Abstract

Against the backdrop of spirited public and academic discourse about women’s low visibility in corporate leadership positions, we examine board gender diversity’s influence on strategic change in firms. Viewing gender as an institutionalized system of social beliefs, the article makes two related arguments. First, it contends that because of gender status difference and bias, more gender diversity will result in less strategic change as a board’s decisions begin to follow the stance of a smaller but relatively more influential ‘boy’s club’. Second, it contends that should a board have a female chair as opposed to a male chair, a recession in the shadow of gender stereotypes will reverse board gender diversity’s negative effect on strategic change. Instrumental variables analysis of data from Fortune 500 firms supports the theory. We discuss the study’s contributions and implications.

Introduction

[In meetings,] I often observed that at times women were invisible to men, who looked right through you as though you weren’t there.

In the wake of vigorous social discourse on gender equality, recent attention in the management and organization literature has centred on gender-linked reward and opportunity disparities in the corporate world and on the rarity of women in leadership positions (e.g. Cook & Glass, 2014; Joshi, Son, & Roh, 2015; Padavic, Ely, & Reid, 2020; Ryan et al., 2016). Another intriguing issue, however, namely, the impact the presence of more women in leadership positions has on organizations’ strategy (e.g. Chen, Crossland, & Huang, 2016; Triana, Miller, & Trzebiatowski, 2013), has not received the attention it deserves despite its important implications for both research and practice. Against this backdrop, our study examines whether board gender diversity, that is, variety in the gender composition of directors on the corporate board of a company, affects the company’s level of strategic change. In the field of strategy, strategic change is a crucial variable reflecting managerial effort to maintain a firm–environment fit. In line with earlier research (Finkelstein & Hambrick, 1990; Golden & Zajac, 2001), we define it as an alteration in the overall pattern of resource allocation, such that a firm’s strategic profile with respect to markets, technology, R&D, and organizational and capital structure changes. Accordingly, we view the absence of strategic change as being indicative of persistence with the status quo (Haynes & Hillman 2010; Zhang & Rajagopalan, 2010).

Past research has often used the framework of resource dependence theory (RDT) to argue that board gender diversity ought to be of benefit since men and women bring different cognitive, experiential and relational resources to the firm (e.g. Hillman, Shropshire, & Cannella, 2007). RDT maintains that firms depend on the external environment for resources essential for survival (Pfeffer & Salancik, 1978). Board gender diversity is, therefore, advocated because it can presumably enable access to a larger set of essential resources via ties with different external constituencies (cf. Adams & Funk, 2012; Nielsen & Huse, 2010a; Triana et al., 2013). While the RDT framework is ideal for building normative theory that proposes women to be a resource of value, this article seeks to build theory that accounts for a social reality that has held back women from leadership positions, and continues to do so. To this end, we employ a sociological lens to explore board gender diversity’s effect on strategic change, conceptualizing gender as an institutionalized system of social beliefs and practices that finds expression in male and female stereotypes (Ridgeway, 2011; Ridgeway & Smith-Lovin, 1999). This construal of gender recognizes that social systems harbour generalized collective views about the capabilities and suitability of men and women for different roles in the social structure (Connell, 1987; Ridgeway, 2011), allowing theory-building that is tethered to the temporal and cultural context of gender-linked beliefs and expectations prevalent in society.

Institutionalized beliefs and expectations are important because they affect gender behaviours in social settings, thus being consequential for the influence companies’ female directors can have on strategy. Across social systems, gender stereotypes have pervasively projected men as being better equipped for leadership roles (Eagly & Karau, 2002; Ridgeway, 2011). This social reality, we maintain, will generally limit female directors’ influence on strategy (cf. Heath, Flynn, & Holt, 2014), unless there are circumstances that negate the stereotypes. This study, accordingly, builds and tests two related arguments. Drawing on the status characteristics theory (e.g. Berger, Cohen, & Zelditch, 1972) and the role congruity theory of prejudice against female leaders (e.g. Eagly & Karau, 2002), it argues first that an increase in board gender diversity will tend to be associated with a decrease in strategic change. Next, seemingly contrariwise, it argues that should a woman be the board chair, there will be a reversal in the negative relationship between board gender diversity and strategic change. The article presents these arguments in their fullness and finds support for them in panel data from United States Fortune 500 firms.

The article contributes new theory about board gender diversity and strategic change that recognizes the possibility of role-linked gender status difference and bias in society. It is widely accepted that women have to contend with invisible glass ceilings, glass cliffs and glass walls erected by social bias (Adams & Funk, 2012; Bruckmüller, Ryan, Rink, & Haslam, 2014; Cook & Glass, 2014; Ryan et al., 2016), which often operate to box women into particular roles and to limit the opportunities available to them. Still, when it comes to theorizing the effects of female leaders (e.g. CEOs, top management team executives and board directors), there has not yet been sufficient exploration of the possible influence of social bias. While from a normative perspective we would want the presence of female directors to result in advantages for a company, our study suggests that the benefits of board gender diversity may only materialize when gender stereotypes do not cast a shadow on the space female directors have to voice opinions, initiate ideas and gain recognition on boards. The study is one of the first to offer this perspective, and to identify the important role a female board chair can play in this regard.

As the influence of board chairs on strategic decisions and outcomes is an under-studied subject (Gabrielsson, Huse, & Minichilli, 2007; Kanadli, Torchia, & Gabaldon, 2018), we also contribute to research on board chairs. The study indicates that a female board chair may be one important catalyst – along with, for example, the use of gender-neutral language for leadership role descriptions (e.g. Schein, 2001) – for unlocking board gender diversity’s potential. More generally, the study expands the theoretical bandwidth of board gender diversity research with a view to stimulate further inquiry that can inform practice and policy concerning an issue of great social and organizational significance.

