Abstract

Maturing renewable energy technologies are birthing new industry configurations, with offshore wind—with the EU holding 80 percent of global capacity—and “energy islands,” as notable examples. However, a clear conceptualization of the role of the state and governance framework is lacking, alongside growing pressure for the state to define the path forward. This paper analyzes recent developments in emerging EU offshore renewable energy regimes, drawing three implications that show the need for new governance frameworks. First, there is a reconfiguration of energy industry structures around changing economics and policies, in a repeat of historical experience. Second, energy islands increasingly represent features of a natural resource in fixed supply, with the economic nature of offshore energy gradually transiting from the sub-domain of renewable energy economics towards natural resource economics. Third, to realize their economic value, governance frameworks are needed to enable these resources to harmonize with other resources in fixed supply, such as the land on which they are sited, which is constitutionally under the stewardship of the state. We set out criteria for governance of these emerging offshore renewables, to underpin the changing industry landscape and new role of the state within it.

1. Introduction

Two interesting trends have emerged in recent years in offshore renewable energy development. The first has been portended by auctions of leases for offshore seabed plots for windfarms off the coast of England and Wales which attracted runaway bids (Jansen et al. 2020; Vasconcelos et al. 2022). These auctions, of sites owned by the Crown Estate and authorized for development under the UK’s 2004 Energy Act, are expected to raise £4 billion over a decade, with much of the proceeds returned to the UK Treasury (and hence the state) under fiscal arrangements through which a quarter of the Estate’s profits are handed back (Jansen, Bieter et al. 2022; Vasconcelos et al. 2022). 1

A second and parallel trend has been the increasing number of zero-subsidy bids for offshore wind power tenders. 2 Analyses suggest that offshore wind auctions in Europe have yielded levelized costs of electricity at the lower end of estimates for fossil fuel-based generation (€50–55/MWh) (Jansen et al. 2020; Jansen, Bieter et al., 2022). These changing dynamics herald an era of “subsidy-free” windfarms in some jurisdictions this decade (Jansen et al. 2020), indicating that state support to renewable energy has enabled their scaling up and cost efficiency.

As renewable energy technologies mature, new concepts and models for offshore energy are beginning to emerge; the most recent relates to offshore energy islands, with Denmark as the first jurisdiction to announce building islands 80 km off its North Sea coast, to be operationalized by 2033 (Marczinkowski, Østergaard and Mauger et al. 2022; McKenna, D’Andrea and González 2021). 3 According to the Danish Energy Agency “the concept covers the definition of an existing island, the construction of an artificial island, or an island based on a platform serving as a hub for electricity generation from surrounding offshore wind farms, that will be connected and distribute power between Denmark and neighboring countries.” It also states that energy islands “envisage the connection of various offshore technical equipment for electricity generation, for example, facilities for energy storage, hydrogen or electrolysis plants, or other energy conversion technologies (e.g., Power to X).” 4 The governance framework aims at “supporting strong private-public cooperation.” In September 2021, a broad political agreement outlined the frameworks for ownership and construction, envisaged as a limited company with a minimum 50.1 percent share of state ownership, but with little detail about the roles of state and private players (Ministry of Climate Change 2021).

Energy islands are also expected to create synergies with regional industrial and maritime economic clusters, as offshore renewables are seen as an integral part of the EU Green Deal (European Commission 2020; Nepal and Jamasb 2015). Examples elsewhere in the region are the Dragon Energy Island project and two projects west of Shetland and in the central North Sea, in the UK. If successfully demonstrable, historical experience suggests that the types of projects and structures that emerge in these countries may also be adopted outside of Europe (Nepal and Jamasb 2015).

The question of how the new configurations will be governed remains open, yet one that is becoming increasingly important, especially given issues around not just ownership and operation, but also the distribution of the benefits that might be generated, in terms of revenues flowing to the state, as well as positive and negative externalities impacting the welfare of citizens and the environment. Like offshore hydrocarbon resources, offshore renewable sites can cross national jurisdictions, requiring economic and political agreements among governments. While technologies and commercial configurations around energy islands are progressing, the conceptualization of the role of the state and governance regime is lagging.

This paper analyses recent developments in offshore renewable energy—the latter technically incorporates different forms such as tidal, geothermal and wind—but in this paper we focus on offshore wind power as the only renewable resource to have birthed a new governance regime. We draw mainly from countries within the EU, which represents 80 percent of global offshore capacity for wind (Wilson 2020). Our analysis highlights three implications for their governance. First, energy islands represent a reconfiguration of established energy industry structures around changing economics and policies, in a repeat of historical industry trends (Sen, Jamasb and Nepal 2018). Second, they present features of a natural resource in fixed supply, with the economic nature of the resource gradually transiting from the sub-domain economics of renewable energy to economics of natural resources. In the latter, renewables such as offshore wind derive their value from being bundled with other natural resources in fixed supply (e.g., land). 5 Third, to unlock their full economic value, offshore energy resources need to be viewed in conjunction with other related natural resources that are in fixed supply—such as land and siting locations, which in most countries is constitutionally under the stewardship of the state on behalf of citizens (Segal 2012).

