Abstract

Building on a historical case study on the first two stock exchanges to adopt the now globally dominant for-profit organizational form, the Stockholm Stock Exchange in 1993 and the Helsinki Stock Exchange in 1995, we argue that interaction among socially proximate peers contributes to pioneering organizational form adoption within an industry, particularly when such forms are introduced by established organizations. Peer interaction can induce a search for technically efficient organizational forms through the sharing of collective experiences, the establishment of collective assumptions, and a joint search for solutions. Together, these factors contribute to the legitimization of novel organizational forms in the local setting before the adoption of the first instantiation of those forms. We propose a context-sensitive multilevel model of peer-interaction-induced pioneering organizational form adoption that considers shared macro environmental drivers, idiosyncratic local environmental drivers, and peer interaction as central social mediators between the two.

Keywords

Introduction

Which organizations are more likely to be first, i.e. pioneers, in adopting an organizational form within an industry? Extant research tends to emphasize institutional entrepreneurs (e.g. Greenwood & Suddaby, 2006; Tracey, Phillips, & Jarvis, 2011) or actors from the periphery (e.g. Leblebici, Salancik, Copay, & King, 1991) as pioneers of new ways of organizing. However, past studies have focused overwhelmingly on pioneering within a single country with a distinctive economic and institutional setting. While, in comparative studies, organizations from different geographical markets tend to be treated independently from one another (Butzbach, 2016; Djelic & Ainamo, 1999; Maurice, Sorge, & Warner, 1980; Morgan & Quack, 2005). Recently, there have been calls in both comparative institutionalism (Hotho & Saka-Helmhout, 2017) and institutional theory (Furnari, 2016) to focus on interdependencies between distinct institutional environments. While there are empirical studies on interaction mechanisms within national institutional settings (e.g. Bridwell-Mitchell, 2016), there have been few empirical studies on interaction mechanisms between organizations located in distinct institutional environments. This is surprising, as interaction among organizations across markets is common, and such interaction can be an important source of institutional change (Lawrence, Hardy, & Phillips, 2002). In this paper, we study pioneering organizational form adoption within an industry globally. We focus on organizational renewal by established organizations in the highly institutionalized industry of stock exchanges by studying the world’s first two for-profit stock exchanges.

We argue that peer interaction—established interaction practices and processes among geographically and socially proximate peers that are similar in size, have existing ties with each other, and have similar positions in the industry—is a previously unidentified contributor to pioneering organizational form adoption, particularly when new forms are introduced to an industry by established organizations. Such organizations are highly embedded in their institutional environment and tend to conform to institutional expectations, which implies that they are stable (Scott, 1994; Seo & Creed, 2002). Nevertheless, even highly embedded organizations continuously evolve with their environment (Tsoukas & Chia, 2002) and, from time to time, experience substantial environmental misfit, which causes a need for organizational renewal. However, when there are no blueprints for organizing in the new environment within the industry that could be adopted, organizations have to search more broadly to find alternative ways of organizing to regain fit and legitimize the new way of organizing. Thus, we ask the following question: How does peer interaction contribute to pioneering organizational form adoption by established organizations?

To answer this question, we conduct an analytically structured history study (Rowlinson, Hassard, & Decker, 2014) on the Stockholm Stock Exchange (SSE) and the Helsinki Stock Exchange (HSE), the world’s first and second stock exchanges to adopt the for-profit organizational form, in 1993 and 1995, respectively, during a turbulent period of technological and regulatory change. We employ a novel approach in which all sources are digitized, organized, and analysed within a relational database. Thus, our study fulfils the dual requirement of historical veracity and conceptual rigor required by historical organization studies (Maclean, Harvey, & Clegg, 2016).

We draw on comparative institutionalism, with specific attention to the ‘interrelationships between societal institutions and collective organizing and its outcomes’ (Hotho & Saka-Helmhout, 2017, p. 648). In varieties of capitalism research, Nordic countries are categorized as coordinated market economies, in which firms are encouraged to coordinate and collaborate with other firms and key stakeholders (Hall & Soskice, 2001). Similarly, in national business systems research, Nordic countries are often categorized as having collaborative business systems (Whitley, 1994, 2000). More recently, Nordic countries have been identified as having a distinct inclusive business system, characterized by low state involvement, high trust, and significant coordination and collaboration across economic actors (Hotho, 2014). Thus, peer interaction across national borders as an enabling mechanism of institutional change can be expected to be especially prevalent in the Nordic context.

Our study makes two contributions. First, by exposing peer interaction as a previously unidentified process contributing to pioneering organizational form adoption within an industry, we extend institutional theory research on new organizational forms (Greenwood & Suddaby, 2006; Leblebici et al., 1991; Maguire, Hardy, & Lawrence, 2004; Tracey et al., 2011). In addition to being a channel for the diffusion of novel ways of organizing (Guler, Guillén, & Macpherson, 2002; K. Lee & Pennings, 2002; Strang & Soule, 1998), interaction among peers can be an engine of search for technically efficient organizational forms and can pre-legitimize such forms; i.e. it can legitimize an organizational form before the first instantiation of that form, thus lowering the barriers to pioneering adoption (Haveman & Rao, 1997).

Second, we analyse the environmental context at multiple levels (Hotho & Saka-Helmhout, 2017; Lewin, Long, & Carroll, 1999; Lewin & Volberda, 1999). Instead of treating this context as unique to each case, we analyse it at three levels, enabling us to theorize how the macro and local environments interact and influence intraorganizational decision-making. The macro environment is shared by a majority of organizations in the global industry, and the local environment is idiosyncratic to each case. In between, there is a level of context shared by a subset of the population, i.e. socially proximate peers. Peer interaction occurs at this intermediate level, where the macro and local environments interact to influence the nature and content of peer interaction. Local settings are not independent of each other but are shaped by the macro environment through peer interaction. Peer processes can function as an updating mechanism influencing convergence and divergence across various local environments (Nadkarni & Narayanan, 2007). Thus, we contribute to the call for more sensitivity to society-specific institutional arrangements in organizational theory and, particularly, interdependencies across distinct institutional environments (Deeg & Jackson, 2007; Furnari, 2016; Hall & Soskice, 2001; Hotho & Saka-Helmhout, 2017; Tempel & Walgenbach, 2007).

Theoretical Background

The focus of pioneering organizational form adoption has mainly been on institutional entrepreneurs and the structural positions of actors as a source of change (Battilana, Leca, & Boxenbaum, 2009). For example, the core–periphery positions of actors have received significant attention, with most studies concluding that new activities emerge from the periphery due to peripheral actors being disadvantaged by prevailing institutional orders and less aware of institutional expectations (e.g. Kraatz & Moore, 2002; Leblebici et al., 1991). Other studies show that elite actors in core positions of an industry initiate change due to their prestige, which enables them to legitimize new organizational forms (Greenwood & Suddaby, 2006; Sherer & Lee, 2002). Less attention has been paid to organizational forms introduced by nonelite established organizations. Such organizations are well aware of institutional expectations and do not enjoy the prestige of elite actors, which limits their ability to become pioneers and legitimize new ways of organizing.

Other studies have emphasized the role of actors who are positioned between social domains (Powell & Sandholtz, 2012; Tracey et al., 2011) or who can leverage a dual insider–outsider role (Nigam, Sackett, & Golden, 2022) as a source of change. These studies suggest a substantial role for individual actors who are capable of overcoming institutional constraints, drawing elements from one domain, and introducing them into another.

In another stream of the literature, the focus is on interactions among actors as a source of institutional change and new practices. Lawrence and colleagues (2002) propose interorganizational collaboration as an important source of institutional change, especially collaboration characterized by high involvement among organizations and embeddedness in the broader interorganizational network. High involvement increases the number of innovations, and embeddedness increases the probability of these innovations diffusing to the broader network (Lawrence et al., 2002). This adds a finer-grained understanding of the core–periphery distinction, with institutional embeddedness being both a constraining and an enabling factor in institutional change.

We suggest that interaction among peer organizations can play a role in pioneering organizational form adoption within an industry. Due to organizations’ limited ability to scan their entire environment (Levinthal & March, 1993), firms tend to mimic the behaviour of similar organizations (DiMaggio & Powell, 1983) that are geographically and socially proximate, similar in size, have existing ties with each other, and similar industry positions (Guler et al., 2002; K. Lee & Pennings, 2002; Strang & Soule, 1998), especially under conditions of market uncertainty and increased competition (Bothner, 2003). Peers have been shown to be a channel for diffusion of technology (Bothner, 2003), production technology (Greve & Seidel, 2015), practices (Guler et al., 2002), and organizational forms (K. Lee & Pennings, 2002). However, interactions among peer organizations prior to pioneering adoption have received less attention in the organizational theory literature, even though innovations tend to arise from collaboration (Lawrence et al., 2002).

Interaction among peer organizations can facilitate the development of new solutions to shared problems and alleviate technical and legitimacy concerns related to these solutions, as the new solutions receive approval from multiple organizations that consider each other peers. Therefore, peer interaction can lower the barriers to the initial adoption and subsequent diffusion of a new solution. In public policy, such theorizing has occurred at the national level in the form of transnational problem solving, where public policy isomorphism is a result of the joint development of solutions to common problems and the subsequent national adoption of the solutions rather than of peer imitation (Holzinger & Knill, 2005).

