Abstract

Prior research has opposing views about the merits of firm-specific managerial experience, and empirical findings are mixed. To address this problem, we ask when firm-specific managerial experience is helpful versus harmful in pursuit of new growth opportunities. We propose that when CEOs’ firm-specific experience is combined with versatile managerial experiences, its growth-constraining effect is alleviated due to increased adaptability of CEOs' human capital to support growth in new business domains. We find support for this argument in a sample of U.S. food firms and their pursuit of the organic food opportunity during 1997 to 2007. We also find that CEOs’ versatile experience by itself is not sufficient for the pursuit of new growth, but it is when the two types of experience are combined synergistically that firms can achieve higher rates of opportunity pursuit. In this vein, our research reconciles the alternative theoretical perspectives on firm-specific experience and invites further consideration of experience combinations where both positive and negative synergies drive the ultimate impact of key managerial experiences.

Managers and in particular chief executive officers (CEOs) play a key role in determining the growth direction of firms, and their experiences shape how they recognize and capture new growth opportunities (Penrose, 1959). Because achieving path-dependent growth involves leveraging existing resources, it requires firm-specific knowledge of idiosyncratic resources for their proper redeployment to support new growth (Mahoney, 1995; Shamsie & Mannor, 2013). While firm-specific managerial experience helps develop such knowledge, strategic management literature suggests that this experience has both value-adding and value-reducing qualities when it comes to the likelihood of the firm pursuing emerging growth opportunities. On the one hand, resource-based theory suggests that firm-specific managerial experience can serve as a key driver of growth (Crook, Todd, Combs, Woehr & Ketchen, 2011; Penrose, 1959) and a source of competitive advantage (Castanias & Helfat, 2001; Wang, He & Mahoney, 2009) by providing in-depth knowledge of the firm's unique bundle of resources and capabilities for growth. On the other hand, upper-echelons and other management research suggest that due to cognitive entrenchment and lower applicability of their human capital in new growth areas (Barker & Mueller, 2002; Campbell, Coff, & Kryscynski, 2012; Dane, 2010; Morris, Alvarez, Barney, & Molloy, 2017), CEOs with extensive firm-specific experience might be less inclined to venture into uncharted business domains. These CEOs tend to be committed to the status quo (Hambrick, Geletkanycz, & Fredrickson, 1993) and might resist organizational and strategic change (Dane, 2010).

Indeed, strategic management scholars have been inquiring about the merits of firm-specific experience for some time—that is, is firm-specific experience valuable or detrimental to the firm? Competing theories do not provide clear guidance about how to reconcile or utilize these opposing views, and empirical findings are mixed. In our inquiry, we suggest that perhaps researchers might have been asking the wrong research question. The question we should be asking is when firm-specific managerial experience is helpful versus harmful for pursuing growth. Asking this question in the context of firm growth prompted us to consider the other key managerial experiences CEOs accumulate throughout their career because it is the bundle of managerial experiences that is likely to shape the CEOs’ human capital and their perception, ability, and motivation to pursue new growth (Ployhart, Nyberg, Reilly, & Maltarich, 2014).

To address our research question, we draw from Penrose's (1959) theory of the growth of the firm, 1 where achieving growth involves managers’ redeploying fungible productive resources in new ways (Nason & Wiklund, 2018), and this requires managers to provide “versatile type of executive service” (Penrose, 1959: 37). This highlights the importance of versatile managerial human capital, which is human capital that is adaptable to multiple knowledge domains. Here we bring to the foreground the idea that the CEO's versatile professional experiences contribute to the development of managerial human capital that is deployable across a broader range of business terrains. We provide theoretical arguments and empirical examination regarding how versatile experience might assist those CEOs with strong firm-specific knowledge to turn a third-person new growth opportunity (an objective growth opportunity that exists in the market and is supposed to be available to any firm) into first-person opportunity that is subjectively perceived and pursued by the firm (cf. McMullen & Shepherd, 2006).

We test our theory in the context of the U.S. food manufacturing industry during 1997 to 2007, which was presented with the opportunity to introduce organic food products in the face of emerging consumer demand for natural and organic-certified foods. Empirical analysis suggests a negative effect of the CEO's firm-specific experience on opportunity pursuit, which is alleviated when the CEO also has versatile experience. Firms can achieve higher rates of opportunity pursuit when CEOs possess higher levels of both firm-specific and versatile managerial experiences, which endorses their complementarity for achieving path-dependent growth.

We contribute to strategy literature by providing new evidence for the inconclusive research about the merits of firm-specific managerial experience. In particular, the resource-based theory considers firm-specific knowledge as a necessary condition for achieving growth; upper-echelons research points to the limiting effect that firm-specific experience might have on managerial cognition and willingness to act on pursuing growth opportunities. We argue that when CEOs with firm-specific experience also possess versatile experience, their human capital becomes more internally deployable to support growth in new business domains. Versatile experience is likely to broaden the perception of new opportunities and enrich managerial ability of CEOs with in-depth firm knowledge. These CEOs perceive lower risk of failure and are more willing to pursue growth where resource reconfiguration is needed. We find that even though CEOs’ firm-specific experience is negatively linked with the pursuit of a growth opportunity, firms can escape this effect when CEOs also possess versatile experience. In this vein, our findings reconcile the alternative theoretical perspectives on firm-specific experience. Our findings also reveal that CEOs’ versatile experience by itself is not sufficient for the pursuit of new growth. It is when the two types of experience are combined synergistically that firms achieve higher rates of opportunity pursuit. Our research thus invites further consideration of experience combinations where both positive and negative synergies drive the ultimate impact of key managerial experiences.

Theory Development

Achieving path-dependent growth requires managers to recognize and capture new opportunities through utilization and renewal of existing resources and capabilities. In Penrose's (1959) theory of the growth of the firm, resources are fungible in the sense that they can be used for different purposes or in different ways and in combination with other resources. It is the services from the resources that are inputs in the production process, where managers serve as a catalyst in converting resources into services (Mahoney, 1995). Firm growth is achieved when managers render new services from existing resources by utilizing and redeploying them in new ways.

Professional experiences of managers affect productive services obtained from the resources of the firm. Managers interact with the firm, industry, and geographical context to generate a repertoire of general and specialized skills and knowledge that shape their managerial human capital (Adner & Helfat, 2003; Argote & Miron-Spektor, 2011; Becker, 1993). CEOs interpret growth opportunities subjectively through the lenses provided by these experiences (Penrose, 1959) and imagine new services that can be generated from existing resources (Foss, Klein, Kor, & Mahoney, 2008). Experiential knowledge shapes managerial judgment about the importance of specific resources for an opportunity (Denrell, Fang, & Winter, 2003) and managerial capability in reconfiguring, bundling, and mobilizing resources for growth (Helfat et al., 2007; Sirmon, Hitt, & Ireland, 2007).

A particularly important type of experience for CEOs is firm-specific managerial experience, which is the managerial experience that they accumulated in the focal firm prior to becoming CEO. Such experience embeds tacit knowledge about the firm's idiosyncratic bundle of resources and capabilities, weaknesses and vulnerabilities, and the unique opportunities and challenges it faces (Hatch & Dyer, 2004). Because resource and capability development follows a path-dependent pattern (Hitt, Bierman, Uhlenbruck, & Shimizu, 2006), managers’ historic knowledge of the firm contributes to proper matching of the firm's resources with emerging opportunities; thus, a “subjective productive opportunity” set is envisioned by managers through firm-specific lenses (Penrose, 1959). With such knowledge, managers choose the new directions of growth and redefine the opportunity boundaries of a firm (Gruber, MacMillan, & Thompson, 2012).

Firm-specific managerial experience also plays a key role in facilitating the resource and capability conversion and recalibration process during the implementation of growth initiatives (Sirmon & Hitt, 2009; Sirmon, Hitt, Ireland, & Gilbert, 2011). A lack or limited availability of managers with firm-specific experience constrains the rate at which a firm can take advantage of new growth opportunities because such managers “provide services that cannot be provided by personnel newly hired from outside the firm” (Penrose, 1959: 46). The pursuit of a growth opportunity requires managers with firm-specific experience to match people to specific jobs and match people in team settings (Kor, 2003). When a new growth opportunity requires changes, such as reconfiguration and redeployment of resources, CEOs with firm-specific expertise can craft and articulate these decisions with common organizational language (March & Simon, 1958). They also have strong intrafirm social networks to gain loyalty from employees and therefore can mobilize resources to pursue the opportunity (Simsek, 2007).

However, even though experiences in specific contexts enable managers to acquire specialized knowledge and skills (Becker, 1993), upper-echelons and other management research also suggests that a high level of firm specificity in managerial experience can elevate cognitive entrenchment (Dane, 2010) and limit the “search” for strategic alternatives and complementary resources (Cyert & March, 1963; Herrmann & Datta, 2005). Managers develop decision-making heuristics based on their experience, and in-depth experience in a specific firm and industry domain can yield a highly structured (routine-like) set of heuristics for searching for and evaluating homogeneous opportunities (Hodgkinson et al., 2009; Maitland & Sammartino, 2015). Such heuristics might limit the range of new services that CEOs can generate from resources and constrain the perception of growth opportunities to only those that can be pursued with similar solutions and processes (e.g., Gruber, MacMillan, & Thompson, 2013; Kor & Mesko, 2013). Since these CEOs have human capital that is less applicable outside the current industry or geographical boundaries of the firm (Campbell et al., 2012; Morris et al., 2017), they might be reluctant to act upon emerging growth opportunities that require different heuristics and processes to create value (Mishra, 2014).