Research Background

Board gender diversity, strategic decisions and outcomes

While the effect of board gender diversity on firms’ performance has been studied often (for a meta-analysis, see Post & Byron, 2015), there is limited literature on board gender diversity’s influence on strategic change in firms, or on strategy more broadly (e.g. Chen et al., 2016; Nielsen & Huse, 2010a, 2010b). A good understanding of whether and how board gender diversity affects strategic change is important, however. Boards have a fiduciary duty to safeguard the interests of shareholders and stakeholders by monitoring and advising the executive function (Bainbridge, 1993; Fama, 1980). In this context, they are expected to effect strategic change in firms by questioning the status quo (Golden & Zajac, 2001; Johnson, Daly, & Elstrand, 1996). A better appreciation of board gender diversity’s impact on strategic change could, thus, be of value to strategy and corporate governance researchers (e.g. Fiss & Zajac, 2006; Westphal & Fredrickson, 2001) studying strategic change. Moreover, as strategic change tends to affect performance (Kraatz & Zajac, 2001; Mitchell, Shaver, & Yeung, 1992), theory and evidence concerning board gender diversity’s influence on strategic change could provide insights into the board gender diversity–performance relationship. Past studies have reported mixed results for this relationship (see e.g. Carter, D’Souza, Simkins, & Simpson, 2010; Dobbin & Jung, 2011; Erhardt, Werbel, & Shrader, 2003; He & Huang, 2011); but strategic change being a more proximal outcome than performance, board gender diversity’s effect on it should be subject to less noise than its effect on the latter and thus relatively easier to establish (cf. Helfat & Martin, 2015; Hillman et al., 2007).

In the literature, one can find normative as well as positive theorizing regarding board gender diversity’s effect. The first approach is more conspicuous and posits relationships that reflect an ideal world, as it presumably ought to be; the second approach, which is attentive to the social reality of gender-linked inequalities, is at a relatively embryonic stage. Normative theory starts with the assumption that men and women differ, and embody different organizationally valuable cognitive, experiential and relational resources (Nielsen & Huse, 2010a; Singh, Terjesen, & Vinnicombe, 2008). It then draws on the framework of the resource dependence theory to advance a business case for board gender diversity, maintaining that it ought to bring benefits. Hillman and her colleagues (2007), for example, combine ‘resource dependence with work-group-level diversity theories and findings to identify potential benefits of female representation on boards of directors’ (Hillman et al., 2007, p. 942) (see also Adams & Funk, 2012; Campbell & Mínguez-Vera, 2008; Daily & Dalton, 2003). Such work suggests that because male and female directors differ in bringing unique and complementary understandings, perspectives, temperaments and relational ties to the external world, board gender diversity should lead to more informed strategic decisions that keep a fit between the firm and its changing environment (Hillman, Cannella, & Harris, 2002; Miller & Triana, 2009).

Contrastingly, two other studies have appeared that start with the premise that female directors differ from male directors, but which posit a more complex picture of board gender diversity’s effect on strategy. In the first one, Triana and her colleagues (2013) draw on diversity research at the work-group level to theorize that male and female directors’ different perspectives will, in fact, slow down decision-making and thus strategic change. Empirically, this study finds that board gender diversity has a negative relationship with strategic change. It also finds the relationship to be most negative when there is both low performance and female directors have more power (structural, expert, or prestige based). This three-way effect is ascribed to the greater potential for disagreements between male and female directors when the latter are more powerful (Triana et al., 2013). In the second study, Chen and his co-authors (2016) draw instead on social identity theory to argue that male–female differences will make decision-making more contentious, and thus more thorough, resulting in fewer and smaller acquisitions. Our research complements these studies by examining the effect of board gender diversity and board chair’s gender through the lens of social bias and directors’ relative influence in boardrooms, in place of the lens that male–female differences produce factious decision-making. In doing so, we take the path of positive theorizing.

As opposed to normative theory’s focus on models that express what ought to be, positive theory in the social sciences lays emphasis on modelling what is (Friedman, 1953; Seth & Thomas, 1994). In the context of board gender diversity research, positive theory is mindful of the what is in taking into account the existence of social bias that has historically kept women from corporate leadership roles (Blommaert & van den Brink, 2020; Fitzsimmons & Callan, 2016) and at the present time appears to limit their influence in boardrooms. Nielsen and Huse’s (2010b) work shows, for example, that regardless of the singular experiences, style, temperament and value orientation female directors might bring to the board, ‘the perception of women directors as non-equal board members can significantly reduce the potential for women to contribute to board decision-making’ (Nielsen & Huse, 2010b, p. 17). They find this to be the case in data pertaining to Norwegian firms. The same what is is also reported by descriptive research in the US (Heath et al., 2014). Along the same lines, other emerging work suggests that gender status difference between male and female directors may keep the latter from having influence on strategy (Bermiss, Burris, & Harrison, 2019; Ma & Stern, 2019).

This article takes forward the positive theory stream of research – it is mindful of the reality of social bias, viewing gender as a social construct that encapsulates society’s beliefs about roles that are suitable for men and women and society’s expectations regarding men and women being able to execute specific roles effectively (Connell, 1987; Eagly, 1987; Ridgeway, 2011; Ridgeway & Smith-Lovin, 1999). These beliefs and expectations undergird gender stereotypes, which work to assign men and women to either a higher or a lower gender status category vis-a-vis specific roles, and which guide people’s behaviours in social settings (Fiske, Cuddy, Glick, & Xu, 2002; Ridgeway, 2001; Ridgeway & Correll, 2004; Wagner & Berger, 1997). In many areas of social activity, including in the corporate world, the assignment of women to the lower status category has held back and slowed women’s ascent to leadership positions (e.g. Ridgeway, 2011; Ryan & Haslam, 2007). While normative theory has paid limited attention to gender status difference on boards, inasmuch as male and female directors do not come together and interact in a social vacuum, recognizing this difference would seem important for theorizing the results of board gender diversity.

Indeed, because gender stereotypes and status difference can be expected to be especially salient at the higher management levels from which women have tended to be excluded (Eagly & Karau, 2002; Randel, 2002), theory that assumes male and female directors to be equals on boards and/or extends work-group level diversity research directly to the board level, may not find confirmation. Below, we build our arguments by drawing on two theories that have contributed greatly to the understanding of gender dynamics and gender-related outcomes in organizations: the status characteristics theory (SCT) and the role congruity theory of prejudice against female leaders (RCT) (Eagly & Karau, 2002; Heilman, Block, & Martell, 1995; Pugh & Wahrman, 1983; Rudman & Phelan, 2008). SCT and RCT provide complementary insights for theorizing the influence of board gender diversity on strategic change and how this relationship is likely to be moderated by the board chair’s gender.

