Abstract

Executive compensation is a key topic in management research, focusing on how firms use incentives to align CEOs’ decisions with shareholders’ interests. Yet, we know little about the influence of stock-option compensation—a major component of CEO pay—on CEO decisions facing adverse events involving multiple stakeholders. Analyzing U.S. medical device recalls between 2004 and 2017, we examine how stock options induce CEOs to protect their existing wealth while pursuing potential gains. We find that CEOs with greater current option wealth are more likely to adopt short-term impression management (IM) tactics, such as strategically timing recalls and maintaining silence in press releases, which can harm shareholders and stakeholders. In contrast, CEOs with higher prospective option wealth are less inclined to employ these tactics. Moreover, negative media scrutiny discourages CEOs with substantial current option wealth from using IM tactics, and encourages those with greater prospective option wealth to further avoid them. These findings highlight the powerful role of executive compensation, particularly stock options, in shaping CEO decisions facing adverse events.

Introduction

CEO compensation plays a crucial role in shaping firm outcomes by influencing CEOs’ strategic decisions and behaviors (Devers, McNamara, Wiseman, & Arrfelt, 2008; Wiseman & Gomez-Mejia, 1998; Wowak & Hambrick, 2010). One major factor influencing CEOs’ strategic choices is stock-based compensation, especially stock options—contracts granting the right to purchase shares at a predetermined price. Stock options have been a standard feature of CEO compensation (Eisenhardt, 1989; Jensen & Meckling, 1976; Nyberg, Fulmer, Gerhart, & Carpenter, 2010; Wang, 2024), accounting for nearly 75% of total CEO pay on average (Aguinis, Martin, Gomez-Mejia, O’Boyle, & Joo, 2018).

Extant research has shown that stock options can steer CEOs toward decisions that align with shareholder interests, such as risk-taking, diversification, and investment in research and development (R&D; e.g., Benischke, Martin, & Glaser, 2019; DesJardine & Shi, 2021; Devers et al., 2008; Larraza-Kintana, Wiseman, Gomez-Mejia, & Welbourne, 2007; Martin, Gomez-Mejia, & Wiseman, 2013; Martin, Wiseman, & Gomez-Mejia, 2016). However, little is known about how stock options shape CEO decision-making during adverse events—especially those that affect a broad set of stakeholders.

This oversight is important for two primary reasons. First, while CEOs are responsible for steering business strategy, their actions during crises—such as product failures or organizational breakdowns—can have long-lasting consequences for shareholders, customers, employees, or other related stakeholders. Second, although stock options are typically designed to align CEO interests with those of shareholders under normal conditions, that alignment may weaken during crises. In these situations, the value of options becomes highly volatile, exposing CEOs to significant short-term financial risk—even as their long-term wealth remains tied to shareholder value. Under such pressure, CEOs may seek to protect their current wealth (Kahneman & Tversky, 1979), potentially at the expense of long-term shareholder value.

This study investigates how CEO stock-option incentives shape impression management (IM) tactics during product recalls—adverse events that impact multiple stakeholders, including patients, medical personnel, and shareholders (Thirumalai & Sinha, 2011; Wowak, Mannor, & Wowak, 2015). IM tactics are typically short-term in focus and often contribute to information asymmetry between executives and external audiences, potentially harming stakeholder trust (Diestre, Barber, & Santaló, 2020). Typical IM tactics employed by CEOs include generating strategic noise (Graffin, Carpenter, & Boivie, 2011; Jin, Li, & Hoskisson, 2022), inserting distractive content into financial reports (Godfrey, Mather, & Ramsay, 2003), soliciting favorable comments from peer CEOs (Westphal, Park, McDonald, & Hayward, 2012), and issuing biased forecasts (Collewaert, Vanacker, Anseel, & Bourgois, 2021).

We focus on two IM tactics in product recall communication: (1) the strategic timing of recall initiation and (2) strategic silence in follow-up press releases. First, in our context of medical device recalls, these tactics span the entire crisis communication process, from initiating recalls with the U.S. Food and Drug Administration (FDA) to addressing stakeholders. Second, these IM tactics differ significantly: Strategic timing is a proactive approach, while strategic silence is a passive one. Prior research has documented the “Friday phenomenon,” whereby firms strategically release bad news on low-attention days (Dellavigna & Pollet, 2009; Diestre et al., 2020). For instance, issuing safety alerts on Fridays can increase drug-related deaths by 22%–36% (Diestre et al., 2020). However, this tactic can also attract greater scrutiny. In contrast, strategic silence obscures safety information, complicating stakeholder responses (Iqbal, Pfarrer, & Bundy, 2024). Once a recall is initiated, stakeholders already have information, making follow-up silence less consequential than strategic timing. Additionally, because silence implies inaction, stakeholders may be less likely to blame the CEO unless the recall is severe.

Our analysis is grounded in the behavioral agency model (BAM), which explains how CEOs balance risk and reward in decision-making (Gomez-Mejia, Welbourne, & Wiseman, 2000; Wiseman & Gomez-Mejia, 1998). The BAM proposes that as CEOs accumulate personal wealth, they adopt more cautious strategies to protect their assets (Devers et al., 2008; Devers, Wiseman, & Holmes Jr, 2007; Martin et al., 2013; Wiseman & Gomez-Mejia, 1998). The “mixed gamble” perspective, an extension of the BAM, suggests that CEOs weigh both potential gains and losses against their current wealth when making strategic decisions (DesJardine & Shi, 2021; Holmes, Bromiley, Devers, Holcomb, & McGuire, 2011; Martin et al., 2013).

Stock options exemplify a mixed gamble because stock price volatility, which often happens when firms facing adverse events, directly affects the value of CEOs’ option wealth (Martin et al., 2013). Since stock option wealth is highly sensitive to price fluctuations, even small changes can significantly impact its value. This creates a dual pressure: CEOs must both protect their existing wealth and pursue additional gains (Bromiley, 2009; Holmes et al., 2011; Martin et al., 2016). We argue that this tension shapes the IM tactics CEOs employ facing adverse events. Additionally, we consider the role of negative media coverage shaping these decisions.

Our study contributes to the executive compensation literature by explaining how stock-option incentives influence CEO decisions and actions facing adverse events, a context that has been understudied in this literature. While CEOs are often “singled out for denigration following a corporate failure” (Wiesenfeld, Wurthmann, & Hambrick, 2008: 238), little is known about how these incentives affect their crisis responses—decisions and actions with significant consequences for stakeholders. By examining the relationship between CEO option incentives and IM tactics, we offer new insights into the trade-offs CEOs navigate when managing product recalls.

We also extend the literature on CEOs’ mixed gambles, which has primarily focused on strategic decisions (e.g., DesJardine & Shi, 2021; Martin et al., 2013, 2016). By analyzing product recalls, we expand this framework to include corrective actions used by CEOs to preserve current or pursue prospective wealth, which have critical implications for both shareholders and other stakeholders. Our findings provide valuable insights for boards, media, and regulators regarding the broader impacts of stock-option incentives for CEOs and their implications for various stakeholders (e.g., Graf-Vlachy, Oliver, Banfield, König, & Bundy, 2020; Hill & Jones, 1992; Li, Bapuji, Talluri, & Singh, 2022; Werder, 2011).

Medical Device Recalls

Medical devices are indispensable for delivering quality healthcare, and any failure can have severe consequences for both customers and company shareholders (Thirumalai & Sinha, 2011; Wowak et al., 2015). The FDA, tasked with “protecting the public health by ensuring the safety, efficacy, and security of human and veterinary drugs, biological products, and medical devices” (FDA, 2021a: para. 1), plays a crucial role in overseeing the correction process of such failures.

When a medical device firm learns of a product failure, it must initiate a “corrective action” or recall. In theory, recalls can be initiated the day the firm becomes aware of the failure. However, firms often take significant time to submit a plan to the FDA outlining various recall elements. For example, Wowak, Ball, Post, and Ketchen (2021) found that firms take 95 days on average from problem awareness to recall initiation (with a minimum of 1 day and a maximum of 1,937 days).

The FDA reviews the firm’s recall plan, requests changes if needed, classifies the severity of the recall, publicizes the recall plan on its website, and monitors it until it is terminated (CFR ‒ Code of Federal Regulations, Title 21, 2020). While the FDA oversees such recalls, it allows firms to decide the course of action and mode of public warning, suggesting that CEOs have considerable leeway in determining when and how to notify users and suppliers of faulty products.

Theory and Hypotheses

The IM literature posits that executives maintain their positions by meeting stakeholders’ expectations (Graffin, Haleblian, & Kiley, 2016), often using IM tactics to counter negative perceptions when they violate (or risk violating) said expectations. For example, Zavyalova, Pfarrer, Reger, and Shapiro (2012) noted that product failures are perceived as organizational wrongdoing—“behaviors that place a firm’s stakeholders at risk and violate stakeholders’ expectations of societal norms and general standards of conduct” (p. 1080).

Given that firm outcomes reflect the decisions and actions of top leadership (Hambrick, 2007; Hambrick & Mason, 1984), it follows that CEOs are likely to mitigate negative impressions after a failure. In such cases, CEOs will engage in “damage control” to prevent negative consequences. However, extant research has yet to address how different types of option incentives might shape CEOs’ IM tactics in response to failures.

Behavioral Agency Model and CEO Decision-Making

Grounded in classical agency theory, stock-option compensation has become a common practice to incentivize CEOs to maximize shareholder returns (Fama, 1980; Jensen & Meckling, 1976). Agents (e.g., CEOs) are risk-averse because they cannot diversify their firm-specific investment of human capital. In contrast, principals (e.g., shareholders) can diversify equity portfolios across multiple firms, making them risk-neutral. This “risk differential” (Beatty & Zajac, 1995) suggests that CEOs make less optimal decisions by avoiding risks. To address this agency problem, classical agency theory suggests the use of stock-based compensation for CEOs, aligning their interests with those of shareholders. Any increase in the firm’s stock price simultaneously increases the value of the CEO’s compensation—an approach commonly termed “incentive alignment” (Fama, 1980).

The BAM, introduced by Wiseman and Gomez-Mejia (1998), posits that agents are loss averse (from prospect theory; Kahneman & Tversky, 1979), in contrast to the classical theory’s assumption of risk aversion (Jensen & Meckling, 1976). The BAM argues that CEOs frame decisions as opportunities to either avoid losses or preserve accumulated gains (Wiseman & Gomez-Mejia, 1998).

Extending the BAM (DesJardine & Shi, 2021; Martin et al., 2013), the “mixed gamble” perspective highlights that CEO decision-making relies on heuristics about their personal wealth, with mental shortcuts used to manage cognitive limitations (Martin et al., 2013). More specifically, it suggests that decision-makers are influenced by two key factors: (1) the avoidance of potential losses to current, or “endowed,” wealth and (2) the pursuit of potential gains to future, or “prospective,” wealth. For CEOs, current option wealth represents what could be lost if a decision fails (the downside), while prospective option wealth reflects the potential future gains if a decision succeeds (the upside). CEOs with substantial current option wealth tend to prioritize short-term strategies to protect their existing wealth, focusing on the downside. Conversely, those with uncertain but significant prospective wealth tend toward long-term strategies aimed at capturing future gains, making the upside more appealing (DesJardine & Shi, 2021; Martin et al., 2016).

