Abstract

We study nascent project-based enterprises (PBEs) through the lens of upper echelons and institutional theory. We analyse the interplay between the different role-congruent reputations of their project entrepreneurs and the institutional endorsement of their project idea, theorizing how these affect PBEs’ ability to attract private investments. In the context of the Italian film industry, we find that the commercial reputation of the project entrepreneur in the producer role is crucial for attracting investors, while the artistic reputation of the project entrepreneur in the creative director role is crucial for attaining institutional endorsement of the project idea. Finally, we find that the effect of the commercial reputation of the project entrepreneur in the producer role on attracting investments is mediated by the institutional endorsement. We contribute to the literature on PBEs by demonstrating how specific combinations of project entrepreneurs’ roles and (role-congruent) reputations can directly and indirectly attract investments.

Keywords

Introduction

A project-based enterprise (PBE) is a particular form of temporary organization that dissolves as soon as the project, for which the organization was specifically set up, is completed (DeFillippi & Arthur, 1998; Ferriani, Cattani, & Baden-Fuller, 2009; Jones, 1996). When PBEs are nascent, they are in a phase in which they need financial resources before they can start their operations, yet they lack a performance-based reputation at the organizational level, which is an important organizational signal of past demonstrations of quality (Shapiro, 1983) to persuade investors (Ebbers & Wijnberg, 2012a; Radoynovska & King, 2019). However, two prominent theories help to explain which signals could attract investments in nascent PBEs: upper echelons theory and institutional theory.

On the one hand, upper echelons theory scholars suggest that, since nascent PBEs lack an organizational reputation, individual-level quality signals associated with nascent PBEs’ key project entrepreneurs – i.e. their top management (founding) team – are of crucial importance for attracting investors (Foo, Sin, & Yiong, 2006; Hermano & Martín-Cruz, 2016; Higgins & Gulati, 2006; Ko & McKelvie, 2018; Manning, 2017; Talke, Salomo, & Kock, 2011). On the other hand, institutional theory scholars observe that, even though nascent PBEs lack an organizational reputation, they are built around a project idea (Hobday, 2000) that, being restricted by social structures at an institutional level, must comply with the standards of its institutional field in order to signal socio-political legitimacy to investors (Brush, Greene, & Hart, 2001; Foo, Wong & Ong, 2005; Jones, Livne-Tarandach, & Balachandra, 2010; Smith & Martí, 2017). While upper echelons theory, with its focus on top executives, is criticized for ignoring the structural constraints highlighted by institutional theory (Hambrick, 2007; Neely, Lovelace, Cowen, & Hiller, 2020), similarly, scholars of temporary organizations call for more fine-grained research at the intersection of agency and structure, affirming that key project entrepreneurs, and their PBEs, are dependent on the (institutional) structure of the field in which they are active (Bakker, DeFillippi, Schwab, & Sydow, 2016; Sydow, Lindkvist, & DeFillippi, 2004). This highlights the need to better understand how investors can conjointly evaluate signals related to project entrepreneurs as well as those emitted by regulatory institutions.

Since nascent PBEs are temporary and often relatively small in size, it is easier to attribute the performance of past PBEs to specific project entrepreneurs. As a consequence, investors place a strong emphasis on the performance-based reputations of the key entrepreneurs associated with the nascent PBE. Yet, these individual reputations are multidimensional – rather than unidimensional – signals (Fombrun & Shanley, 1990) and project entrepreneurs have specific roles, which act as ‘bundle[s] of norms and expectations’ (Baker & Faulkner, 1991, p. 280). Thus, when making investment decisions, investors take into account the dimension of reputation that is congruent with the project entrepreneur’s specific role in the PBE (Ebbers & Wijnberg, 2012a). Moreover, since nascent PBEs lack legitimacy, investors consider the endorsement that PBEs’ project ideas receive from regulatory institutions (Bitektine, 2011; Deephouse, Bundy, Tost, & Suchman, 2017; Zimmerman & Zeitz, 2002) that can signal whether they are aligned with institutional standards (Cattani, Ferriani, Frederiksen, & Täube, 2011; Engwall, 2003).

In this paper, we study the coexistence of – and possible tension between – upper echelons theory and institutional theory by investigating whether the institutional endorsement of a project idea affects the extent to which role-congruent reputations of key project entrepreneurs attract private investments in nascent PBEs. We study this in the context of the creative industries. In particular, the empirical setting of our study is the Italian film industry, which is characterized by PBEs where two hierarchically equivalent key project entrepreneurs and dual leaders – the producer and the director – temporarily combine their skills for the duration of a film project (Ebbers & Wijnberg, 2017; Ferriani et al., 2009). While the producer is predominantly responsible for the business aspects of the film, the director is responsible for the artistic ‘look and feel’ (Delmestri, Montanari, & Usai, 2005). When investors decide to invest in films that are in their nascent phase, they evaluate the producer’s and the director’s respective commercial and artistic reputation (Ebbers & Wijnberg, 2012a). In addition, they evaluate the film’s socio-political legitimacy by taking into account the endorsement that a film project idea – i.e. the film script (Macdonald, 2004) – receives from regulatory institutions (Durand & Hadida, 2016; Durand & Jourdan, 2012; La Torre, 2014).

This paper makes three main contributions to the literature. First, studying the relationship between agency and structure (Bakker et al., 2016; Sydow et al., 2004) and using a mediation model, we provide new insights about how different levels – individual (entrepreneurs) and institutional (endorsement) – can explain private investments in nascent PBEs. On the one hand, we reinforce the view of upper echelons theory that key project entrepreneurs’ roles and reputations are important individual-level signals (Foo et al., 2006; Hermano & Martín-Cruz, 2016; Higgins & Gulati, 2006; Ko & McKelvie, 2018; Talke et al., 2011). On the other hand, we show that key project entrepreneurs’ individual signals can help the PBE’s project idea to obtain institutional endorsement that signals socio-political legitimacy to private investors (Brush et al., 2001; Foo et al., 2005; Jones et al., 2010; Smith & Martí, 2017). Second, building on prior research about entrepreneurs’ reputations (Delmestri et al., 2005), role combinations (Baker & Faulkner, 1991) and role-congruent reputations (Ebbers & Wijnberg, 2012b; Ertug, Yogev, Lee, & Hedström, 2016), we show that attracting investments and institutional endorsement does not only depend on project entrepreneurs’ reputations being role-congruent, but also on the emphasis that is placed on different role-congruent reputations by different stakeholders (Jung, Vissa, & Pich, 2017). Third, we contribute to research on PBEs in the specific context of creative industries. From an upper echelons theory perspective, private investors are expected to give project entrepreneurs with strong reputations an exceptional degree of managerial discretion because of the high ambiguity (Hambrick & Finkelstein, 1987) that characterizes the creative process (Lingo & O’Mahony, 2010). But from an institutional theory perspective, since products in the creative industries are characterized by a high degree of symbolic value (Throsby, 2008), endorsement by government institutions, especially when they consist of industry experts, can be particularly important to convince investors (Lampel, Lant, & Shamsie, 2000).

The paper is organized as follows. First, we present the theoretical background and the hypothesis development. Then, we present the method, describing the empirical setting, the data and the variables. Next, we discuss the results and robustness tests. We conclude with the contributions, implications, limitations and extensions of our study.

Theoretical Background

Reputations, roles and socio-political legitimacy in nascent PBEs

PBEs are common in an increasing number of industries, including construction, biotech (Eccles, 1981) and creative industries such as television (Windeler & Sydow, 2001), theatre (Goodman & Goodman, 1976), film (DeFillippi & Arthur, 1998; Jones, 1996) and architecture (Boutinot, Joly, Mangematin, & Ansari, 2017). In this paper, we focus on PBEs in the creative industries and adopt the definition of Ferriani et al. (2009, p. 1545) who – also studying the film industry – define PBEs as temporary organizations that ‘have limited lives devoted to producing a singular objective or goal, typically grow to their full-size almost immediately after founding, and get disbanded very rapidly when the project ends’.

In particular, we focus on PBEs that are in their nascent stage. In this stage, PBEs first need to compete for factors of production before they can start making the actual product(s) with which they can subsequently compete in the market for end-users or consumers (Ebbers & Wijnberg, 2012a; Radoynovska & King, 2019). Nascent PBEs in most cases consist of a small number of key founding project entrepreneurs (Baker & Faulkner, 1991) and are built around a project idea (Hobday, 2000; Whitley, 2006). In their efforts to attract investors, nascent PBEs lack a track record and, thus, they cannot rely on organizational-level characteristics, such as quality signals related to their recent past performance (Foo et al., 2006; Stjerne & Svejenova, 2016). However, two important theories, upper echelons and institutional theory, can shed light on the signals helping nascent PBEs to attract investments.

