Abstract

To what extent do boards integrate external comparative signals when making CEO dismissal decisions? Drawing on the board information processing perspective, we propose that competitor CEO awards shape the weight boards assign to firm financial performance in dismissal evaluations. Specifically, when competitor CEOs receive prestigious recognition, boards are more likely to interpret firm underperformance as evidence of managerial inadequacy, thereby increasing the likelihood of CEO dismissal. In contrast, when firm performance exceeds that of industry peers, competitor awards amplify positive evaluations of the incumbent CEO’s managerial competence, reducing dismissal likelihood. We further identify three governance-related boundary conditions, i.e., CEO compensation structure, board busyness, and board–CEO demographic similarity, that condition these effects by shaping directors’ evaluative expectations, available attentional resources, and relational biases. Using a longitudinal sample of U.S. publicly traded firms from 2006 to 2020, we find consistent support for our theoretical predictions. Our study contributes to the corporate governance literature by demonstrating the extent to which boards embed firm performance evaluations within a broader comparative informational context. In doing so, we also uncover indirect competitive spillover effects of executive recognition, showing that CEO awards influence not only recipients’ outcomes but also governance decisions within rival firms.

Keywords

Introduction

Boards play a pivotal role in evaluating CEO effectiveness and determining whether leadership changes are warranted (Chemmanur & Fedaseyeu, 2018; Haleblian & Rajagopalan, 2006; Shen, 2003; Zahra & Pearce, 1989). Although prior research consistently identifies financial performance as the primary factor shaping boards’ assessments and subsequent CEO dismissal decisions (Chen & Hambrick, 2012; Jenter & Kanaan, 2015; Park, Boeker, & Gomulya, 2020), directors increasingly acknowledge that relying solely on financial metrics provides an incomplete evaluation of managerial performance (Young, Stedham, & Beekun, 2000; Zhu & Westphal, 2014). Firm outcomes often reflect factors beyond managerial control, such as market fluctuations, industry-wide shifts, and macroeconomic trends (Dess, Ireland, & Hitt, 1990; Simerly & Li, 2000). Consequently, boards supplement accounting-based performance indicators with a broader set of market-based and externally generated evaluative cues, including stakeholder reactions, media coverage, and analyst assessments, to develop more comprehensive judgments of CEO performance (Graffin, Wade, Porac, & McNamee, 2008; Shin, Lee, & Bansal, 2022; Wang, Zhu, Avolio, Shen, & Waldman, 2023; Zorn, DeGhetto, Ketchen, & Combs, 2020).

Despite recognizing boards’ reliance on multiple information sources, prior research provides limited insight into the extent to which boards weigh firm financial performance relative to other comparative evaluative clues when assessing CEOs (Love, Lim, & Bednar, 2017; Young et al., 2000; Zhang & Wiersema, 2009). Boards do not evaluate CEOs in isolation; rather, directors assess firm outcomes relative to comparable firms within their industry (Connelly, Li, Shi, & Lee, 2020). Competitors constitute particularly salient reference points because they face similar strategic challenges, market conditions, and stakeholder expectations (Connelly et al., 2020; Gupta & Misangyi, 2018). Accordingly, competitors’ managerial achievements and strategic choices signal prevailing industry benchmarks of effective leadership, shaping boards’ interpretations of their own CEO’s performance (Connelly et al., 2020; Park, 2023). Yet existing research has not fully examined the extent to which boards integrate firm-level financial outcomes with comparative, externally generated signals in CEO evaluations. Therefore, we ask: To what extent do boards incorporate comparative information signals, particularly those concerning direct competitors, when assessing CEO performance and making dismissal decisions?

To address this research question, we draw on the board information processing perspective, which conceptualizes boards as collective decision-making bodies responsible for acquiring, interpreting, and synthesizing diverse information under conditions of bounded attention and cognitive constrains (Boivie, Bednar, Aguilera, & Andrus, 2016; Busenbark, Krause, Boivie, & Graffin, 2016; Krause, Withers, & Waller, 2025). From this perspective, directors selectively attend to a subset of available performance indicators and evaluative cues to simplify complex managerial assessments (Filatotchev, Lanzolla, & Syrigos, 2025; Krause et al., 2025). Prior research of information processing theory has primarily emphasized boards’ attention to firm-specific performance indicators, such as financial trends and CEO behaviors, while offering limited insight into how boards concurrently process comparative, externally generated evaluative cues (Connelly et al., 2020). Extending this perspective therefore requires clarifying the extent to which comparative information shapes directors’ interpretations of financial performance in CEO evaluations.

Competitor CEO awards provide a particularly suitable context for examining this integrative process. Unlike diffuse environmental cues such as general media tone or analyst commentary, CEO awards constitute third party certifications of managerial quality based on explicitly identified and publicly validated standards endorsed by reputable institutions, including prominent media outlets (e.g., Forbes, Financial Times) and influential industry associations (Graffin et al., 2008; Wade, Porac, Pollock, & Graffin, 2006). When competitor CEOs receive high-profile recognition, directors are prompted to reassess their own CEO’s effectiveness relative to clearly defined and publicly endorsed criteria of managerial excellence.

We argue that boards interpret weak firm performance more negatively when competitor CEOs receive prestigious recognition, as such awards heighten the salience of comparative shortfalls and amplify perceptions of managerial inadequacy, thereby increasing the likelihood of dismissal. Conversely, when firm financial performance remains strong despite competitor recognition, boards are more likely to interpret this combination favorably, viewing competitor awards as contextual validation of their CEO’s potential for similar recognition. In this way, comparative cues systematically condition the weight boards assign to financial outcomes.

The board information processing perspective further emphasizes that directors’ integration of multiple signals is shaped by cognitive and social constraints. We therefore identify three governance characteristics—i.e., CEO compensation, board busyness, and board-CEO demographic similarity—that influence directors’ evaluative expectations, available attentional resources, and relational biases, respectively. These factors serve as boundary conditions that moderate the extent to which comparative signals shape the relationship between financial performance and CEO dismissal.

We empirically test these arguments using a longitudinal sample of publicly traded U.S. firms, linking CEO turnover events to detailed data on financial performance and competitor CEO awards. The results support our predictions, demonstrating that boards assign differential weight to financial outcomes depending on salient comparative cues. These findings underscore that CEO dismissal is not solely a function of firm-level performance indicators, but rather a contextually embedded evaluative process shaped by comparative information.

This study makes several contributions. First, we advance the CEO dismissal literature by demonstrating that boards’ assessments depend not only on firm-specific financial outcomes but also on comparative, externally generated evaluative cues, particularly competitor CEO recognition. Prior research has predominantly focused on organizational determinants such as financial performance or CEO misconduct. By incorporating comparative signals, we explain why CEOs with similar financial records may experience divergent dismissal outcomes depending on competitors’ visibility and recognition, thereby enriching our understanding of CEO evaluation and turnover.

Second, we extend board information processing theory in corporate governance by explicating the extent to which comparative cues influence boards’ interpretation of financial performance. Prior works has emphasized boards’ monitoring and interpretive functions while often treating comparative information implicitly or as secondary (Khanna, Jones, & Boivie, 2014; Krause et al., 2025). By theorizing and empirically validating the role of competitor CEO awards as salient comparative signals, we show that boards embed financial assessments within a broader informational context. This refinement deepens theoretical insight into how directors manage cognitive constraints and selectively prioritize signals in complex governance decisions.

