Abstract

Accounting and auditing are often cited as key sites where business regulation has been privatized, globalized and neoliberalized. Yet, these sites have also undergone a legitimacy crisis in recent years, marked by a shift from self-regulation to increased public oversight. This paper investigates these developments by reference to the evolution of a public/private audit oversight regime (audit of the auditors) in Russia. We show how, in the early stages of post-Soviet reforms, old state-administered forms of financial oversight were replaced with market-oriented arrangements (peer reviews) offered by newly founded private professional accountancy associations as a service to their members. Fifteen years later, the process of regulatory privatization culminated in a reinvigoration of public authority. Our longitudinal analysis highlights the pivotal role of the state in the liberalization of governance by showing how audit oversight privatization was not only enabled by, but also provided a condition for, the strengthening of government actors. We introduce the term ‘legislative layering’ to denote the mechanism that enabled public actors to redeploy themselves in the face of the rising market logic to ensure continuity in their regulatory objectives.

Introduction

Over the past few decades, the relevance of private sector organizations in the governance of business conduct has vastly expanded (Büthe & Mattli, 2011; Djelic & Sahlin-Andersson, 2006). Prior literature has been useful in depicting the significance and complexity of various public-private governance arrays. Particularly, attention has been devoted to cross-national and cross-sectoral variation in the composition of what is widely referred to as the ‘governance triangle’ consisting of state, market, civil society and other non-governmental private organizations, including standard-setting and professional organizations (Abbott & Snidal, 2001; but see also Büthe & Mattli, 2011; Eberlein, Abbott, Black, Meidinger, & Wood, 2014). However, we do not know much about dynamics of change within such regimes: how and why the relative influence and positioning of public and private actors within a specific ‘governance triangle’ may shift over time and with what consequences. Moreover, the literature has not adequately engaged with issues concerning the evolving role of the state in ‘regulatory capitalism’ (Braithwaite, 2008; Levi-Faur, 2005), often portraying public actors as rule-takers rather than rule-makers, particularly in the context of international business regulation (Braithwaite & Drahos, 2000; Büthe & Mattli, 2011).

Meanwhile, governments have continued to be involved in public-private governance arrangements. In some cases, they have stepped back in to reassert their authority, as for example in accounting and audit regulation. Triggered by the demise of Arthur Andersen, the Enron scandal and the 2008 financial crisis, accounting and auditing underwent a profound legitimacy crisis that led to a shift from predominantly privately organized self-regulation to increased public oversight (Canning & O’Dwyer, 2016; Caramanis, Dedoulis, & Leventis, 2015; Hazgui & Gendron, 2015; Malsch & Gendron, 2011). Studies have examined the renewed relevance of government actors in audit regulation. Yet, apart from some exceptions, accounts of rising public oversight have primarily been interested in the state in terms of its role in formally endorsing and facilitating (Canning & O’Dwyer, 2013, 2016; Malsch & Gendron, 2011) or hampering (Caramanis et al., 2015) such regimes. These studies do not explore how changes in the organization of audit oversight may have consequences for the evolution and organization of government itself. We aim to provide better understanding of how government actors maintain and enhance their relevance and authority in public-private regulatory regimes. In so doing, we directly respond to recent calls for further research into the expansion of the state, both ‘in terms of its scope (the range of functions it performs), … [and] its capacity to perform the core functions it has long engaged in’ (Soifer, 2016, p. 188).

This paper focuses on the evolving regime of audit oversight (audits of the auditors) in Russia where the introduction of additional state-organized inspections of audit has challenged the relevance of private regulation, such as peer reviews administered by private professional associations. In auditing, peer reviews refer to a process by which a qualified audit firm reviews the operational procedures of another audit firm to ensure that they meet certain standards. Audit in Russia presents an apt setting for studying change dynamics in public-private regulation because of the nature of institutional transformations it underwent and the varying involvement of government actors in these. Our analysis of the changes in audit oversight organization offers the following contributions.

First, we take a longitudinal approach to show how and why regulatory privatization, far from being a retreat of public governance, may, in effect, be a prelude to the strengthening of government. Both the privatization of audit regulation and the subsequent rise of public audit oversight were made possible by government interventions. We show how government actors reinvent and expand their roles in an evolving public-private regulatory regime. Drawing on historical institutionalism and theories of gradual institutional change (Mahoney & Thelen, 2009; Streeck & Thelen, 2005; Thelen, 2009), we develop the notion of ‘legislative layering’ to draw attention to a particular mechanism of state expansion where government actors draw on law as an organizational resource (Pedriana & Stryker, 2004) to mould their relations with private governance.

Second, we expose the futility of drawing a strict demarcation line between public and private governance forms and actors as they negoiate the organization of dispersed governance domains (Arellano-Gault, Demortain, Rouillard, & Thoenig, 2013; Botzem & Dobusch, 2012). We point to the co-produced nature of the relationship between them and the need to see their regulatory authority as mutually contingent – i.e. as both moderating and extending each other’s organizing influence and capacity to act. We demonstrate that in public-private governance regimes the ability of government actors to maintain and expand their core functions is dependent on their legislative remit, as much as on their ability to co-ordinate and leverage capacities of private governance to convert law into desirable regulatory outcomes.

Regulatory Privatization and Its Limits

With rising globalization, we have seen a proliferation of new technologies for the regulation of business conduct, accompanied by greater reliance on private regulation and self-regulation, and the rise of independent regulatory agencies acting at arms’ length from governments (Braithwaite & Drahos, 2000; Büthe & Mattli, 2011; Djelic & Sahlin, 2012). Also, in accounting and auditing, rule-making has been transferred from governments to globally operating private standard-setting bodies. Political science and regulation scholars have queried the power, accountability and legitimacy of these organizations.

Much has been written about the politics of international accounting and audit standard-setting and its proneness to regulatory capture (Botzem, 2012; Loft, Humphrey, & Turley, 2006; Morley, 2016; Tamm Hallström, 2004), the political and distributional implications of global private accounting and audit rule-making (Arnold, 2012; Büthe & Mattli, 2011; Perry & Nölke, 2006), and the capacity of international standard-setters to push through new practice concepts, sometimes against the will of their constituents (Erb & Pelger, 2015). Scholars, such as Botzem and Dobusch (2012), have examined the formation and diffusion of accounting standards as recursive cycles of input and output legitimacy, usefully articulating a process perspective on private standard-setting. But none of the studies cited above have devoted much attention to the changing roles of government in these processes – such roles are either eclipsed (Büthe & Mattli, 2011; Erb & Pelger, 2015) or touched upon merely implicitly (Botzem & Dobusch, 2012).

Studies of ‘regulatory capitalism’ (Braithwaite, 2008; Levi-Faur, 2005) can offer a useful starting point to redress this shortcoming. They draw attention to processes of regulatory privatization – shifts from ‘government’ (hard law, command and control) to ‘governance’ (soft law, contracting, self-regulation, public-private regulatory arrangements), the delegation of responsibility from ‘political’ (governmental) to ‘professional’ organizations, regulatory agencies or expert networks (Jordana, Levi-Faur, & Fernández i Marín, 2011; Levi-Faur, 2011) – highlighting that such developments have not led to a dismantling of the state.

A focus on ‘regulatory capitalism’ helps situate regulatory privatization in broader processes of societal transformation and organizational change where state, markets and society are not treated as distinct entities or their relationships as zero-sum game (Levi-Faur, 2005, p. 14; Braithwaite, 2008). Any change in governmental configuration is expected to be reflected in the economy and society, and vice versa. As Levi-Faur put it, states and markets are seen as forming part of an integrated ensemble of governance: ‘The regulatory and policy-making institutions of the state are one element of the market, one set of institutions, through which the overall process of governance operates’ (Underhill, 2003, p. 254; quoted in Levi-Faur, 2005, p. 28). States and markets, public and private regulation, act as flexible surrounds for each other, mutually conditioning and shaping each other (Abbott, 2005). Yet, despite this focus on state and market co-evolution, most empirical studies of regulatory capitalism tend to concentrate on the rise and effects of new types of regulatory organization in a given sector (Jordana et al., 2011; Levi-Faur, 2006), giving limited attention to how these are implicated in changing relations between state, market and society over time.