Board gender diversity and directors’ relative influence

Board directors monitor their firm’s state of affairs, question the executive management, and offer advice and counsel to ensure a firm–environment fit (Bosboom, Heyden, & Sidhu, 2019; Haynes & Hillman, 2010). Although being a male or female director should ostensibly be immaterial for executing the directorship role effectively, SCT suggests otherwise. On boards, men belong to the higher-status gender category, having historically been the sole gender category in the directorship role and even today far outnumbering women on mixed-gender boards (Eagly, 1987; Heilman, 2012; Kogut et al., 2014). SCT suggests that in such a setting male directors will be more influential than female directors, inasmuch as their higher status expresses as well as confirms the belief that the wherewithal for effective directorship matches men’s agentic stereotype of being assertive, competitive and dominant, but conflicts with women’s communal stereotype of being caring, nurturing and sympathetic (cf. Ridgeway, 2011; Schein, 1975).

In addition, gender identity being salient in mixed-gender settings (Randel, 2002; Ridgeway & Correll, 2004), SCT indicates that status’s self-fulfilling enactment in line with status-conferring stereotypes (Berger, Fisek, Norman, & Zelditch, 1977; Ridgeway & Correll, 2004) will result in male directors being more assertive, speaking up often, defending their views, and gaining attention; female directors, in contrast, will be less influential by virtue of being more complaisant, cooperative, and willing to listen and be helpful in accordance with the stereotype of being communal (Berger et al., 1972; Lovaglia, Lucas, Rogalin, & Darwin, 2006; Ridgeway, 2001; Ridgeway & Smith-Lovin, 1999). Studies of mixed-gender groups offer compelling evidence for this (Gerber, 1996; Pugh & Wahrman, 1983; Wagner & Berger, 1997). Research also indicates that women are less influential if the saliency of gender status difference is heightened, say, due to minority status or because of affirmative action (Heilman, Block, & Stathatos, 1997; Kanter, 1977). Some have thus drawn the inference that token inclusion of women on boards is the underlying reason for not finding an unequivocal effect of female directors on organizational outcomes (Terjesen, Sealy, & Singh, 2009; Torchia, Calabro, & Huse, 2011).

Male directors’ greater influence on gender-diverse boards is also indicated by studies that show female directors are more likely to sit on the relatively less important committees, such as the public affairs committee (Bilimoria & Piderit 1994; Peterson & Philpot, 2007). A difference in influence is also indicated by the findings of several large surveys and interviews of female leaders in US firms, as reported by Heath and her colleagues (2014). This work highlights that women’s behaviour in meetings filled with domineering personalities is often non-assertive, tending to be facilitative and tentative. The authors also note that women find it difficult to propose and back up their own viewpoint and, generally, ‘have a hard time making their otherwise strong voices heard in meetings, either because they are not speaking loudly enough or because they can’t find a way to break into the conversation at all’ (Heath et al., 2014). Separately, RCT identifies a further psychological mechanism that can suppress female directors’ influence, namely, the bias or prejudice produced by the perceived incongruity between the ‘communal’ stereotype of women and the ‘agentic’ traits effective leaders supposedly have (Eagly & Johnson, 1990; Schein, 1975).

Such bias can erode female directors’ legitimacy by suggesting they are not qualified for the directorship role (Eagly & Karau, 2002; Heilman, 2012). Although female directors can try to counter bias by exhibiting more agentic behaviour, for example, by being more assertive and proactive, studies indicate they are then negatively evaluated and penalized for violating their gender stereotype (Rudman, Moss-Racusin, Phelan, & Nauts, 2012; Rudman & Phelan, 2008). As the fear of backlash disinclines women from becoming stereotype-disconfirming exemplars (Heilman, Wallen, Fuchs, & Tamkins, 2004; Rudman & Fairchild, 2004), female directors may resign themselves to playing a supportive background role that is consistent with their communal stereotype (see also Heath et al., 2014). Although this would mean that a female director has less influence, from a pragmatic, self-interest perspective it would be a rational course of action, in that it could earn positive referrals from peers for future board appointments (cf. Westphal & Stern, 2006, 2007).

Hypotheses

Board gender diversity and strategic change

The preceding discussion underscores that, on average, female directors will be less influential than male directors on gender-diverse boards. This has one non-trivial implication – greater board gender diversity, because of an increase in the proportion of female directors, will also mean a decrease in the number of relatively-more-influential male directors. That is, an attendant byproduct of greater board gender diversity will be a smaller set of male directors with more power over strategy than female directors. As gender identity is salient in mixed-gender settings, it can be anticipated then that the enactment of stereotypes (Berger et al., 1972; Ridgeway & Correll, 2004) and the presence of gender bias (Eagly & Karau, 2002; Heilman, 2012) will result in board discussions and decisions being shaped primarily by a small but dominant ‘boys’ club’. In contrast, when there is less or no board gender diversity, one can expect influence on board discussions and decisions to be distributed across a larger group of male directors.

In light of the above, while it may outwardly seem that decisions will be guided by a richer pool of perspectives when there are both male and female directors on a board (see e.g. Daily & Dalton, 2003; Hillman et al., 2002), actually the case may be otherwise. The dominant influence of fewer male directors can be fateful – decisions are likely to be steered by a smaller pool of people and views, rendering strategy change less probable. That is, with a contraction in the set of people, and thus diversity of thoughts, to guide the board’s agenda, attention and deliberations and to make sense of and interpret the firm’s strategic options, the status quo is less likely to be questioned (cf. Pearce & Zahra, 1992). Indeed, with a smaller group of male directors in control, there is likely to be greater attachment to the strategy in place because of reasons of legacy, past investments, or CEO compensation (Carpenter, 2000; Grossman & Cannella, 2006). This is consistent with the well-accepted finding that, with a few directors, boards are less active in promoting strategic change (Golden & Zajac, 2001). In view of the preceding, we predict an inverse relationship between board gender diversity and strategic change in firms. Formally:

Hypothesis 1: As board gender diversity increases, strategic change in firms will decrease.