CEOs’ Current Option Wealth and IM Tactics in Product Recalls

A CEO’s current option wealth reflects “the value that has already accumulated in options from increases in a stock price above the options’ exercise price” (Martin et al., 2013: 454). However, this wealth remains vulnerable to loss if stock prices decline. For instance, a product recall can negatively impact the company’s share price (Thirumalai & Sinha, 2011), thereby reducing the CEO’s option wealth due to the direct link between option valuations and share prices (Wiseman & Gomez-Mejia, 1998).

Since option values are highly sensitive to share-price fluctuations, even small changes in share prices can dramatically alter their worth, creating powerful incentives for CEOs to protect current option wealth (Bromiley, 2009; Holmes et al., 2011; Martin et al., 2016). To illustrate, consider a CEO holding options with a strike price of $99 while the current market price is $100, giving each option an intrinsic value of $1. A 1% decline in stock price to $99 would cause a 100% loss of the option’s intrinsic value, as the market price would now match the strike price. Similarly, Coles, Daniel, and Naveen (2006) found that CEO wealth is highly sensitive to stock-price fluctuations due to their exposure to options. On average, a 1% decline in a company’s stock price can result in a loss of $600,000 in CEO wealth.

In the case of medical device recalls, Thirumalai and Sinha (2011) demonstrated that recall announcements can negatively affect firms’ stock price, thus eroding CEOs’ option wealth. According to the BAM’s focus on loss aversion, CEOs are likely to take actions to minimize these losses. More specifically, we propose that CEOs might time recall initiations and strategically withhold information in press releases to offset negative stock reactions to recalls.

Strategic timing

CEOs can protect their current option wealth by initiating recalls on Fridays, as research indicates that investors are less attentive to adverse events communicated at the end of the workweek (Diestre et al., 2020; Louis & Sun, 2010). For instance, Diestre et al. (2020) found that drug safety alerts issued on Fridays are less widely disseminated. Similarly, Dellavigna and Pollet (2009) observed a muted market response to disappointing earnings announcements made on Fridays, likely due to people being absent from work (Harrison & Hulin, 1989; Herrmann & Rockoff, 2012) or shifting their attention to upcoming leisure activities (Sotak, Spain, Dionne, & Yammarino, 2015).

CEOs may capitalize on these patterns of inattention to protect option wealth and minimize negative impressions of the firm’s performance. According to the BAM’s mixed gamble perspective, which suggests that loss-averse CEOs tend to adopt strategies that mitigate threats to their wealth (Wiseman & Gomez-Mejia, 1998), we propose that CEOs with greater current option wealth are more likely to time recalls on days of reduced investor attention. By exploiting these inattention windows, CEOs may dampen adverse stock reactions, at least in the short term, thus protecting their current option wealth. Therefore:

Hypothesis 1a: The greater a CEO’s current option wealth, the higher the likelihood that the recall is initiated on an inattentive day.

Strategic silence

Strategic silence can be employed to manage the firm’s public image. For example, Carlos and Lewis (2018) found that some firms withhold prominent sustainability certifications to avoid accusations of hypocrisy from stakeholders. In our empirical context, although the FDA oversees the recall process to ensure public safety, it largely relies on companies to act in good faith in recall communications. Therefore, CEOs of firms recalling medical devices have considerable discretion over public warnings. In fact, the FDA acknowledges that “patients [may] respond to a public warning about a defective product without first having the benefit of consulting with their physician. In these and similar situations, public warnings may be more confusing than helpful” (FDA, 2019: 7). This ambiguity allows CEOs to remain strategically silent in press releases, withholding details about recalls.

We argue that CEOs may use strategic silence to protect their option wealth from potential losses, as product recalls often raise concerns and reduce share prices. From a mixed gamble perspective, CEOs with significant current option wealth may withhold information that could heighten market awareness of a product recall, using strategic silence to mitigate negative market reactions. Therefore:

Hypothesis 1b: The greater a CEO’s current option wealth, the higher the likelihood of strategic silence (i.e., press releases not mentioning product recalls).

CEOs’ Prospective Option Wealth and IM Tactics in Recalls

Prospective option wealth reflects “the potential future gains to wealth that might be realized over and above the current accumulated value in their stock options” (Martin et al., 2013: 454). CEOs with substantial prospective wealth are oriented toward long-term gains, focusing on potential upsides. DesJardine and Shi (2021) supported this distinction, demonstrating that present-focused CEOs endow current wealth while future-focused CEOs maximize prospective wealth.

We argue that CEOs with significant prospective wealth are more likely to prioritize long-term share price growth by opting for open communication during product recalls, rather than timing recalls for periods of market inattention. While recalls may have short-term negative impacts, they are often integral to product development and can signify critical milestones for future success (Li et al., 2022). IM tactics aimed at exploiting market inattention—such as initiating recalls during inattentive periods—or relying on strategic silence might yield short-term benefits. However, as information emerges, these tactics are likely to be revealed, reducing their effectiveness. Furthermore, effective communication can help the firm engage various stakeholders, leading to failure correction and product improvement. Therefore, CEOs motivated by prospective wealth are more inclined to communicate openly about recalls and emphasize future plans, thereby building a foundation for long-term growth. This aligns with findings that prospective wealth encourages investments in long-term capabilities—such as R&D, capital expenditures, and strategic debt—over short-term tactics (Martin et al., 2013).

In summary, high prospective wealth reduces CEOs’ reliance on short-term IM tactics that may fail as additional information emerges over time, shifting the focus away from current wealth preservation. Therefore:

Hypothesis 2a: The greater a CEO’s prospective option wealth, the lower the likelihood that the recall is initiated on an inattentive day.

Hypothesis 2b: The greater a CEO’s prospective option wealth, the lower the likelihood of strategic silence (i.e., press releases not mentioning product recalls).

Moderating Effects of Negative Media Coverage

Current option wealth and negative media coverage

We have argued that CEOs with substantial current option wealth tend to employ the two identified IM tactics. However, this tendency should diminish under negative media coverage. The media is critical in shaping public opinion and setting social agendas (Graf-Vlachy et al., 2020; Petkova, Rindova, & Gupta, 2013; Shoemaker & Reese, 2013). It “can be very influential in focusing attention on specific issues and phenomena” (Ocasio et al., 2023: 115), notably because “as the fourth pillar of democracy, news media are expected to protect and promote the rights of the public and ward it against businesses” (Astvansh, Wang, & Shi, 2022: 4223). By monitoring firms for transgressions, the media increases the visibility of corporate actions (Astvansh et al., 2022; Desai, 2014).

IM tactics are effective when information is ambiguous, difficult to obtain, or unavailable; however, they risk exposure when audiences gain access to clearer data. Negative media coverage amplifies scrutiny from shareholders and stakeholders, putting a CEO’s reputation and job security at risk. This external pressure leads CEOs to exercise greater caution in their use of IM tactics (Eisenhardt, 1989; Tuggle, Sirmon, Reutzel, & Bierman, 2010). Moreover, heightened scrutiny can lead to stricter internal oversight by boards and shareholders, further limiting a CEO’s ability to shape perceptions for personal gain.

The media has increasingly “stigmatized” CEO option pay (Kuhnen & Niessen, 2012), portraying it as a source of “perverse incentives” (Deya-Tortella, Gomez-Mejia, de Castro, & Wiseman, 2005). As society’s watchdog, the media has criticized option pay “based on the presumption that it created strong incentives for corporate leaders to focus myopically on short-term share prices” (Carberry & Zajac, 2021: 158). For CEOs with substantial current option wealth, negative media coverage increases the risks of using IM tactics to conceal such adverse events as product recalls. Under intense scrutiny, concealment can harm a CEO’s reputation and increase occupational risks if exposed, including regulatory sanctions, loss of investor confidence, and reputational damage, potentially outweighing any gains (Astvansh et al., 2022). Prior negative media attention further increases the likelihood of IM efforts being perceived as dishonest (Barnes, 1994; Pennebaker, 2011), amplifying reputational risks (Astvansh et al., 2022; Bednar, Boivie, & Prince, 2013; Pozner, 2008).

In sum, high levels of negative media coverage put significant pressure on CEOs, making those with substantial current option wealth less likely to engage in IM tactics. Therefore:

Hypothesis 3a: The positive relationship between a CEO’s current option wealth and recall initiation on an inattentive day is weaker (less positive) with more negative media coverage.

Hypothesis 3b: The positive relationship between a CEO’s current option wealth and strategic silence is weaker (less positive) with more negative media coverage.

Prospective option wealth and negative media coverage

We previously argued that CEOs with higher prospective option wealth are less likely to use strategic timing or silence as IM tactics to influence market responses, focusing instead on actions supporting long-term growth. We now propose that the negative relationship between prospective option wealth and the use of these IM tactics should be enhanced by a high level of negative media coverage.

Under negative media scrutiny, CEOs must carefully weigh the long-term implications of their decisions and actions. Proactively addressing product issues enables them to portray the firm as responsible, potentially improving long-term stock performance and enhancing their prospective option wealth (Martin et al., 2016). Negative media attention reinforces the importance of transparency, as obfuscation can damage a CEO’s reputation and hinder the perception of integrity. By handling recalls responsibly, CEOs can strengthen both their own and the firm’s reputation for sound governance, thereby mitigating the risks associated with evasive tactics. Thus, a CEO who is already inclined to avoid IM tactics due to higher prospective wealth becomes even less likely to employ timing or silence tactics under greater media scrutiny. Therefore:

Hypothesis 4a: The negative relationship between a CEO’s prospective option wealth and recall initiation on an inattentive day is stronger (more negative) with more negative media coverage.

Hypothesis 4b: The negative relationship between a CEO’s prospective option wealth and strategic silence is stronger (more negative) with more negative media coverage.

Methods

We drew our sample from medical device recalls registered with the FDA. 1 The FDA maintains a comprehensive archive of all medical device recalls since 2003, categorizing them based on severity (see Appendix A for an example). Class 1 recalls represent a reasonable probability of serious health problems or death (FDA, 2021b). Class 2 recalls may lead to temporary or medically reversible health consequences, while Class 3 recalls are considered benign and unlikely to carry health consequences. Given that Class 3 recalls may not preoccupy stakeholders and, thus, may not significantly impact CEO decision-making, we follow prior research by focusing on Class 1 and Class 2 medical device recalls (Wowak et al., 2015).