On the one hand, upper echelons theory suggests that nascent PBEs can signal quality based on the characteristics of their key project entrepreneurs, who constitute the nascent PBE’s founding and – once they enter the production stage – top management team (Hambrick, 2007; Talke et al., 2011). Two particularly important characteristics that can help to distinguish nascent PBEs from competitors are the performance-based reputation and the roles of the key project entrepreneurs associated with a nascent PBE. First, individual reputations can be defined as ‘attributes that are ascribed to an individual by other people’ (Wong & Boh, 2010, p. 129). The performance of the PBEs in which project entrepreneurs have been involved in the (recent) past is a fundamental attribute that can signal project entrepreneurs’ ability to generate superior products or activities (Podolny, 1993; Stern, Dukerich, & Zajac, 2014). Indeed, people often tend to use the quality of products produced in the (recent) past as an indicator of present or future quality (Shapiro, 1983). Second, project entrepreneurs also have specific roles, which are based on unique professional qualifications and related to specific tasks, skills and expertise (Chandler & Jansen, 1992) that they deploy in a serial manner moving from one PBE to another (Ferriani et al., 2009). Assigning roles is fundamental in structuring nascent PBEs because it can help to convince stakeholders that the nascent PBE’s activities are well-defined and oriented towards the realization of the organization’s project idea (Jung et al., 2017).

On the other hand, institutional theorists highlight that nascent PBEs also need to prove their socio-political legitimacy to investors. While individual reputations (Wong & Boh, 2010) and roles (Baker & Faulkner, 1991) are important to be distinguished from competitors, PBEs also need to realize novel project ideas that are considered socio-politically legitimate (Brush et al., 2001; Foo et al., 2005; Smith & Martí, 2017). Legitimacy is an important organizational property that can be defined as ‘the perceived appropriateness of an organization to a social system in terms of rules, values, norms and definitions’ (Deephouse et al., 2017, p. 9). In particular, the legitimacy of a nascent PBE has a socio-political dimension when it is derived from the endorsement that a regulatory institution provides to the nascent PBE’s project idea when it complies with specific quality standards, thus increasing the chance that the idea – and ultimately, its product – will be accepted in the market (Aldrich & Fiol, 1994; Bitektine, 2011; Stuart, Hoang, & Hybels, 1999).

Hypothesis Development

Private investors and nascent PBEs

Private investors are important stakeholders in nascent PBEs (Becker-Blease & Sohl, 2015; Debande, 2018). In creative industries, since the future commercial success of a nascent PBE is difficult to predict (Ferriani et al., 2009; Jones, 1996), private investors scrutinize and take decisions based on the project entrepreneurs’ individual reputation as predictors of possible future revenues. Specifically, there are two crucial dimensions of reputation and their associated types of performance: a commercial reputation based on past market performance, and an artistic reputation based on the opinions of industry experts about past artistic performance (Boutinot et al., 2017; Ebbers & Wijnberg, 2012a). Prior studies show that project entrepreneurs with favourable commercial, rather than artistic, reputation have a greater capacity to attract investors (Ebbers & Wijnberg, 2012a). Indeed, project entrepreneurs with a strong commercial reputation are more focused on market performance and the ambition to increment the mass acceptance of their products, while project entrepreneurs with a strong artistic reputation tend to be more focused on innovation, personal creative inspiration and artistic acclaim (Boutinot et al., 2017; Ertug et al., 2016).

Furthermore, PBEs in creative industries often have a dual leadership structure, where two key project entrepreneurs assume specialized, hierarchically equivalent, roles (Ebbers & Wijnberg, 2017; Reid & Karambayya, 2009): a creative director, who is responsible for design, innovation and vision-related activities, and a producer, who is responsible for resource management, budgeting and planning (Delmestri et al., 2005; Mollick, 2012). In these industries, the key management challenge is to balance the potentially opposing forces of creative freedom and commercial imperatives (Lampel et al., 2000). Thus, besides individual reputations, investment decisions are also based on the project entrepreneurs’ roles in the nascent PBE and whether their reputations are role-congruent, meaning that they are aligned with the specific role and responsibilities of an individual (Ebbers & Wijnberg, 2012b; Ertug et al., 2016).

In particular, the project entrepreneur in the producer role could be expected to be more important to private investors because s/he is responsible for selecting commercially viable ideas and instilling a sense of confidence in investors that the PBE’s products fulfil the market demand (Baldwin & Von Hippel, 2011; Mathias & Williams, 2017). For instance, in the video game industry, Mollick (2012) found that the producer plays a more critical role than the designer in achieving commercial success because the producer is responsible for resource allocation and for tempering the designer’s behaviour. Moreover, in a study of the French television industry, Clement, Shipilov and Galunic (2018) highlight that producers are responsible for guaranteeing that other team members can work efficiently to implement the creative directors’ insights on time and without any loss of quality. Therefore, we hypothesize:

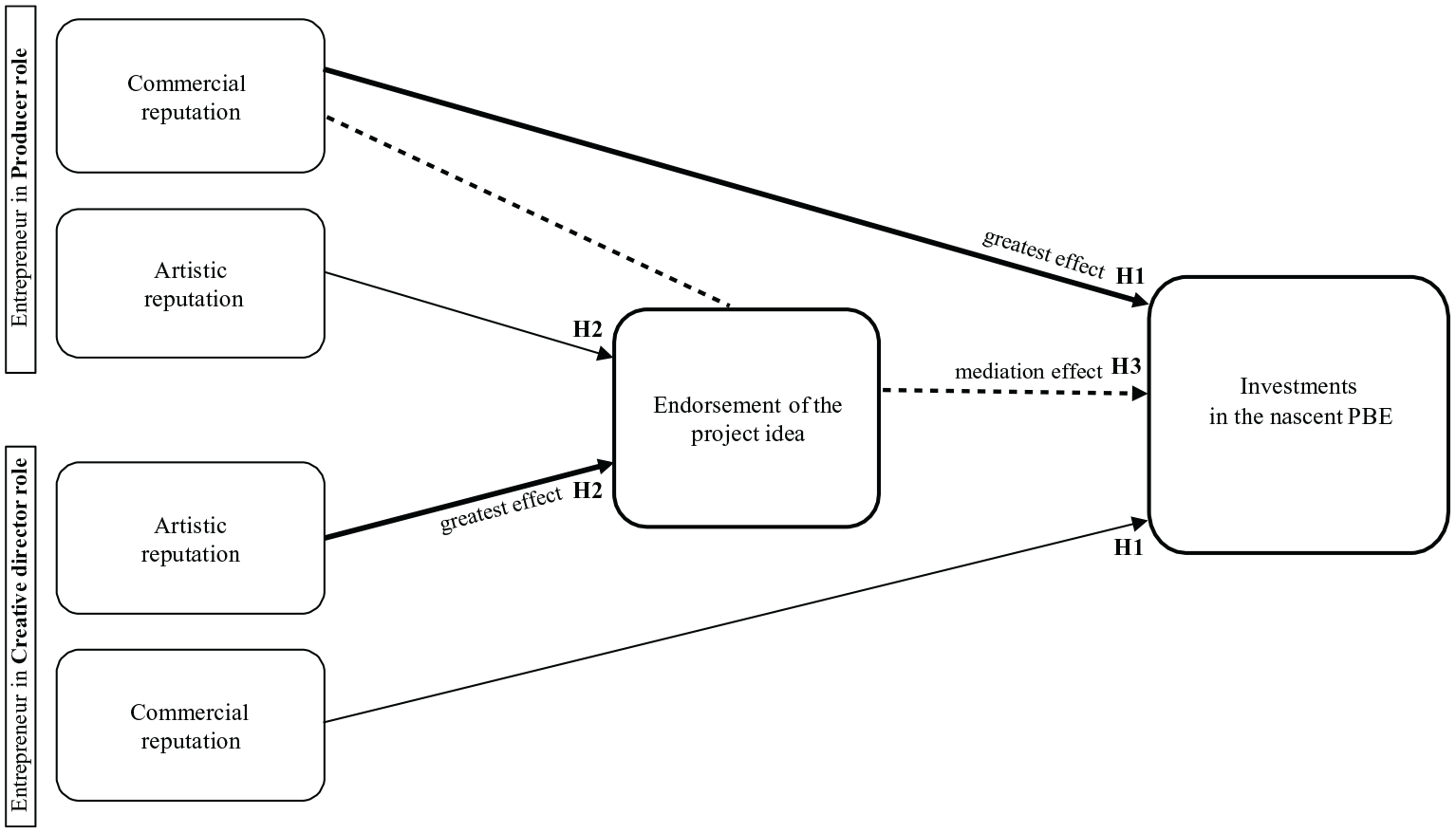

H1: When private investors evaluate a nascent PBE, their investment decision is positively influenced by the commercial reputation of the producer more than the commercial reputation of the creative director.

