Abstract

For four decades, stakeholder theory has played a key role in many research fields, from strategy to business ethics. More recent developments in the field of behavioral stakeholder theory highlight the importance of individual managers and their mindsets. The role of stakeholder theory mindsets of managers, however, has not been empirically investigated. Despite the prominence of stakeholder theory in management research, no measurement scale exists at the level of individuals that would allow scholars to assess the degree to which a manager agrees with the key assumptions of stakeholder theory. This research develops a scale to measure managers’ stakeholder theory mindsets. To do so, we followed scholarly best practices: First, we generated items based on existing stakeholder theory literature and then had expert stakeholder scholars evaluate them. This step was followed by two independent studies for exploratory and confirmatory factor analysis and a nomological network study. The actual scale development was complemented by an additional study, which tests the predictive power of the stakeholder theory mindset scale and demonstrates its incremental validity. As a result, we propose a validated measurement scale of stakeholder theory mindsets, consisting of 18 items that load on four factors corresponding to the four main assumptions in stakeholder theory: value creation, the integration thesis, jointness of stakeholder interests, and the responsibility principle. We draw out how future research can be inspired by using this scale, which inter alia allows testing antecedents of stakeholder theory mindsets, as well as consequences for managerial decision-making.

Introduction

Stakeholder theory is a prominent theory in management studies used across many research domains (Parmar, Freeman, Harrison, Wicks, Purnell, & De Colle, 2010). It offers a perspective on business ethics and organizational management that emphasizes the importance of considering the interests of a broad group of stakeholders—such as employees, customers, suppliers, communities, and shareholders—rather than prioritizing only one group, such as financiers. Stakeholder theory holds that business success and ethical responsibility are best achieved when a company creates value for its stakeholders (Freeman, Harrison, Wicks, Parmar, & De Colle, 2010). Research on stakeholder theory is frequently based on the assumption that if managers endorse stakeholder theory, it will influence managerial decisions, for instance, in accounting (Miles, 2019; Mitchell, van Buren, Greenwood, & Freeman, 2015), strategy (Bosse & Sutton, 2019; Jones, Harrison, & Felps, 2018), and sustainability management (e.g., Hörisch, Freeman, & Schaltegger, 2014; Schaltegger, Hörisch, & Freeman, 2019). For example, in the context of accounting, Mitchell et al. (2015) and Hall, Millo, and Barman (2015) argue that managers endorsing the key argumentation of stakeholder theory would enlarge the scope of what information is reported by companies and for whom.

However, empirical research on the impact of stakeholder theory on managerial choices and behaviors has been limited. Existing quantitative research on stakeholder theory primarily addresses the organizational level (Brulhart, Gherra, & Quelin, 2019; El Akremi, Gond, Swaen, Roeck, & Igalens, 2018) and not the level of individual managers and their decision-making. Furthermore, the scarce existing individual-level research on stakeholder theory does not consistently relate to the content and argumentation of stakeholder theory but to other aspects, such as the salience of specific stakeholder groups (e.g., Agle, Mitchell, & Sonnenfeld, 1999; Wang & Juslin, 2013).

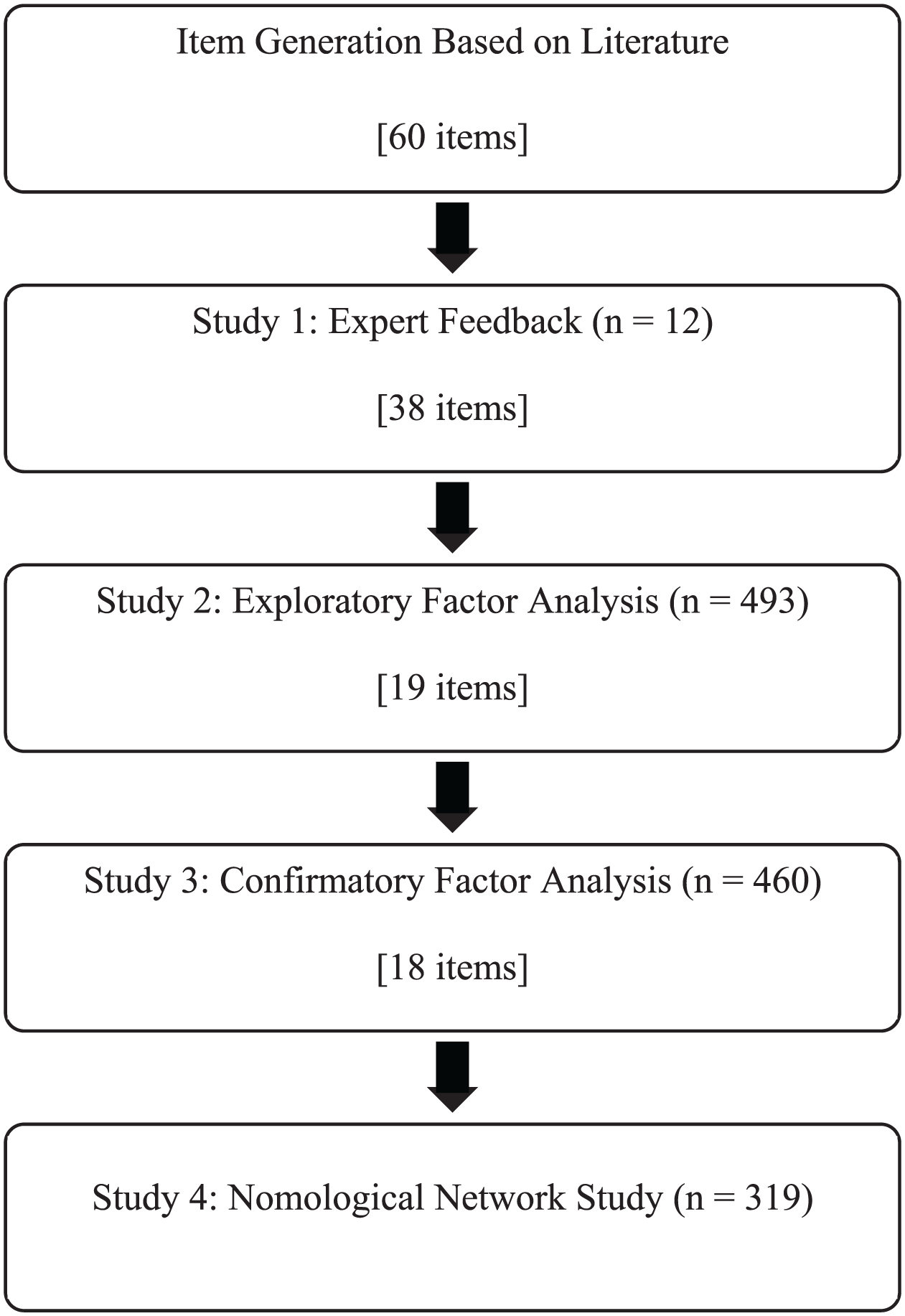

To overcome these research gaps and to enable testing of the impact of stakeholder theory on individual managerial choices and behaviors, it is necessary to be able to measure the degree to which an individual follows the key argumentation of stakeholder theory, that is, whether an individual manager adopts a stakeholder theory mindset. Thus, the purpose of this research was to create a scale to measure a manager’s stakeholder theory mindset. To develop and validate this measurement scale, five sequential steps were implemented based on best practices for scale development (see DeVellis, 2017; Spieth, Röth, Clauss, & Klos, 2021; Tabachnick & Fidell, 2013; Worthington & Whittaker, 2006). First, we generated a broad list of survey items based on extant stakeholder theory literature. Second, this list was evaluated by 12 stakeholder theory experts. Third and fourth, an exploratory factor analysis was conducted, followed by a confirmatory factor analysis; together, they determined the final list of measurement items. Fifth, we assessed the scale’s construct validity with a nomological network study in which we compared our stakeholder theory mindset scale against established related scales to evaluate its novelty. Subsequent to developing and validating the scale, in a final step, we also validated its predictive power using the example of managers’ corporate social responsibility (CSR) decisions, and demonstrated our scale’s utility.

We argue that providing a measurement scale for stakeholder theory mindsets is critical for the following four main reasons. First, our scale operationalizes a core but previously underspecified construct in stakeholder theory—managerial stakeholder theory mindsets—and thus helps in translating abstract theoretical ideas into a form that can be systematically observed, tested, and refined. To do so, we distill four key assumptions of stakeholder theory that have been brought forward by prominent stakeholder theory studies and distinguish stakeholder theory from a shareholder-centered view of corporations (Dmytriyev, Freeman, & Hörisch, 2021; Freeman et al., 2010; Freeman, Dmytriyev, & Phillips, 2021; Hörisch et al., 2014): (1) the integration thesis (proposing that business and ethics are fundamentally linked), (2) the responsibility principle (postulating that in general managers are willing to and do accept responsibility for their decisions that affect others), and the propositions (3) that the purpose of a business is value creation for its stakeholders and not only its financiers and (4) that stakeholders of a business share joint interests. By building on these four key assumptions, the measurement scale developed in this research ensures a fit between what is measured and what stakeholder theory articulates as core assumptions instead of using proxy variables based on available data and measurement constructs, which can be more or less (un)related to the actual core of stakeholder theory.

Second, through the identification and validation of distinct dimensions of stakeholder mindsets, our work contributes to the conceptual clarity of stakeholder theory, resolving ambiguity and enabling more precise theorizing. For example, the scale allows a better understanding of the relative importance of the four assumptions for different types of managerial choices.

Third, the availability of a valid measure allows future research to empirically test stakeholder theory propositions, explore the antecedents and consequences of stakeholder mindsets, and examine boundary conditions and contextual influences. Such research might be particularly helpful to test propositions brought forward in the emerging fields of behavioral stakeholder theory (see Bridoux & Stoelhorst, 2014; Bundy, 2019; Qian, Crilly, Lin, Zhang, & Zhang, 2023; Qian, Crilly, Wang, & Wang, 2021), “new stakeholder theory” (see Barney, 2018; McGahan, 2021), and stakeholder governance (Bridoux & Stoelhorst, 2022; Klein, Mahoney, McGahan, & Pitelis, 2012). Indeed, an increasing number of authors have highlighted the importance of individuals and their mindsets, beliefs, and perceptions for managerial and organizational decision-making (e.g., Buhr & Weissbrod, 2025; Gond, El Akremi, Swaen, & Babu, 2017; Hafenbrädl & Waeger, 2017; Shea & Hawn, 2019). For instance, in their systematic literature review, Gond et al. (2017) identified a need for new measurement constructs on drivers of CSR on the individual level, as the existing constructs lacked conceptual clarity, and there is a need for additional and more theoretically relevant constructs that might explain differences between individual managers with regard to their reactions to CSR. In this sense, our scale provides a foundation for middle-range theory development within the domain of stakeholder theory.