We matched these product recalls to the financial data of the initiating companies in the COMPUSTAT database, 2 which we then matched to the Execucomp database containing top executives’ compensation data. Execucomp only tracks firms listed in the S&P 1500. For companies present in COMPUSTAT but absent in Execucomp, we manually collected compensation data from proxy statements filed with the Securities Exchange Commission. For board-related variables, we used the BoardEx database. To examine these companies’ product-recall communications, we used their press releases and media articles collected from Factiva. Finally, we sought data directly from the FDA through the Freedom of Information Act regarding the dates of problem awareness, which are reported to the FDA but not publicly disclosed by recalling firms. Our final sample included 6,609 Class 1 and Class 2 recalls by 127 firms led by 170 CEOs between 2004 and 2017.

Dependent Variables

Inattentive recall

Our measure of strategic timing for recall initiation was inattentive recall, a binary variable (1/0) reflecting whether the product recall was initiated on an inattentive day (Fridays and the last working days before the four major U.S. holidays: Christmas, New Year’s, Independence Day, and Thanksgiving; Louis & Sun, 2010). 3 In a robustness check, we examined only the likelihood of recall initiation on Fridays, with our results remaining qualitatively identical. Through the Freedom of Information Act, we also sourced the problem awareness data. The average time from problem awareness to recall initiation was 191 days, indicating that firms have discretion in determining when to initiate product recalls.

Strategic silence

We downloaded all press releases from our sampled firms between 2004 and 2017 from Factiva. 4 We first created a special program in R to parse the text, sources, and dates of the articles into separate columns from the downloaded text files. Given our focus on firm-controlled communication, we limited the sample to press releases from two primary sources commonly used by firms to disseminate information: Business Wire and PR Newswire. Applying these filtering criteria, we identified 6,351 unique press releases. 5

Next, we flagged these press releases in R if they contained the following word roots: “recall,” “fault,” “class,” “lawsuit,” or “device” (broad search). Subsequently, two coders—the lead author and an external researcher (a senior Ph.D. candidate well-trained in text analytical methods)—independently reviewed the flagged press releases and developed codes to determine whether they mentioned product recalls. The coders discussed differences in coding (less than 1% of cases) and reached a consensus. We created a binary variable, strategic silence, and assigned it a value of 1 if the firm did not mention the faulty recall in its press releases 30 days after its initiation date, and 0 otherwise (Carlos & Lewis, 2018). Given that firms can craft communication in anticipation of impending recalls (Elsbach, Sutton, & Principe, 1998; Graffin et al., 2011), we widened our window to 60 days (30 days before and after the recall date) as a robustness check and found qualitatively identical results.

Independent Variables

We measured CEO current option wealth as the number of options from each option grant multiplied by their spread (i.e., the positive difference between the exercise and stock prices) for in-the-money options at the fiscal year-end (Devers et al., 2008; Larraza-Kintana et al., 2007; Martin et al., 2013). 6 The Execucomp database provides estimated values for unexercised in-the-money options. These estimates are based on the difference between the option’s exercise price and the company’s year-end stock closing price. This spread forms the basis for the calculations used in our analysis.

CEO prospective option wealth reflects the potential future wealth a CEO could amass beyond the current cash value of stock options (Martin et al., 2013). For its estimation, we used the average annual increase in the Dow Jones Industrial Average throughout the study period: 7%. By increasing the stock price of the focal firm by 7% over the remaining number of years (denoted as “time” in the equation below) (DesJardine & Shi, 2021; Martin et al., 2013), we measured CEO prospective option wealth as follows:

To measure negative media coverage, we used media articles from 30 days to the recall. We conducted a text analysis using the LIWC 2015 software (Pennebaker, Boyd, Jordan, & Blackburn, 2015), which counted the total positive and negative affective words for each article. Following Graf-Vlachy et al., (2020), we measured negative media coverage of these articles using the following formula:

We checked the difference in media coverage before and after product recalls by using t-test and found that media coverage became significantly negative after a recall (mean difference = 0.013%, t = 8.50), supporting the relevance of negative media coverage in shaping CEO IM tactics in product recalls. As a robustness check, we extended the media coverage window to 60 days (30 days before and after the recall) and obtained similar results.

We included various control variables in our regression models. At the recall level, we controlled for the difference in recall severity using a binary indicator, Recall Class 1 (FDA, 2021b), and assigned it a value of 1 if the recall was classified as Class 1, and 0 otherwise. We included previous product recalls (the number of product recalls initiated in the previous years) in all regression models. At the firm level, we controlled for the effects of firm size using the number of employees (log-transformed), R&D intensity (R&D expense divided by sales), market performance (Tobin’s Q), and financial distress (Altman’s Z) (Altman, 1968). We also controlled for industry fixed effects by including industry dummies based on four-digit GICS (Global Industry Classification System) codes and year fixed effects by including year dummies.

At the CEO level, we controlled for the effects of CEO other pay, including the sum of cash bonus, salary, and nonequity incentives (log-transformed). We controlled for CEO stock value using the number of shares held multiplied by the year-end stock price (log-transformed). We also controlled for CEO tenure (years in the CEO position), founder CEO (a dummy variable reflecting whether the CEO is also the founder or cofounder of the firm), and CEO R&D background (a binary indicator reflecting whether the CEO started his or her career in product or process R&D functions; Hambrick & Mason, 1984). At the board level, we controlled for two variables commonly used in corporate governance research: board independence (independent director ratio; Boyd, Haynes, & Zona, 2011; Liu, Miletkov, Wei, & Yang, 2015) and CEO duality (a binary indicator of whether the CEO also serves as the board chair; Boyd, 1995; Krause, Semadeni, & Cannella, 2014).

Results

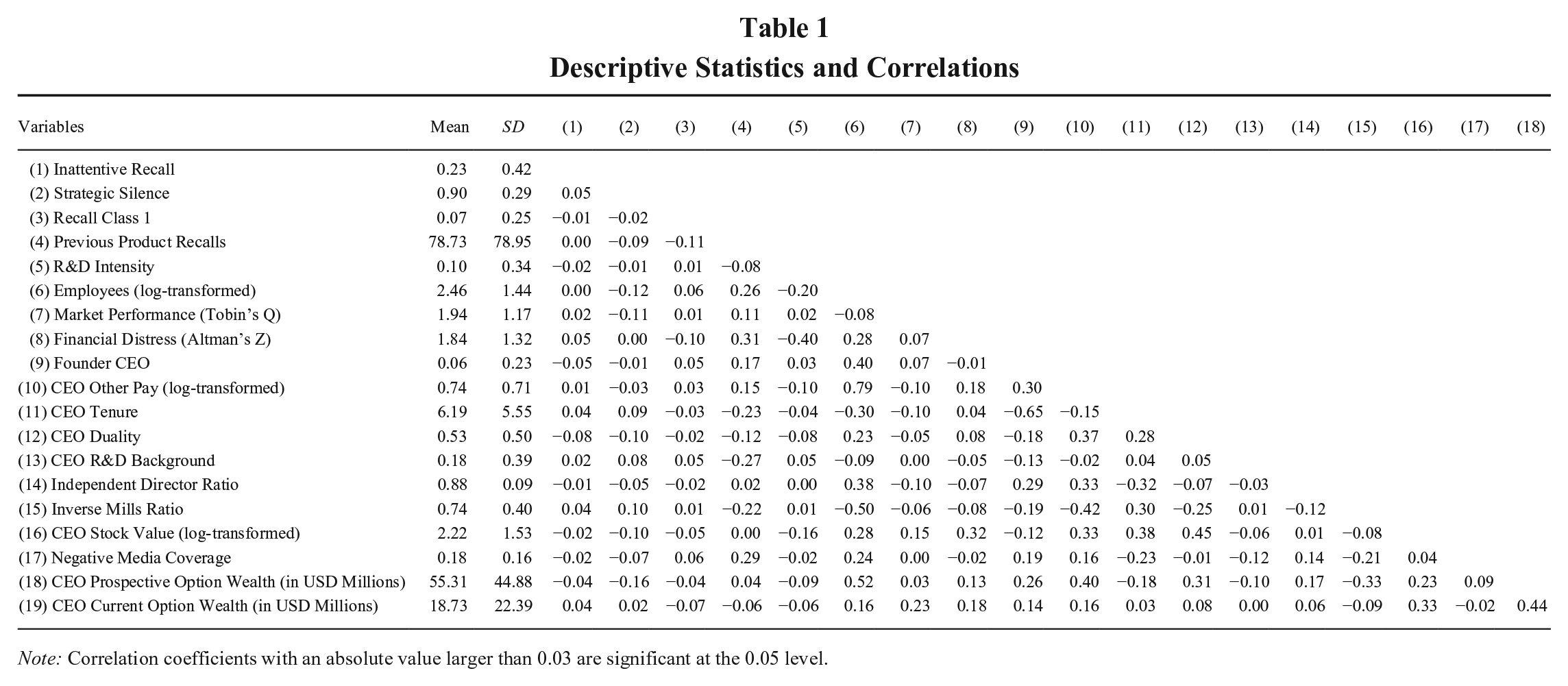

Table 1 presents descriptive statistics and correlations for all variables, excluding industry and year dummies. The mean values for the likelihood of recall on an inattentive day and strategic silence were 0.23 and 0.90, respectively, indicating that, on average, 23% of recalls were initiated on inattentive days and that 90% without press releases. The correlation between the CEO’s current and prospective option wealth was 0.44, consistent with the pairwise correlations of 0.67 and 0.50 reported by Martin et al. (2013) and DesJardine and Shi (2021), respectively. Additionally, a variance inflation factor analysis was conducted and produced values within the acceptable limit of 2, suggesting that multicollinearity was not a significant issue. 7 Tables 3 and 4 detail the impact of CEO option wealth on CEOs’ IM tactics during recalls.

Descriptive Statistics and Correlations

Note: Correlation coefficients with an absolute value larger than 0.03 are significant at the 0.05 level.

