Abstract

Political investorism involves the use of financial investments to promote political aims, but has, with some recent exceptions, received scarce attention from political scientists although there are valid theoretical reasons to consider this a new form of political participation. Here, we add new knowledge to this research agenda by examining empirically whether political investorism constitutes a distinct mode of political participation. Furthermore, we explore the characteristics of political investors and why they use political investorism. We examine these issues using an original survey from Finland (n = 1065). Our results demonstrate that political investorism constitutes a distinct mode of participation that in particular appeals to young and well-educated women living in an urban setting. Finally, cultural ideological divisions (measured with GAL-TAN: Green-Alternative-Libertarian and Traditional-Authoritarian-Nationalist) mediate socio-demographic characteristics when explaining participation.

Introduction

Ethical investments have become a way for people to reconcile moral values with a wish for economic prosperity. By guiding investments to companies and portfolios that, for example, promise to respect labour rights or environmental standards, people hope to make profitable investments without causing detrimental effects to others.

These ethical investments have received attention from economists and philosophers (Hill et al., 2007; Kempf and Osthoff, 2007; Kolers, 2001; Schueth, 2003). However, political scientists have generally paid scant attention to this phenomenon, with notable recent exceptions (O’Brien et al., 2022, 2023). Consequently, despite this recent work conceptualizing political investorism as a form of political participation, our knowledge on how these activities fit into the toolbox of political activists is still scant. This may come as a surprise considering that several studies have debated the proper conceptualization and measurement of how citizens express their political preferences and demands (De Moor, 2017; Stolle et al., 2005; Theocharis and Van Deth, 2017, 2018; Vissers and Stolle, 2014). This inattention is at least partly because political investorism has often been subsumed under the broader label of political consumerism, which concerns the use of the market mechanism for political purposes; for example, through buying certain ethically produced products (Copeland and Boulianne, 2022; Micheletti, 2003; Stolle and Micheletti, 2013; Stolle et al., 2005). However, even if both political consumerism and political investorism make use of the market mechanism to promote political ideas, it may be misguided to assume that they are overlapping dimensions of political participation.

Here, we build on the work of O’Brien et al. (2022, 2023) and examine empirically the extent to which political investorism ought to be considered a separate mode of participation with a distinct placement in the toolbox of political activists. Furthermore, we explore who uses political investorism and probe the explanations for why they do so. We examine our research questions with a novel survey sent to a sample of Finnish citizens in autumn 2022 (n = 1065).

Our results suggest that although political investorism is still not widespread in the Finnish population, it constitutes a distinct mode of participation with a clear potential as a new avenue for expressing political demands. Furthermore, this mode of participation appeals to a specific group of citizens, meaning political investorism will most likely be used to promote specific political demands.

Political investorism as a mode of political participation

Recent decades have witnessed increased market liberalization and free movement of capital across the globe. Among other things, this has led to increased opportunities for individuals to engage in small-scale investments. This prospect gained further impetus from increased possibilities for making independent trading decisions through online banks and other digital services that decreased the need for intermediaries.

Although this development had direct consequences for the financial well-being of many (for better or for worse), it may also indirectly affect how financial markets relate to democracy. For example, technological advancements such as the Robinhood app allow individuals to buy and sell stocks directly from their smartphones, and it is currently debated whether this should be considered a sign of democratization and increased financial inclusion, or whether the increased accessibility mainly promotes risk-taking among inexperienced investors (Tan, 2021).

Another potential consequence concerns the motives driving investment strategies. The idea of ethical or socially responsible investments reminds us that some investors do not only value economic rewards when making decisions on how to place investments (Kempf and Osthoff, 2007; Kolers, 2001; Schueth, 2003). O’Rourke (2003: 684) defines socially responsible investing as ‘an investment process that considers the social and environmental consequences of investments, both positive and negative, within the context of rigorous financial analysis’. This definition calls attention to the fact that investors do not always only consider financial rewards but may also wish to minimize possible negative externalities for society, when deciding on their investment portfolio. Later studies support the idea of value-driven investors. Some studies show that investments in socially responsible funds are less sensitive to economic performance (Benson and Humphrey, 2008; Renneboog et al., 2011). Another study demonstrates that owners of socially responsible funds often have lower returns and pay higher management fees compared to conventional investors (Riedl and Smeets, 2017), a finding which is corroborated by Gutsche and Ziegler (2019), who find that socially responsible investors are willing to pay more for their sustainable investments (Gutsche and Ziegler, 2019). All these studies demonstrate that investors do not only care about economic gains but sometimes also value the consequences for society.

Interest in examining ethical investments has predominantly existed within economics and business studies, whereas political scientists have paid scant attention to the phenomenon. Consequently, many studies have explored the implications for corporations and people involved in the trading business (Hill et al., 2007; Kempf and Osthoff, 2007), but the extent to which individual citizens use investments to influence political decision-making remains unclear. We therefore focus here on the extent to which ordinary citizens consider political goals when deciding how to invest their financial assets. The phenomenon, which we refer to here as political investorism, may be gaining importance as a way for citizens to voice their political preferences. O’Brien et al. (2022) define political investorism as ‘the individual or collective use of a financial stake to express political values’ (2). This definition highlights that individuals can derive political power from their capacity as shareholders, pension fund members, bond holders and even users of financial services such as loans and insurances.

Political scientists may have been wary of political investorism since ethical investment schemes have been considered a marketing ploy by financial actors eager to sell new financial products rather than an instrument for influencing political decision-making. However, even if we concede that ethical or socially responsible investments do not necessarily promote sustainable practices, this does not inevitably entail a need to question the sincerity of the motives of the individual investors making investment decisions based on other than economic incentives. Political investorism in this sense shares commonalities with other recent additions to the toolbox of political activists, where scholars have also questioned whether they entail a genuine desire to influence political matters (Stoker, 2006).

Political investorism may constitute yet another new form of political participation. The concept of political participation was initially a relatively straightforward concept clearly confined to formal political activities in conjunction with the formal political sphere, most clearly embodied by voting in elections (Verba and Nie, 1972). However, since then the modes of political participation considered in academic research on the topic have gradually expanded to include activities such as protest (Barnes and Kaase, 1979), political consumerism (Copeland and Boulianne, 2022; Micheletti, 2003; Micheletti et al., 2006; Stolle et al., 2005), online political participation (Theocharis et al., 2021; Vissers and Stolle, 2014) and lifestyle politics (De Moor, 2017). Today, the toolbox of political activists may at times seem to be bursting. Despite this abundance, comparative research on political participation frequently utilizes a dichotomous distinction between institutionalized and non-institutionalized political participation; that is, whether people participate in top-down activities aimed at the formal political actors and institutions, or in bottom-up activities that are not necessarily aimed at formal political actors (Bäck and Christensen, 2016; Marien et al., 2010). Nevertheless, the literature on political participation generally considers more and more activities as forms of political participation.