Board chair’s gender, board gender diversity and strategic change

SCT, RCT and related empirical evidence suggest that gender status difference and bias on boards is not a constant – it varies subject to the effect of contextual factors ranging from a nation’s culture to personal dispositions (Eagly & Karau, 2002; Lucas, 2003). The factor we examine is the board chair’s gender. We submit that when the incumbent in the board chair’s role is a woman, gender status difference and bias on a board is less likely, and thus one can expect the relationship between board gender diversity and strategic change to be positive. While at first this may appear to run against our thesis above, note that the board chair’s role is different from that of a board director’s role and carries higher status. It is vested with overt power. In performing their duties, board chairs have significant authority as they set the agenda and tone for board meetings and discussions, and establish board routines and procedures (Gabrielsson et al., 2007; Krause, Semadeni, & Withers, 2016). A female chair as the head of a male-majority board is rare, and the single board-chair position on a board stands in contrast to the many board director positions, some of which may be filled simply to satisfy stakeholders, gain legitimacy, or meet regulatory norms (Burgess & Tharenou, 2002). Female incumbency of the chair position is thus likely to make a statement, suggesting a worldview in which gender categories are not relevant for board directorship. Lucas’s (2003) study hints that the visual of a female chair can relay positive information about women’s fitness for board director positions, warding off gender status difference. In the absence of difference, male and female directors should have opportunity to be similarly influential (see also Wagner, Ford, & Ford, 1986).

Adding to the above, Vial, Napier and Brescoll (2016) highlight the salience of leader’s gender, arguing that ‘[l]eader or organizational features that enhance status attributions and/or lower subordinates’ perceptions of power differentials may increase legitimacy for women in leadership roles’ (2016, p. 400). Thus, by disaffirming the stereotype that men are more suited for board directorship, a female chairperson is likely to increase the legitimacy of all female directors on the board; a male chairperson, in contrast, would affirm the stereotype. A female chairperson can, in other words, help disconnect masculine notions of leadership – and, thus, the agentic stereotype – from the board directorship role, with such disassociation having been shown to reduce bias concerning female leaders’ effectiveness (Eagly, Karau, & Makhijani, 1995). In addition, if female chairpersonship functions as a signal that the board directorship role is not masculine, as Eagly and Karau (2002) write, ‘[the role] would be more congruent with the female gender role, and therefore the tendency to view women as less qualified than men should weaken or even disappear’ (p. 577). Moreover, a female chair offers a role model for other female directors on boards. Scholars argue (Hoyt & Murphy, 2016; Terjesen et al., 2009) and studies find that role models decrease women’s fear of being stereotyped negatively, increasing their drive, participation and influence (Latu, Mast, Lammers, & Bombari, 2013; Simon & Hoyt, 2013).

All things considered, thus, the board chair’s gender will matter for the effect of board gender diversity on strategic change. If the board chair is a woman, gender status equality and perceived legitimacy of female directors will mean that they have as much opportunity to influence strategy as male directors. As compared to an all-male board, therefore, on a female-chaired board that has male directors only, strategy making is likely to benefit from the female chair’s distinctive input. On a female-chaired board that is more gender diverse, the say and voice of multiple female directors will result in strategy being informed by a still greater variety of perspectives and understandings. Indeed, on such boards, ideas and views that are uniquely feminine are more likely to find space to enrich deliberations. The preceding implies that on boards with a female chair, the agenda, attention and deliberations of the board are less likely to be controlled by a small clique of male directors. There will thus be greater diversity of thought for making sense of and interpreting the firm’s strategic options. Hence, as issues, events, threats and opportunities surface, the likelihood of the status quo being questioned and, thus, strategic change, can be expected to be greater. We accordingly submit that a female board chair will moderate positively the relationship we had theorized earlier between board gender diversity and strategic change. To test this, we formally propose the following hypothesis:

Hypothesis 2: The negative relationship between board gender diversity and strategic change is conditional on the board chair’s gender, such that the relationship will be moderated positively by a female board chair.

Methods

Sample, data collection and measurement of variables

We used panel data from US Fortune 500 companies for testing the hypotheses. Sampling restrictions were not imposed and we collected data for all years a company was in the Fortune 500 list from 2003 to 2009. While we obtained companies’ financial data from the Compustat database, data on the composition of boards was collected from the ExecuComp and RiskMetrics databases. We furthermore consulted the companies’ annual reports to locate missing data. In all, we were able to collect complete data for a panel of 275 companies, covering 1,545 firm-years of observations. The number of female directors in our dataset ranged from 0 to 6, with the average and the median being respectively 1.57 and 1.0. In contrast, the number of male directors ranged from 5 to 16, for a mean and median of respectively 9.12 and 9.0. In all cases, women were the minority gender category. Furthermore, there were 43 cases of female board chairs.

Strategic change

In line with the definition of strategic change, we operationalized the variable by taking into account alteration in six indicators that capture a firm’s overall strategic profile (Finkelstein & Hambrick, 1990; Zhang & Rajagopalan, 2010): advertising intensity (advertising/sales), R&D intensity (R&D/sales), plant and equipment upgrades (P&E upgrades/sales), non-production overhead (SGA expenses/sales), inventory levels (inventory/sales) and financial leverage (debt/equity). The composite measure was based on the sum of the variances in individual indicators over a four-year period from t–1 to t+2, which allowed us to capture strategic change from just before the focal year of observation, to two years ahead (Finkelstein & Hambrick, 1990).

Board gender diversity

We used Blau’s (1977) index (e.g. Harrison & Klein, 2007) to develop a measure of board gender diversity that took into account the number of female and male directors on a board. The index was operationalized using the following formula:

Board chair’s gender

A dummy variable was created. A coding of 1 recorded instances in which the board had a female chair and a coding of 0 recorded cases in which the board chair was male.

Control variables

Our analysis included several control variables. Specifically, we controlled for firms’ industry membership, which can affect firms’ tendency for strategic change because different industries present different challenges to companies, and the costs and benefits of strategic change differ (Herrmann & Nadkarni, 2014). To record industry membership we created industry dummies at the two-digit SIC level. We also included firm-level controls. Because firm slack might dictate strategic change (Cho & Hambrick, 2006), we controlled for it by considering the ratio of current assets to current liabilities. We also controlled for firm performance inasmuch as it may affect strategic change by shaping the perception of the need for change (Quigley & Hambrick, 2012). We operationalized it in terms of ROA (Chapple & Humphrey, 2014; Triana et al., 2013). We furthermore included the log of the number of years since a firm’s founding to control for firm age – prior work suggests that age might be related to the presence of female directors on a board (Gul, Srinidhi, & Ng, 2011) and that it might affect the likelihood and size of change (Rajagopalan & Spreitzer, 1997). We also controlled for the potential effect of board-related variables. Thus, as the number of board directors may affect decisions relating to strategic change, we included board size as a control. We moreover controlled for the proportion of outside directors because strategic change could be linked to board independence. In addition, as interlocking directorates may affect information availability and strategic decisions (Peng, 2004), we controlled for the average external board seats held by a firm’s directors. Further to this, because the length of CEO tenure and board chair tenure might have a bearing on strategic change (Miller, 1991; Rajagopalan &Spreitzer, 1997), we controlled for the number of years of incumbency as CEO and board chair. Additionally, because CEO duality could affect strategic change by giving the CEO more power, we controlled for it by creating a dummy variable that had a value of 1 if the CEO also held the position of board chair.