The latter point is pertinent in the context of early taxpayer funding of “green subsidies” for the development of renewable energy. As these subsidy regimes—for instance, those based on two-sided Contracts for Difference (CfDs)—run their course, developers would cease receiving government support for the difference between the agreed strike price and market price of electricity, and instead make equivalent pay outs. This raises questions over the distribution of the revenues from these pay outs among citizens, and the sharing of benefits between countries that co-develop the resource (e.g., in the EU energy market) and overall impact on welfare (Tossato et al. 2021). A related implication pertains to the sharing of risks and public and private sector involvement in development of these resources. The question that this review paper addresses is: what are the implications of these developments for the future of governance and economic regimes of offshore energy as a natural resource?

2. Rationale for Governance Regimes—A Return to “First Principles”

The rationale for governance regimes for energy resources in the literature on natural resources pertains to two main aspects, namely, the economic characterization of the resource, and the arrangements around its provision (e.g., ownership structure and industry organization). Energy and related services as well as associated infrastructures can be characterized as global public goods. Different global public energy goods may require provision of specific technologies, financing needs and different industrial and institutional arrangements (Escribano 2015).

This is reflected in the organization of the electricity industry. Its early organization was aligned with the characterization of the resource as a pure public good, and in public policy terms as a public service. It was driven by economies of scale, with large, vertically integrated organizations (often state-owned) responsible for investment and operation of the system, and prices set on a cost-plus basis. As public ownership was diffuse, it was difficult to align the objectives of the owner (the state) with those of managers. Further, state-owned monopolies were unable to apply hard budget constraints to ensure revenue sufficiency and this in turn constrained investments in the sector (Schmidt 1996; Shleifer 1998; Triebs and Pollitt 2017). In the 1990s, market-based reforms led to a configuration of the industry that gradually turned electricity (and more widely, energy) into a marketable public good—that is, rivalrous to the extent that consumers paid to access it, but largely non-excludable (Steiner 2000).

As most countries are moving to decarbonize their energy sectors, new configurations of the energy system based on electrification are being proposed with a view to optimizing across the energy system rather within individual vectors and sectors. In this context, offshore wind energy is a promising technology for achieving renewable energy supply and decarbonization targets in jurisdictions that lack adequate alternative resources that are conducive to other large-scale renewable technologies—such as low solar irradiation regions in Europe (Esteban et al. 2011).

As the offshore wind industry matures, its integration into wider national and international energy systems is proposed through offshore energy islands located in areas with favorable wind conditions. They are also seen as a solution to intermittency, and hence to negative prices, and government and investor interest in them appears to stem from the first-mover advantage of developing the most suitable sites (e.g., through developing associated industry supply chains, and potentially exporting the energy produced). Offshore energy resources (including the emerging concept of offshore energy islands) represent the latest iteration in the configuration of the industry through “green” reforms, of which the primary drivers are technology and policy targets—through private sector involvement, innovation, and public sector funding.

Under this emerging paradigm, the provision of energy can be characterized in further ways. In the EU context, one exposition proposes that while support of renewable energy is a public good, the arrangements around its provision through collective agreements by Member States committing to emissions and renewable energy targets and renewable energy turn it into a club good (non-rival and excludable) (Newbery 2019). Conversely, a case has been made for energy islands—which entail aggregations of energy resources bundled with a network infrastructure to produce and transport them—as common pool resources (rivalrous and non-excludable), referring to a natural or man-made resource system that can make access to it costly, but not impossible to exclude other beneficiaries from its use (Kunneke and Finger 2018). Such infrastructures can be viewed as non-excludable resources: they might be spread through a large geographical area with difficult-to-monitor access points; and, even when access could be monitored, there might be politically motivated universal service obligations, related to the provision of essential services (e.g., energy) (Newbery 2019). Further, once users enter the network, it is difficult to determine the precise services they appropriate from the network; a further feature of common-pool resources are the diffused property rights and decision rights with respect to the resource system and the appropriation of its services (Newbery 2019).

The practical implications of these emerging reconfigurations of the energy industry relate to how the new structures are to be governed and coordinated. In liberalized markets, which were a core feature of “second-generation” electricity reforms, the coordination functions among a multitude of actors across the supply chain were achieved through a combination of market and regulatory incentives (Roques and Finon 2017). The policy and economic dynamics of the “green” transition and technological progress are rapidly reshaping the European energy industry, with implications for other parts of the world that have tended to mimic these configurations. These changes require revisiting important aspects pertaining to governance regimes and the role of the state in the emerging offshore energy sector.

3. Economic Characterization of Offshore Renewables as the “New” Natural Resource

Until recently, the development of offshore renewable energy (primarily wind) was incentivized through subsidy mechanisms which provided a form of revenue stabilization that has allowed projects to get off the ground. These mechanisms served two objectives, (i) technological progress and cost reduction through learning-by-doing, and (ii) increased renewable energy output and security of supply. As the cost of subsidising offshore renewables declines below a threshold level, an increasing share of offshore wind subsidies could effectively begin to work as a tax (or a negative subsidy).