Political investorism was not usually included in this expansion of political participation until the recent exception of O’Brien et al. (2022, 2023). To the extent that these activities were given any consideration, they were considered a form of political consumerism or lifestyle politics (Stolle and Micheletti, 2013: 98). This makes sense since political consumerism also involves political activists taking advantage of the market to further political aspirations (Micheletti, 2003; Micheletti et al., 2006; Stolle and Micheletti, 2013; Stolle et al., 2005). Nevertheless, and while acknowledging that political consumers may be more likely to make sustainable investments (Brunen and Laubach, 2022), it is not necessarily the case that political investorism is simply a specific type of political consumerism.

The recent work by O’Brien et al. (2022, 2023) makes this point particularly clear. Although the authors concede that political investorism shares commonalities with political consumerism, they note that there are at least three important differences between consumers and investors. First, consumption is usually at the end of the production process, whereas investments are made throughout and therefore can prevent harmful practices before they occur. Second, consumers seek to meet individual needs and wants, whereas investors seek profit on behalf of themselves or others. Finally, they have different positions in the societal machinery since investors act as owners rather than consumers.

According to O’Brien et al. (2022), this entails that it is a mistake to subsume political investorism as a form of political consumerism. It is also worth highlighting that political consumerism has been accused of being a low-quality form of participation, where people express their opinions in a shallow manner without interacting with the formal political system, and therefore rarely succeed in achieving their stated political goals (Stoker, 2006: 99). Contrary to this, financial decisions potentially have major repercussions for the actors involved in making them. This may be self-evident for major corporate investments, but also holds true for small-scale private investors. Although the amounts may be smaller, private financial decisions involve investing life savings to ensure financial viability for the whole family. Hence, although the direct impact on society may be minor, it is not a trivial matter for any individual to decide what role ethical or environmental concerns should have when making these decisions.

There are therefore valid reasons to take political investorism seriously as an independent mode of political participation. O’Brien et al. (2022, 2023) make an important contribution by offering a solid conceptual framework for conceiving political investorism as a form of political participation. What is still lacking is solid empirical work on how widespread this phenomenon is in the general population, whether it constitutes an independent mode of participation, and who the political investors are. The profile of the political investors is a salient question for understanding the motivations behind using financial decisions for political purposes.

We contribute to this empirical research agenda by examining the following research questions in Finland:

How many people engage in political investorism?

Does political investorism constitute a distinct mode of political participation, or do the financial decisions coalesce with other political activities?

Who engages in political investorism?

Why do people use political investorism?

Although we conceive our work as closely connected to O’Brien et al. (2022, 2023), there are some differences in how we operationalize the concept. Most importantly, we do not rely on the same activities when we operationalize the concept as they do in their study of Australia. This is mainly because we believe that other types of financial decisions are more appropriate to measure the concept in a Finnish context, since people have other ways to express their political preferences when making financial decisions. We nevertheless adopt the label of political investorism to refer to our main dependent variables. Future studies need to examine how best to measure the concept of political investorism in comparative research, and the extent to which this is contingent on contextual differences across countries. It should also be noted that we perceive this study as exploratory, and therefore we do not form explicit hypotheses, even if we do discuss different possible expectations in connection to each of the research questions.

In the following, we present the research design for examining our research questions.

Research design

We situate our study in Finland, which is an established democracy with a multiparty system and a stable market economy. Finland is a consensual democracy and governments are traditionally formed through coalitions between several parties, frequently traversing ideological divides. Like the other Nordic countries, Finland has high standards of living and relatively generous welfare state entitlements (Karvonen, 2014). At the same time, individual investments are common in Finland, meaning it is more likely that people perform acts of political investorism. According to the European Central Bank (ECB) Household Finance and Consumption Survey (ECB, 2020), Finland is among the countries where most people own financial assets. For example, 21% of all households indicate owning publicly traded shares compared to a European Union (EU) average of 8.6%, and 31.4% have mutual funds compared to an EU average of 10.2%. Accordingly, relatively large shares of the population have the financial assets needed to actively make investment decisions, which also enables them to use these decisions as a political tool.

Our data come from a survey fielded to an online panel of Finnish adults. The panel kanselaismielipiede forms part of the national Finnish Research Infrastructure for Public Opinion (FIRIPO) (https://www.firipo.fi/). It contains adults residing in Finland who volunteered to fill in surveys on a regular basis. The respondents have been recruited from random samples and mail invitations in combination with advertisements on social media, but the panel composition is not representative of the Finnish population.

The survey was administered through Qualtrics from 14–30 November 2022 to a total of 1997 people. After the survey ended, 1153 people (57.7%) had filled in the survey. Some of these had to be deleted due to incomplete responses, and a further 11 respondents filled in the survey in less than 100 seconds and were deleted to ensure data quality. This entails that a total of 1065 respondents (53.9%) are included in the study, although some analyses include fewer respondents due to missing values. Since the final sample did not fully reflect the Finnish population, we constructed raking weights based on known information on age, gender, education and language in the Finnish population (Bergmann, 2011). As can be seen in Appendix 1, weighting the data with these helps ensure that the sample largely represent the general population. Consequently, we use weighting in all descriptive and regression analyses to ensure that results reflect the general population. Nevertheless, these discrepancies entail that we cannot be certain that the results are representative of the Finnish population. However, we can still gain important insights into the use of political investorism as a form of political participation, even if the results should be considered as the starting point of this research agenda rather than yielding definitive answers.

The survey contained questions on attitudes towards political investorism, political participation and various political attitudes, while some socio-demographic background questions had been filled in in previous rounds of the panel (year born, gender, education). In the following, we describe the coding of key variables while the full phrasings of all questions are included in Appendix 1.

Dependent variables

To measure the extent of political participation, we included a battery asking respondents to indicate what activities they had performed (‘Below we mention different types of engagement in society. Please indicate which ones you have done during the last 12 months, and which ones you could do if a cause were very important to you’). For each alternative, respondents could pick 3 alternative answers ‘Has done in last 12 months’, ‘Has not done but could do’ or ‘Would never do’.