Similarly, in the organizational theory literature, relational spaces allow actors to protect themselves from institutional discipline and experiment with new solutions (Zietsma & Lawrence, 2010). These spaces have been studied within both organizational (Kellogg, 2009) and field contexts (Zietsma & Lawrence, 2010). Furnari (2014) argues that interstitial spaces—‘small-scale settings where individuals positioned in different fields interact occasionally and informally around common activities to which they devote limited time’—can induce the genesis of new practices. This contrasts with Lawrence et al.’s (2002) notion of high involvement, as the occasional and informal nature of these spaces for interaction allows actors to disengage from institutional constraints and experiment with new practices. Lawrence et al. (2002) argue that embeddedness in the interorganizational network enables the diffusion of innovations, whereas Furnari (2014) argues that successful interaction rituals and catalyst actors enable new practices to stick. There is still a lack of understanding of the spaces of interaction and, especially, their role in pioneering organizational form adoption.

By focusing on peer interaction, we draw attention to the distinct institutional environments of peers as well as the shared external environment (Hotho & Saka-Helmhout, 2017; Tempel & Walgenbach, 2007). Extant studies have not taken seriously enough the various levels of the environmental context experienced by organizations or the way that they interact to shape organizational change processes. Instead, past studies have treated contexts as unique to the focal case, for example, focusing on the adoption of new organizational forms in a single country (Boxenbaum & Battilana, 2005; Greenwood & Suddaby, 2006), isolated from the global, historically embedded context of institutionalized organizations.

The few studies that have considered multiple institutional settings have concluded that distinctive institutional and environmental conditions create unique contingencies and, thus, explain why the adoption of organizational forms takes place in particular ways and at different points in time (e.g. Butzbach, 2016; Casper, 2000; Djelic & Ainamo, 1999). However, these local settings can be and often are influenced by higher-level environments and institutions. Thus, we cannot treat the environmental context as unique to each case. Instead, we need studies that account for the different levels of the environment experienced by organizations and for how these levels are shared by different sets of organizations in the population.

Research Setting

We focus our analysis on the SSE and the HSE using the theoretical sampling strategy (Eisenhardt & Graebner, 2007). Our analysis is based on the fact that these are the first two stock exchanges in the world to adopt the for-profit organizational form, making them suitable for developing theory regarding pioneering organizational form adoption.

From nonprofit to for-profit stock exchanges

Stock exchanges were both shaped by and a central type of institution in the process of financialization, i.e. ‘the increasing role of financial motives, financial markets, financial actors and financial institutions’ (Epstein, 2005, p. 3) in the global economy over the past 40 years (Petry, 2020). Countries around the world adopted policies that enabled international competition for capital and increased the role of capital markets in the global economy and in everyday life (Davis & Kim, 2015; Polillo & Guillén, 2005). This process led to the demutualization of various mutual financial institutions, such as building societies (Klimecki & Willmott, 2009) and stock exchanges. Technological development enabled electronic trading and, together with reduced capital controls, created international competition among exchanges. The growing role of capital markets made stock exchanges a valuable asset that could be unlocked by exchange members with incorporation (Gorham & Singh, 2009; Zanotti, 2012).

Before the late 1990s, most stock exchanges were organized as member-owned cooperatives with brokers and listed companies as members, with one vote per member in decision-making (Azzam, 2010; R. Lee, 2010). Most exchanges enjoyed monopolistic power within their domestic market. Zanotti (2012) provides three reasons that could explain why the cooperative form was prevalent before the 1990s. First, cooperatives, e.g. insurance companies and savings banks, were historically very common. Second, the members of stock exchanges, mostly brokers, were a very homogeneous group with similar interests, which is essential for the long-run success of cooperatives (Hansmann, 1999). Finally, the stock exchange business requires relationship investments between the exchange and listing companies, for which the cooperative form is appropriate.

In 1993, the Stockholm Stock Exchange was incorporated as the world’s first stock exchange, followed by the Helsinki Stock Exchange in 1995. By 2002 and 2011, 63% and 83% of the world’s stock exchanges, respectively, had demutualized (Angulo, Slimane, & Alidou, 2013; Azzam, 2010).

The Stockholm Stock Exchange

The SSE was founded in 1863 and functioned as a de facto monopoly until the 1979 law made it a de jure monopoly. With this law, the organizational form also changed into a hybrid form, where the majority of the board was appointed by the government rather than by interests acting at the exchange. Including the chair and vice-chair of the board, six of the board members were appointed by the government, while the Central Bank, the Swedish Chamber of Commerce, and an industry association had one representative each. The trading members of the exchange had only two representatives, one representing banks and one representing trading members. As most of the board members did not have experience with financial markets, the CEO had a strong position in decision-making.

The demutualization of the exchange was not legally possible until the 1979 law was replaced with a new law in 1992, which removed the SSE monopoly on trading with most financial instruments. Discussions of how the SSE should be run in a deregulated market started in 1990, and the SSE board decided to incorporate the exchange. In 1993, the SSE was incorporated, and key stakeholders (banks, brokers, the state, and listed companies) were given equity in the newly formed company.

The Helsinki Stock Exchange

The HSE was founded in 1912, and until 1984, its legal status was unclear. However, in 1984, the legal form of the HSE was clarified and changed to a cooperative organizational form. The state did not play a role in the governance of the HSE, and before the Securities Market Act of 1989 the HSE was strongly self-regulating. The above act made the HSE subject to official supervision.

Before the demutualization in 1995, the HSE was owned by its members, who were securities dealers (brokers and banks), commercial and industrial organizations (e.g. the Federation of Employers), and listed companies. Membership was mandatory for securities dealers who wished to trade on the HSE and voluntary for listed companies until 1991. Each member had one vote until 1991, when the participation share structure changed. Each securities dealer received four votes, and membership became mandatory for all listed companies, with one vote each. The HSE was incorporated in November 1995 with the following breakdown of share capital: 40% issuers, 34% brokerage houses, 23% banks, and 3% others. However, the shares became transferable only after November 1996.

Methodology

Data

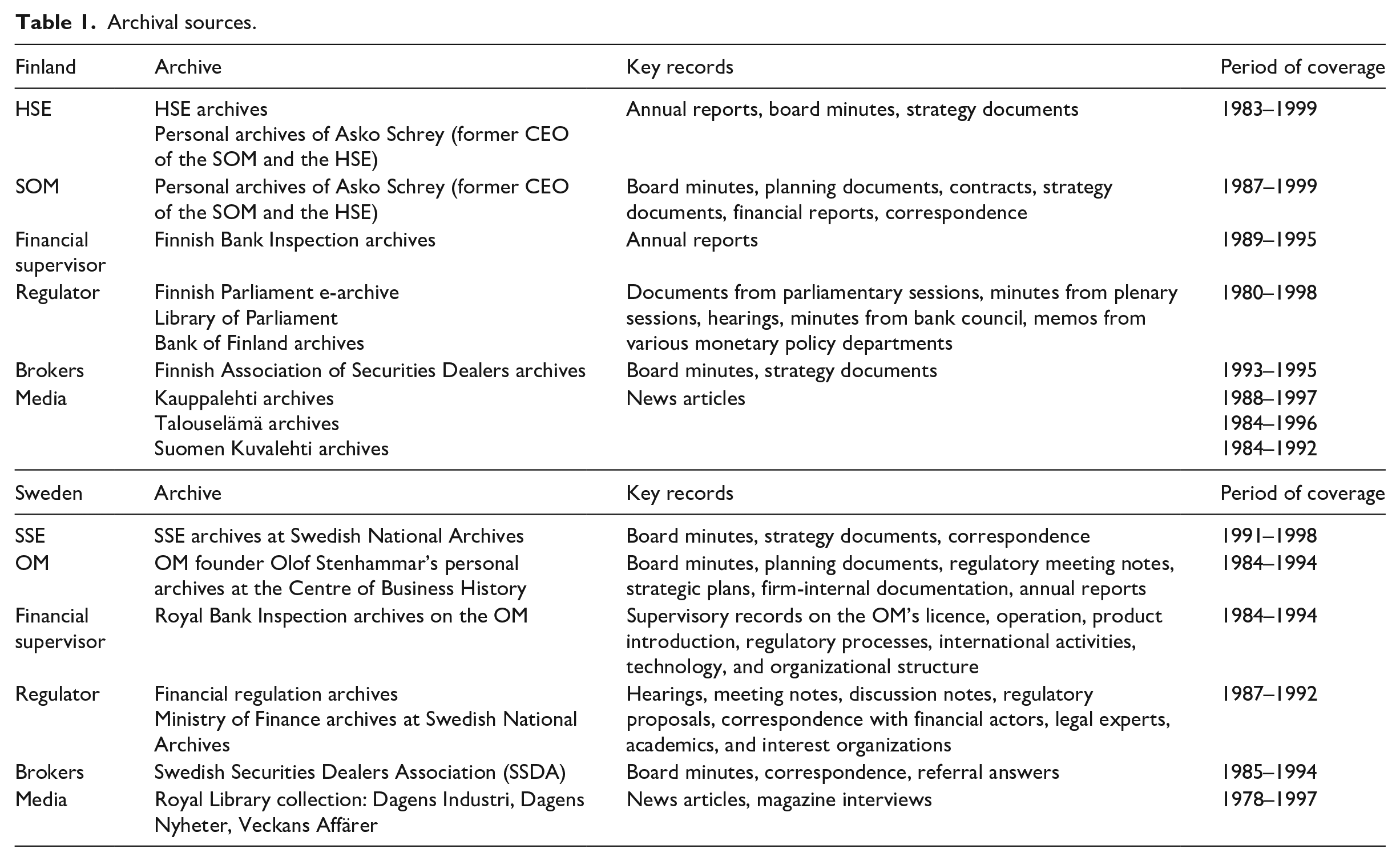

This study is based on an extensive set of archival sources and interviews. We collected a large set of unique archival sources from 1984 to 1998, including documents from both countries’ stock exchanges, entrant option exchanges, financial supervisory organizations, securities dealers associations (SDAs), regulatory agencies, and the media (Table 1). This set of more than 3000 documents consists of board minutes and their attachments, annual reports, strategy documents, correspondence, regulatory documents, and news articles. The archival material was photographed, digitized using optical character recognition (OCR) software, coded, and stored using a relational database, where actors, organizations, times, and incidents were coded with their relations to each other.