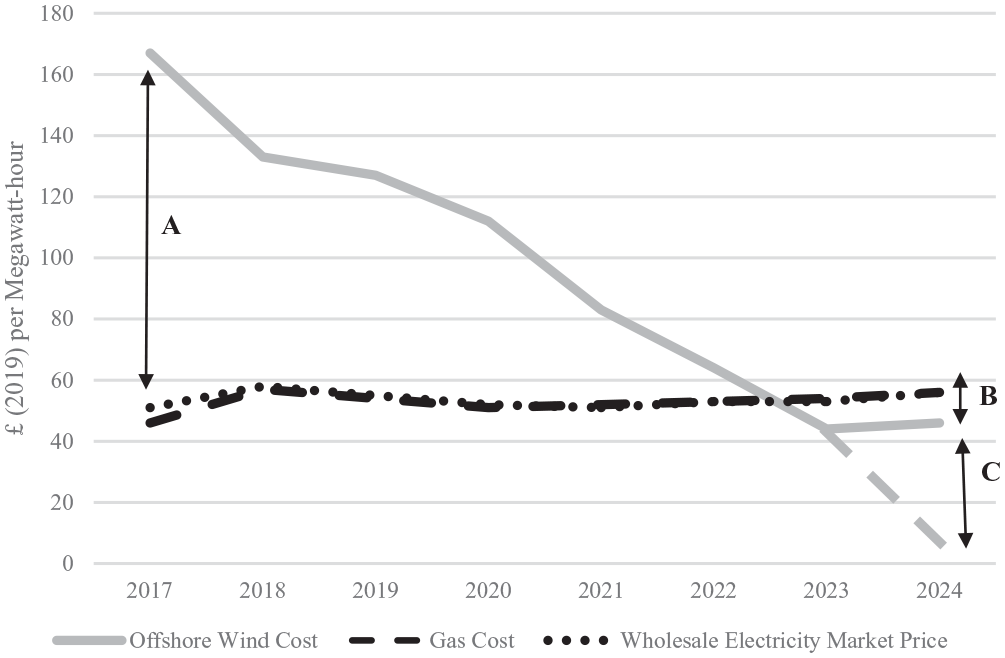

This effect depends on the subsidy regime underpinning the offshore windfarms—ranging from the earliest, legacy contracts to the later CfD auction tenders (e.g., in the UK, from the investment contracts awarded in 2014 through to the CfD auction rounds from 2015–2019)—and on the wholesale market price of electricity. A recent study shows that most remuneration schemes provide some form of revenue stabilization, but their policy design varies and includes feed-in tariffs, one-sided and two-sided CfDs, mandated power purchase agreements, and mandated renewable energy certificates—with less mature markets tending to adopt lower-risk schemes (Jansen, Bieter et al. 2022). For offshore windfarms with two-sided CfD contracts, which have featured heavily across multiple countries, when the cost of offshore wind (and potentially the strike price) falls below the wholesale market price, wind power producers would stop receiving a top-up subsidy that makes up the differential between the CfD strike price and wholesale price (Figure 1, shown by “A”). Instead, they make pay outs to the government of that difference (Figure 1, shown by “B”)—effectively, a negative subsidy. Contingent upon the terms of contracts, if technological advancements were to lower the cost of offshore wind further below the strike price, this could lead to a “windfall” to the producer, that is, the difference between the pay out and the lower costs (Figure 1, shown by “C”).—this could especially hold when grid connection costs are socialized—that is, when offshore developers do not bear these costs, meaning they could achieve positive returns faster.

Costs of UK generation and existing/projected wholesale electricity prices.

These dynamics are crucial for future offshore energy regimes, which can determine the extent to which the state (and other parties) can benefit from the resource flows. There are indications that the zero-subsidy case is beginning to occur. For example, in the UK, in CfD round three, the winning strike prices were 18 percent below the forecasted market prices. In recent rounds, the windfall is expected to accrue to the Crown Estate, under the existing contractual regime (Jansen, Bieter et al. 2022). The Thor tender, a recent offshore wind development in Denmark, was awarded for a record low strike price of 0.01 Danish Krone (DKK)/kWh—implying that all revenues would flow to the state. However, a recent analysis suggests that the government had foregone revenues due to a cap on the payment streams from the winning bidder to the state, set at 2.8 billion DKK; a bid of 0.01 DKK/kWh was thus essentially equivalent to an offer to pay 2.8 billion DKK to the state for permission to build the offshore wind farm (Evans 2019). While a short-term view is that this arrangement was to incentivize the developer, it underscores the fact that governments need to adopt a long-term vision when designing the governance regimes for offshore energy.

As the policy costs of subsidizing intermittent renewables have been borne by consumers, there may be a case for including a provision in the governance regime that explores the utilization of windfalls to further spur on the development of offshore resources or to spread its benefits to consumers, or local communities. For instance, the creation of Offshore Wind Wealth Funds for the UK has been suggested as a condition of support provided in CfD auctions, under which offshore wind farms could pay a minimum community benefit of £0.50 per MWh (approximately £2 m/year for a 1 GW offshore wind farm) (Birkett 2021). This illustrates the need for a new governance regime, separate to the existing incentives for offshore energy development, to capture and distribute any surplus that may be generated over the lifetime of a project. It also raises questions around the true economic value of offshore renewable energy resources, and how this value should be hypothecated and distributed—for instance, as revenue flowing into general government budgets that is allocated towards public expenditures, or alternatively, as an income-generating asset, the proceeds from which should be utilized to improved inter-generational welfare. The latter approach has dominated in the literature on exhaustible natural resources (Segal 2012) for two reasons: first, the feature of exhaustibility necessitates some institution to preserve intergenerational wealth; and second, for reasons of transparency around the utilization of revenues (and in some cases, public support for their development). While the same logic may not fully apply to a “wealth fund” supported through renewable natural resource rents as intergenerational equity may have lower relevance, an argument applies in terms of clearly demarcating revenues from natural resources for a specific economic objective—for instance, reinvesting these revenues to improve environment and sustainability in other areas of the economy and society (Segal 2012).