Estimation Method

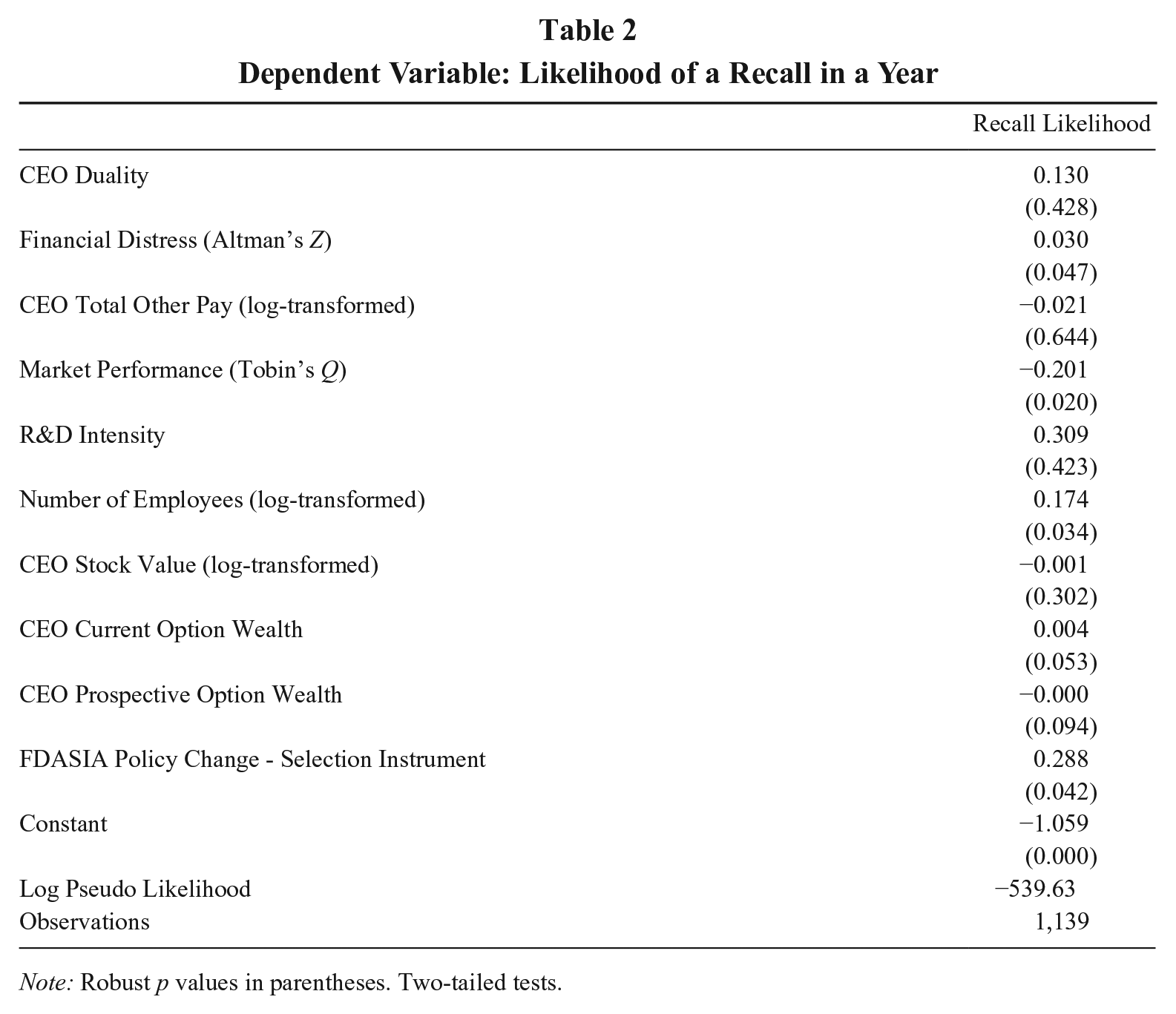

Since not all firms in our sample recalled products in a given year, we used Heckman selection models to control for selection bias by estimating a firm’s likelihood of recalling a product using a selection instrument, which should be related to selection (i.e., recall likelihood) but not outcomes (i.e., CEO IM tactics; Certo, Busenbark, Woo, & Semadeni, 2016). We used the FDA Safety and Innovation Act (FDASIA) as our selection instrument (Office of the Commissioner, 2019). The FDASIA, enacted in July 2012, aimed to improve patient safety, streamline medical product approvals, and strengthen FDA enforcement against unsafe products. The FDASIA expanded the FDA’s authority, leading to more recalls due to improved post-market surveillance and risk-based inspections. However, the FDASIA focused solely on medical device safety and did not specify whether recalls must be initiated on specific days or communicated through press releases. Therefore, it did not directly affect firms’ recall-related IM tactics. We used a binary variable to create this selection instrument, assigning it a value of 1 if a firm-year observation was subject to this policy change (i.e., 2013 and after).

Table 2 presents the first-stage results, where the FDASIA variable exhibits a robust positive coefficient (b = 0.288, p < 0.05), confirming that FDASIA is highly relevant for predicting medical device recalls. Therefore, the instrument is both conceptually valid and statistically significant for isolating the selection effect. 8 Next, we included the predicted inverse Mills ratio in our regression models. Since our dependent variables are binary, we used probit regressions. Following Papke and Wooldridge (2008), we employed a clustered correlation structure grouped by CEOs and used robust standard errors in these regression models.

Dependent Variable: Likelihood of a Recall in a Year

Note: Robust p values in parentheses. Two-tailed tests.