Fourth, by clarifying how stakeholder theory mindsets differ from adjacent constructs (e.g., CSR mindsets and ethical mindsets), this research sharpens theoretical boundaries and enriches the stakeholder theory nomological network. Our scale also provides a mechanism to measure the effectiveness of these adjacent constructs, which are frequently used as proxy variables, by measuring how correlated they are with an individual manager’s endorsement of the fundamental assumptions of stakeholder theory. In so doing, this research shows that the stakeholder theory mindset scale is distinct from these existing proxies and has increased predictive validity using the example of CSR decisions.

Theoretical Background

The Core of Stakeholder Theory and Its Relevance to Management Research

Stakeholder theory has earned a longstanding, esteemed place in research. Often, the seminal work by Freeman (1984) is widely noted as the starting point of stakeholder theory, while the notion of stakeholders is even older (Silbert, 1952). In 2010, some of the most prominent authors in the field (Freeman et al., 2010) synthesized state-of-the-art stakeholder theory. They concluded that stakeholder theory reframes the firm as a system of stakeholder relationships built on value creation, ethics, and shared purpose. Thus, from a stakeholder theory perspective, business is fundamentally about creating value for stakeholders relevant to a given business. Stakeholder theory has been further extended and complemented, introducing distinct variants and extensions of stakeholder theory, such as stakeholder agency theory (Hill & Jones, 1992); instrumental, normative, and descriptive stakeholder theory (Donaldson & Preston, 1995); new stakeholder theory proposed by McGahan (2021, 2023); and behavioral stakeholder theory (Bridoux & Stoelhorst, 2016, 2022; Crilly, 2019).

In contrast to other theories in management, in all variants of stakeholder theory, the unit of analysis is not the business itself, but the relationship between a business and its stakeholders—in other words, those “groups and individuals who can affect or are affected” (Freeman et al., 2010: 5) by the focal business, such as customers, employees, suppliers, and financiers. This unit of analysis has implications for business decisions. Freeman et al. (2010: 7) suggest that business decisions involve the following questions: “(1) If this decision is made, for whom is value created and destroyed? (2) Who is harmed and/or benefited by this decision? (3) Whose rights are enabled and whose values are realized by this decision (and whose are not)?” To predict how managers who adhere to stakeholder theory would address such questions, it is essential to understand its key assumptions of stakeholder theory. Therefore, we analyzed key sources on stakeholder theory (e.g., Dmytriyev et al., 2021; Freeman et al., 2010) to distill the key assumptions (see also Bridoux & Stoelhorst, 2022; Clarkson, 1995; Donaldson & Freeman, 1994; Freeman, 2017; Freeman & Newkirk, 2008; Freeman, Wicks, & Parmar, 2004; Goodstein & Wicks, 2007; Harris & Freeman, 2008; Laplume, Sonpar, & Litz, 2008; Sulkowski, Edwards, & Freeman, 2018). These assumptions form the basis of our measurement approach, ensuring that the measurement approach is consistent with the content and argumentation of stakeholder theory. The four key assumptions are described in the following paragraphs.

First, the integration thesis in stakeholder theory postulates that “almost any business decision has some ethical content” (Freeman et al., 2010: 6). Thus, stakeholder theory explicitly rejects the idea that decisions are either business decisions or ethical decisions (which has been called the separation fallacy; Harris & Freeman, 2008). The integration thesis challenges the assumption of “value-free economics and science” (Freeman et al., 2010) and argues that most human decisions (including managers) are complex (Donaldson & Freeman, 1994; Freeman & Newkirk, 2008).

Second, the responsibility principle in stakeholder theory states that “most people, most of the time, want to, and do, accept responsibility for the effects of their actions on others” (Freeman et al., 2010: 8). Therefore, the theory encompasses a conception of people, particularly business people, which is social and thus distinct from a purely asocial homo economicus conception, as, for example, implied by Friedman (1970). As Dmytriyev et al. (2021) point out, the responsibility principle in stakeholder theory not only considers companies responsible for their stakeholders but also argues for bidirectional responsibility, as stakeholders also bear responsibility toward businesses (see Goodstein & Wicks, 2007).

Third, the unit of analysis used in stakeholder theory and the open questions it suggests for business decisions imply that the purpose of a business is value creation for stakeholders rather than only for shareholders (Bridoux & Stoelhorst, 2022; Dmytriyev et al., 2021; Freeman et al., 2010). Stakeholder theory thus clearly goes beyond the shareholder view, which, according to its proponents, holds that companies exist for their financiers and therefore identifies increasing or even maximizing shareholder value as the purpose of business (e.g., Friedman, 1962; Sundaram & Inkpen, 2004a, 2004b). In contrast, stakeholder theorists assume that the purpose of companies is to create value for a broad group of stakeholders, which is what enables company success (Clarkson, 1995; Freeman et al., 2004; Laplume et al., 2008). This core assumption of value creation for all stakeholders has stimulated an extensive debate on whether all groups of stakeholders should receive an equal amount of value, whether the purpose of stakeholder theory is to reallocate the value created to make this happen (e.g., Marcoux, 2000; Freeman et al., 2004), and whether all stakeholders need to be treated equally (e.g., Gioia, 1999; Marcoux, 2000; Sternberg, 2019). However, the core assumption of value creation for stakeholders is not about the redistribution of value created by one group of stakeholders to another. It is about the aim of managers at harmonizing the interplay of stakeholders in such a way that value is created for all stakeholders in the first place (i.e., in and with value creation processes), that the procedure of value distribution is fair, and that it does not destroy value for other stakeholders (Freeman et al., 2004, 2010).

Fourth, stakeholder theory is distinct from viewing business as competition (see Porter, 1980). Instead of focusing on competition and potentially conflicting interests among stakeholders, Freeman et al. (2010: 15) argue that “the extent to which the interests of customers, suppliers, employees, financiers, and communities go together” is frequently underestimated. Thus, managers need to recognize this jointness of stakeholder interests and enable joint value creation based on common values (e.g., Freeman, 2017; Sulkowski et al., 2018). Consequently, Freeman (2017: 6) summarized that “[s]takeholder interests are joint. That is why business works.”

While these four core assumptions are distinct, they are interrelated. If managers reject the idea that decisions are either business decisions or ethical decisions (integration thesis), this will have consequences for their willingness to accept responsibility for the effects of their own actions on others (responsibility principle). Endorsing the responsibility principle, in turn, is more likely to create constellations among stakeholders that create value for all involved stakeholders (value creation) and for managers’ perspectives on whether stakeholder interactions are based on competition or joint interests (joint interests). From a conceptual perspective, the four core assumptions can be regarded as dimensions jointly forming the overall construct of a stakeholder theory mindset. Empirically, we do not yet know whether these four assumptions co-occur and have limited knowledge of their relative strength in different contexts.

The importance of these core assumptions of stakeholder theory is reflected in their uptake. Indeed, these assumptions are compatible with the emerging stakeholder theory extensions of behavioral stakeholder theory and new stakeholder theory. Relating to the integration thesis, behavioral stakeholder theory (Bundy, 2019; Crilly, 2019; Keevil, 2014) emphasizes that stakeholders care about perceptions of identity, values, moral beliefs, fairness, and trust and thus not just economic performance outcomes (Freeman & Phillips, 2002; Phillips, 2003). Furthermore, new stakeholder theory and stakeholder strategy theory (Barney, 2018; McGahan, 2021, 2023; Parmar et al., 2010) discuss the purpose-driven, inclusive, and long-term strategic character of businesses; links among stakeholder theory, firm performance, and competitive advantage (Harrison, Bosse, & Phillips, 2010); and that profit is an outcome rather than the sole aim of business (Freeman et al., 2010; Mayer, 2021). Likewise, with regard to the responsibility principle, behavioral stakeholder theory highlights that perceived fairness and reciprocity can help shape dynamic, evolving relationships through social norms, experiences, and trust-building (Bosse, Phillips, & Harrison, 2009; Bridoux & Stoelhorst, 2016; Bundy, Vogel, & Zachary, 2018). Stakeholder decisions are characterized by bounded rationality, social influences, emotions, and cognitive biases and are influenced by how management decisions are made (Bundy, 2019). Companies therefore seek to negotiate a “shared social performance reference point with stakeholders who identify with the organization and care about social performance” (Nason, Bacq, & Gras, 2018: 259). Similar to the key assumptions on joint interests and value creation for stakeholders in stakeholder theory, “new stakeholder theory” and stakeholder strategy theory highlight that companies are not just short-term, profit-oriented, and shareholder-centric entities but are long-term, purpose-driven organizations embedded in society (McGahan, 2021, 2023). Furthermore, emphasis is placed on stakeholders not just being individual groups with isolated interests but interconnected entities in dynamic systems (Bridoux & Stoelhorst, 2022; Bundy et al., 2018; Parmar et al., 2010). Mayer (2021), as well as Freeman et al. (2010), therefore emphasizes relationships, networks, and the co-creation of value (Freeman et al., 2010; Mayer, 2021; Ni, Qian, & Crilly, 2014; Qian et al., 2021). Likewise, behavioral stakeholder theory emphasizes shared value creation rather than managers weighing stakeholder interests and profit redistribution (Bridoux & Stoelhorst, 2022; Freeman & Phillips, 2002).

Discussions on stakeholder theory and its core assumptions have also stimulated many other research fields, such as strategic management, business ethics, sustainability management, and CSR. Frynas and Yamahaki (2016) found that stakeholder theory is the most frequently used theory in CSR research. According to Frynas and Yamahaki (2016), stakeholder theory in a CSR context is mainly used to argue that CSR is driven by an organization’s external stakeholders, thus leaving ample room for research analyzing stakeholder theory as an internal driver of CSR via the mindsets of managers.

Current Measurement Approaches in Quantitative Stakeholder Theory Research

Given the importance of stakeholder theory in management research, several approaches to measurement have been used. In this section, we highlight key approaches, while Appendix A provides a more detailed overview of the existing approaches. None of the current approaches directly measure an individual manager’s endorsement of the four key assumptions of stakeholder theory.