In economic terms, the siting of offshore renewable energy is constrained by two factors: First, scarcity of prime sites (e.g., favorable wind conditions, favorable water depth, relative proximity to large electricity markets, and connection to mainland). Second, public concerns related to noise pollution, visual and biodiversity impacts, land utilization, and other environmental concerns (Escribano 2015; Nazir et al. 2020). Siting relates not only to the location of the offshore resource, but also to the landfall connection points: for offshore renewable energy developers this relates to consenting procedures required to gain access to a location on the mainland through which energy produced offshore can be sold on markets. Procedures tend to differ by country, which impacts the supply of suitable sites for harnessing the offshore resource and for bringing it into mainland energy markets. For instance, in the UK, developers are required to undertake all consenting procedures, whereas in the Netherlands the government provides consent and access to the grid, with the developer only required to find a suitable off-taker) (Jansen, Duffy et al. 2022).

Taking the above factors into consideration, as offshore wind energy is bundled with scarce natural resources such as land, and fixed infrastructure (e.g., through interconnected energy islands), offshore energy in addition to deriving its value solely from being a renewable resource (relative to non-renewable, polluting resources, or hydrocarbons) presents some features of a natural resource in fixed supply, which governance regimes need to take into account. Natural resources are characterized as flow (naturally renewed in the short term) and stock (fixed in supply). Offshore energy islands represent resources with both flow and stock properties. Natural resources in fixed supply also generate economic rent, and the governance of natural resources has largely focused on the appropriation and utilization of this rent. For instance, the “Hartwick Rule” suggests that rents from non-renewable resource extraction should be invested in reproducible capital (Hartwick 1977).

The different conceptions of rent focus on the benefits accruing to a factor of production over and above what is required to maintain that factor in the productive activity, though they highlight different circumstances by which these payments come about (World Bank 2021). This is underpinned by the idea that the scarcity of a stock resource leads to the generation of economic rent—the difference between the market price of the resource and the opportunity cost of supplying the resource. Pure rent represents a surplus or financial return not required to motivate economic behavior and does not influence production decisions—this underpins the theoretical argument that governments can appropriate a large share of rent from a resource using different instruments (Baunsgaard 2001). Rent is thus a function of the “supply price of investment,” which is the return required by an investor to justify a decision to invest; this covers the costs of capital and operation, and a risk premium. For a given return on total investment, the lower the supply price of investment, the higher is the rent (Baunsgaard 2001). Whilst the costs of capital and operation (particularly for offshore resources) are set to some extent on world markets, the risk premium is influenced by political risk and commercial risk (Joskow 2011) as well as institutional arrangements (e.g., fiscal or contractual systems) around provision of the resource.

The inexhaustible nature of renewable energy resources poses new challenges to the concepts of value and thus rent. This is most obvious for wind and solar resources, which are globally available (though variable in quality). At foreseeable demand levels, there is no natural scarcity of these resources. Scarcity can arise locally, as a given site can be used for production by one economic unit at a time (Baunsgaard 2001). Scarcity may also be arbitrarily imposed, for example, through legislation granting excludable rights to generate and sell energy from these sources. Though the sun and the wind per se are not scarce, different locations have greater or lesser access to them (BEIS 2019).

Taking this argument further, the economic characteristics of energy islands lend themselves to the generation of Ricardian rent, that is, differential rent accruing to areas with different resource endowments or characteristics. In the long-run, more productive (sunnier, windier, or closer-to-market) sites earn Ricardian rents. Over time, as productive sites become scarce, developers either invest in improving the output of more productive sites (intensive margin), or alternatively, search for less productive, and more costly to develop, sites (extensive margin). In the short-run, opportunities for entrepreneurial and quasi-rents (also called Marshallian rent) also exist; rents are accrued due to innovation or changes in the market and are competed away in the long term.

The value of offshore renewable energy in this context is underpinned by their bundling with other natural resources (e.g., land). Further, new industry (re)configurations can build on this bundling (e.g., energy islands). Price dynamics in electricity markets with high penetration of renewables show that they do not operate in isolation from the wider energy system, mainly due to the intermittency issue. For instance, markets with high intermittent renewables penetration in Europe (e.g., Germany) have seen greater frequency of negative wholesale electricity prices, because of which existing projects receiving subsidies, upon ending of their subsidy contracts, may face competition from more efficient renewable generators added to the system in the interim. A system value-based approach, as opposed to the conventional cost-based approach, has been proposed when assessing the effect of renewables on the system (Jansen, Bieter et al. 2022; Joskow 2011). The rent arising from offshore locations is notionally referred to as “locational rent,” whereas the rent arising from landfall connection points is “positional rent.” There are other factors that can influence locational and positional rent—for example, the presence of congestion on networks.