The empirical evidence on firm-specific experience is mixed. Studies indicate that extended tenure in the firm or industry is negatively associated with internationalization and innovation in dynamic environments (e.g., Herrmann & Datta, 2005; Wu, Levitas, & Priem, 2005), and long-tenured managers can be more reserved in explorative activities and R&D investments (Kor, 2006; Miller & Shamsie, 2001). Finkelstein and Hambrick (1990) find that when managers have long firm tenure, computer and chemical firms are less likely to change their strategy and natural-gas distribution firms are less likely to deviate from rivals’ strategies.

However, research also indicates that well-seasoned CEOs can be more competent and confident in strategic risk-taking (Simsek, 2007). Evidence from the airline industry suggests that as top managers’ experience within the firm increases, a firm tends to be more cautious yet newsworthy (in media) in its competitive actions and more active and faster in its competitive responses (Hambrick, Cho, & Chen, 1996). Research indicates that when a firm pursues a new opportunity that involves adjustment costs (e.g., due to new resource combinations), there is increased demand for firm-specific managerial resources to facilitate knowledge transfer and organizational control (Hutzschenreuter, Voll, & Verbeke, 2011; Tan & Mahoney, 2005).

Given the potential trade-offs associated with firm-specific experience, it is not surprising that strategic changes are often made by introducing managers from outside (e.g., Hambrick et al., 1993; Harris & Helfat, 1997). However, appointment of outside CEOs is often associated with low subsequent firm performance (Shen & Cannella, 2002). Key reasons for low performance include limited transferability of outsider CEOs' skills to focal firm context and the CEOs' lack of firm-specific knowledge (Bailey & Helfat, 2003; Zhang & Rajagopalan, 2010). Indeed, from the perspective of Penrose's (1959) growth theory and the resource-based view, firm-specific human capital is viewed as a necessary condition for identifying and implementing unique, path-dependent growth opportunities (Combs, Ketchen, Ireland, & Webb, 2011; Crook et al., 2011). Therefore, it might be imperative to identify a different type of managerial experience that might mitigate its negative effects while allowing the positive effects to be harnessed.

Versatile Managerial Experience and Its Interactions With Firm-Specific Experience

According to Penrose's (1959) theory of the growth of the firm, versatile managerial human capital is key to achieving firm growth and corporate entrepreneurship. Managerial human capital is versatile when it is internally fungible across multiple knowledge domains such that it can generate a wide range of potential services from a firm's productive resources (Nason & Wiklund, 2018). Managers with versatile human capital have the potential to redeploy resources to generate new services to support growth in new business domains. Penrose notes, There are many examples of firms with vigorous and creative management which have substantially altered their range of products . . . but there are also many examples of other firms which have not been able to make the required adjustments. . . . In such cases, failure to grow is often incorrectly attributed to demand conditions rather than to the limited nature of entrepreneurial resources… A versatile type of executive service is needed if expansion requires major efforts on the part of the firm to develop new markets or entails branching out into new lines of production. Here the imaginative effort, the sense of timing, the instinctive recognition of what will catch on or how to make it catch on become of overwhelming importance. (Penrose, 1959: 36-37; emphasis added)

Versatile experience exposes managers to different knowledge domains and thereby improves the adaptability of their human capital. We propose that CEOs’ versatile experiences can alleviate the negative impacts of the CEOs' firm-specific experience while allowing the benefits to be harnessed. Specifically, when an entrepreneur or manager is faced with an opportunity, uncertainty can act as a barrier against opportunity recognition and entrepreneurial action. Taking the form of doubt, uncertainty can undermine the actor's “beliefs regarding (1) whether an environmental stimulus presents an opportunity for someone in the marketplace, (2) whether this opportunity could feasibly be enacted by the actor, and (3) whether successful exploitation of the opportunity would adequately fulfill some personal desire” (McMullen & Shepherd, 2006: 133). Before a third-person opportunity (i.e., objective growth opportunity that exists in the market and is available to any firm) can be recognized as a first-person opportunity (i.e., opportunity that is subjectively perceived and pursued by the firm), top management needs to believe that the firm has the relevant capabilities to pursue the opportunity, and this includes their own managerial capabilities (McMullen & Shepherd, 2006).

We propose that versatile human capital can reduce CEOs’ uncertainty about a third-person growth opportunity and thus facilitates the conversion of the third-person opportunity into a first-person opportunity. Such uncertainty is especially higher for CEOs with significant firm-specific experience who suffer from limited redeployability of their human capital in new business areas (Nason & Wiklund, 2018). Because they perceive higher risk of failure where their skills and experience-driven heuristics are less relevant, they are less likely to support growth initiatives outside of their area of expertise (Maitland & Sammartino, 2015; Mishra, 2014). A heightened perception of uncertainty by such CEOs can fuel hesitancy, indecisiveness, and procrastination, resulting in missed entrepreneurial opportunities (McMullen & Shepherd, 2006). Yet, when these CEOs also possess versatile experience, their approach to new growth opportunities will be different in three ways.

First, CEOs who also have versatile experience are more likely to recognize an environmental stimulus as a subjective (first-person) growth opportunity. Versatile experience exposes managers to different business domains and expands their cognitive repertoire and information-processing capabilities (Mueller, Georgakakis, Greve, Peck, & Ruigrok, 2021). With both firm-specific and versatile experiences, these CEOs develop a more sophisticated portfolio of heuristics for selecting and capturing opportunities (Bingham & Eisenhardt, 2011) and can better interpret new information under uncertainty (Crossland, Zyung, Hiller, & Hambrick, 2014; Gruber et al., 2012). When they can better recognize the value of the firm's existing resources and capabilities beyond current uses (Nason & Wiklund, 2018), CEOs will be less restrictive in perceiving and considering opportunities that emerge, and their firms’ growth directions will include a broadened view with healthy variations of path-dependent growth. With in-depth knowledge of the firm's unique set of resources and an expanded subjective growth opportunity set, CEOs can apply their superior entrepreneurial judgment to select the best path-dependent growth directions for their firms.

Second, versatile experiences improve the ability of CEOs with substantial firm-specific experience to enact the subjectively perceived growth opportunities. Implementing growth strategies involves generating new services from existing resources by deploying them and combining them with complementary external resources in new ways. Versatile experiences enable the CEOs to draw from a richer (pluralistic) chest of ideas, methodologies, and solutions when pursuing new initiatives (Kor & Mesko, 2013). These CEOs are more resourceful in devising ways to leverage, mobilize, and reconfigure resources to execute the opportunity (Helfat et al., 2007; Teece, 2007). They also benefit from a more diverse advisory network that provides complementary resources to expand into new businesses (Geletkanycz & Hambrick, 1997).

Third, versatile experience improves the willingness of CEOs with substantial firm-specific experiences to engage entrepreneurial actions. CEOs with substantial firm-specific experience are likely to perceive higher failure rates and hence be less interested in venturing new business areas (Mishra, 2014). Versatile experience enhances the adaptability of managerial skills and heuristics in new business contexts (Bingham & Eisenhardt, 2011) and thus reduces their perceived risk of failure. When their human capital is more relevant and applicable during leveraging, reconfiguration, and redeployment of resources and capabilities in new markets (Sirmon, Hitt, & Ireland, 2007), CEOs are less entrenched in the current business domain and more likely to be open to new experiences (McCrae & Costa, 1997).

While CEOs’ versatile experience alleviates the negative impacts of firm-specific experience, CEOs’ firm-specific experience in return complements versatile human capital. Firm-specific experience provides CEOs a guiding lens through which they can make better use of their versatile human capital in identifying and enacting new path-dependent growth opportunities. With an in-depth knowledge of the firms’ unique set of resources, they can develop better managerial judgment for planning and implementing a new growth initiative through resource reconfiguration and mobilization (Penrose, 1959: 8). These CEOs have improved insight about how to combine existing and new resources, consider the firm's interdependencies with its key constituents, and identify new demands on the employees and business partners due to growth (Mosakowski, 1997; Sirmon & Hitt, 2009). They can achieve more effective implementation because they speak the organizational language and are empowered by internal social capital and rapport with stakeholders (Kor, 2003; Simsek, 2007).

Essentially, the combination of firm-specific and versatile experiences is what enables “cognitive versatility” (Hodgkinson et al., 2009: 288) for CEOs where they have an in-depth understanding of the firm's resource and competency base and also a “big picture” of other domain opportunities to pursue. It is the co-presence and interplay of these two types of experiences that facilitate novel managerial intuition (or bisociation) to emerge (Hodgkinson et al., 2009) concerning which resources, heuristics, and processes to utilize for opportunity pursuit. This interaction enhances CEOs’ (dynamic) managerial capabilities for searching, evaluating, and capturing opportunities (Bingham & Eisenhardt, 2011; Maitland & Sammartino, 2015).

Versatile experience involves multidimensionality due to exposure to distinct knowledge domains as part of managerial experience in different industries, geographies, and business functions. Thus, we consider three types of versatile experience. First, managerial experience in related industries can be an important type of versatile experience that helps to improve the adaptability of CEOs’ human capital. CEOs’ related-industry experience allows managers to acquire knowledge of the strategies, technology, competition, and value-chain practices in related industries. Related industry practices are likely to have a mix of similar and dissimilar elements. With some commonality between the focal and related industries, insights and skills gained from the experience can be feasibly adapted to current or other related business settings (Bailey & Helfat, 2003; Farjoun, 1998). Related industries also exhibit some different attributes in industry conditions and require strategies different from those in the current industry. These differences introduce novelty that can broaden the CEOs’ imaginative capacity and repertoire of skills and heuristics (Gruber et al., 2013).

