Abstract

Although some scholars in strategic human resource management (SHRM) research have suggested that HRM investments can be effective in reducing the negative repercussions of employee downsizing, other scholars have argued that such HRM investments could convey contradictory messages to employees, resulting in more negative employee reactions and decreased firm performance. In this research, we addressed this unsettled question by looking into the mergers and acquisitions (M&A) context, where we theorized that the acquiring firm’s HRM investments can positively moderate the negative effect of employee downsizing on firm performance by invoking positive sensemaking processes from remaining acquired firm employees. Moreover, the positive sensemaking effects of HRM investments extend beyond remaining acquired firm employees to influence the overall performance of the merged firm. We examined established HRM investments by acquiring firms prior to the M&A and additional HRM investments made after the M&A. Using a representative sample of 5,467 firm-year observations from 1,214 U.S. publicly traded firms between 2002 and 2018, we found that both pre- and post-acquisition HRM investments by acquiring firms mitigate the negative effect of employee downsizing following M&A on firm performance. We discuss the implications of these findings for both research and practice.

Mergers and acquisitions (M&A) are often followed by employee downsizing—a workforce reduction in which workers’ employment is not terminated for cause (cf. Brauer & Zimmermann, 2019; Datta, Guthrie, Basuil, & Pandey, 2010; Trevor & Nyberg, 2008). Acquiring firms use employee downsizing to achieve smoother post-acquisition integration and/or better financial results (Lehto & Böckerman, 2008; Malikov, Demirbag, Kuvandikov, & Manson, 2021; O’Shaughnessy & Flanagan, 1998). For example, Microsoft announced the layoff of approximately 1,900 employees (about 8% of the total workforce) in its gaming unit just 3 months after completing its acquisition of Activision Blizzard in October 2023, aiming to reduce strategic and operational redundancies (Peters, 2024). However, in contrast to the expected firm-level benefits from post-acquisition downsizing, it has long been documented that remaining employees—downsizing survivors—tend to react negatively to downsizing, with diminished work motivation and productivity, which can substantially undermine firm performance (Datta et al., 2010).

A reading of the strategic human resource management (HRM) literature suggests that investments in HRM may be an effective way to alleviate the negative repercussions of downsizing (e.g., Brockner, Wiesenfeld, Reed, Grover, & Martin, 1993; Chadwick, Hunter, & Walston, 2004; Naumann, Bies, & Martin, 1995). In particular, HRM investments can help employees maintain their motivation (cf. Brockner & Wiesenfeld, 1996; Trevor & Nyberg, 2008) and allow the downsized firms to restore human capital resources by attracting, retaining, and developing skilled employees (Wright, Dunford, & Snell, 2001).

Interestingly, however, some existing research suggests that coupling workforce reduction strategies such as downsizing with HRM investments can produce unintended, counterproductive effects (Iverson & Zatzick, 2011; Wood & Ogbonnaya, 2018; Zatzick & Iverson, 2006). Scholars of these studies argue that this combination sends contradictory signals to employees. Specifically, layoffs are usually perceived as a breach of management’s long-term commitment to the workforce, as signaled by HRM investments, often resulting in psychological distress among surviving employees (e.g., Chadwick et al., 2004). As a result, survivors may view management’s signals of commitment as disingenuous, leading to stronger negative reactions and reduced performance outcomes than otherwise would arise from downsizing alone (Wood & Ogbonnaya, 2018; Zatzick & Iverson, 2006).

These divergent perspectives in the literature suggest that our understanding of the implications of coupling HRM investments with employee downsizing remains limited. Notably, the context in which downsizing occurs may significantly shape its implications, yet this factor is often underexplored. To address this gap, we focused on M&A—a setting characterized by large-scale organizational change where downsizing is common and where two previously independent firms and their workforces must be integrated. This setting presents unique challenges and opportunities for organizations, making it particularly well suited for investigating how HRM investments can influence post-downsizing performance.

Drawing on a sensemaking framework, we propose that in the context of M&A, the acquiring firm’s HRM investments can positively moderate the relationship between employee downsizing and firm performance. Specifically, we argue that the M&A context invokes a nontrivial sensemaking process wherein employees seek to identify and interpret environmental cues to make sense of the newly formed organization (Weick, 1995; Weick, Sutcliffe, & Obstfeld, 2005). We posit that the acquiring firm’s HRM investments can serve as meaningful cues, revealing underlying managerial values and intentions toward the workforce (Bowen & Ostroff, 2004; Nishii, Lepak, & Schneider, 2008). This process is likely to be particularly salient for employees of the acquired firm, who often face heightened ambiguity and uncertainty in the merged firm and thus have a greater need for sensemaking. Furthermore, we suggest that such sensemaking not only enhances attitudes and performance of acquired employees but also contributes to the broader organizational performance of the merged firm. This is because HRM-enabled sensemaking among acquired employees can foster the retention and development of firm-level human capital resources by influencing the behavior, cognition, and affect (Ployhart & Moliterno, 2011) of both acquired and acquiring firm employees—ultimately improving overall organizational effectiveness.

In this study, we examined the role of both HRM investments established prior to the M&A and additional HRM investments made in the post-M&A period. We adopted this comprehensive approach because both the existing stock of human capital resources (built from pre-M&A HRM investments) and the continued flow of such resources (facilitated by post-M&A HRM investments) can influence firm performance (Ployhart, Weekly, & Ramsay, 2009). Moreover, additional HRM investments after M&A can reinforce the sensemaking process by strengthening employees’ belief in positive managerial intentions.

To test our hypotheses, we drew on a representative sample of 5,467 firm-year observations from 1,214 U.S. publicly traded firms spanning the period from 2002 to 2018. We found support for our hypothesis that both the acquiring firm’s established HRM investments (pre-M&A) and the adoption of additional HRM investments (post-M&A) positively moderate the negative effect of post-M&A downsizing on firm performance. Moreover, we found that this moderation effect is not observed in non-M&A contexts.

Our research contributes to multiple research streams. First, given the inconclusive findings on the joint impacts of HRM and downsizing in the strategic HRM (SHRM) literature, we address this gap by highlighting M&A as an important yet underexplored context in which HRM investments can positively influence employee perceptions of downsizing. Second, we contribute to M&A research by highlighting the importance of the “people influence” on post-M&A firm performance (Mirc, 2014; Weber & Fried, 2011). Although previous research has noted that people are a crucial factor in achieving M&A success (Bauer & Matzler, 2014; Larsson & Finkelstein, 1999), most of the existing empirical research only provides evidence from anecdotal stories or case analyses (Aklamanu, Degbey, & Tarba, 2016; Bagdadli, Hayton, & Perfido, 2014; Birkinshaw, Bresman, & Håkanson, 2000; Cooke, Wood, Wang, & Li, 2021; Nikandrou & Papalexandris, 2007; Weber & Tarba, 2010). Last but not least, we respond to calls to investigate the effects of firms’ HRM investments during organizational changes (Chadwick & Flinchbaugh, 2021; Ployhart et al., 2009; Snell & Morris, 2021; Weber & Fried, 2011). M&A are among the most prevalent forms of such change, involving substantial shifts in organizational structures and workforce composition. Understanding the role of HRM investments before and after M&A is therefore critical.

Theory and Hypotheses

Negative Effect of Post-M&A Employee Downsizing

Employee downsizing is frequently conducted in an M&A process for several reasons. First, it is perceived as a means to streamline operations by reducing redundancies created through the merger, thereby enabling the firm to fully realize economies of scale and scope from the acquisition (O’Shaughnessy & Flanagan, 1998). Second, downsizing can be used to focus on the strategic objectives of the newly combined firm after an M&A (Chatterjee, 1992). Third, by cutting costs associated with employees, such as salaries, benefits, and other expenses, firms can use downsizing to improve short-term financial performance after an M&A (Krishnan, Hitt, & Park, 2007).

Outside of the M&A context, however, prior research has consistently found a largely negative association between employee downsizing and people-related dimensions of organizational effectiveness, such as creativity and productivity (Datta et al., 2010). This effect can be explained by two underlying employee-related mechanisms. The first mechanism is a reduction in surviving employees’ morale. Employees who stay with their firm after a downsizing event can be demotivated by psychological contract breaches (Morrison & Robinson, 1997). Consequently, surviving employees may withhold effort (particularly discretionary effort), reduce involvement, increase absenteeism, and even voluntarily leave the organization (Datta et al., 2010; Trevor & Nyberg, 2008). The second mechanism involves losses in human and social capital (Datta et al., 2010). Employee downsizing typically undermines an organization’s human capital resources—a collective form of employee knowledge, skills, and abilities that exists at the firm level (Ployhart et al., 2009). At the same time, downsizing also can disrupt an organization’s collective social connections (Shaw, Park, & Kim, 2013) as well as its strategic routines and capabilities embedded within those networks (Brauer & Laamanen, 2014; Chadwick et al., 2004).

Previous studies have suggested that the negative impacts of downsizing on surviving employees also can occur in the M&A context (Krishnan & Park, 2002; Malikov et al., 2021). In line with the first mechanism discussed above, surviving employees from both the acquiring and acquired firms may experience heightened insecurity and uncertainty about their futures within the merged organization following downsizing (Brockner, Grover, Reed, DeWitt, & O’Malley, 1987; Paulsen et al., 2005). These feelings can lower employee morale and discourage employees from investing effort in the merged firm. Importantly, downsizing may exacerbate “we vs. they” antagonism in the employer–employee relationship (Greenwood, Hinings, & Brown, 1994), particularly among employees who have already undergone significant identity shifts, role changes, and culture shocks during the M&A process.

In addition to its motivational effects, downsizing also can undermine the newly merged firm’s human and social capital—the second mechanism discussed above. By eliminating employees embedded in organizational networks, downsizing may result in the unintended loss of organizational knowledge and expertise essential for post-merger integration and performance (Krishnan et al., 2007). This risk can be particularly acute when the acquiring firm lays off a significant number of employees from the acquired firm, especially those who possess valuable firm-specific human capital—such as tacit knowledge and specialized skills—that cannot be easily replicated. In fact, such human capital often represents a core component of the strategic value sought in the acquisition and plays a critical role in determining the success of the merger.

In short, when downsizing follows an M&A, employee motivation may decline, and the development of firm-specific human capital and social capital can be disrupted, ultimately undermining organizational integration and performance. However, empirical evidence on the negative effect of downsizing in the M&A context remains limited (Krishnan & Park, 2002; Malikov et al., 2021). Accordingly, we began by testing an expected negative relationship between post-M&A downsizing and firm performance as a foundation for our subsequent theoretical development:

Hypothesis 1: Employee downsizing following an M&A is negatively related to firm performance.