Archival sources.

Subsequently, we conducted 19 interviews per case with top-level members such as CEOs, directors, board members, and the minister of finance, representing different stakeholders such as stock exchanges, entrant options exchanges, SDAs, financial supervisors, and the government. The relational database and the archival data were used to enhance the rigor of our informed interviews. The database enabled us to easily find all documents related to an interviewee, either within the content or coded into the database metadata. This allowed us to bring key source material and timelines to the interviews, bring informants back to specific instances and events and enhance their recollection of the events surrounding a specific decision or their recollection of the circumstances and people present at a specific moment in time. All interview questions and the transcribed interviews were input into the database with diverse relational data and incident coded, adding further richness to the data.

Analysis

Our analytical process is a combination of a historically informed process study method in the foreground and an interpretative approach in the background to fully capture the complex dynamics among organizations and their changing environments. Process analysis with extensive incident coding is our main method (Langley, 1999). This approach is a combined realist history approach, where archival data enable us to place the findings into historical context (Vaara & Lamberg, 2016), and interpretative method, where oral history interviews expose how actors interpreted the process (Suddaby & Greenwood, 2009). The interpretative approach is important to fully untangle the dynamics of how stakeholders became sensitive to the need for change. The historical approach is important for gaining a contemporary view of how the organizational misfit and experimentation accumulated.

Both cases were analysed using our relational database by incident coding them separately in multiple rounds and structuring incidents into events and higher-level categories (Van de Ven & Poole, 1990). First, based on the existing understanding of the reasons for global stock exchange demutualization (e.g. Aggarwal, 2002; Fleckner, 2006; Gorham & Singh, 2009; Zanotti, 2012), we used competition, international issues, organization, regulation and supervision, and technology as sensitizing categories in our initial coding (Glaser & Strauss, 1967; Van de Ven & Poole, 1990). Then, the cases were analysed first within-case, and timelines were constructed to analyse the cases separately (Langley, 1999). These timelines were then compared to search for cross-case patterns and differences (Eisenhardt, 1989).

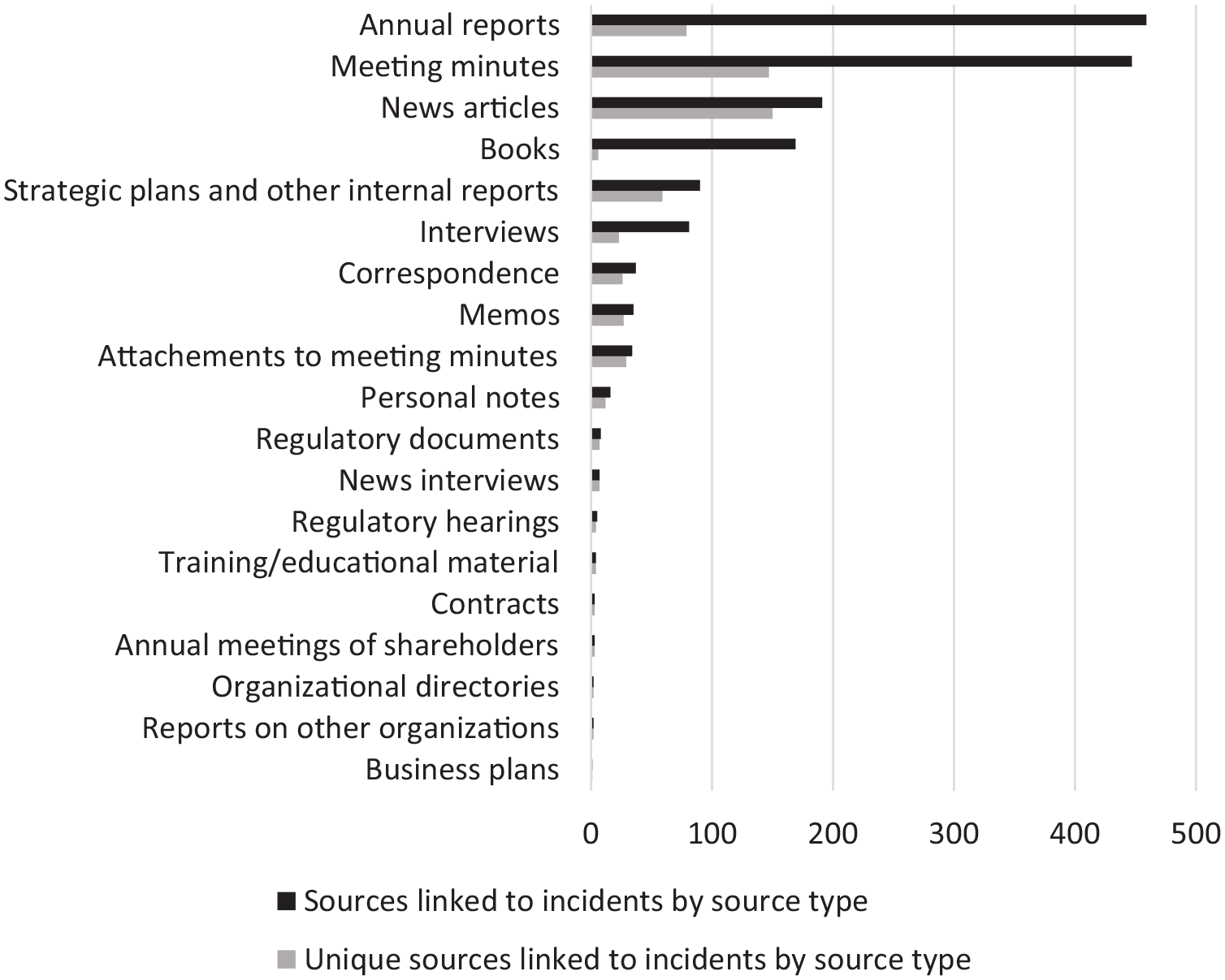

At this point, the prominent role of the interaction between the two stock exchanges became apparent. Therefore, we conducted new rounds of incident coding focusing on interactions among Nordic stock exchanges and their key stakeholders. This extensive incident coding generated 668 incidents for the Swedish case and 376 incidents for the Finnish case, of which 78 were related to Nordic interaction. There are 1594 sources and 591 unique sources linked to the incidents. We leveraged a diverse set of sources consisting of primary social documents (e.g. meeting minutes, reports, and memos), narrative texts (e.g. annual reports, news articles), and secondary sources (e.g. books) (Rowlinson et al., 2014) (Figure 1).

Sources linked to incidents by source type.