For CEOs with significant firm-specific knowledge, their experience in related industries reduces their uncertainty toward a (third-person) entrepreneurial opportunity because they can better recognize the value of the firm's existing resources in new and related business areas. Such experiences also provide CEOs with a richer (yet transferable) skill set that could be combined with their firm-specific experience in generating new services from existing resources of the firm. Therefore, once an opportunity is perceived, CEOs’ capabilities and willingness to engage in capturing the opportunity are improved. When CEOs’ experiences in related industries neutralize the negative effects of firm-specific experience, the CEOs can access, synthesize, and utilize the complementary knowledge and social capital benefits of both experiences for opportunity pursuit.

CEOs' versatile experience in the form of CEO related-industry experience will have a positive interaction with CEO firm-specific experience that results in higher rates of opportunity pursuit.

Second, we propose that CEOs’ international experience can contribute to adaptability of their human capital and thus can be a form of versatile experience. International experience exposes managers to a novel knowledge domain about business practices and trends around the globe (Carpenter, Sanders, & Gregersen, 2001). Managers learn to be more sensitive to similarities and dissimilarities in cultural, economic, and legal environments (McCauley, Ruderman, Ohlott, & Morrow, 1994) and become more skillful in accommodating variations in customer preferences, supply chains, marketing, and distribution systems (Tan & Mahoney, 2005). Adapting to foreign conditions triggers the reconfiguration of resources and capabilities to achieve fit with external conditions. Unusual resource combinations witnessed in international markets prepare CEOs to imagine new resource configurations and improve their ability to devise new business models in new business terrains (Herrmann & Datta, 2005). In addition, international expansion involves engaging a complete set of entrepreneurial activities, including creating products and/or supply chains and distribution channels that often are entirely different from domestic businesses (Carpenter et al., 2001; Carpenter, Geletkanycz, & Sanders, 2004). Such experiences boost the ability of the CEOs in resource reconfiguration and orchestration and are likely to reduce the CEOs’ perceived risk of failure in opportunity pursuit.

CEOs’ international experience also complements their firm-specific experience by improving CEOs’ entrepreneurial alertness. Internationalization, which has been considered as full of risk and uncertainty (Liesch, Welch, & Buckley, 2011), can train managers to make decisions under uncertainty. Expanding in new geographical markets enables managers to develop expertise in evaluating and capturing opportunities (Bingham & Eisenhardt, 2011). CEOs become skilled at assessing which heuristics and processes from their repertoire apply in the new market and quickly decide what to keep, drop, or modify as needed. Consequently, these CEOs perceive less risk and are more skillful in enacting a third-person growth opportunity that exists in the market and converting it into a subjectively perceived (first-person) growth opportunity for the firm.

CEOs' versatile experience in the form of CEO international experience will have a positive interaction with CEO firm-specific experience that results in higher rates of opportunity pursuit.

Third, CEOs’ managerial experience in multiple functions (e.g., finance, marketing, operations) can also contribute to their versatile human capital. Such CEOs are exposed to different knowledge domains instead of being specialized in one function. In making decisions, these CEOs can use a broader framework for decision-making and consider the whole business (Finkelstein, Hambrick, & Cannella, 2009; Hitt & Tyler, 1991). They can better predict how an emerging opportunity might influence the firm from multiple functional angles and envision how to adapt the existing capabilities (Beck & Wiersema, 2013; Cannella, Park, & Lee, 2008). Experience in different functions also expands the cognitive repertoire of the managers, which could improve their ability to process information. These CEOs can utilize multiple lenses when they are screening external stimuli, and thus they are less restricted by their in-depth firm knowledge and have greater entrepreneurial alertness in recognizing new opportunities.

In addition, for CEOs highly embedded in their firms, multifunction experience complements their firm-specific knowledge by enhancing their abilities and willingness to engage new entrepreneurial actions. Given that expanding in new business terrains involves reconfiguring at least part of the value-creating activities, CEOs with multifunction experience can use a broader framework of strategic thinking and provide more comprehensive and integrative solutions that make the best use of the firm's resources and capabilities. These CEOs also have a more diverse advisory network (Bunderson, 2003) that helps them access and mobilize a wider set of resources. With bolstered managerial ability to implement new growth, CEOs are likely to feel more competent and confident when considering a growth opportunity. In sum, CEOs’ multifunction experience enhances entrepreneurial alertness and resourcefulness of CEOs with in-depth firm knowledge and puts their entrepreneurial judgment (deciding whether and how to pursue the opportunity) to better use.

CEO's versatile experience in the form of CEO multifunction experience will have a positive interaction with CEO firm-specific experience that results in higher rates of opportunity pursuit.

Method

Data and Sample

It is important to test our theory in a context where managerial decisions involve making investments under uncertainty such that managerial awareness of the (uncertain) growth opportunity and managerial ability to mobilize internal and external resources for growth matter most. We consider the U.S. organic food segment during the period between 1997 and 2007 as a suitable empirical context where we examine publicly traded U.S. food manufacturing firms and their responses to the emerging organic-food-market opportunity. Firms responded to the opportunity through ownership-based acquisitions and greenfield investments.

In the past few decades, there has been growing interest in the consumption of organic produce and food that are free of toxins, artificial additives and preservatives, and pesticides. New legislation was created in the United States to distinguish between genuine organic products and other food products. Specifically, the Organic Food Product Act was published in the Federal Register in 1997 and enacted in 2002. We consider the Organic Food Product Act as an important signal of an emerging growth opportunity for food firms. Accordingly, our data set starts in 1997 and spans 11 years to 2007, which is 5 years after the law was enacted. During this time, the organic food segment was still emerging such that the decision to pursue the growth opportunity was made under great uncertainty. In terms of demand uncertainty, the U.S. organic food contributed to a tiny portion of total food market share for the entire study period (only 0.8% market share in 1997 and less than 3% as of 2007). 2 This constitutes a small niche, but a strong growth trajectory suggests that it could one day become an important segment. 3

The pursuit of the organic food opportunity also comes with several challenges. Organic food production involves a difficult and lengthy transition from conventional agriculture and food systems to organic farming and production. Given insufficient availability or supply of raw organic foods at a large scale, organic food production might require food firms to invest in development of organic supply chains and work closely with existing organic farms. Food firms cited the shortage of organic raw materials and financial risks with organic production as major constraints to growth in the organic food market (Wolf, 2006). Even though organic food products are usually sold at a premium, profit margins vary by individual products and are based on the overall efficiency of specific organic farms. Thus, organic food represents a growth opportunity that carries implementation risk and outcome uncertainty. 4

We focus on U.S. publicly traded food manufacturing firms, which enables access to financial and other information about them. We included all food firms operating in the Standard Industrial Classification (SIC) 20 food and kindred products industry except those that are producing malt beverages, wines, liquors, carbonated beverages, and water. This resulted in a longitudinal sample of 421 observations from 46 food manufacturing firms. Our data for acquisitions came from the Securities Data Company (SDC) database, which is a comprehensive source of corporate acquisitions. Organic food acquisitions constitute only a small percentage of the total acquisitions made by food firms. To identify organic food acquisitions, we went through all of the acquisitions of food firms listed in SDC, researched each transaction, the target firm and its products, and news coverage about the acquisition to find out whether organic products were a driver of the acquisition. This tedious process enabled us to identify 26 organic acquisitions out of 1,514 acquisitions made by food firms. We also searched the LexisNexis database, the Factiva database, and company websites to identify an additional two acquisitions that were not captured by the SDC database. In addition, 31 greenfield investments were identified through Factiva and LexisNexis databases based on news coverage in various business newspapers and magazines. We verified from company websites that the firm offered a U.S. Department of Agriculture organic certified product.

We hand-collected data about the CEOs’ biographical information and experience from annual reports and proxy statements. Our sample includes both large and small food manufacturing firms (capturing the population of publicly traded U.S. food firms). For small firms, availability of data for the upper-level executives was very limited. Even for large firms, data were not systematically available. This was a key reason why we focused on the CEO, whose biographical information was systematically reported for the full range of food firms regardless of their size. Data on firm size and performance, product scope, and internationalization were gathered from the Compustat database. Data on firm age were individually collected from company websites and historical information.

Dependent Variable

The dependent variable is opportunity pursuit. In measuring opportunity pursuit, we considered both initial entry and subsequent expansion firms made through acquisitions and greenfield investments in the emerging organic food segment during 1997 to 2007. This is consistent with the empirical treatment in growth research, where a firm is considered as responding to a growth opportunity when it enters a market or expands in it through a greenfield investment and/or an acquisition (Hennart & Larimo, 1998; Meyer, Estrin, Bhaumik, & Peng, 2009; Tan, Su, Mahoney, & Kor, 2020). 5

The variable takes the value of 1 if in a given year the firm made an initial entry or sequential expansion in the segment through a wholly owned acquisition or greenfield investment. Of the 46 food manufacturing firms that we studied for the period 1997 to 2007 (with a total of 421 firm-year observations), 41% (19 firms) responded to the organic opportunity while 59% (27 firms) did not. Given a discrete dependent variable, we utilized random-effects logistic regression to analyze the opportunity pursuit in the organic food market.