Mitigating Role of HRM Investments on Post-M&A Downsizing Effects

Studies in the SHRM literature have suggested that investing in HRM may help mitigate the negative effect of employee downsizing. Specifically, investments in practices such as training, internal promotion, career development, flexible working arrangements, diversity and equal opportunity, and employee health and safety—variously labeled in prior research as HRM inducements (Shaw, Dineen, Fang, & Vellella, 2009), maintenance-oriented HRM systems (Gong, Law, Chang, & Xin, 2009), or high-investment HR systems (Jiang, Takeuchi, & Jia, 2021)—have been shown to enhance organizational effectiveness by cultivating a motivated and skillful workforce (Wright et al., 2001) and by promoting a sense of fairness and reciprocity between employers and employees (Brockner & Wiesenfeld, 1996; Tsui, Pearce, Porter, & Tripoli, 1997).

However, some empirical SHRM research has found that coupling HRM investments with employee downsizing can be detrimental to firm performance (e.g., Iverson & Zatzick, 2011; Zatzick & Iverson, 2006). In other words, HRM investments may increase rather than mitigate downsizing’s negative effects on firm performance. Employee downsizing can disrupt the accumulation of firm-specific human capital and hinder the development of organizational capabilities that HRM investments are intended to foster (Paulsen et al., 2005), thereby partially offsetting the gains from such investments. Moreover, downsizing can send signals to workers that starkly contrast with the expectations of reciprocity and mutual benefit that HRM investments are designed to promote (Tsui et al., 1997). These conflicting signals may heighten surviving employees’ perceptions of psychological contract breaches, leading to negative attitudes and behaviors (e.g., disengagement, withdrawal behavior, and absenteeism), reduced in-role and extra-role performance (Turnley, Bolino, Lester, & Bloodgood, 2003), and increased voluntary turnover after downsizing (Trevor & Nyberg, 2008).

The uniqueness of the M&A context

In the context of an M&A, however, employees’ reactions to the combination of downsizing and HRM investments may be different. In a non-M&A context, coupling HRM investments with downsizing is likely to be perceived by employees as a psychological contract breach because contradictory actions from the same management team send mixed signals or meta-messages. A key difference in an M&A context is that these signals may be perceived as coming from a new and different management team—that of the merged entity—from the perspective of the acquired firm’s employees. Indeed, employees of acquired firms often anticipate downsizing and restructuring as part of the M&A process, but they typically have few clear expectations about how the acquiring firm’s management will treat them otherwise. Moreover, because they have not built a history with the acquiring or merged firm’s leadership, acquired firm employees tend to hold a relatively weak psychological contract shortly after M&A.

Accordingly, an M&A context can lessen the immediate sense of psychological contract breach resulting from downsizing (albeit not the anxiety and uncertainty) for acquired firm employees. Rather, the disruptive organizational changes inherent to M&A can trigger surviving employees from the acquired firm to engage in rebuilding their organizational identity within the newly merged organization (Giessner, Horton, & Humborstad, 2016). In this process, they are highly attuned to signals regarding how the acquiring firm (i.e., the new management team) approaches employee relationships and therefore can be reassured by positive signals from the acquiring firm’s managers.

This effect can be understood through the lens of sensemaking (Weick, 1995; Weick et al., 2005). According to the sensemaking perspective, organizational events that have not been frequently encountered in the past induce employees to engage in sensemaking—a process through which individuals give meaning to ambiguous or unexpected experiences. Specifically, during significant organizational changes, employees may undergo a sense-breaking process (Monin, Noorderhaven, Vaara, & Kroon, 2013), whereby their existing understanding of their relationships with the firm—grounded in prior norms—no longer appears applicable. This disruption, in turn, can trigger a new sensemaking process when appropriate cues are presented.

Because M&A events introduce substantial uncertainty and disruption among employees, they tend to prompt employees to question or devalue their prior experiences or attitudes toward the organization—or even toward organizational life more broadly (Monin et al., 2013; Vaara, 2003). Thus, we posit that following an M&A, which serves as a sense-breaking event, employees, particularly those from the acquired firm, are likely to interpret employee downsizing—as part of sensemaking around a distinct organizational phenomenon, based on key cues they perceive in the merged firm—differently than they might in a non-M&A context. 1

Acquiring firm’s pre-M&A HRM investments

In particular, we propose that the acquiring firm’s existing HRM investments, established prior to the M&A, can serve as critical informational cues for acquired firm employees to reconstruct sensemaking positively (Monin et al., 2013; Vaara, 2003). The level and nature of a firm’s investment in HRM can reflect its underlying managerial values and intentions (Bowen & Ostroff, 2004; Nishii et al., 2008). From the employee–employer relationship perspective, such investments signal the firm’s commitment to its workforce and its concern for employee benefits and well-being (Tsui et al., 1997). Prior research (e.g., Cooke et al., 2021) has suggested that investments in HRM practices such as training and development can lead employees to form more favorable perceptions of the organization during post-merger integration. In addition, HRM policies and practices that promote diversity and equal opportunity may encourage employees to interpret layoff decisions relatively more positively (Ellis, Reus, & Lamont, 2009) because such practices are grounded in principles of justice and fairness (Brockner & Wiesenfeld, 1996; Trevor & Nyberg, 2008). Overall, the presence of established HRM investments before an M&A offers acquired firm employees important informational cues about managerial intentions that can help shape their sensemaking positively. Thus, HRM investments can help mitigate (though not entirely eliminate) the potential negative repercussions of employee downsizing amid the discontinuity and ambiguity that often follow an M&A. 2

Although our discussion thus far has focused primarily on the acquired firm’s employees, we further propose that the positive sensemaking effects of HRM investments extend beyond this particular group to influence the overall performance of the merged firm. This broader impact arises through three distinct yet interrelated mechanisms by which acquired firm employees contribute to the accumulation of human capital resources in the merged organization by shaping the behavioral, cognitive, and affective responses (Ployhart & Moliterno, 2011) of employees in the acquiring firm.

First, from a behavioral perspective, when acquired firm employees hold positive attitudes, facilitated by sensemaking triggered through HRM investments, they are more likely to collaborate effectively with colleagues from the acquiring firm. This improved cooperation reduces post-merger coordination costs by freeing the acquiring firm’s employees from unnecessary conflicts and adjustments in workflows and routines. As a result, employees from the acquiring firm can conserve time and cognitive resources.

Second, from a cognitive perspective, favorable sensemaking by acquired firm employees facilitates the sharing and transfer of tacit knowledge within the newly merged organization. Because much of a target firm’s know-how is embedded and difficult to codify (i.e., tacit), acquiring firms often struggle to unlock the full value of mergers (Krishnan & Park, 2002). However, when positive sensemaking induces the acquired firm employees to be more engaged, they are more likely to convert tacit knowledge into transferable knowledge and share it with acquiring firm employees, enabling the merged firm to pursue its strategic objectives from the acquisition more effectively.

Finally, from an affective perspective, positive attitudes can be contagious. When acquiring firm employees encounter openness and cooperation from acquired firm employees, social exchange norms can trigger reciprocal emotional responses. This dynamic can help mitigate the “in-group vs. out-group” biases commonly observed in merged organizations (Greenwood et al., 1994). As a result, morale and commitment among both groups may increase, enhancing their engagement in post-merger integration efforts and improving overall organizational effectiveness. In sum, we argue that an acquiring firm’s established HRM investments can lessen the magnitude of the potential negative effect of downsizing on overall firm performance following an M&A:

Hypothesis 2: Acquiring firms’ established HRM investments positively moderate the negative relationship between post-acquisition downsizing and firm performance such that for acquiring firms with higher established HRM investments, this negative relationship is weaker.

Acquiring firms’ post-M&A HRM investments

Although the acquiring firm’s prior investments in HRM can influence employee sensemaking processes, HRM investments made after the M&A transaction also can carry significant managerial implications. Accordingly, we examined not only the pre-acquisition HRM investments made by the acquiring firm but also its post-acquisition HRM investments. This comprehensive approach acknowledges the importance of both the existing stock of human resources, built through prior investments, and the ongoing flow of resources, maintained through post-acquisition investments, in driving organizational performance (Ployhart et al., 2009).

Sensemaking is a process that evolves over time (Weick, 1995; Weick et al., 2005). Thus, employees refine their understanding of the firm based on continuous interactions with the environment. In the post-M&A context, the further adoption of new HRM policies—alongside existing HRM investments—sends a strong signal to surviving employees that the organization values their contribution and engagement. Such ongoing reassurance can help employees ease negative reactions and adopt a forward-looking perspective regarding their future within the newly merged firm. Indeed, prior research has indicated that employees often interpret additional HRM investments as a sign of the organization’s commitment to its employees (Zacharatos, Barling, & Iverson, 2005; Zatzick & Iverson, 2006).

In addition, the implementation of new HRM practices and policies can signal that the firm is actively addressing emerging HRM challenges associated with the M&A (Weber & Fried, 2011; Weber & Tarba, 2010) and downsizing and is doing so in an employee-oriented manner. Organizational restructuring often brings substantial changes to job roles and requirements. In such circumstances, additional HRM investments may be interpreted by employees as a managerial effort to rebuild and strengthen firm-level human capital resources.

Furthermore, firms may engage in additional HRM investments not only to address immediate HRM challenges but also to adapt to broader and evolving organizational conditions. This reflects the idea that the HRM function is interconnected with other organizational systems and that a static set of policies may be insufficient to meet the demands of a dynamic environment (Helfat & Peteraf, 2003; Sirmon, Hit, & Ireland, 2007; Teece, Pisano, & Shuen, 1997). As such, additional investments in HRM can signal to employees that the firm recognizes broader organizational challenges following the M&A and downsizing and is committed to resolving them, alongside specific HR issues arising from the transition. Against this backdrop, we hypothesize the following:

Hypothesis 3: Acquiring firms’ additional HRM investments positively moderate the negative relationship between post-acquisition downsizing and firm performance such that for acquiring firms with more additional HRM investments, this negative relationship is weaker.

Method

Data and Sample

We used publicly traded U.S. companies to examine our hypotheses, combining information from four independent databases: the Thomson Reuters ASSET4 ESG (now part of the London Stock Exchange Group’s [LSEG’s] ASSET4 ESG) database for firm HRM investments indicated by HRM policies, the Securities Data Corporation (SDC) Mergers and Acquisitions database for M&A records, the Standard & Poor’s (S&P) Capital IQ Key Developments database for layoffs, and the Compustat database for key organizational characteristics and financial performance. Due to data availability, we focused on the period from 2002 to 2018.