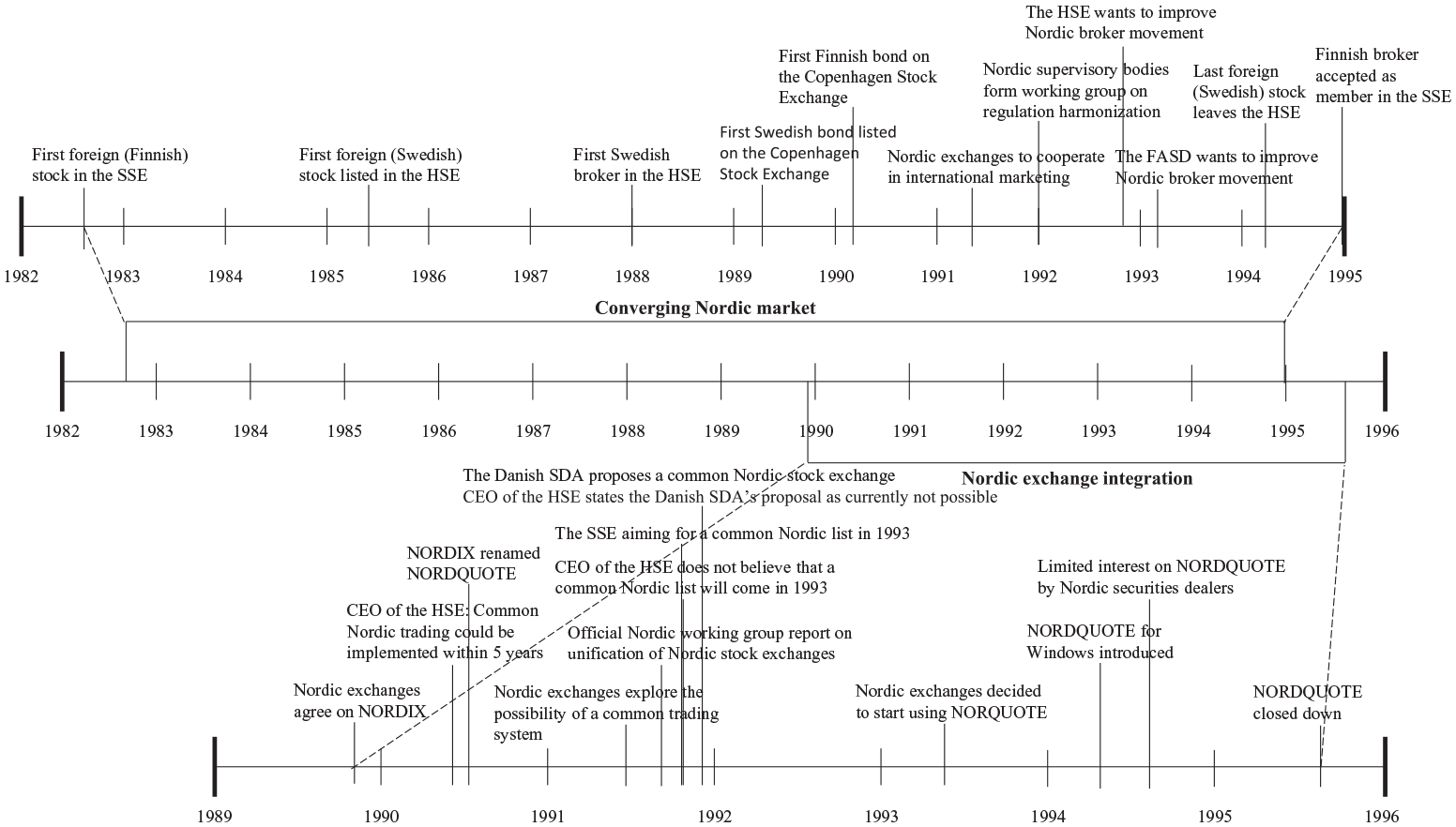

Then, we constructed a timeline of Nordic interactions and analysed it in comparison to the previous timelines depicting the changing landscape of local and international competition, regulation, technology, and organizational form. We discovered that various stock exchange stakeholders had many established interaction practices with their peers across Nordic countries. Additionally, the Nordic stock exchange market was converging, and various joint solutions were proposed by different stakeholders to address the radical changes in the technological and regulatory environment (Figure 2). We gradually progressed to a higher level of abstraction in our analysis through iterations between theory and data to produce the following findings. In the findings, we enclose in brackets references to incidents listed in the accompanying online supplementary file.

Nordic interaction timeline.

Findings

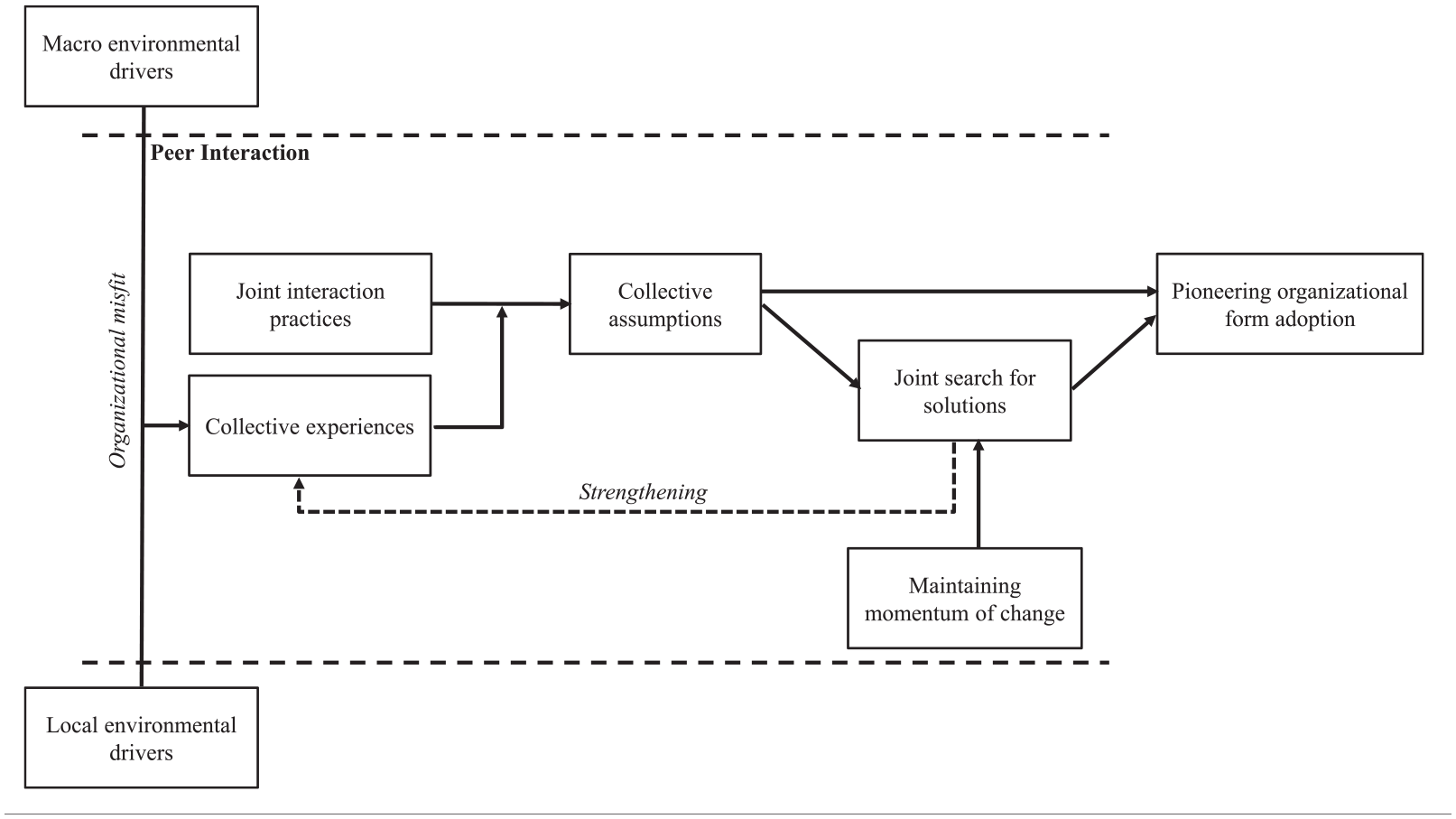

The findings section is structured as follows. We start by discussing macro and local environmental drivers that created the misfit between the nonprofit organizational form and the environment. Next, we present the antecedents—established interaction practices and collective experiences—to construct the collective assumptions among peers in the stock exchange industry. Then, we describe how the stock exchanges jointly searched for solutions to this organizational misfit based on the collective assumptions and how the change momentum was maintained despite multiple failures. Finally, we describe how the two stock exchanges refined their collective assumptions, leading to the pioneering adoption of the for-profit stock exchange organizational form (Figure 3).

Peer-interaction-induced pioneering organizational form adoption.

Contextual drivers of organizational misfit

Macro environmental drivers

We identify two macro environmental drivers that had the most impact on the operating environments of the HSE and the SSE—the deregulation of capital controls and technological development. These were certainly not unique to the Finnish and Swedish contexts but influenced all stock exchanges during the same period.