4. Lessons from Experience in Offshore Energy

The governance of most offshore energy regimes has traditionally been centered around the extraction of rents from exhaustible hydrocarbon resources. These have entailed institutional arrangements for ownership, operation, and sharing of revenues between governments that administer resources on behalf of the state and take on many roles, and private or state-owned firms that develop and extract the resources (Frankel 2010). In designing offshore renewable energy regimes synchronous with the characteristics of this industry, insights can be drawn from the governance of upstream hydrocarbons (Humphreys et al. 2007). Jurisdictions with similar hydrocarbon endowments have adopted different regimes and experienced different outcomes from their development. Some have used the rents from the extraction and monetization of resources to support public welfare and market-shaping policies in sustainable investment and productive activity (Mazzucato, Ryan-Collins and Gouzoulis 2020). In others, natural resources have not increased the welfare of citizens (Mazzucato, Ryan-Collins and Gouzoulis 2020).

A notable example is the different approaches followed by Norway and the UK in developing North Sea offshore hydrocarbon resources. While both countries produced similar amounts of hydrocarbons from their reserves, the Norwegian state earned nearly two and a half times more revenues than the UK (Table 1). This was due to a combination of taxes and fees, the State Direct Financial Interest, and dividend from the participation of state-owned petroleum companies. In contrast, in the UK, revenues were obtained mainly from taxes and fees.

Norway Versus UK Oil and Gas Production and Revenues, 1971–2011.

Regimes for the management of exhaustible natural resources have broadly been categorized as “liberal” or “proprietorial” (Bindemann 1999; Mommer 1999). Liberal regimes are characterized by zero marginal fiscal take, where the state taxes only excess profits, careful not to obstruct the free flow of investment—with the aim of keeping prices low through efficient management of the natural resource and unhampered productivity (Johnston and Johnston 2015). Taxes are based on net income, necessitating information on prices, volumes, costs and investments. Liberal regimes aim at hydrocarbons being produced as soon as they are profitable for firms to do so (Johnston and Johnston 2015). In the UK North Sea regime, fiscal terms were frequently altered to enable more efficient extraction and production.

Proprietorial regimes are characterized by positive marginal rents, reservation ground rents, and taxation of excess profits; the purpose is to collect higher ground rents, and taxes are based on gross income, necessitating information only on prices and volumes (Johnston and Johnston 2015). In Norway’s North Sea hydrocarbon regime, fiscal terms remained unchanged for extended periods and the use of resource revenues by governments was governed by strict rules, enshrined in legislation, and aimed at maintaining the values of the resource rent and cultivating intergenerational equity.

The proprietorial offshore regime approximates to a “concessions” governance regime (royalty combined with taxes) while the liberal regime approximates to a “contractual” governance regime (production/profit/revenue-sharing, combined with taxes on rent). Governance terms can be calibrated to mimic the same outcomes under either regime, and many countries have adopted hybrid systems, combining features of both (Johnston and Johnston 2015). Given that equivalencies can be achieved through the different fiscal instruments, the selection of instruments is contingent upon the objectives that governments wish to achieve, and upon the trade-offs between different instruments. In addition to the capture of resource rent, the governance regime for offshore hydrocarbons has been used for wider fiscal objectives—such as the financing of government expenditures (for which the energy sector can be a substantial source of revenue), the balancing of distributional objectives, discouraging wasteful consumption/encouraging efficiency of energy use, and the pursuit of wider economic goals (Nakhle 2008).

4.1 Key Features of Offshore Renewables Development in Europe

Table 2 summarizes the main regime types, instruments and key features used in the development of offshore renewable energy resources to date in Europe. The development of natural resources is typically characterized by large capital investments, long lead times, incomplete information, differences in the abilities of parties (i.e., the government, or its deputed state-owned company, and private firms) to bear the risks in the venture, and balance of risk-reward sharing (Johnston and Johnston 2015). Offshore governance regimes need to enable parties to enter into institutional arrangements that take cognizance of these factors to develop the resource. When a government or state-owned company enters into arrangements with firms it might expect to be provided with capital, technology and expertise. The objective function of the government is to achieve optimal outcome for consumers and citizens (Johnston and Johnston 2015) while facing constraints such as international competition for risk capital and technology, information asymmetry, and in the case of private firms—the incentive to maximize revenues. Governance regimes for offshore non-renewables have, for instance, been based on governments attempting to design optimal and efficient contract arrangements (Johnston and Johnston 2015) bearing in mind that the parties to the contract may renegotiate at a future period.

Main Features of Offshore Wind Energy Governance Regimes.

Source: Jansen, Bieter et al. (2022), Joskow (2011).

From Table 2, we can identify five different stylized roles for the state in the development of offshore energy resources. These roles are not necessarily mutually exclusive, and a given regime can potentially contain a hybrid of attributes of the five roles. Among these, it could be argued that the fiscal state is the most prevalent across all regimes, as the management of fiscal flows is an existential function of the state.

The Landlord State

The government or state owns the land upon which the resource is situated and leases it to developers. The objective of the state here is to generate as much ground rent as is possible over the lease period. Revenues from the rent could flow into national general budgets and be used as state expenditure.