First, most existing quantitative management research on stakeholder theory deals with the organizational level. The first group of such studies uses measurement strategies that aim to understand managers’ perceptions of their organization. These studies direct questionnaires to managers, asking them to assess the degree of stakeholder orientation of the business or organization for which they work (e.g., Brulhart et al., 2019; Maignan, Gonzalez-Padron, Hult, & Ferrell, 2011; Yau, Chow, Sin, Tse, Luk, & Lee, 2007). Among these studies, Maignan et al. (2011) probably come closest to addressing the four key assumptions in stakeholder theory, as their approach captures the dimensions of stakeholder norms, values, artifacts, and stakeholder-oriented behavior.

A second group of quantitative studies using stakeholder theory at the organizational level assesses employees’ perceptions of corporate responsibility (e.g., El Akremi et al., 2018; Parmar, Keevil, & Wicks, 2019; Parmar, Wicks, & Ginena, 2024; Turker, 2009). These strategies assume that specific behaviors are indicative of endorsing the assumptions of stakeholder theory, and they use the perceived degree of those behaviors as a proxy for the adoption of stakeholder theory.

A third approach to quantitatively assess stakeholder theory in extant research is to use publicly available data or data provided by commercial databases. Examples include Gonzalez-Padron, Hult, and Ferrell (2016), who use the frequency with which a company mentions stakeholders in its sustainability report as a measure of stakeholder orientation, and Berman, Wicks, Kotha, and Jones (1999), who use data provided by Kinder, Lydenberg, Domini, and Company (KLD) on selected socially responsive actions of a firm.

Finally, a fourth group of authors does not attempt to measure stakeholder theory on the level of organizations, but uses vignette studies to manipulate the participants’ perceived stakeholder orientation of companies (e.g., Parmar et al., 2019, 2024).

In summary, multiple measurement approaches to stakeholder theory exist that focus on the organizational level. In line with these relatively numerous examples of stakeholder theory being used in quantitative research at the organizational level, Frynas and Yamahaki (2016) show, with a systematic literature review on different drivers of CSR, that stakeholder theory has been the most frequently applied theory when it comes to analyzing external drivers of CSR. Research on internal drivers, including the individual level of managers, has used stakeholder theory far less often (Frynas & Yamahaki, 2016). This is an indication that the individual manager’s mindset concerning the key assumptions of stakeholder theory remains underexplored.

As no validated approach for measuring the key assumptions of stakeholder theory on the individual level appears to exist, many quantitative studies on the individual level have mainly used validated constructs related to, but still distinct from, stakeholder theory mindsets. Ford and McLaughlin (1984), for example, suggested a measurement construct for the concept of CSR mindsets. The Perceived Role of Ethics and Social Responsibility (PRESOR) scale by Singhapakdi, Vitell, Rallapalli, and Kraft (1996) attempts to measure three factors: social responsibility and profitability, long-term gains, and short-term gains. Hunt, Kiecker, and Chonko (1990) developed a scale on socially responsible attitudes among managers that covers the degree to which managers place an emphasis on the interests of society at large or on shareholders. Lastly, the ethical mindset scale brought forward by Issa and Pick (2010) aims to capture the importance managers ascribe to business ethics, along with the components aesthetic judgment, contentment, harmony, and balance, individual responsibility, optimism, professionalism, spirituality, and truth-telling.

The relatively few existing papers that analyze stakeholder theory (and not a related construct) on an individual level measure an orientation toward stakeholders in general, rather than a manager’s mindset in relation to the core assumptions of stakeholder theory (i.e., the integration thesis, the responsibility principle, value creation as the purpose of business, and the idea of joint interests between stakeholders). For instance, Wang and Juslin (2013) measured how important managers deem specific stakeholder groups. Janani, Christopher, Nikolov, and Wiles (2022: 460) used the marketing experience of CEOs as a proxy for “corporate social performance-supportive mindsets in line with stakeholder theory.” Obviously, such proxies do not relate to the four core assumptions and thus do not address the key assumptions, content, and argumentation of stakeholder theory.

This also applies to one of the most prominent example of surveys addressing stakeholder theory on the individual level: the research of the Global Leadership and Organizational Behavior Effectiveness (GLOBE) Project. It surveys the values of CEOs, differentiating between economic values and stakeholder values. This approach was adopted, for instance, by Agle, Mitchell, and Sonnenfeld (1999); Sully de Luque, Washburn, Waldman, and House (2008); and Washburn, Waldman, Sully de Luque, and Carter (2018), who used the five items on the stakeholder values of CEOs. These items indicate how much importance CEOs ascribe to different stakeholder groups and the aspects related to these groups. Exemplary items include rating the importance of employee relations issues, the welfare of the local community, and/or the effect on the environment. These five items, however, do not relate to the core assumptions of stakeholder theory, such as the integration thesis (i.e., proposing that business and ethics are fundamentally linked). Like all measurement approaches dealing with stakeholder theory on the individual level, the items included in the GLOBE study do not emanate from a scale development process designed to capture the key assumptions of stakeholder theory. Likewise, these scales have not been validated. Therefore, it is impossible to judge whether they actually measure what they claim to measure and whether they show sufficiently high levels of reliability. To sum up, a review of existing measurement approaches for stakeholder theory at the individual level reveals that stakeholder theory mindsets are so far an underspecified construct in stakeholder theory.

The Necessity of a Measurement Scale for Stakeholder Theory Mindsets

As summarized in the previous section (see also Appendix A), the individual level of analysis has so far received scant attention in quantitative stakeholder theory research. No measurement approach exists that measures an individual manager’s endorsement of the key assumptions that stakeholder theory has laid out in the conceptual literature. Still, providing a measurement scale for stakeholder theory at the individual managerial level is of high importance for the three main reasons described in the following paragraphs.

First, organizational outcomes are strongly influenced by the decision-making of managers. In many fields of management research, such as CSR and sustainability management, accounting, and strategy, different authors highlight the importance of individuals’ beliefs, perceptions, and mindsets for managerial and organizational decision-making (e.g., Buhr & Weissbrod, 2025; Gond et al., 2017; Schaltegger & Burritt, 2018; Shea & Hawn, 2019). Using the context of CSR decisions, Hafenbrädl and Waeger (2017) highlighted the importance of managers’ beliefs and ideologies for explaining their CSR-related behavior. Likewise, Gond et al. (2017) used a systematic literature review to highlight the role of individuals in CSR. Specifically, they identified a gap in the theoretical explanations for the reaction of individuals to CSR challenges. Developing a scale that captures stakeholder theory at the managerial level would help address this gap. Likewise, the emerging field of behavioral stakeholder theory (e.g., Bridoux & Stoelhorst, 2022; Bundy, 2019; Crilly, 2019; Keevil, 2014) also highlights the importance of individuals. It is based on psychological realism by recognizing that stakeholders do not just react to economic incentives and are not always rational, utility-maximizing actors (Bridoux & Stoelhorst, 2022; Phillips, 2003). Instead, stakeholder perceptions about fairness, trust, and legitimacy can differ (Bridoux & Stoelhorst, 2014; Hosmer & Kiewitz, 2005) and matter as they can influence decisions and actions (Jones, 1995). Thus, behavioral stakeholder theory aims to generate micro-foundational explanations of the relationships between firms and their stakeholders to understand why different firms and stakeholders react differently to various stakeholder pressures and interactions. Therefore, it examines processes within the firm and investigates the characteristics of individual managers that influence their reactions to stakeholder needs (Bridoux & Stoelhorst, 2022; Crilly, 2019). Behavioral stakeholder theory requires different methods than more conventional stakeholder theory research at the organizational level, such as experiments or laboratory studies (Crilly, 2019). Developing a validated scale for measuring the degree of a manager’s endorsement of stakeholder theory will be an important enabler for conducting such novel forms of quantitative research on stakeholder theory and will help to understand the processes underlying behavioral stakeholder theory.

Second, understanding managers’ mindsets is critical for many practical interventions, for instance, regarding management education (Cullen, 2020; Passarelli, Boyatzis, & Wei, 2018). Thus, developing a measurement scale that captures managers’ endorsement of stakeholder theory at the individual level allows scholars to test and evaluate interventions for fostering their endorsement and developing meaningful practical implications.

Third, based on the criteria of Edmondson and McManus (2007) for the maturity of a research field, stakeholder theory research has room to grow toward higher levels of methodological maturity, particularly regarding stakeholder theory research on the individual level. They described mature theory research as that which builds on quantitative data, relying on existing measurement constructs used in surveys to test formal hypotheses on focused questions. However, no established measurement scale exists for quantifying stakeholder theory at the individual level, which would allow survey research that tests formal hypotheses.

To capture the endorsement of stakeholder theory at the individual level, we use the concept of manager mindsets. Managers’ mindsets, also sometimes referred to as implicit theories, refer to the internalized beliefs that managers use daily in their sensemaking (Kouzes & Posner, 2019; Molden & Dweck, 2006). Thus, the mindsets of managers are of crucial importance in their decision-making (e.g., Abernethy, Anderson, Nair, & Jiang, 2021; Araujo, Picavet, Sartoretto, Dalla Riva, & Hollaender, 2022; Jiang, Zalan, Tse, & Shen, 2018). A manager’s mindset is shaped by the individual’s personal core values as well as domain-specific beliefs and values (Jiang et al., 2018; see also Hay & Gray, 1974). Prominent examples of influential mindsets include a growth mindset (e.g., Abernethy et al., 2021; Dweck, 2016), ecocentric management mindset (Araujo et al., 2022), CSR mindset (Ford & McLaughlin, 1984; Jiang et al., 2018), and ethical mindset (Issa & Pick, 2010).

For the current research, we conceptualized the stakeholder theory mindset as a multidimensional construct about the four key assumptions of stakeholder theory as subdimensions. Therefore, a stakeholder theory mindset is defined by an individual’s beliefs in the key assumptions of stakeholder theory. Freeman et al. (2010) identified the mindsets of managers as one of the three main problems for rethinking business and emphasized the power of stakeholder theory in addressing this problem. Likewise, Wicks, Keevil, and Parmar (2012) acknowledged the importance of manager mindsets in a conceptual discussion and deduced possible implications from three mindsets with regard to implications for the environmental sustainability of a company.

In addition, in the emerging field of behavioral stakeholder theory (Bridoux & Stoelhorst, 2022; Crilly, 2019), the mindset of individual managers is of tremendous importance for explaining their decisions regarding stakeholder relationship management. A measurement scale for stakeholder theory mindsets would allow research to address the central question that behavioral stakeholder theory posits (i.e., understanding the behavior of individuals to explain why different firms react differently to stakeholder pressures and interactions).