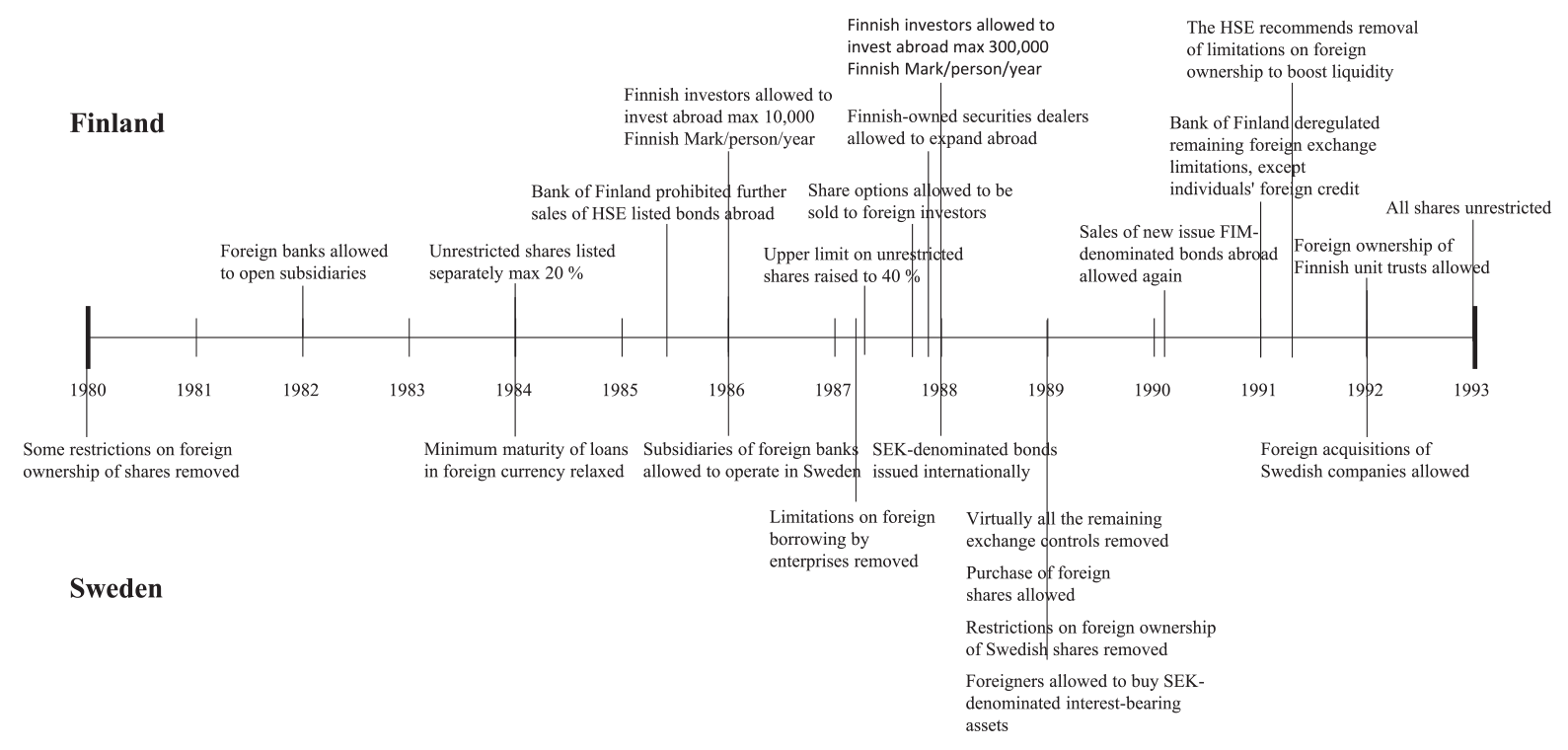

The removal of capital controls was part of the larger global financial regulation liberalization trend (Kaminsky & Schmukler, 2003). This process occurred at different paces and through different paths in Finland and Sweden (Figure 4). However, the outcome was similar in the two countries (Englund & Vihriälä, 2003). The most important aspects of such financial regulation liberalization for the stock market were the deregulation of foreign ownership restrictions and foreign exchange restrictions.

Comparative cross-border financial regulation timeline.

These changes were seen as inevitable by the exchanges themselves, by stakeholders, and by governmental organizations. Some changes were not beneficial for all stakeholder groups. The removal of capital controls allowed foreign brokers to trade on the exchange, which transformed them from customers to competitors for local brokers. There were also attempts to prevent deregulation that mainly succeeded only in postponing specific stages of the deregulation process. Although the stock exchanges considered the regulatory shift a measure dictated from above by the central bank or legislators, the central banks, in turn, considered the adopted changes reactions to the changing global environment.

Technological readiness for electronic trading systems (ETSs) that allow remote trading was achieved in the late 1970s. The Cincinnati Stock Exchange implemented the first ETS in 1978, followed by stock and options exchanges in the 1980s (Ernkvist, 2015). Both the SSE and the HSE visited and were visited by the Cincinnati Stock Exchange in 1986 to learn about the ETS [1627; 1628; 1630; 2150; 2151] and were among the first stock exchanges in the world to implement ETSs. Both exchanges decided to develop their own ETSs [453; 736], started to test their systems with a subset of shares in 1989 [389; 847], and closed their trading floors in 1990 [400; 693]. In addition to ETSs, there were other systems that together digitalized the stock market: trading information systems, book-entry systems, and automatic clearing and settlement systems, implemented in the overall exchange industry either within the stock exchange organization or by a dedicated clearing and settlement organization [363; 398; 459].

Although national regulation or the rules of the exchange restricted foreign brokers (brokers with no permanent office in the country) from joining the exchange until the EU-level Investment Service Directive came into force in 1993 among EU member states [409], Finland and Sweden joined the EU only in 1995. The above restriction was removed in Sweden and Finland in 1995 [2160] and 1996 [441], respectively.

Deregulation of capital controls allowed foreign ownership of shares but also caused capital outflows. ETSs required heavy initial investments, created significant economies of scale and scope, removed physical limitations, and enabled the emergence of options exchanges based on ETSs right from the founding. Additionally, the coevolution of these two external drivers enabled direct international competition (i.e. the same products listed on multiple exchanges) and indirect international competition (i.e. different products competing for the same capital).

These changes caused the interest of various stakeholders to diverge. First, the removal of capital controls caused an outflow of capital, which the management and listed companies aimed to offset by attracting foreign capital by allowing remote brokers to join the exchange [769]. This was strongly opposed by brokers, as trade from foreign brokers through local brokers was a significant business [1058; 2154]. Second, small brokers saw themselves paying disproportionately large costs for technological investments [446]. The increasing heterogeneity among stakeholders hampered decision-making, whereas the increasing competition required more flexibility from the exchanges. Thus, the misfit between the current organizational form of the stock exchanges and the regulatory and technological environment gradually increased. This divergence in stakeholder interests was further amplified by local environmental drivers.

Local environmental drivers

Two local environmental drivers intensified the organizational misfit of the stock exchanges caused by the macro environmental drivers. These drivers were the economic crisis of the early 1990s and changes in the financial transaction tax, which amplified tensions among stock exchange stakeholders.

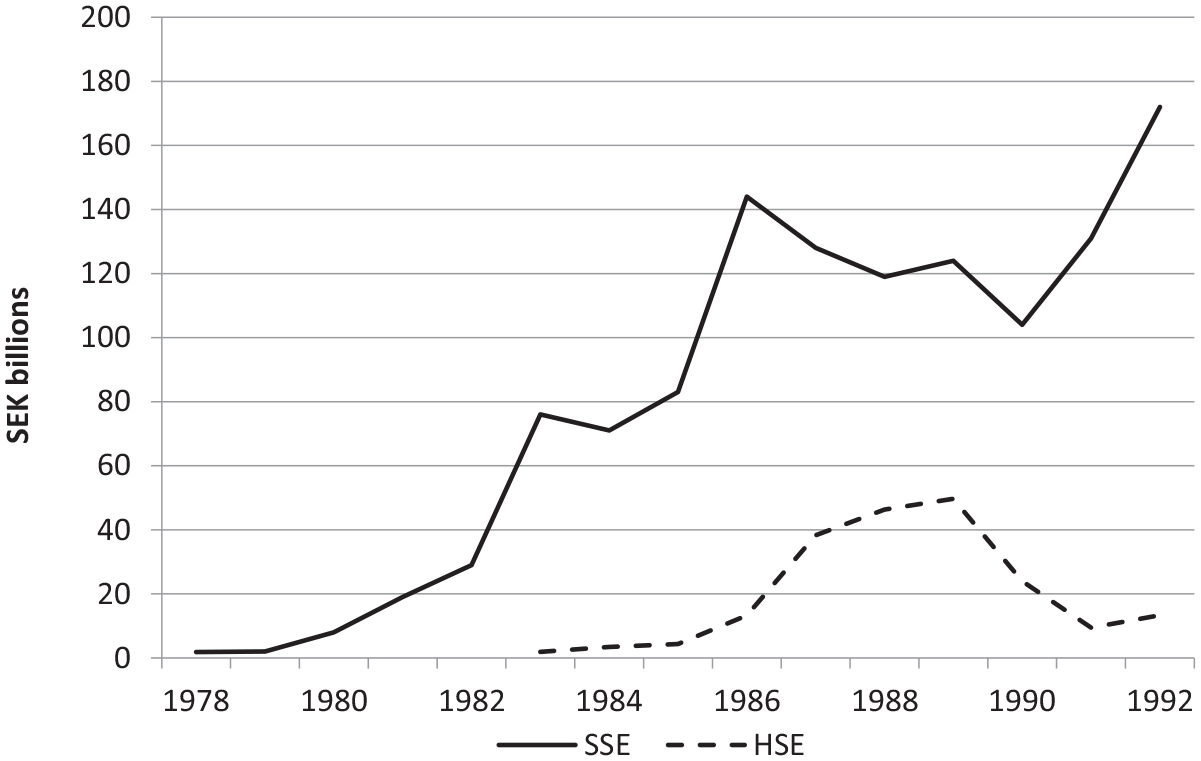

The economic crisis started in 1990 in Finland, which had 12% GDP growth in 1989 and only 5.9% in 1990, with the later quarters recording negative growth percentages quarter on quarter. The effect on the stock market can be seen in the HSE’s total market capitalization of shares, which dropped approximately 30%, and nominal share turnover, which dropped approximately 50% for two consecutive years (Figure 5). This severe crisis combined with heavy investments in electronic trading and clearing systems in the second half of the 1980s and early 1990s raised the debt of the HSE from zero to over 50% of earnings. The HSE, being a cooperative, was required to distribute most of the surplus collected from trading fees back to brokers in the form of lower fees. Therefore, investments had to be financed with loans from financial institutions.

Share turnover in Swedish krona (Finnish mark converted using annual averages).