Independent Variables

We captured the entire managerial career of the CEOs, including all of the managerial positions they held. Prior studies of CEOs often captured only a fraction of their managerial experience (e.g., the most recent 5 years), which resulted in significant omission of the accumulation of experience and gave a curtailed picture of experience profile. Our data collection approach addresses this important weakness.

CEO Firm-Specific Experience

We measure CEO firm-specific experience as the CEO's total number of years of managerial experience (tenure) in the focal firm. Duration of the experience can be seen as a proxy for the number of times specialized tasks have been performed, and such performance enhances the proficiency of skills (Tesluk & Jacobs, 1998) and accumulation of human capital (Adner & Helfat, 2003). We focus on managerial experience because it involves a higher level of responsibility (McCauley et al., 1994).

CEO Versatile Managerial Experience

Three kinds of versatile managerial experience are captured in the following way. First, CEO related-industry experience is calculated as the total years of prior managerial experience the CEO had in industries related to the food industry. Related industries include the industries that are vertically or horizontally related to the food manufacturing industry. Vertically related industries include agriculture industries and food retail and wholesale industries (SIC 100, 200, 700, 5140, 5150, 5400). We included them because the knowledge of upstream and downstream industries can help the CEO better envision how the opportunity can be successfully pursued and how to make the essential changes in the supply chain and distribution for organic food production and marketing. Horizontally, the beverage industry (SIC 208) and the personal-care products industry (SIC 2840) both have similar and dissimilar features as the food industry, allowing CEOs to develop transferable but different experience. Also, there has been increased consumer interest in personal-care products (e.g., skin care, hair care, and cosmetics products) that are safe and organic. 6 Second, CEO international experience is measured as the number of years of prior experience in managing international markets (Carpenter et al., 2001; Herrmann & Datta, 2002). Third, CEO multifunction experience refers to the number of functions in which the CEO had managerial-level experience. In measuring this variable, we coded functional experience in administration, finance, marketing, manufacturing and operations, human resources, and other areas (Finkelstein et al., 2009). Given that all CEOs have administration experience, only additional functional experiences count toward the multiple-function experience variable. We required a minimum of 3 years of experience for a particular functional expertise to be developed, either in a single appointment or cumulatively over time. 7 We summed the number of functions where the CEO has 3 years or more of managerial experience as an indicator of this variable.

Control Variables

We control for CEO age and its squared value because a manager's willingness to invest in risky initiatives might decline with age (Barker & Mueller, 2002). We controlled for CEO change (a dummy variable that takes the value of 1 when there is a change) because new initiatives might be introduced by a new CEO. We control for firm size (i.e., the logarithm of total assets) given that the economies of scale a firm enjoys might facilitate its opportunity pursuit. Firm age is controlled as a proxy for firm-level entrenchment in certain strategies and business logics and recipes. We control for return on assets (ROA) because the profitability of the firm can influence its opportunity pursuit.

We also control for corporate governance variables. CEO duality and outsider directors ratio are controlled for as indicators of board leadership structure and board independence. CEO duality takes the value of 1 when the CEO is also the chair of the board of directors. Outsiders ratio is calculated as the percentage of nonexecutive directors on the board. To control for CEO's ownership, board directors’ and executives’ ownership, and block ownership, we calculated ownership as the percentage of company stock owned by the CEO, directors and executives, and block owners, respectively. Block owners are defined as individuals or institutions that own 5% or more of the outstanding company common stock.

Lines of business captures the industry scope of the firm. With each additional industry, the diversity of the firm's resources increases. This variable is calculated as the number of four-digit SIC industries in which the firm operates. Foreign sales ratio captures the international scope of the firm and is calculated as the percentage of sales generated from foreign markets.

Furthermore, we control for a firm's prior experience in organic food market, organic food experience, measured by the firm's cumulative number of prior acquisitions and greenfield investments in this market. We also control with a dummy variable whether the firm is making a healthy food market entry or expansion in that year (healthy food entry/expansion). Healthy food products are designed to reduce some of the potential harmful effects of high salt, high saturated fat and/or transfat content, and artificial ingredients and additives. These products are not subject to regulations but might still appeal to health-conscious buyers. Finally, we control for year (time) effects with yearly dummies, leaving out the 1st year of data (1997).

Results

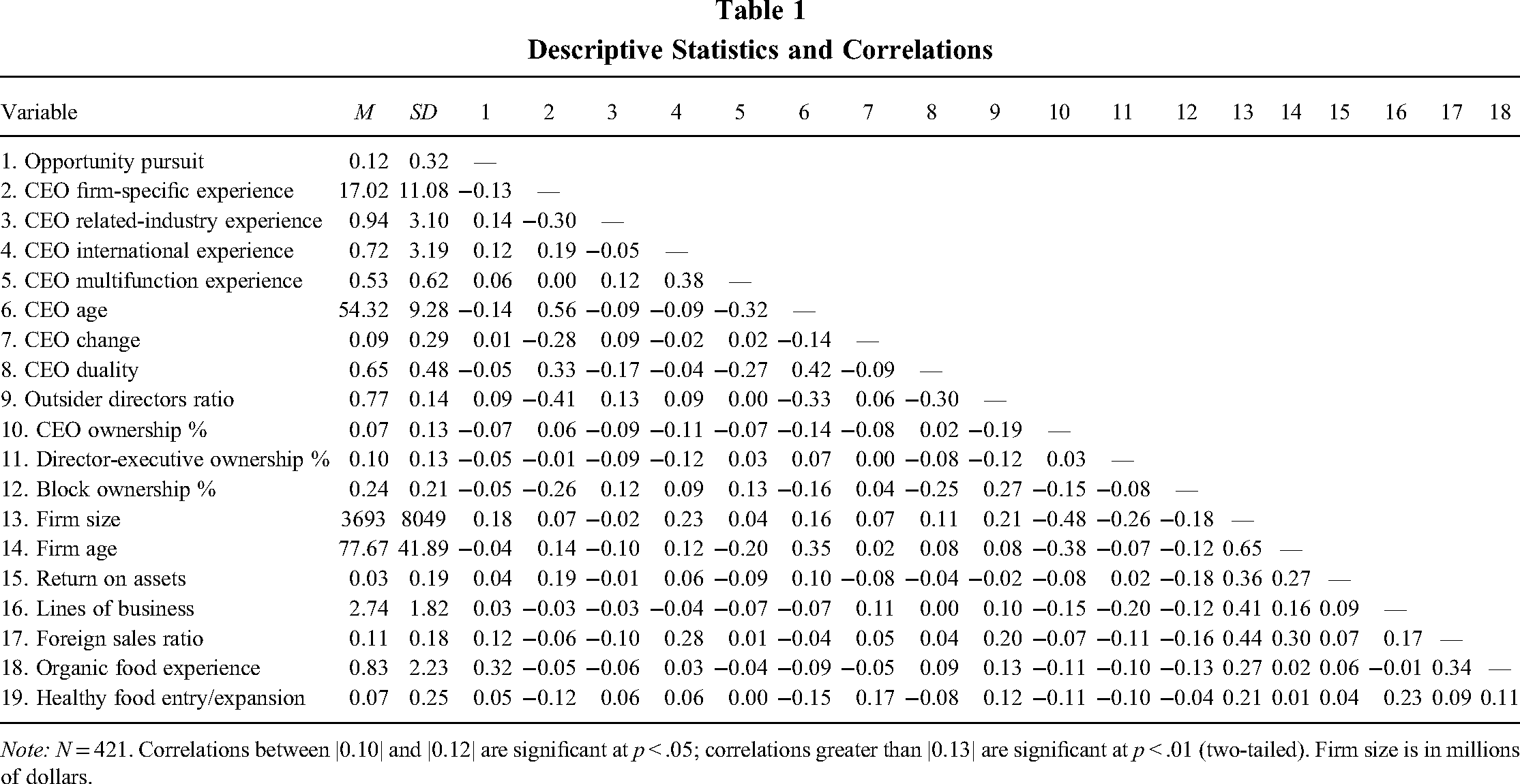

Table 1 shows descriptive statistics and correlations. Of the year-firm observations in our data, 11.64% (49 out of 421) involve opportunity pursuit. Some of the predictor variables are moderately correlated. CEOs with greater firm-specific experience tend to be older (r = .56), have less related-industry experience (r = −.30), but have more international experience (r = .19). CEOs with greater multifunction experience are younger (r = −.32), work in younger firms (r = –.20), and have more international experience (r = .38).

Descriptive Statistics and Correlations

Note: N = 421. Correlations between |0.10| and |0.12| are significant at p < .05; correlations greater than |0.13| are significant at p < .01 (two-tailed). Firm size is in millions of dollars.