Third, we contribute to the literature on executive recognition and CEO awards by uncovering important indirect competitive effects of these awards. Existing scholarship largely focuses on benefits accruing to award recipients, including enhanced reputation, career mobility, and resource access (Gallus & Frey, 2016; Jensen, Twardawski, & Younes, 2022). Our findings reveal that executive recognition also generates governance spillovers across rival firms. Competitor awards not only elevate recipients’ standing but also shape how boards of competing firms evaluate and potentially replace their own CEOs. Thus, executive recognition produces meaningful competitive consequences that extend beyond the focal firm, influencing managerial evaluation and strategic governance decisions within industries.

Theory and Hypotheses

Board Information Processing in CEO Dismissal

Board decisions to dismiss CEOs represent critical governance judgments that significantly shape firms’ strategic trajectories, organizational stability, and competitive positioning (Park, Chung, & Rajagopalan, 2021; Park et al., 2020; Zhu & Westphal, 2014). Existing research primarily identifies financial performance as the core driver of CEO dismissals (Balkin, Markman, & Gomez-Mejia, 2000; Gentry, Harrison, Quigley, & Boivie, 2021; Heyden, Kavadis, & Neuman, 2017). However, scholars also note that the relationship between performance and dismissal is weaker and less consistent than often assumed, suggesting that additional forces influence dismissal decisions. For example, Gentry et al. (2021) show that performance explains only part of the variance in turnover outcomes, indicating that boards look beyond firm results when evaluating whether leadership change is warranted. One explanation is that financial outcomes alone rarely offer a complete or unambiguous basis for assessing CEO effectiveness, as they may reflect environmental factors beyond managerial control, including macroeconomic shifts or changes in industry conditions (Flickinger, Wrage, Tuschke, & Bresser, 2016; Jenter & Kanaan, 2015). In response, boards rely on broader informational cues, including stakeholder perceptions, media coverage, and analyst evaluations when forming judgments about the CEO (Shin et al., 2022; Wang et al., 2023; Zorn et al., 2020). This expansion of information sources highlights the interpretive complexity boards face as they navigate diverse and sometimes conflicting signals about organizational leadership (Khanna et al., 2014; Krause et al., 2025).

The board information processing perspective offers valuable insight into how boards manage this complexity. This perspective conceptualizes boards as collective bodies responsible for acquiring, interpreting, and synthesizing diverse streams of information to reach governance decisions (Boivie et al., 2016; Krause et al., 2025). Drawing on social information processing theory (Salancik & Pfeffer, 1978; Thomas & Griffin, 1983), scholars argue that boards’ assessments are shaped by cognitive constraints such as selective attention, information overload, and social pressures that can limit directors’ ability to fully process available information (Forbes & Milliken, 1999; Westphal & Bednar, 2005; Wowak, Busenbark, & Hambrick, 2022). Effective governance therefore depends on deliberation structures that support interpretive clarity, encourage open discussion, and facilitate meaningful consensus building among directors (Forbes & Milliken, 1999; Rindova, 1999; Veltrop, Bezemer, Nicholson, & Pugliese, 2021).

Despite growing scholarly attention to board information processing, research has largely focused on how boards draw on organizational information, such as financial indicators, CEO characteristics, or stakeholder feedback (Cao, Maruping, & Takeuchi, 2006; Staw & Epstein, 2000; Zajac, 1990). Much less attention has been devoted to how boards incorporate comparative environmental informational cues as part of their interpretive work. Yet boards rarely evaluate organizational signals in isolation. Directors routinely place organizational outcomes in context by attending to comparative events, including competitors’ actions, industry developments, and stakeholder reactions. What remains insufficiently theorized, however, is how boards reconcile organizational and comparative signals when evaluating CEO performance and determining whether leadership change is warranted (Khanna et al., 2014; Krause et al., 2025; Shen, 2003).

Comparative Information Cues in CEO Dismissal: CEO Awards

From an information processing perspective, boards should likely evaluate CEOs by relying on contextual cues derived from their environment. Directors continually interpret and integrate signals from peer firms to place their own CEO’s performance in context. For example, prior research has demonstrated that, early in a CEO’s tenure, boards predominantly rely on heuristics unrelated to direct performance metrics to judge effectiveness; however, as CEOs accumulate a record of performance more clearly tied to their decisions, boards increasingly focus on these organizational performance indicators (Graffin, Boivie, & Carpenter, 2013). In a similar manner, publicly recognized competitor achievements, particularly those receiving extensive media coverage or stakeholder attention, have the potential to become salient referents. These competitive signals should enable directors to compare their firm’s leadership effectiveness against evolving industry standards.

Among such competitive signals, CEO awards granted to rival executives serve as highly visible and credible indicators of managerial excellence, institutionally endorsed by prominent media outlets and professional associations (e.g., Forbes, Financial Times, BusinessWeek). Often referred to as certifications of managerial quality, these awards explicitly highlight exemplary leadership practices and superior organizational outcomes (Graffin et al., 2008; Wade et al., 2006). Rigorous selection processes, typically involving expert panels composed of directors, executives, and professional analysts, further enhance the legitimacy and interpretability of these awards, making them particularly valuable reference points for boards’ assessments (Frey, 2006; Pfarrer, Pollock, & Rindova, 2010; Rossman & Schilke, 2014).

Receiving these awards bestows substantial strategic benefits upon recipients, including increased legitimacy, enhanced stakeholder trust, greater symbolic authority, and improved access to critical resources (Gallus & Frey, 2016; Jensen et al., 2022; Malmendier & Tate, 2009). Such enhanced visibility and elevated status significantly strengthen recipient firms’ competitive positions within their respective industries. Importantly, these recognitions simultaneously heighten competitive pressures on non-recipient firms by publicly defining exemplary leadership practices, effectively recalibrating stakeholder expectations across the industry.

For boards of firms whose CEOs do not receive these prestigious awards, competitor CEO awards should serve as influential comparisons that potentially recalibrate standards for evaluating managerial effectiveness. Extensive media coverage and robust institutional endorsements make such awards difficult for directors to disregard, implicitly raising the performance standard by which their own CEOs are assessed. Even in the absence of direct changes to a firm’s underlying capabilities, competitor awards shift stakeholders’ perceptions and place additional pressures on directors to reassess their CEO’s performance relative to newly established models of leadership excellence (Li, Liao, & Han, 2022; Li, Yin, Shi, & Yi, 2022).

Consequently, boards are expected to incorporate these competitive signals into their evaluation processes, interpreting competitor CEO awards in conjunction with performance information. Therefore, competitor CEO awards likely shape the interpretive context within which boards assess financial performance, potentially influencing their judgments regarding whether CEO dismissal is warranted.

Competitors’ CEO Awards, Underperformance, and CEO Dismissal

Building on this logic, we argue that when a firm’s financial performance falls below that of its industry peers, a higher presence of award-winning CEOs in competing firms should increase the likelihood of CEO dismissal through three mechanisms.

First, additional award-winning CEOs among competitors elevate the standards of effective leadership, making the focal firm’s underperformance more salient. CEO awards recognize a range of leadership attributes, including social impact, innovation, governance quality, and financial success (Gallus & Frey, 2016; Shi, Zhang, & Hoskisson, 2017). As more competitor CEOs receive such recognition, boards are exposed to a wider set of leadership exemplars that extend beyond financial metrics. When the focal firm lags behind industry peers, the contrast between its weaker performance and the achievements associated with these recognized leaders becomes more pronounced. Boards should be increasingly aware that their CEO may be falling short on multiple valued dimensions, which strengthens the interpretation that the firm’s underperformance may stem from leadership deficiencies.

Second, a greater number of award-winning CEOs among peer firms signals that strong leadership is both attainable and influential, thereby raising boards’ expectations for potential improvement through leadership change. Because award-winning CEOs represent credible examples of leaders who have successfully guided their firms across financial, social, or governance domains, their visibility provides boards with concrete models of what effective leadership can accomplish (Jensen et al., 2022; Love et al., 2017; Shi et al., 2017). When the focal firm performs below industry peers, this heightened visibility should reinforce the perception that its underperformance may be attributable to managerial inadequacy, making leadership change appear more likely to yield improvement.