We took four steps to construct our data. First, we matched firms from the ASSET4 ESG database without missing values for HRM policies with publicly traded firms from the Compustat database. It resulted in 11,812 firm-year observations from 2,045 firms. Second, we identified acquiring firms that engaged in M&A activities. Initially, we used the SDC M&A database to identify instances where publicly traded acquiring firms acquired other publicly traded companies. We further supplemented our sample of acquiring firms with the Compustat database. This allowed us to capture M&A cases involving non–publicly traded acquired firms, which are not covered by the SDC database. In total, 5,620 firm-year cases from 1,245 firms that reported their HRM policies and engaged in M&A activities were identified. 3 Third, we coded firm layoff announcements from the Capital IQ Key Developments database. Finally, we extracted firm characteristics and financial performance from the Compustat database. After excluding observations with missing values, our final sample was comprised of 5,467 firm-year observations from 1,214 firms. As we describe below, we corrected for possible sample bias arising from data missingness/endogeneity in M&A and HRM investments.

Measures

Firm performance

To assess firm performance, we examined total sales conditioned on firm size. Specifically, we used the logged total sales as the dependent variable in models that included the number of merged firm employees (i.e., firm size) as a control variable. This approach allowed us to capture a firm’s overall productivity while addressing empirical concerns associated with ratio variables (Certo, Busenbark, Kalm, & LePine, 2020).

Conceptually, labor productivity reflects the extent to which a firm uses its labor force efficiently. It has been widely adopted as a performance indicator in SHRM research and is considered a proximal and important performance indicator related to the effectiveness of both firm downsizing and HRM (e.g., Datta, Guthrie, & Wright, 2005; Zatzick & Iverson, 2006). Similarly, in the M&A literature—particularly in studies focused on employees and human capital resources (e.g., Siegel & Simons, 2010)—labor productivity frequently has been used as a key performance outcome.

Empirically, labor productivity is conventionally operationalized as the ratio of total sales to the number of employees. Although this measure is intuitive and widely used, it presents methodologic challenges. Specifically, ratio variables such as this can produce biased (often inflated) estimates in regression models (Certo et al., 2020). To mitigate these concerns, we used total sales as our performance measure and included the number of employees as a control variable. This specification captures a conceptually similar construct to traditional labor productivity while avoiding the statistical issues associated with ratio variables.

Although our primary analyses presented results from models using total sales conditioned on employee size as the dependent variable, as a robustness check, we also estimated models using the conventional labor productivity measure (i.e., logged sales per employee) as the dependent variable (see “Supplemental Analyses” below). The results across both approaches are consistent. To account for the potential time lag in the organizational effects of M&A and downsizing, we measured short-term firm performance using total sales in year t + 1 and long-term performance using the average of total sales in years t + 1 and t + 2.

Downsizing

To operationalize the downsizing variable, we examined data from public announcements made by publicly traded firms from the Standard & Poor’s (S&P) Capital IQ Key Developments database. Organizational announcements are recognized as reliable indicators of firm decision making and have been used in management research on downsizing (e.g., O’Shaughnessy & Flanagan, 1998). Specifically, we extracted layoff announcement data from the “Discontinued Operations/Downsizings” subcategory within the broader category of “Potential Red Flags/Distress Indicators.” This dataset has been validated and used in previous research (e.g., Guenzel, Hamilton, & Malmendier, 2023). Each entry includes a headline summarizing the news in brief text, such as “RealNetworks slashes 10% of its staff” and “Siebel Systems to cut nearly 1,200 jobs.” Following the procedure of Guenzel et al. (2023), we coded layoff-related keywords found in headlines that occurred in year t, which corresponds to the year of the M&A. 4 Some examples of keywords (regardless of capitalization and verb tense) include layoff, cut, reduce, axes, fire, slash, and eliminate. If a headline contained one of these keywords, we coded it as 1 to indicate a layoff announcement; otherwise, it was coded as 0. Two authors (PL & ML) of the paper independently reviewed and verified the coding.

In “Supplemental Analyses,” we also assessed downsizing severity (the proportion of employees laid off in the newly merged firm), hand coded from the same dataset. On average, 19.7% of firms downsized following M&A, with an average severity of 6.4% of employees among downsizers. The correlation between downsizing incidence and downsizing severity was 0.56.

Our announcement-based measure offers distinct advantages over the commonly used year-to-year employment change measure with a cutoff to indicate a significant downsizing event (e.g., a 5% cutoff; Ahmadjian & Robinson, 2001; Cascio, Young, & Morris,1997; Freeman & Cameron, 1993). The latter measure is less precise and can be misleading, especially in M&A settings, where headcount changes may result from the merger itself.

HRM investments

We extracted firm-level HRM policy data prior to M&A and downsizing (i.e., year t – 1) from the ASSET4 ESG database to examine the acquiring firm’s HRM investments. The ASSET4 ESG database includes more than 400 metrics that measure the environmental, social, economic, and governance dimensions of more than 7,000 global publicly traded firms (Thomson Reuters, 2017). Although this database has been commonly used to capture firms’ social responsibilities to various stakeholders (de Villiers, Hsiao, Zambon, & Magnaghi, 2022), it also reports companywide HRM policies that have been used in previous research (e.g., Jiang et al., 2021). HRM policies in the ASSET4 ESG data are collected from publicly available sources, including annual reports, sustainability reports, press releases, and news articles. Companies often publish these reports to detail their HRM policies, new initiatives, and changes in employment policies that apply across their organizations. These data are further supplemented by third-party sources, such as nongovernment organization (NGO) reports, government databases, and media outlets, which provide additional insights into companies’ HRM policies and practices and compliance with labor regulations. To ensure accuracy and reliability, trained analysts review and cross-reference the collected data from multiple sources, checking for any inconsistencies.

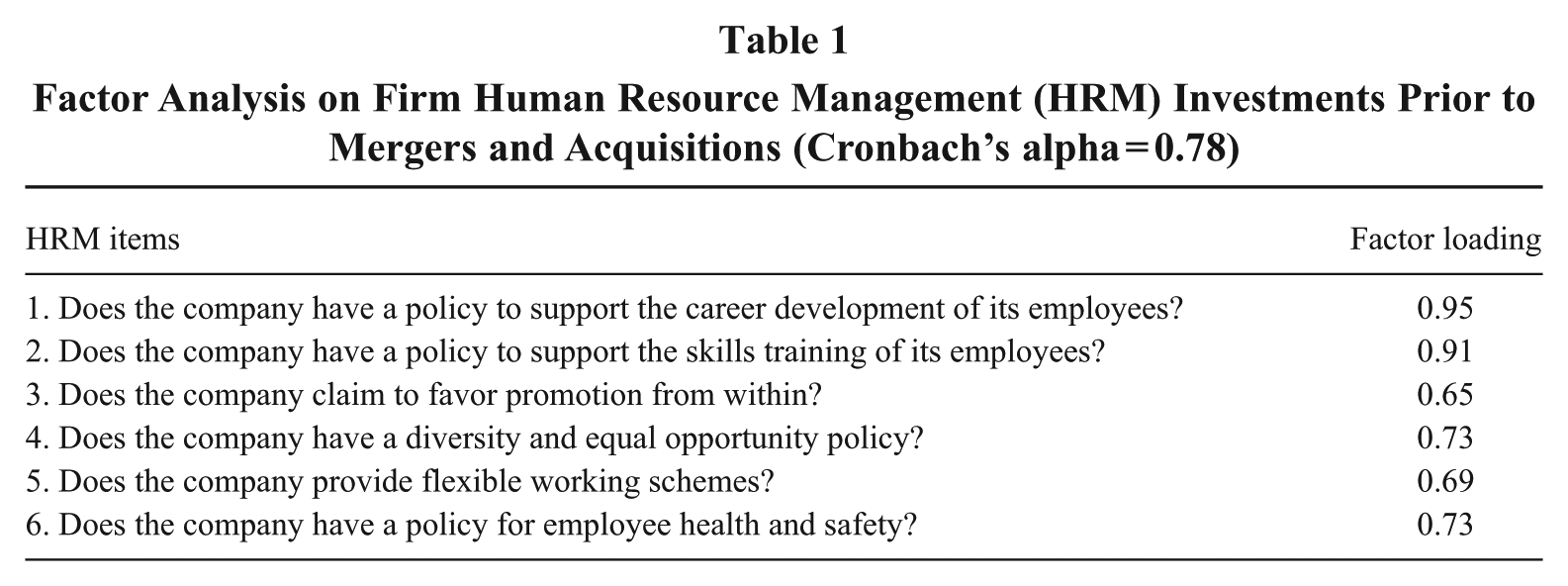

Following prior research (Gong et al., 2009; Jiang et al., 2021; Shaw et al., 2009), we identified six firm-level HRM items from the ASSET4 database that indicate HRM investments in year t – 1. These HRM items were reported at the policy level (i.e., as general orientations of the HRM system rather than specific HRM practices; Jiang, Lepak, Han, Hong, Kim, & Winkler, 2012). If a firm implemented a certain HRM policy, ASSET4 reported it as 1; otherwise, 0. These HRM policies include skill training, career development, internal promotion, diversity and equal opportunity, flexibility work, and health and safety, highlighting the companies’ investments in their employees.

Table 1 reports these specific HRM policies. Using the same database, Jiang et al. (2021) included these policies as a part of firms’ high-investment human resource systems. 5 The internal reliability of these six HRM policies, indicated by Cronbach’s alpha, was 0.78. To validate whether they belong to a single construct, we further conducted a factor analysis with these dummy policy indicators by using tetrachoric from Stata. This command first calculates polychoric correlations from these indicators and then uses the correlation matrix as the input for the factor analysis. As indicated in Table 1, the factor loadings for a single-factor solution ranged from 0.65 to 0.95. Overall, the single-factor model accounted for 91.8% of the observed variance and fit the data better than alternative models (e.g., two- or three-factor models). As such, we used an additive index of all six of these items to represent HRM investments (i.e., 0–6).