IM Tactics With Recalls

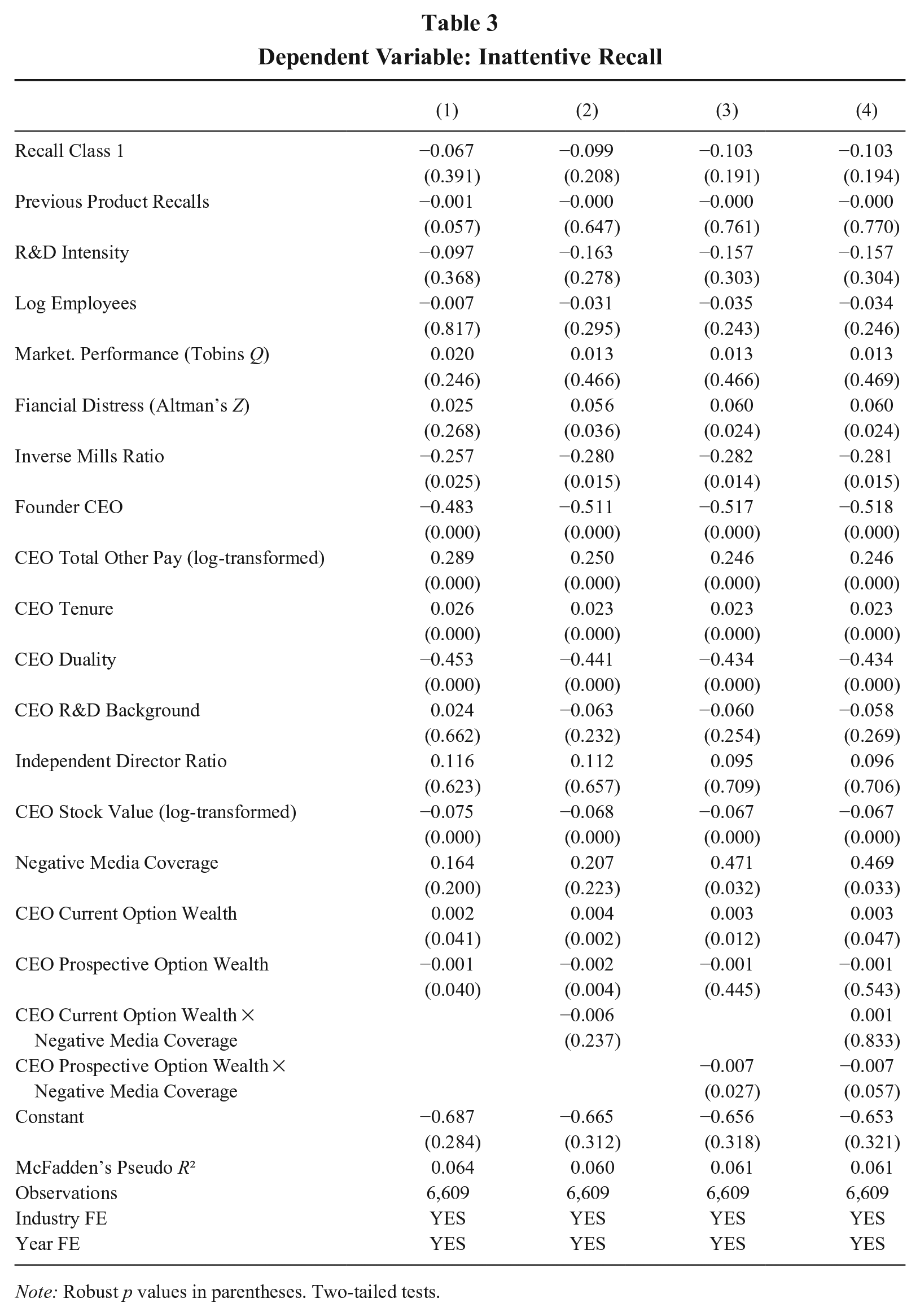

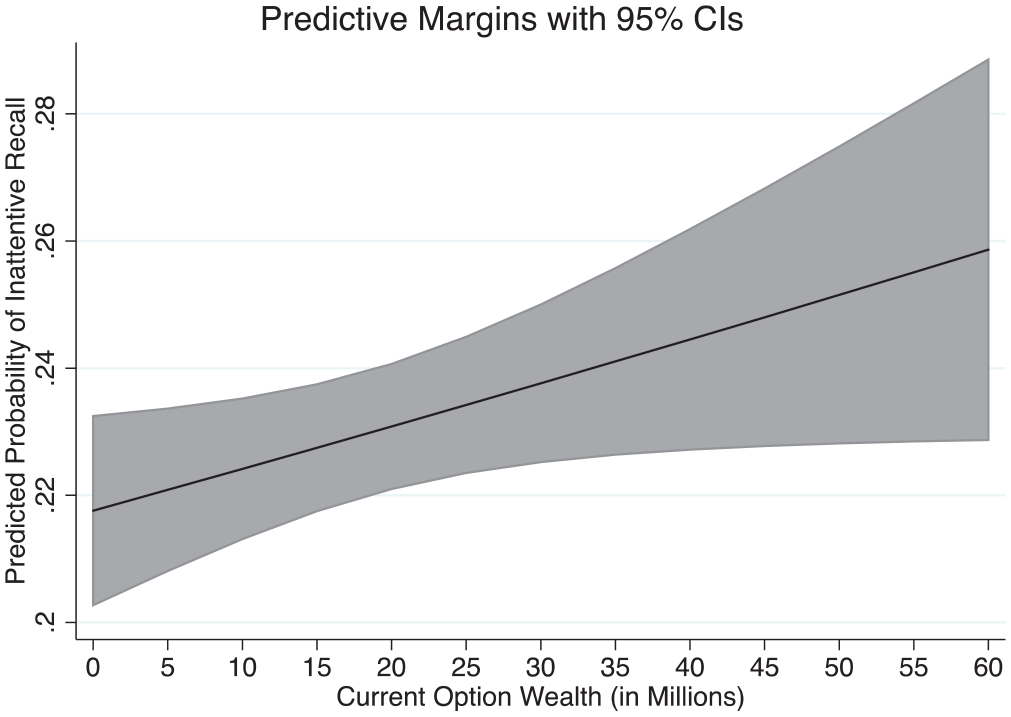

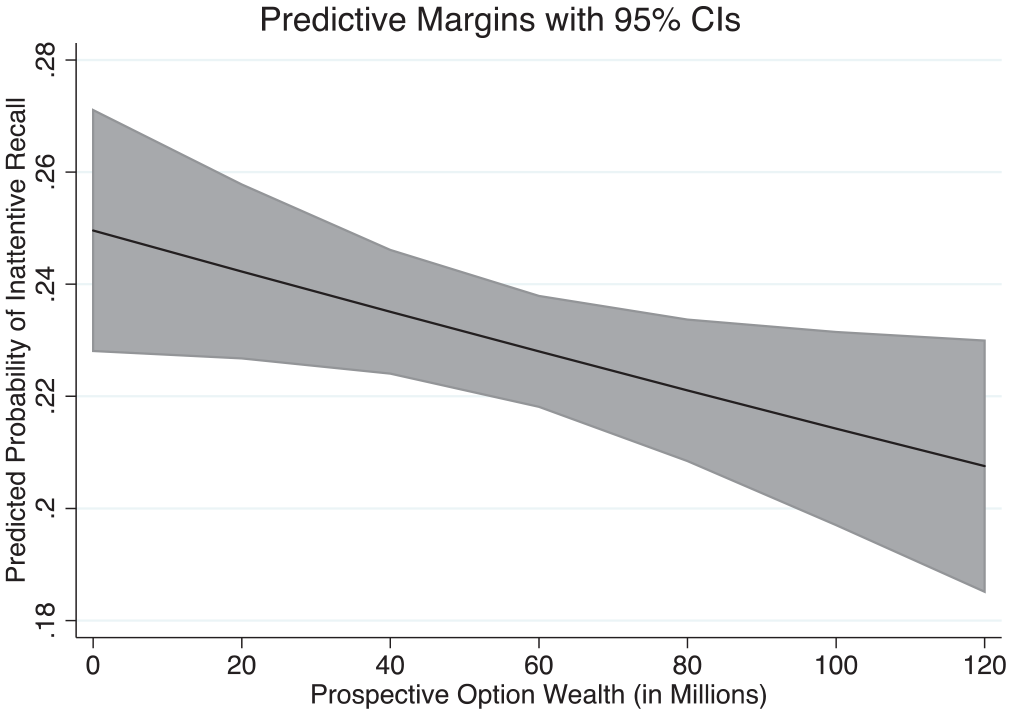

Model 1 (Table 3) reports the second-stage results of the Heckman selection probit model. The analysis shows a positive and significant coefficient for CEO current option wealth (b = 0.002, p = 0.041). Due to the difficulty in directly interpreting regression coefficients and significance levels in probability models (Wiersema & Bowen, 2009), and as hypotheses should not be tested solely by examining p-values (Busenbark, Graffin, Campbell, & Lee, 2022), the average marginal effect is visualized in Figure 1. The confidence intervals (CIs) of the marginal effects do not cross zero, thus supporting Hypothesis 1a. A one-standard-deviation increase in the CEO’s current option wealth from the mean value (18.7 to 44.1 million USD) increased the probability of initiating an inattention recall from 23% to 25%. Additionally, the coefficient for CEO prospective option wealth was negative and significant (b = −0.001, p = 0.04). Figure 2 plots the marginal effect, showing that a one-standard-deviation increase in CEO prospective option wealth from the mean value (55.3 to 100.1 million USD) decreased the probability of initiating an inattention recall from 23% to 21%, supporting Hypothesis 2a.

Dependent Variable: Inattentive Recall

Note: Robust p values in parentheses. Two-tailed tests.

Main Effect of Current Option Wealth on Inattentive Recall

Main Effect of Prospective Option Wealth on Inattentive Recall

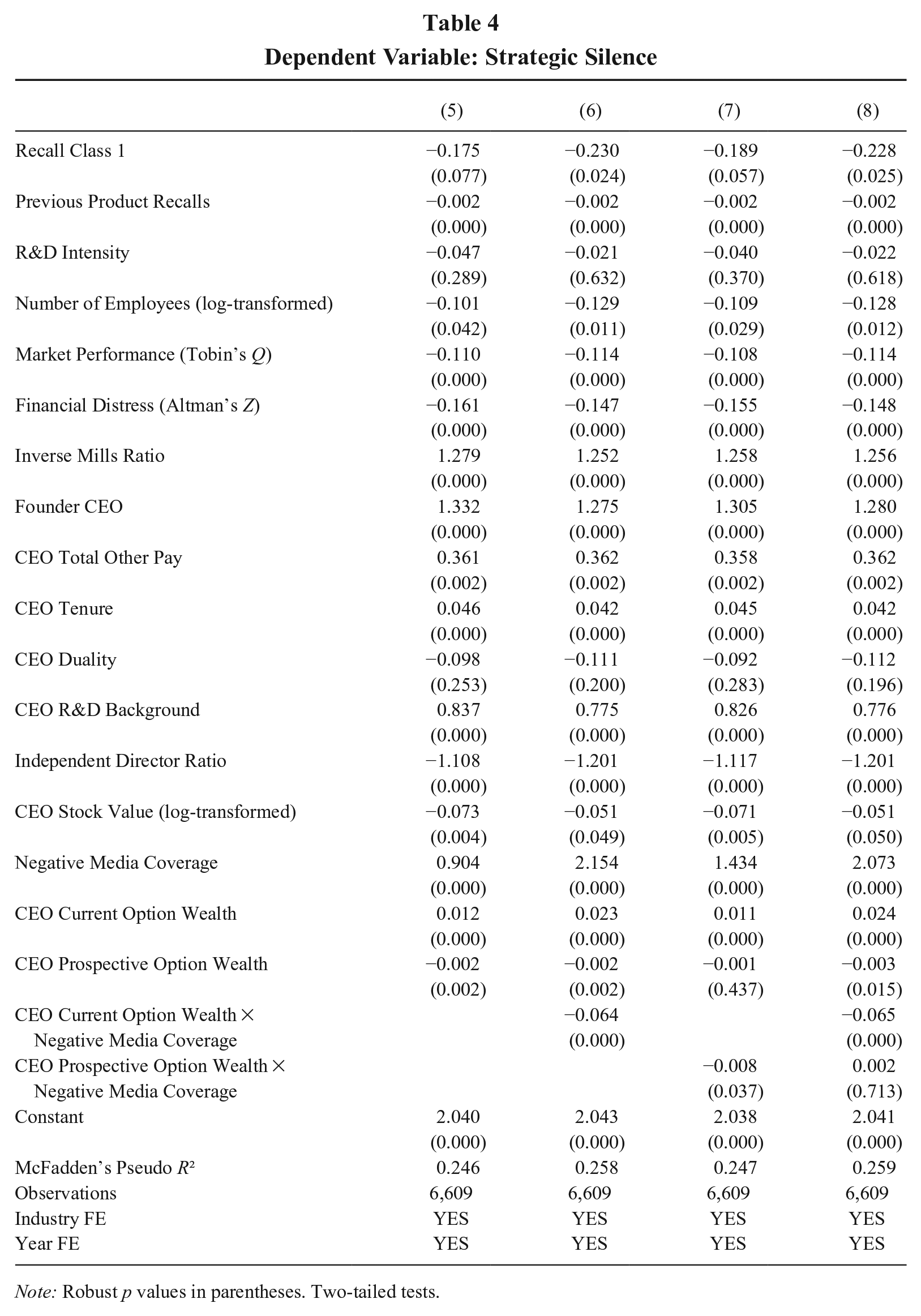

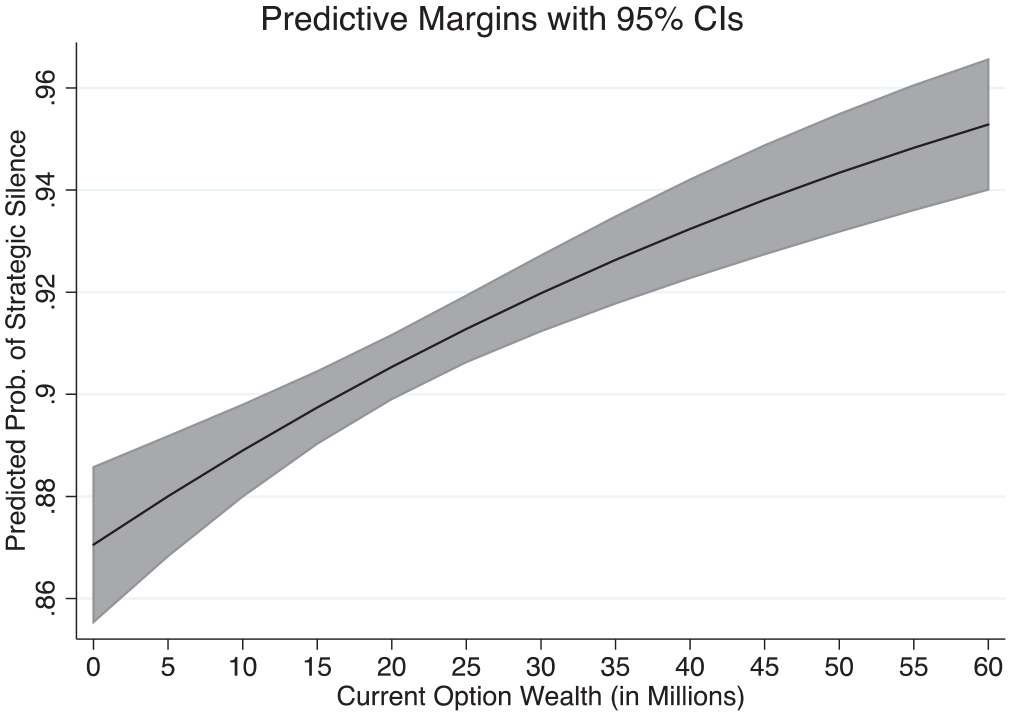

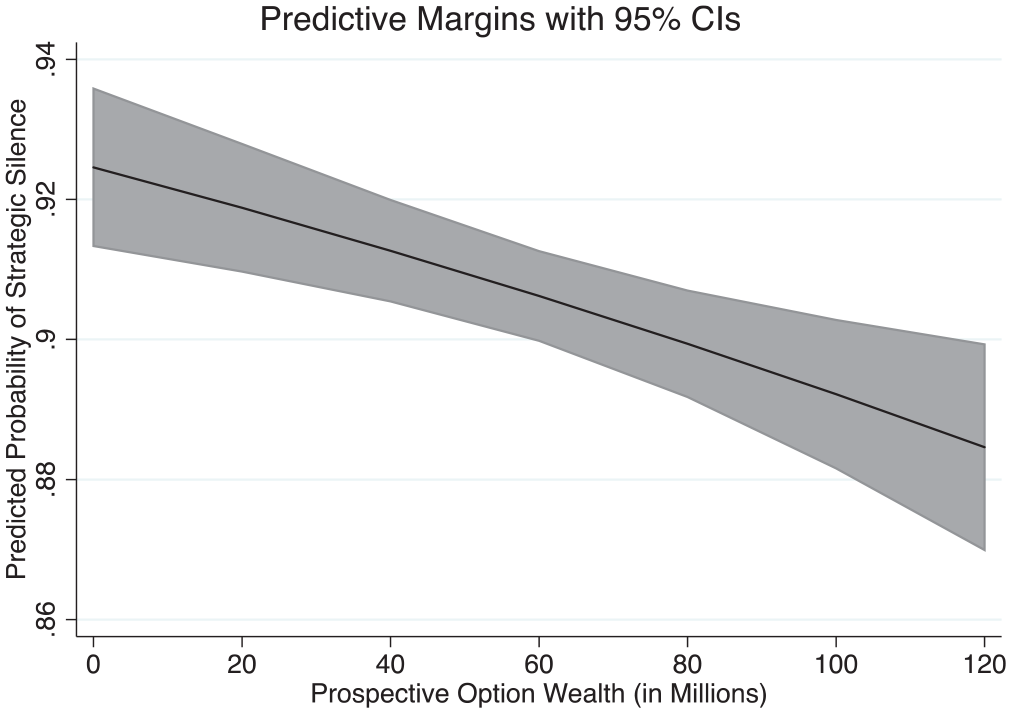

As Model 5 (Table 4) reports, the coefficient for CEO current option wealth was positive and significant (b = 0.012, p < 0.001). Figure 3 plots the marginal effect, supporting Hypothesis 1b. A one-standard-deviation increase in CEO current option wealth from the mean value (18.7 to 44.1 million USD) increased the likelihood of strategic silence from 90% to 93%. Furthermore, the coefficient for CEO prospective option wealth was negative and significant (b = −0.002, p < 0.01). Figure 4 visualizes the marginal effect, supporting Hypothesis 2b. A one-standard-deviation increase in CEO prospective option wealth from the mean value (55.3 to 100.1 million USD) reduced the probability of strategic silence from 91% to 89%.