Some of the activities included were used in previous research on political participation, including traditional activities such as contacting officials and being active in political parties (Verba and Nie, 1972; Verba et al., 1995), protest activities such as demonstrations and civil disobedience (Barnes and Kaase, 1979), political consumerism in the form of buycotting and boycotting products (Stolle and Micheletti, 2013; Stolle et al., 2005; Yates, 2011), and various online activities (Theocharis et al., 2021; Vissers and Stolle, 2014). This selection covers a broad selection of institutionalized and non-institutionalized political activities that have formed part of several previous studies. Moreover, most activities have been used in the Finnish National Election Survey in various years, and therefore have particular relevance in a Finnish context (Bäck and Christensen, 2020).

In addition to these more customary political activities, we include three items that are specifically designed to probe the use of political investorism. The first of these was ‘Actively investing in specific funds or stocks to influence society despite a risk for lower profits’, which mimics the act of boycotting; that is, selecting what products to buy based on political concerns. The second mimicked boycotting in the stock market: ‘Actively not investing in specific funds or stocks to influence society despite a risk for lower profits’. Finally, we included an item on housing since for many this is the largest financial decision they make during their lifespan: ‘Adapt my selection of housing to minimize environmental impact’. Although these items do not directly reflect the discussion of O’Brien et al. (2022), they constitute types of financial decisions in Finland where political or societal concerns may matter when deciding how to invest.

Independent variables

We also explore the associations between political investorism and individual characteristics. The aim here is not to provide a comprehensive account of who the political investors are, but to construct a profile of the political investors that we can compare to similar efforts from previous research on political participation. To this end, we rely on two sets of variables: socio-demographic characteristics and political attitudes. Although these are not the only relevant characteristics, they have been used widely in previous research on political participation in Finland and elsewhere (Bäck and Christensen, 2016; Marien et al., 2010; Verba et al., 1995), and are therefore important indicators for discerning the profile of the political investors.

We include the following socio-demographic characteristics that have been shown to be important for political participation (Marien et al., 2010; Verba et al., 1995): age in years (calculated from year born), gender (male/female), education (recoded to primary, secondary or tertiary education), household income per month (6 categories from 0–2000 to more than 10,000), marital status (whether in steady relationship/married/cohabiting or single, including widowed or divorced) and degree of urbanicity (five categories from most rural to most urban). These all indicate important characteristics of the political investors that simultaneously indicate their social status (Verba et al., 1995).

For political attitudes, we include political trust (sum index based on level of trust in government, parliament and politicians, coded 0–10) and satisfaction with democracy (scale 0–10) as two measures of political dissatisfaction with the political system, which is frequently considered important for political participation (Barnes and Kaase, 1979; Braun and Hutter, 2016; Marien et al., 2010). Previous studies suggest that leftist/progressive individuals are more likely to let their political values guide how they place their financial assets (Gutsche and Ziegler, 2019; Hong and Kostovetsky, 2012; Hood et al., 2014). We therefore include a measure of left/right ideology (scale 0–10, 0 = furthest to the left, 10 = furthest to the right) and GAL-TAN: Green-Alternative-Libertarian and Traditional-Authoritarian-Nationalist (index based on factor scores adapted from Ilmarinen et al. (2022), varies between −1.48 and 2.32) to probe the importance of both traditional socio-economic ideological cleavages and more recent cultural ideological differences. Finally, we include social trust (scale 0–4) since this has been argued to be an important predictor for political participation that also indicates what type of people that use political investorism (Bäck and Christensen, 2016; Kaase, 1999).