The Fiscal State

The state carries out its “traditional” role of taxation of income and rents over and above what is necessary to earn a normal return. The state may also, from time to time, revisit the fiscal terms ex ante or (e.g., windfall taxes on resources) or ex post (e.g., higher corporate income taxes). Ideally, the regime under which a fiscal state operates should have an equilibrating effect on the flow of normal profits and revenues.

The Custodian State

The state serves as a custodian of the energy resource on behalf of citizens; the objective is to maximize the value of the resource for citizens. Governments would use their bargaining positions to offer contractual terms that provide sufficient incentives for private companies to enter into a contractual arrangement and to develop resources, while ensuring that they will not appropriate all incremental benefits. State participation could be one route to maximizing the value of the resource for citizens.

The Entrepreneur State

The state takes a more active role in the development and monetization of the resource—this could be through direct equity participation or joint operatorship, or through a state-owned enterprise (e.g., an energy producer or an infrastructure provider) acting on behalf of the state’s interests. The state-owned entity would operate at an arm’s length and be subject to the standard regulatory rules like other actors in the institutional arrangement.

The Regulatory State

The state does not directly engage in the provision of energy (and other welfare) goods and essential services, but intervenes to correct particular market failures, provides conditions conducive to the competitive provision of energy goods and services through loosely coordinated sets of public agencies, and through replacing pure public ownership of energy assets with a network of private (or public) developers or providers, regulated by specialized agencies operating at arms’ length from the government under a transparent legislative framework. The regulatory state also could refer to a supra-national state with democratic and hence political legitimacy (Yeung 2010).

A useful approach for analyzing governance arrangements between the parties to a contract to develop a natural resource is principal-agent analysis (Bindemann 1999). This emphasizes the actions of a principal (e.g., a government), as the owner of an asset, and an agent (e.g., private investor), who develops and manages the asset and whose decisions can affect its value. The approach focuses on the design of contracts between the parties. If the private entity is a consortium, this becomes a principal-agent problem with many agents. The principal will aim to design a contractual regime such that its interest will be advanced by the agent although the interest of the latter may diverge from that of the former. The principal needs to provide incentives to induce the agent to act in the principal’s interest in the presence of information asymmetry; it also needs a monitoring system to measure the agent’s performance and avoid moral hazard—achieved through structures such as incentive contracts which reward agents for good performance, or through penalties for underperformance (Joskow 2011).

An alternative is for the state as the principal to become its own agent—for instance, through state-owned enterprises. In practice, this has been translated into offshore governance regimes based on mechanisms such as production and profit-sharing agreements, technical service agreements, and state-owned enterprises acting on behalf of the state (Johnston 1994). Such regimes tend to distinguish between two periods: in the first period investments are sunk into preparing the resource for monetization and could involve the principal (e.g., the state) investing jointly with the agent (e.g., the private company leasing the offshore field in return for payment of a “ground rent”); as a result the value of the resource can increase in the second period. Theory and evidence suggest that it is in the interest of the principal to keep the first period as short as possible and draw up a new contract for the second period in order to achieve a higher ground rent (Bindemann 1999).

In the development of offshore energy, one could envisage multiple configurations of principal-agent contracts: for instance, several principals (e.g., neighboring states in the North Sea) and one agent, one principal acting on behalf of a consortium of principals, and several agents (acting in coordination, or as a consortium). The above configurations have been applied to the ownership and management of exhaustible natural resources—notably, in the exploration and development of hydrocarbons. However, in case of the latter, property rights are clearer, and there is usually a singular principal (or government as “custodian” of the resource), and singular or multiple agents (private sector entities).

5. Governance of Offshore Renewable Resources

The technological and cost developments in the offshore wind sector suggest that governments will increasingly find themselves as a stakeholder and custodian of a natural resource bundled with other resources in fixed supply, and critical infrastructure, raising debates around ownership, operatorship, and the division of risks and revenues. This implies the need for a forward-looking framework for the governance and management of offshore energy resources which capture the economic value of the resource. While the resource base and market price of the commodity produced (e.g., electricity) are exogenously determined, governance arrangements are endogenous and can play a key role in determining how the value is maximized and captured for the benefit of all stakeholders. In designing governance regimes for developing offshore energy resources, policymakers need to account for a set of criteria, outlined in Table 3.

Criteria for Effective Governance Regimes for Natural Resources.

Source: Carlaw and Lipsey (2021), Joskow (2011).

In practice, there are trade-offs among these criteria that need to be balanced as in the following (Humphreys et al. 2007; Nakhle 2008).

There is a trade-off between neutrality and simplicity. The design of neutral regimes requires detailed information (e.g., on a field-by-field or farm-by-farm basis) and the calculation of different levels of rent. An example of a simple tax is a royalty, which is easy to calculate and administer but is not neutral.

Similarly, neutrality trades off with revenue generation and with efficiency. An example of a neutral tax conceived (but rarely applied) for offshore oil and gas resources was the “Brown Tax.” This involved governments paying out a subsidy to incentivize exploration, which was converted into a tax when production reached a particular level.

Equity trades off with simplicity and efficiency—the former is due to the fact that “equity” or “fairness” takes different meanings to different taxpayers. The latter is because an equitable tax is not simple to administer—for instance, a “progressive profit tax” requires information on costs and profits (e.g., on a field or farm basis).