Regulatory institutions and nascent PBEs’ project ideas

Private investors often invest in industries where regulatory institutions are important stakeholders in nascent PBEs (Bakker et al., 2016; Bechky, 2006). In creative industries (Becker, 1982) these institutions are often constituted by industry experts with the authority to confer socio-political legitimacy through institutional endorsements, which signal the compliance of project ideas with respect to expected quality standards in a specific market (Aldrich & Fiol, 1994; Bitektine, 2011; King & Whetten, 2008). However, institutional actors providing endorsements for a nascent PBE’s project idea might focus on different dimensions of reputation than investors (Ebbers & Wijnberg, 2012a). While project entrepreneurs’ commercial reputation could signal a general ability to satisfy the consumption preferences of a broad audience, their artistic reputation could affect the likelihood of a project idea being endorsed by industry experts because it adheres to institutional expectations concerning quality standards in the industry (Boutinot et al., 2017; Ertug et al., 2016).

Besides different dimensions of reputation, institutional actors providing endorsements for a PBE’s project idea can also put a stronger emphasis on different project entrepreneur roles. While the project entrepreneur in the producer role might play an important role in attracting investors, the project entrepreneur in the creative director role can positively influence a regulatory institution’s decision to endorse a project idea by presenting innovative ideas in the language of existing institutions (Micheli, Perks, & Beverland, 2018; Söderlund & Sydow, 2019; Svejenova, Strandgaard Pedersen, & Vives, 2011) and thus invoking existing institutional standards in their design (Hargadon & Douglas, 2001). The role of the creative director in obtaining institutional endorsement for a nascent PBE’s project idea could be particularly important. For example, in the music industry creative directors play an important function in performing music that meets the expectations and standards of professional critics (Durand & Kremp, 2016), while in contemporary art, creative directors use rhetorical strategies to gain approval from public authorities and the art world in which they are active (Svejenova et al., 2011). Therefore, we hypothesize:

H2: When regulatory institutions evaluate a nascent PBE’s project idea, their endorsement decision is positively influenced by the artistic reputation of the creative director more than the artistic reputation of the producer.

The influence of institutional endorsements on private investors in nascent PBEs

Because of the temporary nature of PBEs, project entrepreneurs ‘face the repeated challenge of gaining legitimacy with every new project [idea]’ (Smith & Martí, 2017, p. 486). As argued earlier, to reduce their financial risk, investors can take into account the commercial reputation (Boutinot et al., 2017; Ebbers & Wijnberg, 2012a) of the project entrepreneur in the producer role because of its ability to select viable ideas and efficiently manage resources (Mathias & Williams, 2017; Mollick, 2012), while keeping the creative director in check (Clement et al., 2018). In addition, when evaluating the appropriateness of project ideas, regulatory institutions with the capacity to provide endorsements are also likely to be influenced by the commercial reputation of the project entrepreneur in the producer role. In turn, these institutional endorsements reduce the investment risk of private investors (Bruton, Fried, & Manigart, 2005; Stuart et al., 1999) by signalling that the nascent PBE’s project idea meets widely accepted quality standards in the field (Aldrich & Fiol, 1994; Graffin & Ward, 2010; King & Whetten, 2008; Zimmerman & Zeitz, 2002). Therefore, we hypothesize:

H3: The endorsement of a nascent PBE’s project idea by a regulatory institution mediates the effect of the producer’s commercial reputation on private investments in the PBE.

We summarize our hypotheses in the following conceptual model (see Figure 1), where we show how the reputations and roles of the two key project entrepreneurs help to attain the institutional endorsement of a project idea as well as to attract investments in the nascent PBE.

Conceptual Model.

Method

Empirical setting, data and variables

The empirical setting of this paper is the Italian film industry. The film industry is characterized by PBEs – i.e. film productions – where project entrepreneurs temporarily combine their skills for the duration of a film project, and the organization is disbanded once the film is completed (DeFillippi & Arthur, 1998). In Italy, private investors are a very important financial resource to start film productions (Debande, 2018). These investors are external to the film industry (e.g. financial intermediaries, fashion, food, consumer electronics companies), are motivated by commercial objectives, and in most cases lack specific knowledge of the film industry (La Torre, 2014). As a consequence, private investors evaluate individual characteristics of two key project entrepreneurs: the producer and the director (Baker & Faulkner, 1991; Delmestri et al., 2005).

The producer, on the one hand, is the project entrepreneur who manages the overall film production, maintaining a balance between time, costs and quality (Pardo, 2010). Film producers have the task to acquire financial resources, they are the main interlocutor for investors and are ‘at the core of the film’s financial, managerial and commercial networks’ (Hadida, 2010, p. 48). The director, on the other hand, is responsible for the ‘look and feel’ of the film. Directors need to craft a film’s artistic vision within the resource and commercial restrictions imposed by the producer (Delmestri et al., 2005). The individual reputations of the producer and director are important quality signals for investors when evaluating investment opportunities in a specific film. More specifically, investors distinguish between commercial reputation, derived from past commercial success (mostly box office), and artistic reputation, derived from past critical acclaim (Delmestri et al., 2005; Ebbers & Wijnberg, 2012a).

Producers and directors also aim to attract investors by demonstrating the film’s compliance with prevailing industry standards (Lampel et al., 2000). Similar to most other European countries, the Italian film industry is highly regulated by the government with the goal of stimulating the production of high-quality films. As a result, socio-political legitimacy can be signalled to investors by government endorsements (Durand & Jourdan, 2012; La Torre, 2014). In particular, the Italian government exercises control over national film productions through its Directorate General for Cinema (DGC), an agency of the Italian Ministry of Cultural Heritage, Activities and Tourism.

The DGC annually selects and appoints a committee of different experts (i.e. directors, scriptwriters, producers, distributors, exhibitors, critics, legal and financial professionals). This committee provides endorsements that are based on the evaluation of the quality of film projects – jointly submitted by directors and producers seeking government subsidies – and that, being publicly visible, can attract private investments in a film. In this paper, we focus on the endorsement of a film script, which reflects the embodiment of the project idea of the PBE (Macdonald, 2004) in its nascent stage. The endorsement considered is based on a publicly visible score (called ‘Value of subject and script’) that is composed of four dimensions that are conjointly taken into account: (a) the quality of the script (level of development); (b) the value of the story and theme (content originality and export potential); (c) the value of the characters, dialogue and narrative structure; and (d) the cinematic style (genre and vision) (cinema.benculturali.it/archivio, 2016a). We transformed the original scale of the score in hundreds for easier interpretation of our coefficients.

We collected all film script evaluations and private investment data from the subsidies and the external investors’ tax credit sections of the DGC website (cinema.beniculturali.it/tax-credit, 2016b). Our initial dataset included 309 investments made by private investors between 2010 and the beginning of 2014. Using Italian financial law no. 244/2007, investors began to invest equity in national films only in 2010: this year marks the beginning of our study period and dataset. During the exploratory stage of our study, we interviewed some of these investors, including an investor in an Oscar-winning film, to confirm that their investment decisions indeed depended on the commercial and artistic reputations of the producer and director, and the evaluation of the film idea by the DGC. We also removed all short films from the sample because they were not intended for cinematic release. The final sample consists of 235 investments.

Dependent variable

In our regression models, private investments in a nascent PBE represent our dependent variable, which is measured by the absolute size of investments (inflation-adjusted) in a single film production (Morawetz, Hardy, Haslam, & Randle, 2007). Because the variable has a skewed distribution, we used a logarithmic transformation (Ferriani et al., 2009).

Explanatory variables

In the film industry, a reputation based on past performance is a signal that an individual contributed to the success of a particular film (Jones, 1996). We constructed performance-based reputation variables for the two main project entrepreneurs of PBEs – producers and directors – before investments were made in their films (Delmestri et al., 2005). To exclude potential effects of role overlap, we also checked if in our dataset the producer and director roles were occupied by the same individual but found no such cases.

Commercial reputation was calculated using previous box office performance (e.g. Delmestri et al., 2005; Sorenson & Waguespack, 2006). We used the same procedure of Ebbers and Wijnberg (2012a) by calculating the average (mean value) of the total box office revenues (inflation-adjusted) that producers and directors obtained in their three most recent films, right before the film that was the object of investors’ decisions. This was based on information about the investment date reported on the Italian DGC website. Considering the last three films enables one to capture a reputation based on recent performance, which can attract the audience to theatres and therefore investment decisions (Ebbers & Wijnberg, 2012a). We also assigned a reputation value of 0 when it was the first film of a producer or director. We collected box office data from two sources: Cinetel, the Italian agency responsible for monitoring national ticket sales (cinetel.it, 2016), and the Internet Movie Database (IMDb, 2016), the most authoritative web source for the film industry (Hsu, 2006).