Factor Analysis on Firm Human Resource Management (HRM) Investments Prior to Mergers and Acquisitions (Cronbach’s alpha = 0.78)

We further evaluated the criterion-related validity of this measure by using employee review ratings from the crowdsourcing platform Glassdoor.com. We obtained employee-ratings data from Glassdoor in 2008–12. We used three employee rating items—career opportunities, compensation and benefits, and work–life balance—to construct employee satisfaction with the company’s HRM. All three items were reported on a 1–5 Likert scale and showed good internal reliability (Cronbach’s alpha = 0.74). A factor analysis also indicated a single-factor solution for these three items. To enhance interrater reliability, we removed firms with fewer than 10 ratings in a year. For the subset of our primary sample that also had Glassdoor ratings (N = 744), we found a significant positive relationship between this employee-rated firm HRM satisfaction measure and our HRM investments measure (r = 0.25, p < .001), supporting the validity of our measure of HRM investments (detailed results available on request).

Additional HRM investments

To capture the changes in firm HRM investments, we compared newly adopted HRM policies after M&A and downsizing (year t + 1) with those in place prior to M&A and downsizing (year t – 1). Accordingly, we calculated 2-year HRM policy changes between the period of year t – 1 and year t + 1 to capture a firm’s further HRM investments after M&A and downsizing (Zatzick & Iverson, 2006). For example, if a firm adopted one new HRM policy from the six policies after M&A, we coded it as 1; we coded it as 2 if two new policies were adopted, and so on, up to a possible maximum of 6. If a firm did not adopt any new policies, we coded the adoption measure as 0. Online Appendix B presents the relative frequencies of the newly adopted policies in our data.

Control variables

We controlled for a range of firm characteristics and environmental variables that may be correlated with both M&A and downsizing and also may affect subsequent firm performance. Unless otherwise indicated, the control variables are measured in year t – 1.

As noted earlier, to capture overall productivity while avoiding concerns associated with ratio variables, we used total sales as the dependent variable conditioned on firm size. In addition, firm size is a key factor influencing the likelihood of acquisition and downsizing. Accordingly, we included the logarithm of the number of employees as a control variable.

Capital intensity, which reflects the organizational difference in capital use, also can influence firm performance in the context of downsizing (Guthrie & Datta, 2008). Additionally, acquiring firms’ research and development (R&D) capability has been regarded as important for absorbing acquired firms’ knowledge and technology resources in M&A research (King, Slotegraaf, & Kesner, 2008). We therefore controlled these two variables by including the averages of the previous 2 years (t – 1 and t – 2) to mitigate the effects of short-term fluctuation. Firm capital intensity was measured by firm fixed assets divided by total sales, whereas firm R&D intensity was measured by firm R&D expenditures divided by total sales (King et al., 2008). Following convention, for both firm capital intensity and R&D intensity, we derived the relative intensity by dividing the firm-level value by the corresponding industry-level intensity (Datta et al., 2005; King et al., 2008).

We also controlled for changes in the firm’s physical assets to account for possible confounding factors from workforce reduction not accompanied by layoffs (e.g., spinoffs and divestitures). This variable was proxied by the percentage change in the total value of property, plant, and equipment between the current and previous years (Cascio, Chatrath, & Christie-David, 2021; Guthrie & Datta, 2008).

We further controlled for firm profitability and debt in the previous year because they provide information about a firm’s financial leverage (Bergh, 1997). Firm profitability was measured by return on sales (i.e., net income divided by total sales) from the prior year (King et al., 2008). Firm debt was calculated as the ratio of total liabilities to total assets. In addition, we controlled for acquisition size (measured by asset value) and acquisition experience. We measured acquisition size by acquisition costs (reported as aqc from the Compustat database), which serve as a proxy for a firm’s cash spending on other companies, businesses, or subsidiaries; this variable was log transformed. If the firm had engaged in any acquisition activity within the previous 3 years, we coded acquisition experience as 1; otherwise, we coded it as 0.

At the industry level, we controlled for industry growth, which is calculated as the rate of growth in the total sales of the industry divided by the average industry sales in the study period (Dess & Beard, 1984). We also examined industry dynamism as a potential control, which is measured following the two-step procedure from Keats and Hitt (1988). Finally, we included year fixed effects to account for the influence of macroeconomic trends.

Due to multicollinearity concerns, we dropped firm acquisition experience and industry dynamism in our later regression analyses. The hypothesis test results remained consistent both with and without these control variables.

According to Certo et al. (2020), including ratio control variables could bias estimated results. As such, we also examined the results using control variables that were not ratios (see online Appendix C) and without control variables (see online Appendix D). Our substantive results remained consistent across these alternative specifications.

Analytic Techniques

Heckman selection bias correction

Our final sample included only the firm-year observations for companies whose levels of HRM policies were identified and reported by Thomson Reuters (now LSEG) analysts. As such, our sample may not be representative of all publicly traded firms that conducted M&A with varying levels of HRM policies, possibly giving rise to sample selection bias (Certo, Busenbark, Woo, & Semadeni, 2016). 6 We used a two-stage Heckman procedure (Heckman, 1976) to address this issue. We used a probit model in the first stage to predict the likelihood of an observation from the full sample being included in our final sample. In the second stage, we added the inverse Mills ratio calculated from the first-stage analysis to control for potential selection bias related to HRM policies that had been reported.

To effectively mitigate such sample bias, the Heckman procedure needs instrumental variables (exclusion restrictions) that meet two requirements: (a) in the first-stage analysis, they predict the likelihood of an observation appearing in the final sample, and (b) they do not influence the dependent variable of interest in the second-stage analysis (Certo et al., 2016). The ASSET4 database omits firms whose level of environmental, social, and governance (ESG) activities (HRM policies in our case) is not publicly available. Given that firms strategically decide which activities and how much information to disclose to the public, we chose to use two exclusion restriction variables: (a) the firm’s employee relations concerns and (b) the industry average level of HRM investments. First, a firm that has more employee relations concerns is more likely to be reluctant to disclose information about its HRM to the public, which makes it more challenging for Thomson Reuters to collect data on the level of the focal firm’s HRM policies. Second, research has shown a peer effect where firms tend to adopt HRM policies when other firms in the same industry have done so (e.g., Jiang et al., 2021). As such, the average level of HRM investments at the industry level can influence the likelihood of a focal firm adopting these HRM policies and, subsequently, its willingness or reluctance to make information about its HRM investments publicly available.

Thus, in the first-stage model, these two variables (employee relations concerns and industry average of HRM investments) are expected to predict the likelihood of an observation to be included in our sample with nonmissing information on HRM in ASSET4. However, these variables are not likely to directly affect the focal firm’s productivity beyond other covariates in the second-stage model, especially the HRM policies of the firm. We obtained the number of employee relations concerns from the KLD database, an ESG database from WRDS. The industry average HRM investments were calculated by using the four-digit SIC codes to capture a close-peer effect. Online Appendix E reports the first-stage analysis results. In this model, both variables were significantly related to the likelihood of being included in our final sample. Furthermore, our additional analyses indicated that neither of them was significantly related to the error term in the second-stage models. Thus, we added the inverse Mills ratio generated from the first-stage analysis as a control variable in the second-stage analysis to control for potential sample selection bias.

Two-stage least squares estimation with instrumental variables

Although this study examined the impact of downsizing on firm performance, it is possible that even when supporting results are obtained, such statistical associations may not originate from the hypothesized impact of downsizing on performance. Instead, our findings may result from the influence of firm performance on the managerial decision to conduct downsizing (i.e., reverse or concurrent causality) or from a third unobservable variable that affects both downsizing and firm performance. Both concerns are issues of endogeneity.

We used two-stage least squares (2SLS) estimation with instrumental variables for employee downsizing, our key predictor, to address these endogeneity concerns. 7 Effective instrumental variables should be conceptually and empirically relevant to the potentially endogenous variable but not directly correlated with the dependent variable (Wooldridge, 2010). We used two instrumental variables that satisfy these conditions: the political affiliation of a state (blue or red) and layoff contagion based on a firm’s geographic location.

Blue and red states in the United States indicate whether a focal state leans Democrat or Republican. This designation is typically based on which party—Democrat or Republican—receives the majority of votes in that state during the U.S. presidential election every 4 years. This distinction can be an effective instrumental variable for our setting because it is expected to be strongly correlated with the potentially endogenous variable—downsizing—but not directly associated with firm performance after controlling for the covariates in our model. Indeed, the political climate of a state can influence firms’ downsizing decisions in that state (cf. Chadwick, Guthrie, Xing, & Yan, 2024). Democrat-leaning states are more likely to have strong labor protections, high unionization, and relatively good unemployment benefits, which make layoffs harder and more costly. In contrast, Republican-leaning states are more likely to have right-to-work laws, low unionization, and low unemployment benefits, which make layoffs easier and less costly. However, these state-level differences in political orientation are not likely to directly impact firm performance when individual firms’ financial and strategic characteristics are controlled. We assigned a value of 1 if a firm’s headquarters was located in a blue state and 0 otherwise.

Additionally, employee layoff research has provided substantial evidence for layoff contagion within the same geographic area (Bhabra, Bhabra, & Boyle, 2011; Goins & Gruca, 2008). Thus, the average level of layoffs in nearby areas—such as within the same city—is likely to influence a focal firm’s decision to downsize. However, such contagion is highly unlikely to affect the firm’s labor productivity beyond the influence of the firm’s own downsizing event and the aforementioned rich set of control variables. In particular, we aggregated the downsizing announcements made in the year t – 1 from the IQ Key Developments data. To capture layoff contagion, we aggregated downsizing announcements made within the city where the firm’s headquarters is located.

We used the command xtivreg in Stata to perform the 2SLS regression estimation. Online Appendix F shows the results from the first-stage model of 2SLS with these two instrumental variables, both of which are significantly related to the focal firm downsizing announcement. Based on common practice, we further assessed the empirical suitability of the instrumental variables by examining whether they satisfied two conditions—relevance and exogeneity (Wooldridge, 2010). First, for relevance of the instrumental variables, we used the postestimation of the Kleibergen–Paap rk LM statistic to assess whether the instrumental variables have robust associations with the potentially endogenous variable (downsizing). The significant chi-squared value rejected the null hypothesis that the instrumental variables and the endogenous variable are not correlated. As shown in Table 3 for 2SLS regression results, all Kleibergen–Paap rk LM statistics were significant, supporting the relevance of our instrumental variables. Second, we used the postestimation Hansen–Sargan statistic (also known as Hansen J statistic) to assess the exogeneity of our instrumental variables. Its null hypothesis is that the instrumental variables are uncorrelated with the error term at the second stage (Hansen, 1982). As indicated in Table 3, the Hansen–Sargan statistics for all regressions were not significant, suggesting that the null hypothesis cannot be rejected. Thus, the exogeneity of our instrumental variables is supported. Overall, these assessments support the validity of our instrumental variables.