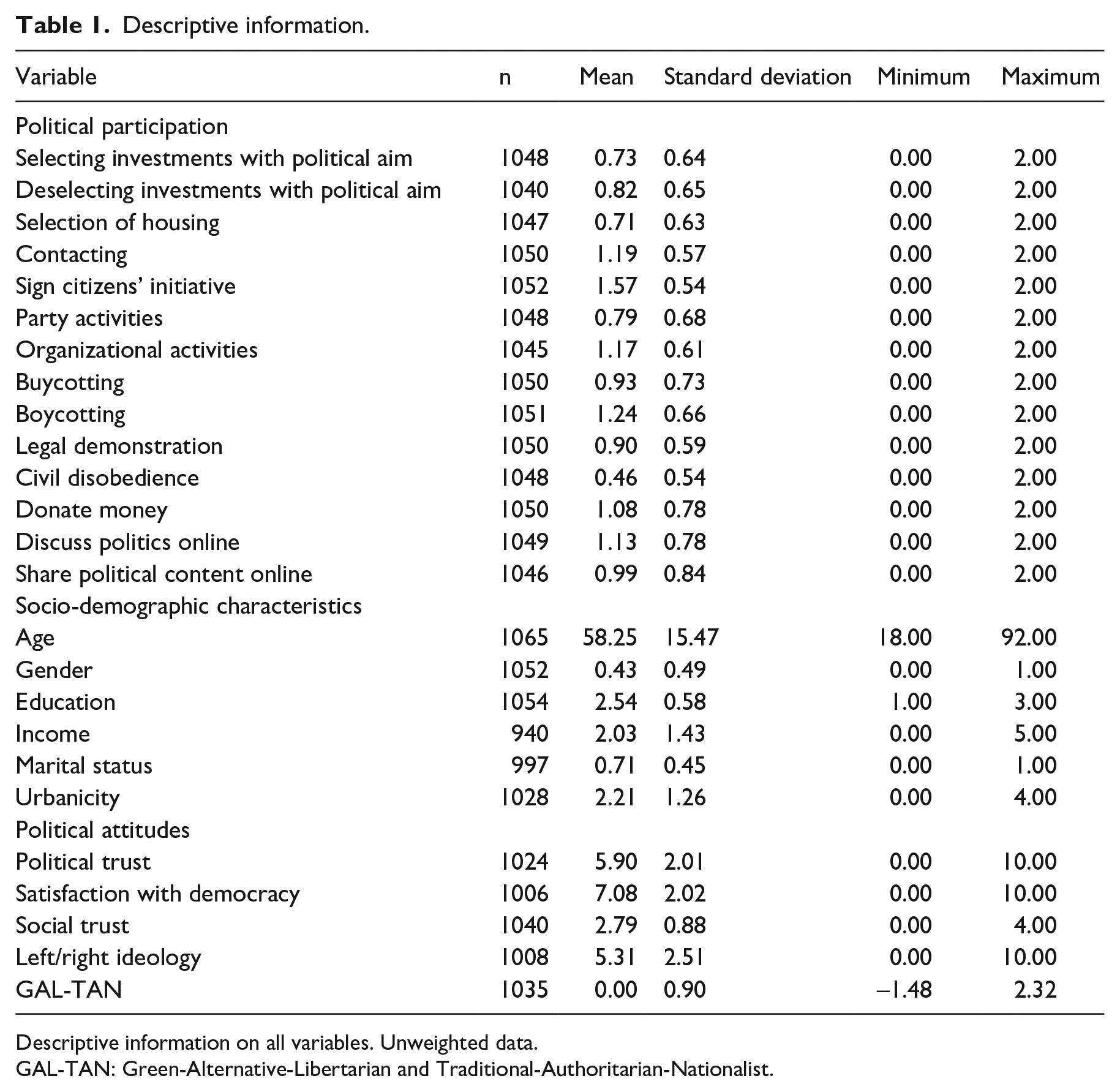

In Table 1, we present descriptive information on all variables included in the analyses.

Descriptive information.

Descriptive information on all variables. Unweighted data.

GAL-TAN: Green-Alternative-Libertarian and Traditional-Authoritarian-Nationalist.

We describe the methods that we use in the text when relevant.

Empirical results

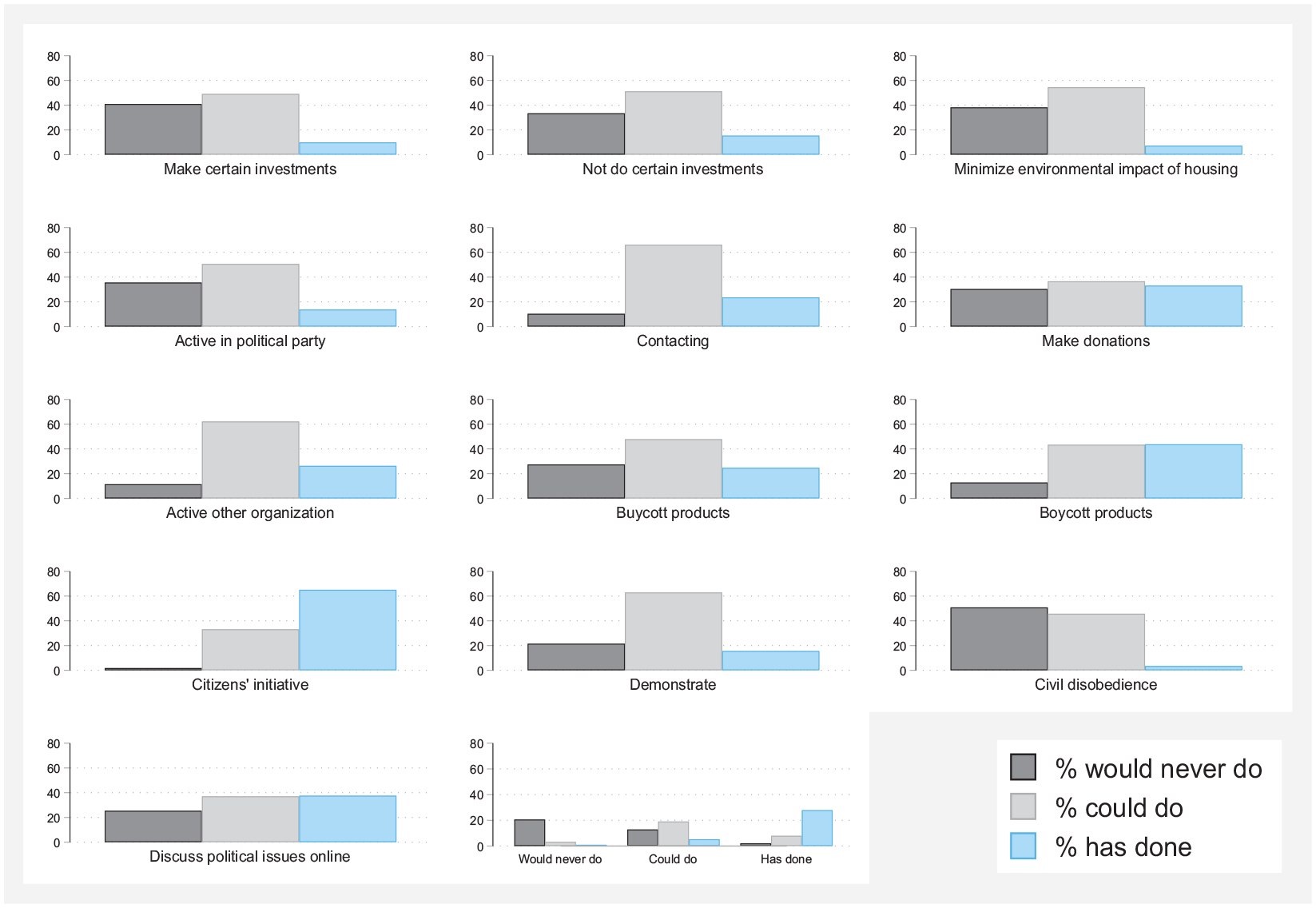

Our first research question concerns the popularity of using political investorism in comparison with other activities. In Figure 1, we show for each political activity what percentages of the respondents have performed the activity, could perform it or would never perform it.

Percentage answers to various political activities (weighted data).

The most popular political activity is signing citizens’ initiatives, which about 65% have done, and boycotting products, which about 44% of the respondents have done. This is in line with previous research showing the popularity of this activity in the Finnish context (Bäck and Christensen, 2020).

Other popular activities include discussing political matters online, which 37.6% indicate having done. The activity that the fewest have performed is civil disobedience, which only 3.5% say they have done, although 45.7% say they could do it if needed, so the protest potential nonetheless exists among respondents (Barnes and Kaase, 1979). A general pattern is that the less demanding activities are more popular to use, but many nevertheless indicate willingness to perform more demanding activities should the need arise.

For political investorism, there are also relatively few respondents who have performed these activities: 10% indicate having made investments and 15.4% have refrained from making some investments, while only about 7% have made housing decisions with the environment in mind. This result may be considered as support for the argument in the theoretical section that political investorism is more demanding than popular activities such as political consumerism. Although relatively few respondents use financial decisions to influence political matters, about half of the respondents indicate being willing to use them if necessary (49% for making investments, 51% for not making investments and 55% for housing decisions). This indicates that while the current usage may be limited, these activities may become a force to be reckoned with.