Artistic reputation was derived from critical acclaim in the form of reviews from expert film critics (Delmestri et al., 2005). We operationalized artistic reputation as a score ranging from 0 to 1, representing an average of the review scores received by the producer and the director. Consistent with the other measure of reputation (Ebbers & Wijnberg, 2012a), we considered their three most recent films, which were released right before the film that was the object of investors’ decisions. We assigned a reputation value of 0 when it was the first film of a producer or director. We retrieved the review scores from MyMovies (2016), the most popular online source for film reviews in Italy, whose review score (called ‘Dizionari’) is based on the evaluations of the most important Italian film critics, Paolo Mereghetti, Pino Farinotti and Morando Morandini (Delmestri et al., 2005).

Moreover, using the individual reputations described above, we also constructed two cumulative reputation measures. First, cumulative commercial reputation, which is the average between the producer’s and director’s commercial reputation. Second, cumulative artistic reputation, which is the average between the producer’s and director’s artistic reputation. This enabled us to apply two steps to test our first two hypotheses, where we compare the models using the cumulative reputations with the models using the individual (artistic and commercial) reputations of the producer and director.

Script endorsement is a continuous measure of legitimacy (Deephouse et al., 2017; Zimmerman & Zeitz, 2002). The endorsement of a nascent PBE’s project idea confers socio-political legitimacy to the overall organization, signalling compliance with specific quality standards (Aldrich & Fiol, 1994; King & Whetten, 2008; Zimmerman & Zeitz, 2002). We therefore operationalized this endorsement as the score, ranging from no legitimacy (0) to maximum legitimacy (1), assigned to the film script by an industry expert committee consisting of directors, scriptwriters, producers, distributors, exhibitors, critics, legal and financial professionals, that works for the Italian DGC.

Control variables

The score assigned to the film script by the DGC influences whether the film will also receive government subsidies. To exclude investors who invested in a film production because of these subsidies and not because of the legitimacy provided by the endorsement, we included a dummy variable in the regression models with investments as the dependent variable, which assumes a value of 1 for films that received subsidies and 0 for films that did not.

To control for the effect of project entrepreneurs who are new entrants, i.e. directors and producers who are new to the industry and therefore do not have any released films, we created control variables called director’s and producer’s first film, which assumes a value of 1 when a film was the first film released in the cinema by a particular director or producer, 0 otherwise (Ebbers & Wijnberg, 2012a).

We also controlled for individual pragmatic legitimacy of the project entrepreneurs, which is measured in the form of industry experience (Cohen & Dean, 2005; Packalen, 2007). Since professionals who have been more active in an industry might attract more resources, we counted the total number of films for which the director and the producer were credited on the IMDb database (2016) in their entire career and prior to the film that was the object of investors’ decisions (Cattani & Ferriani, 2008). Moreover, we controlled for producer–director past collaborations, since they could affect a film’s success (Sorenson & Waguespack, 2006) and, thus, investors’ decisions (Shane & Cable, 2002). Consistent with the way we measure reputations, we considered the producer and the director of the film that is the object of investment decisions and counted the number of past films in which they had collaborated (Ebbers & Wijnberg, 2012a).

In addition, the green-lighting decision for films can be contingent on the participation of reputable stars (Hofmann, 2012). We, therefore, controlled for the main cast’s commercial reputation, using the same approach as for the producer and director. The variable is based on the first two credited cast members, actress or actor, of the film that is the object of investors’ decisions (Cattani, Ferriani, Mariani, & Mengoli, 2013), who are reported on cinemaitaliano.it (2020), an important source of information about Italian films. The variable is the average of the commercial reputation of these two main cast members. This reputation is calculated as the average box-office revenues of the three most recent films in which the two cast members featured. When any of these two main cast members is a new entrant in the film industry (i.e. no prior films), her/his commercial reputation is coded as 0. As a result, if both cast members are new entrants, this variable is coded as 0. Furthermore, we added a control variable, called cast size, which is a count variable of the total number of cast members credited in the film, to account for the possibility that the importance of the two main cast members might depend on the total cast.

Next, we also considered that film consumers can have different preferences due to cultural differences (Kim & Jensen, 2014). Locally produced comedies are more likely to have domestic commercial success because humour tends to be country- and culture-specific (Friedman, 1992). Since investors prefer films that are more likely to generate high profits, we created a dummy variable for comedy, assuming a value of 1 when the film was classified as a comedy (or a related sub-classification) and 0 otherwise. In addition, because dramas tend to be associated with higher aesthetic value and critical acclaim (Simonton, 2005), scores conferred by the DGC, which are based on assessments of quality standards, could be higher for films in the drama genre. Therefore, we created a dummy variable for drama, assuming a value of 1 when the film was classified as a drama (or a related sub-classification) and 0 otherwise. Even though the films in the sample are mostly comedy (40%) and drama (50%), we also performed additional regressions where we specified the remaining 10% of genres: comedy-drama, thriller, horror, documentary, animation and biopic. The results (available upon request) do not change.

Moreover, before they invest, private investors consider the number of opening screens in film theatres. This is the number of screens that are expected to be allocated to the film in the first weekend of its theatrical release. This is important because films released with a relatively large number of opening screens are more likely to attract a larger number of visitors and influence the final number of screens allocated to a film (Sorenson & Waguespack, 2006), both of which affect overall box office revenues (Elberse & Eliashberg, 2003). This is also illustrated by earlier studies suggesting that ‘a bank which decides to finance a film project cannot do it without a careful analysis of the distribution deal’ (La Torre, 2014, p. 139).

Finally, we included a dummy variable to identify private investors that are financial intermediaries, such as banks, finance companies, investment companies, credit unions and private equity funds (Gup, 2011). Like other types of investors, financial intermediaries are external to the film industry. However, they are especially concerned with direct financial returns on their investments, whereas firms from other types of industries (e.g. fashion, food, consumer electronics) might invest in films with the objective of promoting their products to consumers (Hofmann, 2012).

Regression models

A single investment in a film production is our unit of analysis. To test our hypotheses, we estimated all models using ordinary least square regressions with robust standard errors to correct for possible heteroskedasticity (Imbens & Kolesar, 2016). For all models, the variance inflation factor (VIF) values (reported in our tables) do not exceed the threshold of ten, indicating no collinearity problems (Sorenson & Waguespack, 2006).

To test hypotheses 1 and 2, we calculated standardized coefficients (p-value based on a two-tailed test) that enabled us to compare the effects of variables based on different measures (Bring, 1994), i.e. artistic reputation and commercial reputation. In particular, we followed two steps. First, we show a benchmark model in which we estimated the standardized coefficients of the cumulative commercial and artistic reputations of the two project entrepreneurs. Second, we show the main models of interest in which we estimated the standardized coefficients of their individual artistic and commercial reputations. These two steps show the added value and importance of focusing on the individual reputations of the producer and director roles. Moreover, we performed a (two-tailed) paired t-test to check if there is a significant mean difference between the individual reputations we compare.

To test hypothesis 3, which hypothesizes a mediation effect, we applied a causal step approach (Baron & Kenny, 1986) that is based on four conditions, as in Kirkpatrick, Altanlar and Veronesi (2017). To satisfy the first condition, we tested the existence of a direct effect to be mediated, showing that the main predictor considered (producer’s commercial reputation) significantly affects the dependent variable (private investments) when the mediator (script endorsement) is not included. To satisfy the second condition, we tested whether the predictor significantly affects the mediator. To satisfy the third condition, we tested whether the mediator significantly affects the dependent variable. To satisfy the fourth (and last) condition, we tested whether a mediation effect occurs when the mediator is added to the model and the significance of the predictor decreases.