Outside the regulatory capitalism paradigm, studies of transnational governance in international relations and law have placed more explicit emphasis on interactions between state and non-state regulation. Abbott and Snidal (2009) depict the diversity of regulatory standard-setting in a ‘governance triangle’ whose main players are made up by state actors (national and international governmental organizations), firms and nongovernmental (private) organizations. The triangle is mobilized for representing situations in which different (combinations of) actor categories dominate the governance of a particular domain (Abbott & Snidal, 2009, p. 513; Eberlein et al., 2014). Yet, it is static in orientation and therefore of limited use in understanding change in the composition and relative influence of public and private actors.

Our study seeks to redress this shortcoming by combining regulatory capitalism and historical institutionalist perspectives (Mahoney & Thelen, 2009) to get to grips with long-term processes of institutional change in public-private regulation of post-Soviet audit oversight. Responding to recent calls for better understanding of the expansion of the state in public-private regulation regimes (Soifer, 2016), we are particularly interested in the implications of such processes for the regulatory roles played by government actors. The case of Russia is interesting as we are dealing with a state in transition, where regulatory privatization has been unfolding against the background of transforming governmental authority and shifting relationships between state and non-state actors.

With the collapse of the Soviet Union, the roles of government had been called into question and, as a consequence, spheres of state action and non-action had to be reworked. Privatization of state-owned enterprises, and also of regulation itself, was envisaged by government actors (e.g. the Finance Ministry) as a means to create a new regulatory space through which Russia’s government and economy could be reorganized according to Western constructs of a globally integrated market economy (Djelic, 2006; Mennicken, 2010). New political and economic institutions had to be established, including private sector audit and audit regulation, as well as distinctions between public and private realms of business and regulatory activity.

The first private audit firms were founded in Russia in the late 1980s; additionally, the big international audit firms began to open branch offices at that time (Cooper, Greenwood, Hinings, & Brown, 1998). Before 1998, the Big Six global audit firms included Coopers & Lybrand, Price Waterhouse, KPMG, Deloitte, Arthur Andersen, and Ernst & Young. They later became the Big Four following the establishment of PricewaterhouseCoopers (PwC) and the demise of Arthur Andersen.

Until 1993, private sector auditing was largely unregulated. Auditors, for example, were not required to have a professional qualification to carry out audits, nor were audit firms subject to any licensing or external quality control. This institutional ‘void’ was the product of, and legitimized by, early post-Soviet privatization, marketization and liberalization. Yet, in the years that followed we observe a shift towards public re-regulation where regulatory privatization, the control of audit by private professional audit associations, came to be orchestrated and superintended by government actors.

Such shifts in audit oversight re-regulation are not unique to Russia. After Enron, WorldCom, and the demise of Arthur Andersen, we see a rise in public audit oversight schemes in many countries, replacing or complementing self-regulatory arrangements, such as peer reviews, with government-led (or endorsed) audit inspections. Prior studies have examined local manifestations of this global regulatory trend, drawing attention to the workings of emerging independent oversight bodies, many of which were modelled on the United States’ Public Company Accounts Oversight Board (PCAOB) founded in 2002 (Canning & O’Dwyer, 2013, 2016; Caramanis et al., 2015; Hazgui & Gendron, 2015; Malsch & Gendron, 2011). These studies have stressed the contextually contingent nature of local enactment of global regulatory trends, highlighting the proneness of such regimes to regulatory capture by international audit firms and local professional associations (see Caramanis et al., 2015, for the case of Greece, and accounts of local resistance by Malsch & Gendron, 2011; Hazgui & Gendron, 2015; Canning & O’Dwyer, 2016). These accounts are useful in depicting local variability in public audit oversight implementation. However, the broader issues of governmental transformation and the (re)building of governmental capacity and authority have largely remained unexplored. Also, the role of regulatory privatization as a governance process whose outcomes may themselves have consequences for the trajectory of governmental re-regulation has not been explicitly addressed.

Studying Dynamics of Institutional Change in Audit Oversight

We see the interplay between regulatory privatization and public re-regulation not in terms of a lucid distinction between the public and the private, or regime replacement (from public to private and back), but as a ‘dance’ between public and private regulation where regulatory privatization is established and reworked by reference to the past and in collaboration with government organizations. We draw on the historical institutionalist literature (Conran & Thelen, 2016; Mahoney & Thelen, 2009; Streeck & Thelen, 2005) that sees changes in institutional arrangements as incremental, subtle transformations occurring over time and engendered by the very properties of an institution subject to change. Following these studies, the institution of audit oversight can be defined as a ‘social regime’, i.e. ‘a set of rules stipulating expected behavior and “ruling out” behavior deemed to be undesirable … [which] involves rule makers and rule takers, the former setting and modifying, often in conflict and competition, the rules with which the latter are expected to comply’ (Streeck & Thelen, 2005, pp. 12–13). Institutions thus emerge not as self-reinforcing enduring outcomes of prior political battles but as ‘compromises or relatively durable though still contested settlements … [which are] always vulnerable to shifts’ (Mahoney & Thelen, 2009, p. 8). Institutional change and stability, thus, far from being separate analytical categories, represent ‘two sides of the same coin [in the sense that] the explanation of political change rests upon an analysis of the foundations of political stability’ (Conran & Thelen, 2016, p. 63). The chance of a triumph for the advocates of change is, to a great extent, contingent on the outcomes of the efforts of those who push for continuity.

Following Mahoney and Thelen (2009), what determines the particular type of incremental change that unfolds is a function of two factors, namely: (i) the character of the existing rules supporting an institution, such as audit oversight (‘rule ambiguity’), and (ii) the prevailing political context and whether it affords the defenders of the status quo the power (‘veto possibilities’) to ensure continuity (Mahoney & Thelen, 2009, p. 7; Streeck & Thelen, 2005; Thelen, 2009). Such a perspective focuses not only on the environmental conditions that invite particular change strategies, but also on the very design of the institutional arrangements creating ‘openings for creativity and agency’ (Mahoney & Thelen, 2009, p. 12) and enabling actors to seek competing interpretations of one and the same rule in order to achieve favourable outcomes. A second factor shaping institutional change concerns the political context in which the change takes place and the ‘veto possibilities’ that public and private actors have to hinder or promote change. Such veto possibilities, we argue, rest on the knowledge and expertise of actors as well as other resources, including administrative and legal resources.

Particular mixes of (strong/weak) ‘rule ambiguity’ and (strong/weak) ‘veto possibilities’ determine the type of institutional change that ensues (Mahoney & Thelen, 2009; Streeck & Thelen, 2005). Displacement, i.e. the removal of existing rules and the introduction of new ones, occurs when agents have little discretion to mould existing institutional arrangements and opt to replace them in the face of little resistance from the defendants of the status quo. When veto possibilities are strong, displacement is unlikely and change occurs through layering when new rules, as a result of amendments, revisions and subtle modifications, are attached to the existing ones to change the way in which the original rules structure behaviour (Mahoney & Thelen, 2009, p. 16). Drift and conversion occur when a targeted institution, such as audit oversight, affords actors significant interpretational freedom. Here, the rules themselves (e.g. audit oversight rules) remain untouched. They are either interpreted in new ways (conversion) or deliberately neglected (drift) in the face of changing environmental conditions and strong veto possibilities.