Third, the combination of underperformance and an increasing number of award-winning competitors should heighten boards’ sense of urgency for corrective action. As directors observe more competitor CEOs achieving recognition in areas where their own firm is struggling, they may feel growing pressure to respond. These examples likely reinforce the belief that the focal firm cannot maintain its competitive position without decisive action (Krause et al., 2025; Marcel, Barr, & Duhaime, 2011). This perception should motivate boards to consider leadership change as a necessary step to restore the firm’s relative standing. Therefore, we propose:

Hypothesis 1a: As the number of award-winning CEOs in competing firms increases, the positive association between a firm’s underperformance relative to industry peers and CEO dismissal becomes stronger.

Competitors’ CEO Awards, Outperformance, and CEO Dismissal

On the other hand, when a firm’s financial performance exceeds that of industry peers, we argue that the presence of more award-winning competitor CEOs reduces the likelihood of CEO dismissal through three mechanisms.

First, competitor CEO awards underscore the demanding leadership standards required for superior performance in such a highly competitive environment (Ammann, Horsch, & Oesch, 2016; Gallus & Frey, 2016). When more competitor CEOs receive media recognition, it signals to directors that achieving superior outcomes under such conditions requires exceptional managerial capability (Love et al., 2017). Thus, when their CEO outperforms industry peers in this context, directors are more likely to attribute this superior performance to the CEO’s distinctive managerial skills. Consequently, competitor awards validate the incumbent CEO’s effectiveness, strengthening boards’ confidence and reducing motivations for dismissal.

Second, competitor CEO awards signal the potential for future media recognition of the focal CEO. Boards value such validation because it confirms leadership quality and enhances reputational standing (Love et al., 2017; Young et al., 2000; Zhang & Wiersema, 2009). When boards observe multiple competitor CEOs receiving prestigious awards, directors perceive this recognition as achievable. Given their own CEO’s consistent superior performance relative to peers, directors likely interpret the current absence of similar recognition as temporary rather than indicative of managerial inadequacy. Thus, competitor awards shape boards’ expectations by signaling that continued strong performance should eventually translate into comparable recognition for their CEO, further decreasing motivations for leadership change.

Third, extensive media recognition of competitor CEOs increases boards’ perceived risks associated with leadership change. Operating within an industry populated by more media endorsed CEOs suggests intense competitive pressures and a high standard for managerial effectiveness (Ammann et al., 2016; Wade et al., 2006). Under such demanding conditions, superior performance is challenging and replacing a proven, high-performing CEO introduces significant uncertainty and strategic risk. Therefore, boards become more inclined to retain their incumbent leader, viewing leadership continuity as strategically prudent in such a competitive landscape. Accordingly, we propose:

Hypothesis 1b: As the number of award-winning CEOs in competing firms increases, the negative relationship between a firm’s outperformance relative to industry peers and CEO dismissal becomes stronger.

Boundary Conditions Affecting Board Information Processing

Effective board decision-making depends substantially on directors’ ability to overcome challenges associated with processing complex and ambiguous information (Busenbark et al., 2016; Connelly et al., 2020; Forbes & Milliken, 1999; Rindova, 1999). Prior research has predominantly examined cognitive barriers such as biases, information overload, and dysfunctional group dynamics (Hambrick, Misangyi, & Park, 2015; Khanna et al., 2014; Wowak et al., 2022). However, boards also face significant interpretive challenges, particularly when attempting to utilize ambiguous signals from competitors to interpret their own firm’s performance (Graffin et al., 2008; Pfarrer et al., 2010; Wade et al., 2006). Competitor CEO awards exemplify such interpretive complexity, as these awards encompass diverse evaluation criteria, including financial performance, stakeholder perceptions, and media preferences (Gallus & Frey, 2016). Directors thus confront substantial uncertainty about how to appropriately weigh competitors’ recognition in assessing their own CEO’s effectiveness and determining whether performance outcomes primarily reflect managerial capability or favorable environmental conditions.

According to the board information processing perspective, boards address these interpretive complexities not only through the quantity or quality of available information, but also through cognitive and social mechanisms that influence directors’ interpretation and integration of signals (Busenbark et al., 2016; Forbes & Milliken, 1999; Rindova, 1999). Specifically, board evaluations rely on three interconnected processes: how directors form evaluative expectations, how they allocate limited attentional resources, and how they socially interpret informational cues (Krause et al., 2025). Collectively, these mechanisms shape boards’ efforts to integrate ambiguous signals, such as competitor CEO awards, with performance indicators when making CEO dismissal decisions.

Drawing from this theoretical logic, we propose governance characteristics that directly correspond to these cognitive and social mechanisms, specifically CEO compensation, board busyness, and board-CEO demographic similarity, as boundary conditions that influence boards’ effectiveness in interpreting competitor signals to clarify evaluations of performance.

Contingency Effects of CEO Compensation

We propose CEO compensation as an important boundary condition influencing how boards interpret competitor CEO awards when evaluating their own CEO’s underperformance relative to industry peers. Specifically, we argue that high CEO compensation intensifies the positive effect of competitor CEO awards on the likelihood of dismissal for underperforming CEOs.

First, high CEO compensation elevates the evaluative standards used by boards, increasing the salience of underperformance relative to award-winning competitors. Substantial compensation packages serve as prior indicators of boards’ strong expectations regarding CEO capabilities, accountability, and potential for delivering superior outcomes (O’Reilly, Main, & Crystal, 1988; Wang, Zhao, & Chen, 2017; Zajac, 1990). Consequently, when a highly paid CEO delivers weaker performance while more competitor CEOs are recognized, the contrast between high rewards and low results becomes sharper. Such discrepancies intensify boards’ dissatisfaction, reinforcing the perception that the CEO has failed to meet both financial and symbolic criteria of effective leadership.

Second, high CEO compensation shapes the attributions boards make regarding poor firm outcomes. Boards that provide substantial compensation inherently assume that CEOs possess the managerial capabilities and authority necessary to significantly influence firm performance (Zajac, 1990; Zhu, 2014). Thus, when performance lags behind industry peers, especially in contexts where more competitor CEOs have received prominent media recognition, directors become less likely to attribute these shortfalls to uncontrollable environmental factors such as market conditions or competitive dynamics. Instead, boards tend to view the disappointing performance as a direct reflection of managerial inadequacy or misalignment of incentives.

Third, generous CEO compensation heightens boards’ urgency to undertake corrective actions due to increased accountability pressures. When highly paid CEOs underperform relative to competitors receiving prestigious media awards, directors face intensified scrutiny from stakeholders who question the justification for high executive pay in the context of weak firm outcomes (Wang et al., 2017; Zhu, 2014). Boards, therefore, must act decisively, often through CEO dismissal, to restore legitimacy and credibility, mitigate reputational risks, and satisfy stakeholders’ expectations. Thus, we propose:

Hypothesis 2a: CEO compensation functions as a boundary condition, such that the positive joint effect of an underperforming firm and more award-winning CEOs in competing firms on CEO dismissal is stronger when CEO compensation is higher.

On the other hand, we propose that CEO compensation strengthens the negative relationship between a firm’s outperformance and CEO dismissal when more competitor CEOs receive media awards.

First, as argued in Hypothesis 1b, competitor CEO awards amplify the perceived significance of a firm’s outperformance. High CEO compensation sets further elevated expectations regarding managerial performance (O’Reilly et al., 1988; Zajac, 1990), causing boards to interpret superior performance in this competitive context as clear evidence that their CEO is meeting or surpassing these ambitious expectations. Because boards expect highly compensated CEOs to excel relative to industry peers, observing outperformance provides credible confirmation that the CEO’s managerial capabilities justify the substantial compensation investment, thus reducing motivations for dismissal.