Results

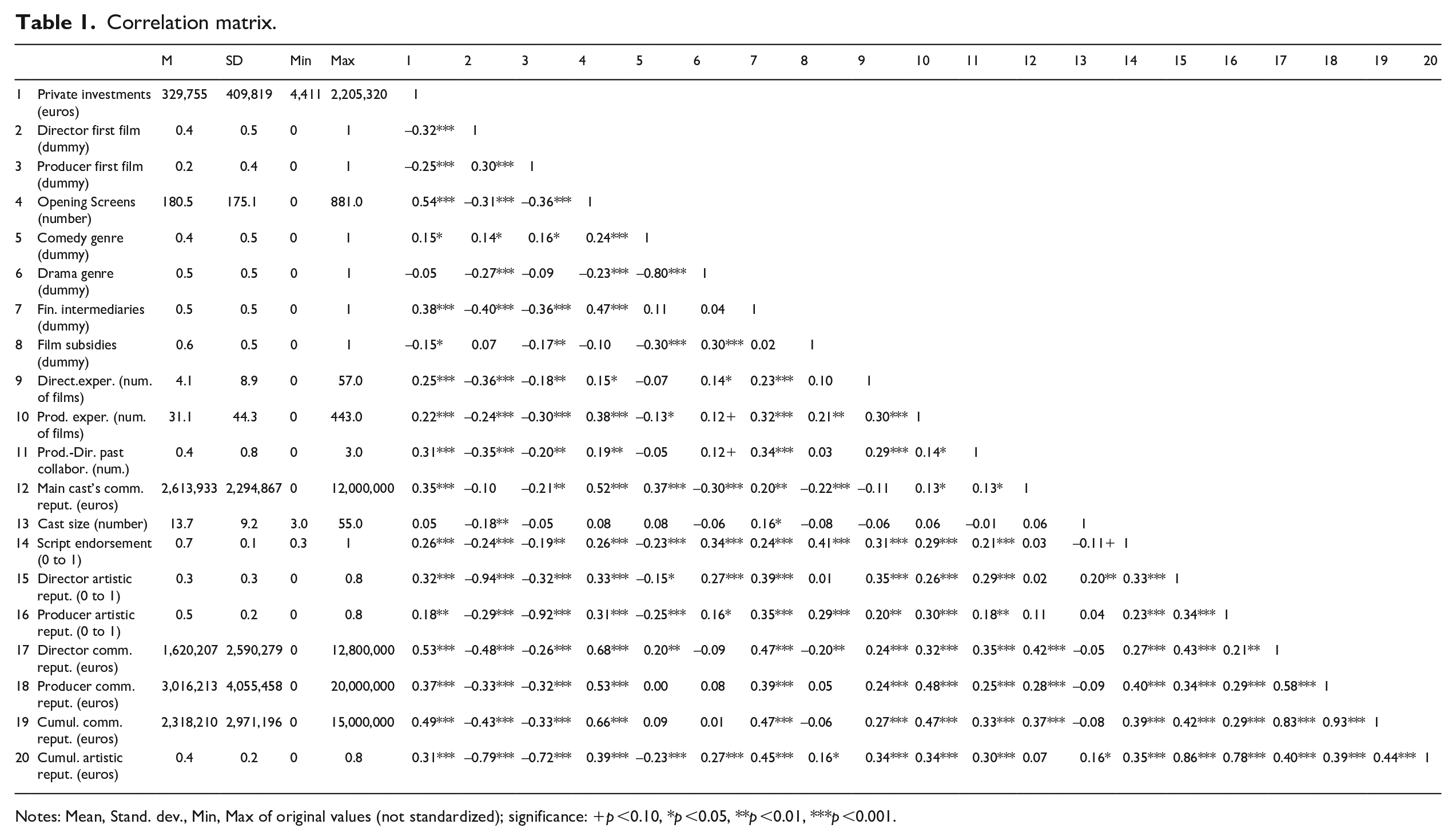

We report descriptive statistics and correlations in Table 1. Significant correlations exist between our dependent variable private investments and our main predictors: director’s commercial reputation (0.53), producer’s commercial reputation (0.37), director’s artistic reputation (0.32) and producer’s artistic reputation (0.18). This indicates the possibility of direct effects. Significant correlations also exist between the mediator variable script endorsement and our main predictors: director’s commercial reputation (0.27), producer’s commercial reputation (0.40), director’s artistic reputation (0.33) and producer’s artistic reputation (0.23). Finally, a significant correlation exists between the mediator and the dependent variable, indicating the possibility of an indirect effect (0.26).

Correlation matrix.

Notes: Mean, Stand. dev., Min, Max of original values (not standardized); significance: +p <0.10, *p <0.05, **p <0.01, ***p <0.001.

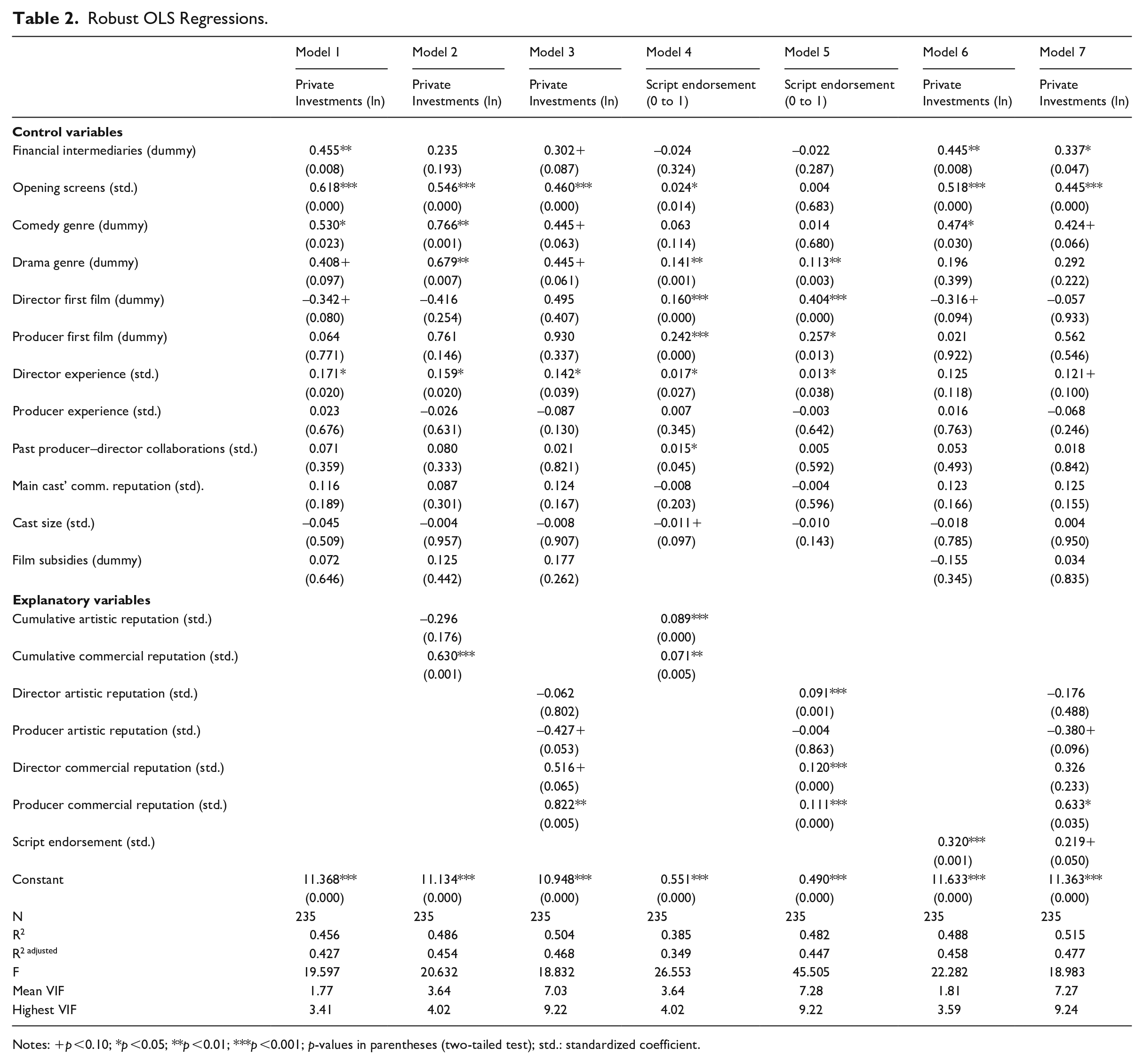

We present the regression models with robust standard errors in Table 2. Before estimating the models, we performed an outlier test of the data for private investments. We identified outliers with values below the 1st percentile (only 1 found) and above the 99th percentile (only 3 found) of the distribution and assigned the values of the variable at the 1st and the 99th percentiles. The percentiles method has the advantage of being viable regardless of the data probability distribution. Following the recommendations of Ghosh and Vogt (2012), we chose the 99th percentile instead of the 95th percentile to reduce possible statistical bias.

Robust OLS Regressions.

Notes: +p <0.10; *p <0.05; **p <0.01; ***p <0.001; p-values in parentheses (two-tailed test); std.: standardized coefficient.

The results in Table 2 support hypothesis 1: When private investors evaluate a nascent PBE, their investment decision is positively influenced by the commercial reputation of the producer more than the commercial reputation of the creative director. Indeed, in model 2 the cumulative commercial reputation (β = 0.630, p <0.001) has the most significant effect on private investments compared to the cumulative artistic reputation (β = -0.296, n.s). Then, in model 3, the producer’s commercial reputation (β = 0.822, p <0.01) has the most significant effect on private investments compared to the director’s commercial reputation (β = 0.516, p <0.10). This is also supported by the t-test (H0: mean difference of producer and director’s commercial reputation = 0, p <0.001). Since the dependent variable is a logarithm, a one standard deviation increase in a producer’s commercial reputation leads to an 82.2% increase in private investments, corresponding to an increase of €271,059 if we consider an investment equal to the mean of the variable private investments. A one standard deviation increase in a director’s commercial reputation leads to a 51.6% increase in private investments, corresponding to an increase of €170,154 if we consider an investment equal to the mean of this variable.