Mahoney and Thelen (2009, p. 22) acknowledged, but did not systematically problematize, the premise that ‘administrative capacities may be especially important’ for actors pursuing particular types of change, as their deficiencies or strengths here can create openings for the reinterpreting or amending of rules. Below, we extend Mahoney, Streeck and Thelen’s framework by placing greater attention on ‘law as resource’ (Pedriana & Stryker, 2004) (see also Edelman, Krieger, Eliason, Abiston, & Mellema, 2011; Edelman & Suchman, 1997) for shaping the capacity of state and non-state actors with consequences for the resulting regulatory set-up. As Pedriana and Stryker (2004, p. 709) write, ‘capacity is a “moving target”, with state and societal actors building on legal as well as administrative resources to construct and transform capacity.’ In line with the above, we see regulatory capacity as comprising both administrative resources (money, trained personnel, bureaucratic infrastructure) and legal capacities (statutory construction, legal interpretation) that are necessary for state and non-state actors to be able to deliver and/or co-ordinate the delivery of regulation. Here, legal capacities may relate to law-making (law on the books) but also an ability to mobilize law in pursuit of specific regulatory objectives (law in practice) (Bartley, 2011). Furthermore, law, first and foremost, should not be understood in terms of state-centred command and control but as an organizing device shaped by state and non-state actors. Law encompasses thus not only legislation but also legal-interpretive activity in a broader sense, including the drafting of guidelines which interpret legislation involving state and non-state actors (Edelman & Suchman, 1997; Halliday & Carruthers, 2007; Pedriana & Stryker, 2004). We are particularly interested in how the role and capacity of the Russian government in the regulation of audit oversight was expanded through law over time, concurrent with regulatory privatization.

Methods and Data

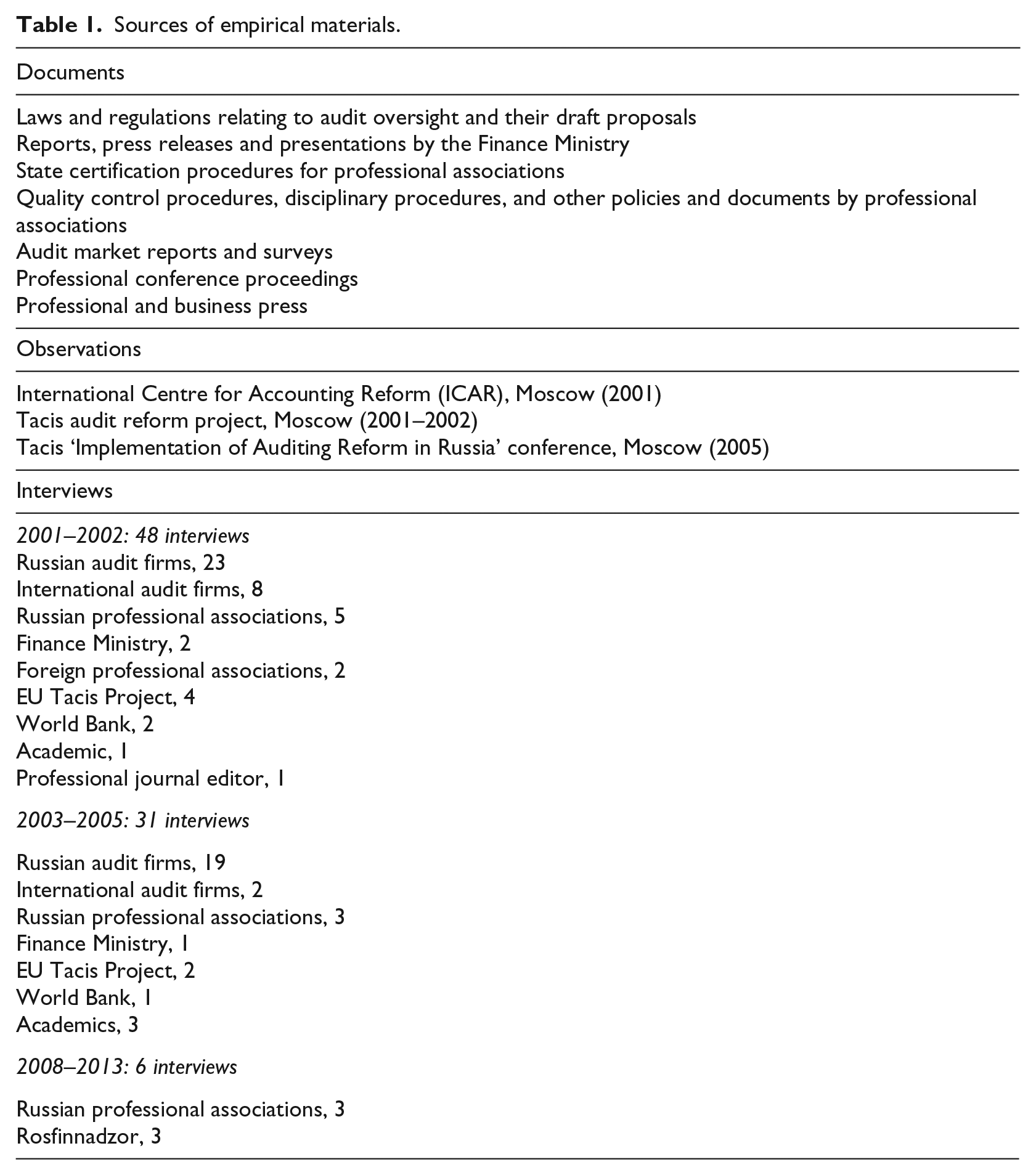

We utilize a historical case study approach (Eisenhardt & Graebner, 2007; Yin, 2008) to examine how regulatory change unfolds over time (Funk & Hirschman, 2014), including change in the prescriptiveness of law, actors’ veto possibilities and ensuing public/private regulation dynamics. We draw on a rich body of empirical materials collected during several rounds of fieldwork between 2001 and 2015 (Table 1). This includes documentary materials (government reports, professional associations’ documents, journal articles, press releases, audit market reports, legislative documents) to understand the changing (historical) context surrounding audit oversight. We also conducted 85 interviews (from 30 to 180 minutes in length) with key stakeholders. Participant observations of audit professional gatherings and audit rule production (including the (re)drafting of the federal audit law over time) made it possible to situate the collected interviews and documents and study the evolving interactions between state and non-state actors in constructing audit oversight.

Sources of empirical materials.

Most interviews were conducted during two periods of fieldwork. All interviews were conducted in Russian, except for eight interviews with representatives from the World Bank, foreign professional associations and international audit firms, which were conducted in English. During the first period (2001–2002), one of the authors conducted interviews with leading auditors, representatives of the Russian government, local and foreign professional accountancy bodies, World Bank officials and EU Tacis Project employees. The same author carried out participant observations in the International Centre for Accounting Reform, an internationally sponsored Moscow-based agency promoting development of Western-oriented accounting and audit. The author also participated in an EU-funded Tacis Audit Reform project. This allowed access to key documentary evidence, such as the first country-wide database of Russian professional audit associations compiled in 2002, and a sequence of proposals for the landmark 2001 Federal Audit Law which introduced, for the first time, a formal framework for audit regulation, including audit oversight.

The second period of fieldwork (2003–2005), conducted by another author, focused on further data collection to trace the effects of the 2001 Audit Law. This included follow-up interviews with some of the individuals who had been interviewed during the first stage. The author participated in the Tacis project’s ‘Implementation of Audit Reform’ conference in Moscow (2005), which assembled Russian audit firms, professional bodies, government officials as well as members of major European professional and regulatory organizations. The same author conducted a small number of further follow-up interviews with representatives from Russian professional associations and the government between 2008 and 2013 to collect views on amendments to the 2001 Audit Law which came into effect in 2008. Further, these interviews were corroborated with documentary evidence collected from online resources, professional and other media outlets, as well as government organizations.