Second, high CEO compensation influences how boards interpret the absence of media recognition for their CEO, given the presence of competitor CEO awards (Zhu, 2014). When the highly compensated CEO outperforms industry peers, boards are likely to believe media recognition for their CEO is forthcoming rather than overdue. Generous compensation signals boards’ pre-existing belief that the CEO possesses the managerial talent and leadership reputation required for eventual recognition (Zajac, 1990). Thus, instead of interpreting competitor CEO awards negatively, directors become more likely to interpret them as signals that media validation for their own highly compensated CEO is inevitable (Frey, 2006, 2007). This interpretation further reduces motivations for leadership change.

Third, high CEO compensation further strengthens directors’ commitment to maintaining leadership continuity amid competitor recognition. Directors who have made substantial investments in CEO compensation implicitly commit to their CEO’s strategic vision and leadership approach. Observing outperformance even as more competitor CEOs receive media awards reinforces the strategic validity of their substantial compensation investment (Zorn et al., 2020). Changing a highly compensated CEO who delivers strong performance in such intensive competitive environments involves considerable strategic and reputational risks. Therefore, boards’ prior compensation commitments symbolically and strategically reinforce their confidence that retaining their current CEO remains the best course of action. Thus, we propose:

Hypothesis 2b: CEO compensation acts as a boundary condition, such that the negative joint effect of an outperforming firm and more award-winning CEOs in competing firms on CEO dismissal is stronger for firms with higher CEO compensation.

Contingency Effects of Board Busyness

Building on board information processing theory, we further propose that board busyness, i.e., the extent to which directors have multiple external board commitments, also acts as a boundary condition to shape how boards interpret the combined signals of firm underperformance relative to industry peers and the presence of award-winning competitor CEOs (Ferris, Jagannathan, & Pritchard, 2003; Fich & Shivdasani, 2006; Harris & Shimizu, 2004). Specifically, when board busyness is lower, the positive relationship between a firm’s underperformance and CEO dismissal strengthens as the number of award-winning competitor CEOs increases.

First, lower board busyness provides directors with greater cognitive resources to recognize that their firm’s underperformance occurs simultaneously across multiple dimensions, particularly financial outcomes and managerial effectiveness, when more competitor CEOs receive prestigious awards. Directors with fewer external commitments have sufficient attentional capacity to integrate these distinct signals effectively (Harris & Shimizu, 2004; Ocasio, 1997). As a result, they clearly perceive that underperformance combined with competitors’ external recognition indicates serious managerial shortcomings, rather than isolated or temporary issues. Thus, less busy boards more readily identify critical leadership deficiencies within the firm.

Second, lower board busyness enhances directors’ ability to accurately attribute their firm’s underperformance to managerial deficiencies rather than comparative factors (Ferris et al., 2003; Haleblian & Rajagopalan, 2006; Seo, 2017). Directors with fewer external obligations have greater cognitive capacity to carefully assess competitor CEO recognition as clear evidence that superior leadership is attainable within the current environment. Consequently, they are more likely to interpret their firm’s underperformance as reflecting leadership issues rather than uncontrollable external circumstances, increasing their inclination toward CEO dismissal to achieve performance improvement.

Third, lower board busyness provides directors with sufficient capacity to better recognize stakeholder concerns and external scrutiny (Brandes, Dharwadkar, Ross, & Shi, 2022; Seo, 2017), clarifying the urgency to address managerial inadequacies revealed by firm underperformance and competitor CEO awards. Directors with fewer external commitments have greater capability to communicate with stakeholders and carefully interpret external evaluations, improving their understanding of stakeholders’ expectations for managerial accountability. Consequently, less busy boards become more attuned to stakeholders’ demands for decisive corrective actions, prompting quicker and more decisive responses, including CEO dismissal. Therefore, we propose:

Hypothesis 3a: Board busyness acts as a boundary condition such that the positive joint effect of firm underperformance and the presence of more award-winning competitor CEOs on CEO dismissal is stronger for firms with lower board busyness.

We further argue that the negative joint effect of firm outperformance and the presence of more award-winning competitor CEOs on CEO dismissal is stronger when board busyness is lower.

First, less busy boards possess greater cognitive capacity to systematically and comprehensively evaluate competitor CEO awards. Compared with their busier counterparts, whose limited attentional bandwidth constrains the depth of their assessments, less busy boards can more carefully consider the demanding standards reflected in these awards (Harris & Shimizu, 2004; Khanna et al., 2014). This fuller evaluation allows them to appreciate that achieving superior firm performance in an environment populated by externally validated competitors is a meaningful indicator of the incumbent CEO’s exceptional managerial capabilities rather than a product of favorable external conditions. Such nuanced interpretation strengthens their confidence in the CEO’s effectiveness and reduces the inclination toward dismissal.

Second, less busy boards have more attentional resources to examine why their CEO has not yet received external recognition despite strong and sustained performance (Harris & Shimizu, 2004; Ocasio, 1997; Seo, 2017). Directors with fewer external commitments can more accurately recognize that external awards often follow prolonged visibility and cumulative achievements, rather than immediate performance outcomes. Consequently, they are less likely to interpret the absence of current recognition as a managerial deficiency. Instead, they view it as a temporary lag that is likely to resolve as continued superior performance enhances the CEO’s visibility. This more informed assessment reduces the perceived need to initiate a leadership change.

Third, directors with lower levels of busyness have greater capacity to engage deeply with stakeholders and to carefully evaluate the strategic risks associated with replacing a high-performing CEO in a competitive landscape marked by frequent recognition of rival leaders (Brandes et al., 2022; Seo, 2017). Unlike busier directors, who have limited opportunities for such engagement, less busy boards can gather richer and more nuanced insights into stakeholder expectations surrounding leadership continuity. They can also more thoroughly assess the uncertainties and potential performance disruptions associated with leadership replacement in a context where strong competitor CEOs are externally validated. This broader and more comprehensive understanding reinforces their view that maintaining the incumbent CEO is strategically prudent, further decreasing the likelihood of dismissal. Therefore, we propose:

Hypothesis 3b: Board busyness acts as a boundary condition such that the negative joint effect of firm outperformance and the presence of more award-winning competitor CEOs on CEO dismissal is stronger for firms with lower board busyness.

Contingency Effects of Board-CEO Similarity

Demographic similarity between a CEO and board of directors also influences boards’ interpretation of the combined signals of firm underperformance and competitor CEO awards (Haleblian & Rajagopalan, 2006; Zhu & Westphal, 2014). Specifically, we argue that lower board-CEO demographic similarity strengthens the positive relationship between firm underperformance and CEO dismissal as the number of award-winning competitor CEOs increases.

First, board directors who share fewer demographic attributes with the CEO are less susceptible to interpersonal biases arising from shared identity and relational affinity (Fracassi & Tate, 2012; Westphal & Zajac, 1995; Zhu & Westphal, 2014). This lower level of relational identification enables them to evaluate the joint signals of firm underperformance and competitor CEO awards with greater objectivity. When their firm is underperforming relative to industry peers and more competitor CEOs are publicly recognized for strong leadership, demographically dissimilar directors are better able to see the contrast between their own firm’s disappointing performance and the attainable leadership standards exemplified by award-winning rivals. This clearer perception of the joint signal strengthens their assessment that the underperformance reflects genuine managerial inadequacy.

