Abstract

Integrating signaling research with the institutional perspective on capital markets, we argue that, in conditions of radical technological change, investor perceptions about firm value are enhanced by the CEO's orientation toward digital technologies that exceeds the firm's industry peers. This base relationship is moderated by board characteristics so that the board members’ digital expertise and knowledge diversity enhance the effect of the CEO's relative digital technology orientation on firm value. Furthermore, the monitoring power of independent board members who do not have digital expertise negatively moderates our baseline hypothesis, whereas board monitoring exerted by independent board members with digital expertise has a positive moderating effect. To test our theory, we use advanced natural language processing techniques to develop the CEO's relative digital technology orientation construct combined with a unique, hand-collected set of measures associated with board members’ digital expertise and knowledge diversity in a sample of S&P 500 companies. Our article offers novel insights on how technology-related signals associated with the CEO's communications to shareholders interact with board characteristics in determining investor perceptions of the firm's value in conditions of high technological uncertainty.

Introduction

Over the past several years, a significant—and multidisciplinary—body of research has investigated how stock market investors evaluate the strategic decisions of the firm's CEO in an environment of high uncertainty (Gamache & McNamara, 2019; Liu, Fisher, & Chen, 2018; Uotila, Maula, Keil, & Zahra, 2009). In this research area, the signaling theory has been an influential theoretical perspective that offers important heuristic lenses to explore stock market reactions to CEO strategic decisions. Signaling theory research suggests that investors look at the CEO's communications to stock market audiences as an important signal when making their value judgments (Cho & Hambrick, 2006; Kaplan, 2011; Keil, Maula, & Syrigos, 2017; Ling, Simsek, Lubatkin, & Veiga, 2008; Westphal & Zajac, 1995). Further, extant studies assume that investors are fully aware that the firm's CEO makes strategic decisions within the parameters of internal governance systems and that the characteristics of boards of directors present important contingency factors that may also affect investor perceptions of value (e.g., Arthaud-Day, Certo, Dalton, & Dalton, 2006; Pfeffer & Salancik, 1978; Westphal & Graebner, 2010).

Within the signaling theory research stream, a relatively less explored area is the investigation of investor responses to the CEO's strategies in conditions of radical technological change (Benner, 2007; Benner & Ranganathan, 2017). Radical technological change presents multiple challenges for investors. Consider, for instance, the digital revolution, which gained momentum in the early 2000s and was driven by “the adoption of novel strategies and business models that are enabled by a myriad of new information technologies” (Furr, Ozcan, & Eisenhardt, 2022: 597). The possibilities associated with digital technologies—for example, cloud and quantum computing, machine learning, big data, artificial intelligence (AI), internet of things, and augmented reality, among many others—are numerous, and the diffusion and adoption of digital technologies has often been associated with transformational, or even revolutionary, changes in businesses, institutions, and societies (Hess, Matt, Benlian, & Wiesböck, 2016; Petrillo, De Felice, Cioffi, & Zomparelli, 2018; Westerman & Bonnet, 2015). Yet, organizational outcomes of digital technology adoption are far from unidirectional, unambiguous, and always positive (e.g., Lanzolla, Pesce, & Tucci, 2021), thus creating much uncertainty among investors around the efficiency and effectiveness of different “digital strategies.” With this in mind, our research questions are as follows: How do stock market investors evaluate signals associated with the CEO's commitment to digital technologies in conditions of radical technological change? As the CEO's strategic decisions are made within the context of the firm's corporate governance, how is this evaluation affected by the monitoring and strategy roles of the board?

In developing our theory, we start from the core focus of signaling theory on the “deliberate communication of positive information in an effort to convey positive organizational attributes” (Connelly, Certo, Ireland, & Reutzel, 2011: 44). Yet, in the context of radical technological change, it is not clear what this positive information signal might even be when investors make their valuation decisions. For instance, prior agency-grounded studies provide two opposed predictions on how investors react to communications associated with the CEO's high-risk strategic intentions in uncertain conditions. On the one hand, in line with Jensen's (1986) “free cash flow” hypothesis, agency theory research predicts that investors should be wary of the CEO's excessive risk-taking, and strategic decisions with highly uncertain outcomes, such as announcements of unrelated diversification, should lead to an “investor discount” in terms of the firm's value (Baysinger & Hoskisson, 1990; Hitt, Hoskisson, Johnson, & Moesel, 1996). On the other hand, another strand of agency-grounded research assumes that “an agent is more risk averse than the principal” (Eisenhardt, 1989: 60-61), and public market investors with widely diversified investment portfolios would value high-risk/high-reward strategy communications from the CEO.

More recent studies have developed an institutionally grounded perspective on financial markets and suggested that investors’ perception of the firm's market value and stock market reactions to firm-level strategic decisions tend to be socially constructed (Bell, Filatotchev, & Aguilera, 2014; Krause, Priem, & Love, 2015; Zajac & Westphal, 2004) and may be based on the workings of wider societal factors, such as social comparison with peers, in line with DiMaggio and Powell (1983). As a result, stock market valuations are an outcome of investors’ perceptions of the firm's signals associated with enhancing its legitimacy rather than rational, efficiency-centered evaluations of cost-benefit properties of strategic signals. Legitimacy here is defined as a “generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate, within some socially constructed system of norms, values, beliefs, and definitions” (Suchman, 1995: 574). In other words, the stock market audiences might have a higher value perception of firm-level signals that fit their cognitive frames, beliefs, and expectations, even if there is no compelling evidence that specific strategic decisions will lead to efficiency outcomes.

In this article, we build on this institutional perspective and integrate it into signaling research to develop hypotheses on the interactions between the CEO's commitment toward radical new technologies, board characteristics, and the stock market investors’ perceptions of firm value. The period from the early 2000s to the late 2010s is the focal time frame of our investigation as, according to Costello and van der Muelen (2018), the major technologies fueling digital transformation—for example, digitization, AI, cloud, and blockchain—emerged and developed in this period. As a starting point, we introduce the construct of the CEO's digital technology orientation, defined as the extent to which CEOs communicate to investors and wider groups of stakeholders their intent to adopt digital technologies. Our core theoretical assumption is that stock market audiences engage in aggregating CEO signals within a particular competitive segment and evaluate the salience of the focal firm's signal in relation to its peer group and not in absolute terms. In other words, CEOs with digital technology orientation that is stronger than the average for the industry would lead to an investor value assessment premium, resulting in a company's better long-term stock market performance. To develop our prediction, we integrate insights from the legitimacy perspective (Bell et al., 2014; Bitektine, 2011; Pollock, Rindova, & Maggitti, 2008) with theoretical arguments from social comparison theory (e.g., Abrahamson & Rosenkopf, 1993; Alexander, 1972; Lindenberg, 1977; Thibaut & Kelley, 2009), including threshold models of collective behavior (Rosenkopf & Abrahamson, 1999; Granovetter, 1978).

Further, we explore contingency factors that may affect salience of signaling of firm value through the CEO's relative digital technology orientation. Extant strategy and governance literature shows that in the context of radical technological change, there is often a “divide” between technology adoption and technology use (Lanzolla & Suarez, 2012) and that effective use of new technologies requires organizational adaptation (e.g., Faraj, von Krogh, Monteiro, & Lakhani, 2016; Felin, Lakhani, & Tushman, 2017; Leonardi, 2012; Majchrzak & Malhotra, 2016; Orlikowski & Scott, 2014) and sometimes even business model transformation (Massa, Tucci, & Afuah, 2017). These theoretical perspectives reflect investors’ concern that technology strategy might be adopted but not implemented. Building on these premises, we argue that investors will react stronger to signaling of digital technology adoption when the firm's board governance factors are seen as more enabling of implementation and use rather than restrictive in terms of limiting the CEO's strategic discretion. We identify three contingency (moderating) factors that potentially capture the enabling/disabling impacts of the board on the CEO's technology-related signals: board directors’ digital expertise, board directors’ knowledge diversity, and board directors’ monitoring power. We hypothesize that, given the investors’ recognition of changes brought forward by digital technology diffusion, the board members’ digital expertise and knowledge diversity would play complementary roles to the CEO's relative digital technology orientation when affecting investor perceptions of firm value, especially when the CEO's technology ambitions go beyond and above the industry average. Further, we nuance the prevailing assumption in economics and finance literature that board monitoring power is a sign of “good governance” (e.g., Gompers, Ishii, & Metrick, 2003; Hermalin & Weisbach, 1998). In line with our earlier arguments, we suggest that board monitoring exerted by independent board members with digital expertise will positively moderate our baseline hypothesis. However, the monitoring power of independent board members who do not have digital expertise will negatively moderate the relationship between the CEO's digital technology orientation relative to the firm's peers and investor perceptions of its value.

To test our hypotheses, we use a longitudinal sample (covering the years from 2003 to 2019) of S&P 500 companies and data on individual experiences and expertise in the digital domain for each and every board member of the companies in our data set. To measure our variables, we make extensive use of the latest advances in natural language processing techniques (Guo, Sengul, & Yu, 2021; Hirschberg & Manning, 2015). Overall, our empirical findings provide a strong support to the hypotheses. Our results appear to be robust to different specifications of the key constructs as well as various specifications of empirical tests.

Our study offers several theoretical contributions. First, we integrate signaling and institutional perspectives and show theoretically and empirically that in the context of high technological uncertainty triggered by digital change, investors pay a premium when CEOs show orientation to adopt new digital technologies over and above their industry peers. This not only nuances our understanding of how stock market investors aggregate CEOs’ signals in the context of high technological uncertainty but also provides support to the idea that investors would pay a premium for a company in which the CEO aligns with, and goes beyond, socially constructed, longer-term expectations on drivers of organizational performance. By doing this, on the one hand, we contribute to the development of a novel perspective on the effectiveness of signaling strategies that is focused on the workings of an innovation diffusion process (Abrahamson, 1991), as little research has discussed the use of technology-focused signals as a comparative legitimation mechanism among investors in the context of technological change within a specific industry (Bitektine, 2011). On the other hand, we add a salient new signal valued by stock markets that complements the extant, mostly “tangible,” signals derived from technology strategy, such as investment in R&D, timing of market entry, and investments in new products and processes. Scholars rarely conceptualize the CEO's relative digital technology orientation as a tool firms can use to manage stock market uncertainty, but the results of our study suggest they should.

Second, we contribute to research on the complex interrelationship among firm value, corporate governance, and strategy signals (Krause, Filatotchev, & Bruton, 2016; Westphal & Graebner, 2010) by showing that board governance functions have contingency effects on the impact of the CEO's relative digital technology orientation on investor perceptions of the firm's value. Prior strategy research suggests that the CEO's hubris and overconfidence may lead to various negative strategic outcomes, such as excessive risk-taking (e.g., Li & Tang, 2010) or a large premium paid for acquisitions (Hayward & Hambrick, 1997). These researchers emphasize the importance of the board's monitoring and vigilance in moderating the effect of CEOs’ traits. We contribute to these theoretical perspectives by exploring a balance between enabling and monitoring roles of board members in the conditions of radical technological change. Specifically, we show that board digital expertise and knowledge diversity amplify the relationship between the CEO's strategic signals and stock market performance.

Third, our contribution is to offer a more nuanced theoretical perspective on the role of board monitoring power in the context of signaling through digital strategies. Specifically, we suggest that (a) board monitoring power is not always positively perceived by investors as widely implied in the extant agency-grounded governance literature and (b) effective board monitoring is associated with complementarities between digital expertise of independent directors and their capacity to influence the CEO's strategic decisions. Overall, our theory brings forward the idea that stock market investors value complementarities between CEOs and boards that are conducive to technology adoption, experimentation, and organizational adaptation.