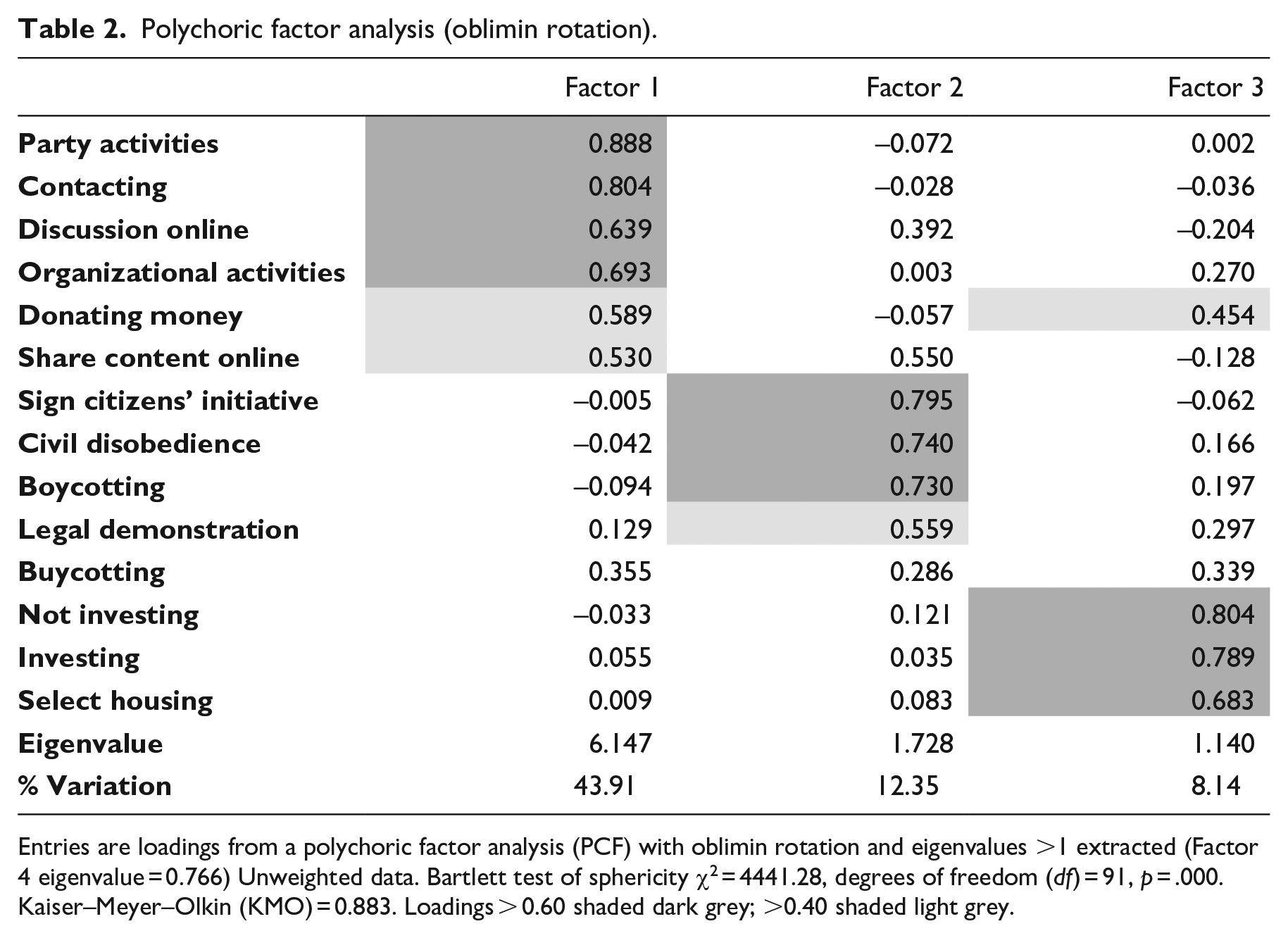

The second research question concerns whether political investorism constitutes a distinct mode of participation, or the financial decisions instead coalesce with other activities such as boycotting and buycotting. To examine this, we examine the dimensionality with exploratory factor analysis (EFA) which allows us to identify underlying dimensions of activities that participants tend to combine. Since the items on political participation are ordinal, we use polychoric factor analysis. Furthermore, we use oblimin rotation that does not assume that dimensions are orthogonal since the participatory dimensions may be expected to be correlated. The results are shown in Table 2.

Polychoric factor analysis (oblimin rotation).

Entries are loadings from a polychoric factor analysis (PCF) with oblimin rotation and eigenvalues >1 extracted (Factor 4 eigenvalue = 0.766) Unweighted data. Bartlett test of sphericity χ2 = 4441.28, degrees of freedom (df) = 91, p = .000. Kaiser–Meyer–Olkin (KMO) = 0.883. Loadings > 0.60 shaded dark grey; >0.40 shaded light grey.

The analysis leads to the identification of three distinct dimensions of political participation by using the Kaiser criterion of extracting dimensions with eigenvalues greater than 1. Since this approach has been argued to entail the extraction of too many dimensions (Koc, 2021), we confirmed the three-dimensional structure with a parallel analysis, which suggested a similar conclusion.

Hence, the political activities can be summarized by three distinct dimensions of political participation. The two first dimensions with some caveats correspond to the traditional institutionalized/non-institutionalized distinction common in research on political participation (Bäck and Christensen, 2016; Marien et al., 2010). The third dimension is of direct interest for the current purposes. Here we find relatively strong loadings (>.60) from the three observed items concerning political investorism, which entails that respondents are likely to combine these activities. We also see a weak loading (>.40) from donating money, but this item loads slightly stronger onto the first dimension. Overall, we interpret these results as evidence supporting the notion that political investorism forms a coherent and separate mode of participation.

To confirm this interpretation, we tested a single-factor model with four observed indicators using confirmatory factor analysis (CFA): donating money, ethical housing, financial boycotting and ethical investing. The results indicated an acceptable fit (Comparative Fit Index (CFI) = .989, Root Mean Square Error of Approximation (RMSEA) = .062, Tucker-Lewis Index (TLI) = .968), with standardized factor loadings in the range .45–.75 (see Appendix 1). 1 We take this as further evidence that political investorism constitutes an independent mode of participation rather than a subcategory of political consumerism.