Scale Development

Methodological Steps and Results

The process that we used for developing and validating a measurement scale for stakeholder theory mindsets followed a five-step procedure (Figure 1), which was in line with best practice recommendations for scale development (see e.g., DeVellis, 2017; Worthington & Whittaker, 2006). We first generated items based on the extant stakeholder theory literature, which we evaluated together with experts. This step was followed by two independent studies utilizing exploratory and confirmatory analysis, with a final scale obtained as a result. Finally, construct validity was assessed with a nomological network study in which we compared our measurement scale against established related scales.

Scale Development Process

In these five steps, we followed a reflective modeling approach. This method was specifically chosen for the following reasons (see Blalock, 1964): First, it allowed stakeholder theory mindsets to be conceptualized as latent constructs that were reflected through various observable indicators (items). Second, in this approach, the items capturing the stakeholder theory mindset were intended to reflect the same underlying attitude or belief. Third, changes in the latent construct (stakeholder theory mindset) were expected to lead to changes in item responses. For example, a manager’s shift in mindset toward stakeholder theory would alter how they respond to related survey items.

The actual scale development was complemented by an additional study. This final study tested the predictive power of the stakeholder theory mindset scale developed via the preceding steps and demonstrated the incremental validity of the measurement scale.

Item Generation

As a starting point for measuring stakeholder theory mindsets, we used statements consistent with stakeholder theory to help determine a manager’s mindset related to stakeholder theory (see Jiang et al., 2018). Following Hinkin (1995), we created substantially more statements than items intended for inclusion in the final scale. To generate the statements, we worked with the aforementioned four key assumptions of stakeholder theory on (1) the integration thesis, (2) the responsibility principle, (3) the belief that stakeholders of a business share many joint interests, and (4) the belief that the purpose of a business is value creation for its stakeholders. 1 For each of these assumptions, 15 items were created, resulting in 60 items that were then evaluated by the experts. These items include direct citations from seminal works on stakeholder theory (primarily Freeman et al., 2010), as well as paraphrased statements building on this work (i.e., indirect citations). Alternative wordings for the direct and indirect citations were added to generate a multitude of items. Additionally, for each of the four assumptions of stakeholder theory, counterstatements were included as reverse-coded items in the initial broad set of potential items. These counterstatements also included direct citations from seminal works opposing the key assumptions of stakeholder theory (Friedman, 1962; Sundaram & Inkpen, 2004b).

Study 1: Expert Feedback

Following best practice (e.g., Dossinger, Wanberg, Song, & Basbug, 2025; Kaptein, 2008; Liden & Maslyn, 1998), the 60 items (15 per key assumption) were sent to a group of 18 experienced scholars via an online questionnaire. These scholars were selected because they had published on stakeholder theory in mainstream management journals; 12 of the experts (66.67% response rate) provided their feedback. The experts who provided feedback included seven male and five female scholars with an average of 15 years of experience in the field.

We first presented an explanation of the theoretical construct and its four key dimensions (integration thesis, responsibility principle, value creation, and joint interests). The experts were asked to provide feedback on the four dimensions (e.g., adding or deleting dimensions), and no expert suggested adding a fifth key dimension of stakeholder theory or changing or deleting one of the four proposed dimensions. We then asked the experts to assign each item to one of the four dimensions or to select “other/none” when they did not see a match to one of those assumptions. The experts also judged each item for its relevance to measure the “stakeholder theory mindset” using a three-point scale (very relevant, moderately relevant, and not relevant). In addition, respondents were able to add comments on content, clarity, and conciseness regarding the items or assumptions of stakeholder theory and could suggest alternative wordings.

To systematically document content adequacy, we conducted the following steps of analysis (see Hinkin, 1998): First, we removed all items assigned to the proper a priori category by less than 10 experts, which was consistent with the 80% rule applied by MacKenzie, Podsakoff, and Fetter (1991). Furthermore, we removed all items that were assigned by more than 10% of our experts to “other/none” (see Spieth et al., 2021). This led to the exclusion of 15 items. Finally, we calculated the content validity ratio (CVR) for all 60 items (see Appendix B). We removed an additional seven items that were rated as moderately or very relevant by less than 80% of the experts (which corresponded to a CVR of 0.6 or higher), leaving us with 38 items for the subsequent studies (see Appendix C). These 38 items were distributed across all four key assumptions (integration thesis, 7 items; responsibility principle, 7 items; value creation, 12 items; joint interests, 12 items).

Study 2: Exploratory Factor Analysis (EFA)

To explore the structure of the construct “stakeholder theory mindset,” we conducted an exploratory factor analysis (DeVellis, 2017) based on data from an online survey. In the survey, we asked participants to express their agreement with the 38 items on a 7-point rating scale ranging from 1 (strongly disagree) to 7 (strongly agree). The data collection was organized via the Prolific online recruiting platform (see Palan & Schitter, 2018; Peer, Brandimarte, Samat, & Acquisti, 2017). This allowed us to prescreen participants for management experience as well as for fluent English proficiency. Prior to administering the actual survey, we conducted a pilot study. 2 After completion of the pilot study (n = 8), we collected actual data from 544 respondents. Eliminating incomplete datasets and “speeders” (i.e., respondents who finished the survey in an unusually short timeframe) led to 493 remaining respondents who shared common characteristics of managers with regard to gender and age (62% male, 37% female; Mage = 41.4 years, SDage = 11.6; 37% lower management, 49% middle management, and 14% top management).

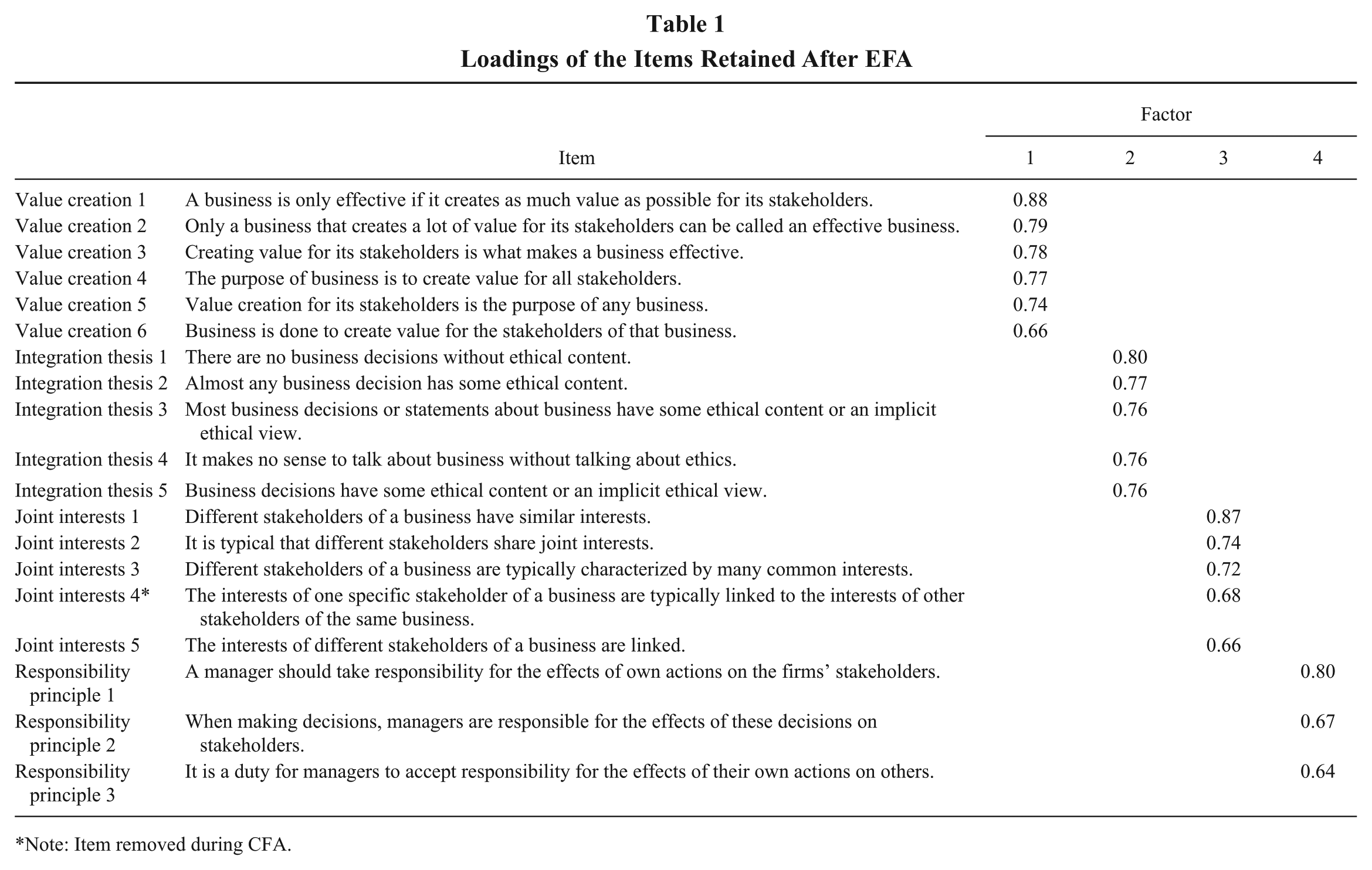

We conducted a factor analysis with maximum likelihood extraction and direct oblimin rotation. The Kaiser–Meyer–Olkin (KMO) criterion of sampling adequacy (KMO = 0.95) and the Bartlett test of sphericity [χ2 (703) = 11394, p < 0.001] both indicated that the data could be used for conducting an EFA. A parallel analysis suggested retaining five factors, the criterion of eigenvalues >1 suggested three factors, and the screen test indicated four factors, which was also what could be expected based on the a priori structure of our construct. As suggested by Costello and Osborne (2005), we conducted multiple factor analyses, for which we manually set the number of factors to retain between two and six. We removed items with factor loadings of less than .6 or cross-loadings of more than .3 (see Tabachnick & Fidell, 2013). The final solution of our EFA consisted of 19 items (see Table 1), loading on four factors and explaining 61.8% of the total variance. While the initial 60 items included 12 reverse-coded items, the remaining 19 items did not include reverse-coded items, as these were excluded during the expert feedback (Study 1) and the exploratory factor analysis (Study 2) due to low CVRs, low factor loadings, or high cross-loadings (see Tabachnick & Fidell, 2013). Content-wise, the four factors on the items loaded represented the key assumptions of the stakeholder theory mindset, which we included in our a priori construct (integration thesis, 5 items; responsibility principle, 3 items; value creation, 6 items; joint interests, 5 items), without a single item being allocated to the wrong dimension of stakeholder theory mindsets. Cronbach’s alpha values were calculated for each factor to assess the reliability of this solution. Ranging from 0.80 to 0.91, all Cronbach’s alpha values were clearly above the threshold of 0.70 suggested in the literature (see Cortina, 1993).