All authors are proficient in English and Russian and were able to participate equally in the cross-examination of the empirical materials. In our analysis, we utilized an approach associated with examining qualitative process data from varied sources (Langley, 1999). We adopted a ‘temporal bracketing strategy’ (Langley, 1999, p. 703) to trace dynamics of audit oversight privatization and re-regulation and examine how actions during one period led to changes in the context that affected actions in subsequent periods. We decomposed our material into two successive periods of audit oversight development (1993–2001 and 2001–2008). These periods were derived from an analysis of key events which identified the 2001 Audit Law and the revised 2008 Audit Law as the two key pieces of legislation governing the reorganization of audit oversight. Based on the provisions in both laws, we identified two types of actors – (public) government organizations and (private) professional associations – as key constituents in audit oversight development. Audit firms officially did not enjoy any regulatory powers. Nevertheless, some firms were involved in the establishment of private oversight through membership in professional associations, and we traced their involvement where appropriate.

We tracked the prescriptiveness/ambiguity of different clauses in the laws over time, with a focus on the specified structure of professional associations, components of audit oversight, and the roles assigned to key players. We analysed documents and interviews to identify key events and activities preceding the issuance of the 2001 and 2008 laws, as well as accounts of interactions among government and professional actors and the way these shaped pathways of action in audit oversight (re)regulation. We also examined changing degrees to which the laws formally (re-)defined the audit oversight arrangements and related responsibilities. We studied the capacities of key actors (government and professional bodies) to block change (i.e. their veto possibilities), as derived from formal regulatory remit as well as their (changing) capability to fulfil it in practice. The combination of different types of materials made it possible to compare, contrast and situate different representations of actors’ involvement in audit (re)regulation, thereby facilitating a multi-layered understanding of how law was mobilized as a resource by state and non-state actors in the reorganization of audit oversight.

The Rise and Fall of Private Audit Oversight: Empirical Analysis

Privatizing audit oversight: From Temporary Rules to the 2001 Audit Law

After the collapse of the Soviet Union, between 1991 and 1993, the Russian government advanced private auditing as an institution for dealing with economic and social transition. The privatization of audit, first and foremost, was initiated by the Ministry of Finance and its financial control division in an attempt to redefine its roles and relevance within an emerging market economy (Danilevsky, 1991, 1994). It was envisaged that conditions of market competition and the ensuing private [sobstvenny] and economic [khozraschetny] interests of commercial auditors would allow for quality and self-discipline in the conduct of market-oriented audits (Danilevsky, 1991). Yet, this does not mean that the government completely withdrew itself. The initial decision to privatize audit (and audit regulation) kicked off a longer process of institutional change, whereby the roles of the government in the market and, vice versa, the market in government were gradually redefined, and relations between state and non-state actors reworked. As we show below, law played an important mediating role here. Mobilized by both public and private actors, law became a resource for the setting and shifting of public/private boundaries and reorganizing of the audit regulatory space.

Auditing in Russia was largely unregulated. That changed in 1993 with the government’s endorsement of the Temporary Rules (Vremenniye Pravila) on Auditing which, for the first time, explicitly addressed the issue of audit oversight and the need for ‘effective certification and licensing procedures’ for new entrants to the profession. These Rules were endorsed by Presidential Decree No. 2263 of 22 December 1993. In 1994, two governmental agencies – Central Certifying and Licensing Auditing Commissions (TsALAK) – were established by the government to oversee the issuing and withdrawal of audit firm licences and professional certificates for audit practitioners. One agency was attached to the Ministry of Finance and responsible for general audit licences. The other agency was accountable to the Central Bank and in charge of licences for the audits of banks. The new licensing agencies specified the amount of training hours and work experience needed for obtaining an audit licence, but not their content. These bodies, as well as the Temporary Rules, were also silent about the ongoing maintenance of audit quality. As one auditor commented on this period, ‘You received a certificate to practise, and no one really cared about what you were doing after that’ (Auditor in a Russian audit firm, 2004, Moscow). The auditing landscape was colourful and diverse. Next to the big international audit firms operated a small fraction of large indigenous firms, seeking to emulate their international counterparts. At the other end of the spectrum existed small audit firms and sole practitioners, often servicing only one or two clients. The Rules left it to the audit firms to define their work, and the controls thereof, by stating that ‘auditors and audit firms have the right to define methods and forms of audit controls themselves, provided that they are not in conflict with the laws of the Russian Federation’ (Temporary Rules on Auditing, 1993, Art. 13). In so doing, the ambiguity of the Rules opened up a space for the emergent audit profession to organize itself and proactively define its tasks and jurisdiction.

The issuing of the Temporary Rules coincided with the creation of new, private professional associations: e.g., the Russian Collegium of Auditors (RCA) (1992); Moscow Audit Chamber (1992); Russian Audit Chamber (1995); Union of Professional Audit Organizations (SPAO) (1996); Institute of Professional Accountants (1997). The Rules encouraged the foundation of such associations by stating that ‘auditors and audit firms can, in accordance with the laws of the Russian Federation, form consortiums, associations and other forms of alliance to coordinate their activities or protect their professional interests’ (Temporary Rules on Auditing, 1993, Art. 8). Most associations accepted firms and individuals as members, and it was possible to hold memberships in more than one association.

Newly founded audit firms played a key role in the formation and running of the associations. SPAO, for example, was founded under the leadership of Unicon, which became one of Russia’s leading audit firms; and the RCA was founded by Alexander Ruf, director of Rufaudit. Associations were not regulated or accredited. Initially, they had no legally defined regulatory remit and served mainly as ‘socialization fora’ for Russian audit firms and auditors to articulate common approaches in their dealings with government, clients and other parties. The associations shared similar objectives: to contribute to the development of the auditing profession, to represent member interests and to provide training.

1

Entry barriers were not high. Anyone interested (firms or individuals) could join, and no association at that time had formalized systems of disciplinary procedures applied to their members. Furthermore, membership was not compulsory. Hence, many auditors and audit firms remained professionally ‘unorganized’ and ‘unsupervised’. With time, however, one could see signs, at least in some associations, of growing dissatisfaction with the status quo and calls for the widening of their regulatory remit, also with regard to overseeing the quality of their members’ work, which often was seen to be low: Representing member interests has always been a relevant function, and our association has been doing that, but then we also understood it was not enough, that there was a need for an effective system of quality control [audit oversight] that should be formally delegated to the professional associations. (President of Professional Association A, Moscow, 2001)

The vagueness of the Temporary Rules in defining and locating audit oversight opened up possibilities for the associations to pursue state-independent attempts to establish in-house (private) audit oversight arrangements in the form of peer reviews. Peer reviews had long been among the core activities of professional associations elsewhere (United Kingdom, the US, France, Germany). In Russia, the Institute of Professional Auditors in Russia (IPAR), formerly SPAO, was among the first associations to introduce a programme where quality controllers from member firms (peers) came to check the work performed by other member firms. The President of IPAR, Daria Dolotenkova, emphasized the procedural rigour of her association’s approach: IPAR’s Quality Committee has developed a detailed framework for the IPAR quality control [audit oversight] system that comprises the following guidelines: (1) the Concept of Assessing the Quality of Audits Undertaken by IPAR’s Member Firms/Auditors, (2) Quality Control Policies for Audits Undertaken by IPAR’s Member Firms and Individual Auditors, (3) the Regulation ‘On the Principles of Selecting IPAR’s Quality Controllers’, (4) the technical guidance ‘On Reviewing the Quality of Auditor’s Reports’, and others. (Dolotenkova, 2001)