In the following, we use the predicted index score from the EFA as our dependent variable (mean = .00, standard deviation (SD) = .95, minimum = −2.35, maximum = 2.72) when examining relationships with individual characteristics. 2

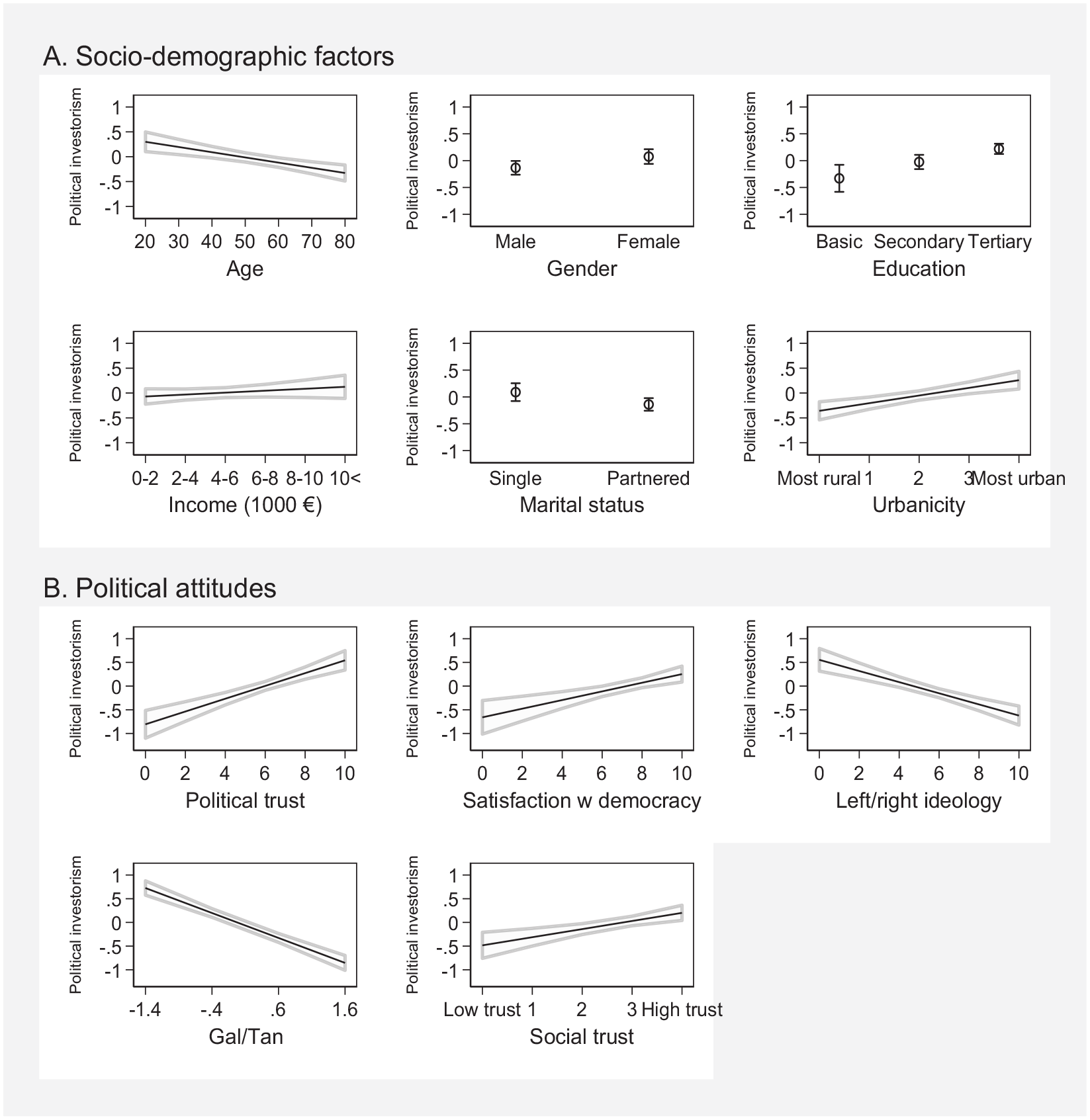

Our third research question involves examining who is more likely to make use of political investorism. We here explore how predicted scores on the political investorism index differ across socio-demographic characteristics and political attitudes. Although these associations are purely descriptive, they help establish the profile of the political investors. We show the results in Figure 2.

Bivariate relationships (weighted data).

These bivariate relationships show that those who use investments as political participation tend to be younger, female, highly educated, high-income, single and live in an urban setting. It is noteworthy that the differences for the socio-demographic characteristics are relatively small. For example, people with the lowest income have an average score of about −.07 compared to .12 for those with the highest income. Hence, while income matters, it is hardly the only salient characteristic of the political investors.

We see more pronounced differences in political attitudes, indicating that political investors are characterized more by their beliefs. Somewhat surprisingly, higher levels of trust and satisfaction are associated with more use of political investorism, which implies that the political investors tend to be satisfied with the workings of the traditional democratic system and the key actors. Hence, using political investorism should not be considered a sign of alienation from more traditional politics. Left-wing people and those leaning toward the Green-Alternative-Libertarian pole of the GAL-TAN scale are also more likely to use political investorism.