Dependent Variable: Strategic Silence

Note: Robust p values in parentheses. Two-tailed tests.

Main Effect of Current Option Wealth on Strategic Silence

Main Effect of Prospective Option Wealth on Strategic Silence

Moderation by negative media coverage

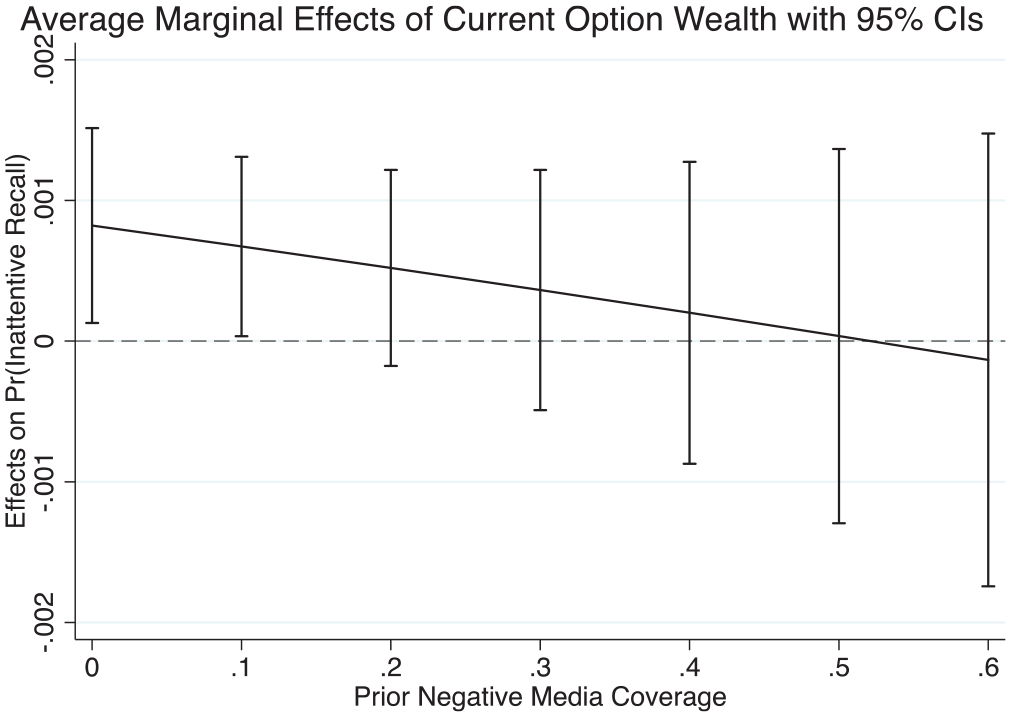

Model 2 (Table 3) adds the interaction term between negative media coverage and CEO current option wealth, yielding a negative coefficient for the likelihood of initiating an inattentive recall (b = −006, p = 0.237). Although this interaction term is not statistically significant at the conventional p = 0.05 threshold, Figure 5 indicates that the marginal effect of CEO current option wealth is significant for negative media coverage levels below 0.15. Thus, Hypothesis 3a is partially supported.

Interaction Effect of Current Option Wealth and Negative Media Coverage on Inattentive Recall

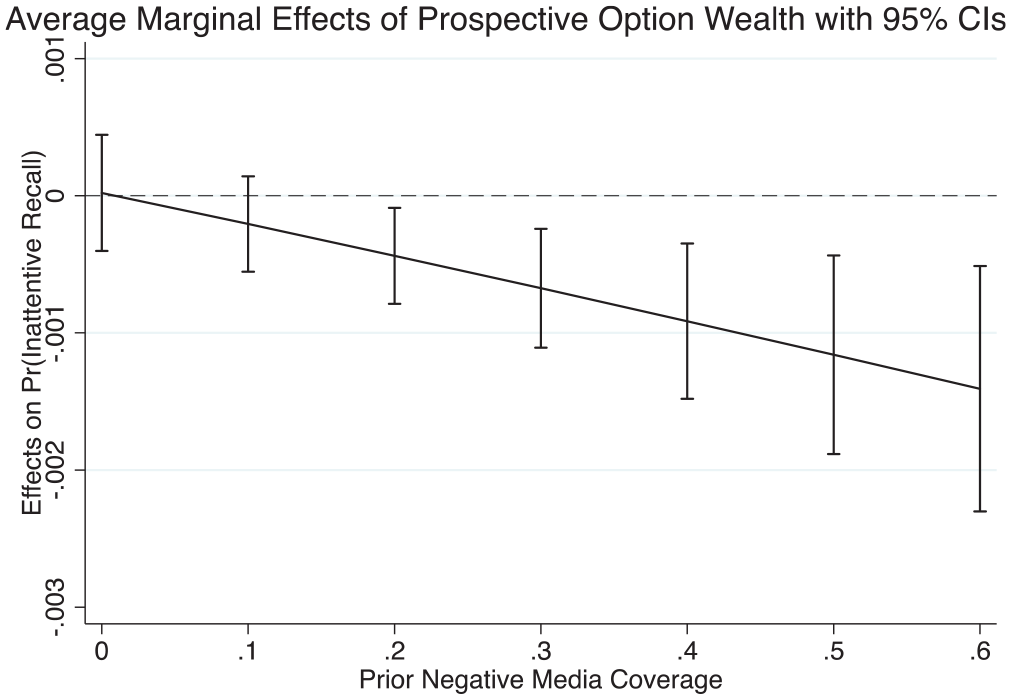

In Model 3 (Table 3), the interaction term between negative media coverage and CEO prospective option wealth yields a negative and significant coefficient for the likelihood of initiating an inattentive recall (b = −0.007, p = 0.027). Figure 6 illustrates the marginal effect of CEO prospective option wealth across varying levels of negative media coverage. The marginal effect is significant for negative media coverage levels above 0.15, partially supporting Hypothesis 4a. Model 4 includes both interaction terms and produced similar results.

Interaction Effect of Prospective Option Wealth and Negative Media Coverage on Inattentive Recall

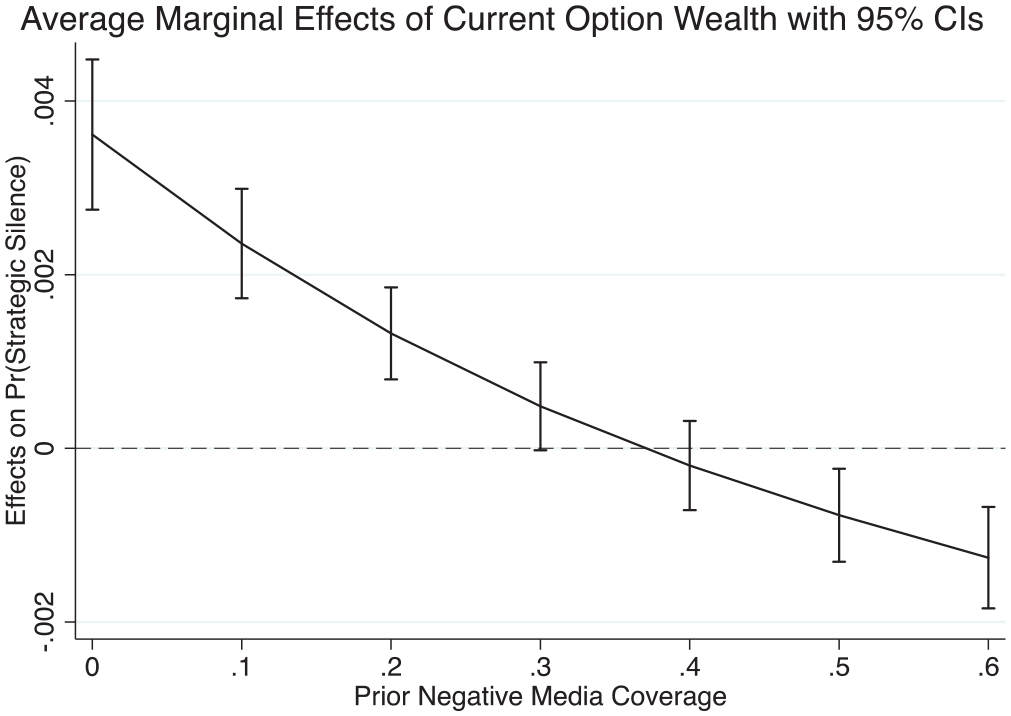

Model 6 (Table 4) adds the interaction between negative media coverage and CEO current option wealth, yielding a negative coefficient for the likelihood of strategic silence (b = −0.064, p < 0.001). Figure 7 illustrates the moderation effect, showing that negative media coverage significantly reduces the likelihood of strategic silence, supporting Hypothesis 3b.