Our theory has several implications for technology strategy, leadership, and governance practices. We suggest that, in conditions of high uncertainty, CEOs should show vision to adopt new technologies and courage to experiment with them. At the same time, boards should rewire their composition and practices to complement CEOs rather than solely control and monitor them. More specifically, our results are in line with recent board leadership studies that suggest that boards should equip themselves with new dimensions of diversity (Miller, Chiu, Wesley, Vera, & Avery, 2022), as we focus on digital expertise and diverse industry and functional knowledge.

Theory and Hypotheses

Digital Technology Diffusion, Organizational Outcomes, and Firm Value

Digital technologies are widely predicted to be transformative for institutions, societies, and organizations. Their transformative power is often associated with the wider availability of data (e.g., through digitization and the so-called internet of things), higher computing power (e.g., cloud computing), and increased scope of application of smart algorithms (e.g., AI). However, the exact scope and breadth of this “digital transformation” (e.g., Weinelt, 2018) is still being debated, and outcomes are far from always positive and certain (Faraj, Pachidi, & Sayegh, 2018; Kellogg, Valentine, & Christin, 2020; Porter & Heppelmann, 2015; Tripsas & Gavetti, 2000), as most recent debates around the development and applications of AI clearly illustrate. For instance, a McKinsey report (de la Boutetière, Montagner, & Reich, 2018) found that around 50% of digital transformation efforts fail to deliver fully on their goals.

On the one hand, several scholars have shown that digital technology broadens the scope for coordination and collaboration (Bloodgood & Salisbury, 2001; Trantopoulos, von Krogh, Wallin, & Woerter, 2017). Digitization might also enhance organizational efficiency and effectiveness by “liquefying” resources and increasing resource density (Lusch & Nambisan, 2015), leading to performance benefits (Chellappa, Sambamurthy, & Saraf, 2010). Other scholars have highlighted that digital technologies may enable new organizational dynamics, such as boundary-spanning innovation (Levina & Vaast, 2005; Lindgren, Andersson, & Henfridsson, 2008), business model innovation (e.g., Adner & Kapoor, 2010; Eisenmann, Parker, & Van Alstyne, 2006; Jacobides, Cennamo, & Gawer, 2018; Teece, 2010), and the use of ecosystems to deliver on strategy (Boland, Lyytinen, & Yoo, 2007; Jacobides et al., 2018; Powell, Staw, & Cummings, 1990; Van de Ven & Poole, 2005; Von Hippel, 2007).

On the other hand, several other authors have indicated that the technical processes of adopting digital technologies does not lead per se to better organizational outcomes and that these require, for instance, new sociotechnical approaches (Yoo, Boland, Lyytinen, & Majchrzak, 2012; Yoo, Henfridsson, & Lyytinen, 2010), the onboarding of new organizational skills (Troilo, De Luca, & Guenzi, 2017), the establishment of new organizational structures (Viscusi & Tucci, 2018), and the adoption of new business models (Adner & Kapoor, 2010; Eisenmann et al., 2006; Jacobides et al., 2018; Teece, 2010). Therefore, there is a great deal of ambiguity and even uncertainty regarding organizational outcomes of digital technology adoption (e.g., Furr et al., 2022). It follows that in this context, investor perceptions of the value added by digital technologies cannot be underpinned by historical evidence or predictions of some form of efficiency modeling using past performance of other firms.

The CEO's Digital Technology Orientation and Investors’ Perception of Firm's Value

Building on these considerations, the key assumption of our analysis is that, in the high-uncertainty environment of digital transformation, stock market investors’ perceptions of its value-adding potential for the adopting firms may be less based on rational, efficiency-centered considerations. Instead, investor expectations that digital technologies are key factors in the firm's future success may be mostly driven by their cognitive and normative frames associated with what the founder and CEO of the World Economic Forum, Klaus Schwab, referred to as a rapidly evolving conviction that “digital technologies are bringing about unprecedented transformation in ways we have never anticipated” (Schwab, 2016). For instance, virtually all leading consulting firms and investment banks—for example, McKinsey, Bain, Goldman Sachs—systematically release reports and “recommendations” on the imperatives of digital transformation. Governments and (inter-) governmental institutions are on the same wavelength and set digital transformation as one of their key policy goals, if not the key goal—for example, the European Union's digital single-market policies and “Industry 4.0” policies, among many others. Popular and business press publications follow suit and echo the importance for firms and organizations to digitally transform to thrive and not to succumb to the fourth industrial revolution and digital disruption. For instance, a Google search for “digital transformation” returns more than 40 million pages. These forces shape normative and cognitive expectations of a positive long-term impact of digital technologies on the adopting firms (Pollock et al., 2008; Shipilov, Greve, & Rowley, 2019; Tetlock, 2007).

This socioeconomic trend is increasingly reflected in strategic approaches to digitalization among businesses and the investment community. For example, Microsoft's CEO, Satya Nadella, in 2017 wrote in his letter to shareholders, With this new paradigm comes new opportunity. Every customer is looking for both innovative technology to drive new growth and a strategic partner that can help them build their own digital capability. Customers are looking to change how they use digital technology and to reimagine how they empower their employees, engage customers, optimize their operations, and change the very core of their products and services. They are building their own digital systems of intelligence to drive growth.

Two aspects of digital technology adoption attract particular attention of authors within this growing field of research and practice: the extent of adoption (e.g., Rothaermel, 2016) and the ability to experiment in the implementation of the new capabilities brought forward by digital technologies (e.g., Lanzolla & Giudici, 2017). For instance, Rothaermel (2016) shows that electricity took 52 years to reach 50% of the U.S. population, while social media, smartphones, and tablets took only a few years to do so. Lanzolla and Giudici (2017) show that from 2003 to 2013, Axel Springer experimented with different strategic frameworks and organizational forms and embarked on dozens of acquisitions (and subsequent divestitures) before becoming a leader in digital publishing.

To encompass both (often unobservable) aspects of strategy adoption and experimentation, prior studies have usefully applied a theoretical construct of “CEO orientation” in various strategic contexts, including marketing (e.g., Filatotchev, Su, & Bruton, 2017) and strategic entrepreneurship (Keil et al., 2017). We know from extant research that investors look at the CEO's strategic orientation as an important signal for the firm's value creation (Cho & Hambrick, 2006; Keil et al., 2017; Westphal & Zajac, 1995). Furthermore, organizational theorists long emphasized that the strategic orientation of key decision-makers, such as the CEO, may play an important role in translating organization-level strategies into the perceptions of external audiences, such as stock market investors (Krause et al., 2016).

Building on these research strands, we introduce the construct of the CEO's digital technology orientation, defined as the extent to which CEOs communicate to the stock market audiences their intent to adopt and experiment with digital technologies, including some of the untested and emerging ones. Prior studies suggest that the CEO's orientation has a direct impact in terms of resource allocation (Keil et al., 2017) leading to a formation of an observable, credible, and costly signal. Westphal and Graebner (2010) conducted what is perhaps the most complete test of how strategic communications by the CEO form powerful signals that can bolster firm legitimacy through a better alignment with expectations of stock market investors and analysts. Although Westphal and Graebner's (2010) study is focused on intended changes to board structural characteristics, their analysis reveals that securities analysts respond to these signals of intended changes by issuing more positive subsequent appraisals; this positive response occurs despite the fact that these changes had no effect on the board's actual control over the CEO. The authors conclude that a CEO's signal aligning the firm's strategy with the dominant institutional logic has the important consequence of enhancing the legitimacy of a firm with financial stakeholders, even without evidence of substantive efficiency outcomes.

To summarize, theoretical perspective on the diffusion of digital technologies we have outlined suggests that stock market participants may consider the current trend of digital technology development and diffusion as a new and powerful institutional logic that has a material impact on their portfolio decisions (Benner & Ranganathan, 2017). In a signaler-centric perspective, our arguments thus far imply that the CEO's digital technology orientation may constitute an important factor shaping investors’ perception of firm value. In sum, the CEO's digital technology orientation contributes to “organizational legitimacy, the acceptance of an organization by its external environment” (Deephouse, 1996: 1042). And yet, this would be too simplistic.

Research in behavioral decision theory (e.g., Kahneman & Tversky, 1981, 1984) and related literature on social comparison (e.g., Alexander, 1972; Lindenberg, 1977) and social exchange (e.g., Thibaut & Kelley, 2009) suggest that a more comprehensive model of investors’ perception of value must move beyond a sole focus on the CEO's signals and should consider how investors process and respond to signals. For example, extant research shows that investors differ in terms of their past experiences that may act as a “reference point” to make value judgements (Qualls & Puto, 1989; Rowe & Puto, 1987; Russell & Thaler, 1985). Yet, in the context of radical technological change, we maintain that past experiences have a limited role as reference points. Therefore, we argue that investors build their value assessments of the CEO's digital technology orientation on different reference points.

First, digital transformation is not an objective state but rather a strategic choice from an array of alternatives and their combinations. As a result, “digital transformation will likely look different and be different for different executives, even for those whose firms compete in the same industry” (Furr et al., 2022: 598). Integrating this insight with research focused on institutional aspects of stock markets (Bell et al., 2014; Westphal & Zajac, 1998; Zajac & Westphal, 2004), we argue that, in the face of radical technological change, stock market investors become more likely to consider as a reference point industry bandwagons (e.g., Abrahamson & Rosenkopf, 1993; Lanzolla & Suarez, 2012; Powell, Koput, & Smith-Doerr, 1996; Rosenkopf & Abrahamson, 1999). This is also in line with the notion of “rationalized myths,” in the form of commonly known general or industry-specific “taken-for-granted means to accompany organizational ends” (Meyer & Rowan, 1977: 344). Although some authors have emphasized that “myths” may not lead to efficiency outcomes (Brickley & Zimmerman, 2010), “one of the key features of rationalized myths is that they appear so obvious that no one questions their veracity: they just seem right” (Edelman, Uggen, & Erlanger, 1999: 416). As Furr et al. (2022: 596) summarize this argument in the context of increasing adoption of digital technologies: [They] have led to a common belief that digital transformation “changes everything.” The dire warning to incumbents is “disrupt or be disrupted.”

Second, we note that if everyone does the same thing, the effect of a CEO's strategy can, at best, lead to competitive parity (Porter, 1980, 1985). As such, we argue that investors will notice and appreciate CEO digital technology orientation signals that exceed the industry average, as above-industry average orientation is likely to lead to above-industry average long-term returns. This prediction is also in line with the threshold models in the institutional theory that link audience behavior to the overcoming of some threshold points (e.g., Granovetter, 1978, and the rich literature that has sprung from his seminal study).

