Meliopoulos (2010). Figure 1 presents a schematic depiction of the network along with node-level supply and demand bids in the wholesale market expressed as a function of the quantity of power

Six-node test case.

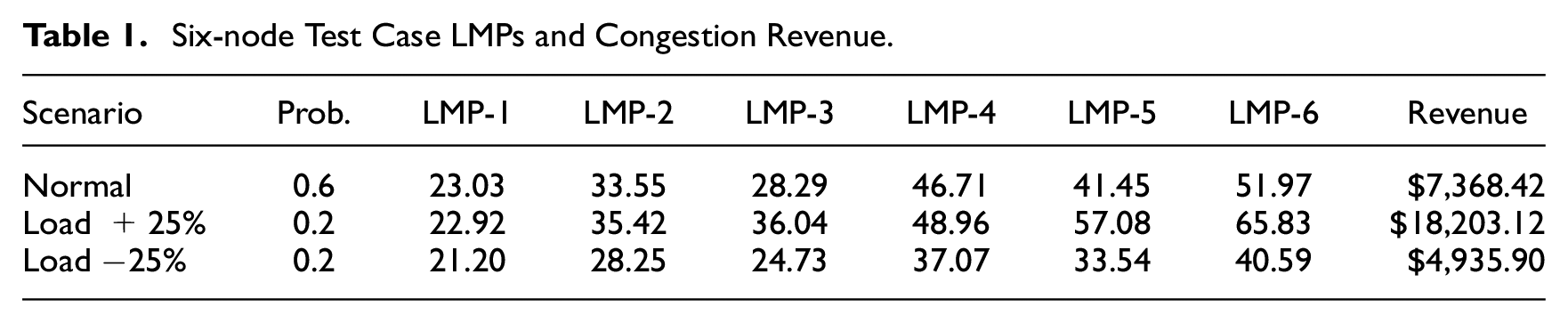

Following Deng, Oren and Meliopoulos (2010), I assume that the intercepts of the wholesale inverse demands can be 25 percent higher or 25 percent lower with known probability, resulting in uncertainty over future congestion. Table 1 indicates the assumed probability of each demand scenario and resulting node-level locational marginal prices (LMPs), which determine FTR payoffs, along with the net congestion revenue earned by the market operator under each scenario. Expected congestion revenue is $9,048.86.

Six-node Test Case LMPs and Congestion Revenue.

The main purpose of this exercise is to compare the FTR auction described in Section 2 with a benchmark mechanism in which the market operator holds parallel uniform price auctions for each distinct FTR. To implement the latter, the market operator must first determine a quantity of FTRs to be sold on each path. To facilitate comparison, I focus on the allocation in which the quantity of FTRs sold on each path coincides with the quantity allocated on that path in the equilibrium of the FTR auction game. 17

All FTRs are purchased by symmetric, risk averse financial speculators.