In 1990, the HSE reacted to this with a financial restructuring in which the participation fee for brokers was raised from FIM 10,000 to FIM 600,000. Membership became mandatory for listed companies, with a participation fee of FIM 150,000 and an annual listing fee [446; 447; 946; 947; 961]. This restructuring also changed the governance structure of the exchange, as a significant portion of the voting rights shifted from brokers to listed companies. This amplified the divergent interests of various stakeholders caused by the macro environment drivers.

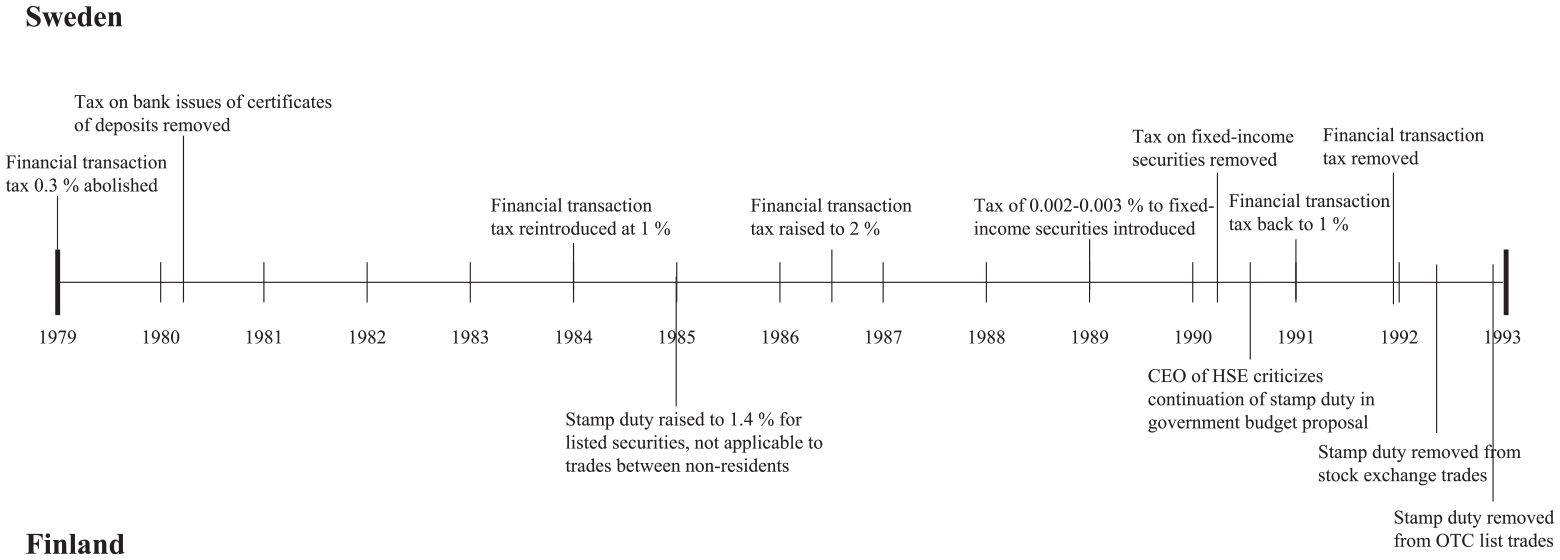

The financial transaction tax in Sweden had a similar financial pressure effect. The SSE faced a significant drop in trading volume during 1986–90 when the financial transaction tax was doubled to 2% in 1986 [2156], lowered back to 1% in 1991 [2158], and removed at the end of 1991 [2157] (Figure 6). During this time, more than 50% of the trading volume moved to the Stock Exchange Automated Quotation (SEAQ) system in the London Stock Exchange (Figure 5). Finland also had a financial transaction tax called the stamp duty, but it was not applied to trades between nonresidents [366; 880]. Some Finnish traders took advantage of the possibility of trading Finnish shares in the SEAQ to avoid the stamp duty, but the impact on volume was significantly less than that in the SSE. Management still pushed for the removal of stamp duty to stimulate trading and fend off international competition [931].

Comparative financial transaction tax timeline.

Despite this dramatic shift combined with the economic downturn at the beginning of the 1990s, the SSE did not need to raise additional capital from members due to its more diverse sources of income, including exchange fees and the selling of exchange information. Additionally, the board with limited broker representation allowed the SSE to use revenue more freely to invest in technology than the HSE board. However, the fear of trading moving abroad to financial centres such as London was discussed continuously, even after the removal of the tax.

These factors had an impact on both exchanges, but the scale of their impact varied significantly in the two markets. The banking crisis and financial depression were more severe for Finland due to the collapse of the Soviet Union in 1991 (Englund & Vihriälä, 2003), whereas the Swedish financial transaction tax had a direct impact on trading volume in the SSE. The divergence of interests among brokers of different sizes was more visible in the HSE. Nevertheless, allowing remote brokers to access the SSE trading system led to much criticism from brokers toward management [2154].

Antecedents of collective assumptions

We categorize the SSE and the HSE as peers that are relatively similar in size in relation to the global population of stock exchanges, are interconnected with cross-listings and broker firms operating in both exchanges, and are geographically proximate (K. Lee & Pennings, 2002). We find multiple established interaction practices among different actors in the industry, many of which were at the Nordic level and included Denmark and Norway. Additionally, the HSE and the SSE shared collective experiences of organizational misfit driven by macro and local environmental factors. We theorize that as organizational misfit increased, interaction practices were employed to share the experiences. Based on the similarity of these experiences, collective assumptions on the future development of the stock exchange industry emerged.

Joint interaction practices

Joint interaction practices are repeated patterns of interaction among actors from peer organizations that can be both formal and regularly held or informal and irregularly held. We find many such practices among the Nordic exchange organizations. Since 1972, annual meetings have been held among the Nordic stock exchanges [645]. Nordic SDAs also had official biannual meetings among themselves [1041]. These meetings were at the level of the CEO and chair of the board. In addition to these official meetings, there were many irregular events, such as stock exchange visits [287; 2050; 2065]. The meetings focused on the exchange of ideas, experiences, and industry trends and on the finding of common ways of operating [1004]. However, this exchange of ideas became more cautious as competition increased among the Nordic exchanges.

Interaction practices are maintained even when the market environment of the exchange industry is stable. When there is turbulence in the market environment that causes organizational misfit, the established interaction practices can be employed to find solutions to regain fit. Thus, these established interaction practices can be considered dormant resources that can be activated when needed.

Likewise, intergovernmental collaboration is well established in the Nordic countries. For example, the interparliamentary Nordic Council was established in 1971. Nordic collaboration is taken for granted and can be observed at all levels of society. Such collaboration occurs not only within but also across the state and industry levels. The work to harmonize financial regulations across Nordic countries and the official working group regarding the unification of Nordic exchanges are good examples of this cross-level collaboration among the regulators and managers of exchanges from different Nordic countries [976; 977; 1009; 2056].

Collective experiences during environmental change

The other antecedent to constructing collective assumptions between the HSE and the SSE is the collective experiences shared by the stock exchanges and the interconnectedness of the markets. We define collective experiences as experience of market environment changes that have similar consequences in different markets. In our cases, the macro environmental changes had similar effects on the development of both local and international competition in the two stock exchange markets.

The stock exchange industries across the Nordic countries and especially between Finland and Sweden converged starting in the early 1980s, with an increasing number of cross-border activities. The first foreign share to be listed in the SSE was the Finnish KONE company in 1982 [721]. The first foreign share to be listed in the HSE was the Swedish AGA AB in 1985 [882]. Thus, there was investor interest across Nordic stock markets, but rigidities, such as regulations and broker restrictions, hindered direct investments. Additionally, cross-listing is a signal of emerging international stock exchange competition. Nordic supervisory bodies aimed to harmonize regulations among Nordic countries [1009], and different stakeholders pushed to improve broker movement among these countries [997; 1015].

The most significant collective experience shared by the HSE and the SSE is the emergence of for-profit option exchanges in the two markets. Technological development enabled the creation of derivative exchanges based solely on ETSs. The Swedish OM (Optionsmäklarna)—which was founded in 1983 [33] and started options trading in mid-1985 [74]—was both the first commercially successful digital options exchange and a pioneer of for-profit exchanges (Ernkvist, 2015).

In August 1986, the HSE started investigating the potential of the futures and options market in Finland [357; 369]. However, a bloc of HSE member banks and brokers initiated a second options exchange initiative while continuing to participate in the investigation of the HSE-led initiative [1631]. This second initiative later became the Finnish Options Market (SOM, Suomen Optiomeklarit) [372]. The motivation behind the founding of the SOM was the competition between two banking blocs and the great potential value of a for-profit options exchange [1631].

Both Finnish options exchange projects visited the OM within a month of each other to investigate the possibility of using the OM system in Finland [1631]. Finally, in September 1987, the SOM was founded, and the OM became a shareholder, with an 11% equity stake in the beginning [372]. This launched the international expansion efforts of the OM. In addition to the OM and SOM, there were multiple other option exchange projects, but none of them became significant in the market [374; 381; 963; 1442].