Overall, these arguments suggest that in conditions of radical technological change, investors evaluate the CEO's digital technology orientation signals not in terms of their absolute level (or strength) but vis-à-vis signals emanated by their industry peers and pay a premium for firms that exceed the industry average. This leads to our baseline hypothesis:

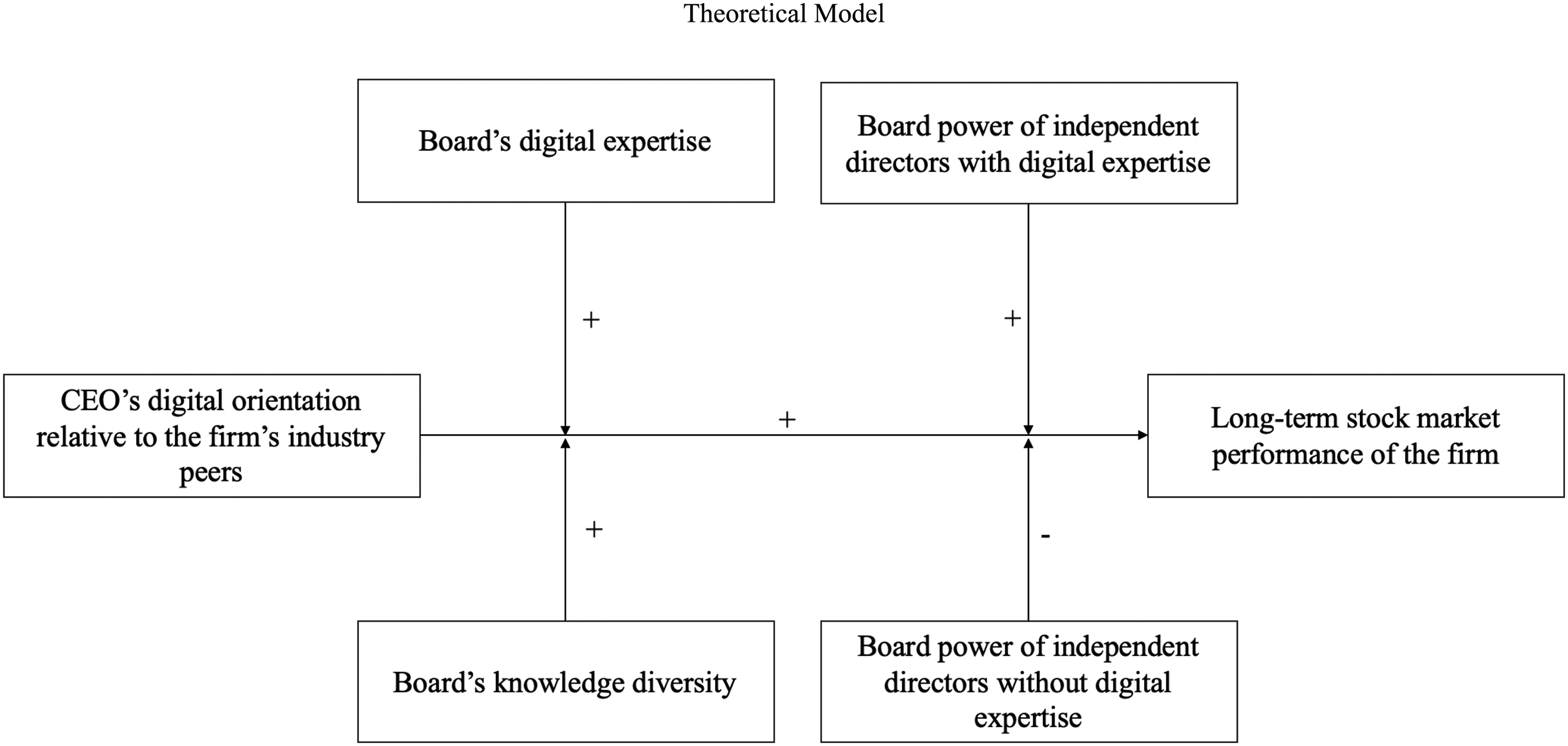

Hypothesis 1: The extent of the CEO's digital technology orientation relative to the firm's industry peers is positively associated with the long-term stock market performance of the firm, other things being equal.

Corporate Governance, CEO Digital Technology Orientation, and Firm Value

A firm may readily subscribe to a new technology but then fail to use it (Lanzolla & Suarez, 2012). Unlike entrepreneurial “digital firms,” such as Uber, established firms are incumbents with legacy operations: “Such firms may be vulnerable to the well-known inertial forces that inhibit adaptation to change” (Furr et al., 2022: 597). Investors are acutely aware of this chasm as well of the fact that technology exerts an impact often through profound changes to organizational practices and routines. As noted by Dougherty and Dunne (2012), “digitalization cannot simply be dumped into organizations.” Our baseline hypothesis suggests that the CEO's digital technology orientation above and beyond that of the firm's peers is a powerful signal that should boost investor perceptions of the firm's value, other things being equal. However, the salience of the CEO's signal alignment with investor expectations depends not only on the relative strength of the CEO's digital technology orientation but also on the governance arrangements, as stock market investors are aware that the way the CEO's commitment to digitization translates into strategic actions depends on the firm board's support and approval.

Traditionally, companies rely on their corporate governance systems for developing, approving, and implementing their strategic responses to, and for dealing with, business challenges. In the corporate governance field, a board of directors is an important group within the firm because it provides the formal link between shareholders and managers (Forbes & Milliken, 1999; Mintzberg & Mintzberg, 1983; Monks & Minow, 1995). For example, Fama and Jensen (1983: 311) describes boards as the “apex of the firm's decision control system.” Therefore, boards’ important monitoring and “strategizing” roles are expected to have an impact on the relationship between the CEO's relative digital technology orientation and stock market performance.

The institutional perspective on corporate boards shifts focus from the economic efficiency imparts of boards toward their contribution to social legitimacy vis-à-vis stock market audiences (Krause et al., 2016; Krause, Chen, Bruton, & Filatotchev, 2021). According to this research stream, strategic signals associated with the CEO's communications to investors are “nested” within broader characteristics of corporate boards that investors consider as proper and legitimate. An important subset of board research focused on the strategy and legitimacy roles of boards suggests that directors are potentially a source of strategic advice, including access to tangible and intangible resources, for the CEO (Baysinger & Hoskisson, 1990; Hillman, Withers, & Collins, 2009). In particular, board directors with complementary knowledge and expertise regularly interact with the CEO to provide helpful advice and influence strategy (Kor & Misangyi, 2008; Kroll, Walters, & Wright, 2008; Rindova, 1999). The key finding is that the more diverse a board is with complementary expertise or characteristics, the higher the firm's strategic flexibility, meaning that the firm is more able to respond to various demands from dynamic competitive and technological environments (Filatotchev & Toms, 2003).

Going back to our base argument that the CEO's commitment to digital technologies above and beyond the firm's industry peers should generate higher investor perceptions of the firm's value, it would be naive to assume that investors rely solely on the CEO's communications, outside the context of the company board. As we emphasized earlier, investors will react stronger to signaling of digital technology adoption when the firm's board governance factors are seen as more enabling of implementation and use rather than restrictive in terms of limiting the CEO's strategic discretion.

Specifically, we argue that the presence of board members with digital expertise is another contributing factor to a legitimacy buildup through signaling the CEO's digital technology orientation and, therefore, makes this signal more salient. They can help the CEO to adopt the right technology and engage in the experimentation with its use, especially when the CEO entertains technology ambitions that go beyond what the firm's peers do. Hambrick, Misangyi, and Park (2015) in their “quad model” of corporate boards emphasize the importance of director expertise for the effective functioning of corporate boards. Building on these arguments, we suggest that the board's digital technology expertise will complement the CEO's digital technology orientation and amplify the positive impact of CEO relative digital technology orientation on the long-term stock market performance.

Hypothesis 2: The extent of the board's digital technology expertise positively moderates the relationship between the extent of the CEO's digital technology orientation relative to the firm's industry peers and long-term stock market performance of the firm.

In addition to the operational uncertainties, digital transformation brings forward a new innovation paradigm whereby innovation will come at the intersection of once disconnected knowledge domains. The emergence of acronyms such as fintech, agritech, and so on is associated with ventures that are created at the intersection of once disconnected industries, with often “disruptive” outcomes. For instance, technology companies—for example, Google, Apple, and Amazon—are seeking to leverage their acquired technological superiority to enter industries that were previously off-limits to them. Consider Google's efforts in driverless cars; Apple Pay; Facebook's digital currency, Libra; or Amazon's entry into the grocery market and, more recently, into prescription medicines. As such, digital transformation requires knowledge diversity, both for “born digital” and traditional companies, as core mechanisms for a company's sustainability. Therefore, corporate boards that traditionally involve members with a high level of specialization in functional areas such as finance, accounting, or marketing may not have the right set of expertise to respond to strategic challenges across the domains.

We argue that the diversity of board members’ knowledge is another factor that may amplify the salience of signaling value through the CEO's relative digital technology orientation as it increases the scope for technology search and connectivity outside the firm's focal industry. Specifically, board knowledge diversity may strengthen the CEO's signal to investors as it offers the right environment for the technology-related experimentation and recombination to happen. First, a diverse board's knowledge may help the CEO to broaden the scope of technology adoption by overcoming the cognitive and knowledge constraints of an individual. Second, a diverse board's knowledge is more likely to provide the CEO with the necessary resources to overcome the aforementioned digital challenges as it is more open to experimentation. A board with diverse knowledge would be more prepared to help the CEO to address these challenges because board members will be more experienced with synthesizing and combining diverse knowledge domains. Overall, it is reasonable to suggest that board members with diverse knowledge are powerful enablers of signaling associated with the CEO's relative digital technology orientation, in a sense that investors would expect that, if the board's knowledge base is more diverse, the CEO would more effectively utilize and apply digital technology orientation for attaining superior long-term performance.

Hypothesis 3: The extent of the board's knowledge diversity positively moderates the relationship between the extent of the CEO's digital technology orientation relative to the firm's industry peers and long-term stock market performance of the firm.

Our previous arguments suggest that board members’ digital expertise and knowledge diversity should enhance the positive effect of the CEO's digital technology orientation on investor perceptions of the firm's value. Prior studies on signaling firm value through corporate governance have almost universally recognized board monitoring capacity as a potent signal of firm value (see Bell et al., 2014, for a review). Therefore, another important contingency within our research framework is whether board members are empowered to monitor and influence executive decisions (Chatterjee, Harrison, & Bergh, 2003; Daily, Dalton, & Cannella, 2003; Fama & Jensen, 1983; Hillman & Dalziel, 2003; Westphal, 1999). An effective monitoring means that the board has the power over the CEO to demand justifications and explanations for proposed strategic initiatives and to make him or her accountable when targets are not met (Baysinger & Hoskisson, 1990; McNulty & Pettigrew, 1999). Extant studies indicate that investors associate the extent of monitoring with the power of independent board members (Krause et al., 2016). Prior corporate governance studies link independent directors’ power to increases in firm efficiency (Daily & Johnson, 1997) and legitimacy (Bednar, 2012; Tost, 2011; Westphal & Graebner, 2010; Westphal & Zajac, 1998; Zajac & Westphal, 2004).

However, governance literature grounded within institutional and behavioral perspectives has also highlighted the pitfalls of “overmonitoring” (Krause et al., 2016, 2021). For instance, investors may realize that a powerful board of directors would be prone to promote their own agenda that is usually structured around less risky, more orthodox and familiar decisions (Combs, Ketchen, Perryman, & Donahue, 2007). Intense monitoring activity of the board may deincentivize lower echelons and limit their scope of attention (Brews & Tucci, 2004; Lyytinen, Yoo, & Boland, 2016; Malone, Yates, & Benjamin, 1987). Faleye, Hoitash, and Hoitash (2011) provide evidence that the improvement in monitoring quality comes at the significant cost of weaker strategic advising and greater managerial myopia. According to these authors, firms with boards that monitor intensely exhibit worse acquisition performance and diminished corporate innovation.