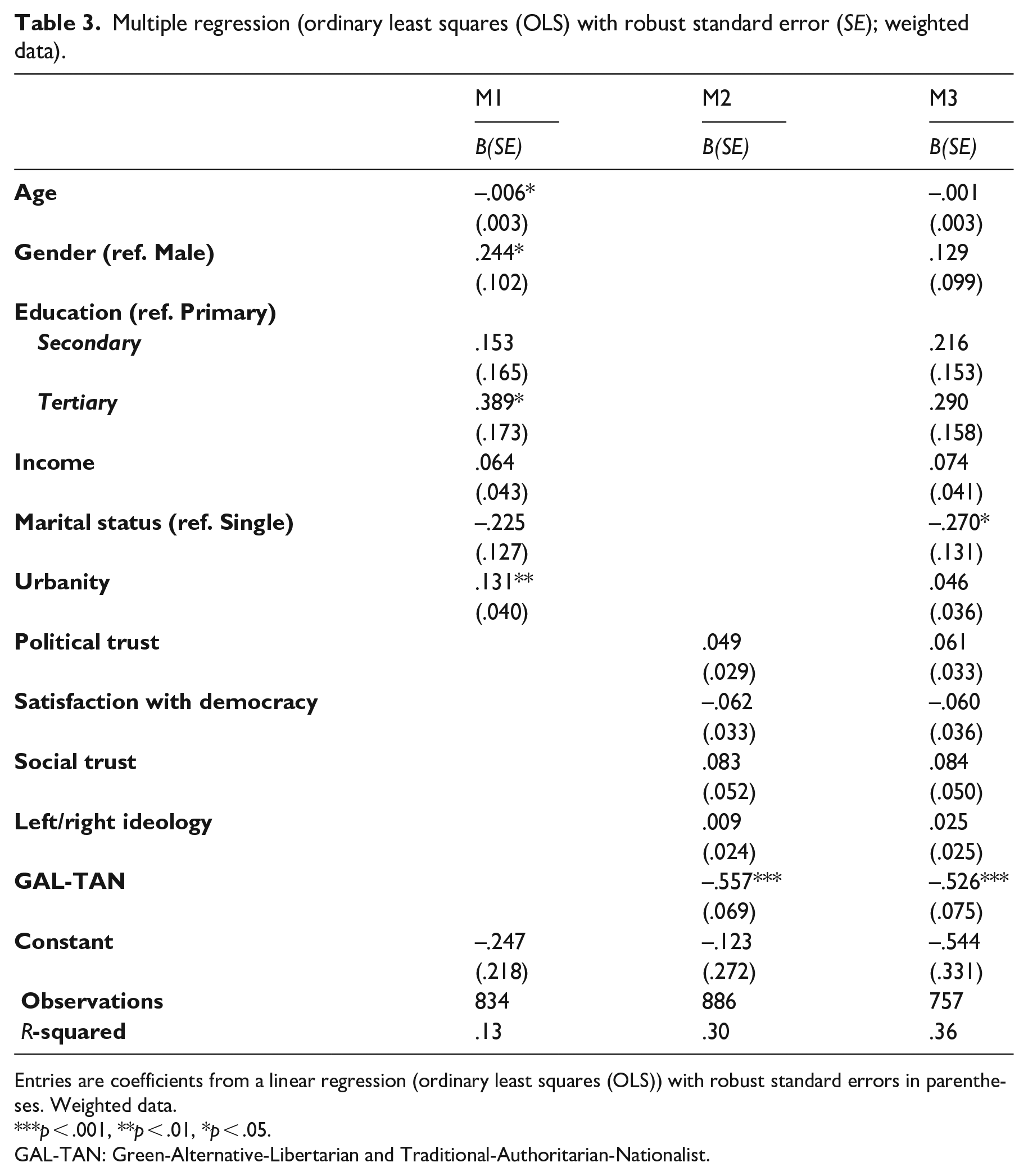

Although this profile shows us what characterizes the political investors, it does not allow us to draw firm conclusions about the explanatory value of these characteristics. Our fourth and final research question concerns what can help explain why someone uses political investorism. Here we first use multiple linear regression analysis to help sort out what individual characteristics can predict participation when considering other factors. We report three models in Table 3. In the first model, we include all socio-demographic variables, in the second we include all political value variables, and in the third and final model we include both sets of variables simultaneously.

Multiple regression (ordinary least squares (OLS) with robust standard error (SE); weighted data).

Entries are coefficients from a linear regression (ordinary least squares (OLS)) with robust standard errors in parentheses. Weighted data.

p < .001, **p < .01, *p < .05.

GAL-TAN: Green-Alternative-Libertarian and Traditional-Authoritarian-Nationalist.

The only characteristic that maintains a consistent significant relationship with political investorism is the GAL-TAN scale. Consequently, even when considering all other aspects, those who lean toward being green/alternative/libertarian are more likely to use political investorism as a form of political participation.