Loadings of the Items Retained After EFA

Note: Item removed during CFA.

Study 3: Confirmatory Factor Analysis (CFA)

To explore the reliability measures of our items, as well as the structure of our scale, we conducted a confirmatory factor analysis. Similar to the sample for the exploratory factor analysis, we prepared an online survey in which we asked participants to express their agreement with the items on a 7-point rating scale ranging from 1 (strongly disagree) to 7 (strongly agree). Data collection was again organized via the online recruiting platform Prolific, and we used the same prescreening setting as in our previous study. Participants in the previous study were excluded from being part of this study. Due to a change in our technical setup, we conducted two pilot studies with eight and five participants, respectively. In our main study, we collected data from 529 participants. We eliminated 49 incomplete datasets and unusually fast respondents, resulting in 460 remaining participants (65% male, 34% female; Mage = 39.9 years, SDage = 11.5; 43% lower management, 45% middle management, and 12% top management).

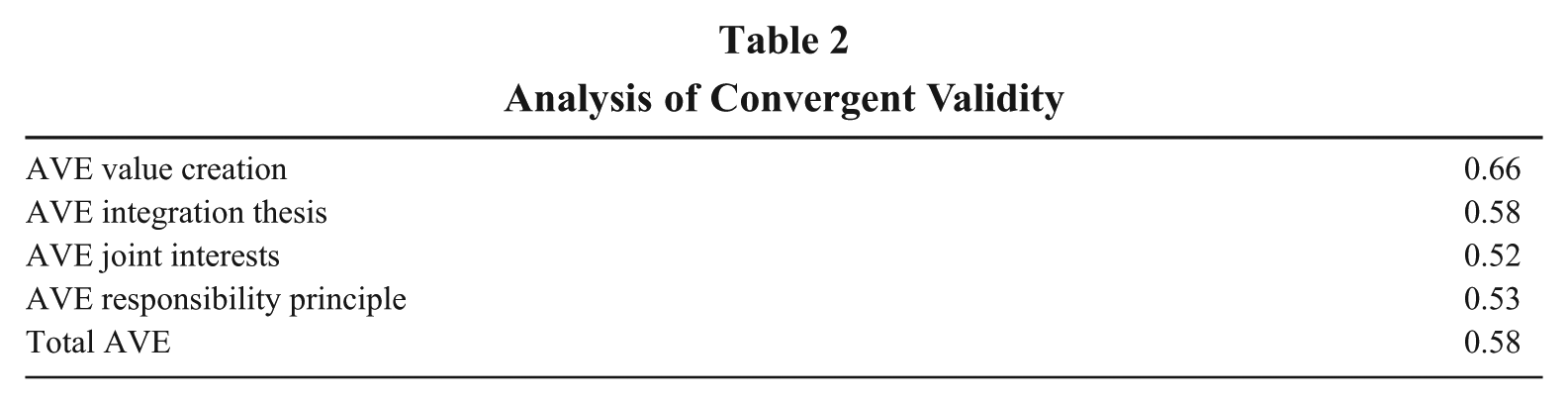

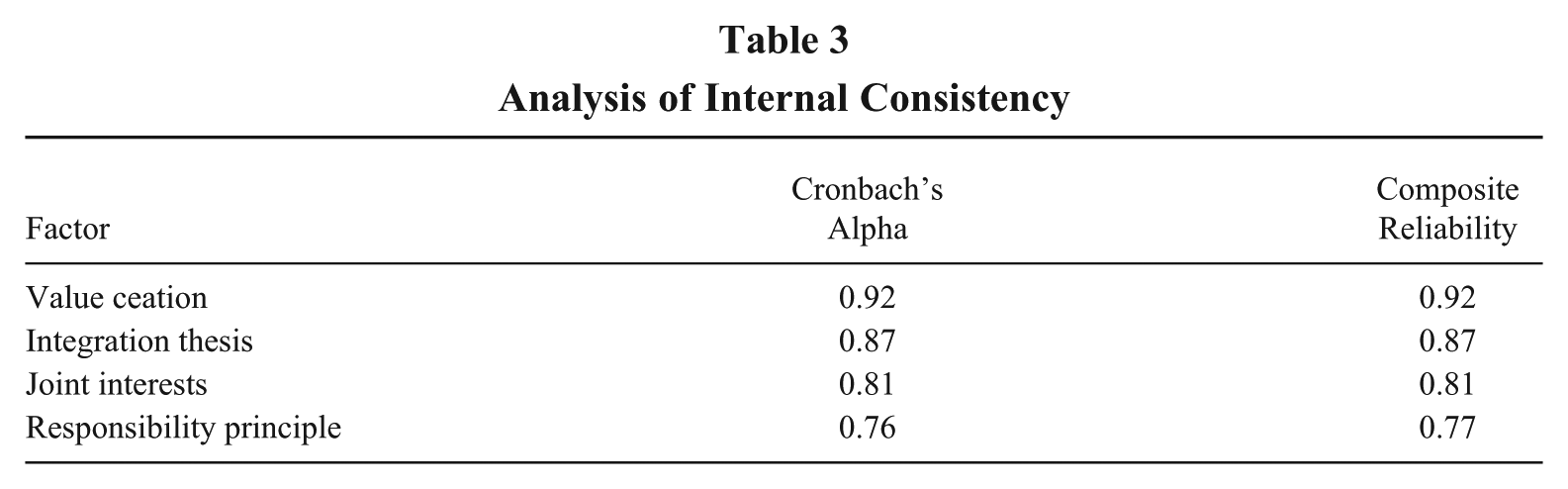

Our analysis led to a four-factor solution with 18 items (after Item JI_4 was removed due to its relatively poor reliability measures), resulting in five items on the integration thesis, three on the responsibility principle, six on value creation, and four on joint interests (see Appendix D). The fit statistics for this construct were at a good level (χ2/df ratio = 2.88, root mean square error of approximation [RMSEA] = 0.06 [0.06–0.07], standardized root mean square residual [SRMR] = 0.05; see also Hooper, Coughlan, & Mullen, 2008; Hu & Bentler, 1999). The average variance extracted (AVE) was calculated to assess the convergent validity of the model (see Table 2). For each factor, the AVE was above the recommended cutoff of 0.50 (see Fornell & Larcker, 1981). The total AVE was 0.57.

Analysis of Convergent Validity

To demonstrate discriminant validity, AVE estimates should be larger than the squared correlations between the factors (Fornell & Larcker, 1981). Because the correlations (see Appendix E) were between 0.28 (Value Creation and Integration Thesis) and 0.54 (Value Creation and Responsibility Principle), this requirement was met in our study. The Cronbach’s alpha values, as well as composite reliability values, were calculated to assess internal consistency and ranged from 0.76 (Responsibility Principle) to 0.92 (Value Creation) (see Table 3).

Analysis of Internal Consistency

To ensure a balance between the four key assumptions of stakeholder theory, we suggest a four-factor model, with the four key assumptions (i.e., integration thesis, joint interests, the responsibility principle, and value creation) each representing one of the four factors. Thus, the overall construct of stakeholder theory mindsets should first be computed by calculating the mean value for the items of each key assumption. Subsequently, using the average across the four mean values guarantees that the final construct represents a balance between the four key assumptions without assigning one assumption a higher weight than the others. To test alternative measurement models, we compared this four-factor model, building on a second-order structure, with a one-factor model. The one-factor model showed substantially worse fit statistics, indicating that the four-factor model fit the data better than an alternative specification with only one factor (AVEone-factor model = 0.36; χ2/df ratioone-factor model = 12.74, RMSEAone-factor model = 0.16).

Study 4: Nomological Network Study

In the next step, we used the final list of items of the stakeholder theory mindset scale (see Appendix F) to explore the construct validity of the scale. Construct validity, also called nomological validity, describes the degree to which the stakeholder theory mindset relates to established scales in this field. Consequently, we selected the following measurement scales for comparison: CSR mindset (Ford & McLaughlin, 1984), PRESOR (Singhapakdi et al., 1996), Socially Responsible Attitudes (Hunt et al., 1990), and ethical mindset (Issa & Pick, 2010).

We chose the CSR mindset (Ford & McLaughlin, 1984) for comparison in the test for nomological validity, as stakeholder theory is sometimes regarded as a subset of CSR (e.g., Kurucz, Colbert, & Wheeler, 2008; Scherer & Palazzo, 2011) or even a synonym for CSR (e.g., Crane & Glozer, 2016; Maloni & Brown, 2006). Given the huge debate on the relationship between CSR and stakeholder theory (Dmytriyev et al., 2021), it was essential to test whether a stakeholder theory mindset scale was indeed distinct from CSR mindset scales, such as the most prominent one brought forward by Ford and McLaughlin (1984). Given the distinct differences between CSR and stakeholder theory, such as the unilateral direction of responsibility and focused perspective on business in CSR and the multilateral direction of responsibility and a rather holistic perspective on business in stakeholder theory (Dmytriyev et al., 2021), we expected that while the two scales would be positively correlated, they would also show substantial differences and thus would not be considered identical constructs.

The PRESOR scale by Singhapakdi et al. (1996) includes three factors: (1) social responsibility and profitability, (2) long-term gains, and (3) short-term gains. Based on these factors, Parnell, Scott, and Angelopoulos (2013) argued that PRESOR measures whether managers prioritize stakeholders over stockholders. While we saw similarities between the factors of social responsibility and profitability in the PRESOR scale and the stakeholder theory mindset scale, stakeholder theory mindsets do not directly relate to the factors of long- and short-term gains. Additionally, the PRESOR scale does not capture the core assumptions of stakeholder theory. To demonstrate the distinctiveness of the stakeholder theory mindset scale compared to the PRESOR scale, we included the PRESOR scale in the test of nomological validity.

The scale by Hunt et al. (1990) focuses exclusively on the aspect of socially responsible attitudes among managers. It consists of four items that cover the degree to which managers place an emphasis on the interests of society at large or on shareholders. Thus, while the scale shares an interest in managers’ social responsibility with the stakeholder theory mindset scale, the reference points chosen are considerably distinct. First, in contrast to stakeholder theory, this scale implies a trade-off between the interests of shareholders and broader interests. Second, these broader interests are understood as society at large and not as the interests of a specific firm’s stakeholders. Thus, we expected the socially responsible attitude scale to correlate on a moderate level with our stakeholder theory mindset scale.