IPAR quality controllers reviewed audit files, internal audit manuals and other documentation relating to specific audit engagements to ascertain compliance with internationally oriented auditing standards, ethical principles and state licensing requirements. The controllers were selected from certified auditors of member firms with prior quality control experience. Those applying to become a quality controller needed to undertake training and obtain a certificate from the association to conduct reviews. Yet, unlike their prototypes in the West, the peer reviews were not so much used to control, oversee and, where appropriate, discipline members. Participation in them was voluntary and largely inconsequential. Rather, they were offered by the association as a service to their members, so that they could mutually learn from each other and enhance their expertise, if wanted. Particularly large Russian firms were key promoters: Large audit firms that are members of the association simply decided to impose upon themselves oversight measures. It was their voluntary decision. They helped the associations like ours to define and carry out quality control based on their firms’ internal practices, they also travelled around the country to teach others. (Presentation, Daria Dolotenkova, ‘Implementation of Auditing Reform’ Conference, Moscow, 2005)

Ties with foreign counterparts played an important role in enabling the development of expertise to conduct peer reviews. A president of another professional association emphasized cooperation with the Compagnie Nationale des Commissaires aux Comptes, a French professional accountancy body, in establishing their peer review scheme.

As noted, the peer reviews were not so much a mechanism that allowed professional associations to systematically enhance oversight across the board. But they were instrumental for the creation of pockets of expertise; and they could be used by the associations to set themselves and their members apart from the ‘audit riffraff’, including quack auditors. Furthermore, the peer reviews allowed professional associations to demonstrate self-regulatory capacity vis-a-vis the government which, at that time, lacked resources, particularly expertise and an administrative apparatus, to implement effective audit oversight arrangements. Comments below show that this view was shared not only by the associations and their members but also within government circles: The Finance Ministry has not the personnel [to run audit inspections]. You need a lot of people to check the 40,500 licence holders that we currently have […]! They [the Ministry] don’t have the proper methodology [for audit oversight] either. (President of Professional Association D, Moscow, 2001) It is clear that the government needs relevant resources and expertise to do this [audit inspections] to be the regulator, the thought leader, to show direction. […] Realistically, the Finance Ministry alone cannot achieve this. (Deputy Director of a large Russian audit firm, Moscow, 2001) There are important roles to play for self-regulatory professional associations, one is the authority to oversee [audit] quality. (Official from the Finance Ministry’s Research Institute, Moscow, 2001)

Whereas the Temporary Rules did not contain any specific audit oversight provisions, this was changed with the adoption of the Federal Audit Law which replaced the Temporary Rules in August 2001. Work on the law had already begun in the 1990s with significant input from international organizations, including the World Bank and European Commission (via their Tacis Audit Reform project whose primary beneficiary was the Ministry of Finance). Alongside these organizations, national professional associations were actively involved in the drafting and debating of the law. Their claim to authority as knowledgeable experts and legitimate representatives of the audit profession were evident at a working group meeting in February 2001, set up to debate the draft law. Here, one of the authors observed how the opening speech of the TsALAK official from the Ministry of Finance was quickly aborted by a representative from one association with: ‘Bureaucrats will speak later, first the professionals.’ The interview excerpt below provides additional insight into the power dynamic surrounding the debate: The Government and Duma do not have many audit experts; they are not equipped to make judgements as to which [audit] law draft is better, what will work and what won’t work. So, the professional associations then have to tell them, ‘Do this, and don’t do that’! (Head of International Audit in a large Russian audit firm, Moscow, 2001)

The professional associations and their [firm] members gained political support for private peer reviews from international counterparts (Samsonova, 2009). In particular, the European partners in the EU-funded Tacis Audit Reform project pointed to the lack of widely accepted peer review mechanisms as a threat to public confidence in Russian auditing. 2 Similar views were also voiced in our interviews by members of international audit firms in Russia who expressed preference for self-regulation.

The first Federal Law on Auditing was signed by President Putin in August 2001. The Law formally delegated to professional associations a range of regulatory duties, including the responsibility for monitoring the quality of audit work. Article 20 of the Law stated that professional associations: […] perform independently, or as delegated by the federal agency, quality control for their members, [and] take disciplinary actions.

Through the provisions of the Law, the government effectively granted a formal status to the private voluntary audit oversight arrangements. While formally recognizing the primary role of the associations in enacting such arrangements, the Law, however, also contained the following Article: The system of external oversight over auditors and audit firms is established by the authorized federal agency which can perform the quality inspections independently but can also delegate such inspections to accredited professional associations which can implement the process for their members. (Federal Law on Auditing, 2001, Art. 14)

A reference to ‘accredited professional associations’ indicates that, while extending the associations’ regulatory remit, the system of regulation was not fully ‘privatized’. The government retained a form of residual control through provisions introducing a government-administered accreditation of the associations. Further, a reference to the ‘authorized federal agency’ effectively provided a ‘back door’ for government actors to re-emerge as a dominant force and, if necessary, impose an additional layer of state-administered oversight at any point in the future. It has to be noted, however, that the Law itself did not contain any explicit detail about the nature of such oversight arrangements, nor did it specify through what organizational infrastructure these would be enabled. But the Law opened up possibilities for more legislative detail in the future, for example through Presidential Decrees and Ministerial Resolutions.

In sum, the early post-Soviet government lacked both knowledge and administrative capacities to either define or execute audit oversight. These limits of the government with regard to both rule development and enactment coupled with significant interpretational freedoms arising from the vague nature of the Temporary Rules enabled professional associations to engage in rule conversion (Mahoney & Thelen, 2009; Streeck & Thelen, 2005) and mobilize the law (in our case Temporary Rules) as a resource in pursuit of their own interests. Paraphrasing Streeck and Thelen (2005, p. 26), we could say that the Temporary Rules were reinterpreted to ‘fit the interests of new actors’, in our case the newly formed professional associations and their goals of organizational self-preservation and regulatory expansion. The 2001 Federal Audit Law can be seen as formally entrenching this new status quo. The above demonstrates new veto possibilities acquired by the profession (professional associations and their [firm] members) vis-a-vis government actors, as part of wider processes of post-Soviet market-oriented transformation. Yet, at the same time, the Law also provided government actors (in our case the Finance Ministry) with new possibilities for intervention and expansion (e.g. in providing for the creation of an ‘authorized federal agency’ to oversee the profession’s activities). In other words, the Law enabled elements of public surveillance to be ‘layered’ (Mahoney & Thelen, 2009) onto the evolving private forms of audit oversight as a means to ensure that, although delegated to private actors, the enactment of audit oversight could be ultimately controlled and, if necessary, revisited by the government.

Re-regulating audit oversight: Towards the 2008 Audit Law

The 2001 Law had laid the foundation for the formal institutionalization of self-regulation. It had also set parameters for further professional consolidation by stipulating that professional associations should not have fewer than 1,000 certified auditors and/or 100 licensed audit firms, thereby withdrawing the breeding ground for small associations. At some point there were more than 100 associations.

3

Details of the accreditation process were set out in guidance prepared by the Ministry of Finance in cooperation with the associations (particularly, IPAR and RCA)

4

demanding that any accredited association followed generally accepted auditing standards, a code of ethics, and procedures for audit quality control (e.g. through peer review). As the president of a professional association stated: The Law put quality control on the agenda. […] We first started with quality controllers, with the decision on who can be a quality controller. We developed a set of requirements for these people. We then realized that we needed to certify them. So, we conducted controller certification in all major cities where we had our branches. This generated 150 controllers. We developed review programmes and had them approved by our Executive Team. (President of Professional Association C, Moscow, 2005)

Daria Dolotenkova, IPAR’s President, argued at the ‘Implementation of Auditing Reform’ conference in Moscow in 2005: Audit oversight [via peer reviews] was created by the associations [in Russia]. Without us, there would be no quality control [oversight].