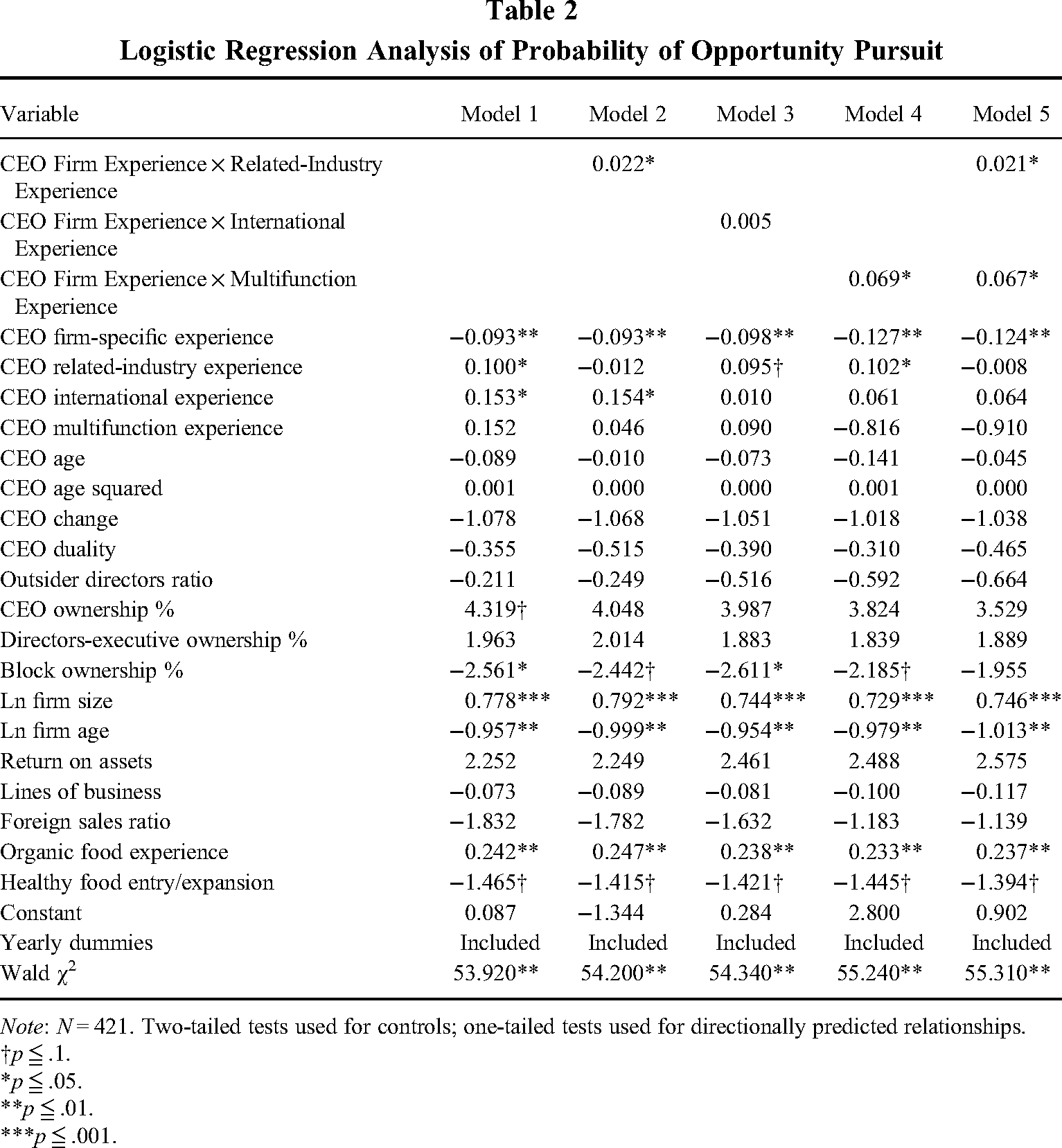

Table 2 reports the results of hypotheses testing. One-tailed tests are used to test directional hypotheses, and two-tailed tests are used in the explorative analysis (Tiwana, 2008). Model 1 includes only control variables. In terms of CEO experiences, CEO firm-specific experience is negatively linked to opportunity pursuit (β = −0.093, p = .008). CEO related-industry and international experiences are positively associated with opportunity pursuit (β = 0.100, p = .047; β = 0.153, p = .033). For firm-level control variables, older firms and firms with greater block ownership are less likely to pursue the opportunity (β = −0.957, p = .006; β = −2.561, p = .05). In contrast, larger firms are more likely to pursue the opportunity (β = 0.778, p = .000). Finally, a firm's organic food experience (β = 0.242, p = .002) is positively linked with opportunity pursuit.

Logistic Regression Analysis of Probability of Opportunity Pursuit

Note: N = 421. Two-tailed tests used for controls; one-tailed tests used for directionally predicted relationships.

†p ≦ .1.

*p ≦ .05.

**p ≦ .01.

***p ≦ .001.

Hypotheses1, 2, and 3 predict positive interactive effects of CEOs’ versatile experiences and firm-specific experience on opportunity pursuit, and they are tested in Models 2 through 5. Model 2 includes the interaction term between CEO firm-specific experience and CEO related-industry experience. The coefficient for the interaction term is positive and significant (β = 0.022, p = .038), supporting Hypothesis 1. Regarding the size of the effect, for a CEO without any related-industry experience, an increase in CEO firm-specific experience from 6 to 17 years (one standard deviation) decreases opportunity pursuit by 5.5 percentage points (or 61.7%), whereas for a CEO with 4 years of related-industry experience (which is mean plus one standard deviation), this decrease will be only 0.7 percentage points (or 0.05%). When the CEO has 5 years of related-industry experience, the increase in CEO firm-specific experience will increase, rather than decrease, opportunity pursuit by 2.4 percentage points.

Model 3 enters the interaction term between CEO firm-specific experience and CEO international experience. The coefficient for the interaction term is positive but not significant (β = 0.005, p = .227). The interaction term is highly correlated with CEO international experience (r = 0.975), and the variance inflation factor value for the interaction term (24.62) is above the maximum acceptance level of 10. Thus, the lack of significance for Hypothesis 2 might be due to collinearity (Hair, Black, Babin, & Anderson, 2010; Sheather, 2009).

Model 4 enters the interaction term between CEO firm-specific experience and CEO multifunction experience. The interaction term is positive and significant (β = 0.069, p = .038), which supports Hypothesis 3. Regarding the size of the effect, for a CEO without any multifunction experience, an increase in CEO firm-specific experience from 6 to 17 years (one standard deviation) decreases opportunity pursuit by 8.3 percentage points (or 72.8%), whereas for a CEO with one multifunction, this decrease will be more than halved (3.6 percentage points, or 44.6%). When a CEO has two multifunctions, the rise in firm-specific experience will increase, rather than decrease, opportunity pursuit by 0.75 percentage points.