Interaction Effect of Current Option Wealth and Negative Media Coverage on Strategic Silence

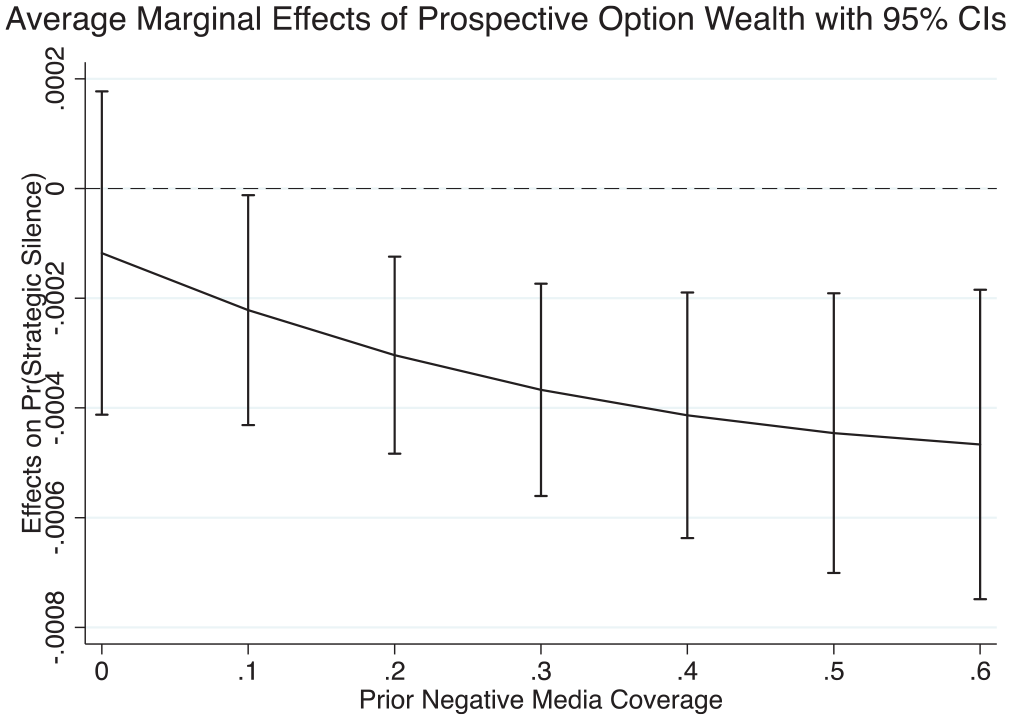

In Model 7 (Table 4), the interaction term between negative media coverage and CEO prospective option wealth produces a negative and significant coefficient for strategic silence (b = −0.008, p < 0.05). Figure 8 depicts the marginal effect, supporting Hypothesis 4b. Finally, Model 8 includes both interaction terms and yields similar results.

Interaction Effect of Prospective Option Wealth and Negative Media Coverage on Strategic Silence

Robustness Checks and Additional Analyses

Two-stage instrumental variable regressions

Unobservable industry-, firm-, or CEO-level factors could affect CEO option wealth and IM tactics regarding product recalls. Some of these factors may introduce the possibility of reverse causality, omitted variable bias, or both, leading to potential endogeneity in our study. A common approach to this problem is using two-stage least squares modeling (Sanders & Hambrick, 2007). Regarding CEO current option wealth, we used two instruments: Bartik IV and the lagged number of exercisable options. Bartik IV (Bartik, 1991) exploits the heterogeneous effect of a nationwide regulatory change or exogenous “shock” (Breuer, 2022; Goldsmith-Pinkham, Sorkin, & Swift, 2020). Known also as a “shift-share” instrument, it acts as a difference-in-difference analysis, with the shock affecting the independent variable (Adão, Kolesár, & Morales, 2019). It leverages “exogenous variation in the shocks, allowing the variation in exposure shares to be endogenous” (Borusyak, Hull, & Jaravel, 2022: 182), ensuring that the shocks are uncorrelated with unobserved factors that could influence the outcome at the level of analysis.

The Financial Accounting Standards Board changed the reporting of stock options in 2006, requiring all firms to expense firm stock options. We used this shock to randomize our treatment variable (CEO current option wealth). The change in regulation (shift) should be correlated with the CEO options granted after 2007 by all U.S. firms. Therefore, we created a regulatory “shift” dummy variable (1 for all firm years in our sample from 2007 onwards and 0 otherwise) and multiplied it by a firm’s lagged “share” of CEO current option wealth in its industry (4-digit GICS codes) to account for the panel-level variation (Adão et al., 2019). The identifying rationale is that the policy change was exogenous to CEO decision-making, except through its effect on CEO current option wealth. Regarding the lagged number of exercisable options, our rationale is that it primarily determines the CEO’s current option wealth (Benischke et al., 2019). However, any effect on IM tactics related to product recalls, if present, operates solely through current option wealth. From a CEO’s perspective, it is not the number of exercisable options, but rather the underlying value of those options that influences their IM decisions.

With respect to CEO prospective option wealth, we used another two instruments: the lagged number of unexercisable stock options and the average time to expiry of CEO options (number of years) (Benischke et al., 2019; Martin, Wiseman, & Gomez-Mejia, 2019). Both variables can largely influence the CEO’s prospective option wealth, as indicated by our formula for measuring prospective option wealth. However, their effects on IM tactics regarding product recalls, if present, are likely to operate exclusively through prospective option wealth.

As reported in Appendix B (Models 9 and 10), we used the Sargan-Hansen test to examine the validity of these instruments (Semadeni, Withers, & Trevis Certo, 2014). The test results suggest that our instruments are exogenous (Hansen’s J chi2(2) = 0.9509, p = 0.6216). Furthermore, the second-stage regression models (Models 11 and 12) produced results consistent with those of Models 1 and 5, respectively.

Differences in IM tactics

We also assessed whether the two IM tactics—strategic timing and silence—indeed differ in meaningful ways as we discussed previously. Our results suggest that CEOs who also serve as board chairs are significantly less likely to initiate Friday recalls (Models 1–4 in Table 3), but do not exhibit a notable preference for strategic silence (Models 5–8 in Table 4). Dual CEOs, often perceived as powerful leaders, tend to attract greater media and stakeholder attention. Consequently, initiating recalls on market-inattentive days may invite stricter scrutiny from regulators and stakeholders. These CEOs may fear that exposure could jeopardize their dual roles within their companies, thus having reduced the use of strategic timing in recall initiation.

Founder CEOs are less likely to initiate recalls on low-attention days (Models 1–4, Table 3) but more likely to remain silent about product recalls in press releases (Models 5–8, Table 4). Management and entrepreneurship research suggests that founder CEOs exhibit a stronger sense of psychological ownership than non-founder CEOs (Hsu, 2013; Zhu, Smith, & Brown, 2024). Their deep connection to the company makes them less inclined to initiate recalls on low-attention days, as such timing has been linked to greater harm for product users (Diestre et al., 2020). However, since strategic silence in press releases does not prevent the recall itself, founder CEOs may perceive it as less harmful. Therefore, their psychological ownership appears to make them more proactive in disclosing product recalls to regulators and stakeholders, while also increasing their inclination to withhold recall details in press releases. Overall, these additional analyses suggest that, while strategic timing and strategic silence are both relevant IM tactics that CEOs may adopt during product recalls, strategic timing is likely to be primary and more active than strategic silence.

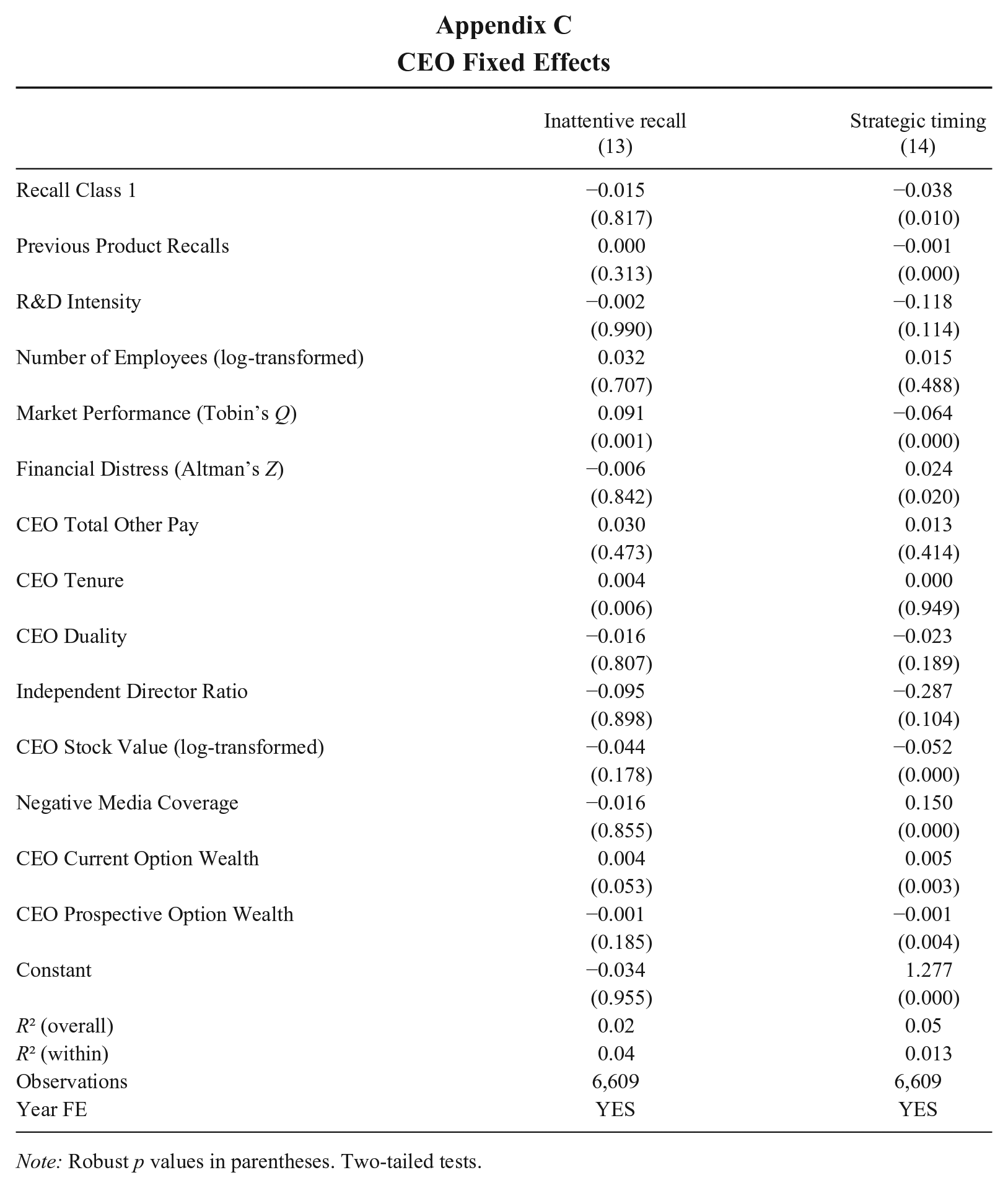

CEO fixed effects

Our primary theoretical interest lies in whether CEOs with substantial option wealth are more inclined to make mixed gamble decisions during adverse conditions. As shown in Appendix C, the effects observed within CEOs were slightly weaker, probably due to the reduced variation within CEOs over time in estimating heuristics about their option wealth.

Discussion

We sought to examine the role of CEO compensation in shaping decision-making and behaviors when facing adverse events. We proposed that CEOs, given their substantial discretion, may strategically time recalls or remain silent to protect their current option wealth, or avoid these IM tactics to pursue their prospective option wealth. Additionally, we have presented evidence that negative media coverage can mitigate these tactics by making CEOs more cautious. These insights provide a foundation for understanding the situational dynamics influencing CEO decision-making under adverse conditions.