Fixed-effects panel regression models

Because our sample includes repeated observations of the same firms over multiple years, panel data analysis was appropriate for this firm-year structure. The Breusch–Pagan test (Breusch & Pagan, 1979) rejected the null hypothesis of no heteroskedasticity (F value = 97.15, p < .001), indicating the presence of firm-level effects and supporting the use of panel analysis. The Hausman test result was significant (χ² = 150.65, p < .001), favoring a fixed-effect model. A fixed-effect model also offers the advantage of controlling for unobserved time-invariant firm-specific factors. Accordingly, we employed fixed-effects panel regression for our primary analysis. In a supplemental analysis described below, we also estimated a random-effect model and found consistent results. All models used robust standard errors to account for potential heteroskedasticity across firms.

Results

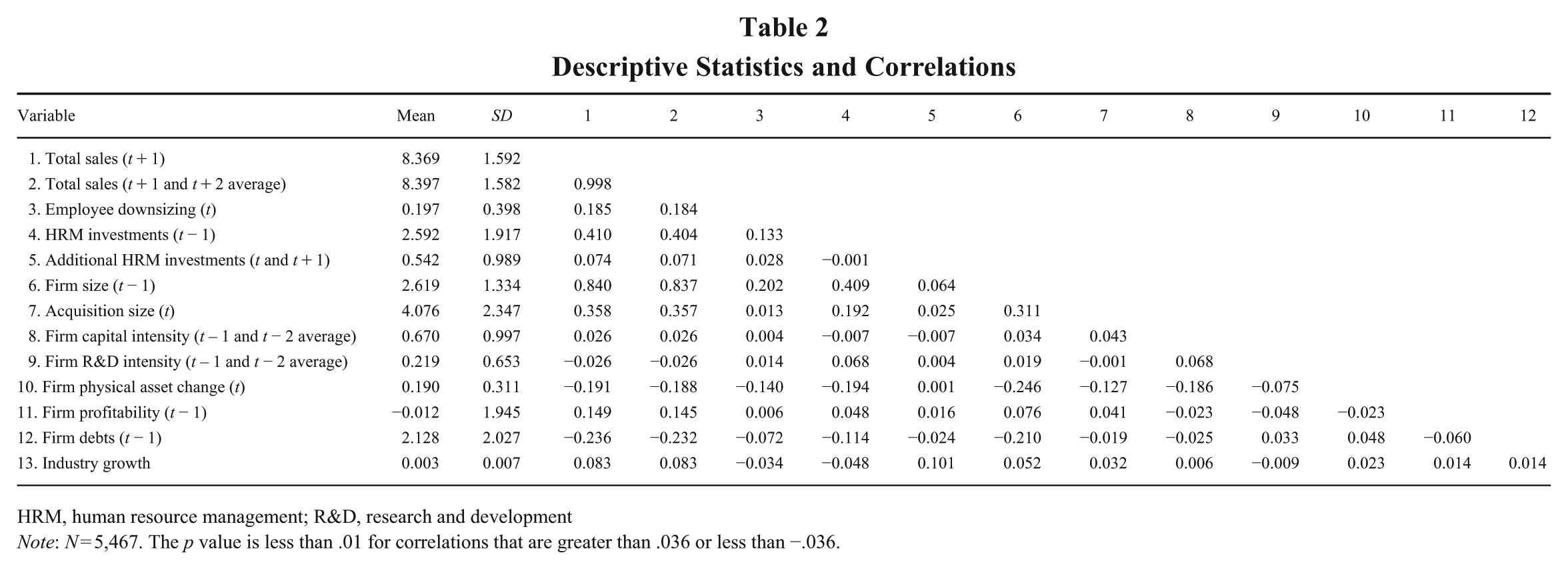

Table 2 indicates means, standard deviations, and correlations for all variables. As with other organizational datasets, firm performance in total sales was positively correlated with firm size and profitability and negatively correlated with changes in physical assets. Consistent with other SHRM research, HRM investments were positively correlated with firm size and profitability and negatively correlated with changes in physical assets.

Descriptive Statistics and Correlations

HRM, human resource management; R&D, research and development

Note: N = 5,467. The p value is less than .01 for correlations that are greater than .036 or less than −.036.

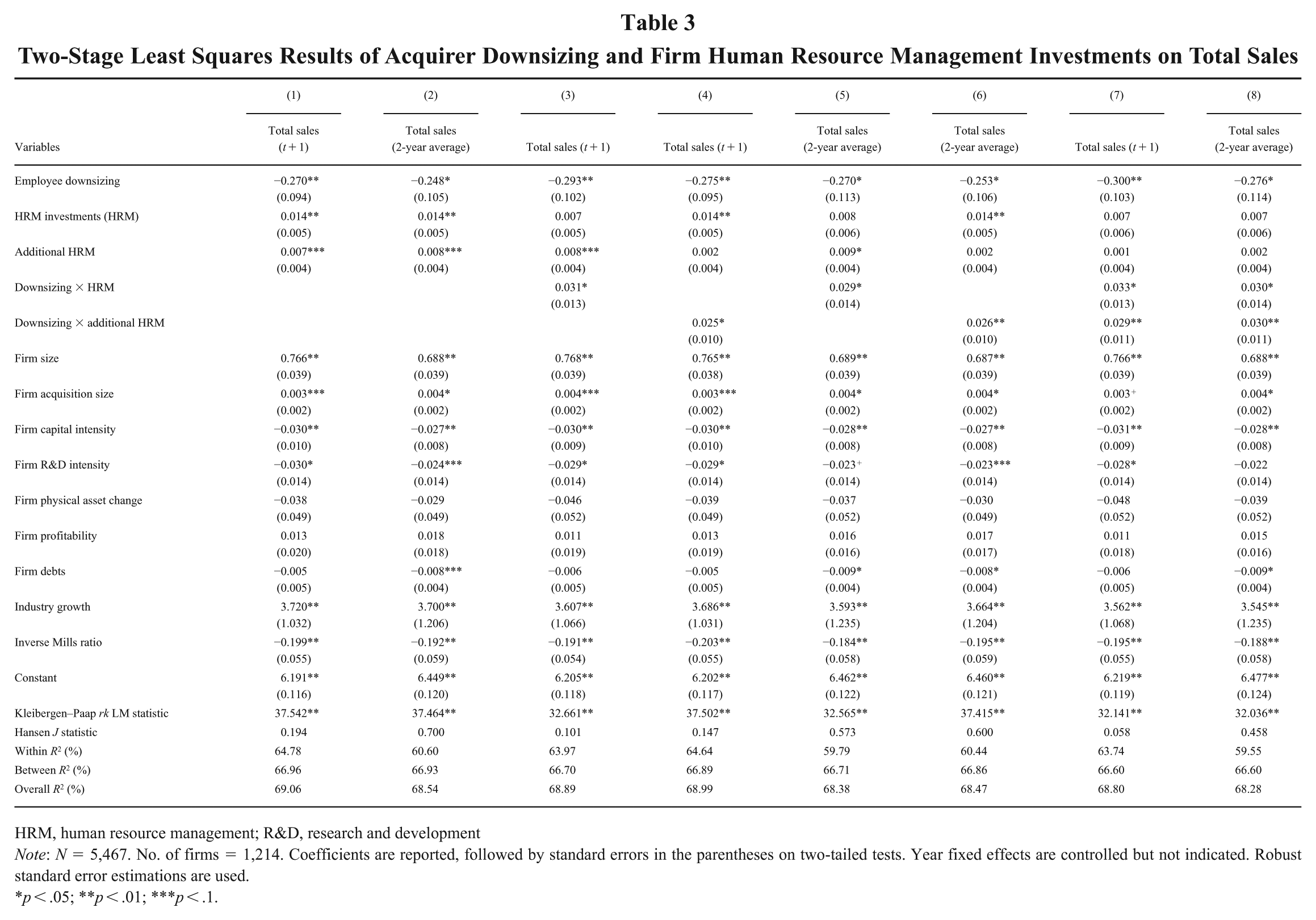

Table 3 reports the results from the 2SLS estimations with total sales as the dependent variable. We first evaluated multicollinearity by using the average variance inflation factor for all variables and dropped the control variables that caused unacceptable multicollinearity as noted above. Models 1 and 2 in Table 3 present the direct effects of downsizing, firm HRM investments, and additional HRM investments on short- and long-term total sales, respectively. As predicted, employee downsizing was negatively related to total sales in both the short term (year t + 1; b = −0.270, SE = 0.094, p = .004) and long term (average of the 2 years t + 1 and t + 2; b = −0.248, SE = 0.105, p = .018), supporting Hypothesis 1. Moreover, HRM investments showed a significant and positive relationship with both short-term (year t + 1; b = 0.014, SE = 0.005, p = .004) and long-term total sales (average of the 2 years t + 1 and t + 2; b = 0.014, SE = 0.005, p = .004), which is consistent with existing SHRM research findings.

Two-Stage Least Squares Results of Acquirer Downsizing and Firm Human Resource Management Investments on Total Sales

HRM, human resource management; R&D, research and development

Note: N = 5,467. No. of firms = 1,214. Coefficients are reported, followed by standard errors in the parentheses on two-tailed tests. Year fixed effects are controlled but not indicated. Robust standard error estimations are used.

p < .05; **p < .01; ***p < .1.