Data analysis

Because board gender diversity may be a function of unobserved firm- and industry-level factors, data analysis should account for potential endogeneity. For example, better performing companies may have more female directors because they are better positioned to pursue diversity goals (Farrell & Hersch, 2005). Or a larger board may have more female directors because female non-executive directors tend to be added to boards to satisfy equal opportunity requirements that are otherwise difficult to fulfil (Brammer, Millington, & Pavelin, 2007). Industry membership too may affect board gender diversity – female directors are noted to be more common in certain industries such as banking, media and retail (Hillman et al., 2007). In view of this, we did an initial Wu-Hausman analysis to ascertain whether board gender diversity was endogenous in our model. We regressed board gender diversity on all the study’s explanatory variables, and saved the regression residuals. The residuals were subsequently included as an additional explanatory variable when regressing strategic change (the outcome variable) on the explanatory variables. As the coefficient of the residual was significantly different from zero, the ordinary least squares (OLS) assumption of the residuals’ expected value being zero was violated, indicating an endogeneity issue. We moreover examined whether board chair’s gender might also be endogenous. This was not the case. As an endogenous explanatory variable can render OLS estimation inconsistent, for estimating unbiased coefficients a two-stage instrumental variables (IV) approach is viewed as the suitable analytical technique (Bascle, 2008; Baum, 2006). We thus did an IV analysis using the “ivreg2” command in STATA 15 (Baum, Schaffer, & Stillman, 2007).

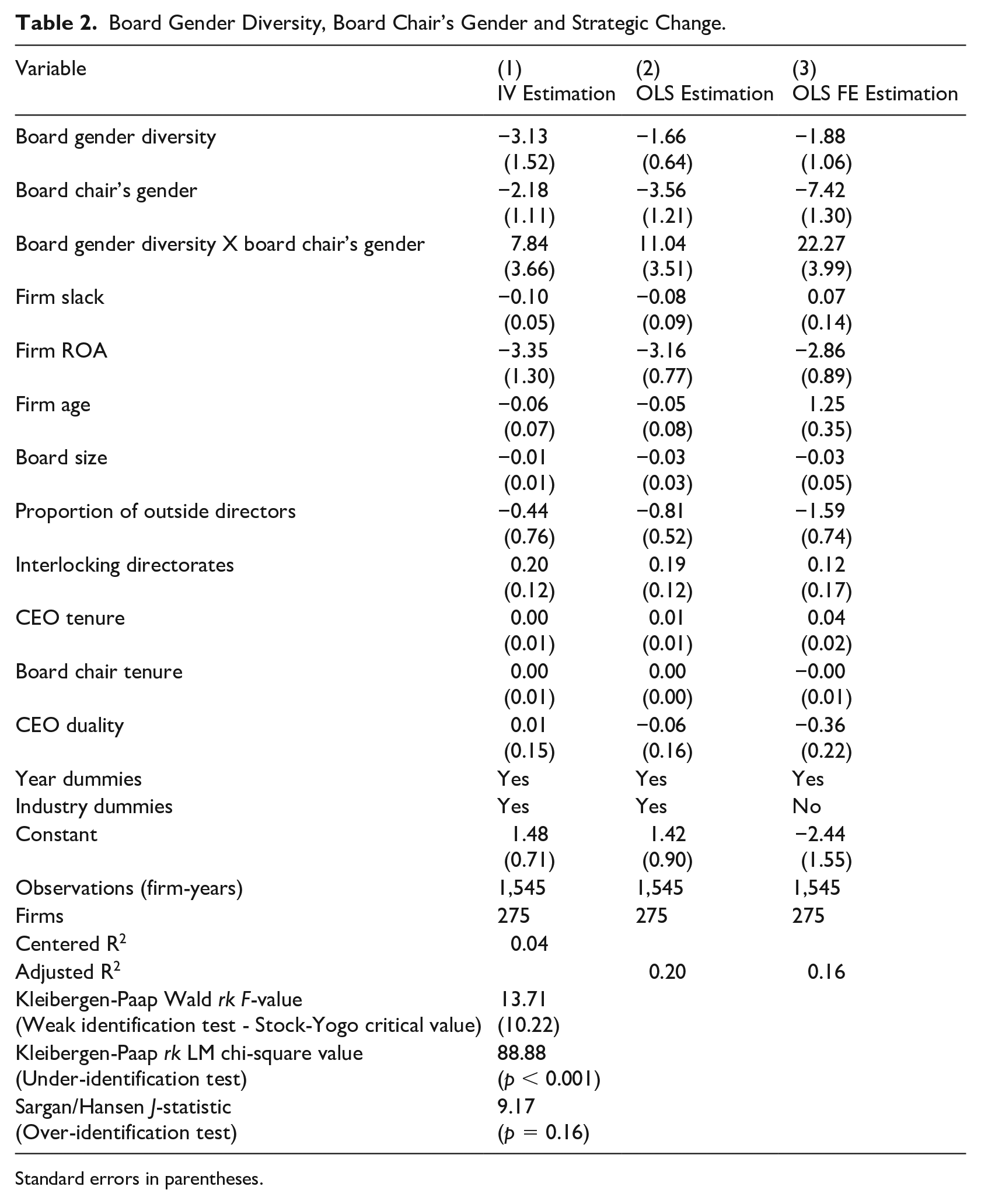

IV estimation depends on finding relevant instruments that correspond to the endogenous variable in the first-stage reduced form equation and also satisfy the exogeneity condition of not being correlated with the error term of the second-stage structural equation (Baum, 2006; Semadeni, Withers, & Trevis Certo, 2014). Moreover, for testing instrument exogeneity, the availability of multiple instruments is important (Baum, 2006; Semadeni et al., 2014). Based on a review of past studies, we identified four feasible instruments. First, because variation in the proportion of women in the working population can affect board gender diversity (Chen et al., 2016), we employed the civilian non-institutional gender ratio in US states (in which the firms’ headquarters were situated) as an instrument. The data came from the US Census Bureau. Second, because board gender diversity may depend on the proportion of an industry’s labour force constituted by women (Liu, Wei, & Xie, 2014), we used this as an additional instrument. The data was obtained from the US Bureau of Labor Statistics. Third, we followed Huang and Kisgen (2013) in using a gender status equality index proposed by Sugarman and Straus (1988). This captures how dedicated a US state is to pursuing women’s equality, which may affect the appointment of female directors by companies headquartered in different states. Lastly, we used a firm’s log of net sales as an instrument because firms with bigger revenues might be under greater pressure and might be more able to implement board-level gender diversity (Farrell & Hersch, 2005). None of these four instruments showed correlation with strategic change, the study’s outcome variable.