Second, directors with lower demographic similarity experience fewer interpersonal barriers when attributing responsibility for poor outcomes directly to the CEO (Haleblian & Rajagopalan, 2006; Zhu & Westphal, 2014). Because they lack the relational closeness that often leads similar directors to give the CEO the benefit of the doubt, demographically dissimilar directors are more willing to scrutinize the CEO’s role in the firm’s underperformance. In the presence of visible external cues such as competitor CEO awards, boards composed of more demographically dissimilar directors can more effectively compare their CEO’s leadership against these validated benchmarks. Their reduced relational attachment enables these boards to assign accountability directly and confidently, making them more inclined to attribute the firm’s weak performance to the CEO’s decisions rather than to environmental factors.

Third, lower demographic similarity reduces directors’ relational constraints when taking corrective action in the face of the joint signals of underperformance and competitor CEO awards (Shen, 2003; Zhu & Westphal, 2014). Directors who do not share demographic characteristics with the CEO feel less interpersonal discomfort initiating a leadership change. When the firm is underperforming and competitors’ CEOs are being publicly recognized, demographically dissimilar directors interpret these signals as evidence that stronger leadership is realistically attainable. Because they are less encumbered by personal loyalty or identification, these directors are more comfortable acting on this conclusion and supporting dismissal as a necessary corrective response. As a result, boards composed of more demographically dissimilar directors are more responsive to the joint signals of firm underperformance and competitor CEO awards, thereby strengthening the positive relationship between these signals and CEO dismissal. Therefore,

Hypothesis 4a: Board-CEO demographic similarity acts as a boundary condition such that the positive joint effect of firm underperformance and the presence of more award-winning competitor CEOs on CEO dismissal is stronger when board-CEO demographic similarity is lower.

We further propose board-CEO demographic similarity as a boundary condition shaping directors’ interpretation of the joint signals from firm outperformance and competitor CEO awards, such that the negative relationship between firm outperformance relative to industry peers and CEO dismissal, intensified by the presence of more award-winning competitor CEOs, is stronger when board-CEO demographic similarity is lower.

First, directors with lower demographic similarity to their CEO rely less on relational affinity and more on objective performance indicators when evaluating managerial effectiveness (Goergen, Limbach, & Scholz, 2015; Westphal & Zajac, 1995). Unlike demographically similar directors, whose favorable assessments may be viewed as biased due to interpersonal closeness, demographically dissimilar directors’ evaluations carry greater credibility with stakeholders. Consequently, when competitor CEOs receive prestigious awards, demographically dissimilar directors clearly and credibly recognize that firm outperformance, achieved within this highly competitive context, objectively demonstrates their CEO’s superior managerial ability. This credible endorsement significantly reinforces board confidence in the incumbent CEO and reduces incentives for dismissal.

Second, directors with lower demographic similarity are better positioned to credibly assess their CEO’s potential for future media recognition. Although demographically similar directors might reach the same conclusion, namely that their CEO’s current lack of awards is temporary, their evaluations are more likely discounted by the broader board as relationally biased or overly optimistic (Haleblian & Rajagopalan, 2006). In contrast, demographically dissimilar directors, less influenced by interpersonal affinity, objectively interpret media recognition as likely to follow superior performance and industry visibility. Consequently, their assessments are perceived as more impartial and rigorous, enhancing not only the board’s confidence in the CEO’s future media validation but also the overall credibility of the board’s evaluation process. This increased credibility further reduces motivations for CEO dismissal.

Third, lower demographic similarity reduces directors’ relational constraints, enabling more objective assessment of the strategic risks associated with CEO replacement. Unlike demographically similar directors who may hesitate due to relational affinity, demographically dissimilar directors experience fewer interpersonal barriers in objectively evaluating leadership continuity within highly competitive environments (Shen, 2003; Zhu & Westphal, 2014). Their objective endorsement of a consistently high-performing CEO signals to stakeholders that the retention decision is strategically sound rather than driven by interpersonal bias. This impartial assessment, perceived as more legitimate, reinforces directors’ strategic preference for maintaining leadership continuity, further diminishing the likelihood of dismissal.

As a result, boards composed of more demographically dissimilar directors are more likely to process the joint signals of firm outperformance and competitor CEO awards as credible validation of their CEO’s distinctive managerial capabilities, thereby strengthening the negative relationship between these signals and CEO dismissal. Therefore, we propose:

Hypothesis 4b: Board-CEO demographic similarity acts as a boundary condition such that the negative joint effect of firm outperformance and the presence of more award-winning competitor CEOs on CEO dismissal is stronger when board-CEO demographic similarity is lower.

Method

Sample and Data Collection

To test our hypotheses, we utilized data from multiple sources, including Standard and Poor’s (S&P) 1500 firms listed in the Institutional Shareholder Services (ISS) database, BoardEx, Compustat, Compustat Execucomp, and I/B/E/S, spanning the years 2006 to 2020. Our dataset comprises detailed director-, CEO-, firm-, and industry-level information. For consistency, we integrated CEO dismissal data from Gentry et al. (2021).

Given our focus on nonwinning CEOs, we restricted the sample to firms without star CEOs during the study period and excluded observations with incomplete data. This yielded an initial sample of 12,403 observations from 1,132 firms.

Using a conditional fixed-effects logit model as our primary analytical approach necessitated dropping firms without CEO dismissal events, resulting in a final sample of 3,498 observations from 300 firms. All predictor variables were lagged by one year.

To address potential right-censoring and sample attrition concerns inherent to conditional fixed-effects logit models, we also conducted event history analyses as robustness checks. These analyses consistently supported our main findings.

Variables

CEO dismissal

We employed the CEO departure dataset from Gentry et al. (2021), identifying dismissals based on their classification of “involuntary CEO dismissal.” This dataset ensures accuracy through rigorous validation of each turnover event using media reports and SEC filings. Our final sample comprises 402 CEO dismissal events.

Independent and Moderating Variables

C-awarded CEOs

We operationalized this variable in two stages. First, we identified industry competitors using the Text-based Network Industry Classification (TNIC-3) database (Hoberg & Phillips, 2010, 2016). Compared to traditional SIC classifications, TNIC-3 employs textual analysis of product descriptions from SEC 10-K filings, offering dynamic, customer-perceived product similarity measures that are updated annually. Consistent with prior research, we selected the 64 closest competitors per firm based on TNIC-3 similarity rankings. This threshold approximates the sample mean (51.18) plus 0.25 standard deviations (49.2), reflecting competitor distributions among S&P 1500 firms. To ensure size comparability, we included only competitors within 40%–60% of the focal firm’s size (Shi et al., 2017), thus enhancing measurement precision.

Second, we identified award-winning CEOs recognized by reputable outlets such as Businessweek, Chief Executive, Forbes, Morningstar, Barron’s, Fortune, and Institutional Investor (Malmendier & Tate, 2009; Shi et al., 2017). This yielded 1,053 firm-year observations from 354 unique firms.

Our final measure was a Griliches-deflated weighted count of award-winning competitor CEOs over the preceding three years. Following George, Kotha, and Zheng (2008), weights were assigned as 1 for the most recent year, 0.8 for one year prior, and 0.6 for two years prior, reflecting diminishing influence over time. Firms without award-winning competitors during this period received scores of zero.

Robustness checks varying competitor count thresholds and size parameters consistently supported our main findings.

Underperformance

Following prior research (e.g., Hu, Gentry, Quigley, & Boivie, 2023; Greve, 2003; Shin et al., 2022), we used ROA, calculated as net income divided by total assets, as our primary measure of firm performance. ROA is particularly suitable for board monitoring (Gentry et al., 2021; Shin et al., 2022) and provides a clearer measure of managerial capability compared to alternative metrics such as stock returns, which contain substantial market noise (Graffin, Carpenter, & Boivie, 2011), and ROE, which is influenced by capital structure (Simerly & Li, 2000). We measured firm underperformance relative to competitors by calculating the absolute difference between each firm’s ROA and the average ROA of its competitors (Greve, 2003). Firms whose ROA equaled or exceeded this competitor average were assigned a value of zero.