Peer reviews had advanced to become an accepted mechanism of self-regulation, as the Law required all accredited associations to adopt audit quality control programmes that, among other things, could be based on peer reviews. By 2006, all six newly accredited associations had introduced in-house peer review systems. By that time, after years spent effectively on the sidelines of Russia’s audit regulatory scene, the Big Four international audit firms became more active. In 2004, both KPMG and PwC announced simultaneously their membership in the Russian Audit Chamber.

5

In addition, KPMG also joined IPAR. Until the adoption of the 2001 Law, the Big Four had not visibly participated in audit regulation debates. Yet, with the official recognition of professional associations as self-regulatory organizations this changed. The firms did not want to be left behind in the process of professional consolidation and sought to strengthen their and the associations’ positioning vis-a-vis government actors: A certain catalyst for this process was the bill providing for amendments to the [2001] Audit Law. We understood that if we did not convey our united view to the Ministry of Finance and the Duma, we could be kicked out of here, from this country. (Big 4 Partner and representative in a professional association, Moscow, 2008)

However, despite these developments, peer reviews did not come to work as a systematic, nationwide mechanism of professional control. In 2006, only 20 percent of Russian audit firms were reported to have undergone peer reviews, which could be seen as a direct result of the fact that under the Law professional membership remained voluntary (for both audit firms and auditors), and only member firms were subject to the reviews (Bikbaeva, 2006). Privately organized oversight was thus still patchy and fragmented. Besides, a survey of Russian auditors conducted by the Tacis project in 2006 revealed a common perception that peer reviews were concerned mainly with maintaining an appearance of conformity, also noting strong competition among associations over members and their poor public accountability (Tacis Audit Reform, 2007). Similar views were expressed by the European Commission in a report on Russian audit development (European Commission, 2006), which highlighted that many associations lacked authority with their members to conduct effective peer reviews. This is not surprising given the competitive environment surrounding the associations where attraction of members in terms of quantity (rather than quality) was what the Law had primarily stipulated.

In parallel, the Ministry of Finance had begun to reorganize itself. Following the Law, in 2002, the Ministry had signed statutes [polozhenie] to establish an Audit Council under its direction. The Council brought together representatives from government, professional associations, audit practitioners and academics to: gauge opinions from professional audit market participants in relation to questions concerning the formation and realization of government policies in auditing. (Ministry of Finance Resolution [prikaz] N 47H of 3 June 2002)

The Council was an organizational device that brought government actors closer to the profession, and vice versa. It exposed government officials to professional audit expertise and could be used as a platform to jointly work out audit oversight regulation. Also, within the Ministry of Finance new personnel with practical audit experience were hired. In 2004, Leonid Shneidman became the new Head of the Finance Ministry’s Department responsible for audit regulation. Prior to that he had spent twelve years with the Russian branch of PwC, where he had progressed from senior manager to partner. These changes enabled the state to build in-house administrative capacity close to, and drawn from, the audit market.

Shneidman introduced additional layers of (government) oversight over the profession, mobilizing and further specifying the Law (particularly Article 18 setting out functions of the abovementioned ‘authorized federal agency’). Under Shneidman’s leadership, resolutions regarding the governmental accreditation process and control of professional associations were issued (see Ministry of Finance Resolution [prikaz] N74H of 17 June 2005). Following these, the Ministry began to audit the peer review schemes of the associations. In 2006, the Ministry identified seven problem areas, including a lack of transparency in the selection of participants and reporting of review outcomes, and varying levels of expertise of peer reviewers (Ministry of Finance, 2007). A year later, it reported no improvement in the problem areas, while also noting competition among associations as one of the reasons for their unwillingness to apply a more rigorous peer review approach (Ministry of Finance, 2008).

Thus, over time, the government had become more sceptical about the associations’ capacity to self-regulate. Publicly showing up the weaknesses of the profession, the Ministry of Finance repositioned itself as a vigorous regulatory actor. This coincided with a major overhaul of the 2001 Audit Law, which reconfigured relations between government actors and the professional associations. In contrast to the drafting of the 2001 Audit Law, this time, the professional associations had a significantly diminished role in the development of the Law. As noted by the president of one association: The [new] version of the law under consideration was not discussed and not published on the MinFin’s [Ministry of Finance’s] site. We had to use unofficial sources [to exercise influence], which I consider wrong. There should have been a public discussion, at least with the professional associations. (President of Professional Association D, Moscow, 2008)

The amended Audit Law (Federal Law on Auditing, 2008), signed by Putin in December 2008, provided the legal basis for revising private audit oversight as a preferred mode of audit firm governance. First, the new Law, for the first time, specified the scope and objectives of peer reviews. It made professional membership mandatory for all practising auditors and audit firms and stipulated that all member firms are peer-reviewed every three years. The Law specified further that the federal agency should oversee the audits of public interest entities (listed or large companies, banks, insurance providers, pension funds), alongside the professional associations. Second, the Law contained provisions which required the professional associations themselves to be subject to regular (biennial) control reviews by the Ministry of Finance. It charged the federal agency with the task of maintaining a register of professional associations and their members. Third, the Law set out new membership thresholds for the professional associations (at least 700 certified auditors or 500 licensed audit firms).

Rationalizing the need for the overhaul, Finance Ministry officials stressed not only the capacity deficits of the self-regulating professional associations. They also appealed to the post-Enron realities in European countries as a legitimate reason for questioning the role of private actors (associations) in the conduct of audit oversight. The collapse of US energy giant Enron and the demise of its auditor Arthur Andersen in 2002 had led to a global rise of public audit oversight.

6

Andrey Krikunov, former Head of the Finance Ministry’s Department responsible for audit regulation, wrote in this respect: In our work, we should not lose sight of international developments. […] We have seen a series of transformative changes in matters relating to audit oversight taking place internationally and in regions, such as Europe, over the past four years. The global audit profession effectively has come to realize that audit oversight should be administered by the profession [professional associations, added] as well as organizations with public interest remit. (Krikunov, 2007, p. 85)

Government officials in charge of audit regulation emphasized that any oversight arrangement should be in the interest of the public. They saw state actors, rather than private actors, as legitimate guardians of the public interest: External audit oversight is better handled by the authorities because their role is to guarantee overall functioning of capital markets and the economy. If you look at the activities of the state in matters of audit oversight, they clearly lie within the public interest remit. (Leonid Shneidman, Krikunov’s successor)

7

The international developments presented the Russian government with an opportunity to legitimately reaffirm its sovereignty in matters of audit regulation. This was also in line with President Putin’s ongoing efforts to cultivate an image of the Russian government as assertive and a power to be reckoned with, also abroad. A rhetoric of ‘state revival’ was a common feature of the public discourse and assessments of the Russian political sphere at the time. 8

Prior to adopting the new Law, the Finance Ministry had at least initially been eager to soften the perceived impact of the changes on the associations by emphasizing ‘a significant extension of the role of associations in matters of audit quality’ (Shneidman, 2005). Subsequently, however, the Finance Ministry came to adopt a progressively tougher approach in its dealings with the associations. This continued after the 2008 Law had been enacted. Assessing the results of peer reviews conducted in 2009, the Ministry noted that, despite ongoing concerns over audit quality, only 3 out of 611 firms reviewed had been cautioned by their association (Ministry of Finance, 2010). In 2010, the government passed additional amendments to the 2008 Audit Law that entrusted a new ministerial agency, Rosfinnadzor [Russian Financial Oversight], operating under the Finance Ministry, with the task to conduct audit inspections of public interest entities. In many respects, the agency’s responsibilities paralleled the oversight function performed by the associations and included a remit to singlehandedly revoke audit licences, thus, bypassing the associations.