As we test not only the effect of board gender diversity on strategic change but also whether board chair’s gender moderates the main effect, our model entails an interaction term involving an endogenous regressor. To instrument the interaction term, we multiplied each of the four instruments with the dummy variable for board chair’s gender to create a further four instruments for the interaction term (Wooldridge, 2010). We then established the relevance and exogeneity of the instruments using a range of diagnostic checks. In support of the instruments’ relevance, the first-stage heteroskedasticity-robust F-statistics for how well the instruments predicted the endogenous regressor (F-value: 14.67) and the interaction term based on it (F-value: 3.66) were both highly significant (p < 0.001). Moreover, we could exclude weak identification as a concern because the heteroskedasticity-robust Kleibergen-Paap Wald rk statistic (F-value: 13.71) exceeded the Stock-Yogo critical value (for two endogenous terms and eight instruments) of 10.22 for a relative bias of 10% or less (Stock & Yogo, 2005), indicating our instruments to be relevant and strong. In addition, the Kleibergen-Paap rk LM statistic (chi-square: 88.88) was highly significant (p < 0.001), allowing us to rule out under-identification. Furthermore, providing support for the instruments’ exogeneity, the Sargan/Hansen J-statistic could not reject the null hypothesis of the instruments being exogenous and uncorrelated with the error term (p = 0.16). As a post-estimation diagnostic, we examined the endogeneity test statistic, which is robust to homoskedasticity violations and tests the null hypothesis that an endogenous regressor can actually be treated as exogenous (Baum et al., 2007). In this case, the statistic affirmed the endogeneity of board gender diversity (chi-square: 4.12; p < 0.05).

Results

Table 1 shows the descriptive statistics and the correlation matrix of all variables. The second-stage IV estimation results are shown in column 1 of Table 2. As regards firm-level control variables, slack and ROA have a significant negative effect on strategic change. Apparently, financially successful firms prefer not to alter their course. Regarding board-level controls, there is a significant positive effect of interlocking directorates on strategic change. This may be expected because of the greater variety of information flowing in when more external board seats are held by directors (cf. Peng, 2004). Importantly, as predicted in hypothesis 1, increase in board gender diversity has a significant negative effect on strategic change. Hypothesis 1 is thus supported. Regarding hypothesis 2, which predicted a reversal in board gender diversity’s negative effect on strategic change in the event of a female chair, the significant positive coefficient of the interaction term confirms the prediction. To facilitate interpretation, Figure 1 shows the moderation visually – whereas greater board gender diversity results in less strategic change when the board chair is male, the opposite is the case when the board chair is female.

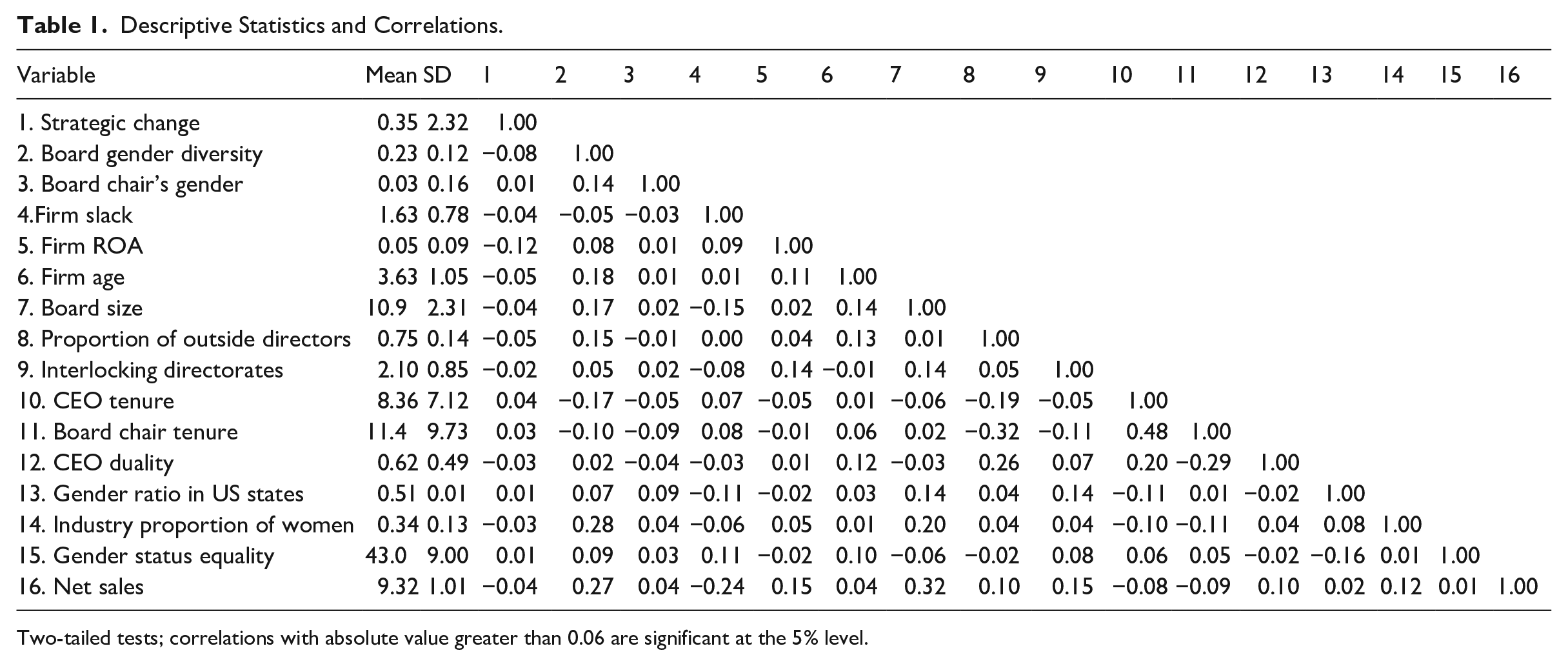

Descriptive Statistics and Correlations.