Outperformance

We measured firm outperformance based on their performance relative to competitors’ average ROA (Greve, 2003). Specifically, we calculated the absolute difference between each firm’s ROA and the competitors’ average, assigning zero to firms whose ROA was equal to or below this average.

CEO compensation

CEO compensation was measured as the natural logarithm of total realized compensation, including salary, bonus, restricted stock grants, exercised option values, long-term incentive payouts, and other compensation. Realized compensation reflects actual value received, making it relevant to board evaluations in dismissal (Chiu, Oxelheim, Wihlborg, & Zhang, 2016).

Board busyness

Following Ferris et al. (2003), we classified directors as busy if they held two or more directorships in a year, then calculated board busyness as the proportion of busy directors, excluding CEOs. To reduce annual variability, we used the average proportion of busy directors over the preceding three years (Richardson, 1987).

Similarity between boards and their non-winning CEOs (B-C similarity)

We measured board-CEO similarity across six demographic dimensions: age, gender, ethnicity, highest degree earned, Ivy League education, and functional background (Zajac & Westphal, 1996; Zhu & Westphal, 2014). Data for age, gender, and ethnicity were sourced from ISS. Education was categorized into PhD, master’s, bachelor’s, or lower. Ivy League education indicated graduation from one of the eight Ivy League universities, and functional background was classified as throughput, output, or peripheral functions (Westphal & Zajac, 1997).

We created dummy variables for similarity on each dimension, with age similarity defined by a difference less than one standard deviation (7.3 years in our sample). Using discrete principal components analysis, we combined these indicators into a single board-level similarity index (Zhu & Westphal, 2014). The average principal component scores between CEOs and directors provided a comprehensive measure of board-level demographic similarity, effectively addressing potential skewness (Harrison, Boivie, Sharp, & Gentry, 2018).

Control Variables

We accounted for potential confounding effects at multiple levels. At the firm level, we controlled for firm size using the natural logarithm of total assets, and for industry-adjusted firm performance, calculated as firm ROA minus the mean ROA within the same 4-digit SIC industry (Wang et al., 2017). Firm slack was captured using available slack (current assets/current liabilities), absorbed slack (working capital/sales), and potential slack (equity/debt), standardized and combined into a slack index (Tyler & Caner, 2016). We also controlled for advertising intensity (advertising expenses/sales ratio; Graffin et al., 2013), analyst assessments (analyst-number-weighted mean recommendation from I/B/E/S; Harrison et al., 2018), and negative earnings surprise, a binary indicator coded 1 if annual earnings fell below analysts’ consensus estimates, otherwise 0 (Wiersema & Zhang, 2011).

At the board level, we controlled for board independence (proportion of outside directors; Zajac & Westphal, 1996) and board minority ratio (proportion of ethnic minority directors).

For CEO-level controls, we measured CEO power using four indicators: CEO duality (binary variable, CEO as board chair), CEO ownership (percentage of shares owned), proportion of directors appointed during the CEO’s tenure, and CEO external board appointments. These indicators were standardized and combined into a CEO power index (Haynes & Hillman, 2010).

We also controlled for three industry-level factors. To capture competitive intensity, we included a binary indicator (more competitors) coded 1 if the firm’s competitor count exceeded the median within its TNIC competitive set, and 0 otherwise. Industry concentration was measured using the Herfindahl index, calculated from squared market shares within each 4-digit SIC industry (Finkelstein & Boyd, 1998). Industry dynamism was measured based on fluctuations in industry sales over a five-year window (Dess & Beard, 1984).

Finally, we included year dummy variables to account for time-fixed effects, though their coefficients are not reported for parsimony.

Analytical Approach

Given our binary dependent variable (CEO dismissal, coded as 0 or 1), we utilized a conditional fixed effects logit model (Hoetker, 2007; Wooldridge, 2020). This method appropriately captures probabilistic outcomes and effectively addresses unobserved, time-invariant firm characteristics through firm fixed effects (Greene, 2018; McFadden, 1973; StataCorp, 2019). By isolating within-firm variation, our approach inherently controls for numerous unobserved firm-specific factors potentially influencing CEO dismissal decisions (Greene, 2018). Standard errors were clustered at the firm level to correct for within-firm correlation and heteroskedasticity, enhancing estimate reliability (Wooldridge, 2020). Additionally, continuous variables were standardized before constructing interaction terms to minimize multicollinearity and improve interpretability of coefficients.

Sample Selection Bias Correction

We were aware that our study could experience sample selection bias, as we excluded firms with award-winning CEOs from hypothesis testing (Certo et al., 2016). Although our theory emphasizes nonwinning CEOs, award-winning status itself might affect board dismissal decisions (Park, Kim, & Sung, 2014). To address this, we applied a Heckman two-stage correction model (Heckman, 1979).

In the first stage, we conducted a probit regression predicting the likelihood that a firm lacked an award-winning CEO, using our control variables and an exclusion restriction, lack of analyst attention. Lack of analyst attention, defined as the difference between total available analysts and those covering the focal firm, is an appropriate instrument since lower analyst coverage implies reduced visibility and award likelihood. First-stage results confirmed that lack of analyst attention significantly predicts firms not having award-winning CEOs (β = 0.08, p < 0.001). A Wald-test supported this exclusion restriction’s validity (χ2 = 30.97, p < 0.001) (Wolfolds & Siegel, 2019).

In the second stage, we integrated the inverse Mills ratio from the first-stage regression into our analyses to correct for sample selection bias (Certo et al., 2016; Heckman, 1979). This step ensures more robust estimates by adjusting for potential bias due to excluding award-winning CEOs. The inverse Mills ratio is calculated as:

where pr is the predicted probability from the probit model,

Results

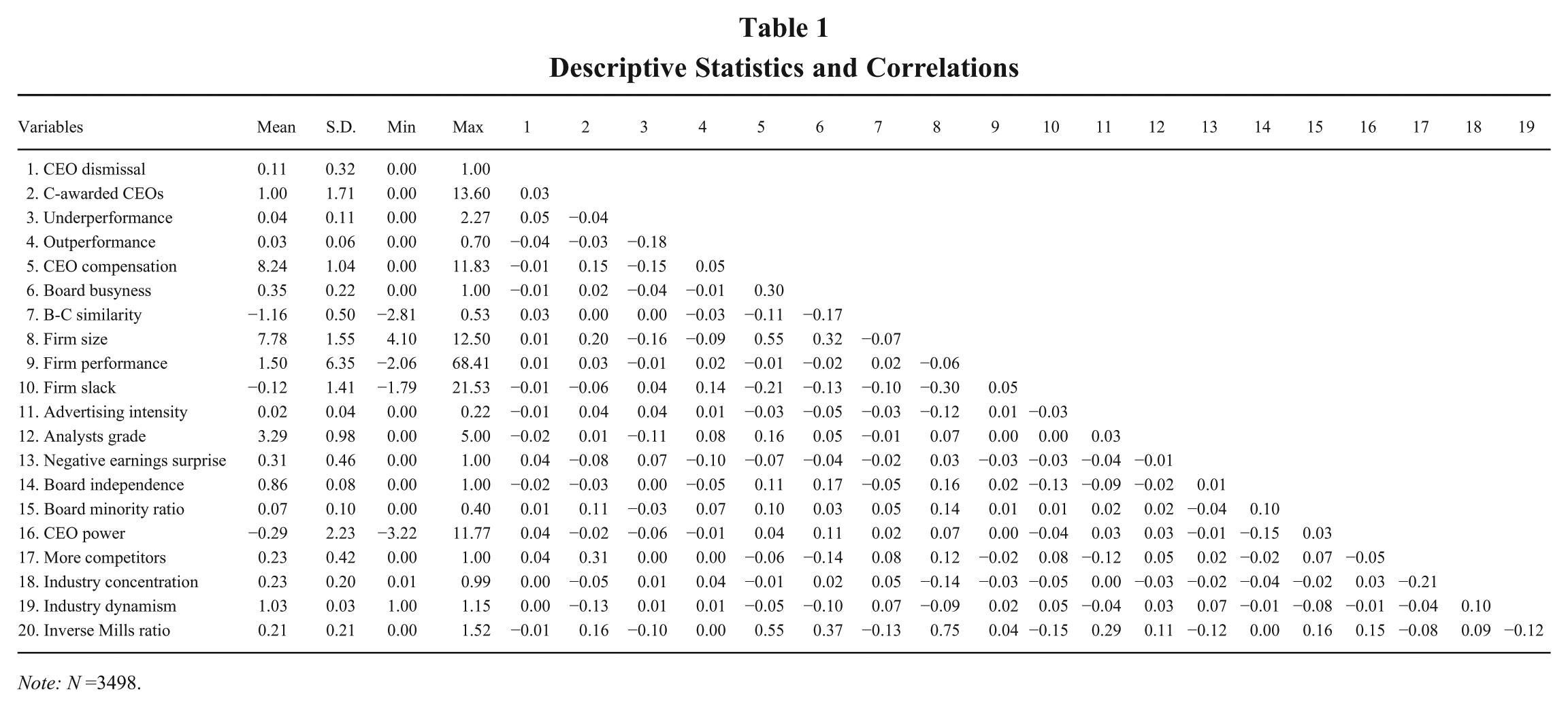

Table 1 provides descriptive statistics and correlations. To address potential multicollinearity, we computed variance inflation factors (VIF), with values ranging from 1.05 to 6.04, below the standard threshold of 10, indicating no significant multicollinearity concerns (Hair, Black, Babin, & Anderson, 2010).

Descriptive Statistics and Correlations

Note: N =3498.

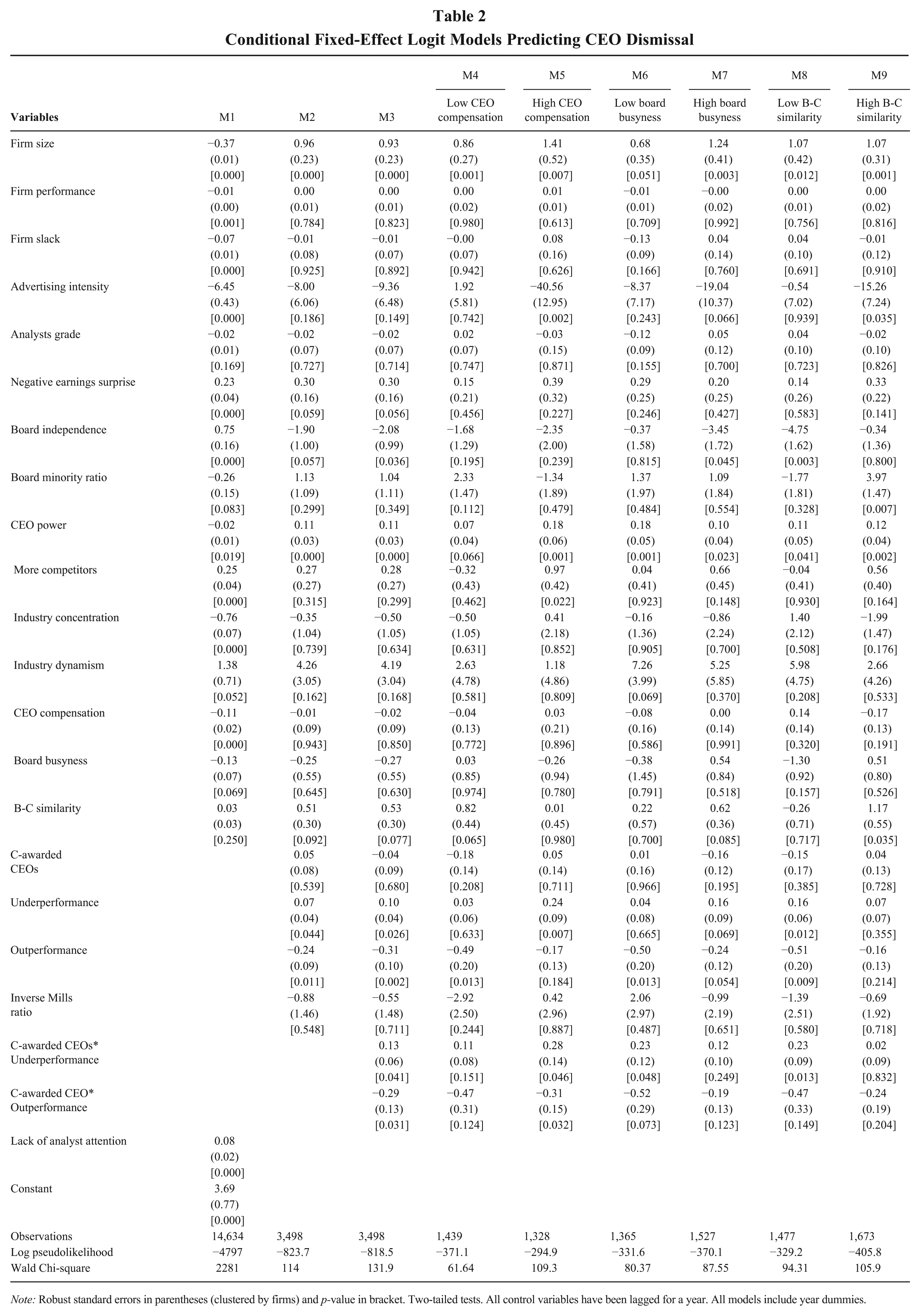

Table 2 presents the regression models. Model 1 presents results from the first-stage Heckman selection analysis, while Models 2–9 report hypothesis-testing results. Model 2, our baseline, includes only control variables. Model 3 adds interactions of underperformance and outperformance with competitor-awarded (C-awarded) CEOs. Models 4–9 explore moderating effects through subsample analyses of CEO compensation, board busyness, and board-CEO demographic similarity.

Conditional Fixed-Effect Logit Models Predicting CEO Dismissal

Note: Robust standard errors in parentheses (clustered by firms) and p-value in bracket. Two-tailed tests. All control variables have been lagged for a year. All models include year dummies.

In testing Hypotheses 1a and 1b, Model 3 reveals that underperformance interacting with C-awarded CEOs significantly increases dismissal likelihood (β = 0.13, p = 0.041), supporting Hypothesis 1a. Conversely, outperformance interacting with C-awarded CEOs significantly decreases dismissal likelihood (β = −0.29, p = 0.031), supporting Hypothesis 1b. While interaction interpretation in nonlinear models is complex, the coefficient directions clearly indicate these general effects.

To illustrate interaction magnitudes, we computed percentage changes in odds ratios. With each unit increase in C-awarded CEOs, dismissal odds associated with underperformance rose from 1.51% to 3.51%, confirming a positive effect. Conversely, dismissal odds associated with outperformance decreased from −2.45% to −4.69%, confirming a negative effect.

To test boundary conditions, we conducted subsample analyses. For CEO compensation (Models 4 and 5), the interaction between C-awarded CEOs and underperformance is significant only for high compensation (Model 5: β = 0.28, p = 0.046), supporting Hypothesis 2a. Increasing C-awarded CEOs raised dismissal odds from 3.67% to 8.11% in high-compensation firms. Similarly, the negative interaction with outperformance was significant only for high compensation (Model 5: β = –0.31, p = 0.032), supporting Hypothesis 2b, decreasing dismissal odds from −1.35% to −3.77%.