Stability conflicts with fiscal risk—Fiscal systems resemble incomplete contracts and they seldom remain unchanged for long periods of time. This is often due to sustained exogenous economic changes, and the accountability of governments to their electorates.

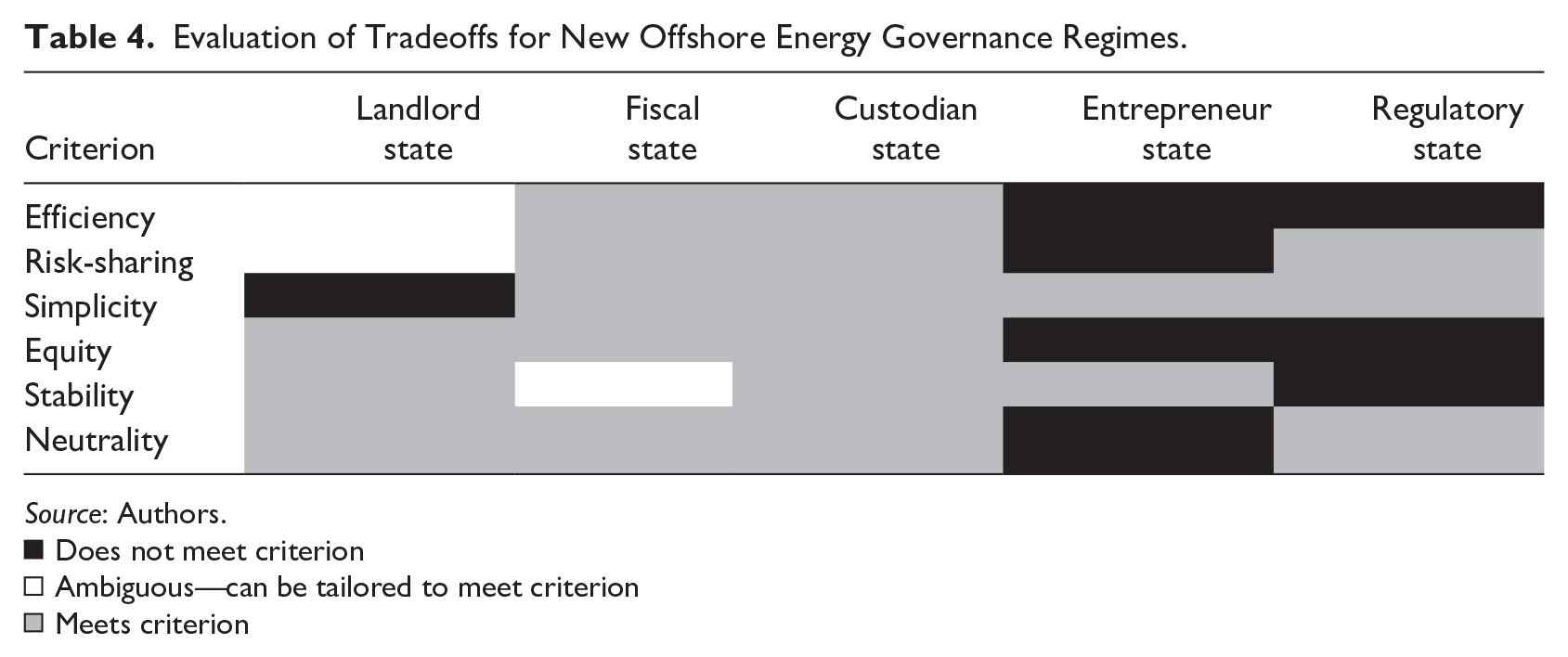

Based on the discussion above, Table 4 maps the trade-offs amongst different criteria in relation to the different roles of the state in the new offshore energy governance regime.

Evaluation of Tradeoffs for New Offshore Energy Governance Regimes.

Source: Authors.

Does not meet criterion

Does not meet criterion

Ambiguous—can be tailored to meet criterion

Ambiguous—can be tailored to meet criterion

Meets criterion

Meets criterion

Four broad implications can be drawn for new and emerging offshore renewable energy regimes. First, future offshore governance regimes will differ from those of offshore hydrocarbon resources in that the products are not traded on international markets but are supplied to localized (regional or country) markets with specific characteristics and contexts. Economic and security of supply considerations invoke the “logic of collective action” in the governance arrangements for a harmonized regulatory framework to coordinate and optimize the use of these resources. The logic of collective action suggests that a subset of members of a group with specific interests tend to organize themselves to achieve specific common objectives. For instance, within the EU, North Sea countries arguably have a common interest to promote offshore renewable resources and are exploring joint solutions to a coordinated development of these resources.

This links back to the role of the regulatory state. One could look to other governance regimes framing ownership and operatorship of services that are connected with natural resources in constrained supply (in the context of positional or locational rent)—for example, ports, which represent a mix of public and private goods. The location of ports, for instance, is related to locational/positional rents drawn from their siting for example, proximity to larger markets, or which facilitate lower transport costs. While ports generate direct economic benefits to the state, in the form of flow of trade or commerce, their development and operatorship may be conducted by private parties which aim to optimize their revenues from the same. Contractual arrangements for ports need to balance the risk/reward structures for port operators, the state, and port authorities. One outcome that emerges from our review and worthy of further investigation is therefore path dependency—and the extent to which states with experience in offshore non-renewable energy resources (e.g., UK and Norway) have replicated their experience for new offshore resources.