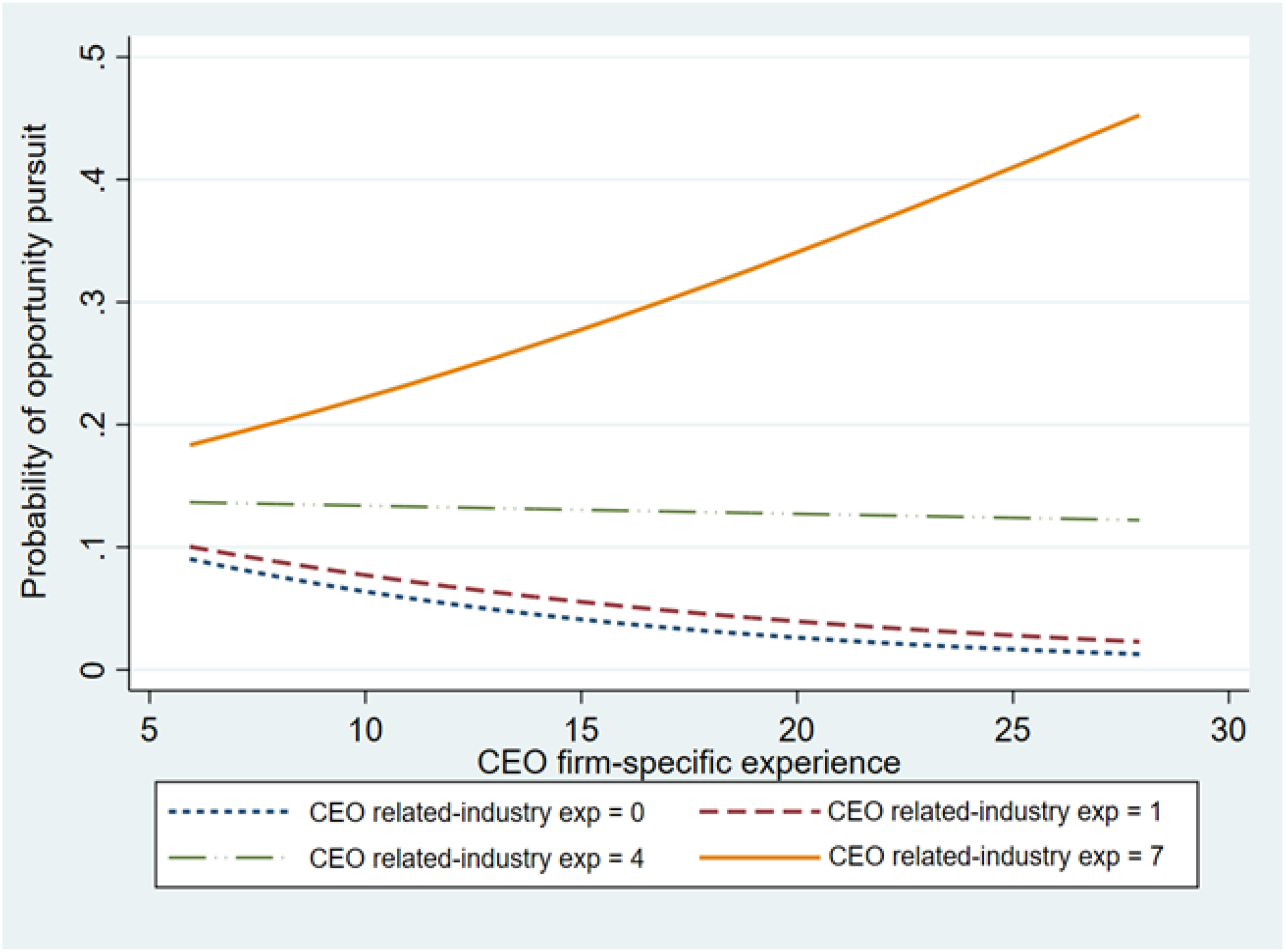

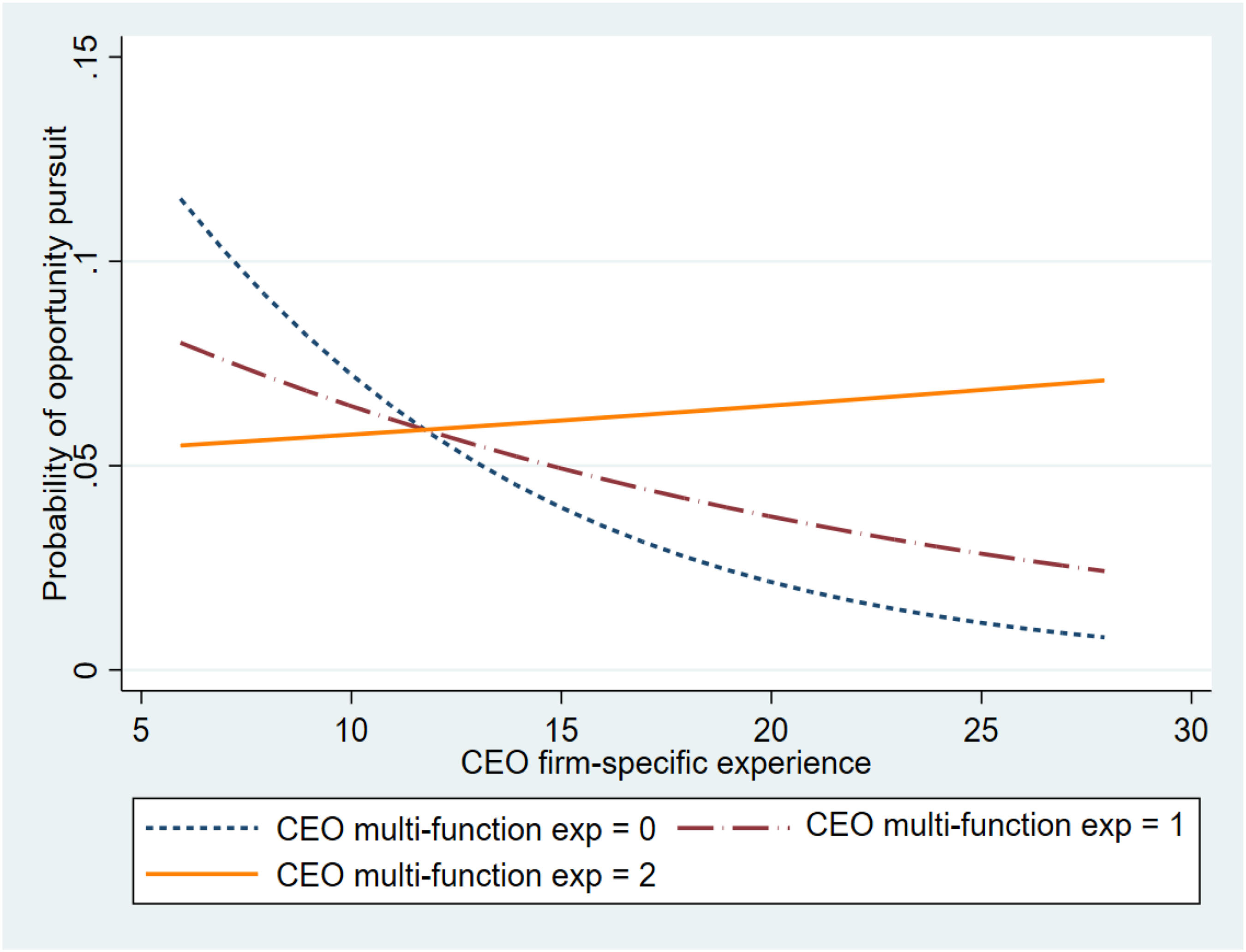

Model 5 includes the two statistically supported interactions simultaneously. We found that both interactions are significant at p < .05 (β = 0.021, p = .046, and β = 0.067, p = .045 respectively), which is consistent with our findings in Models 2 and 4. In order to confirm whether the estimated coefficients capture the direction and magnitude of the interaction effects (Ai & Norton, 2003; Kolasinski & Siegel, 2010), we illustrate the interaction effects in Figures 1 and 2. These figures are revealing. Figure 1 indicates that when a CEO has 0 or 1 year of related-industry experience, CEO firm-specific managerial tenure is negatively linked to opportunity pursuit. When CEO related-industry experience reaches 4 years (mean plus one standard deviation), the relationship between CEO firm-specific experience and opportunity pursuit becomes flattened. When the CEO has at least 5 years of related-industry experience, firm-specific experience has a positive impact on opportunity pursuit. CEOs with at least 5 years of this experience made up 6.65% of our observations. Likewise, Figure 2 shows that CEO firm-specific experience has a negative effect on opportunity pursuit when the CEO has limited multifunction experience (zero or one additional function). This negative effect is transformed into a positive effect when the CEO has two types of functional experience (which represents 6.41% of our observations).

Interaction Effect of CEO Related-Industry Experience and CEO Firm-Specific Experience

Interaction Effect of CEO Multifunction Experience and CEO Firm-Specific Experience