Building on our previous arguments, we suggest that investor perceptions of signals associated with the CEO's relative digital technology orientation may also be shaped by their views of board power in relation to the effective monitoring of the CEO. We extend prior studies on signaling the firm's value to investors through powerful boards by suggesting that, in conditions of rapid technological change, value-enhancing effects of board power are far from being unambiguous and are shaped by the board members’ digital expertise. In other words, investor value judgment with regard to the CEO's signals will depend on the extent of board members’ understanding of, and expertise with, digital technologies, in line with arguments developed by Hambrick et al. (2015). Specifically, we argue that the salience of the CEO's signal vis-à-vis investors would be higher when the firm has in place a corporate board with monitoring capacity provided by independent board members who possess digital expertise. As both technology adoption and experimentation increase levels of uncertainty associated with managerial decisions, independent board members who possess digital expertise might be better positioned to monitor the CEO's digital strategy execution and accept experimentation, making technology orientation signal more tangible. Conversely, we argue that investors would see the monitoring power of independent board members who are not expert in digital technologies as a potential limiting factor in relation to signaling through the CEO's digital technology orientation, as they (a) might overcontrol, and perhaps unduly hinder, the scope of the CEO's strategy execution in the context of digital technologies, especially when the CEO's strategic plans go beyond those of other CEOs in the same industry, and/or (b) might not be able to complement—and hopefully augment—the CEO's strategic experimentation with digital technologies. Hence, we suggest two joint hypotheses:

Hypothesis 4a: Board power of independent directors with digital expertise positively moderates the relationship between the extent of the CEO's digital technology orientation relative to the firm's industry peers and long-term stock market performance of the firm.

Hypothesis 4b: Board power of independent directors without digital expertise negatively moderates the relationship between the extent of the CEO's digital technology orientation relative to the firm's industry peers and long-term stock market performance of the firm.

Figure 1 presents our theoretical model that brings together all hypotheses within a comprehensive contingency framework.

Theoretical Model

Method

Sample

To test our hypotheses, we use a panel of firms included in the S&P 500 index for the years 2003 to 2019 (inclusive). The years of our sample cover a major part of the digital transformation trend as during this period the major technologies underpinning digital transformation—for example, digitization, AI, cloud, and blockchain—emerged and developed (Costello & van der Muelen, 2018). We use S&P 500–indexed companies, which have been widely used in empirical corporate governance studies (Goranova, Alessandri, Brandes, & Dharwadkar, 2007; Walls, Berrone, & Phan, 2012) as they include the largest and most technologically advanced companies in the world, and they are subject to public reporting requirements and obligatory disclosure of important relevant information about their strategic actions and corporate governance practices. To exclude the possibility of survivorship bias, we include only companies that were part of the S&P 500 in the beginning of the study period (2003) and follow them until the end of the study period (2019). Also, due to the lagged independent variables structure of our models, we include only the companies that had at least 2 consecutive years of nonmissing observations. This approach generates an unbalanced panel of 2,332 firm-year observations for 156 companies.

To measure the dependent, independent and control variables of our study, we use data from several different sources, including Compustat, ExecuComp, BoardEx, Morningstar, Mergent Online, and Westlaw databases. In addition, we manually analyzed company proxy statements, personal biographies on company websites, “Who's Who” publications, and other, multiple sources to collect personal information on board members of the firms in our sample.

Measures

Long-term performance

We use the market-based measure of Tobin's Q as our dependent variable. Compared with accounting-based performance measures, market-based measures have the advantage of capturing not only short-term but also long-term performance effects (Allen, 1993). This is particularly important in our case, where the impact of CEO digital technology orientation often takes time to materialize (March, 1991; Uotila et al., 2009), thereby rendering Tobin's Q an appropriate proxy of stock market investor perceptions of the firm's long-term value. We operationalize Tobin's Q as the market value of assets divided by the book value of assets (Bebchuk & Cohen, 2005). To calculate the Tobin's Q, we collected data from Compustat. In the robustness tests, we also used the buy-and-hold return, which is another stock market–based proxy of investor perceptions of the firm's value.

CEO's digital technology orientation relative to the firm's industry peers

Building on recent methodology advances in strategic management research, we have utilized machine learning algorithms to analyze textual material, as this approach allows the organization and processing of very significant volumes of row data that would be impossible to accomplish with traditional manual methods of data gathering and processing (Guo et al., 2021; Hirschberg & Manning, 2015). Specifically, to measure this variable, we examined the absolute level of the CEO's digital technology orientation by measuring the extent to which the CEO's letters to shareholders show content similarity with a book that we consider as “digital strategy benchmark.” The higher the content similarity between these two documents, the higher the CEO's digital technology orientation. Next, we provide rationales about the selection of the specific data sources and a systematic description of how these measures of similarities were derived.

Letters to shareholders are legally binding strategy documents in S&P 500 companies. Extant studies indicate that the CEO as the ultimate person in charge of strategy development and execution is, at the very least, heavily involved in outlining, proofreading, and tailoring the letter to shareholders (Bowman, 1984; Duriau, Reger, & Pfarrer, 2007; Gamache, McNamara, Mannor, & Johnson, 2015). The CEO has a fiduciary duty to ensure that the letter is honest and accurate, taking personal responsibility for its contents (Eggers & Kaplan, 2009; Kaplan, 2008). Furthermore, a vast literature has shown the predictive power of letters to shareholders in a variety of organizational and strategic outcomes (Gamache et al., 2015), including the penetration into emergent technology sectors (Kaplan, 2008; Yadav, Prabhu, & Chandy, 2007), strategic maneuvers and alterations (Barr, Stimpert, & Huff, 1992; Nadkarni & Barr, 2008; Nadkarni & Narayanan, 2007), performance following mergers (Daly, Pouder, & Kabanoff, 2004), international strategic stance (Levy, 2005), and aggressive competitive behavior and response (Marcel, Barr, & Duhaime, 2011). Finally, the letters to shareholders are public documents that, although primarily addressed to (current) shareholders, may impact perceptions of the broader public, including potential new investors.

As we mentioned earlier, there are no universally accepted “digital strategy benchmarks” that can be used to assess the extent of digital technology orientation of a specific CEO. We reviewed several handbooks that have been written by academics and practitioners that contain summaries of how to manage digital technology adoption and organizational adaptation and that have been published up to 2018. Since our goal was to identify the most popular book encompassing digital technology adoption approaches as generally as possible, we excluded all books that presented analysis of a specific successful digital technology adoption. Finally, we opted for The Digital Transformation Playbook by Rogers (2016) for two reasons: its popularity and its broader approach to digital transformation issues. We also considered Westerman, Bonnet, and McAfee (2014) as another comprehensive account of digital transformation strategies and found that this publication covers similar concepts, opportunities, and challenges. While we selected Rogers’s book as the benchmark for the reasons stated already, our methods are robust with respect to using Westerman et al. (2014).

Building on these data sources, following Guo et al. (2021), we measured two types of similarities: lexical similarity (which captures the number of words in common) and semantic similarity (which captures the similarity of the meanings of those words). To measure both types of similarities, we used a combination of cosine similarity (which accounts for lexical similarity) and text embedding (which accounts for semantic similarity) to compare the contents of two documents (Baroni, Dinu, & Kruszewski, 2014; Jurafsky & Martin, 2008). We followed a three-step approach to measure these similarities and leveraged the Google Gensim application programming interface in Python. First, we created a vector of the counts of all content words used in the CEO's letter to shareholders and a vector of the counts of all content words used in The Digital Transformation Playbook. We used an open-source Python library—Word2Vec from Gensim—to identify content words and group together the different inflected forms of a word so they can be analyzed as a single item. This step mainly allows us to measure the lexical similarity of each CEO's letter to shareholders per year with The Digital Transformation Playbook. Second, we measured the semantic similarity of each pair of words in our corpora by using Gensim pretrained text-embedding vectors composed of about 100 billion words from the Google News data set (see Mikolov, Sutskever, Chen, Corrado, & Dean, 2013, for a detailed description of this text-embedding vectors approach). Finally, to create a measure that combines these two similarities, we calculated the dot product of the two vectors we created in the first step for each word, weighing each word pair by the semantic similarity scores created in the second step, and adjusted the dot product for document length following procedures used by Guo et al. (2021) and Lee (2016).

Our theory arguments are focused on the relative signals that the CEO digital technology orientation provides compared with the firm's industry peers. To measure the extent of the CEO's digital technology orientation relative to the firm's industry peers, we adopted the spline specification methodology (Greve, 1998, 2003; Tarakci, Ateş, Floyd, Ahn, & Wooldridge, 2018). Specifically, we calculated our key independent variable—the CEO's digital technology orientation relative to the firm's industry peers—for firm i at time t as CEO digital technology orientation minus industry average when CEO digital technology orientation it is higher than industry average it . Otherwise, the variable is set to zero. In line with the spline methodology, we also created the second part of the spline—the CEO's digital technology orientation relative to the firm's industry peers—to be used in all regression models as a control (e.g., Greve, 1998). This variable was defined as the absolute difference of CEO digital technology orientation it minus industry average it (i.e., |CEO digital technology orientation it – industry average it |) when CEO digital technology orientation it is lower than industry average it ; otherwise it is zero. To calculate the industry average benchmark, we used the average of CEO digital technology orientation values for all firms in the same industry defined on the basis of the two-digit Standard Industrial Classification code.

Digital expertise of the board of directors

We introduce a novel measure of digital technology expertise of the board of directors, which is a composite index of three key measures of the digital experience of a board member. Specifically, each board member has three different ways to acquire knowledge related to digitization: He or she (a) had a “digital” education, (b) has worked in positions that helped him or her gain digital expertise (e.g., a chief technology officer), and (c) has worked in an industry where digitization is widespread (e.g., the information technology [IT] industry). We measured digital education by the number of board members who had education in digital-related fields, such as engineering, IT, mathematics and physics. These fields are most relevant for digitization as they study the development of hardware and software applications of digital technologies. To collect these data for all board members of the S&P 500 companies, we used BoardEx and publicly available biographies (e.g., Bloomberg.com, LinkedIn profiles). However, BoardEx information was in several cases not clear enough to conclude if a board member had a digital education (e.g., BoardEx usually includes only a level of degree—e.g., a bachelor's degree—without indicating the field of study). Therefore, after this initial check, we manually checked all board members (9,421 individuals) to identify if they had a degree that was related to digital education. In the appendix (Table A1), we present all the different degrees that were coded as digital. We compiled this list by (a) identifying any discipline of an educational degree that has at least a word from our digital technology orientation list of keywords and (b) manually checking all remaining disciplines if they connote any digital experience.

We measured digital work expertise by the number of board members who had roles related to the digital domain. As for digital education, we collected the data from BoardEx and publicly available biographies (e.g., Bloomberg.com, LinkedIn profiles). In the appendix (Table A2), we present all the different roles or posts that were coded as digital. We compiled this list by (a) identifying any role that has at least a word from our digital technology orientation list of keywords and (b) manually checking all remaining roles if they connote any digital experience.

We measured digital expertise through work experience in a digital industry by measuring the number of board members who had work experience in one of the following industries: aerospace and defense, automobiles and parts, business services, electronic and electrical equipment, engineering and machinery, information technology hardware, media and entertainment, software and computer services, and telecommunication services. These industries are connected with a high degree of digitization in three main aspects (i.e., assets, usage, and labor) and were categorized as digitally “savvy” industries in the McKinsey Global Institute industry digitization index (de la Boutetière, Montagner, & Reich, 2018). Table A3 in the appendix presents all the digitally savvy industries.