18

Each speculator bids on one and only one FTR, and there are

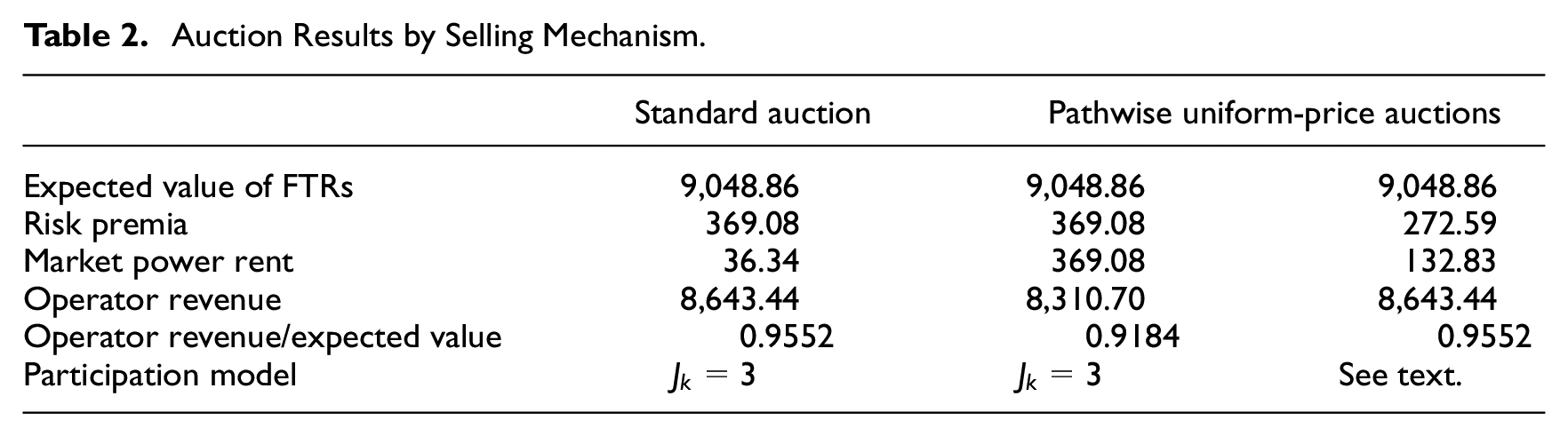

The first two columns of Table 2 present the market operator’s revenue under each mechanism. The standard FTR auction recovers 95.5 percent of expected congestion revenue, while the uniform price benchmark recovers only 91.8 percent. The table decomposes auction revenue shortfalls into risk premia demanded by the bidders and market power rents. Since bidders hold identical portfolios in either case, risk premia are the same for each mechanism. However, the FTR auction reduces market power rents by 90 percent as compared with the uniform price benchmark. In a larger and more realistic network, this effect could be even larger.

Auction Results by Selling Mechanism.