For board busyness (Models 6 and 7), the interaction with underperformance was significant for less busy boards (Model 6: β = 0.23, p = 0.048), supporting Hypothesis 3a, with dismissal odds increasing from 0.60% to 4.13%. The interaction with outperformance was marginally significant for less busy boards (Model 6: β = −0.52, p = 0.073), supporting Hypothesis 3b, with odds decreasing from −3.92% to −7.84%.

Regarding board-CEO similarity (Models 8 and 9), the interaction between C-awarded CEOs and underperformance was significant for low similarity boards (Model 8: β = 0.23, p = 0.013), supporting Hypothesis 4a, increasing dismissal odds from 2.43% to 6.02%. The interaction with outperformance was nonsignificant for both subsamples, failing to support Hypothesis 4b.

Coefficient comparisons using Z-tests provided statistically significant support for H4a (p < 0.10, one-tailed). For H2a, H3a, H3b, and H4b, the direction of differences aligned with hypotheses but lacked significance, likely due to reduced power in conditional subsample analyses.

Robustness Checks

We conducted multiple additional analyses to verify the robustness of our findings (see Online Appendix). These include addressing potential omitted-variable bias, employing alternative definitions of competing firms, using different analytical models, and applying alternative measures of key boundary conditions. The results consistently support our primary conclusions (Online Appendix Tables A1–A7).

Discussion

Our study advances the literature on CEO dismissal by shedding new light on how boards integrate comparative information, specifically competitor CEO awards, into their CEO performance evaluations. While prior research has extensively documented the influence of financial performance and organizational conditions on dismissal decisions (Chen & Hambrick, 2012; Jenter & Kanaan, 2015; Park et al., 2020), relatively few studies explicitly examine how social signals from competitors shape directors’ interpretations of financial performance (Graffin et al., 2013; Shin et al., 2022). Existing work has implicitly acknowledged boards’ attention to competitive contexts but has rarely examined systematically how such contexts influence governance decisions (Khanna et al., 2014; Zorn et al., 2020). By demonstrating that competitor CEO awards serve as salient benchmarks influencing boards’ evaluations, our research provides a more contextually embedded understanding of CEO dismissal.

Contributions and Implications

Our findings thus make several contributions. First, our insight extends prior CEO dismissal studies, which largely emphasize absolute performance indicators such as profitability or market share (Flickinger et al., 2016; Jenter & Kanaan, 2015). While acknowledging that financial results remain central, our findings emphasize the critical role comparative signals play in amplifying or mitigating the implications of these results for dismissal decisions. Specifically, when competitors’ CEOs are publicly recognized, boards interpret underperformance as more severe evidence of managerial inadequacy, prompting decisive governance actions. Conversely, when a CEO consistently outperforms industry peers despite visible media recognition of competitors, directors interpret such performance as exceptional, reinforcing their commitment to retaining the incumbent leader. By integrating comparative benchmarks explicitly into our theorizing, we enrich the dismissal literature by illuminating a previously underexplored contextual dimension of CEO evaluation.

Further, our findings deepen the application of board information processing theory in governance research. This theoretical lens emphasizes directors’ bounded rationality and selective attention, highlighting how boards manage informational complexity to reach effective governance decisions (Boivie et al., 2016; Busenbark et al., 2016; Forbes & Milliken, 1999). While existing research applying this perspective primarily focuses on boards’ processing of firm-specific information (Krause et al., 2025; Wowak et al., 2022), our study explicitly demonstrates that boards also integrate and interpret comparative signals from competitors. Competitor CEO awards, which serve as credible and institutionally endorsed indicators of managerial excellence (Graf-Vlachy, Oliver, Banfield, König, & Bundy, 2020; Jensen et al., 2022), represent precisely the type of complex, ambiguous information that boards must process collectively. Our empirical analyses illustrate how directors selectively prioritize and interpret these comparative signals to contextualize financial performance. This insight broadens the theoretical understanding of board decision-making, highlighting directors’ active engagement with comparative information as a fundamental component of their governance responsibilities.

Our study also contributes to literature on social evaluation and managerial awards by highlighting important indirect competitive effects. Prior research extensively documents how executive awards enhance recipients’ status, legitimacy, and stakeholder trust, often focusing on direct benefits to individual awardees and their organizations (Gallus & Frey, 2016; Graf-Vlachy et al., 2020; Malmendier & Tate, 2009). However, we extend this literature by revealing meaningful spillover effects that influence managerial evaluations within competing firms. Specifically, we demonstrate that recognition awarded to competitors’ CEOs not only elevates those executives’ status but also recalibrates broader industry standards, affecting evaluations of nonrecipient CEOs. This extends recent discussions by Graf-Vlachy et al. (2020) regarding the symbolic and legitimacy-enhancing functions of executive awards, suggesting that such awards have industry-wide implications beyond individual recipients. Thus, our findings underscore the significant competitive externalities of social recognition, revealing executive awards as powerful governance-relevant benchmarks that shape strategic decision-making across firms.

Practically, our results offer substantial implications for boards and governance practitioners. Directors need to recognize explicitly that their evaluations of CEO performance inherently involve comparative judgments informed by benchmarks, particularly the visibility of competitor CEOs’ achievements. Awareness of these comparative influences can help boards manage stakeholder expectations and ensure that their leadership assessments remain credible and well-justified. By proactively incorporating comparative evaluations into their deliberative processes, boards can enhance strategic decision-making, effectively navigate governance challenges, and reduce unintended biases.

Limitations and Avenues for Future Research

Despite these contributions, our study has several limitations highlighting opportunities for future research. First, our theoretical discussion centers on boards’ reactions to nonwinning CEOs without differentiating between shortlisted CEOs and those never shortlisted. Being shortlisted itself may confer status benefits or legitimacy signals, potentially affecting board evaluations differently than complete exclusion. Future research could explicitly explore this distinction to deepen our understanding of how boards interpret other environmental signals.

Second, data constraints prevented consideration of additional dimensions of CEO status, celebrity, or reputation that may also affect boards’ evaluations. Subsequent studies could incorporate broader measures, such as media coverage, social media influence, and executive reputation scores, to provide a more comprehensive view of how multiple validation forms collectively influence governance outcomes.

Third, our theoretical framework focuses on boards’ evaluation of managerial operating capability through financial indicators. Accordingly, our empirical findings demonstrate robust interactions with ROA, a direct measure of operating efficiency, but not with market-based measures such as industry-adjusted stock returns or ROE. The insignificance of these alternative metrics implies that competitor comparisons primarily shape boards’ interpretation of managerial effectiveness rather than their reactions to market sentiment or capital structure decisions. Future studies could investigate conditions under which market-based performance indicators might interact with peer recognition to affect board decision-making.

Supplemental Material

sj-docx-1-jom-10.1177_01492063261436351 – Supplemental material for How Boards Use Competitor CEO Awards to Interpret Firm Performance in CEO Dismissal Decisions

Supplemental material, sj-docx-1-jom-10.1177_01492063261436351 for How Boards Use Competitor CEO Awards to Interpret Firm Performance in CEO Dismissal Decisions by Jingyu Li, Steven Boivie and Yi Yang in Journal of Management

Footnotes

Acknowledgements

The authors gratefully acknowledge the Associate Editor, Prof. Wei Shi, and the two anonymous reviewers for their constructive and insightful feedback, which significantly improved the manuscript. This work was supported by the National Natural Science Foundation of China (Grant No. 72202198).

Supplemental material for this article is available with the manuscript on the JOM website.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.