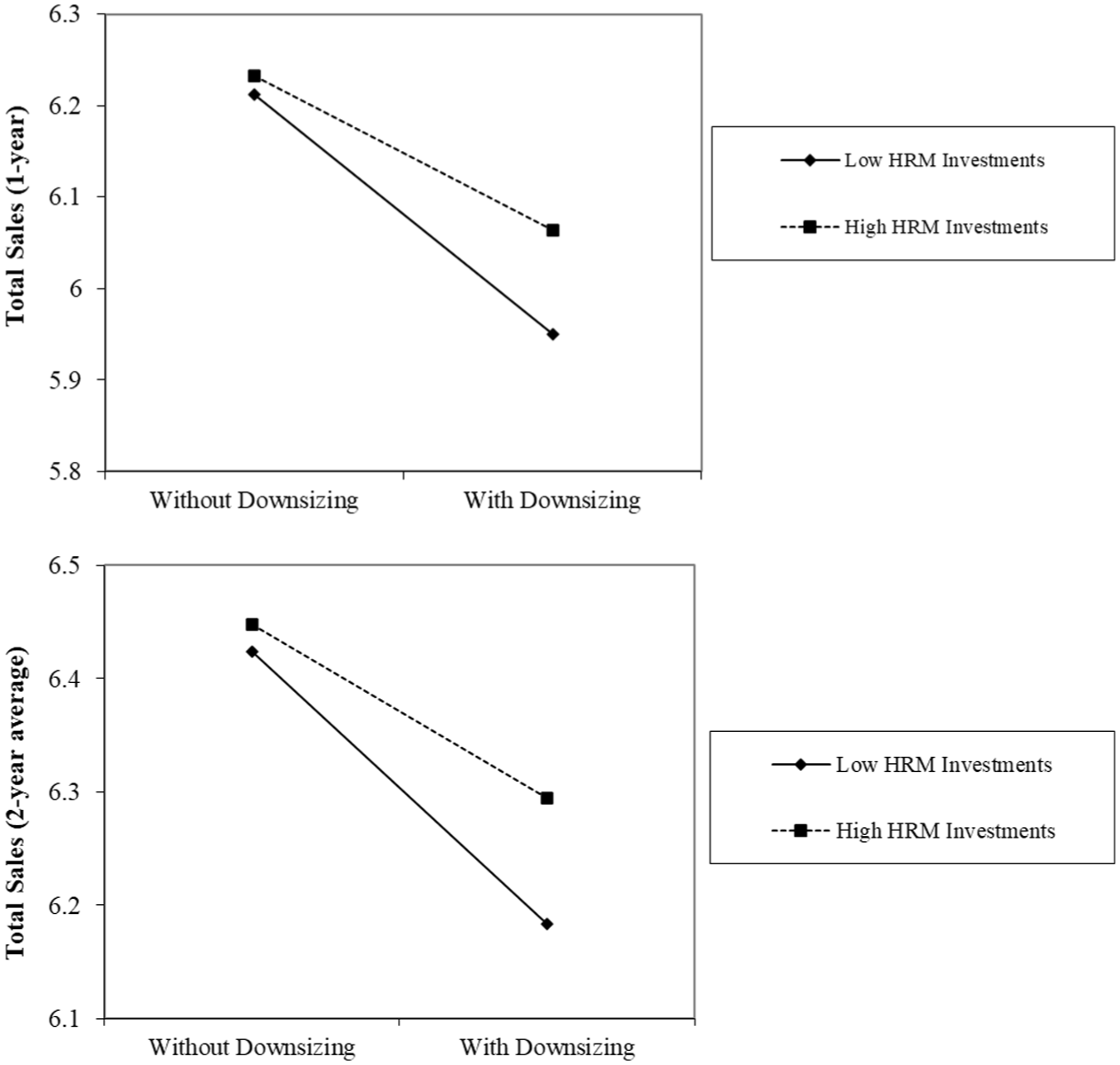

Model 3 reports a significant moderating effect of HRM investments on the relationship between downsizing and total sales in year t + 1 (b = 0.031, SE = 0.013, p = .016). Figure 1 illustrates this moderating effect. The downsizing–firm performance slope was negative for both groups, but the decline was less pronounced for M&A firms with high HRM investment (four of six HRM policies) than for those with low HRM investment (one of six policies). This result is consistent with Hypothesis 2, suggesting that acquiring firms with high HRM investments experience a smaller reduction in performance from post-M&A downsizing than firms with low HRM investments. Practically speaking, downsizing is associated with a 26.2% decrease in total sales (an average of $1,129,567) for firms with low HRM investment (one of six HRM policies) compared with a smaller 16.9% decrease (an average of $728,614) for firms with high HRM investment (four of six policies). The difference between these two groups is $400,953.

The Interaction Effect of Firm Pre–Merger and Acquisition Human Resource Management Investments and Downsizing on Total Sales

Model 5 presents the moderating effect of firm HRM investments on the relationship between downsizing and long-term total sales (b = 0.029, SE = 0.014, p = .036), which is similar to the findings in Model 3 and again supports Hypothesis 2. The simple slopes plot of this moderating effect is shown in Figure 1. Specifically, among M&A firms with low HRM investment (one of six HRM policies), total sales are significantly higher for firms that did not downsize compared with those that did. In contrast, among firms with high HRM investment (four of six HRM policies), the sales loss associated with downsizing is less pronounced. Practically speaking, downsizing is associated with a 24.1% decrease in total sales (an average of $1,063,203) for low HRM investment firms compared with a 15.4% decrease (an average of $679,391) for high HRM investment firms. The difference between these two groups is $383,812.

Model 4 tests the moderating effect of additional HRM investments on the short-term impact of downsizing on total sales (b = 0.025, SE = 0.010, p = .011). This moderating effect is shown in Figure 2. The figure shows that for M&A firms with low additional HRM investments (one of six HRM policies), the negative slope is steeper than for firms with high additional HRM investments (three of six HRM policies). Practically speaking, for firms with low additional HRM investments, downsizing is associated with a 25.0% decrease in total sales, averaging $1,077,831. In comparison, firms with high additional HRM investments experience a smaller 17.5% decrease, averaging $754,482. The difference between these two groups is $323,349.

The Interaction Effect of Firm Post–Merger and Acquisition Additional Human Resource Management Investments and Downsizing on Total Sales

Similarly, Model 6 presents the moderating effect of additional HRM investments on the long-term relationship between downsizing on total sales (b = 0.026, SE = 0.010, p = .009). Simple slopes shown in Figure 2 also suggest that for M&A firms with low additional HRM investments (one of six HRM policies), the sales loss is more pronounced than for M&A firms with high additional HRM investments (three of six HRM policies). Practically speaking, for firms with low additional HRM investments, downsizing leads to a 22.7% decrease in total sales, averaging $1,001,440; for high additional HRM investments, total sales decrease by 14.9%, averaging $657,333. The difference between these two groups is $344,107.

Models 7 and 8 present results with all interaction terms included simultaneously. These findings are consistent with those from the previously discussed models. Overall, the results support Hypotheses 1, 2, and 3.