Hypothesis 2 is supported: When regulatory institutions evaluate a nascent PBE’s project idea, their endorsement decision is positively influenced by the artistic reputation of the creative director more than the artistic reputation of the producer. In model 4, the cumulative artistic reputation (β = 0.089, p <0.001) has the most significant effect on the script endorsement compared to the cumulative commercial reputation (β = 0.071, p <0.01). Then, in model 5, the effect of the director’s artistic reputation (β = 0.091, p <0.001) on the script endorsement is significant, positive and stronger than the effect of the producer’s artistic reputation (β = -0.004, n.s.). This is supported by the t-test (H0: mean difference of producer and director’s artistic reputation = 0, p <0.001). Because values for the dependent variable range between 0 and 1, a one standard deviation increase in a director’s artistic reputation leads to a 9.1% increase in the endorsement score.

Hypothesis 3 is supported: The endorsement of a nascent PBE’s project idea by a regulatory institution mediates the effect of the producer’s commercial reputation on private investments in the PBE. To test our third hypothesis, we checked that all the conditions of our causal approach (Baron & Kenny, 1986) are satisfied. In model 3, the significant positive effect of the producer’s commercial reputation on private investments satisfies the first condition (direct effect). In model 5, the significant positive effect of producer’s commercial reputation on the script endorsement satisfies the second condition (β = 0.111, p <0.001). In model 6, the significant positive effect of the script endorsement on private investments (β = 0.320, p <0.001) satisfies the third condition; specifically, a one standard deviation increase in the endorsement score leads to a 32% increase in private investments. Finally, in model 7, the effect of the producer’s commercial reputation is still significant but lower (β = 0.633, p <0.05), suggesting partial mediation: in particular, the proportion mediated is 0.23 of the total effect. In this model, a one standard deviation increase in the producer’s commercial reputation leads to an increase of 63.3% in private investments, which corresponds to an increase of €208,735, considering an investment equal to the mean value of private investments.

Robustness tests

We performed several robustness tests. First, to control for the non-independence of producers and directors involved in our sample, we checked the possibility that our observations could be clustered according to the identity of a producer or director (i.e. non-completely independent). Thus, we performed additional regressions using cluster adjusted-standard errors (Abadie, Athey, Imbens, & Wooldridge, 2017) twice, once adjusting our standard errors for producers’ identity (65 producers) and once for directors’ identity (105 directors). The regressions cluster-adjusted for producers’ identity show that all hypotheses are supported (Table 3 in the appendix): H1 (β prod.comm.rep. = 0.822, p <0.10; βdir.comm.rep.= 0.516, n.s.; t-test rep.diff.=0, p <0.001), H2 (β dir.art.rep. = 0.091, p <0.05; βprod.art.rep.= -0.004, n.s.; t-test rep.diff.=0, p <0.001) and H3, which shows full mediation, rather than partial, since the effect of producer commercial reputation on private investments becomes not significant (β prod.comm.rep.. = 0.633, n.s.) when the mediator is included. The regressions cluster-adjusted for directors’ identity also show that all hypotheses are supported, obtaining very similar effects (results available upon request): H1 (β prod.comm.rep. = 0.822, p <0.10; βdir.comm.rep.= 0.516, n.s.; t-test rep.diff.=0, p <0.001), H2 (β dir.art.rep. = 0.091, p <0.05; βprod.art.rep.= -0.004, n.s.; t-test rep.diff.=0, p <0.001) and H3 (β prod.comm.rep. = 0.633, n.s.).

Second, in some studies, legitimacy has been treated as a continuous construct (Deephouse et al., 2017; Zimmerman & Zeitz, 2002), while in others it has been treated as a dichotomous construct (Deephouse & Suchman, 2008). We therefore performed additional regressions with script endorsement as a dummy instead of a continuous variable (results available upon request), by distinguishing between films with scores above (coded as 1) or below (coded as 0) the median value (Cattaneo, Meoli, & Signori, 2016). Except for the magnitude of a few coefficients, our results do not change: H1 (β prod.comm.rep. = 0.822, p <0.01; βdir.comm.rep.= 0.516, p <0.10; t-test rep.diff.=0, p <0.001), H2 (β dir.art.rep. = 2.545, p <0.01; βprod.art.rep.= -0.291, n.s.; t-test rep.diff.=0, p <0.001) and H3 (β prod.comm.rep. = 0.735, p <0.05) are supported.

Third, instead of coding the reputations of new entrants as 0, we performed regressions coding these reputations as the lowest value in the sample to account for the possibility that new entrants acquired reputations in fields related to the film industry, like theatre or television (Ebbers & Wijnberg, 2012a). These results (available upon request) confirm that H1 (β prod.comm.rep. = 0.535, p <0.01; βdir.comm.rep.= 0.379, p <0.10; t-test rep.diff.=0, p <0.001), H2 (β dir.art.rep. = 0.060, p <0.001; βprod.art.rep.= -0.002, n.s.; t-test rep.diff.=0, p <0.001) and H3 (β prod.comm.rep. = 0.412, p <0.05) are supported.

Fourth, we performed regressions without excluding the outliers below the 1st percentile and above the 99th percentile. The results (available upon request) confirm that H1 (β prod.comm.rep. = 0.827, p <0.01; βdir.comm.rep.= 0.522, p <0.10; t-test rep.diff.=0, p <0.001), H2 (β dir.art.rep. = 0.091, p <0.001; βprod.art.rep.= -0.004, n.s.; t-test rep.diff.=0, p <0.001) and H3 (β prod.comm.rep. = 0.634, p <0.05) are supported.

Fifth, although a film script can be submitted to the Italian DGC only by film producers and directors, which are the film’s founders and prospective managers (Delmestri et al., 2005), a film scriptwriter might also affect the quality of the film (Eliashberg, Hui, & Zhang, 2007). We performed additional regressions including the scriptwriter’s quality, operationalizing it by counting the number of award nominations and wins that scriptwriters received throughout their career until the focal film (Cattani & Ferriani, 2008). We considered the two most prestigious awards for scriptwriters in Italy: the Davide di Donatello and the Nastro d’argento. We also added a dummy variable to control for cases in which the scriptwriter role overlaps with the director role (71% of the cases). We did not find any cases in which the scriptwriter role overlaps with the producer role. These results (available upon request) confirm that H1 (β prod.comm.rep. = 0.813, p <0.01; βdir.comm.rep= 0.553, p <0.05; t-test rep.diff.=0, p <0.001), H2 (β dir.art.rep. = 0.077, p <0.01; βprod.art.rep.= -0.005, n.s.; t-test rep.diff.=0, p <0.001) and H3 (β prod.comm.rep. = 0.611, p <0.05) are supported.