Finally, we chose the ethical mindset scale, as brought forward by Issa and Pick (2010), for the nomological network. It captures the importance managers ascribe to business ethics, and stakeholder theory is frequently considered a cornerstone of business ethics. The scale consists of 34 items across the following components: aesthetic judgment, contentment, harmony and balance, individual responsibility, optimism, professionalism, spirituality, and truth-telling. As with the PRESOR scale, we saw similarities to stakeholder theory mindsets regarding some components of the scale, such as individual responsibility. However, we did not expect the correlation between both scales to go beyond a moderate level due to the distinct focus of stakeholder theory on creating value for and joint interests among stakeholders, which was not captured in the ethical mindset scale. Likewise, the stakeholder theory mindset scale does not capture components such as spirituality, which are included in the ethical mindset scale. Thus, for all the related scales, we did not expect a relationship that went beyond moderate levels of correlation with stakeholder theory mindsets, indicating that our scale assessed related but not identical constructs (Evans, 1996).

Similar to the samples for the previous two studies, we prepared an online survey in which we asked participants to express their agreement with different items. Stakeholder Theory Mindset and Socially Responsible Attitudes (Hunt et al., 1990) were assessed on a 7-point rating scale. For the PRESOR scale (Singhapakdi et al., 1996), a 9-point rating scale was used. CSR mindset (Ford & McLaughlin, 1984) and ethical mindset (Issa & Pick, 2010) were assessed on a 5-point rating scale. These differences were based on the rating scales used in their original corresponding articles. In addition, we included five items to assess social desirability (Hays, Hayashi, & Stewart, 1989) to account for the normative content of some of the scale items. We also used two backward-counting distraction tasks taken from Petersen, Hörisch, and Jacobs (2021) and removed participants who did not complete these tasks correctly. Data collection was again organized via the online recruiting platform Prolific. We used the same prescreening settings as in our previous studies, and participants from the previous two studies were excluded from this research. Again, a pilot study was conducted (n = 8) before the actual study. In the actual study, after eliminating 33 incomplete datasets, unusually fast respondents, and participants who failed both distraction tasks, 319 participants remained. In addition, in this study, the participants shared common characteristics of managers (60% male, 40% female; Mage = 42.8 years, SDage = 12.2) and primarily occupied middle management positions (34% lower management, 56% middle management, and 11% top management).

The psychometric analysis of this study confirmed the structure of the stakeholder theory mindset scale: A CFA on the data again provided a fair model fit (χ2/df ratio= 2.89, RMSEA = 0.07 [0.07–0.08], SRMR = 0.05; see also Hooper et al., 2008; Hu & Bentler, 1999). As in the previous study, AVE was compared to the squared correlations between factors (Fornell & Larcker, 1981). As all AVE values were not only higher than 0.5 but also exceeded the squared correlations, convergent and discriminant validity were assumed. The Cronbach’s alpha values ranged from 0.75 (Responsibility Principle) to 0.89 (Value Creation), and the CR values were also high, from 0.75 to 0.89.

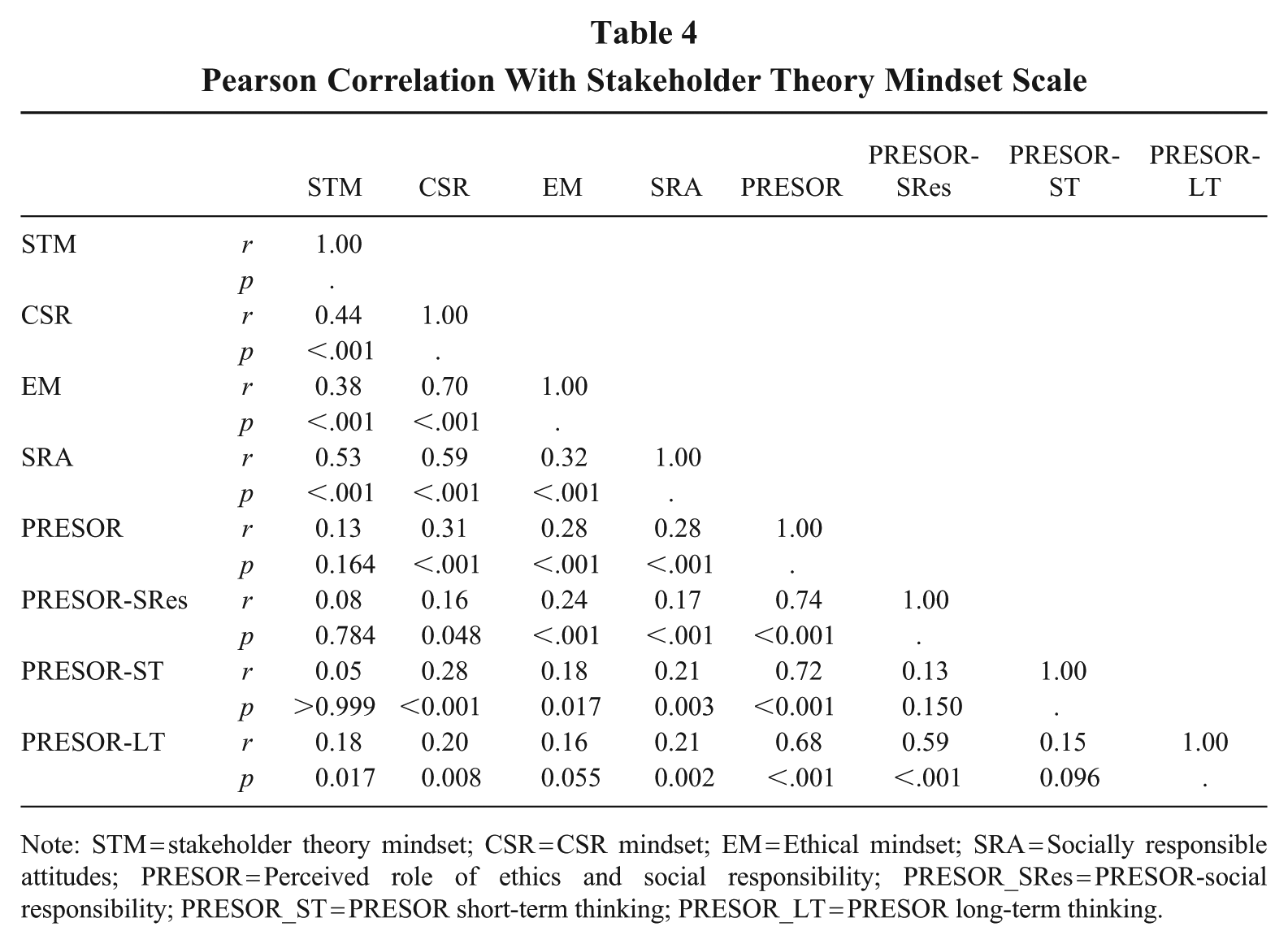

Table 4 indicates that, as expected, the correlations between the stakeholder theory mindset scale and the other scales of our nomological network were at a medium level (CSR: r = 0.44, p < 0.001; PRESOR: r = .13, p = 0.164; Socially Responsible Attitudes: r = 0.53, p < 0.001; ethical mindset: r = 0.38, p < 0.001). This indicates that the stakeholder theory mindset scale measures a related but still distinct construct (DeVellis, 2017). The PRESOR scale only correlated with the stakeholder theory mindset scale at a low level. An analysis of the PRESOR subscales showed that only the second factor (long-term gains; r = 0.18, p = 0.017) was correlated at a significant level with the stakeholder theory mindset scale.

Pearson Correlation With Stakeholder Theory Mindset Scale

Note: STM = stakeholder theory mindset; CSR = CSR mindset; EM = Ethical mindset; SRA = Socially responsible attitudes; PRESOR = Perceived role of ethics and social responsibility; PRESOR_SRes = PRESOR-social responsibility; PRESOR_ST = PRESOR short-term thinking; PRESOR_LT = PRESOR long-term thinking.

Social desirability (Hays et al., 1989) was not part of our nomological network, but was included to test whether endorsement of the stakeholder theory mindset scale reflected socially desirable responding. We found no significant correlation between social desirability and stakeholder theory mindset (r = 0.15, p = 0.096). As social desirability did not exert a substantial or significant influence, this indicates that the new scale on stakeholder theory mindsets was not substantially affected by issues of social desirability.

Furthermore, we conducted an examination of the sample to identify possible survey biases. First, we tackled the potential issue of common method bias by incorporating pre-established design criteria. These criteria included ensuring respondent anonymity and presenting survey constructs in a varied manner (Podsakoff, MacKenzie, Lee, & Podsakoff, 2003). Second, we assessed for nonresponse bias using a two-sample t-test. This analysis confirmed that responses from the initial 25 percent of participants did not significantly vary from those of the final 25% (Armstrong & Overton, 1977).