The two exchanges also faced similar international competition, as the London Stock Exchange’s SEAQ system had started to trade major HSE and SSE stocks [1002; 2159]. The SSE faced a significant drop in trading volume during 1986–90 due to the financial transaction tax. In Finland, in the first half of 1992, 25% of transactions of Finnish shares were traded in London. By December 1992, after the removal of the stamp duty on stock exchange trades in May, this figure dropped to 9% [788; 993], which shows that local traders sought the least expensive trading venue.

Constructing collective assumptions

As the external environment of the HSE and the SSE changed, the established joint interaction practices were employed to discuss collective experiences of these changes. As a result, the exchanges formed collective assumptions about how changes in the external environment would impact the stock exchange industry. We define these collective assumptions as jointly constructed interpretations among peer organizations regarding how changes in the external environment would impact their industry and organization in the future (Nadkarni & Narayanan, 2007).

With changes in the technological and regulatory environment, two collective expectations about the future development of the stock exchange industry emerged between the HSE and SSE. Furthermore, these collective expectations led to common aims to survive and sustain performance within the evolving industry boundaries and rules of competition. First, the shift from physical to electronic securities trading and the deregulation of capital controls created significant network effects, making large exchanges even larger as geographical boundaries diminished. This was due to large exchanges having better liquidity and attracting more investors and more listing companies, thus creating a virtuous cycle. The Nordic exchanges feared that this would lead to the stock exchange industry becoming dominated by a few global exchanges and to national exchanges becoming extinct [2057].

Second, the shift to ETSs required significant upfront investments in technology and changing the cost structure from variable to fixed costs. Before electronic trading, fixed costs were low, consisting mainly of the physical stock exchange buildings and administrative staff. With ETSs, the marginal cost of an additional trade is minimal. The trading volume became central to keeping trading costs low, which made stock exchanges more sensitive to slumps in trading volume than they had been in the pre-electronic trading era.

These two collective assumptions led to three strategy frames for survival. First, as the restrictions on investing in foreign securities and on foreigners buying Finnish and Swedish shares were lifted [346; 378; 407; 965; 985; 987] and electronic trading removed geographical boundaries in trading shares to balance the outflow of investments [356; 906; 911; 923; 950; 980], the SSE and the HSE needed to attract foreign investors to trade in local shares [769; 961; 964; 2054].

Second, the exchanges had to keep the trading volume of Finnish and Swedish shares in the home market by preventing local investors from changing trading venues and attracting foreign investors to trade shares in their respective home exchanges [1002]. As only a few large companies in the Nordic markets attracted international interest, it was critical to keep the trading of these large companies in their home market [2054; 2147]. The trading volume of large listed companies keeps national exchanges alive to serve smaller listed companies, which have less liquidity and attract less international interest.

Third, the change in the cost structure with the adoption of ETSs meant that volume could be increased by incorporating additional products such as options and bonds into the trading system [294; 386; 673; 702; 2065]. Although bonds were already traded on the stock exchanges to some extent (especially in Copenhagen [927; 928; 2059; 2066]), most of the trading occurred over the counter, with banks as intermediaries. Options, in turn, were traded mostly in dedicated options exchanges. Technically integrating additional products became simple in ETSs, but managing different stakeholder interests proved to be very challenging.

Joint search and the momentum of change

Based on their collective assumptions, both the HSE and the SSE searched for internal solutions that were aligned with the collective strategy frames. The HSE changed its ownership structure [446], collaborated with its local option exchange competitor, the SOM, to integrate trading systems [973; 1001], and eventually merged with the SOM [1440]. The SSE focused on extending its product scope with pushes into bonds and options to increase scale and efficiency [266; 288; 294; 702; 799; 2065]. Most interestingly, Nordic exchanges engaged in the joint search for solutions, including various configurations of trading system and organizational integration. This joint search produced multiple solution proposals that failed at various stages. Regardless of these failures, the momentum of change was maintained due to pressure from multiple stakeholders, and the Nordic exchanges continued to develop NORDQUOTE throughout the period.

Joint search for solutions

As collective assumptions were formed among peers, the established interaction practices were employed in the joint search for solutions. This joint search occurred at both the state and industry levels. Different Nordic actors proposed various ways of organizing to increase scale and to better compete with international exchanges.

In 1989, the Nordic exchanges signed an agreement to develop a common stock information system [854; 2063] (NORDIX, which later became NORDQUOTE [765]), and a working group was formed to harmonize Nordic exchange regulation to win back investors from abroad [976; 977], especially since the largest Nordic publicly traded companies have higher trading volume in London than in their respective home exchanges. The Nordic exchanges considered NORDQUOTE an important tool to regain their competitiveness. These developments were jointly deployed with marketing efforts geared toward international investors, where the Nordic markets were marketed as a single market [976]. Although NORDQUOTE was the only project that was implemented and was in use beginning in 1994 [1047; 1073], it was halted in 1995 due to a lack of interest among brokers [1052; 1099].

The joint search was especially active in 1991 during the financial crisis. The Danish SDA’s proposal for a common Nordic exchange [958], which was strongly opposed by the Swedes and Norwegians [1660; 2055], and the formation of an official working group to merge the Nordic exchanges [977] represented deep-integration solutions. The SSE’s push for a Nordic share list with the largest companies from each Nordic country and the proposal to provide members of one Nordic exchange with the opportunity to trade in other Nordic exchanges to improve liquidity represented lighter-integration solutions [2054]. These propositions converged mostly into reorganizations for scale and sharing of technology. Despite various proposals for more integration of stock exchange organizations, nothing concrete was realized until the incorporation of the exchanges due to disagreement on the form of deeper integration among the stock exchanges and their stakeholders.

Maintaining the momentum of change

The proposals emerging from the joint search for solutions were unsuccessful. The main problems were the diverging interests between small and large brokers and between brokers and stock exchange management. Then, stock exchange management, especially between Copenhagen and Stockholm, fought to become the financial centre of the Nordic countries. However, the Nordic exchanges maintained their interaction practices and continued to use them in the joint search for solutions [2059; 2061; 2074].

We identify two forces that helped maintain the momentum of the joint search for solutions. First, various external actors pushed the exchanges to work toward integration, and this discussion spread to local business media outlets. These external actors were already active in the early 1980s in initiating Nordic stock exchange collaboration. In 1980–1983, Swedish private stock investors’ representatives [642], the Nordic union of industrial companies [657], and even the largest Swedish business newspaper, Dagens Industri [2050], publicly endorsed the idea of a Nordic exchange. In the late 1980s, major Nordic industrialists in the influential European Roundtable of Industrialists pushed for Nordic integration beyond that in the European Community—one part of this integration involved creating a Nordic stock exchange [2068]. Later, in the early 1990s, the Danish industry was active in promoting the idea of a Nordic stock exchange [2149].

Second, NORDQUOTE, the project to build an information exchange system among Nordic stock exchanges, started in 1989 [854; 2063], and the development of this system continued until 1995 [1099]. NORDQUOTE was supported by the management of different Nordic exchanges, the system was often discussed in joint interaction events, and many proposals that resulted from the joint search were extensions of this system. For example, the Nordiclist proposal, which involved having a share list of major Nordic companies, was planned as part of NORDQUOTE [2054]. However, SDAs in Sweden, Finland, and Norway never supported the system and prevented the development of additional features that would have made the Nordic stock exchanges more integrated [1052; 2058]. Nevertheless, having an ongoing project helped maintain momentum in the joint search for solutions.

Pioneering organizational form adoption

The stock exchanges took several steps to adjust their collective assumptions about the changing environment. They adopted ETSs [389; 847], opened the exchanges for remote brokers [1058; 2154], added new products to the exchanges [294; 386; 673; 702; 2065], and the HSE and SOM integrated their ETSs [412; 973; 1001]. However, there were further steps, mainly local and cross-border organizational integration, that were overwhelmingly unsuccessful. This further strengthened the collectively experienced misfit of the Nordic stock exchanges. In particular, the increasingly divergent interests of different stakeholders were challenging to reconcile. This gradually led to the collective assumption that the nonprofit form did not suit their perceptions about the changing environment.

The similar for-profit option exchanges in both countries that were efficient and highly profitable provided suitable organizational guidelines for the changing environment. In particular, as the same stakeholders, such as banks and brokers, operated at both stock and options exchanges, the discrepancies between the stock and options exchanges were made visible to the management and boards of the stock exchanges. In Finland, the banks and brokers that were stakeholders in both the HSE and SOM were actively pushing for incorporation of the HSE and merger with the SOM, whereas the management of the HSE and the representatives of listed companies were passive but not against incorporation. In the HSE, when all main stakeholders were activated, the incorporation process itself was very smooth, with unanimous decision-making [432].

The ability to raise funding through retained earnings and equity for further investment in technology was a key benefit of the for-profit organizational form [428]. This was especially important for the HSE, as the financial crisis showed that the cooperative form did not respond well to financial shocks. In the SSE, throughout the late 1980s, there was a heavy push for incorporation by the CEO of the SSE to gain more flexibility in decision-making. This was opposed by some of the left-wing political representatives on the board [740]. However, with the law that removed the SSE’s monopoly status in 1992 [250; 261], the resistance of these political representatives was overcome, and the incorporation process moved forward [1671; 1674].