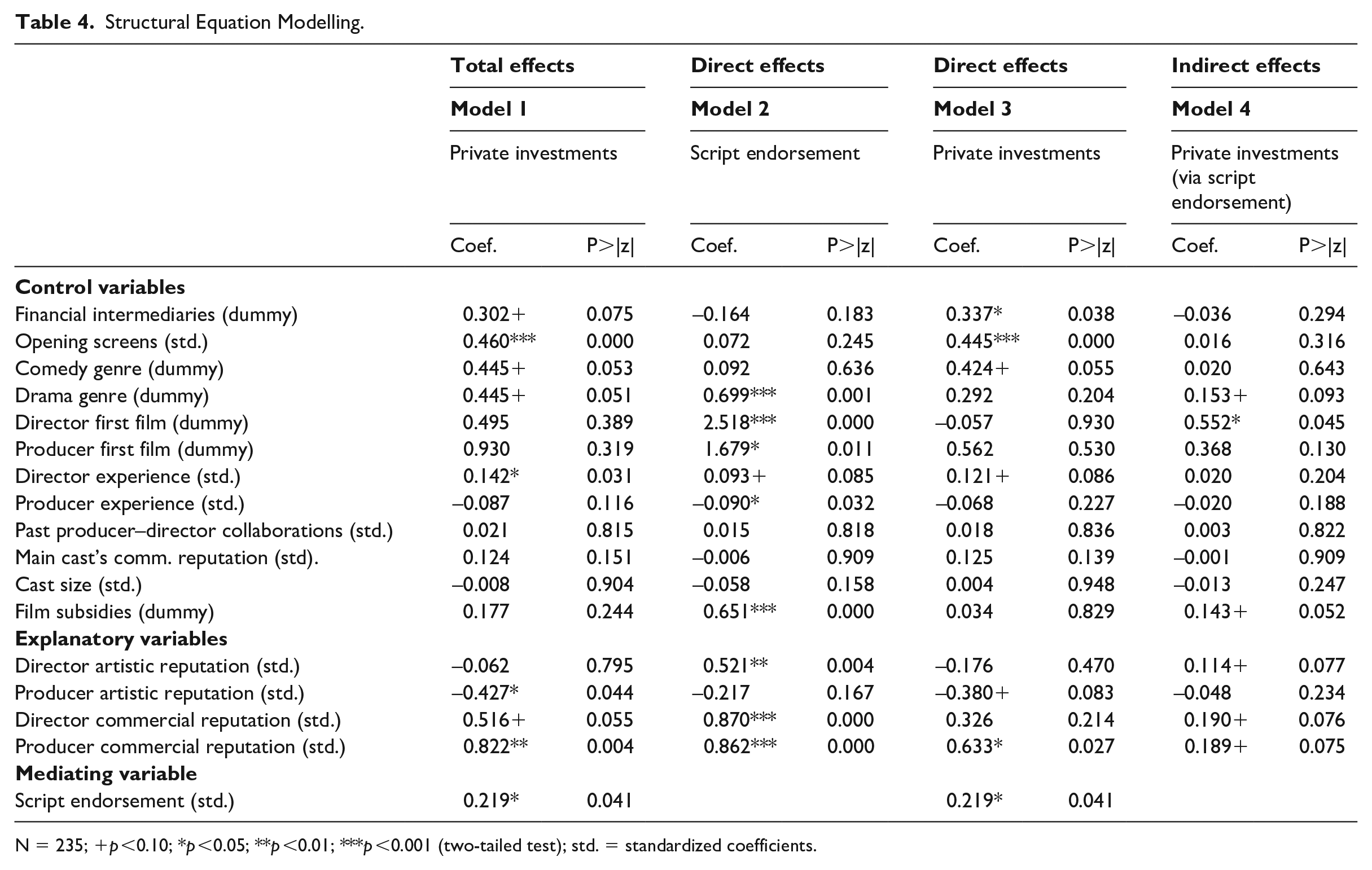

Finally, we performed two complementary checks to confirm the validity of our causal step approach (Baron & Kenny, 1986) in testing mediation. We developed structural equation models (SEMs) with robust standard errors, using Stata’s sem command (Zhao, Ishihara, Jennings, & Lounsbury, 2018). SEMs enable one to visualize direct and indirect effects and consider possible correlation of error terms across systems of equations (Shaver, 2005). Results are in line with the step approach, supporting our mediation hypothesis 3 (Table 4 in the appendix). Indeed, both the direct effect (model 3, β = 0.633, p <0.05) and the indirect effect (model 4, β = 0.189, p <0.10) of producer’s commercial reputation on private investments are significant. SEMs also confirms that the portion of the total effect mediated is 0.23. Moreover, following Hayes (2013), we also implemented a bootstrap test (with 1000 replications as resampling), which can detect the type I error more accurately than the step approach or the Sobel test (Caron, 2019). This bootstrap test does not rely on the assumption of normality, it considers the sampling distribution of the indirect effect as asymmetric, with nonzero skewness and kurtosis (Aguinis, Edwards, & Bradley, 2017). As in the case of SEMs, also this test confirms the step approach and supports hypothesis 3, showing that the direct effect (β = 0.633, p <0.05) and the indirect effect (β = 0.189, p <0.10) of producer’s commercial reputation are both significant.

Discussion and Implications

In this paper, we studied the extent to which specific individual characteristics of key project entrepreneurs, namely their professional roles (Mollick, 2012) and reputations (Boutinot et al., 2017; Ebbers & Wijnberg, 2012a; Ertug et al., 2016), and the socio-political legitimacy of their project idea in the form of an endorsement by a government institution (Brush et al., 2001; Foo et al., 2005), affect investments in PBEs (Ferriani et al., 2009). In particular, we focused on nascent PBEs (Ebbers & Wijnberg, 2012a; Radoynovska & King, 2019), built on a single project idea (Hobday, 2000) led by two key project entrepreneurs: the producer, who is responsible for resource management, budgeting, and planning; and the creative director, who is predominantly responsible for converting the project idea into a product (Mathias & Williams, 2017; Mollick, 2012). Both of them have a commercial and an artistic reputation that we show to be important quality signals, especially when these reputations are role-congruent (Ebbers & Wijnberg, 2012a; Ertug et al., 2016).

We studied this in the context of creative industries. In particular, the specific empirical setting of our study is the Italian film industry, which is a highly appropriate context for our study because it is characterized by PBEs consisting of freelance professionals with a dual leadership – the producer and the director – who temporarily combine their skills for the duration of a single film project (DeFillippi & Arthur, 1998; Ebbers & Wijnberg, 2017). First, we found support for our first hypothesis that the commercial reputation of the producer has a stronger effect on attracting private investments than the commercial reputation of the (creative) director. Second, we found support for our second hypothesis that the artistic reputation of the director – rather than the artistic reputation of the producer – has a stronger effect on attaining an institutional endorsement by a committee of industry experts that assesses the extent to which a project idea – or film script in our case – meets the quality standards in the industry. Third, we found support for our third hypothesis that this endorsement mediates the positive effect of the commercial reputation of the producer on attaining private investments.

Our study has three main theoretical contributions. First, we answer the calls for studies on temporary organizations to carry out more research that considers the relationship between agency and structure, focusing on different levels of analysis (Bakker et al., 2016; Sydow et al., 2004): the individual (role-congruent reputations of project entrepreneurs), the institutional (endorsement of a project idea) and the PBE (capacity to attract investments). Building on prior studies suggesting that investors can evaluate reputational and socio-political legitimacy signals simultaneously (Bitektine, 2011; Deephouse & Suchman, 2008; Deephouse et al., 2017), our mediation model provides new insights into the temporal order in which these two levels (inter-)operate in the PBEs’ nascent stage. Primarily, we show that individual-level reputations not only directly attract investors, but also help in gaining acceptance in the field (King & Whetten, 2008; Petkova, 2016) through the institutional endorsement of the entrepreneurs’ project ideas. Next, we show that this endorsement, in turn, has a positive effect on investors, mediating the relationship between project entrepreneurs’ reputations and investments. By doing so, we demonstrate the interplay between upper echelons theory, with its emphasis on the characteristics and actions of top management team members, and institutional theory, which suggests that there are constraints to managerial discretion (Hambrick, 2007; Hambrick & Mason, 1984; Neely et al., 2020) since nascent (project) ideas need to meet certain field-level standards to receive institutional endorsements that signal socio-political legitimacy (Brush et al., 2001; Foo et al., 2005; Jones et al., 2010; Smith & Martí, 2017). Particularly, we respond to recent calls for more research on PBEs being embedded in their institutional field (Söderlund & Sydow, 2019; Stjerne & Svejenova, 2016). While prior research shows that PBEs are often embedded in (relatively) permanent organizational structures, such as parent organizations (Stjerne & Svejenova, 2016) and interorganizational networks (Windeler & Sydow, 2001), in our study we show the extent to which nascent PBEs can be supported by powerful legitimizing (government) bodies in their institutional field that evaluate not only the appropriateness of the PBE’s project idea but also the role-congruent reputations (Ertug et al., 2016) of the key project entrepreneurs (Ebbers & Wijnberg, 2012a).

Second, prior studies show that specific project entrepreneurs’ reputations (Delmestri et al., 2005) and role combinations (Baker & Faulkner, 1991) can affect the nascent PBE’s ability to attract investments. Recent scholars show that specific dimensions of reputation only have a positive effect on investors (Ebbers & Wijnberg, 2012b) and on other stakeholders (Ertug et al., 2016) when a particular dimension reflects an ability or quality that corresponds with an individual’s particular role and responsibility. We contribute to this prior research by showing that whether or not key project entrepreneurs associated with a nascent PBE – the producer and creative director – affect investor behaviour and institutional endorsement depends not only on project entrepreneurs’ reputation being role-congruent (Ebbers & Wijnberg, 2012b; Ertug et al., 2016) but also on the amount of emphasis that is being placed on role-congruent reputations by different types of stakeholder. By focusing on predicting investments rather than fame, and individual- rather than organization-level reputations, we also answer the call of Boutinot et al. (2017) for more research on the interplay between reputations, gatekeepers and audiences in creative industries. Moreover, in the broader field of entrepreneurship, our work responds to a recent call to conjointly study the way in which founders’ roles are internally structured within nascent ventures as well as how their individual reputations are externally evaluated by key stakeholders that can affect organizational performance (Jung et al., 2017).

Third, we contribute to research on PBEs in the specific context of creative industries. Creative industries, such as the film industry, are a particularly interesting context for our study because they are characterized by products with high symbolic – rather than functional – value (Throsby, 2008), a high degree of process ambiguity (Lingo & O’Mahony, 2010) and high demand uncertainty (Lampel et al., 2000), which make investments very risky. On the one hand, from an upper echelons theory perspective, and considering the high degree of process ambiguity in creative industries, one might expect investors to give the key project entrepreneurs an exceptional degree of managerial discretion (Hambrick & Finkelstein, 1987) in the production stage. However, precisely because they give so such managerial discretion, to mitigate their risk investors can be expected to put a relatively strong emphasis on evaluating the specific role-congruent reputations in their investment decision-making process. On the other hand, from an institutional theory perspective, since products in creative industries are characterized by a high degree of symbolic value (Throsby, 2008), one would expect a strong effect of socio-political legitimacy on investments through the endorsements of (government) institutions, which consist of knowledgeable industry experts acting as important gatekeepers, whose quality judgements constitute valuable symbolic resources (Rafaeli & Vilnai-Yavetz, 2004) to persuade investors of the potential market demand.