Two-tailed tests; correlations with absolute value greater than 0.06 are significant at the 5% level.

Board Gender Diversity, Board Chair’s Gender and Strategic Change.

Standard errors in parentheses.

Gender Diversity and Strategic Change – Moderating Effect of Board Chair’s Gender.

Columns 2 and 3 of Table 2 additionally show estimation results using OLS regression and OLS fixed-effects regression. These models were estimated using the “xtreg” command in STATA. Because greater estimator consistency comes at the expense of loss of efficiency when IV estimation is used, the complementary OLS analysis gives insight into the difference in findings across estimation approaches. Column 2 results indicate that without a correction for endogeneity, OLS estimation would in fact have yielded the same pattern of findings, but parameter estimates would need to be viewed with caution on account of bias. In contrast to OLS, fixed-effects OLS does allow one to control for omitted variables bias because coefficient estimates are based on within-firm variation over time. As can be seen in column 3, with fixed-effects estimation too, the general pattern of findings remains the same. However, there is a lower probability of an effect of board gender diversity. In contrast to IV estimation though, fixed-effects estimation is not able to correct for endogeneity arising from unobserved firm heterogeneity over time and the approach also does not allow inclusion of industry membership as a covariate. Despite these differences in the estimation approaches, the results converge to show that strategic change is affected negatively by board gender diversity and that this effect is moderated positively by the board chair’s gender.

Supplementary analysis

Past research has drawn attention to the glass cliff phenomenon – a greater tendency for women to be appointed to risky and precarious leadership positions (e.g. Rink, Ryan, & Stoker, 2013; Ryan et al., 2016). We thus tested whether poor firm performance and/or lack of strategic change may explain the appointment of women as board chairs, and thus perhaps the subsequent positive moderation effect on strategic change. We employed two analytical techniques. First, because the appointment or non-appointment of women as board chair is a binary variable, we ran probit regression models with robust standard errors to determine whether the variable in year t was predicted by firms’ performance (using first ROA and then ROS as indicators), level of strategic change, and the study’s other control variables in (i) Year t–1; (ii) average values of the predictor variables over a two year period t–1 to t–2; and (iii) change in values of the predictor variables from t–2 to t–1. We did not find any significant effect supporting a possible glass-cliff explanation for the appointment of female board chairs.

Second, we employed treatment effect estimation based on propensity score matching (PSM) (Rosenbaum & Rubin, 1983). Viewing weak performance (i.e. decrease in ROA in t–1 relative to the average of the preceding two-year period) as the treatment and the appointment of a female board chair as the outcome, we obtained propensity scores reflecting the estimated probability of treatment in the form of fitted values produced by a logistic regression of treatment assignment – a 1–0 binary – on observed covariates. We then used similarity of propensity scores to identify in the set of untreated cases (i.e. cases in which ROA had increased) those that matched the treated ones in all respects but the treatment. We used the “teffects psmatch” command in STATA 15. The matched cases were used to estimate the average treatment effect on the treated (i.e. the ATT estimator). The estimator was not significant, indicating that weak performance did not predict appointment of women to board chair. Similar analysis with treatment groups defined by ROS and strategic change decline also did not predict appointment of women to the board chair position. These results do not offer support for a glass cliff effect in relation to the appointment of women as board chairs. Perhaps such an effect is more likely with respect to CEO appointments, because accountability and responsibility rest with the CEO in relation to firm-level strategic decisions and outcomes (cf. Cook & Glass, 2014; Fitzsimmons, Callan, & Paulsen, 2014).

Discussion and Conclusion

To advance understanding of the implications of gender diversity at the corporate board level, this research examined gender diversity’s influence on strategic change in firms. Theory building in the article is located in the idea that gender is a social reality and construct, which finds expression in gender stereotypes (Eagly, Wood, & Diekman, 2000; Ridgeway, 2011). It is in the shadow of these stereotypes that the realm of corporate leadership has been a non-level playing field, a point evident, for instance, in women’s low representation in the upper-echelon managerial positions. Because male and female directors on boards do not meet and interact in a social vacuum, we took account of these stereotypes when developing testable new propositions. In being mindful of possible gender-linked prejudice, our article speaks to a recent editorial hinting at the possibility of covert and subtle gender bias in Western companies (Joshi, Neely, Emrich, Griffiths, & George, 2015). We argue that although because of gender status difference and bias (cf. Berger et al., 1972; Bilimoria & Piderit, 1994; Eagly & Karau, 2002; Heath et al., 2014) an increase in board gender diversity may be associated with less strategic change, its effect on strategic change should be positive for boards headed by a female chair. Data from Fortune 500 firms provides support for the theory. The study has important implications.

Although research shows that women’s performance in leadership roles hinges on the degree of gender status difference and bias in companies (Lucas, 2003; Vial et al., 2016), this issue has not received due attention in strategy and corporate governance work. If the board chair’s gender affects whether or not a smaller circle of male directors calls the tune on a gender-diverse board, this study highlights the need for systematically researching a theme that earlier studies have all but ignored, namely, what factors contribute to enhancing women’s status attributions and legitimacy for board roles, and under what circumstances (e.g. Eagly et al., 1995; Latu et al., 2013). The answers would speak to the plea for research on conditions under which gender diversity has positive and negative effects (Eagly, 2016) and could provide insights crucial for managerial and policy prescriptions. Furthermore, inasmuch as gender status difference and bias are more salient in mixed-gender domains that are associated particularly with the competency set of only one gender (e.g. Randel, 2002; Ridgeway & Correll, 2004), this study indicates that circumspection would be prudent when using diversity arguments and empirical findings from non-leadership, non-board settings to theorize the effects of board gender diversity.