Sensitivity Checks

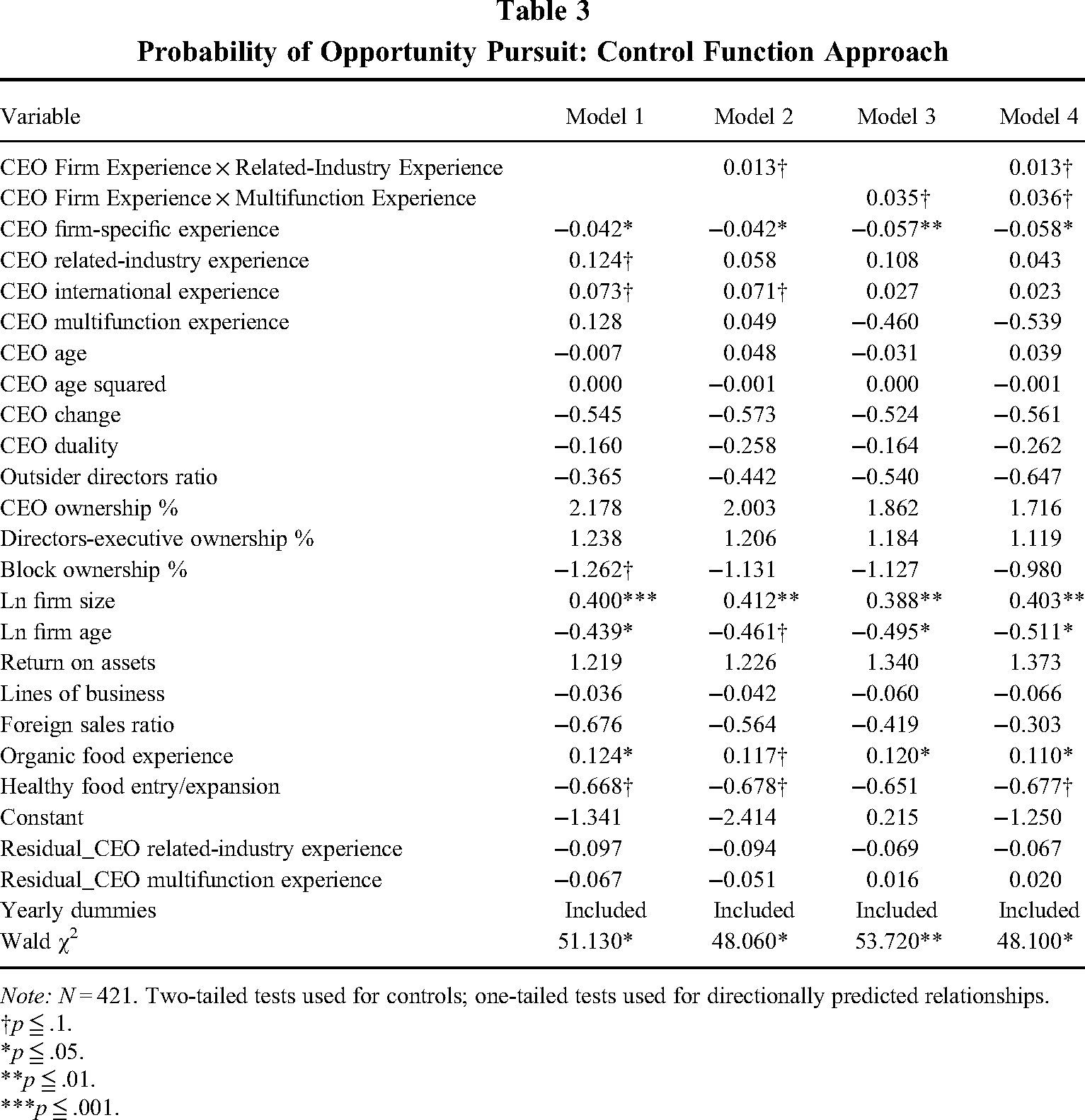

As with most strategy research, we considered the issue of potential endogeneity, which occurs when independent variables, such as CEO human-capital variables, are potentially choice variables that correlate with unobserved variables (Greene, 2000). In our context, innovative and forward-thinking boards might hire or promote CEOs with versatile experience to pursue growth opportunities. In these cases, it is such boards that influence both CEO versatile experience and opportunity pursuit. Most likely, this potential endogeneity issue should not create serious concerns, because all of our hypotheses are concerned with interaction effects. Research has shown that the estimated coefficient of an interaction effect is still consistent even when one variable is endogenous (Bun & Harrison, 2019; Nizalova & Murtazashvili, 2016). Despite this, we used the control function approach (Rivers & Vuong, 1988; Wooldridge, 2015) to examine whether the two statistically significant interaction effects in Table 2 are still supported after controlling for potentially endogenous versatile experiences. The concept of the control function approach originates from Heckman (1979) and Hausman (1978) and is implemented in two steps. First, we regress each suspected endogenous variable on a set of exogenous variables and one instrumental variable (IV). We then enter the residuals from the first-stage regression into estimation of opportunity pursuit. The residuals from the first-stage regression serve as the Hausman test, where the lack of significance of the residuals suggests the absence of endogeneity (Wooldridge, 2015). The control function approach does not need to specify an additional first-stage equation for the interaction term and therefore provides a straightforward way to account for interaction terms that involve endogenous variables (Wooldridge, 2015). In the first-stage regression for CEO related-industry experience, we employed CEO tenure in nonfood businesses as an instrument. This instrument is likely to be a good predictor (r = .587, p < .000) because a CEO's related-industry experience constitutes part of his or her tenure in nonfood businesses. Comparison between R-squares for the first-stage regression with and without CEO tenure in nonfood businesses shows that the instrument is indeed relevant to CEO related-industry experience (F = 212.07, p < .000). Regarding the condition for exclusion restriction, we expect that CEO tenure in nonfood businesses affects opportunity pursuit only through CEO related-industry experience; thus, the IV is unlikely to be correlated with the error term of the second-stage estimation. Next, in terms of the instrument for CEO multifunction experience, we used CEO's total number of prior managerial positions with the logic that the greater the CEO's number of managerial positions, the more likely these positions vary across different functions. Indeed, these two variables are highly correlated (r = .39, p < .000), and comparison between R-squares for the first-stage regression with and without the IV shows that this IV is relevant to CEO multifunction experience (F = 58.96, p < .000). Similarly, we expect that the IV is not likely to be correlated with the error term of the second-stage estimation.

The results of the second-step regressions are reported in Table 3. The lack of significance in both residual terms across all models suggests that endogeneity is not an issue for either CEO related-industry experience or CEO multifunction experience. Model 2 shows that the coefficient of the interaction term between CEO firm-specific experience and CEO related-industry experience is positive and significant at p < .1 level (β = 0.013, p = .06). Model 3 indicates that the coefficient of the interaction term between CEO firm-specific experience and CEO multifunction experience is also positive and significant at p < .1 level (β = 0.035, p = .055). Thus, results regarding the interaction effects (i.e., Hypotheses 1 and 3) are robust when we accounted for potential endogeneity.

Probability of Opportunity Pursuit: Control Function Approach

Note: N = 421. Two-tailed tests used for controls; one-tailed tests used for directionally predicted relationships.

†p ≦ .1.

*p ≦ .05.

**p ≦ .01.

***p ≦ .001.

Our analysis focuses on the firm's opportunity pursuit during the study period (1997-2007), but one may inquire about the speed with which firms made the first response to the opportunity. Even though the speed of response involves other theoretical considerations (e.g., Schoenecker & Cooper, 1998) that are beyond the scope of the current study, we conducted a post hoc event history analysis. We found that CEO international experience is weakly associated with early response (p = .093), while CEO firm-specific experience is associated with late response (p = .042). Also, the interaction of CEO firm-specific experience and versatile experience in the form of multifunction experience promotes early response (p = .036). These are largely consistent with our findings. The hazard model suggests that combination of CEO firm-specific experience and multifunction experience promotes the speed of first response, whereas our main analysis shows that interactions of CEO firm-specific experience with CEO related-industry experience and multifunction experience are more prominent in facilitating opportunity pursuit throughout the study period.

Our results show healthy-food-segment entry or expansion is weakly associated with the pursuit of organic growth opportunity (β = −1.465, p = .052), which implies this expansion might be a substitutive response to increasing demand for organic food. When we replicated the estimation with healthy foods entry or expansion (as a choice variable), we found that the models (both main and interaction effects) have poor prediction powers. Given that introducing healthy foods requires minor changes in production and distribution systems, it involves less investment and lower risk. Therefore, decisions leading to healthy-foods-segment expansion are likely to be influenced by a different set of factors from decisions to pursue the organic-food opportunity.

Our theory draws from Penrose’s (1959) theory of the growth of the firm and assumes that firms pursue profitable growth. But is opportunity pursuit in the organic food segment a profitable one? We performed a post hoc analysis to see whether opportunity pursuit generates shareholder value by examining the stock market reactions to the organic food acquisitions that took place in our sample. We were able to collect stock returns data on 26 organic food acquisitions from the Event Study of the Wharton Research Data Services database. The mean cumulative abnormal return based on the standard and shorter 3-day windows (which include the announcement day and 1 day before and after the announcement day) for these acquisitions is 2.95%, which is positive and significantly greater than zero (t = 2.48, p = .047). 8 We also performed an additional post hoc analysis by examining how opportunity pursuit affects the overall ROA and sales growth of the U.S. food firms. Given that a pursuit in the organic food segment might take years to generate profit, our key explanatory variable is the accumulated number of organic food pursuits at time t – 1. To control for other growth directions, we included the accumulated number of healthy-food pursuits, as well as the accumulated number of food acquisitions and unrelated acquisitions, along with other variables. Our findings show that accumulated number of organic food pursuits is positively associated with ROA and sales growth (p = .095 and p = .035, respectively), while accumulated numbers of healthy-food pursuits and of food acquisitions are negatively associated with sales growth (p = .018 and p = .041). Thus, opportunity pursuit in the organic food segment results in greater profitability and higher sales growth during our study period.

Finally, our study period covers an 11-year span. To see whether there was a pattern change in the impact of CEO experiences, we created a period dummy that separates our study period into early (1997-2002) and later (2003-2007) periods, where 2002 was the year when the Organic Food Product Act was enacted. We created new interaction terms by multiplying this period dummy with each of the CEO experience variables and each of the interaction terms. If there is any pattern change with the impact of any of the CEO experiences (or the interactions between CEO firm-specific and versatile experiences), the newly created interactions will be significant. We did not find any significant results for these interaction terms, suggesting there was no difference in the impacts of CEO experiences for early and later periods.

Discussion

We developed and tested the new idea that versatile experience has a neutralizing effect on the negative aspects of firm-specific experience while enabling its benefits. We find that when CEOs possess high levels of both firm-specific managerial experience and versatile managerial experiences—specifically, in the form of related-industry experience and multifunction experience—firms are more likely to pursue growth opportunities. A noteworthy aspect of this finding is that CEOs' versatile experience by itself often does not have the expected effect on opportunity pursuit. It is the combination of firm-specific and versatile managerial experiences that passes the sufficiency condition for opportunity pursuit. Thus, even though past management research (often building on upper-echelons theory) cast serious doubt on the value of firm-specific managerial experience, we show that firms benefit from CEOs with more firm-specific managerial experience, not less, when such experience is complemented by significant versatile experience. In so doing, our approach in considering CEO experiences as a bundle reconciles alternative theoretical views on the merits of firm-specific experience.

Theoretical Implications

Our research offers theoretical implications for Penrose's (1959) growth theory and the resource-based view by jointly considering the importance of both firm specificity and versatility of managerial experience. Firm-specific managerial experience may be thought as a resource with qualities of being valuable, rare, inimitable, and nonsubstitutable (VRIN) because it embeds contextualized knowledge and relational capital that are hard to imitate and substitute (Crook et al., 2011). Yet, in a meta-analysis, Nason and Wiklund (2018) showed that versatile firm resources are more conducive to facilitating firm growth than VRIN resources. This was also confirmed by Combs et al. (2011), who found that flexible resources can be leveraged to access new markets. Our research highlights a different insight that the combinations of versatile and VRIN qualities in resources might be even more powerful in inducing new growth than resources of either of these qualities are alone. Given this insight, future research can further examine how CEOs with different human-capital profiles perform in leveraging and redeploying different types of resources (versatile/nonversatile and VRIN/non-VRIN resources) to pursue opportunities in related markets, international markets, and platforms and ecosystems across markets.