To calculate the composite index of a firm's board of directors’ digital expertise, we used the number of board members who had digital education or a digital role or worked in digital industries divided by the total number of board members.

Knowledge diversity of the board of directors

In line with prior research (Goodstein, Gautam, & Boeker, 1994) and bearing in mind our focus on technology diffusion, we calculated knowledge diversity as a composite index of three diversity measures: (a) educational diversity, (b) diversity in the roles or posts that the focal firm's board members have had, and (c) diversity in the industries in which the focal firm's board members have worked. Specifically, educational diversity was measured by the number of unique two-digit instructional program codes (as classified by the U.S. Department of Education's National Center for Education Statistics Classification of Instructional Programs, 2000) the firm's board members had. Diversity in the roles or posts was measured as the number of unique roles or posts the focal firm's board members had. Diversity of industry experience was measured as the number of unique three-digit North American Industry Classification System codes of industries the focal firm's board members had worked in. Finally, the composite index of the knowledge diversity was measured as the average standardized values of these three indices (i.e., educational diversity, role diversity, and industry diversity).

Board power

To test our joint Hypotheses 4a and 4b related to the moderating role of board power, we calculated board power of two groups of independent board members (e.g., board power of independent directors with or without digital expertise). To capture the extent of digital expertise of the independent board members, we used three criteria: whether a board member (a) had a digital education, (b) has worked in positions that helped him or her gain digital expertise (e.g., a chief technology officer), or/and (c) has worked in an industry where digitization is widespread (e.g., the IT industry). When a specific director possesses at least one of these characteristics, we allocate her or him to a group of independent directors with digital expertise. The rest of independent directors would belong to a group of directors without digital expertise.

Second, to calculate the actual value of board power for each of the two subgroups, and in line with prior research (Cannella & Shen, 2001), we measure the monitoring capacity of the board of directors as the index of independent board members’ power. Specifically, the independent board members’ power was measured as a summative index of the three main sources of independent members’ power: percentage of independent board members, measured as the number of independent board members divided by the total number of board members (Deutsch, Keil, & Laamanen, 2011); independent board members’ ownership, measured as the percentage of total outstanding common voting shares owned by outside board members (Cannella & Shen, 2001); and independent board members’ tenure, measured as the sum of the number of years that each outside board member served on the board of directors in a given company divided by the number of independent board members (Johnson, Hoskisson, & Hitt, 1993). The final independent board members’ power composite index included the sum of the standardized values of these three components. This procedure generates two separate measurements of board power for independent directors with and without digital expertise that we use to test Hypotheses 4a and 4b.

Control variables

We include several control variables that have been previously used in the corporate governance literature to explain performance variations across firms (Bebchuk & Cohen, 2005; Finkelstein & Mooney, 2003; Gompers et al., 2003; Krause et al., 2015; Luo, Kanuri, & Andrews, 2014; Uotila et al., 2009). Specifically, we control for firm size (measured as the natural logarithm of a firm's total number of employees), short-term financial performance (return on assets [ROA]), capital expenditures (capital expenditures divided by total assets), and leverage by obtaining related firm-year data from Compustat. Further, we include a number of governance-related controls that have been shown to affect long-term performance: board size, measured as the number of board members (Deutsch et al., 2011), and institutional ownership, measured by the percentage of ownership held by banks, investment firms, and pension funds (George, Wiklund, & Zahra, 2005). Also, we control for the firm's international or geographical diversification measured as income from foreign operations before tax (Sullivan, 1994). Furthermore, we added two CEO-related variables to control for CEO characteristics: (a) a dummy variable taking the value 1 if the CEO had a PhD in digital-related fields (see Table A1 for the list of keywords used) and (b) CEO compensation, which was measured as the sum of pay, bonuses, and stock options. Finally, we also included year dummies to control for unobserved temporal-level heterogeneity.

Analytical Approach

We conducted our analyses and hypothesis testing using dynamic linear regression modeling (Judson & Owen, 1999) employing Bruno's (2005) corrected least squares dummy variable approach and dynamic fixed-effects linear modeling. First, our data contain multiple observations per firm, causing concerns with an unobserved heterogeneity, so we used fixed-effects models with least squares dummy variable approach to control for unobservable variables. To test the fixed-effects assumption, we further conducted a Hausman test that confirmed that fixed-effects models should be used, as there was a significant (p = .001) systematic difference in the coefficients of random effects versus fixed-effects models. Second, prior research on corporate governance (Flannery & Hankins, 2013) tends to use an autoregressive or dynamic model that includes the lagged dependent variable as a control to capture the possible effects of unobserved variables on the dependent variable. This model specification may induce bias in the standard fixed-effects regression model. To correct for this autocorrelation problem, we used Bruno's (2005) technique of bias approximations, which utilizes an Arellano-Bond consistent estimator. We used the Stata command xtlsdvc, which implements least squares dummy variable correction based on the theoretical approximation formulas of Bruno (2005) and estimates a bootstrap variance covariance matrix for the corrected estimator. We note that our results are similar with a simple fixed-effects model.