Downsizing and HRM Investments in Non-Acquiring Firms

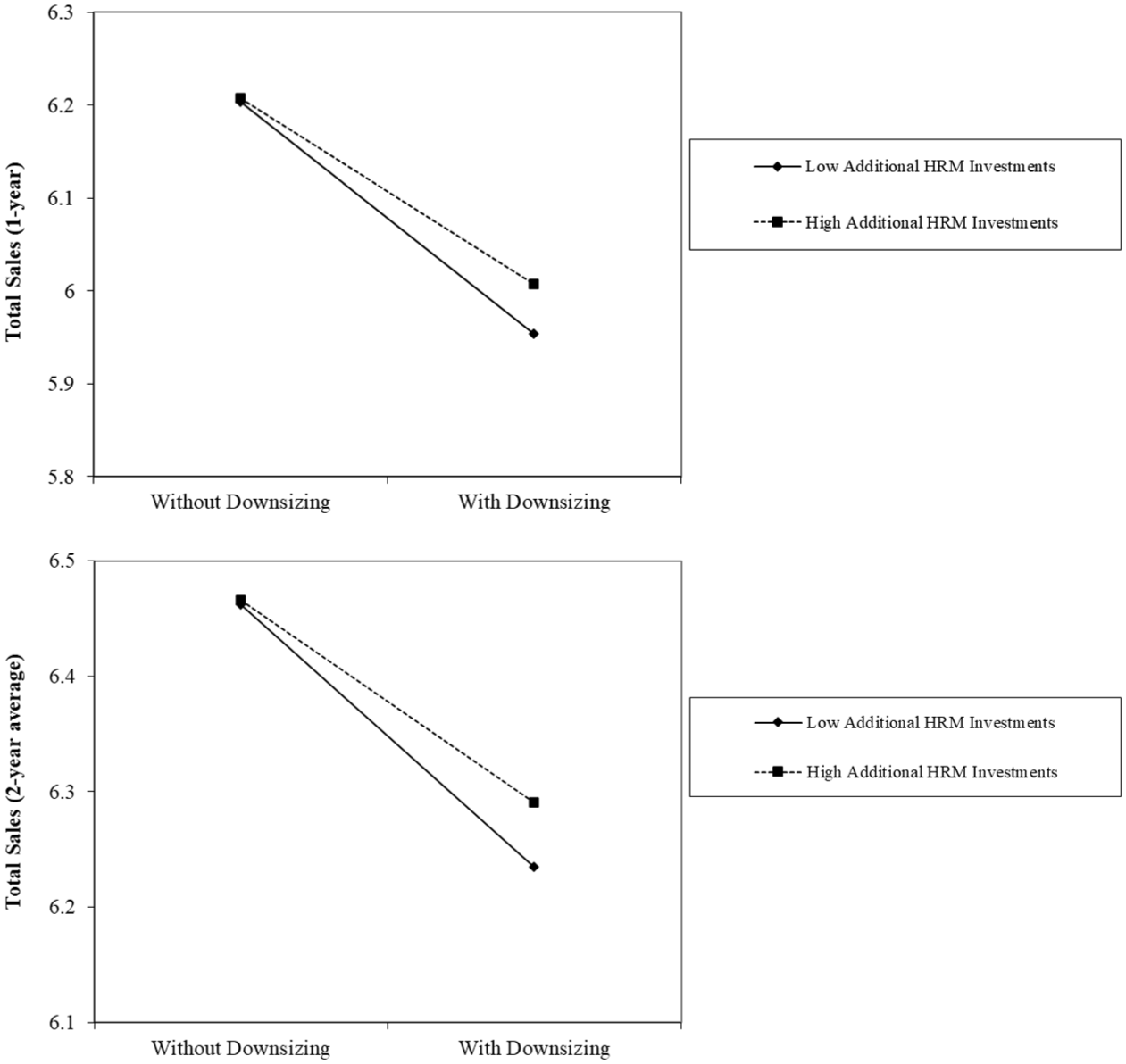

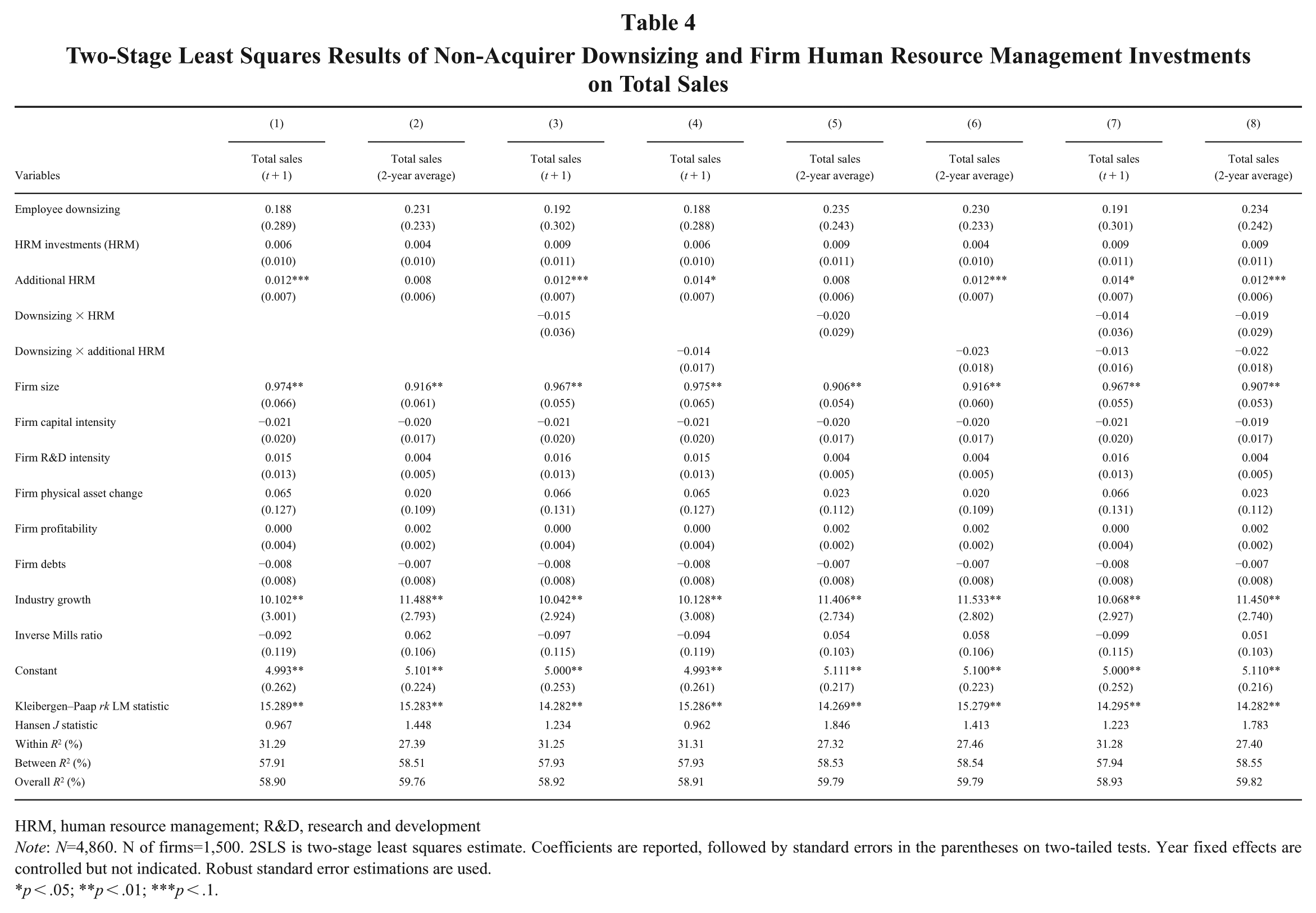

We propose that M&A serves as a sense-breaking event that creates a particularly conducive context for the aforementioned positive moderating effect of HRM investments to emerge. However, it is possible that the positive moderating effect of HRM investments in our analysis is not unique to acquiring firms in the M&A context; that is, non-acquiring firms’ HRM investments also may help reduce the negative effect of downsizing. To assess this possibility in our data, we tested the same downsizing models using an alternative sample of firms that were not involved in an M&A (4,860 firm-year observations from 1,500 firms).

The results for this analysis are presented in Table 4. Importantly, we did not find a significant interaction between downsizing and HRM investments among these non-M&A firms, nor between downsizing and additional HRM investments. 8 Further, we compared the coefficients for the interaction effects between the two samples of acquiring firms and non-acquiring firms. We found that the coefficients for the interaction effect of downsizing and HRM investments were significantly larger for acquiring firms for both short- and long-term total sales (χ² = 6.18, p = .013). Similarly, the coefficients for the interaction effect of downsizing and additional HRM adoption were significantly larger for acquiring firms for both short- and long-term total sales (χ² = 9.46, p = .002). 9

Two-Stage Least Squares Results of Non-Acquirer Downsizing and Firm Human Resource Management Investments on Total Sales

HRM, human resource management; R&D, research and development

Note: N=4,860. N of firms=1,500. 2SLS is two-stage least squares estimate. Coefficients are reported, followed by standard errors in the parentheses on two-tailed tests. Year fixed effects are controlled but not indicated. Robust standard error estimations are used.

p < .05; **p < .01; ***p < .1.

Supplemental Analyses

We conducted a series of supplemental analyses to check the robustness of our results. All these supplemental analysis results can be accessed in the online Appendices. 10

Impact of downsizing severity

Our measure of downsizing announcements captures the discrete or shock effect of the downsizing occurrence. However, a measure of the magnitude of the downsizing event also can be meaningful (Brauer & Zimmermann, 2019; Datta et al., 2010). As such, we also collected information on the number or ratio of employees cut, as reported in the downsizing announcements. We measured downsizing magnitude by scaling it using the acquiring firm’s total number of employees prior to downsizing. We then followed the operationalization from Trevor and Nyberg (2008) and logged the highly positively skewed downsizing rates (adding a constant of 0.0001 due to an undefined natural logarithm of zero). We replaced this for the downsizing announcement’s measure used above and ran the same 2SLS analyses. As shown in online Appendix H, all results remained similar to those that we reported for the downsizing announcement measure.

Furthermore, we examined the separate effects of downsizing occurrence (our primary measure of downsizing using layoff announcements) and downsizing severity (measured as the ratio of downsized employees to total employees) within the same model. This approach allowed us to distinguish between the impact of initiating downsizing (i.e., the transition from nondownsizing to downsizing) and the effect of a higher degree of severity, conditional on downsizing having occurred. As shown in online Appendix I, both the negative main effect of downsizing occurrence and the positive interactions between downsizing occurrence and both prior and additional HRM investments remain significant—even after controlling for downsizing severity—consistent with our predictions.

Acquired firms’ characteristics

Acquired firms’ characteristics potentially could influence the relationships hypothesized in this study. This is why we controlled for the acquisition size (in asset value), as described above, which captures the overall economic and strategic value of the acquired firms. Firm size in assets and firm size in employees tend to be highly correlated. However, to address this issue more directly, we collected additional data on acquired firms—firm size and financial performance. We did not add these variables to the main analysis because the information was available for only a subset of our sample (firm size N = 1,050; financial performance measured by return on sales [ROS]: N = 503). We then conducted multiple imputations for acquired firm size and financial performance. After missing-data imputation, we added them as control variables to our models. As indicated in online Appendix J, the results remained substantively consistent with those in our main analysis.

Random-effects panel regression

Online Appendix K presents the results from the random-effects estimator. The results were consistent with the fixed-effect estimation results.

Conventional labor productivity as the dependent variable

Despite the potential estimation bias discussed earlier, we also ran the same set of analyses as our primary models, substituting conventional labor productivity—measured as the logarithm of the ratio of total sales to the number of employees—as the dependent variable. The results, presented in online Appendix L, were largely consistent with those of the main models, except that the direct effect of downsizing on long-term labor productivity became nonsignificant.

Alternative HRM investment measure

Although our count-based HRM investment measure demonstrated strong construct validity, as discussed earlier, its limited range (0–6 practices) may not have fully captured broader HRM investments. To address this concern, we used LSEG’s workforce summary score as an alternative measure. This score includes the practices in our primary measure and reflects a firm’s overall commitment to HR issues, albeit without detailing specific HRM practice bundles. Importantly, it is continuous (0–100; rescaled to 10), offering greater sensitivity to variation. As shown in online Appendix M, the results using this alternative measure align with our primary findings.

Discussion

Firms often use employee downsizing as a managerial tool to realize organizational efficiency and effectiveness after M&A (Malikov et al., 2021; O’Shaughnessy & Flanagan, 1998). As an important firm activity, M&A has received extensive research attention from organizational scholarship (King, Wang, Samimi, & Cortes, 2021). However, although integration of people is often deemed the most critical and challenging factor in post-M&A integration, the existing research lacks substantial evidence on the effects of addressing the “people issue” (Cooke et al., 2021; Friedman, Carmelim Tishler, & Shimizu, 2016; Khan, Soundararajan, & Shohham, 2020; King, Bauer, Weng, Schriber, & Tarba, 2020). Notably, although downsizing literature generally suggests a negative relationship between layoffs and firm performance (Datta et al., 2010), empirical evidence for this relationship is scarce in the M&A context. As such, we addressed this gap by focusing on employee downsizing after M&A and investigating the role of the acquiring firm’s HRM investments in this context.

Consistent with the suggestions in the existing literature, our study confirms that a negative main effect of downsizing and a positive main effect of HRM investments also occur in the M&A context. More importantly, we found that the negative effect of employee downsizing following M&A on firm performance can be partially mitigated by the acquiring firm’s preexisting (i.e., before M&A) HRM investments and by additional HRM investments after M&A. These mitigating effects of HRM investments are not observed in the non-M&A context.

Theoretical Implications

Theoretically, our research emphasizes the importance of organizational context in shaping the joint impacts of HRM and employee downsizing on firm performance. Previous SHRM research (Zatzick & Iverson, 2006) has suggested that firms’ HRM investments exacerbate the negative effect of employee downsizing by sending out contradictory meta-messages from management to employees, thereby conflicting with the consistency principle of HRM strength theory (Bowen & Ostroff, 2004) and violating the psychological contract that employees have built with the employer. However, we argue that in the M&A context, HRM investments from the acquiring firm play a critical role in employee sensemaking, reducing the negative effect of downsizing.