Our study also has a number of practical implications. First, when key project entrepreneurs – in particular producers and creative directors – are evaluating potential partners to establish a nascent PBE with, they can increase their chances of attracting private investments by taking into account the complementarity of their – role-congruent – reputations. While producers need a commercial reputation to convince investors, creative directors need a favourable artistic – as well as a commercial – reputation to attain institutional endorsement that, in turn, helps to attract investments.

Second, project entrepreneurs can benefit from the insight that the artistic reputation of the project entrepreneur with a creative director role can be a double-edged sword in the investment stage of a nascent PBE because there is a trade-off between having a favourable artistic versus commercial reputation. While creative directors’ artistic reputation does not help to attract investments directly, their artistic – as well as commercial – reputation does have a positive effect on attaining institutional endorsement which, in turn, has a positive effect on attracting investments.

Third, we noticed an interesting empirical finding that, although out of the scope of our hypotheses, is worthwhile to highlight because of its potential practical implication. We found that the positive effect of the director’s artistic reputation on attaining institutional endorsement is stronger than the producer’s artistic reputation. However, it is not stronger than the commercial reputation of either the producer or the director. This suggests that the committee of industry experts that provides quality evaluations of new film ideas on behalf of the government places more emphasis on the reputation of the project entrepreneur in the creative role – the film director – because this role is most directly associated with transforming the project idea (the film script) into the final product (the film). The fact that the director’s artistic as well as commercial reputation have a positive effect on attaining institutional endorsement suggests that directors need to signal not only their capacity to convince important tastemakers, such as professional film critics, but also their capacity to meet the preferences of the end-consumers.

Fourth, from an investors’ perspective, regulatory institutions can play an important role in reducing investment uncertainty, which can be related to two sources of uncertainty: a performance-based uncertainty, concerning project entrepreneurs’ past track record and capabilities to create successful products, and a standards-based uncertainty, concerning the project entrepreneurs’ capacity to create products that meet specific standards (Graffin & Ward, 2010). While individual performance-based reputations are quality signals that can reduce the first source of uncertainty, institutional endorsements are quality signals that can reduce the second source of uncertainty by showing how the project entrepreneurs’ product ideas are judged against specific institutional standards.

Finally, this paper has a number of limitations that also provides avenues for future research. First, our study focuses on two project entrepreneurs, namely the film director and producer. Even though these two represent the key roles of nascent PBEs in creative industries characterized by a dual-leadership structure (Ebbers & Wijnberg, 2017; Reid & Karambayya, 2009), future studies could focus on other roles. In particular, scholars could investigate in more detail how main cast members affect institutional endorsement and investment decisions by identifying for which films the main cast members were affiliated with the nascent PBE already in the investment stage and therefore may have affected investment decisions. Second, our measure of legitimacy mostly captures a socio-political dimension (Bitektine, 2011). However, endorsements are often a combination of socio-political and cognitive elements of legitimacy that are difficult to disentangle (Wang, Thornhill, & De Castro, 2017). Although the DGC in our study provides socio-political legitimacy, it employs industry experts to perform the actual evaluation of the film scripts that could introduce a cognitive dimension of legitimacy. Future research could try to disentangle these two dimensions. Third, the endorsement score used in our study is based on four underlying dimensions (story, dialogues, etc.) that are jointly taken into account. Future studies could consider other measures. For example, evaluating other kinds of quality dimensions regarding the project idea could lead to new insights about the relationship between a director’s artistic reputation and its capacity to obtain institutional endorsement. Finally, the film industry produces experience goods for which quality is hard to evaluate before consumption (Nelson, 1970), and where value judgements focus more on symbolic and aesthetic dimensions rather than functional ones (Rafaeli & Vilnai-Yavetz, 2004). Although we expect our findings to be generalizable to other creative industries, it would be interesting to extend this research to investments in start-ups in non-creative industries, focusing on key serial entrepreneurs (Medcof & Lee, 2017) with the CEO and the CTO role (e.g. the software industry) or the CEO and the CSO role (e.g. the biotech industry).

Footnotes

Appendix

Structural Equation Modelling.

|

|

|

|

|

|||||

|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

|||||

| Private investments |

Script endorsement |

Private investments |

Private investments (via script endorsement) |

|||||

| Coef. | P>|z| | Coef. | P>|z| | Coef. | P>|z| | Coef. | P>|z| | |

|

|

||||||||

| Financial intermediaries (dummy) | 0.302+ | 0.075 | −0.164 | 0.183 | 0.337* | 0.038 | −0.036 | 0.294 |

| Opening screens (std.) | 0.460*** | 0.000 | 0.072 | 0.245 | 0.445*** | 0.000 | 0.016 | 0.316 |

| Comedy genre (dummy) | 0.445+ | 0.053 | 0.092 | 0.636 | 0.424+ | 0.055 | 0.020 | 0.643 |

| Drama genre (dummy) | 0.445+ | 0.051 | 0.699*** | 0.001 | 0.292 | 0.204 | 0.153+ | 0.093 |

| Director first film (dummy) | 0.495 | 0.389 | 2.518*** | 0.000 | −0.057 | 0.930 | 0.552* | 0.045 |

| Producer first film (dummy) | 0.930 | 0.319 | 1.679* | 0.011 | 0.562 | 0.530 | 0.368 | 0.130 |

| Director experience (std.) | 0.142* | 0.031 | 0.093+ | 0.085 | 0.121+ | 0.086 | 0.020 | 0.204 |

| Producer experience (std.) | −0.087 | 0.116 | −0.090* | 0.032 | −0.068 | 0.227 | −0.020 | 0.188 |

| Past producer–director collaborations (std.) | 0.021 | 0.815 | 0.015 | 0.818 | 0.018 | 0.836 | 0.003 | 0.822 |

| Main cast’s comm. reputation (std). | 0.124 | 0.151 | −0.006 | 0.909 | 0.125 | 0.139 | −0.001 | 0.909 |

| Cast size (std.) | −0.008 | 0.904 | −0.058 | 0.158 | 0.004 | 0.948 | −0.013 | 0.247 |

| Film subsidies (dummy) | 0.177 | 0.244 | 0.651*** | 0.000 | 0.034 | 0.829 | 0.143+ | 0.052 |

|

|

||||||||

| Director artistic reputation (std.) | −0.062 | 0.795 | 0.521** | 0.004 | −0.176 | 0.470 | 0.114+ | 0.077 |

| Producer artistic reputation (std.) | −0.427* | 0.044 | −0.217 | 0.167 | −0.380+ | 0.083 | −0.048 | 0.234 |

| Director commercial reputation (std.) | 0.516+ | 0.055 | 0.870*** | 0.000 | 0.326 | 0.214 | 0.190+ | 0.076 |

| Producer commercial reputation (std.) | 0.822** | 0.004 | 0.862*** | 0.000 | 0.633* | 0.027 | 0.189+ | 0.075 |

|

|

||||||||

| Script endorsement (std.) | 0.219* | 0.041 | 0.219* | 0.041 | ||||

N = 235; +p <0.10; *p <0.05; **p <0.01; ***p <0.001 (two-tailed test); std. = standardized coefficients.

Acknowledgements

The authors would like to thank the journal editors, Renate Meyer and Jörg Sydow, and the three anonymous reviewers for their constructive guidance. The authors are grateful for the feedback received at the Academy of Management Conference (2016) and at the Reputation Symposium (2016) of Oxford University Centre for Corporate Reputation; in particular they would like to thank David Deephouse and Daniel Gamache. The authors are grateful to Giovanni Cardillo, Michele Piazzai, Simone Ferriani, Deniz Maden, Salvatore Torrisi, Tao Wang, Alexander Alexiev and all the scholars who participated in the paper’s presentation at the Amsterdam Business School. This study has been made possible with the help of film experts and investors, who gave important advice about the mechanisms underlying the film industry. In particular, the authors are grateful to Iole Maria Giannattasio (Mibact – Italian Directorate General for Cinema), Alberto Baldini and Luca Giordano (BNL Paribas), Andrea Cirla (Good Films), Paolo Capurro and Fabio Bollini (Banca Popolare di Sondrio), Andrea Graciotti (Rainbow Spa), Michele Fasano (Sattva Film), Nicola Giuliano (Indigo Film), Stefano Massenzi (Lucky Red) and Valerio Vago (Banca Popolare di Vicenza). Finally, the authors would like to thank John Dodds for proofreading.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.