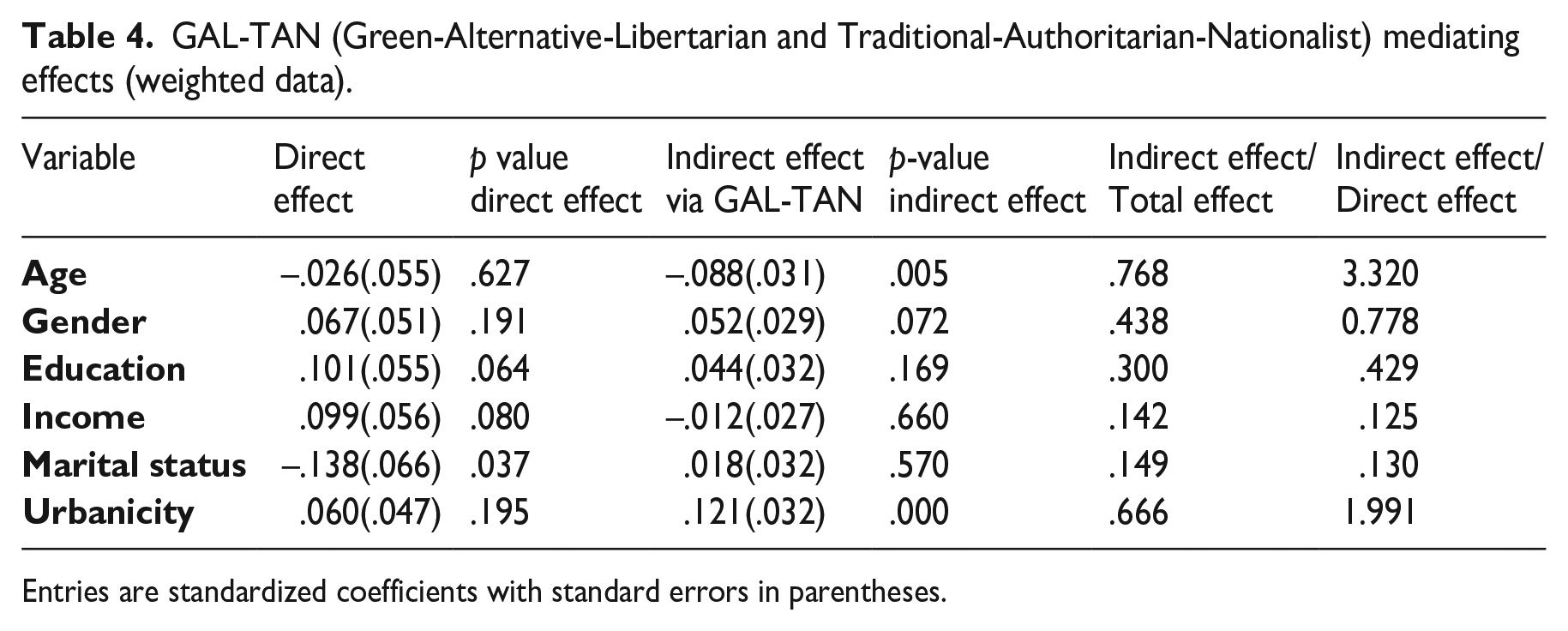

This does not entail that other characteristics are irrelevant for explaining the use of political investorism. A more sensible interpretation considers potential mediating effects (Baron and Kenny, 1986; Zhao et al., 2010). This entails that the differences for socio-demographic that we observe in the first model for characteristics such as age, gender and education could be mediated through the GAL-TAN dimension. There may even be more complex causal interplays between all potential explanatory factors, but to disentangle these is beyond our current aspirations. Here, we examine the extent to which socio-demographic factors are mediated through individual positions on a new ideological cleavage here measured with GAL-TAN. To do this, we rely on the medsem package for Stata (Mehmetoglu, 2018). We report the results from the approach developed by Zhao et al. (2010), who rely on a one-step bootstrapping approach to replace the traditional mediation analysis framework developed by Baron and Kenny (1986). This entails first implementing the model in Structural Equation Modelling (SEM) to identify both direct and indirect paths. 3 Based on this, it is possible to establish whether there is complete mediation (all of the effect is mediated), partial mediation (some of the effect is mediated) or no mediation exists. We report the results in Table 4.

GAL-TAN (Green-Alternative-Libertarian and Traditional-Authoritarian-Nationalist) mediating effects (weighted data).

Entries are standardized coefficients with standard errors in parentheses.

The effects of both age and urbanicity are completely mediated by GAL-TAN. This is in line with the observation that people with more liberal cultural attitudes tend to be younger and live in urban areas (Inglehart, 1997). For the other socio-demographic variables, we do not observe any kind of mediation through GAL-TAN.

Hence, there is a complex interplay between our explanatory factors in determining who uses political investorism, but new ideological cleavages here measured with GAL-TAN play a pivotal role by mediating effects from socio-demographic factors.

Discussion and conclusions

We explored the use of political investorism as a political tool in this article and our results showed that although political investorism is still not among the most popular political activities, usage is on a par with other, more demanding political activities, which form an established part of the participation repertoire. More importantly, our results show that political investorism constitutes a separate mode of political participation that should not be clustered with activities such as political consumerism. The political investors tend to be young and well-educated women living in an urban setting. The attitudinal profile also showed that they are to the left on the traditional left–right ideological dimension and have green, alternative, libertarian values on the cultural dimension. A more surprising finding for the attitudinal profile was that the political investors are satisfied with democracy and have higher levels of political trust. Finally, we showed that cultural cleavages, here measured with GAL-TAN, play a key role in determining who participates in political investorism. It was the only consistent predictor in regression analyses, and mediation analyses showed that cultural cleavages mediate effects from key socio-demographics age and urbanicity.

These results indicate that political investorism should not be understood as an expressive form of participation that does not necessarily aim to influence political decisions, as has been suggested by some (Stoker, 2006). While political investorism may share commonalities with individualized forms of political participation and lifestyle politics (De Moor, 2017; Micheletti, 2003), it is important to note the important differences that exist. These differences were also apparent when we examined whether political investorism constitute a separate mode of participation, a question which has traditionally been central within research on political participation (Barnes and Kaase, 1979; Koc, 2021; Marien et al., 2010; Theocharis et al., 2021; Verba and Nie, 1972; Vissers and Stolle, 2014). Rather than coalesce with relatively ‘easy’ activities such political consumerism or signing initiatives, political investorism emerged as a separate mode of participation. Hence, there is nothing to suggest that political investorism is a type of political consumerism or lifestyle politics, as has sometimes, at least implicitly, been presumed (Stolle and Micheletti, 2013). Instead, we find that political investorism is emerging as a new independent avenue for citizens to express their political preferences.

A second noticeable finding concerns the profile of the political investors since our results show that they have a distinct socio-demographic and attitudinal profile. That the political investors tend to be younger, well-educated and urban women may not come as a great surprise. This shows that the political investors share affinities with Inglehart’s (1997) postmaterialists, who embrace new, more egalitarian values. That income is of little relevance is more surprising and shows that political investorism is not only for the rich but is potentially open for all regardless of income. Another unexpected finding was that the political investors are relatively satisfied with the current political system, which shows that political investorism should not be considered a sign of growing dissatisfaction with the existing political system (Stoker, 2006). Instead, it may be a sign that political opinions spill over into other spheres of life, as is the case with the responsibility-taking ethos that permeates lifestyle politics (De Moor, 2017; Theocharis et al., 2021).

Third, our results concerning the causal mechanisms underpinning the choice to use political investorism are worth highlighting, even if they should be taken with some caution due to the exploratory nature of our analyses. Nevertheless, the pivotal role of cultural cleavages, measured with GAL-TAN, in influencing political investing is an interesting finding that provides further evidence that cultural cleavages are becoming increasingly important for understanding political behaviour (Ilmarinen et al., 2022; Inglehart, 1997).

These results should not be taken as definitive since several issues still need to be resolved. It is necessary to develop adequate measures of political investorism that function in comparative research. It is without a doubt possible that our battery missed important activities that these people perform, as is also indicated by the work of O’Brien et al. (2022, 2023). A particular challenge in connection to this is that it is necessary to be aware of the subtle differences that exist across countries in how individuals can use their financial assets for political purposes. Creating a battery of questions that can be used in a comparative perspective is an important task for future research on political investorism to be able to examine causes and consequences in a comparative perspective.

To establish the range of relevant activities will also help establish how widespread these activities are in contemporary societies. When it comes to understanding who performs these activities and why, it is worth underlining that there may be other potential explanatory factors that we did not include here. Furthermore, our results indicate that there is a complex interplay between the explanatory factors that it was impossible to fully disentangle here. Furthermore, the interplay between these explanatory factors may hinge on the context, meaning that our results from Finland do not necessary travel outside this specific context.

Despite these uncertainties, these results demonstrate that political investorism ought to be taken serious as a new mode of political participation.

Footnotes

Appendix 1

Acknowledgements

The authors would like to thank Rasmus Sirén and Janette Huttunen for assistance with the preparation of the survey and collection of data.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Anton Brännlund received funding from Vetenskapsrådet (Grant no. 2021-06666).