Results

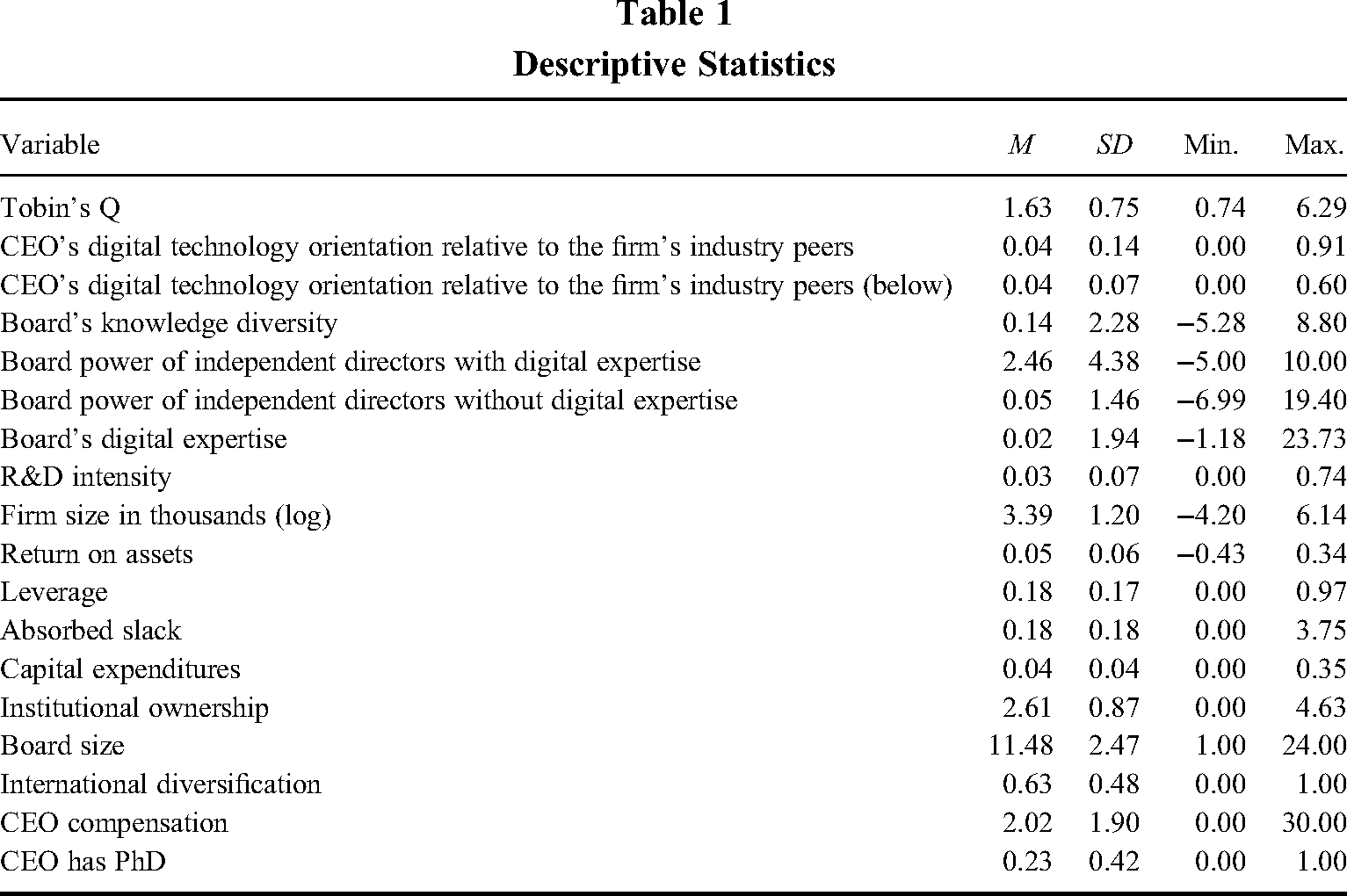

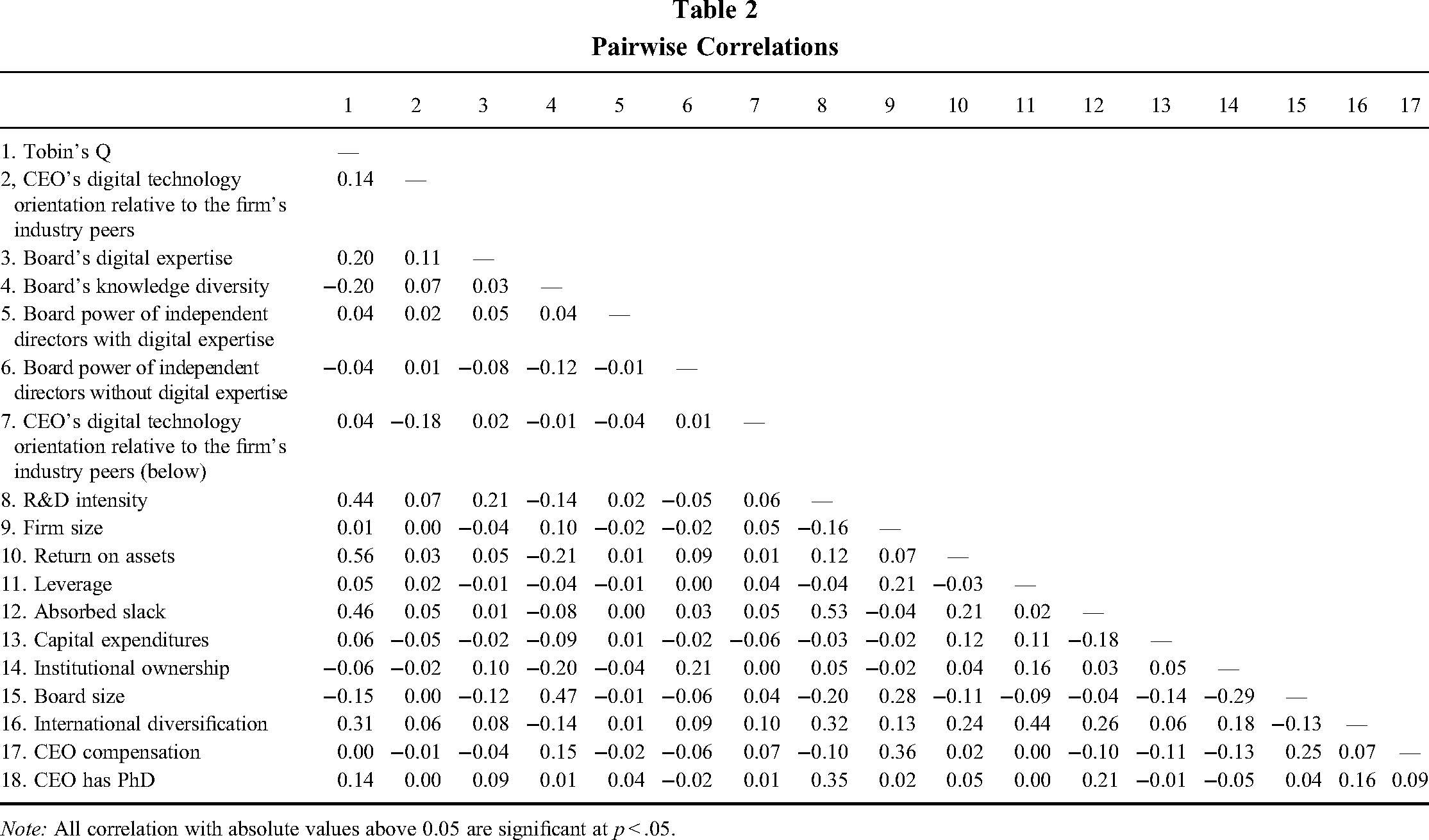

Tables 1 and 2 present the correlations, while the results of our hypothesis testing are provided in Table 3. In Table 1, all bivariate correlations are below the 0.60 threshold, thereby mitigating concerns about multicollinearity. We further calculated the variance inflation factors (VIFs) for each coefficient. The maximum VIF was 2.99, substantially below the most commonly used cutoff values (Cohen, Cohen, & West, 2003), providing further evidence that multicollinearity was not a problem in our analyses. We note that about half of the companies had at least one board member who had digital education or worked in the digital sector or had a digital position in our sample period. Rather surprisingly, this number is relatively small if someone considers the size of these companies and the fact that our sample includes most of the top high-tech companies in the world (e.g., Microsoft, Adobe Systems, Cisco Systems, General Electric). Further, 41% of the companies had at least one board member who had digital education, and about 21% of the companies had at least one board member who had worked in a digital industry. We note that 16% of the companies had at least one board member who had one or more digital positions. Finally, there is relatively low correlation between the relative CEO digital technology orientation variable and R&D intensity (i.e., 0.07) and capital expenditure (−0.05). Clearly, the relative CEO digital technology orientation is not a proxy for (or driven by) the firm's past tangible investments, and this provides further support for our focus on the forward-looking, legitimization aspects of signaling firm value through digital technology orientation.

Descriptive Statistics

Pairwise Correlations

Note: All correlation with absolute values above 0.05 are significant at p < .05.

Panel Data Regression Analyses With Fixed Effects and Bruno's Corrected Least Squares Dummy Variable Approach

Note: All models include year dummies. All analyses are conducted with two-tailed tests.

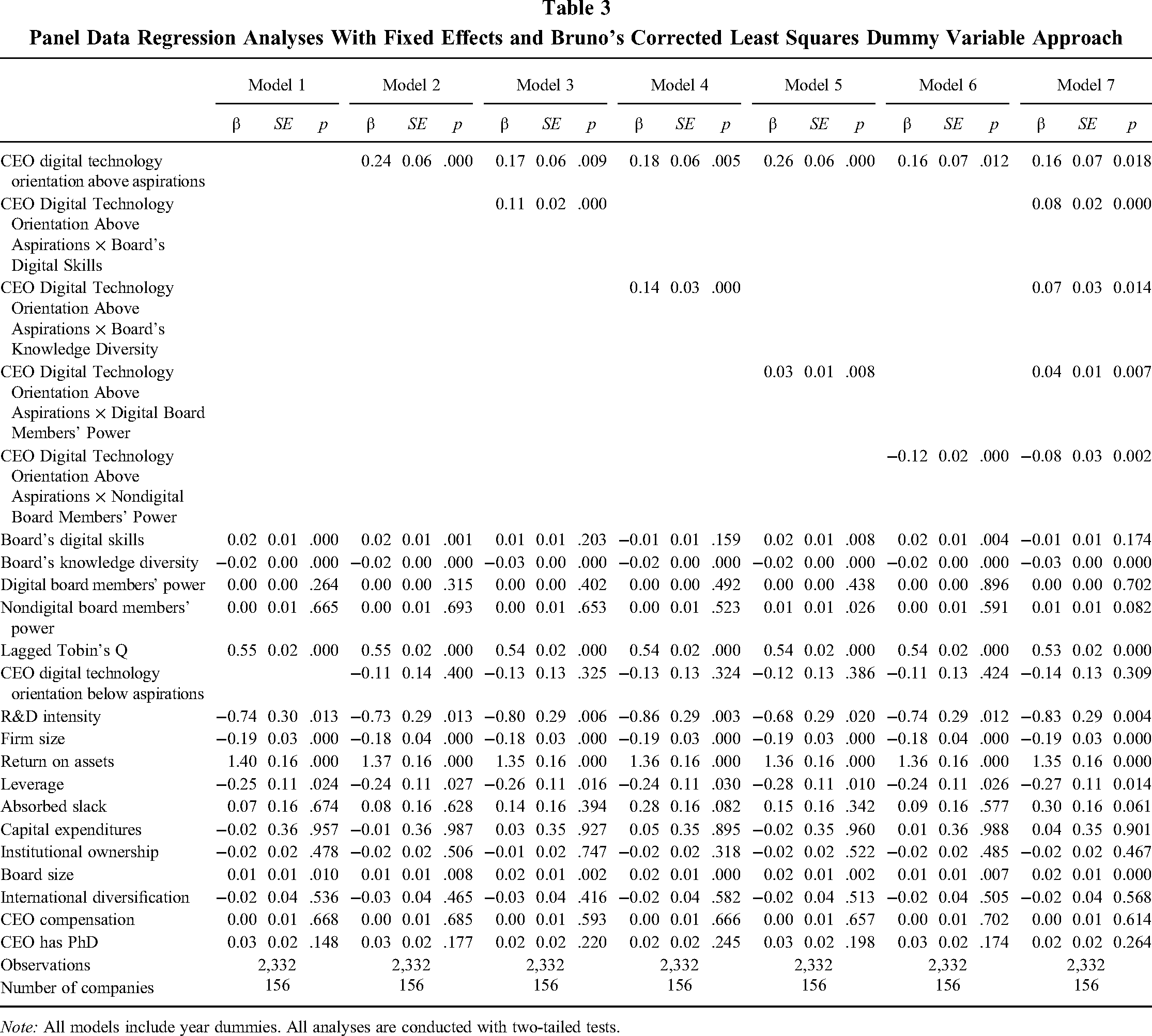

Table 3 shows the results of our analysis with Bruno's (2005) corrected least squares dummy variable approach. We interpret the results based on the partial models (Models 2, 3, 4, 5, and 6), but, as shown in Table 3, the results are similar for the full model (Model 7). We find support for Hypothesis 1, which posits that relative CEO digital technology orientation (i.e., in Table 3 named “CEO digital technology orientation above aspirations”) is positively and significantly related to Tobin's Q (β = 0. 24, p = .000; Model 2, Table 3). In economic or monetary terms, this means that a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 4% increase in the Tobin's Q. For a firm in our sample with average size (i.e., a book value of US$1.13 billion), this would mean a US$73 million increase in its market value within a year.

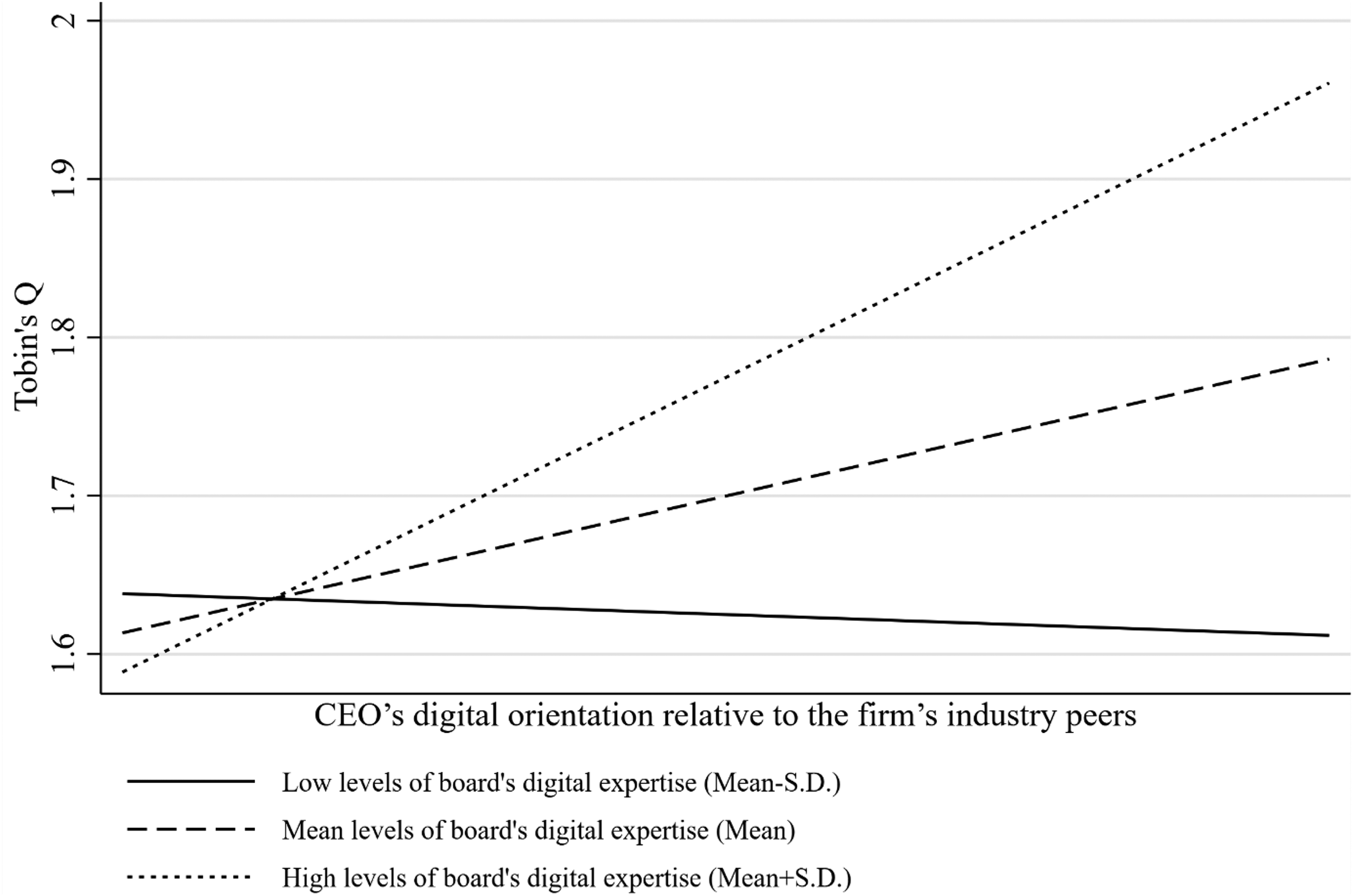

Also, we found support for Hypothesis 2, which posits that board digital expertise positively moderates the relationship between relative CEO digital technology orientation and Tobin's Q. The interaction term between board digital expertise and relative CEO digital technology orientation was found to be positive and significant (β = .11, p = .000; Model 3, Table 3). In practical terms, this means that for the firms that have a board with high digital expertise (i.e., one standard deviation above mean), a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 5% increase in the Tobin's Q. Again, for the average-sized firm, this will mean a US$92 million increase in its market value within a year. Contrary, for the firms that have a board with low digital expertise (i.e., one standard deviation below the mean), a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 0.8% increase in the Tobin's Q (US$14 million increase for the average-sized firm in its market value within a year). To further interpret this result, we plotted the interaction effect in Figure 2. The graphical analysis of Figure 2 shows that firms exhibit higher long-term performance (i.e., Tobin's Q) when there is a board of directors with high digital expertise compared with the firms with the same relative CEO digital technology orientation but with a board of directors with low digital expertise.