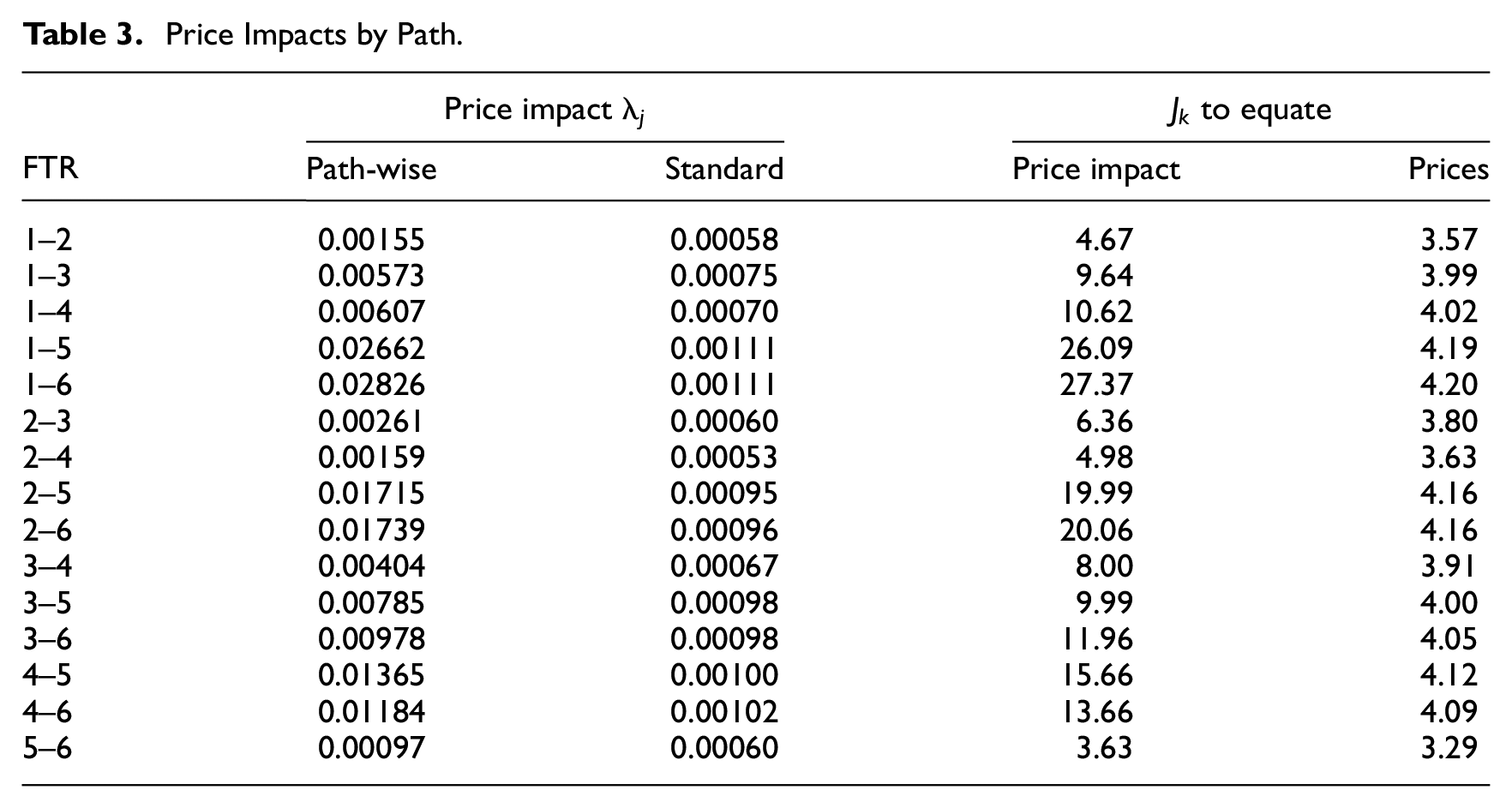

The striking difference in market power rents in Table 2 is a direct result of the cross-path competitive linkages induced by the constraints in (1). In this network, there are fifteen distinct FTRs. All are strategically connected for the relevant range of parameters. The first two columns of Table 3 indicate that the price impact

Price Impacts by Path.

The last statistic describes the degree of competitiveness among bidders in terms of the slope of the equilibrium bid functions. Because new entry dilutes risk, fewer new bidders would be required to eliminate price differences across mechanisms. The fourth column shows the number of bidders needed to replicate the FTR auction clearing prices, accounting for the dilution of risk. Strictly more bidders are required on every path, and 31.5 percent more participation is needed overall. The final column of Table 2 reports aggregate outcomes with this new entry level. Total revenues are the same as in the standard FTR auction by construction, but a greater share of the total shortfall is attributable to market power rents.

For any level of participation, the difference in market power rents across mechanisms depends crucially on the concavity of bidders’ valuations, which is determined by bidders’ risk preference

These findings suggest that for meaningful levels of concavity in bidders’ preferences the FTR auction delivers lower market power rents for the same level of participation on the one hand, and for the same level of auction shortfalls on the other. It is natural to question the sensitivity of these findings to the maintained participation assumptions. Given the seeming complexity of bidders’ potential participation strategies and the likely multiplicity of equilibria, I leave the development of a model of FTR auctions with endogenous entry to future work. Like any other analysis of imperfect competition, the results are predicated on the existence of entry barriers. With sufficient competition, there is no difference across mechanisms. As

4. Conclusion

Persistent underpricing in FTR auctions raises important questions for the design of restructured electricity markets. In this paper, I investigate the contribution of unilateral market power to underpricing. I use a simple theoretical model to demonstrate that the market clearing mechanism used in FTR auctions can facilitate high levels of cross-path competition, which can significantly dampen bidders’ incentives to exercise market power. The numerical model presented in Section 3 suggests that in an FTR auction, market power rents may contribute relatively little to auction revenue shortfalls in comparison to other sources of concavity in FTR bidders’ valuations (such as risk premia or inventory costs).

Today, most ISOs directly allocate some FTRs to LSEs, while selling only “residual” FTRs in the FTR auction. Some observers have suggested eliminating the FTR auction and instead directly allocating 100 percent of FTR capacity to LSEs. Individual LSEs could then choose to sell their FTRs in a decentralized fashion. The analysis suggests that by breaking the strategic linkages across auctions, decentralization could enable speculative buyers to extract significant market power rents at current participation levels. Anticipating this, LSEs would be incentivized to hold larger FTR portfolios, which could be inefficient.