Specifically, we propose that employees will engage in a sensebreaking process after a traumatic post-M&A downsizing event (Monin et al., 2013), during which their previous understanding of the organization is disrupted. In response, they will seek cues in the new organizational environment to reconstruct their perceptions (Weick, 1995; Weick et al., 2005). We posit that when employees perceive management’s interest in long-term commitment to their welfare and benefits through the HRM investments, they interpret this as a meaningful cue that reduces the extent to which they view post-M&A downsizing negatively. This sensemaking effect is expected to be most pronounced among employees of the acquired firm, who experience a complete shift in organizational context and leadership following an M&A. For them, information about the acquiring firm’s orientation toward employees is both novel and highly salient, thereby aiding their sensemaking process. As such, the proportion of downsized employees from the acquired firms may influence the implications of our story. A smaller proportion of downsized employees in the acquired firm likely would weaken the positive moderating effect of the acquiring firm’s HRM investments on the relationship between post-M&A downsizing and firm performance. In other words, although the acquiring firm’s HRM investments still can mitigate the adverse effects of downsizing, the effect is less likely to be pronounced when the majority of downsized employees come from the acquiring firm.

Moreover, we theorize that sensemaking would influence firm productivity following post-M&A downsizing through two different facets of the organization: (a) employee morale, which influences key antecedents to productivity, including motivation, discretionary effort, and organizational citizenship behaviors, and (b) human capital and social capital, which serve as essential firm-level strategic resources that shape organizational capabilities and routines. A question that future researchers could explore is how much of HRM investments’ effect is driven by each of these different facets of organizations.

More broadly, our theory and findings emphasize a need for further investigation into the specific sensemaking mechanisms in the post-M&A setting. For example, the sensemaking literature (Weick, 1995; Weick et al., 2005) suggests that employees’ interpretation of their environment is strongly influenced by the opinions and perceptions of those around them. Therefore, examining the roles and attitudes of coworkers and middle managers may offer deeper insights into how employees’ sensemaking unfolds during and after post-M&A downsizing.

Our findings suggest that introducing even a limited set of new HRM policies in the wake of post-M&A downsizing can positively influence firm performance. This may appear to be a more cost-effective alternative to making a comprehensive set of HRM investments before M&A. However, our findings indicate that the positive effects of adopting new HRM policies after M&A are smaller than those of pre-M&A HRM investments (based on our estimate, practically, one more established pre-M&A HRM can offset about $51,736 more in sales losses than adopting one more new HRM policy after M&A). One possible explanation is that surviving employees may be more skeptical of HRM policies introduced during or immediately after a disruptive event such as M&A, perceiving them as reactive or insincere. Surviving employees who feel vulnerable in the face of downsizing may view such efforts as symbolic rather than substantive. In a similar vein, we still lack understanding of how sensemaking unfolds in firms that undergo repeated M&A and associated downsizing. In such cases, employees may develop greater skepticism toward HRM practices, undermining the intended message that they are valued.

Practical Implications

Although prior research consistently suggests that firms may not benefit from workforce downsizing due to the loss of valuable human capital and diminished morale and motivation among remaining employees (Datta et al., 2010; Guthrie & Datta, 2008), downsizing remains a common practice in the business world. In some circumstances, acquiring firms need to lay off employees for justifiable reasons. For instance, many firms undertake employee downsizing following M&A as part of their organizational restructuring or to eliminate redundant functions across the two entities. Our research offers guidance to firms that cannot avoid downsizing entirely, suggesting ways to mitigate its negative effects after M&A from an HRM perspective.

First, the HRM investments we highlight in this paper provide guidance to HR professionals and leaders, especially for firms that frequently engage in M&A and downsizing together. HRM policies to support employee career development, skill training, internal promotion, diversity and equal opportunity, flexible work schemes, and employee health and safety send out messages to acquired firm employees that the acquiring organization cares about their well-being and benefits. This, in turn, helps maintain employee morale and enhances integration within the newly merged organization, which are essential for achieving the intended goals of the M&A.

Second, for firms anticipating an M&A and subsequent downsizing but lacking such HRM investments beforehand, our findings suggest that beginning to invest in these HRM policies, even after M&A, also can yield positive outcomes. The post-M&A environment is characterized by ambiguity and uncertainty, prompting surviving employees to seek cues to make sense of the situation. Implementing new HRM policies can deliver a strong message to employees (Bowen & Ostroff, 2004) indicating that the organization values their contributions and is committed to their well-being, thereby positively shaping their sensemaking process. This, in turn, can help the merged firm build trust, reduce uncertainty, and ultimately achieve more successful M&A outcomes.

However, it can be challenging for firms that have not previously invested in HRM to suddenly start formulating and implementing HRM policies with or soon after an M&A event. Therefore, although ideally firms would commit to such HRM investments, if this is not feasible, they could alternatively attempt to facilitate positive sensemaking through other means. For example, the sensemaking literature highlights the crucial role of leaders (Maitlis, 2005; Monin et al., 2013). That is, employees’ sensemaking about downsizing can be significantly influenced by leaders through actions such as clear and sincere communication from top management, meetings that explain the downsizing process, or Q&A sessions that address individual concerns. Also, certain downsizing implementation practices—such as outplacement assistance (Chadwick et al., 2004)—may serve a similar signaling function, shaping employee perceptions in the firm’s favor. The crucial point is to convey an employee-focused message to reassure employees that they are valued and cared for, that downsizing is part of a strategic reorientation associated with the M&A, and that it will be conducted fairly.

Limitations and Future Research

We acknowledge that this study has several limitations. First, our research design and analysis were constrained by the information available in archival data. Although downsizing more often occurs after M&A than before, and acquired employees are frequently the primary targets of downsizing, we cannot definitively determine whether the downsizing in the M&A year occurred before or after the acquisition, nor do we have information on which employees were affected. Future research would benefit from more precise data on the timing of M&A and downsizing events and the specific targets of downsizing to better assess the proposed sensemaking mechanism we propose here.

Furthermore, data limitations prevented us from exploring the (mis)alignment of HRM investments between acquiring and acquired firms, which is a promising avenue for future research (Datta, 1991). In particular, the relative levels of HRM investments in both firms prior to M&A may reflect the level of cultural fit and human capital compatibility, significantly influencing employee sensemaking and post-M&A integration (Chatterjee, Lubatkin, Schweiger, & Weber, 1992; Friedman et al., 2016). From this perspective, the positive moderating effect of HRM investments observed in our data may reflect a relative improvement in the HRM experience within the merged firm—compared with that of the pre-M&A firm (i.e., a better-than-before HRM experience)—rather than a sensemaking effect, particularly when the acquired firm had significantly lower HRM investments than the acquiring firm.

Another possible concern stemming from the limited availability of archival data is from the nature of our downsizing measure. Because we relied on corporate announcements reported in news headlines, it is possible that our downsizing variable underrepresents the actual mass layoff events given that firms might be reluctant to fully disclose their downsizing activities. Therefore, we recommend that future research use multiple methods to capture the size and frequency of downsizing.

More broadly, limited information available in archival data can create omitted-variable bias. For instance, voluntary turnover, which is expected to be significantly associated with both our predictor (downsizing) and outcome variable (productivity), could not be controlled for due to data unavailability. Although we employed Oster’s (2019) approach to estimate the impacts of potential unobserved variables (including voluntary turnover) and found that omitted-variable bias is unlikely to overturn our findings, this remains a limitation inherent in studies using archival data. However, our fixed-effect specification helps mitigate this concern by accounting for unobserved factors that remain stable over the observation period.

Second, although we extend existing theory by discussing how sensemaking processes in the M&A context drive the observed effects, we could examine these mechanisms only indirectly, without directly measuring and analyzing them. To address this limitation, future research could employ other approaches such as event studies or longitudinal qualitative research to provide additional evidence on the distinct reactions of employees to downsizing in comparing M&A and non-M&A firms.

Third, although our primary focus was on the discrete effect of the downsizing shock (i.e., downsizing occurrence), we also explored the separate effects of downsizing occurrence and severity in our supplementary analyses (online Appendices H and I). Their dynamic interplay, however, warrants more systematic investigation in future research, as suggested by Trevor and Nyberg (2008). For instance, when we only included downsizing severity in the model without considering downsizing occurrence (online Appendix H), downsizing severity was negatively associated with firm performance. Yet, when we included downsizing occurrence as a control (online Appendix I), downsizing severity changed to have a marginally significant positive effect (p < .10), suggesting that firms may benefit from increased severity once the initial shock is accounted for. These findings suggest that downsizing may have mixed strategic implications. However, this issue lies beyond the theoretical scope and empirical design of this study. We therefore encourage future researchers to more rigorously examine the distinct and combined effects of downsizing occurrence and severity.

Fourth, although we focused on M&A and downsizing occurring in publicly traded firms and thus in relatively large firms, it is possible that smaller private firms may face different HR challenges in the M&A process. Thus, the impact of downsizing following M&A could be different. Indeed, prior research has indicated that the relative size of acquiring and targeted firms is a crucial factor in determining M&A success (King et al., 2021), suggesting that, for example, smaller acquiring firms may encounter distinct challenges compared with larger firms in an M&A context. This implies that our proposed mechanisms may work differently, depending on the size of either the acquiring firm or the acquired firm. Future researchers could investigate this possibility.

Fifth, other psychological mechanisms beyond sensemaking also may be relevant to the role of HRM investments in the post-M&A downsizing context and could be further explored. For example, HRM attribution theory (e.g., Nishii et al., 2008) could be leveraged to examine employees’ interpretations of HRM investments, offering additional insights into their positive influence on employees in the face of downsizing or other organizational changes.

Sixth, a more fine-grained measure of HRM investments could help capture greater variance in the relationships examined. Although the index of HRM investments used in this study demonstrated sound validity (Jiang et al., 2021), future research would benefit from more nuanced measures of HRM systems. For instance, rather than simply noting the presence of a training and development policy, data on hours of training or the proportion of employees covered by the training program would be more informative. Although we believe that this study’s abstraction at the HRM index level is not likely to bias our substantive findings, practice-level measures could offer opportunities for more nuanced insights because different HRM practices may influence employees’ perceptions in distinct ways during the sensemaking process.

Finally, we believe that the mechanisms we proposed warrant further investigation in different cultural or international contexts. Because sensemaking is inherently a sociocultural process, we recommend examining the generalizability of our findings across these varied settings.

Conclusion

The findings from this study demonstrate that HRM investments in acquiring firms play a crucial role in mitigating the negative effects of downsizing on firm performance following M&A. In particular, HRM investments emphasizing employee well-being and benefits serve as key environmental cues in helping employees positively interpret management actions after M&A. Our findings suggest that acquiring firms should invest in HRM before conducting M&A and/or make additional HRM investments after M&A to reduce the negative repercussions of employee downsizing following M&A events.

Supplemental Material

sj-docx-1-jom-10.1177_01492063251382856 – Supplemental material for It’s Different: Examining the Effect of HRM Investments on Employee Downsizing Following Mergers and Acquisitions