The study also helps reconcile the seemingly conflicting results of some of the earlier research. Consider, in this respect, the contrasting findings suggesting on the one hand that female directors are more risk-loving (Adams & Funk, 2012), and on the other that when there are more female directors there is decline in change (Triana et al., 2013), acquisition intensity (Chen et al., 2016) and performance (Adams & Ferreira, 2009). These divergent effects are in fact concurrently possible if theory-building allows for the possibility of gender-linked prejudice on boards (see e.g. Eagly & Karau, 2002; Nielsen & Huse, 2010b). Female directors may be more risk-loving, but this will not find reflection in a firm’s strategy if female directors do not have the same influence on strategy as the male directors do. Moreover, inasmuch as mixed empirical findings indicate the need for identifying overlooked moderator variables (Aiken & West, 1991), the moderating effect of board chair’s gender offers a basis for resolving the inconsistent positive and negative effects of board gender diversity that earlier studies have reported (cf. Dobbin & Jung, 2011, Erhardt et al., 2003). Furthermore, the results of this study are also of interest in relation to quota-based legislative regimes seeking to increase the number of female directors on boards.

Whereas quotas are motivated by a desire to promote social justice through removal of impediments to women’s participation on boards, those who attach primacy to property rights and free market principles are critical of quotas because the costs of policy must be borne by firms (Ahern & Dittmar, 2012; Kogut et al., 2014). With regard to this debate, while number-based quota regimes contribute to the goal of social equity, our results suggest that for firm-level benefits it is vital to also pay attention to the board positions held by female directors. While this study focused specifically on the board chair position, female directors’ inclusion in and chairpersonship of important board committees is also a key element that could contribute to countering gender status difference and bias on boards (see e.g. Bilimoria & Piderit, 1994; McGuire, Taylor, & Turgut, 2019). Thus, in addition to numerical goals – for example, the regulatory aim in European Union countries is often 40 percent female representation on boards (Mensi-Klarbach & Seierstad, 2020) – public policy debate can consider the inclusion of a ‘positional’ emphasis in regulatory regimes, which obliges the selection of women to key board positions. Numerical and positional goals as complementary instruments – either in the form of voluntary target-setting or comply-or-explain regulatory codes – may jointly have greater potential to contribute to the cause of both greater gender equality and a more effective board.

There is another issue worth considering in the light of this study. A failure to find validation for board gender diversity’s predicted effects in some of the past studies has fuelled the conjecture that an effect may only emerge after some critical mass of women is reached on boards – the number three has been suggested as a rule of thumb (Cabeza-García, Fernández-Gago, & Nirto, 2018; Konrad, Kramer, & Erkut, 2008; Torchia et al., 2011). The conjecture draws inspiration from Kanter’s (1977) work on how work-group processes are affected by the number of women in a group. However, at lower levels in the organizational hierarchy, gender status difference and bias are likely to be less pronounced than at the board leadership level (see Eagly & Karau 2002; Ridgeway, 2011). With this in mind, our research suggests that on boards the key issue may not only be the specific number of female directors, but also whether the female directors have influence on decision-making and outcomes. As our analysis is based on the examination of boards on which there was almost always a large male majority, an intriguing question arises whether our findings would hold if boards had a female majority or if the male and female directors were evenly balanced. A definitive answer, of necessity, must await a time when greater gender equality and the recession of gender stereotypes in society lead to more female directors being on boards. Such a social context may mark the boundary condition for the theory presented here.

The study also has practical implications for companies that have or plan to have female directors. While board gender diversity is usually viewed to be important for establishing credentials as a socially responsible corporate citizen, our work shows that it can also have relevance for strategy. Inasmuch as gender status difference stifles female directors’ influence (McGuire et al., 2019; Nielsen & Huse, 2010b), those in charge would do well to review whether gender status equality prevails in the boardroom. It is worth noting in this regard that the omnipresent ordinariness of social beliefs and norms may make it hard to spot that gender status difference and bias exist. In this regard, past work suggests that female directors’ inclusion in and chairpersonship of important board committees may help counter status difference by signalling a mindset and company culture that regard gender as an irrelevant category for leadership roles (see e.g. Lucas, 2003; Wagner et al., 1986). In view of this study’s findings, a company could also consider appointing women to the board chair position. Gender status equality could moreover be nurtured by disassociating directorship roles from a masculine construal of leadership corresponding to the male gender stereotype (Eagly & Karau, 2002; Schein, 2001). It may thus help to use gender-neutral, androgynous language for describing directorship roles (Schein, 2001).

Potential limitations and opportunities for future research

This study’s results are based on data from large US firms, which face public scrutiny and pressure but no legal requirements for greater female representation on boards. The findings, thus, cannot be generalized to firms in other institutional settings. Research on companies embedded in other social environments would therefore be of value in expanding understanding of how the effects of board gender diversity and the board chair’s gender vary with context. There are additional significant opportunities to extend our work. For instance, as the roles, responsibilities and processes of selection, evaluation and dismissal of a CEO and other TMT members are different from those of board members, our findings cannot be assumed to hold for TMTs as well. Thus, we encourage research that examines the extent to which the present results are generalizable to the TMT level. Furthermore, it would be very interesting to use the SCT and RCT to examine the influence of men and women who are ethnic minorities on decision-making in boardrooms.

This study reflects our interest in understanding how companies can harness the potential of gender diversity in boardrooms. Although our focus was on examining the moderating influence of board chair’s gender, there are also other relevant factors likely to offset board gender diversity’s negative effect. For instance, future research could study the effect of female directors’ inclusion in and chairpersonship of important board committees. More broadly, future researchers could investigate how board gender diversity’s effect is shaped by the wider culture, systems and practices in companies. For example, gender stereotypes may be reinforced or disavowed by a company’s human-resources hiring, development, and promotion and remuneration practices, the phraseology of formal texts and communications, and the language and rhetoric characterizing informal social interactions. Examination of these additional factors should lead to a fuller picture about the extent to which they individually and collectively offset board gender diversity’s negative effect, delivering valuable practical suggestions for benefitting from gender diversity.

Furthermore, we only examined the effect of board gender diversity on strategic change. Researchers interested in establishing board gender diversity’s effect on financial performance could extend our theoretical arguments by modelling strategic change as the mediating variable. Besides, we did not study whether and why some individual female directors are more influential than others despite gender stereotypes. Scholars could therefore go beyond the analysis of central tendencies to study whether individual-level factors such as personality and network ties affect female directors’ influence. Clearly, there is still much we need to understand regarding gender diversity in boardrooms. We hope the research directions identified here will stimulate the pursuit of further knowledge.

Footnotes

Acknowledgements

Ying Feng acknowledges the support of XJTLU Research Development Fund 18-02-27.

Funding

The other author(s) received no financial support for the research, authorship, and/or publication of this article.