Study 5: Testing the Predictive Power of the Stakeholder Theory Mindset Scale

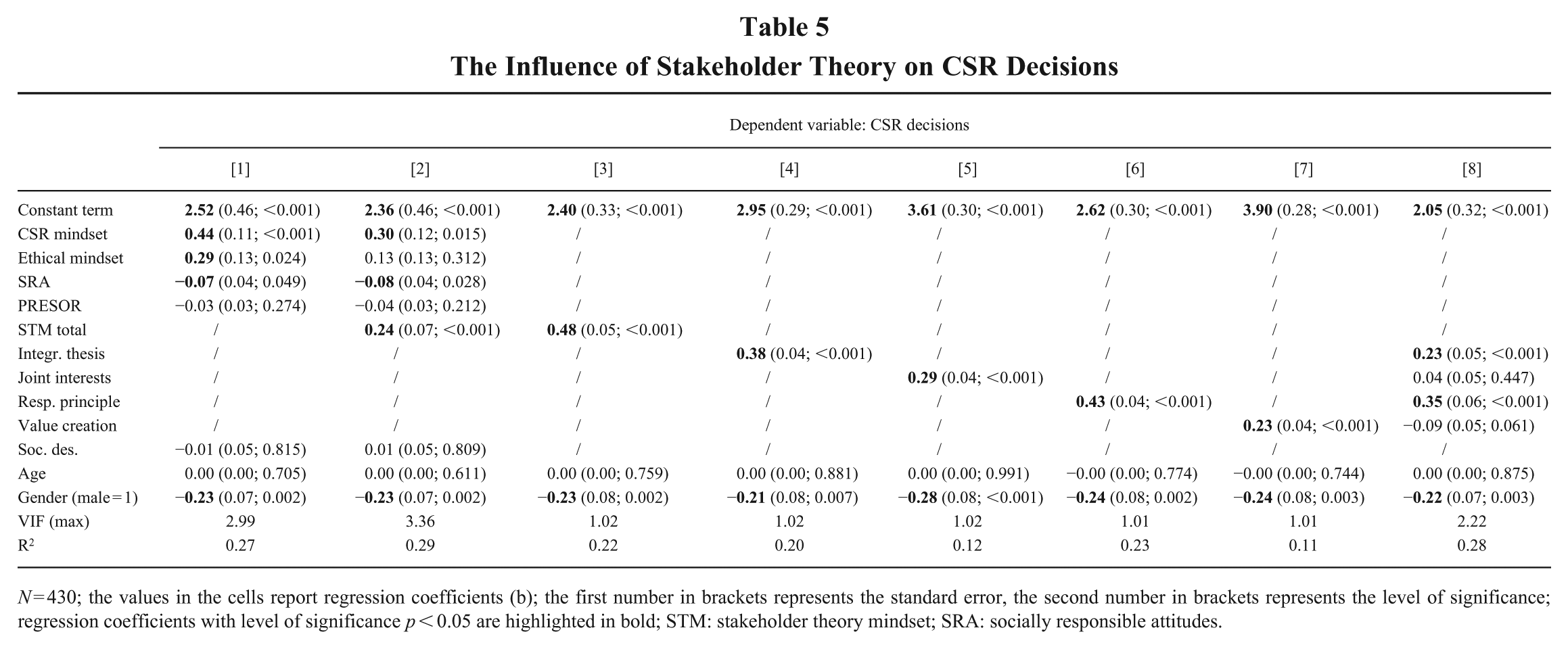

As the final step of our research on developing a stakeholder theory mindset scale, we aimed to demonstrate the predictive power and incremental validity of the newly developed measurement scale. To do so, we chose the context of managers’ CSR decisions, which is also of great relevance for the debate on stakeholder theory and environmental, social, and governance (ESG; e.g., Bellandi, 2023; Forcadell, Lorena, & Aracil, 2023; Nirino, Santoro, Miglietta, & Quaglia, 2021). Like Studies 2, 3, and 4, we prepared an online survey in which we asked participants to express their agreement with the items on stakeholder theory on a 7-point rating scale ranging from 1 (strongly disagree) to 7 (strongly agree). Additionally, to capture managers’ decisions on CSR, we included the vignette study by Feder and Weißenberger (2019), which uses decision-making scenarios. We chose CSR decisions as the dependent variable for testing predictive power and incremental validity, as CSR is a very common research field for applying stakeholder theory (Frynas & Yamahaki, 2016). We selected this specific dependent variable on CSR developed by Feder and Weißenberger (2019), as it was an established construct. Additionally, it used a vignette study approach, which ensured that our analysis did not entail risks of reverse causality. The scenarios included in the vignette study are listed in Appendix G. Respondents indicated on a six-point rating scale whether they would decide in the same way if they were the described person. Thus, high values of the construct “CSR decisions” signal that a manager has high intentions to perform CSR measures.

Again, data collection was organized via the online recruiting platform Prolific, using the same prescreening setting as in previous studies: the instrument was exclusively directed toward managers, and participants in previous studies were excluded. We conducted a pilot study with 20 participants. In our main study, we collected data from 627 participants. We eliminated 197 incomplete datasets, resulting in 430 remaining participants. All participants were managers, most of them in middle management (60.9%, with 15.1% lower management and 24.0% top management; 53.7% female; Mage = 38.51 years, SDage = 12.82).

Appendix H summarizes the descriptive statistics and presents a correlation matrix for all variables included in the analysis of Study 5. To test the predictive power and incremental validity of the stakeholder theory mindset scale, we conducted a hierarchical multiple regression using CSR decisions as the dependent variable (Table 5). In Model 1, the five established predictors explained 25.3% of the variance in the outcome variable (R2 = 0.27). In Model 2, adding the new scale on stakeholder theory mindsets explained an additional 2.0% of the variance (ΔR2 = 0.02), which was a statistically significant increase [F(1, 42) = 11.86, p < 0.001], supporting the incremental validity of the new scale. The results of Model 2 also confirm the general predictive power of the stakeholder theory mindset scale, as stakeholder theory mindsets significantly (and positively) predicted CSR decisions (b = 0.24, p < 0.01; see Model 2 in Table 5). Thus, the regression analyses not only demonstrate the predictive power of the scale, but also illustrate how it can be used for theoretical advancement. In the specific case of the influence of stakeholder theory mindset on CSR decisions, it highlights that managers with higher levels of stakeholder theory mindsets are more likely to make management decisions in favor of CSR. As in Study 4, we controlled for the influence of social desirability in Models 1 and 2 and did not find significant effects (pmodel1 = 0.815; pmodel2 = 0.809).

The Influence of Stakeholder Theory on CSR Decisions

N = 430; the values in the cells report regression coefficients (b); the first number in brackets represents the standard error, the second number in brackets represents the level of significance; regression coefficients with level of significance p < 0.05 are highlighted in bold; STM: stakeholder theory mindset; SRA: socially responsible attitudes.

In Models 3 through 8 of Table 5, we further specified the analysis by testing the influence of the different subdimensions of stakeholder theory mindsets on CSR decisions. Model 3 included only the overall construct of stakeholder theory mindsets; Models 4 through 7 included only one subdimension of the stakeholder theory mindset scale each (i.e., integration thesis, joint interests, responsibility principle, and value creation). The results show that each subdimension exerted a significant influence on CSR decisions when analyzed separately, demonstrating the importance of each assumption. If all subdimensions were included in the same model (Model 8), only the subdimensions of the responsibility principle (b = 0.13; p < 0.01) and the integration thesis (b = 0.24; p < 0.01) exerted significant influences on CSR decisions. However, the explanatory power of the model was highest when all subdimensions were included in the model (r 2 = 0.28 in Model 7) than when only individual subdimensions were included and also higher than when only the overall construct was included (Model 3). This highlights the necessity of including all four key assumptions in our measurement constructs. The models showed no indication of substantial multicollinearity (all variance inflation factors [VIFs] far below 10, no correlation between the independent variables showing values above .8; see Kennedy, 1992). 3

Overall, the results of Study 5 confirmed the predictive validity of the stakeholder theory mindset. We have shown that stakeholder theory mindsets can explain the CSR-related decisions of managers. The newly developed measurement scale can even explain variations in CSR decisions, which goes beyond the variation explained by combining all existing constructs included in the nomological network. The results show that including the construct of stakeholder theory mindsets significantly increased the predictive power and that stakeholder theory mindsets alone can explain 20% of the variance in CSR decisions.

Discussion and Conclusions

Discussion of the Key Results

In this research, a measurement scale was developed and validated to quantitatively assess managers’ endorsement of stakeholder theory (see Appendix F). The resultant stakeholder theory mindset scale facilitates the quantitative examination of numerous assumptions regarding the antecedents and outcomes of managers endorsing stakeholder theory, which had previously been difficult to assess. Consequently, the results of this study propel stakeholder theory research toward greater methodological maturity (Edmondson & McManus, 2007) by establishing a framework for quantitatively evaluating the managerial implications of stakeholder theory and better disentangling which assumptions in stakeholder theory matter for specific kinds of decisions. With this scale, stakeholder theory research at the individual level can now build on quantitative data and established measurement constructs from surveys to systematically test formal hypotheses on specific inquiries.

Developing a measurement scale for a theoretical construct constitutes an important theoretical contribution for the following reasons (see Chun, Shin, Choi, & Kim, 2013; Cole, Walter, Bedeian, & O’Boyle, 2012; MacKenzie, Podsakoff, & Podsakoff, 2011; Podsakoff et al., 2003). First, our scale operationalizes a core but previously underspecified construct in stakeholder theory—stakeholder theory mindsets. It thus translates abstract theoretical ideas into a form that can be systematically observed, tested, and refined. Second, through distilling and validating distinct dimensions of stakeholder mindsets, our work contributes to the conceptual clarity of stakeholder theory, resolving ambiguity, and enabling more precise theorizing. Third, the availability of a valid measure allows future research to empirically test stakeholder theory propositions by exploring antecedents and outcomes of stakeholder mindsets. In this sense, the scale provides a foundation for middle-range theory development. Finally, by clarifying how stakeholder mindsets differ from adjacent constructs (e.g., CSR mindsets and ethical mindsets), our work sharpens theoretical boundaries and enriches the nomological network of stakeholder theory.

The measurement scale consists of 18 items, loading on four factors that constitute a stakeholder theory mindset (i.e., value creation, the integration thesis, joint interests, and the responsibility principle). Thus, the results show that stakeholder theory can be understood along these four dimensions. Still, these dimensions are not independent of each other. Instead, the high levels of construct reliability for the overarching construct of stakeholder theory mindsets suggest that it is indeed the stakeholder theory mindset that is formed by these interrelated dimensions.

As validated in the nomological network study, one important strength of the stakeholder theory mindset scale is that it is considerably distinct from other mindsets in the field of ethical business conduct. As expected, significant correlations (p < 0.001) were found with the scale and constructs such as CSR mindset (Ford & McLaughlin, 1984), ethical mindsets (Issa & Pick, 2010), and socially responsible attitudes (Hunt et al., 1990), 4 with “socially responsible attitudes” showing the strongest correlation (r = 0.53) and “ethical mindset” showing the weakest correlation (r = 0.38). This indicates that the stakeholder theory mindset scale measures a construct that is related to but still distinct from these existing scales (DeVellis, 2017; Evans, 1996). In contrast, no significant relationship was found with the PRESOR scale. 5 Thus, our results provide an indication that PRESOR does not measure the priority of stakeholders over stockholders, as assumed by Parnell et al. (2013).

The distinctiveness we found between the socially responsible attitude (Hunt et al., 1990) and stakeholder theory mindset scales might be due to the underlying assumptions concerning the scope of responsibility assumed in the stakeholder theory literature (i.e., responsibility to a firm’s specific stakeholders) and in the literature on responsible management (i.e., responsibility to society at large; Dmytriyev et al., 2021; Laasch, Suddaby, Freeman, & Jamali, 2020). Another reason for the distinction between the two scales was the assumption underlying the socially responsible attitude scale by Hunt et al. (1990) that trade-offs are a common management context, which contrasts with the assumptions of stakeholder theory. Thus, by highlighting the empirical distinctiveness between the stakeholder theory mindset and the socially responsible attitude scale brought forward by Hunt et al. (1990), we also show that a stakeholder theory mindset is distinct from simply deemphasizing the interests of shareholders.