In summary, the worldwide public re-regulation of audit oversight in the post-Enron era enabled the government to call into question the self-regulatory remits of the national professional associations. Growing (governmental) evidence of the low effectiveness of peer reviews had tarnished the associations’ image as ‘experts’ of audit oversight, thereby diminishing their ‘veto possibilities’ with regard to interpreting, enacting and further developing the Audit Law (Mahoney & Thelen, 2009; Streeck & Thelen, 2005). The associations’ weakening veto possibilities were in juxtaposition to a growing image of the Finance Ministry as a more astute regulatory actor, laying the groundwork for a shift from passive to more assertive government policy.

The 2008 Audit Law and subsequent 2010 amendments provided the government with a means for oversight re-regulation, granting government actors – the Finance Ministry and Rosfinnadzor – a more defined and expansive role in overseeing the work of the associations as well as directly executing some of their oversight duties (e.g. with respect to inspections of public interest audits). Through the revised Law, government actors were now in a position to define not only what is a professional association but also what constitutes effective audit oversight. In this emerging layered infrastructure of oversight, they had reinserted themselves as a key player. The Finance Ministry had developed additional layers of oversight (accreditation, peer review inspection) that challenged the self-regulatory capacity of private associations. Prior literature has highlighted that amendments to rules initially supporting an institution may eventually come to challenge its very existence as new practices resulting from the amendments gain prominence (Streeck & Thelen, 2005, p. 24). In our case, such challenge has not led to a displacement, but to a governmental reframing of private audit regulation. On the one hand, self-regulating professional associations came to be more firmly embedded in Russia’s audit oversight architecture. 9 On the other hand, the Finance Ministry emerged as key orchestrator of the new public-private governance arrangements. Earlier privatization of audit regulation contributed to the subsequent strengthening of public authority not only in providing government organizations with a target of criticism against which they could re-legitimize governmental intervention. Privatization was also a resource that enabled the Finance Ministry to tap into market-oriented audit and regulation expertise (through the professional associations) while specifying and expanding its own remit.

Discussion and Conclusion

We trace a long-term process of institutional change to get to grips with dynamics of change in the composition and relative influence and capacity of public and private actors over time, focusing on the case of audit oversight re-regulation in post-Soviet Russia. We show how regulatory privatization can work as a means through which government actors (in our case the Russian Finance Ministry) can maintain or enhance their relevance and authority. We highlight the particular role of ‘legislative layering’ in this process. We define legislative layering as a process in which government actors, through laws and other forms of legislative provisions and guidance, introduce layers of regulation that build on and expand existing regulatory structures. Attention to legislative layering does not only help explore dynamics of change observed in the case of audit oversight reorganization in Russia. It is also of broader relevance, as it helps us rethink the relationship between organization, law and public-private regulation more generally.

First, it underscores that we should not treat law simply as an instrument of regulation, namely command and control, that sits next to, or interacts with, other regulatory instruments, such as private voluntary standards. Law can also function as an organizational resource, as a tool to reorganize ‘regulatory space’ (Hancher & Moran, 1989) and (re)build regulatory capacity (see here also Pedriana & Stryker, 2004; Lodge & Wegrich, 2014). Of course, law does not do that by itself. It shapes, and is shaped by, the actors mobilizing it – public and private. Second, the notion of legislative layering highlights the role of ‘the indeterminacy of the law’ (rule ambiguity) (Edelman, 1992; Halliday & Carruthers, 2007) in moulding public-private governance relations, and processes of regulatory capacity-building, respectively. It stresses the importance of attending to different types and levels of indeterminacy in law-making (law on the books) and law enactment (law in practice) (Abbott & Snidal, 2000; Bartley, 2011; Halliday & Carruthers, 2007). We need to be attentive to the influence of the form of law itself, and the dynamics and tensions unfolding between law-making and law enactment. Third, our study shows the relevance of both exogenous and endogenous factors, national and transnational processes and actors, in facilitating legislative layering and the building of regulatory capacity. In doing so, we also draw attention to the co-constituted nature of public-private regulation. We highlight that in public-private governance, state and non-state actors moderate and extend each other’s organizing influence and capacity to act.

Building on and extending Mahoney, Streeck and Thelen’s historical institutional framework (Conran & Thelen, 2016; Mahoney & Thelen, 2009; Streeck & Thelen, 2005; Thelen, 2009), we suggest that the manner in which government actors employ legislative layering as a resource, and the regulatory outcomes that ensue, are determined by the institutional properties of the regulatory regime itself (regulatory ambiguity/prescriptiveness), actors’ veto possibilities in law-making and law enactment, as well as exogenous factors, transnational events, actors and processes. We see the links between regulatory capacity, legislative layering and the historical institutionalist framework as two-fold.

First, capacity considerations shape the properties (ambiguity/prescriptiveness) of law, as law provisions are developed with a view of what can be enacted in principle. In our case, the 2001 Audit Law contained reference to, but not an explicit delineation of, the role of the government in the operation of audit oversight, which may be seen as a consequence of the Finance Ministry’s lacking resources (personnel, administrative and expertise) at the time. Here, maintaining ambiguity in what Abbott and Snidal (2000) termed ‘law on the books’ may be seen as a strategy that state actors employ to manage capacity-related deficiencies that would become apparent in ‘law in practice’.

Second, regulatory capacity, comprising both administrative resources (money, trained personnel, bureaucratic infrastructure) and legal capacity (statutory construction, legal interpretation) conditions the veto possibilities of public and private actors to secure continuity of regulatory arrangements. In public-private governance regimes, the mutually contingent nature of such veto possibilities is a feature of an often-dispersed regulatory set-up in which capacities required to maintain a given governance regime are shared between state and non-state actors.

As our case reveals, government actors’ veto possibilities are rarely secured purely on the basis of their legislative remit (the authority to develop law); they are also dependent on their problem-solving capacities, ability to enact law, and image as authoritative decision-maker. Government actors that depend on private actors for the delivery of public outcomes (such as audit quality) may seek to strengthen their political authority by developing coordination capacities that enable control, or that provide scope for future discretionary action to contain private actors or reassert public authority. Here, strategies of hands-on involvement give way to more layered, arms-length forms of influence to ensure that private governance retains accountability to government (see also Arellano-Gault et al., 2013). At the same time, such processes need not be one way; whether and how government actors will be able to exercise their veto possibilities and shape legislative layering in the future is dependent on the ongoing interactions between state and non-state actors, as well as developments in the transnational regulatory field (Djelic & Sahlin, 2009, 2012).