Theoretical Contributions

This study offers several contributions to the CEO compensation literature. First, we propose a new mechanism to explain how CEO stock-option incentives influence their decision-making and stakeholder communication during adverse events (e.g., Davidson, Jiraporn, Kim, & Nemec, 2004; Gamache, McNamara, Graffin, Kiley, Haleblian, & Devers, 2019; Quigley, Hubbard, Ward, & Graffin, 2020; Whittington, Yakis-Douglas, & Ahn, 2016). While past research has shown that firm outcomes reflect the influence of upper management (Hambrick, 2007; Hambrick & Mason, 1984), it has not fully explored how option-based incentives shape CEOs’ responses to organizational failures. This gap limits our understanding of how compensation affects CEO behaviors.

More research is needed to understand how CEO-specific factors, such as incentives and biases, influence IM strategies (Devers et al., 2008; Gomez-Mejia, Berrone, & Franco-Santos, 2014; Wiseman & Gomez-Mejia, 1998). For instance, Boiral (2016) highlighted how IM strategies mitigate reputational risks, while Dimitrov and Jain (2011) demonstrated that CEOs with higher at-risk pay are likely to release favorable news ahead of shareholder meetings to manage stakeholder perceptions. Extending this line of inquiry, our findings reveal two distinct effects of stock options on IM tactics: (1) a wealth-preservation effect linked to current option wealth, encouraging the adoption of short-term IM tactics, and (2) a wealth-maximizing effect tied to prospective option wealth, which may reduce reliance on such IM tactics. Whether one effect dominates depends on the relative weight of these incentives in the CEO’s option portfolio. By framing these insights within existing IM and behavioral agency research, we shed new light on the nuanced ways that compensation structures drive CEO decision-making.

Second, our study advances the mixed gamble literature, which has primarily focused on CEO decisions involving strategic risk-taking, such as R&D investments, capital expenditures, and mergers and acquisitions (e.g., DesJardine & Shi, 2021; Martin et al., 2013, 2016). This body of work has not examined the agency consequences of CEO stock options during adverse events, such as product failures. These situations pose unique challenges for CEOs, who must navigate “looming losses” (Kahneman & Tversky, 1979) while making decisions under heightened urgency. This decision-making process is distinct from the evaluation of gains and losses associated with traditional strategic risks, offering a new perspective on the complexities of CEO behaviors facing adverse events.

Third, we contribute to the literature on stakeholder welfare and crisis management (Bundy, Pfarrer, Short, & Coombs, 2017; Freeman, Harrison, & Wicks, 2007), highlighting how CEO IM tactics aimed at protecting or maximizing option wealth can divert attention from stakeholder interests, creating confusion and uncertainty (Desai, 2014). This deviates from the stakeholder-focused frameworks dominating crisis management research, which emphasize proactive and accommodating behaviors toward stakeholders (Bundy et al., 2017; Hersel, 2022). Instead, CEO IM tactics during failures can heighten information asymmetry, undermining stakeholder trust and complicating accountability.

From the perspective of stakeholder agency relations, such tactics lead to agency costs for shareholders, who rely on CEOs to act transparently and in their best interests (e.g., Hill & Jones, 1992; Werder, 2011). Shareholders may make suboptimal decisions because CEOs distort the risks reflected in stock prices, leading to misaligned incentives and inaccurate investment decisions (Davidson et al., 2004). For example, equity-based pay schemes can overcompensate CEOs by failing to account for undisclosed risks (see Bamberger, Homburg, & Wielgos, 2021). These behaviors further demonstrate that markets may not always act as efficient monitors, challenging the assumption that they accurately reflect genuine information (Davis, 2009; Shiller, 2015).

Customers, another critical stakeholder group, face even greater challenges due to heightened information asymmetry and power imbalances (Werder, 2011). They often lack the ability to verify or question firms’ actions during recalls, particularly in such specialized industries as medical devices, where alternatives may be limited or even absent. For example, issuing recalls on Fridays delays public awareness, resulting in serious consequences (Diestre et al., 2020). Similarly, strategic silence in CEO communications prevents consumers from making timely, informed decisions (Iqbal et al., 2024).

Finally, our results speak to the role of the media as a monitor (e.g., Astvansh et al., 2022; Graf-Vlachy et al., 2020; Shoemaker & Reese, 2013). “We live in a mediatized world, and this is also reflected in many if not most of the phenomena we are studying” (Ocasio et al., 2023: 114); therefore, it is crucial to consider media influence. The media plays a key role in shaping public opinion, often acting as society’s watchdog (Graf-Vlachy et al., 2020). It plays “a major role in the allocation of attention in markets by setting the agenda for public discourse” (Petkova et al., 2013: 866). Our results suggest that social control agents, such as the media, may shape CEO IM tactics through negative coverage of the firm.

Practical Implications

This study highlights the critical role of boards and compensation committees in mitigating information asymmetry between CEOs and shareholders and stakeholders. Boards should adopt compensation schemes that align CEO decision-making with the firm’s long-term goals. By emphasizing prospective option wealth, boards can discourage CEOs’ use of short-term IM tactics, particularly in recall scenarios.

Moreover, boards can use negative media coverage to monitor CEO behavior and promote transparency. In the context of medical recalls—our empirical focus—short-term incentives driven by higher levels of current option wealth can have severe consequences for customers, including physical harm or even death. Our findings underscore the importance of monitoring CEOs’ option portfolios, specifically the balance between current and prospective wealth, to ensure that key stakeholders—beyond short-term equity investors—are adequately considered in critical firm decisions.

Policymakers and government watchdogs must remain vigilant against manipulations in product recalls, as exemplified by the Boeing 737 Max crashes. Investigations by the U.S. Congress indicated that Boeing was aware of safety concerns as early as 2012 but withheld this information from the Federal Aviation Administration (Levin, 2020). The U.S. Congressional Committee criticized what it viewed as a corporate culture marked by concealment and deception. Upon taking office in January 2020, CEO Dave Calhoun acknowledged that Boeing needed to restore transparency (Levin, 2020). Experts maintain that the second crash—causing 157 fatalities on an Ethiopian Airlines flight—could have been prevented had Boeing acted more promptly to recall the defective aircraft. 9

At the time of writing, Calhoun had been dismissed, and Boeing was under investigation by the National Transportation Safety Board for manufacturing errors after a door-plug failure on a Boeing 737 during an Alaska Airlines flight in 2024. Calhoun’s successor, Robert Ortberg, continues to face scrutiny as ongoing quality issues threaten the 777X program. Although it is difficult to prove, some contend that executive incentive systems may encourage harmful practices. According to Talton (2022), the victims of these crashes were affected by a corporate culture focused on short-term profits and stock performance. These failures highlight the risks posed by incentive systems that prioritize immediate earnings over broader societal responsibilities. Ensuring executive accountability is thus crucial for fostering a corporate culture focused on transparency and stakeholder welfare rather than self-serving decisions (Haney & Simpson, 2019).

Limitations and Future Research

This study has several limitations that suggest important avenues for future research. One key area is the long-term impact of CEO IM tactics on their careers and firm-performance. For example, do CEOs tend to leave the company after securing their current option wealth, or stay to maximize prospective option wealth? Our analysis focused on the IM tactics CEOs employ in the context of product recalls, leaving open the question of how their IM tactics shape their careers and firms’ long-term performance.

Additionally, Friday recalls in our sample (23%) are not significantly more frequent than recalls on other work days (20%). This raises important questions about the nature of Friday recalls. For instance, do Friday recalls reflect CEOs’ opportunistic behaviors, or do they pose a greater risk to CEO credibility than strategic silence? Given that the Friday effect has been extensively studied across various domains (Dellavigna & Pollet, 2009; Diestre et al., 2020), could it be that some CEOs, aware of its potential consequences, intentionally avoid stakeholder scrutiny by not initiating recalls on Fridays? Exploring these questions could provide valuable insights and extend this body of literature.

Another important direction involves understanding how monitors and shareholders respond to CEOs exploiting their limited attention. Do these stakeholders become more vigilant toward CEO IM tactics, or does information asymmetry continue to benefit CEOs due to their privileged position? Exploring these questions can provide deeper insights into CEO IM tactics and the long-term effectiveness of control mechanisms.

Conclusion

This study examined two IM tactics CEOs use when dealing with product recall communication. Our findings reveal that CEOs may strategically time recalls or remain silent to protect their current option wealth, or avoid these IM tactics to gain from their prospective option wealth. Importantly, we demonstrated that these tactics can be mitigated by media scrutiny, which serves as a potential tool for accountability. By identifying these IM tactics and offering prevention strategies, our research contributes to a deeper understanding of CEO decision-making and provides actionable insights for boards, policymakers, and other stakeholders.

Footnotes

Appendix

CEO Fixed Effects

| Inattentive recall |

Strategic timing |

|

|---|---|---|

| Recall Class 1 | −0.015 | −0.038 |

| (0.817) | (0.010) | |

| Previous Product Recalls | 0.000 | −0.001 |

| (0.313) | (0.000) | |

| R&D Intensity | −0.002 | −0.118 |

| (0.990) | (0.114) | |

| Number of Employees (log-transformed) | 0.032 | 0.015 |

| (0.707) | (0.488) | |

| Market Performance (Tobin’s Q) | 0.091 | −0.064 |

| (0.001) | (0.000) | |

| Financial Distress (Altman’s Z) | −0.006 | 0.024 |

| (0.842) | (0.020) | |

| CEO Total Other Pay | 0.030 | 0.013 |

| (0.473) | (0.414) | |

| CEO Tenure | 0.004 | 0.000 |

| (0.006) | (0.949) | |

| CEO Duality | −0.016 | −0.023 |

| (0.807) | (0.189) | |

| Independent Director Ratio | −0.095 | −0.287 |

| (0.898) | (0.104) | |

| CEO Stock Value (log-transformed) | −0.044 | −0.052 |

| (0.178) | (0.000) | |

| Negative Media Coverage | −0.016 | 0.150 |

| (0.855) | (0.000) | |

| CEO Current Option Wealth | 0.004 | 0.005 |

| (0.053) | (0.003) | |

| CEO Prospective Option Wealth | −0.001 | −0.001 |

| (0.185) | (0.004) | |

| Constant | −0.034 | 1.277 |

| (0.955) | (0.000) | |

| R2 (overall) | 0.02 | 0.05 |

| R2 (within) | 0.04 | 0.013 |

| Observations | 6,609 | 6,609 |

| Year FE | YES | YES |

Note: Robust p values in parentheses. Two-tailed tests.

Acknowledgements

We thank Dr. Chandrika Rathee, Dr. Laura Dupin, Dr. Kevin Curran, Dr. Yuval Engel, Dr. Timothy Quigley, Dr. Abhinav Gupta, and seminar participants at the Amsterdam Business School, Copenhagen Business School, and Madrid Work and Organizations Workshop for friendly feedback on the paper. We also benefited from presenting an earlier version of the paper at the AOM 2020. We thank Action Editor Wei Shi and two anonymous reviewers during the review process; this article benefited tremendously from their constructive and thoughtful comments.