Second, governance regimes should unlock, maximize, and balance the economic value of offshore renewable energy for stakeholders and citizens. This could potentially be through lower or less volatile electricity prices, or capturing value in other ways (e.g., through fiscal arrangements). This implication necessitates a clearer definition of “value” for offshore renewable energy, and recognizing they have elements of flow and stock characteristics of other natural resources. The differences in flows of revenues from similar grades of offshore renewable resources (e.g., Demark and the UK) demonstrate the importance of recognizing that urgency to develop these resources to meet climate change targets. At the same time, a long-term view is also needed on the value of these resources to investors, governments, and citizens, in alignment with the entrepreneurial role of the state.

Third, governance regimes should incentivize investments in alignment with the entrepreneurial and regulatory roles of the state. The governance regime could identify and allocate the balance of risks between the different parties involved, ensuring that risk-takers receive sufficient incentives to carry the projects to completion. Contractual regimes could ensure that rents are maximized and distributed optimally, as for instance, has been the case with offshore hydrocarbons. The experience in offshore renewable energy has thus far been mixed in this regard, partly because the “ideal” configuration of the offshore energy sector is yet to take shape. The trade-offs discussed above can provide a taxonomy of principles to design such regimes.

Fourth, offshore renewable energy systems could be viewed as an unprecedented innovation effort in terms of scale and scope of activities. At the early stages of development of this new sector, considerable innovation is required to achieve maturity. Experience with innovation and development of complex new systems suggests that government support plays an important role—in alignment with the entrepreneurial state (Carlaw and Lipsey 2021). The governance regime should recognize that the sector is likely to be in a state of transition before it reaches commercial scale and technological maturity. The policies in place relating to offshore wind and energy islands are also aimed at driving innovation and serving the development of a (ideally in the future) tax-paying industry, compared to oil and gas extraction as a mature industry at the far right of the cost/learning curve.

3. Conclusion

The value of renewable energy resources has, thus far, been defined entirely in relation to their utility from replacing fossil fuels. However, the analysis of recent developments in this paper suggests that offshore renewables will rapidly mature into the domain of natural resources in their own right. Therefore, lessons from the governance and economic management of natural resources will increasingly become relevant if governments, as custodians of these resources, are to ensure that the sustainability and long-term economic value of these resources is maximized.

This paper contributes to the literature by highlighting three implications for new governance frameworks. First, there is a reconfiguration of energy industry structures around changing economics and policies, in a repeat of historical trends. Second, energy islands will increasingly represent features of a natural resource in fixed supply, with the economic nature of offshore energy gradually transiting from the sub-domain of renewable energy economics towards natural resource economics. And third, to realize their economic value, frameworks are needed to enable these resources to harmonize with other resources in fixed supply, such as the land on which they are sited, which is constitutionally under the stewardship of the state.

This paper also makes a case for a measured approach to developing offshore renewable energy governance regimes. We identified the distinct potential roles of the state: “the landlord state,” “the custodian state,” “the entrepreneur state,” “the fiscal state,” and the “regulatory state,” as well as the issues and options associated with each on the development of the offshore renewable energy sector. A hybrid regime combining these roles is conceivable, but this needs to be carefully devised. The offshore renewable sector is at an early stage of development and could evolve further before attaining maturity. Therefore, the institutional and economic features of the governance regime will need to promote innovation and be adaptive as the sector develops. To conclude, the energy sector is undergoing radical changes which require institutions and governance to evolve not just within it, but across multiple areas such as land use and port regulation. The need for governance regimes for offshore renewable resources represents a wide-ranging trend that is likely to perpetuate going forward. In future, the scope of this work could be expanded to formalize our arguments and apply them to the design and empirical modeling of new governance regimes.

Supplemental Material

sj-docx-1-enj-10.1177_01956574241281565 – Supplemental material for The New Energy State: Offshore Governance Regimes for Renewables as Natural Resources

Supplemental material, sj-docx-1-enj-10.1177_01956574241281565 for The New Energy State: Offshore Governance Regimes for Renewables as Natural Resources by Anupama Sen and Tooraj Jamasb in The Energy Journal

Footnotes

Acknowledgements

We would like to thank three anonymous referees for their comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Tooraj Jamasb acknowledges financial support from the Copenhagen School of Energy Infrastructure (CSEI). The CSEI is funded jointly by Copenhagen Business School and energy sector partners.

Supplemental Material

Supplemental material for this article is available online.

1

Also see “Queen’s property manager and Treasury to get windfarm windfall of nearly £9bn” The Guardian, 8 February.

2

For instance, in Germany in 2017 and 2018, the Netherlands in 2017 and 2019, the UK Contract-for-Difference (CfD) auctions in 2020 (Jansen et al. 2020), and offshore wind tenders in Denmark in 2021 (![]() ).

).

3

Also see “Denmark approves artificial island to site 10GW Offshore Wind hub” Energy Post EU, 10 March.

4

Also see “This is what the world’s first energy island might look like”, State of Green, 26 January 2021.

5

This feature of renewable energy resources is evident, for instance, in solar energy development, where the most favourable sites are utilized first.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.