Relatedly, Sirmon and his colleagues (e.g., Sirmon et al., 2007, 2011) have emphasized the importance of resource management and orchestration in generating growth. They conceptualized resource orchestration as a revitalizing process of structuring a firm's resource portfolio, bundling the resources to build capabilities, and leveraging the capabilities to create value, which can be just as critical as the qualities of resources (D’Oria, Crook, Ketchen, Sirmon, & Wright, 2021; Sirmon, Gove, & Hitt, 2008). Our article connects with their idea in that the combination of CEO firm-specific and versatile human capital facilitates synchronization of the resource structuring, bundling, and leveraging processes (Sirmon et al., 2011). While firm-specific knowledge and relational capital enable CEOs to exploit, mobilize, and deploy a firm's existing resources, versatile human capital allows the CEOs to explore new opportunities, acquire external resources, and pioneer to create new capabilities. Thus, synergistic structuring and bundling of both types of CEO human capital (as the building blocks of ambidextrous managerial human capital) serve as a precursor to synergistic orchestration of resources and capabilities of the firm for growth. This implies the intertwined nature of the resource management and orchestration process and the bundling of versatility and firm specificity in the CEO's managerial human capital. It also bolsters the criticality of developing and testing a theory of firm performance centered on resource bundles and bundling as noted by D’Oria et al. (2021). For example, future research can examine how CEOs’ experience combinations shape choices in development of new technology (e.g., R&D project selection, patenting strategies, and licensing vs. commercialization) and how the productivity of technology assets might differ under CEOs with different human-capital attributes (Nasirov, Li, & Kor, 2021). Future studies can also investigate how CEOs’ experience combinations might shape the utilization of mergers, acquisitions, and alliances to facilitate opportunity pursuit.

Our research also has implications for research on ambidexterity. To achieve balance in exploitation and exploration requires leaders who can “orchestrate the allocation of resources between the old and new business domains” (O’Reilly & Tushman, 2013: 332). Smith and Tushman (2005) emphasize the critical role of top managers for effectively managing exploitation and exploration within firms. Our research implies that CEOs with both firm-specific and versatile managerial experiences might have both the operational competence required to exploit existing resources and the entrepreneurial competence required to explore new business in an ambidextrous organization. Future research might therefore advance by examining the impact of such CEOs on the development of ambidextrous firms.

Further, our research has implications for human-capital research. Past research has largely focused on the mobility of managers across firms and its implications for value capture (e.g., Campbell et al., 2012; Morris et al., 2017) while somewhat neglecting the internal redeployability of managers for value creation. Our research implies that without such managers, firms might suffer from an unrealized potential to grow and achieve renewal because internal adaptability of human capital is crucial for deployment of the firm's resources in current and new markets simultaneously (i.e., resource sharing) and for redeployment of resources from one business to another (Folta, Helfat, & Karim, 2016). Although Nason and Wiklund (2018: 53) argue that “since Penrosean growth theory is free of the inimitability criterion, the distinction between externally or internally fungible resources is not important,” our research suggests that this distinction matters for opportunity pursuit. If a large portion of versatile experience is gained outside the firm, the CEO lacks sufficient firm-specific knowledge as a key ingredient in productive resource reconfiguration and mobilization. Future research can examine the relative criticality of internal versus external sourcing of versatile experience in driving outcomes such as the performance effects of opportunity pursuit under different environmental conditions.

In addition, by differentiating between versatile and firm-specific human capital, our research has implications for research on general management skills that can be transferred to any firm or industry (e.g., Chen, Huang, Meyer-Doyle, & Mindruta, 2021; Mueller et al., 2021; Nasirov et al., 2021) and the use of composite indicators of such skills (Custodio et al., 2013). Such indicators tend to collapse the separate dimensions of versatility and firm specificity into one continuum; yet, our research shows that CEOs can have both high versatility and high firm specificity, and that is precisely what creates the most synergistic combinations that propel growth. For a more holistic understanding of CEO human capital and its contributing elements, future research can theorize about and examine combinations of managerial experience. Rather than a composite human-capital variable (or managerial experience index), research could consider entering experience variables individually and interacting them to detect specific combinative synergies, understand their effect sizes, and visualize them.

It is important to note that versatile experience is different from experience diversity because the latter does not distinguish the specific contexts where CEOs gain experience. In literature that focuses on strategic novelty (Crossland et al., 2014), any variation in managerial experience can contribute to innovation. However, in pursuing growth in the current or related business domains, the context of CEOs experiences matters in terms of both novelty and applicability. For example, experience from CEOs moving across different firms within the same industry deepens industry-specific knowledge. Such intraindustry experience does not necessarily improve the internal applicability of human capital and constitutes nonversatile experience (Nason & Wiklund, 2018). On the other end, experience in unrelated industries might expose managers to new ideas, frameworks, and solutions (thereby contribute to the breadth of human capital), but this experience can be difficult to transfer to current and related business growth settings (Sirmon et al., 2007) and incompatible with the current knowledge domain (Dane, 2010). We performed post hoc analysis to examine the impact of CEO unrelated-industry experience on opportunity pursuit. This analysis revealed that the main effect of this experience is not significant (β = 0.058, p = .331) and the interaction effect between CEO unrelated-industry experience and firm-specific experience is negative and significant (β = −0.018, p = .044). These findings show that distant knowledge domains are less useful for pursuit of path-dependent growth. It may be the case that when CEOs’ expertise from two different domains yields incompatible insights, distant domain expertise is discarded, leaving current business expertise as dominant and entrenching. This is consistent with evidence from advice utilization literature, which suggests that in the face of conflicting advice, individuals might discount (underweight or discard) advice that goes against their view (Ma, Kor, & Seidel, 2020). Yet, for non-path-dependent growth, there could be value for managers who can “integrate previously unrelated matrices of information” (Sirmon et al., 2007: 282). Unrelated-industry experience might enhance managerial ability to conduct explorative learning and facilitate acquisition and integration of new resources, which calls for further research.

Finally, a practical implication of our study is that a firm could boost its growth potential when it grooms managers who have both firm specificity and versatility in their human capital. What is interesting is that an ideal CEO is equipped with both qualities, and it is possible to have best of both worlds when a CEO develops these qualities during one's managerial tenure within the same firm. Thus, even with very long periods of managerial tenure in a single focal firm, CEOs can have versatility in their human capital. Indeed, this is the approach of some very successful multinational firms (e.g., ABB, P&G, and 3M) where managers have abundant opportunities to rotate through various assignments in related industries, in functions, and globally.

Limitations and Future Research

Our article is subject to a number of limitations. First, our theory is focused on pursuit of path-dependent growth opportunities that allows partial leveraging and deployment of existing resources. These aspects of our theory define its boundaries. Generalizability of our findings to other types of firms or growth requires further examination. For example, entrepreneurial and/or born-global firms pursue growth opportunities soon after they are founded (Oviatt & McDougall, 1994). By definition, managers in such firms do not have extensive firm-specific experience; therefore versatility of their prior experience could be crucial in driving the success of opportunity pursuit.

Second, we focused on the role of the CEO's experience. Yet, growth initiatives are likely to involve a team of managers at multiple levels to plan and execute growth (Carpenter et al., 2004; Martin, 2011), such that CEOs might rely on other senior executives to compensate for their lack of experience. Although a complete substitution might not be possible given the tacit (private) nature of the experience and the personal nature of relational capital and trust, future research can examine whether synergistic combinations of firm-specific and versatile experiences at the executive team level can make up for their absence at the CEO level (and vice versa). It would be intriguing to identify and test the specific experience combinations across CEO and executives that promote productive collaboration at the upper echelons.

Third, our operationalization of experience was primarily based on the duration of experience, which captures accumulation of knowledge and managerial skills. However, what happens during the tenure of a specific managerial appointment can differ significantly based on the nature of the opportunities and challenges encountered during the experience (e.g., Bingham, Eisenhardt, & Furr, 2007). Thus, future research can consider ways to capture the extent to which specific managerial experiences offer rich learning and development opportunities, which could help to further differentiate managerial experience. Future research can also consider whether CEOs’ other experiences, such as entrepreneurial (start-up) experience, market-entry experience, or experience in high-growth firms, also influence opportunity pursuit.

Fourth, ownership structure, including block ownership and/or family ownership, can influence the growth strategy. The typical blockholder owner in our sample is an investment or asset management firm, which might have been attracted to the conventional food manufacturing business for relatively stable returns rather than higher-risk, higher-return opportunities that might be found in other sectors (e.g., technology). This explains why their presence was linked negatively with the pursuit of organic food opportunity, which was still emerging at the time. There is also family firm ownership in the sample, but its effect is mixed. In three cases where family ownership involved nonprofit foundations created by the company founders, two pursued organic food opportunity (Kellogg Company and Hershey Foods) but the third did not (Hormel Corporation). Thus, future research might advance by examining the effects of family ownership on path-dependent growth. Future research might also investigate how publicly traded versus privately held firms differ in their responses to emerging opportunities that vary in their risk and time horizon.

Conclusion

Prior research offered competing theory and mixed evidence regarding the benefits of firm-specific experience. Our resolution is to suggest that the value of such experience depends on the other experiences it is combined with. We theorized and found evidence that firms can escape growth-constraining effects of firm-specific managerial experience when CEOs also possess versatile experiences. Our hope is that our research helps spurs a deeper conversation about the nature of managerial experiences that best help firms capitalize on their resources and capabilities to grow and prosper.

Footnotes

Acknowledgments

We are grateful to associate editor Jim Combs for his insightful guidance and exceptional diligence throughout the process. We thank two anonymous reviewers for their valuable comments and suggestions. Without high-quality feedback from reviewers and the editor Combs, this article would not have reached full fruition. We also thank Alberto Feduzi, Royston Greenwood, Don Hambrick, Pol Herrmann, Shenghui Ma, Chris Marquis, Will Mitchell, Alex Mohr, Cher Li, Andrea Patacconi, Karen Schnatterly, Brian Silverman, and Jeff York for their comments on an early draft of this article. The remaining errors are ours. We acknowledge that the study received funding from Taiwan National Science and Technology Council (NSC-99-2410-H-004-012-MY2).