Moderating Effect of Board Members’ Digital Expertise (Hypothesis 2)

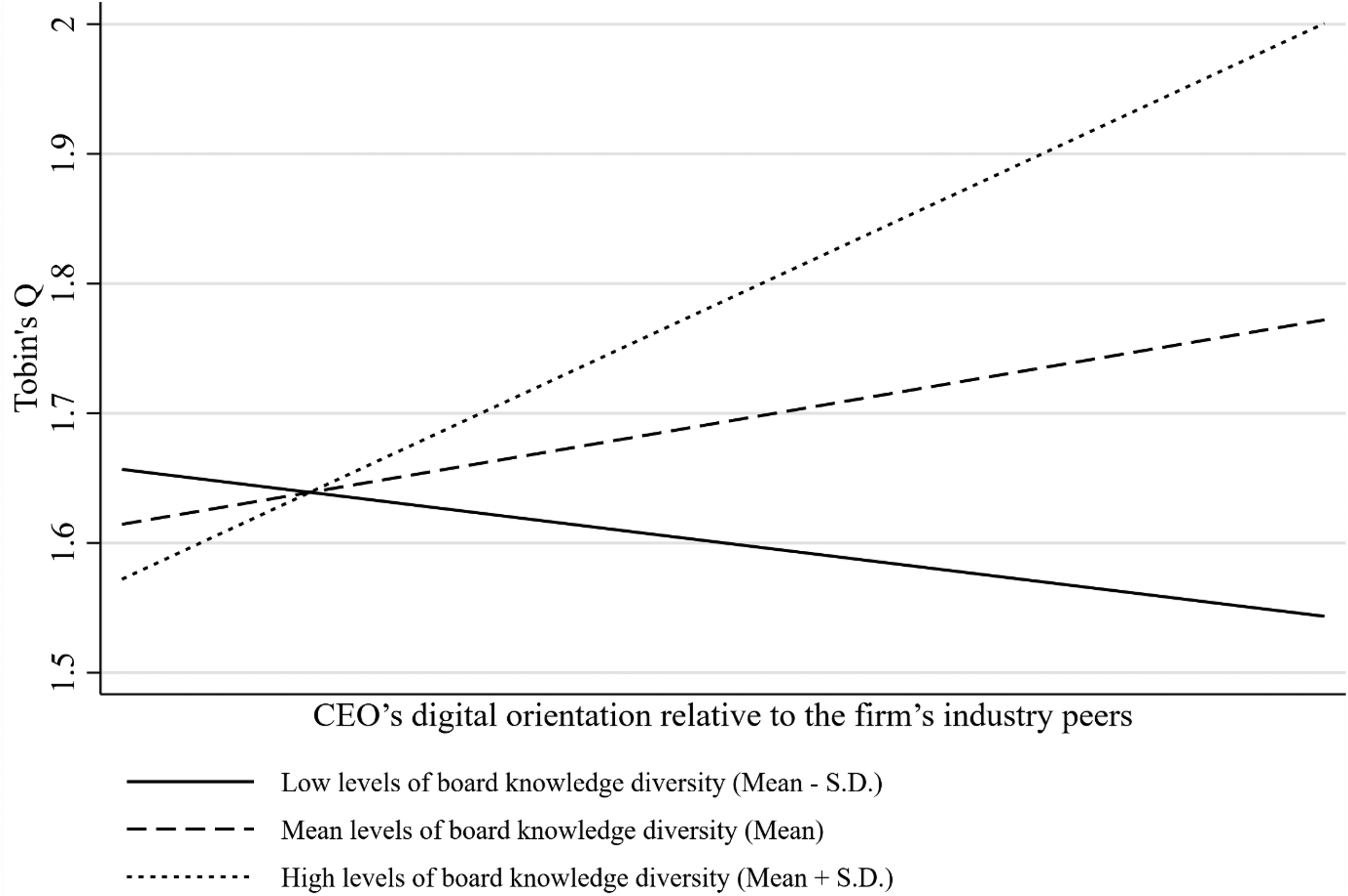

Board knowledge diversity positively moderates the relationship between relative CEO digital technology orientation and Tobin's Q, in line with Hypothesis 3, as the interaction term between board knowledge diversity and relative CEO digital technology orientation was found to be positive and significant (β = 0.14, p = .000; Model 4, Table 3). This means that for the firms that have a board with high knowledge diversity (i.e., one standard deviation above the mean), a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 10% increase in the Tobin's Q (US$184 million increase for the average-sized firm). Contrary, for the firms that have a board with low knowledge diversity (i.e., one standard deviation below the mean), a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 0.6% decrease in the Tobin's Q (an increase of only US$11 million for the average-sized firm). To further interpret this result, we plotted the interaction effect in Figure 3. The graphical analysis of Figure 3 (section on Hypothesis 3) shows that firms exhibit higher long-term performance (i.e., Tobin's Q) when there is a board of directors with high knowledge diversity compared with the firms with the same relative CEO digital technology orientation but with a board of directors with low knowledge diversity.

Moderating Effect of Board Members’ Knowledge Diversity (Hypothesis 3)