Likewise, our results enrich the discussion of the relationship between CSR and stakeholder theory (see Dmytriyev et al., 2021; Frynas & Yamahaki, 2016). The nomological network analysis showed that, while the two concepts were positively correlated, they were not synonymous, as, for example, implied by Crane and Glozer (2016) and Maloni and Brown (2006). This can be explained by the unilateral nature of responsibility embraced in CSR versus the multilateral responsibility emphasized in stakeholder theory as well as by the narrower business-focused perspective of CSR compared to the more holistic business perspective inherent in stakeholder theory (Dmytriyev et al., 2021). The test for nomological validity also revealed that stakeholder theory mindsets were distinct from business ethics mindsets in general (Issa & Pick, 2010). This suggests that while stakeholder theory is an important part of the business ethics field, both concepts should not be misunderstood as synonymous.

The results of Study 5 demonstrated the predictive power of the stakeholder theory mindset scale. This study used the context of managers’ CSR decisions and highlighted that managers with stronger stakeholder theory mindsets were indeed more likely to decide in favor of CSR activities. The analysis revealed that the predictive power was largest if all dimensions of the construct were included (i.e., the four key assumptions of the integration thesis, joint interests, responsibility principle, and value creation). The test of incremental validity confirmed that the stakeholder theory mindset scale was even able to explain variance that went beyond the explanatory power of the existing measures.

Limitations and Avenues for Future Research

The newly introduced measurement scale provides ample avenues for further empirical research. Still, when applying the stakeholder theory mindset scale, some limiting characteristics need to be considered and call for further research. First, we used the individual level of single managers as the unit of analysis for scale development. The individual level is easier to observe in future empirical studies, for example, behavioral studies or surveys of individual managers, which will allow for broad application. Furthermore, the individual level is easier to influence in practical interventions, such as management education. Nevertheless, we acknowledge that the scope of decision-making on the individual level of single managers can be limited. Therefore, systematically analyzing how far existing approaches toward measuring stakeholder theory at the organizational level adhere to the key assumptions of stakeholder theory and potentially creating a new measurement scale for stakeholder theory orientation at the group and organizational levels are promising areas for future research. In addition, future research could examine whether the stakeholder theory mindsets of individual managers (measured with the scale developed in this research) have implications for stakeholder theory-related outcomes at the organizational level.

Second, the scale we developed is capable of measuring stakeholder theory mindsets, building on the understanding of stakeholder theory, as brought forward by Freeman (1984) and colleagues (e.g., Freeman et al., 2010; Harrison, Barney, Freeman, & Phillips, 2019; van der Linden, Wicks, & Freeman, 2024). However, interpretations and adaptations of this integrative version of stakeholder theory are considerably different, such as instrumental, normative, and descriptive forms of stakeholder theory (see Donaldson & Preston, 1995). Thus, the scale proposed in the current research is unable to capture whether manager mindsets follow such distinct variations of stakeholder theory. Future research could thus aim to make these variations, including instrumental stakeholder theory or stakeholder theories with specific normative cores, such as feminist stakeholder theory (e.g., Wicks, Gilbert, & Freeman, 1994), quantitatively observable.

Third, the focus of this research was on scale development, and Study 5 only served to indicate the predictive validity of the scale. It needs to be acknowledged that the dependent variable on CSR decisions in Study 5 relied on hypothetical scenarios and showed only a modest effect size (R2 = 0.29). Future research using the stakeholder theory mindset scale (e.g., in the field of behavioral stakeholder theory) should aim to use actual decisions as dependent variables, for example, in the context of behavioral lab experiments, vignette studies, in-basket exercises, or real-choice experiments.

Beyond addressing the limitations of this study, future research can use the measurement scale on stakeholder theory mindsets to address some of the most fundamental questions Freeman et al. (2010) identified for future stakeholder theory research, including questions on the antecedents and outcomes of stakeholder theory mindsets. Future research on the antecedents of stakeholder theory mindsets may include questions such as “How can managers adopt a mindset that puts business and ethics together to make decisions on a routine basis?” or “What should be taught in business schools?” (Freeman et al., 2010: 5). For example, using the stakeholder theory mindset scale allows interventionist studies to quantitatively examine the degree to which managers endorse stakeholder theory. Such research on the antecedents of stakeholder theory mindsets will help assess which teaching formats aimed at fostering a stakeholder theory mindset are most promising. Both management education in business schools and assessment centers can use the scale to identify strengths and areas of improvement needed to develop a stronger stakeholder theory orientation for current and future managers, as well as to identify how manager mindsets change over time.

Likewise, the developed measurement scale also offers a path for future research on the outcomes of stakeholder theory mindsets. Previous research has discussed the essential implications of manager mindsets, such as implications for resource management practices (Abernethy et al., 2021), type of business cases pursued (Schaltegger & Burritt, 2018), and leadership behavior (Kouzes & Posner, 2019). Indeed, various prominent researchers in management have suggested that current management mindsets are not appropriate for today’s business environment (Freeman et al., 2010; Ghoshal, 2005; Pfeffer & Fong, 2002). In this context, previous, primarily conceptual research assumed that the stakeholder theory mindsets of managers would have important consequences for their decision-making regarding, for instance, sustainability management, reporting, accounting, or strategy, as well as for actual organizational performance regarding these domains (e.g., Jones et al., 2018; Schaltegger et al., 2019; Wicks et al., 2012). The measurement scale developed in this research will help with the empirical testing of these conceptual assumptions. More specifically, future research could test the argumentation by Mitchell et al. (2015) and Hall et al. (2015) that managers endorsing the assumptions of stakeholder theory enlarge the scope of what information is reported by companies and for whom. Likewise, future research could test whether managers with higher degrees of stakeholder theory mindsets indeed have broader, more integrative understandings of business cases (see Schaltegger et al., 2019), for instance, regarding for whom a business case should create value and what kinds of value beyond financial values count in business cases.

In addition, the scale can be used to analyze a wide range of topics and concepts addressed in behavioral stakeholder theory research. These include the influence of the stakeholder theory mindsets of managers with respect to individual stakeholder relationships and social networks, in other words, how managers respond to the simultaneous influence of multiple stakeholders (Rowley, 1997). Likewise, using the stakeholder theory mindset scale, the role of reciprocity and fairness in stakeholder relationships could be empirically tested (see also Bosse et al., 2009). For instance, future research could analyze how the existence or lack of a stakeholder theory mindset among managers influences perceptions of fairness among employees and results in reciprocity among different stakeholders of the firm and how this affects firm performance. In line with Bundy et al. (2018), who highlighted value congruence and strategic complementarity as two dimensions of organization–stakeholder fit, the proposed measurement scale could help in analyzing manager–stakeholder fit to explain cooperative behavior between managers of an organization and the organization’s stakeholders at the individual level, testing the influence of shared stakeholder theory mindsets among both managers and stakeholders. In the context of Lange and Bundy’s (2018) proposition that business purpose is a mediating factor between ethics and stakeholder theory, the scale can help to analyze whether managers with a stakeholder theory mindset tend to work for companies with more ethical business purposes than managers without such a mindset. Another important concept of behavioral stakeholder theory that could be empirically tested is whether and how managers with a stakeholder theory mindset pursue “stakeholder synergy” (Tantalo & Priem, 2016)—the goal of increasing the size of the value “pie” available for essential stakeholder groups—and whether specific aspects of a stakeholder theory mindset (i.e. the four dimensions on value creation, integration thesis, joint interests, and responsibility principle) are particularly related to how managers aim to contribute to social welfare (Bridoux & Stoelhorst, 2016). Concerning stakeholder governance, building on the analysis by Bridoux and Stoelhorst (2022) on the comparative effectiveness of different governance forms regarding joint value creation activities (hub-and-spoke governance, lead role governance, and shared governance), the proposed scale can be used to investigate what governance forms managers with a stakeholder theory mindset prefer and adopt.

The scale can also be used to analyze the stakeholder theory mindsets of stakeholders and how they influence the stakeholders’ relationships with companies. For example, Qian et al. (2021: 605) found that employee-friendly firms often benefit from lower costs of debt financing and “theorize that banks use employee treatment as a screen to assess firms’ trustworthiness, which encompasses not only confidence in firms’ ability to perform well but also the belief that they will act with good intent toward their creditors.” An analysis of whether differences in the stakeholder theory mindsets of financiers influence their assessment of financial trustworthiness and the relationship between financiers and companies could help to support and further develop behavioral stakeholder theory.

The stakeholder theory mindset scale can also be applied to the context of governments and political actors. De Bussy and Kelly (2010) found in their study that there “is a gulf between how politicians think stakeholder status should be accorded in principle and what happens in reality,” and that power plays a greater role than legitimacy in determining stakeholder salience among political decision-makers. To deepen our understanding of stakeholder identification and salience in government, the stakeholder theory mindset scale could support the analysis of whether differences between political actors with different degrees of stakeholder theory mindsets exist in their assessment of the role of legitimacy and political power of different stakeholders. The stakeholder theory mindset scale can also help advance political stakeholder theory (Olsen, 2017) with empirical studies on how state policies influence stakeholder legitimacy among managers with varying degrees of stakeholder theory mindsets.

The proposed measurement scale could also help in predicting managerial decision-making in the realm of managing stakeholder relationships. Such future research could, for example, use experiments, in-basket exercises, or laboratory studies (see Crilly, 2019; Meyer, 1970) to explore the consequences of management decisions dealing with stakeholder relationships when managers show differing beliefs about the four dimensions of stakeholder theory that we have identified (i.e., value creation, integration thesis, joint interests, and responsibility principle). Such research would also help to analyze which of these dimensions are more or less important in different types of decisions, or if they are all necessary.

Making stakeholder theory mindsets observable and progress toward making this mindset measurable constitutes an important first step in stimulating more appropriate mindsets for the increasingly complex business environment, both in education and corporate practice. The scale to measure the stakeholder theory mindsets of managers proposed in this research allows for empirical analysis of whether the expectations many stakeholder theorists have toward disseminating the key ideas of stakeholder theory hold true in practice, whether further differentiation is needed regarding what constitutes a socially and sustainably productive mindset, and what empirically validated consequences can be drawn for management research and practice.

Supplemental Material

sj-docx-1-jom-10.1177_01492063261438089 – Supplemental material for Measuring Stakeholder Theory Mindsets: Development and Validation of a Measurement Scale