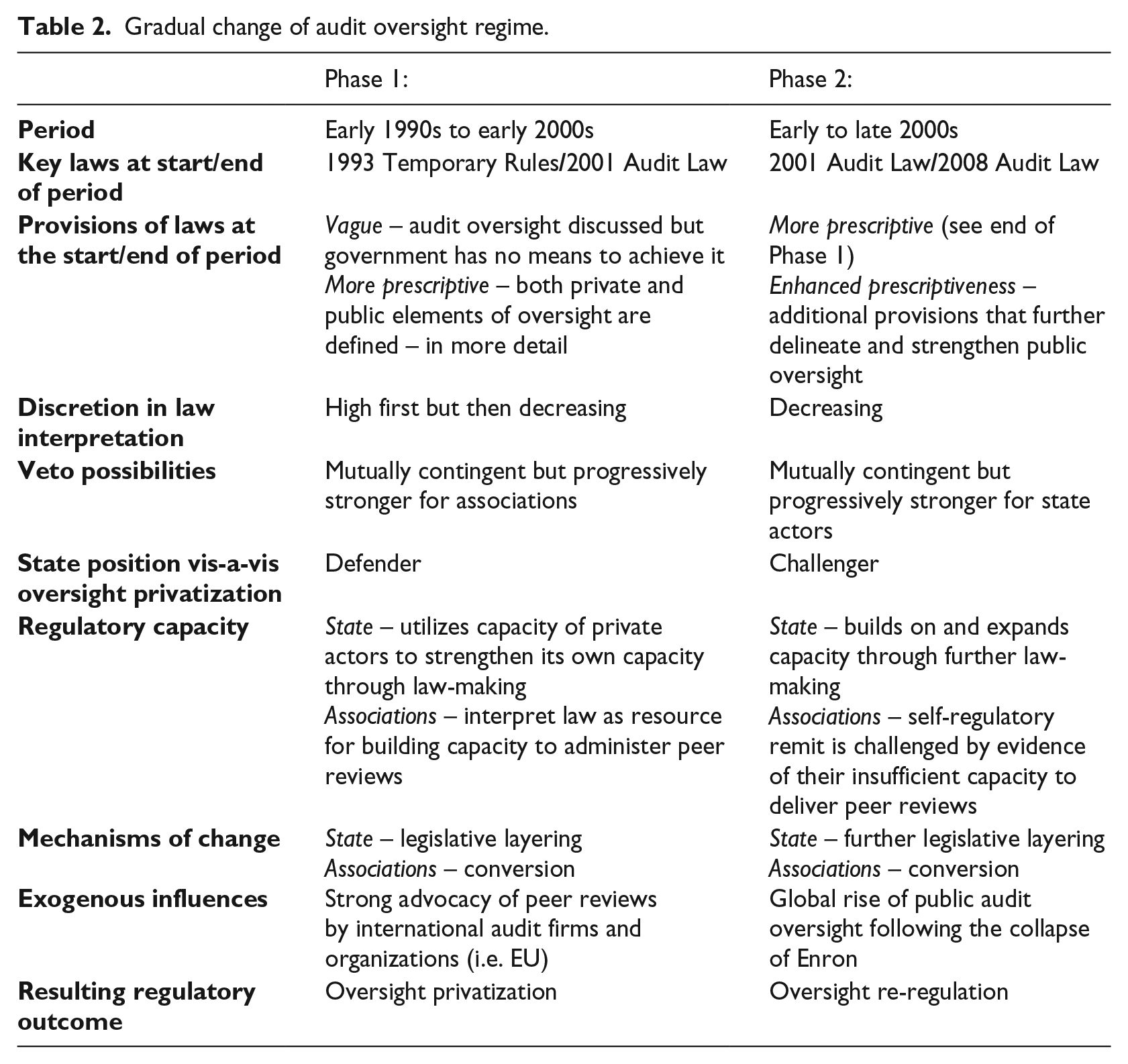

Table 2 shows how initially the ambiguity of the law (of the Temporary Rules and 2001 Audit Law) provided the professional associations with organizational and interpretational freedoms that allowed them to mobilize (convert) law in pursuit of their own, self-preserving interests (see Phase 1). The Finance Ministry maintained legislative provisions sufficiently vague to encourage the building of oversight capacity by the private actors themselves (professional associations and their members). For the associations, the experience and knowledge of member firms as well as exchange relationships with European counterparts played a major role in boosting their veto possibilities vis-a-vis government actors. The Big Four firms were motivated to join the associations and share their audit quality review expertise, thereby enhancing the associations’ capacity and reputation. All this helped the associations to represent themselves as effective administrators of audit oversight and a central hub for audit development.

Gradual change of audit oversight regime.

Phase 2, on the other hand, saw a progressive strengthening of the capacities and standing of government actors. The Finance Ministry re-established itself as a key audit regulatory authority. Progressive legislative layering, through the issuing of more detailed legal provisions (e.g. with regard to professional accreditation requirements), locked in more government-oriented regulatory strategies. The 2008 Law and subsequent statutory work, which established Rosfinnadzor as a recognized public regulatory actor, transformed the Finance Ministry into an operator of audit oversight alongside the associations. The Ministry engaged in a process of reorganization which involved, among other things, the inclusion of senior private sector auditors in its ranks to develop stronger in-house regulatory capacity. Furthermore, it was able to mobilize external resources in support of its changed regulatory strategy. A series of international events, spearheaded by the collapse of Enron, provided the Ministry with a legitimate blueprint against which it could rationalize and defend the shift from regulatory privatization toward oversight re-regulation vis-a-vis the profession.

Reflecting on the implications of these observations for our broader understanding of dynamics of incremental institutional change (Streeck & Thelen, 2005; Thelen, 2009), it is noteworthy that legislative layering and rule conversion remained key change mechanisms in both phases, yet they produced very different regulatory outcomes – oversight privatization in Phase 1 and re-regulation in Phase 2 (Table 2). The historical institutionalist framework puts much emphasis on ‘veto players’, next to ‘rule ambiguity’, as key drivers of change (or stability). Our study highlights the need to problematize, and further specify, the resources that afford such veto players their power (‘veto possibilities’). In the case studied here, important stimuli for institutional change came not only from within but also from without (the EU Tacis Programme, international audit firms, transnational audit scandals and resultant external legislative reforms, such as the Sarbanes-Oxley Act). These exogenous influences mediate (local) institutional change, the authority of governance actors and the legitimacy of their activities (Djelic & Sahlin, 2009, 2012). Such exogenous influences need to be conceptualized as important co-determinants of institutional change, as they shape actor constellations and their respective veto possibilities, as well as the form that mechanisms of legislative layering and conversion take.

Further, we would like to point out that in our case neither government nor private actors were in a position to unequivocally dominate institutional change agendas. Although the government and the associations played different roles in the development and enactment of audit oversight rules in the respective phases studied here, neither could exercise exclusive control over the oversight regime. Instead, their veto possibilities were mutually contingent and reciprocally conditioned. Laws were mutually reinterpreted and layered rather than ‘displaced’. This points to the need to adopt a dynamic, relational approach when studying interactions between state and non-state actors in public-private governance regimes. Relations between state and non-state actors co-evolve over time; each acts as a (flexible) surround for the other (Abbott, 2005). In our case, regulatory privatization provided a fruitful ground for a subsequent strengthening of state actors. By readjusting its regulatory remit (first, as a proponent and then as a challenger of oversight privatization – see Table 2) the Finance Ministry was able to maintain continuity of regulatory provisions for audit quality enhancement. Change (through legislative layering) was a key means for it to preserve its influence, albeit in altered form.

To conclude, far from being a triumph of markets or a de facto displacement of the state, processes of regulatory privatization appear greatly reliant on public authority to be operational. Through legislative layering, state actors can shape the very possibilities of what may be achieved by private regulation, and the particular forms and modes in which it develops. Our study highlights the need to appreciate the multifaceted ways in which market-oriented neo-liberal governance is conditioned by public authority. This contributes not only to a better understanding of the vulnerabilities and limits of private/market governance, but also to the possible sources of the claimed revival of the government as a dominant regulatory actor.

Footnotes

Acknowledgements

We are grateful for the guidance we received from the special issue editors, Jeremy Moon, Marie-Laure Salles-Djelic, Arno Kourula and Christopher Wickert, and the three anonymous reviewers. Further, we thank Martin Lodge, Brendan O’Dwyer and Claire Garnier for their helpful comments. We have benefited from seminars at the University of Edinburgh Business School, HEC Montreal, University of Essex Business School, as well as the 32nd EGOS Colloquium in Naples, Italy, and the Critical Perspectives on Accounting Conference in Quebec City, Canada.

Funding

Anna Alon acknowledges the financial support from the Norwegian Research Council for the project ‘Internationalization of Financial Reporting and Auditing’.