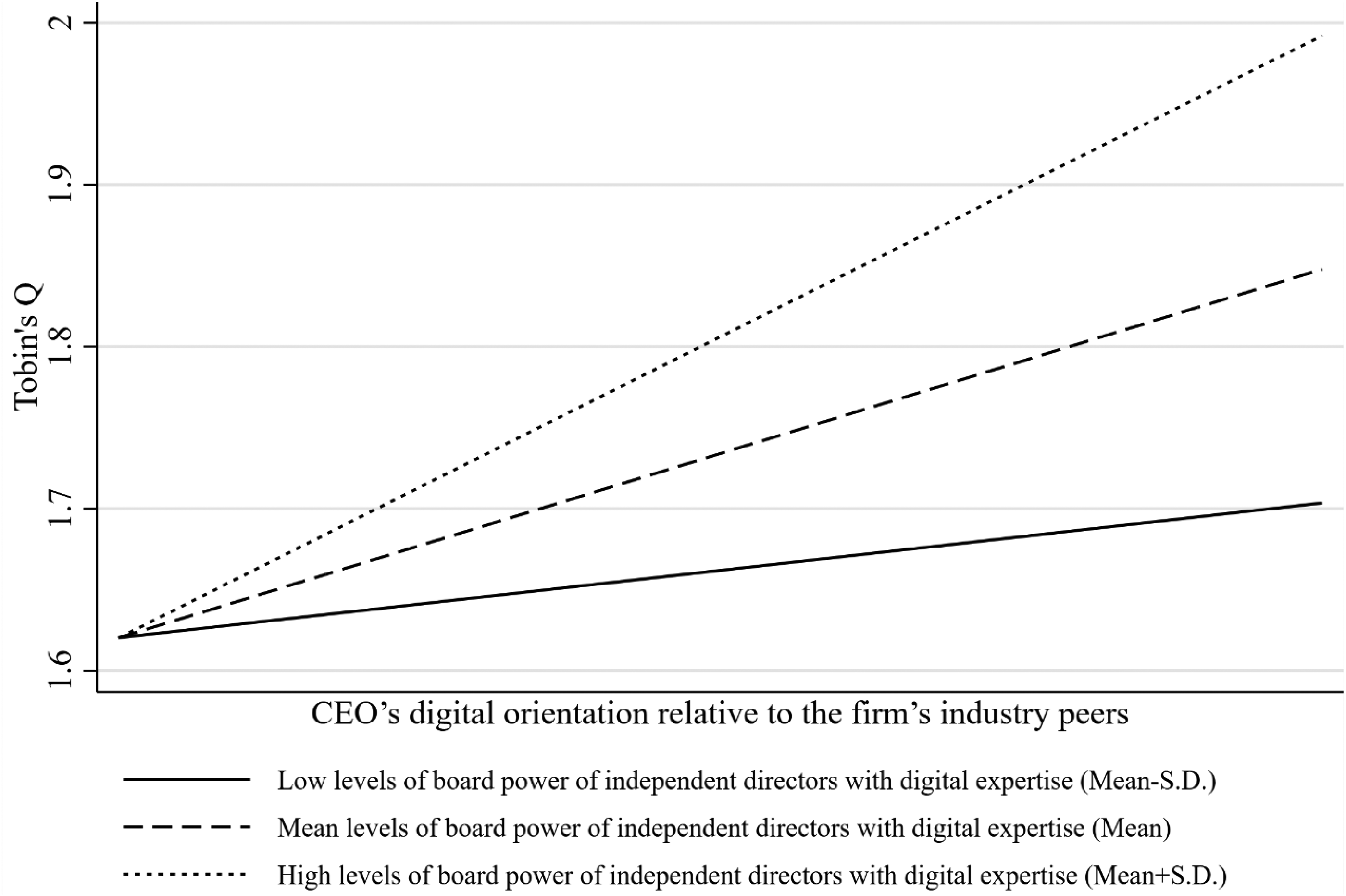

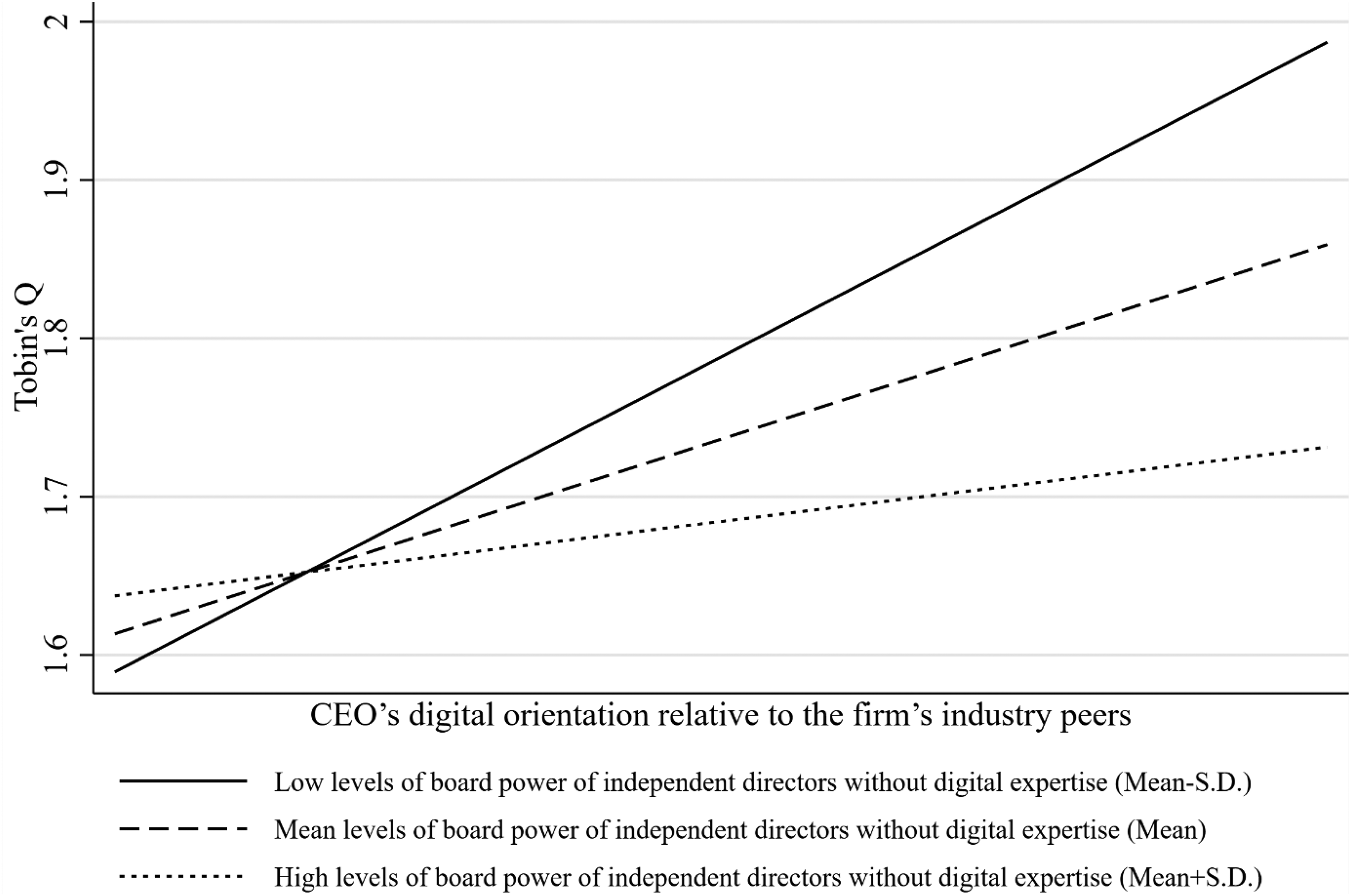

Finally, we find support for both Hypotheses 4a and 4b: Board power of directors with digital expertise positively moderates the relationship between relative CEO digital technology orientation and Tobin's Q (β = 0.03, p = .008; Model 5, Table 3), while board power of directors without digital expertise negatively moderates the relationship between relative CEO digital technology orientation and Tobin's Q (β = −0.12, p = .000; Model 6, Table 3). In monetary terms, for the firms that have a board with high board power of directors with digital expertise (i.e., one standard deviation above mean), a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 9% increase in the Tobin's Q within a year (an increase of almost US$165 million in market value for the average-sized firm in our sample). Contrary, for the firms that have a board with low board power of directors with digital expertise (i.e., one standard deviation below the mean), a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 0.9% increase in the Tobin's Q (or a US$16 million increase in market value for the average-sized firm). On the other hand, for the firms that have a board with high board power of directors without digital expertise (i.e., one standard deviation above mean), a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 0.8% increase in the Tobin's Q (or US$14 million for the average size firm). However, for the firms that have a board with low board power of directors with digital expertise (i.e., one standard deviation below the mean), a one-standard-deviation increase in the relative CEO digital technology orientation will lead to a 5% increase in the Tobin's Q (or US$92 million for the average-sized firm). To further interpret these results, we plotted the interaction effect between relative CEO digital technology orientation, board power variables, and Tobin's Q (Figures 4 and 5) to provide visual evidence on these interactions.

Moderating Effect of Board Power of Independent Directors With Digital Expertise (Hypothesis 4a)

Moderating Effect of Board Power of Independent Directors Without Digital Expertise (Hypothesis 4b)

Additional Analysis

We conducted a number of robustness tests. First, although our dependent variable is the most common measure of investor perceptions of the firm's market value, we decided to verify if our results are robust with regard to other measures of the firm's long-term stock market value, such as the buy-and-hold abnormal returns (BHAR) variable (Lyon, Barber, & Tsai, 1999). BHAR shows the return for an investor who bought a firm's stock on an important announcement at a specified later date (usually past 12 months). We used publication of the letter to shareholders as an information event. As the publication date of a letter to shareholders varies for each company, we used the last day of the fiscal year as a conservative time frame for the focal firm. Finally, the 12-month return from a buy-and-hold (BHR) strategy was computed for the year following this date. The results of this analysis were similar to our main analysis (Hypothesis 1, β = 0.03, p = .000; Hypothesis 2, β = 0.02, p = .001; Hypothesis 3, β = 0.02, p = .001; Hypothesis 4a, β = 0.01, p = .021; and Hypothesis 4b, β = −0.02, p = .001), thereby alleviating concerns regarding our usage of the Tobin's Q as dependent variable.

Second, to address possible limitations of the letters to shareholders as a signal of the CEO's digital technology orientation, we decided to combine it with another investor-focused communication that most CEOs use to signal their strategic views to the stock market, media, and general public: the quarterly earnings conference calls (Pan, McNamara, Lee, Haleblian, & Devers, 2018). The quarterly earnings calls are teleconferences or webcasts that are typically preceded by a press release announcing a company's latest quarterly results. As a rule, the CEO is present in these earnings calls and her or his presentation has a substantial effect on shaping perceptions about firm value (Pan et al., 2018). In our additional analysis, we collected all available transcripts of CEOs’ presentations to the quarterly earnings conference calls and added them to the corpus of text that we use to measure our main independent variable, that is, CEO's relative digital orientation. The results of the additional analyses are very similar to our main analysis (Hypothesis 1, β = 0.26, p = .002; Hypothesis 2, β = 0.12, p = .000; Hypothesis 3, β = 0.14, p = .002; Hypothesis 4a, β = 0.04, p = .023; Hypothesis 4b, β = −0.12, p = .005), thereby further corroborating the suitability of the letter to shareholders for investor value perceptions. We believe this is a strong further empirical test of the robustness of our measure and, more broadly, of our theory.

Endogeneity Tests

In our study, we have identified and addressed two potential endogeneity issues: (a) omitted variables and (b) measurement error. The other two commonly encountered endogeneity concerns—simultaneity and selection bias—pose less of a threat in our context. The risk of simultaneity is minimized due to our twofold approach, which builds on (a) utilizing a lagged structure where the dependent variable is assessed a year subsequent to the independent variable and (b) conducting an omitted-variables analysis, as detailed next, indicating a low likelihood of any omitted variable significantly altering our results. Likewise, selection bias is unlikely to be a significant concern as the factors determining inclusion in our study are not correlated with the outcomes under investigation.

As per addressing omitted-variables concerns, we calculated the requisite partial correlations with a confounding variable to invalidate our main predictions given our analyses context (e.g., sample size, predictors included, estimate values). Specifically, we used the Busenbark, Yoon, Gamache, and Withers (2022) impact threshold of a confounding variable (ITCV) technique to calculate the correlation threshold that an omitted variable should have to invalidate our findings. By following their suggestions (we run linear ordinary least squares models -xtreg- with fe, as the command “konfound” does not run with Bruno's [2005] approach), we found that for an omitted variable to invalidate our findings, it would need to be correlated at r > .08 with both Tobin's Q and with the CEO's relative digital technology orientation. We found that to invalidate our main predictions, an omitted variable needs to have a pattern of partial correlations (i.e., positive with the outcome and the focal predictor) that we do not observe for any variable in our models. Specifically, the highest ITCV value is approximately 75% larger than the strongest partial correlation in our analyses. This means that the comparative thresholds of the omitted variable have to be at least 75% larger than the largest partial correlation in our data suggests, something that is very unlikely (Busenbark et al., 2022).

Furthermore, to alleviate the possibility for measurement error in our independent and moderating variables, we conducted additional analysis with instrumental variables. Specifically, we decided to use dynamic instruments (i.e., lagged values of the independent, control, and dependent variables) to address potential measurement errors in any core variable (independent and moderators). There are several reasons that make this choice effective. To begin with, lagged values of independent variables might influence current values as prior CEO digital technology orientation might affect the current and past board's digital characteristics. Similarly, prior values of control variables or the dependent variable might affect the level of the independent variables. To test if our results are robust, we ran generalized method of moments (GMM) regression analysis. Specifically, we used the Arellano and Bond (1991) dynamic GMM estimator (Fremeth & Shaver, 2014; Roodman, 2011) and treated the independent and moderating variables as endogenous, while control variables were considered exogenous. We used the two-step robust estimator developed by Windmeijer (2005) because it corrects panel-specific autocorrelation and heteroskedasticity. This analysis provided similar results (Hypothesis 1, β = 1.19, p = .017; Hypothesis 2, β = 0.11, p = .002; Hypothesis 3, β = 0.03, p = .002; Hypothesis 4a, β = 1.03, p = .000; and Hypothesis 4b, β = −0.12, p = .021) and thus supports our theory. We also tested the strength of the instruments used; therefore, we address a recognized drawback of the dynamic panel GMM regression method (Fremeth & Shaver, 2014). Specifically, to evaluate whether the instruments are exogenous, and to confirm the validity of the GMM estimates, we use the Hansen J-test. All Hansen J-tests are above 0.05, thus supporting our choice of instruments.

Discussion

In this research, we explore how stock market investors evaluate signals associated with the CEO's commitment to new technologies in conditions of radical technological change. We further analyze how this evaluation is affected by the firm's governance characteristics associated with the monitoring and strategy roles of the board. The empirical context of our research is the diffusion of digital technologies (2003 to 2018) during which high expectations for the positive “revolutionary” effects of the digital transformation were often obfuscated by disappointments regarding the actual benefits of technology adoption. In this context, investors do not have any past reference point to assess the impact of these “revolutionary” technologies on firm value. Our theory is that, in conditions of radical technological change, investors look at the strategy signals sent by the CEO and interpret them vis-à-vis expectations about the (long-term) impact of such technologies. This theory has two underlying corollaries: (a) Investors expect that companies should adopt new technologies, and (b) investors expect that companies should adapt to the new realities enabled by such technologies. Following these arguments, we then show theoretically and empirically that investors look at the CEO's signals of adoption not in absolute terms but vis-à-vis the average level of such signals in industry peers. Specifically, we extend and nuance extant literature by showing that to make value judgements, stock market investors are likely to consider as a reference point the industry bandwagon (e.g., Abrahamson & Rosenkopf, 1993; Lanzolla & Suarez, 2012; Powell et al., 1996; Rosenkopf & Abrahamson, 1999).

Our theory adds a new hitherto-overlooked dimension to the signaling perspective: Stock market investors pay a premium for signals of technology adoption over and above the average of the signals emanated by CEOs in peer groups. By doing this, we contribute to the development of a novel perspective on the effectiveness of signaling strategies that is focused on the workings of a social construction process, as little research has discussed the use of technology-focused signals as a comparative legitimation mechanism among investors in the context of technological change within a specific industry (Bitektine, 2011). Our framework also contributes to signaling theory by showing that communications related to technology orientation are powerful signals for stock market investors. In doing this, we complement signaling theory, which has traditionally explored investor responses to signals associated with costly, visible, and difficult-to-imitate strategies (Connelly et al., 2011), such as investment in R&D, introduction of new products, and processes in the context of technological change. Scholars rarely conceptualize the CEO's relative digital technology orientation as a tool firms can use to manage stock market uncertainty, but the results of our study suggest they should.