Another potential policy response to persistent auction revenue shortfalls is to eliminate bidding on FTRs that are perceived to be more vulnerable to strategic bidding. This approach was taken by the California ISO (CAISO) in 2018, which banned bidding on so-called “non-deliverable” FTRs. The framework in this paper suggests that this policy could have increased market power rents on the remaining “deliverable” FTRs, since bids on non-deliverable FTR paths exert competitive pressure elsewhere. However, the model presented here sets aside many details relevant to the CAISO’s intervention. I leave an empirical evaluation of the CAISO’s reforms for future work.

Apart from these specific policies, my findings reinforce the importance of separating the question of market power in FTR auctions from broader consideration of the efficiency of ISOs’ congestion revenue management practices. Even if trading profits earned by financial speculators do not reflect the exercise of market power, the central question remains whether the social benefits from FTR auctions exceed observed shortfalls. Conversely, the existence of trading profits (even those earned via market power) does not in itself imply that proposed alternatives would be welfare-improving.

Footnotes

Appendix A

Appendix B

Acknowledgements

This work is adapted from the third chapter of the author’s PhD thesis at Northwestern University. I gratefully acknowledge the support and guidance of Rob Porter, Mar Reguant, and Vivek Bhattacharya. I thank William Hogan, Jingyuan Wang, the editor Richard Green, and two anonymous referees for helpful comments.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

1

Estimates in the literature suggest that financial participants in FTR auctions earn trading profits on the order of $ 0.5 B per year across all US ISOs. This includes approximately $300 M/year in PJM (Leslie 2021), $50 M/year in NYISO (Leslie 2021), and $55 M/year in CAISO (2019). To obtain the $ 0.5 B dollar figure, I divide the sum of these figures by the average share of congestion revenues in these markets among the seven ISOs (as reported in ![]() )). FTRs are also referred to as congestion revenue rights (CRRs) or transmission congestion contracts (TCCs).

)). FTRs are also referred to as congestion revenue rights (CRRs) or transmission congestion contracts (TCCs).

2

I use the term “path” to refer to particular point-to-point FTRs. This terminology is consistent with the ISOs’ own usage, but should not be confused with the older concept of a “contract path” referring to transmission rights on specific combinations of flowgates.

3

Detailed transmission network information is considered Critical Energy Infrastructure Information by the US federal government and is subject to strict non-disclosure policies. Consequently, research on large-scale power systems is typically limited to “synthetic” grids of varying complexity.

4

The identity of the source and sink nodes is not important as negative FTR capacity (“counterflow”) is generally permitted.

5

Note that I consider FTR obligations only. The holder of an FTR obligation is required to pay the ISO when realized congestion is negative. Some ISOs also issue FTR options, which do not require such payments. FTR options are jointly cleared with FTR obligations using a mechanism similar to (1), but with additional constraints (![]() ). As such, the cross-path competitive forces identified in this paper would also be present in a market that included FTR options.

). As such, the cross-path competitive forces identified in this paper would also be present in a market that included FTR options.

6

For the purpose of exposition, I assume that

7

Simultaneous feasibility is enforced by the ISO in order to sure that congestion revenues are sufficient to fund FTR payouts. In practice, FTR payouts are often underfunded due to discrepancies between the network model used in the FTR auction and the network model that is ultimately used in the physical market (see, e.g., ![]() ).

).

9

In reality, some bidders may have superior information for forecasting FTR payouts (Leslie 2021). It appears that private information can be incorporated into the model by extending prior work on uniform price auctions (![]() ), at the cost of considerable technical complication.

), at the cost of considerable technical complication.

10

Since

11

12

13

14

15

16

I do not impose the additional 340MW North-South flowgate constraint discussed in Chao et al. (2000). Relative to Deng, Oren and Meliopoulos (2010), I divide the slopes of the wholesale bids by two, as this results in a more complex equilibrium for the standard FTR auction when the flowgate consraint is omitted.

17

In practice this particular allocation would be unknown and hence infeasible; however, the particular assumption made here does not affect the slope of the resulting bids.

18

In a richer environment with both financial speculators and “hedgers” (firms with significant ex ante congestion exposure and possibly greater risk aversion), the choice of mechanism could have important implications for the surplus of different groups. I thank an anonymous referee for this insight.

19

The main qualitative conclusions should remain unchanged for alternative exogenous specifications of participation. However, even in the polar case of full participation (