The for-profit form also enabled stock exchange mergers. Stock exchange stakeholders saw that the separation of ownership and membership solved multiple issues. Conflicts between small and large members were no longer an issue, as ownership was no longer based on equal voting rights among members but rather share ownership. Conflicts between brokers and management were eliminated, as the stock exchange’s mission changed from minimizing trading costs and, thus, maximizing benefits for members to maximizing shareholder value. In the era of local and international stock exchange competition, trading costs are kept low through price competition. Stock exchange stakeholders believed that decision-making became more efficient [2161].

The SSE and the HSE were incorporated in 1993 and 1995, respectively, to improve the efficiency of decision-making [1091; 2162]. Additionally, the HSE’s merger with the SOM and internationalization were considered reasons to incorporate [469; 471; 1439]. HSE management considered incorporation a necessary step toward mergers and internationalization to increase scale and improve competitiveness with foreign exchanges.

Discussion

The main contribution of our study is to expose peer interaction as a previously unidentified factor of renewal and legitimation that contributes to pioneering organizational form adoption, particularly when new-to-the-industry organizational forms are introduced by established organizations. We propose that in addition to being a channel for diffusion (DiMaggio & Powell, 1983; K. Lee & Pennings, 2002), interaction among peers can be an engine of pioneering organizational form adoption. Established interaction practices, which are common across many sectors in the Nordic inclusive business system (Hotho, 2014), can be considered dormant enabling resources for organizational renewal that can be activated during times of organizational misfit.

The organizations in our case study employed established joint interaction practices to share how they experienced changes in the technological and regulatory environment, which resulted in collective assumptions. These were a result of the enactment of the macro and local environmental drivers through peer interaction. These collective assumptions amplified the perceived need for organizational renewal (Nadkarni & Narayanan, 2007). For example, the collective assumption that the global stock exchange industry would become dominated by a few global stock exchanges induced fear among stock exchange stakeholders and created an urgency to scale up, which contributed to the pioneering organizational form adoption. Retrospectively, we know that national exchanges are still commonplace, and stock exchange companies have consolidated to operate multiple national stock exchanges. Today, the stock exchanges in Copenhagen, Helsinki, and Stockholm are operated by Nasdaq, whereas the Oslo Stock Exchange is owned by Euronext.

Pioneering organizational form adoption is more likely to occur among organizations that have peers with which to interact, for two reasons. First, due to the lack of a benchmark within the industry for organizing in the changing environment and the collective experience of organizational misfit, peers can form collective assumptions and jointly search for an organizational form that would fit their assumptions. Second, interaction among peers can legitimize the organizational form in the local context before its first adoption. As the first adopter is convinced that there will be followers, the barriers to becoming the pioneer become lower. Thus, the first reason focuses on finding a technically efficient solution, and the second reason focuses on establishing legitimacy for the new-to-the-industry organizational form (Haveman & Rao, 1997).

The extant institutional literature has presented evidence of pioneering organizational form adoption by both peripheral (Leblebici et al., 1991; Maguire et al., 2004) and elite (Greenwood & Suddaby, 2006) actors. We argue that the role of peers is more important for established actors than for peripheral actors because the latter have fewer legitimacy constraints (Haveman & Rao, 1997; Leblebici et al., 1991). However, peer interaction might also be an important engine of pioneering organizational form adoption for elite actors. For example, Greenwood and Suddaby (2006) studied a group of elite actors in the accounting industry that introduced a new organizational form and described the frequent interactions among these peers. Thus, we put forth the following proposition.

We emphasize the importance of peers in pioneering adoption when there are no benchmark cases within the industry. The first three for-profit stock exchanges—Stockholm (1993), Helsinki (1995), and Copenhagen (1996)—were all peers. They were then followed by Amsterdam (1997), the Borsa Italiana (1997), Australia (1998), Singapore (1999), and Athens (1999) (Aggarwal, 2002; Zanotti, 2012). Thus, after initial adoption, diffusion continued through isomorphic forces (DiMaggio & Powell, 1983; Guler et al., 2002; Strang & Soule, 1998; Weber, Davis, & Lounsbury, 2009). However, there is a need to revisit studies that have found peers to be a channel for the mimetic diffusion of organizational forms (e.g. K. Lee & Pennings, 2002) and analyse whether peer interaction was present among the first adopters. If that is the case, then we should observe initial diffusion among peers and then a decrease in the role of peers as the new organizational form becomes more prevalent. Thus, we put forth the following proposition.

The established interaction practices that were maintained during stable periods and employed for the joint search during turbulent periods support the idea of experimental spaces, in which actors can protect themselves from institutional discipline and experiment with new solutions (Zietsma & Lawrence, 2010). Our findings also support Furnari’s (2014) proposition that although spaces for interaction facilitate the generation of new ideas, there is a need for successful interaction rituals and catalysts to maintain the momentum of change.

However, the interaction practices that we observe differ from interstitial and experimentation spaces (Furnari, 2014; Zietsma & Lawrence, 2010) in an important aspect: they are not only spaces for collaborative experimentation (Lawrence et al., 2002). Many of the solutions, although they included peers, were generated independently from peers. The interaction practices that we observe were spaces for information exchange and the sharing of experiences, where through repeated contacts, collective assumptions evolved (Nadkarni & Narayanan, 2007; Powell, Packalen, & Whittington, 2012). With the changing global environment and adoption of different organizational aspects, such as ETSs, the information and experiences shared in these spaces converged around collective assumptions. Stock exchange stakeholders became a community with a common fate (Powell et al., 2012). These spaces for interaction are a structural element for a subset of actors in the global industry that adds an element of structural vulnerability during industry reconfiguration, which makes these peer organizations more poised to pioneering organizational form adoption.

We also contribute to the calls to bring the environment back to the study of organizational form adoption by analysing the environmental context at multiple levels (Hotho & Saka-Helmhout, 2017). Comparative institutionalism research has mainly treated the institutional environment in a static way, focusing on differences between countries (Deeg & Jackson, 2007). Few studies have considered interaction mechanisms between actors across countries (Schrage & Rasche, 2022). We show that peer interaction can be a mechanism for updating the institutional environment and can induce institutional convergence across countries. As such, peer interaction can become a comparative institutional advantage in times of technological change (Deeg & Jackson, 2007).

Instead of treating the environmental context as unique to each case, we propose a multilevel model of pioneering organizational form adoption. This model allows us to consider both the macro environmental drivers shared by stock exchanges around the world and the local environmental drivers unique to each exchange. Between these two levels, there is a third level, where the environmental context is shared by a group of socially proximate communities of actors, in our case, the exchanges as a subset of the global stock exchange population. Within this intermediate peer level, established joint interaction practices serve as dormant enabling resources for organizational renewal that can be activated during periods of environmental turbulence. Our methodological approach allows us to distinguish the levels of contextual factors that contribute to the pioneering organizational form adoption and, specifically, expose the interconnected role of the three levels in creating organizational misfit and their effect on peer interaction.

Our model of peer-interaction-induced pioneering organizational form adoption integrates a coevolutionary perspective and takes a historically embedded view (Lewin et al., 1999; Lewin & Volberda, 1999). Thus, it allows researchers to take a longitudinal perspective on industry reconfiguration and study the highly complex and, many times, long processes of pioneering organizational form adoption. In our case of stock exchanges, the pioneering adoption of the for-profit stock exchange organizational form is only one organizational episode in a continuous organizational change process (Tsoukas & Chia, 2002). This episode of for-profit stock exchange emergence was preceded by other significant organizational changes, such as the adoption of ETSs and the removal of trading floors. The organizational change process continues today with the ongoing consolidation of stock exchange companies.

We only study peer interaction in the Nordic stock exchange context, the members of which have multiple similarities that make them peers (Hotho, 2014; Kristensen & Lilja, 2011). However, we cannot analyse the prevalence of peer interaction among countries belonging to other business systems or across different business systems (Hall & Soskice, 2001; Hotho & Saka-Helmhout, 2017; Whitley, 1994). Thus, there is a need for further investigation of which characteristics, e.g. institutional, cultural, and geographical proximity, are most important for peer interaction to emerge. Additionally, we looked at exchanges that initially operated in nationally demarcated markets, which might lower the barriers to peer interaction, as peers do not form an immediate competitive threat. Further elaboration is needed to understand the dynamics of peer interaction when peers operate in the same market, making them competitors.

Supplemental Material

sj-xlsx-1-oss-10.1177_01708406211024570 – Supplemental material for Peer Interaction and Pioneering Organizational Form Adoption: A tale of the first two for-profit stock exchanges

Supplemental material, sj-xlsx-1-oss-10.1177_01708406211024570 for Peer Interaction and Pioneering Organizational Form Adoption: A tale of the first two for-profit stock exchanges by Zeerim Cheung, Robin Gustafsson and Rasmus Nykvist in Organization Studies

Footnotes

Acknowledgements

We are grateful for the helpful suggestions provided by Jasper Hotho and the three anonymous reviewers. We also want to thank the DIGIHIST consortium, Robert Demir, Mirko Ernkvist, Santi Furnari, and everyone who gave us valuable feedback at various conferences and seminars.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work received partial support from the Niilo Helander Foundation, The Finnish Science Foundation for Technology and Economics KAUTE, The Finnish Foundation for Share Promotion, the Marianne and Marcus Wallenberg Foundation, and the Digital Disruption of Industry project that the Strategic Research Council [grant 292889] of Finland funded.

Supplemental material

Supplemental material for this article is available online.

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.